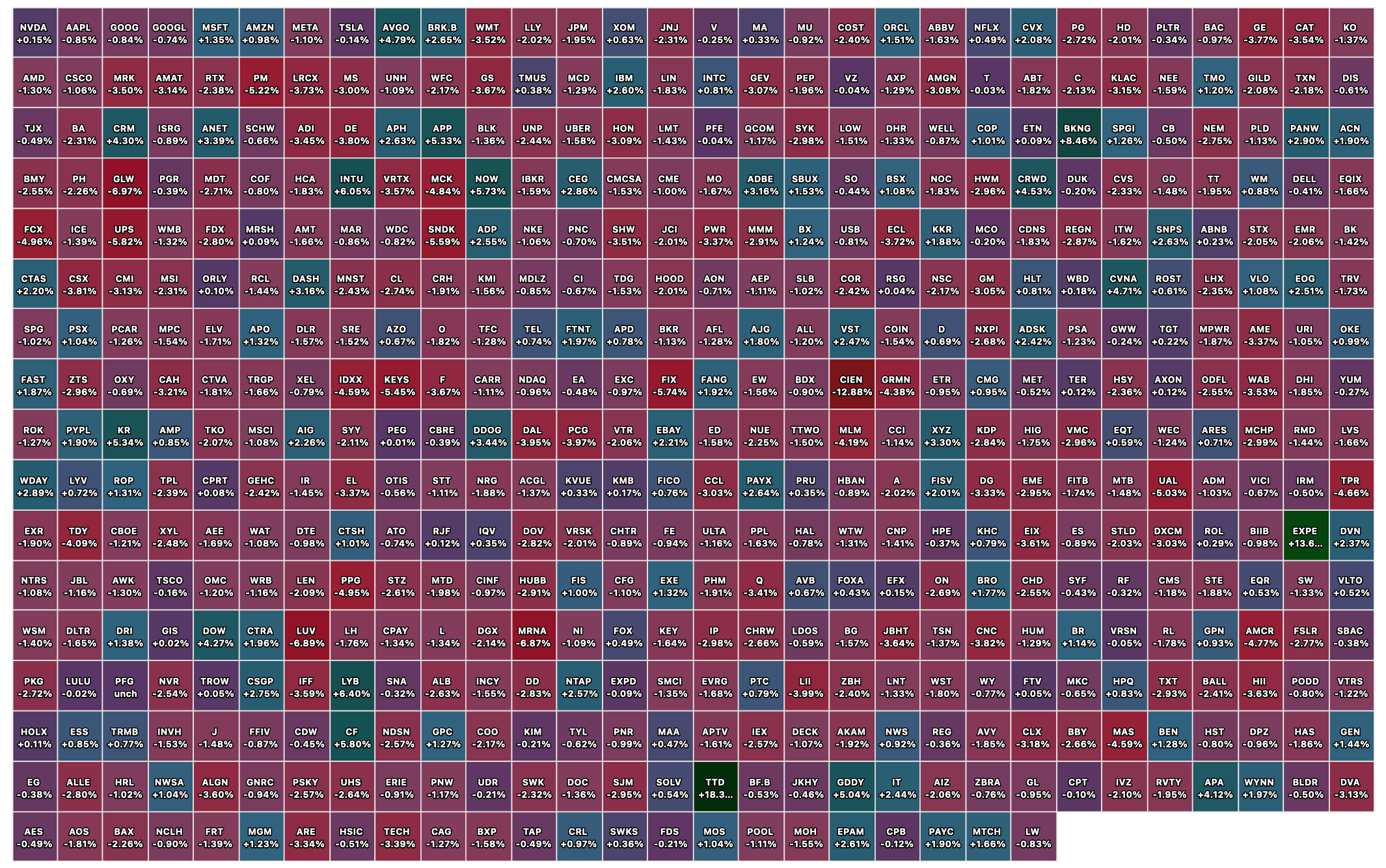

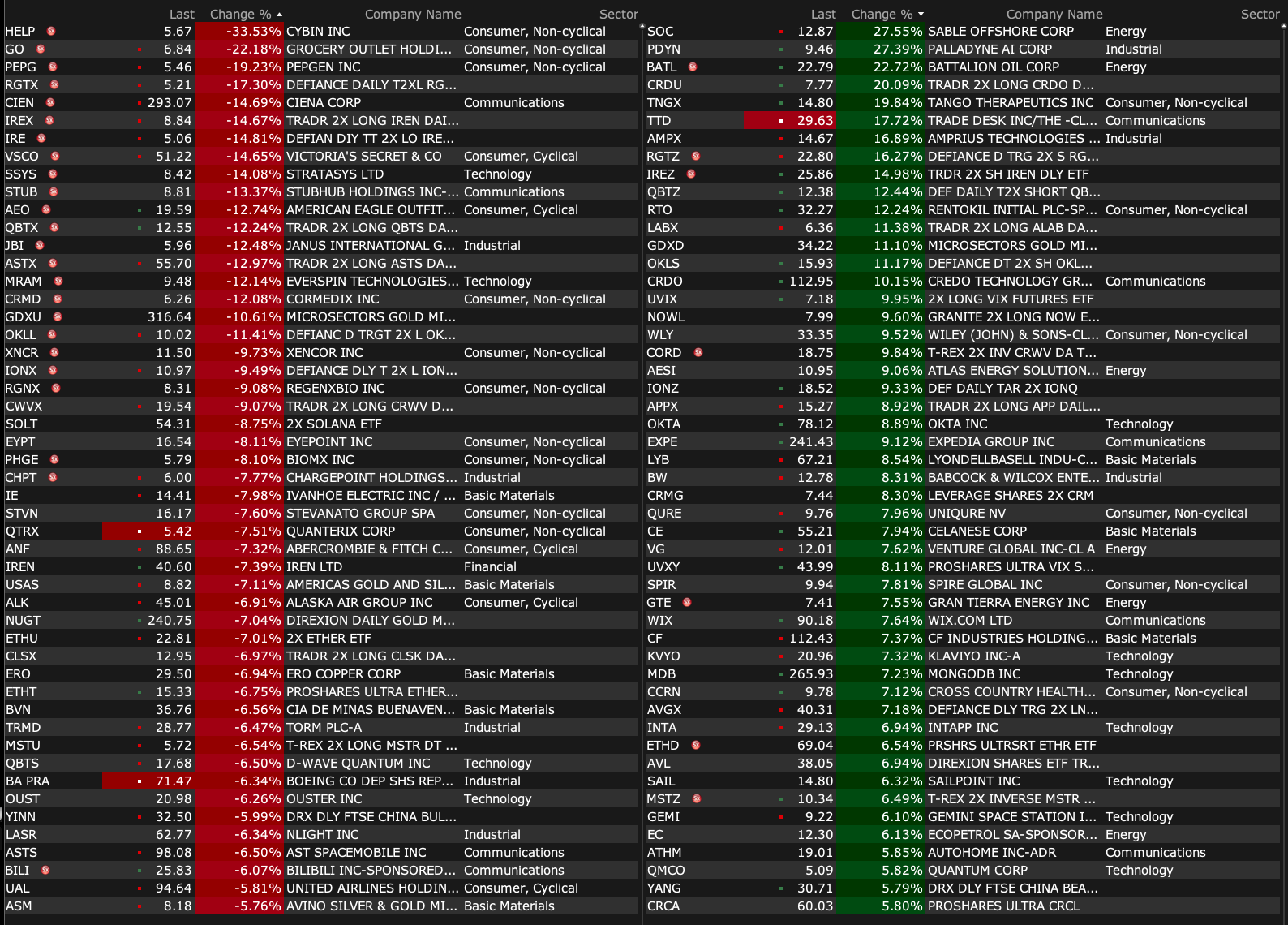

Thursday's Closing S&P 500 Heat Map

BY Doug Kass · Mar 5, 2026, 4:45 PM EST

BY Doug Kass · Mar 5, 2026, 4:45 PM EST

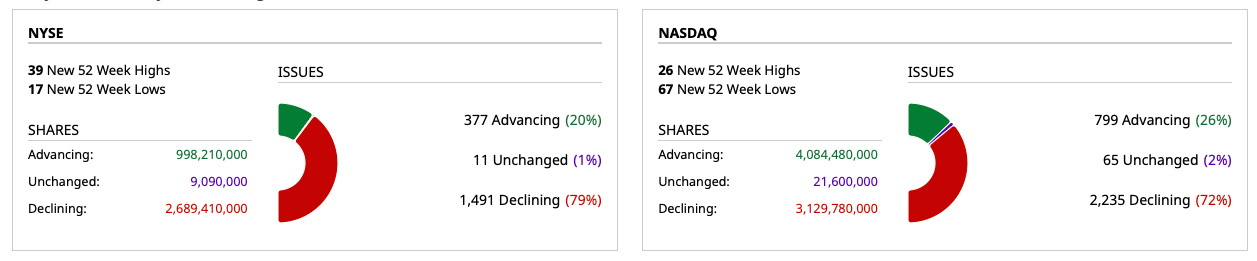

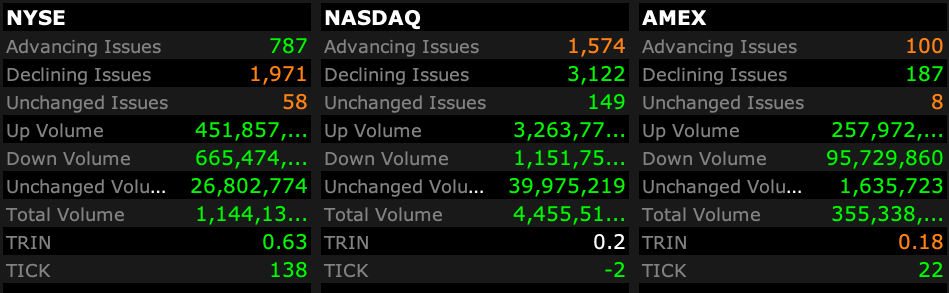

Breadth

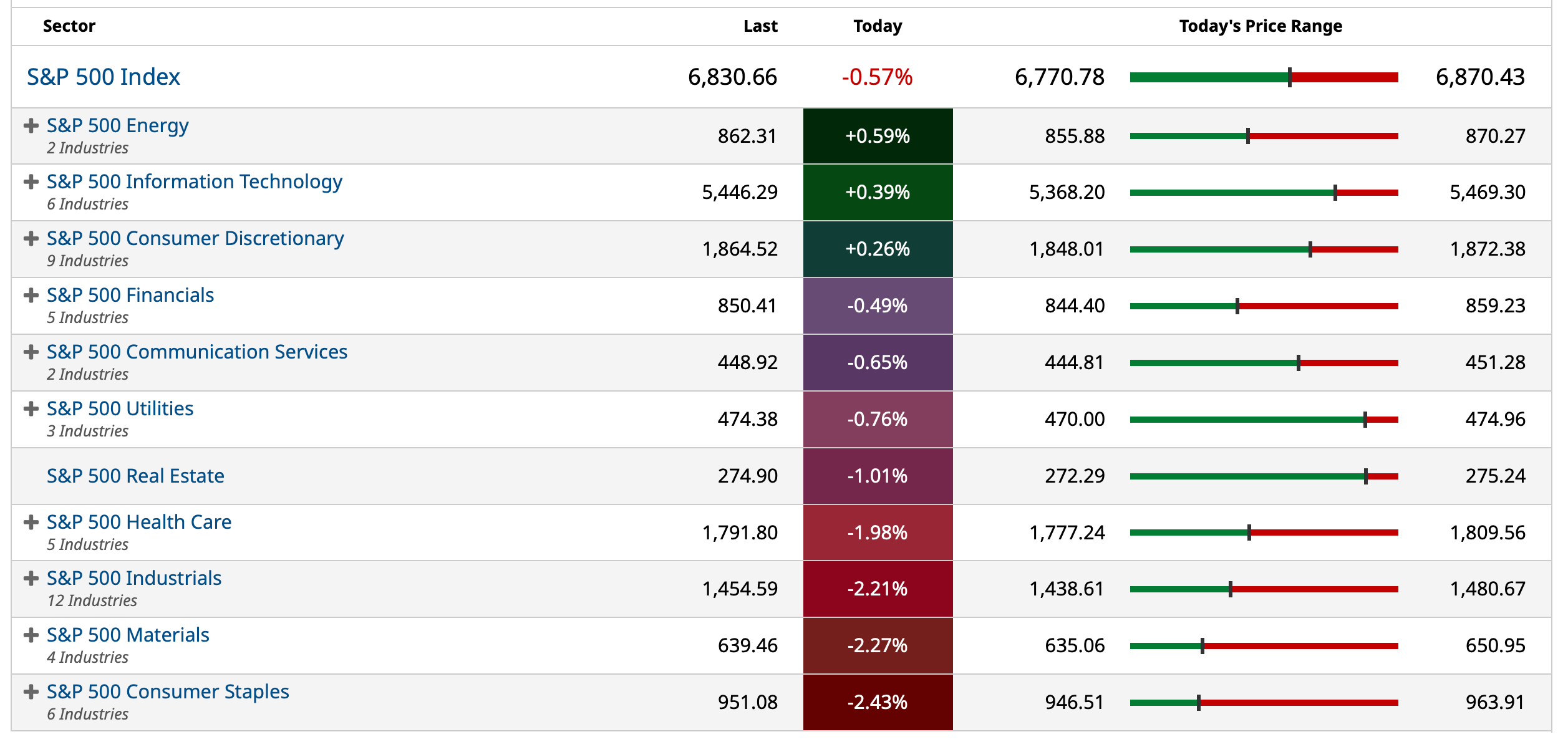

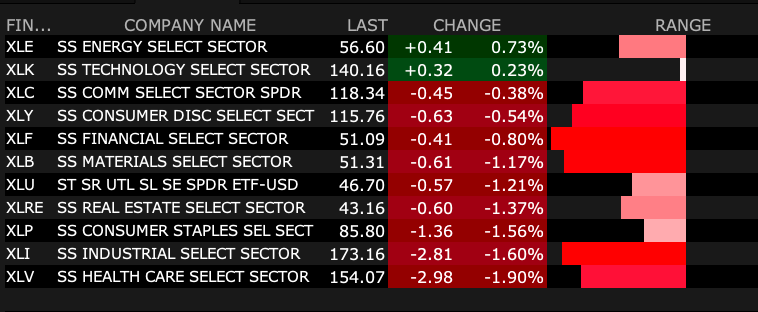

S&P 500 Sectors

% Movers

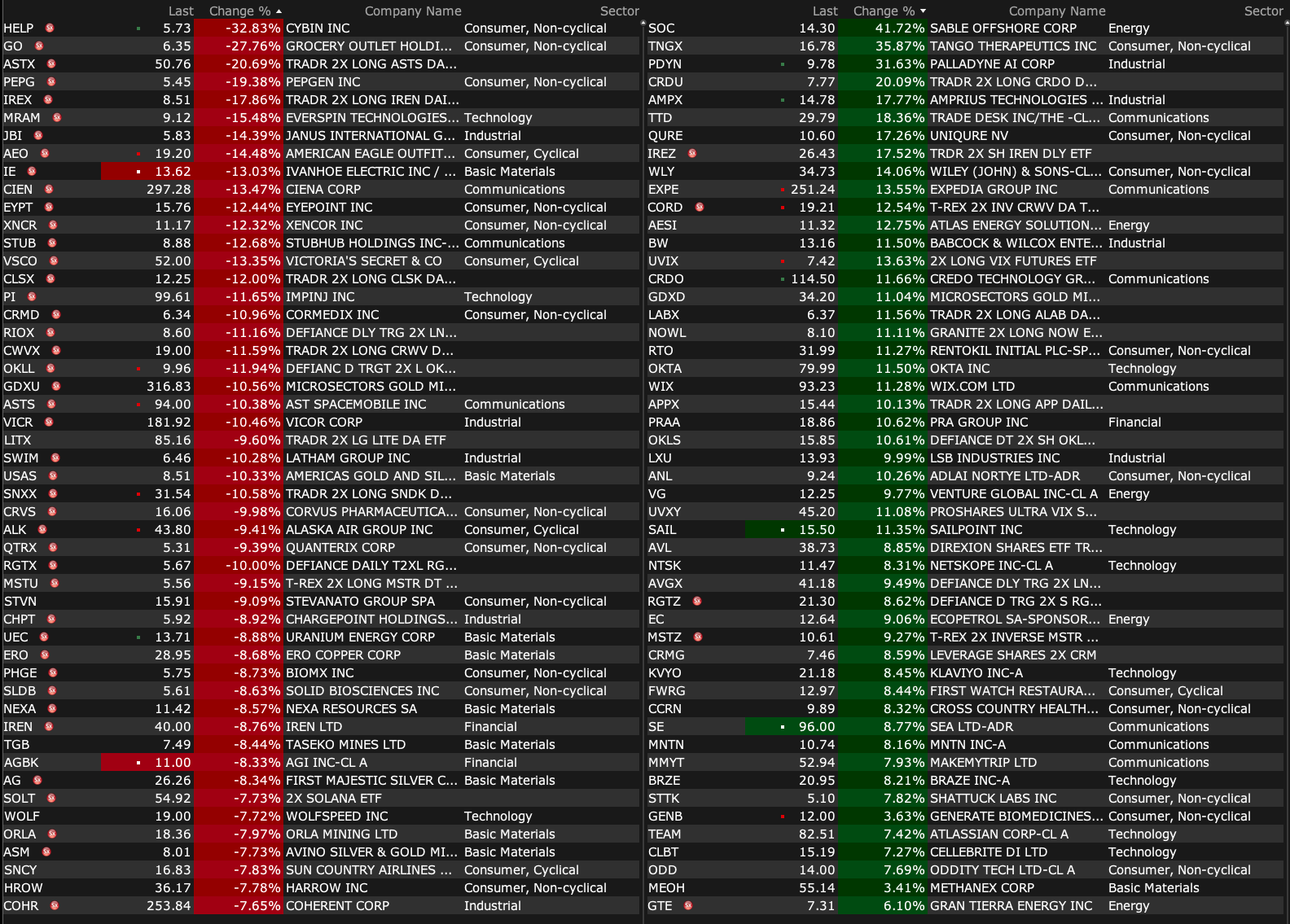

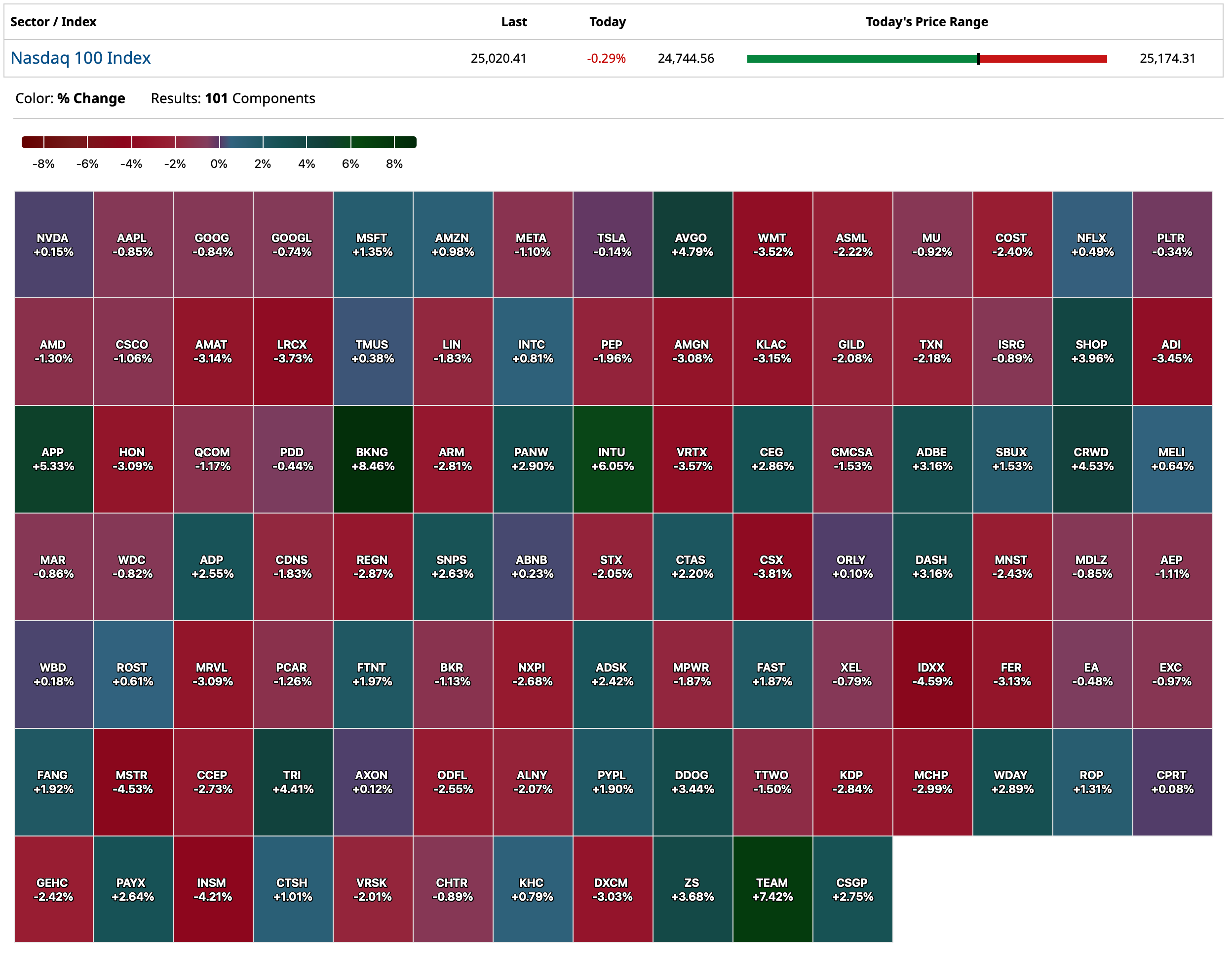

Nasdaq 100 Heat Matp

BY Doug Kass · Mar 5, 2026, 4:35 PM EST

I have mentioned the strong value-added contributions of "The Dales Report" and its suite of products often in my Diary.

Shadd Dales and Anthony Varrell are among the most informed sector participants.

Dales' "Trade to Black Live" podcast at 4 p.m. ET today with the manager of the (MSOS) ETF Dan Ahrens is likely an especially worthwhile watch.

Let's go to the tape!

🎦 TRADE TO BLACK

— The Dales Report (@TheDalesReport)

📊 Presented by @FlowhubCo

🕓 *LIVE* @ 4pm ET

🎦 What's Really Happening With Cannabis ETF MSOS?

🎙️ Dan Ahrens @InvestinginCan1, @AdvisorShares COO & $MSOS Portfolio Manager

🚨 Bring your Qs!

🌿 ETFs: 🌎 $YOLO 🇺🇸 $MSOS 📈 $SPY $QQQhttps://t.co/nKFofe2oSk

Run, don't walk to watch Shadd and Varrell.

I am.

BY Doug Kass · Mar 5, 2026, 4:24 PM EST

With S and P cash -40 handles I am back shorting Index calls.

BY Doug Kass · Mar 5, 2026, 4:04 PM EST

I have established new cannabis positions in (VRNOF) and (CURLF) today.

Speculative.

BY Doug Kass · Mar 5, 2026, 3:35 PM EST

I mentioned on Monday that I would be back buying consumer staples on another 3% to 5% percent pullback:

We have sold most of our consumer (defensive) staples on strength over the last month.

Today the sector came back to earth:

PG -$4.58

KMB -$4.53

PEP -$3.16

I would be patient and let them sell off another 3-5% before considering a repurchase of the three stocks above.

Position: Long KMB (VS), PG (VS)

BY DOUG KASS MAR 3, 2026 11:46 AM EST

We are getting close.

Buy pads are out for (PG) , (PEP) , (KMB) .

BY Doug Kass · Mar 5, 2026, 2:53 PM EST

BY Doug Kass · Mar 5, 2026, 2:29 PM EST

Housekeeping item.

Bitcoin is -3.3% today after the recent runup.

I covered my trading short rental in bitcoin ( (IBIT) - $40.09) just now for a very small profit (I had averaged up yesterday).

BY Doug Kass · Mar 5, 2026, 1:10 PM EST

* Over the last fifteen minutes...

From Randorama:

Randy

US Officials Have Written Draft Regulations That Would Restrict AI Chip Shipments To Anywhere In The World Without American Approval

BY Doug Kass · Mar 5, 2026, 1:04 PM EST

I covered (GRNY) short at $24.65 for a gain.

I will re-short strength.

BY Doug Kass · Mar 5, 2026, 12:43 PM EST

All Mag 7 are negative at 12:22 pm except (AMZN) and (MSFT) :

BY Doug Kass · Mar 5, 2026, 12:38 PM EST

Tech (XLK) vs Financials (XLF) as of 12:19 pm:

BY Doug Kass · Mar 5, 2026, 12:30 PM EST

BY Doug Kass · Mar 5, 2026, 12:14 PM EST

Buying more (MSOS) ($3.73), MSOX ($2.54) and MSOS calls.

BY Doug Kass · Mar 5, 2026, 11:50 AM EST

- NYSE volume 11% below its one-month average;

- Nasdaq volume 61% above its one-month average;

- VIX index: up 9.08% to 23.07

BY Doug Kass · Mar 5, 2026, 11:41 AM EST

BY Doug Kass · Mar 5, 2026, 11:20 AM EST

Pete

19 minutes ago

Doug, Maybe sometime in future you can explain why you paired Amazon (AMZN) as your long versus the other 2. Is it because Amazon is more diversified with different business like Aws and a Ad Business?

Reply

Dougie Kass

STAFF

Just Now

1. yes, correct on the fundies

2. the developed incongruities of price earnings ratios of the three stocks (AMZN pe was compressed, (COST) / (WMT) near record high pe)

BY Doug Kass · Mar 5, 2026, 10:55 AM EST

Chart from 9:48 a.m. ET

BY Doug Kass · Mar 5, 2026, 10:30 AM EST

* I added to my (GRNY) short at $25.03...

If the market truly corrects I want to be large-sized short GRNY -- as it holds most of the most speculative and vulnerable stocks extant.

Here is a holdings list:

GRNY Holdings List - Fundstrat Granny Shots US Large Cap ETF

Being short GRNY is being the anti-Tom Lee.

I am fine with that!

BY Doug Kass · Mar 5, 2026, 10:25 AM EST

I pressed my short bitcoin today.

BY Doug Kass · Mar 5, 2026, 10:15 AM EST

The three way pairs trade (long (AMZN) /short (COST) and (WMT) ) is really paying off. Today:

* (AMZN) +$2.35

* (COST) -$15.20

* (WMT) -$3.20

BY Doug Kass · Mar 5, 2026, 10:05 AM EST

I will have more about the opportunities available (for the opportunistic trader) in trading ranges tomorrow.

But for now, I covered all my Index short calls (for a profit) on the whoosh lower.

I plan to reshort strength.

phew!

BY Doug Kass · Mar 5, 2026, 9:56 AM EST

From Peter Boockvar:

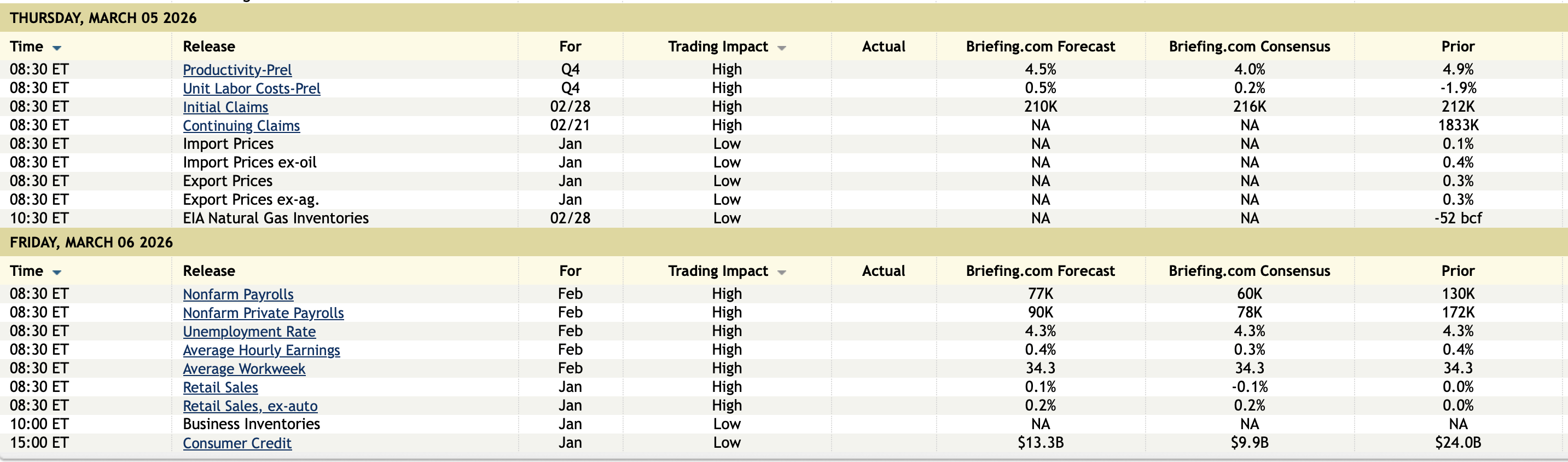

Initial jobless claims were little changed at 213k vs 212k last week and just below the estimate of 215k. The 4 week average fell to 216k from 221k as a print of 232k 5 weeks ago drops out. Continuing claims, delayed by a week in reporting, rose to 1.868mm from 1.822mm and that was 23k above the estimate.

Bottom line, the theme of modest firing’s (as measured here as some get gig jobs instead of filing for claims) and moderate hiring remains the same.

The pace of firing’s slowed as seen in the Challenger March report with 48,307 job cuts, lower by 72% y/o/y. Technology was the sector that led the cuts and Challenger said specifically with this group, “Tech is responding to a number of pressures right now. AI is the big story, but there are also global regulatory concerns, a slowdown in digital advertising driven by tariffs and economic uncertainty, and higher costs to both employ workers and access funding, forcing companies to make difficult decisions.”

The always important question as to why companies lay people off, Challenger said this, “In February, store, unit, or department Closings led all reasons for job cuts, with 10,736 announced during the month. Market and Economic Conditions followed with 10,114 cuts. Restructuring was cited for 9,146 job cuts, while Cost-Cutting accounted for 5,636 planned layoffs.”

On the hiring side, of course offsetting the layoffs, they totaled 12,755, down by 63% y/o/y, though up from 5,306 in January.

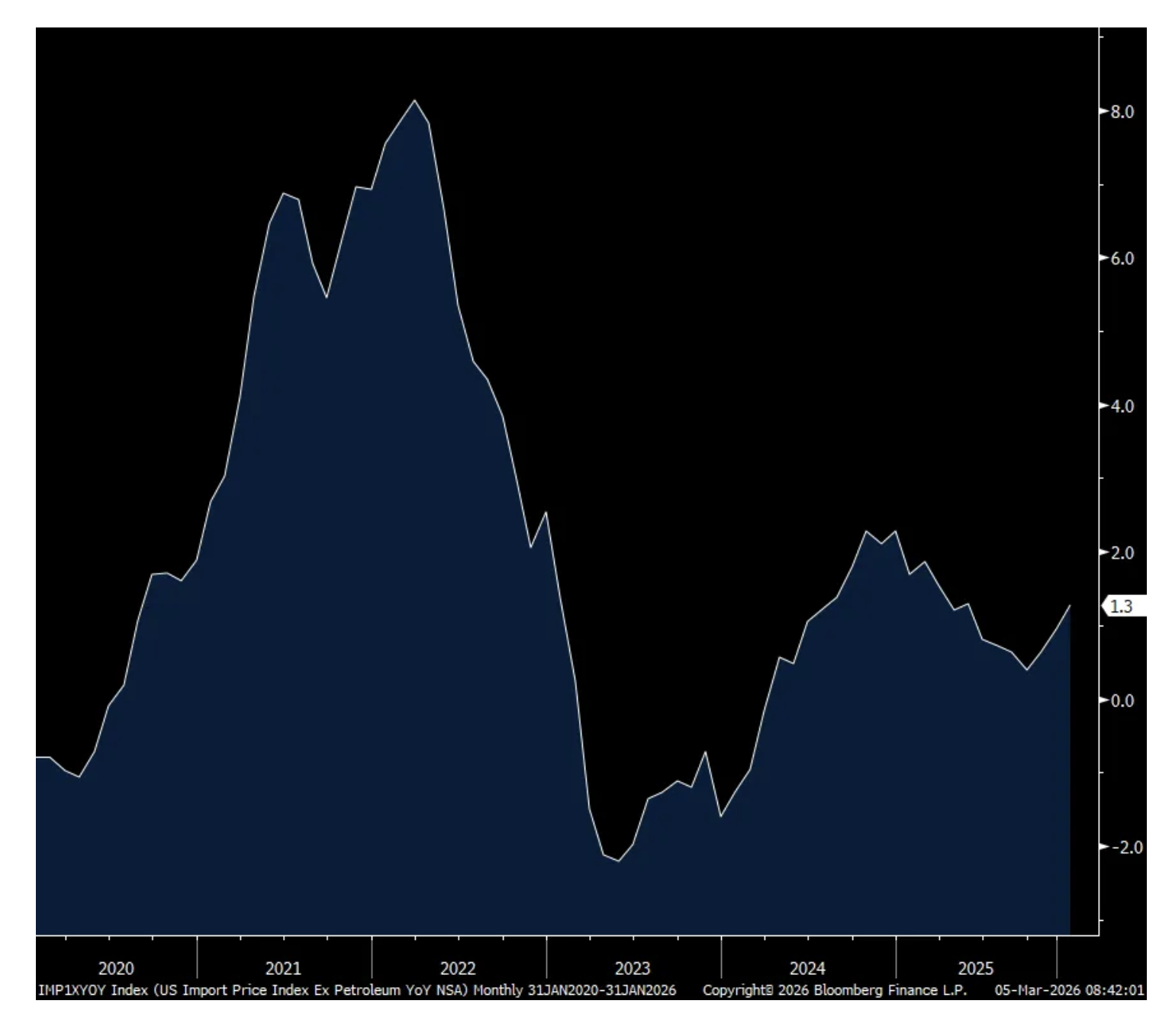

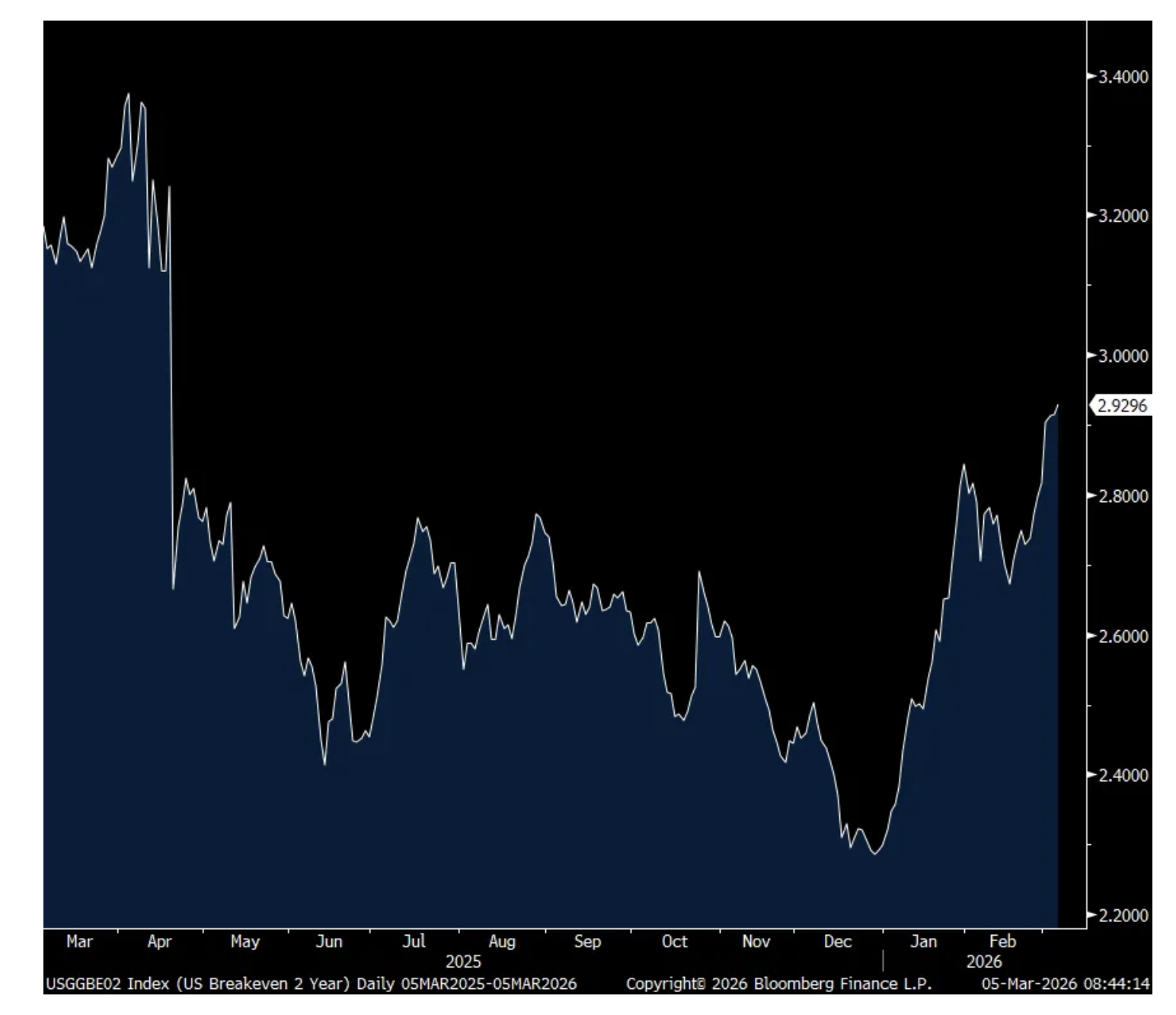

With respect to January import prices, they were as expected when including the December upward revision. Prices ex food and fuel jumped .5% after a .3% rise in December and higher by 1.6% y/o/y. Capital goods prices rose .4% m/o/m after no change in December. Autos/parts prices were up .2% m/o/m for a 2nd month. Consumer goods prices ex autos saw just a one tenth gain after no change in the month before. On the heels of the industrial metals jump, ‘finished metals’ import prices jumped 4.1% m/o/m after rising by 4.7% in December and higher by 17% y/o/y.

Import prices are never market moving but the 2 yr inflation breakeven is moving up for the 11th day in the past 12 to 2.93%, up 26 bps over this time frame.

Import Prices ex petro y/o/y

2 yr Inflation Breakeven

BY Doug Kass · Mar 5, 2026, 9:51 AM EST

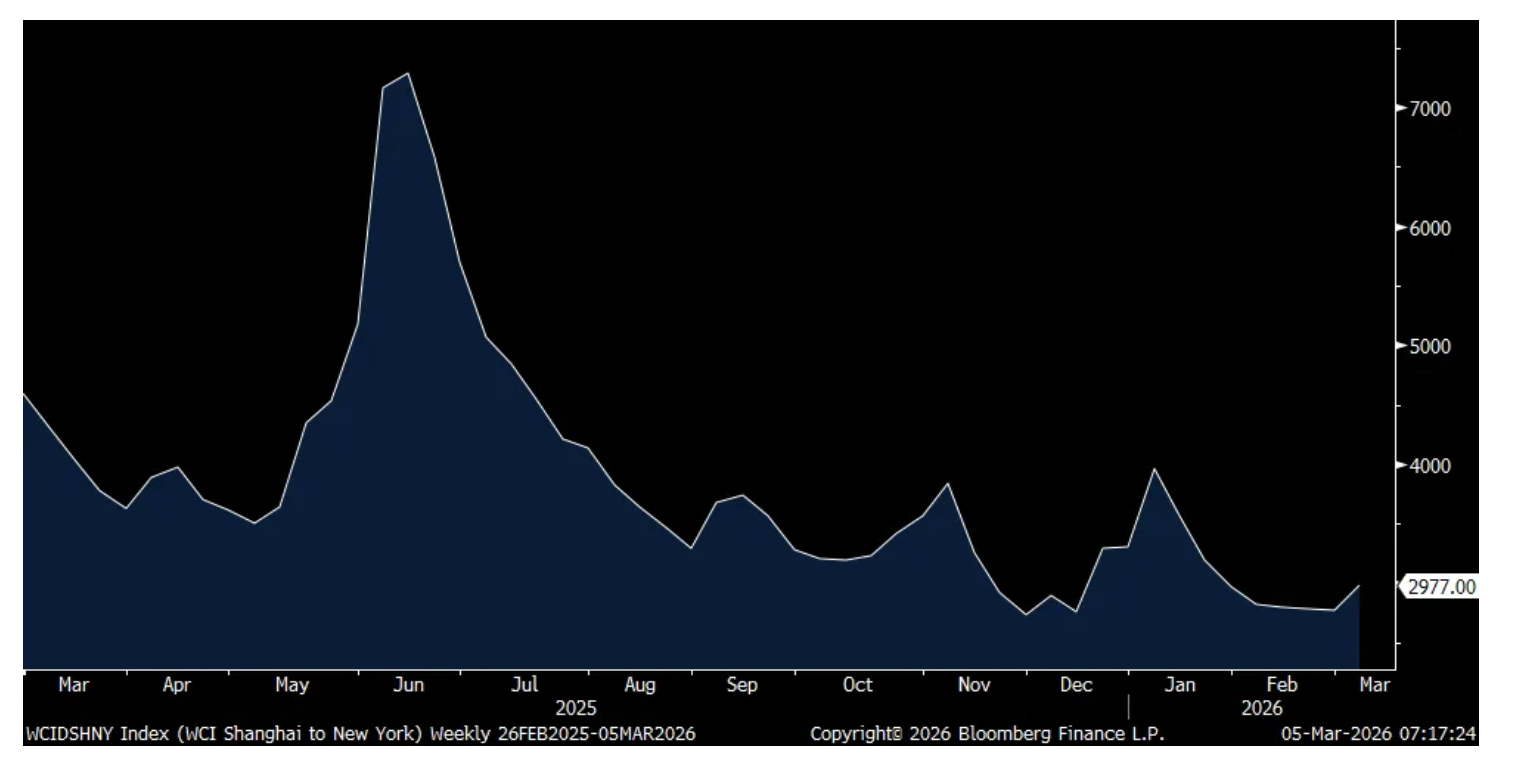

From Peter Boockvar

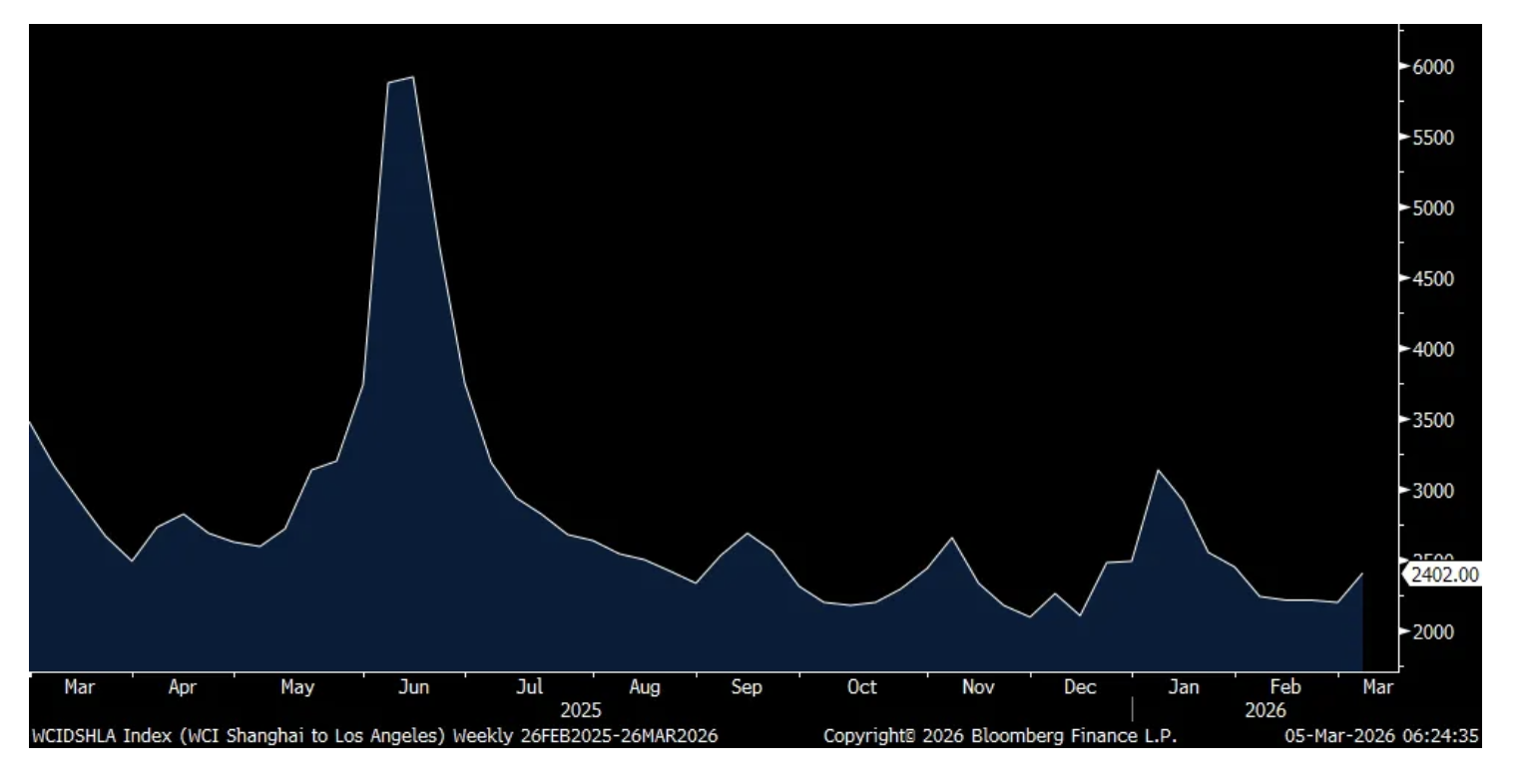

In the first look at global container shipping prices according to the World Container Index saw the Shanghai to NY trip jump by 7% to $2,977 per 40 foot container, after 7 weeks of declines though still cheap as it’s below where it was a year ago. Shanghai to LA lifted by a similar amount to $2,402. The Shanghai to Rotterdam route though saw a modest fall in prices to $2,052. We of course start watching this as container ships now get re-routed, again, from the Red Sea.

I am reading some stories that the Chinese, in a desperate move to get oil/LNG shipments from their Gulf partners, are putting signs on ships saying ‘China Owner’ in order to get safe passage through the Strait.

Shanghai to NY

Shanghai to LA

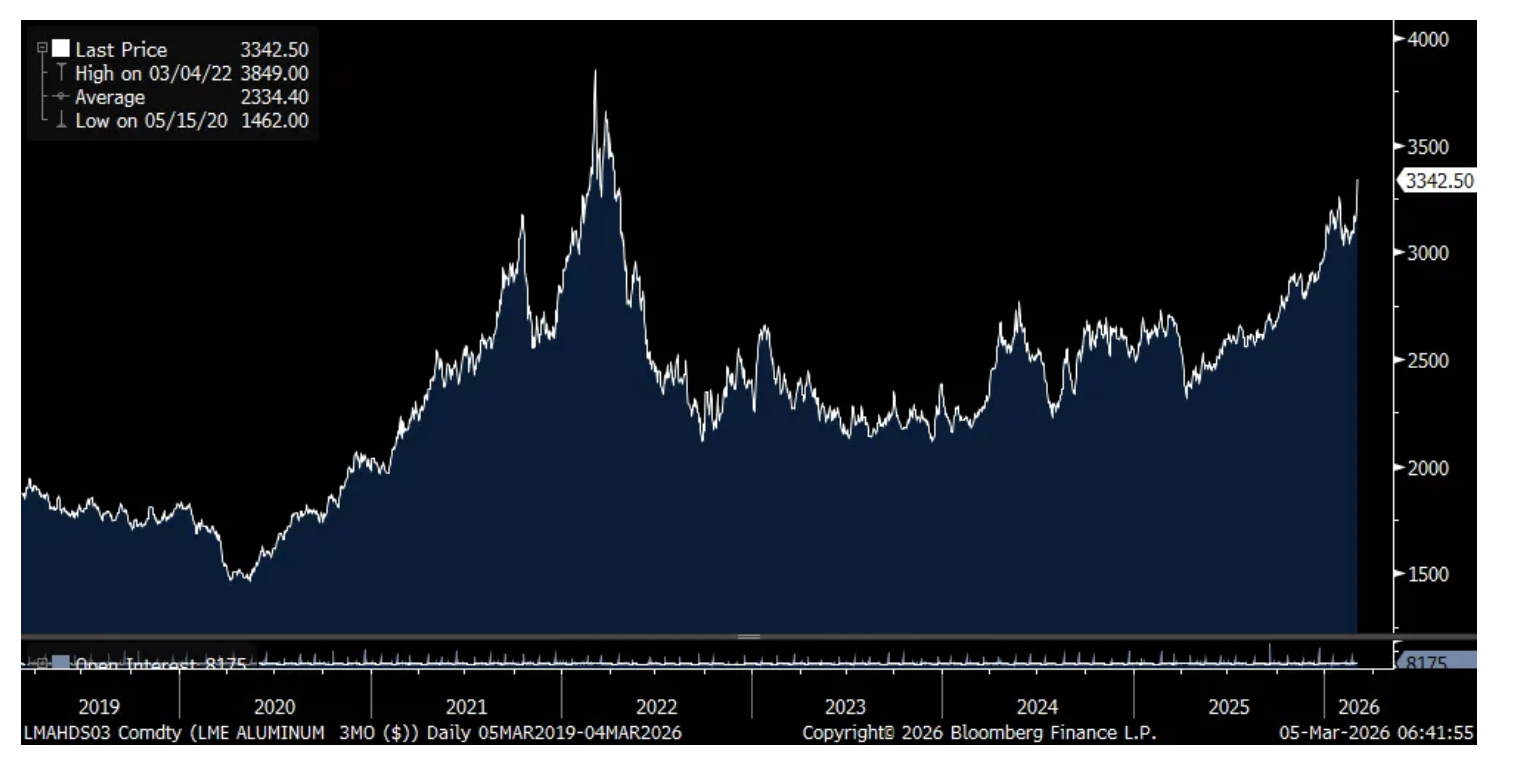

We talk mostly about the transportation of oil and gas out of the Gulf but not enough about aluminum where smelters in that region make up about 10% of global supply. The price of aluminum yesterday closed at the highest level since early 2022 right after Russia invaded Ukraine.

Aluminum on the LME

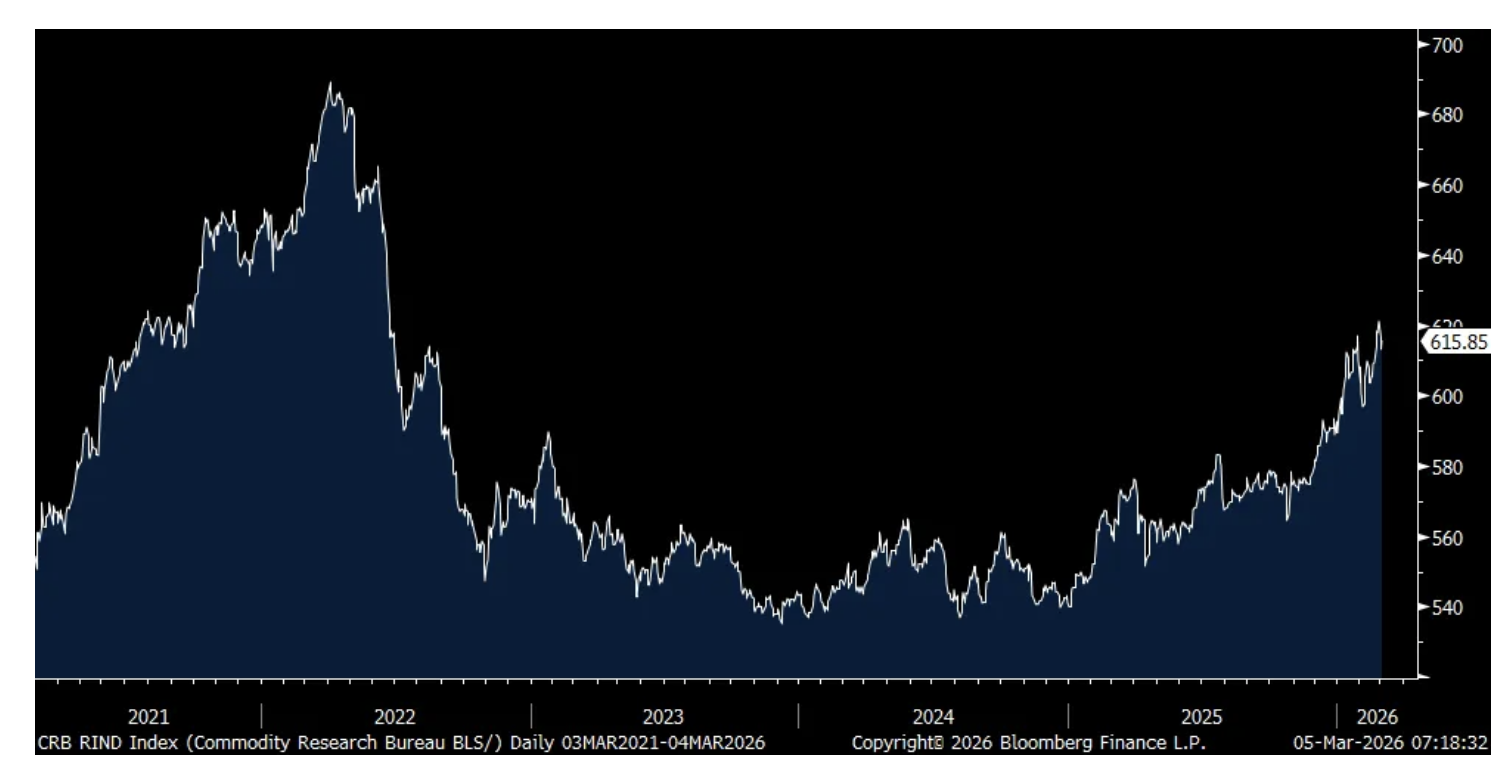

Looking at the CRB raw industrials index, with everything going on, is just off its highest level since June 2022.

CRB Raw Industrials Index

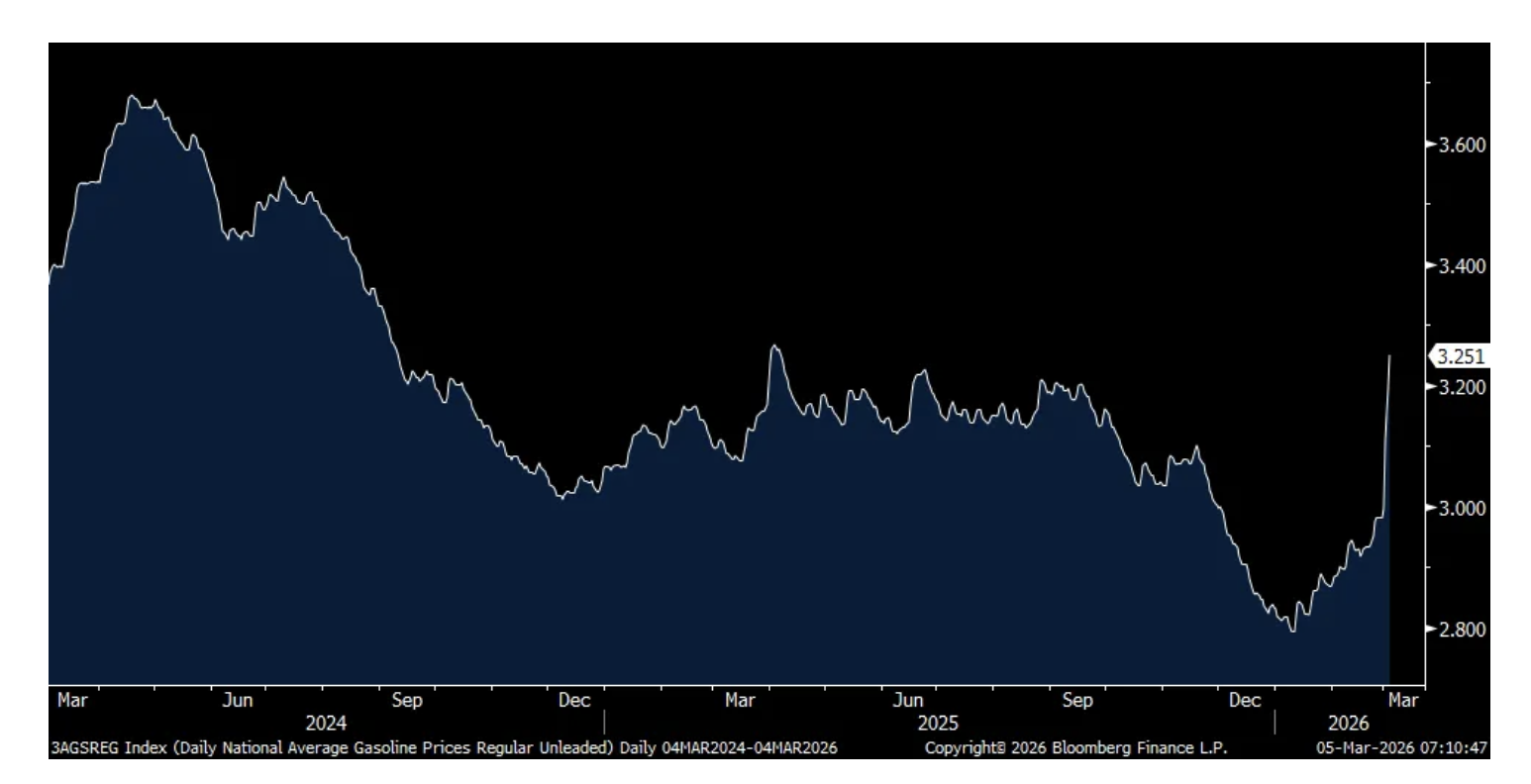

Here is a fresh chart on gasoline prices according to AAA as they rose another nickel yesterday to $3.25 and now up 4.5% y/o/y. Still pretty cheap though but we’re of course sensitive to a consumer that is tired of paying ever higher prices for things.

Average Gallon of Gasoline

Again, the Fed’s Beige Book reads quite different and softer than the headline GDP reports we are getting that reflect about 2.5% growth y/o/y. From yesterday’s release, “Overall economic activity increased at a slight to moderate pace in seven of the twelve Federal Reserve Districts, while the number of Districts reporting flat or declining activity increased from four in the prior period to five in the current period.”

Under the hood and on the US consumer, “Although consumer spending increased slightly on balance, two Districts reported ongoing declines, and many noted that sales were dampened by economic uncertainty, increased price sensitivity, and lower-income consumers pulling back on spending. Districts impacted by winter storms said that retail traffic generally slowed, and one District said immigration enforcement activity negatively affected customer demand in urban areas. Auto sales were mostly down for Districts that reported on them, with many citing continuing affordability issues.”

Similar to what we saw in the ISM this week, signs of a bottom in manufacturing, “Manufacturing activity improved overall since the previous reporting period, with eight Districts reporting varying degrees of growth and two reporting declines. Manufacturing contacts in many Districts reported increases in new orders, and several cited boosts in demand from data centers and, relatedly, energy infrastructure.”

Also, “Transportation activity was mixed across Districts that reported on it, with three reporting contractions and two reporting modest growth.” I’ll add, trucking prices keep firming up because of the continued reduction in demand, now in part due to stricter rules on who can drive a truck.

On finance and real estate, “Overall, financial services activity was reported as stable to up, with commercial lending being the primary area of strength. For most Districts that reported on residential real estate and construction, sales and activity decreased slightly, with low inventories and affordability remaining key issues. Nonresidential construction activity was mixed across reporting Districts but increased slightly on net.”

Keep in mind, that ‘nonresidential construction activity’ includes data center building so ex that, things are weak with construction.

As to the economic future, “Overall, economic expectations were optimistic, with most Districts expecting slight to moderate growth in the coming months.”

Is the slowdown in hiring more slack demand or shrinking supply? The Beige Book said, “Employment levels were generally stable in recent weeks as seven of the twelve Districts reported no change in hiring. Contacts in several Districts cited rising nonlabor input costs, softer demand, or uncertainty about overall economic conditions as reasons for flat or lower employment levels. Firms in some Districts and in various sectors looked to AI or other forms of automation to gain efficiencies, with most emphasizing the goal of productivity enhancement rather than worker replacement.”

Who is eating the persistent cost pressures, us or them? “Many Districts reported that costs rose across several nonlabor inputs, including insurance, utilities and energy, and metals and other raw materials. Nine Districts mentioned that tariffs contributed to increased costs. Some firms continued to pass tariff-related cost increases through to their customers, and others began to do so after having absorbed previous increases. Still, most Districts received reports of some firms holding selling prices stable despite higher costs because their customers were increasingly price sensitive. On balance, firms expected prices to rise at a somewhat slower pace in the near term,” said the Beige Book.

With a check on stock market sentiment, the mood has definitely cooled but in the weekly Investors Intelligence number, the reduction in Bulls over the past few weeks has only saw them fall into the Correction camp as Bears are still in hibernation. Bulls fell to 52.7 from 55.6 after getting over 60 a few weeks ago. Bears though continue to slip, down to just 14.6 from 14.8 in the week before. That’s the smallest number of Bears since October 2025 while those expecting a Correction rose to the most since November 2025. These stats DO NOT include the attacks over the weekend as it is as of last Friday.

What does include the sentiment post the weekend was the AAII retail survey where Bulls were actually little changed at 33.1, though that is the least since last November. Bears fell 4.3 pts to 35.5 off the highest since last November. The Citi Panic/Euphoria index stands at about 50, still above the .41 threshold into Euphoria but off its highs. The CNN Fear/Greed index is at 38, in the ‘fear’ category.

Bottom line, while the extreme level of Bullishness has cooled off from the hot pace last month, market sentiment is now overall mixed.

Just a few earnings calls to go through.

From Bath & Body Works, up almost 3% yesterday:

In Q4, net sales were “down 2.3% versus last year and better than the guidance floor we set of down high single digits. This performance reflects improvement as the quarter progressed, following a soft start in early November when we navigated significant macroeconomic pressure that impacted our consumer demand.”

With their 2026 guidance, “We expect net sales to be down 4.5% to down 2.5%. Key assumptions behind our net sales include a macro environment similar to 2025 with continued value oriented consumer behavior...Promotions are assumed at comparable levels to 2025 and will remain an important tool to drive traffic and customer engagement.”

From Abercrombie & Fitch that fell 4% on a lighter than expected guide:

“For the fourth quarter, we delivered net sales growth of 5%, which was balanced across regions, brands, and channels.” Comps were up 1%, “with approximately 100 bps of benefit from foreign currency.” Hollister was the stand out with a 3% comp gain while Abercrombie fell 1%.

With the Abercrombie brand in particular, “We continue to see strong traffic along with growth in customer counts and good retention trends.”

They do have some exposure with stores in the Middle East and “On the evolving Middle East conflict, we currently anticipate a slight sales headwind, and we’ll continue to actively monitor the situation alongside our in-market franchise and joint venture partner, with safety as our highest priority.”

From Broadcom, up about 6% after great numbers as they continue to ride the GenAI CapEx orgy:

Their Q1 52% revenue jump “was driven by AI semiconductor revenue, which grew 106% y/o/y to $8.4 billion, way above our outlook.”

“The ramp of custom AI accelerators across all our five customers is progressing very well. For Google, we continue our trajectory of growth in ‘26 with strong demand for the 7th generation Ironwood TPU.”

BY Doug Kass · Mar 5, 2026, 9:35 AM EST

-TTD +21% (OpenAI reportedly held early AD sales discussions with Trade Desk)

-PDYN +18% (earnings, guidance)

-BTAI +12% (announces Positive Phase 2 Topline Results from Columbia University-Led Study of BXCL501 for Treatment of Opioid Withdrawal)

-VEEV +10% (earnings, guidance)

-CBRL +8.2% (earnings, guidance)

-AVGO +6.3% (earnings, guidance)

-UAMY +5.3% (selected for Strategic Antimony Supply Chain Expansion Under DoW Initiative)

-GO -26% (earnings, guidance)

-PEPG -19% (U.S. FDA places FREEDOM2 trial on partial clinical hold related to preclinical pharmacology and toxicology; earnings)

-STUB -13% (earnings, guidance)

-BJ -6.2% (earnings, guidance)

-IREN -5.7% (expands AI cloud capacity to 150K GPUs)

-RGTI -5.2% (earnings)

-CIEN -4.2% (earnings, guidance)

-VSCO -3.9% (earnings, guidance)

-BABA -2.5% (according to large US brokerage firm, the departure of tech lead increases execution risk)

-AEO -2.4% (earnings, guidance)

-BULL -2.4% (earnings)

-KR -2.1% (earnings, guidance)

BY Doug Kass · Mar 5, 2026, 9:20 AM EST

BY Doug Kass · Mar 5, 2026, 9:05 AM EST

BY Doug Kass · Mar 5, 2026, 8:48 AM EST

11:00 a.m.: Treasury announces a 6-Week, 3 and 6 month bill auction.

11:00 a.m.: Treasury note announcement.

11:30 a.m.: Treasury hosts a $105B 4 and a $95B 8 Week Bill Auction;

2:00 p.m.: Treasury buyback (liq support)

1:15 p.m.: Fed Vice Chair for Supervision Bowman (Voter) speaks before virtual New York Bankers Association "Navigating What's Next: Perspective on the Economy and Innovation" event, Nasdaq MarketSite, NYC (Topic and livestream link TBA. No text. Q&A from moderator);

7:00 p.m.: Fed Bank of Chicago Goolsbee (Non-Voter) attends the Foreign Policy Association Financial Services Dinner and will receive an award and deliver brief, non-policy related remarks at the start of the event. (no Live Stream, no Embargoed Text)

BY Doug Kass · Mar 5, 2026, 8:32 AM EST

BY Doug Kass · Mar 5, 2026, 8:21 AM EST

* As wage growth slows and inflation rises...

Wolf Street howls about rising inflation and slowing wage growth.

More:

Record Numbers of Workers Are Raiding Their 401(k) Savings

We remain short Costco (COST) and Walmart (WMT) (against an Amazon (AMZN) long).

I want to short more consumer stocks.

BY Doug Kass · Mar 5, 2026, 7:15 AM EST

BY Doug Kass · Mar 5, 2026, 7:00 AM EST

BY Doug Kass · Mar 5, 2026, 6:45 AM EST

BY Doug Kass · Mar 5, 2026, 6:35 AM EST

Typically one considers buying at the sound of cannons.

This could be an exception to the rule. Better said, it might be too early to be buying.

I am not equipped to analyze the Iranian situation accurately so I rely on experts to determine the likely outcome, extent and duration of the conflict.

Unfortunately there are reasons to believe that short-term optimism is not called for.

Day five:

BY Doug Kass · Mar 5, 2026, 6:25 AM EST

BY Doug Kass · Mar 5, 2026, 6:15 AM EST

BY Doug Kass · Mar 5, 2026, 6:05 AM EST

The S&P Short Range Oscillator moved back towards neutral but remains slightly oversold at -0.42% vs. -0.65%.

BY Doug Kass · Mar 5, 2026, 5:55 AM EST

It was another wild night in futures — providing some excellent trading opportunities.

S&P futures, as an example, peaked at about +30 handles and traded down to -35 handles on reports of Iran's massive missile and drone attack on Israel:

While I didn't get the full benefit of the decline, we covered both (SPY) and (QQQ) for nearly a $2/share (each) profit.

From last night:

At 6:05PM I shorted:

* SPY $686.38

* QQQ $611.69

Position: Short SPY common VS calls VS QQQ common VS calls VS

By Doug Kass Mar 4, 2026 6:25 PM EST

We remain short index calls.

BY Doug Kass · Mar 5, 2026, 5:45 AM EST

🎦 TRADE TO BLACK 📊 Presented by @FlowhubCo 🕓 *LIVE* @ 4pm ET 🎦 What's Really Happening With Cannabis ETF MSOS? 🎙️ Dan Ahrens @InvestinginCan1, @AdvisorShares COO & $MSOS Portfolio Manager 🚨 Bring your Qs! 🌿 ETFs: 🌎 $YOLO 🇺🇸 $MSOS 📈 $SPY $QQQ youtube.com/watch?v=uLFby0…