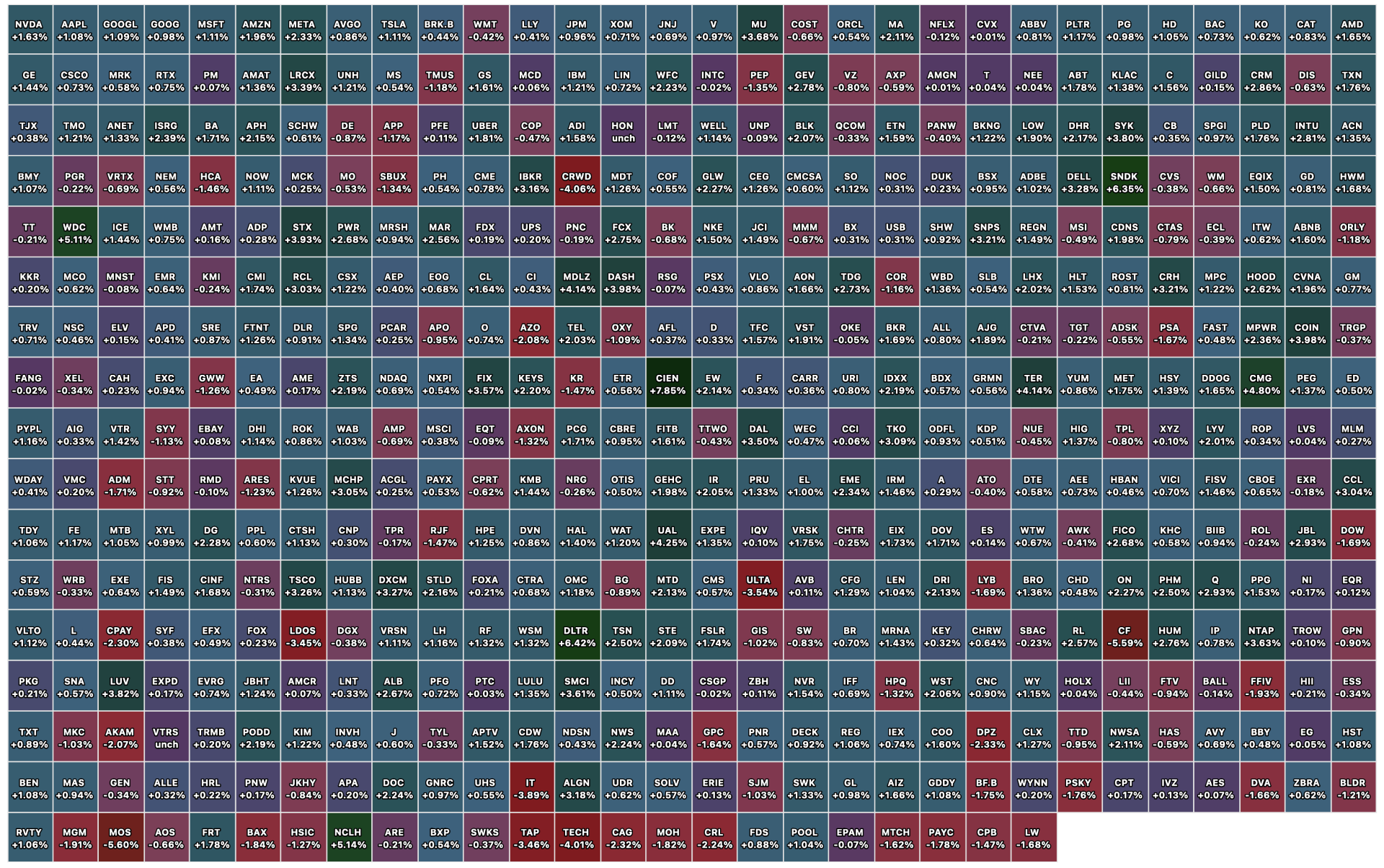

This is astounding... I can't believe that the line of sight of business is double.. I can't believe how many doubt this man. A trillion dollar book of business.. And that's blah? That's nothing? That's some yawner?

— Jim Cramer (@jimcramer)

Someone please tell Jim that Nvidia's (NVDA) Jensen Huang added a year to the projected revenues.

Using Marijuana Is More Morally Acceptable Than Gambling And Abortion, Americans Say In New Poll

"But in the U.S., where nearly all states have enacted some form of cannabis legalization for either medical or recreational purposes and where federal rescheduling may be imminent, adults involved in the survey strongly signaled that they didn’t view marijuana use as a moral shortcoming.

In fact, 76 percent of Americans said using cannabis is either morally acceptable (24 percent) or not a moral issue (52 percent), compared to 23 percent who called the activity morally unacceptable.

The act of simply buying more and higher powered chips does not cut it (which should have been obvious about two years ago).

But whatever. What is a few trillions of dollars down the tubes and a credit mess amongst friends?

Also, the fact that Meta (META) and XAi are now realizing their models are not that good, woof! Especially Meta, after Zuckerberg hands out all that money in salary on top of the capital (including the off balance sheet stuff), and it still is not good. This is a bigger fail than the Metaverse. Then if you back out the economics from their scam ads, which on an incremental basis accounts for a huge portion of their cash flow, it’s an ugly picture.

In a weird way the AI space (and the markets overall) is lucky that Iran conflict broke out.

A lot of bad news re AI and private credit has seemingly been missed:

Boockvar on the Big Data, Big Week and Big Nitrogen Hike

From Peter Boockvar:

Is it Friday yet?

With everything going on in the Middle East, busy week ahead with central bankers. The Fed, the ECB, the BoE, the SNB, the BoJ and the RBA all give us their thoughts and possible policy moves this week. The RBA is the only one expected to move on the rate side and that is up by 25 bps to 4.10%. The rest we’ll get to hear how they are viewing things. To them, is the rise in energy prices something to worry about with respect to inflation that they need to act against or something to look through on the belief it is temporary? With the Fed, they of course also have to balance the labor market side (even though the others do too implicitly) and how is Powell viewing the slowdown in hiring with respect to both the supply for workers and the demand for them? I think we’ll get a lot of ‘I don’t know’ and ‘let’s wait and see.’ Either way, the world’s major central banks are done for now in cutting rates and we’ll soon see how Kevin Warsh balances what his boss wants and what he really wants to do.

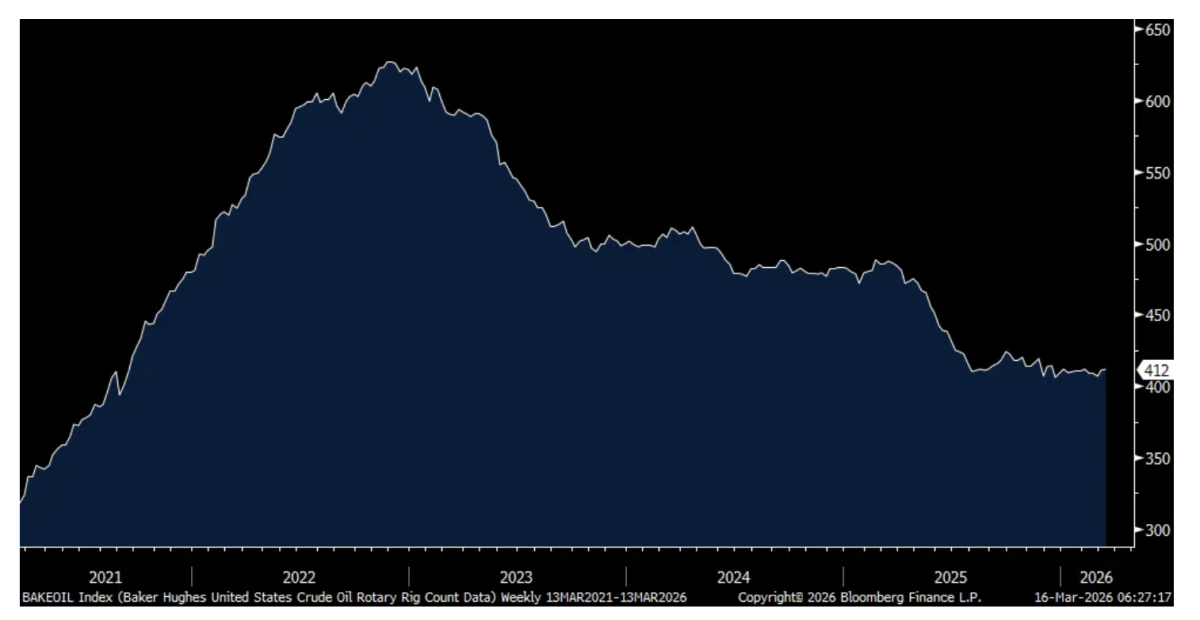

At least through the lens of the US crude oil rig count, US drillers haven’t responded much yet to the spike in prices. For the week ended Friday, the rig count went up by just one rig to 412, still bouncing along the lowest level since September 2021. With respect to natural gas, something the rest of the world really needs now and the US an export powerhouse in LNG, particularly to Asia and Europe that can’t get deliveries from the Mideast, it rose by just one rig too.

The average gallon of gasoline rose by almost another nickel over the weekend to $3.72 a gallon, up by 21% y/o/y.

Crude Oil Rig Count

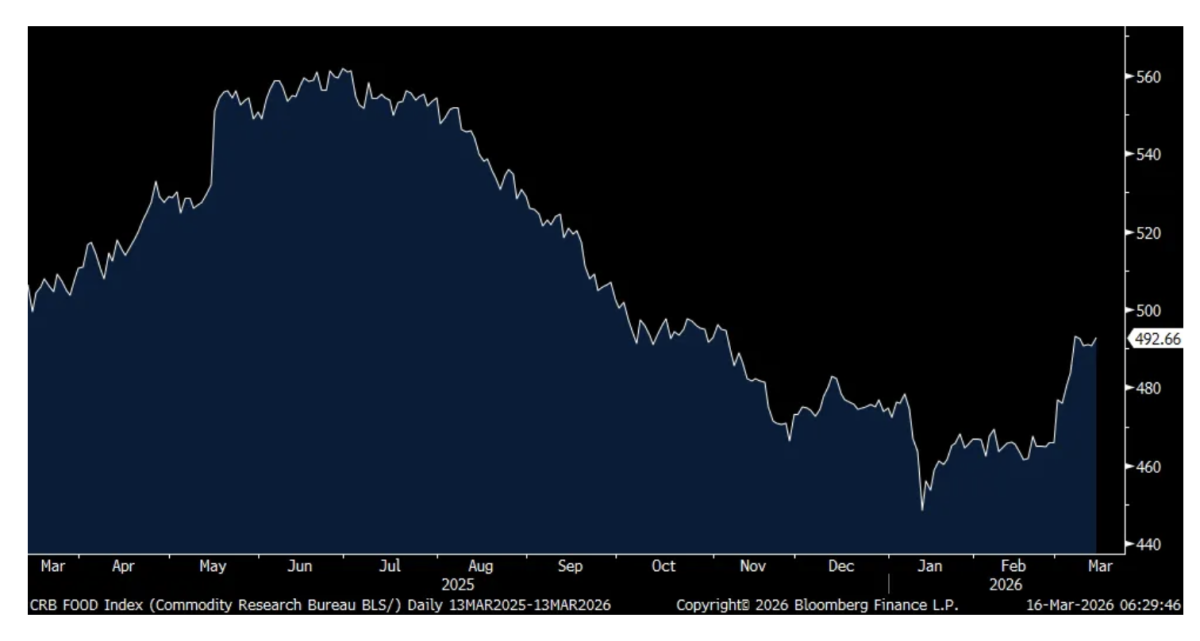

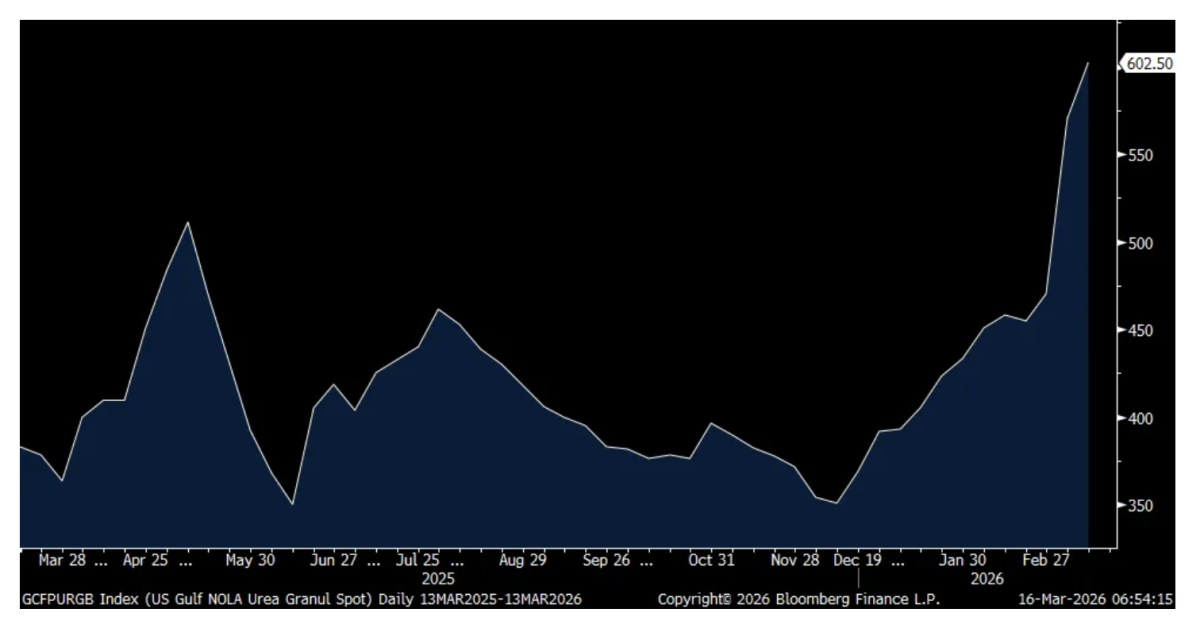

We’re also watching the price of food as fertilizer shipments slow, resulting in a jump in fertilizer prices. The CRB Food Stuff index closed Friday within pennies of the highest since last November.

CRB Food Stuff index

Price of Nitrogen (urea) per ton

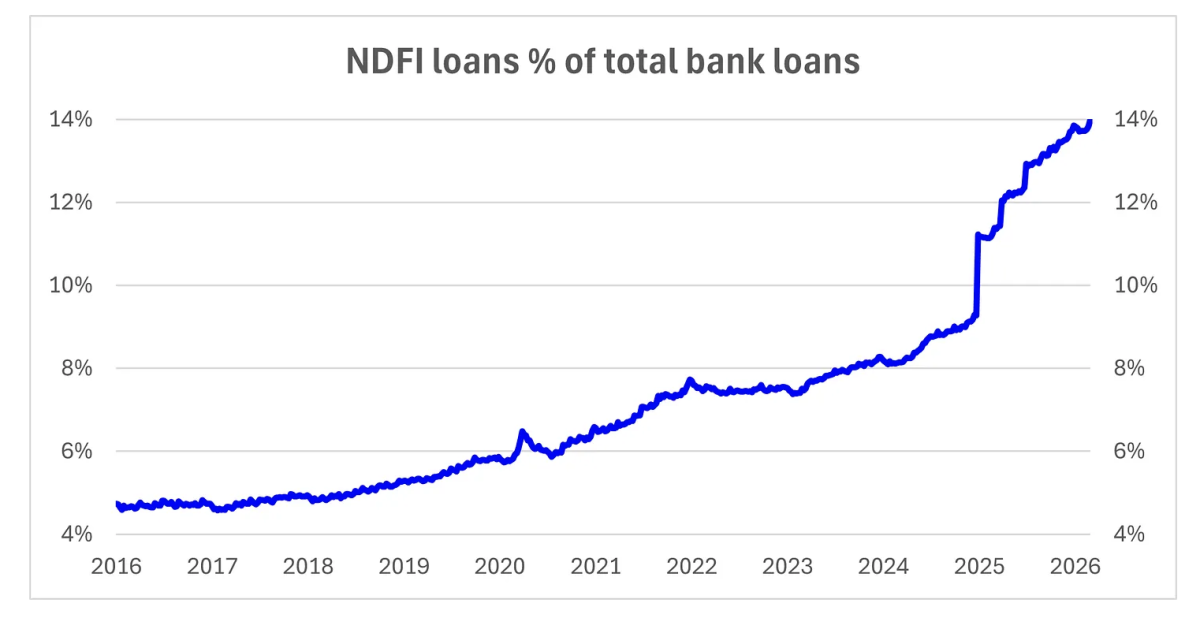

It was private credit that we know filled the void of bank lending post the GFC regulatory screws on the banks. It has been though banks that have been now lending to private credit and to what extent? This chart from my friend Adam Josephson. For those that aren’t watching closely, NDFI are non-depository financial institutions.

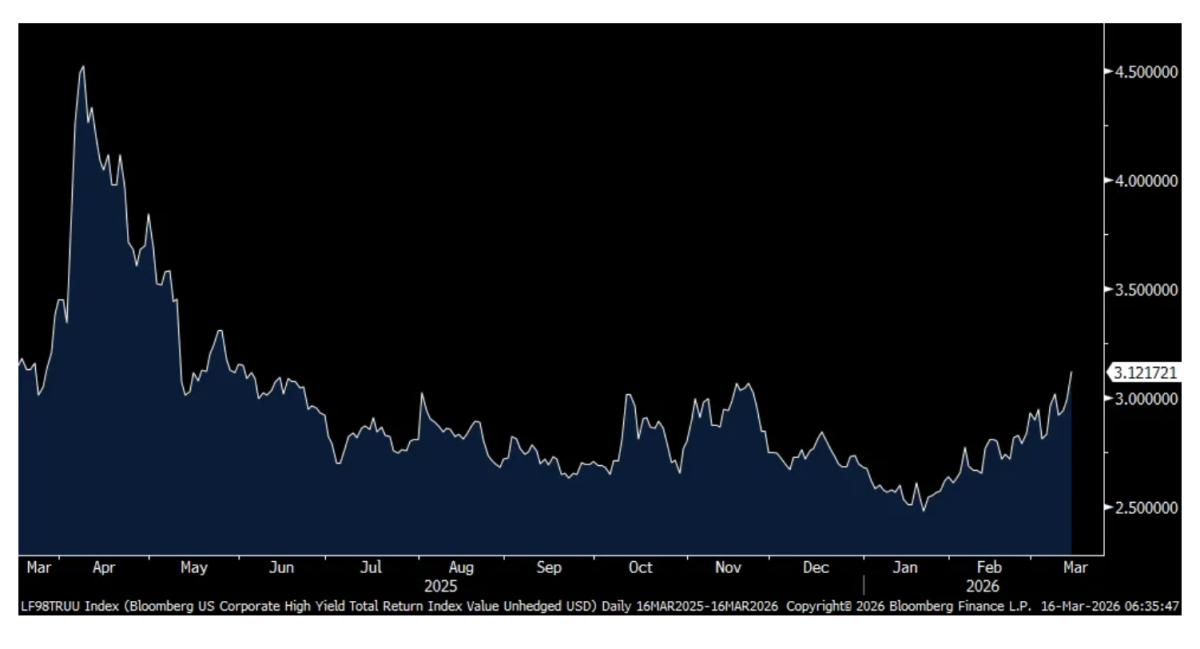

On Friday, the high yield spread to Treasuries broke above 300 bps to 312, the most since last June as we watch to see if there is any spillover from the private credit/leveraged loan markets.

High Yield spread to US Treasuries

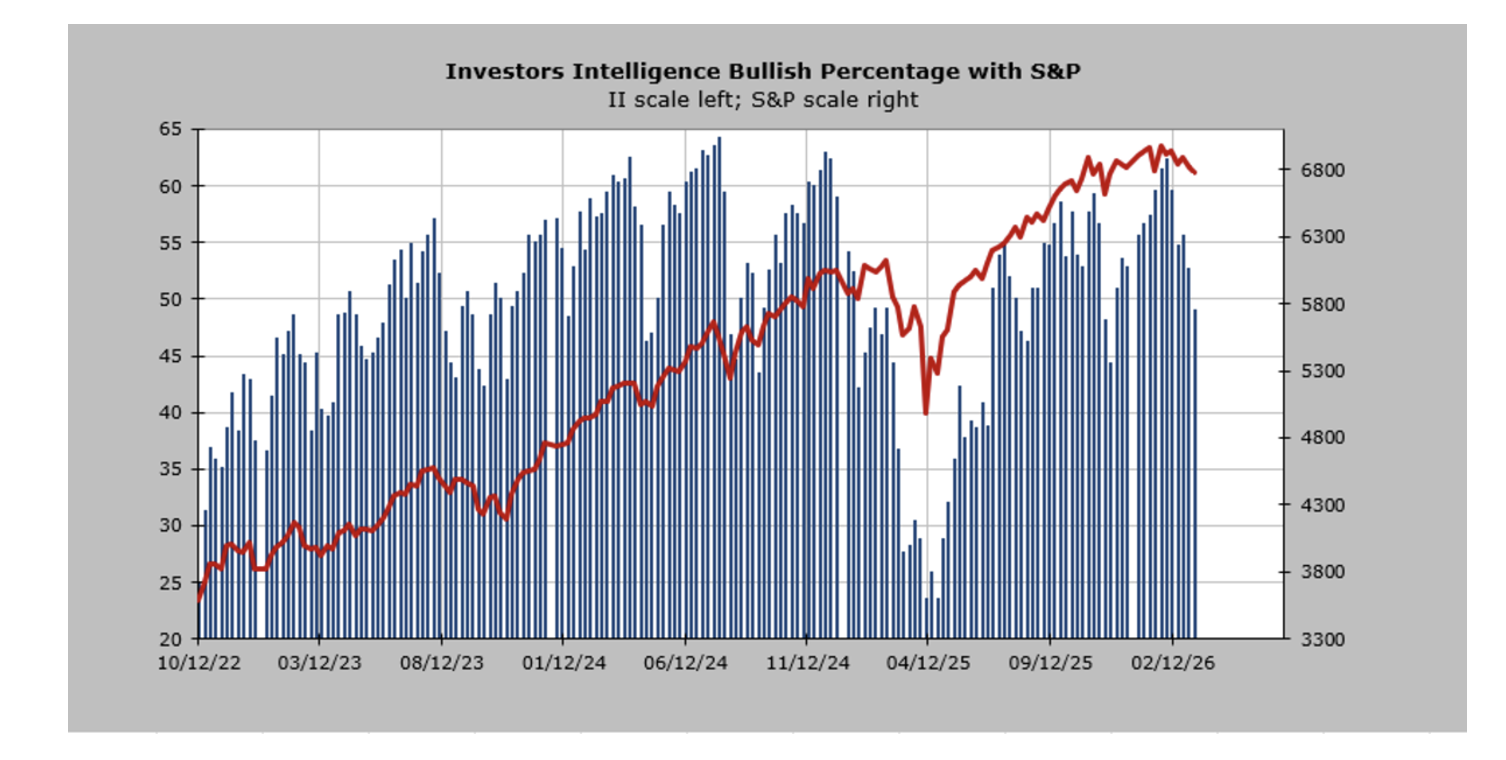

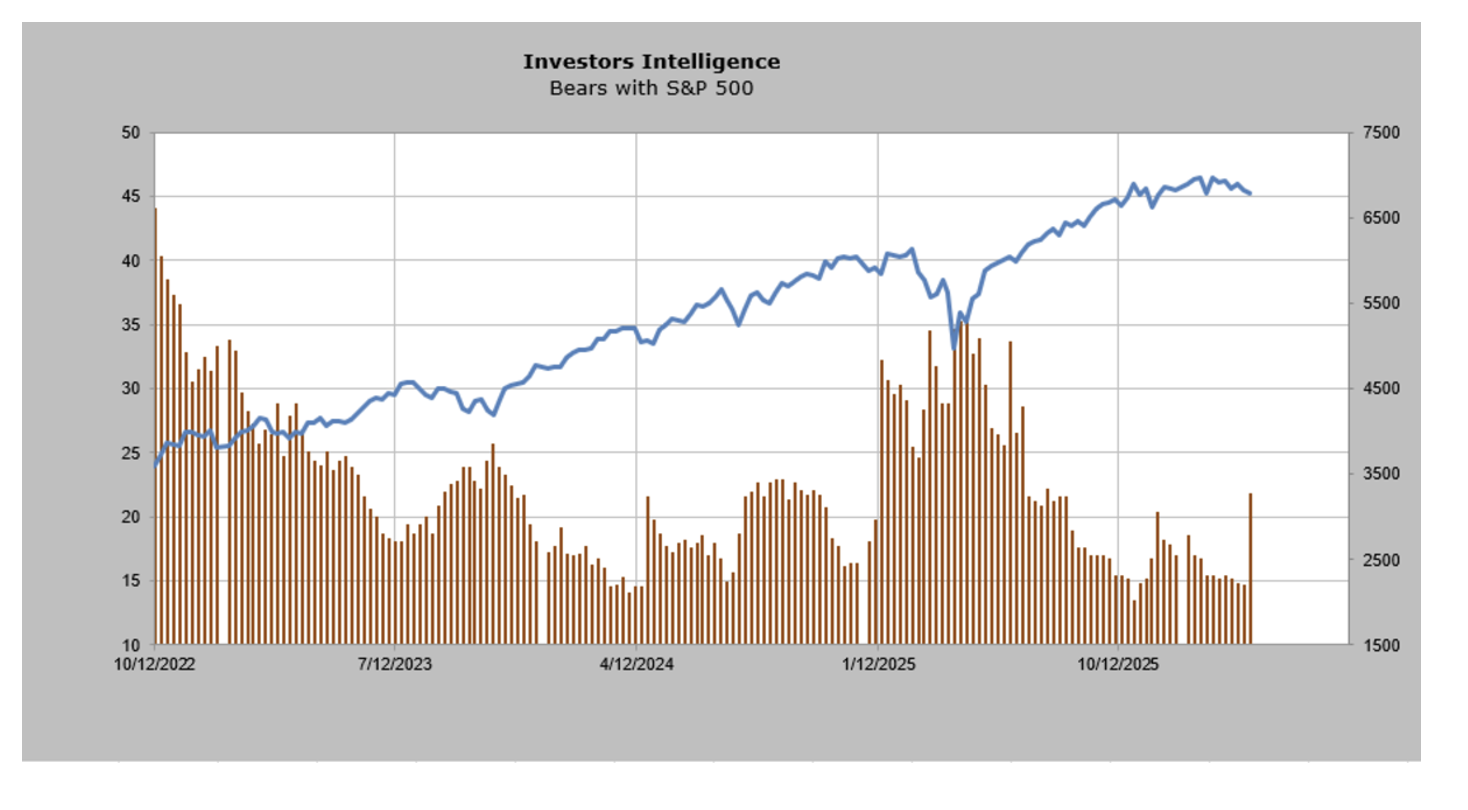

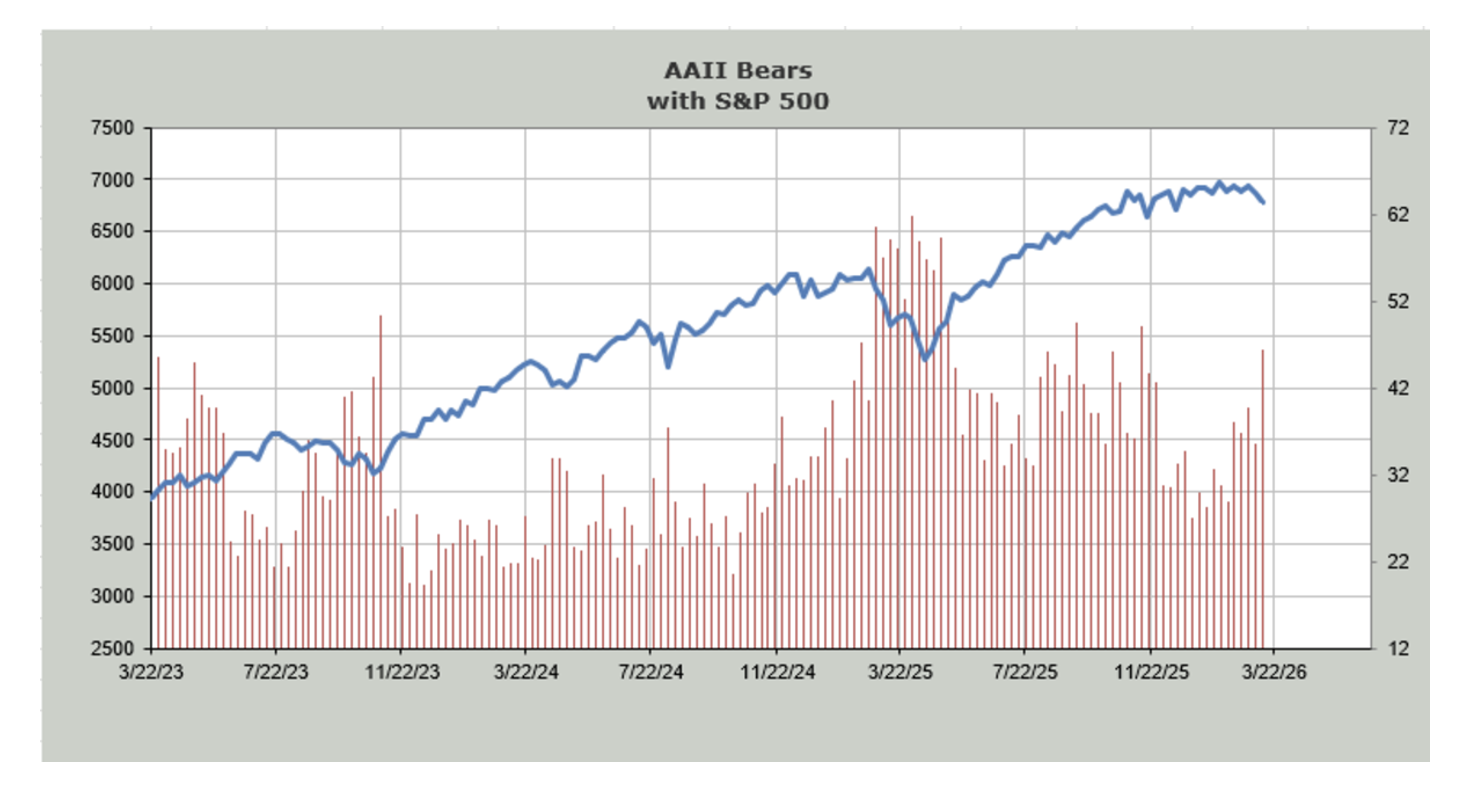

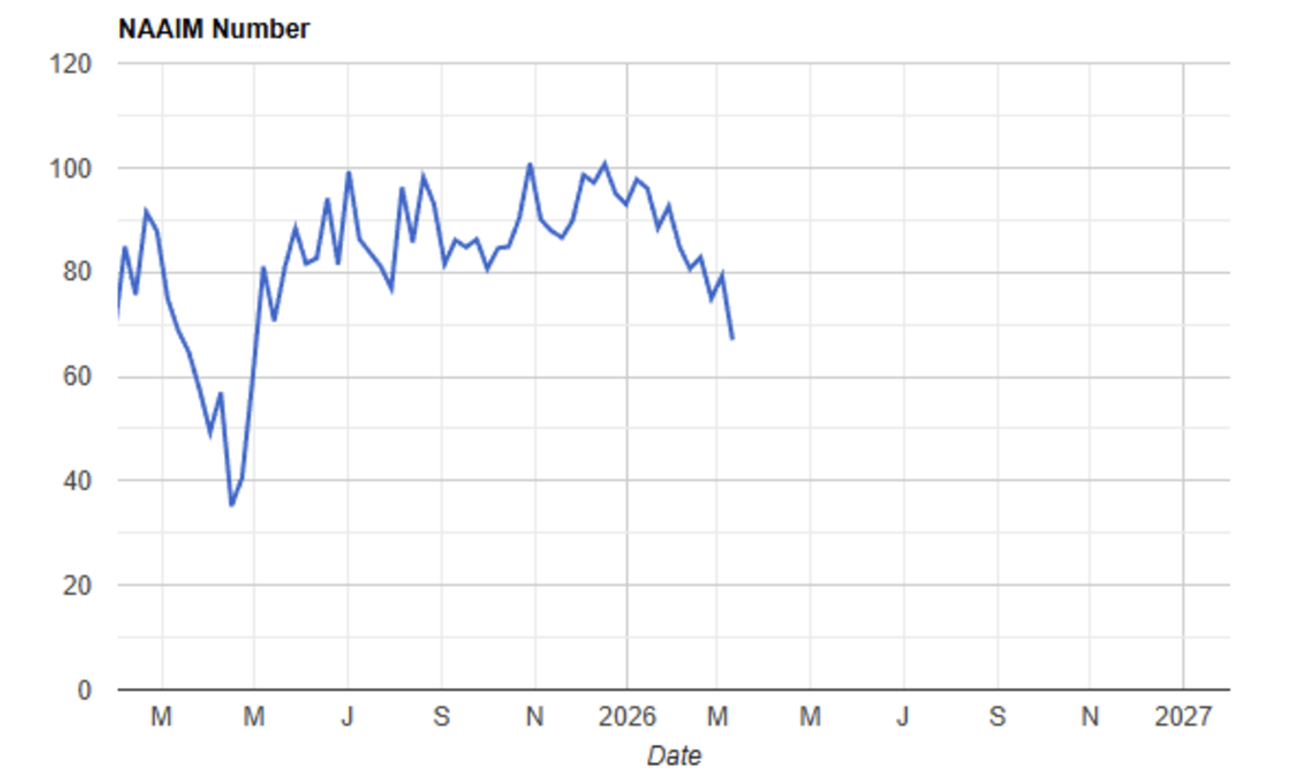

Time for a stock market sentiment check where bullishness has definitely cooled further. Last week, Investors Intelligence said Bulls fell to 49.1 from 52.7, and was over 60 last month, and that is the least since last November. Bears, stuck in hibernation over the past month, jumped to 21.8 from 14.6. The Citi Panic/Euphoria index finally slipped out of Euphoria, but barely as a .40 print compares with the Euphoria threshold of .41. AAII on Thursday said Bulls fell for a 6th straight week, by 1.2 pts to 31.9. Bears jumped by 10.9 pts to 46.4. The CNN Fear/Greed index is at just 22, in the ‘extreme fear’ quadrant. The NAAI Exposure Index is down to 67.

Bottom line, from a contrarian standpoint, this quieting of the Bull sentiment and the lift in bearishness is the set up for a rally with only the timing and extent the question and most likely surrounding the end of the war with Iran and/or opening of the Strait.

Dollar Tree just reported earnings that were about as expected. Comps rose 5% as forecasted “driven by a 6.3% increase in average ticket, partially offset by a 1.2% decline in traffic.” We await more from their call at 8am est.

China reported a bunch of February data, combined with January to smooth out the Lunar New Year influence. Retail sales, industrial production and fixed asset investment all exceeded expectations. Home prices fell again but at a slightly slower pace. I continue to believe that home prices need to stop going down in order to get a more sustainable lift in consumer spending, the missing piece of economic activity in China. The Hang Seng rallied by 1.5% overnight.

As Iran has allowed Chinese ships to traverse through the Strait, outside of the price rises in a variety of things, China has been relatively insulated from what is going on from a volume standpoint. Also, they have been huge buyers over the last year of crude oil to stock up their strategic reserves and we know they have gone huge into hybrids and full EVs in order to reduce their reliance on imported fuels, not because they are a bunch of clean energy fans, evidenced by the amount of coal plants they continue to bring on line. We remain long some stocks trading in Hong Kong.

"Friday also marks the March monthly options expiration, which is historically one of the largest of the year. From a market structure perspective, expirations can be significant events as stale contracts expire and fresh positioning is rolled into the next month… pic.twitter.com/nYFhabC1xn

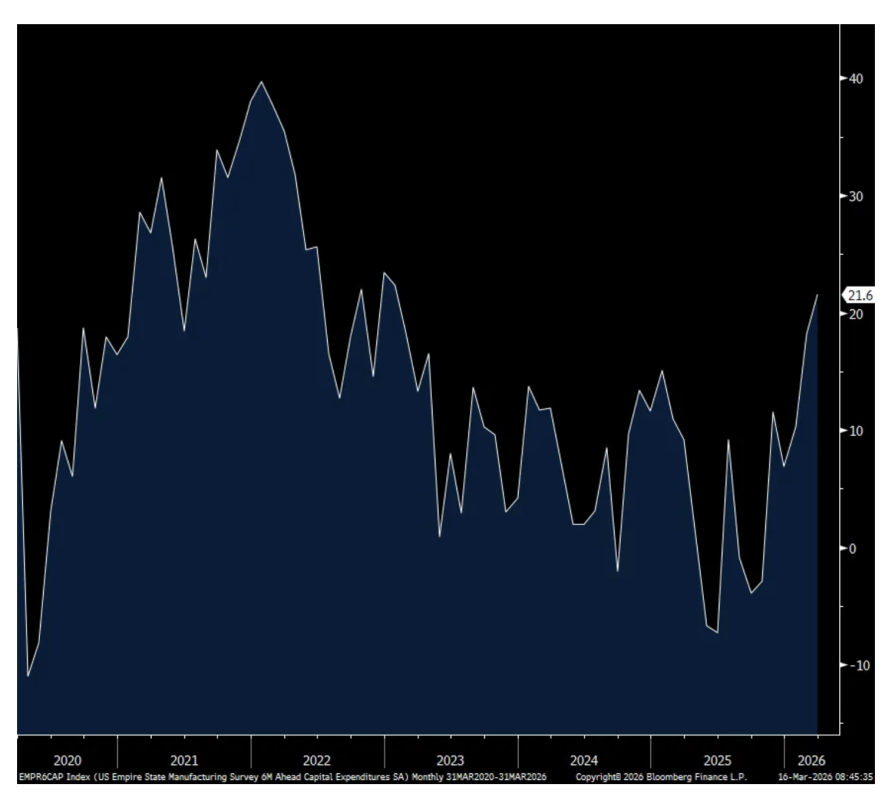

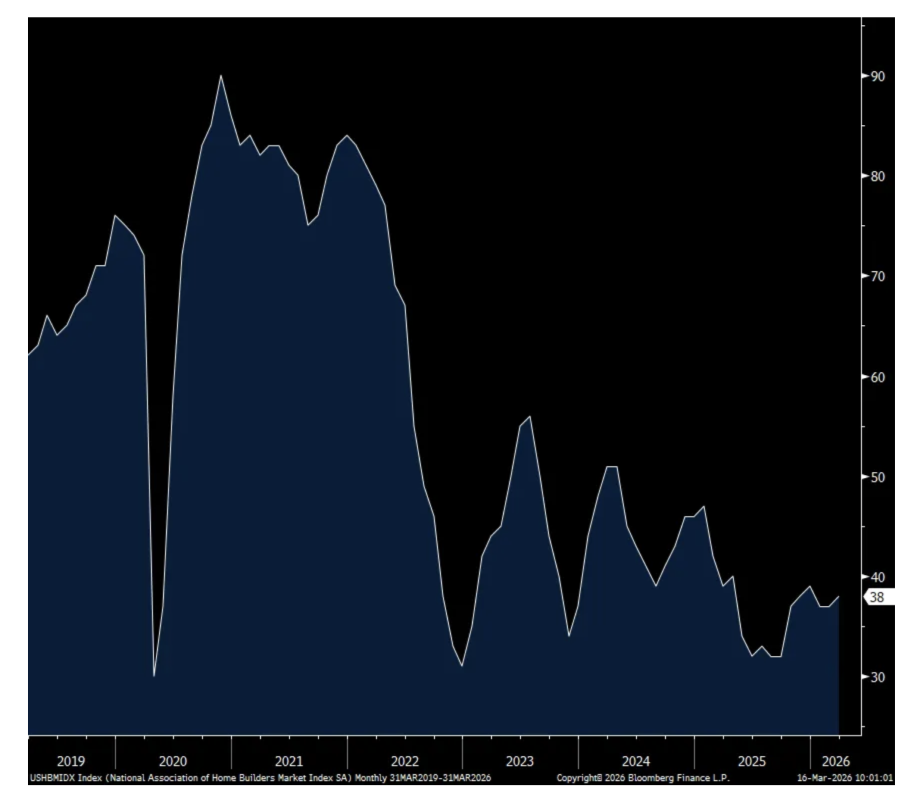

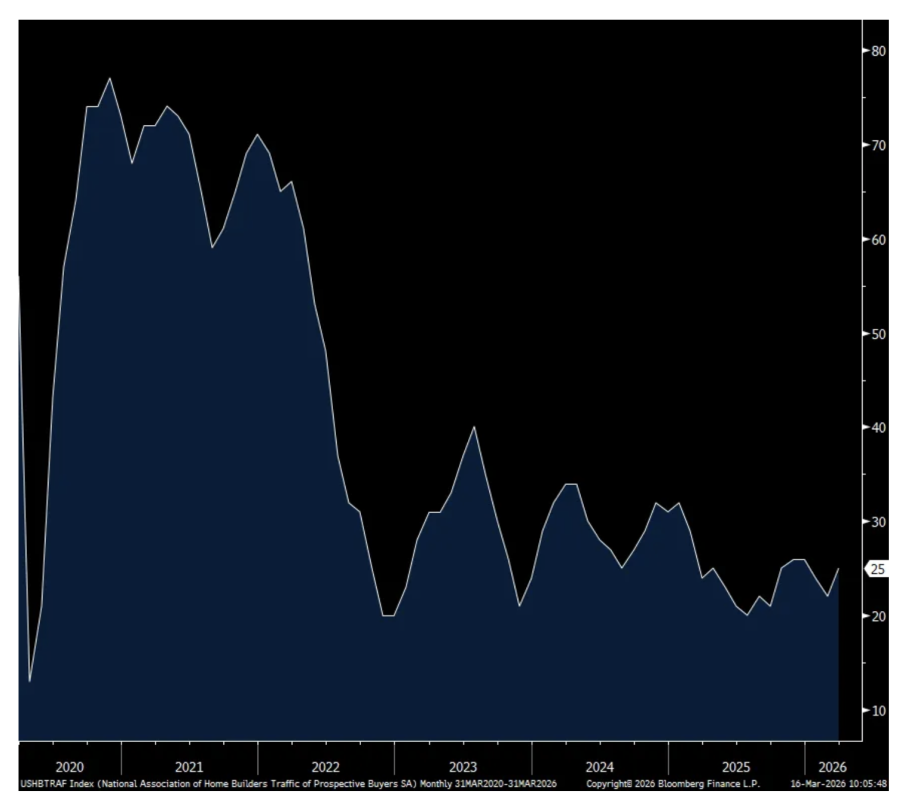

Boockvar on New York Manufacturing, Skittish Homebuilders/Buyers

From Peter Boockvar:

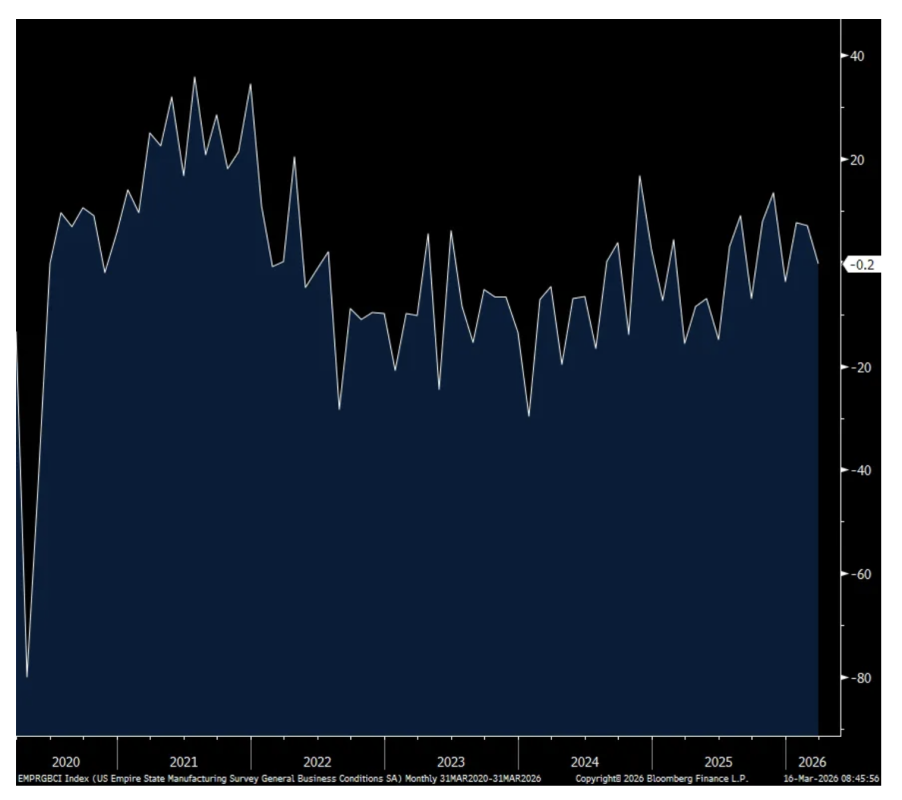

NY manufacturing/IP still being driven by data centers/Home builders still skittish as are buyers

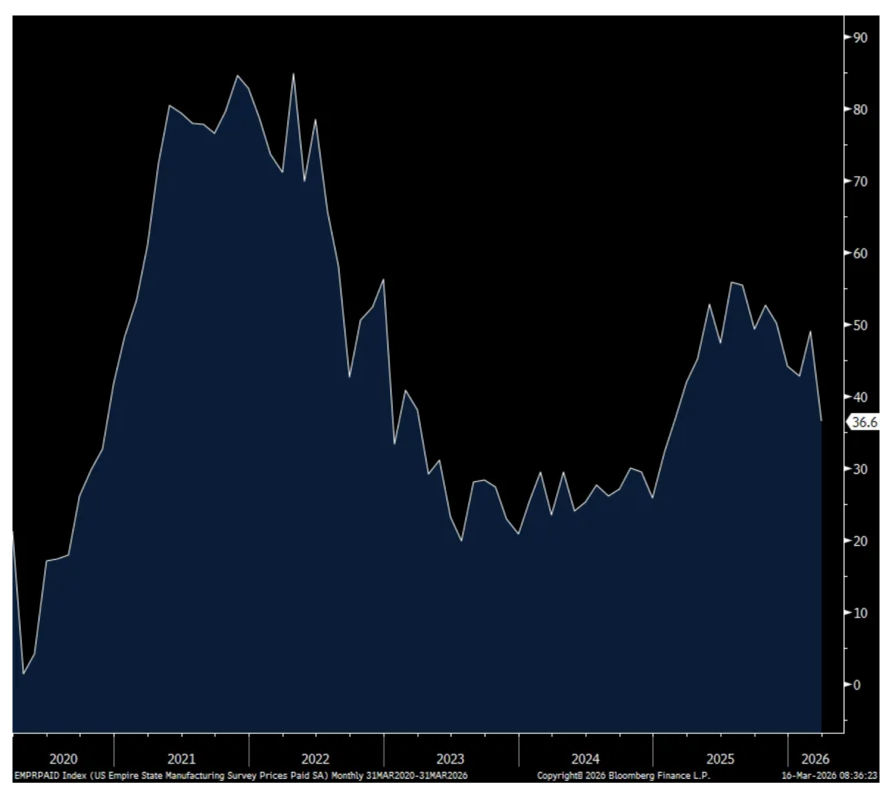

The March NY manufacturing index slipped back to flat from +7.1. Noteworthy though within the data was the drop in prices paid to the lowest since January 2025 but I’m guessing that survey participants haven’t yet gotten their fresh fuel bills. Prices received were little changed.

New orders and backlogs were little changed too m/o/m in this very volatile data set. Inventories, which I believe is responsible for the recent improvement in manufacturing around the world, held its prior month level, printing 6.9, about double the six month average. Employment lifted to 5.8 from 4 and that is above the 6 month average.

The six month outlook for business was 31 vs 34.7 in the month before but slightly above the half yr average of 29.4. Expectations for prices paid and those received fell surprisingly in light of what’s going on in the other part of the world. Capital spending expectations rose for a 3rd month as maybe companies are taking advantage of the CapEx tax incentives.

Bottom line, US manufacturing is trying to carve out a bottom, with the help from inventory builds but as seen at least in the NY region, it’s still a choppy environment out there.

NY Mfr’g

Prices Paid

Capital Spending Plans

Spending on data centers continues to be reflected in the US industrial production figures. In February, the ‘high tech industries’ category saw a .7% m/o/m gain and up 8.6% y/o/y with help from semi’s/electronics, communications equipment and computers (though down .3% in Feb but after jumping by 3.1% in Jan). Electrical equipment was up 1.1% and up solidly over the past six months.

Also boosting production overall was a 1.7% rise in the makings of autos/parts. Machinery production was a drag of 1.2% m/o/m but after increasing by 1.5% in the month before.

The March NAHB home builder sentiment index was 38 vs 37 in February and remaining well below 50. The estimate was 37. The Present Situation rose 1 pt m/o/m to 42 while the Future Outlook was up 2 pts to 49. Prospective Buyers Traffic rose 3 pts to 25, but half of the 50 breakeven.

And why is buyer traffic still so depressed? We know why and the NAHB tells us again, “Affordability for buyers and builders remains a top concern. Many buyers remain on the fence waiting for lower interest rates and due to economic uncertainty.”

And, offsetting the drop in mortgage rates over the past few months, “downpayment hurdles and uncertainty from the conflict with Iran and the price of oil will be headwinds going forward.”

On the supply side, “Builders are facing elevated land, labor and construction costs and nearly two-thirds continue to offer sales incentives in a bid to firm up the market.” And to what extent? “37% of builders cut prices in March, up slightly from 36% in February. The average price reduction remained stable at 6%. The use of sales incentives was 64% in March, down one percentage point from February, and marking the 12th consecutive month this share has exceeded 60%.”

I don’t have much to add with a bottom line as we know the continued challenge for many first time home buyers in being able to afford a home. I’ll add again, attempts that just focus on the demand side without a coincident increase in supply will just further juice home prices.

Growing Less Bearish — But Certainly Not Yet Bullish

* Though P/E ratios remain elevated — investor sentiment has soured, positioning is defensive and many of our concerns are being realized

* Uncertainty remains present and a strong conviction (either way) does not yet seem appropriate

* Given the plethora of multiple challenges and headwinds — that have only recently been acknowledged by many investors — I expect a longer bottoming process than in the past... so the customary "V" market bottoms (made over the last three years) seem unlikely

* We are applying "second-level thinking" today and with many stocks -25% or more, a modestly net long exposure now seems appropriate (a shift from our long standing and slightly net short exposure)

* It is increasingly possible that I will be "returning to the land of the living" by sensibly and gradually expanding my long exposure in the weeks and months ahead

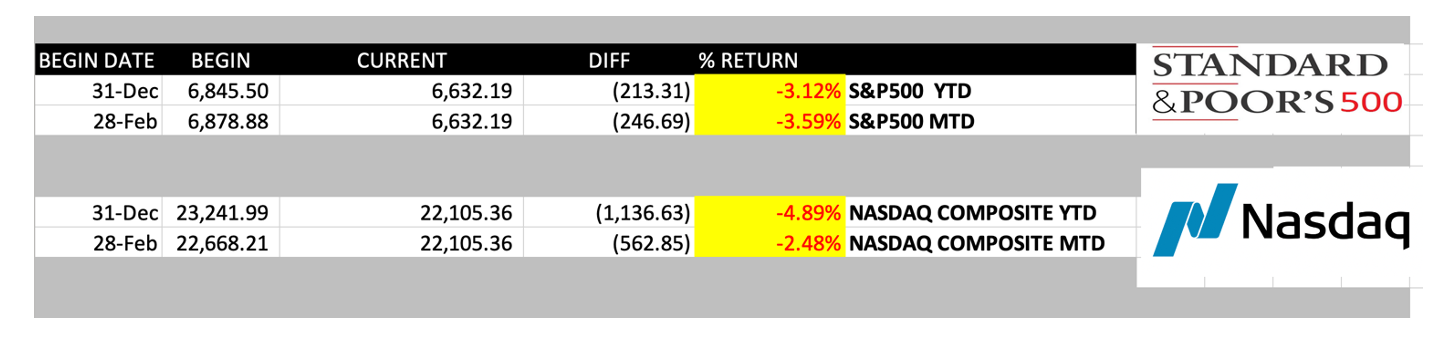

* The S&P Index is down by about -4% year to date — I continue to expect a high-single-digit negative to low-double-digit negative return for the year

* Over the balance of the year (as was the case in January-March), stock picking will be crucial and, when done well, value-added to portfolios

* Always remember: short selling protects capital, long buying creates capital

"Buy to the sound of cannons, sell to the sound of trumpets."

- Baron Nathan Rothschild

In recent weeks, equities have finally begun to reflect my prevailing fundamental, valuation and geopolitical concerns:

The purpose of today's opening missive is to convey that, to me, the times (and markets) they are a-changin':

Come writers and critics

Who prophesize with your pen

And keep your eyes wide

The chance won't come again

And don't speak too soon

For the wheel's still in spin

And there's no tellin' who

That it's namin'

For the loser now

Will be later to win

For the times they are a-changin'

- Bob Dylan, The Times They Are A Changin'

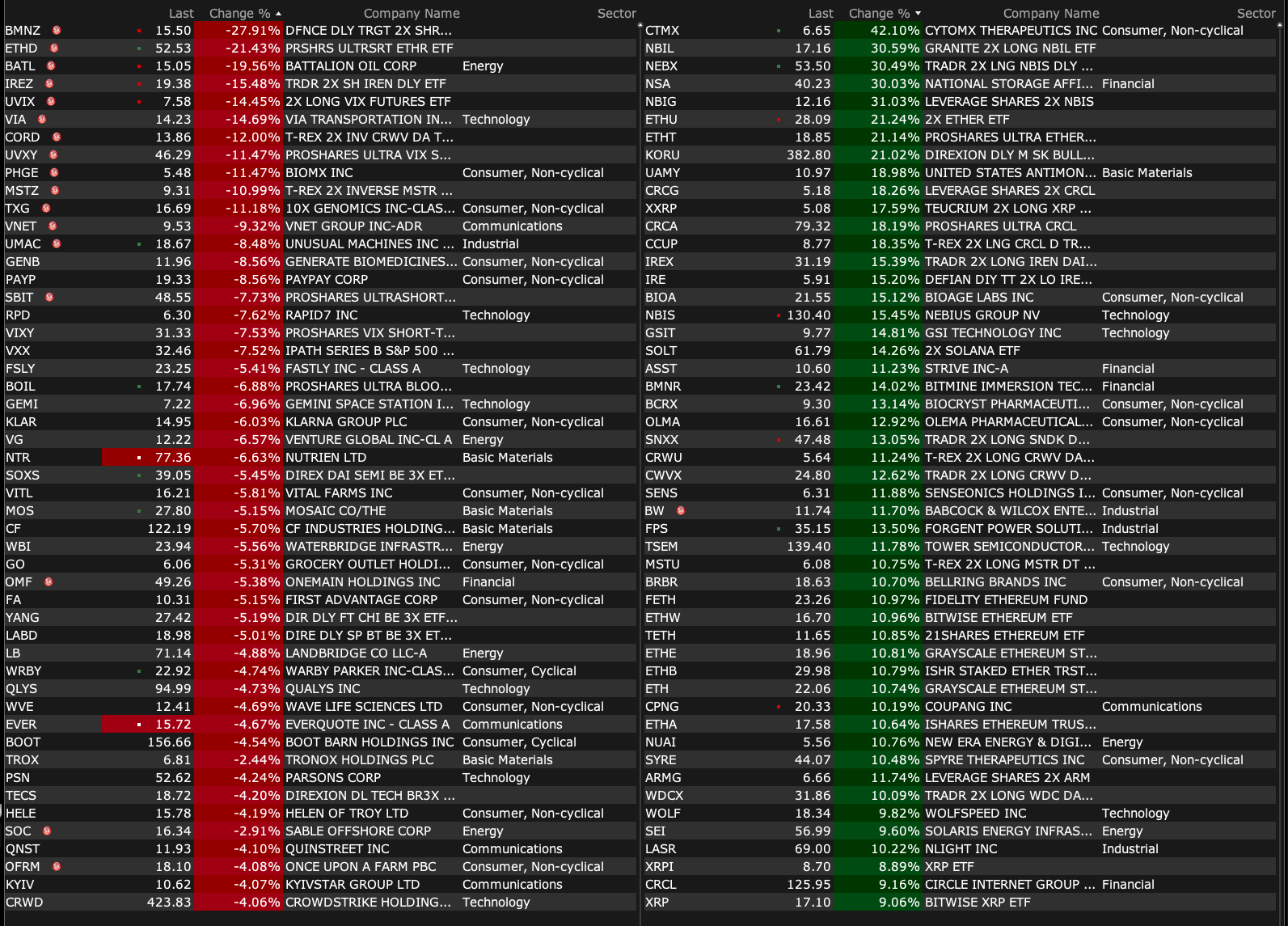

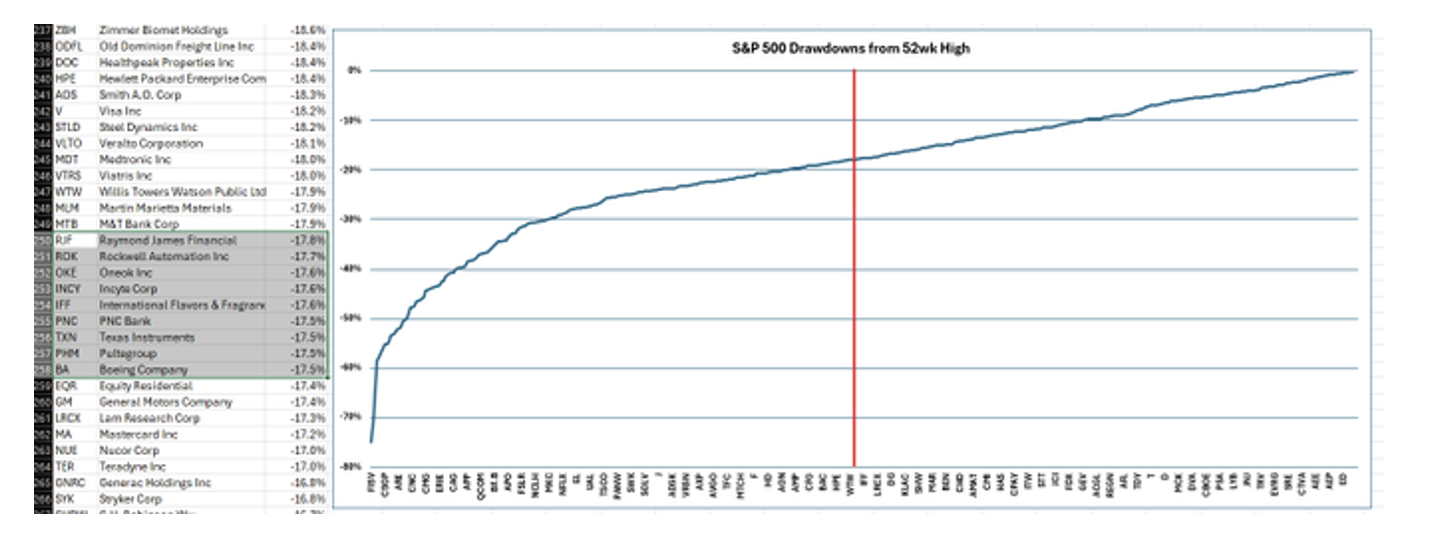

Under the ominous cover of the Iran conflict (and its economic ramifications), many stocks have quickly turned down by -25% or more, creating potential opportunities. The median S&P 500 Index stock drawdown is -18% (from the 52-week high):

The S&P Index is now -5.4% from its peak in late January 2026. That is the 32nd pullback greater than 5% since the March 2009 Generational Bottom:

The S&P 500 is down 5.4% from its Jan 28 peak, the 32nd pullback >5% since the March 2009 low.

The "league leading" Mag 7 bubble has burst — falling more than -10% below its October record. For the first time since 2022, all seven constituents are negative year to date:

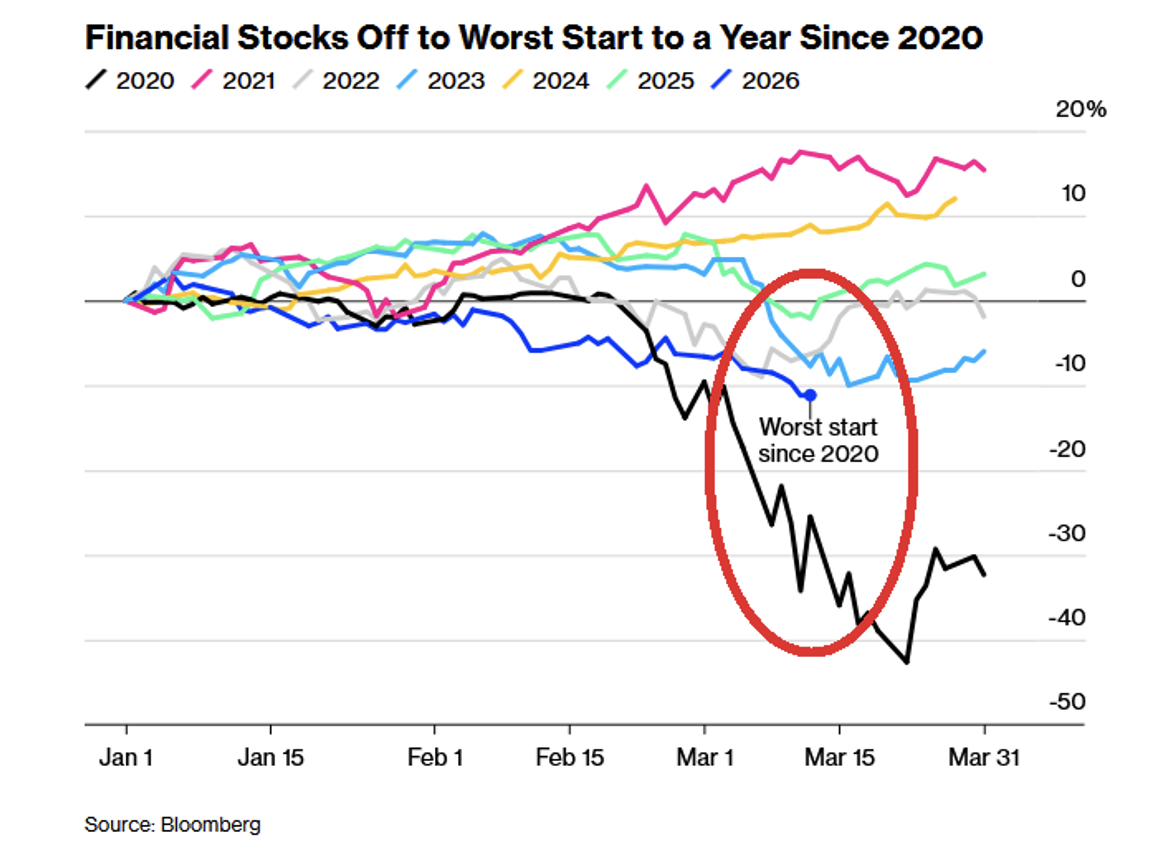

The S&P 500 Financials Index is -12% year to date — on track for the largest quarterly decline since early 2020. Private credit equities are down by over -30% year to date:

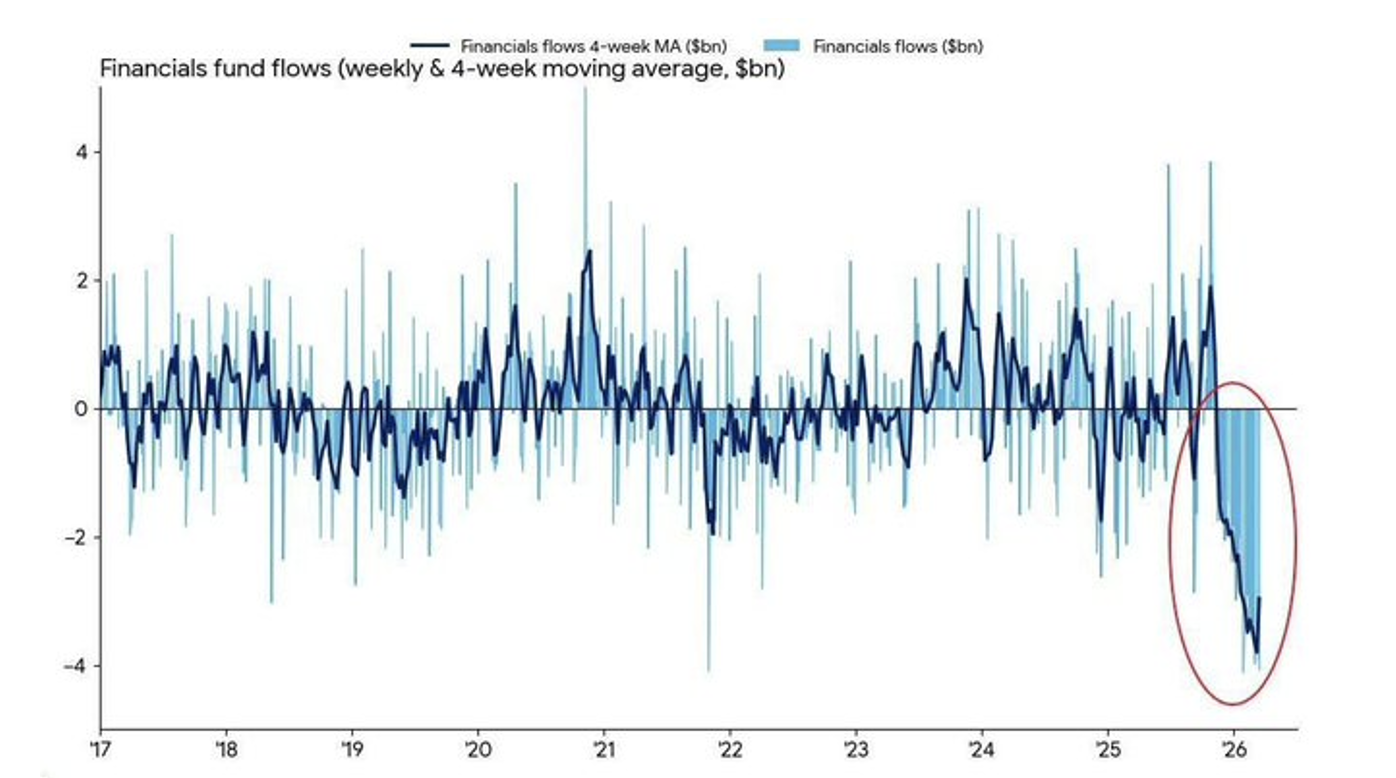

According to Bank of America, financial fund inflows are breaking records:

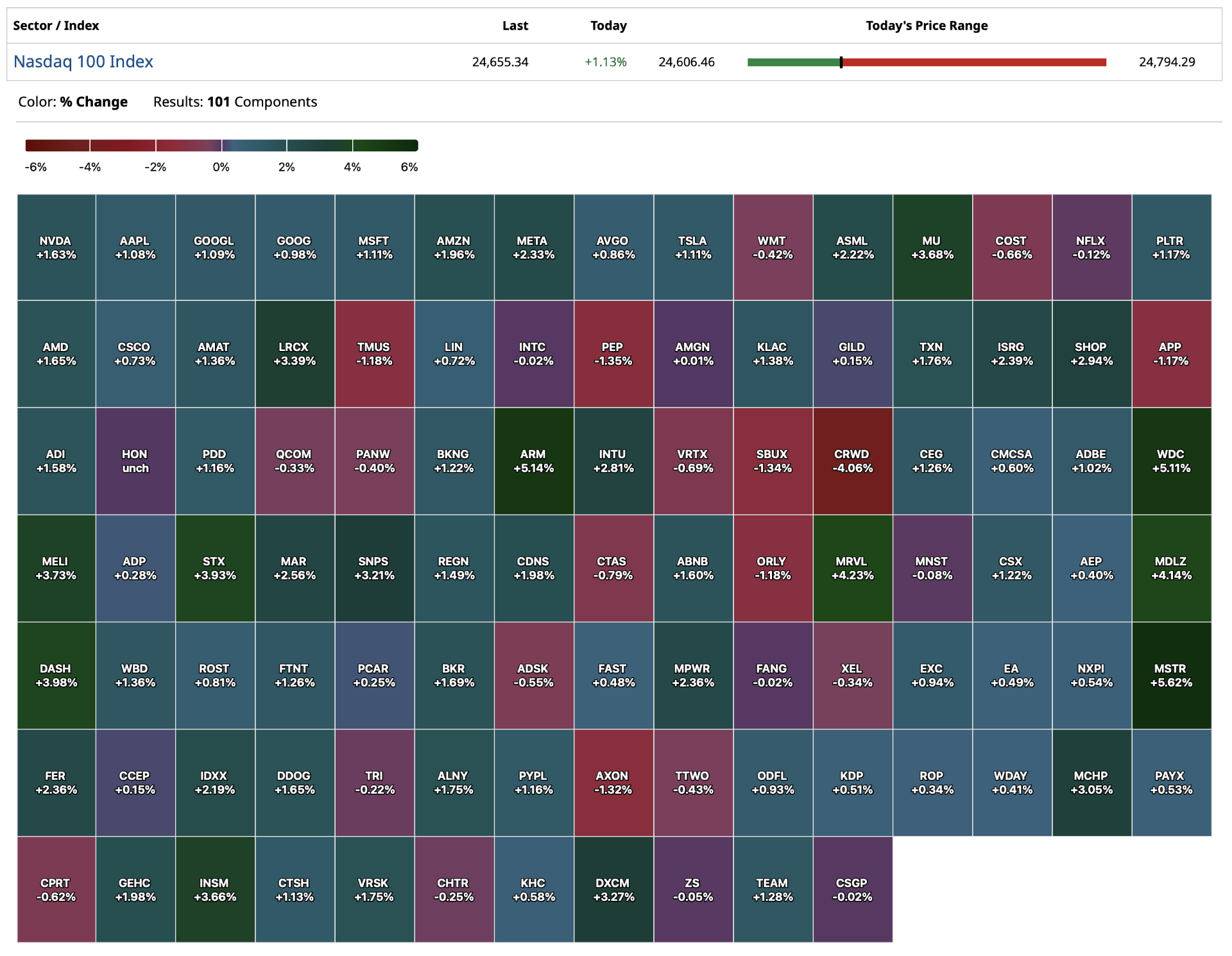

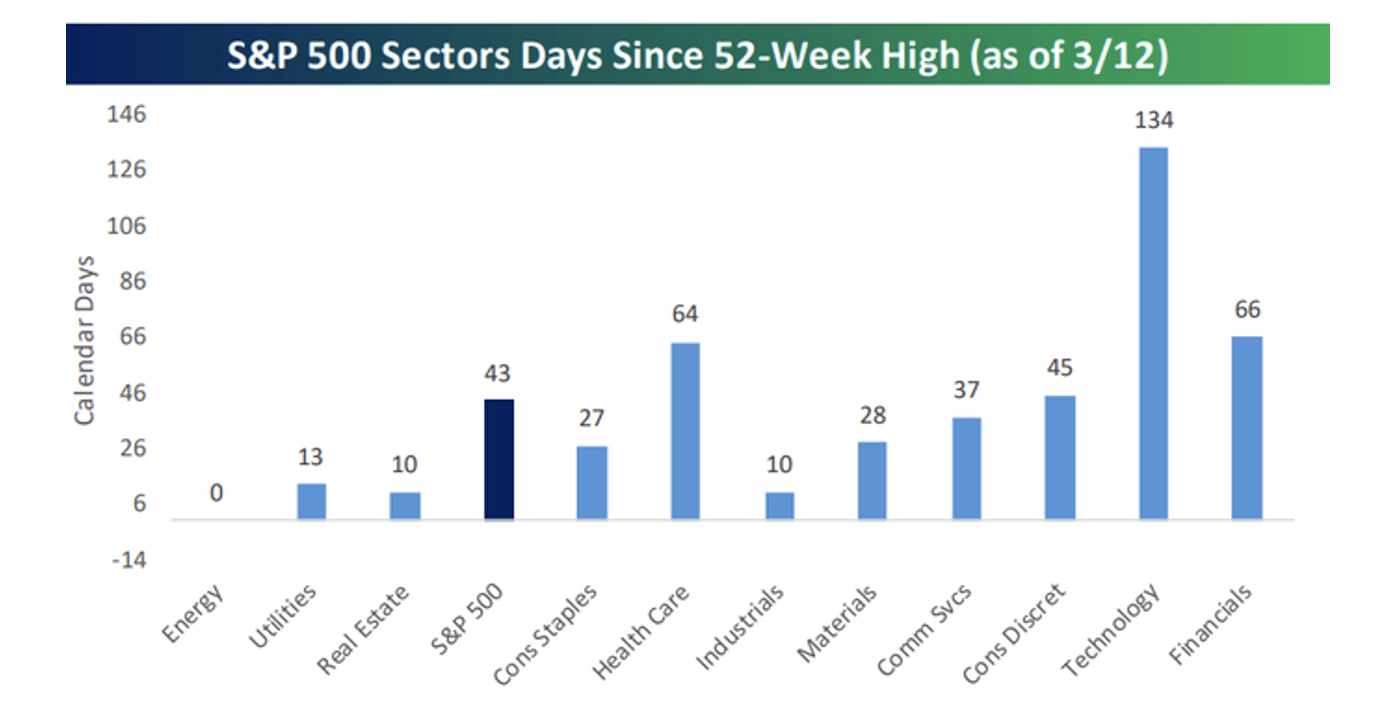

It has been over 40 days since the S&P Index reached its last 52-week high but 134 days since the Tech sectors' last 52-week high:

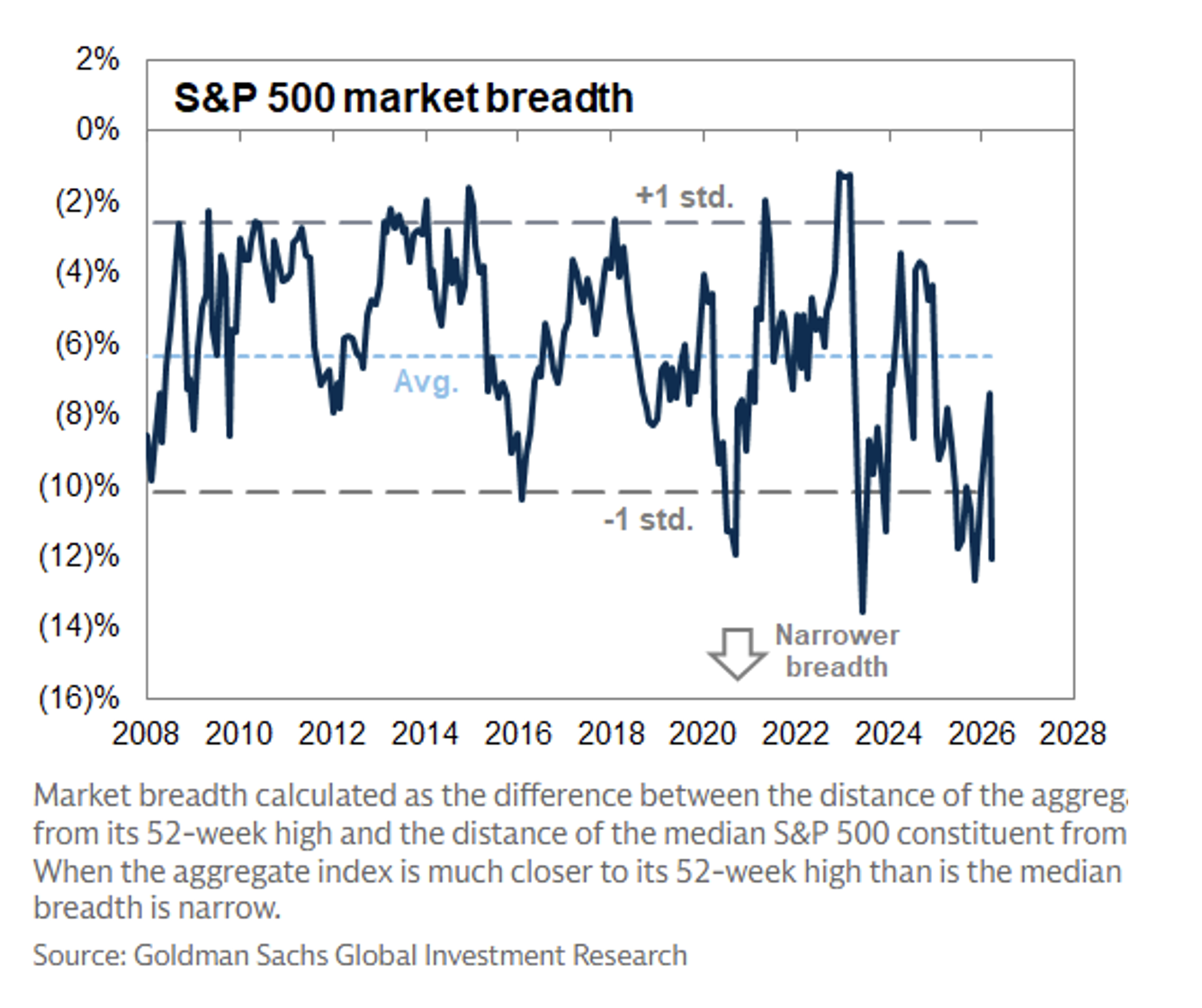

Meanwhile, market breadth (measured below by the gap between the S&P Index and its median stock relative to their 52-week highs) has a foul odor and may be approaching an extreme:

Besides the sharp fall in several market sectors, I am increasingly encouraged by the buildup in fear and that many market participants are coming around to acknowledging our multiple concerns.

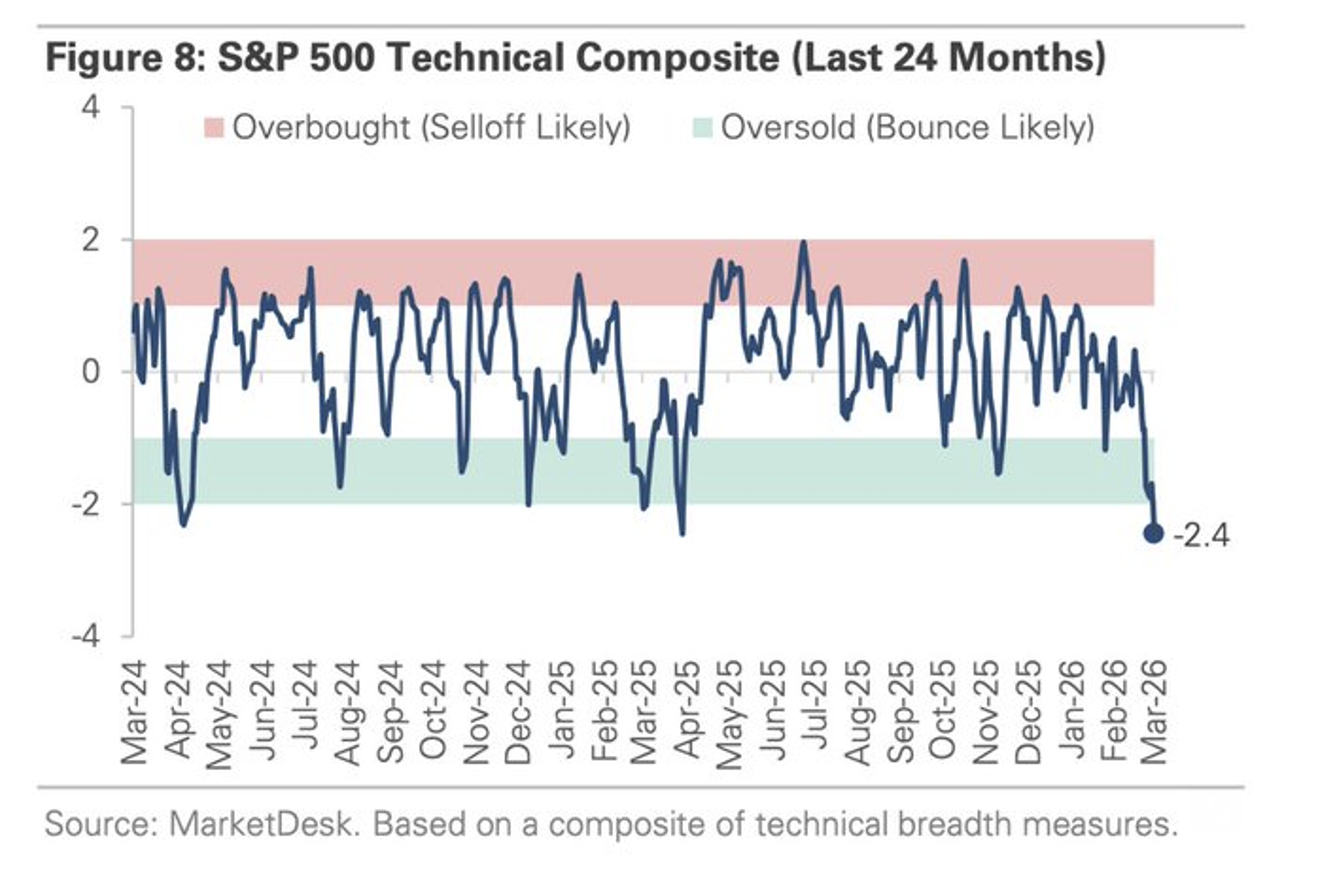

No longer overbought, the S&P Index has hit the most oversold in 24 months (this morning the S&P Short Range Oscillator hit -7.87%):

Money flows into (SPY) (the largest ETF) are nearing a bottoming level seen during the 2018, 2020, 2022, and 2025 crashes (a bottom is near in terms of time, not necessarily in the magnitude of the flush. A bounce must be sustained in the short and long term. See the local bottom of March 2022 for context):

As to Iran, today I am reminded of Baron Nathan Rothschild's famous quote (mentioned earlier):

"Buy to the sound of cannons, sell to the sound of trumpets."

Along with lower stock prices I have turned less bearish. As an example, I recently wrote in a letter to Seabreeze investors (my hedge fund):

In anticipation of a market correction/bear market we have substantially bolstered our cash position in order to take advantage of the possible developing long opportunities.

The purpose of today's (mid-month) commentary Is to highlight that while markets have and may continue to move lower — considering the recent pace of decline, better values in the U.S. stock market are likely to emerge.

Accordingly, I have moved from a small net short exposure to a small net long exposure over the last several days. Should equities continue to fall — and subject to macro conditions (inflation, interest rates, economic and corporate profit growth, etc.) — it is increasingly possible that I will be "returning to the land of the living" by sensibly and gradually expanding our long exposure in the weeks and months ahead.

Though fear is elevated, over the short term much will depend on how long the Strait of Hormuz is closed. If the Strait remains closed another two weeks, the price of crude oil will remain high. This makes interest rates very challenging given how elevated P/E multiples are (below). This uncertainty suggests that a strong conviction (either way) does not seem appropriate — and a modestly long net exposure seems appropriate.

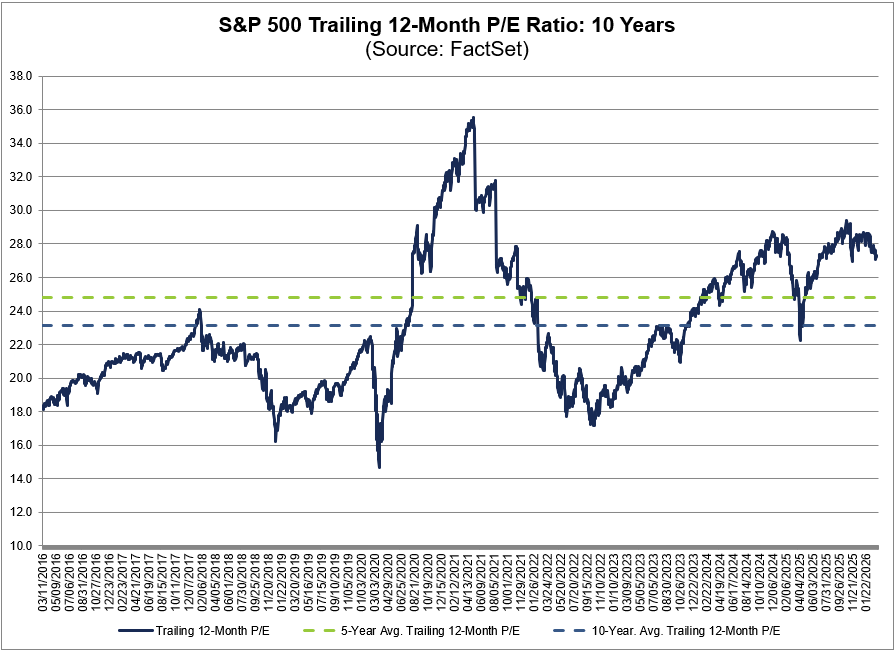

Equities continue to appear overpriced against history — this should be a limiting factor against "V" rallies:

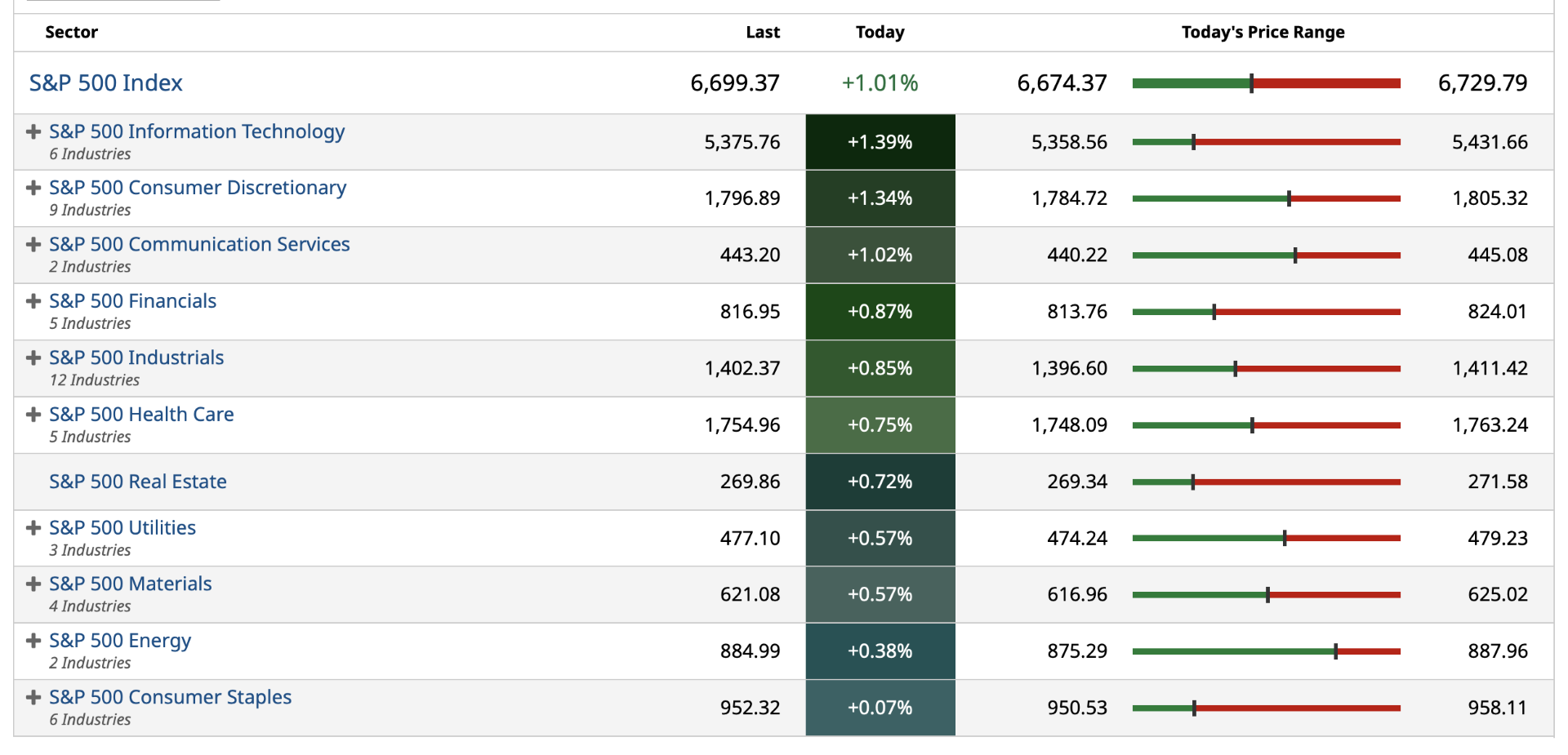

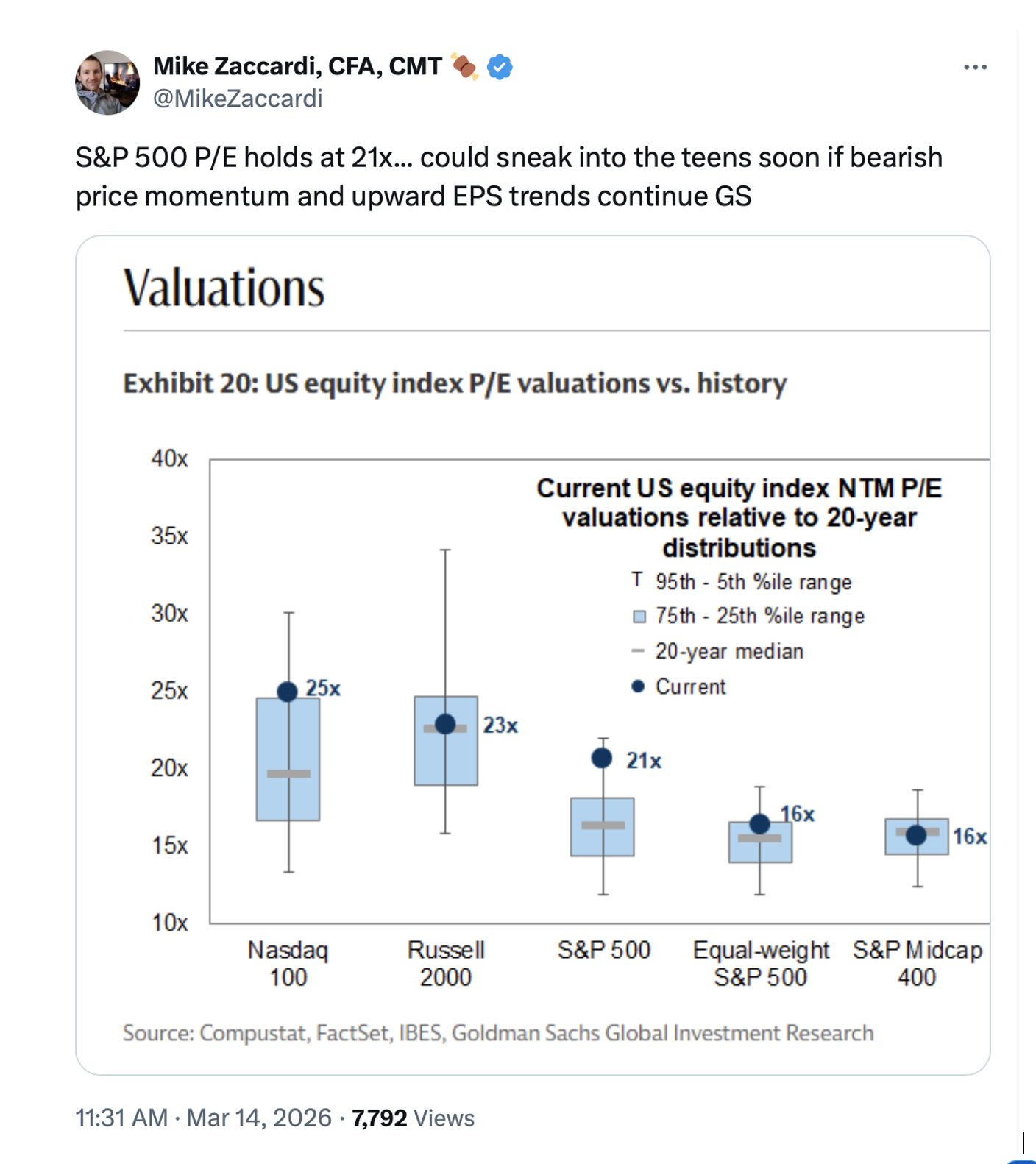

The trailing 12-month P/E multiple for the S&P Index is 27.2x, above the five-year average (24.8x) and above the 10-year average (23.2x):

No "V" Market Bottom Expected

I recognize that buying opportunities since early 2023 have been very brief and short-lived. With the benefit of hindsight, it was important to be prepared and bold to capture previous opportunity sets. This time, given the plethora of multiple challenges and headwinds — that have only recently been acknowledged by many investors — I expect a longer bottoming process that in the past. Accordingly, I will likely proceed in buying on a measured basis, waiting for the "right pitch."

Rarely Have Outcomes Been So Wide

For some time, I have been of the view that investors were underappreciating the risks of adverse geopolitical, economic and/or market outcomes — with many of them not friendly to stock prices and valuations. These concerns existed with valuations at about the 98%-tile and an equity risk premium that was slowly moving in the direction of being an equity risk discount.

Despite elevated valuations as well as reckless fiscal policy and rising geopolitical uncertainty — market participants put all of the concerns on the shelf. Stocks marched higher in 2023-2025. steadily climbing even though the probability of adverse outcomes were multiplying and gaining in probability.

The recent outbreaks of war in Iran (and Venezuela) are examples of adverse geopolitical developments (that I warned about in my 10 Surprises for 2026) that were universally ignored. The more serious U.S. incursion into Iran, in particular, is not an isolated adverse outcome. It is happening at a time in which the U.S. economy is slowing down, the rate of inflation is accelerating, and interest rates are rising:

* Slowing Economic Growth: According to the Commerce Department (on Friday) 4QGDP growth was only +0.7% — revised from the previous estimate of +1.4% and well below the consensus of +1.5%. Moderating domestic economic activity will feed into and weaken consensus S&P 2026-27 EPS expectations which remain too high.

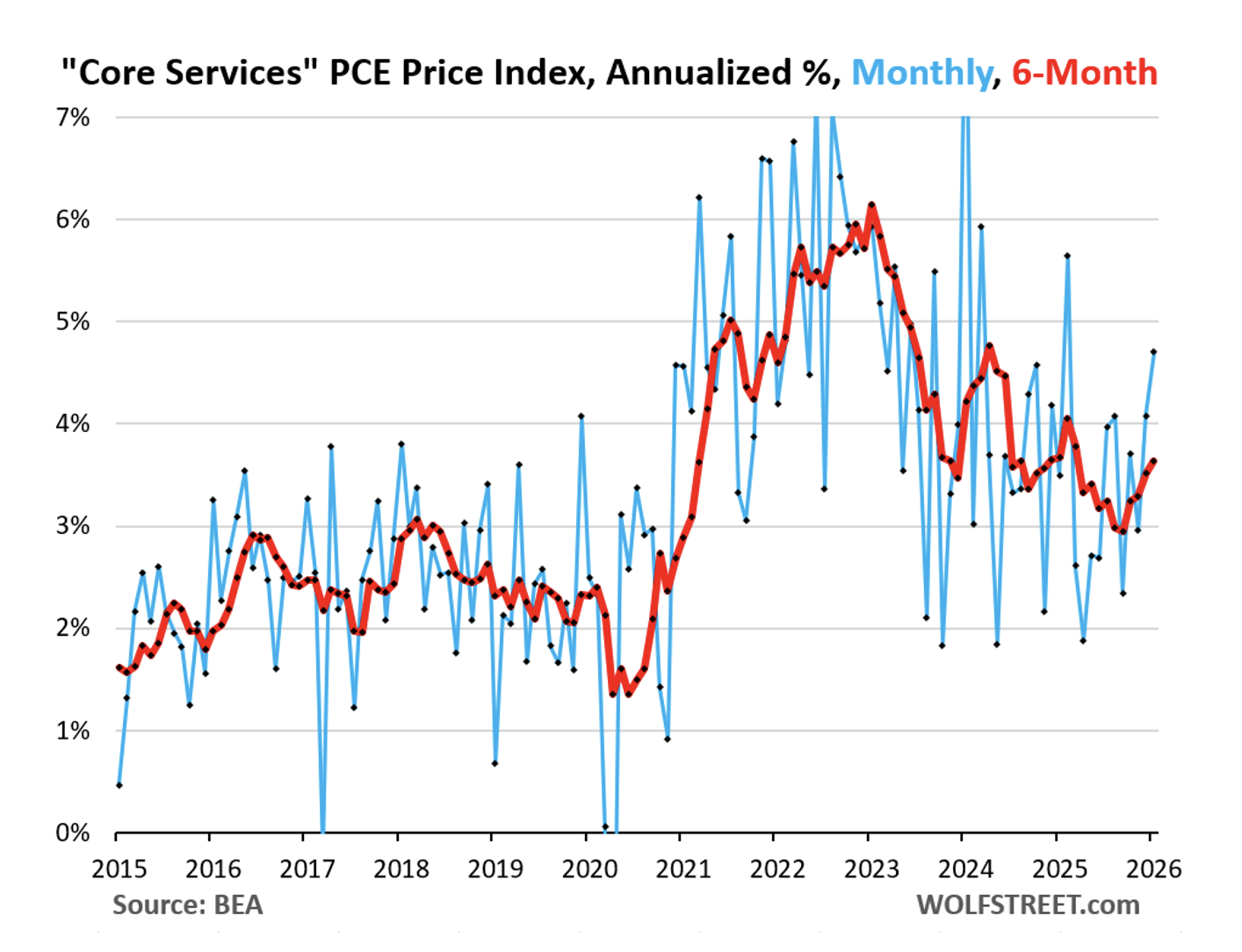

* Prickly Inflation: It was reported on Friday that February’s core PCE inflation rate (the Fed's favored inflation measure) hit 3.15%, the worst in two years — driven principally by core services which account for roughly 60% of the overall PCE price index (the energy spike is still to come).

The previously reported January core services PCE price index accelerated sharply both on a month-to-month basis (+0.38% or +4.7% annualized, blue line in the chart), and a six-month basis (+3.6% annualized, red line). This acceleration in January came on top of the acceleration in December. Year over year, the core services PCE price index accelerated to 3.4%. And it did so despite the deceleration of its housing components:

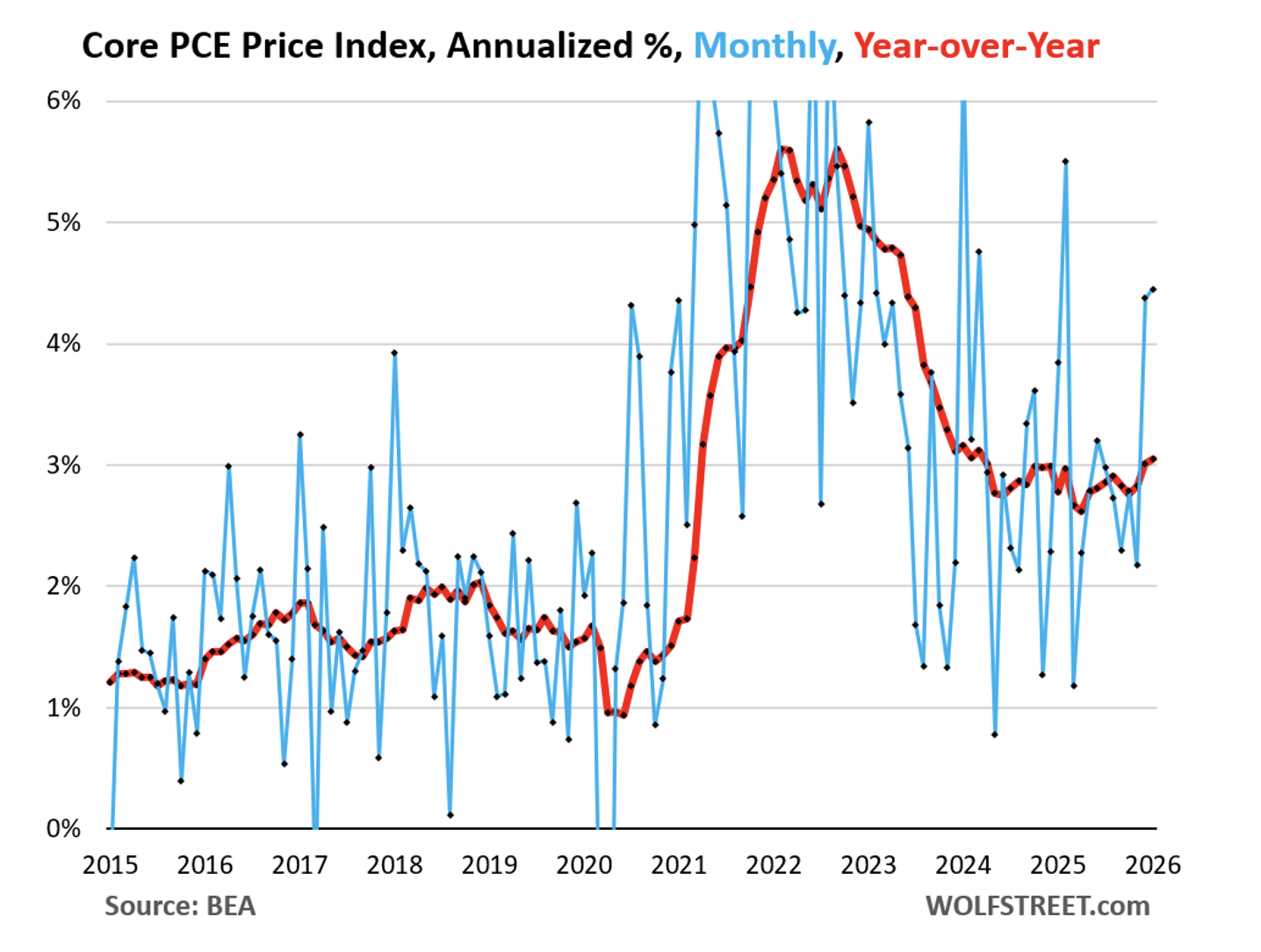

The January core PCE price index, driven by core services, jumped by +0.36% (+4.5% annualized, blue line) in January, after the big jump in December. Year over year (red line), it accelerated to +3.1%, the worst in nearly two years. It has been zigzagging higher and ever further away from the Fed’s 2% target since May 2025:

* Rising Interest Rates: Since the Iran conflict started on February 25, the yield on the 10-year Treasury note has risen by 38 basis points. This has contributed to a sharp rise in mortgage rates (from slightly below 6.00% last month to 6.28% today) and to an expanding equity risk discount.

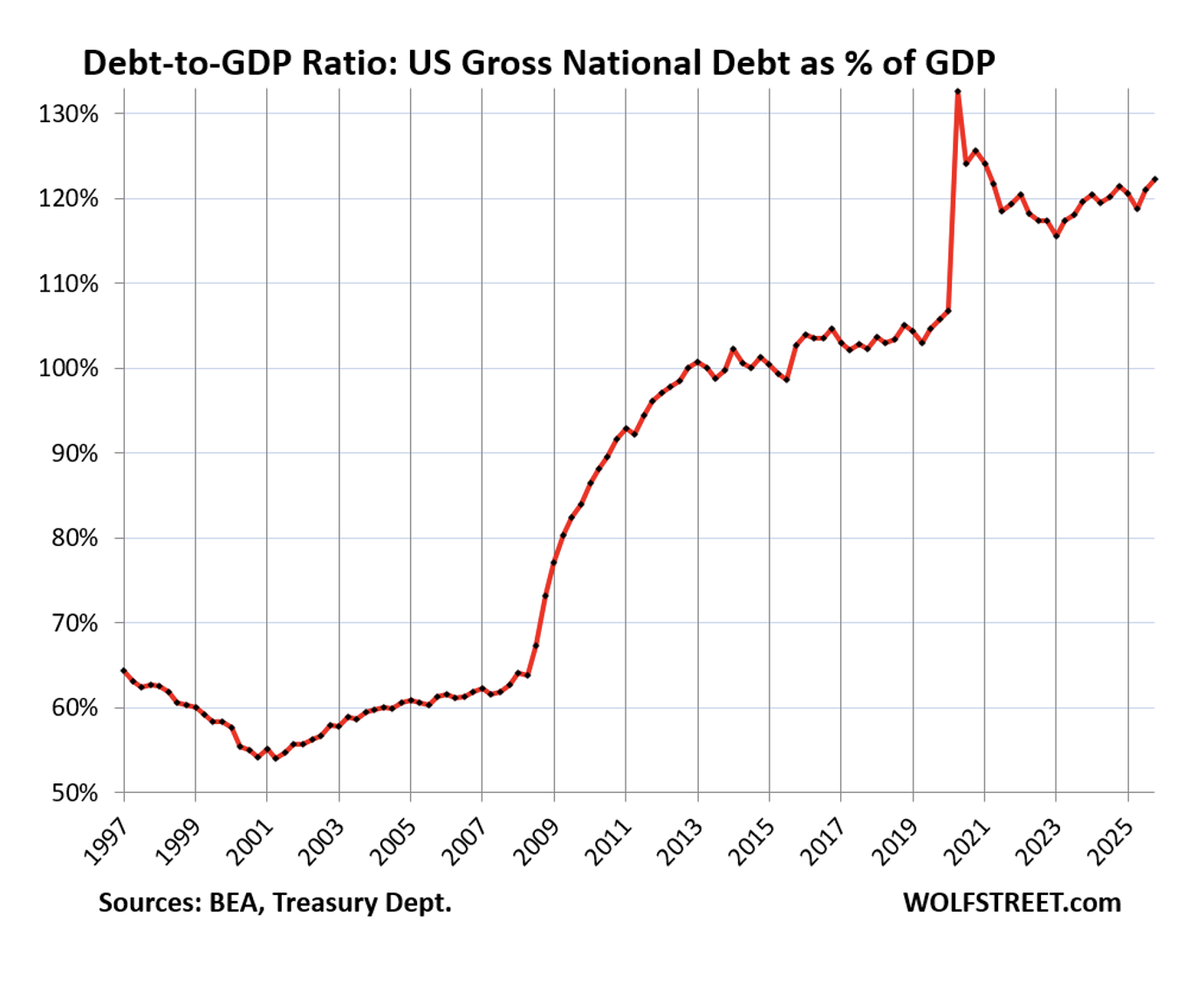

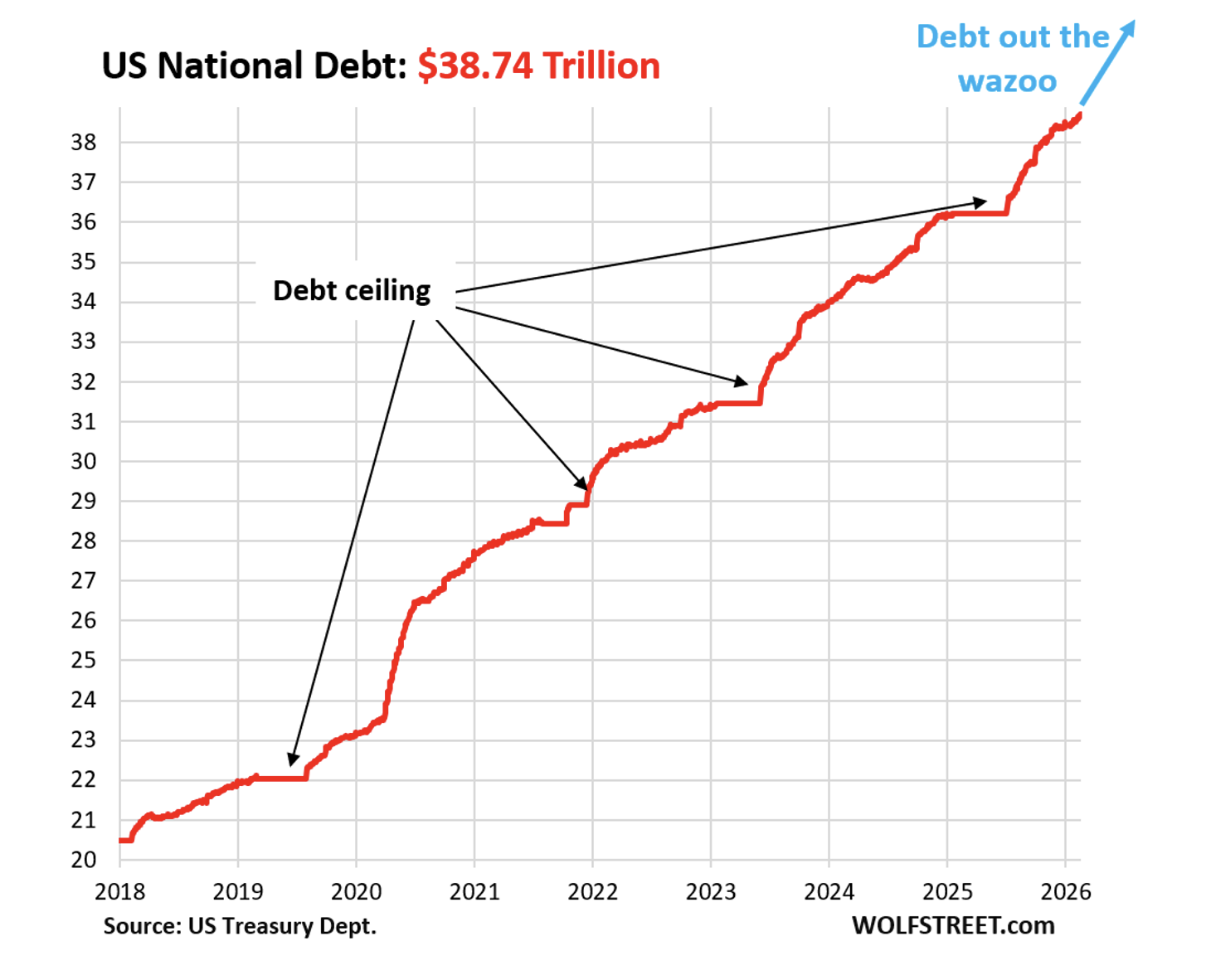

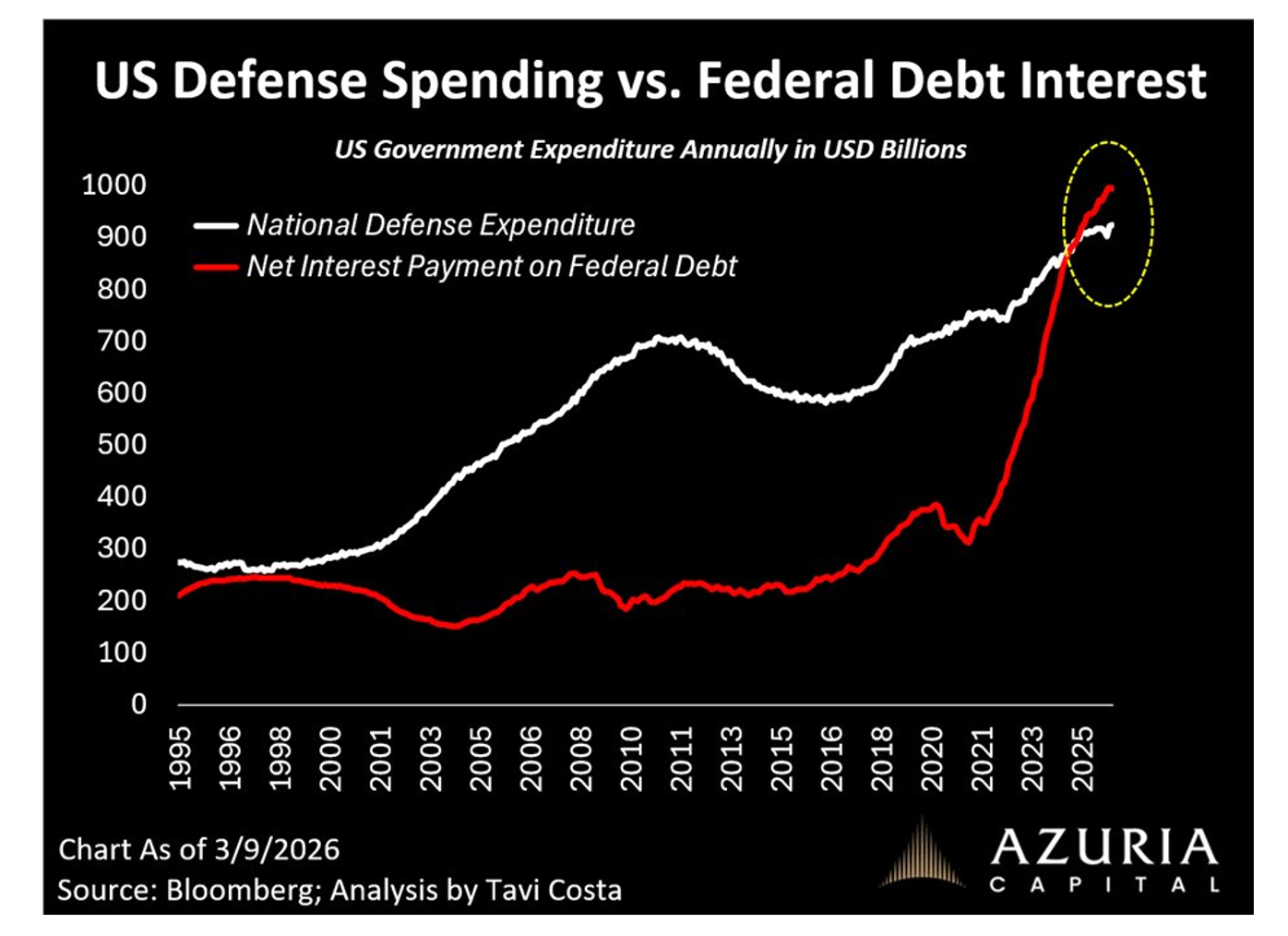

* An Uncontained National Debt and U.S. Deficit.

The war with Iran will ultimately be resolved. From an intermediate-term standpoint it is the cost and amount of U.S. debt that represents a growing existential threat:

* The Federal Reserve's Hands Are Tied: The Fed is now in something of a box as it needs to pay attention to the rise in the core PCE price index (of 3.1% and far from its 2.0% target) — especially with so much fiscal stimulus in the economy (government deficit spending, tax cuts for companies and individuals, bigger tax refunds to consumers now during tax-refund season, massive corporate investments in anything related to AI, too-low interest rates, and too narrow spreads.

Inflation feeds on these combined conditions.

Be Greedy When Others Are Fearful?

While the major indices are down only modestly from all-time highs, many equities are down in excess of -25%.

Until recently, we have seen a Bull Market in Complacency, as over the last year, fear and doubt have left Wall Street.

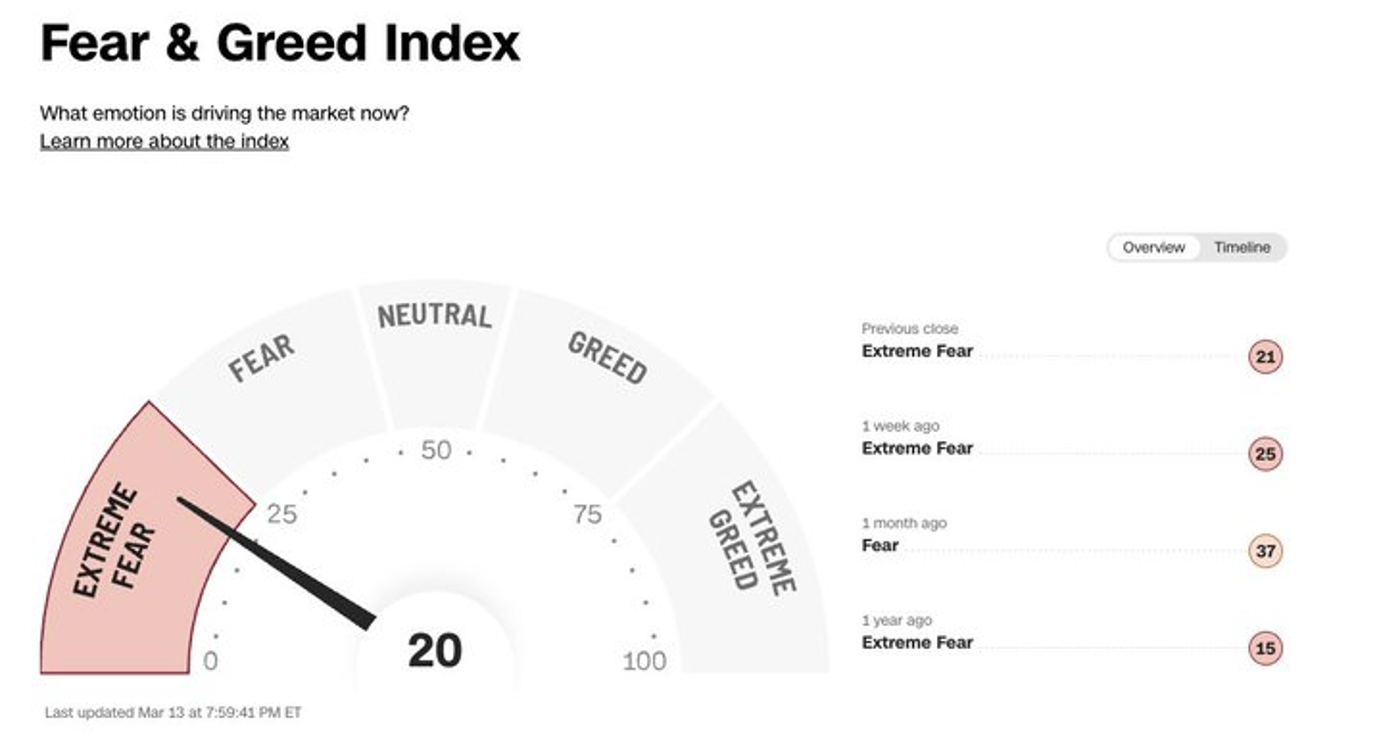

Over the last two weeks, fear has risen sharply and sentiment has flipped negative (as measured by The Fear & Greed Index, the Oscillators (S&P Short Range Oscillator (07.87%) and the Overbought/Oversold Oscillator), and the surveys (Investors' Intelligence, AAII, and NAAIM):

The Investors’ Intelligence Bulls have dropped off to 49% (compared to 63% in early February):

But what has caught our eye has been the large surge in bears — now at 21.8%, the highest reading since last summer:

Joining in the pessimism of the Investors' Intelligence survey, is the AAII survey. The AAII folks joined the Investors’ Intelligence folks (shown here yesterday) in pulling back their horns. Like Investors' Intelligence, AAII bulls stayed mostly steady but the bears shot up by eleven points to 46%:

Following the previous surveys, the NAAIM survey also suggests that bulls are falling and bears rising. In December, their exposure was just over 100 (on margin). Now it’s down to 67, which is the lowest since the panic low of April 2025. Again, not extreme, but finally some movement off that complacency we were in for so long:

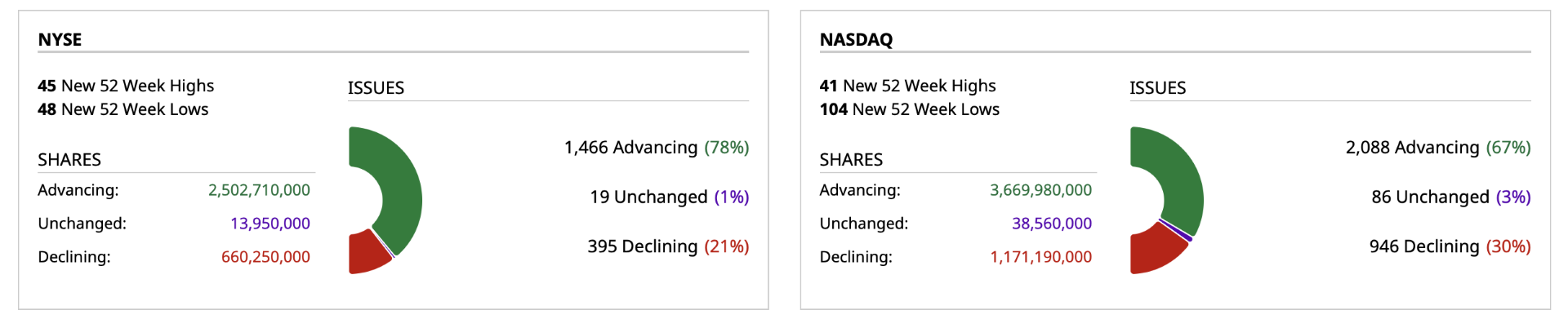

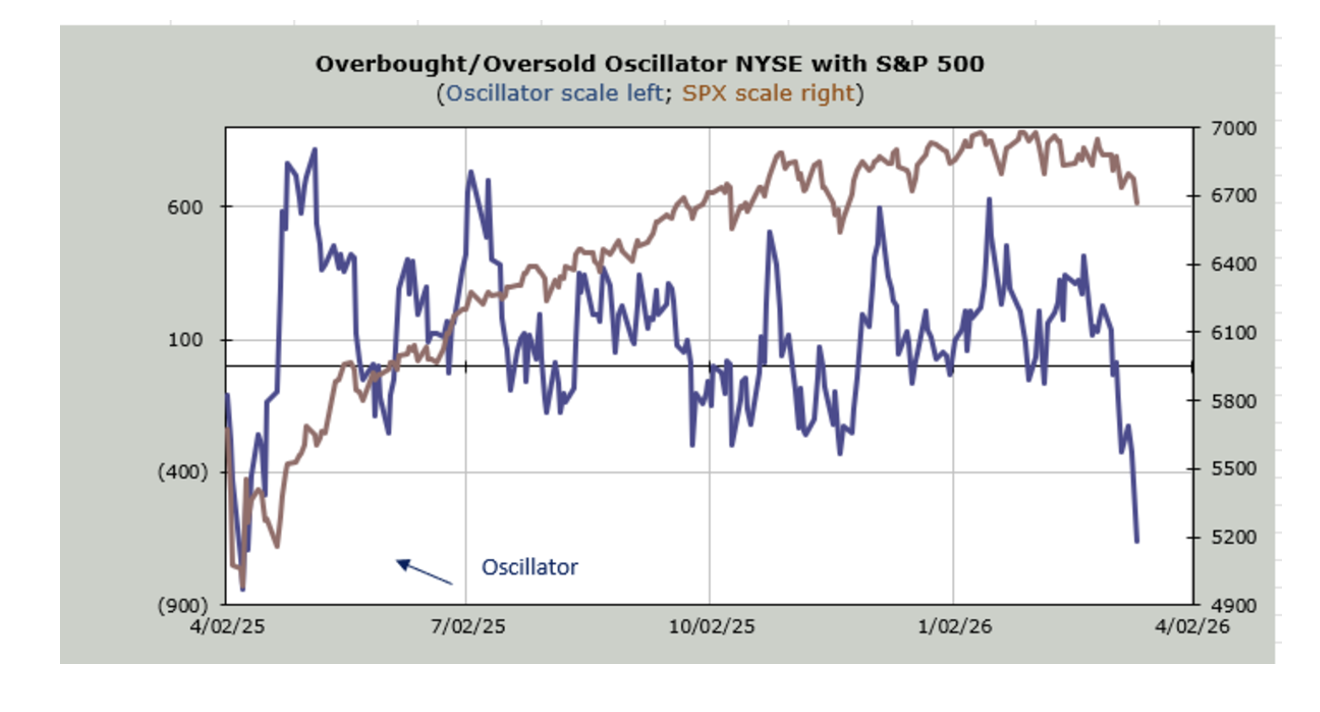

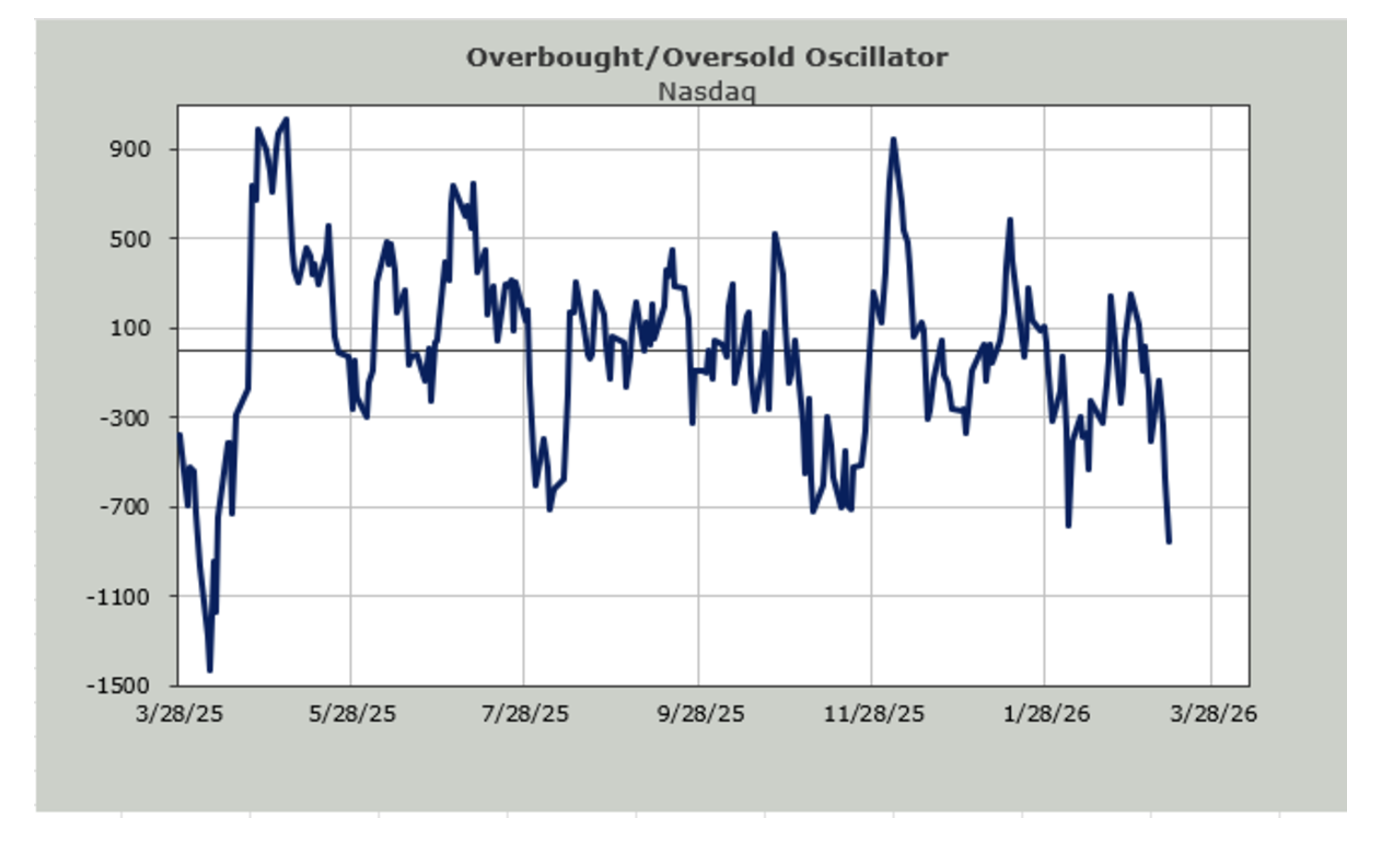

The Overbought/Oversold Oscillator is now nearing the April 2025 lows. (So is the S&P Short Range Oscillator reading near new oversolds). The last six trading days’ breadth has been red. And for seven out of eight, it has been red.

Here is the NYSE Overbought/Oversold Oscillator:

Here is the Nasdaq Overbought/Oversold Oscillator:

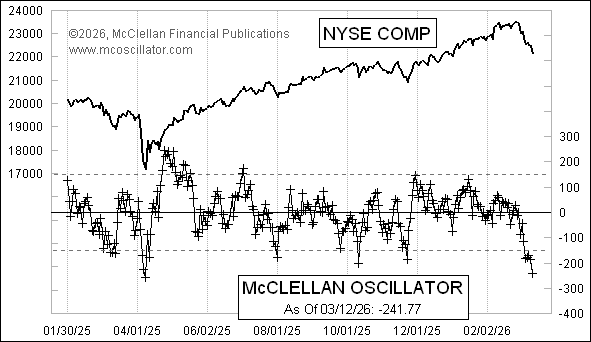

Finally, the NYSE’s McClellan Advance/Decline Oscillator has reached its most oversold levels since last April:

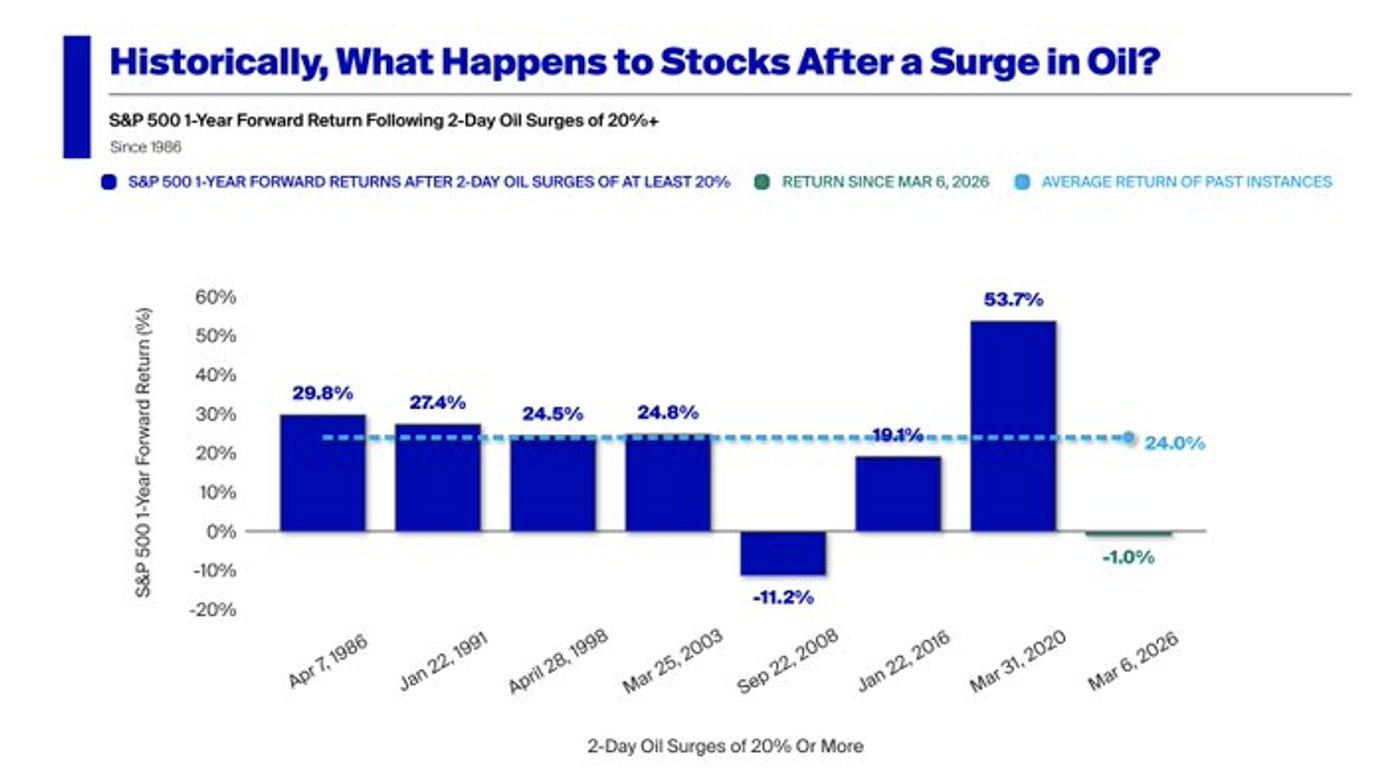

The War in Iran is Frightening But It Will Likely Create Investing Opportunities

Baron Nathan's Rothschild's quote (mentioned earlier) has some historical weight, as equities usually respond smartly to conflicts that lead to a surge in oil.

There have been eight oil shocks in the last four decades. In seven of those instances, equities were higher one year later, with an average gain of +24%:

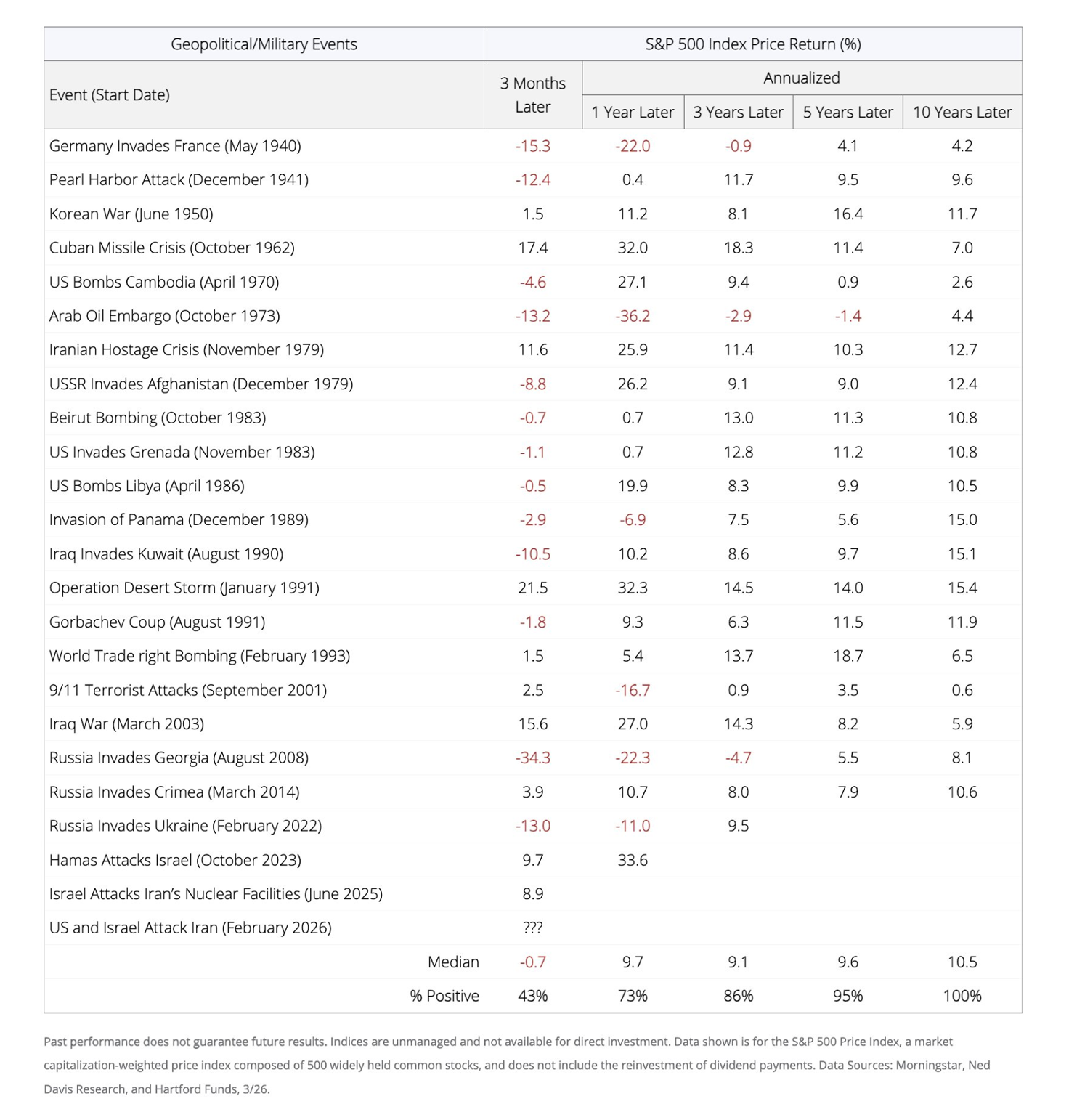

According to Harford Funds, equities generated positive performance 12 months after an act of aggression for 73% of the armed conflicts since World War II:

Bottom Line

I have always written that being short protects capital and being long creates capital.

For some time, I have operated defensively at my hedge fund.

Let me make it clear that I am in no rush to buy stocks. But I do plan to move slowly away from defense and towards more offense as sentiment has eroded, positioning has moved far more conservative and many of our concerns are now being acknowledged ("second-level thinking").

Importantly, the war in Iran has rapidly transformed investor optimism to investor pessimism as sentiment and stock prices have fallen.

Coincident with lower stock prices, investors are beginning to acknowledge our fundamental concerns and some investment opportunities have now emerged.

Warren Buffett emphasized that investing requires rational, cold, "no-emotion" decision making, rather than reacting to market fear or greed, to achieve long-term success in the quote below:

"Until you can manage your emotions, don't expect to manage money."

So, as always, I will approach emerging long opportunities dispassionately and with a calculator in hand — calculating upside reward vs. downside risk while adopting the "margin of safety" principle in all of our buys.

-ULY +163% (Agero enters into agreement to acquire Urgently for $5.50/shr cash; earnings)

-CTMX +56% (Varsetatug Masetecan (EpCAM PROBODY ADC) continues to demonstrate positive data supporting potential as a new treatment option in late-line Colorectal Cancer; earnings)

-DSGR +28% (reportedly receives bid from LKCM)

-NSA +28% (Public Storage to Acquire National Storage Affiliates in all stock transaction EV value of $10.5B)

-NBIS +14% (signs new AI infrastructure agreement with Meta; Meta to pay as much as $27B over the next five years for access to AI infrastructure of Nebius)

-TLS +12% (earnings, guidance)

-GPCR +9.6% (reports positive topline data from Phase 2 ACCESS 2 Trial with Once-Daily Oral Small Molecule GLP-1 Receptor Agonist, Aleniglipron)

-SOC +7.6% (resumes Oil Flow as Ordered by the Federal DPA with Expected Gross Oil Rate of 50,000 Bbls/d)

-COGT +7.3% (US FDA accepts Bezuclastinib NDA in patients with NonAdvanced Systemic Mastocytosis (NonAdvSM) with Dec 30, 2026 PDUFA date)

-POET +6.3% (strategic collaboration with LITEON Technology)

-MSTR +4.8% (momentum)

-RDW +4.7% (awarded prime contract for Belgium's first national security satellite)

-LITE +4.6% (Marvell and Lumentum to Demonstrate Optical Circuit Switching for Next-generation AI Scale-up Infrastructure)

-UPST +4.2% (BTIG Raised UPST to Buy from Neutral, price target: $43)

-MU +3.9% (reportedly plans second manufacturing facility in Taiwan)

-SMPL +3.9% (Jefferies Raised SMPL to Buy from Hold, price target: $22)

-META +3.0% (Meta signs new AI infrastructure agreement with Nebius; Meta to pay as much as $27B over the next five years for access to AI infrastructure of Nebius)

-SAIL +2.7% (signs strategic collaboration agreement with AWS to secure agentic AI with a unified identity governance layer)

#Iran War Update No. 16 (focus on Iranian strategic narrative):

🔹The economic fallout of the war is becoming clearer. According to Bloomberg estimates, if the Strait of Hormuz remains closed for around two months, Qatar and Kuwait could see GDP contractions of up to 14%, while…

This is astounding... I can't believe that the line of sight of business is double.. I can't believe how many doubt this man. A trillion dollar book of business.. And that's blah? That's nothing? That's some yawner?

BREAKING: The US Treasury budget deficit jumped +225% MoM in February, to $308 billion.

Over the first 5 months of FY2026, US deficit is now at $1.00 trillion, the 3rd-worst start to a year in history.

This is only below $1.05 trillion seen in 2021 and $1.15 trillion in 2025.Show more

#Iran War Update No. 16 (focus on Iranian strategic narrative):

🔹The economic fallout of the war is becoming clearer. According to Bloomberg estimates, if the Strait of Hormuz remains closed for around two months, Qatar and Kuwait could see GDP contractions of up to 14%, whileShow more

OPEX

@t1alpha

"Friday also marks the March monthly options expiration, which is historically one of the largest of the year. From a market structure perspective, expirations can be significant events as stale contracts expire and fresh positioning is rolled into the next month