Where I Sold

BY Doug Kass · Mar 20, 2026, 5:33 PM EDT

BY Doug Kass · Mar 20, 2026, 5:33 PM EDT

Selling all my index common (for profit) after President Trump says Iran conflict is close to "winding down."

BY Doug Kass · Mar 20, 2026, 5:33 PM EDT

BY Doug Kass · Mar 20, 2026, 4:45 PM EDT

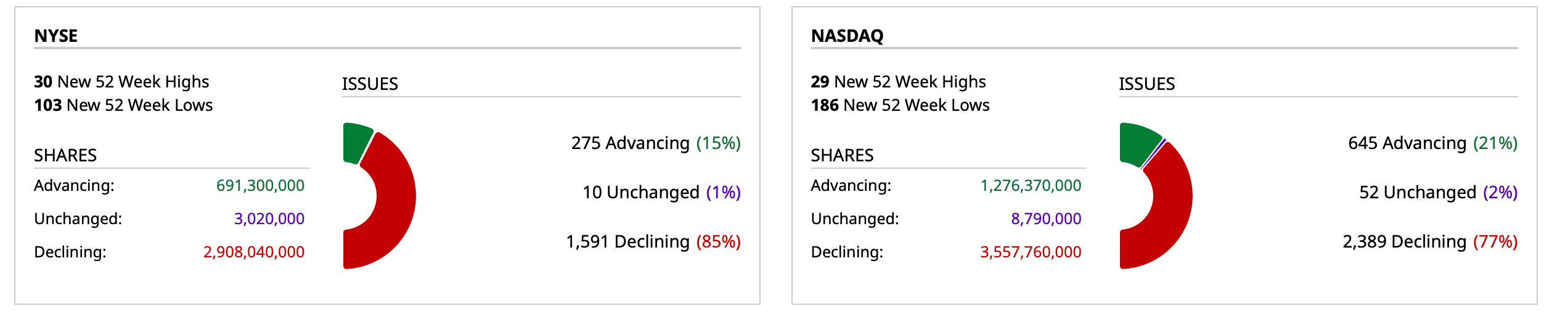

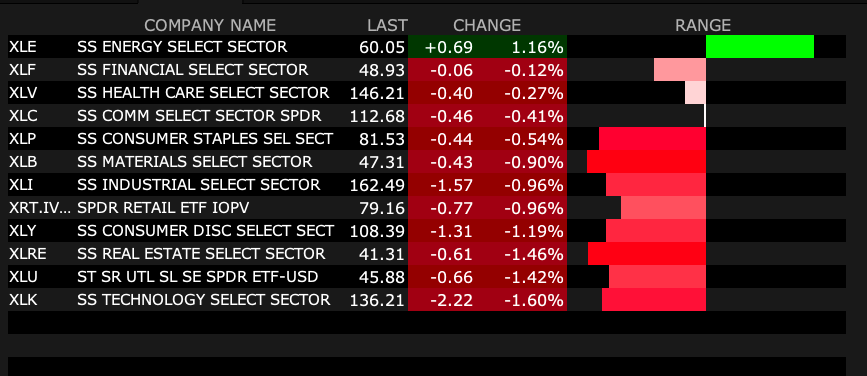

- NYSE volume 42% above its one-month average;

- NASDAQ volume 7% below its one-month average;

- VIX index: up 11.47% to 26.79

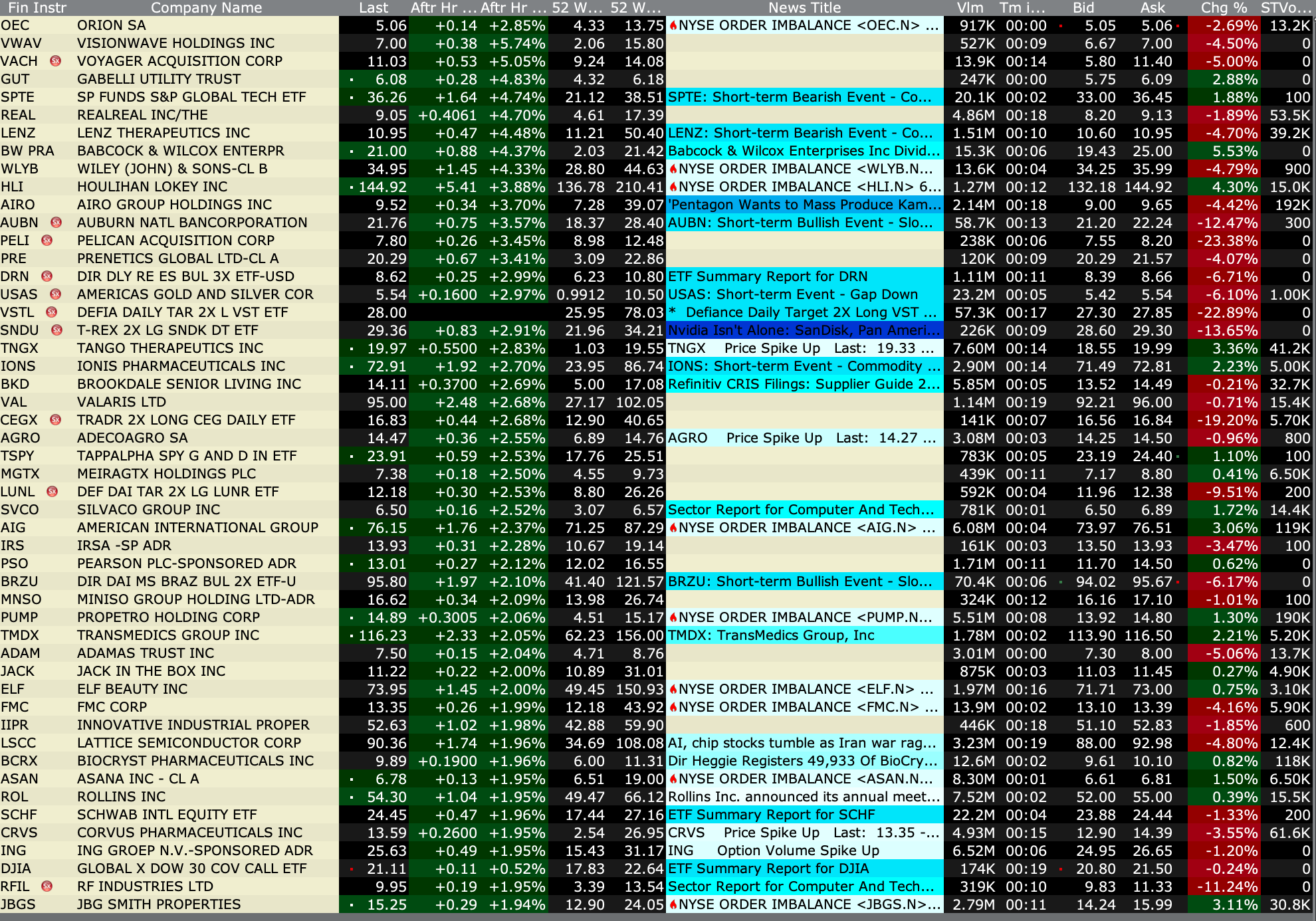

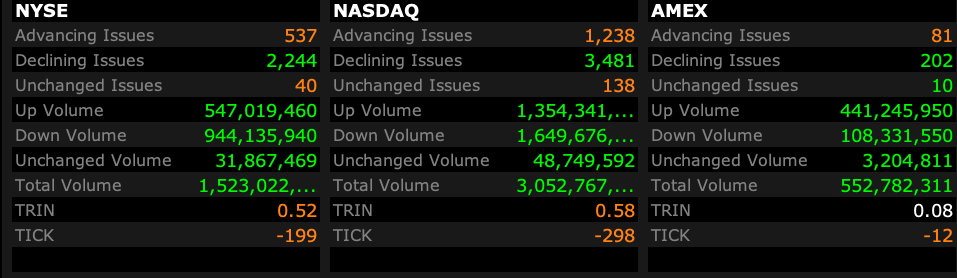

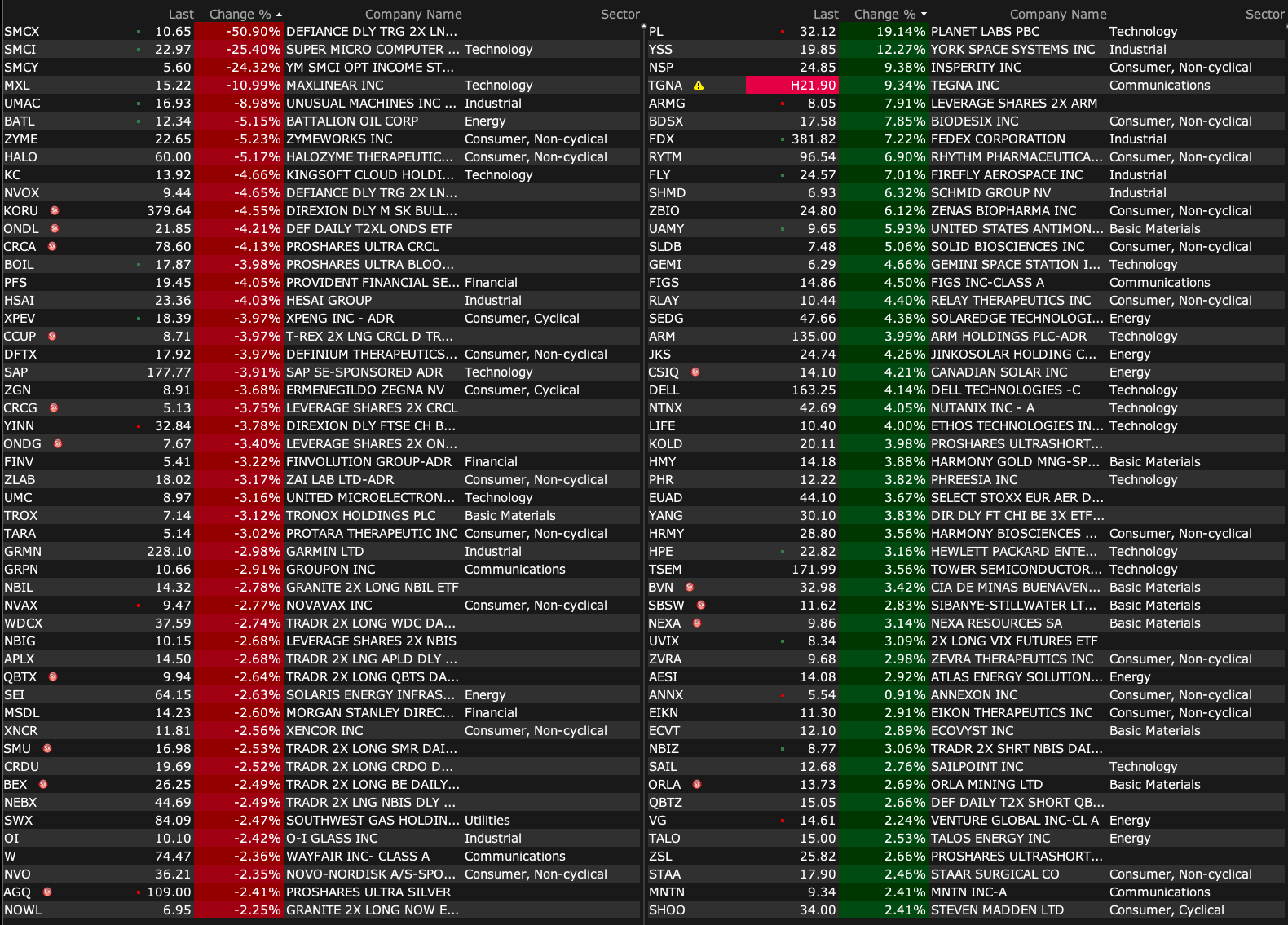

Breadth

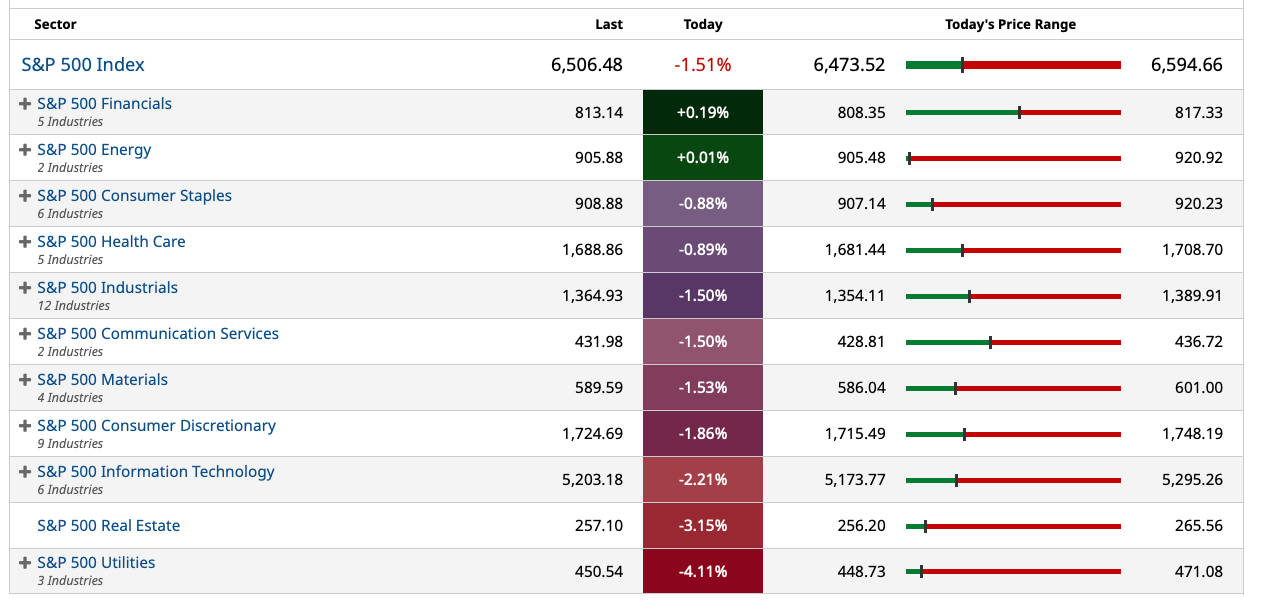

S&P 500 Secotrs

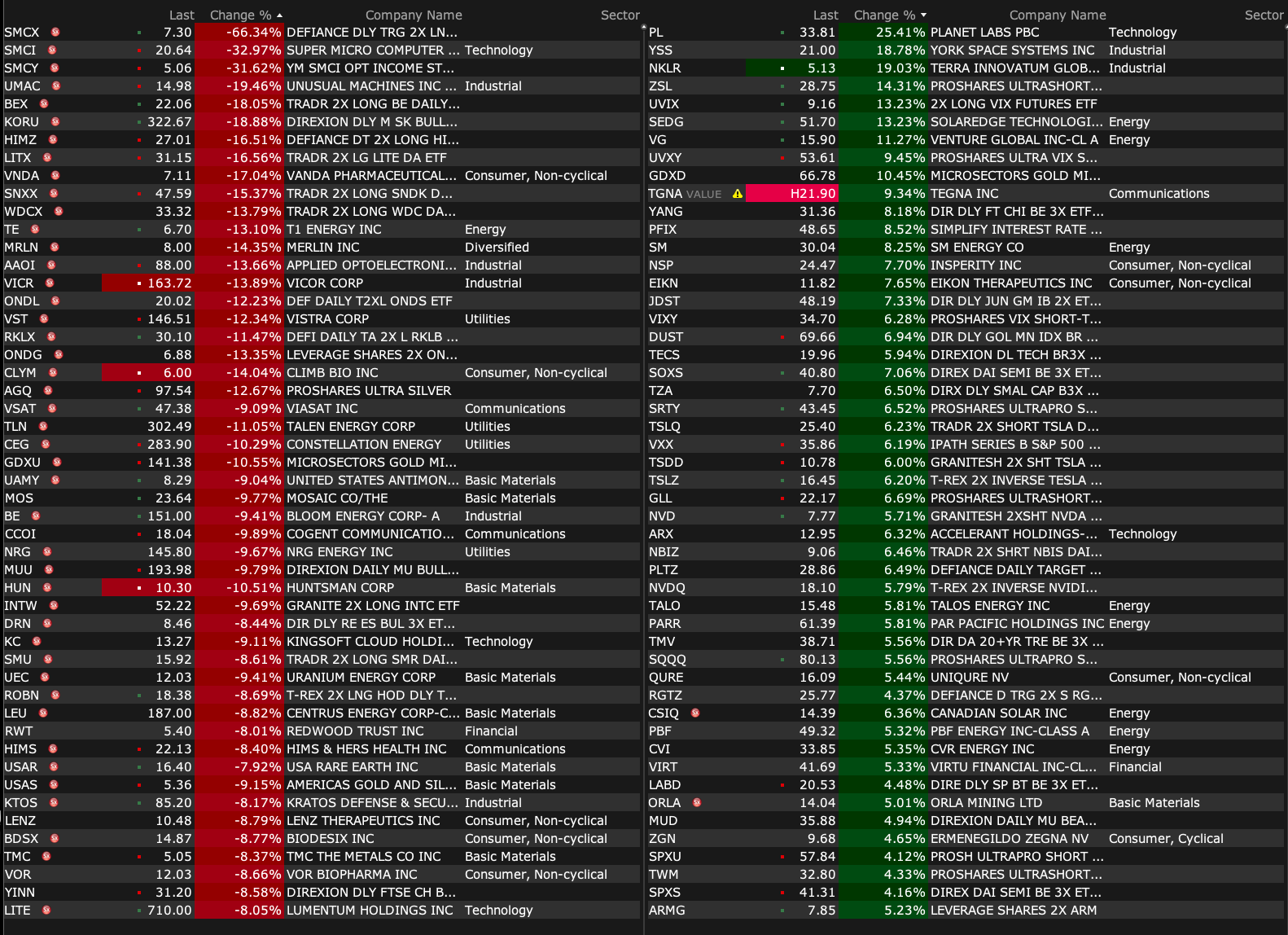

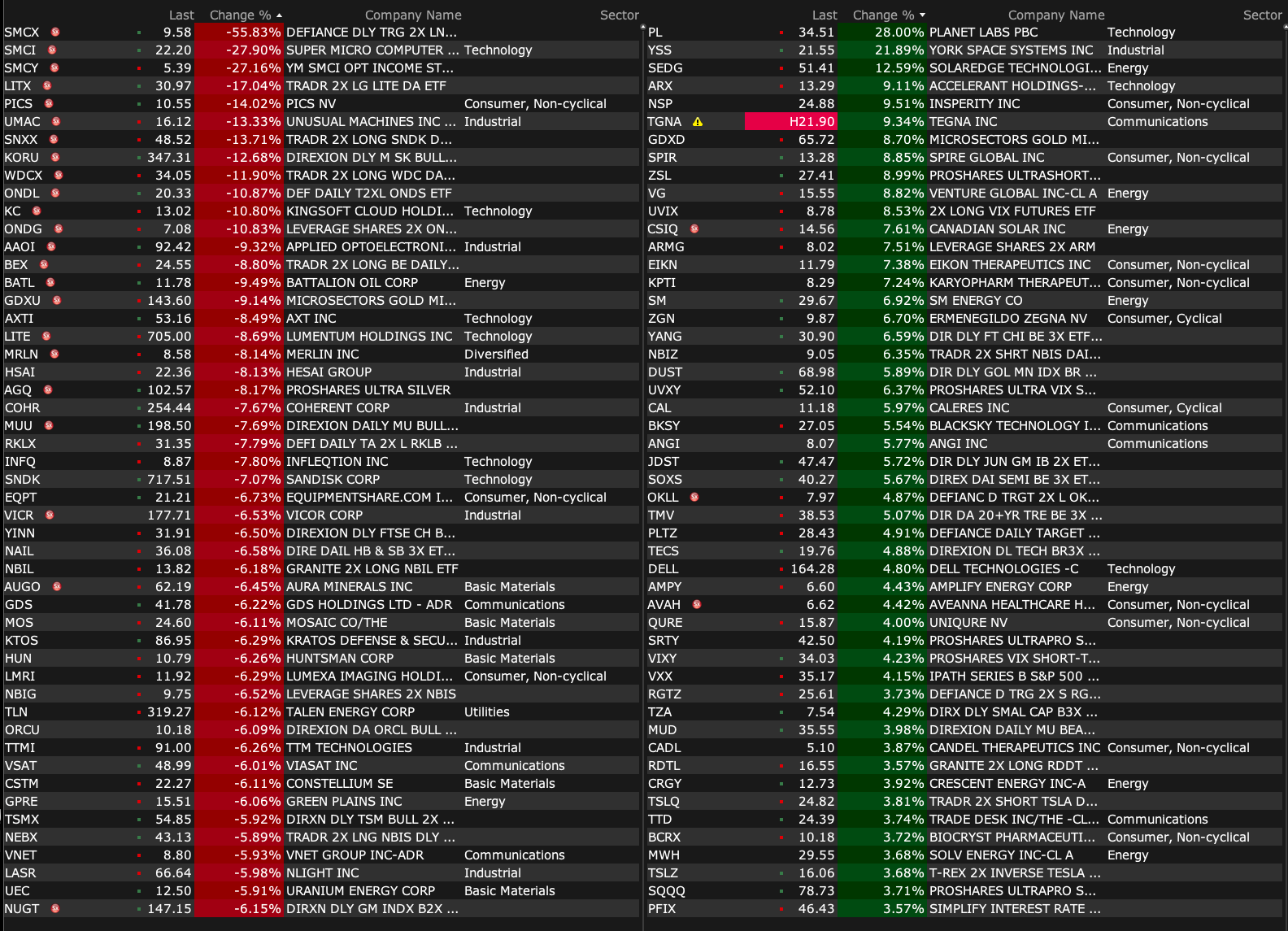

% Movers

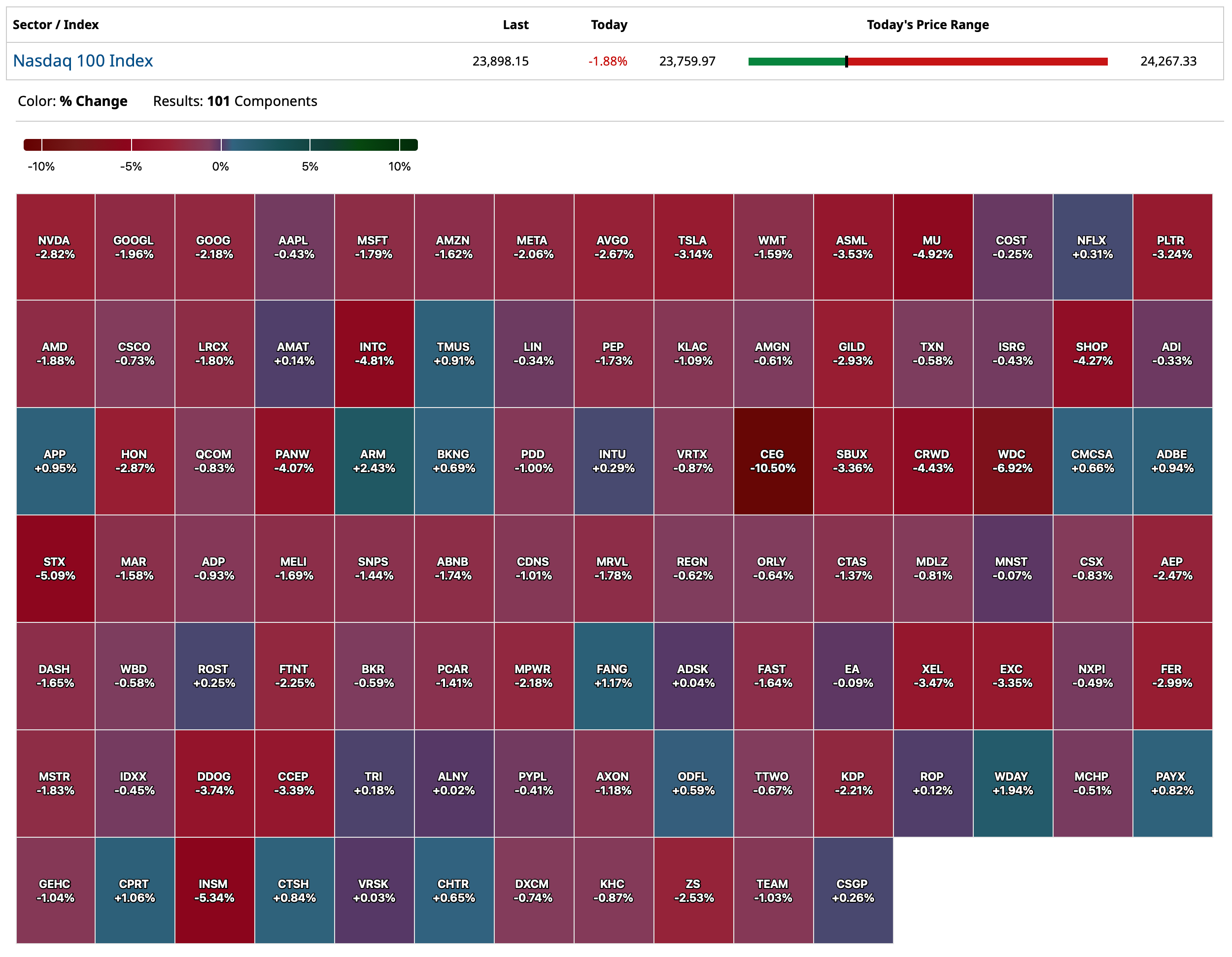

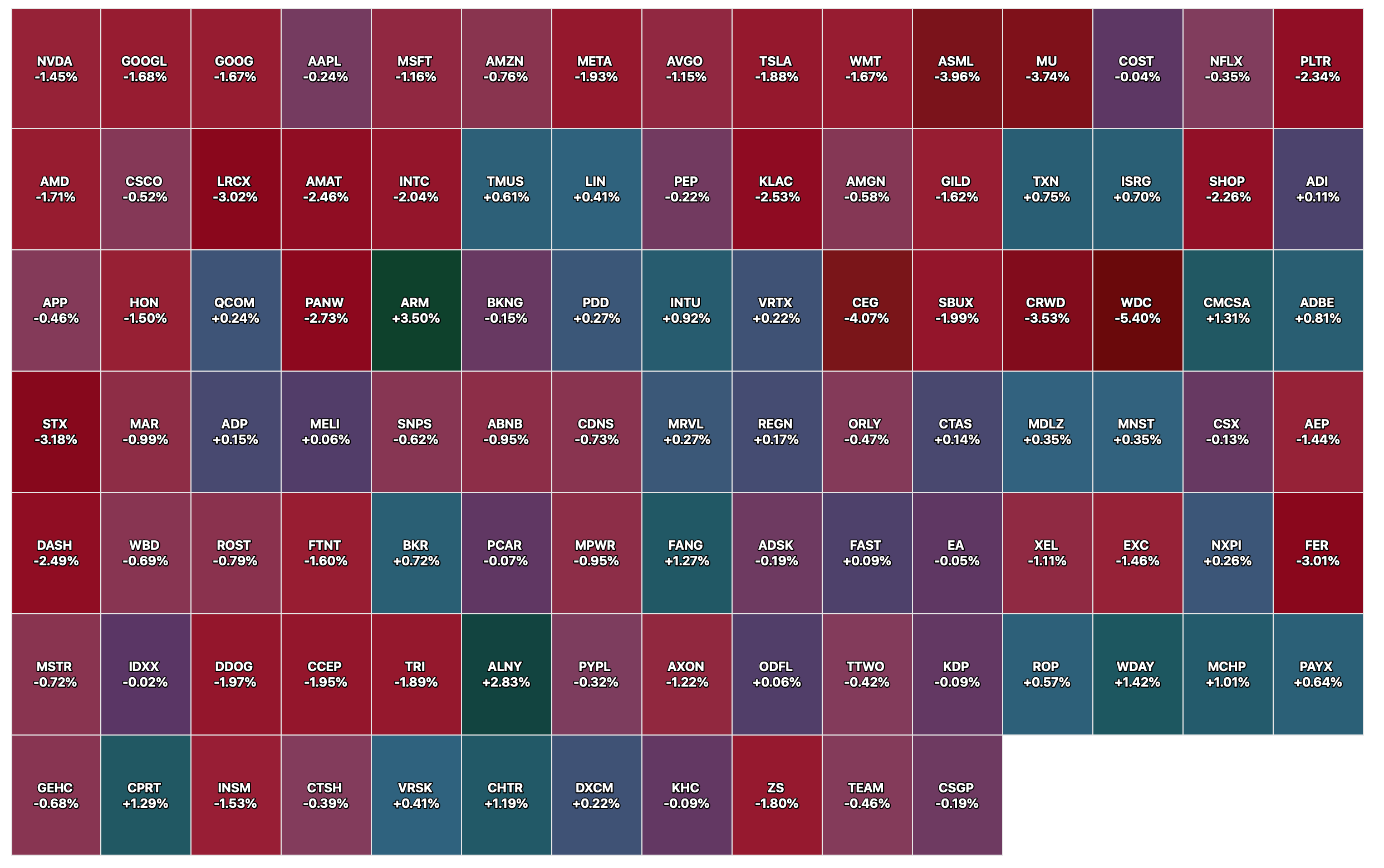

Nasdaq 100 Heat Map

BY Doug Kass · Mar 20, 2026, 4:35 PM EDT

BY Doug Kass · Mar 20, 2026, 4:24 PM EDT

With the averages at their day's lows and S&P cash -102 handles, I am adding to indices and tech stocks.

BY Doug Kass · Mar 20, 2026, 3:22 PM EDT

Equities taking another leg lower on a CBS report that the U.S. is readying ground troops to enter Iran.

BY Doug Kass · Mar 20, 2026, 2:27 PM EDT

Morgan Stanley (MS) is +$4.10 in a sea of market red.

I am taking some off at $162.65.

BY Doug Kass · Mar 20, 2026, 2:01 PM EDT

Though equities are near the day's lows, I am emboldened by the renewed strength in brokerages and banks (I have emphasized both sectors as buys over the weakness this week).

BY Doug Kass · Mar 20, 2026, 12:53 PM EDT

Our computer technician is here for some upgrades in our system. (Again!)

Radio silence for about an hour.

BY Doug Kass · Mar 20, 2026, 11:40 AM EDT

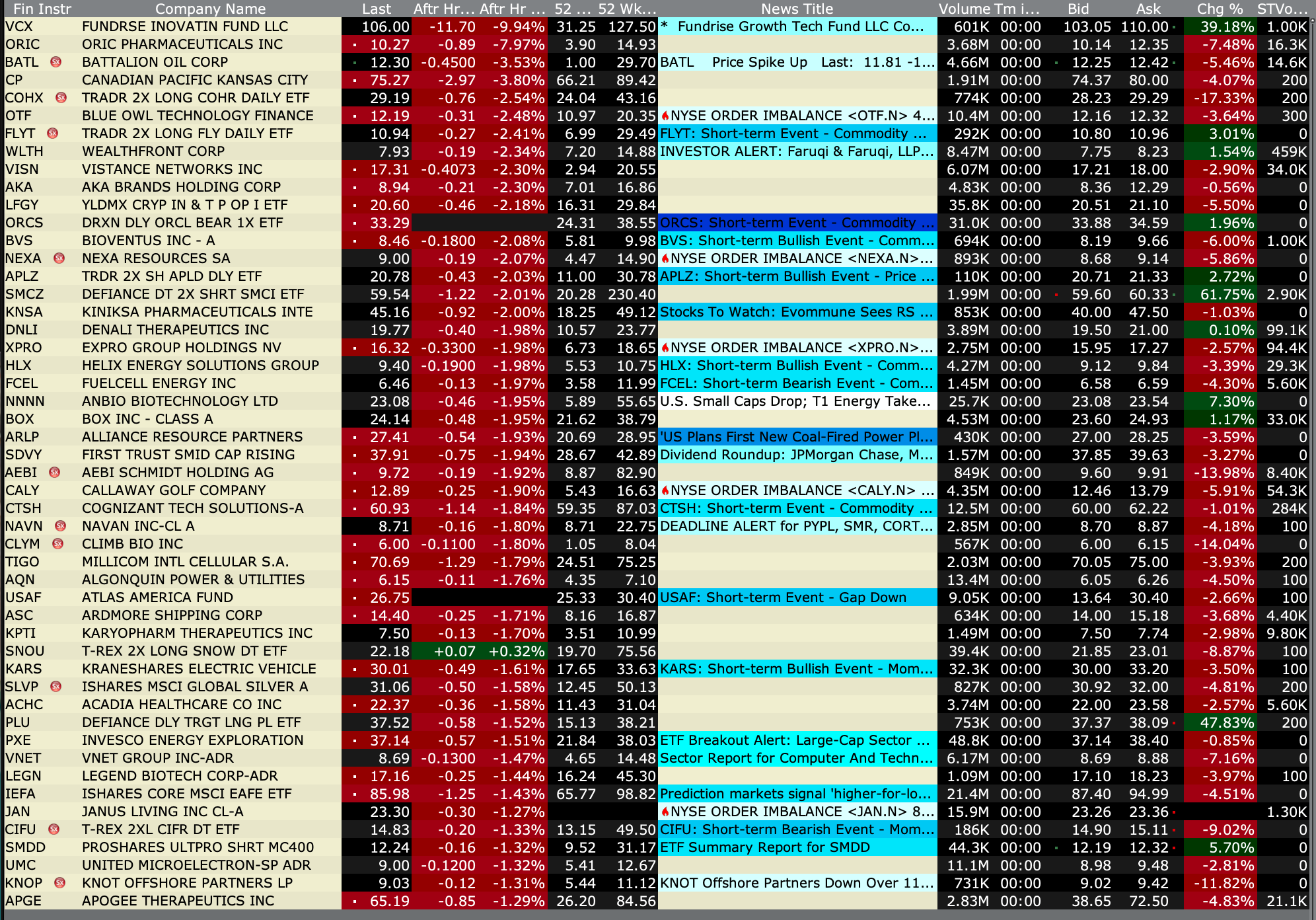

Breadth

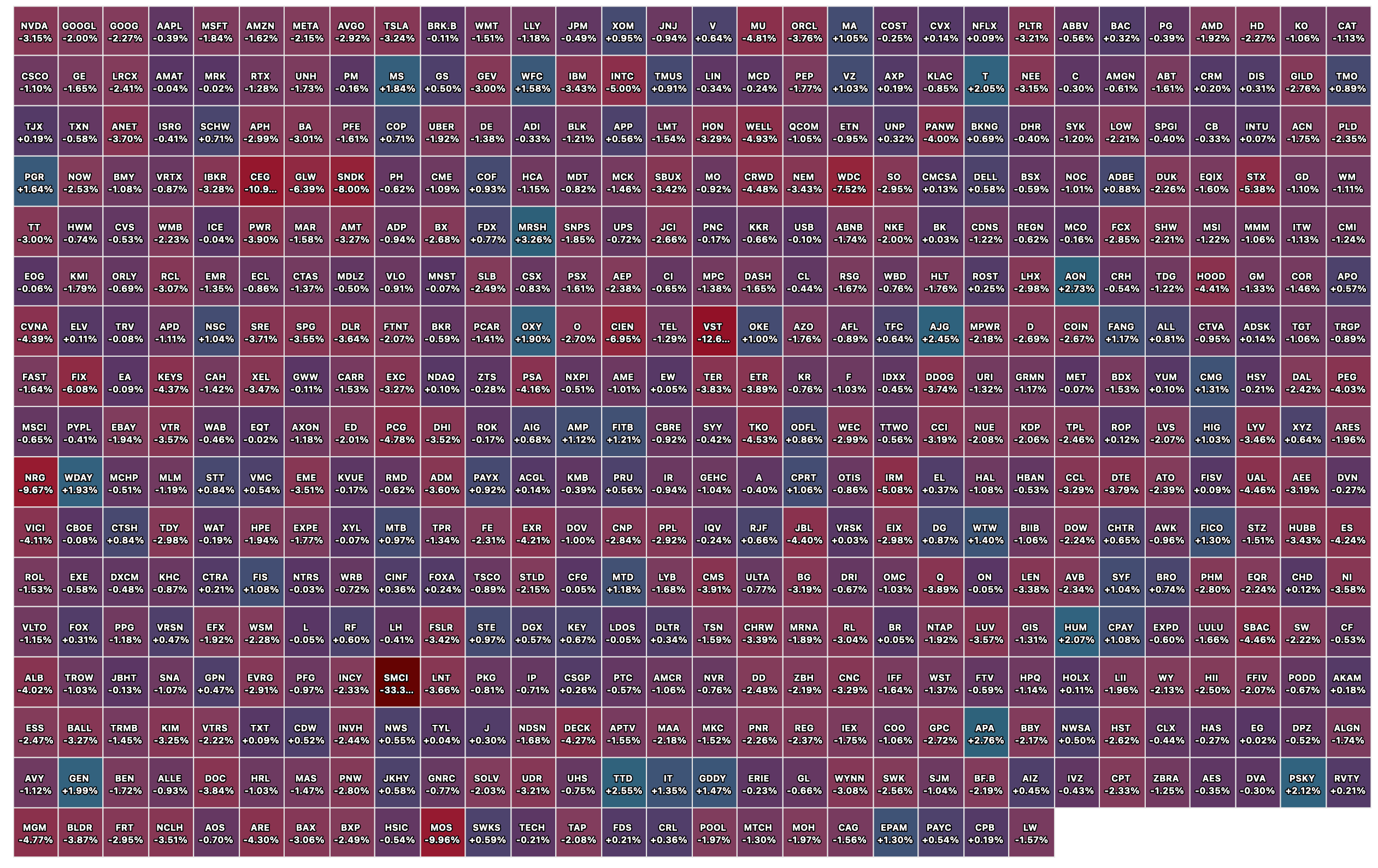

S&P 500 Sector ETFs

% Movers

Nasdaq 100 Heat Map

BY Doug Kass · Mar 20, 2026, 11:30 AM EDT

Bought small trading long rentals in large-cap technology:

* (META) $592.94

* (MSFT) $383.92

* (GOOGL) $300.94

BY Doug Kass · Mar 20, 2026, 11:15 AM EDT

Adding to two cannabis names - Curaleaf (CURLF) $2,29 and Verano (VRNOF) $1.25.

BY Doug Kass · Mar 20, 2026, 10:52 AM EDT

From Peter Boockvar:

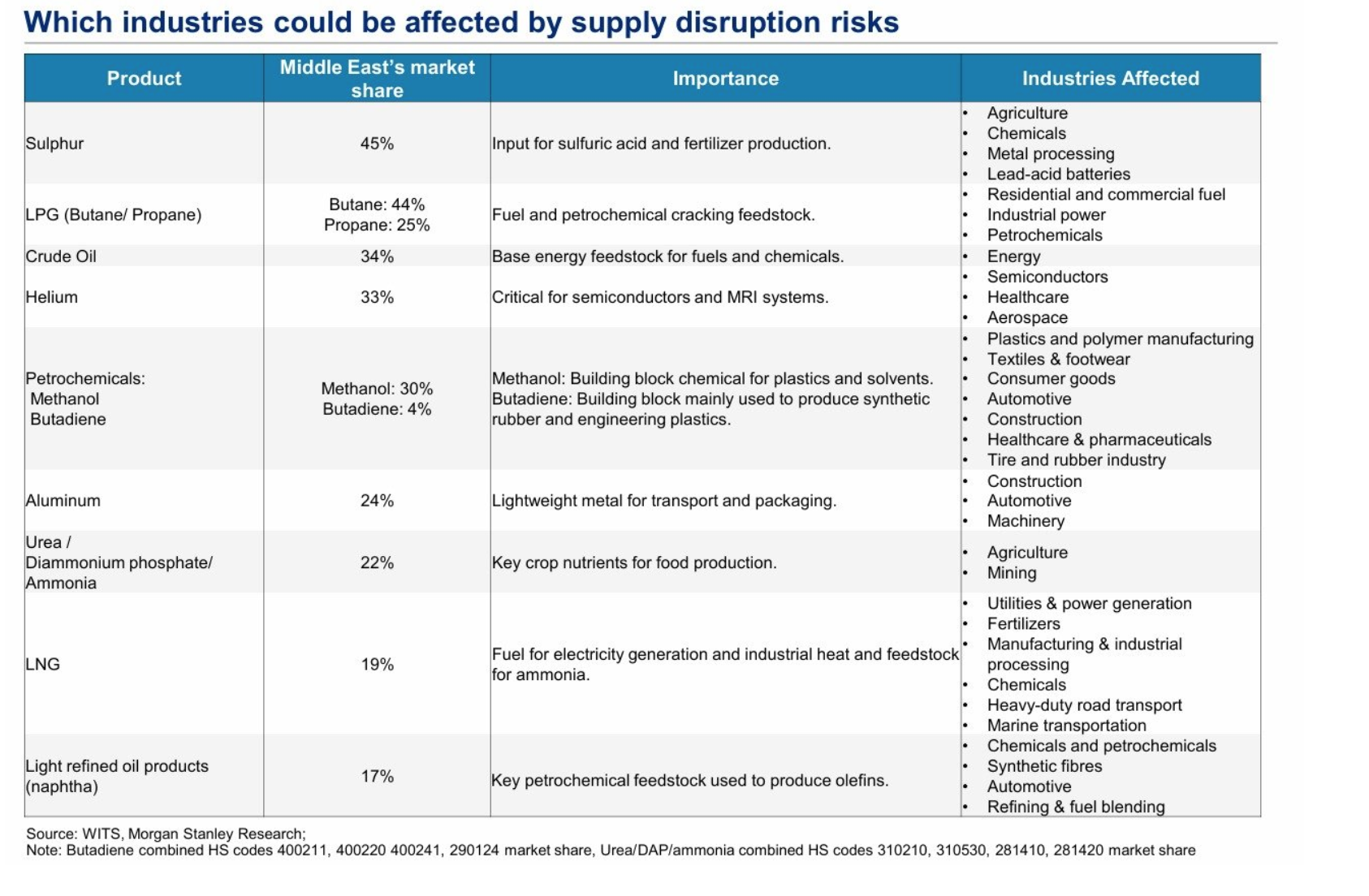

The commodity (oil, gas, fertilizer, etc...) price/supply concern continues to flow into an interest rate worry as they move higher again.

After the BoE told us they are “ready to act” if necessary and only a few hours after the ECB meeting ended, Bloomberg News reported this, “ECB policymakers would be ready to raise interest rates as soon as their next meeting should fallout from the war in Iran push inflation too far above target, according to people familiar with the situation. While nothing has been decided yet and a later date may be more appropriate, factors including signs of second round effects could trigger such a move at the April 29-30 gathering, the people said, asking not to be identified because discussions are confidential.”

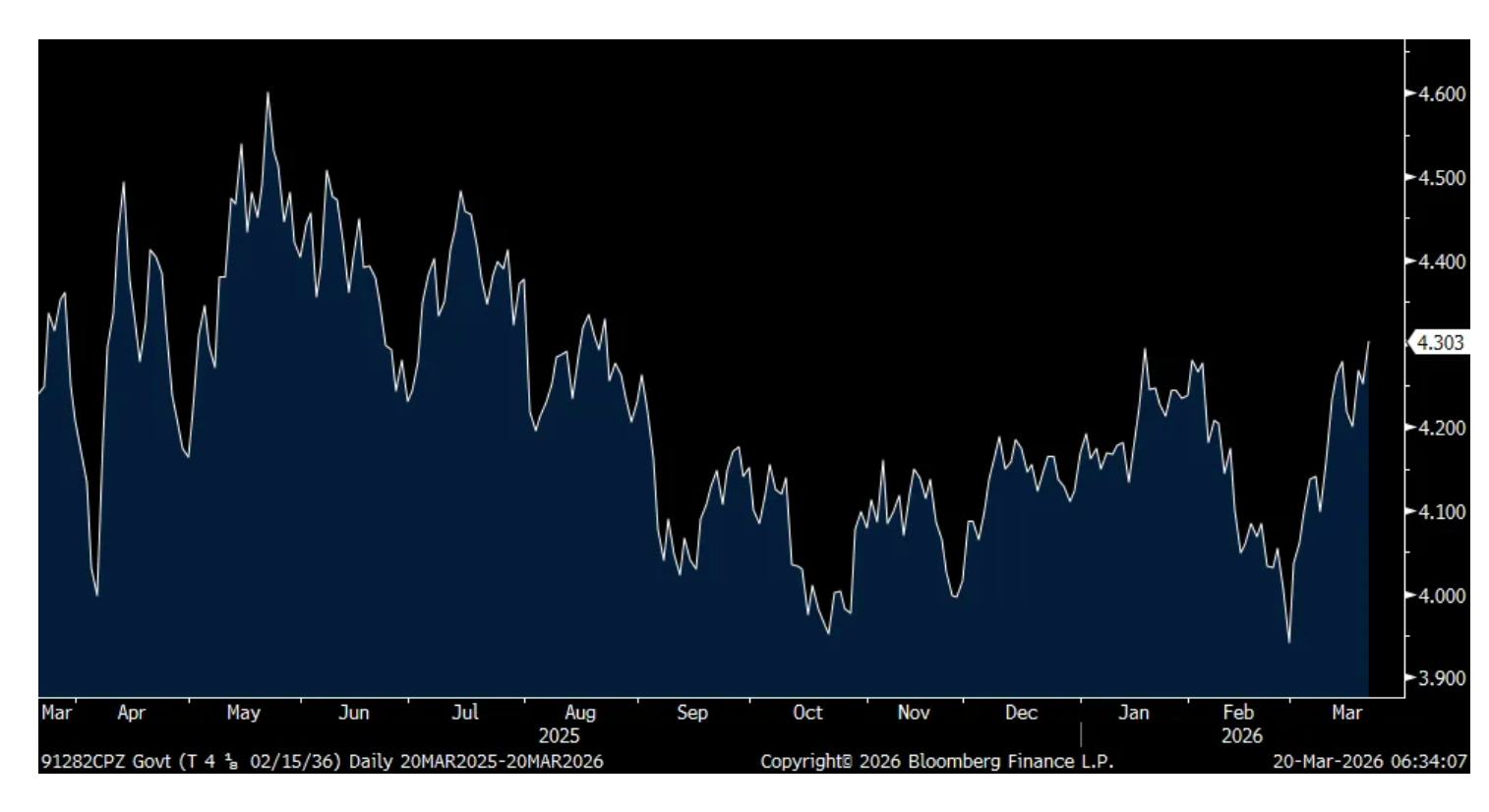

Three ECB rate hikes this year are now priced in and bonds are reacting in kind with yields up across the European sovereign curves and US yields are rising again in sympathy. The US 10 yr yield at 4.30% is now at the highest level since last August. The UK 10 yr gilt yield is breaking out to an 18 yr high. The 10 yr German bund yield is at a rate last seen in July 2011. The French 10 yr yield is at the highest since November 2011.

For the first time that I’ve seen since the Fed started cutting interest rates in September 2024, the fed funds futures are now beginning to price in some rate increases, albeit very small odds. By December the odds of one rate increase is now at 12%. Prior to the FOMC meeting, we were pricing in a 100% chance of one cut. Right after the meeting it was down to 50% and now the major shift today.

I remain bearish on long duration sovereign bonds with still no interest in owning them. Short duration bonds are attractive enough in terms of yield without taking rate risk.

US 10 yr yield

10 yr Gilt yield

German 10 yr yield

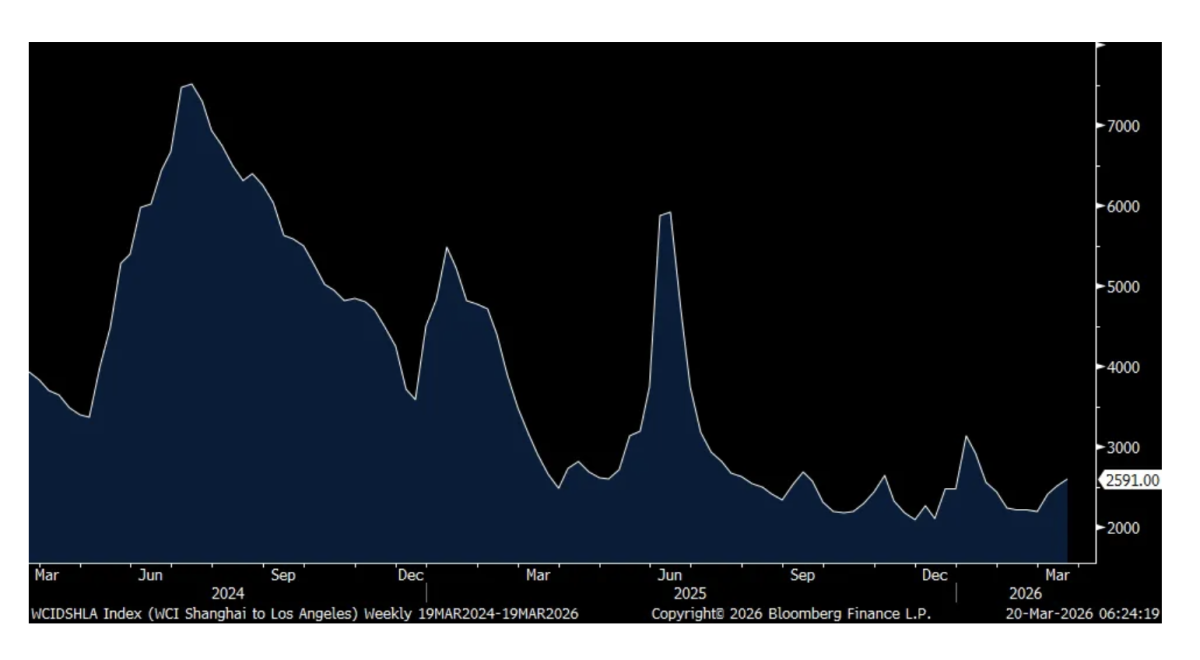

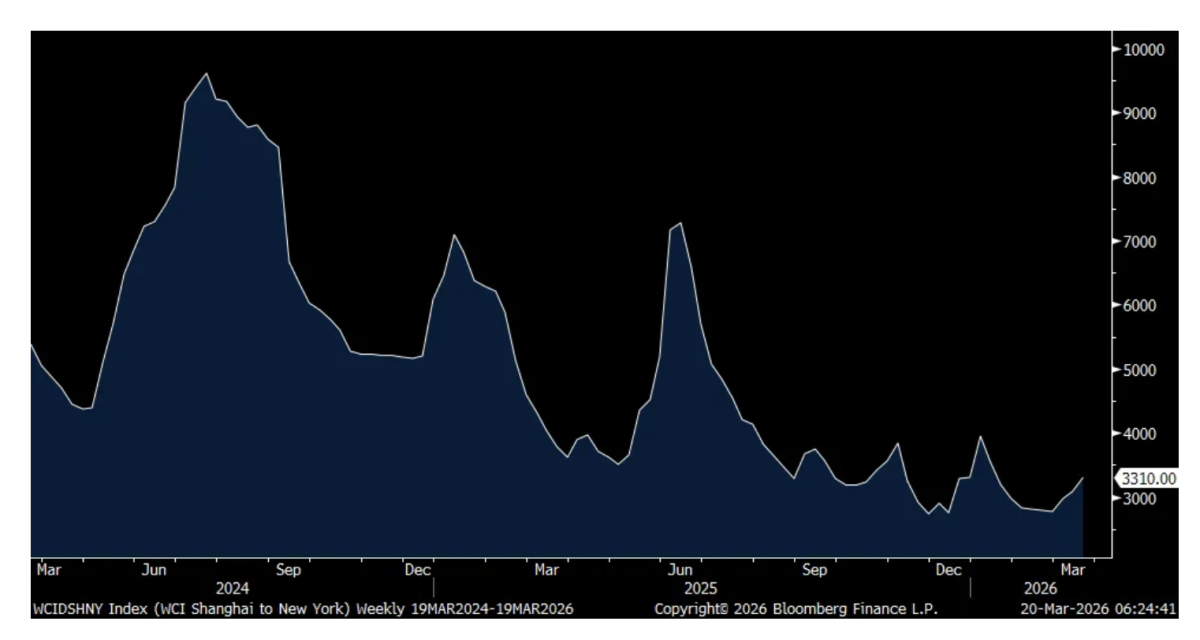

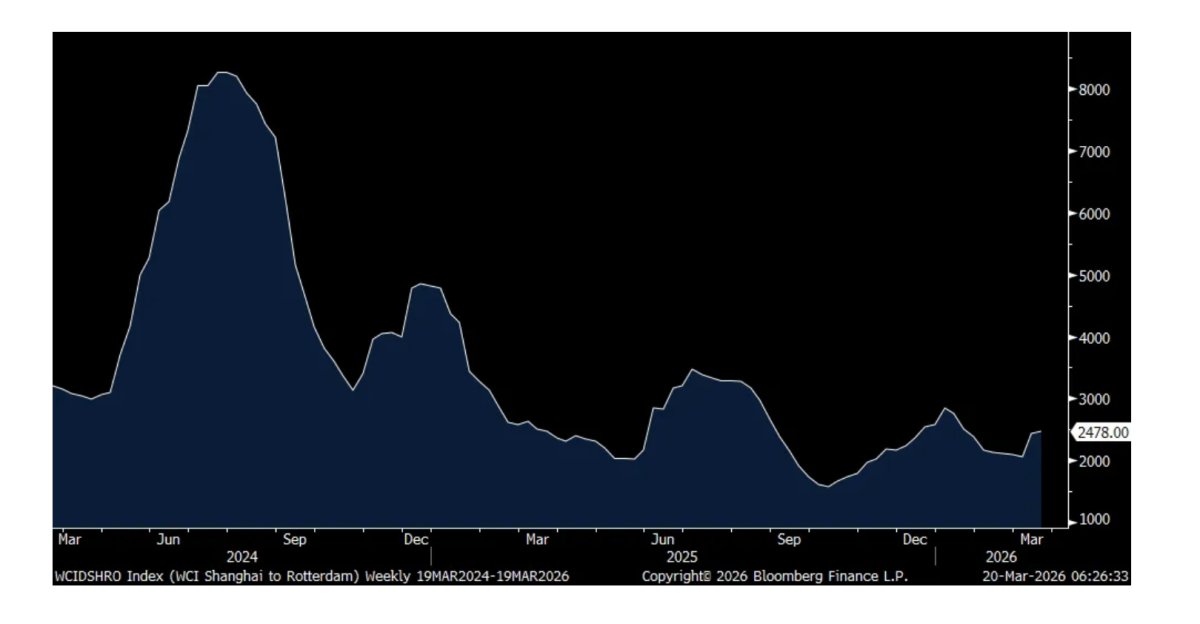

With about 90% of the stuff made in the world ending up on a ship at sea for delivery, we watch again the weekly World Container Index data. The Shanghai to LA route saw container prices rise by another 3.5% w/o/w to $2,591, the highest since mid January but still bouncing along a bottom for now. The trip to NY was up 7.5%. To Rotterdam from Shanghai, it was up a more modest 1.4% but after jumping by 19% in the week before.

Nothing concerning yet with respect to absolute levels but we of course watch to see for any follow through in coming weeks.

Shanghai to LA

Shanghai to NY

Shanghai to Rotterdam

After going through Q1 earnings calls from all the trucking companies I’ve highlighted the firming up of spot rates. Yesterday Freightwaves said “The US truckload spot market just hit a cycle high at $2.82 per mile on the National Truckload Index - that’s the 7 day moving average of booked dry van spot rates, fuel included.” Also this, positively, “Volumes are holding firm at multi-year peaks we haven’t seen since last 2022.”

Further, “This isn’t random noise. Outbound tender rejections nationally are near 13% - highest since early 2022 - meaning carriers are rejecting loads because they can. When rejections spike alongside sustained volumes, it’s classic tightness: capacity meeting demand head-on.”

And a major factor in the capacity reduction, outside of the businesses lost in the manufacturing recession, “the compliance crackdown began last summer with FMCSA audits of state CDL (commercial drivers license) issuance, training provider registries, and non-domiciled licenses, and it’s now starting to show real, measurable impacts on available capacity - just as the freight market appears to be turning up.”

And then let’s take this to FedEx and who reported a solid quarter with a good guide and the stock is jumping in response:

“Revenue was up 8% y/o/y driven by yield and volume strength across nearly all our packaged services.” They took this sales growth and drove a 7% operating income gain “as we successfully managed headwinds tied to changing global trade policies, a challenging LTL demand environment, and the grounding of our MD-11 fleet. We also effectively overcame significant weather related service constraints.”

“As anticipated, freight results remain pressured as a result of ongoing LTL industry trends, along with increased separation related expenses. Importantly, we are laser focused on revenue quality. As a result, higher rates and revenue per shipment at FedEx Freight helped mitigate lower shipment volumes.” Their delivery and express business outperformed freight.

“Our pricing strategy is driving yield growth...We have seen a strong capture rate on the 5.9% general rate increase we implemented in January.”

In their delivery and express business, “We expect US domestic volume growth to continue in Q4...At FedEx Freight (which is being spun out), we now expect fiscal year ‘26 revenue to be down low single digits y/o/y, with revenue flat to down slightly in Q4 due to the continued LTL industry demand weakness.”

The Middle East is a small portion of their business but they of course are watching the situation closely.

Signet Jewelers stock had a great day yesterday, rising by 14% and they said this of note:

“we delivered positive comps for the vast majority of the past year...Turning to fiscal ‘27, sales momentum continued into the year with a positive Valentine’s Day performance, which has continued quarter to date.”

They also strongly improved its execution and merchandising.

“November and the first half of December was the slowest period of the quarter, down around 3%. We implemented broader promotions ahead of our high volume days in December to deliver a positive performance in the back half of the month with further improvement in January. By category, this quarter’s results reflect mid single digit comp growth in services and low single digit declines in bridal and fashion.”

Darden Restaurants is always a good earnings call to go through because of their range of restaurants with everything from Olive Garden, LongHorn Steakhouse, Yard House, Ruth’s Chris, Capital Grille, Season’s 52, Eddie V’s and Cheddar’s Scratch Kitchen. From them:

“All of our segments delivered positive same restaurant sales as our restaurant teams continued to be brilliant with the basics.”

Olive Garden comps rose 3.2% with value a focus as they added “seven more dishes under $15.” LongHorn saw comps jump by 7.2% with likely help from higher beef prices.

‘Fine dining’ comps were up 2.1%.

“We expect overall inflation to be in the mid-3s and our pricing to be in that mid 3s.”

On what they are seeing with this move higher in gas prices, “the data doesn’t show a really strong correlation between gas prices and restaurant spending. I would say historically higher gas prices had more of an impact on durable goods and less of an impact on services. And I’ve been through a number of these cycles...When there’s a sudden and significant price increase in gas, there can be a brief pullback, but that’s usually in a few weeks.”

“The biggest driver we see in traffic for restaurants is GDP. So if gas prices remain high for a long period of time and make a big impact to GDP, there may be some softness. But in general, we’re not too worried about gas prices. And we’ll be able to react however we need to if they stay really high for a while.”

From Accenture and their big picture view of the environment that they see:

“We saw again this quarter clients continuing to prioritize their most strategic and large scale transformational programs which positions us in the center of their reinvention agendas. As clients finalize their budgets going into calendar year 2026, we are seeing spending similar to 2025.”

“Demand continues to be driven by a few major themes. First, clients are implementing foundational programs with our ecosystem partners to capture the full opportunity of AI.”

“Second, clients continue to look to reinvent faster, leverage our proprietary platforms and expertise and achieve greater efficiencies through managed services across the enterprise...And third, clients with more advanced digital cores are starting to take on larger AI programs.”

Finally, the one thing of note with the economic data overseas, the March UK CBI industrial orders index was little changed at -27 and trying to put in a bottom. CBI said “There are signs that conditions are beginning to stabilize for manufacturers, with a long period of falling output expected to bottom out and selling price growth anticipated to slow over the next three months. Conditions remain challenging nonetheless, with the orders pipeline still historically weak. The conflict in the Middle East is pushing up energy costs and risks further disrupting supply chains, adding to the cost pressures already facing manufacturers.”

BY Doug Kass · Mar 20, 2026, 10:50 AM EDT

Added to (AMZN) At $206.61

BY Doug Kass · Mar 20, 2026, 10:29 AM EDT

With S&P cash -61 handles I am moving toward medium-sized indexes.

BY Doug Kass · Mar 20, 2026, 10:21 AM EDT

BY Doug Kass · Mar 20, 2026, 10:10 AM EDT

Chart from 9:46 a.m. ET

BY Doug Kass · Mar 20, 2026, 10:10 AM EDT

With S&P cash -53 handles I am moving up to small-sized long the indexes:

BY Doug Kass · Mar 20, 2026, 10:06 AM EDT

BY Doug Kass · Mar 20, 2026, 9:50 AM EDT

BY Doug Kass · Mar 20, 2026, 9:15 AM EDT

BY Doug Kass · Mar 20, 2026, 9:05 AM EDT

BY Doug Kass · Mar 20, 2026, 8:55 AM EDT

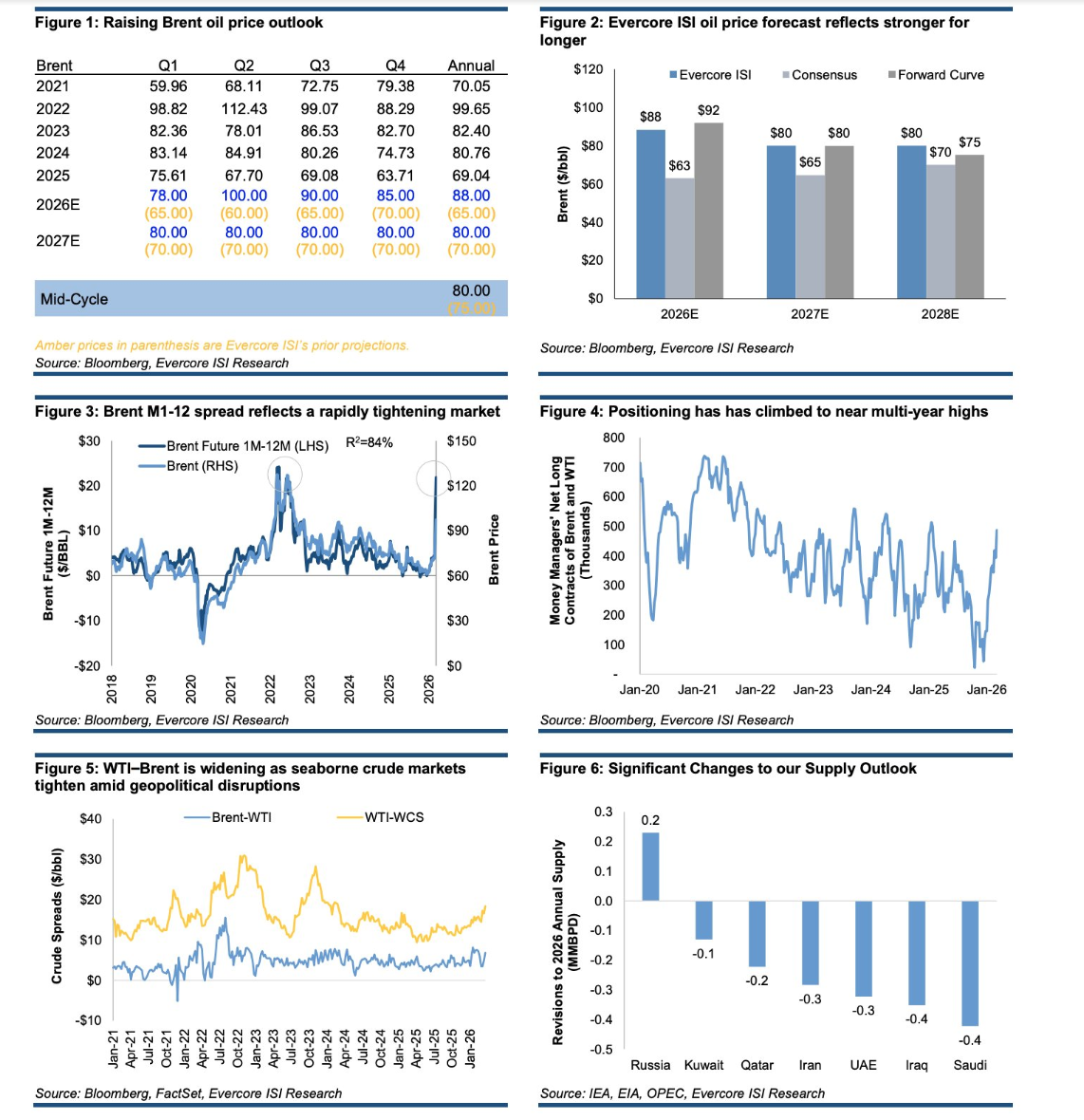

* "Slugflation" is now almost guaranteed to be a semi permanent condition...

The problem is that we now have to get comfortable with the notion of higher oil prices for longer.

Here is Evercore ISI's oil price forecast:

Evercore ISI Oil Price Outlook

BY Doug Kass · Mar 20, 2026, 8:45 AM EDT

The bear flattening of the US yield curve continues today, driven by two primary factors: first, market consensus pushing expectations for a Federal Reserve rate cut past 2026 and into 2027; second, while inflation concerns are pressuring longer-term yields upward, that is being… pic.twitter.com/BlgEGssb6T

— Mohamed A. El-Erian (@elerianm)

BY Doug Kass · Mar 20, 2026, 8:35 AM EDT

* Amazon remains our only investment in large cap technology

* The share prices of the MAG7 "Generational Compounders" remain in a clear downtrend...

It may seem to you that I'm acting confused

When you're close to me

If I tend to look dazed, I've read it someplace

I've got cause to be

There's a name for it

There's a phrase that fits

But whatever the reason, you do it for me

Oh-oh, what's love got to do, got to do with it?

What's love but a second-hand emotion?

What's love got to do, got to do with it?

Who needs a heart, when a heart can be broken?

- Tina Turner - What's Love Got To Do With It (Official Video) [HD]

While it can be argued (accurately) that the "love affair" with the Magnificent 7 has produced most of the intermediate-term gains in the S&P index over the last decade, as noted in the Mag 7 chart (below), large cap technology continues in a clear downtrend since 4Q 2025, something I have warned about over the last 24 months (as the hyperscalers moved from capital light to capital intensive):

The percentage and $ price declines from the 2025-26 highs are becoming meaningful - avoiding the stocks since then has contributed to portfolio alpha:

% Below All-Time High

— Charlie Bilello (@charliebilello)

Chevron: 0%

S&P 500: -5%

Google: -12%

Apple: -13%

Gold: -14%

Nvidia: -15%

Amazon: -19%

Tesla: -21%

Meta: -23%

Palantir: -27%

Microsoft: -29%

Netflix: -30%

Bitcoin: -44%

Ethereum: -56%

MicroStrategy: -74%

Fartcoin: -92%

Trump Coin: -95%

Melania Coin: -99%

At times over the last 10 years I have been long every member of MAG7 (except (AAPL) , which sporadically, I have been short). I even briefly held Nvidia when the shares traded close to par in the market correction of early 2Q 2025.

In the last year Seabreeze has successfully traded (META) , (AMZN) and (GOOGL) .

However, since late 2025 I have only been long a small position in Amazon.

Panelists and guests on the "shows" continue to demonstrate Pavlovian behavior in coming back (in their daily commentary) to Mag 7 - reminding me of one of Bob Farrell's 10 Rules of Investing:

Rule #9. When all the experts and forecasts agree – something else is going to happen.

Translation: This rule fits with Farrell's contrarian streak. When all analysts have a buy rating on a stock, there is only one way to go (downgrade). Excessive bullish sentiment from newsletter writers and analysts should be viewed as a warning sign. Investors should consider buying when stocks are unloved, and the news is all bad. Conversely, investors should consider selling when stocks are the talk of the town, and the news is all good. Such a contrarian investment strategy usually rewards patient investors.

Nvidia (NVDA) , in particular, seems to be the new "value play" to many on CNBC - as panelists cite its "remarkably low) low PEG rates. I would note that low PEG rates Price/Earnings-to-Growth (PEG) Ratio: What It Is and the Formula are historically associated with a peak and maturing EPS cycle - which I believe to be the case with Jensen Huang's company.

By contrast, I intend to continue the strategy of avoiding the last cycle's market leaders for the many reasons mentioned in my Diary.

Finally, a further breakdown in large cap technology would (obviously) portend poorly for the broader market:

My focus continues to be on the Mag 7, which has remained in its narrow range since last October. Should we break the lows, the broader indices will be at risk of a deeper correction. pic.twitter.com/DCwPOyMXCH

— Jurrien Timmer (@TimmerFidelity)

BY Doug Kass · Mar 20, 2026, 8:05 AM EDT

Chart of the Day

Coal ETF

The Range Global Coal ETF (COAL), launched in January 2024, closed at new all-time highs and posted its best day of the year.

Meanwhile, the original VanEck Vectors Coal ETF (KOL) was liquidated almost perfectly at the cycle lows in 2020, right before coal equities began their historic run.

Markets have a funny habit of pulling the plug at the wrong time, with delistings and closures often aligning with major bottoms.

The Takeaway: Coal stocks continue to be a strong group within Energy, with the Coal ETF making record highs today.

The last 3 FOMC interest rate decisions. $QQQ pic.twitter.com/xbcPi7IWSt

— Beardo (@BeardoTrader)

Breadth Studies Update: Midterm breadth continues to deteriorate, and now long-term breadth is nearing a bearish cross. When this occurs, it signals the risk of a deep correction or the start of a bear market. $SPY $QQQ $IWM $STUDY pic.twitter.com/ohM5pGC035

— Victor Riesco, CMT (@vriesco_cmt)

Week isn't over, but weekly momentum for the S&P 500 is at a pretty low level..... pic.twitter.com/4q8LlgwKjX

— Andrew Thrasher, CMT (@AndrewThrasher)

they gave up on $MAGS pic.twitter.com/0zK4egmWSC

— Nir (@NirAoo7)

Energy’s dominance over Big Tech / Mag Seven has accelerated.

— Ricardo Sarraf (@nullcharts)

Many moves across the space may feel extended, but history suggests there is still meaningful room for further outperformance.

If anything, the trend and momentum profiles today resemble November 2021 more than… https://t.co/S6Ak5woWlx pic.twitter.com/Mt2c4Xdfo8

Might be time to admit secular #disinflation is history. When excluding the pandemic 5-year…5 year!...#breakevens are the now highest in 20 years! pic.twitter.com/LZu8De7G0U

— Richard Bernstein Advisors (@RBAdvisors)

Gold futured $GC_F coming into important VWAP level of interest ~4585 $GLD pic.twitter.com/lq9bfbpMn5

— Brian Shannon, CMT (@alphatrends)

The selloff in silver over the past 15 days has been one of the most extreme moves we’ve seen in history.

— Otavio (Tavi) Costa (@TaviCosta)

Only two other episodes are comparable:

One marked a major peak, the other a major bottom.

Personally, I have never seen a true peak in precious metals under conditions… pic.twitter.com/g4vIUMcI5A

Bonuses - here are some great links:

Is Tech Breaking Down? Is Tech About to Break Down?

BY Doug Kass · Mar 20, 2026, 7:48 AM EDT

$3.9 trillion in $SPX notional open interest flow expires today. pic.twitter.com/3A9Nx1A0LU

— Hedgeye (@Hedgeye)

BY Doug Kass · Mar 20, 2026, 7:30 AM EDT

With S&P futures down by only 21 handles (and up 39 handles from the morning lows) I have sold my Index longs for a small profit:

(SPY) $656.26

(QQQ) $590.54

BY Doug Kass · Mar 20, 2026, 7:19 AM EDT

JUST IN: Iran is charging $2 million per tanker to pass through the Strait of Hormuz. The Financial Times reported the payment. The IRGC confirms it by radio. And the world’s most important chokepoint has been converted from a military blockade into a toll road.

— Shanaka Anslem Perera ⚡ (@shanaka86)

The mechanism is… pic.twitter.com/jrLo86q79G

BY Doug Kass · Mar 20, 2026, 6:45 AM EDT

BREAKING: The value of US data centers under construction has officially surpassed the value of office buildings under construction for the first time in history.

— The Kobeissi Letter (@KobeissiLetter)

Data centers under construction are up+29% YoY, to a record $45.1 billion.

Meanwhile, the value of offices under… pic.twitter.com/1fJNVj0A5R

BY Doug Kass · Mar 20, 2026, 6:35 AM EDT

Near‑term inflation expectations have risen on supply shocks tied to energy and geopolitics, which tend to be episodic and act more like a tax on consumers. By contrast, longer‑term inflation expectations tied to wages, services, and consumption remain well anchored, suggesting… pic.twitter.com/DU5POvkpcR

— Rick Rieder (@RickRieder)

BY Doug Kass · Mar 20, 2026, 6:25 AM EDT

The Administration is considering plans to occupy or blockade Iran's Kharg Island in order to pressure Iran to reopen the Strait of Hormuz.

I am buying the weakness.

BY Doug Kass · Mar 20, 2026, 6:15 AM EDT

* At 6:05 AM...

With S&P futures -45 handles, I am taking a long rental (again) in the Indices:

BY Doug Kass · Mar 20, 2026, 6:10 AM EDT

The S&P Short Range Oscillator remains in oversold territory at -6.61% vs. -7.45%.

BY Doug Kass · Mar 20, 2026, 6:05 AM EDT

#Iran War Update No. 20 (focus on Iranian strategic narrative):

— Hamidreza Azizi (@HamidRezaAz)

🔹The Strait of Hormuz is being increasingly framed in Tehran as a tool of Iranian leverage rather than a temporary wartime tactic. Iranian officials are openly discussing a post-war regulatory regime, including…

BY Doug Kass · Mar 20, 2026, 6:00 AM EDT

JUST IN: Iran is charging $2 million per tanker to pass through the Strait of Hormuz. The Financial Times reported the payment. The IRGC confirms it by radio. And the world’s most important chokepoint has been converted from a military blockade into a toll road. The mechanism is Show more

$3.9 trillion in $SPX notional open interest flow expires today.

The bear flattening of the US yield curve continues today, driven by two primary factors: first, market consensus pushing expectations for a Federal Reserve rate cut past 2026 and into 2027; second, while inflation concerns are pressuring longer-term yields upward, that is being Show more

% Below All-Time High Chevron: 0% S&P 500: -5% Google: -12% Apple: -13% Gold: -14% Nvidia: -15% Amazon: -19% Tesla: -21% Meta: -23% Palantir: -27% Microsoft: -29% Netflix: -30% Bitcoin: -44% Ethereum: -56% MicroStrategy: -74% Fartcoin: -92% Trump Coin: -95% Melania Coin: -99%

The last 3 FOMC interest rate decisions. $QQQ

BREAKING: The value of US data centers under construction has officially surpassed the value of office buildings under construction for the first time in history. Data centers under construction are up+29% YoY, to a record $45.1 billion. Meanwhile, the value of offices under Show more

Near‑term inflation expectations have risen on supply shocks tied to energy and geopolitics, which tend to be episodic and act more like a tax on consumers. By contrast, longer‑term inflation expectations tied to wages, services, and consumption remain well anchored, suggesting Show more

My focus continues to be on the Mag 7, which has remained in its narrow range since last October. Should we break the lows, the broader indices will be at risk of a deeper correction.

they gave up on $MAGS

The selloff in silver over the past 15 days has been one of the most extreme moves we’ve seen in history. Only two other episodes are comparable: One marked a major peak, the other a major bottom. Personally, I have never seen a true peak in precious metals under conditions Show more

Energy’s dominance over Big Tech / Mag Seven has accelerated. Many moves across the space may feel extended, but history suggests there is still meaningful room for further outperformance. If anything, the trend and momentum profiles today resemble November 2021 more than Show more

Might be time to admit secular #disinflation is history. When excluding the pandemic 5-year…5 year!...#breakevens are the now highest in 20 years!