BREAKING: MUST WATCH FOR EVERYONE WHO OWNS STOCKS.

Legendary Investor Howard Marks appearing yesterday on Bloomberg discussed Retail being pushed to invest in Private Credit, Stock Market Cycles and "Cockroaches in the Coal Mine".

BREAKING: Qatar’s Prime Minister stood at a podium today and delivered one sentence that will fracture Gulf alliance architecture for a generation: “Everyone knows who the main beneficiary of this war is.”

🚨🚨🚨BREAKING: NEW CANNABIS UPLISTING BILL, HR 7987, HAS BEEN FILED!

The bill intends to amend the Securities Exchange Act of 1934 and allow the listing of securities for cannabis-related legitimate businesses $MSOSpic.twitter.com/2EVivEporN

Boockvar on Commodity Prices, Limits of Monetary Policy

From Peter Boockvar:

Commodity prices/Monetary policy "can't fix the war"/Pulse of the US consumer

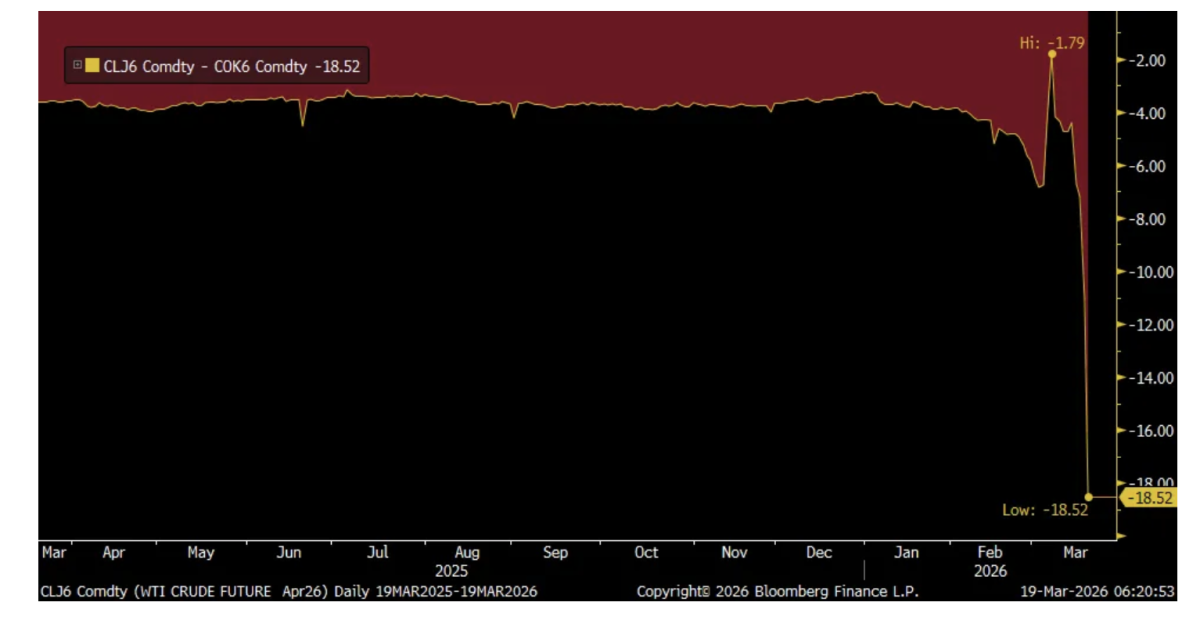

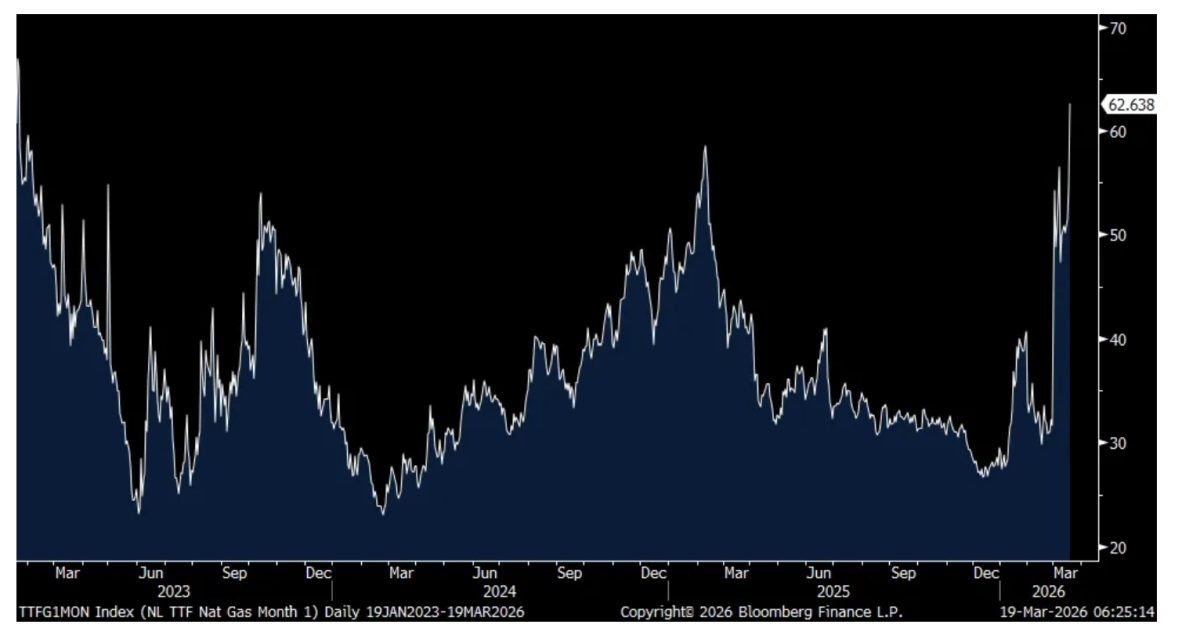

The brent crude/WTI spread has really blown out on the Ras Laffan LNG attack with Iran literally going scorched earth by bombing its neighbors with whoever is left of that government and TTF natural gas in Europe is higher by 16% to 63.17 euros/mwh.

Brent/WTI crude oil spread

TTF Natural Gas

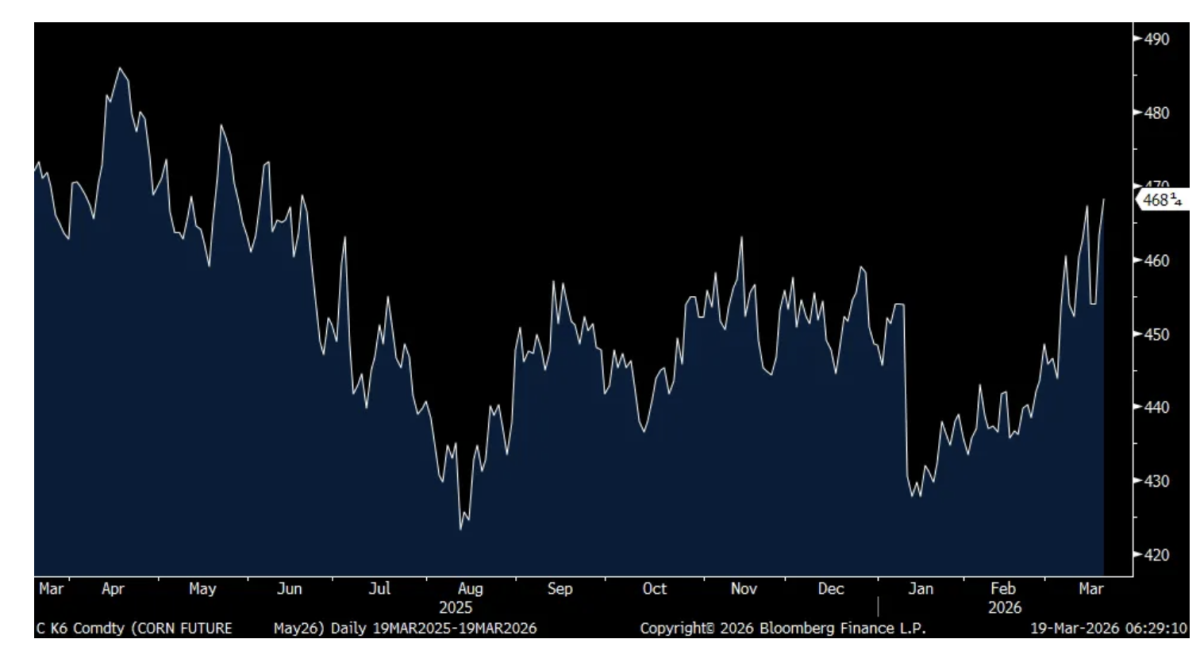

With the fertilizer disruptions and jump in prices, mostly nitrogen, corn prices have broken out to the highest since last June at $4.68 a bushel for the May contract with the planting season now upon us. Wheat is 3 cents from the highest since June while soybeans continue to trade around $11.50-$12.

I want to emphasize, the farmer needs much higher crop prices from here to offset costs rising aggressively for diesel and fertilizer. That won’t be good for consumers of course but a trade off that will have to be balanced.

Corn

With respect to the Fed and the post bond market response, odds of a rate cut by December is now down to just 40% vs 100% priced in on Tuesday. The BoJ did nothing overnight as expected but they could hike in April. Here were some notable quotes from Governor Ueda:

“Even if the economy comes under downward pressure, if we judge that such downward pressure would be temporary and will not affect underlying inflation, it would be possible for us to raise interest rates.”

With what is going on with the spike in energy prices, “One standard idea would be to look through the impact if it is a temporary supply shock. But it’s not clear whether the shock would be temporary, making it hard to say in advance how much it could take to determine the impact on underlying inflation.”

“We need to be mindful that recent developments come at a time when companies are already actively pushing up prices and wages, which suggests they could pass on costs more aggressively than after the war in Ukraine.”

“The biggest point would be what happens to our baseline scenario when we review our quarterly forecasts in April, as well as the balance of risks. We will need to look at whether we can maintain our baseline scenario and even if so, judge the likelihood of this scenario materializing. We also need to look at upside and downside risks. If we see risks that we cannot leave unattended, I won’t rule out the chance of shifting policy from a risk management perspective.”

And we await the results of this, “It will likely become increasingly difficult to gauge underlying inflation partly due to the government’s steps to cushion the blow from inflation, and rising oil prices. As such, we will release more thorough information on core consumer inflation. We will also re-calculate Japan’s estimated natural rate of interest and release our findings once necessary preparations are completed.”

The 2 yr JGB yield rose 2 bps with the bigger moves in the long end of their curve, as it is for all sovereign bonds around the world today with another jump in brent crude and natural gas prices. The yen is rallying on the possibility of an April hike and Ueda said this, “We need to be mindful that currency fluctuations could have a stronger impact on underlying inflation than in the past.”

Also helping the yen was this comment from the Japanese Finance Minister on the yen weakness, “We’re maintaining a very high sense of urgency. We are prepared to respond fully at any time, having the impact of currencies on people’s lives in mind.” It’s obvious now that 160 is their line in the sand and why the BoJ will likely hike rates in April.

Brazil has REAL rates of about 11% so they have room to cut and they did last night by 25 bps as expected to 14.75%. With still very high REAL rates and being a major commodity producer, we own Brazilian bonds.

The Swiss National Bank held rates at zero and said they will continue to try to drive the Swiss franc lower via intervention but luckily they are avoiding NIRP for now. SNB President Martin Schlegel said “A rapid and excessive appreciation of the Swiss franc poses a risk to price stability. To counter this risk, our willingness to intervene in the foreign exchange market has increased.”

This is what the Bank of Canada said of note yesterday as they kept their policy rate unchanged at 2.25%. “With recent data pointing to weaker economic activity and uncertainty elevated, risks to growth look tilted to the downside. At the same time, inflation risks have gone up due to higher energy prices.” Sounds like the same conundrum that all central banks now have. Governor Macklem in his presser said that the higher level of economic slack gives them time to access the CPI risk from higher energy prices.

And this was the most important point I believe he made, monetary policy “can’t fix the war” though also said “Governing council will look through the war’s immediate impact of inflation but if energy prices stay high, we will not led their effects broaden and become persistent.”

The Riksbank also held steady with its rate at 1.75% as did the Taiwanese central bank at 2%.

Here are some earnings comments of importance.

From Five Below, the discount retailer that is jumping this morning pre market after widely beating estimates:

Comps jumped by 15.4% in Q4 y/o/y and “this growth was both broad and balanced as we further strengthened our position as a portfolio driven product business.” They saw 8% in comparable ticket and a 7% rise in transactions.

“We saw strength across all our merchandising worlds and we grew in all 170 districts, all vintages of stores and across all income cohorts.”

They still though want to be prudent with their planning. On the macro environment, “we just don’t think it gets easier from here, whether it’s the prices at the pump or this sticky inflation that seems to be hanging around or a job market that is somewhat sluggish. We think the environment here is going to continue to be challenging.”

Williams Sonoma rose 1% yesterday in a tough tape after earnings. Comps rose 3.2% in Q4 and “we delivered these results despite no material changes in the macroenvironment and continued unpredictability around geopolitics and tariffs.”

With Pottery Barn, “While furniture was better, it was not enough to offset the softness in non-furniture.” West Elm had a good 4.8% comp gain. “I’m proud to say that West Elm is officially on a roll.”

For the Williams Sonoma brand, comps jumped 7.2% in Q4 as “customers came to us for holiday gifting, cooking, and entertaining.”

Their overall guidance does not assume any meaningful pick up in housing turnover from its current “anemic” level as they referred to it.

Macy’s jumped by 4.5% yesterday and they said this:

“Customers responded favorably to our merchandising, marketing, and promotional events supported by an improved omnichannel shopping experience.”

“Thus far, our customers have remained resilient...Our customers across nameplates skew more towards the middle to upper income tiers. Performance remains stronger in these cohorts, while the lower tiers remain more choiceful. As we look ahead, there are many macroeconomic and geopolitical factors that could influence discretionary spend. While we remain confident in our strategy and believe we are well positioned to build on our momentum, we are taking a prudent approach to guidance.”

General Mills had a tough quarter hit by winter storms, a “stressed” consumer and “With the backdrop of this heightened volatility, we saw short term changes in customer order patterns that resulted in a reduction in retailer inventory in the quarter. And storm disruptions in our supply chain network drove lower service and higher costs in Q3.”

One data point overseas of note was in the UK where payroll growth in February was better than expected, rising by 20k vs the estimate of a loss of 10k. Jobless claims though did rise by almost 25k. Wage growth in the three months ended January though was up less than forecasted while the unemployment rate held at 5.2%.

I recently started to buy (NKE) (I paid $52.96 this morning):

UBS analyst Jay Sole lowered the firm's price target on Nike to $58 from $62 and keeps a Neutral rating on the shares. Channel checks indicate soft global sales momentum through March, leading to expectations for roughly in-line Q3 EPS and a below-consensus implied Q4 EPS outlook of 3c-18c versus the Street at 23c, with Q4 sales likely down low-single digits ex-FX and no initial FY27 guidance, the analyst tells investors in a research note.

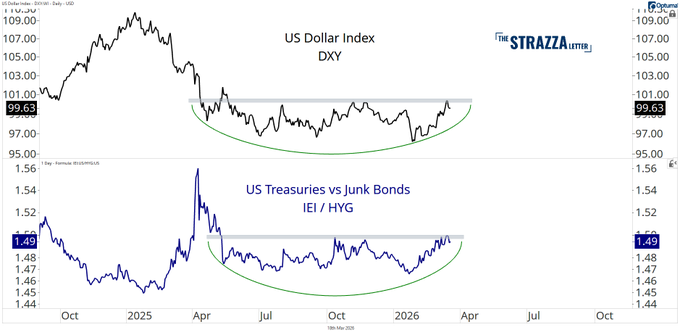

All those critical levels in play for risk assets... are likely to be violated if these bases break higher$DXY$HYGpic.twitter.com/uF7nG5qda6

— Steven Strazza (@sstrazza)

Producer Prices - How much oil data (days > $80) is in this PPI inflation data?

PPI vs Brent Move -- Zero days above $80 in this Feb PPI print—WTI cruised the entire month between $61–$67 (avg ~$64.50, peak 67.31 on the 28th, even after the Iran strikes kicked off).... pic.twitter.com/lN7kpVWonh

— Lawrence McDonald (@Convertbond)

Yesterday was day #17 of the war.

The national average of gasoline is up 86 cents (middle panel) Or 28.8% (bottom panel) pic.twitter.com/I26G2JAxHr

— Jim Bianco (@biancoresearch)

There’s a pretty good chance energy notches another higher weekly close, adding to its historic win streak. pic.twitter.com/FPv2OyB2bM

— Turning Point Market Research (@TPMRSignals)

BTC well that ended bad. The failure of a bullish pattern is extremely BEARISH. I did not get sucked in, The previous pattern resembled the current one. A break of that current uptrend would be very bearish. pic.twitter.com/GkeNaQ8vey

10 a.m.: Federal Reserve Board holds open meeting to discuss proposals to revise its capital requirements for the largest, most internationally active banks and its requirements for other large banks, as well as to make adjustments to the surcharge for U.S. global systematically important banks, Washington, DC

Treasury Auctions

11 a.m.: Treasury announces a 3 and 6 month bill auction;

11:30 a.m.; Treasury hosts a $90B 4 and an $85B 8 Week Bill Auction;

1:00 p.m.: Treasury hosts a $19B 10-Year TIPS Auction.

* Not providing two way discourse/debate (and relying on formulaic programming) has prepared investors poorly for when the halcyon days are over and the tides starts going out...

"So much for objective journalism. Don't bother to look for it here--not under any byline of mine; or anyone else I can think of. With the possible exception of things like box scores and race results, there is no such thing as objective journalism. The phrase itself is a pompous contradiction in terms.”

― Hunter S. Thompson, Fear and Loathing

My comments below should be a familiar refrain for those that follow me on Twitter and elsewhere...

Hubert Humphrey once said, "Freedom is hammered out on the anvil of discussion, dissent, and debate." The same applies to the generation and display of ideas -- in this case, market, economic and company views/outlooks. They are best presented and hammered out in disputation.

The business media, especially Fin TV, has once again failed to properly serve their most important stakeholder - their viewers and readers.

Journalists best serve their constituents by providing balanced and objective reporting. It is especially important for the media to always inject a degree of skepticism. This is even more important when the tide is coming in and the salad days of bullishness (come euphoria) are upon us. The media should do so to prepare for the inevitable downturn in fundamentals, stock prices and investors' sentiment.

It is also important for journalists to remain independent of view and to not have personal relationships (or the desire to have access) with company managements to influence their views. (Salesforce (CRM) , ServiceNow (NOW) and Nvidia (NVDA) come to mind!)

The business media has not provided this service. Instead, formulaic programming offers up the same (day after day) uber confident and non objective "talking heads" and their ever superficial "analysis" that is miles long but only inches deep (by practitioners who would never even qualify for interviews as analysts in any serious hedge fund and who never met a market they did not like) -- and, too often, are not supported by rigorous analysis or investment process.

"Praise by individual, criticize by category."

- Warren Buffett

My comments are not intended to be ad hominem, they are (like Meet The Press' Tim Russert was) fact based - taken from archived videos and interviews.

Without time stamps, guests and panelists in the business media are not held accountable. (Worse yet, they are too often filled with hubris). Case in point, a panelist on CNBC's Halftime, who, in the last three years, has endorsed only three specific stocks as his foundational, "forever" and largest holdings - Alibaba (BABA) , Moderna (MRNA) and UnitedHealth (UNH) :

* BABA missed last night and the shares are -$7 overnight - the shares have receded from $192 to $128 (he has recommended all the way down - as recently as two weeks ago Trade Tracker: Steve Weiss buys more Alibaba )

* MRNA dropped precipitously from $500 to a low of $22 (now $52)

* UNH declined from $595 to $282

(I should note that in the case of Alibaba, the panelist berated the other panelists who purchased BABA due to the ownership structure in which you are not a shareholder but own an interest in an offshore vehicle! Then he bought near the top of the chart.)

Contrary views (read: bearish) are underemphasized or not delivered at all in a backdrop of giddiness and FOMO ("fear of missing out").

Discipline and assessment of downside risk relative to upside reward are nearly always abandoned as an extreme level of complacency is urged at just the time markets mature and overvalued equity prices peak (in a valuation promise of a new never ending bullish cycle and paradigm).

Geopolitical risks, extreme valuations and private equity/credit concerns - were risks that some of us ursine types have been warning about for twelve months. Yet these factors were given little discussion or weight in the media. It is only "after the horse left the barn" (when the problems have surfaced), that a proper discussion is permitted.

Memo to the business media:

There are some situations one simply cannot be neutral about, because when you are neutral you are an accomplice. Objectivity doesn't mean treating all sides equally. It means giving each side a hearing.

The Strait initially closed because of missiles — it remains closed because of paperwork:

Seven insurance companies filed paperwork. The Strait of Hormuz closed.

Not because Iran mined the channel. Not because the US Navy blockaded the waterway. Not because any sovereign authority declared it shut. Between March 1 and March 2, seven of the twelve clubs belonging to… pic.twitter.com/1aQ95Vtwiw

JUST IN: Kuwait’s Mina Al-Ahmadi refinery is on fire. Iranian drone strike. Operations suspended. Roughly 346,000 barrels per day of refining capacity offline. Kuwait Petroleum Corporation confirmed it.

🚨🚨🚨 ISRAEL JUST MADE THE SINGLE MOST DANGEROUS MILITARY DECISION OF THE ENTIRE WAR. AND NOBODY UNDERSTANDS WHAT THEY JUST TRIGGERED. 🚨🚨🚨

Israel and the U.S. struck South Pars — the LARGEST gas field on the planet. But here's what they either didn't know or didn't care… pic.twitter.com/Zvxda0eY19

— LimitLess (@NoAlphaLimits)

BREAKING: Iran just struck Ras Laffan. The world’s largest LNG export facility. Qatar’s crown jewel. The facility that funds the country’s sovereignty, its World Cup stadiums, its airline, and its entire economic model.

JUST IN: President Trump just published the most extraordinary statement of the entire war. It was not a press conference. It was not a briefing. It was a Truth Social post. And it contained more strategic architecture than every NSC meeting of the past nineteen days combined.… https://t.co/1XyR6Hytebpic.twitter.com/GLAI5P9dJ8

BREAKING: MUST WATCH FOR EVERYONE WHO OWNS STOCKS.

Legendary Investor Howard Marks appearing yesterday on Bloomberg discussed Retail being pushed to invest in Private Credit, Stock Market Cycles and "Cockroaches in the Coal Mine".

"It's only during tough economic times that weShow more

US$18–$20 eighths as the endpoint is WILDLY optimistic.

In Canada, eg, $CBWTF sells 28g ~C$65 gross - C$28 excise= ~C$37 net (US$27!!!)— w/highest gross margins in the 🇨🇦.

Pricing won’t stop at (C$7/g) ha ha!

Put that in your pipe and smoke it $MSOS

🚨🚨🚨BREAKING: NEW CANNABIS UPLISTING BILL, HR 7987, HAS BEEN FILED!

The bill intends to amend the Securities Exchange Act of 1934 and allow the listing of securities for cannabis-related legitimate businesses

$MSOS

JUST IN: Kuwait’s Mina Al-Ahmadi refinery is on fire. Iranian drone strike. Operations suspended. Roughly 346,000 barrels per day of refining capacity offline. Kuwait Petroleum Corporation confirmed it.

Count the Gulf states now.

UAE: zero gas production at Shah and HabshanShow more

BREAKING: Qatar’s Prime Minister stood at a podium today and delivered one sentence that will fracture Gulf alliance architecture for a generation: “Everyone knows who the main beneficiary of this war is.”

He did not name the country. He did not need to. The Arab diplomaticShow more

Seven insurance companies filed paperwork. The Strait of Hormuz closed.

Not because Iran mined the channel. Not because the US Navy blockaded the waterway. Not because any sovereign authority declared it shut. Between March 1 and March 2, seven of the twelve clubs belonging toShow more

BTC well that ended bad. The failure of a bullish pattern is extremely BEARISH. I did not get sucked in, The previous pattern resembled the current one. A break of that current uptrend would be very bearish.

Shanaka Anslem Perera ⚡

@shanaka86

BREAKING: The world thought Hormuz was an oil story. Then it became an LNG story. If the damage assessment holds, it becomes a civilisation-input story that lasts half a decade.

There is a difference between a shipping shock and a capacity shock that the market has not yet

Georgia at the finish line to officially go medical

Virginia IS going AU

Texas banning hemp and expanding TCUP

PA has movement but I won't hold my breath

Bondi on the clock

Up listing bill intro'ed

MSO's survived the "deadly debt cliff"

$MSOS has tailwinds

Producer Prices - How much oil data (days > $80) is in this PPI inflation data?

PPI vs Brent Move -- Zero days above $80 in this Feb PPI print—WTI cruised the entire month between $61–$67 (avg ~$64.50, peak 67.31 on the 28th, even after the Iran strikes kicked off)....

The Dank Informer

@TheDankInformer

🚨🚨🚨BREAKING: NEW CANNABIS UPLISTING BILL, HR 7987, HAS BEEN FILED!

The bill intends to amend the Securities Exchange Act of 1934 and allow the listing of securities for cannabis-related legitimate businesses

$MSOS

Here's your intermarket cheat sheet

All those critical levels in play for risk assets... are likely to be violated if these bases break higher

$DXY$HYG

BREAKING: Iran just struck Ras Laffan. The world’s largest LNG export facility. Qatar’s crown jewel. The facility that funds the country’s sovereignty, its World Cup stadiums, its airline, and its entire economic model.

Explosions. Fires. Partial production halt at a facilityShow more

JUST IN: President Trump just published the most extraordinary statement of the entire war. It was not a press conference. It was not a briefing. It was a Truth Social post. And it contained more strategic architecture than every NSC meeting of the past nineteen days combined.Show more

Abu Dhabi intercepted the missiles. The debris shut down the gas fields anyway.

Habshan gas processing facilities and the Bab field were both taken offline today as a precautionary measure after falling debris from successful missile interceptions struck the sites. Abu Dhabi