Nvidia ... Another Lesson Learned?

"Just one last thing."

- Lt. Columbo

BY Doug Kass · Feb 25, 2026, 5:50 PM EST

"Just one last thing."

- Lt. Columbo

BY Doug Kass · Feb 25, 2026, 5:50 PM EST

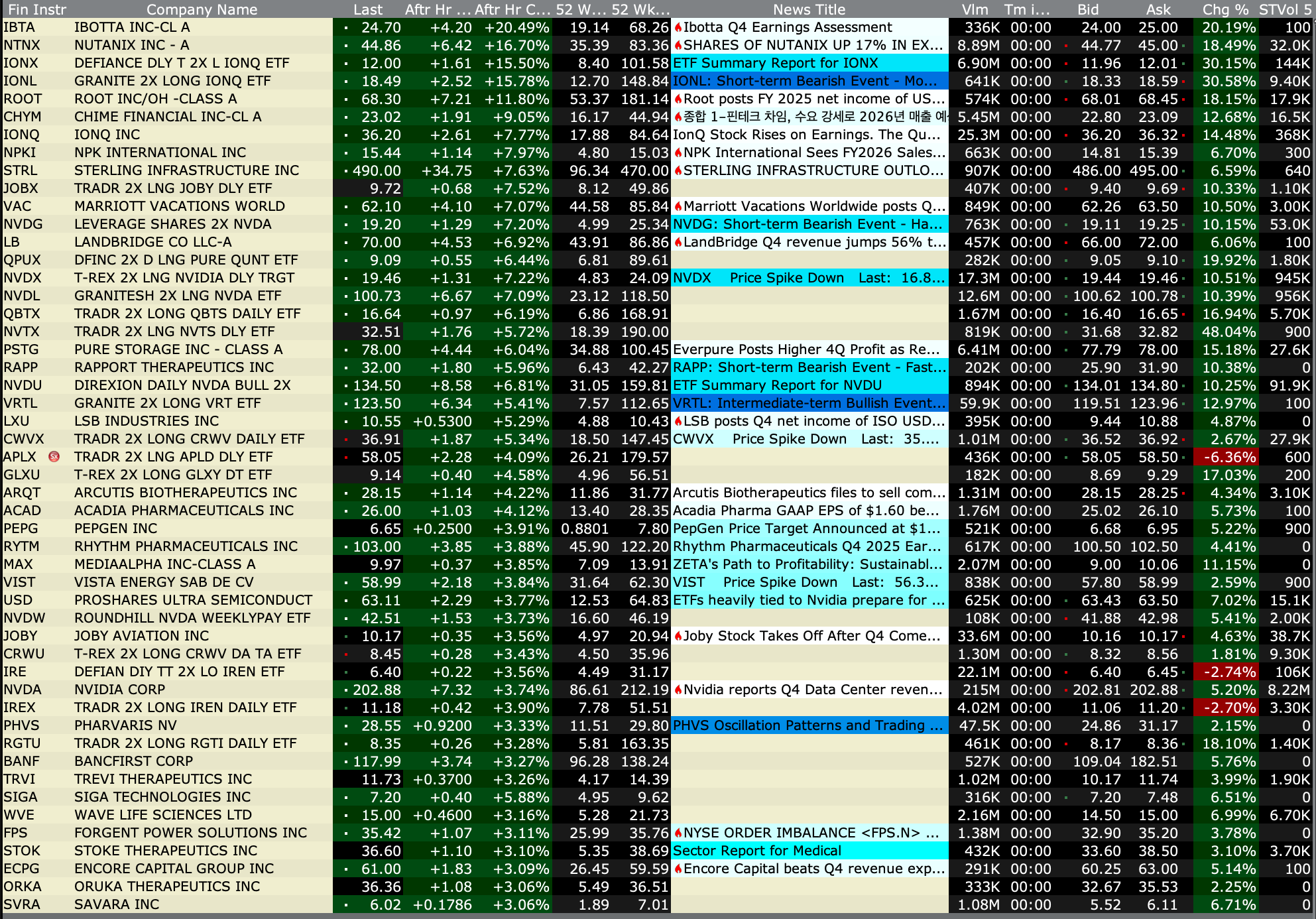

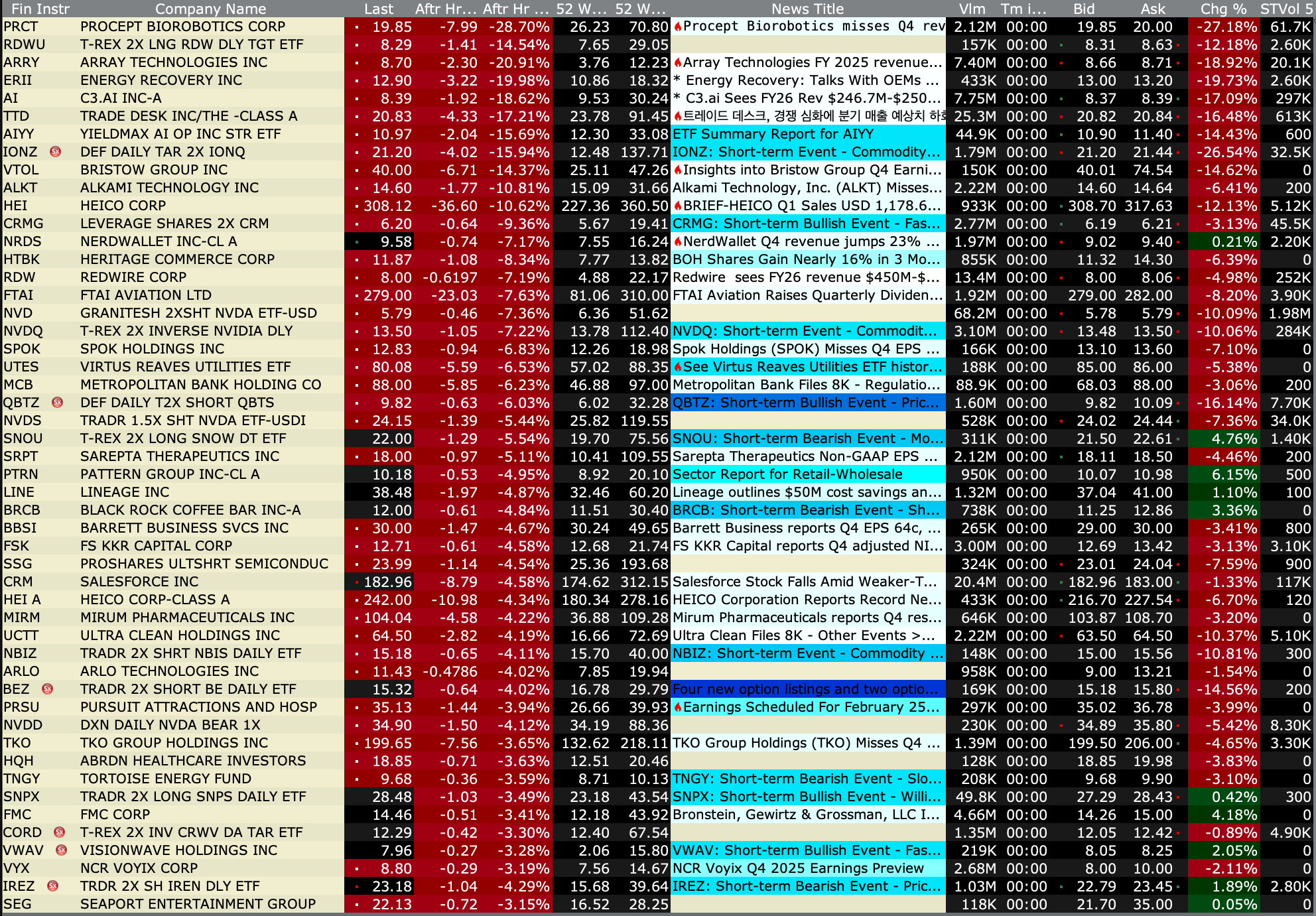

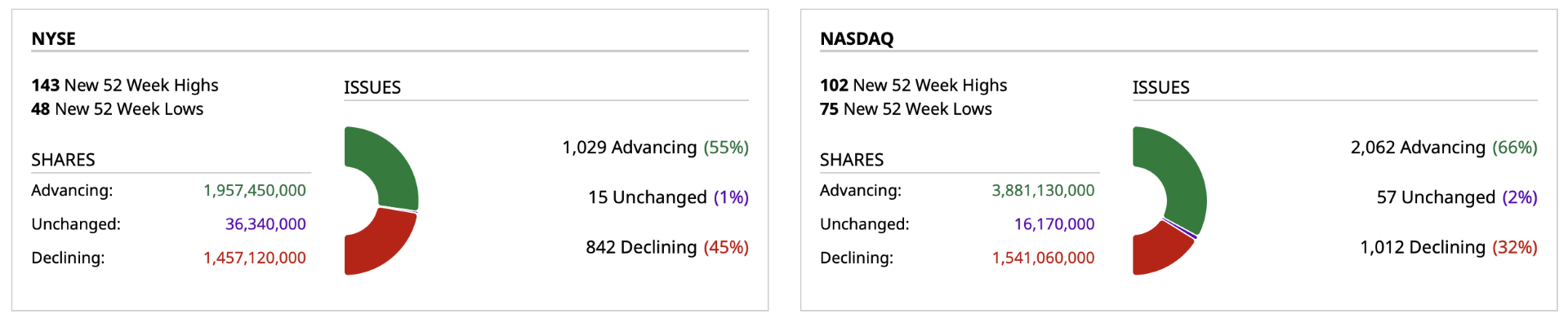

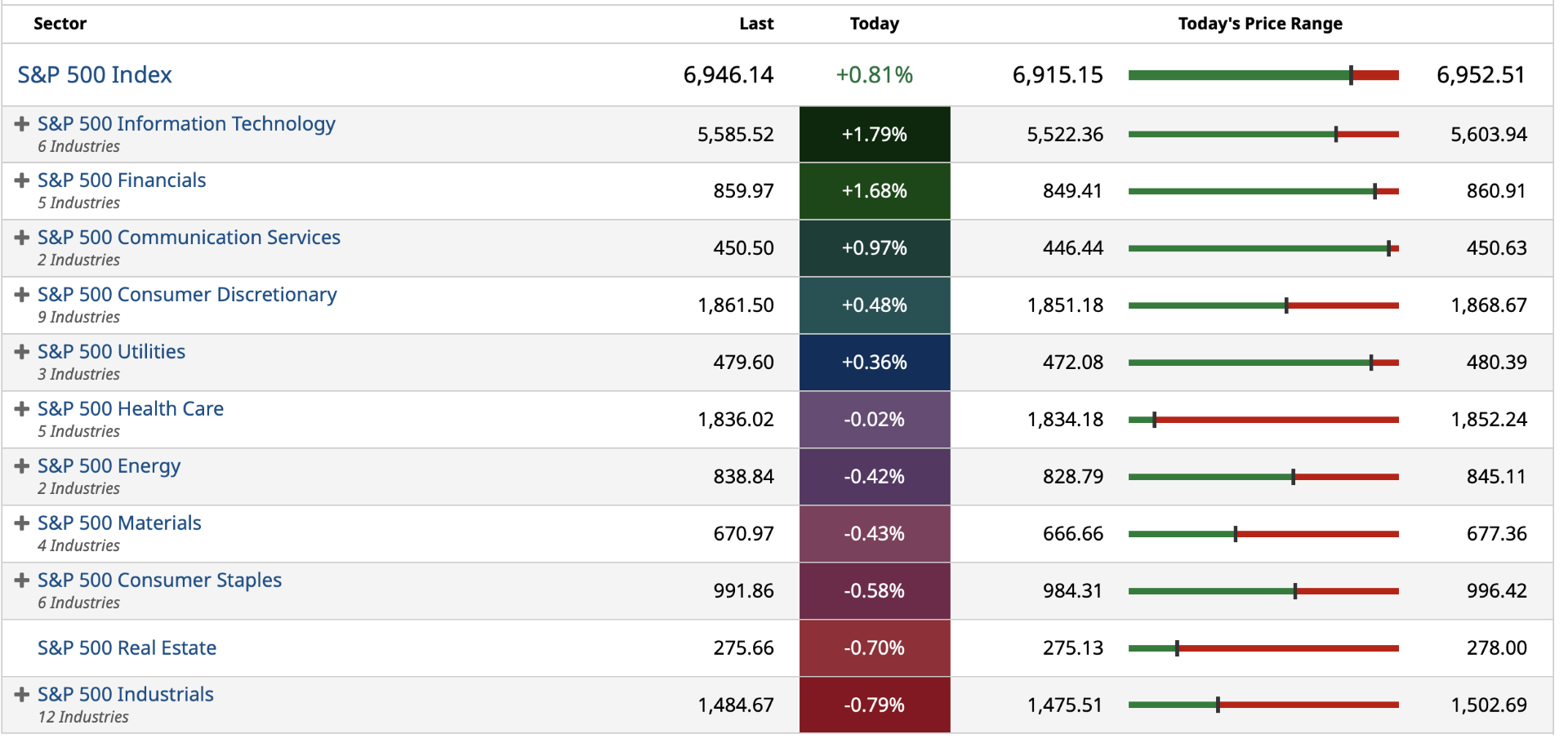

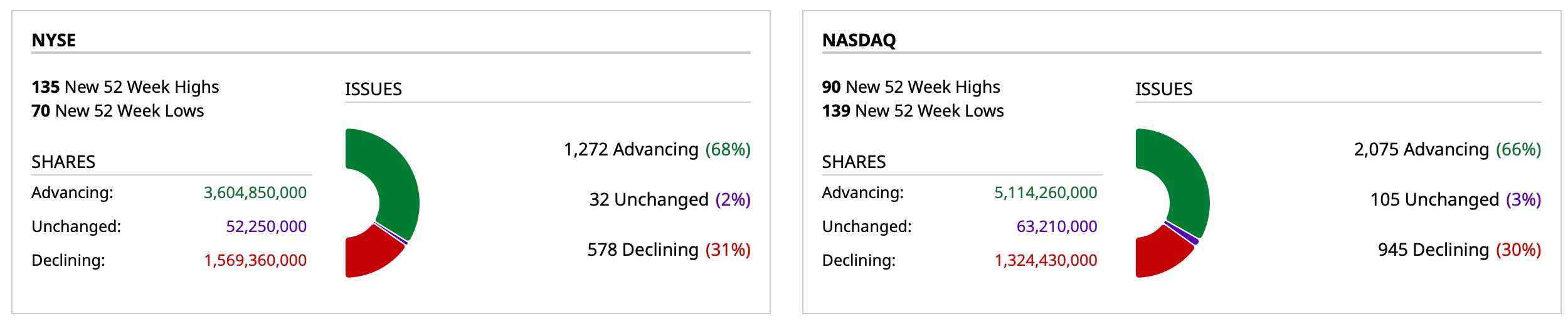

As of 4:35 PM:

BY Doug Kass · Feb 25, 2026, 4:43 PM EST

- NYSE volume 16% below its one-month average

- NASDAQ volume 3% below its one-month average

- VIX index: down 8.24% to 17.94

BY Doug Kass · Feb 25, 2026, 4:31 PM EST

I am wrapping it up for the day as I have a trip to take (I will not be here for the EPS fireworks!)

I will be back on Friday morning.

Thanks for reading my Diary.

Enjoy the evening.

Be safe.

BY Doug Kass · Feb 25, 2026, 3:45 PM EST

Earnings After the Close Wed., Feb. 25

Earnings Before the Open Thurs., Feb. 26

BY Doug Kass · Feb 25, 2026, 3:20 PM EST

Steve Jobs lectures at MIT:

BY Doug Kass · Feb 25, 2026, 3:09 PM EST

BY Doug Kass · Feb 25, 2026, 1:50 PM EST

This summary of the reactions/rebuttals to the Citrini report from the AI bulls is quite funny and self-damning.

Citrini’s Dystopian AI Vision Draws Global Investor Criticism

Their defense seems to be that AI does not do much.

Exactly!

You guys finally have it right.

Sorry, this is not how you cover trillions of dollars of aggregate investment including debt capital.

“According to Citadel Securities, current data show little sign of widespread AI-driven labor disruption, citing surveys from the St. Louis Fed and labor market indicators. Job postings for software engineers — a field seen as vulnerable to automation — have jumped in recent months, and construction hiring appears to be picking up, supported by a boom in AI-related data center projects, wrote macro strategist Frank Flight in a report. Instead of replacing human workers, “it seems more likely that AI will be a complement” for labor in many areas, similar to past technological revolutions, he said.”

Post Script:

This is interesting too .

The probability of earning any return on the gross AI investment seems much lower than the probability of failure/Netscape in my view:

BY Doug Kass · Feb 25, 2026, 1:00 PM EST

Housekeeping item.

I have sold out my Netflix (NFLX) long at $82.12 just now (+$4.08).

BY Doug Kass · Feb 25, 2026, 12:50 PM EST

First:

Second:

Homebuilders' share prices are down between 4% to 5% today.

BY Doug Kass · Feb 25, 2026, 12:40 PM EST

BY Doug Kass · Feb 25, 2026, 12:25 PM EST

BY Doug Kass · Feb 25, 2026, 12:15 PM EST

From Peter Boockvar:

Those of us focused on the private credit space and what is going on with its corporate sponsors and publicly traded BDCs have mostly focused on concerns with software loans but Fitch yesterday said that space is actually the 3rd biggest area seeing defaults. In a piece yesterday titled “US Private Credit Default Rate Continues Upward March to 5.8% in January 2026” Fitch said “Healthcare providers remained the sector with the highest number of unique defaulters in the TTM (trailing 12 months). The sector’s 13 unique defaulters produced a 7.8% default rate, up from 7.2% in December 2025 and 6.1% in January 2025.”

The second largest component of defaulters was in the consumer products sector as they had “eight unique defaulters...The sector’s default rate rose to 12.8% from 11% in December 2025 and more than doubling from 6.1% from January 2025.”

Interestingly on software where almost all the AI angst is on saw “only three unique defaulters for the TTM ending January 2026. The sector’s default rate sank to 1.9% from 7.5% in January 2025.” They said this on the fundamental situation, “While AI could lower barriers to entry for new competitors, the mission critical nature and high switching costs of many enterprise software products continue to protect traditional operators.”

Overall, Fitch’s default rate is now at 5.8% for the TTM ending January 2026, up from 5.6% in December 2025. This marks the highest rate since inception in August 2024.”

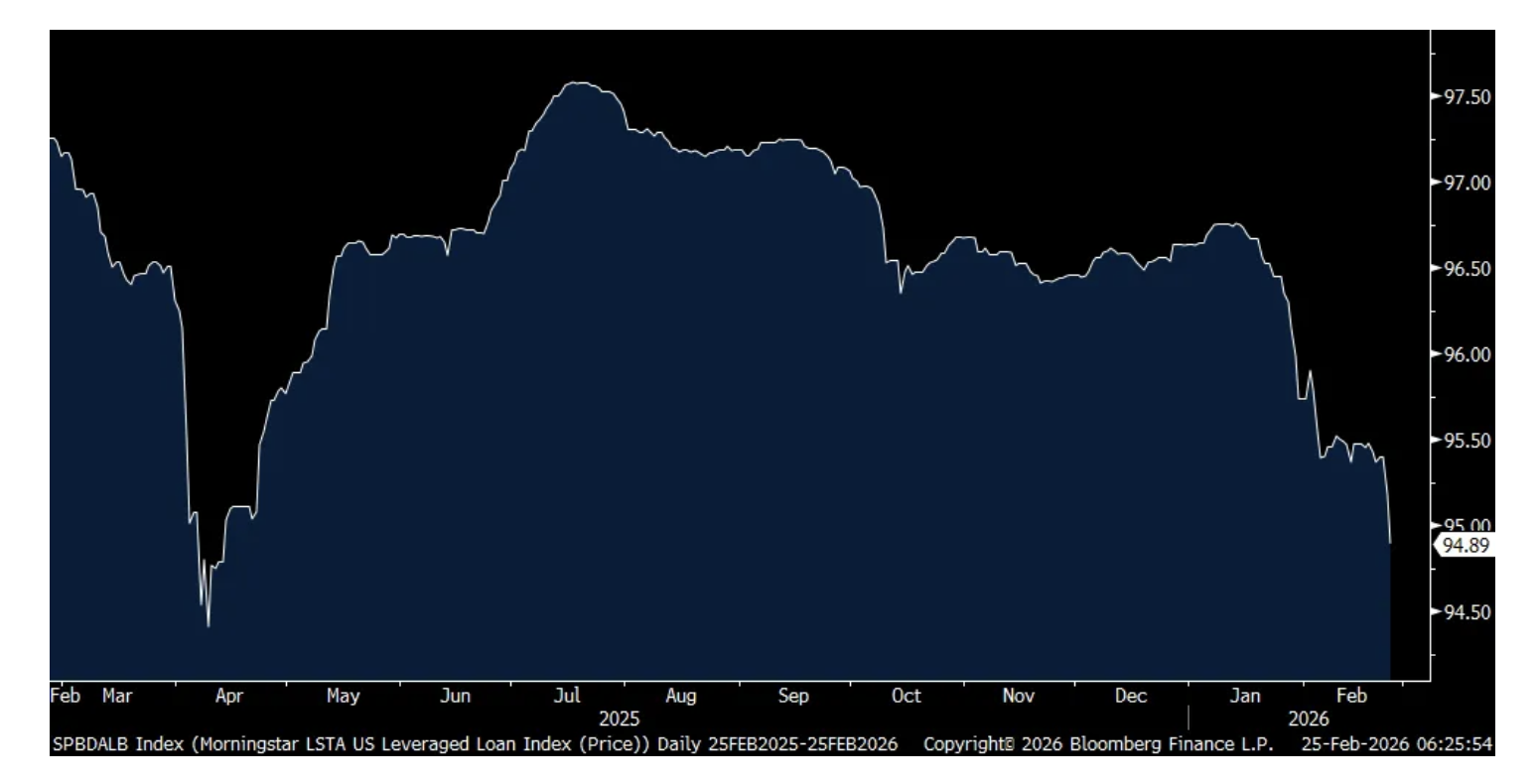

The LSTA Leveraged Loan index closed down again yesterday and to the lowest level since mid April 2025, right after the tariff kerfuffle, and below 95 cents on the dollar.

Outside of the specific credits that are being sold and those seeing rising defaults, what we are going to experience broadly is further redemptions at private credit firms most likely, especially from the retail cohort that is hearing what is going on and a subsequent rise in the cost of capital for everyone with lower quality balance sheets.

LSTA Leveraged Loan Index

Notable today, again, is what is going on in Japan. PM Takaichi appointed two new members to the BoJ who are reputed doves, Toichiro Asada and Ayano Sato. In response the yen is falling by almost 1% to a 2 ½ week low but the 2 yr yield was flat. Not liking a more dovish committee, the yields in the 10s, 30s and 40s were up 5 bps, 7 bps and 9 bps respectively.

Bottom line, either the BoJ is going to hike rates to calm inflation and the yen weakness or the longer end of their yield curve is going to do it for them.

To some important earnings calls.

From Home Depot, that rose 2% yesterday after falling 1.4% on Monday:

“During the fourth quarter, our comp average ticket increased 2.4% and comp transactions decreased 1.6%. The growth in comp average ticket primarily reflects some price increases, a greater mix of higher ticket items and customers continuing to trade up for new and innovative products.”

“Big ticket comp transactions or those over $1,000 were positive 1.3% compared to the fourth quarter of last year. We were pleased with the performance we saw in categories such as power, plumbing and electrical. However, larger discretionary projects remain under pressure.”

“During the fourth quarter, Pro posted positive comps and outperformed DIY.”

As for their big picture take on the macro, “The current mortgage rate environment and significant increase in home prices since 2019 have impacted housing affordability. Housing turnover has remained at historical lows since 2023, which has significantly reduced demand for projects and other purchases associated with buying and selling a home. Our customers also tell us they have concerns over general economic uncertainty, including inflation, growing job concerns, and higher financing costs. As we look ahead to fiscal 2026, we anticipate these pressures will persist as we have not yet seen a catalyst for an inflection in housing activity.” I bolded for emphasis.

From Cava and whose stock is trading up pre market:

Comps grew .5% in Q4. “As guests become more intentional with their spend, they are choosing brands like Cava that deliver real differentiation through bold flavors, helpful food, and hospitality that creates meaningful human connection.”

“in January 2026, we implemented an approximate 1.4% in restaurant menu price adjustment, and we do not plan to take any additional price in 2026. Importantly, this adjustment did not include price increases to our base bowl, allowing us to maintain strong everyday value for our guests.”

“On the cost side, we expect low single digit inflation across food, beverage, and packaging and low to middle single digit labor inflation.”

“we’re seeing strength across all of our vintages of restaurants, all of our geographies across the country, all the income cohorts of our restaurants based on median household incomes in those markets.”

From Workday, defending its business model, pushing back against the idea that AI is going to push them aside, and whose stock is down 10% pre market because of slightly weaker than expected guidance:

“You’ve all heard the narrative out there that HR and ERP will be placed or relegated to the background by AI. I personally just don’t see that happening. Our application domains are really, really hard to build. I’ve been working in the HR and ERP space for over 30 years. These are true systems of record that must process transactions with absolute accuracy and speed, enforce complex security models, and comply with statutory and regulatory environments all over the world. That kind of complexity is very hard to replicate. No amount of vibe coding is going to produce an HR or an ERP system.”

“And importantly, our underlying business processes are deterministic by nature. There is a start and end to a business process. Its goal is to deliver consistent audible outcomes. AI for all of its incredible capabilities is probabilistic by nature. It reasons, predicts, and recommends based on patterns and likelihoods. Maybe it will eventually become a state machine, a system that follows the same steps and gets the same results every time, but it is not there today. You can’t have outcomes in running a payroll, it needs to be 100% accurate and completed 100% of the time.”

From HPQ and whose stock is down pre market as they are getting squeezed by higher chip costs:

Sales rose 7% “driven by performance in Personal Systems as we continue to see the positive impact on PC demand in the Windows 11 refresh cycle and the continuing momentum of AI PCs.”

“In print, our results were in line with expectations, with continued momentum in consumer subscriptions, which grew revenue double digit, and industrial print, which grew mid single digit, with continuing shifts from analog to digital production.”

“Like others, we are seeing increased input costs driven primarily by the rising prices of DRAM and NAND. We expect this volatility to remain throughout fiscal ‘26 and likely into fiscal ‘27.”

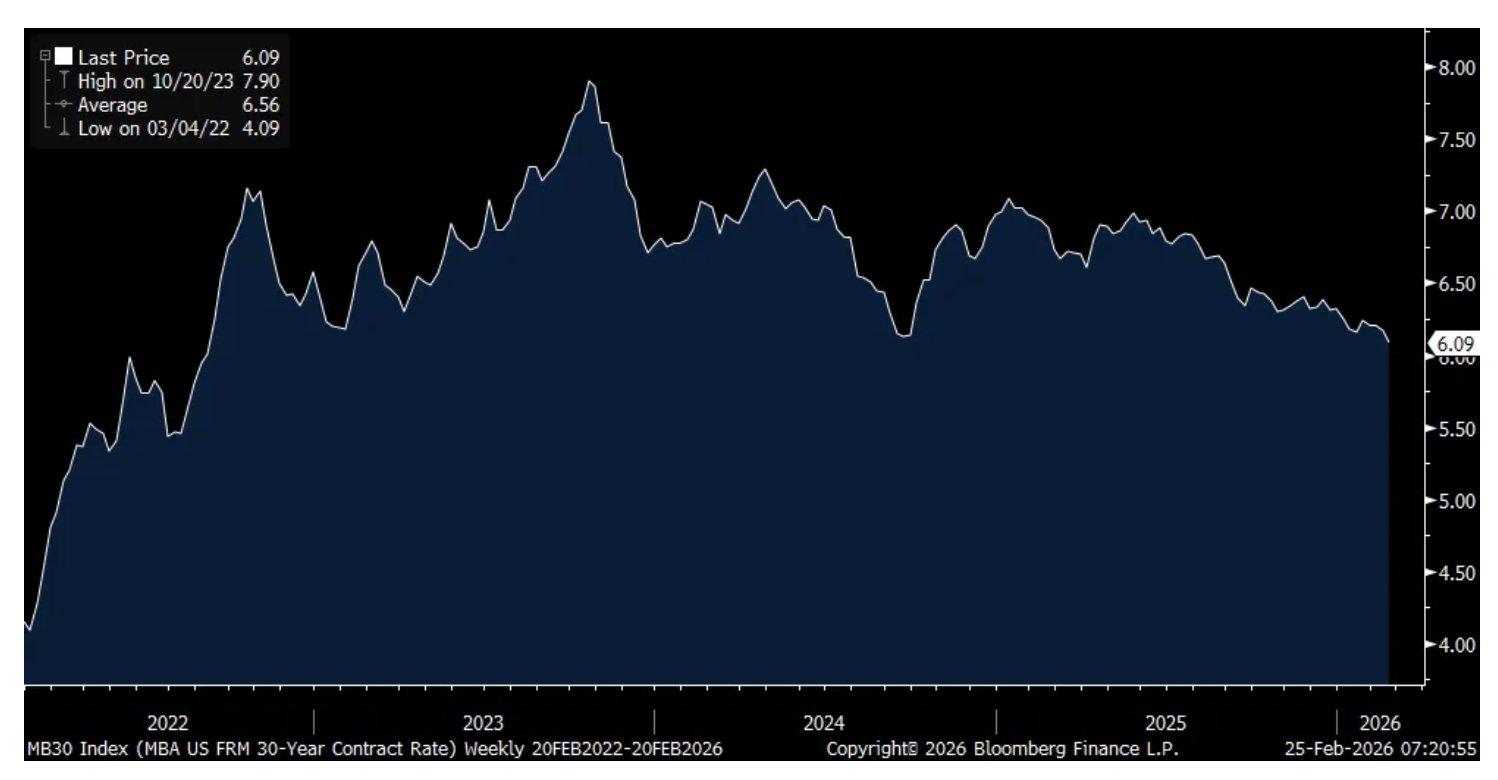

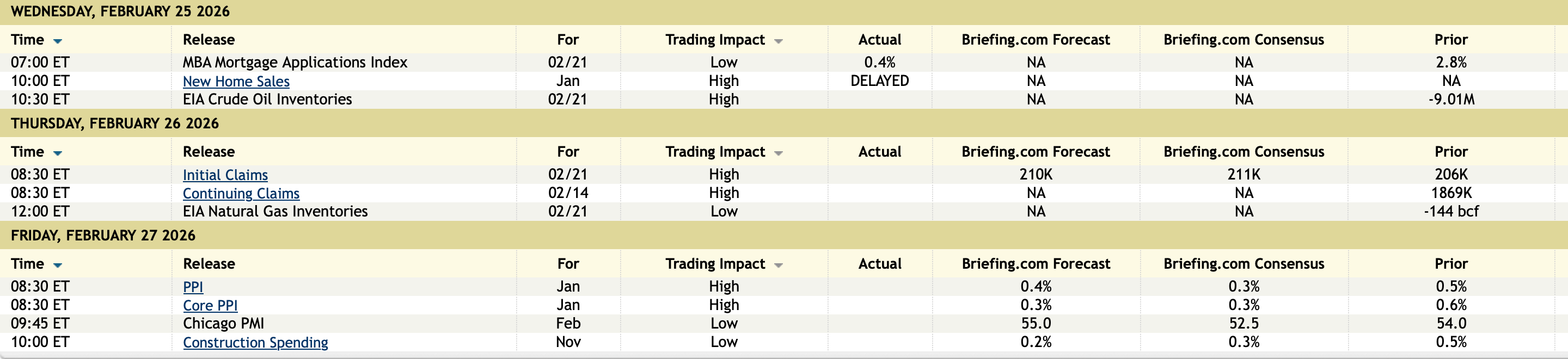

To some economic data. Mortgage apps were mixed as purchases fell for the 5th straight week and by 4.7% w/o/w. It now stands at the lowest since April 2025 while refi’s grew 4.1% w/o/w. That purchase drop occurred even though the average 30 yr mortgage rate fell by another 8 bps to 6.09%, the lowest since September 2022.

Lower mortgage rates are not driving more purchases because the price of the home is still too expensive. Sorry to existing home owners but this housing market needs lower home prices in order to spur more demand and/or we need a bunch more supply.

Average 30 yr Mortgage Rate

The RBA is still going to lean towards raising rates after January trimmed CPI rose 3.4% y/o/y vs the estimate of 3.3% and vs 3.3% in December. Aussie yields ticked up in response and the Aussie$ is higher.

BY Doug Kass · Feb 25, 2026, 12:05 PM EST

BY Doug Kass · Feb 25, 2026, 11:50 AM EST

I am back shorting (GRNY) and (JOET) — with a scale on strength.

BY Doug Kass · Feb 25, 2026, 11:27 AM EST

On the move higher I am now medium-sized short (SPY) .

BY Doug Kass · Feb 25, 2026, 11:16 AM EST

With S and P cash +35 handles I am adding to my short SPY calls and moving towards medium sized. Converted short SPY common to short calls.

BY Doug Kass · Feb 25, 2026, 9:40 AM EST

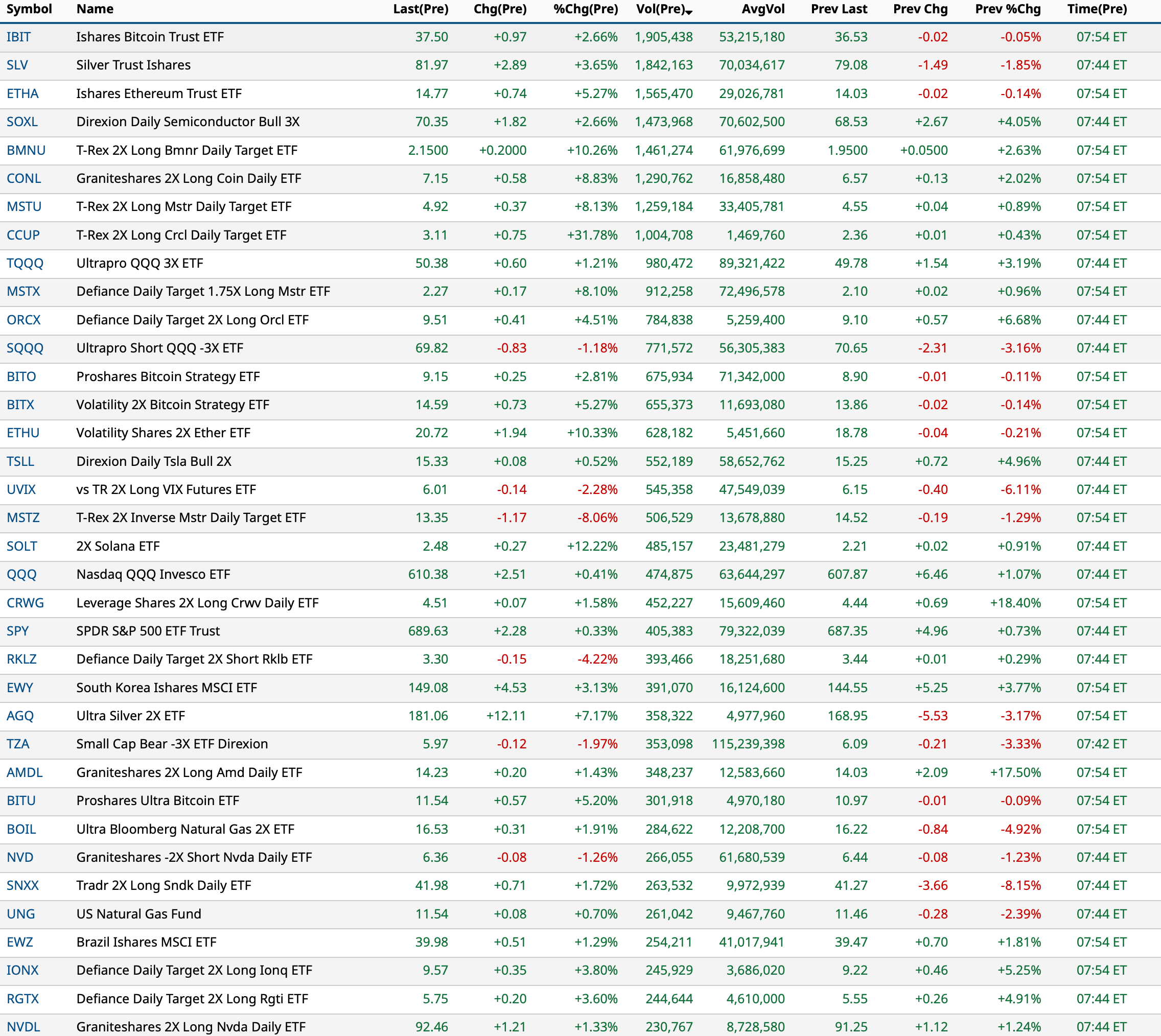

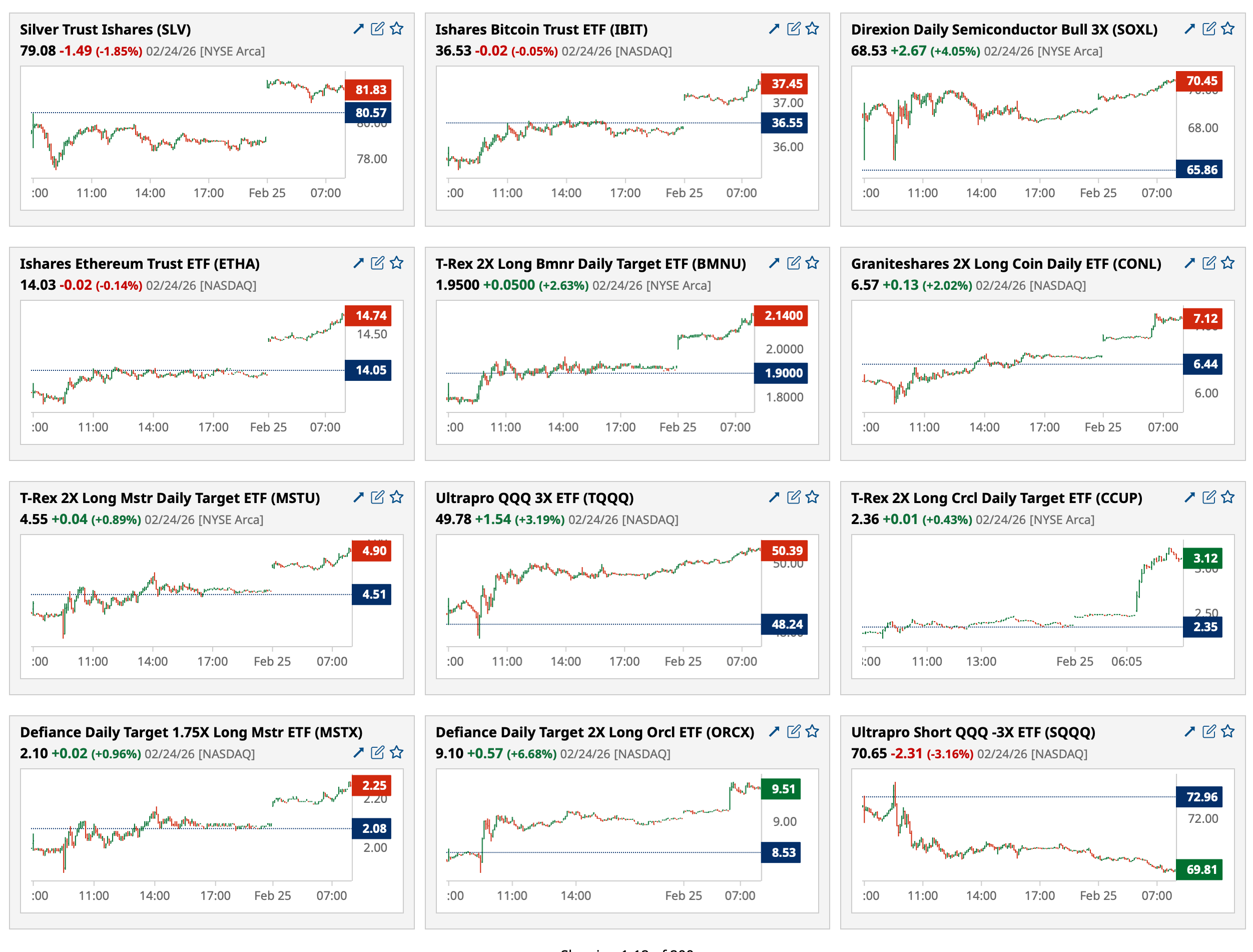

* On this, Nvidia's EPS release day...

Stars shining bright above you

Night breezes seem to whisper, "I love you"

Birds singin' in the sycamore tree

Dream a little dream of me

Say "nighty-night" and kiss me

Just hold me tight and tell me you'll miss me

While I'm alone, and blue as can be

Dream a little dream of me

- Gus Kahn, Dream a Little Dream of Me

Per More Tales (Issue #183!), regarding the slim possibility that the outcomes from “AI” turn out well, below is a link to a rebuttal.

I do not know who the author is but I would hazard a guess he is either an ivory tower academic or someone with a vested interest in the space — such as a VC that has put money into it or the CEO of an AI startup.

From my perspective, the rebuttal is fundamentally and grossly flawed. It starts with the presumption that generative AI works well and that its economic and ignores how it is being financed as well. He starts with this notion, which presumes that Gen AI is all it is cracked up to be, and does not acknowledge all of its attendant issues, failings, and lack of underlying economics.

If you start with erroneous assumptions you will end with unrealistic conclusions. I think the only thing missing from this essay is an offer to sell me a used car, kind of like the previously discussed and dismissed Matt Shumer hype tweet. If the AI is so good, I wonder why he didn’t use it to write his essay too? Interesting both he and Shumer had to write it themselves and then in Shumer’s case, we know from his own tweet he needed three humans to proofread it for him and offer feedback!

“But it depends on a series of assumptions about how economies, labor markets, and human behavior respond to technological deflation, assumptions that have been wrong every single time they’ve been tested over the past two centuries.”

THE 2028 GLOBAL INTELLIGENCE BOOM

Here are some more recent thoughts from someone that has actually been right, a thoughtful and insistent Gary Marcus:

BREAKING: LLM “reasoning” continues to be deeply flawed

About that Matt Shumer post that has nearly 50 million views

I published Issue #183 of More Tales late in the day on Tuesday... so, if you missed it, here is a repost:

FEB 24, 2026 3:39 PM EST

I have been thinking a bit more about the bigger picture regarding Generative AI and then also AI in total and where it may evolve. I think the possibility of it working out well is quite slim and I am no luddite.

This is simplistic, but for arguments sake, assume there are two potential outcomes: It works really well, or it ends up just being what it is now.

What it is now is marginally productivity enhancing for narrow use cases while being wildly dis-economic at the same time and quite resource consumptive (power, water, etc.).

The math does not work once it is not given away for free. Even when free, the productivity benefit is questionable. Once Gen AI providers up and down the stack need to start charging to cover the full underlying costs of delivering the product, forget it. Way more expensive:

That math is if it even works, which it may not, and instead just cause mass chaos on top of not working, which I guess is a different version of the same thing:

We know this is what is now, because we can see the economics in the financials of the businesses involved in Gen AI (for those able to read balance sheets, cash flow statements and be willing to dig into all the off balance sheet stuff and related party transactions as well in addition to goofy things like booking revenue from cloud credits and all sorts of other baloney). We can also see Gen AI’s lack of overall impact on the economy by looking at reported economic statistics. Nothing has changed, with the exception of dollars dumped into the product. No job losses, no productivity gains, no nothing with the exception of money invested, higher electricity costs and higher component costs, including memory that is also used in consumer goods, which implies that to date, Gen AI has been nothing but broadly inflationary.

The result could be the greatest amount of capital destruction in history. The moral equivalent of having paid people to dig holes and then fill them back up, but maybe worse due to all of the attendant issues. I guess they can circularly finance this thing for a while, but the ultimate end is obvious. The longer the players in the Ponzi scheme play the game, the worse the end will ultimately be. No matter how much money the technocrats spend, they all lose.

Take the case where it ends up working really well. Two ways for that to happen.

The Gen AI approach, after not scaling no matter how much money is thrown at it, and continuing to hallucinate, somehow all of the sudden reverses that trend (which has not ever happened with the do more of what is not working approach), and lives up to its promise. Or, Gen AI is scrapped, because a new approach like world models or neurosymbolic AI is developed and actually works.

If it is the latter, that a new approach works, well then the entirety of dollars invested in Gen AI was a massive waste, and many of the entrenched players and investment capital are entirely wiped out. That even includes Nvidia (NVDA) , whose chips likely will not be the backbone of a new approach. There will be new winners that come out of nowhere, but a massive amount of business and capital will have been flushed down the toilet in the process. It would be fine if it was smaller dollars, that is creative destruction. But when ludicrous dollars (including massive amounts of debt financing) are poured into buggy whips, and it is destroyed in rapid fashion, you have a problem.

I guess there is some sort of grey area interim case, that it works OK for some narrow things, but that really is case 1, that it does not work. There is much too much in the way of investment dollars required for marginal and narrow use cases to cover the cost of the investment, and its attendant operating costs.

In either case, if it ends up working, I still cannot see how it ends well. I suspect everyone is familiar with the report from Citrini Tesearch by now: THE 2028 GLOBAL INTELLIGENCE CRISIS

I think this understates reality to some degree. The U.S. and global economy cannot sustain this type of outcome. It is fantasy land. There is no such notion where massive amounts of the population do not work and are supported by some form of universal basic income. That is just voodoo economics and a different version of communism. Are the businesses and individuals that invested trillions into this technology going to turn around and take all the money they made from it and redistribute it to those not working? If so, where is their return on investment, and what was the point? Then on top of it all, prior to this happening, without people working, there is no income for them to spend to generate the consumption that drives revenue in the economy. None of it makes sense. You cannot pencil out an outcome where massive amounts of the population is unemployed, the economy holds itself together, and there is no form of massive civil unrest. It is all voodoo economics and B.S. being sold by the technocrats.

I have a hard time believing the highest probability outcome is that this ends well. For the time being, it is an economic house of cards that is surviving by spinning its own flywheel. Cash flow is already being driven to near zero to do this, so the flywheel cannot be spun any harder than it is now. The fact that OpenAI's latest round of financing is seemingly coming entirely from related parties that are seemingly wrapped up in the flywheel speaks volumes to me.

BY Doug Kass · Feb 25, 2026, 9:30 AM EST

BY Doug Kass · Feb 25, 2026, 8:50 AM EST

11:30 a.m.: Treasury hosts a $69M 17-Week Bill Auction; Treasury hosts a $70B 5-Year Note Auction

9:35 a.m.: Fed Bank of Richmond President Barkin (Non-Voter) speaks and participates in a panel Q&A before the

Northern Virginia Chamber Annual State of the Region event, Tysons, VA (No new text);

11:00 a.m.: Fed Bank of Kansas City President Schmid (Non-Voter) speaks on monetary policy and the economic outlook in fireside chat and moderated Q&A before the Economic Club of Colorado, Denver, CO (No text. Audience Q&A expected. Livestream available);

1:20 p.m.: Fed Bank of St. Louis President Musalem (Non-Voter) participates in moderated discussion on "The Role of the Federal Reserve in the St. Louis Region" before the Missouri Athletic Club Speaker Series, St. Louis, MO (In-person event with virtual option. No text anticipated. No media availability)

BY Doug Kass · Feb 25, 2026, 8:40 AM EST

BY Doug Kass · Feb 25, 2026, 8:30 AM EST

BY Doug Kass · Feb 25, 2026, 8:25 AM EST

"The way to wealth in a bull market is debt. The way to oblivion in a bear market is also debt and nobody rings a bell."

- James Grant

BY Doug Kass · Feb 25, 2026, 8:10 AM EST

BY Doug Kass · Feb 25, 2026, 7:55 AM EST

BY Doug Kass · Feb 25, 2026, 7:42 AM EST

From JPMorgan:

US: Futs are higher into NVDA earnings release (+0.6% pre-mkt) and the risk-on tone in the US yesterday has spread globally with NVDA’s earnings a catalyst for maintaining the rally aided by Tech. Keep an eye on Software if TMT gains positive momentum. Bond yields are +1-3bp, USD is flat, and cmdtys are bid led by Metals with precious outperforming base esp silver / platinum. In Eqys, pre-mkt Mag7 are higher ex-AAPL and TSLA with Cyclicals bid, led by Fins / Indu / Mat and Defensives mostly lower pre-mkt, ex-HC, reflecting the risk-on tone. Today’s macro data releases are light ahead of tmrw’s jobless claims and Friday’s PPI, but with multiple Fedspeakers. Yesterday we saw better weekly ADP data, weaker regional Fed data, and improving consumer sentiment.

and...

Yesterday, we saw a retracing of Monday’s losses as Tech performed well, as did recently sold off sub-sectors related to AI Anxiety / Obsolescence. One example is our OpenAI Ecosystem basket (JPAIOPEN Index) outperformed our Google AI Ecosystem basket (JPAIGOOG) by 326bp, narrowing the OpenAI basket’s YTD underperformance to 29.5%. One key going forward is the message from Anthropic that Software companies will be partners and not competitors; IGV had its best day in two weeks and may be poised for an upside breakout. Regarding Anthropic, keep an eye on the tension between the company and the Federal Government where the Pentagon set a Friday deadline for Anthropic to accept its terms or else have its military contracts terminated. Further, Hegseth is said to have threated to either (i) declare Anthropic a supply-chain risk, similar to companies alleged to work with the militaries of US adversaries or (ii) invoke the Defense Production Act, forcing the use of Anthropic’s software (Axios; BBG; The Hill). The disagreement is centered on Anthropic’s unwillingness to give the Government access without guardrails, specifically, Anthropic wants to prevent to use of its software to conduct surveillance on US citizens or to autonomously target enemy combatants. Last night, Anthropic adjusted firm policy, loosening their safety pledge, which may be a step towards a formal agreement with the Government (BBG). It is unclear if this is an implied endorsement for Anthropic’s products over that of its competitors but keep an eye on how the OpenAI Ecosystem basket (JPAIGOOG Index) trades in the near-term.

BY Doug Kass · Feb 25, 2026, 7:15 AM EST

The three-way pairs trade of long (AMZN) /short (COST) and (WMT) remains among my favorite:

BY Doug Kass · Feb 25, 2026, 7:00 AM EST

Shorting (SPY) at $689.11.

BY Doug Kass · Feb 25, 2026, 6:50 AM EST

* Software in the panic zone and other stories...

Bonus — Here are some great links:

BY Doug Kass · Feb 25, 2026, 6:35 AM EST

Wolf Street howls about the whoosh in electricity demand.

BY Doug Kass · Feb 25, 2026, 6:10 AM EST

BY Doug Kass · Feb 25, 2026, 5:55 AM EST

The S&P Short Range Oscillator remained modestly overbought at 1.26% vs. 1.03%.

BY Doug Kass · Feb 25, 2026, 5:45 AM EST