Wednesday Night Trading

At 6:05PM I shorted:

* SPY $686.38

* QQQ $611.69

BY Doug Kass · Mar 4, 2026, 6:25 PM EST

At 6:05PM I shorted:

* SPY $686.38

* QQQ $611.69

BY Doug Kass · Mar 4, 2026, 6:25 PM EST

BY Doug Kass · Mar 4, 2026, 4:36 PM EST

BY Doug Kass · Mar 4, 2026, 4:33 PM EST

- NYSE volume 18% below its one-month average;

- NASDAQ volume 26% above its one-month average;

- VIX index: down 9.04% to 21.44

BY Doug Kass · Mar 4, 2026, 4:29 PM EST

I reshorted GRNY at $25.135.

BY Doug Kass · Mar 4, 2026, 4:09 PM EST

My long Amazon (+$8.55)/short Costco (unchanged) and WalMart (unchanged) is working well today.

BY Doug Kass · Mar 4, 2026, 3:57 PM EST

The Fed’s Beige Book just came out and actually showed, at the margin, a less ebullient tone to the economy compared to what we saw in January. Our proprietary diffusion index went in the opposite direction as the two ISMs — faltering to 28% from 61% two months ago. Adjusting the various Fed Districts by population share, the total share of the economy expanding fell considerably to just 60% from 69% in January.

The consumer may well be resilient, but apparently less so than at the turn of the year. Auto sales definitely were weaker. But business capex was marked significantly higher. The housing market moved from being soft to modest contraction mode. At the margin, just a little bit of improvement in the jobs market. But the big surprise, despite all the anxiety out there, is that many more districts are reporting benign inflation citations.

Read on:

January: “Overall economic activity increased at a slight to modest pace in eight of the twelve Federal Reserve Districts, with three Districts reporting no change and one reporting a modest decline.”

March: “Overall economic activity increased at a slight to moderate pace in seven of the twelve Federal Reserve Districts, while the number of Districts reporting flat or declining activity increased from four in the prior period to five in the current period.”

January: “Most banks reported slight to modest growth in consumer spending this cycle, largely attributed to the holiday shopping season. Several Districts also noted that spending was stronger among higher-income consumers with increased spending on luxury goods, travel, tourism, and experiential activities. Meanwhile, low to moderate income consumers were seen to be increasingly price sensitive and hesitant to spend on nonessential goods and services.”

March: “Although consumer spending increased slightly on balance, two Districts reported ongoing declines, and many noted that sales were dampened by economic uncertainty, increased price sensitivity, and lower-income consumers pulling back on spending.”

January: “Auto sales were little changed to down across most Districts.”

March: “Manufacturing activity improved overall since the previous reporting period, with eight Districts reporting varying degrees of growth and two reporting declines. Manufacturing contacts in many Districts reported increases in new orders, and several cited boosts in demand from data centers and, relatedly, energy infrastructure. ”

March: “Auto sales were mostly down for Districts that reported on them, with many citing continuing affordability issues.”

January: “Manufacturing activity varied with five Districts reporting growth and six reporting contraction. Nonfinancial services demand was generally seen as steady to increasing somewhat.”

January: “Residential real estate sales, construction, and lending activity softened in the majority of Districts that report on the sector.”

March: “For most Districts that reported on residential real estate and construction, sales and activity decreased slightly, with low inventories and affordability remaining key issues.”

January: “Employment was mostly unchanged in the most recent period, with eight of the twelve Districts reporting no changes in hiring.”

March: “Employment levels were generally stable in recent weeks as seven of the twelve Districts reported no change in hiring.”

January: “Prices grew at a moderate rate across a large majority of Districts, with only two Districts reporting slight price growth.”

March: “Prices increased moderately in recent weeks, with eight Districts reporting moderate price growth and four seeing slight or modest increases.”

BY Doug Kass · Mar 4, 2026, 3:40 PM EST

I added to my short bitcoin position of (IBIT) at $41.97.

BY Doug Kass · Mar 4, 2026, 3:28 PM EST

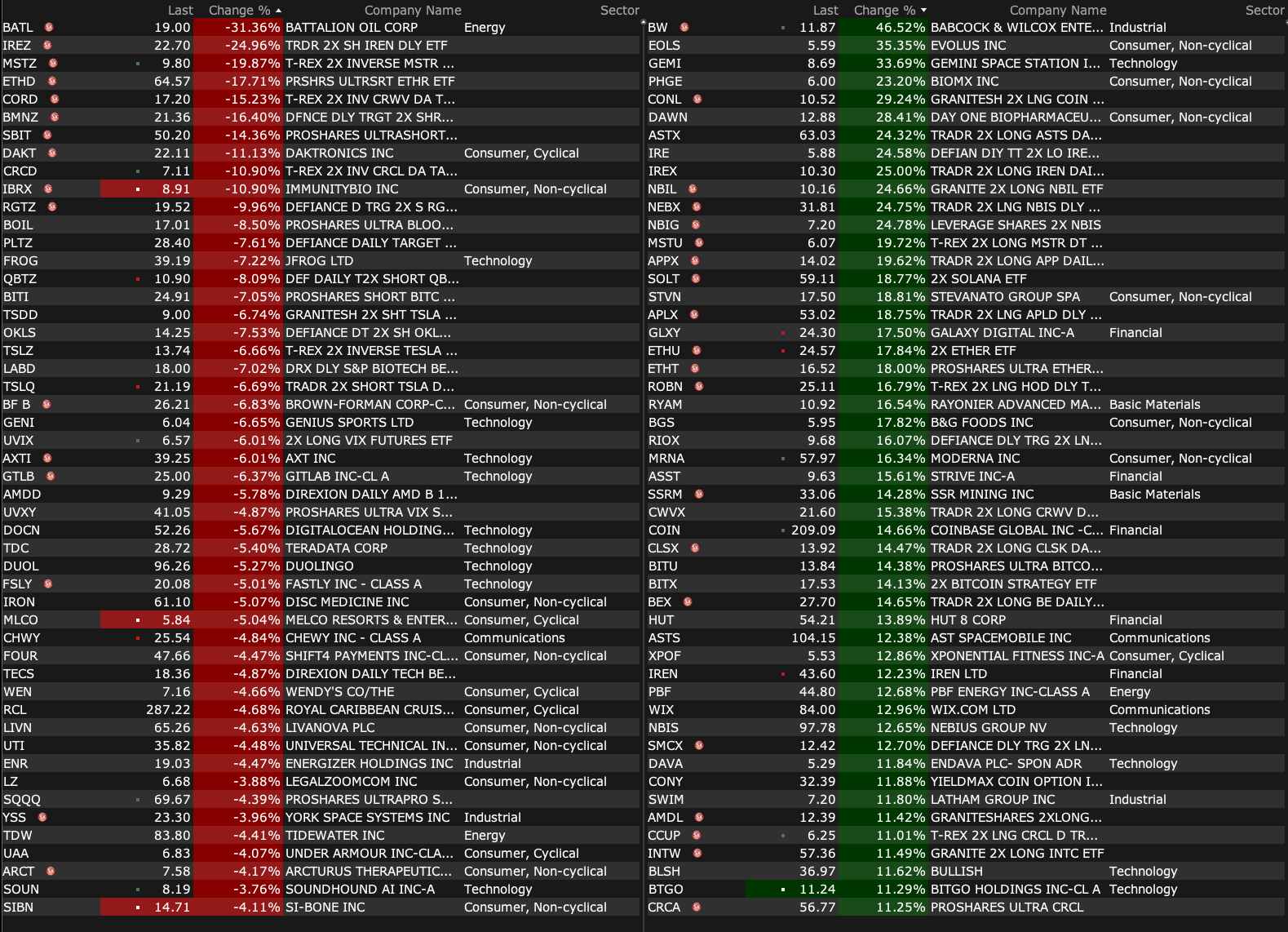

As of 3:19 pm:

Advancers

Decliners

BY Doug Kass · Mar 4, 2026, 3:24 PM EST

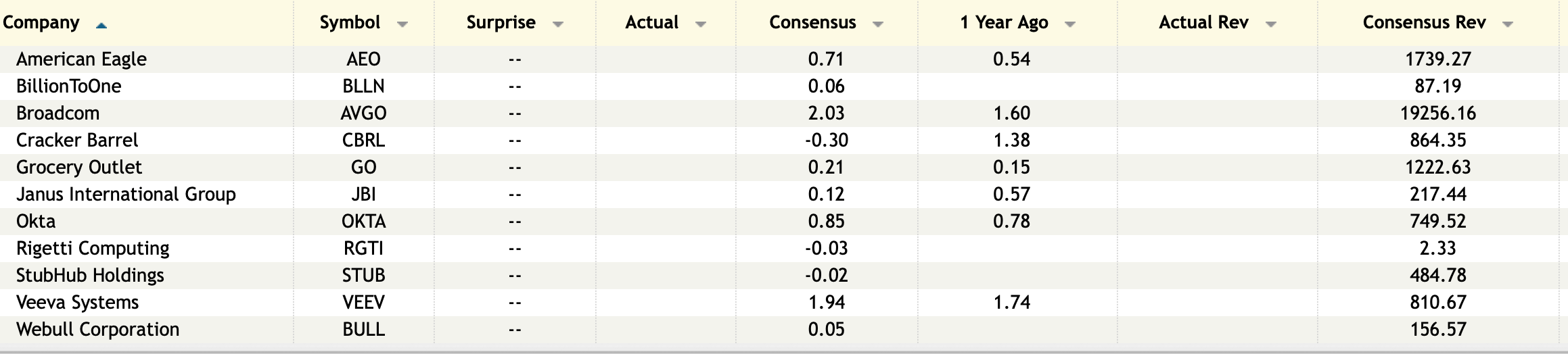

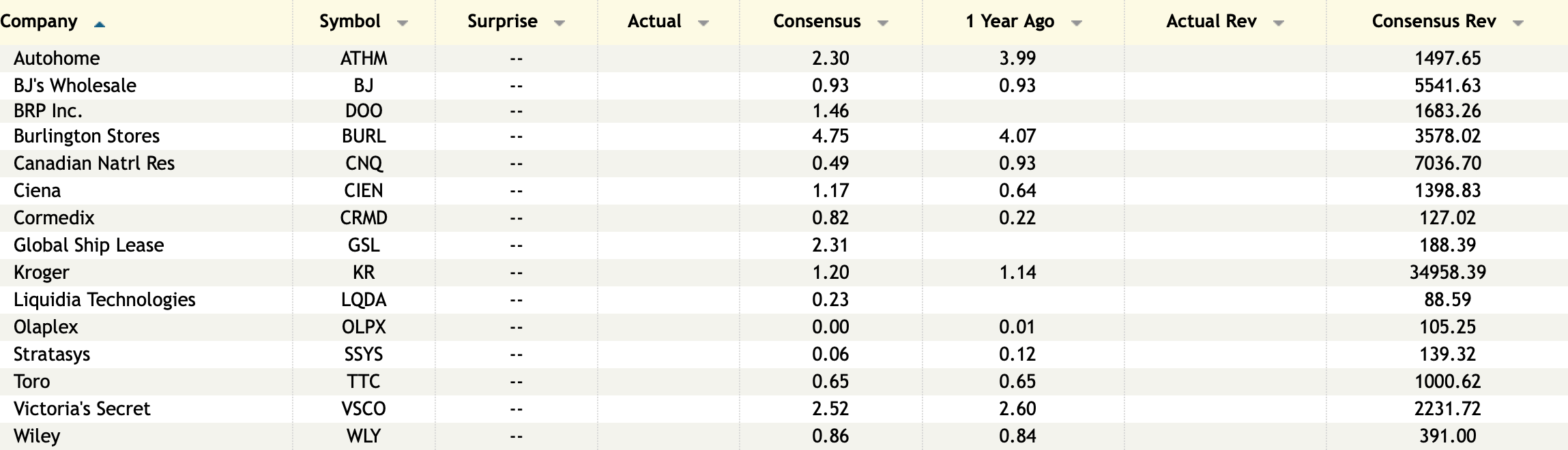

From Whitney Tilson's Daily:

BY Doug Kass · Mar 4, 2026, 2:45 PM EST

BY Doug Kass · Mar 4, 2026, 2:33 PM EST

With S&P cash +6 handles I am putting on my next tranche of short index calls.

BY Doug Kass · Mar 4, 2026, 2:20 PM EST

BY Doug Kass · Mar 4, 2026, 1:13 PM EST

I have a business lunch between noon and 2 p.m. today.

BY Doug Kass · Mar 4, 2026, 11:45 AM EST

- NYSE volume 16% below its one-month average;

- Nasdaq volume 37% above its one-month average;

- VIX: down 11.96 to 20.75

BY Doug Kass · Mar 4, 2026, 11:25 AM EST

From Peter Boockvar:

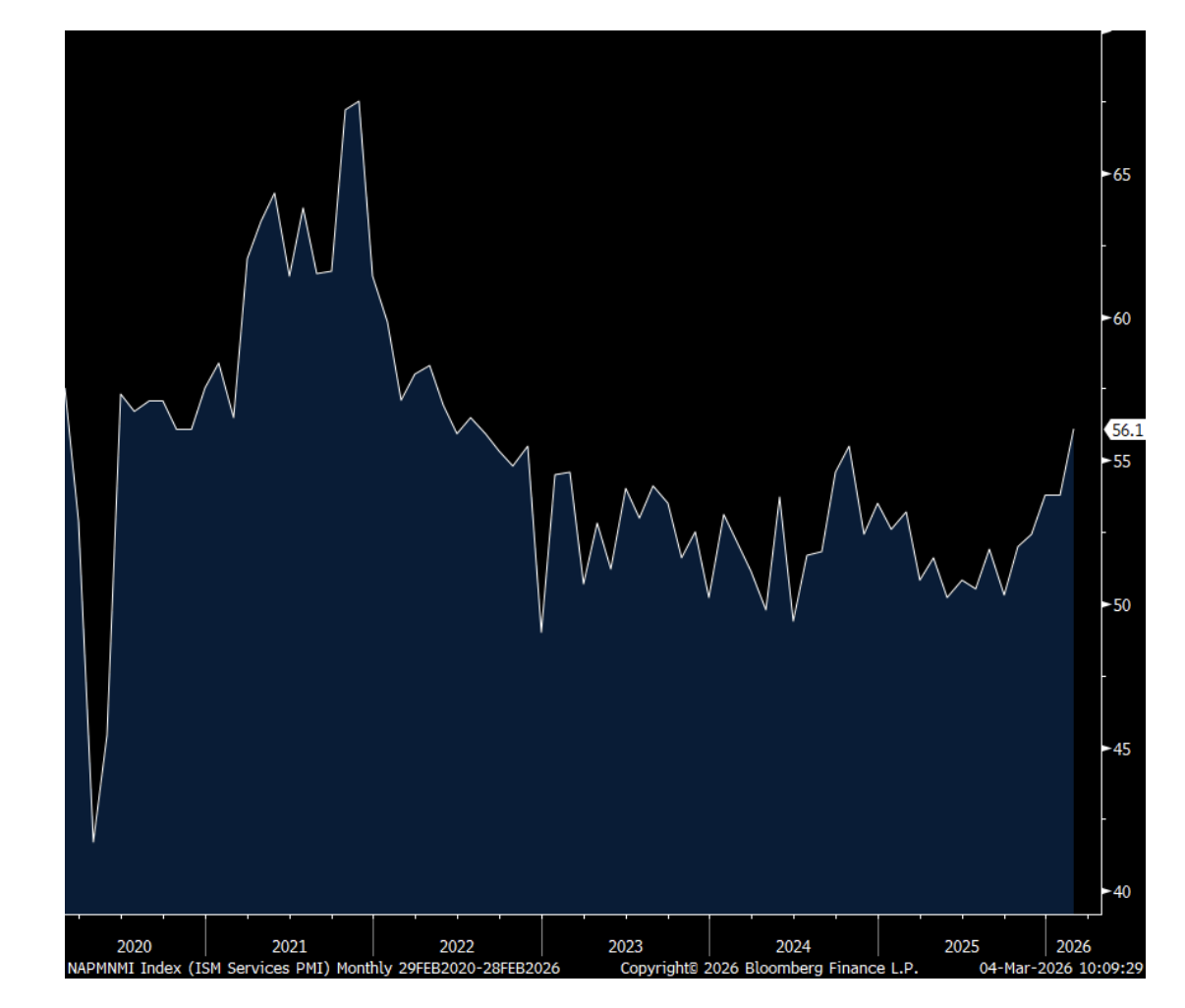

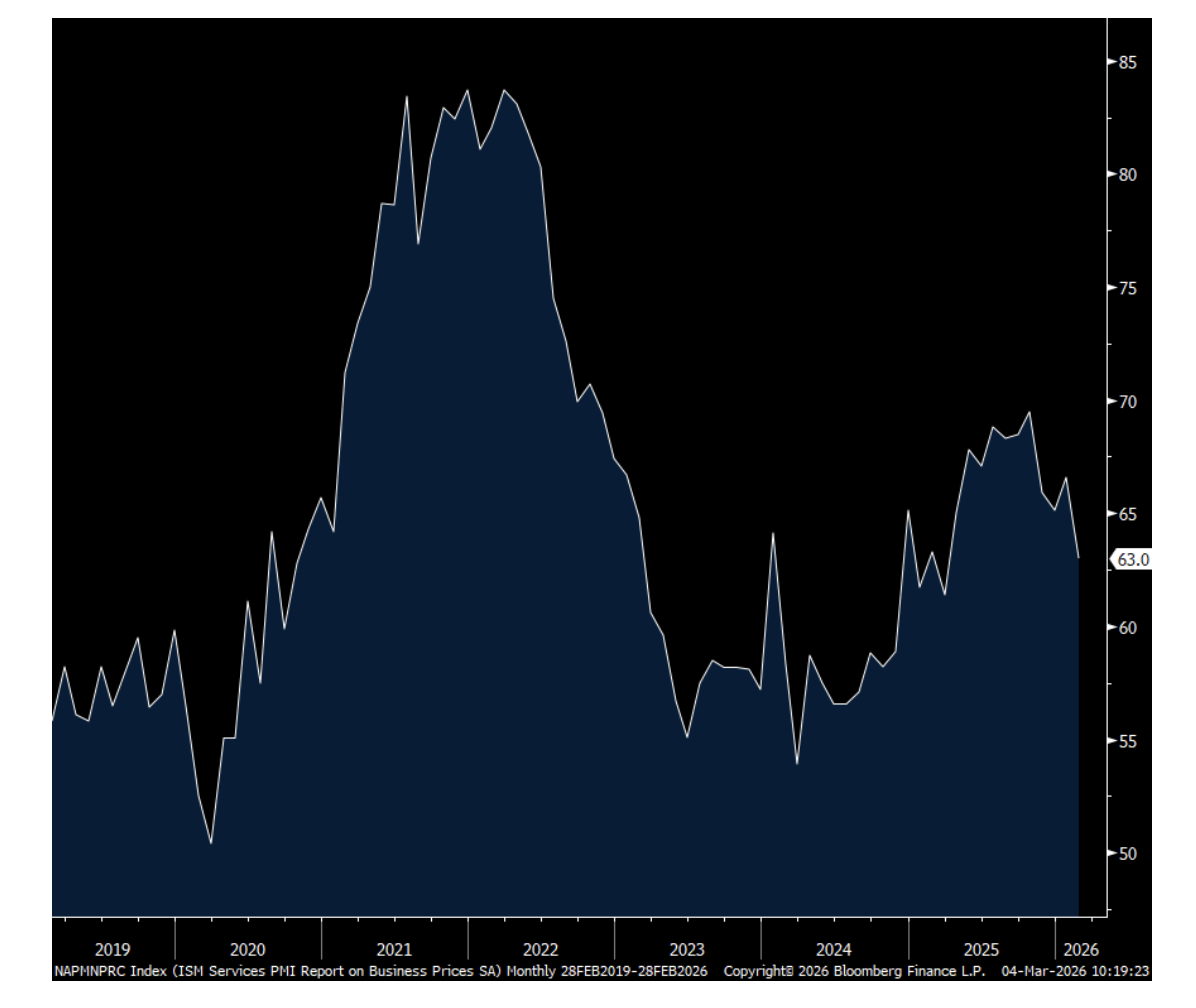

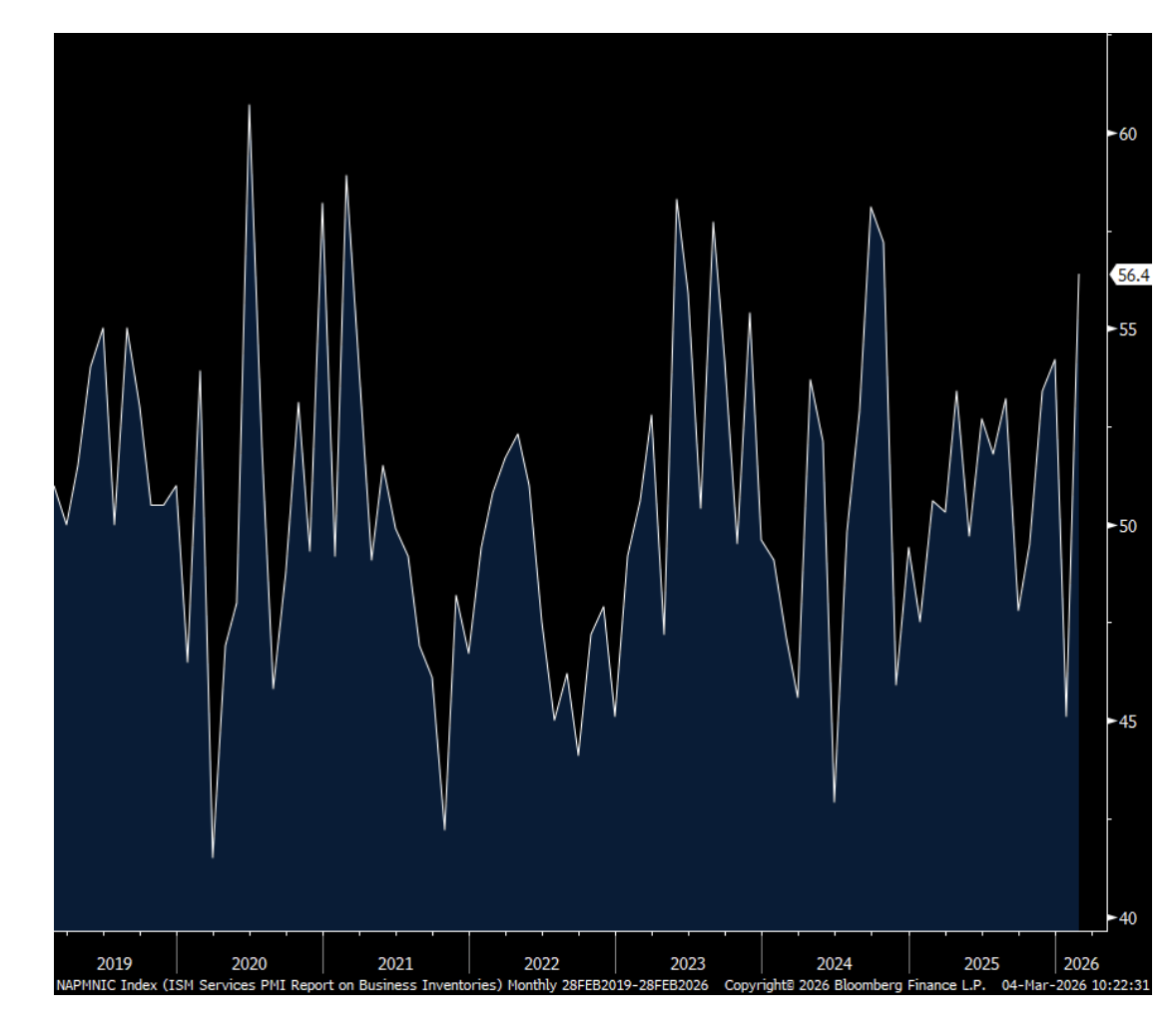

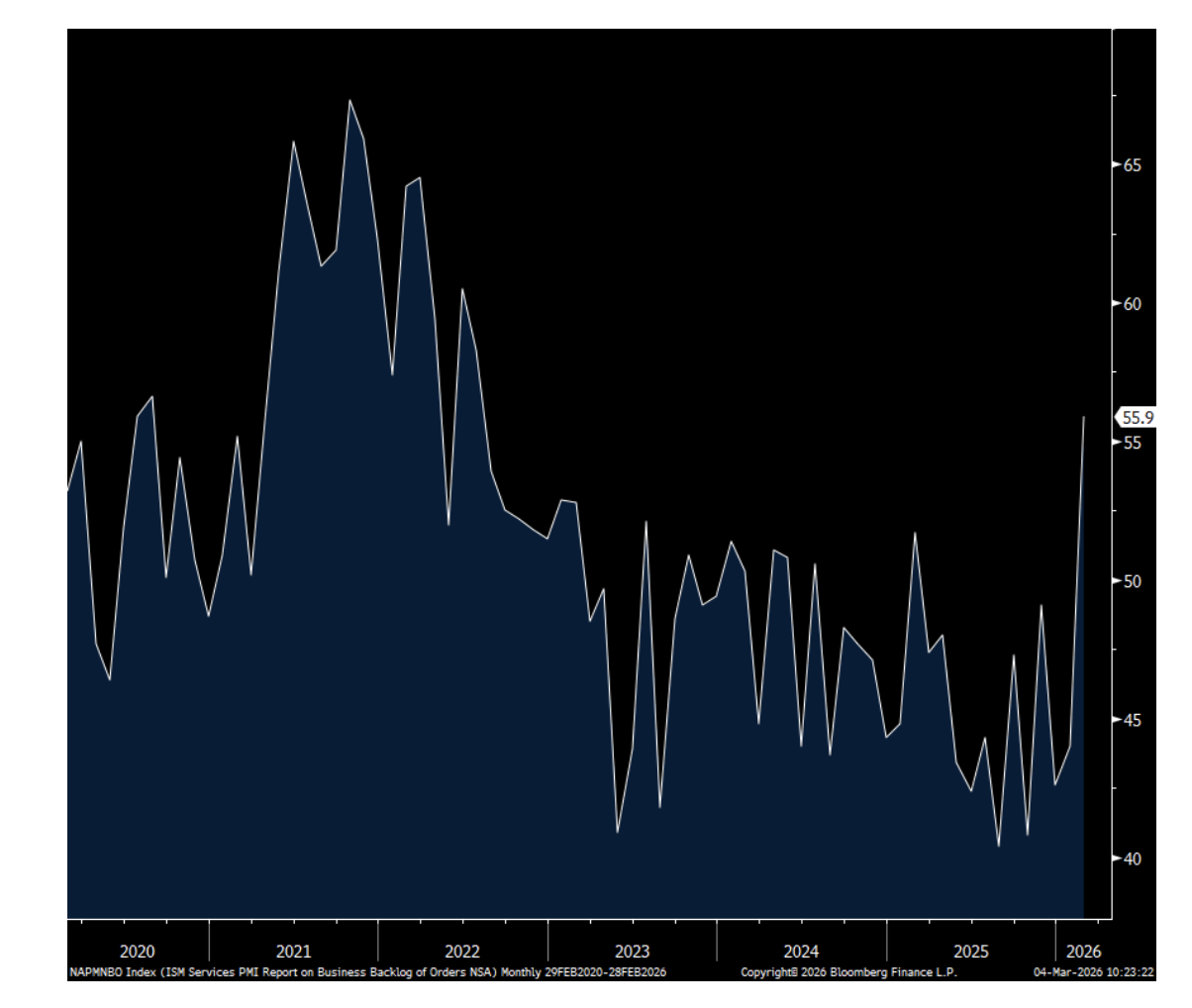

The February ISM services index jumped to 56.1 from 53.8 and well above the estimate of 53.5. That’s the best level since July 2022. The business activity component rose to 59.9 from 57.4 and almost 5 pts above its 6 month average.New orders were up by 5.5 pts to 58.6 and 4 pts above its half year average. Backlogs spiked by 12 pts to back above 50 at 55.9. A major factor in the lift in all of these stats was the 11.3 pt rise in inventories to 56.4. The ISM said with inventories, “Comments from respondents include: ‘After maintaining and reducing some inventories at the end of the year, inventory levels are starting to build up in preparation of the activity for the next three quarters’ and ‘Getting ready for spring volume.’Of note too, the employment component was 51.8, up 1.5 pts m/o/m and above 50 for a 3rd month. Supplier deliveries were little changed, down .3 pts to 53.9 while prices paid fell 3.6 pts, though still high at 63.Industry breadth improved too with 14 of 18 industries seeing growth vs 11 in January while 3 saw business decline vs 5 in the prior month.From the ISM, “The services sector is heating up…Gasoline was noted by some respondents as a commodity up in price for the first time since February 2025, and copper was up in price for the third month in a row. Commentary on trade uncertainty increased, with respondents commenting that tariff impacts have stabilized and are now embedded in supply chain costs. Although there were several comments on tariff uncertainty regarding the U.S. Supreme Court decision, there was no alarm regarding supply chain performance, suggesting that services companies have developed capabilities to routinely address shifts in tariff policies.” I will say though, this is mostly for bigger companies, not smaller ones which ISM doesn’t really capture here.Bottom line, the services sector continues to drive US growth and this data point was definitely good. Some inventory building was a factor and that came along with a big jump in backlogs. Strong end demand will be needed to keep this going.Here is a copy and paste of the company comments in a variety of industries:

ISM Services

Prices Paid

Inventories

Backlogs

BY Doug Kass · Mar 4, 2026, 11:15 AM EST

With S&P cash +52 handles I have moved to medium-sized short the Index calls.

BY Doug Kass · Mar 4, 2026, 10:30 AM EST

With S&P cash +32 handles I am adding to my short index calls.

BY Doug Kass · Mar 4, 2026, 10:19 AM EST

Adding to (MSOS) and (MSOX), again.

BY Doug Kass · Mar 4, 2026, 10:03 AM EST

As I suggested earlier the Iran/CIA dialogue was BS (and the reason I was shorting the indexes on strength):

09:36 *(IR) IRAN SEMI-OFFICIAL TASIM: DENY NYT REPORT THAT WE REACHED OUT TO CIA FOR TALKS TO END WAR **Reminder: earlier, Iran Intelligence Ministry reached out indirectly to CIA to discuss terms ending the Iran war a day after the war began; US officials are skeptical, at least in the short term, that either the Trump administration or Iran is really ready for an offramp - NYT

BY Doug Kass · Mar 4, 2026, 10:00 AM EST

Chart is from 9:36 a.m. ET

BY Doug Kass · Mar 4, 2026, 9:59 AM EST

With S&P cash +26 handles I am adding to my short index calls.

I have converted my short index common to short Index calls.

BY Doug Kass · Mar 4, 2026, 9:42 AM EST

From Peter Boockvar:

While it is a great idea to have a government insurance backstop for ships passing thru the Strait of Hormuz, the possible loss of life due to a drone strike is the offsetting factor in limiting passage so I think we need a cessation of Iranian attacks in order to really feel comfortable about flowing supplies again there.

This headline just crossed by news headlines on Bloomberg, *CONTAINER SHIP HIT WHILE TRANSITING HORMUZ: UKMTO SAYS

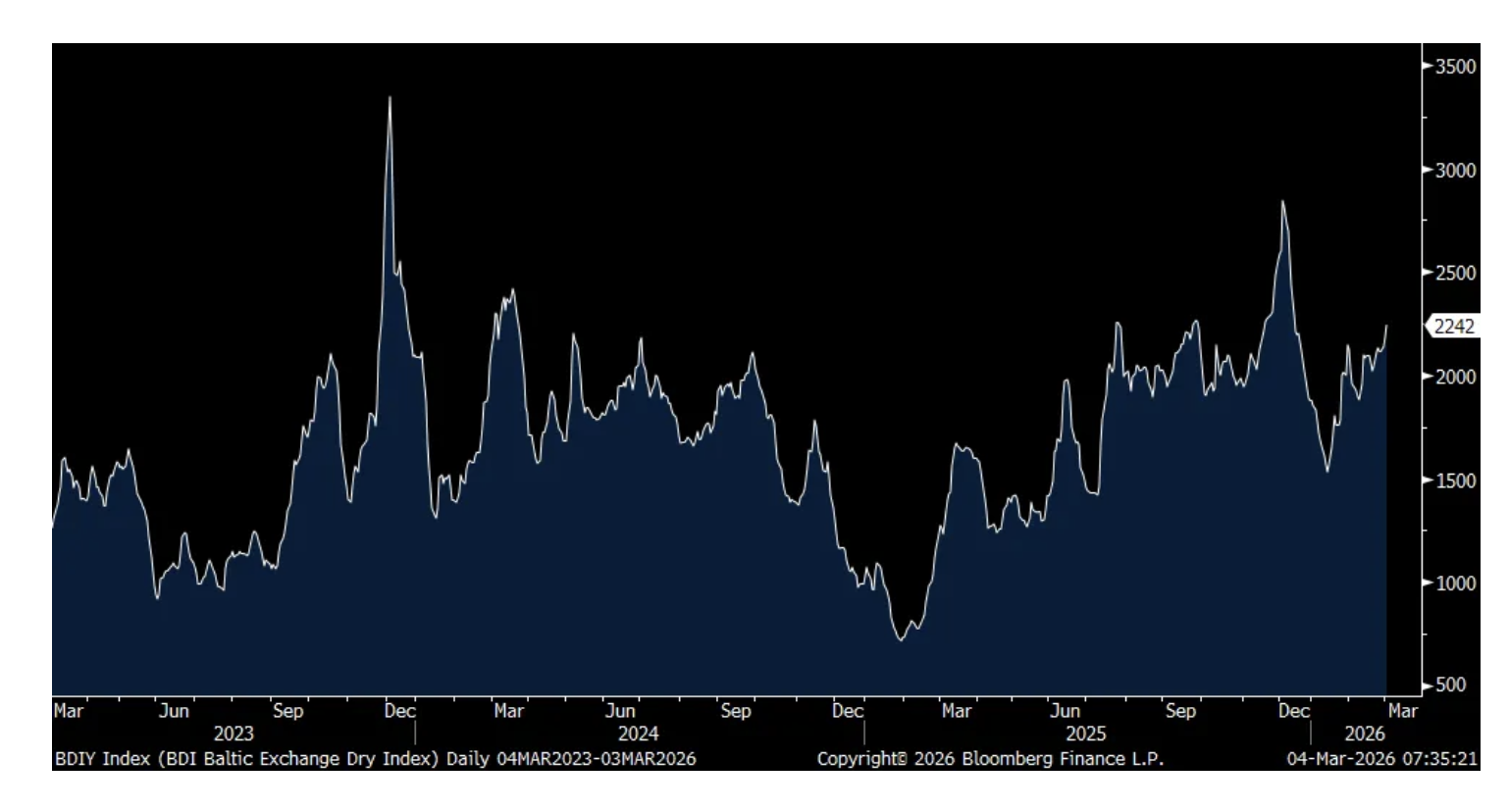

The Baltic Dry Index, taking stuff like grains and coal and less impacted by what’s going on in the Middle East, rose yesterday to the highest since mid December, though still well off its early December highs.

Baltic Dry Index

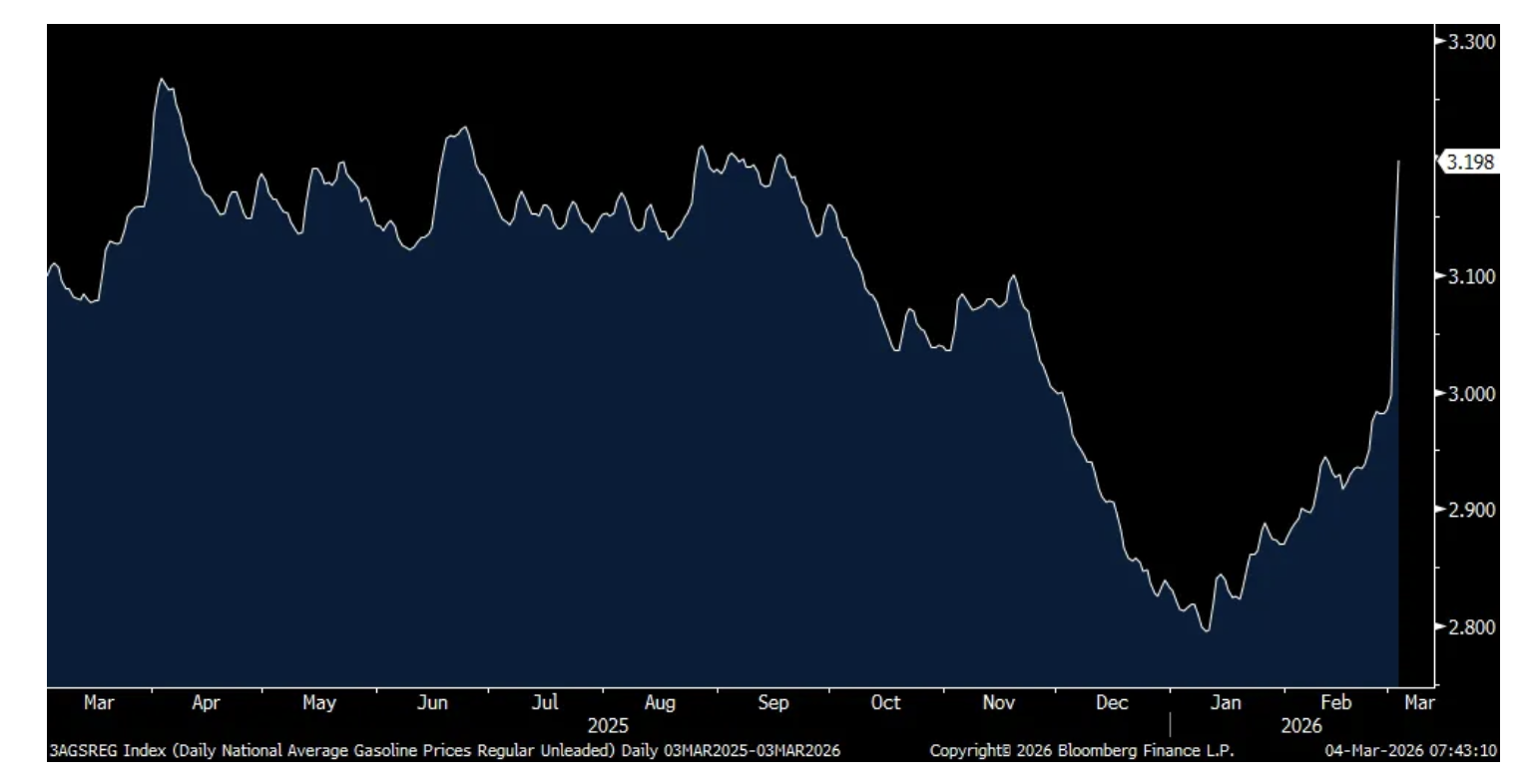

According to AAA, the average price of a gallon of gasoline at the pump is up $.20 over the past two days to $3.20 in the initial response to the crude jump.

AAA Average Gallon Price

Froth continued coming out of some Asian markets overnight, particularly South Korea where the Kospi was up about 80% in 2025 and around 40% up until Monday, mostly driven by Samsung and SK Hynix. Japan, a big importer of energy, too it on the chin by 3.6% while the Hang Seng was lower by 2%. I’m still a believer in the investment options overseas and believe opportunities are being created on this selloff.

BoJ Governor Ueda told us overnight that he still plans to raise rates again and the yen is getting a modest boost in response. He said to parliament, “While we intend to carefully monitor the impact of the situation in the Middle East, we believe it is appropriate to continue raising the policy rate and adjusting the degree of monetary accommodation if the economy and prices improve in line with our quarterly outlook.”

To my continued point about enjoying the deceleration in rental growth while it lasts because it won’t, this is what Barry Sternlicht said last week on the earnings call of Starwood Property Trust, a stock we own:

With regards to multi family where they own some buildings and lend to others, “I think it’s safe to say as we look forward that we have tailwinds now. The decreases in supply in the multi family market dropping 60%, 70% eventually, we will see record absorption’s of apartments in the last year in the US, record absorption’s.”

“So, with supply down and people still being unable to buy homes, we expect the multi family markets to turn around, and that will help our borrowers, and that will lower LTVs.”

More of what he said of interest. “The economy is bifurcated. I know the administration doesn’t like to talk about a K economy, but you see it. You see it in the hotel industry. The only sector of the market that was up last year was luxury. Every other sector, upscale, upper upscale, mid-scale, lower scale economy, everything was down.”

“And also cost to build, replacement costs continue to stay high. And while they may have dropped a little bit, the cost of building a home, they still remain well above our basis in almost any of the assets in our book. So, new supply will be hindered until rents begin to rise again.”

From Target, up 7% yesterday:

“sales trends have improved in recent months, showing early signs we’re on the right path...one month does not make a full year trend, but we’re encouraged by the healthy sales growth we’ve seen in February, and that’s been broad-based, and traffic’s played an important role there, and so we think that’s momentum on which to build.”

Best Buy rallied by 7% too and said this of note:

“We saw softer than expected sales in November and the beginning of December. We then experienced strong sales in the last two weeks of December and the start of January, and sales were negatively impacted by weather induced store closures during the last week of the quarter.”

“We were prepared for a promotional holiday, and the environment was even a bit more promotional than we factored heading into the quarter.”

“From a product category perspective, we delivered our 8th consecutive quarter of positive comparable sales in computing, driven by laptops, desktops, and accessories. In mobile phones, we delivered our 4th consecutive quarter of growth, driven by our expanded partnerships and in-store operating model improvements with large carriers. We grew our gaming category revenue, but at a much slower rate than the previous two quarters as expected. We also saw strong growth in newer and emerging categories, like AI glasses, 3D printers, collectibles and toys, health rings, and PC gaming handhelds. These positive growth categories were offset by declines in home theater and appliances.”

On their customer, “Consistent with the past several quarters, we expect to see a consumer who is still spending but is value focused and attracted to sales moments. Importantly, while customers continue to be thoughtful about big-ticket purchases, they are willing to spend on high price point products when they need to or when there is technology innovation. We do expect consumers to spend a portion of their higher tax refunds at Best Buy concentrated in the first quarter.”

From Ross Stores, the value retailer and whose stock is jumping pre market:

They saw a 9% comp gain as “our business momentum accelerated further in the 4th quarter with both sales and earnings significantly surpassing our expectations.”

“We were quite pleased with the health of the comp growth as it was driven mainly by an increase in transactions and customers, with a modest increase in basket. We saw broad based strength across both departments and geographies. Every major merchandise category showed solid positive sales growth, with shoes and cosmetics performing the best.”

They saw particular strength in their women’s business, a recovery in home and “we finished up the holiday quarter with very strong business in toys.”

From On Holdings and whose stock fell 6% yesterday because of a guidance miss but still saw overall strong growth:

“We had a good start into the year across all the different regions. We expect that the first half of the year is growing slightly higher than the full year. We leave in some cushioning for the second half of the year. We indicated that we have a strong order book, which puts us in a good position also for the second half to deliver additional growth. So I think the momentum that we have seen in our numbers in 2025, and especially into Q4, just reflects the momentum of the brand.”

From Thor Industries, the RV maker and whose stock was down 6% yesterday too:

“Our fiscal second quarter results reflect continued execution in line with our expectations in a challenging retail environment...Even in a down market, our teams continuously demonstrate the ability to drive performance through operational focus and thoughtful capital deployment.”

“As we enter the spring selling season...Dealer engagement remains strong, consumer interest in the RV lifestyle continues to be encouraging and our innovation pipeline is robust.”

Business overall is still tough as shipments fell 23% in the quarter for towable RVs. Their motorized segment did much better with shipments up 28% “that was bolstered by shipments to rental customers as well as products that continue to resonate with customers at critical retail price points.”

On the guide, “Recent geopolitical events have clouded our outlook, though, and have created too much short term uncertainty for us to raise our full year guidance at this time...we remain mindful of broader consumer uncertainty and how recent events could impact that uncertainty.”

From Auto Zone that was also down 6% yesterday as bad weather impacted their numbers:

“Our domestic DIY same store sales grew 1.5%, while our domestic commercial sales grew 9.8% vs last year’s Q2.”

“While our commercial sales increase was below our expectations, our results were negatively impacted due to the winter storms across much of the country during the last four weeks segment of the quarter.”

“With regard to inflation’s impact on DIY sales, we saw like-for-like same SKU inflation up north of 6% for the quarter, which contributed to our DIY average ticket being up 5.2%.”

“Based on our inflation expectations, we continue to expect our average ticket to grow sequentially through the 3rd fiscal quarter, which ends in May, and then peak during the 4th quarter where we will begin to lap the increases in inflation we saw in this past year’s 4th quarter.”

In contrast to Norwegian Cruise, Viking had a better quarter. They said this of note:

“we increased the capacity by 12% y/o/y. This reflects both the expansion of our fleet and the continued demand for our product. At the same time, our net yields grew 7.4%, demonstrating our ability to attract high quality demand and to maintain pricing power. Together, these factors drove a 21.9% increase in total revenue, which reached a record of $6.5 billion in 2025.”

“Occupancy for the period was 95%...these results reflect the strong demand from our core consumer, the loyalty of our guests, the value of our premium products...”

“As of February 15, we were already 86% booked for the 2026 season. This is in line with the same time last year, while our capacity is increasing by 7%.” Their advanced bookings are 13% above 2025 levels at the same point last year.

To some economic data, refi’s rose by another 14% w/o/w with mortgage rates holding at multi year lows at 6.09% on average. Purchase apps after 5 weeks of declines rebounding by 6.1% w/o/w.

Ahead of the US ISM services index, the Eurozone and UK services PMI’s were left about unrevised from its initial print. They stand at 51.9 and 53.9 respectively and continue to contribute most of the economic growth in Europe.

China’s private sector PMI for February improved for both manufacturing and services with the former up to 52.1 from 50.3 and the latter jumping to 56.7 from 52.3. Say what you will about China, but the world can use stronger economic growth there.

Also out was the PMI for Singapore which was quite the bright spot at 59.2 vs 56.8. We remain positive and long Singapore stocks. Hong Kong’s PMI was 53.3 vs 52.3.

BY Doug Kass · Mar 4, 2026, 9:20 AM EST

BY Doug Kass · Mar 4, 2026, 8:59 AM EST

BY Doug Kass · Mar 4, 2026, 8:50 AM EST

11:30 a.m.: Treasury hosts a $69B 17-Week Bill Auction;

2:00 p.m.: Treasurybuyback (liq support);

7:00 p.m.: Fed Bank of Chicago President Goolsbee (Non-Voter) speaks at the Foreign Policy Association Financial Services Dinner

BY Doug Kass · Mar 4, 2026, 8:35 AM EST

As telegraphed earlier, I am a seller on strength.

With S&P futures back +28 handles I am shorting the indexes:

* (SPY) $682.82

* (QQQ) $605.68

BY Doug Kass · Mar 4, 2026, 8:32 AM EST

Knowledge@Wharton:

BY Doug Kass · Mar 4, 2026, 8:20 AM EST

BY Doug Kass · Mar 4, 2026, 8:17 AM EST

BY Doug Kass · Mar 4, 2026, 8:10 AM EST

BY Doug Kass · Mar 4, 2026, 8:00 AM EST

BY Doug Kass · Mar 4, 2026, 7:50 AM EST

* So sick and tired of pros not taking ownership of investment boners...

BY Doug Kass · Mar 4, 2026, 7:40 AM EST

S&P futures are now flat (having given up a near +30 handle rally off of BS story referenced earlier).

Doug's Daily Diary - TheStreet Pro

We just covered our index shorts for a profit:

* (SPY) $680.19

* (QQQ) $602.06

BY Doug Kass · Mar 4, 2026, 7:29 AM EST

BY Doug Kass · Mar 4, 2026, 7:20 AM EST

BY Doug Kass · Mar 4, 2026, 7:10 AM EST

I am a (short) seller on any strength.

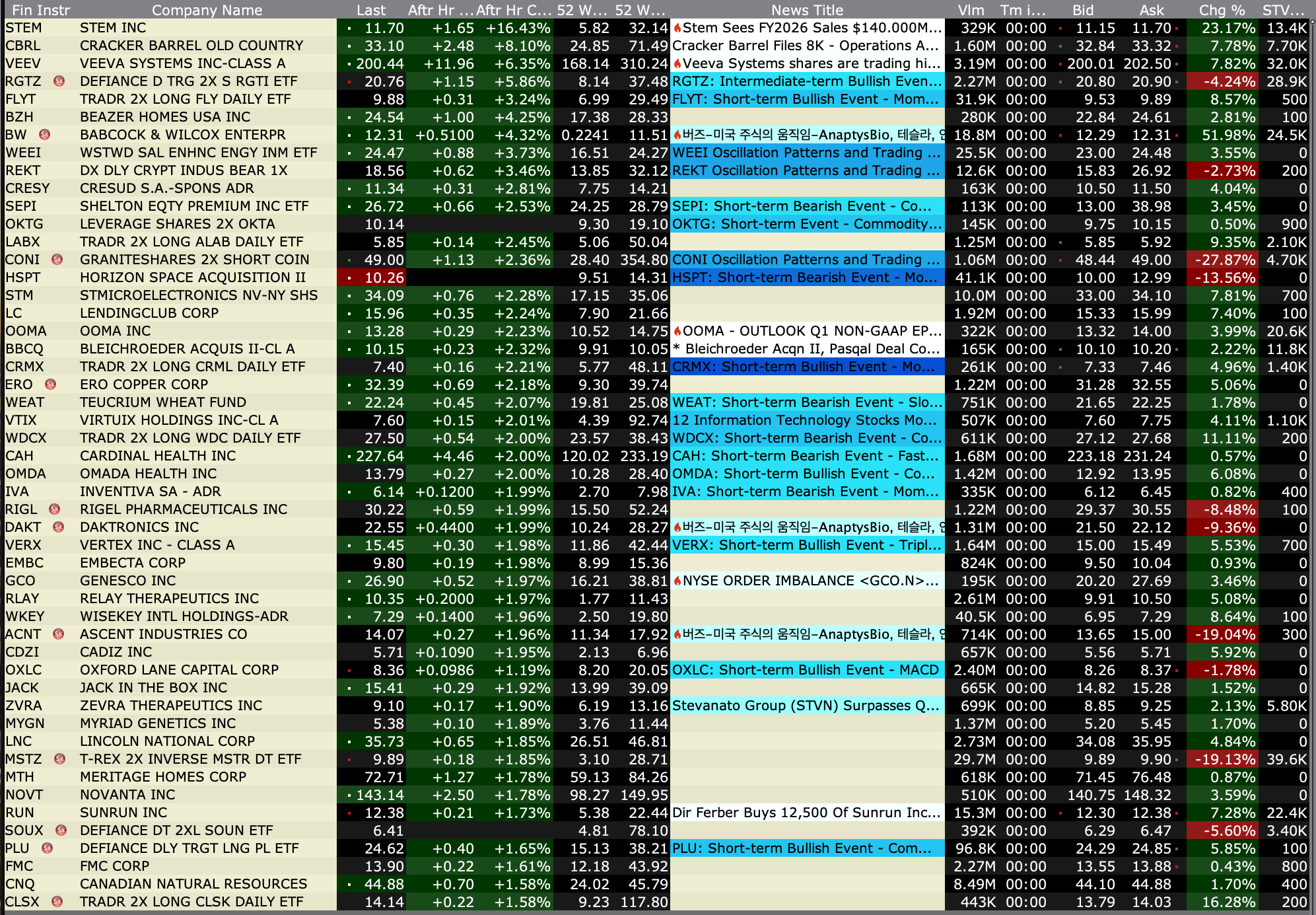

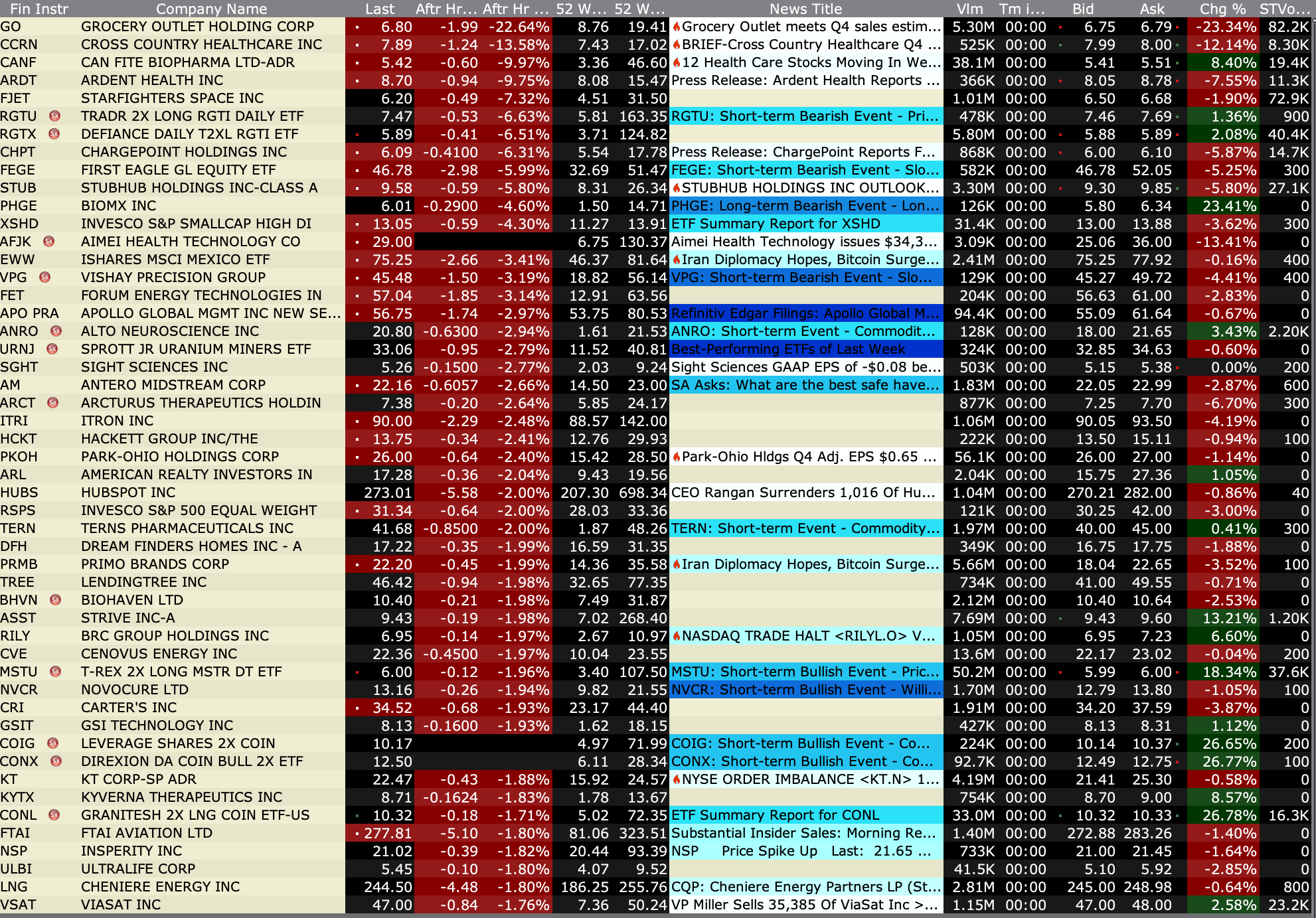

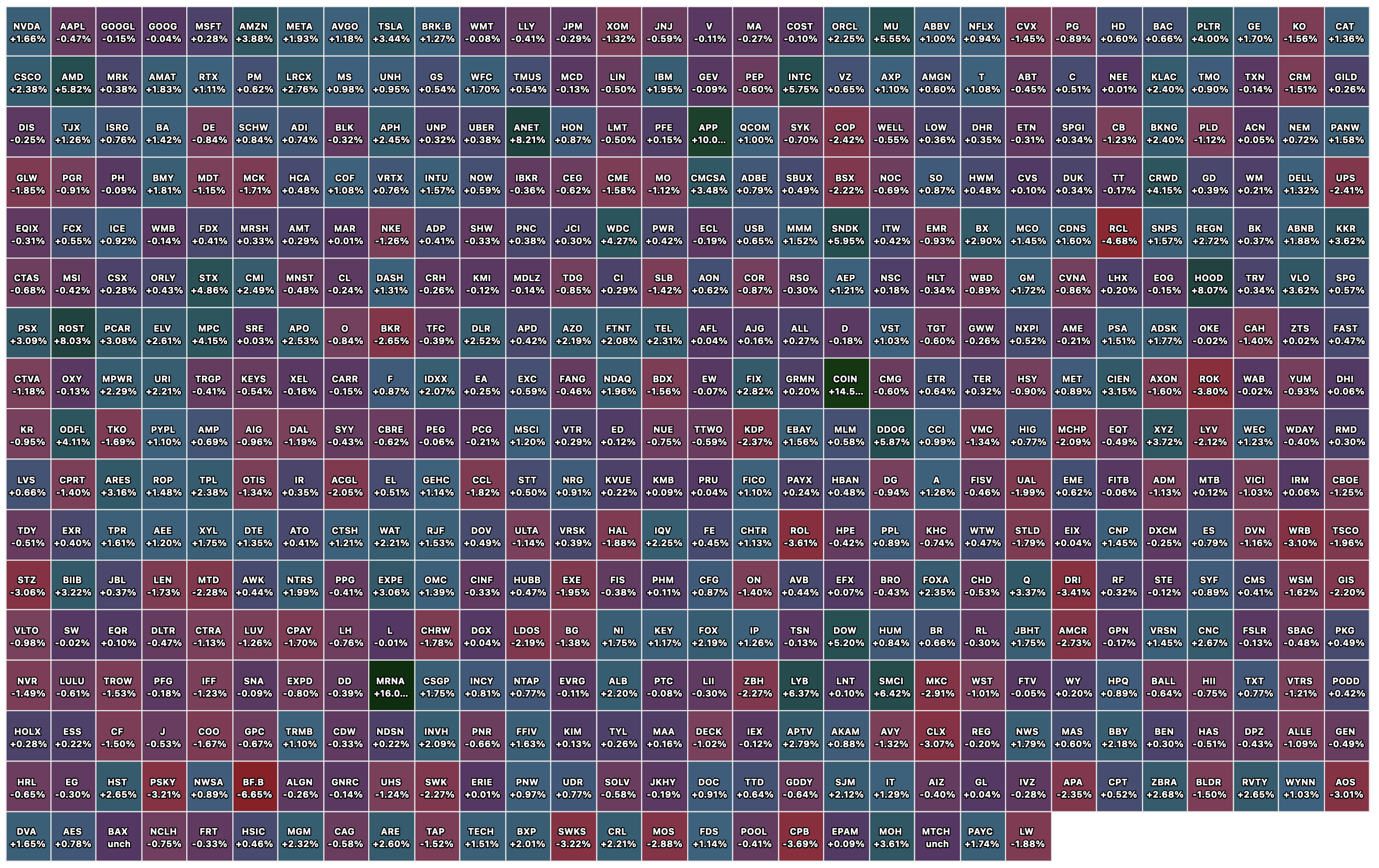

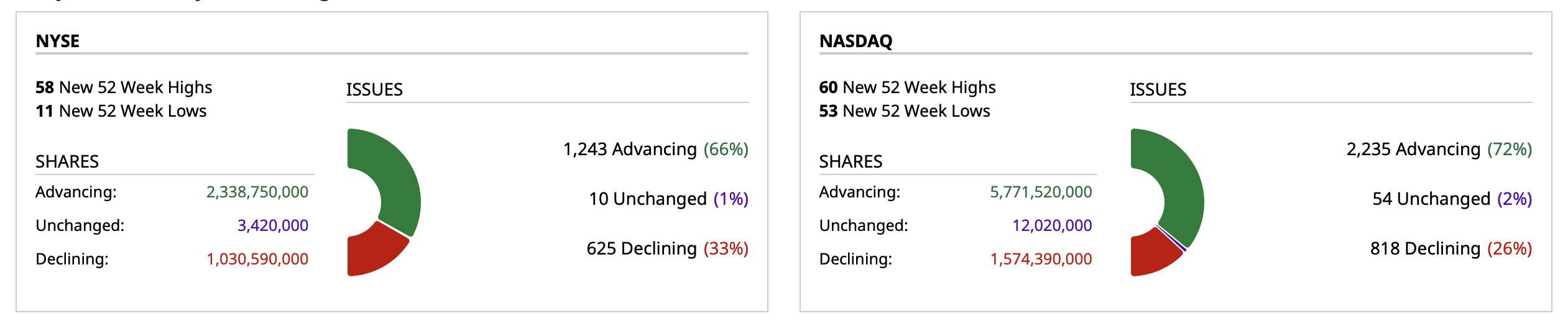

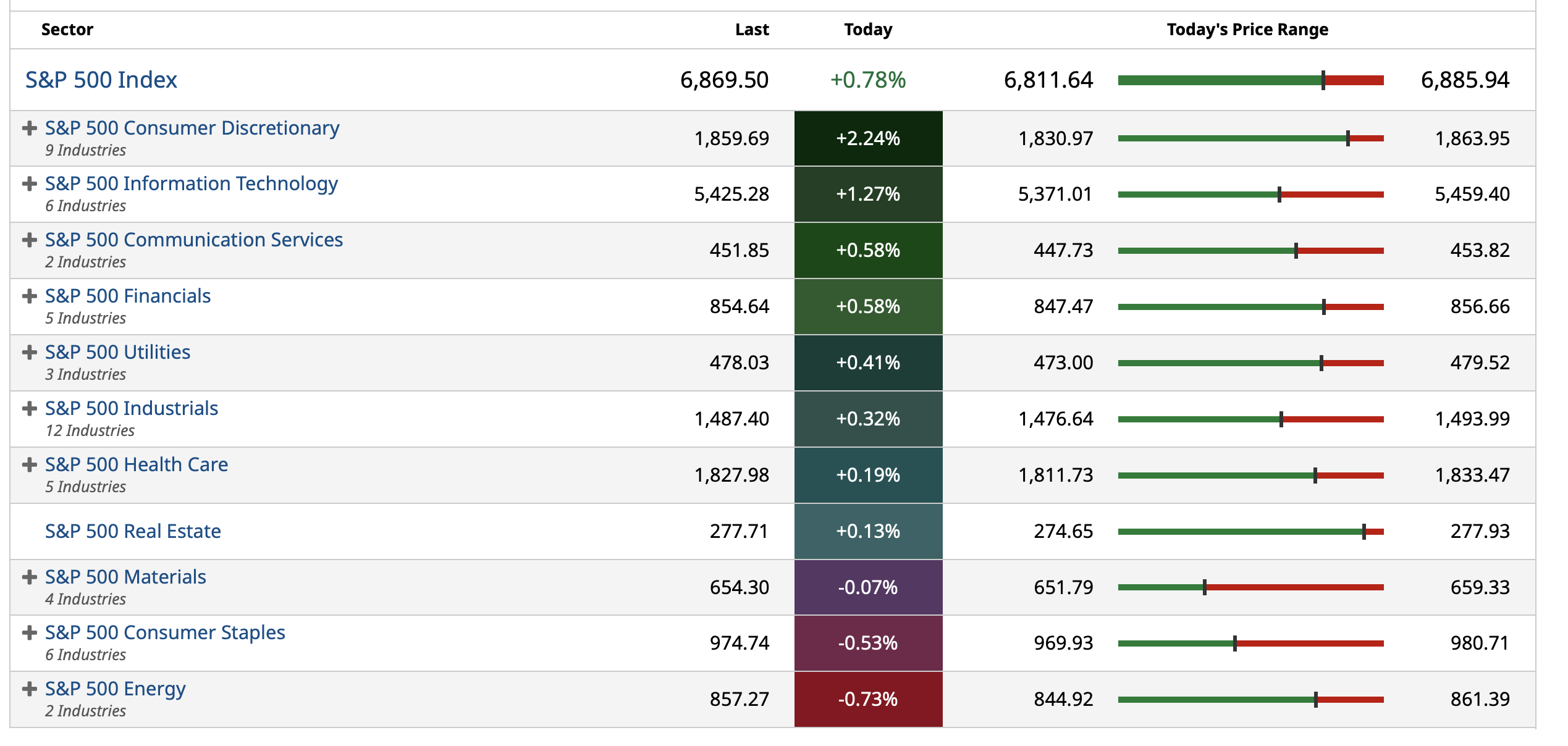

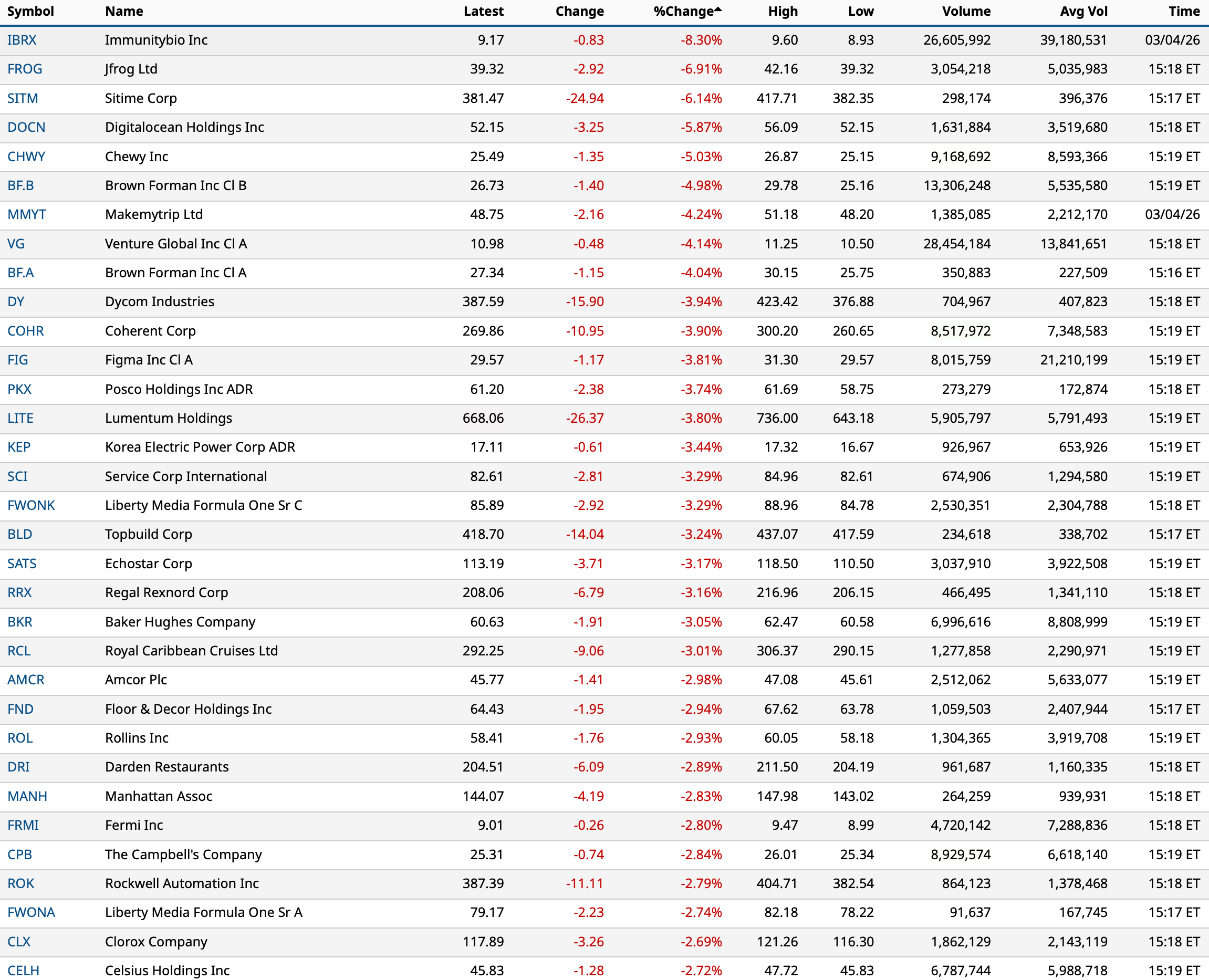

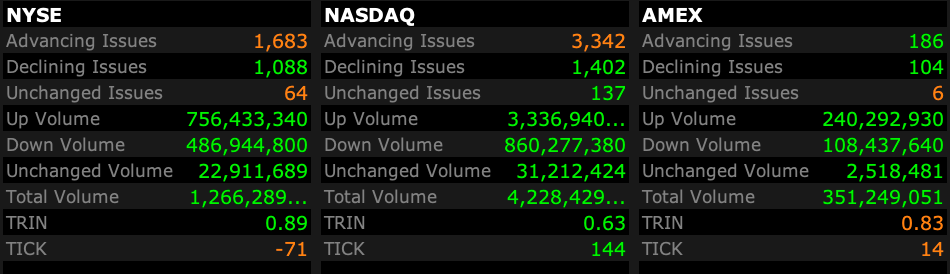

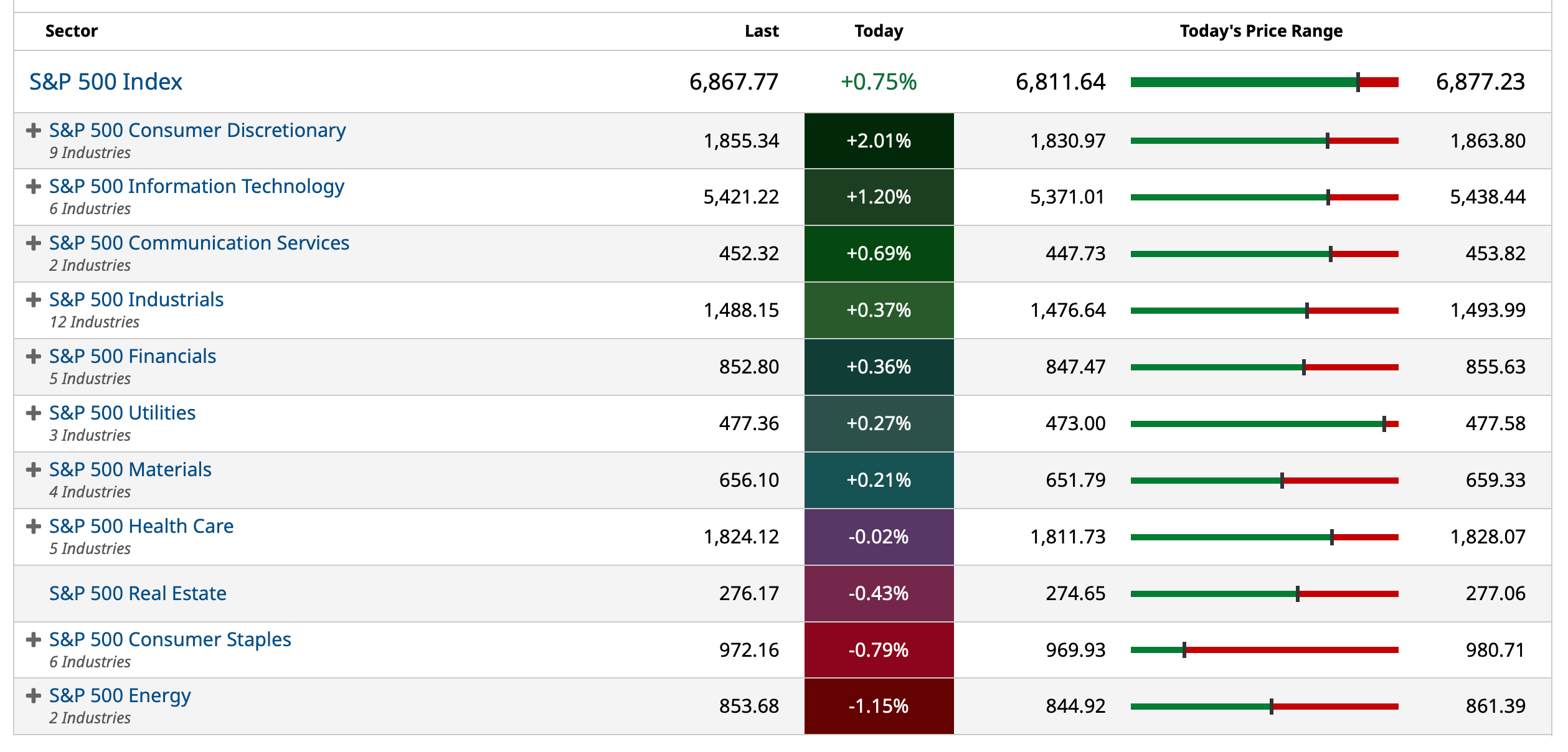

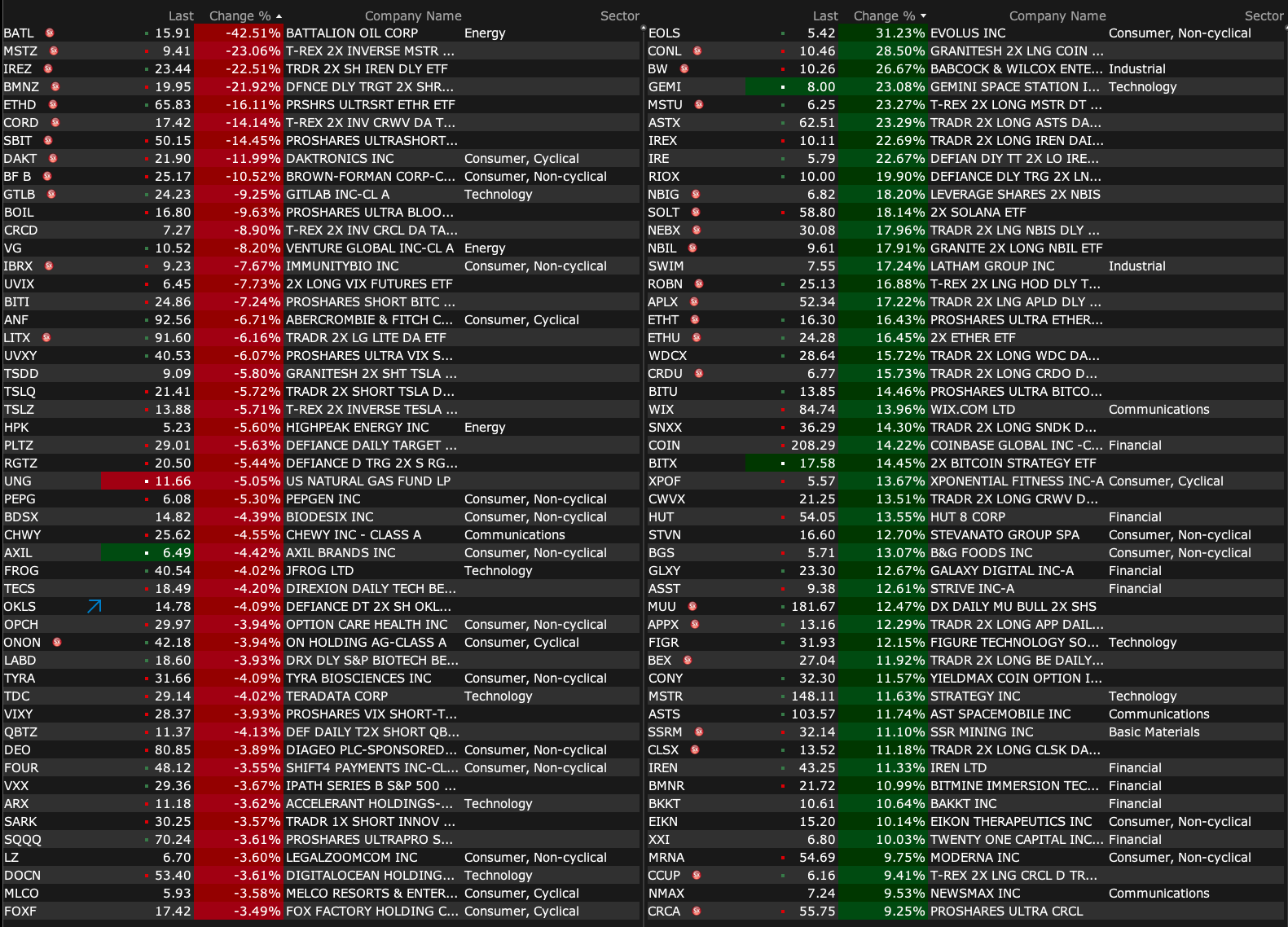

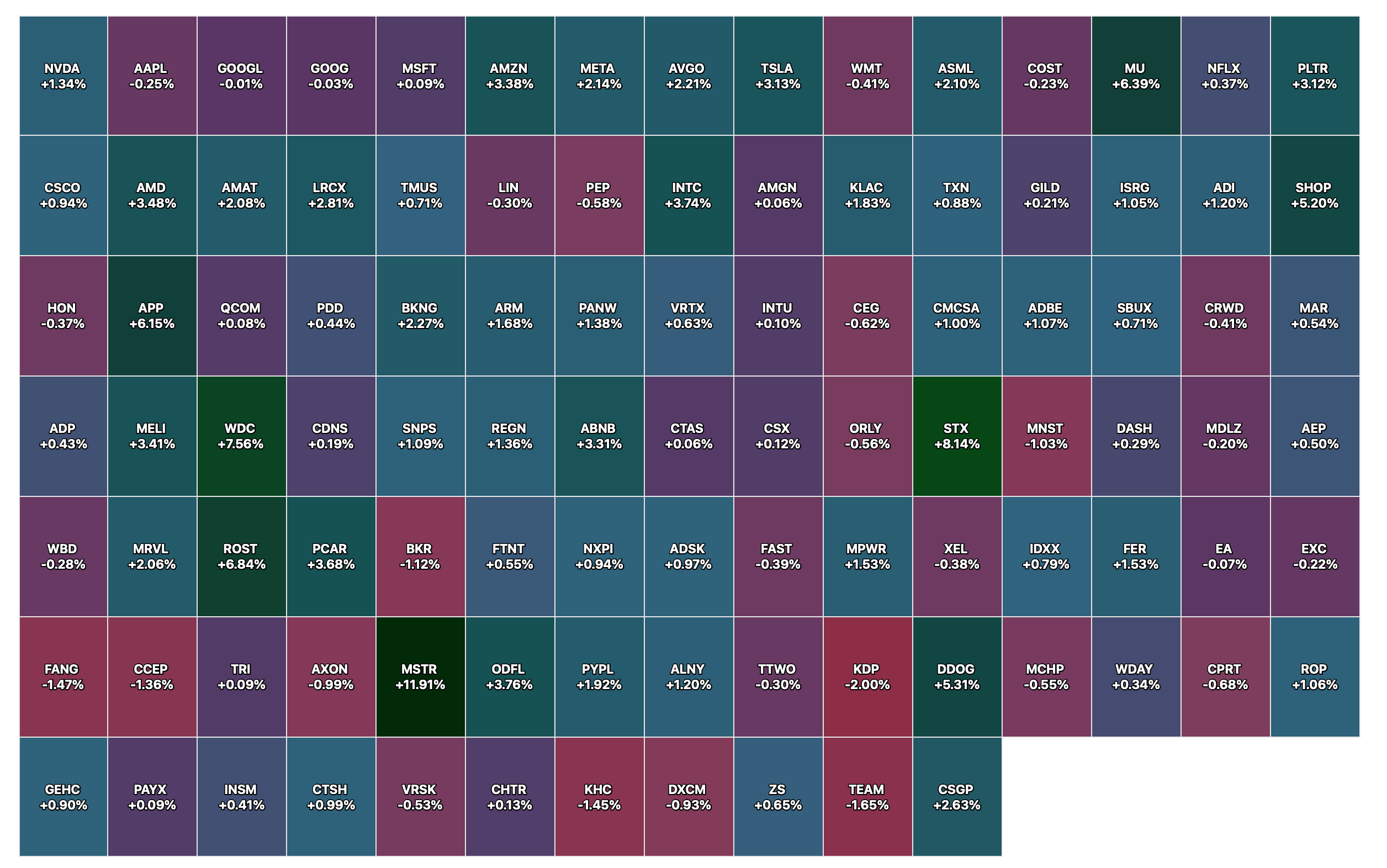

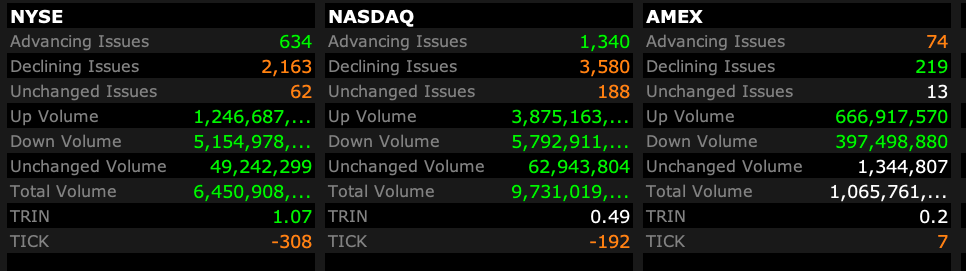

Market breadth had a foul odor yesterday:

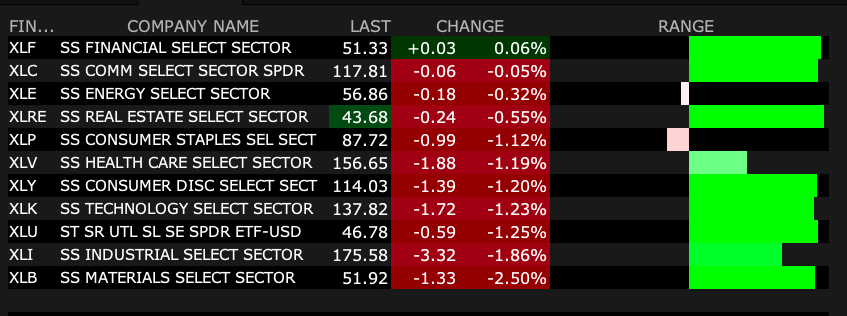

As well, there was broad-based sector weakness:

While the rally off of the lows has been impressive (+100 S&P handles), one of the reasons I re-shorted the indices was the fact that (at 1:30PM only 1 of 11 sectors was positive. (Note: By day's end every sector was lower!):

By Doug Kass Mar 3, 2026 2:19 PM EST

BY Doug Kass · Mar 4, 2026, 7:00 AM EST

About 30 minutes ago, there was a BS tweet that Iran is reaching out to the CIA for a possible ceasefire.

I shorted (SPY) and (QQQ) +28 handles on the gap higher in reaction to that tweet:

* SPY $682.35

* QQQ $604.37

BY Doug Kass · Mar 4, 2026, 6:49 AM EST

Chart of the Day:

Rotational Investing (@rotationalinvesting): "Looks like oil is going for the leadership position."

Bonus — Here are some great links:

BY Doug Kass · Mar 4, 2026, 6:45 AM EST

Most investors in the U.S. are not cognizant of the carnage over there over the last few days:

and...

BY Doug Kass · Mar 4, 2026, 6:35 AM EST

BY Doug Kass · Mar 4, 2026, 6:25 AM EST

I found Hamidreza Azizi to be a good source on the Middle East:

He chronicles the conflict:

BY Doug Kass · Mar 4, 2026, 6:15 AM EST

* South Korea's Kospi plunges...

BY Doug Kass · Mar 4, 2026, 6:05 AM EST

I have taken a small trading short rental in bitcoin (+5.2% this morning):

I won't be holding this position long — just shorting the overbought.

BY Doug Kass · Mar 4, 2026, 5:55 AM EST

The S&P Short Range Oscillator just moved back into oversold at -0.65% vs. 0.93%.

BY Doug Kass · Mar 4, 2026, 5:45 AM EST