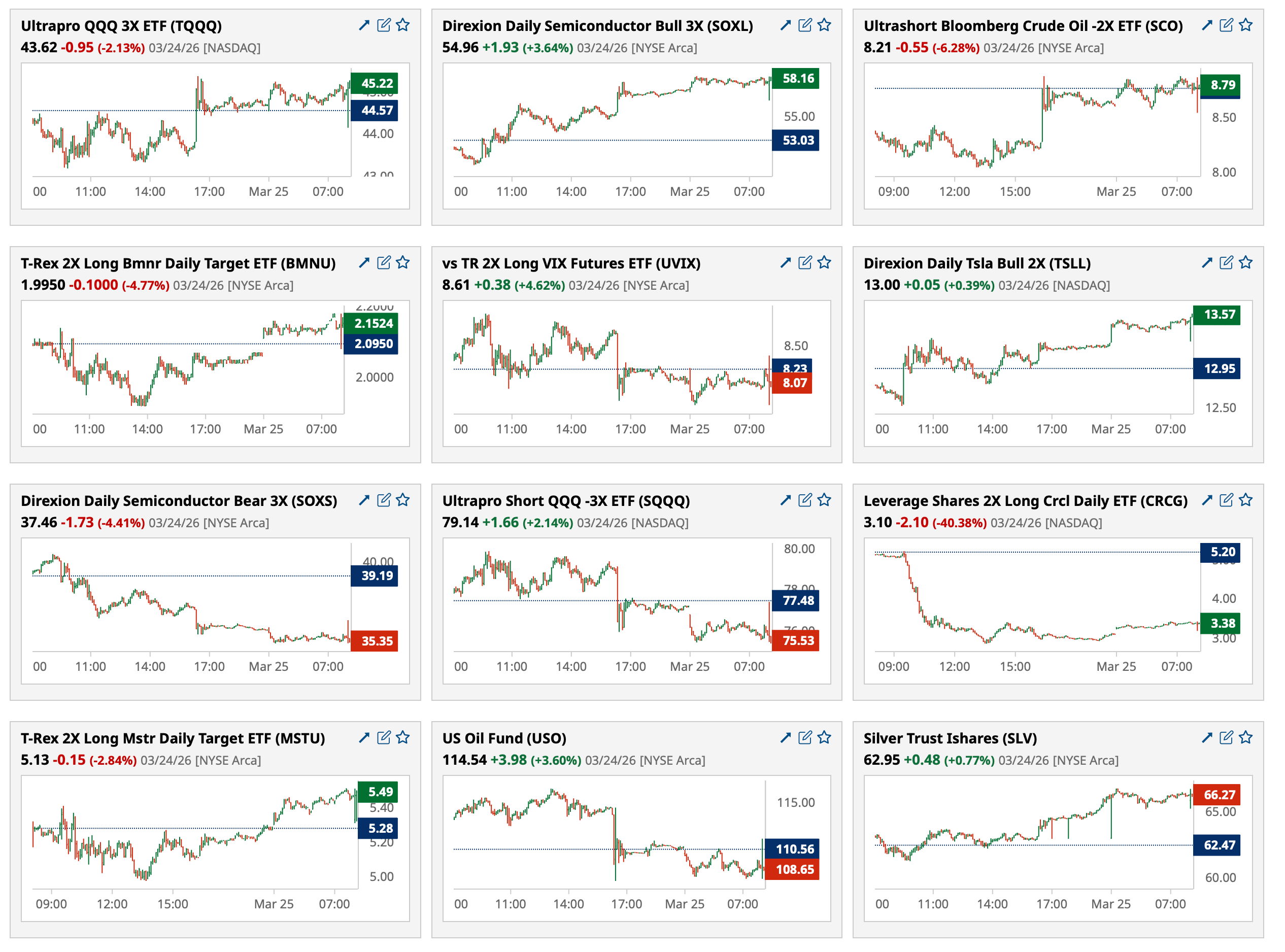

Wednesday's After-Hours Advancers and Decliners

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Mar 25, 2026, 4:40 PM EDT

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Mar 25, 2026, 4:40 PM EDT

Closing Volume

- NYSE volume 10% below its one-month average

- NASDAQ volume 9% below its one-month average

- VIX index: down 5.86% to 25.37

Breadth

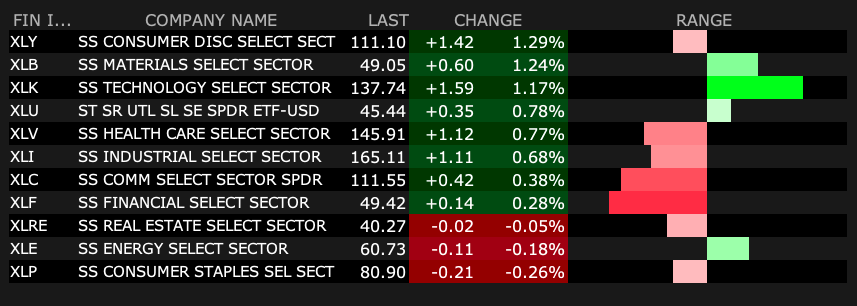

Sectors

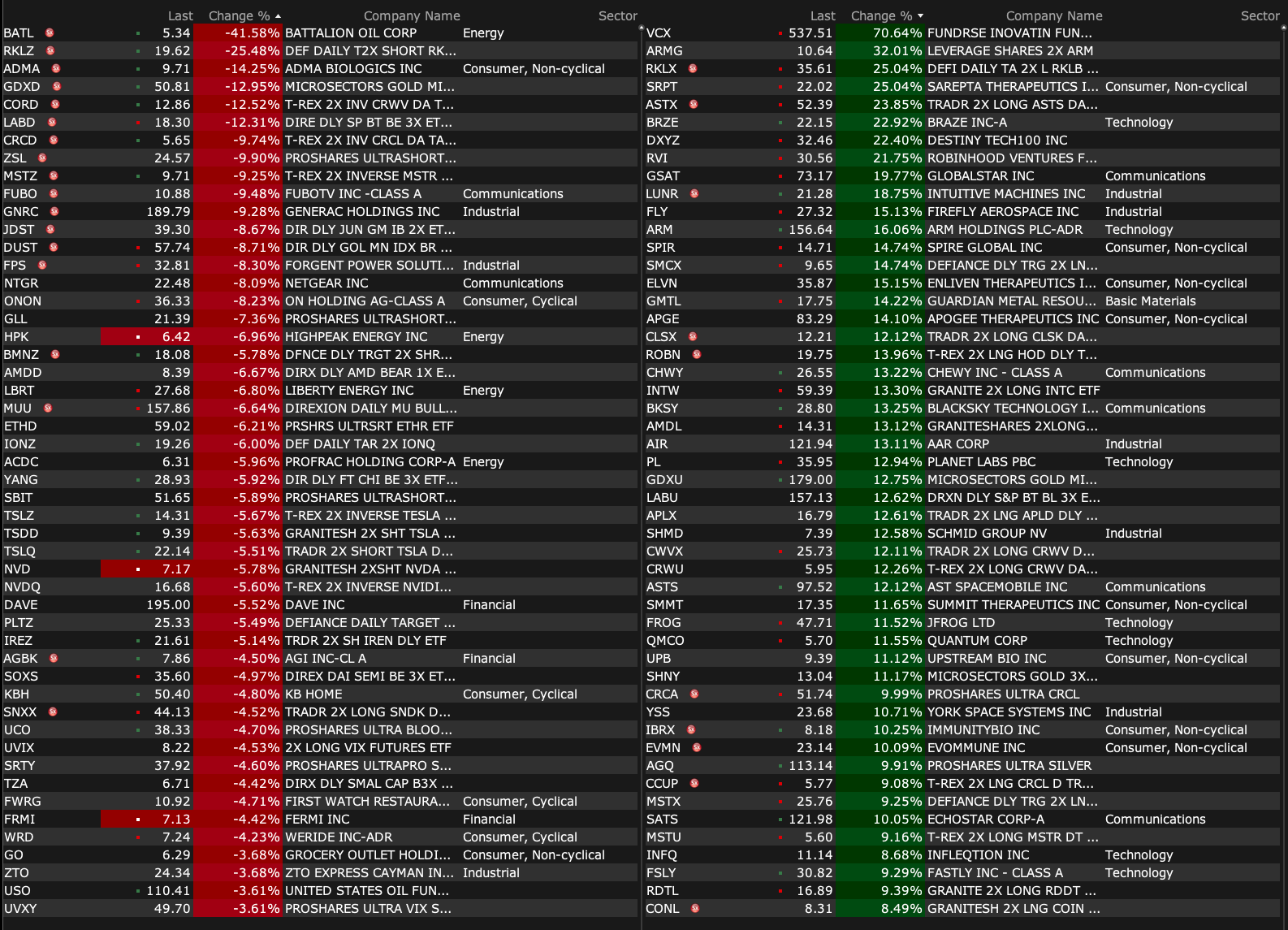

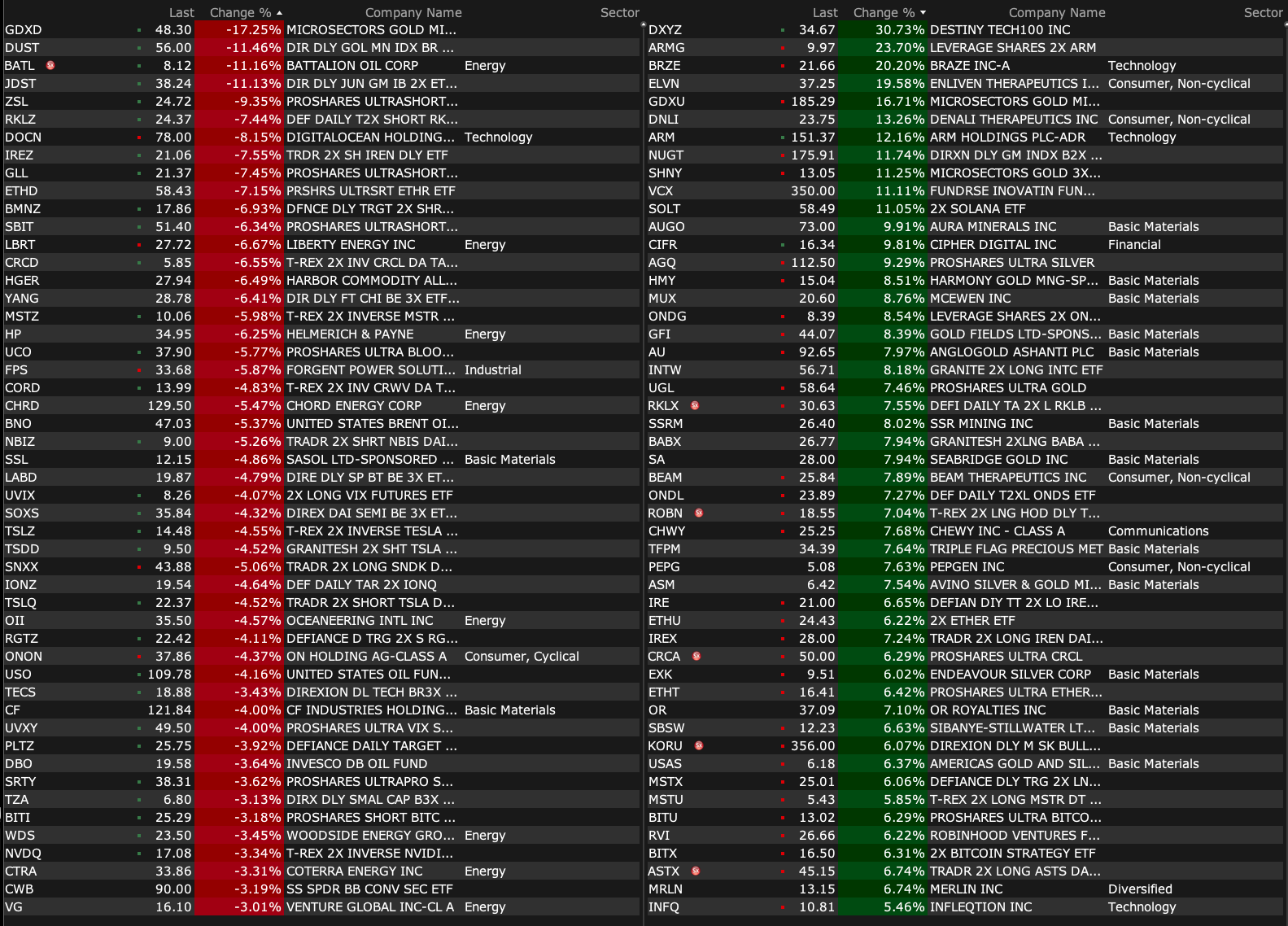

% Movers

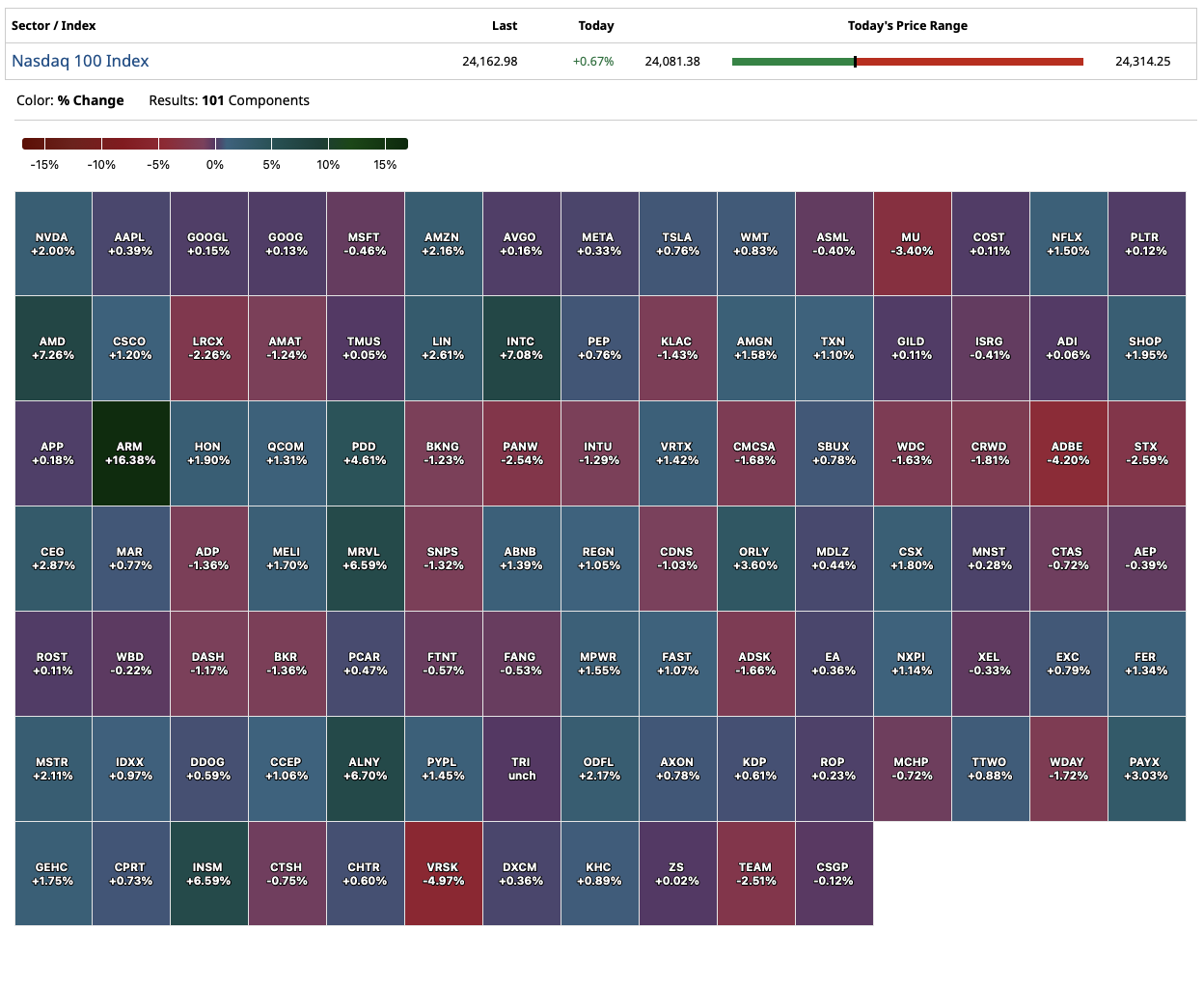

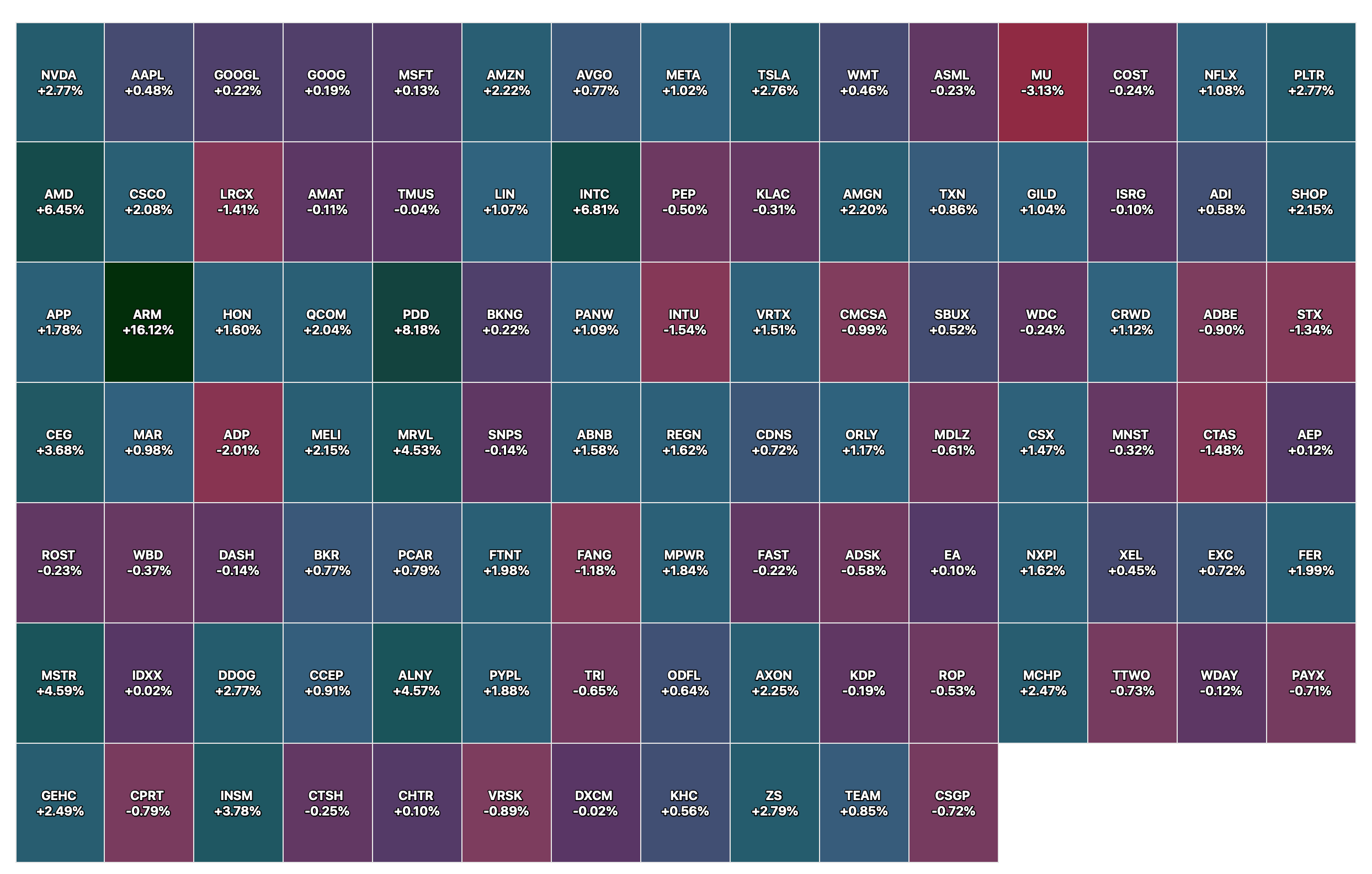

Nasdaq 100 Heat Map

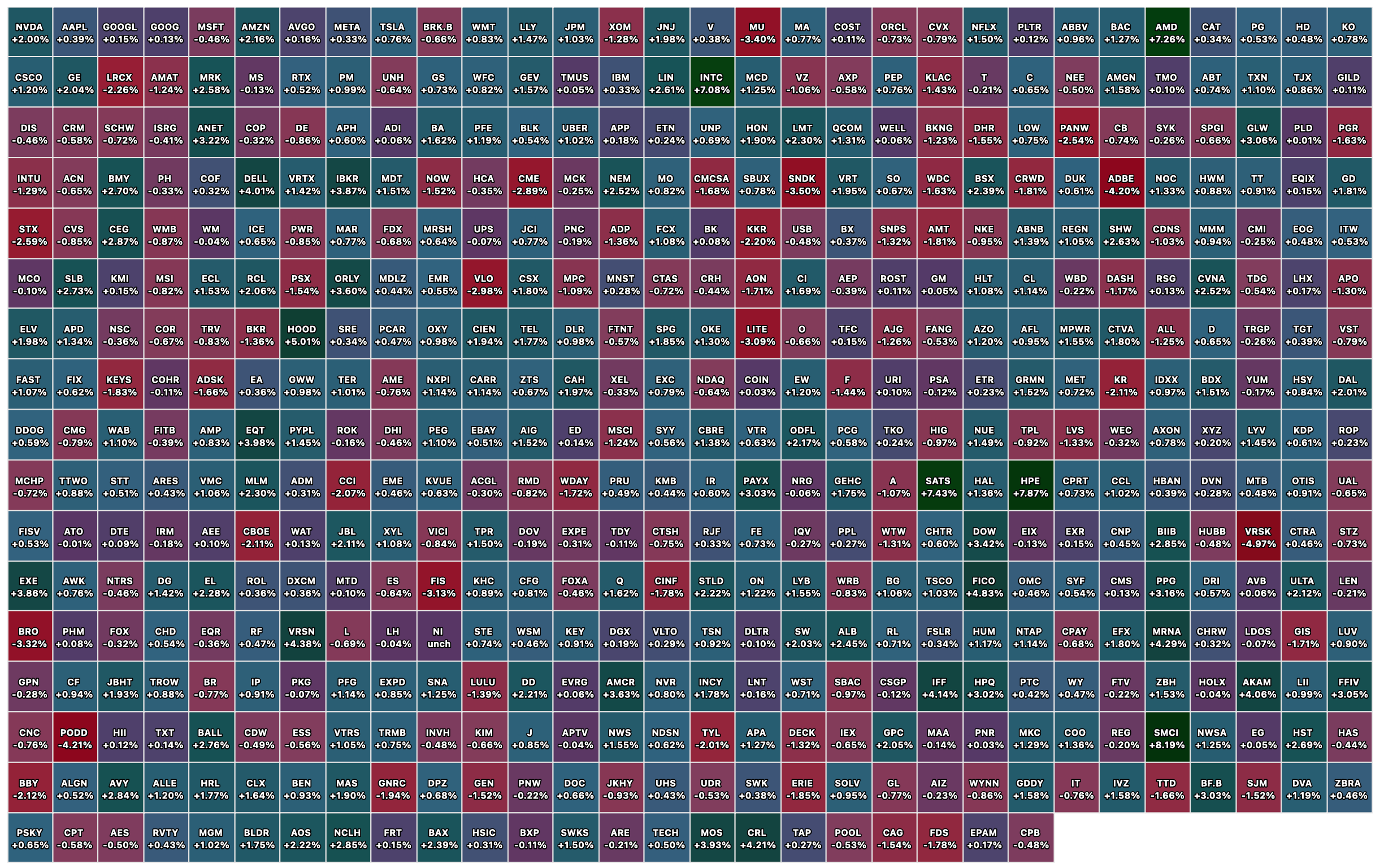

Closing S&P 500 Heat Map

BY Doug Kass · Mar 25, 2026, 4:31 PM EDT

From Shadd and Anthony of The Dales Report — an important interview with Dr. Leigh Vinocur who discusses the CBD pilot program.

I found this quite informative.

🎦 TRADE TO BLACK

— The Dales Report (@TheDalesReport)

📊 Presented by @FlowhubCo

🚨🕧 SPECIAL TIME: *LIVE* @ 12:30pm ET

🎦 Top Cannabis Physician Explains CBD Pilot

🎙️ Dr. Leigh Vinocur, @natcarecouncil Chief Medical Advisor

🌿 ETFs: 🌎 $YOLO 🇺🇸 $MSOS

📈 $SPY $QQQ $IWM #FinTwithttps://t.co/o88cD7wJkA

Position: Long Cannabis

BY Doug Kass · Mar 25, 2026, 4:00 PM EDT

Interesting article on Sora, which was OpenAI's widely hyped animation tool. It is already toast:

Why did OpenAI’s Sora crash and burn?

Despite all the different reasons offered in the article, the real reason was economics. It was a cash sinkhole to the tune of $15 million per day. That works out to $5.5 billion/year. The losses for the system are probably more extreme because the third-party infrastructure providers that they lease capacity from also lose money hand over fist, and so-on. The whole ecosystem is dis-economic.

Yes, there are things that Gen AI can do. But it does them dis-economically. What may appear as productivity enhancing on the margin for certain applications, at times, really is not productivity enhancing because it is delivered at an incredible loss. If it was priced economically for the supply chain, in many cases the human being would be cheaper:

Take the monetary cost first. OpenAI was estimated to be spending $15 million a day on inference to enable users to produce videos, Forbes reported in late 2025. It’s little wonder that the head of Sora, Bill Peebles,

BY Doug Kass · Mar 25, 2026, 3:15 PM EDT

* We are now likely "at the beginning of the end" of the conflict in Iran...

… One can have a broken heart

living in misery.

Two can really ease the pain

like a perfect remedy.

One can be alone in a bar,

like an island he's all alone.

Two can make just any place

seem just like bein' at home.

- Marvin Gaye and Kim Weston, It Takes Two Baby Frankie Gaye And Kim Weston - It Takes Two

My baseline expectation — based solely on my Washington input (who are far more informed than me) — is that the Iranian conflict is at the "beginning of the end" and not the "end of the beginning."

… One can have a dream, baby.

Two can make a dream so real.

One can talk about being in love.

Two can see how it really feels.

Both parties, for different reasons, need to come to an agreement.

Iran has been devastated and is likely defenseless going forward. They will continue to use aggressive rhetoric because that is what regimes that are about to be defeated do.

The Trump Administration doesn't want the conflict to linger. There is an upcoming election in November, oil prices are a regressive tax (hurting those least able to tolerate the increase) and the stock market will likely be imperiled by any further escalation in the conflict. Meanwhile, interest rates and inflationary expectations are rising.

I remain short-term bullish and intermediate-term bearish.

Note: The use of lyrics and the double entendre ("It takes two baby") is not to meant to minimize the horrors of the Iran/U.S. conflict.

BY Doug Kass · Mar 25, 2026, 2:25 PM EDT

I thought the amounts awarded in the Meta/Google court decision were less than expected — a mild positive.

Jury finds Meta and Google liable in social media addiction trial | Reuters

Position: Long META (S), GOOGL (S)

BY Doug Kass · Mar 25, 2026, 1:44 PM EDT

BREAKING: Two senior administration officials have confirmed to CNN that the White House is arranging for Vice President JD Vance to travel to Pakistan this weekend for talks to end the war with Iran. Trump is expected to make an urgent announcement at 7:20 PM ET tonight. The… https://t.co/TVdoMUNi3Z pic.twitter.com/pqW2MVC0EG

— Shanaka Anslem Perera ⚡ (@shanaka86)

BY Doug Kass · Mar 25, 2026, 1:40 PM EDT

Here are today's things:

* Bought and sold (SPY) / (QQQ) three times, all for profits. Net long the indices now.

* Purchased more (AMZN) at $211.14, (GOOGL) at $290.71,0, (META) at $597.25, (MSFT) at $371.90.

* Purchased more (APO) at $111.08, (BX) at $108.94 and (KKR) at $90.07.

* Purchased more (DIS) at $95.61, (NKE) at $53.08.

* Purchased more (KMB) at $98.31, (PEP) at $149.87 and (PG) at $142.64.

* Added to (MSOS) at $3.79 and MSOX at $2.504.

* Added to (UNH) at $268.48.

Position: Long SPY common (S), QQQ common (S), AMZN (S), GOOGL (S), META (S), MSFT (S), APO (S), BX (S), KKR (S), DIS (S), NKE (S), KMB (S), PEP (S), PG (S), MSOS (L), MSOX (S), UNH (S)

BY Doug Kass · Mar 25, 2026, 12:45 PM EDT

I'm back going long the indices:

* (SPY) $656.48

* (QQQ) $587.02

Position: Long SPY common (S), QQQ common (S); Short SPY calls (S), QQQ calls (S)

BY Doug Kass · Mar 25, 2026, 12:27 PM EDT

I sold index calls against my purchase of (SPY) and (QQQ) common with S&P cash +44 handles.

On a delta-equivalent basis I am neutral the indices.

Positions: Long SPY common (S), QQQ common (S); Short SPY calls (S), QQQ calls (S)

BY Doug Kass · Mar 25, 2026, 12:00 PM EDT

Buying back the indices with S&P cash +18 handles (down in reaction to the strike at Iran's nuclear plant):

Iran Bushehr nuclear power plant has reportedly been struck again; Unclear if the plant or the adjacent site has been damaged - press

Buys at:

* (SPY) $654.81

* (QQQ) $586.32

Position: Long SPY (S), QQQ (S)

BY Doug Kass · Mar 25, 2026, 11:27 AM EDT

- NYSE volume 20% below its one-month average;

- Nasdaq volume 9% below its one-month average;

- VIX index: down 6.20% to 25.28

None.

BY Doug Kass · Mar 25, 2026, 11:14 AM EDT

From Peter Boockvar:

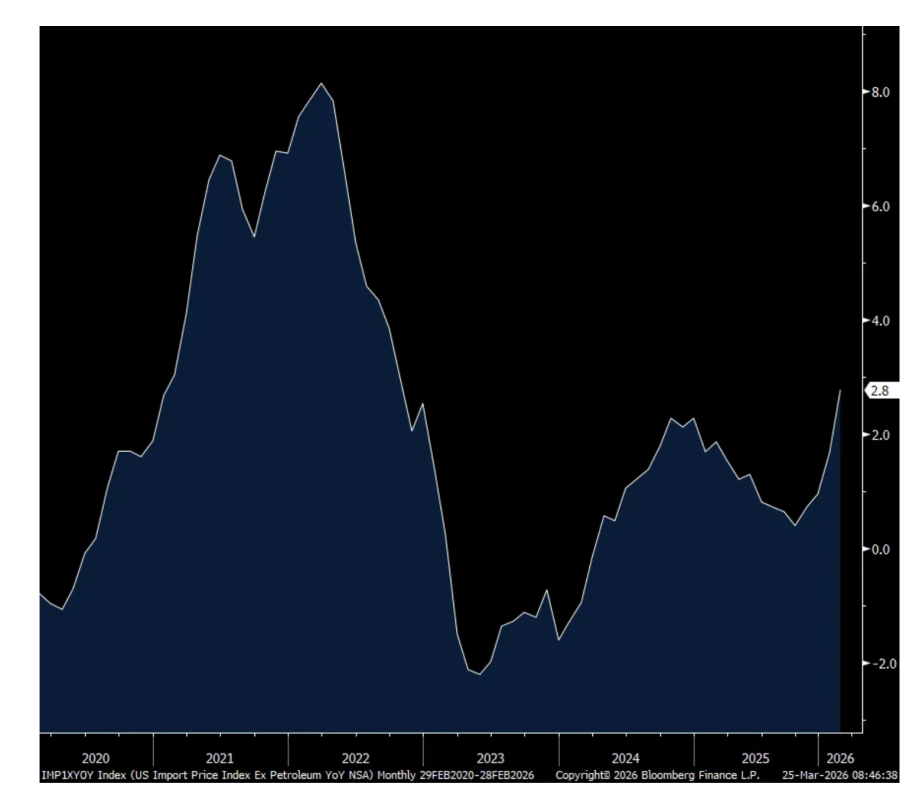

Even before the war, we saw last week the February PPI jump and today for February import prices did as well. They rose 1.3% m/o/m, about double the estimate of up .6% and also comes off an upward revision to January which saw an .8% rise vs the initial print of up .4%. Prices ex food and fuels saw prices rise by 1.2% in the month and are now up 3% y/o/y. They are up 2.8% y/o/y ex fuels.

Driving the gains was a 3% rise in industrial supplies m/o/m, a 1.3% increase in capital goods, a .5% gain in consumer goods, an .8% move up in foods/beverages and a more modest rise of .2% in autos/parts.

Again, consumer price inflation statistics are not the only measure and arbiter of inflation as just because there might not be full pass through of cost pressures doesn’t mean the cost pressures have disappeared as they get eaten by lost profit margin instead. And this also ties into the slowdown in the demand for hiring. Companies are looking to cut costs and labor is the biggest expense for most.

This then gets into the debate over monetary policy. If the labor market further weakens, should the Fed focus on that and cut rather than stick tight until inflation falls? Well, if inflation is the reason for the slowdown in hiring, rate cuts are not going to drive more hiring.

Import Prices ex petro y/o/y

BY Doug Kass · Mar 25, 2026, 10:39 AM EDT

From Peter Boockvar:

It is even more apparent that there is a clear desire for an exit ramp from this war, whatever it might look like and the war trade is reversing in kind.

Following the poor 2 yr note auction yesterday, the US Treasury will sell $70b of 5 yr notes today but I will be in transit to CNBC and won’t be writing on it. I will rely on Rick Santelli and his grading of it.

I’m sure we all are trying to find ever article to read about the ripple effects of the Strait closure. Here are a few of note that I’ve found. From Nikkei News, “Japan relies on the Middle East for more than 40% of its supply of naphtha, which has become tougher to procure...Although around 40% of demand is met through domestic supply, this is produced from crude oil, more than 90% of which is imported from the Middle East. At least six of Japan’s 12 ethylene production facilities have cut production to conserve naphtha.”

From a Bloomberg News article yesterday, “Sulfur is trading at an 18 year high as key Persian Gulf supplies are kept off the market.” Not only is sulfur used to make sulfuric acid which is a key input to making the fertilizer phosphate, but it’s also used for the leaching process in mining copper and other metals to strip the metal from the ore. “In normal times, more than 90% of sulfur supply to the African copper belt, which uses about 1.2 million tons a year to extract metal from ores, is shipped via Hormuz...Inventories at the Tanzanian port of Dar es Salaam, a key sulfur storage hub for African miners, should last two months, but concerns are growing over the risk of a protracted supply shock,” said Argus in the article.

From a story from them today, “Signs are growing that Asian countries are hoarding jet fuel after the Iran war sent oil prices surging, reflecting growing strain on the aviation industry. South Korean carriers got notified about refueling restrictions from some countries and the government is discussing whether to redirect export bound jet fuel to the local market, the nation’s transport ministry said in a statement to Bloomberg on Wednesday. Philippine Airlines president said in an interview that the Southeast Asian nation may soon resort to fuel rationing. In Vietnam, the aviation agency warned of potential jeet fuel shortages from early April and is cutting flights as a result.”

Lori Ann LaRocco wrote for gCaptain Daily yesterday:

“Over 80% of the world’s 454 ports mapped are deemed in critical status, 60-70% are severely congested, and 45-59% are considered highly congested.” According to a market analyst at Xeneta, “This shows the impact of the three waves of disrupted cargo. The first wave was vessels already in or near the Persian Gulf when the conflict started, the second wave was vessels that departed from Asia before suspensions were announced, and the third wave is of cargo bookings currently being made.” As a result, “All of this has led to the deterioration of vessel schedules.”

And what is the industry reaction? “To circumvent the container contagion, ocean carriers are making the logical decision to suspend services, update their services on other routes, and charge more. The longer routes burn more fuel, and that fuel is way more expensive. Slow steaming is also used, but it adds time to an already behind schedule.”

https://gcaptain.com/container-contagion-global-trade-choked-as-war-driven-congestion-hits-ports/

To a few earnings reports.

From Smithfield Foods, the packaged meat company, a stock up 4% yesterday and who recently announced they are buying Nathan’s Famous:

“Protein demand is strong and growing across consumer demographics, valued for its nutrition and health benefits. Pork, which is not our only protein but is our primary offering, is well positioned within the protein complex. Pork presents a strong relative value to beef and its nutritional profile with lean cuts like pork tenderloin offers a superior nutritional alternative to chicken breast. Pork is also central to Asian and Latin cuisines, which are popular with US consumers, particularly among Gen Z and Millennials.”

They did mention that “Industry wide volume growth has been challenged due to inflation and consumers’ tight budgets.” And, “The higher average selling price was driven primarily by higher market prices across the pork value chain with key raw materials such as bellies up 19%, trim up 19% to 35% and ham up 9% y/o/y.”

As to the impact of the war, “It’s still too early to predict the full impact...but there are three main components of our business that this could impact. First, the direct impact of fuel costs such as diesel. Second, corn prices, which are tightly correlated to the oil markets. Third, the petroleum derived supplies that we use, such as resin based packaging.”

KB Home is looking down pre market and they said this of note:

“Consumers have been faced with a variety of challenges over the past two years. And the conflict in the Middle East that began at the end of February has added another layer of uncertainty. Against this backdrop, and taking into consideration that our net orders in the first quarter were below the level we needed to hold our prior full year delivery guidance, we are lowering our range for the year.”

“Near term, buyers continue to demonstrate the desire for homeownership and the ability to qualify, although tepid consumer confidence, elevated mortgage interest rates, and affordability pressures have stifled underlying demand.”

As for the cadence of business, “December was a slower start for us and put us behind on our y/o/y comp. Then we saw solid momentum through January and February and ultimately finished the quarter up 3% y/o/y. As to March, the last couple of weeks of March have been a little softer than we would have liked, and this conflict in the Middle East which kicked off right at the end of February, beginning of March, there’s clearly some near term pressure on the consumer psyche from that, and that’s one of the things that’s limiting some of the visibility in the short term.”

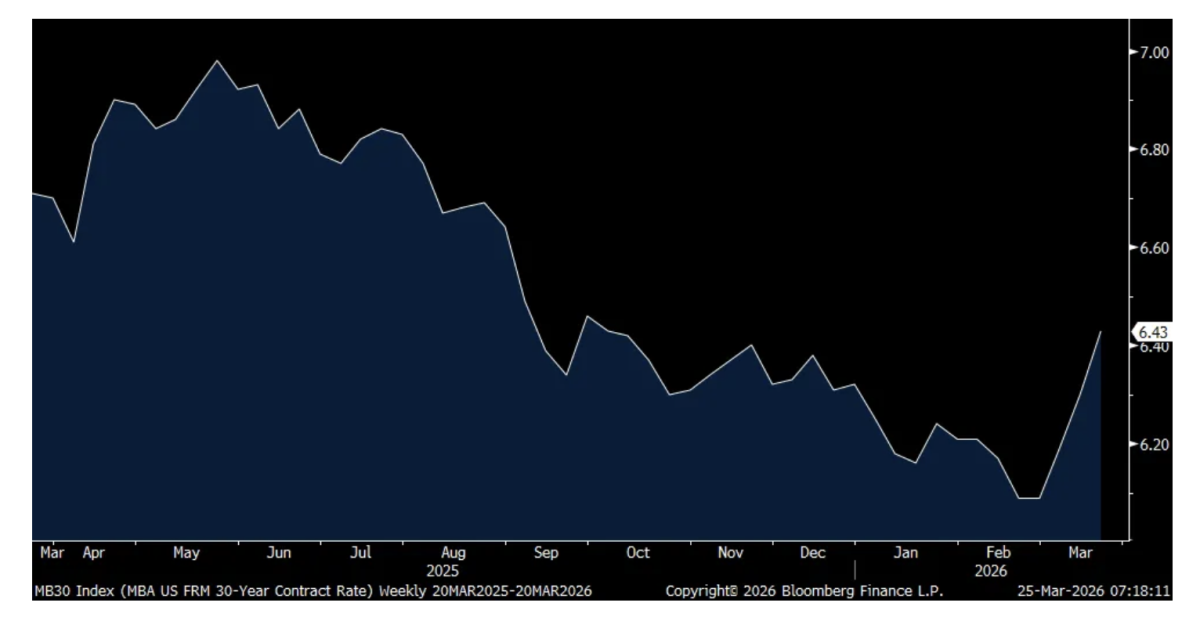

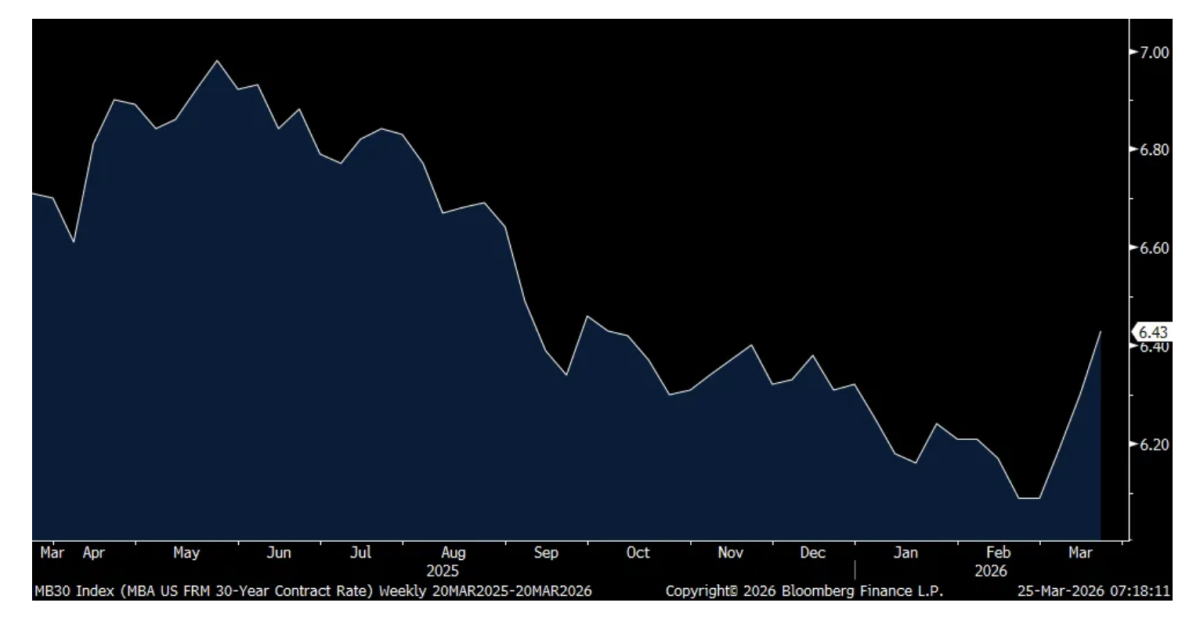

The jump in mortgage rates and maybe some of the change in consumer psyche was reflected in weekly mortgage applications where purchases fell 5.4% w/o/w. With refi’s, solely driven by rates, dropped by 14.6% after falling by 18.5% in the week before. The average 30 yr mortgage rate has moved up to 6.43% from 6.09% just before the war.

Average 30 yr Mortgage Rate

To some data overseas. The March German IFO business confidence index fell 2 pts m/o/m to 86.4, the lowest since February 2025, with all of the weakness in the Expectations component as the Current Assessment was unchanged. IFO stated the obvious, “Uncertainty among companies has increased noticeably. The war in Iran has put any hope of a recovery on ice for the time being.”

IFO

On the heels of the RBA rate increase last week, the pre war, February Australian trimmed mean CPI rose 3.3% y/o/y, the same pace seen in January while the headline figure rose 3.7%.

In the UK, February CPI was up 3% y/o/y as expected with a core rate increase of 3.2% because of continued high inflation in services which rose 4.3% y/o/y. PPI jumped .8% m/o/m, above the estimate of .5% but all of this is old news as we know.

BY Doug Kass · Mar 25, 2026, 10:15 AM EDT

* For now, "home home on the (trading) range"

* However, my baseline expectation is that the S&P index has likely made a year high and that a high single-digit to low-double-digit return is likely in 2026

Several subscribers have asked me why I have gotten so aggressive in buying individual equities over the last two weeks, especially into the teeth of the Iranian/U.S. conflict and, given my belief that the administration is undertaking questionable, uncertain and, possibly dangerous policy moves in the Middle East.

To quote Jeremy Grantham:

"The market does not turn when it sees light at the end of the tunnel. It turns when all looks black, but just a subtle shade less black than the day before."

While I am encouraged short term, as noted in "Growing Less Bearish" last month , I remain of the view that we have likely seen the highs of the year and that a high single digit to low double digit loss in the S&P Index is my baseline expectation.

In the meantime, I continue to trade opportunistically and, into what I consider to be a broadening trading range over the next few months. (Baby steps and opportunistic trading is my mantra!)

With differing market views by many, it is a good time to repost my previous column (of three weeks ago) in its entirety this morning:

MAR 16, 2026 9:35 AM EDT

* Though P/E ratios remain elevated — investor sentiment has soured, positioning is defensive and many of our concerns are being realized

* Uncertainty remains present and a strong conviction (either way) does not yet seem appropriate

* Given the plethora of multiple challenges and headwinds — that have only recently been acknowledged by many investors — I expect a longer bottoming process than in the past... so the customary "V" market bottoms (made over the last three years) seem unlikely

* We are applying "second-level thinking" today and with many stocks -25% or more, a modestly net long exposure now seems appropriate (a shift from our long standing and slightly net short exposure)

* It is increasingly possible that I will be "returning to the land of the living" by sensibly and gradually expanding my long exposure in the weeks and months ahead

* The S&P Index is down by about -4% year to date — I continue to expect a high-single-digit negative to low-double-digit negative return for the year

* Over the balance of the year (as was the case in January-March), stock picking will be crucial and, when done well, value-added to portfolios

* Always remember: short selling protects capital, long buying creates capital

"Buy to the sound of cannons, sell to the sound of trumpets."

- Baron Nathan Rothschild

In recent weeks, equities have finally begun to reflect my prevailing fundamental, valuation and geopolitical concerns:

The purpose of today's opening missive is to convey that, to me, the times (and markets) they are a-changin':

Come writers and critics

Who prophesize with your pen

And keep your eyes wide

The chance won't come again

And don't speak too soon

For the wheel's still in spin

And there's no tellin' who

That it's namin'

For the loser now

Will be later to win

For the times they are a-changin'

- Bob Dylan, The Times They Are A Changin'

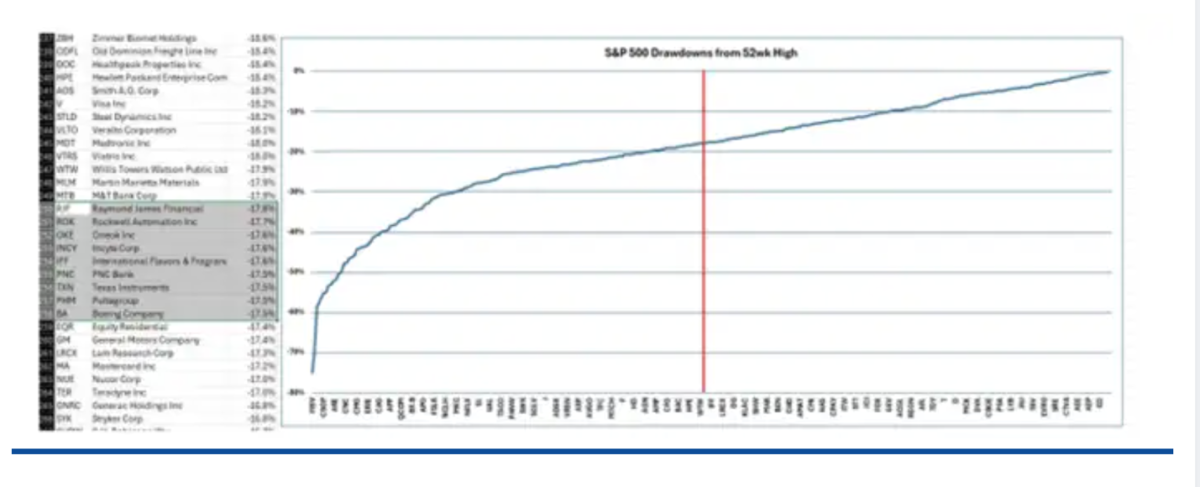

Under the ominous cover of the Iran conflict (and its economic ramifications), many stocks have quickly turned down by -25% or more, creating potential opportunities. The median S&P 500 Index stock drawdown is -18% (from the 52-week high):

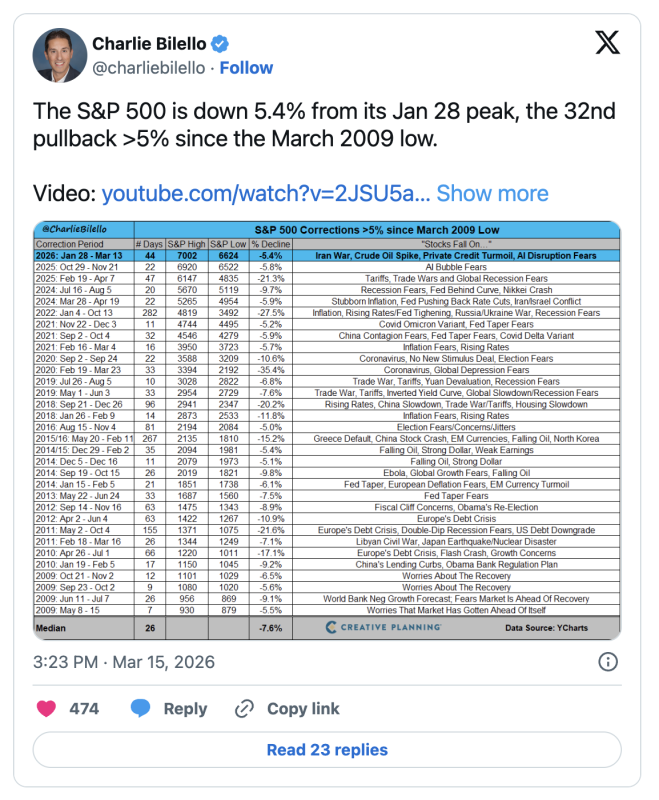

The S&P Index is now -5.4% from its peak in late January 2026. That is the 32nd pullback greater than 5% since the March 2009 Generational Bottom:

The "league leading" Mag 7 bubble has burst — falling more than -10% below its October record. For the first time since 2022, all seven constituents are negative year to date:

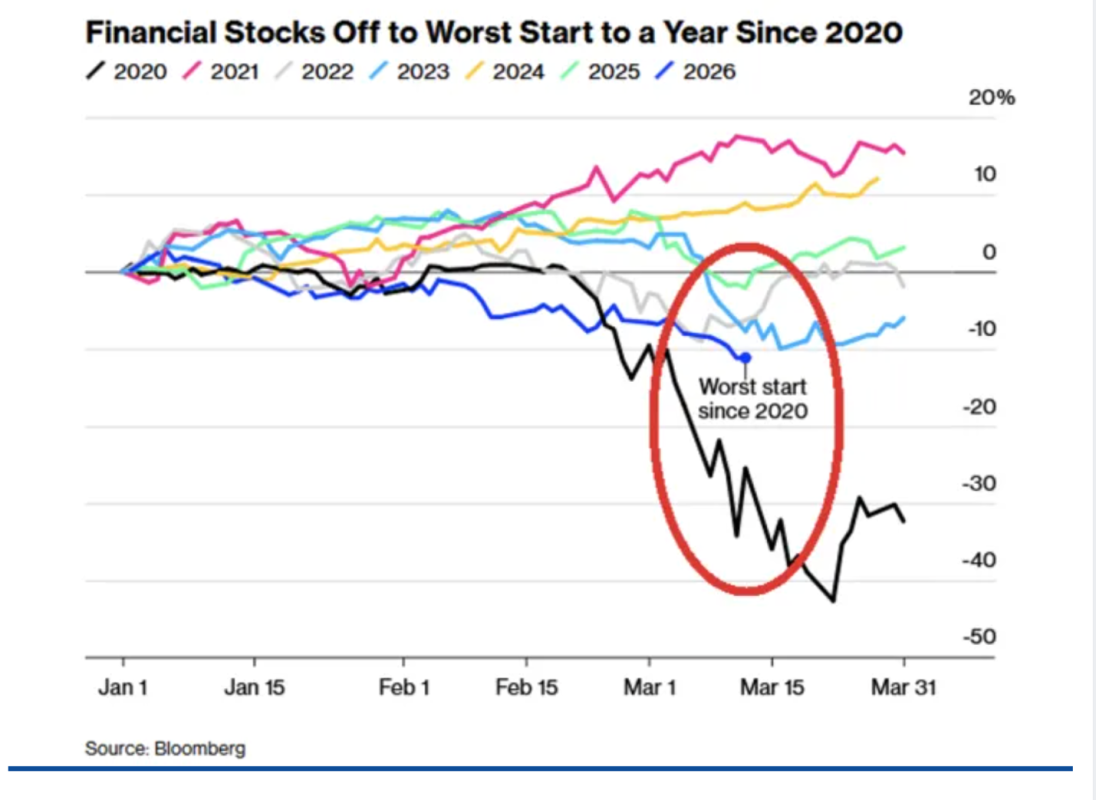

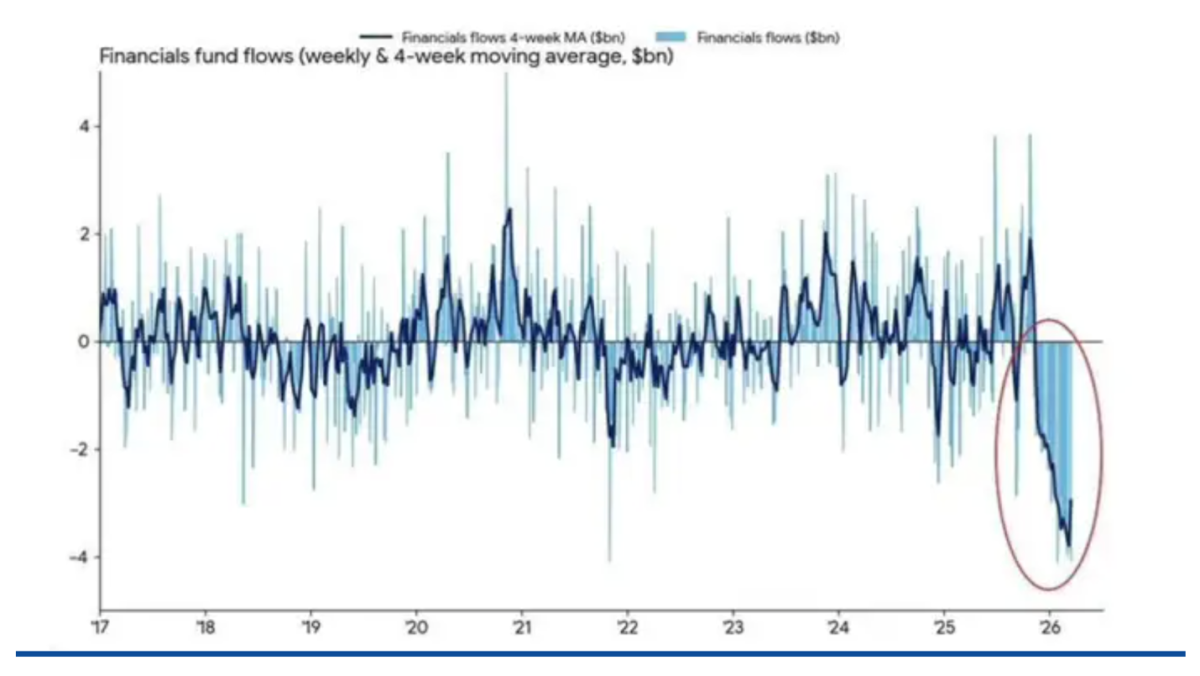

The S&P 500 Financials Index is -12% year to date — on track for the largest quarterly decline since early 2020. Private credit equities are down by over -30% year to date:

According to Bank of America, financial fund inflows are breaking records:

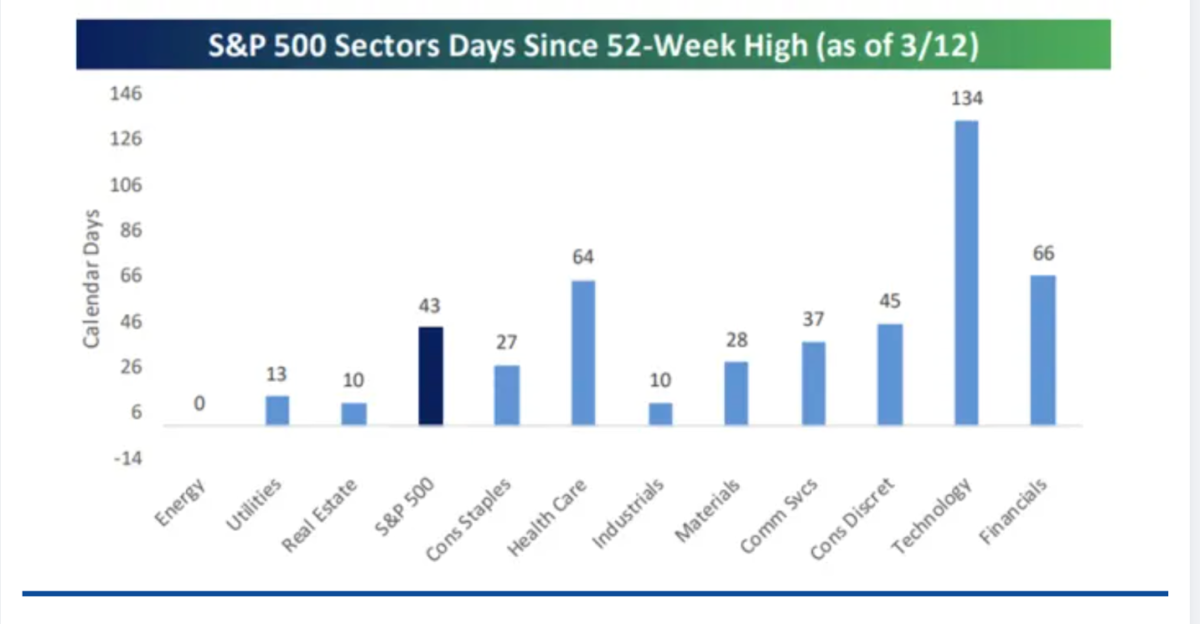

It has been over 40 days since the S&P Index reached its last 52-week high but 134 days since the Tech sectors' last 52-week high:

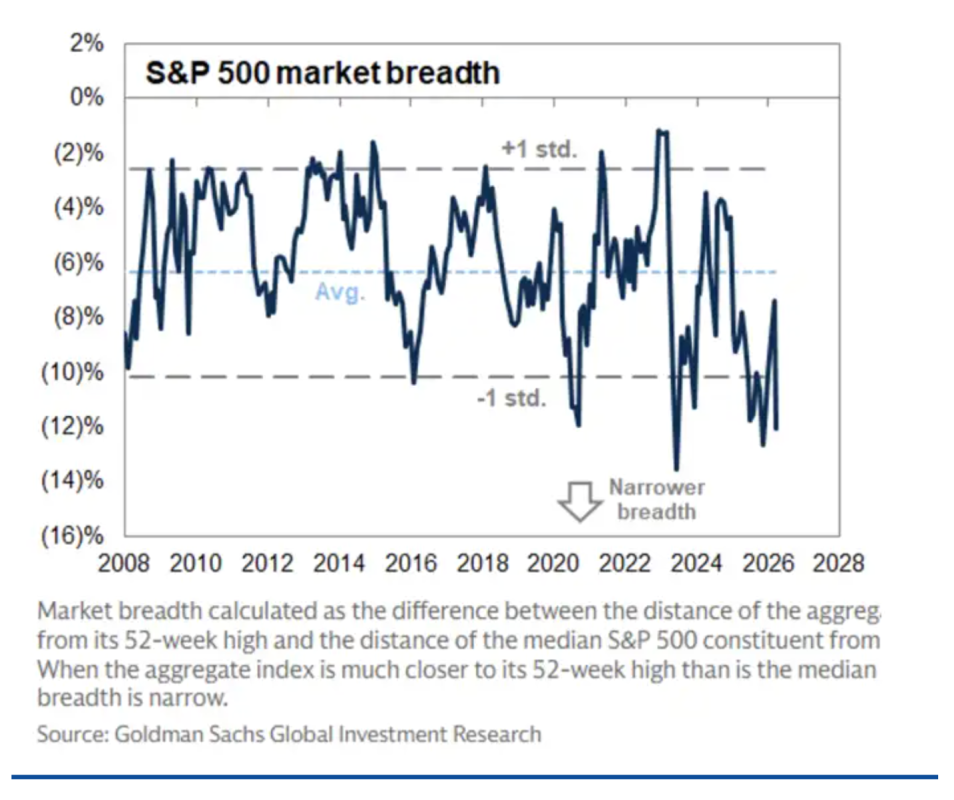

Meanwhile, market breadth (measured below by the gap between the S&P Index and its median stock relative to their 52-week highs) has a foul odor and may be approaching an extreme:

Besides the sharp fall in several market sectors, I am increasingly encouraged by the buildup in fear and that many market participants are coming around to acknowledging our multiple concerns.

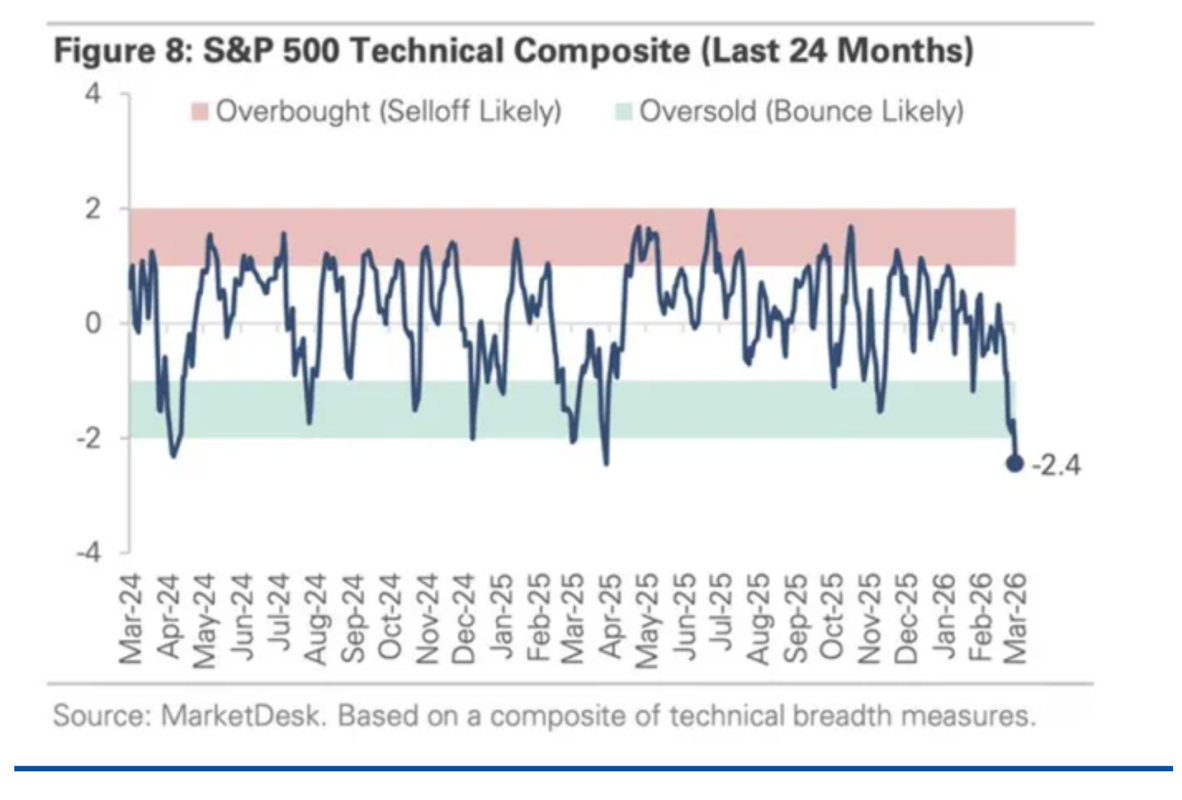

No longer overbought, the S&P Index has hit the most oversold in 24 months (this morning the S&P Short Range Oscillator hit -7.87%):

Money flows into (SPY) (the largest ETF) are nearing a bottoming level seen during the 2018, 2020, 2022, and 2025 crashes (a bottom is near in terms of time, not necessarily in the magnitude of the flush. A bounce must be sustained in the short and long term. See the local bottom of March 2022 for context):

As to Iran, today I am reminded of Baron Nathan Rothschild's famous quote (mentioned earlier):

"Buy to the sound of cannons, sell to the sound of trumpets."

Along with lower stock prices I have turned less bearish. As an example, I recently wrote in a letter to Seabreeze investors (my hedge fund):

In anticipation of a market correction/bear market we have substantially bolstered our cash position in order to take advantage of the possible developing long opportunities.

The purpose of today's (mid-month) commentary Is to highlight that while markets have and may continue to move lower — considering the recent pace of decline, better values in the U.S. stock market are likely to emerge.

Accordingly, I have moved from a small net short exposure to a small net long exposure over the last several days. Should equities continue to fall — and subject to macro conditions (inflation, interest rates, economic and corporate profit growth, etc.) — it is increasingly possible that I will be "returning to the land of the living" by sensibly and gradually expanding our long exposure in the weeks and months ahead.

Though fear is elevated, over the short term much will depend on how long the Strait of Hormuz is closed. If the Strait remains closed another two weeks, the price of crude oil will remain high. This makes interest rates very challenging given how elevated P/E multiples are (below). This uncertainty suggests that a strong conviction (either way) does not seem appropriate — and a modestly long net exposure seems appropriate.

Equities continue to appear overpriced against history — this should be a limiting factor against "V" rallies:

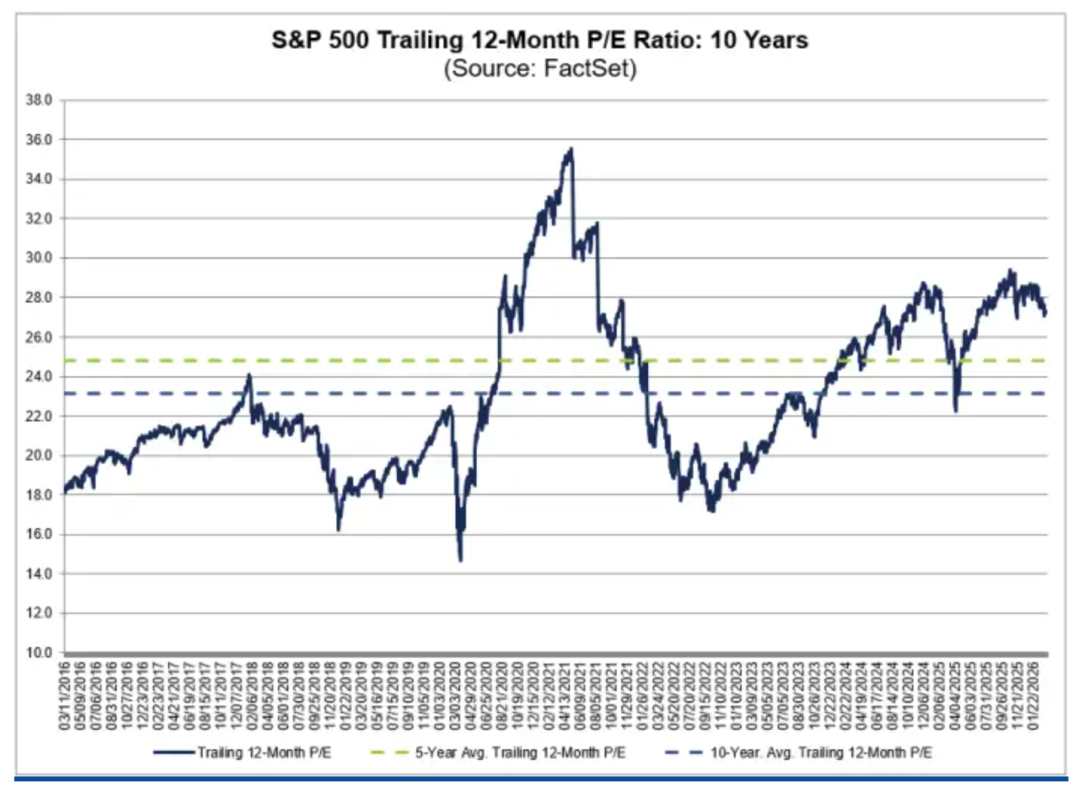

The trailing 12-month P/E multiple for the S&P Index is 27.2x, above the five-year average (24.8x) and above the 10-year average (23.2x):

No "V" Market Bottom Expected

I recognize that buying opportunities since early 2023 have been very brief and short-lived. With the benefit of hindsight, it was important to be prepared and bold to capture previous opportunity sets. This time, given the plethora of multiple challenges and headwinds — that have only recently been acknowledged by many investors — I expect a longer bottoming process that in the past. Accordingly, I will likely proceed in buying on a measured basis, waiting for the "right pitch."

Rarely Have Outcomes Been So Wide

For some time, I have been of the view that investors were underappreciating the risks of adverse geopolitical, economic and/or market outcomes — with many of them not friendly to stock prices and valuations. These concerns existed with valuations at about the 98%-tile and an equity risk premium that was slowly moving in the direction of being an equity risk discount.

Despite elevated valuations as well as reckless fiscal policy and rising geopolitical uncertainty — market participants put all of the concerns on the shelf. Stocks marched higher in 2023-2025. steadily climbing even though the probability of adverse outcomes were multiplying and gaining in probability.

The recent outbreaks of war in Iran (and Venezuela) are examples of adverse geopolitical developments (that I warned about in my 10 Surprises for 2026) that were universally ignored. The more serious U.S. incursion into Iran, in particular, is not an isolated adverse outcome. It is happening at a time in which the U.S. economy is slowing down, the rate of inflation is accelerating, and interest rates are rising:

* Slowing Economic Growth: According to the Commerce Department (on Friday) 4QGDP growth was only +0.7% — revised from the previous estimate of +1.4% and well below the consensus of +1.5%. Moderating domestic economic activity will feed into and weaken consensus S&P 2026-27 EPS expectations which remain too high.

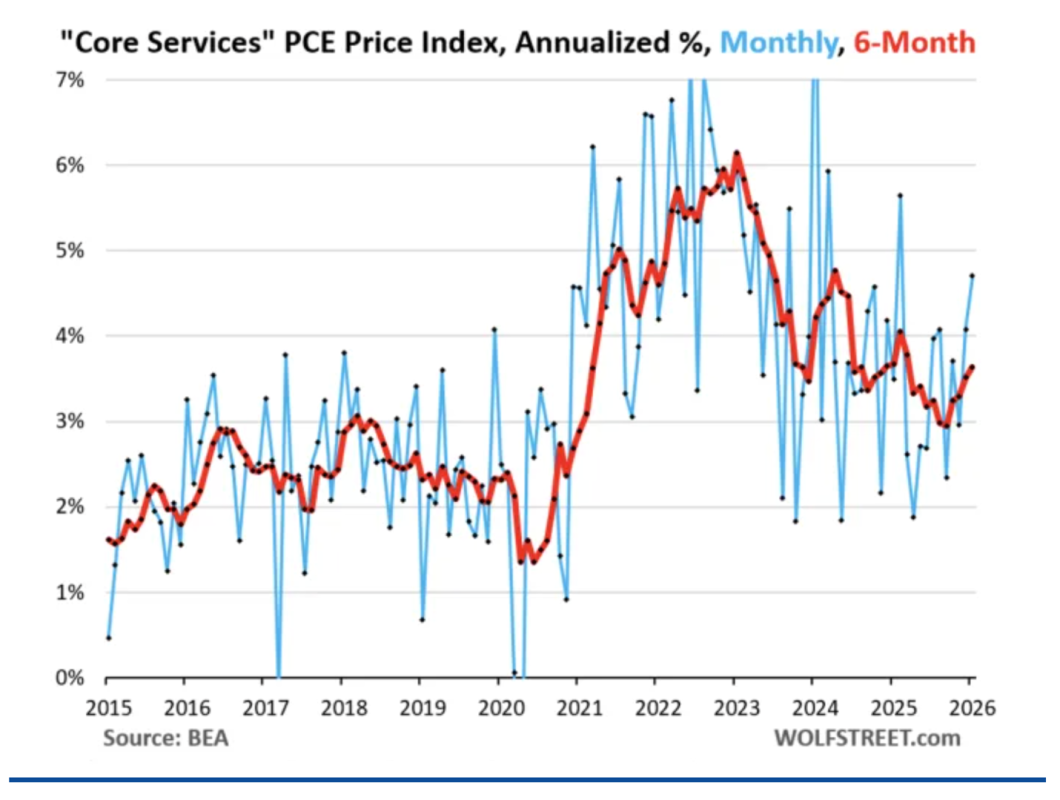

* Prickly Inflation: It was reported on Friday that February’s core PCE inflation rate (the Fed's favored inflation measure) hit 3.15%, the worst in two years — driven principally by core services which account for roughly 60% of the overall PCE price index (the energy spike is still to come).

The previously reported January core services PCE price index accelerated sharply both on a month-to-month basis (+0.38% or +4.7% annualized, blue line in the chart), and a six-month basis (+3.6% annualized, red line). This acceleration in January came on top of the acceleration in December. Year over year, the core services PCE price index accelerated to 3.4%. And it did so despite the deceleration of its housing components:

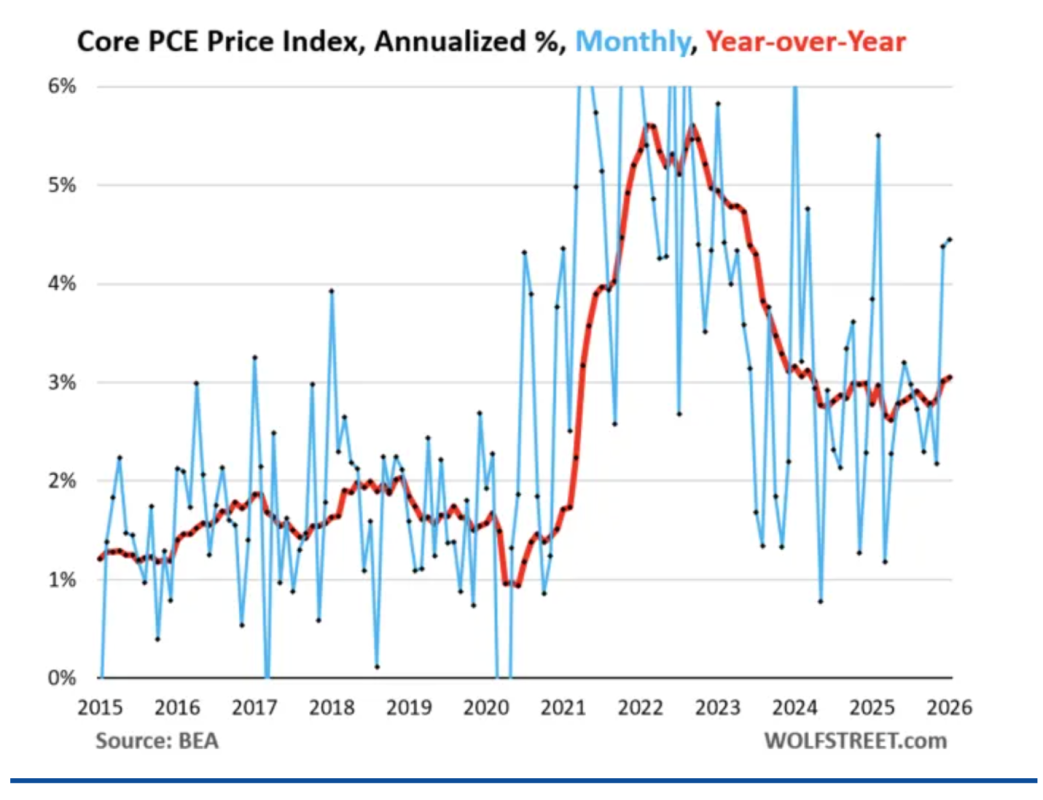

The January core PCE price index, driven by core services, jumped by +0.36% (+4.5% annualized, blue line) in January, after the big jump in December. Year over year (red line), it accelerated to +3.1%, the worst in nearly two years. It has been zigzagging higher and ever further away from the Fed’s 2% target since May 2025:

* Rising Interest Rates: Since the Iran conflict started on February 25, the yield on the 10-year Treasury note has risen by 38 basis points. This has contributed to a sharp rise in mortgage rates (from slightly below 6.00% last month to 6.28% today) and to an expanding equity risk discount.

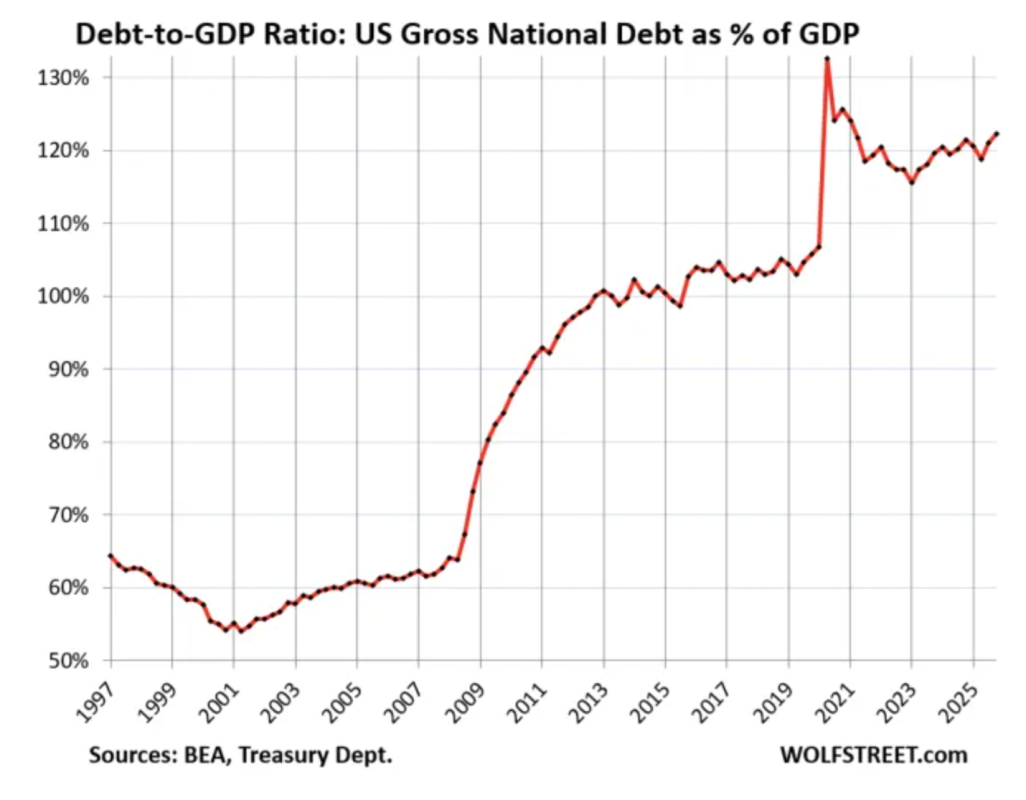

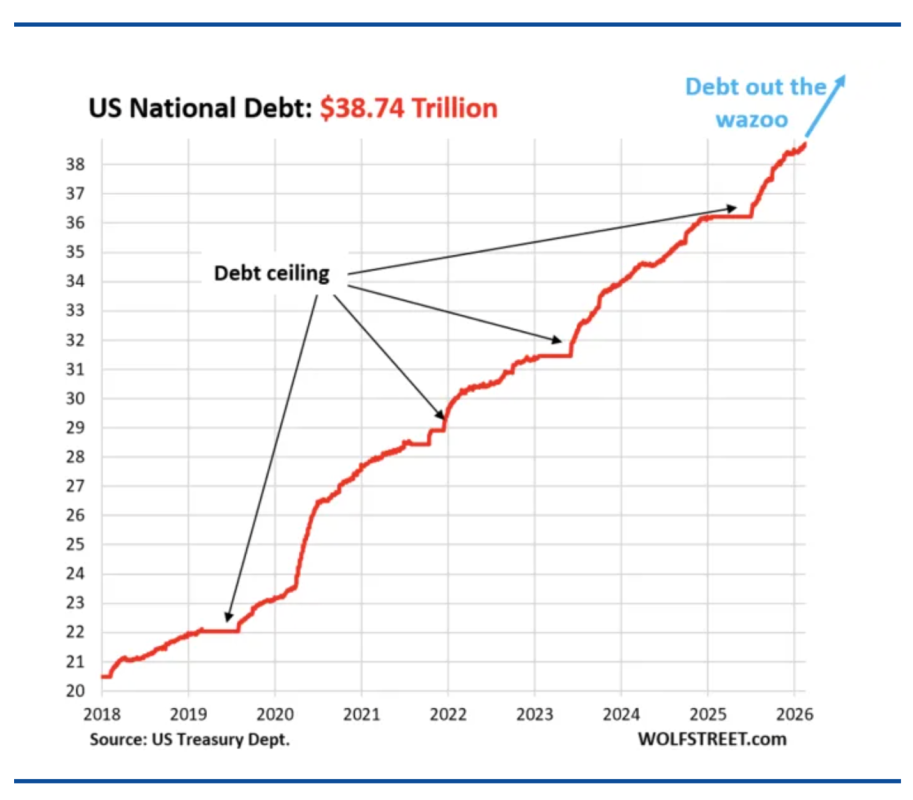

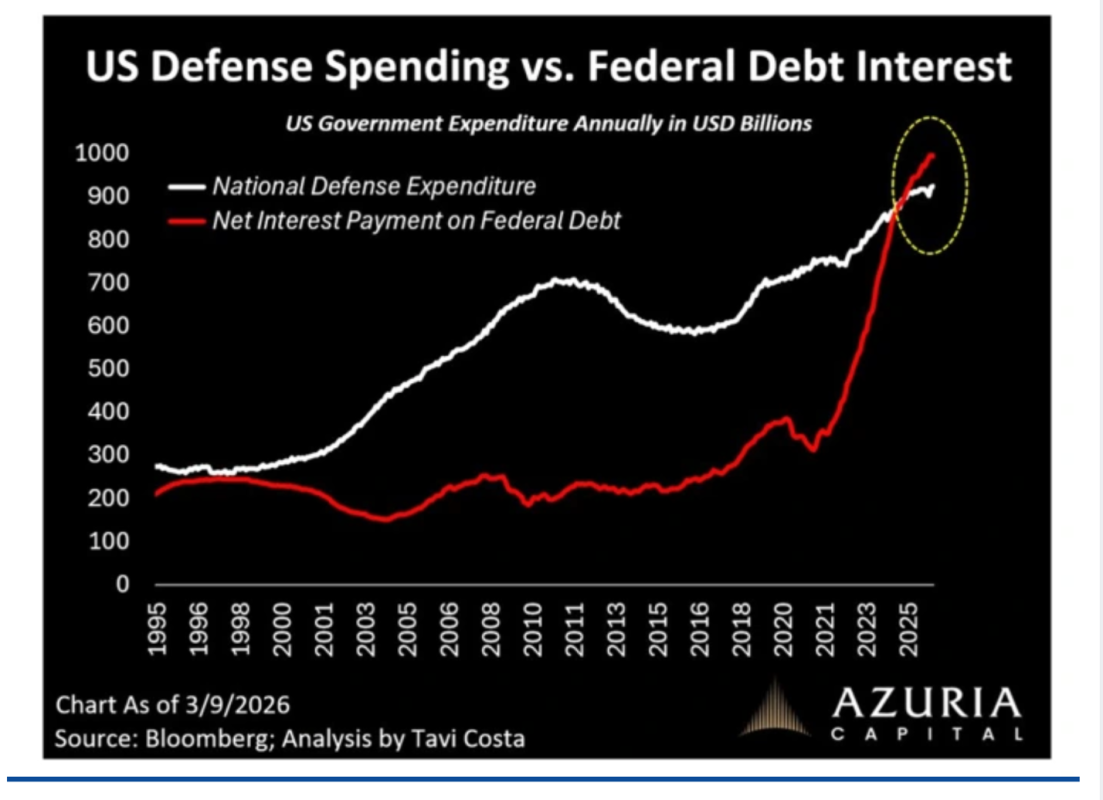

The war with Iran will ultimately be resolved. From an intermediate-term standpoint it is the cost and amount of U.S. debt that represents a growing existential threat:

* The Federal Reserve's Hands Are Tied: The Fed is now in something of a box as it needs to pay attention to the rise in the core PCE price index (of 3.1% and far from its 2.0% target) — especially with so much fiscal stimulus in the economy (government deficit spending, tax cuts for companies and individuals, bigger tax refunds to consumers now during tax-refund season, massive corporate investments in anything related to AI, too-low interest rates, and too narrow spreads.

Inflation feeds on these combined conditions.

Be Greedy When Others Are Fearful?

While the major indices are down only modestly from all-time highs, many equities are down in excess of -25%.

Until recently, we have seen a Bull Market in Complacency, as over the last year, fear and doubt have left Wall Street.

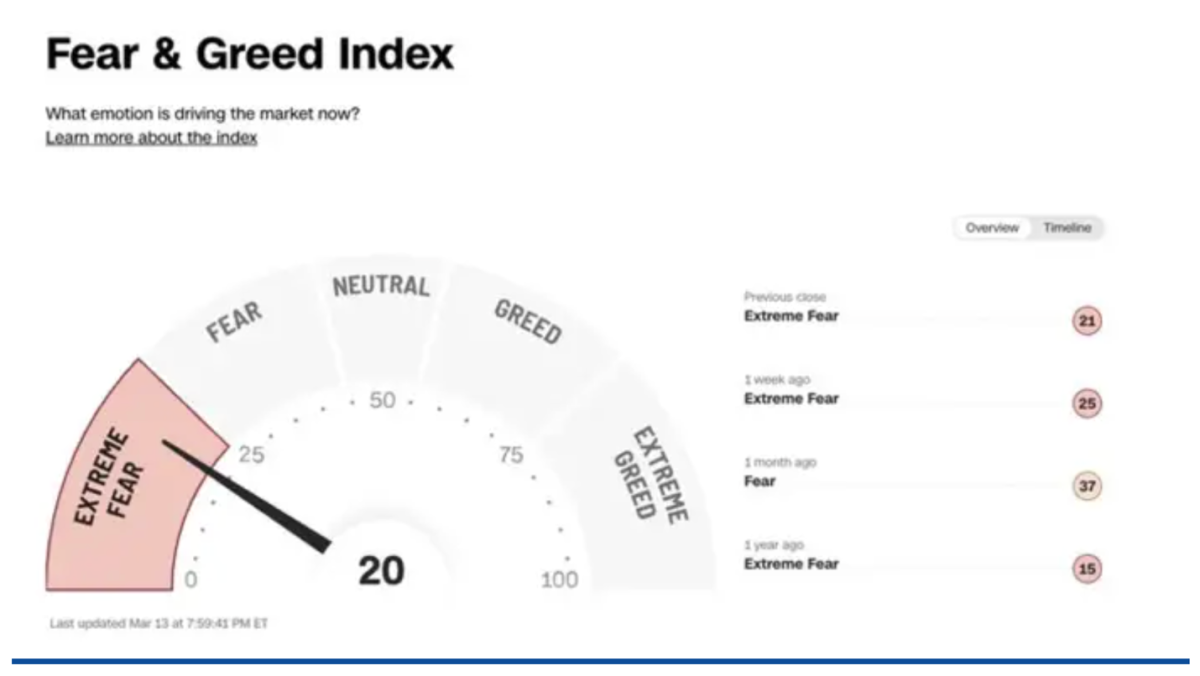

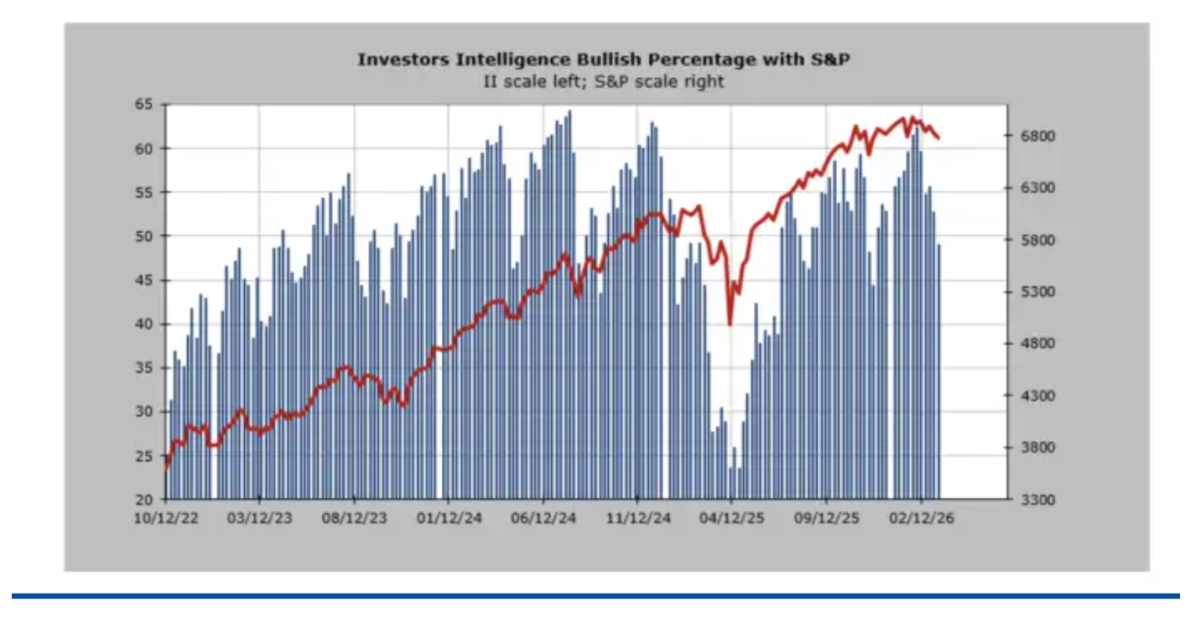

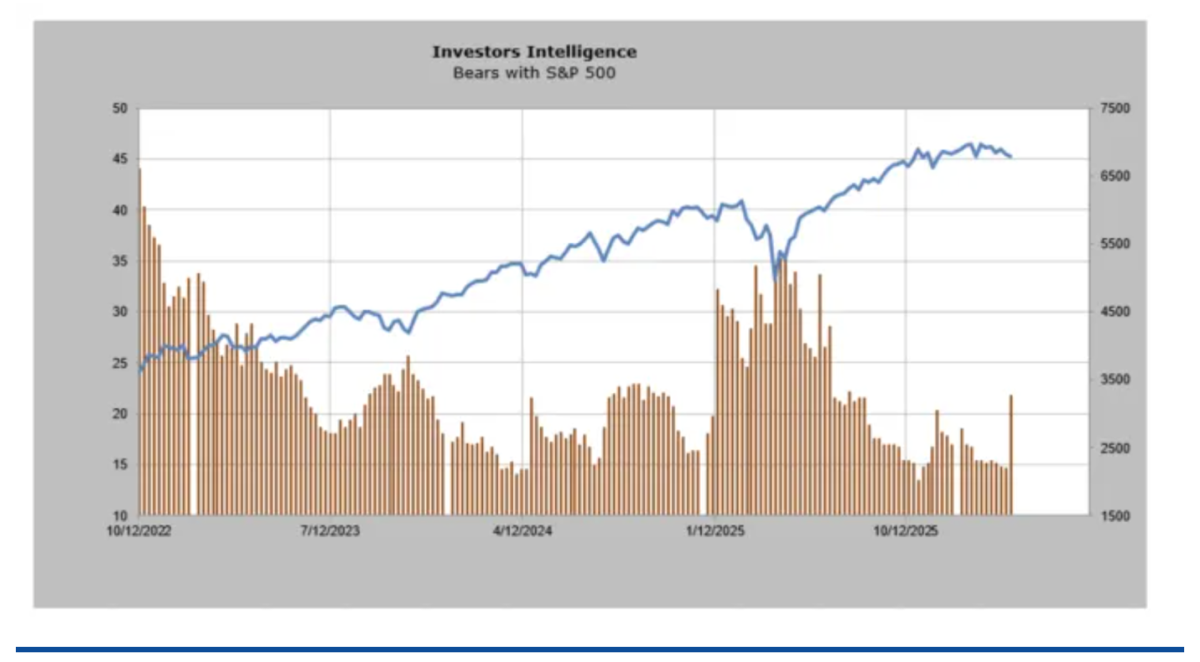

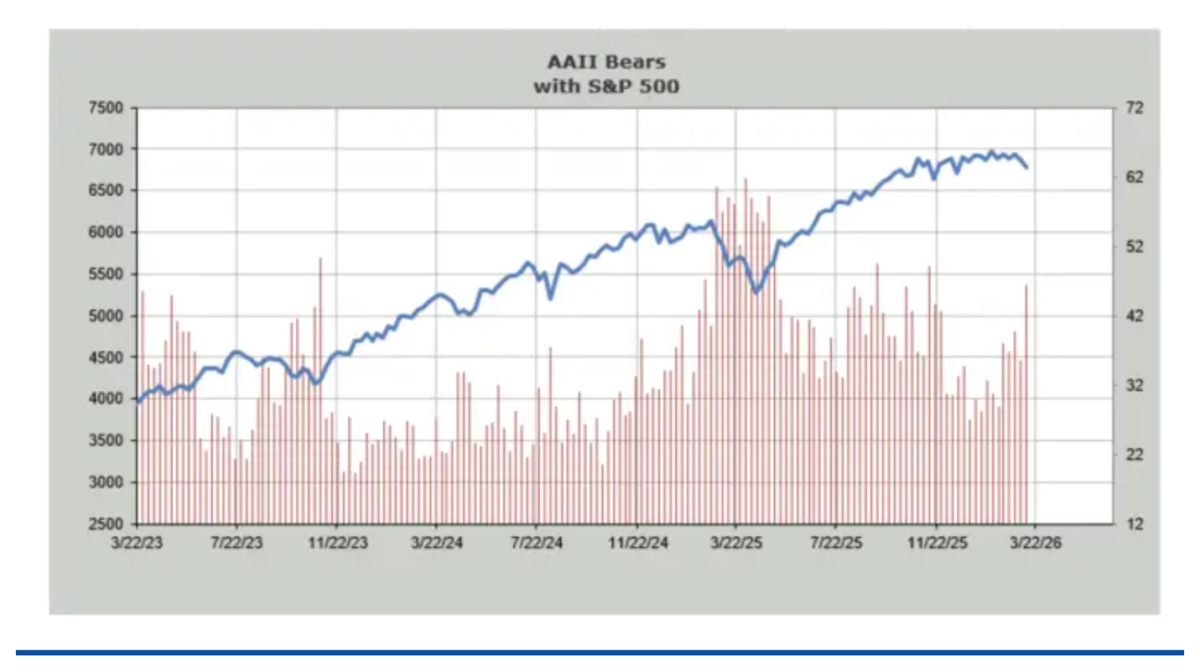

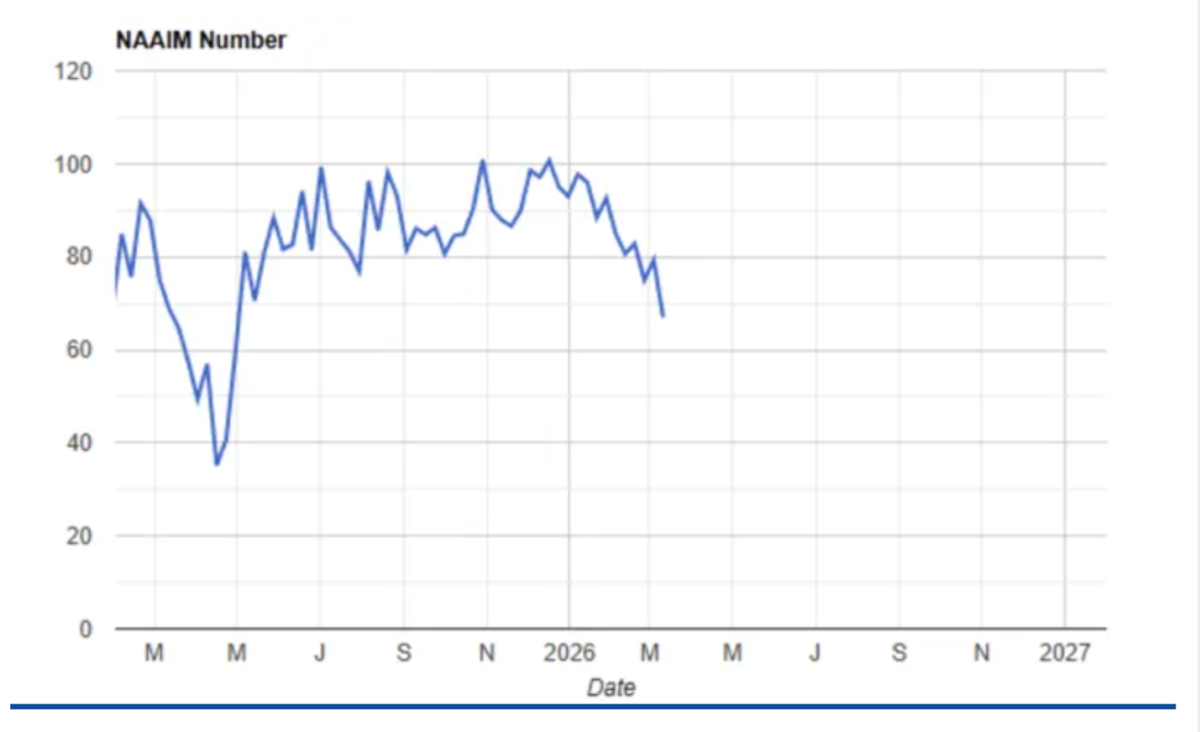

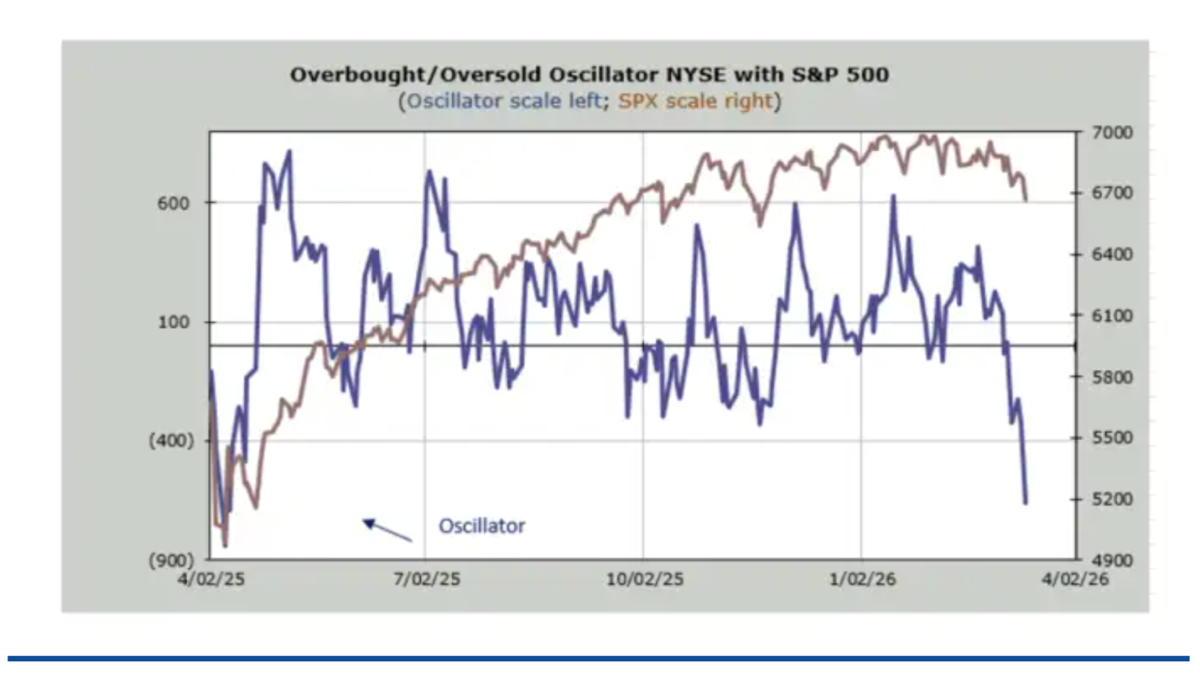

Over the last two weeks, fear has risen sharply and sentiment has flipped negative (as measured by The Fear & Greed Index, the Oscillators (S&P Short Range Oscillator (07.87%) and the Overbought/Oversold Oscillator), and the surveys (Investors' Intelligence, AAII, and NAAIM):

As reported by The Divine Ms M:

The Investors’ Intelligence Bulls have dropped off to 49% (compared to 63% in early February):

But what has caught our eye has been the large surge in bears — now at 21.8%, the highest reading since last summer:

Joining in the pessimism of the Investors' Intelligence survey, is the AAII survey. The AAII folks joined the Investors’ Intelligence folks (shown here yesterday) in pulling back their horns. Like Investors' Intelligence, AAII bulls stayed mostly steady but the bears shot up by eleven points to 46%:

Following the previous surveys, the NAAIM survey also suggests that bulls are falling and bears rising. In December, their exposure was just over 100 (on margin). Now it’s down to 67, which is the lowest since the panic low of April 2025. Again, not extreme, but finally some movement off that complacency

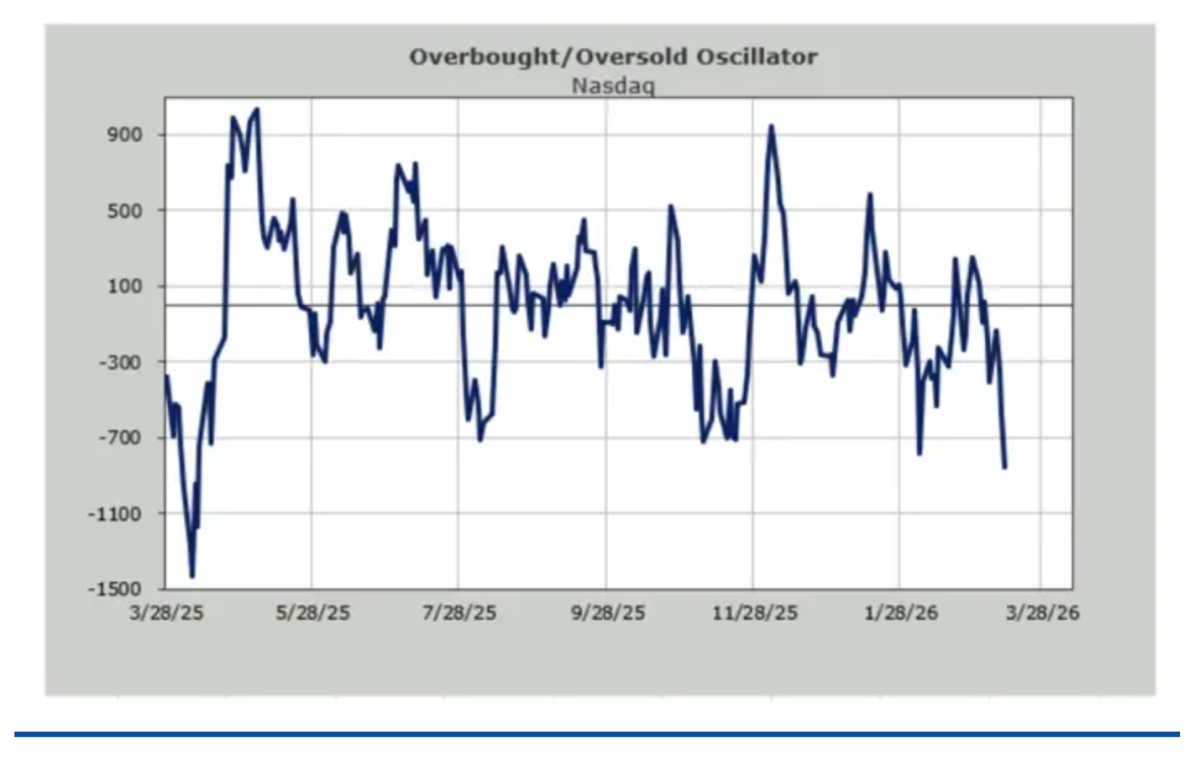

The Overbought/Oversold Oscillator is now nearing the April 2025 lows. (So is the S&P Short Range Oscillator reading near new oversolds). The last six trading days’ breadth has been red. And for seven out of eight, it has been red.

Here is the NYSE Overbought/Oversold Oscillator:

Here is the Nasdaq Overbought/Oversold Oscillator:

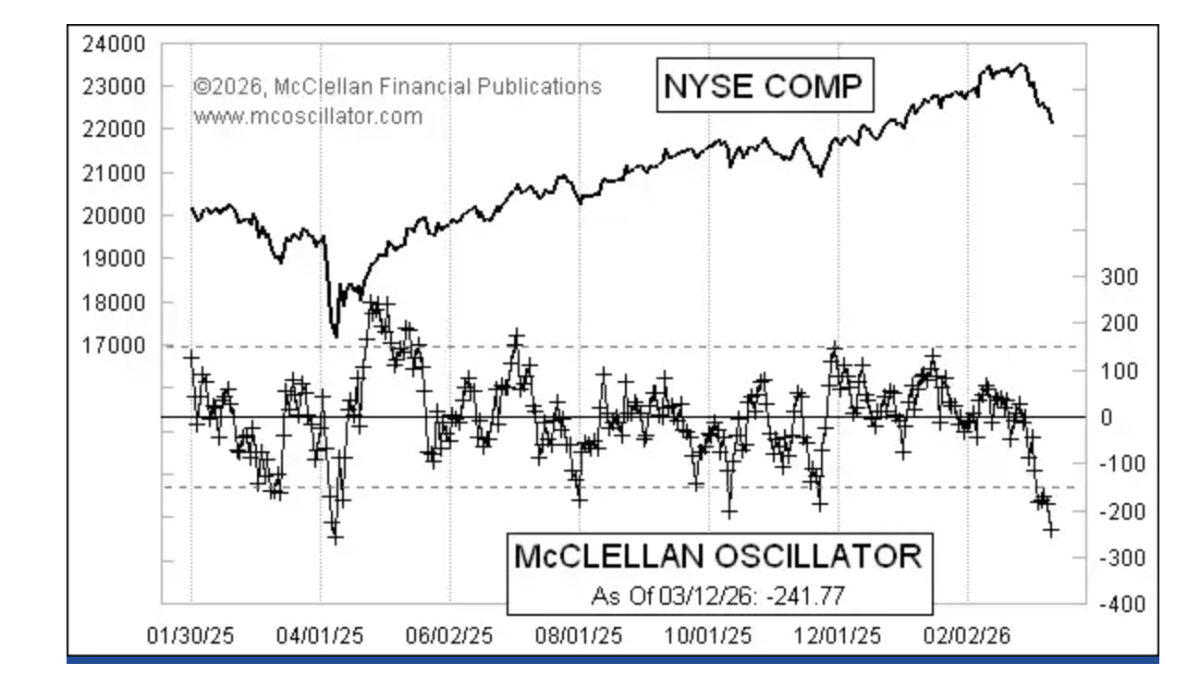

Finally, the NYSE’s McClellan Advance/Decline Oscillator has reached its most oversold levels since last April:

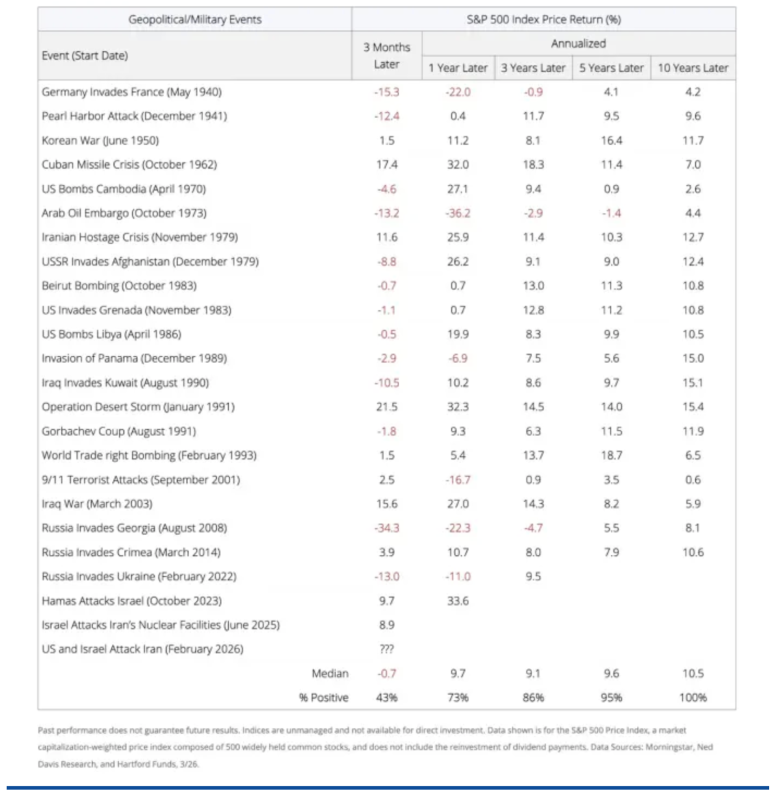

The War in Iran is Frightening But It Will Likely Create Investing Opportunities

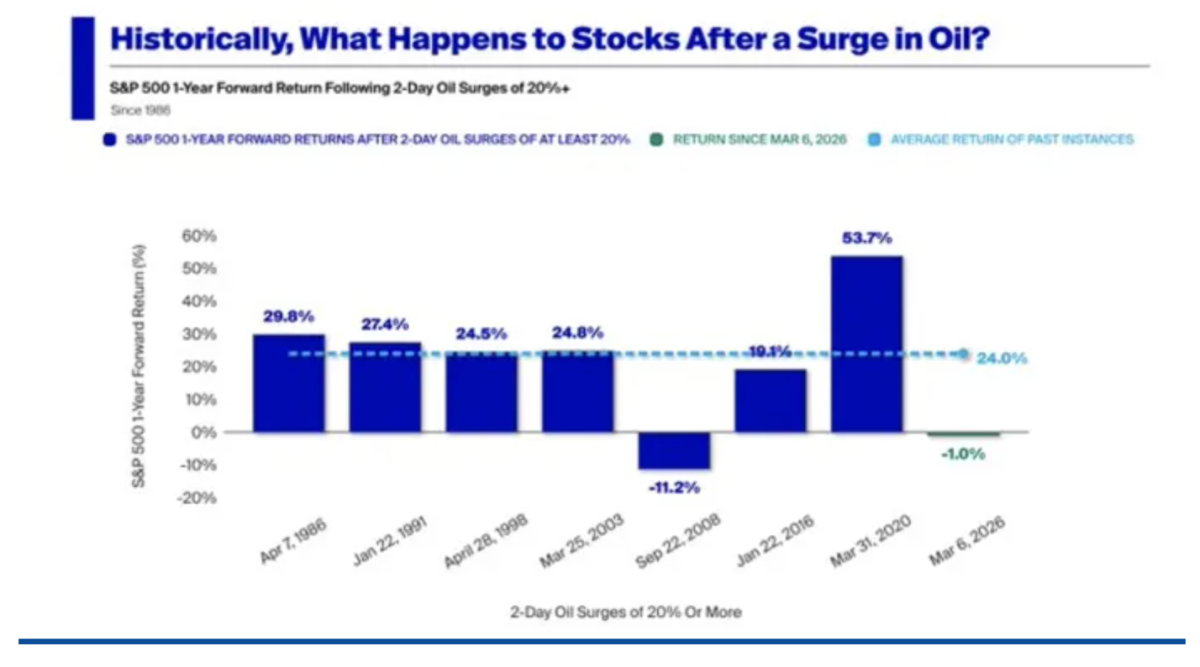

Baron Nathan's Rothschild's quote (mentioned earlier) has some historical weight, as equities usually respond smartly to conflicts that lead to a surge in oil.

There have been eight oil shocks in the last four decades. In seven of those instances, equities were higher one year later, with an average gain of +24%:

According to Harford Funds, equities generated positive performance 12 months after an act of aggression for 73% of the armed conflicts since World War II:

I have always written that being short protects capital and being long creates capital.

For some time, I have operated defensively at my hedge fund.

Let me make it clear that I am in no rush to buy stocks. But I do plan to move slowly away from defense and towards more offense as sentiment has eroded, positioning has moved far more conservative and many of our concerns are now being acknowledged ("second-level thinking").

Importantly, the war in Iran has rapidly transformed investor optimism to investor pessimism as sentiment and stock prices have fallen.

Coincident with lower stock prices, investors are beginning to acknowledge our fundamental concerns and some investment opportunities have now emerged.

Warren Buffett emphasized that investing requires rational, cold, "no-emotion" decision making, rather than reacting to market fear or greed, to achieve long-term success in the quote below:

"Until you can manage your emotions, don't expect to manage money."

So, as always, I will approach emerging long opportunities dispassionately and with a calculator in hand — calculating upside reward vs. downside risk while adopting the "margin of safety" principle in all of our buys.

None.

BY Doug Kass · Mar 25, 2026, 9:45 AM EDT

-DXYZ +30% (strength after report SpaceX to potentially file for IPO as early as this week)

-BRZE +20% (momentum)

-ELVN +18% (strength following Merck announcement to acquire Terns in $6.7B deal)

-QNRX +16% (FDA indicated that a single Phase 3 study may be sufficient to support marketing approval in the U.S. after Constructive Type C Meeting with U.S. FDA for QRX003 in Netherton Syndrome)

-ARM +12% (guidance from investor event)

-DNLI +11% (receives US FDA BLA Type 1 approval for Avlayah)

-NOTE +11% (launches PolicyNote MCP in OpenAI app store)

-CHWY +7.9% (earnings, guidance)

-TERN +5.6% (Merck confirms to acquire Terns, including lead asset TERN-701, for $53/shr)

-PDD +4.5% (earnings, color)

-ONDS +4.4% (earnings, guidance)

-BEAM +4.2% (announces updated clinical data from ongoing Phase 1/2 Trial of BEAM-302 in Alpha-1 Antitrypsin Deficiency (AATD) to support advancement to Pivotal Development)

-JD +3.8% (recent notable strength being attributed to China authorities stepped up efforts to end the intense competition in the food-delivery sector that has driven down profits)

-HOOD +3.5% (Board authorizes $1.5B common share repurchase program)

-BABA +3.4% (recent notable strength being attributed to China authorities stepped up efforts to end the intense competition in the food-delivery sector that has driven down profits)

-SRPT +3.4% (early clinical results of αvβ6 integrin-targeted siRNA approach achieves high muscle concentrations without dose limiting toxicity for facioscapulohumeral muscular dystrophy type 1 (FSHD1) and myotonic dystrophy type 1 (DM1))

-PAYX +3.3% (earnings, guidance)

-AVXL -31% (withdraws application for marketing authorization of blarcamesine in EU as an add-on therapy for treatment of early Alzheimer’s disease in adults, which had been under review by European Medicines Agency (EMA))

-ARTL -16% (issues glaucoma study update)

-ABSI -8.6% (earnings)

-DOCN -7.9% (prices upsized common stock offering)

-LBRT -6.4% (files to sell $450M in convertible notes due 2032 with up to $50M option)

-FPS -5.1% (Holders to offer 20.6M shares and announces offering of 9.3M shares)

-ONON -5.1% (announces leadership change and share conversion)

-KBH -3.1% (earnings, guidance)

None.

BY Doug Kass · Mar 25, 2026, 9:26 AM EDT

BY Doug Kass · Mar 25, 2026, 9:21 AM EDT

None.

BY Doug Kass · Mar 25, 2026, 9:15 AM EDT

4:10 p.m.: Fed Board Governor Miran (Voter) participates in conversation before the Digital Asset Summit 2026, Javits Center,NYC (No text. Q&A from moderator. Livestream here)

11:30 a.m.: Treasury hosts a$69B 17-Week Bill Auction;

11:30 a.m.: Treasury hosts a $28B 2-Year Floating Rate Note Auction;

1:00 p.m.: Treasury hosts a $70B 5-Year Note Auc-tion;

2:00 p.m.: Treasury buyback (liq support)

None.

BY Doug Kass · Mar 25, 2026, 9:05 AM EDT

None.

BY Doug Kass · Mar 25, 2026, 8:55 AM EDT

I have taken a long position in the indices (on Iran not accepting the ceasefire):

* (SPY) $657.06

* (QQQ) $588.82

Position: Long SPY (S), QQQ (S)

BY Doug Kass · Mar 25, 2026, 8:47 AM EDT

* I don't know if my observations below are sad or laughable...

Just when you think the business media's output can't get worse...

Why is @halftimereport Twitter site basically a primer on Josh Brown's Best Stocks of the Market? Why aren't any other panelists' ideas ever mentioned on the network's Twitter account?

Let's go to the tape, err... the X thread of Halftime Report:

Nearly every single repost is a compilation of Josh Brown's recommended list - chosen by a one factor model (the charts) many of which are outright and embarrassing losers.

* There is no explanation of what qualifies as a "Best Stock in the Market"

* Not one idea is timestamped (in price) so, again, viewers can't evaluate the merit of his ideas (In perusing the performance I think I know why!)

* There is never a followup on how the ideas fared? (In perusing the performance of "The Best Stocks" I think I know why!)

* Are CNBC's personnel (responsible for the Halftime twitter account) just lazy - as there are no other guests/panelists recommendations/related tweets listed in the X thread?

Here is what I recently wrote about the business media:

* Not providing two way discourse/debate (and relying on formulaic programming) has prepared investors poorly for when the halcyon days are over and the tides starts going out...

"So much for objective journalism. Don't bother to look for it here--not under any byline of mine; or anyone else I can think of. With the possible exception of things like box scores and race results, there is no such thing as objective journalism. The phrase itself is a pompous contradiction in terms.”

― Hunter S. Thompson, Fear and Loathing

My comments below should be a familiar refrain for those that follow me on Twitter and elsewhere...

Hubert Humphrey once said, "Freedom is hammered out on the anvil of discussion, dissent, and debate." The same applies to the generation and display of ideas -- in this case, market, economic and company views/outlooks. They are best presented and hammered out in disputation.

The business media, especially Fin TV, has once again failed to properly serve their most important stakeholder - their viewers and readers.

Journalists best serve their constituents by providing balanced and objective reporting. It is especially important for the media to always inject a degree of skepticism. This is even more important when the tide is coming in and the salad days of bullishness (come euphoria) are upon us. The media should do so to prepare for the inevitable downturn in fundamentals, stock prices and investors' sentiment.

It is also important for journalists to remain independent of view and to not have personal relationships (or the desire to have access) with company managements to influence their views. (Salesforce (CRM) , ServiceNow (NOW) and Nvidia (NVDA) come to mind!)

The business media has not provided this service. Instead, formulaic programming offers up the same (day after day) uber confident and non objective "talking heads" and their ever superficial "analysis" that is miles long but only inches deep (by practitioners who would never even qualify for interviews as analysts in any serious hedge fund and who never met a market they did not like) -- and, too often, are not supported by rigorous analysis or investment process.

"Praise by individual, criticize by category."

- Warren Buffett

My comments are not intended to be ad hominem, they are (like Meet The Press' Tim Russert was) fact based - taken from archived videos and interviews.

Without time stamps, guests and panelists in the business media are not held accountable. (Worse yet, they are too often filled with hubris). Case in point, a panelist on CNBC's Halftime, who, in the last three years, has endorsed only three specific stocks as his foundational, "forever" and largest holdings - Alibaba (BABA) , Moderna (MRNA) and UnitedHealth (UNH) :

* BABA missed last night and the shares are -$7 overnight - the shares have receded from $192 to $128 (he has recommended all the way down - as recently as two weeks ago Trade Tracker: Steve Weiss buys more Alibaba )

* MRNA dropped precipitously from $500 to a low of $22 (now $52)

* UNH declined from $595 to $282

(I should note that in the case of Alibaba, the panelist berated the other panelists who purchased BABA due to the ownership structure in which you are not a shareholder but own an interest in an offshore vehicle! Then he bought near the top of the chart.)

Contrary views (read: bearish) are underemphasized or not delivered at all in a backdrop of giddiness and FOMO ("fear of missing out").

Discipline and assessment of downside risk relative to upside reward are nearly always abandoned as an extreme level of complacency is urged at just the time markets mature and overvalued equity prices peak (in a valuation promise of a new never ending bullish cycle and paradigm).

Geopolitical risks, extreme valuations and private equity/credit concerns - were risks that some of us ursine types have been warning about for twelve months. Yet these factors were given little discussion or weight in the media. It is only "after the horse left the barn" (when the problems have surfaced), that a proper discussion is permitted.

Memo to the business media:

There are some situations one simply cannot be neutral about, because when you are neutral you are an accomplice. Objectivity doesn't mean treating all sides equally. It means giving each side a hearing.

Position: Long UNH S

By Doug KassMar 19, 2026 7:40 AM EDT

Position: Long UNH S

BY Doug Kass · Mar 25, 2026, 8:25 AM EDT

Here is a list of some 17 individual (quality) equities that I am currently long that I want to add to on weakness:

Financials

American Express (AXP)

Morgan Stanley (MS)

Goldman Sachs (GS)

Citigroup (C)

Wells Fargo (WFC)

Bank of America (BAC)

Private Equity

Apollo (APO)

KKR (KKR)

Blackstone (BX)

Technology

Microsoft (MSFT)

Alphabet (GOOGL)

Meta (META)

Amazon (AMZN)

Consumer

Procter & Gamble (PG)

PepsiCo (PEP)

Kimberly-Clark (KMB)

Disney (DIS)

Positions: Long all of the above

BY Doug Kass · Mar 25, 2026, 8:03 AM EDT

All the while, the PPT has battled it out with market intervention

— Keith McCullough (@KeithMcCullough)

"more than 112 trading sessions since the SPX recorded a decline of -2.5% or greater" @t1alpha pic.twitter.com/ekNhSBrMlE

BY Doug Kass · Mar 25, 2026, 7:30 AM EDT

As I mentioned yesterday:

Software is getting smoked today after Anthropic shipped their new update that lets your AI control your computer for you. White collar work is toast.$IGV getting smoked pic.twitter.com/A1gcH8WiYI

— Negligible Capital (@negligible_cap)

BY Doug Kass · Mar 25, 2026, 7:30 AM EDT

Whitney Economics says legal marijuana sales are on track to rebound in 2026 after falling from $30 billion in 2024 to $29 billion in 2025 (the market's first decline), with revenue projected to climb to $43.3 billion by 2030 despite price compression. https://t.co/P2VnTgoDY2

— Anthony Martinelli (@AMartinelliWA)

BY Doug Kass · Mar 25, 2026, 7:20 AM EDT

BREAKING: The IRGC has launched its 88th wave of ballistic missiles and drones since February 28. Targets: Tel Aviv, Bnei Brak, Kiryat Shmona, Dimona, Arad, Safed. US bases in Bahrain, Kuwait, and Jordan. One hundred and eighty people injured across recent Israeli waves. Cluster… pic.twitter.com/ZIJ4lNFOGf

— Shanaka Anslem Perera ⚡ (@shanaka86)

BREAKING. The Wall Street Journal reports Iran’s demands to end the war. Closure of all US military bases in the Gulf. Ironclad guarantees of no further attacks. An immediate end to Israeli strikes on Hezbollah. Full lifting of all sanctions with binding economic guarantees.… pic.twitter.com/UkGsAp6H37

— Shanaka Anslem Perera ⚡ (@shanaka86)

BREAKING: Iranian drones struck a fuel storage tank at Kuwait International Airport shortly after 2am local time this morning. Fire broke out. Firefighting teams contained it. No casualties. Kuwait Civil Aviation Authority confirmed the strike and activated emergency measures.… pic.twitter.com/BHE0yrYxTe

— Shanaka Anslem Perera ⚡ (@shanaka86)

BREAKING: President Trump announced a 5-day pause on strikes against Iranian power plants on March 23. In the 48 hours since, Israel struck over 50 missile sites across northern and central Iran. The IDF hit IRGC and Intelligence Ministry headquarters in Tehran with over 100… pic.twitter.com/Rvb7Y0sxl0

— Shanaka Anslem Perera ⚡ (@shanaka86)

BY Doug Kass · Mar 25, 2026, 7:10 AM EDT

As I mentioned previously:

BlackRock's Larry Fink: If Iran remains a threat after the bombing stops, there could be "years of above $100, closer to $150 oil, which has profound implications in the economy" and an outcome of "a probably stark and steep recession." (1/2) https://t.co/HRW2yYNXM9

— Lisa Abramowicz (@lisaabramowicz1)

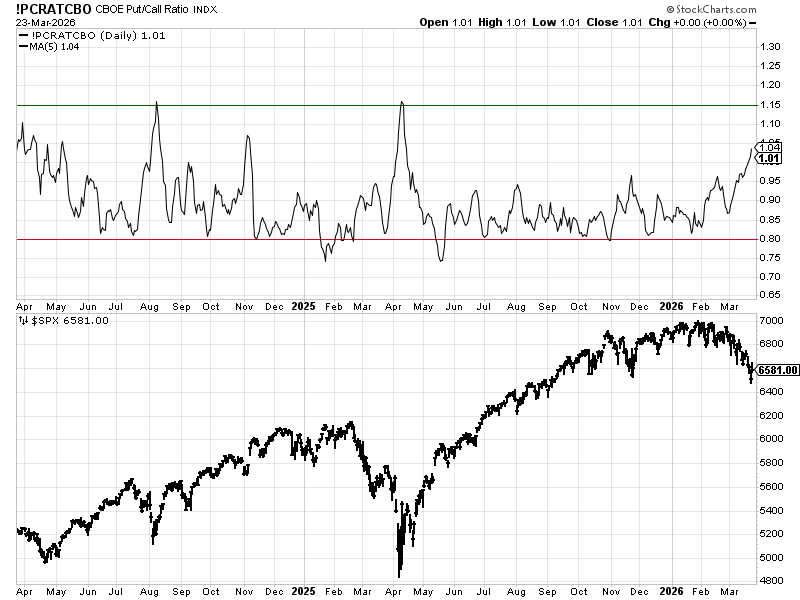

BY Doug Kass · Mar 25, 2026, 7:00 AM EDT

Chart of the Day: Put/Call Ratio

Since February, the market has been steadily grinding lower, making tactical trades like shorting rallies more effective than buying dips.

The CBOE Put/Call Ratio has notably reached multi-month highs, reflecting rising fear and growing demand for protection.

Though still short of prior extreme washout levels, sentiment is nearing points where shorting could lose its edge, making a contrarian long position increasingly compelling.

The Takeaway: While tactical shorts have so far been successful, sentiment is approaching points where opposing bets may pay off.

- Wesley Mattox, CFA, CMT (@WesleyJMattox) / X

This bull market is in year four, which historically is quite strong.

— Ryan Detrick, CMT (@RyanDetrick)

Assuming the bull market doesn't end (by definition a 20% decline) you can see this year tends to be pretty strong. pic.twitter.com/QQ3WWxzHfG

In the chart below we can see that the MOVE index (bond market implied vol) shot up and took over as the fastest moving metric.

— Jurrien Timmer (@TimmerFidelity)

The drawdown in the S&P 500 reached 7.6% last week, which is not that big a deal (so far) by historical standards. Robust earnings growth is masking… pic.twitter.com/fxbgsawPIG

The real whoosh down for the market likely doesn't happen until and if semiconductors $SMH loses this 375 zone. pic.twitter.com/x8REbNaFPj

— Evan Medeiros (@evanmedeiros)

Energy sector, 20 new 52-week+ highs. $CVX $XOM $PSX +++ pic.twitter.com/WtYZiF4Uk8

— Larry Tentarelli, Blue Chip Daily (@bluechipdaily)

Showing a high degree of alignment. pic.twitter.com/EqnqF1J6Lm

— Turning Point Market Research (@TPMRSignals)

Something to keep an eye on...$BTC pic.twitter.com/Fg9obvAfXv

— David Rath (@DJwrath)

Bonus — Here are some great links:

BY Doug Kass · Mar 25, 2026, 6:45 AM EDT

And, after the Iranian war is over, there will still be this:

⚠️This is INSANE:

— Global Markets Investor (@GlobalMktObserv)

The US deficit-to-GDP ratio hit 5.8% in 2025, far above the 50-year historical average of 3.8%.

The US is running one of the worst deficits ever, excluding WWII, the 2008 Financial Crisis, and the 2020-2021 pandemic response.

The deficit is also nearly DOUBLE… pic.twitter.com/cKRe4WhTuy

BY Doug Kass · Mar 25, 2026, 6:35 AM EDT

Iran and the U.S. will ultimately declare an end to the conflict but it is important to recognize that inflation was already hot going into the war and will not cool off after the war.

BY Doug Kass · Mar 25, 2026, 6:25 AM EDT

ETF trading is taking over the US stock market:

— The Kobeissi Letter (@KobeissiLetter)

ETFs now account for 37% of total US stock market volume, the highest monthly average on record.

This percentage has soared +13 points since the start of 2025.

This also surpasses the previous peaks of ~36% during the 2020… pic.twitter.com/V8zb88DKad

BY Doug Kass · Mar 25, 2026, 6:15 AM EDT

Here is the cannabis podcast of the day:

Schedule III is not the final destination for cannabis.🍃

— AdvisorShares (@AdvisorShares)

Dan Ahrens @InvestinginCan1 explains why listings on major exchanges and real banking access are what could change the investing landscape, and why the CLIMB Act matters in that context.

Which cannabis operators would you… pic.twitter.com/Mqu1r6PsoB

Position: Long Cannabis

BY Doug Kass · Mar 25, 2026, 6:05 AM EDT

BREAKING: The Philippines has declared a state of national energy emergency due to a severe shortage of oil amid the Iran War.

— The Kobeissi Letter (@KobeissiLetter)

Details include:

1. The Philippines imports 98% of its oil from the Gulf, with gas prices up over +100% since February 28th

2. The government is also…

BY Doug Kass · Mar 25, 2026, 5:55 AM EDT

The S&P Short Range Oscillator remains oversold at -5.12% vs. -5.00%.

BY Doug Kass · Mar 25, 2026, 5:45 AM EDT

BREAKING: President Trump announced a 5-day pause on strikes against Iranian power plants on March 23. In the 48 hours since, Israel struck over 50 missile sites across northern and central Iran. The IDF hit IRGC and Intelligence Ministry headquarters in Tehran with over 100 Show more

Software is getting smoked today after Anthropic shipped their new update that lets your AI control your computer for you. White collar work is toast. $IGV getting smoked

All the while, the PPT has battled it out with market intervention "more than 112 trading sessions since the SPX recorded a decline of -2.5% or greater" @t1alpha

The real whoosh down for the market likely doesn't happen until and if semiconductors $SMH loses this 375 zone.

BREAKING: Two senior administration officials have confirmed to CNN that the White House is arranging for Vice President JD Vance to travel to Pakistan this weekend for talks to end the war with Iran. Trump is expected to make an urgent announcement at 7:20 PM ET tonight. TheShow more

BlackRock's Larry Fink: If Iran remains a threat after the bombing stops, there could be "years of above $100, closer to $150 oil, which has profound implications in the economy" and an outcome of "a probably stark and steep recession." (1/2) bbc.com/news/articles/…

⚠️This is INSANE: The US deficit-to-GDP ratio hit 5.8% in 2025, far above the 50-year historical average of 3.8%. The US is running one of the worst deficits ever, excluding WWII, the 2008 Financial Crisis, and the 2020-2021 pandemic response. The deficit is also nearly DOUBLEShow more

BREAKING: The IRGC has launched its 88th wave of ballistic missiles and drones since February 28. Targets: Tel Aviv, Bnei Brak, Kiryat Shmona, Dimona, Arad, Safed. US bases in Bahrain, Kuwait, and Jordan. One hundred and eighty people injured across recent Israeli waves. ClusterShow more

BREAKING. The Wall Street Journal reports Iran’s demands to end the war. Closure of all US military bases in the Gulf. Ironclad guarantees of no further attacks. An immediate end to Israeli strikes on Hezbollah. Full lifting of all sanctions with binding economic guarantees.Show more

Something to keep an eye on... $BTC

BREAKING: Iranian drones struck a fuel storage tank at Kuwait International Airport shortly after 2am local time this morning. Fire broke out. Firefighting teams contained it. No casualties. Kuwait Civil Aviation Authority confirmed the strike and activated emergency measures.Show more

BREAKING: Iran has rejected peace talks with Steve Witkoff and Jared Kushner and indicated a preference for negotiating with Vice President JD Vance, per CNN’s Iranian source. On Day 25 of a war that Iran publicly says does not involve any negotiations, Tehran is now selecting

ETF trading is taking over the US stock market: ETFs now account for 37% of total US stock market volume, the highest monthly average on record. This percentage has soared +13 points since the start of 2025. This also surpasses the previous peaks of ~36% during the 2020 Show more

BREAKING: The Philippines has declared a state of national energy emergency due to a severe shortage of oil amid the Iran War. Details include: 1. The Philippines imports 98% of its oil from the Gulf, with gas prices up over +100% since February 28th 2. The government is also Show more

Whitney Economics says legal marijuana sales are on track to rebound in 2026 after falling from $30 billion in 2024 to $29 billion in 2025 (the market's first decline), with revenue projected to climb to $43.3 billion by 2030 despite price compression. themarijuanaherald.com/2026/03/whitne…

🎦 TRADE TO BLACK 📊 Presented by @FlowhubCo 🚨🕧 SPECIAL TIME: *LIVE* @ 12:30pm ET 🎦 Top Cannabis Physician Explains CBD Pilot 🎙️ Dr. Leigh Vinocur, @natcarecouncil Chief Medical Advisor 🌿 ETFs: 🌎 $YOLO 🇺🇸 $MSOS 📈 $SPY $QQQ $IWM #FinTwit youtube.com/watch?v=QuWfHs…

Schedule III is not the final destination for cannabis.🍃 Dan Ahrens @InvestinginCan1 explains why listings on major exchanges and real banking access are what could change the investing landscape, and why the CLIMB Act matters in that context. Which cannabis operators would you Show more