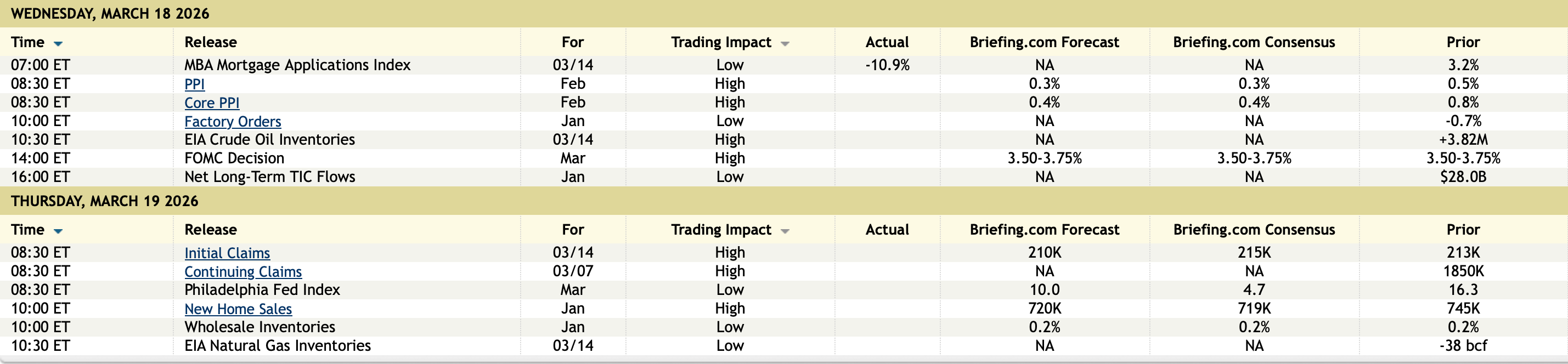

That was a yawner of an FOMC statement, on purpose

In light of everything going on in the Middle East and the global ripple effects, the FOMC could not have crafted a more non-event statement that was essentially little changed with the January meeting while adding this line, “The implications of developments in the Middle East for the US economy are uncertain.”

Again, Stephen Miran dissented in favor of a 25 bps rate cut as he sees little inflation pressures (?) and is more worried about the labor market (I get it), according to his recent speeches/media appearances.

With respect to the economic projections, GDP and unemployment were about unchanged with the December forecast while they raised their PCE inflation estimates to 2.7% headline from 2.4% previously and the core to 2.7% from 2.5%. I won’t bother with the 2027 guesses because that crystal ball is broken, always has been and always will be.

On the projected policy path, the median still expects one cut this year which is exactly what the fed funds futures have priced in, no more. Two people want two cuts this year, two want three and Stephen Miran (I’m guessing) wants four. Seven want one cut and seven want no cut.

Bottom line, yawn on the statement and the dots. The presser is where the action, if any, will come and where I don’t expect much. I’m expecting a lot of “we’ll have to see” from Jay Powell as he approaches his last meeting and sets up his tee times for June.

Silos of confirmation bias with massive amounts of adverts thrown in for your viewing enjoyment or displeasure. Doug K thanks for your rigor and ongoing skeptical look at dispensers of financial info. Blessings.

Dougie Kass

++++

Speaking of economy - its a poor dispersion of spending with lower/middle class weakening in the K shaped economy.

Thanks god for AI cap ex and high end spending.

As Rosie has frequently noted, looking under the hood without AI and high end spending -- economy would be foundering will nearly zero real growth.

The non AI economy, lower and middle class getting screwed by the persistent 2.75%- 3% inflation rate (well above Fed target of 2%), absence of job growth. In fact there wasnt a month that was close to target.

A near 3% inflation rate means it is pesky.

Limited econ growth (away from AI and high end spend) means sluggish econ growth.

Pesky inflation and sluggish economic growth (its a good idea to take out AI because current rate is not sustainable) = slugflation. Been with us for two years now.

Meanwhile, from "Growing Less Bearish" column on Monday:

* Slowing Economic Growth: According to the Commerce Department (on Friday) 4QGDP growth was only +0.7% — revised from the previous estimate of +1.4% and well below the consensus of +1.5%. Moderating domestic economic activity will feed into and weaken consensus S&P 2026-27 EPS expectations which remain too high.

Dougie I have some thoughts around the comment of the day. I totally understand your issues with mainstream financial media like CNBC. They represent themselves as a place to gain information that will help investors. This of course, is not the actual case, for the many examples you have highlighted over the years.

I think it upsets you because you envision investors that want to improve their process tuning in for those reasons. Then, ultimately being pushed in the opposite direction of no thought or process. I will argue that is not why people tune in. I believe they tune in to be comforted for being long the same boat everyone else is. They cheer it together on the way up and comfort each other on the way down. It’s the same as other specialty media like CNN and Fox News. People don’t watch that garbage to be better informed. The woke watch CNN to be told they are 100% right about everything. The MAGA watch Fox News to be told they are 100% right about everything.

IMHO there are two huge obstacles to a world where mainstream financial media is valuable. The first is what I outlined in the previous paragraph. The viewers don’t want to do all the work you talk about. They actually want a quick answer as to how they can avoid FOMO. If it required more detailed thought, analysis and most importantly work. Then they wouldn’t tune in and the station would go out of business. The second issue is you can’t find/afford anchors capable or willing to take that job over the alternatives. If CNBC offered you ANY anchor role there you wanted. Would you close up Sea Breeze Capital and go to work at CNBC? Gemini says the highest paid anchor on CNBC is Becky Quick at $3m. so let’s assume that’s they pay they are offering you as well. Not chump change but I’m guessing less then you make now to do something you would enjoy much less.

The last thing I will say is for the people out there that truly want to be better investors and are willing to put in the work to get there. There are endless places for them to go in the modern word to get the information. Your and other daily blogs on The Street.com, excellent twitter follows, endless books (market wizard series being my personal favorites). I hope this perspective helps you tolerate the CNBC, CNN, Fox News and others who perpetuate stupidity.

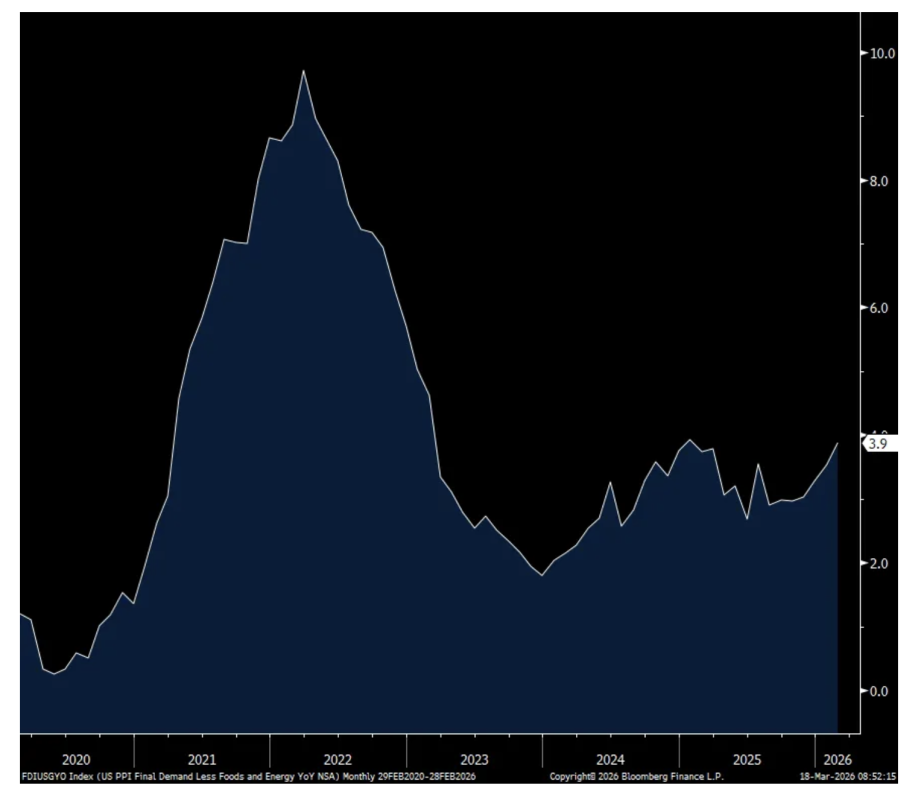

Price pressures continue to grow, even before this recent jump in commodity prices

Even before the spike in oil prices and other commodities, headline February PPI jumped by .7% m/o/m after rising by .5% in January. That was .4% above the estimate and the core rate was higher by .5% after an .8% gain and that was .2% more than anticipated. The y/o/y gain went from 2.9% to 3.4% and the core rate is now up by 3.9% y/o/y vs 3.5% in January.

After rising by .7% in January, core goods prices were up by .3% and now by 4.3% y/o/y. Food prices were up a large 2.4% in the month but after falling by 1.4% in the month before and little changed y/o/y. There was a 49% spike in prices for fresh and dry vegetables. Energy prices, old news of course, got back what it lost in January and down .7% y/o/y.

Services inflation was up .6% in December, .8% in January and another .5% in February. Versus last year, prices are up 3.8%. The BLS said “About 20% of the February advance in the index for final demand services is attributable to a 5.7% jump in prices for traveler accommodation services.” Elsewhere, prices rose of note in food/alcohol wholesaling, securities brokerage/dealing/investment advice, fuels/lubricants retailing, trucking, and inpatient care. They fell for apparel/footwear/accessories retailing and airline passenger services.

Specifically on trucking, where I keep mentioning the firming up in spot prices, ‘truck transportation of freight’ prices rose 1.2% in February after being up 1% in January.

Bottom line, we can’t just look at CPI in telling us what we think the Fed should do because wholesale inflation is a problem and just because some of it doesn’t pass through to the consumer doesn’t mean it disappeared. Also, I’ve heard from one Fed Governor over the past few months who thinks the only area of inflation we’re experiencing is from ‘portfolio management fees’. I encourage that person to look again with a broader lens.

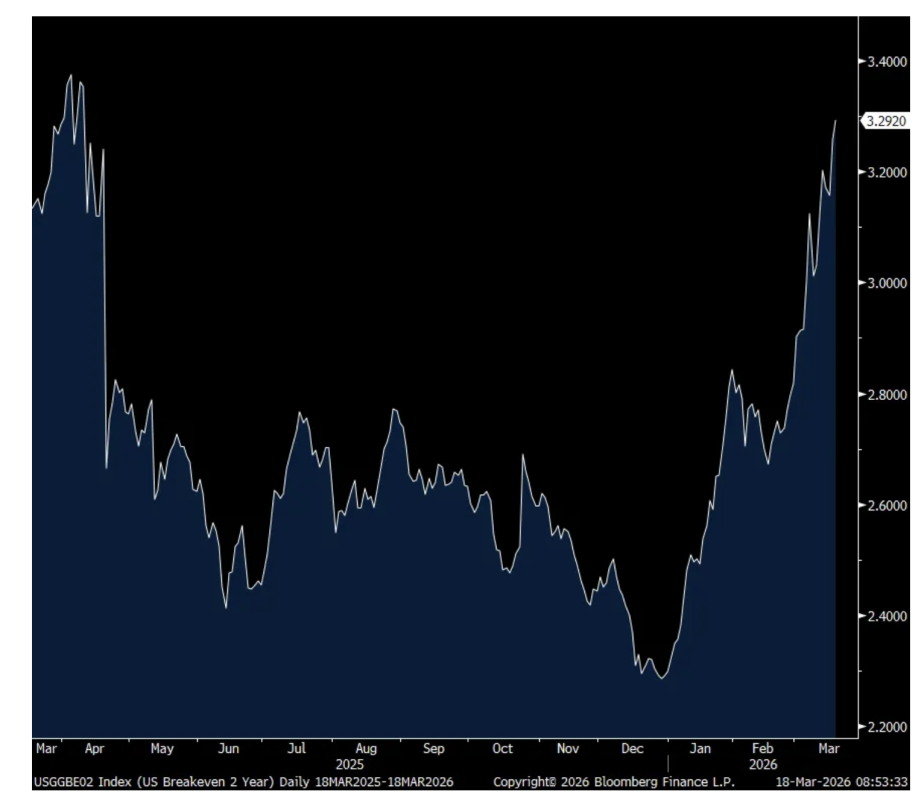

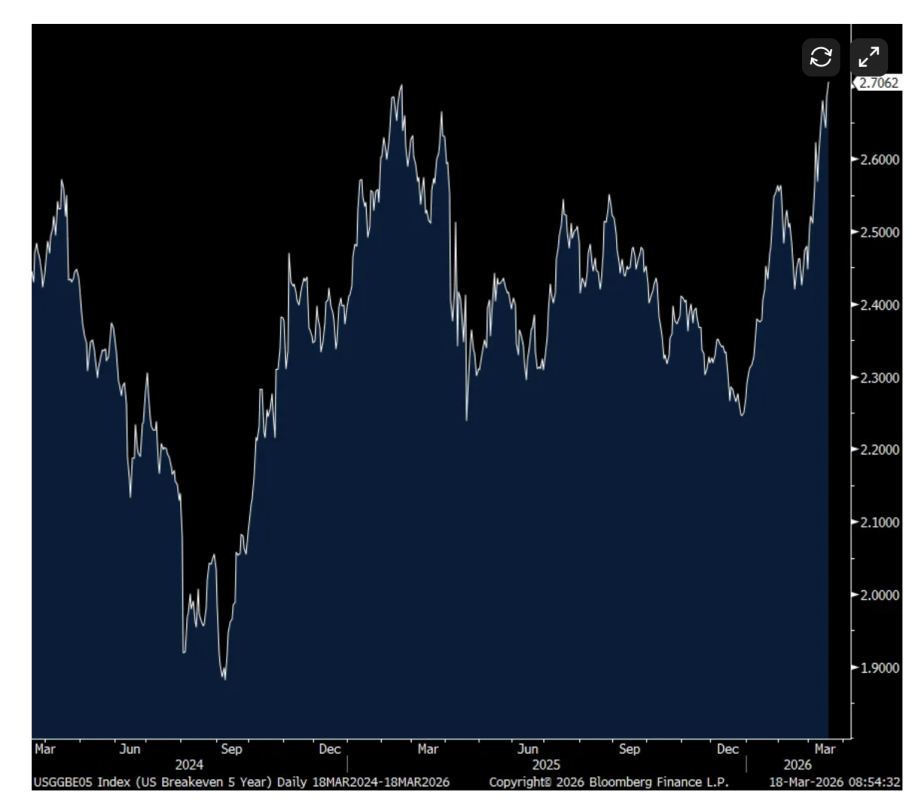

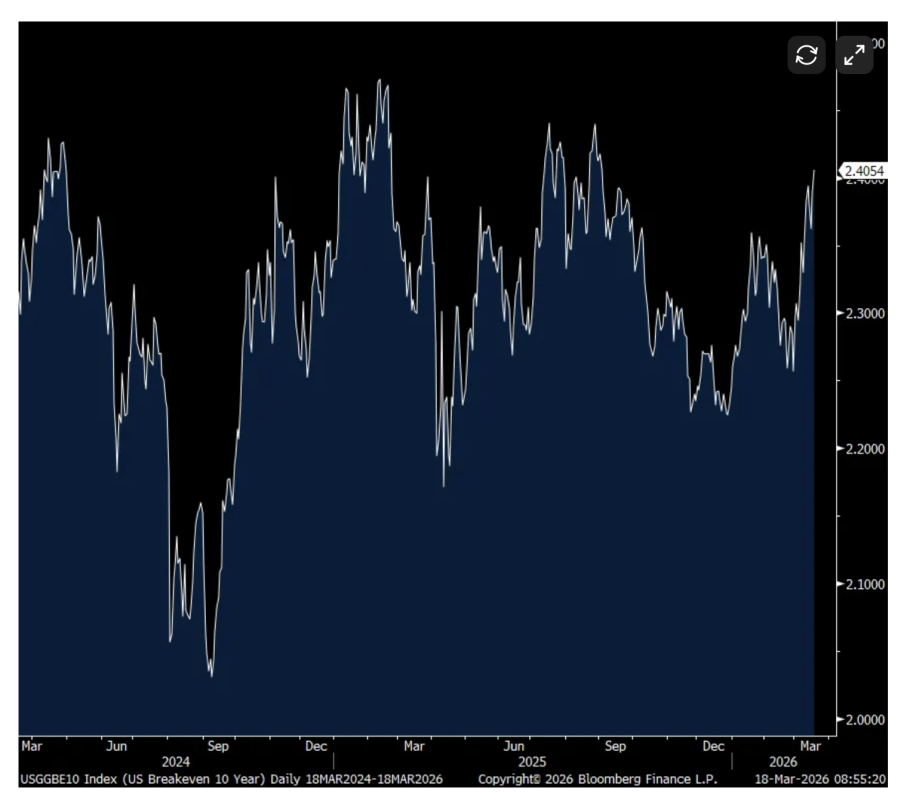

Inflation breakevens are rising in response, particularly the 2 yr which is up by another 3.5 bps to 3.29%, approaching the tariff Liberation Day highs last April. The 5 yr breakeven is now right at the April highs at 2.70%, up 2 bps today. The 10 yr is at a more modest 2.41%, but up from 2.26% right before the war started.

But remember - Slink, Farmer Jim, Belski, Weiss, The Floor Trader, et al told you the credit spreads were at record lows and the yield curve was steepening. They opined that these conditions would provide a very positive backdrop for equities.

They either lied to their viewers, have no investment process or did no modelling/forecasting.

And they did this with expression of total confidence.

They are fugazzis - nonsensical perma bulls who make up narrative without doing analysis.

So,what was their process? They gazed at the charts and the rear view mirror (where investment vision is always 20/20).

This is why I warned so frequently here and on Twitter.

I tried to protect the innocent when the tide was coming in so they could prepare for the tide going out.

* So far, so good - as the markets have rallied briskly this week...

In my Monday column,Growing Less Bearish, I suggested that bearish investor sentiment (and deep oversold on the S&P Short Range Oscillator and McLellan Indicator), defensive positioning, the preponderance of so many stocks suffering 25% or more declines, etc. could contribute to a better market tone in the near term.

We thought that buying at the sound of cannons made some sense and we moved to a net long exposure - adding about 10 long positions (mostly depressed financials) to our portfolio. (See recent "Things" columns).

This view has paid off thus far.

Since then (and including the +30 handle rise in S&P futures this morning), the S&P has risen by about +110 points, or close to 2%.

On yesterday's upside gaps, I reduced my financial exposure (taking many long positions from medium-sized to small-sized). The upside move in private equity stocks was particularly conspicuous, with gains of +3% to +5%.

I suspect there could be some more upside ahead - consistent with Monday's column - but the harder we rise, the harder we will likely fall (at some point in time).

Specific headwinds that could curtail the upside might include the company buyback blackout window (which is now closing) and systematic (quant) selling which is likely to take place later during the current month.

As well, a large stock expiration looms on Friday (so look for renewed volatility):

"Friday also marks the March monthly options expiration, which is historically one of the largest of the year. From a market structure perspective, expirations can be significant events as stale contracts expire and fresh positioning is rolled into the next month… pic.twitter.com/nYFhabC1xn

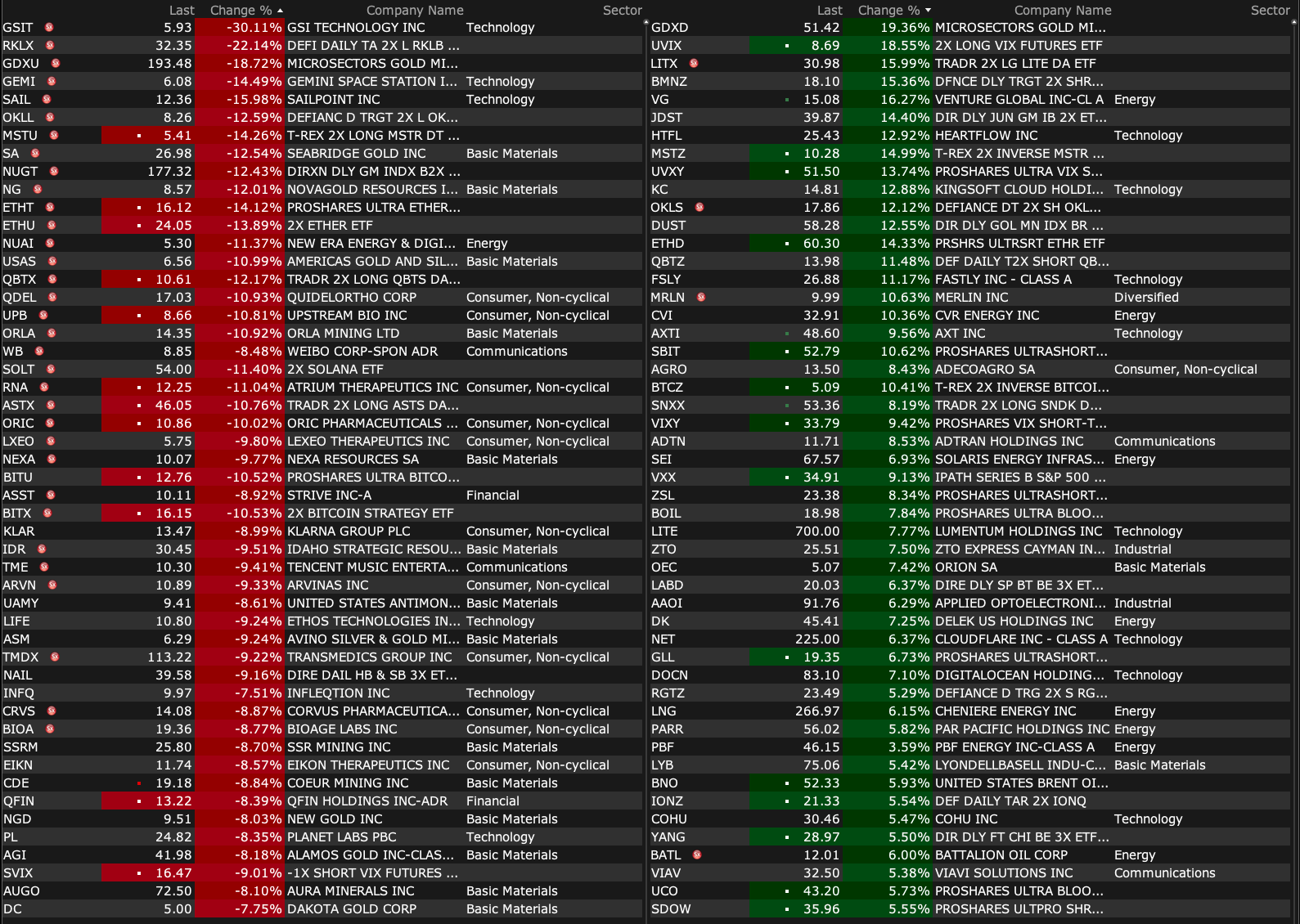

-ARTL +36% (announces Third-Party Fully Funded Clinical Study Agreement to Evaluate ART27.13 in Glaucoma Patients) -SWMR +24% (momentum following IPO) -PERF +23% (receives going-private proposal at $1.95/shr) -OVID +19% (OV329 (7 mg dose) demonstrated favorable safety and tolerability profile, reinforcing best-in-category potential for refractory epilepsies, supporting Indication Expansion; reports earnings and prices 29.9M common share offering at $2.01/unit in Private Placement) -HIT +18% (Health In Tech and Amazon Web Service Advanced Tier Service Partner Ciklum Announce Strategic Collaboration to Accelerate Development of AI-Driven InsurTech Platform) -PDYN +13% (subsidiary selected by U.S Navy to develop low cost near hypersonic missile) -M +7.8% (earnings, guidance) -PTGX +3.9% (receives U.S. FDA approval of ICOTYDE (icotrokinra) for the treatment of moderate to severe plaque psoriasis) -SPIR +2.9% (earnings, guidance) -SLG +2.5% (Deutsche Bank Raised SLG to Buy from Hold, price target: $44) -KNX +2.3% (UBS Raised KNX to Buy from Neutral, price target: $66 from $54) -GRAL +2.1% (TD Cowen Raised GRAL to Buy from Hold, price target: $65 from $114)

Downside:

-SAIL -14% (earnings, guidance) -IAUX -11% (files to sell $200M convertible senior note offering) -TTD -4.9% (Rosenblatt Securities Inc. Cuts TTD to Neutral from Buy, price target: $25) -DUOL -2.7% (Argus Cuts DUOL to Hold from Buy) -LULU -2.1% (earnings, guidance) -GIS -2.0% (earnings, guidance)

Boockvar on Why Oil Is in Charge of Fed, AI Trade Shakeup

From Peter Boockvar:

Meet the new Chairman of the Federal Reserve, and it's not Kevin Warsh

The price of oil is the new Chairman of the Fed and dictating interest rates and the actual Fed is just going to have to sit back and watch for now. The fed funds futures has just one cut priced in this year and not fully until December.

Meanwhile, I saw this press release from BASF today, the large German chemical company, that said “BASF is increasing prices on all products in its Home Care, Industrial & Institutional Cleaning (I&I) and Industrial Formulators portfolio in Europe by up to 30%, or more for selected products, effective immediately or as existing contracts allow.”

“The move primarily comes in response to significant volatility in the pricing and availability of key raw materials, increasing domestic and transcontinental logistics costs, and soaring packaging and energy costs.”

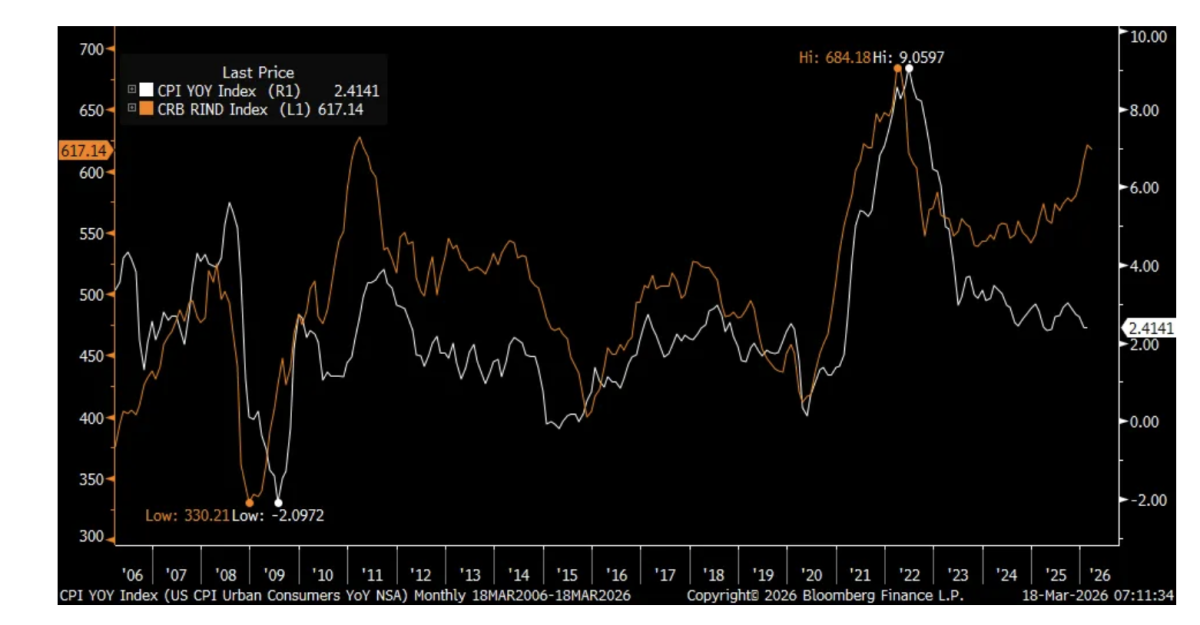

I will include here a chart going back 20 years, something I posted a few months ago, that shows the CRB Raw Industrials Index with the US CPI y/o/y change.

CRB Raw Industrials index in orange/US CPI in white

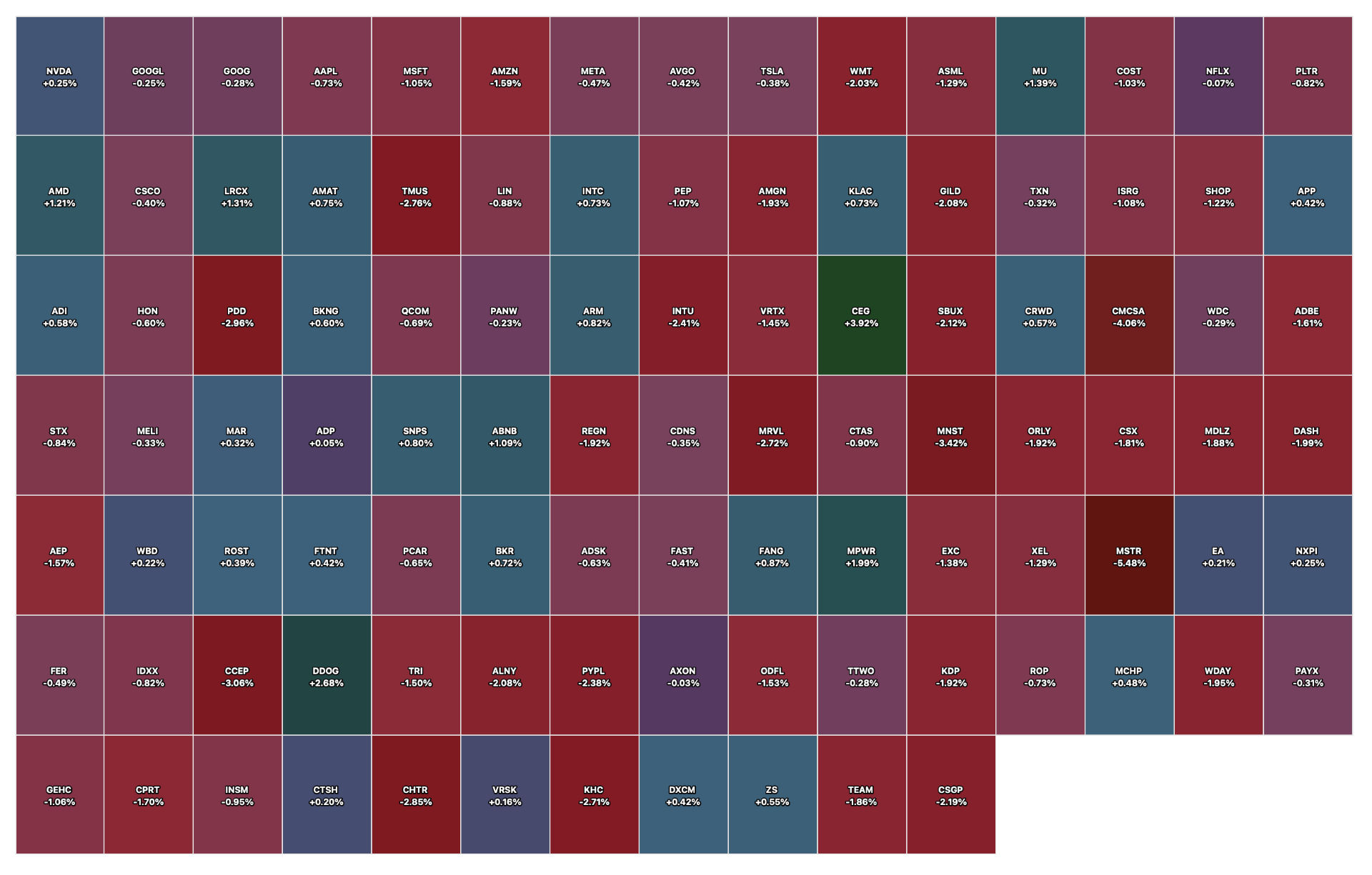

After seeing the stock of Nvidia that is no higher than last August in the face of so much good news whether earnings wise or product, I’m going to argue again that the GenAI tech trade is losing its leadership position and market dominance. My belief is mostly with the large hyperscalers and is all because of their shrinking cash flows as they spend massively to create this incredible ecosystem that will very much benefit the rest of us. Free cash flow shrinks, multiples re-rate, though Microsoft is still producing strong free cash as seen below but its stock multiple has compressed anyway.

I will highlight here what has happened to hyperscaler free cash flows, using data from my Bloomberg terminal:

Oracle in fiscal 5/24 generated $11.8b in free cash vs an expected burn of $23.6b in their fiscal yr ending 5/26.

Amazon in fiscal 12/24 generated $32.9b in free cash vs an expected burn of $6.2b in their fiscal yr ending 12/26.

Google/Alphabet in fiscal 12/24 generated $72.7b in free cash and that is expected to shrink to $23.8b in fiscal 12/26.

Meta in fiscal 12/24 generated $54b in free cash and that is expected to be ‘just’ $7.7b in fiscal 12/26.

Microsoft is still expected to generate strong free cash flow of $70b in fiscal 6/26, similar to its pre AI spend ramp.

These stocks can still do fine in the coming years as this is not a bear call. I’m just believing that the rate of return for them in the coming 3-5 years is going to lag other parts of the market, both domestic and international, after an incredible 15 year period of outperformance, especially since late 2022.

To some earnings calls and comments too from some Wall St conference presentations of note:

From Bob’s Discount Furniture who reported earnings for the first time last night as a public company:

“In 2025, we saw meaningful increase in new customers earnings over $150,000, underscoring the broad appeal of our value proposition. We also see a strong balance across age cohorts, which makes sense given that consumers often purchase furniture at major life milestones, whether setting up their first home, growing a family, or entering retirement and downsizing.”

“we had a strong start to the year, with comparable sales growth in the first few weeks of the quarter running modestly ahead of our low single digit algorithm. However, that was followed by significant snowfall and prolonged cold weather that materially impacted store traffic and sales across most of our footprint. We are no strangers to winter weather, yet this year was exceptional, as winter storm Fern and the February blizzard struck on weekends, which typically generate more than double our weekday sales, resulting in 5x more operational hour losses than last year.”

“Encouragingly, as we’ve moved into March, traffic has rebounded, and our recent sales trends have benefited from a partial recapture of lost sales from the weather impacted weeks.”

From Lululemon that beat street estimates for both top and bottom lines but guided light:

North American comps fell 2% while jumping by 26% in China.

In North America specifically, “We are already seeing green shoots related to our new product launches and our recent brand activation’s. But I want to also acknowledge that an improvement in overall trends in North America will likely progress over the course of the year and into 2027, as we return to a healthier baseline of full price sales.”

“Tariffs had a gross negative impact of 520 bps in the quarter, offset by 110 bps related to our enterprise efficiency initiatives, while markdowns increased by 130 bps.” Dollar wise it cost them $380 million with offsets of about $160 million.

This was what JB Hunt, the trucking company, said of note at the JP Morgan industrials conference yesterday:

“I think it was about three months ago, I forgot who it was, but the company described the market as being fragile. And I think there were some chuckles and laps at the use of that word. But in hindsight, we were seeing it, right? We felt that if there was any hiccup in one direction or the other, whether it be storm driven, whether it be demand driven, whether supply continues to sort of come out of the market”

“It just didn’t feel like there was a lot of elasticity, and we’ve had a couple of bumps or elements that have disrupted supply or disrupted the supply chain...Obviously the market is tracking what’s happening with spot rates (they are going higher), and that’s a real time indicator of the relationship between supply and demand. So I will go back and reiterate that we continue to believe that the market is in a fragile state.”

Fuel surcharges are here, more so with trucks than intermodal that also uses rail. And with what is going on with rising fuel prices from the perspective of their customers, “it’s not yet driving strategy discussions. I think that the overarching theory is that nobody knows how long this will last. And so, there’s a lot of caution on that.”

From Alcoa, at the same conference:

“If you look at our aluminum order book before the conflict, we were characterizing the demand as very stable. With the markets that were strong in ‘25 continuing into ‘26. So primarily packaging, electrical construction, non-residential also strong when you look at the build out for data centers as well as renewable energy infrastructure. All of that has continued.”

“We’re actually seeing an uptick in orders from customers and inquiries related to second quarter and the second half of the year because these were customers that are taking a portion or a majority of supply from Middle East smelters, and they’re now worried about getting supply for the second half. So we do have additional spot orders coming in, and that should help us later in the year.”

Here is what MMM, the maker of so many product lines, said on the things going on, also at the JP Morgan conference:

“As we go into ‘26, we see a lot of the same trends that we saw through last year continue on into this year...With this added volatility with what’s going on in the Middle East with the elevated price of oil, we certainly are impacted like everybody else around the world. We don’t have a very large business in the Middle East. It’s kind of like less than 2% of our revenue. We do see shipments and transshipments through a couple of important logistics hubs in the Middle East. So airfreight logistics will be a little bit, have some friction to it.”

“We’re watching very carefully, with the price of oil being elevated, we certainly use oil based polymers in our products. We’ll see how that affects over time. If the price of oil stays elevated, we’re going to take action like we had to do last year and be responsive on pricing, like we were with tariffs, we’re going to do the same thing with oil this year. But it’s something that we watch very, very carefully and we’ll be responsive on. So again, economic conditions continue almost like they were last year coming into this year.” I bolded to highlight.

From my friend and "fellow stooge," Peter Boockvar:

The large chemicals company, BASF provides a clear vision of "slugflation" that lies ahead:

“BASF is increasing prices on all products in its Home Care, Industrial & Institutional Cleaning (I&I) and Industrial Formulators portfolio in Europe by up to 30%, or more for selected products, effective immediately or as existing contracts allow... The move primarily comes in response to significant volatility in the pricing and availability of key raw materials, increasing domestic and transcontinental logistics costs, and soaring packaging and energy costs.”

Right now, in barns and equipment sheds across the American Midwest, farmers are making the most consequential decision of this war. Not generals. Not senators. Farmers.

At $683 per ton urea, corn economics have collapsed. Nitrogen is the single largest input cost for corn… pic.twitter.com/KVhRNEgAaF

An Important Cannabis Podcast Took Place Yesterday Afternoon

* Run, don't walk to listen at the 56-minute mark of the The Dales Report interview...

Yesterday The Dales Report's Anthony Varrell interviewed Curaleaf's (CURLF) Chairman, Boris Jordan.

Here are some excerpted quotes from the chairman of the largest multi state cannabis operator:

At the end of today's podcast 56 minutes he (the chairman of the largest multi state cannabis operator) flat out said that the company is very close to Washington DC regulatory operatives and legislators and virtually guaranteed rescheduling will happen soon. He said, "its not a question of if, but when and I am now happy to say that," "the government is diligent in the process and it can't be reversed, " " obviously we are privy to more information than I can tell you all about" and "there is urgency on the matter from DOJ, White House to Congress to get rescheduling across the wire."

Moreover (to make things even more attractive), at 59 minutes 0 seconds he says, when rescheduling is announced it will be transformational, hastening major industry mergers and consolidations in the space as the cost saves are so great. "It will not only happen with tuck ins, it will happen at the largest level." "There is no need to have five mutli state operators in the same market". (He calculates a merger of two of the largest MSOS would create an astounding $200 million of cost saves in the first twelve months!)

Over the past 20 years, every time credit spreads made 9-month highs while the S&P remained within 5% of its high, a bear market followed.@jasongoepfertpic.twitter.com/HoNlp3tDXV

Does a spike in bond default protection signal equity market headwinds?

• CDS Signal: Bond default insurance prices jump to a 9-month high (100% of its 189-day range) • Broad Market: S&P 500 posts 46% win rate and negative median return 2 months after the signal • Sector… pic.twitter.com/AuTPx524oz

"We are expecting the next blackout window to begin this week ~3/18, estimating ~45% of the S&P 500 to be in blackout by that point, assuming entry 6 weeks prior to earnings ... We expect blackout to run through the end of April."

#Iran War Update No. 18 (focus on Iranian strategic narrative):

🔹The maritime dimension of the war is moving toward a more dangerous phase. Reports suggest Israel may join the U.S. in expanding operations around the Strait of Hormuz, while Iranian discussions increasingly point…

— Hamidreza Azizi (@HamidRezaAz)

There are two clocks running in the Hormuz crisis. One belongs to the insurance industry. The other belongs to biology. They cannot be reconciled. And that irreconcilability is the single most important fact in the global food system right now.

Over the last 75 years, the average intra-year market drop has been 14%. If you are overly stressed out about the current 5% drawdown, the stock market isn’t for you. Downside volatility is the price investors pay for long-term outperformance. pic.twitter.com/XIGzarUcya

The equity market was "resilient" at the start of the Russia-Ukraine war as well...it took five weeks of high oil prices before stocks started to capitulate to inflation pressures in 2022. pic.twitter.com/CXaKnBXbHv

The oil-price shock is taking a bigger toll on European markets, particularly in fixed income, making the ECB's meeting this week arguably more interesting than the Fed's. Yields on French 10-year bonds are back up to the highest since 2011. pic.twitter.com/q63YK1ZSRv

While credit markets are open to many companies, they're starting to close for others. Qualtrics, which makes online survey tools, had to ice a $5.3 billion loan and bond deal due to lack of investor appetite. https://t.co/DE0BfMnHYT

Over the past 20 years, every time credit spreads made 9-month highs while the S&P remained within 5% of its high, a bear market followed.

@jasongoepfert

"We are expecting the next blackout window to begin this week ~3/18, estimating ~45% of the S&P 500 to be in blackout by that point, assuming entry 6 weeks prior to earnings ... We expect blackout to run through the end of April."

-GS Morgan

Does a spike in bond default protection signal equity market headwinds?

• CDS Signal: Bond default insurance prices jump to a 9-month high (100% of its 189-day range)

• Broad Market: S&P 500 posts 46% win rate and negative median return 2 months after the signal

• SectorShow more

While credit markets are open to many companies, they're starting to close for others. Qualtrics, which makes online survey tools, had to ice a $5.3 billion loan and bond deal due to lack of investor appetite. bloomberg.com/news/articles/…

Over the last 75 years, the average intra-year market drop has been 14%. If you are overly stressed out about the current 5% drawdown, the stock market isn’t for you. Downside volatility is the price investors pay for long-term outperformance.

There are two clocks running in the Hormuz crisis. One belongs to the insurance industry. The other belongs to biology. They cannot be reconciled. And that irreconcilability is the single most important fact in the global food system right now.

The insurance clock: P&I clubsShow more

Right now, in barns and equipment sheds across the American Midwest, farmers are making the most consequential decision of this war. Not generals. Not senators. Farmers.

At $683 per ton urea, corn economics have collapsed. Nitrogen is the single largest input cost for cornShow more

#Iran War Update No. 18 (focus on Iranian strategic narrative):

🔹The maritime dimension of the war is moving toward a more dangerous phase. Reports suggest Israel may join the U.S. in expanding operations around the Strait of Hormuz, while Iranian discussions increasingly pointShow more

The oil-price shock is taking a bigger toll on European markets, particularly in fixed income, making the ECB's meeting this week arguably more interesting than the Fed's. Yields on French 10-year bonds are back up to the highest since 2011.

OpenAI is an actual cash furnace. Just setting money on fire. 🔥💵🔥

The company is expected to burn through $68M per day in 2026.

That figure rises to a staggering -$156M per day in 2027.

Then -$200M per day by 2028.

This sets up for a cash burn of $665B by 2030.

No wonder Show more

The equity market was "resilient" at the start of the Russia-Ukraine war as well...it took five weeks of high oil prices before stocks started to capitulate to inflation pressures in 2022.

The bond market is getting twitchy.

Over the past 20 years, when credit spreads blew out but the S&P 500 wasn't even beyond a pullback yet, it was 3-for-3 in bear markets.

h/t @sentimentrader

I've been slowly starting a position in $IBB toward the lower end of this range, under 170.

Biotech as a group, has been digesting last year’s run-up in a pretty healthy fashion [so far]. Chart from @IBDinvestors

OPEX

@t1alpha

"Friday also marks the March monthly options expiration, which is historically one of the largest of the year. From a market structure perspective, expirations can be significant events as stale contracts expire and fresh positioning is rolled into the next month

returns is 20-28. The quicker we leave it, the better.

I swear it feels like we live in a simulation.

Same playbook as 2022.

Bitcoin sells off during the start of a new conflict, finds a low in February, then bounces into March.