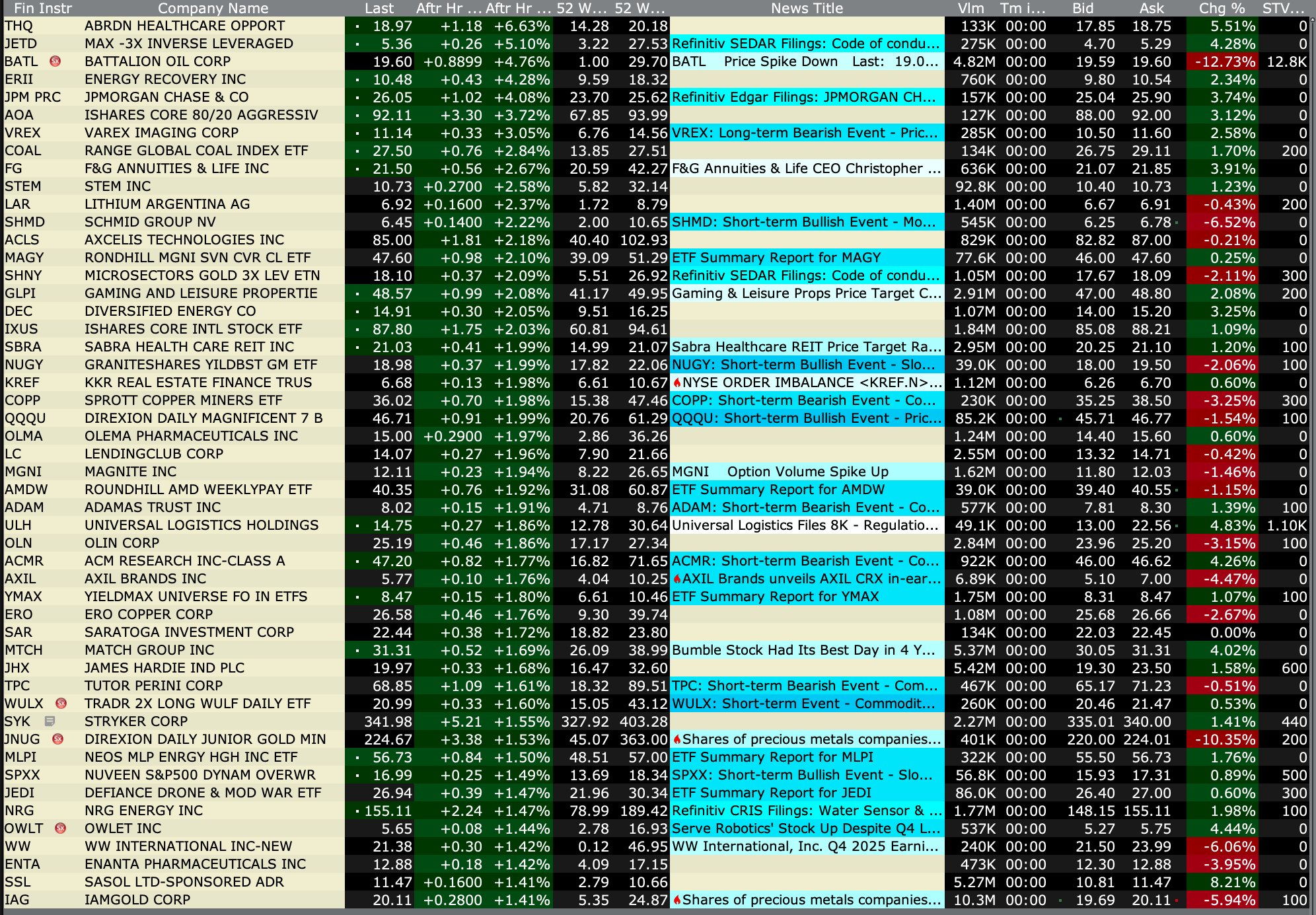

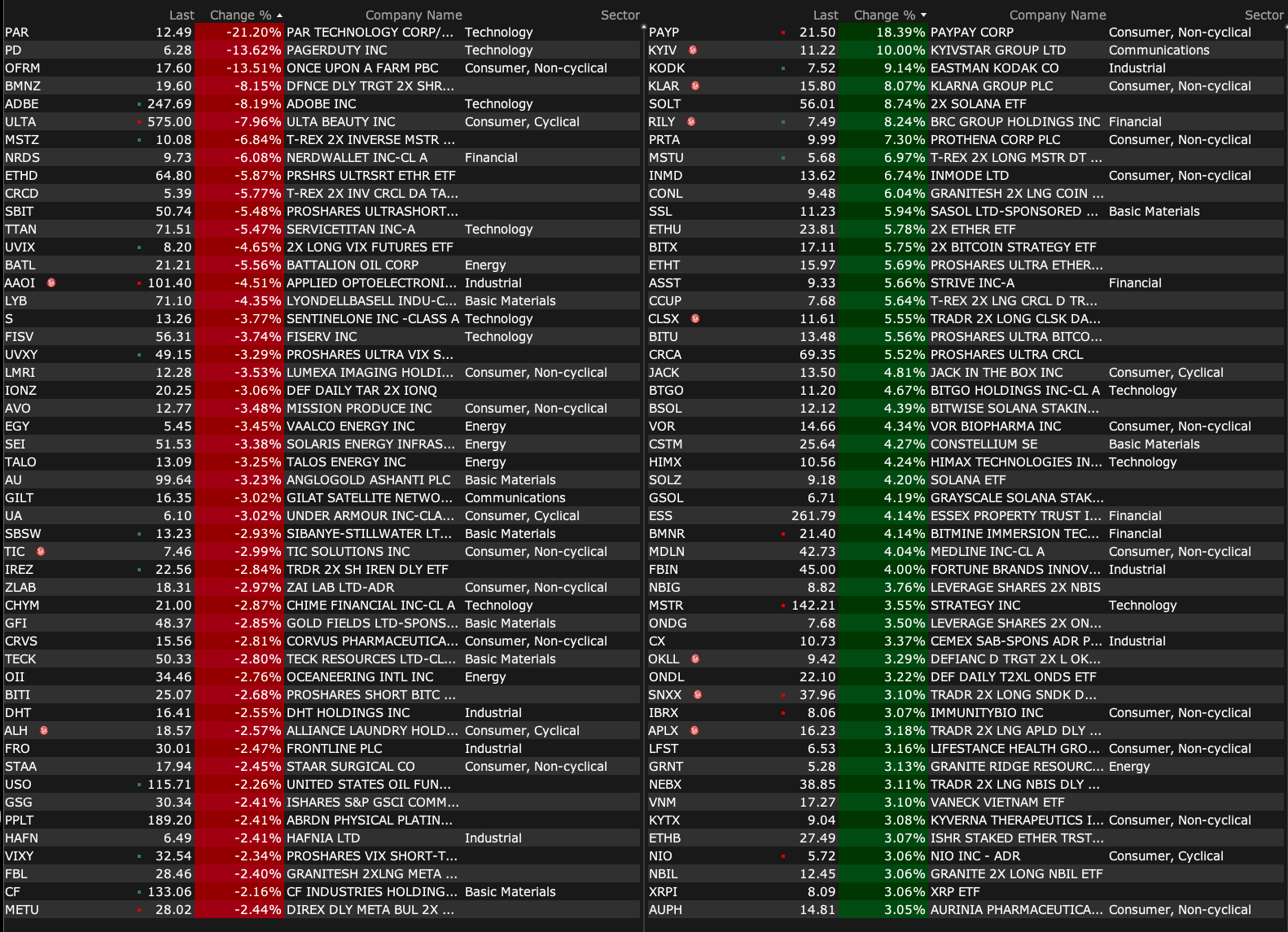

Friday's After-Hours Advancers and Decliners

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Mar 13, 2026, 4:45 PM EDT

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Mar 13, 2026, 4:45 PM EDT

Closing Volume

- NYSE volume 7% below its one-month average

- NASDAQ volume 6% below its one-month average

- VIX index: down 0.33% to 27.20

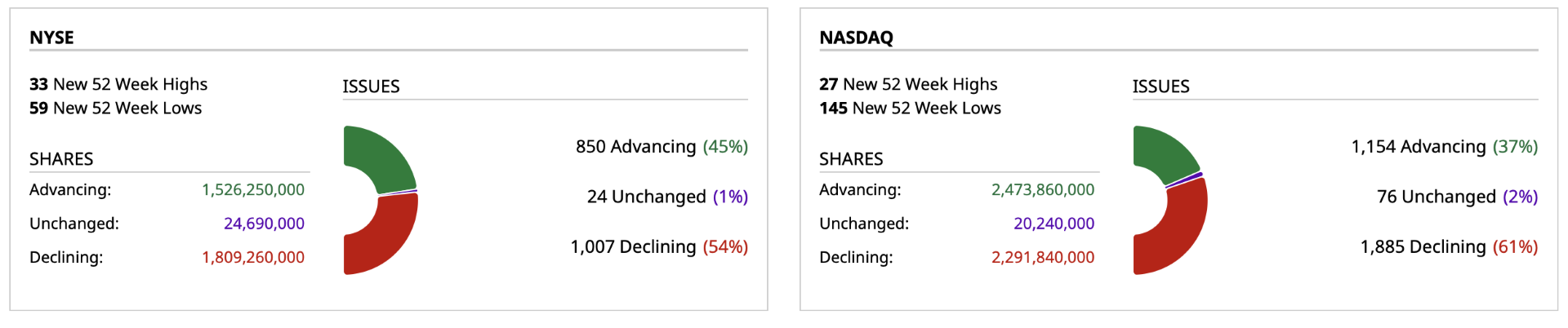

Breadth

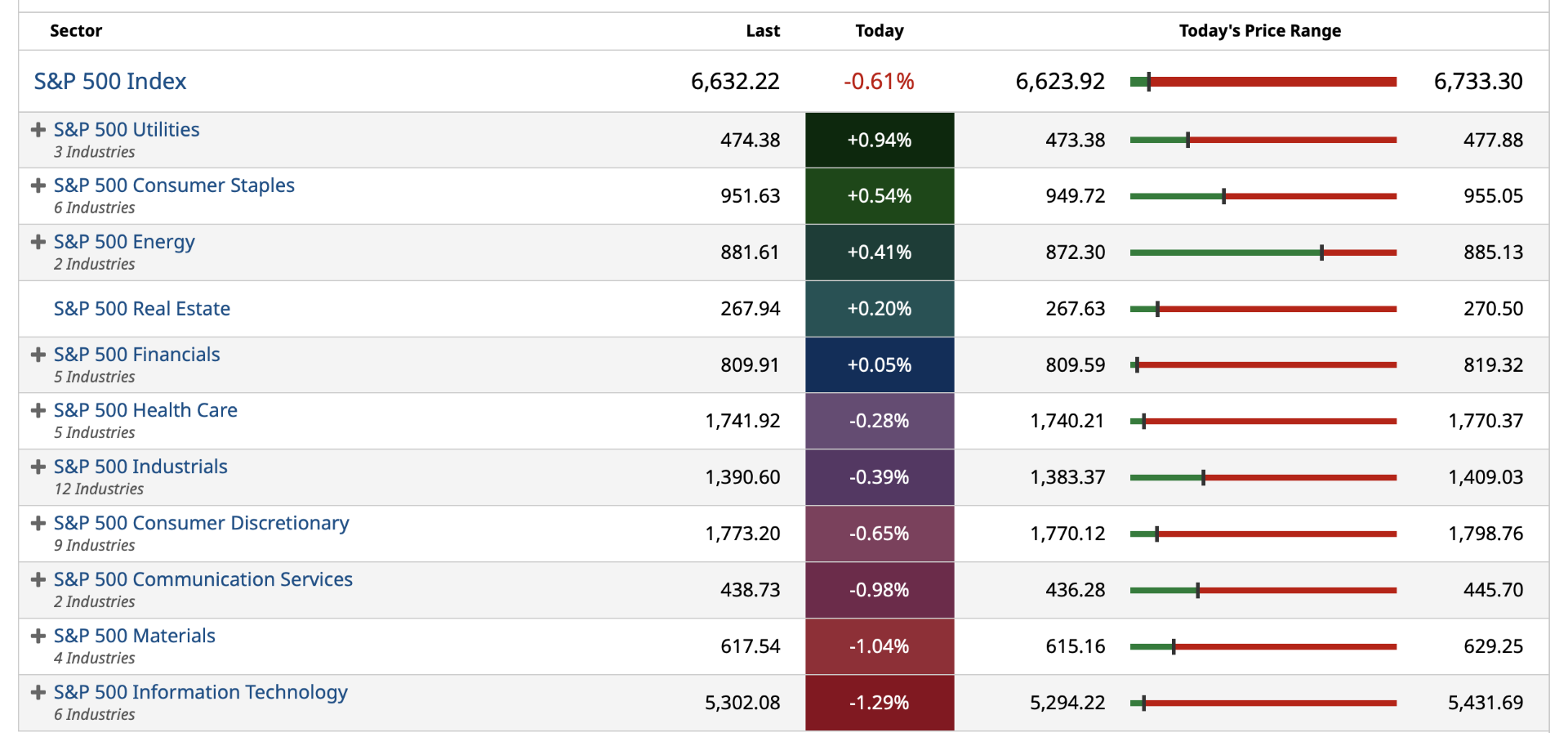

S&P 500 Sectors

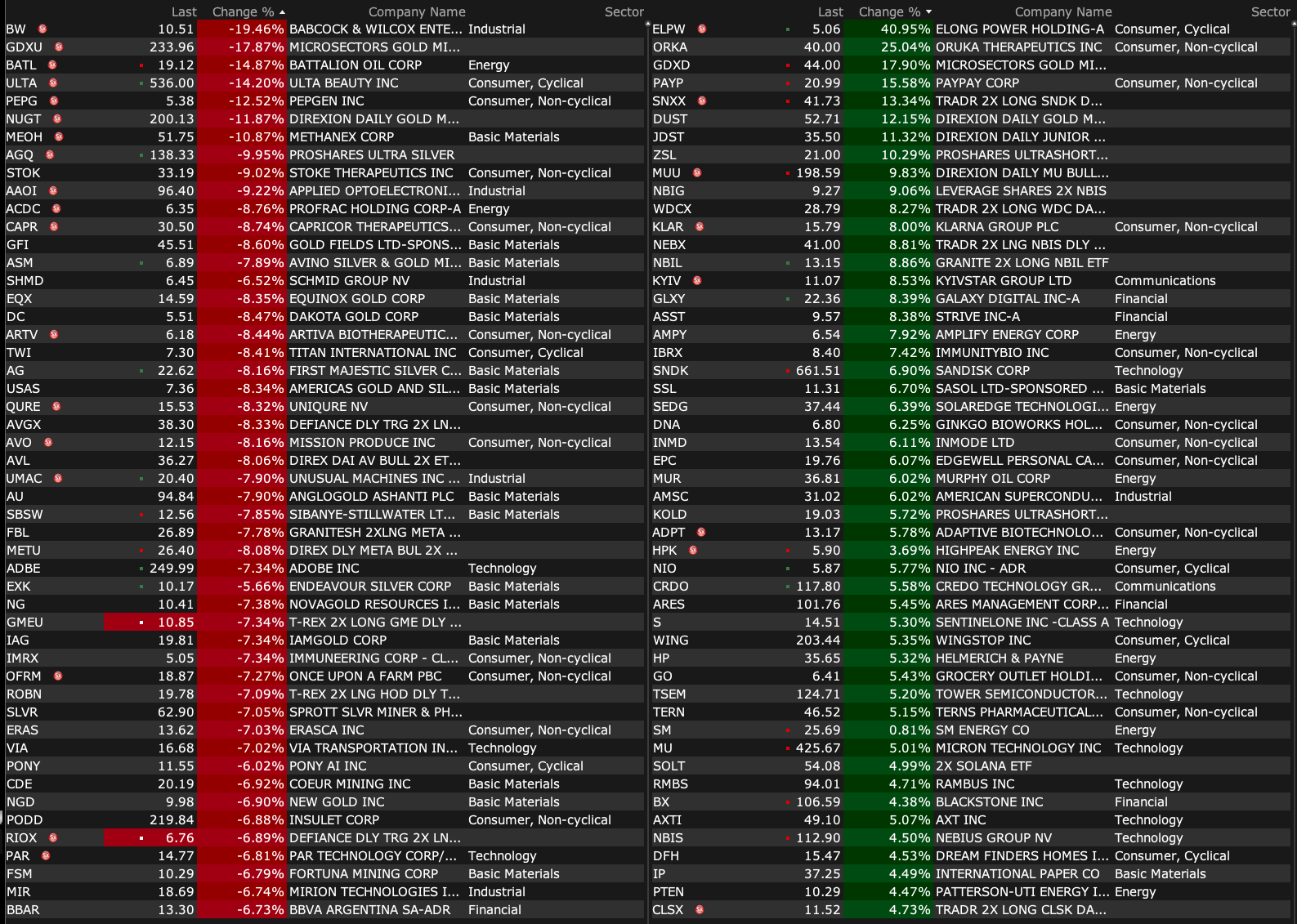

% Movers

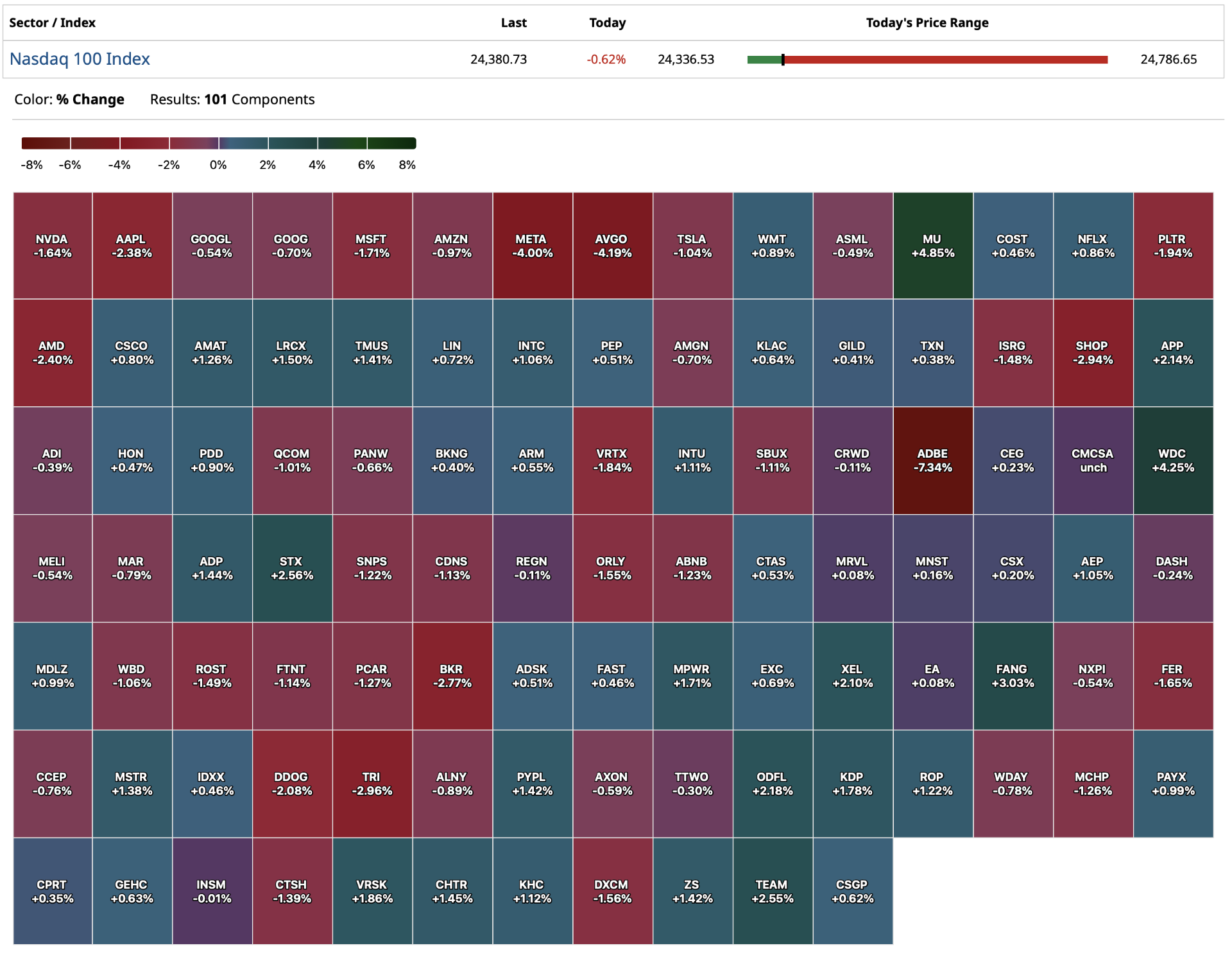

Nasdaq 100 Heat Map

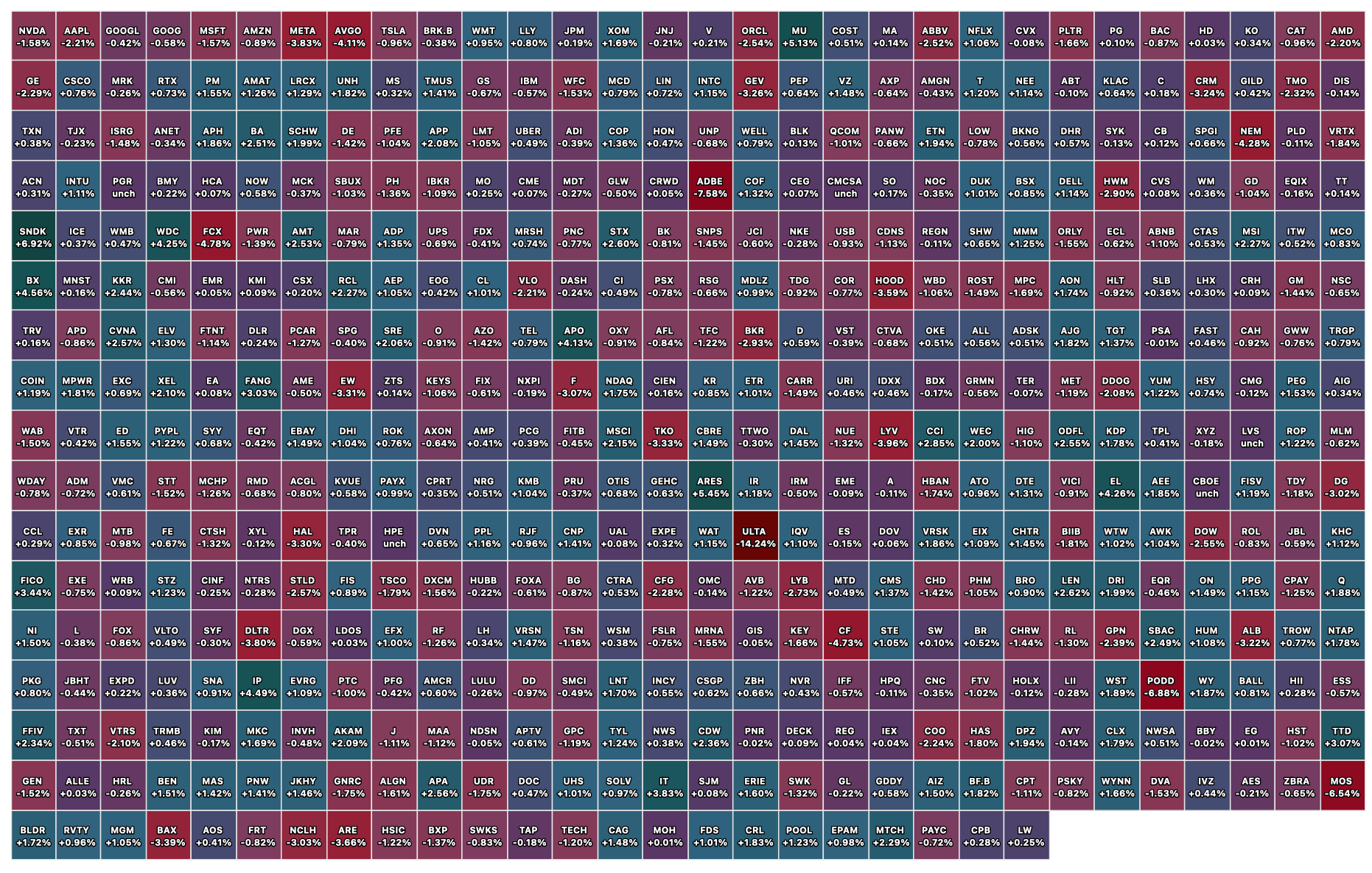

Closing S&P 500 Heat Map

BY Doug Kass · Mar 13, 2026, 4:32 PM EDT

The Dales Report interviews Verano management.

🤔 What are most significant moves Verano made in 2025 that don't show up in the numbers?

— The Dales Report (@TheDalesReport)

▶️ $VRNO @veranobrands Chief Investment Officer Aaron Miles @_AaronMiles_

🎦 WATCH the full interview: https://t.co/wgBN0x5A2F

🌿 ETFs: 🌎 $YOLO 🇺🇸 $MSOS

📈 $SPY $QQQ $IWM #FinTwit pic.twitter.com/LZG8nAzaE9

I have been an active buyer of Verano all week...

BY Doug Kass · Mar 13, 2026, 3:10 PM EDT

As we approach the close of trading I wanted to repost a column I wrote a few days ago which summarized my principal market concerns.

This column, Stocks Still Between Highly Overvalued And Pornographically Overvalued, continues to ring true (as it focuses on a number of factors that have concerned me for quite a while):

Below is a summary of some recent commentary to my Seabreeze Partners (hedge fund) investors and other observations made in my Diary.

In anticipation of a market correction/bear market I have substantially bolstered my cash position recently in order to take advantage of the possible developing long opportunities. (Meanwhile, I am trading more aggressively from the short side than I have in a while.)

Most people know that Michael Burry bet and profited against subprime in 2008 - it became known as the Big Short (and a movie was even made out of his experience.). But fewer people know what happened before the payoff. For two years, Burry's Scion Capital was bleeding -- as his trade/investment was under water. His Limited Partners threatened lawsuits. His founding backer, Joel Greenblatt, flew across the country to call him a liar. Burry was forced to "side-pocket" his subprime trades, locking up withdrawals in order to survive. He refused to let anyone leave even as the fund's losses mounted. His partners stopped speaking to him. Then the market broke. Scion ultimately made about $725 million and his investors saw +489% total return. Burry was a genius, but six months earlier, he was nearly out of business. The lesson is the cost to hold. Being early and being wrong feel exactly the same; until they don't.

Most people don't survive the "until." (Ultimately Burry shut down his Fund because managing human emotion during the wait was too painful). I have felt like Michael Burry over the last 18-20 months as our ursine market outlook did not match the market participants' enthusiasm and robust investment returns. The difference, of course, between Seabreeze Partners and Scion Capital is that while being negative in view, we have managed risk well (as for 25 of the last 26 months our Partnership has delivered a positive investment return).

Over the last two years I have made the case that the markets have materially underpriced risk - that there is a broad and growing list of possible market and economic outcomes that are market unfriendly. I continue to hold to this view. Fundamentally, our concerns continue to be justified:

* Geopolitical risks are multiplying. (The recent attack on Iran is illustrative of this concern as the most immutable rule of war is the law of unintended consequences.)

* A period of disappointing economic growth and persistent inflation lie ahead: As you all know by now I call this "slugflation." (Recent hot inflation coupled with the rise in crude oil are supportive of this view.)

* I remain skeptical about the circular financing of massive AI projects as well as the likelihood of generating adequate returns on that capital investment. (The MAG7 and peripheral companies represent a large portion of the S&P Index.)

* The private equity and debt markets are deteriorating. (See my Surprise List where I highlighted the risk in Apollo, KKR, Blackstone and the others). From earlier in the week:

Remember when the panelists on the shows (especially Slink, Drawdown, Belski et al) universally said an important reason why they were bullish were paper thin credit spreads - that is, there was no systemic risk?

What were they doing in the market to reflect that view - they were buying private equity and credit stocks at or near their highs. Those stocks (Blue Owl (OWL) , Ares (ARES) , (KKR) , Blackstone (BX) , Apollo (APO) , etc. are now -40% or thereabouts. (Many of these stocks I purchased yesterday after the fall as I rent at the sound of cannons).

You will never hear about these investment boners - that is their way.

That is an example "investment vision being 20/20 when viewed in the rear view mirror" and "first level thinking" -- that I have been so critical about.

Here is an update of widening credit spreads and its upwardly sloped trend - which have taken out 7-8 month base:

By Doug Kass Mar 10, 2026 9:41 AM EDT

* Consensus forecasts for 2026-7 S & P profits are likely too optimistic.

* Neither political party seems to have any fiscal discipline - as measured by our country's growing deficit and ever-expanding debt load.

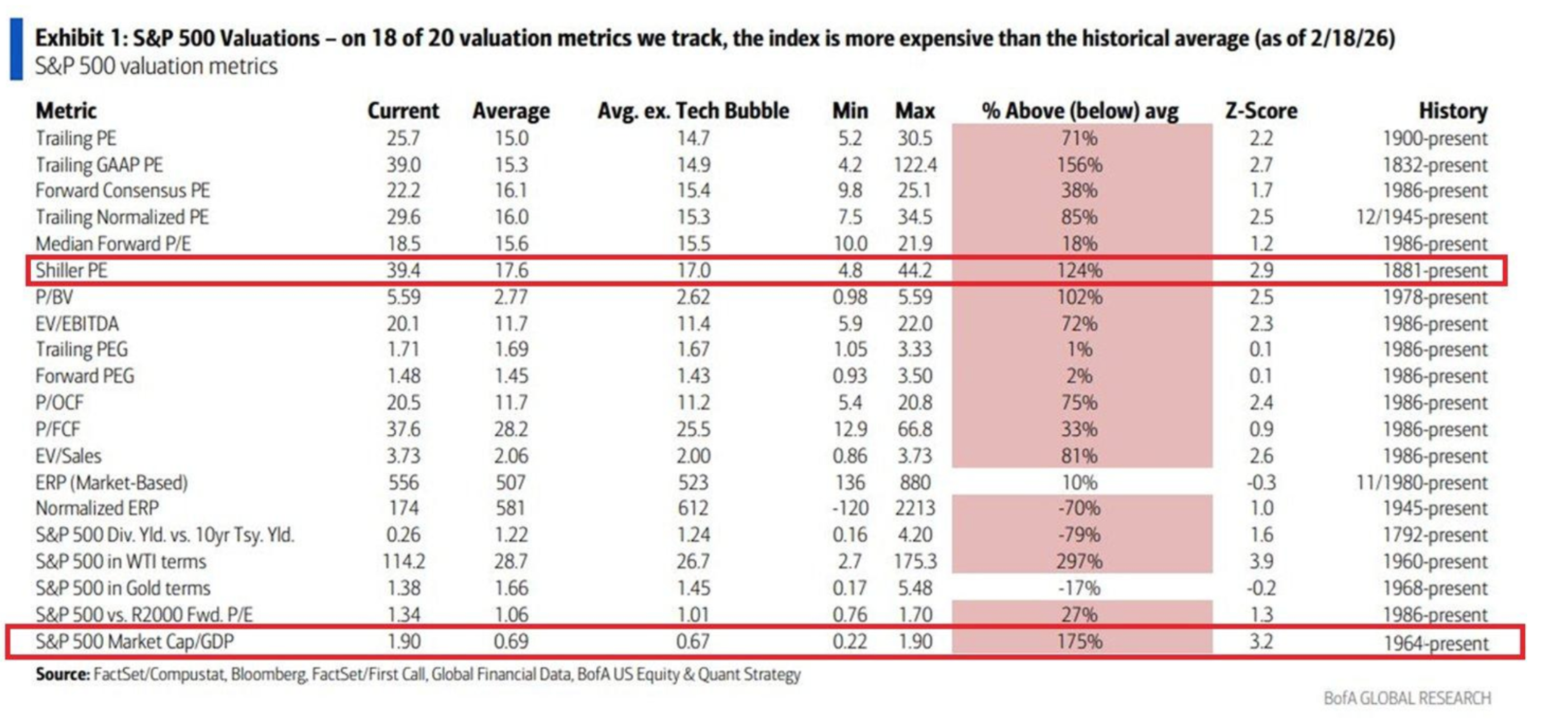

* The equity risk premium has become, for the first time in almost three decades, an equity risk discount. Historically, this is an indicator that current valuations provide a poor launching pad for future returns. It also means that investors believe there is more risk in owning bonds than stocks - truly a foolish (and dangerous) notion. From a valuation standpoint stocks remain somewhere between highly overvalued and pornographically overvalued. Most traditional valuation metrics support this view:

I continue to expect at least a small double-digit decline in the S&P Index this year.

Based on recent events and price action, the correction of the multi-year Bull Market may come sooner than later.

BY Doug Kass · Mar 13, 2026, 3:00 PM EDT

I'm bidding more (MSOS) (common and calls) and MSOX with the objective of moving towards large-sized.

BY Doug Kass · Mar 13, 2026, 2:08 PM EDT

Speaking of surprises.... and my previous post on market structure risks:

With so many positioned on the same side of the (bullish) boat, retail investors begin to liquidate from equity funds - reversing the experience of the last few years. The movie of the last decade (of inflows) goes into reverse in 2026 - its October 1987 (portfolio insurance was to blame) all over again. More than one quarter of the listed ETFs close during the year due to "indifference".

BY Doug Kass · Mar 13, 2026, 1:20 PM EDT

My old pal Brian Wesbury must have been reading my Diary:

Real (inflation-adjusted) consumer spending was up just 0.1% in January. Durable goods orders were flat, and real GDP was revised down to just 0.7% annualized growth in Q4 (remember when people were saying it would be over 5%?).

— Brian Wesbury (@wesbury)

The stock market has been flat since September.

We…

From my Surprise #1 (10 Surprises for 2026):

A recession in 2027 appears likely.

Equities (led by the Magnificent Seven tech stocks) succumb to slowing economic and corporate profit growth, the reappearance of inflation, questionable foreign and domestic policy, growing political uncertainties, emerging "problems" for the hyperscalers (as AI capital spending plans are reduced) and elevated valuations.

The K-shaped economy's weakness in the lower income cohort spreads into the middle and upper middle class as the cumulative (or stacked) inflation since Covid finally has an impact -- causing a spending freeze. With the outlook for global economic growth dissipating, consumer and business sentiment plummets. BNPL and credit defaults rise and auto repossessions increase dramatically.

Drawdowns in the global equity markets and a moribund housing market contribute to a negative "wealth effect" and an air pocket with the high end consumer as the investor optimism of 2023-25 is abandoned.

There is no place to run, no place to hide - most asset classes fall in the 2026 Bear Market.

BY Doug Kass · Mar 13, 2026, 1:07 PM EDT

Scott Galloway's No Mercy/No Malice:

BY Doug Kass · Mar 13, 2026, 12:53 PM EDT

BY Doug Kass · Mar 13, 2026, 12:05 PM EDT

* Are debts about to be settled?

* Is there impending doom?

I have warned about the perils of market structure for several years.

I sense (in watching the renewed volatility) that the dominance of passive products and strategies (who worship at the altar of price momentum) could now come home to roost with so many on the same side of the market's (long) boat.

Expect wild intraday swings — in both directions.

My advice would be to keep your portfolio's VAR (value at risk) low by adjusting position sizes lower.

Of course The Ides of March in the Roman calendar is at the middle of the month — a deadline for settling debts. It was also the date of Julius Caesar's assassination in 44 BC (immortalized by William Shakespeare).

The soothsayer had warned Caesar of The Ides of March — a famous warning of impending danger and, possibly, betrayal.

The Ides of March, March 15, looms ahead (on Sunday).

Et tu, Brute?

Et tu, Mr. Market?

BY Doug Kass · Mar 13, 2026, 11:33 AM EDT

Chart from 10:57 a.m. ET.

BY Doug Kass · Mar 13, 2026, 11:25 AM EDT

From Peter Boockvar:

Before I get to the confidence data and January job openings, after seeing the Q4 GDP data, growth averaged about 2% in 2025 and the Q4 ‘25 vs ‘Q4 ‘24 growth rate was also 2%. In light of everything thrown at it, meaning the tariff barrage and on and off use of them, 2% is pretty good but we know how bifurcated the contribution was with data center buildouts in particular making up almost half of that growth.

Again, with the January PCE inflation stats, we’ve already seen February CPI and a war since so the January data is very old news.

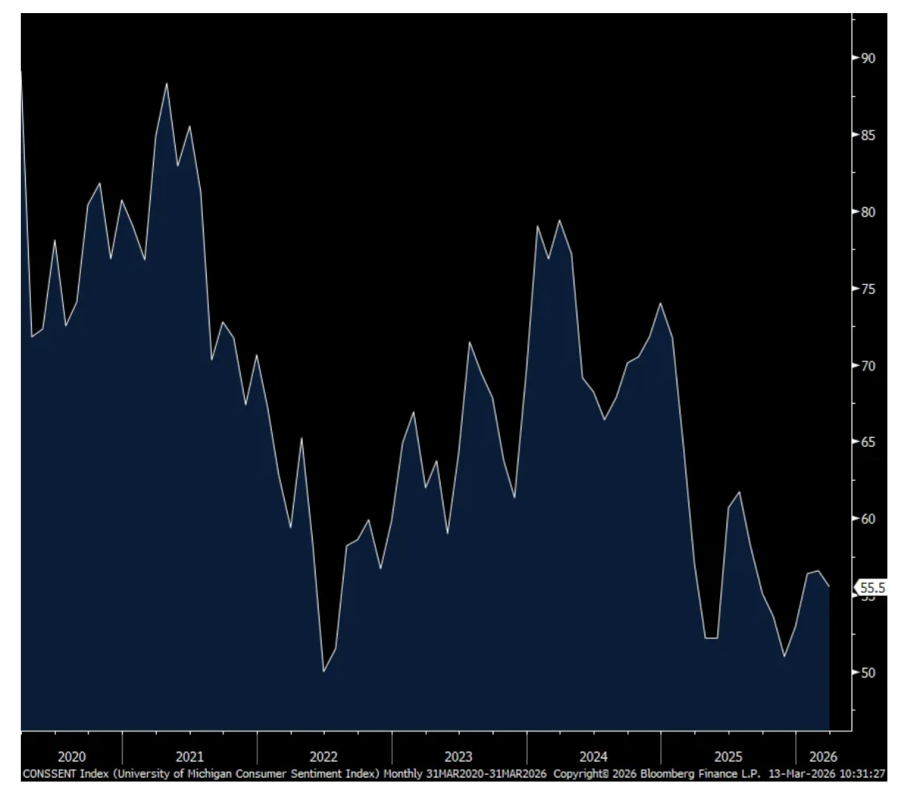

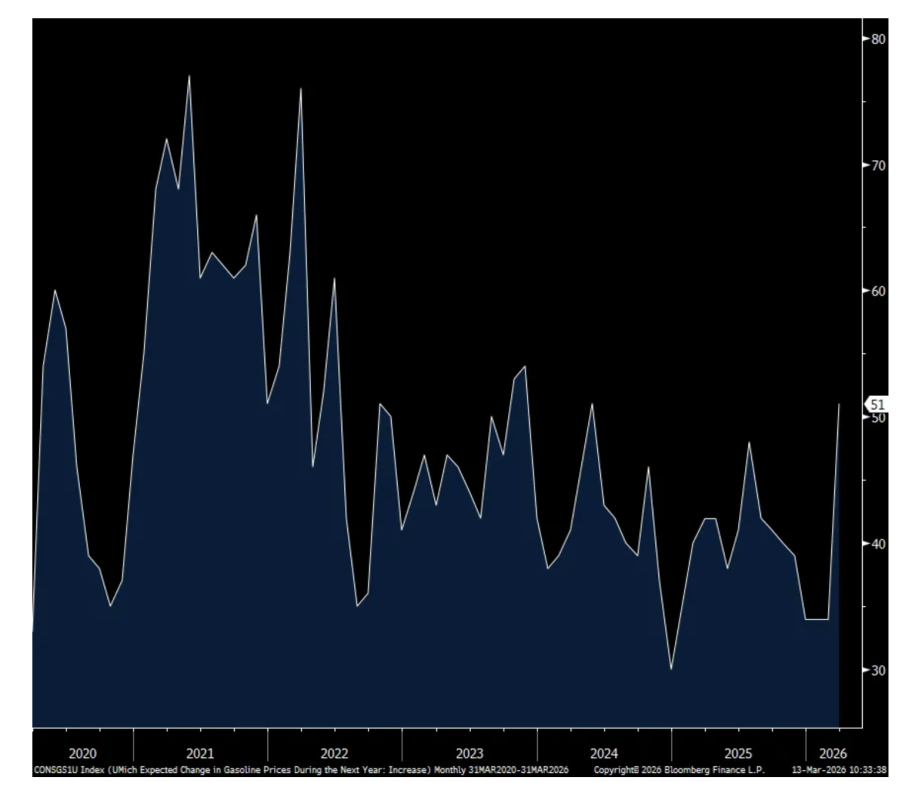

Reflecting some answers pre and some post the start of the war, March consumer confidence from the UoM did slip a modest 1.1 pts from February to 55.5 and that was a bit better than the estimated 54.8. The internals were mixed as Current Conditions were up while Expectations fell. One year inflation expectations did not lift with the sharp rise in gasoline prices, yet. They held at 3.4% and the 5-10 yr guess fell by one tenth to 3.2%. So maybe the belief that prices in other things will trend lower offsetting the rise in energy prices and the filtering thru to other things that came from that. On gas prices specifically, seeing the obvious, those that say they are going up jumped to 51 from 34.

I want to emphasize that last point because the impact from higher energy prices directly via gasoline prices and/or heating cooling bills is not just a percent of income thing only with gasoline prices because energy prices impact so many other things (transportation, packaging, clothing, etc…) and takes time to flow through if sustained.

The UoM said, “Note that for both time horizons, interviews completed after February 28th exhibited higher inflation expectations than those completed before that date.” Of course no surprise there.

Also from them, “Indeed, inflation uncertainty, as measured by the middle 50% of expectations, also surged after the start of the Iran conflict. These trends likely reflect uncertainty over how the conflict will evolve and the ensuing volatility seen in oil markets. As such, the relatively limited initial response in median inflation expectations may well grow as the conflict continues.”

The employment component fell 2 pts but after rising 5 pts last month. The income component was still negative but improved by 5 pts to -2.

With respect to spending intentions, they were mixed, rising for vehicles and major household items and falling slightly for homes.

As part of the survey was taken place before the war and the balance after, this is what UoM said, “Interviews completed prior to the military action in Iran showed an improvement in sentiment from last month, but lower readings seen during the nine days thereafter completely erased those initial gains. Gasoline prices have exerted the most immediate impact felt by consumers, though the magnitude of passthrough to other prices remains highly uncertain.”

UoM

Expected Change in Gasoline Prices

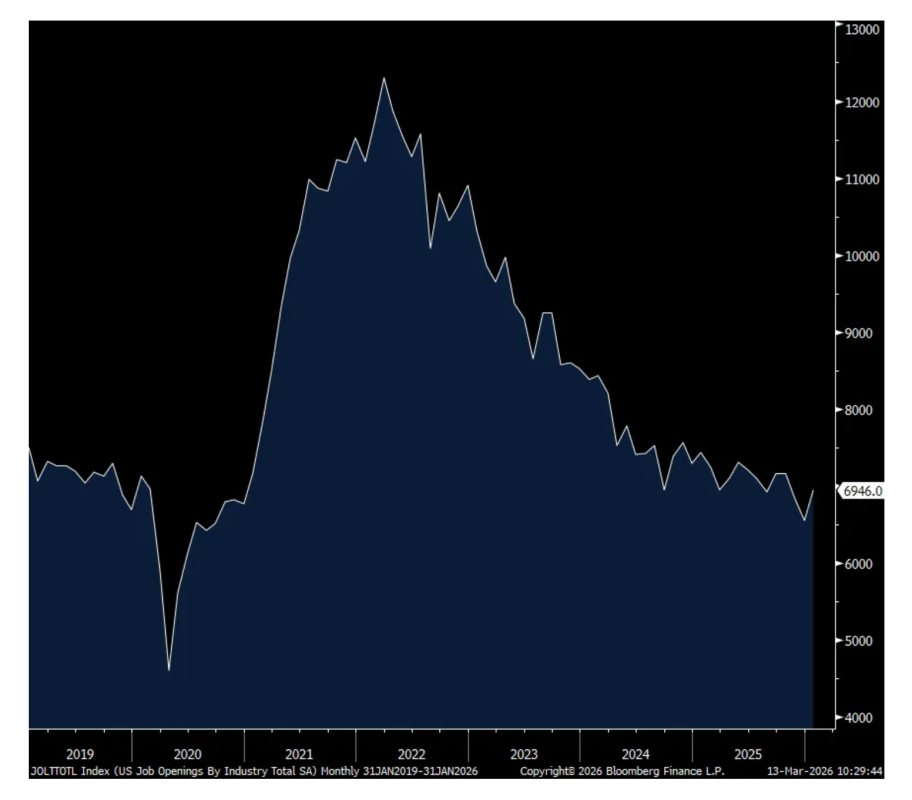

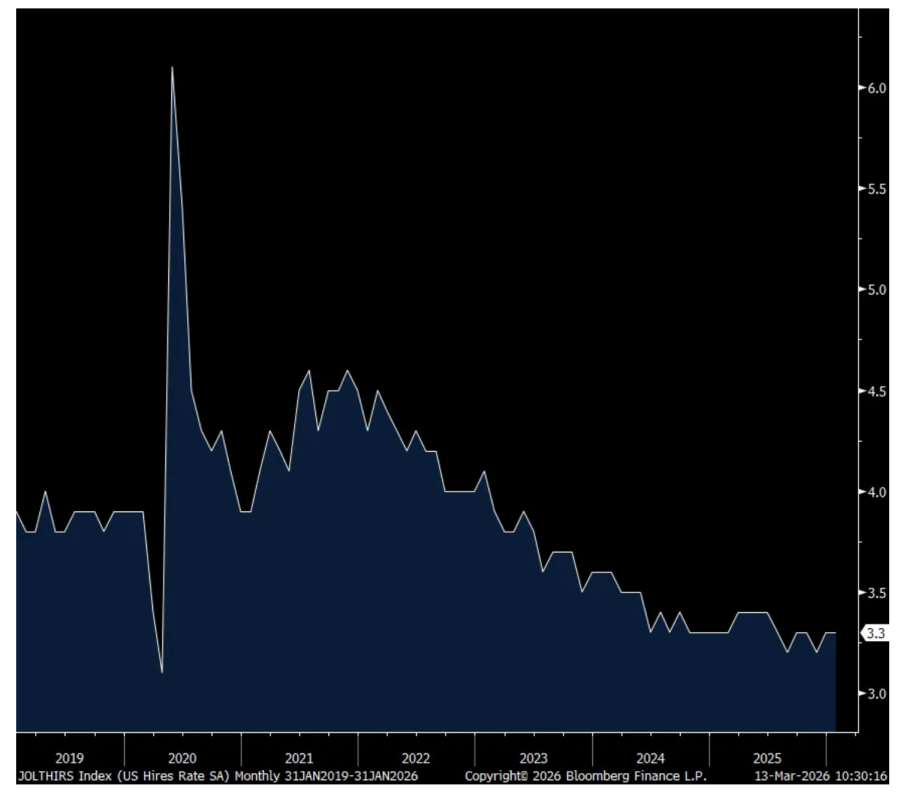

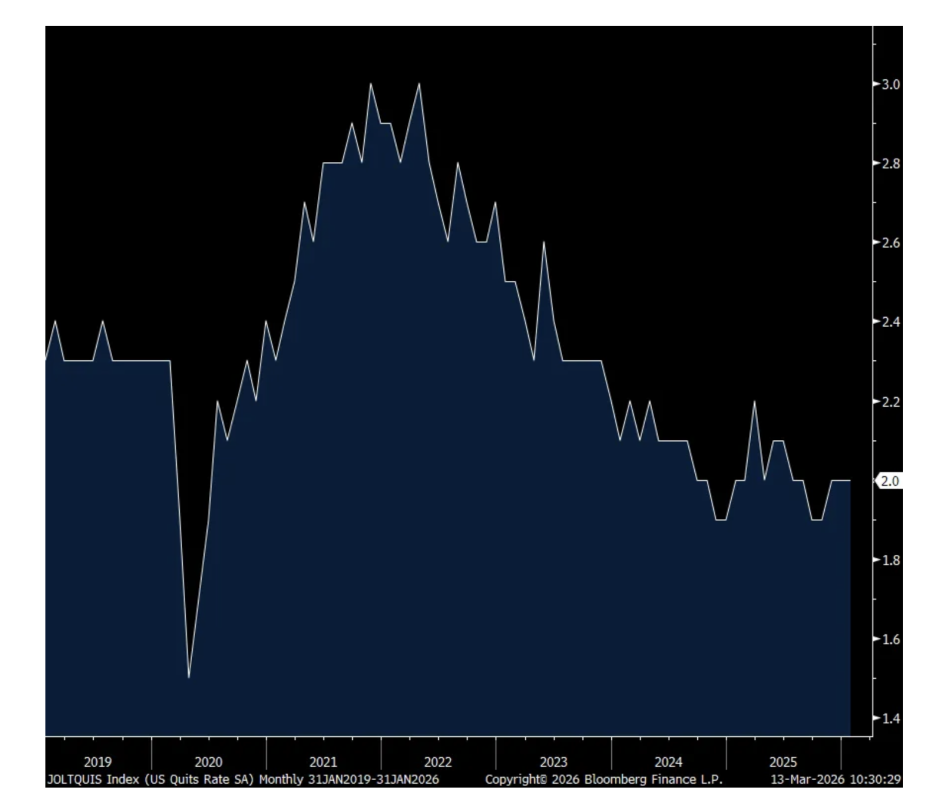

January job Openings, also somewhat dated data but always is when it is released, totaled 6.946mm, rebounding from the drop to 6.55mm in December which was the least since 2020. The hire rate though still remained low at 3.3% while the quit rate held at 2%. I believe we’re pretty clear on the state of the labor market right now with the muted pace of firing’s and the notable slowdown in hiring’s, with a combination of supply and demand factors there.

Job Openings

hiring rate

Quit Rate

BY Doug Kass · Mar 13, 2026, 11:20 AM EDT

NYSE volume is 5% below its one-month average;

Nasdaq volume is 13% below its one-month average;

VIX index: down 6.52% to 25.51

BY Doug Kass · Mar 13, 2026, 10:54 AM EDT

I took a profit in (JPM)

(sold at $286.17(+$3.26) as I would like to concentrate on other banks.

BY Doug Kass · Mar 13, 2026, 9:59 AM EDT

The largest financial hurdle (that I previously feared) facing the cannabis industry has been successfully leapt over by most of the multi-state operators.

Over the last several months Verrano, Green Thumb, Trulieve, TerrAscend, Curaleaf and others have refinanced their debt with credit facilities at very attractive interest rates (9.5% to 11.5%) and have extended maturities:

* Green Thumb Green Thumb Industries Announces an Additional $50 Million Senior Debt Financing

* TerrAscend TerrAscend Completes $79 Million Non-Dilutive Debt Financing | Cannabis Business Times

I view the refinancings (above) as an underappreciated factor facing cannabis investors — suggesting that the industry's share price outlook has measurably improved.

BY Doug Kass · Mar 13, 2026, 9:30 AM EDT

-PAYP +22% (strength following IPO)

-KLAR +7.5% (Chairman insider buy)

-INMD +6.4% (authorizes ~6.4M share buyback)

-NIO +3.5% (HSBC Raised NIO to Buy from Hold, price target: $6.80)

-TNXP +3.4% (earnings)

-RBRK +2.1% (earnings, guidance)

-KLC -34% (earnings, guidance)

-PAR -22% (prices upsized $250M of 4.00% convertible senior notes due 2031)

-OFRM -15% (earnings, guidance)

-TBCH -15% (earnings, guidance)

-PD -13% (earnings, guidance)

-ADBE -8.2% (earnings, guidance)

-ULTA -8.1% (earnings, guidance)

-PODD -4.7% (initiates Voluntary Medical Device Correction for Certain Omnipod 5 Pods in the U.S.)

-S -3.8% (earnings, guidance)

BY Doug Kass · Mar 13, 2026, 9:09 AM EDT

*From Liz Ann....

AAII bull-bear spread down to -14.5% as pessimism continues to rise at a relatively quick pace pic.twitter.com/KtHFJt2pJW

— Liz Ann Sonders (@LizAnnSonders)

BY Doug Kass · Mar 13, 2026, 8:55 AM EDT

France and Italy are reportedly trying to negotiate a deal with Iran.

That explains the whoosh higher.

I sold all of my Index common on the move:

* (SPY) $670.50

* (QQQ) $601.49

BY Doug Kass · Mar 13, 2026, 8:52 AM EDT

BY Doug Kass · Mar 13, 2026, 8:45 AM EDT

BY Doug Kass · Mar 13, 2026, 8:35 AM EDT

From Peter Boockar:

Keep in mind that today’s PCE inflation stats along with income, spending and also the release of durable goods are all January data. With inflation specifically, we saw the CPI for February last week so this is all old news, especially with what has happened over the last few weeks.

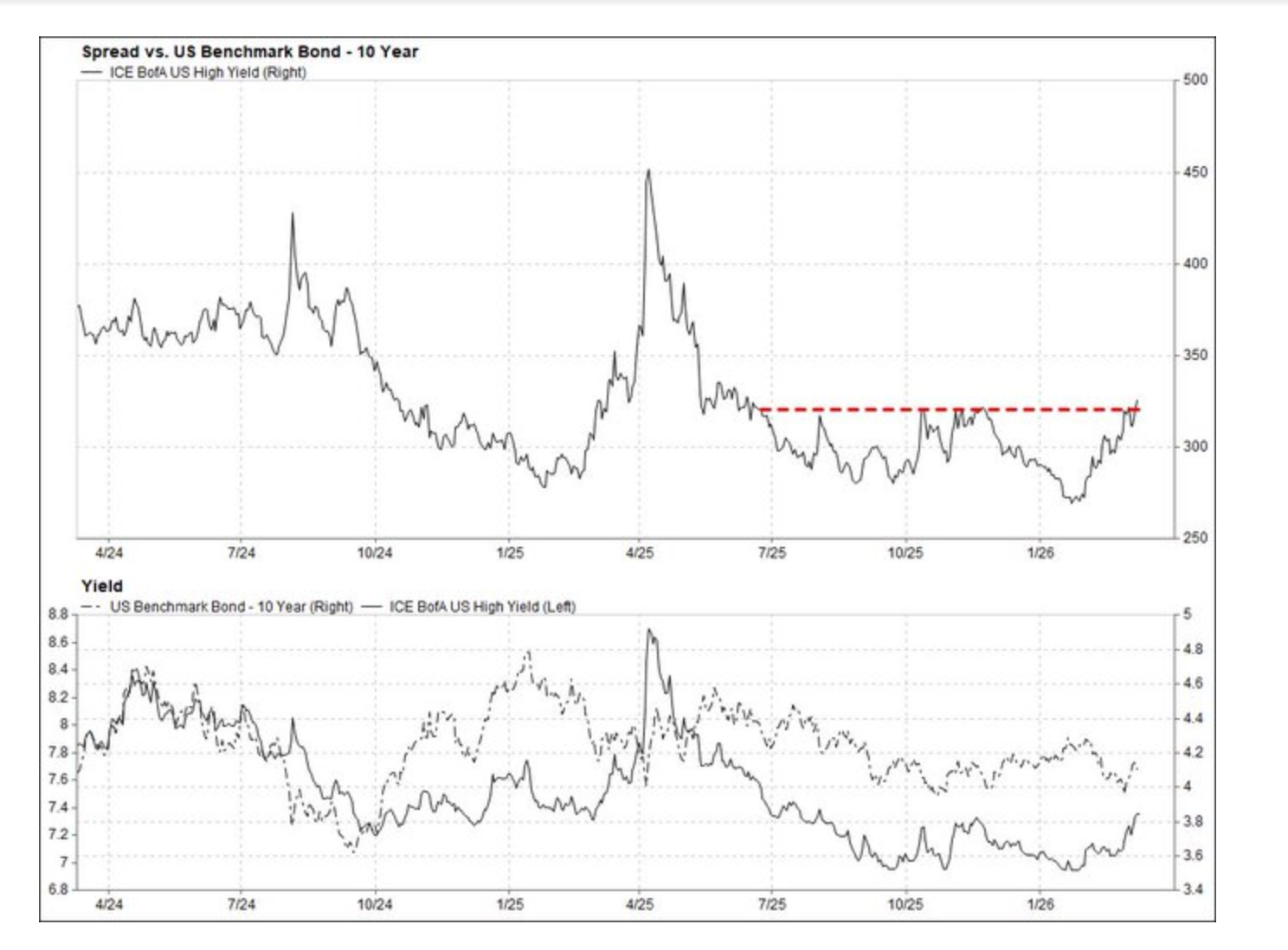

With the heightened focus on what is going on in private credit, I keep watching to see if there is any spillover into high yield. While there has been a lift off the lows in spreads, it still remains near the multi year bottom at just under 300 bps.

High Yield Spread to Treasuries

Right to some earnings call highlights and great insight into the US consumer.

From Dick’s Sporting Goods, up 1% yesterday in a tough tape:

The Dick’s business saw comps up 3.1% in Q4 as “We saw more athletes purchase from us and they spent more each trip compared to the prior year.” The comps “were driven by a 4.4% increase in average ticket, partially offset by a 1.3% decrease in transactions.”

“In terms of the category performance, we saw broad based strength across our three primary categories of footwear, apparel and hardlines.”

“we’re finding that consumers are doing very, very well. So we have seen growth across all income demographics. We haven’t seen trade down and we’re finding that when a consumer sees something that’s new or innovative or technically impactful, it’s resonating with them and they are coming. And we think that’s only going to continue as we look to the year and the incredible excitement around sport and the influence it has on culture as we head into the World Cup coming up, well, March Madness and then the World Cup. So we’re really, really confident.”

Comps for Foot Locker fell 3.4% in Q4.

From Dollar General, down 6% yesterday:

“We grew market share in both dollars and units in highly consumable product sales once again during the quarter. In addition to growing market share in non-consumable product sales.”

“Same store sales increased 4.3% during the quarter, and included healthy growth in customer traffic, as well as average basket size. The growth in average basket was driven by an increase in average unit retail price per item, partially offset by a decrease in average number of items.”

They “feel good about that comp, and I would tell you the drivers, real quickly, really its value, value, value at this point.“ I bolded to emphasize.

“From a monthly cadence perspective, while January was the strongest period of the quarter, and included a benefit from consumer stock-up activity ahead of winter storms, all three periods delivered comp sales growth above 3.5%.”

“we finished 2025 with three consecutive quarters of meaningful growth in customer traffic, reflecting the essential role we play for our customer and communities as we help them save time and money every day. Customers across all income brackets continue to stress the importance of finding value as they shop and we are meeting this need as we continue to grow penetration with households of all income levels.”

From El Pollo Loco, the Mexican restaurant and whose stock fell 2% yesterday:

“In Q4, we delivered a positive quarter of same store sales growth including stable traffic despite the ongoing macroeconomic challenges that persisted across the industry.” Comps grew .4% y/o/y with “a 2.7% increase in average check size, partially offset by a 2.3% decrease in transactions.”

“During the fourth quarter, our effective price increase versus 2024 was about 3.2%...We expect commodity inflation to be in the 1% to 2% range for the full year 2026.” I guess that assumes corn and wheat prices don’t go up much from here. They expect wage inflation this year of 2-3%.

They are now getting more in tune with the protein craze. “We further capitalized on the macro trend by launching our version of a protein menu which is a collection of menu items with more than 20 grams of protein.”

On their customer, “So the consumer is still looking for great food at a great value. So wanting to have a meal that is healthy, better for them, quality ingredients, all indulgent at times, but wanting to do it within their budget. So certainly more budget conscious. So we’re seeing that we’re able to serve that for the consumer...in Q4 we saw the consumer responding to value particularly with our burrito bowls and with some of our offers in our app and then also with third party delivery.”

Ulta Beauty is trading down pre market after a lower than expected guide. From their call:

“Throughout 2025, we closely monitored consumer behavior and observed continued resilience, a strong focus on value and affordability, and increasing discernment in spending decisions. At the same time, engagement with the beauty category remained healthy, and the landscape remained competitive. We expect these themes to continue into fiscal 2026, though we are increasingly mindful of rising global conflicts that could impact economic conditions.”

“Absent increased broader macro disruption for the year, our expectation for the beauty category growth is in line with the average historical growth rate, with expected growth in the 2-4% range.”

Comps grew 5.8% “driven by a 4.2% increase in average ticket and a 1.6% increase in transactions. Looking at the cadence of sales through the quarter, comp sales were fairly consistent, reflecting both a strong holiday season and the lapping of softness in January last year. I would note that we did see some impact from the weather at the end of January this year.”

On their 2.5-3.5% comp guidance that is responsible for the stock drop, “We’re cautious about how the consumer demand could evolve given the macro pressures and rising conflicts, but beauty has been a resilient category to these macro pressures. So we see that the beauty engagement is going to continue to be healthy in 2026.”

Also, “There’s no plan for us to accelerate promotion, but it’s going to be competitive out there.”

From Lennar’s earnings release:

“Our first quarter of fiscal year 2026 was defined by the same persistent headwinds that have challenged the housing market for over three years - high mortgage rates, constrained affordability, cautious consumer sentiment, and geopolitical uncertainty, especially now including the recent conflict in Iran.”

“Our average sales price was $374,000, reflecting the continued use of approximately 14% in incentives, along with base price adjustments necessary to sustain volume in a market where affordability remains the defining constraint.”

That is down from $408,000 y/o/y and “was primarily due to continued weakness in the market and an increased use of sales incentives to homebuyers.”

BY Doug Kass · Mar 13, 2026, 8:27 AM EDT

BY Doug Kass · Mar 13, 2026, 8:07 AM EDT

VOLUME: yesterday was Day1 of legit oh shit selling pic.twitter.com/d4ea24pHA1

— Keith McCullough (@KeithMcCullough)

BY Doug Kass · Mar 13, 2026, 7:30 AM EDT

Here are Thursday's (and Friday morning's) things:

* Long indices: (SPY) $671.01 and (QQQ) $603.30. (Evening buys: SPY $666.37 and QQQ $597.35 Friday morning buys: SPY $664.55 and QQQ $595.09)

* Covered short SPY and QQQ calls on whoosh lower on Thursday.

* Initiated buys in (BAC) $47.36, (C) $106.15, (GS) $785.79, (JPM) $281.76, (BX) $104.65, (KKR) $84.85, (APO) $102.95, (MS) $154,97 and (WFC) $75.16

* Purchased (DIS) $99.63

* Added to (MSOS) $3.76 and VRNOF $1.09.

* Added to (AMZN) $209.70.

BY Doug Kass · Mar 13, 2026, 7:15 AM EDT

BREAKING: A record 6.0% of workers in Vanguard-managed 401(k) plans took hardship withdrawals in 2025.

— The Kobeissi Letter (@KobeissiLetter)

This is up from 4.6% in 2024 and has nearly QUADRUPLED since 2020.

Hardship withdrawals have increased for 6 consecutive years, with last year's median withdrawal being… pic.twitter.com/TIB6wh0epK

BY Doug Kass · Mar 13, 2026, 7:00 AM EDT

Chart of the Day: Ethereum

From David Rath (@DJwrath) / X:

Ethereum ($ETH) is attempting to snap its third-longest weekly losing streak on record as it continues to coil within a tight consolidation.

Following a death cross, the last period of digestion resulted in a roughly 45% decline in less than a month.

Crypto has led the downside in risk assets, so a breakout in $ETH could provide an early signal that risk appetite is beginning to recover.

The Takeaway: Ethereum is nearing an inflection point, and its next move could help determine the near-term path for markets.

Chart of the day! Traders may be interested to see all four major averages $SPX, $NDX, $DJX, $RUT with key #MovingAverage Crossovers, as the 20-day MA has dipped below the 50-day MA. Could set up for additional short-term weakness across the broader markets. Not a… pic.twitter.com/Qo5ue32b2y

— Joe Mazzola (@JoeMazzolaCS)

The cost of protection is near the most expensive levels in history.

— Macro Charts (@MacroCharts)

*Is it sustainable? / What happens next? pic.twitter.com/c2ruCJC9SP

This chart keeps deteriorating. The major private equity houses have had their stock prices collectively lopped by more than a third, yet the S&P 500 sits 3% below record highs. Disconcerting. pic.twitter.com/cQwXT1ikKf

— Jeff Weniger (@JeffWeniger)

Oil was still coiled in the low 60s.

— Ricardo Sarraf (@nullcharts)

No one was looking at the fertilizers as they printed a double bottom.

That was back in mid January.

Now they are some of the only sources of strength, as everything else stalls or suffers.

Echoes of mid 2007 and early 2022...

History… https://t.co/KiB2QAxMkW pic.twitter.com/EE4lS8YtLk

Bonus — Here are some great links:

BY Doug Kass · Mar 13, 2026, 6:45 AM EDT

Quite a move in the US yield curve — 2s-10s below (source: Bloomberg). #economy #markets pic.twitter.com/39W9mfdU7X

— Mohamed A. El-Erian (@elerianm)

BY Doug Kass · Mar 13, 2026, 6:35 AM EDT

Another example of people choosing not to hedge when the cost is low and paying up when the need to hedge is obvious. https://t.co/Cgp3gxMmn2

— Scarlett & Carter's BaPa (@KASDad)

BY Doug Kass · Mar 13, 2026, 6:25 AM EDT

The S & P Short Range Oscillator is extremely oversold now — at 7.65% vs. -5.48%.

It might be time to consider some buys (I have been!) if you are comfortable buying a falling knife!

BY Doug Kass · Mar 13, 2026, 6:15 AM EDT

Dougie Kass

6PM Moved up to small sized Index longs:

Dougie Kass

330AM Added:

* SPY $664.55

BY Doug Kass · Mar 13, 2026, 6:05 AM EDT

War continues. I am watching the cross asset class correlations. So far, bond yields and oil have moved together on inflation concerns. But eventually high oil prices are negative for growth. When bond yields fall as oil prices rise it’s a signal of shifting market concerns.

— Kathy Jones (@KathyJones)

BY Doug Kass · Mar 13, 2026, 5:55 AM EDT

#Iran War Update No. 13 (focus on Iranian strategic narrative):

— Hamidreza Azizi (@HamidRezaAz)

🔹Day 13 of the war indicated continued escalation across maritime, energy, and regional fronts, while Iranian officials signaled that the war may be entering a new phase characterized by more asymmetric tactics.…

BY Doug Kass · Mar 13, 2026, 5:45 AM EDT

Real (inflation-adjusted) consumer spending was up just 0.1% in January. Durable goods orders were flat, and real GDP was revised down to just 0.7% annualized growth in Q4 (remember when people were saying it would be over 5%?). The stock market has been flat since September. We Show more

🤔 What are most significant moves Verano made in 2025 that don't show up in the numbers? ▶️ $VRNO @veranobrands Chief Investment Officer Aaron Miles @_AaronMiles_ 🎦 WATCH the full interview: youtube.com/live/bjGyWY5PL… 🌿 ETFs: 🌎 $YOLO 🇺🇸 $MSOS 📈 $SPY $QQQ $IWM #FinTwit

BREAKING: A record 6.0% of workers in Vanguard-managed 401(k) plans took hardship withdrawals in 2025. This is up from 4.6% in 2024 and has nearly QUADRUPLED since 2020. Hardship withdrawals have increased for 6 consecutive years, with last year's median withdrawal being Show more

The cost of protection is near the most expensive levels in history. *Is it sustainable? / What happens next?

Oil was still coiled in the low 60s. No one was looking at the fertilizers as they printed a double bottom. That was back in mid January. Now they are some of the only sources of strength, as everything else stalls or suffers. Echoes of mid 2007 and early 2022... History Show more

Fertilizer stocks tend to move in sync with energy and crude oil. Strip away the noise and it is effectively the same trade. Sometimes oil leads, often times its fertilizers. That is why it pays to watch both trends closely. With crude oil volatility near record lows and