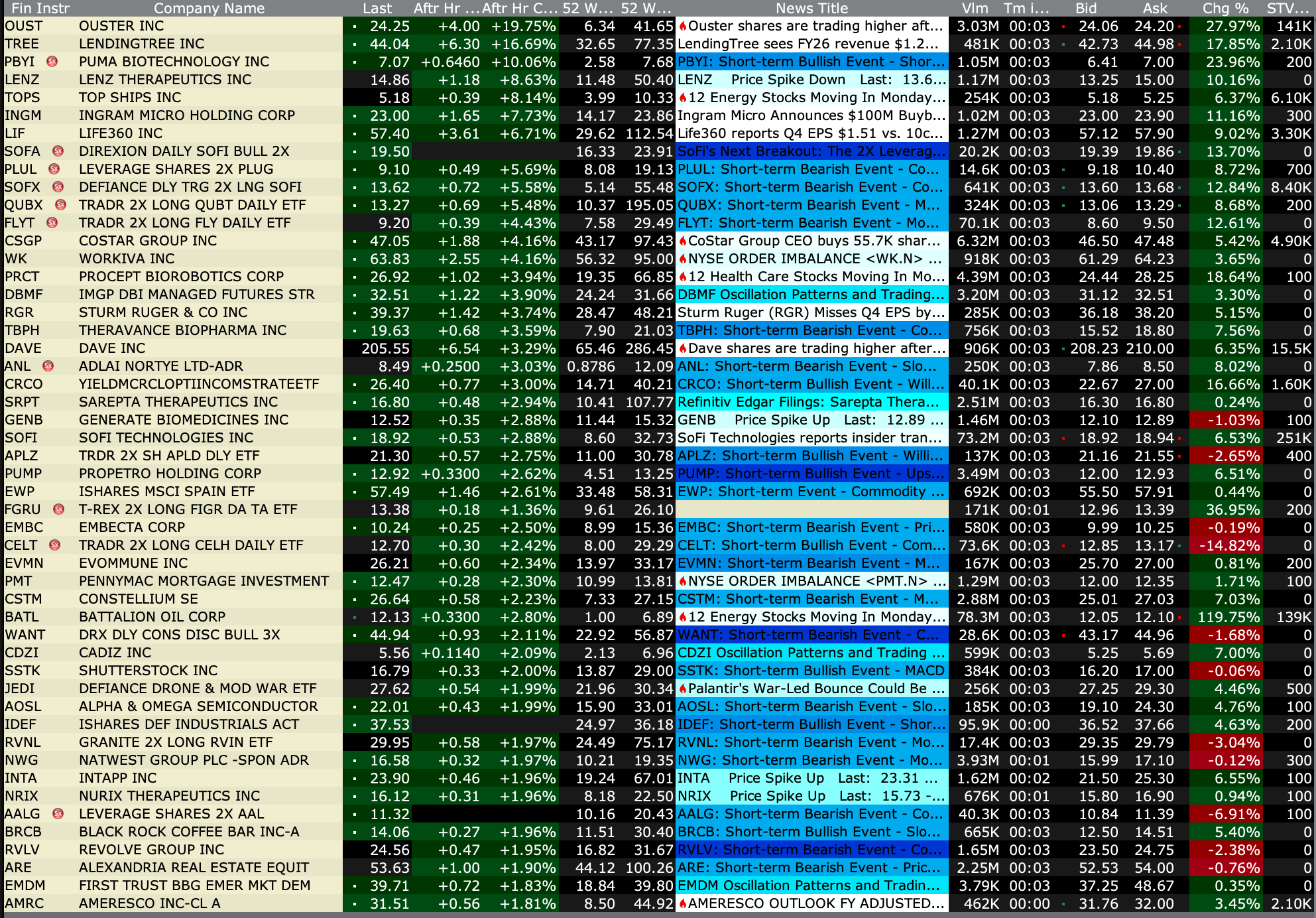

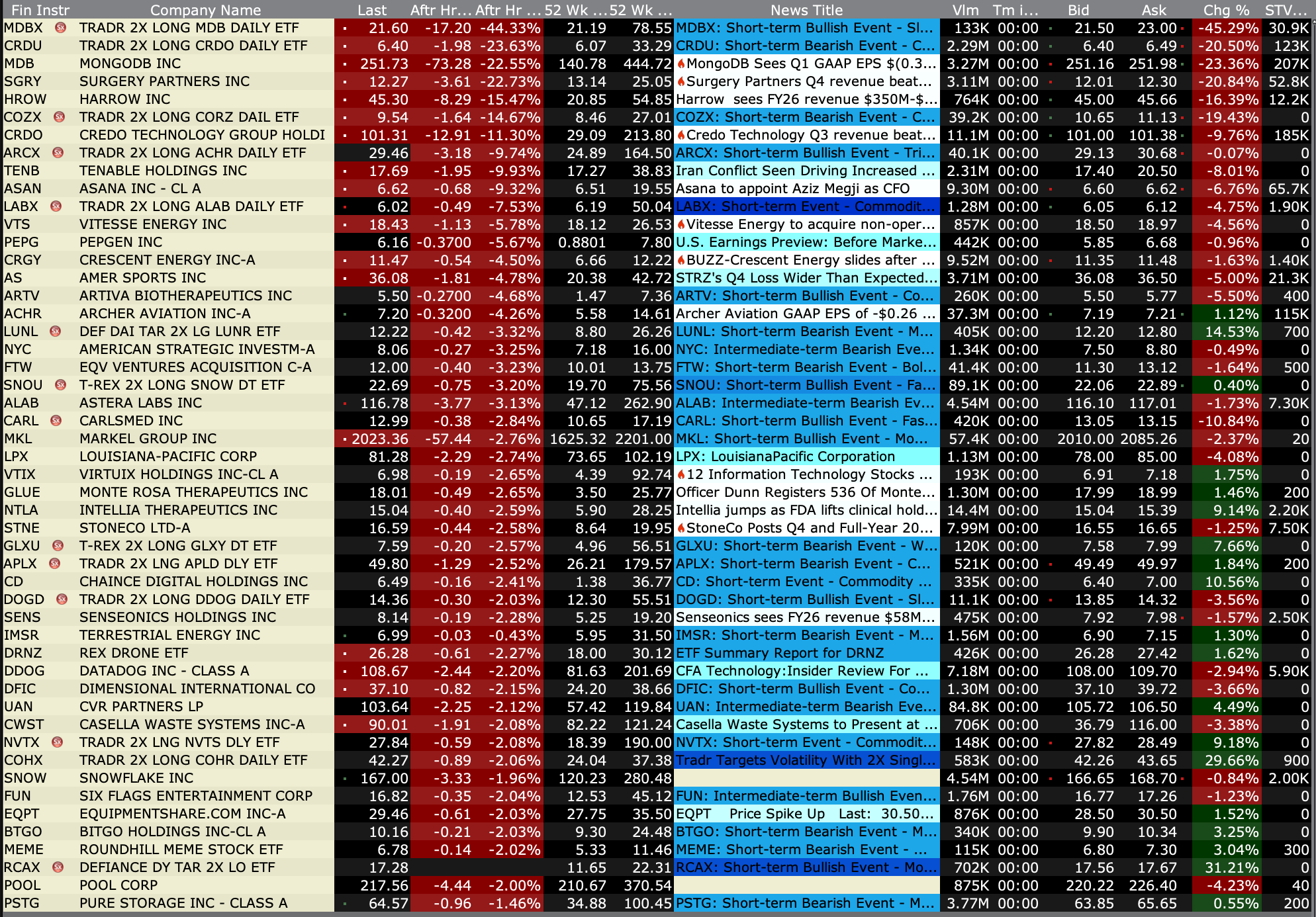

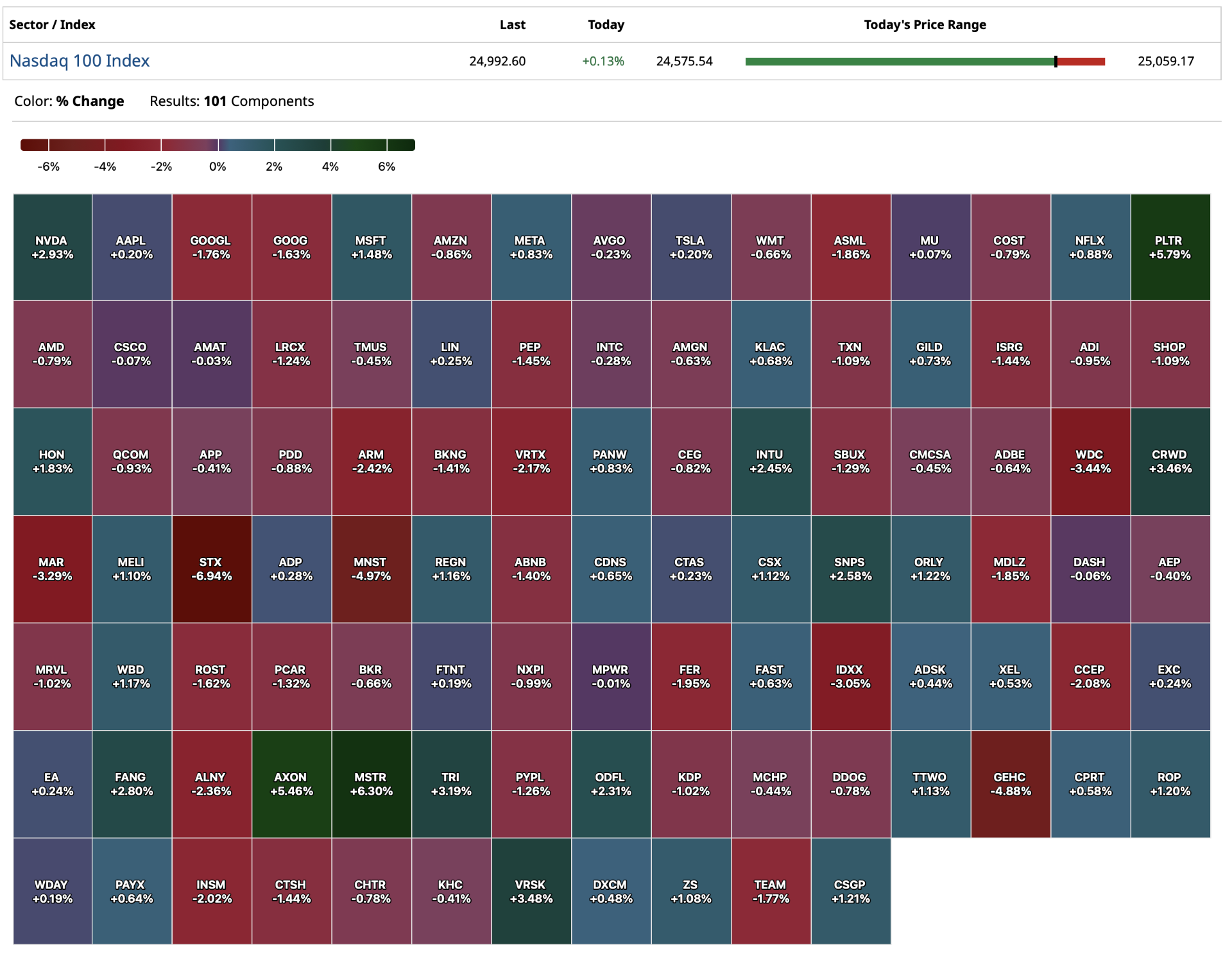

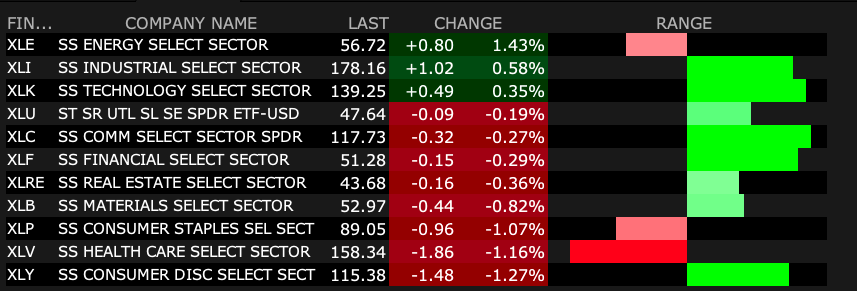

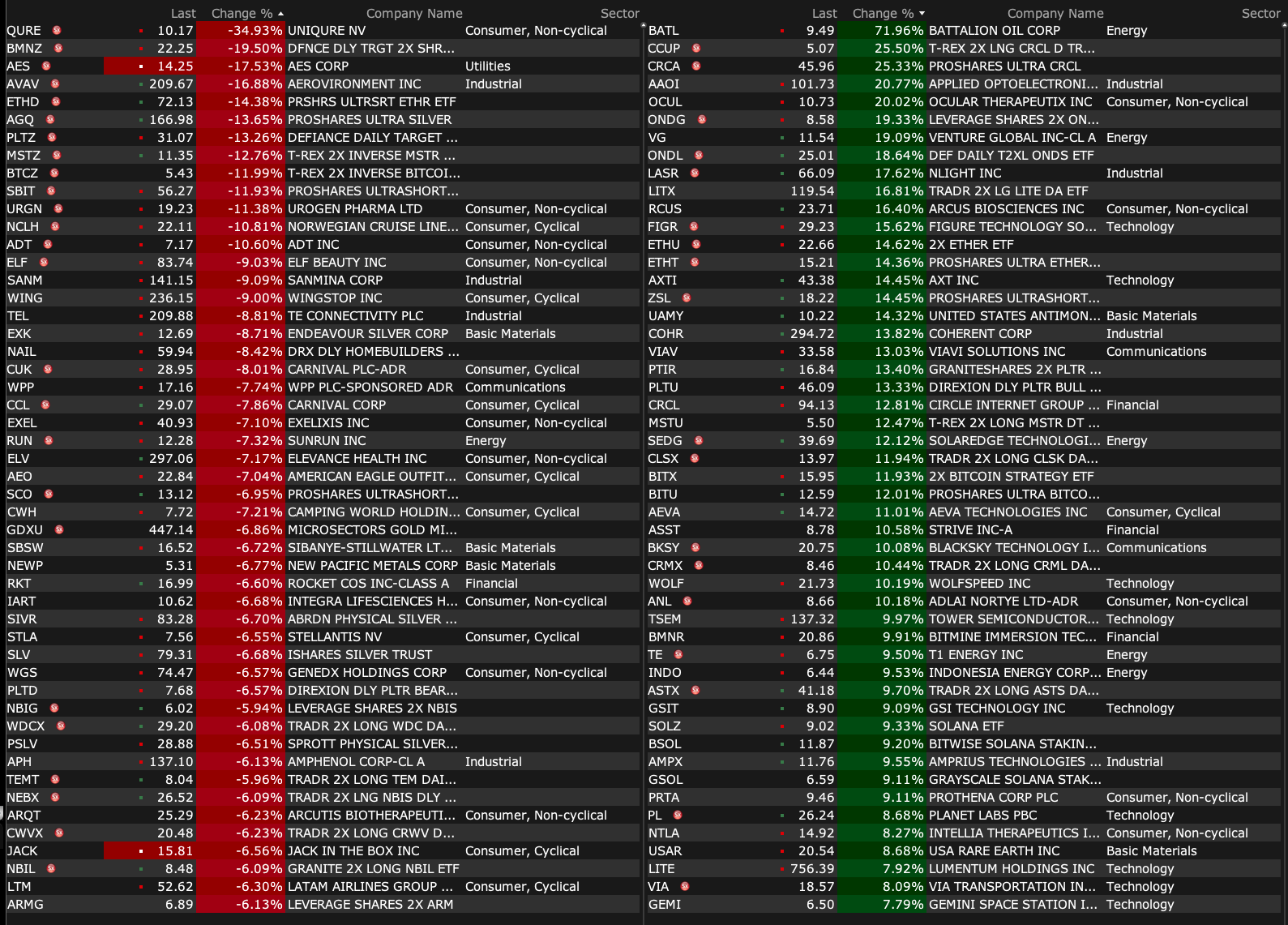

After-Hours Advancers and Decliners

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Mar 2, 2026, 5:00 PM EST

BY Doug Kass · Mar 2, 2026, 5:00 PM EST

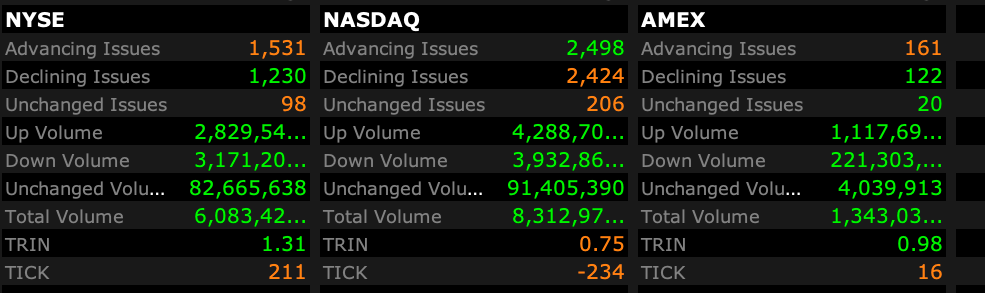

- NYSE volume 10% above its one-month average

- NASDAQ volume 7% below its one-month average

- VIX index: up 7.75% to 21.40

BY Doug Kass · Mar 2, 2026, 4:40 PM EST

Paulie C

Good stuff on UBER ☺

Dougie Kass

Several problems with UBER.

BY Doug Kass · Mar 2, 2026, 4:15 PM EST

BY Doug Kass · Mar 2, 2026, 3:37 PM EST

Stocks swoon after this report:

With S&P cash -8 handles after being up greater than 20 handles, I have taken off my short SPY calls for a profit (again).

BY Doug Kass · Mar 2, 2026, 3:27 PM EST

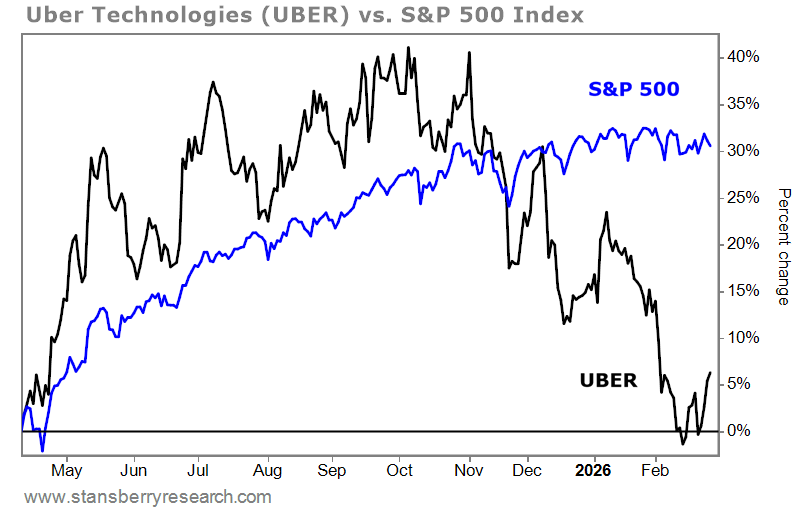

I have been doing some research on Uber (UBER) over the last two weeks — with the share price dropping from over $100 to close to $70.

I have taken a very small starter position in the name, preferring to add in the low $70s.

My pal Whitney Tilson on Uber:

Uber Technologies (UBER) is back on my radar screen...

As longtime readers will recall, I took a "first look" at the ride-hailing and food-delivery giant in my April 10 e-mail last year.

At the time, I was impressed with Uber's growth in revenue, operating income, and free cash flow ("FCF"). But I concluded that its forward price-to-earnings (P/E) multiple of about 30 times was "too high a price for me." I also warned about "the threat from Waymo and other self-driving vehicle services."

It was a good call...

Uber has risen by only 6% since then, while the S&P 500 Index has jumped 31% over the same period:

However, the stock hit my radar screen again a month ago when private stock and real estate investor David Leiter pitched it at the ValueX conference in Switzerland.

David kindly gave me permission to share his full presentation with readers, so I'll do so today. Afterward, I'll also share my thoughts on the stock right now...

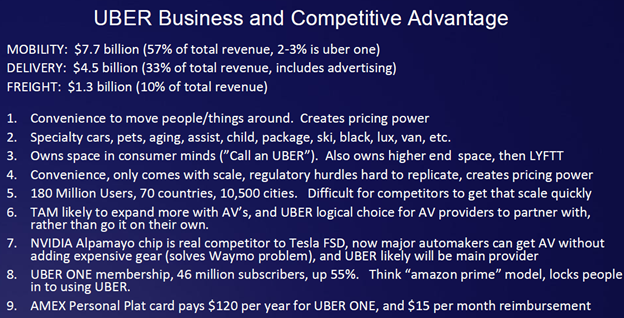

In his presentation, David starts by highlighting Uber's strong, diverse, market-leading business. Here's the first slide:

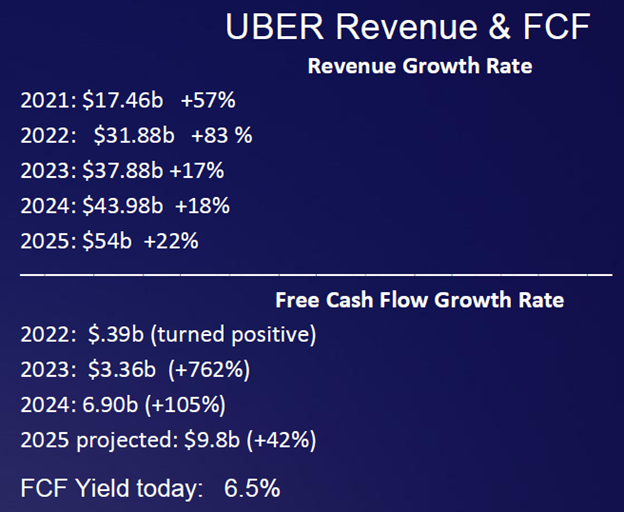

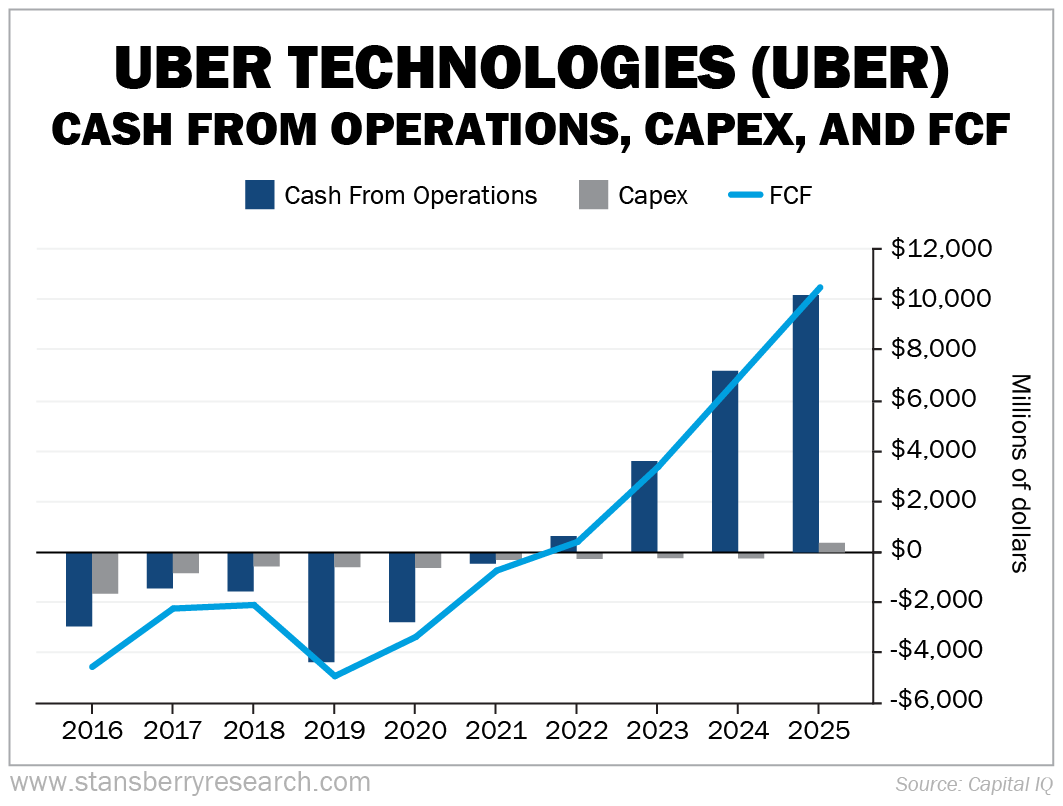

Next, he shows Uber's strong growth in revenue and FCF in this slide:

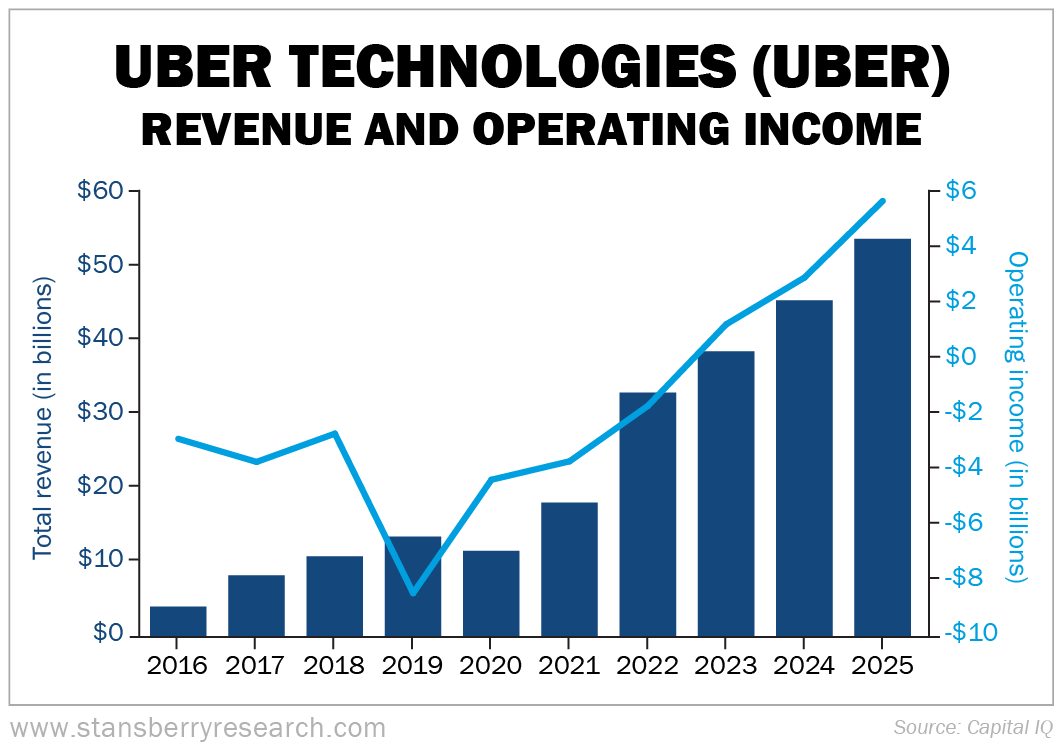

To see this visually, I updated the below charts that I included in my April 2025 e-mail...

First up is Uber's revenue and operating income through last year:

And here's historical operating cash flow, capital expenditures ("capex"), and FCF through 2025:

These are indeed extraordinary numbers.

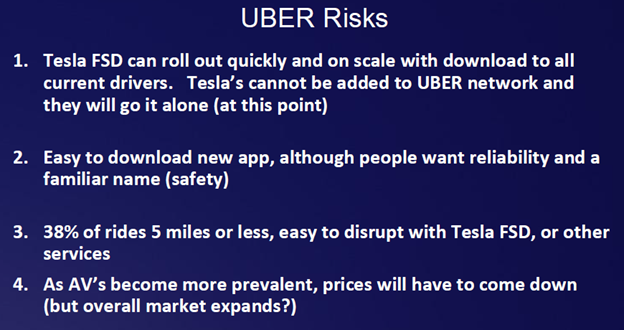

Coming back to David's presentation, he then acknowledges four risks in this next slide:

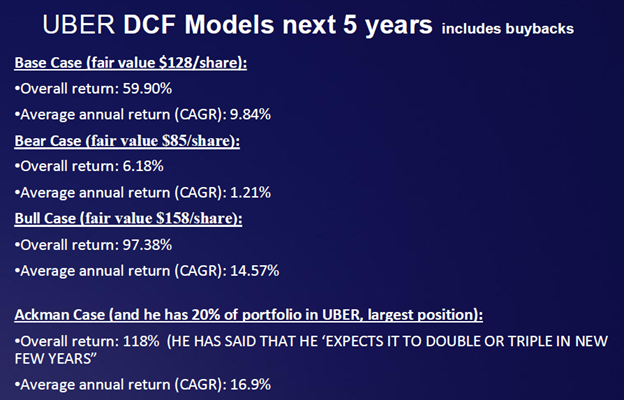

Lastly, David concludes with his base-, bear-, and bull-case scenarios for the stock over the next five years (gains of 59.90%, 6.18%, and 97.38%, respectively, from when he gave his presentation).

He also notes that Pershing Square's Bill Ackman – my old college buddy – thinks it's a "double or triple" in a few years.

Here's the full slide:

I like this stock idea... and I think David (and Bill) are likely to be proved right.

Uber continues to grow rapidly. And the company's operating income and FCF are exploding upward.

However, the forward P/E multiple on the stock is now only about 22 times – down from 30 times about a year ago.

As regular readers know, I like buying the stocks of far-above-average companies when they're trading for market-average multiples.

As for one of the big overhangs on the stock – that Tesla's (TSLA) robotaxi service will expand rapidly and take share from Uber – I have the opposite point of view...

For reasons I outlined in detail in my December 11 and December 17 e-mails, I think Tesla's long-promised robotaxis are years away from prime time. And when investors realize this, Uber's stock will be a major beneficiary.

Thanks for sharing your slides, David!

BY Doug Kass · Mar 2, 2026, 3:00 PM EST

BY Doug Kass · Mar 2, 2026, 2:36 PM EST

Steve Eisman on the next Big Short:

BY Doug Kass · Mar 2, 2026, 2:26 PM EST

BY Doug Kass · Mar 2, 2026, 1:57 PM EST

I covered my (GRNY) short lower on 2/27:

I covered yesterday's (GRNY) short at $24.80.

Position: None.

By Doug Kass Feb 27, 2026 9:49 AM EST

Back shorting a $25.13.

BY Doug Kass · Mar 2, 2026, 1:35 PM EST

From Peter Boockvar:

US manufacturing above 50 for 2nd month, though prices paid jump

More signs of a global manufacturing recovery with the US ISM February print of 52.4, the 2nd month in a row above 50 after a 52.6 figure in January. The estimate was 51.5.

Lunch is not free though as the prices paid component jumped to 70.5 from 59 and that is the highest since June 2022. Maybe part of this was the supplier delivery component which reflected slower lead times with it now at 55.1.

With prices, ISM said “The Prices Index reading continues to be driven by increases in steel and aluminum prices that impact the entire value chain, as well as tariffs applied to many imported goods...Higher prices were reported by 45.4 percent of respondents in February, up 16.4 percentage points from January’s 29 percent but lower compared to the 49.2 percent in April 2025, which was the highest share since June 2022 (65.2 percent).”

This was a quote from a company in the transportation equipment space:

“Today, American produced commodities like steel and aluminum are the highest priced in the world, by far. Hence, the Section 232 tariff policy is having the exact opposite effect of their intention on an American manufacturer like us: It is raising prices while lowering demand and profitability.”

Another in machinery, “Tariff policy changes affect total acquisition costs and purchasing source decisions. So far this year, tariff instability still exists. Due to the tariffs, most raw materials used in manufacturing, such as steel and wire, need to be sourced domestically, and the cost keeps going up.”

New orders slipped 1.3 pts to 55.8 but after jumping by about 10 pts in January. ISM said, “As was the case in January, for every negative panelist comment about new orders, two comments indicated optimism about near-term demand.”

Backlogs were also above 50 for a 2nd month, rising by 5 pts m/o/m to 56.6. Inventories still remain below 50 at 48.8, up 1.2 pts m/o/m and remaining still low at the customer level at 38.8. Export orders held above 50 at 50.3, up .1 pt.

Lastly component wise, employment stayed below 50 at 48.8, though up .7 pts m/o/m. ISM said “Companies continued to focus on accelerating staff reductions due to uncertain near- to mid-term demand. The main head-count management strategies continue to be holding off on filling open positions.”

With respect to breadth, 12 of 18 industries saw growth and five said their business was in contraction. In January, 9 industries grew.

Here were some more company quotes from other industries:

Bottom line, US manufacturing and the global presence as well, is trying to put in a bottom and the key question is whether this is just an inventory build or end demand is improving. For now I think it is the former but we watch closely for improvements in the latter.

And, we have persistent cost pressures that are clearly still with us.

BY Doug Kass · Mar 2, 2026, 1:15 PM EST

Wolf Street howls about bond volatility.

BY Doug Kass · Mar 2, 2026, 12:55 PM EST

At 12:07 PM:

BY Doug Kass · Mar 2, 2026, 12:15 PM EST

With S&P cash +3 handles I am adding to my short (SPY) calls.

Now small sized from very small sized.

BY Doug Kass · Mar 2, 2026, 11:51 AM EST

With S&P cash -9 handles (a big rally from the lows of -70 handles) I am back shorting (SPY) calls.

BY Doug Kass · Mar 2, 2026, 11:21 AM EST

I covered my small trading short rental in (MS) at $167.56 - for a small profit.

BY Doug Kass · Mar 2, 2026, 10:44 AM EST

I have been adding to (MSOS) and (MSOX) this morning.

As well, I took a trading short rental in Morgan Stanley (MS) at $169.12.

BY Doug Kass · Mar 2, 2026, 10:39 AM EST

* The U.S. launches an attack on Iran over the weekend...

Though it has been only two months since I delivered my 2026 Surprise List - a majority of my 10 Surprises have already occurred.

From my 10 Surprises from 2026:

I won't bury the lede.

Pres. Trump, like The Godfather's MIchael Corleone, becomes a wartime President - initially with no opposition in his Cabinet or in Congress (and without a wartime consigliere like Tom Hagen to smooth things over!)

”Goddamn it, if I had a wartime consigliere... a Sicilian...“ |The Godfather

After attacking Venezuela and failing to learn the expensive lessons of regime change attempts with Iraq and Afghanistan, Pres. Trump sees his popularity plummet. Like Corleone, Trump grows more unhinged and the Administration's rhetoric against Mexico's President (Claudia Sheinbaum Pardo) becomes more heated. Pres. Trump gives the Mexican President an ultimatum as an attack on that country is openly discussed on Truth Social. Other regimes, like that of Cuba's Miguel Diaz-Canel's (whose security forces are behind the protection of Venezuela's President Maduro), are also highlighted by the Administration as possible targets early in the year. With the cover of U.S. aggression, Russia becomes more aggressive against Ukraine (there is no peace) and China invades Taiwan in late Summer.

Separate from geopolitics The Epstein Files uncover a deeper (and unsavory) relationship with Pres. Trump.

A week long investigative report entitled "Trump First (Not America First") by The Washington Post discloses how much the Trump family has profited from his Presidency. President Trump's base is fractured - his popularity moves to unprecedented and low depths as the Marjorie Taylor Greene-led America First movement permeates both political parties.

Several high level Trump Administration resignations are announced in the first half of 2026. A number of senior Republican Senators and Congressman distance themselves from the President.

By mid year impeachment is openly discussed. Surprisingly, four women - Marjorie Taylor Greene, Elise Stefanik, Alexandria Ocasio-Cortez and Ellisa Slotnick - emerge as the leaders of their respective political parties. Georgia's Congressman Marjorie Taylor Greene doesn't disappear - just the opposite occurs. Greene becomes the titular leader of the "America First" movement of the Republican Party, which is at odds with MAGA:

The "America First" movement gains ever more prominence and popularity within the Republican Party. Marjorie Taylor Greene overtakes Vice President JD Vance in the polls as the likely next Republican Presidential Nominee. New York Congresswoman Alexandria Ocasio-Cortez takes a large lead in the polls to be the next Democratic Presidential Nominee. Michigan Sen. Elissa Slotnick becomes the leading moderate in the Democratic party.New York Congresswoman Elise Stefanik (who, after stepping down from Congress, breaks with Pres. Trump and announces that she plans to run for Sen. Shumer's NY Senate Seat), becoming another important leader in the "America First" faction of the Republican Party, joining the growing ranks of her party who finally split ranks with Pres. Trump.

Another woman is in the limelight - as First Lady Melania Trump begins divorce proceedings against Pres. Trump. (This was a surprise last year that was wrong....) The divorce settlement is nearly $1 billion, calling further attention to how Trump has profited from his presidency. Pres. Trump unexpectedly resigns under the intense political, social (Epstein) and mainstream media pressure - citing his deteriorating health as the reason.

Despite all of the Administration's woes (and that of the domestic economy), the Democratic Party fails to offer a coherent alternative message as the Party remains hostage to the Left. (New York City Mayor Zohran Mamdani, Senator Bernie Sanders and Congressman Alexandria Ocasio-Cortez denounce the apprehension of Venezuela President Maduro.)

In a surprise (considering all of the above factors adversely impacting Republicans), the Democratic Party (barely) wins a narrow majority in the House. The U.S. economy weakens as the year proceeds. By year's end unemployment rises above 5% and the consumer price index is back near 4%.

The 2026 deficit approaches a staggering $2.5 trillion (and U.S. debt exceeds $40.5 trillion).

A recession in 2027 appears likely.

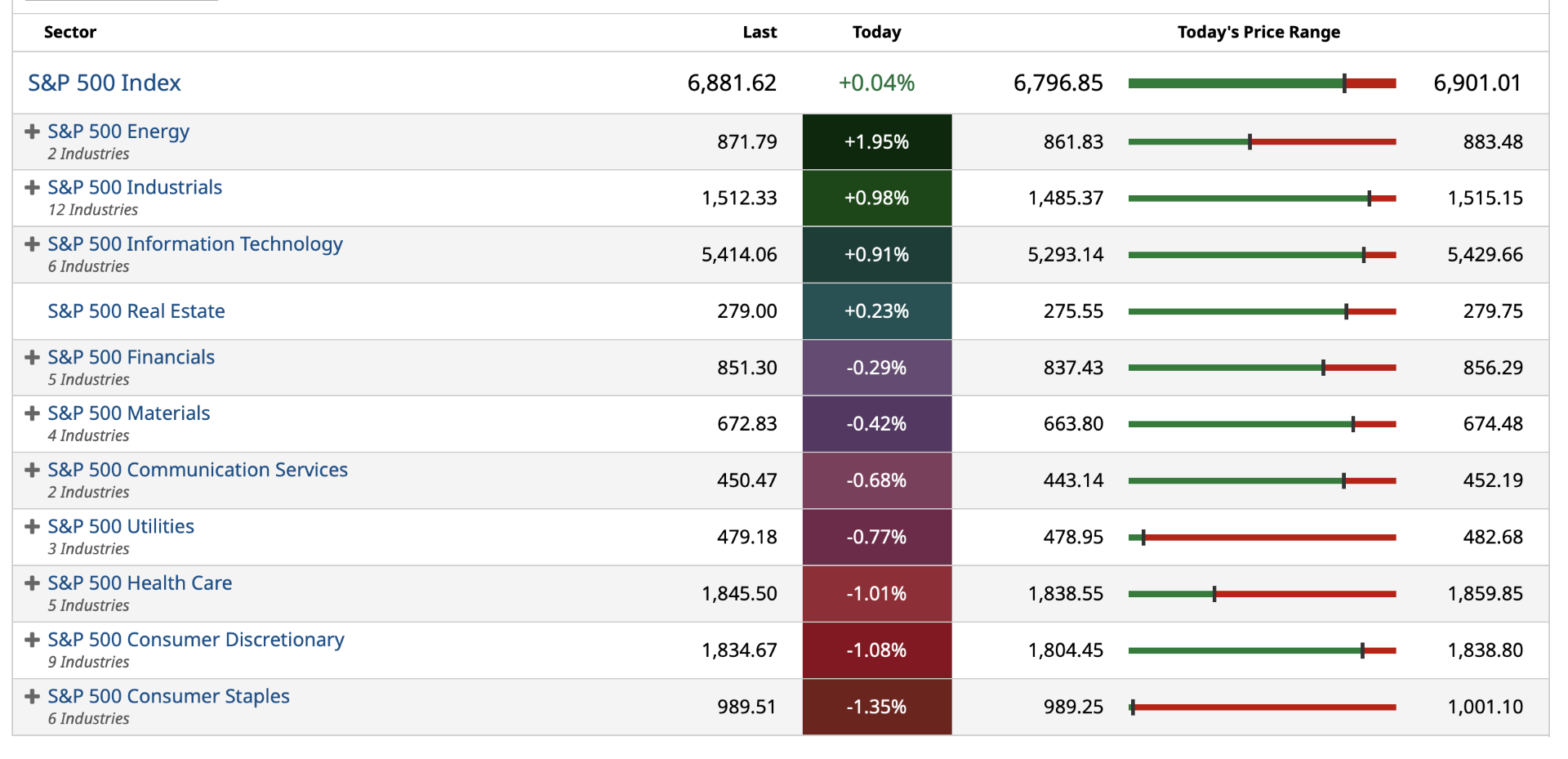

Equities (led by the Magnificent Seven tech stocks) succumb to slowing economic and corporate profit growth, the reappearance of inflation, questionable foreign and domestic policy, growing political uncertainties, emerging "problems" for the hyperscalers (as AI capital spending plans are reduced) and elevated valuations.

The K-shaped economy's weakness in the lower income cohort spreads into the middle and upper middle class as the cumulative (or stacked) inflation since Covid finally has an impact -- causing a spending freeze. With the outlook for global economic growth dissipating, consumer and business sentiment plummets. BNPL and credit defaults rise and auto repossessions increase dramatically.

Drawdowns in the global equity markets and a moribund housing market contribute to a negative "wealth effect" and an air pocket with the high end consumer as the investor optimism of 2023-25 is abandoned.There is no place to run, no place to hide - most asset classes fall in the 2026 Bear Market.

Precious metals, commodities and crypto currencies all collapse (after a strong start early in the year) -- in Martha Reeves' Revenge. Bottom line: After starting the year positively, the S&P Index drops by more than -- 20% in 2026 -- with three separate drops of -10%.

And another post from early (January) 2026:

“Successful investing is having everyone agree with you... later.”

- Jim Grant

The last several trading days have been characterized by a further rise in global bond yields (turning the equity risk premium to an even larger discount), large intragroup action, disparate performance in Mag 7/Large-Cap Tech (Apple (AAPL) vs. Amazon (AMZN) yesterday), spastic and casino-like daily moves in individual stocks (e.g. Micron (MU) ) and in precious metals ( (SLV) , (GLD) and (PPLT) ), short squeezes in heavily shorted stocks and extreme bullish investor sentiment (my CNBC Blather Index has 32 CNBC bulls and 1 bear in the last week).

This has all occurred against a backdrop of unsettling geopolitical events and foreign policy that would typically weight on equities — but algorithms and new money into the markets (in a new year) have countered rising geopolitical risks.

As for me, it looks to be the beginning of the end of a maturing bull market.

I have raised my short exposure accordingly.

Position: None

By Doug Kass Jan 7, 2026 8:00 AM EST

BY Doug Kass · Mar 2, 2026, 9:30 AM EST

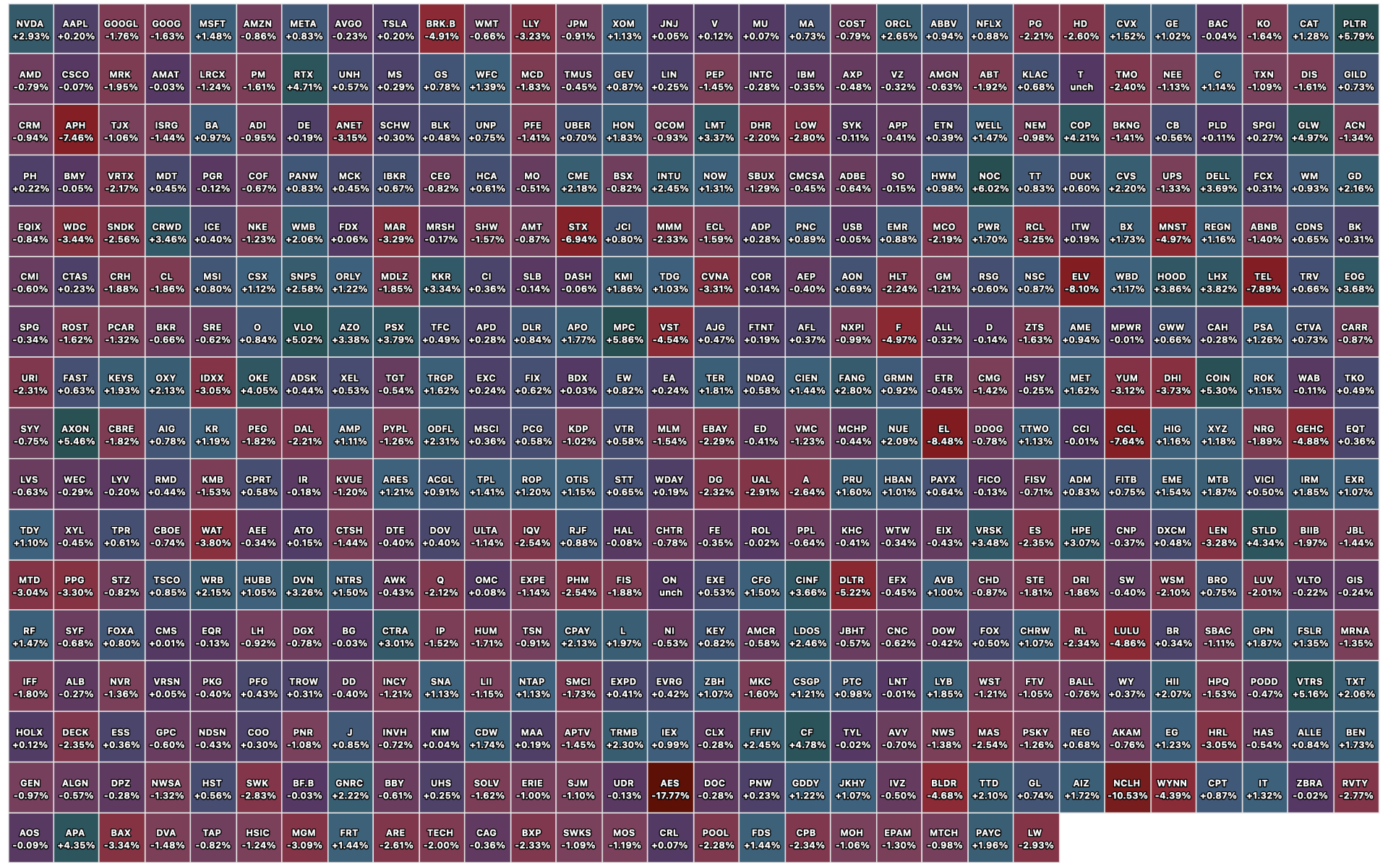

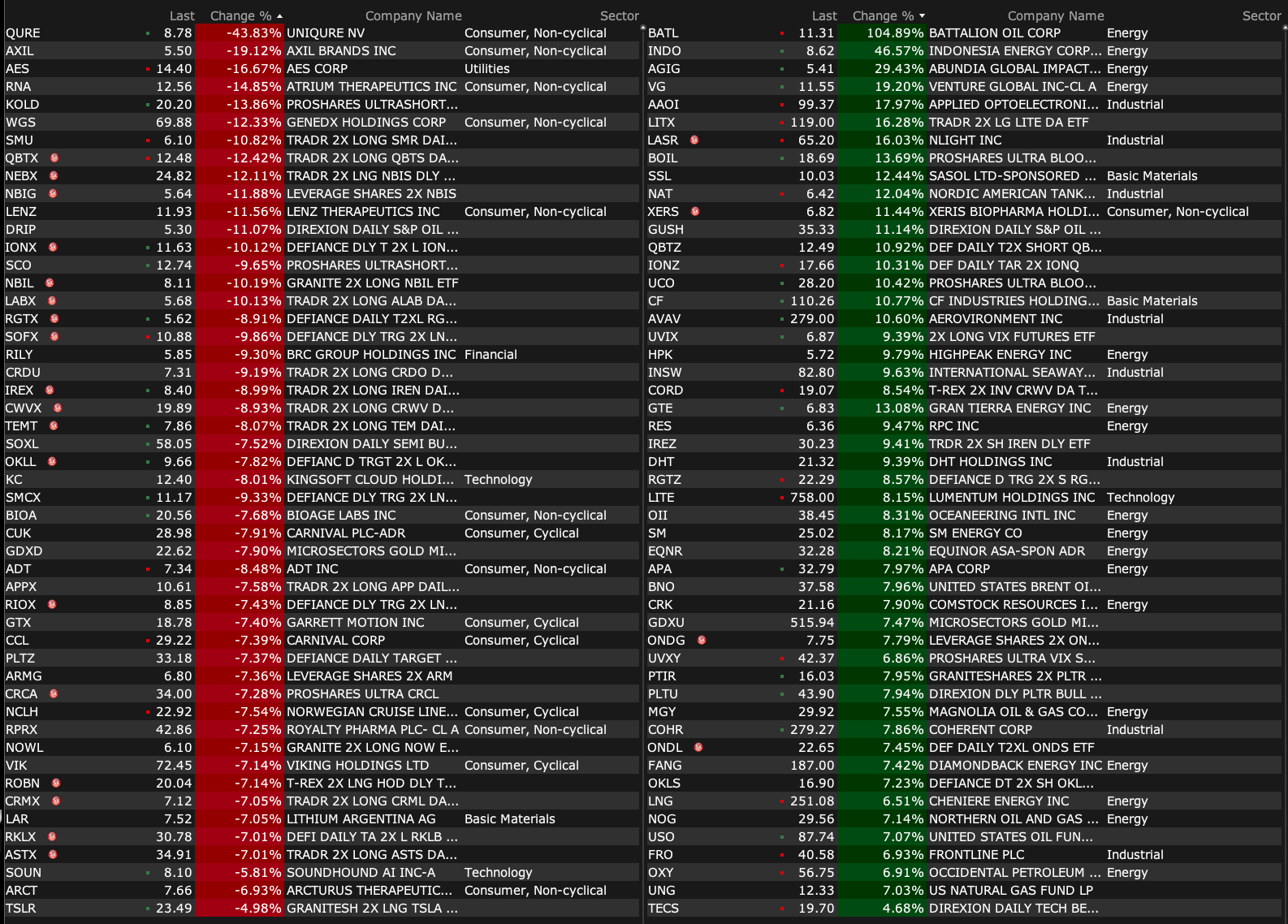

-AAOI +23% (momentum; B. Riley Securities, Inc Raised AAOI to Neutral from Sell, price target: $54 from $15)

-LASR +23% (strength following Iranian strikes; to showcase high-energy laser weapon at conference)

-VG +20% (earnings, guidance)

-CF +11% (sector strength following Iranian strikes)

-XERS +11% (earnings, guidance)

-DHT +8.8% (sector strength following Iranian strikes)

-COHR +7.8% (NVIDIA and Coherent Announce Strategic Partnership to Develop Optics Technology to Scale Next-Generation Data Center Architecture; NVIDIA is investing $2B in Coherent)

-ECO +7.6% (momentum)

-LITE +7.4% (NVIDIA Announces Strategic Partnership With Lumentum to Develop State-of-the-Art Optics Technology; Nvidia investing $2B in Lumentum to support R&D)

-RTX +6.6% (sector strength following Iranian strikes)

-LNG +6.4% (natural gas strength following Iranian strikes)

-CTRA +5.5% (energy sector strength following Iranian strikes)

-PSKY +5.2% (strength following acquisition of WBD)

-NTLA +5.1% (confirms US FDA Lifts Clinical Hold on MAGNITUDE Phase 3 Clinical Trial in ATTR-CM)

-NOC +4.9% (sector strength following Iranian strikes)

-XOM +4.8% (energy sector strength following Iranian strikes)

-HAL +4.7% (sector strength following Iranian strikes)

-KVYO +4.7% (authorizes $500M share repurchase program with $100M accelerated share repurchase)

-INSW +3.9% (sector strength following Iranian strikes)

-LHX +3.8% (sector strength following Iranian strikes)

-CVX +3.6% (energy sector strength following Iranian strikes)

-SLB +3.0% (energy sector strength following Iranian strikes)

-AARD -54% (announces Voluntary Pause of Phase 3 HERO Trial in Prader-Willi Syndrome based on reversible cardiac observations at above target therapeutic doses; No longer anticipates topline data from HERO trial in 3Q26)

-QURE -43% (received final meeting minutes from U.S. FDA regarding Type A meeting held on January 30, 2026 to discuss AMT-130, an investigational gene therapy for Huntington’s disease (HD); FDA cannot agree Phase I/II data is sufficient; reports earnings)

-TPB -34% (earnings, guidance)

-CLPT -25% (insider selling)

-AES -16% (consortium led by Global Infrastructure Partners and EQT to acquire AES for $15.00/shr in cash at $10.7B equity value)

-BIOA -9.4% (downside momentum)

-ADT -8.2% (earnings, guidance)

-NCLH -7.5% (earnings, guidance; sector concern following Iranian strikes)

-EXEL -5.2% (downside momentum)

-GTLB -3.8% (TD Cowen Cuts GTLB to Hold from Buy, price target: $29)

-PINS -3.4% (Argus Cuts PINS to Hold from Buy)

-DUOL -3.0% (weakness following broker downgrades)

-LI -2.2% (reports Feb deliveries)

BY Doug Kass · Mar 2, 2026, 9:22 AM EST

From Peter Boockvar:

Obviously depending on who gains control next in Iran, the Middle East should be a freer and safer place with the downfall of another despot, and possibly to the greatest extent in our lifetimes. That potentially historic moment aside, we know markets are completely dispassionate when it comes to geopolitics. They don’t care about the politics and they have no feelings, they only care about the economic impact and of course we’re talking about oil here. While I am an oil bull, expressed here many times, I do not recommend chasing it on these events as once the Strait of Hormuz starts fully flowing with tankers again, and it will, the geopolitical premium will quickly reverse. The Strait has not been shut, it’s just been voluntarily stunted with shipments because of the lack of insurance and obvious safety concerns.

With the rise in crude prices, most global bond yields are higher, stocks lower, US dollar up (Fed not cutting yet with rising oil prices) as well as gold. The sector stock reaction is to be expected with defense stocks, supply constrained commodity stocks and shipping stocks higher while travel/airline stocks are down and countries that rely on energy imports weak as well.

Most of the global manufacturing PMI’s improved in February from January as a bottom is trying to be set after about 3 years of contraction. Here is what I saw:

Taiwan 55.2 vs 51.7

Japan 53 vs 51.5

Australia 51 vs 52.3

India 56.9 vs 55.4

Indonesia 53.8 vs 52.6

Vietnam 54.3 vs 52.5

Thailand 53.5 vs 52.7

Philippines 54.6 vs 52.9

The Eurozone manufacturing PMI remained at 50.8 after the initial print seen a few weeks ago and up from 49.5 in January. The UK’s index was 51.7 vs 51.8.

A few notable quotes from S&P Global.

On Japan, “Firms were also much more upbeat about the year-ahead, with confidence rising to the highest since mid-2024. There were expectations that global demand conditions will continue to revive and push up sales in the months ahead, particularly in key sectors such as technology and automotives.”

On Taiwan: “Stronger global demand conditions drove the sharpest increases in output and new orders for over four-and-a-half years, which prompted firms to raise both their purchasing activity and inventory levels at stronger rates.”

On the Eurozone: “This seems to be a broad based recovery of the Eurozone manufacturing sector, with six out of the eight countries surveyed now in growth territory. Germany’s industry, which experienced a big jump in the headline PMI, has returned to growth for the first time in 3 ½ years. Among the four economic powerhouses of Europe, Germany is showing the fastest growth rate in manufacturing. To be sure, we are not talking about a boom, but a moderate recovery coming from a low activity level amid persisting structural challenges like high energy prices, intense competition from China and US tariffs among other things.”

From Carter’s, the children’s clothing maker and retailer and whose stock plunged by 20% Friday:

The positive in the quarter, “Sales, operating income and earnings per share all exceeded our prior forecast. Industry data suggests it was a good holiday season for many companies as the consumer was clearly out shopping, we saw broad based demand across our business in the fourth quarter and achieved sales growth in each of our business segments.”

“Baby continues to be the strength in our product assortment.”

The negative, while sales rose in the quarter profits fell with “the lion’s share of the decline in operating income was driven by the net negative impact of higher tariffs as well as higher product costs related to investments in product make and spending deleverage” among other reasons.

“Obviously, the developments over the last week have introduced new uncertainty regarding the topic of tariffs. There’s a lot left to play out on this subject, including the potential to recover the significant additional tariffs we’ve already paid to date.” In Q4 tariffs impacted them by $40mm gross, “roughly double the impact we experienced in the third quarter.”

On mitigation efforts of tariffs, “offsetting that are significant assumed pricing increases across the business, across all of our channels, as well as other supply chain mitigation actions.”

From Sunstone Hotel, a REIT that owns upper scale properties:

“While we see reasons to be optimistic about the year ahead, we remain cautious while still in these initial months. Based on what we see today,” they expect about 1.5% RevPAR growth in 2026.

To some other economic data points overseas, the Lunar New Year in China seemed to have brought out a good rise in consumer spending. Macau in particular announced that casino revenue rose 4.5% y/o/y, above the estimate of 1%. We remain long Las Vegas Sands and Melco Entertainment.

BY Doug Kass · Mar 2, 2026, 9:05 AM EST

BY Doug Kass · Mar 2, 2026, 8:55 AM EST

BY Doug Kass · Mar 2, 2026, 8:36 AM EST

11:30 a.m.: Treasury hosts a $89B 3 and $77B 6-Month Bill Auction

Morning: Federal Reserve Bank of Chicago Austan Goolsbee (Non-Voter) Podcast Appearance -- Trading Secrets (Episode to pub-lish across podcast platforms early Monday morning)

BY Doug Kass · Mar 2, 2026, 8:24 AM EST

DaveInKenya

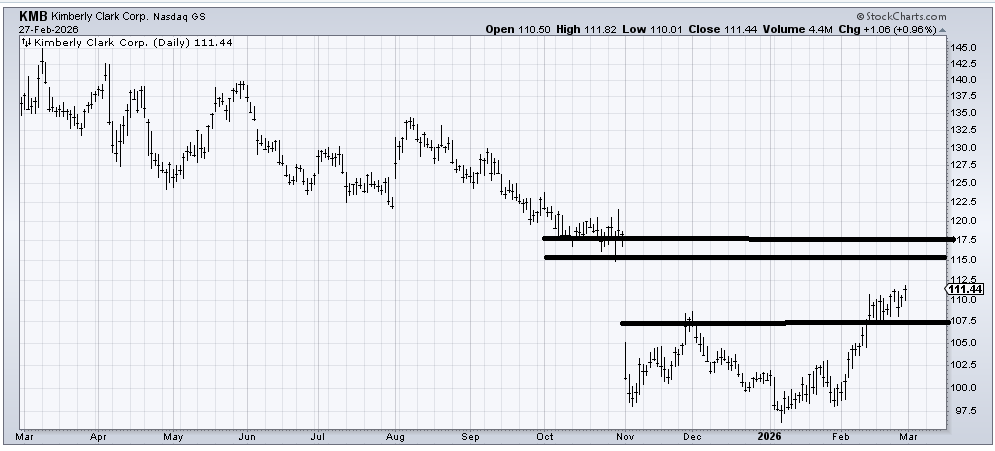

helene on (KMB)

It’s been about six weeks since I first recommended Kimberly-Clark KMB, and it has been a slog getting this stock to rally a bit more than ten percent. I just want to note that there is a gap to be filled around 115 and resistance around 117. Should it get there, I would be inclined to take a few profits.

BY Doug Kass · Mar 2, 2026, 7:40 AM EST

BY Doug Kass · Mar 2, 2026, 7:30 AM EST

BY Doug Kass · Mar 2, 2026, 7:20 AM EST

BY Doug Kass · Mar 2, 2026, 7:10 AM EST

BY Doug Kass · Mar 2, 2026, 7:00 AM EST

BY Doug Kass · Mar 2, 2026, 6:45 AM EST

Wolf Street howls about drilling (baby, drill).

BY Doug Kass · Mar 2, 2026, 6:35 AM EST

BY Doug Kass · Mar 2, 2026, 6:25 AM EST

BY Doug Kass · Mar 2, 2026, 6:15 AM EST

BY Doug Kass · Mar 2, 2026, 6:05 AM EST

BY Doug Kass · Mar 2, 2026, 5:55 AM EST

The S&P Short Range Oscillator remains in overbought at 1.72% vs. 1.40%.

BY Doug Kass · Mar 2, 2026, 5:45 AM EST