From Peter Boockvar:

What is the per gallon of gasoline price point that destroys demand, according to one operator?

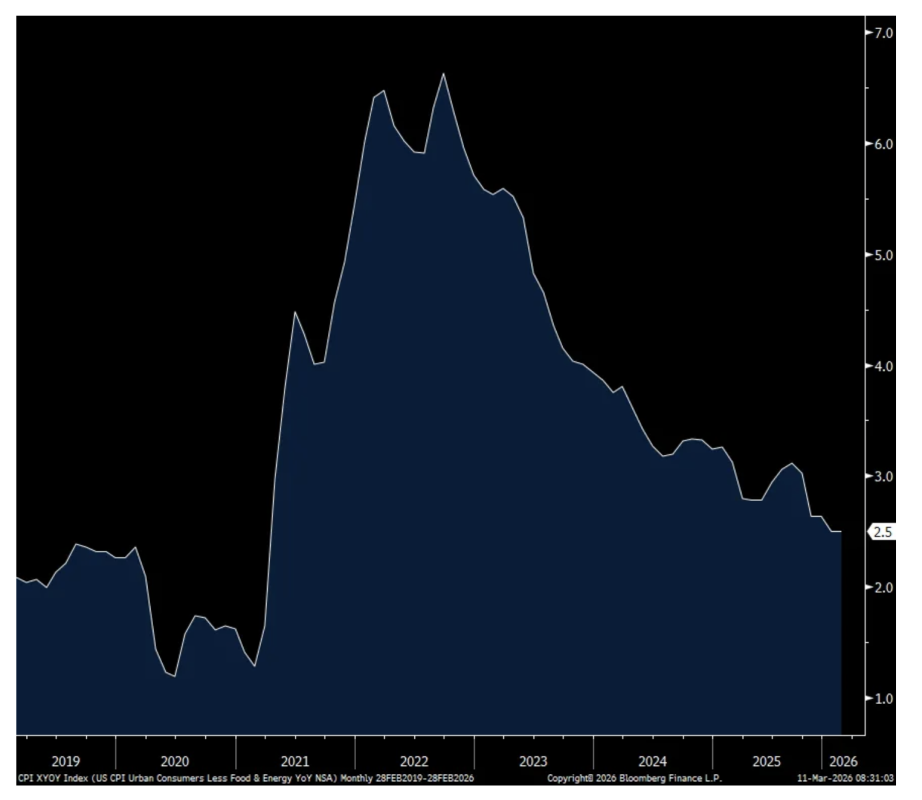

February CPI is of course in focus today but it should be viewed as old news for certain obvious components like energy, food, airfares, and new cars (price of aluminum) to name a few items. But also for other things touching the consumer like restaurants as more money gets diverted to paying for gasoline. I still think the bigger picture trend of slowing service price gains mostly due to moderating rental price increases (for now) and rising goods prices after the period of disinflation post inflation spike is intact.

Hopefully the G7 release of oil reserves will relieve some of the shortages at refineries but these countries still need to get the crude oil to them via shipping and eventually these reserves will have to be refilled, and then some, as I argued yesterday. Japan is going ahead itself on releasing direct to its own refineries.

Can central banks hike rates soon in response to the newly created inflation worry? The RBA might and today ECB member Peter Kazimir said they could too at some point. “For the time being, we need to stay calm” but “I’d say a reaction by the ECB is potentially closer than many people think. I don’t want to speculate about April or June. But we will be ready to act if needed.” In response to the comments, yields are up across the board in Europe, though the euro is little changed.

Another story of note in the private credit space, this time from the Financial Times saying “JPMorgan Chase has clamped down on its lending to private credit groups, with bankers looking to cut risk as concerns mount over the credit quality of companies in their stables. The bank informed private credit lenders that it had marked down the value of certain loans in their portfolios, which serve as the collateral the funds use to borrow from the bank, according to people familiar with the matter.”

“The move will limit how much money JPMorgan lends to private credit groups against those loans going forward - a sign traditional Wall Street banks are growing cautious of an industry that has grown rapidly as non-bank lenders became top creditors to higher-risk borrowers.”

I want to be clear that not all private credit is created equal and I see countless deals on my desk. There are very good loan underwriters and many that are not. The asset class suffered from too much money chasing not enough good loans to mostly single B rated companies. And, many of these loans were given to private equity leveraged buyouts which just put more debt on to a business. I prefer those that lend more directly to companies that help them grow their business instead and those with EBITDA north of $200 million that can better handle the economic gyrations and cycles.

https://www.ft.com/content/389a0003-d8de-4afd-9de9-be6e9fc6888c

To a few earnings calls.

From Casey’s General Store, the Midwest convenience store operator and one of my go to earnings calls in gauging the state of the consumer since they cater to them all:

“Continuing the momentum from the prior quarter, whole pies and hot sandwiches in all-day parts performed well during the third quarter...Energy drinks and nicotine alternatives continue to outperform the category with double digit growth.”

“we had a little under 3% pricing reflected in our current quarter. And that’s primarily on the nicotine category, where we tend to just pass through the manufacturer price increases that we have.” On prepared food, “we took almost no price.” And, “On the grocery side, we do use pricing to preserve margin. That’s a contractual business for us annually. And so we will continue to take price in that category commensurate with the inflation we take from our partners. And the pricing we do receive...in the grocery category especially is often largely or completely offset by promotional support from our vendor partners.”

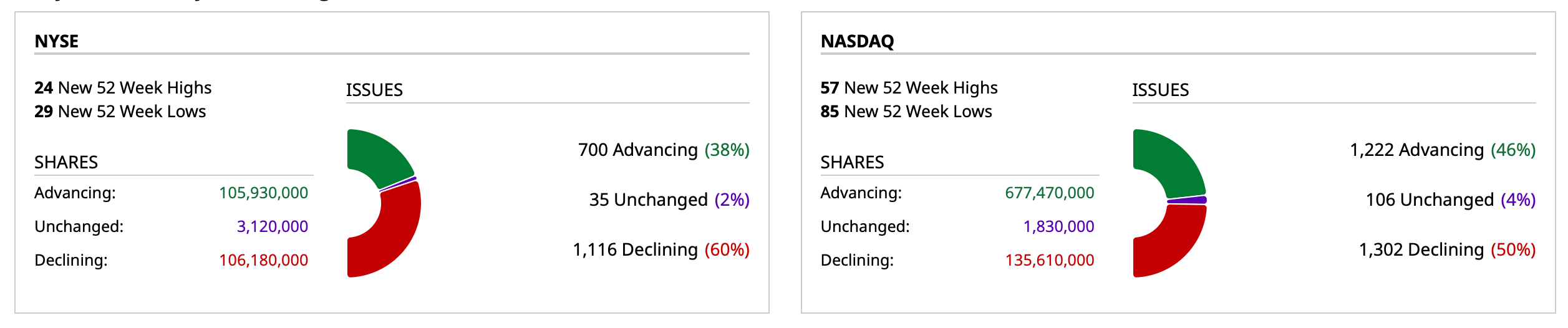

And importantly on the gas station business, “on the volume side of things, with absolute retail prices, we really don’t start to see any level of demand destruction until we’re approaching $5 a gallon at retail. As we sit here today, we’re right around $3 a gallon in our footprint. So we have quite a ways to go before we would be concerned from a volume standpoint.” I bolded to emphasize.

On the state of their consumer, “we’re still seeing customers shop at our stores across all income cohorts. For sure, the upper income cohorts are stronger, but we’re growing business across the low income cohorts as well. And what we’re seeing in terms of behavior difference, I’d say the middle and upper income cohorts are performing about the same. They’re still shopping at our stores. They’re shopping across all categories. Very little change in their behavior.”

“The lower income cohorts are still growing with us. I think that’s an important thing to call out. They are growing at a slower rate than the other cohorts, except in prepared foods where they’re actually growing as strong, if not stronger, than the higher income cohorts. I think that’s really a reflection of the value proposition that our prepared foods category offers relative to QSRs and other of our national brand pizza competitors. They’re also leaning a little bit heavier on the dispensed beverage side within prepared foods because that typically represents a better value than the bottle and can beverages on the non-alcohol or on the grocery and general merchandise side.”

I’ll add, when someone is going for fountain soda instead of a can or bottle, that tells you how stretched financially and value conscious some are.

“On grocery and general merchandise, lower income consumers are buying at a little bit slower rate, but still growing again. And that kind of holds together logically, as they may have opportunities to go to a grocery store and buy in bulk at a lower unit cost than what we would be able to provide...I still feel very good about the overall health of the consumer and their shopping habits.”

From Kohl’s, which certainly has its own competitive dynamic in the department store space:

“Beyond our category performance, it is also important to acknowledge that the consumer is behaving differently in this challenging macroeconomic environment. We know our core low to middle income customers continue to face financial pressure, and they are seeking value. As we expect this customer behavior to persist, we are adapting our strategies to ensure we are delivering great value to better serve this customer.”

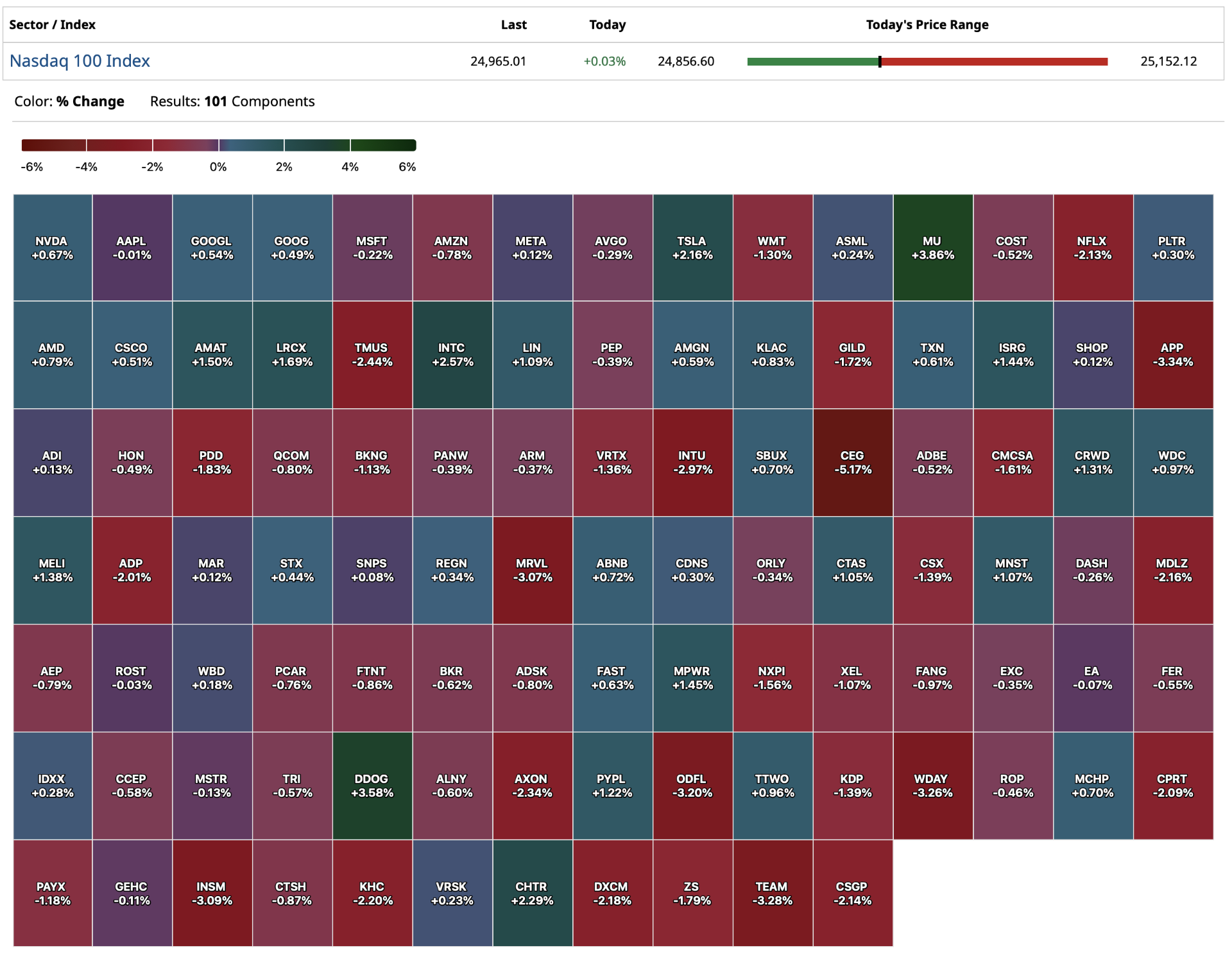

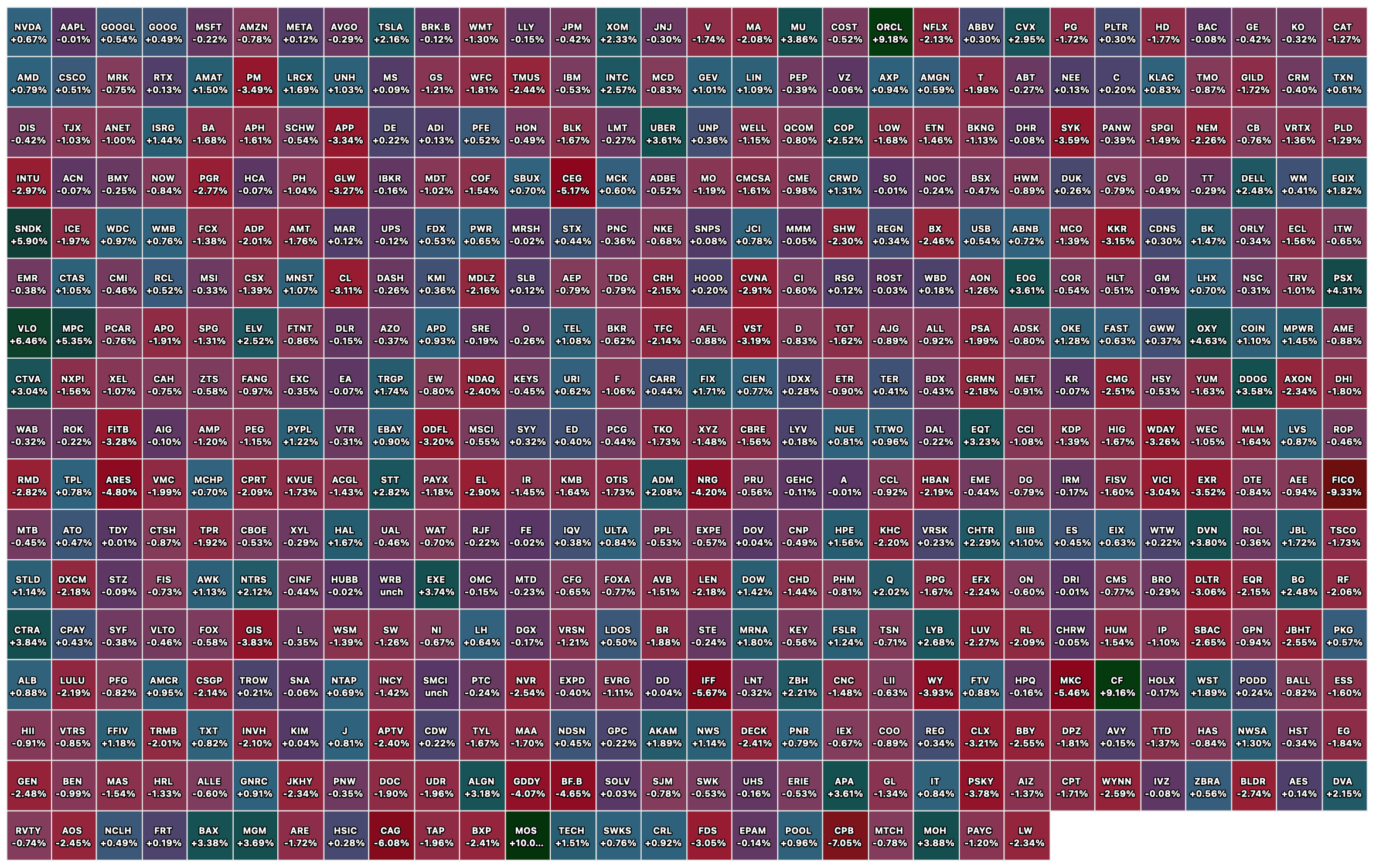

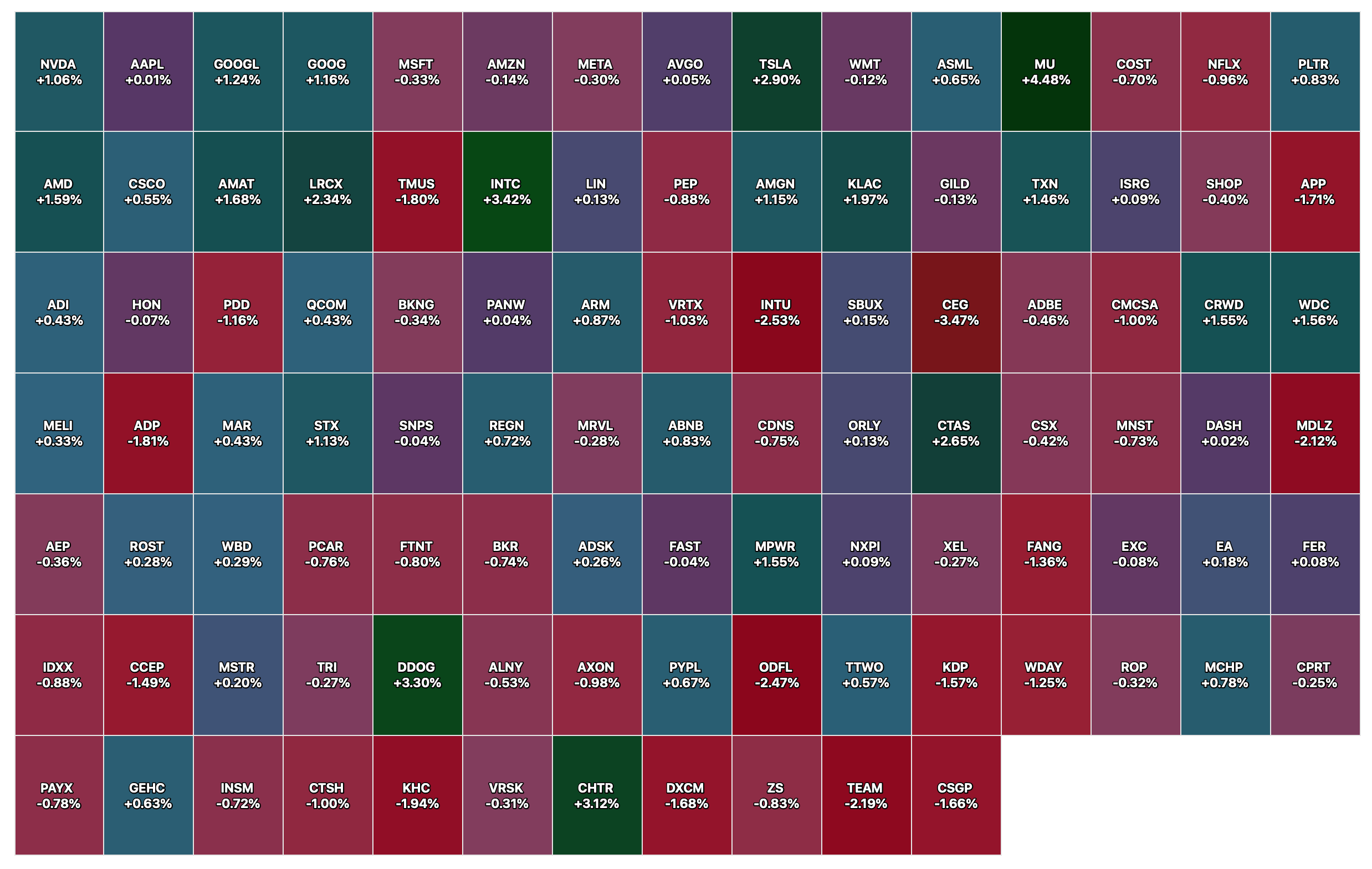

Oracle we see is jumping pre-market off a near 52 week low and they said this of note:

Defending its software business against the haters, “I’ll say a few words about the reported SasS Apocalypse. You’ve all heard the thesis or theory that new companies coding quickly using AI will spell the death of SaaS. I don’t agree with that at all. I do think that AI tools and their coding capabilities would be a threat if we weren’t adopting them, but we are and very rapidly. Oracle is using the best AI coding tools and the best developers not only to accelerate our SaaS business, but to deliver solutions that enable entire ecosystems across numerous industries.”

On their AI infrastructure business, “Demand for AI infrastructure, both GPU and CPU, continues to exceed supply. This is directly visible in our $553 billion RPO (remaining performance obligations).” They then went through how they are ramping up the needed data center supply to meet the demand. “Demand for AI and advanced compute will continue to expand broadly across the economy. There will be many successful models, agentic platforms and businesses that emerge.”

CapEx was left unchanged at $50b, which is an extraordinary 75% of expected revenue vs about 10% in fiscal ‘22.

To one economic data point. Weekly mortgage applications saw a pop in purchases, rising 7.8% w/o/w even with the 10 bps rise in mortgage rates for the week ended March 6th which we know rose after the oil price spike. Refi’s were unchanged after jumping in the prior three weeks.