The state of the US economy from the S&P Global PMI

These were some of the comments from S&P Global in their just released March PMI on manufacturing and services (that miss key sectors like retail/wholesale trade and construction) where the former was 52.4 vs 51.6 in February and the latter was 51.1 vs 51.7 in the month before:

“The service sector was harder hit as manufacturers reported an upturn in output and new order book growth. A similar divergence was also seen regarding output expectations, with a weaker outlook among service providers contrasting with a more upbeat perspective among manufacturers, the latter buoyed in part by fewer tariff related worries. However, overall private sector confidence declined and contributed to the first fall in employment for over a year.”

Also of note, “Average input costs meanwhile rose at a sharp rate again, posting the largest monthly increase for ten months and feeding through to the largest increase in average selling prices since August 2022. Higher prices were widely linked to the war related spike in energy costs and tightening supply conditions. Supplier delivery times in manufacturing lengthened to the greatest extent since October 2022.”

The bottom line from S&P Global, “The flash PMI survey data for March signal an unwelcome combination of slower growth and rising inflation following the outbreak of war in the Middle East. Companies are reporting a hit to demand from the additional uncertainty and cost of living impact generated by the conflict. Travel, transport and tourism related issues are compounded by financial market jitters and affordability constraints, notably including concern over the impact of higher interest rates, surging energy prices and supply chain delays.”

And, “Companies are meanwhile building safety stocks amid concerns that the war may lead to more protracted supply issues and price rises while trimming headcounts to reduce overheads.”

Nothing more for me to add. Strictly from a market and economic perspective, the war either ends or continues and the Strait of Hormuz either fully reopens safely or does not. There is no in between at this point it seems.

Fox News has learned that the Commander of the 82nd Airborne Division Maj Gen Brandon Tegtmeier and his “command element,” members of his headquarters staff, have been ordered to deploy to the Middle East as the Pentagon and White House weigh whether to send the 82nd Airborne…

Maybe naive, but optimistic/The real world impact of what's going on/Privates

I’m going to be optimistic and say the 5 days Trump has given to a negotiated cessation of the war will be successful. Not successful in changing the regime unfortunately, which is a tremendously missed opportunity, though not for lack of trying, but succeeding in ending the current fight after massively degrading the military capabilities of Iran and the reopening of the Strait that follows in terms of ending Iranian threats which will let ships flow freely. Maybe naïve but hopeful as I’m happy to see the UAE and Saudi Arabia about to get more involved in fighting Iran according to reports.

If the case and this current war ends soon, we need to start thinking about what the world will look like after in terms of global supply chains. We of course did this after Covid but it obviously needs to be revisited. Something I said a few weeks ago, I do not think the price of crude oil goes back to $65. I think what we’re going to see for the rest of the year and maybe then some, is a global restocking and hoarding of a variety of commodities by those countries that import what they need. And it’s not just going to be crude oil. It will be natural gas, fertilizers, aluminum, copper, silver, uranium, etc… I’m still a believer that we’re in a commodity bull market that has now spread to energy and ag and we are positioned long in a variety of them.

As for what the current economic situation is around the world in response to the major supply disruptions and spikes in key price inputs, some March PMI’s came out today and this is what was said by S&P Global when interpreting the figures they compiled.

Japan’s composite March PMI held above 50 at 52.5 vs 53.9 in February with both components lower. S&P Global said, “The slowdown coincides with the recent outbreak of the war in the Middle East, which contributed to a sharp rise in input costs amid reports of supply chain difficulties and higher prices for fuel. A weak yen exchange rate and rising labor costs also contributed to the upturn in expenses, further adding to the squeeze on company margins.”

Also, “With so much uncertainty around the length and impact of the Middle East war, firms were less confident around future output. Optimism among services companies fell more notably than across the manufacturing sector, however, with the latter hoping that stronger global demand across key industries such as AI, defense and semiconductors will continue to drive growth in the months ahead.”

Australia’s March PMI fell to 47 from 52.4, mostly driven by the drop in services to 46.6 from 52.8. Manufacturing stayed above 50, barely, at 50.1 vs 51 last month. S&P Global said, “Businesses faced steep cost pressures, with the rate of inflation at a more than 3 year high. At least some of this increased cost burden was passed through to customers, however, with selling prices rising at the sharpest rate since August 2023…Qualitative evidence linked lower output to a deterioration in demand conditions, in part a reflection of global uncertainty and economic disruption due to the Middle East war.”

India remains an economic standout but certainly not immune to what is going on as they import much of their energy needs and the rupee continues to weaken. Its PMI fell to 56.5 from 58.9 with most of the decline in manufacturing which went to 53.8 from 56.9. Services slipped by .9 pts to 57.2. S&P Global said, “The largest slowdown was seen at goods producers, who reported that the war in the Middle East weighed on production growth by exacerbating market instability, driving inflationary pressures higher and restricting demand through heightened future uncertainty among clients and end consumers. March’s increase in factory output was the softest since August 2021.”

With its services PMI, “Anecdotal evidence particularly pointed to disruptions to international travel.”

The March Eurozone PMI fell to 50.5 from 51.9 but interestingly the manufacturing component lifted to 51.4 from 50.8 (but maybe due to the jump in supplier deliveries because of slowing supply chains) with the services side seeing the weakness, down to 50.1 from 51.9. S&P Global said “The flash Eurozone PMI is ringing stagflation alarm bells as the war in the Middle East drives prices sharply higher while stifling growth. Firms’ costs are rising at the fastest rate for over three years amid the surge in energy prices and choking of supply chains resulting from the war. Supplier delays have jumped to their highest since mid-2022, largely linked to shipping issues.”

To quantify, “The survey data are indicative of Eurozone GDP growth slowing to a quarterly rate of just below .1% in March with the forward looking indicators pointing to a heightened risk of a downturn in the coming months. The survey’s price gauge is meanwhile indicative of consumer price inflation accelerating close to 3%, with cost pressure likely to add still further to selling price inflation in the coming months.”

The March UK PMI dropped to 51 from 53.7 with most of the decline led by services which went to 51.2 from 53.9. Manufacturing was down by just .3 pts m/o/m to 51.4. S&P Global said succinctly, “The war in the Middle East has hit the UK economy in March, stalling growth while driving inflation sharply higher.”

Further, “Output growth across manufacturing and services has slowed to a crawl as companies blamed lost business directly on the events in the Middle East, whether through heightened risk aversion among customers, surging price pressures, higher interest rates, or via travel and supply chain disruptions.”

And, “Inflationary pressures have surged higher on the back of rising energy prices and fractured supply chains. The acceleration in cost growth in the manufacturing sector was especially severe, being the sharpest since the depreciation of sterling following Black Wednesday in 1992.” I bolded to highlight.

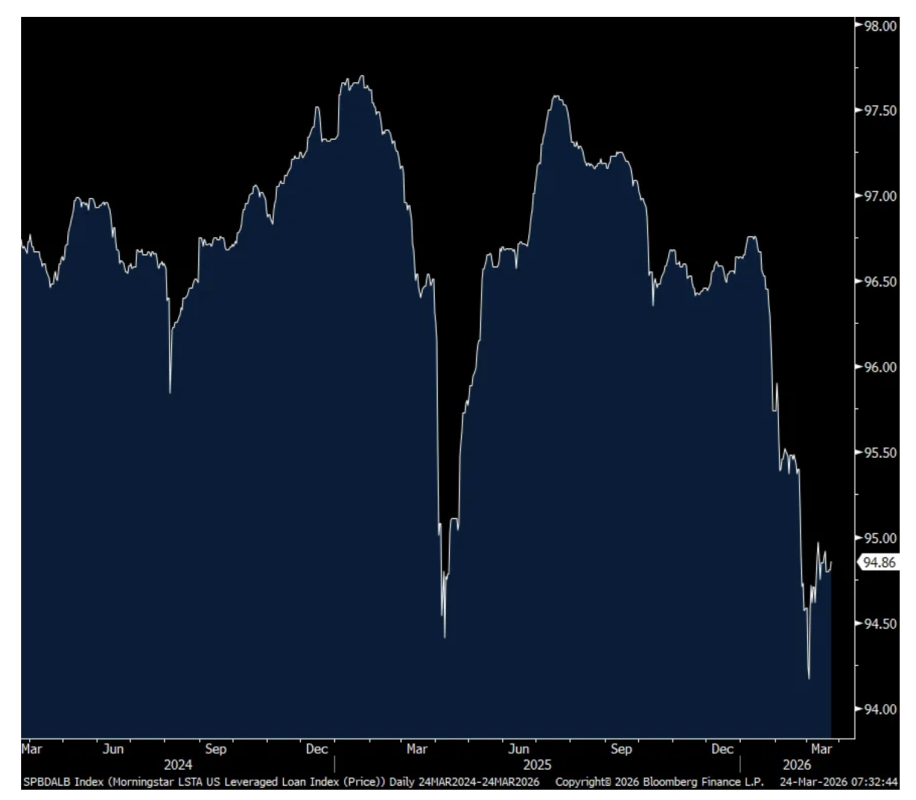

Shifting gears to private credit, I’m sure you all saw the Apollo news in keeping its withdrawal rate at 5%, which is the right thing to do, rather than satisfy the 11% requested. Also, the Moody’s downgrade of the FS KKR Capital Corp private credit fund to junk status. Yes, I do believe some credit issues are surfacing but will instead state here again, the unhealthy relationship between private credit and some in retail with the differing time horizons and views on liquidity. I say ‘some’ in retail because there are others in retail that are long term investors, similar to pension funds, insurance companies, and endowments, that are not asking for their money back.

Either way, an increase in redemptions and a rise in default rates, will lead to a higher cost of capital for borrowers and a tightening of lending standards.

Here is an updated chart of the LSTA Leveraged Loan Index

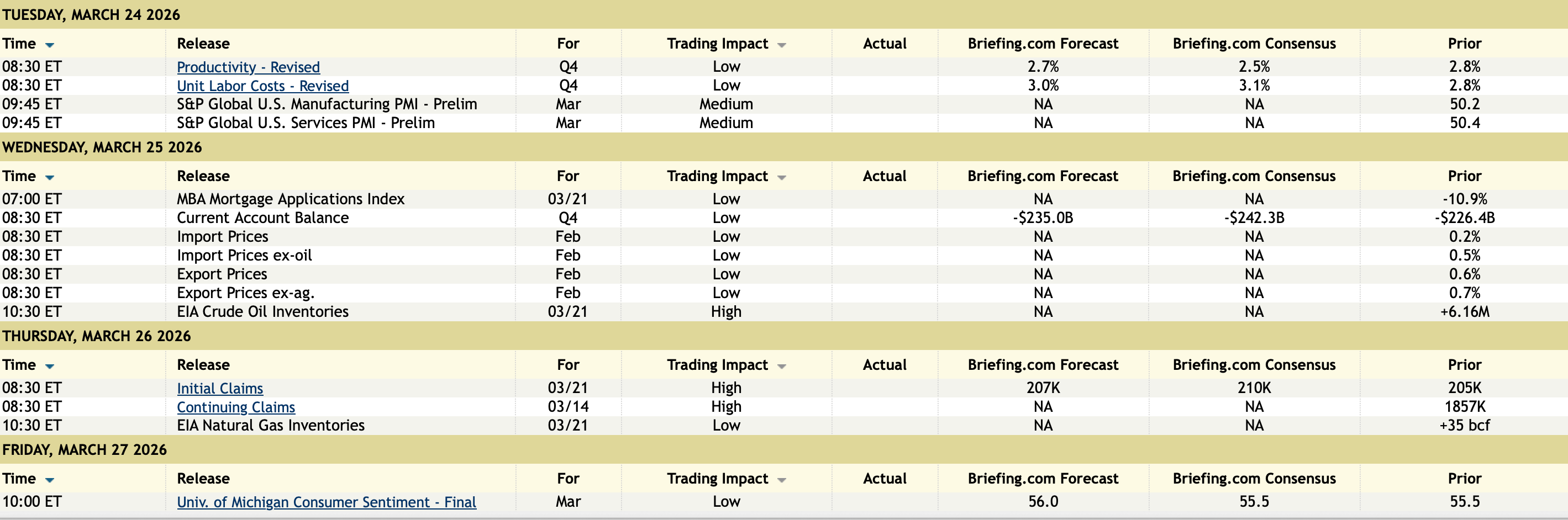

US: Futs are lower as overnight headlines induced choppiness. Those headlines include strikes on Iranian gas facilities, Saudis considering entering the war, Iranian lawmaker ruling out US negotiations, and then reports of Iran / Egypt discussions on the region pointing toward mediation. Bond yields are +2-3bp giving back most of yesterday’s moves; USD is recovering losses. In cmdty space Energy leads and precious metals have caught a bid despite the stronger USD. In Eqys, Mag7 are mostly lower, Energy is higher with the balance of Cyclicals flat to Defensives. Today’s macro data focus is on weekly ADP, regional Fed activity indicators, and Flash PMIs which may give us an early look at the impact of the Middle East conflict.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Yesterday, pre-market, Trump announced that negotiations with Iran began over the weekend and that they were close to a deal; Trump is also said to want the conflict ended by April 9 and extended his deadline to reopen the Strait of Hormuz to Friday. Headlines swirled throughout the session with limited ability to verify the veracity of headlines. US troop moves continue as UK looks to move missile defense armament into the region; Iran is said to have deployed sea-based mines in Strait of Hormuz (CBS). WSJ is reporting that US Marines are scheduled to arrive in the Middle East on Friday. Later it was reported that Israel pushed back on the US hypothesis that a deal could achieve more at this stage than a continued military campaign.

Israeli Prime Minister Netanyahu said, “Earlier today, I spoke with our friends, President Trump. President Trump believes that there is a chance to leverage the great achievements of the IDF and the US military to realize the war goals of the agreement. An agreement that will protect our vital interests. At the same time, we continue to attack both Iran and Lebanon. We sanctify the missile and nuclear programs to the last detail and continue to severely harm Hezbollah. Just a few days ago we eliminated two more nuclear scientists, and the hand is still outstretched. We will protect our vital interests in any situation.”

Danny Citrinowicz, former Head of Iran Branch for Israeli Military Intelligence, said in an X post, “Indeed, so far, nothing fundamental has changed. Israel continues striking in Iran, the U.S. is likely involved, and Iran continues its own attacks. What also hasn’t changed is that Iran hasn’t backed down — and there’s little indication it will. It still controls the Strait of Hormuz and is not prepared to compromise on its core demands in any negotiation. What has changed is Trump’s apparent recognition of the limits of force. He issued an ultimatum and threatened action but ultimately stepped back without securing anything from Iran. Messages may have been exchanged, but there’s little evidence of real Iranian flexibility. Tehran is clearly not willing to reopen the Strait on Washington’s terms. Trump now faces a stark choice: escalate with significant force to reopen the Strait, a move that could widen the conflict, deepen its global economic impact, and still fail — or move toward a deal that requires concessions to Iran, even if framed domestically as a win. That’s where things stand. The real test of Trump’s flexibility is still ahead, and this episode may have underscored, perhaps for the first time for him, that Iran is not Venezuela.”

Such pablum... and the show's moderators don't even pushback the silly narrative.

Tom Lee believes that higher oil prices are good for the market — and so are lower oil prices (as he formerly has discussed).

He is in the camp now that investor sentiment is so bearish that it is bullish — that everyone is bracing the view of a long war.

Not only is that not likely the truth (or consensus) regarding the war expectations that the consensus believes the war will be long lasting — but he fails to discuss (because it is inconvenient to his upside view of equities) sticky inflation, slowing global economic growth and rising geopolitical risks.

To Tom Lee and the many other perma-bulls on Fin TV — who never met a market they did not like — their credibility is undermined by the facts and their unwillingness to provide an objective view of the markets.

It is for this reason that the bullish cabal has led investors over the abyss in 2007, 2020 and 2022.

We have no way to conclude if 2026 will be the same but we can conclude that a "heads I win and tails I win" narrative (when looking at oil, interest rates, inflation, economic growth, monetary and fiscal policy, valuations, etc.) is no way to approach markets.

Mark my word, the next thing we will hear out of his mouth will be the "cash on the sidelines" argument!

George Noble Simplifies the Reality and Risks of Private Credit

Private credit returns 11.5% on loans that yield 9.5%.

Nobody asks how.

I'll tell you how:

Leverage.

They take a portfolio of loans yielding 9.5%, lever it 2x, and the gross return doubles to 19%. Subtract financing costs and fees, hand the client 11.5%, and show them a chart… pic.twitter.com/tUzjogHIAP

Intraday reversals in S&P 500 over the past few days were off the charts!

In 50 trading days, $SPX saw 24 sessions that flipped positive to negative and vice versa.

Similar whipsaws were last seen only during the 2022 bear market and ahead of the 2008 financial crisis. pic.twitter.com/VTAemtjUkG

— Bluekurtic Market Insights (@Bluekurtic)

Bloomberg: The recent decoupling of the Magnificent 7 and the wider S&P 500 may be good news for tech stocks. The last time correlations were this negative, in 2023, it marked the start of a period of dramatic outperformance for Big Tech.  pic.twitter.com/i7m3A1fwRR

— Menthor Q (@MenthorQpro)

No position in the US Dollar presently, but definitely NOT a buyer anytime soon. Seasonality "guarantees" nothing BUT will favor the short side if it starts to break down late March or after. Not advice, just the ramblings of a market-addled mind. @sentimentraderhttps://t.co/4ofNJtz70Epic.twitter.com/5LU6JP72sM

— Jay Kaeppel (@jaykaeppel)

Credit Markets: JNK near upward-sloping 200-day moving average. Click image to enlarge. pic.twitter.com/HqKi3h87x4

Michael Burry will no longer post on X after leaving an ominous message "Lights Out" 🚨 The last time he did this was right before the massive 2022 stock market dump 👻😱 pic.twitter.com/ZkTAwGO5IH

A leveraged fund says it has enough liquidity to meet 5% redemptions each quarter for the next year without selling a single position or asset.

Is “liquidity” a euphemism for “borrowing capacity” here?

If so, just more leverage.

Whoopsie!

— Jeffrey Gundlach (@TruthGundlach)

Bloomberg:

Moody’s ratings lowered its assessment of FS KKR Capital Corp to Ba1, one level into junk, because of what it described as “continuing asset quality challenges”.

— Jeffrey Gundlach (@TruthGundlach)

Of course assets would have to be pledged as collateral for any borrowings to meet redemptions, under this thought experiment.

Doubtful the lenders would accept anything other than the “best” collateral.

The great Lloyd Blankfein on Bitcoin:

“It’s not a medium of exchange…it’s not a good store of value…it’s not an asset you retreat to when you need safety.”

“It could go to a million dollars for a bitcoin, but it’s going to get there without me.”

Good inter with ARS.

The circular relationships within the private credit ecosystem are fascinating.

For example, Cliffwater invests in Carlyle's private credit fund.

On the other end, Carlyle's private credit fund lends to Cliffwater (first lien loan shown below).

So it appears that ultimately,Show more

🚨 TOM LEE: MARKETS ARE IGNORING THE BEARISH SETUP

Wall Street came in ready to short. Positioning was for downside. Long war, risk off, lower prices.

Instead, markets are rallying.

That’s the signal.

When everyone expects bad news and price refuses to go down, it means the Show more

Bloomberg:

Moody’s ratings lowered its assessment of FS KKR Capital Corp to Ba1, one level into junk, because of what it described as “continuing asset quality challenges”.

A leveraged fund says it has enough liquidity to meet 5% redemptions each quarter for the next year without selling a single position or asset.

Is “liquidity” a euphemism for “borrowing capacity” here?

If so, just more leverage.

Whoopsie!

Fox News has learned that the Commander of the 82nd Airborne Division Maj Gen Brandon Tegtmeier and his “command element,” members of his headquarters staff, have been ordered to deploy to the Middle East as the Pentagon and White House weigh whether to send the 82nd AirborneShow more

Private credit returns 11.5% on loans that yield 9.5%.

Nobody asks how.

I'll tell you how:

Leverage.

They take a portfolio of loans yielding 9.5%, lever it 2x, and the gross return doubles to 19%. Subtract financing costs and fees, hand the client 11.5%, and show them a chartShow more

Michael Burry will no longer post on X after leaving an ominous message "Lights Out" 🚨 The last time he did this was right before the massive 2022 stock market dump 👻😱

Intraday reversals in S&P 500 over the past few days were off the charts!

In 50 trading days, $SPX saw 24 sessions that flipped positive to negative and vice versa.

Similar whipsaws were last seen only during the 2022 bear market and ahead of the 2008 financial crisis.

No position in the US Dollar presently, but definitely NOT a buyer anytime soon. Seasonality "guarantees" nothing BUT will favor the short side if it starts to break down late March or after. Not advice, just the ramblings of a market-addled mind. @sentimentrader

Of course assets would have to be pledged as collateral for any borrowings to meet redemptions, under this thought experiment.

Doubtful the lenders would accept anything other than the “best” collateral.

Think about it.

Bloomberg: The recent decoupling of the Magnificent 7 and the wider S&P 500 may be good news for tech stocks. The last time correlations were this negative, in 2023, it marked the start of a period of dramatic outperformance for Big Tech.