After-Hours Advancers and Decliners

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Feb 24, 2026, 4:45 PM EST

BY Doug Kass · Feb 24, 2026, 4:45 PM EST

- NYSE volume 14% below its one-month average

- NASDAQ volume 9% below its one-month average

- VIX index: down 6.95% to 19.55

BY Doug Kass · Feb 24, 2026, 4:28 PM EST

I have been thinking a bit more about the bigger picture regarding Generative AI and then also AI in total and where it may evolve. I think the possibility of it working out well is quite slim and I am no luddite.

This is simplistic, but for arguments sake, assume there are two potential outcomes: It works really well, or it ends up just being what it is now.

What it is now is marginally productivity enhancing for narrow use cases while being wildly dis-economic at the same time and quite resource consumptive (power, water, etc.).

The math does not work once it is not given away for free. Even when free, the productivity benefit is questionable. Once Gen AI providers up and down the stack need to start charging to cover the full underlying costs of delivering the product, forget it. Way more expensive:

That math is if it even works, which it may not, and instead just cause mass chaos on top of not working, which I guess is a different version of the same thing:

We know this is what is now, because we can see the economics in the financials of the businesses involved in Gen AI (for those able to read balance sheets, cash flow statements and be willing to dig into all the off balance sheet stuff and related party transactions as well in addition to goofy things like booking revenue from cloud credits and all sorts of other baloney). We can also see Gen AI’s lack of overall impact on the economy by looking at reported economic statistics. Nothing has changed, with the exception of dollars dumped into the product. No job losses, no productivity gains, no nothing with the exception of money invested, higher electricity costs and higher component costs, including memory that is also used in consumer goods, which implies that to date, Gen AI has been nothing but broadly inflationary.

The result could be the greatest amount of capital destruction in history. The moral equivalent of having paid people to dig holes and then fill them back up, but maybe worse due to all of the attendant issues. I guess they can circularly finance this thing for a while, but the ultimate end is obvious. The longer the players in the Ponzi scheme play the game, the worse the end will ultimately be. No matter how much money the technocrats spend, they all lose.

Take the case where it ends up working really well. Two ways for that to happen.

The Gen AI approach, after not scaling no matter how much money is thrown at it, and continuing to hallucinate, somehow all of the sudden reverses that trend (which has not ever happened with the do more of what is not working approach), and lives up to its promise. Or, Gen AI is scrapped, because a new approach like world models or neurosymbolic AI is developed and actually works.

If it is the latter, that a new approach works, well then the entirety of dollars invested in Gen AI was a massive waste, and many of the entrenched players and investment capital are entirely wiped out. That even includes Nvidia (NVDA) , whose chips likely will not be the backbone of a new approach. There will be new winners that come out of nowhere, but a massive amount of business and capital will have been flushed down the toilet in the process. It would be fine if it was smaller dollars, that is creative destruction. But when ludicrous dollars (including massive amounts of debt financing) are poured into buggy whips, and it is destroyed in rapid fashion, you have a problem.

I guess there is some sort of grey area interim case, that it works OK for some narrow things, but that really is case 1, that it does not work. There is much too much in the way of investment dollars required for marginal and narrow use cases to cover the cost of the investment, and its attendant operating costs.

In either case, if it ends up working, I still cannot see how it ends well. I suspect everyone is familiar with the report from Citrini Tesearch by now: THE 2028 GLOBAL INTELLIGENCE CRISIS

I think this understates reality to some degree. The U.S. and global economy cannot sustain this type of outcome. It is fantasy land. There is no such notion where massive amounts of the population do not work and are supported by some form of universal basic income. That is just voodoo economics and a different version of communism. Are the businesses and individuals that invested trillions into this technology going to turn around and take all the money they made from it and redistribute it to those not working? If so, where is their return on investment, and what was the point? Then on top of it all, prior to this happening, without people working, there is no income for them to spend to generate the consumption that drives revenue in the economy. None of it makes sense. You cannot pencil out an outcome where massive amounts of the population is unemployed, the economy holds itself together, and there is no form of massive civil unrest. It is all voodoo economics and B.S. being sold by the technocrats.

I have a hard time believing the highest probability outcome is that this ends well. For the time being, it is an economic house of cards that is surviving by spinning its own flywheel. Cash flow is already being driven to near zero to do this, so the flywheel cannot be spun any harder than it is now. The fact that OpenAI's latest round of financing is seemingly coming entirely from related parties that are seemingly wrapped up in the flywheel speaks volumes to me.

BY Doug Kass · Feb 24, 2026, 4:00 PM EST

With S&P cash +49 handles I am back shorting (SPY) calls.

Screw the operation!

BY Doug Kass · Feb 24, 2026, 3:39 PM EST

Earnings After the Close Tuesday, February 24

Earnings Before the Open Wednesday, February 25

BY Doug Kass · Feb 24, 2026, 2:45 PM EST

I am calling an audible on my short Index calls and covering with S&P cash +46 handles.

I have some (routine) surgery to prepare for and I want to be light over the remainder of the week. I basically broke even on the trade after a few really good trades in the indices.

BY Doug Kass · Feb 24, 2026, 2:35 PM EST

From Peter Boockvar:

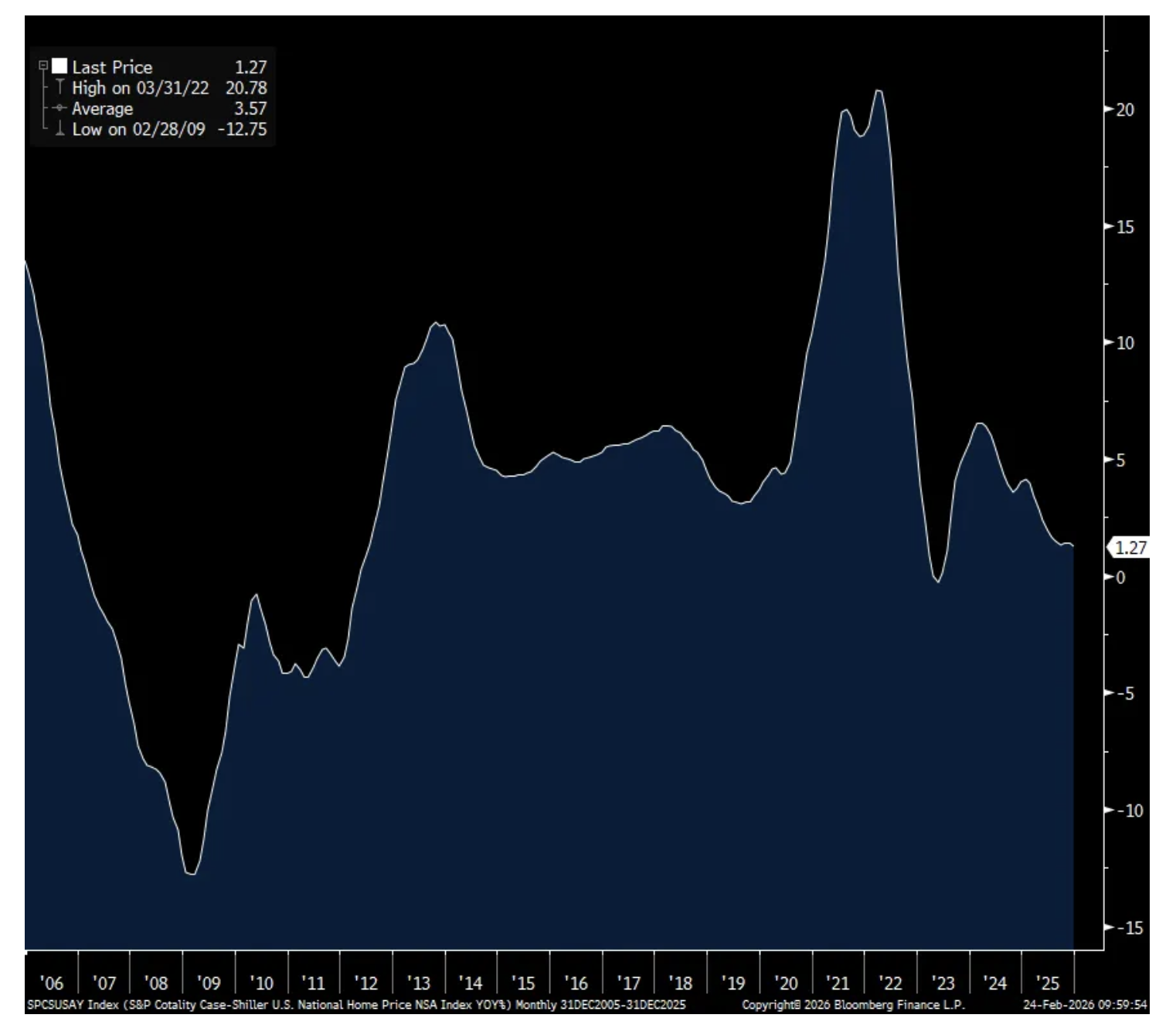

Home price growth in December rose 1.3% y/o/y in S&P Cotality’s national home price index. That’s the slowest rate of gain since July 2023 but I think a very well needed breather in home price gains for those looking to buy a home.

Where most of the home supply has come over the past few years is where the biggest declines are being seen. Such as Tampa, Miami, Phoenix , Denver and Dallas. The biggest price gains are in the supply constrained areas like New York, Chicago, Cleveland and Minneapolis.

Bottom line, after a 50% national gain on average over the past 6 years, I’d say it is a good thing that the pace of increases is slowing down. Yes, for those of us who own our homes we want prices to continue their perpetual gains but in order to add more dynamism to what is still a frozen market with the pace of transactions at 30 yr lows, we need wages to rise faster relative to home price gains and/or an actual drop in home prices, combined with lower mortgage rates and more housing supply to bring in more first time buyers into the market.

Home Price change y/o/y

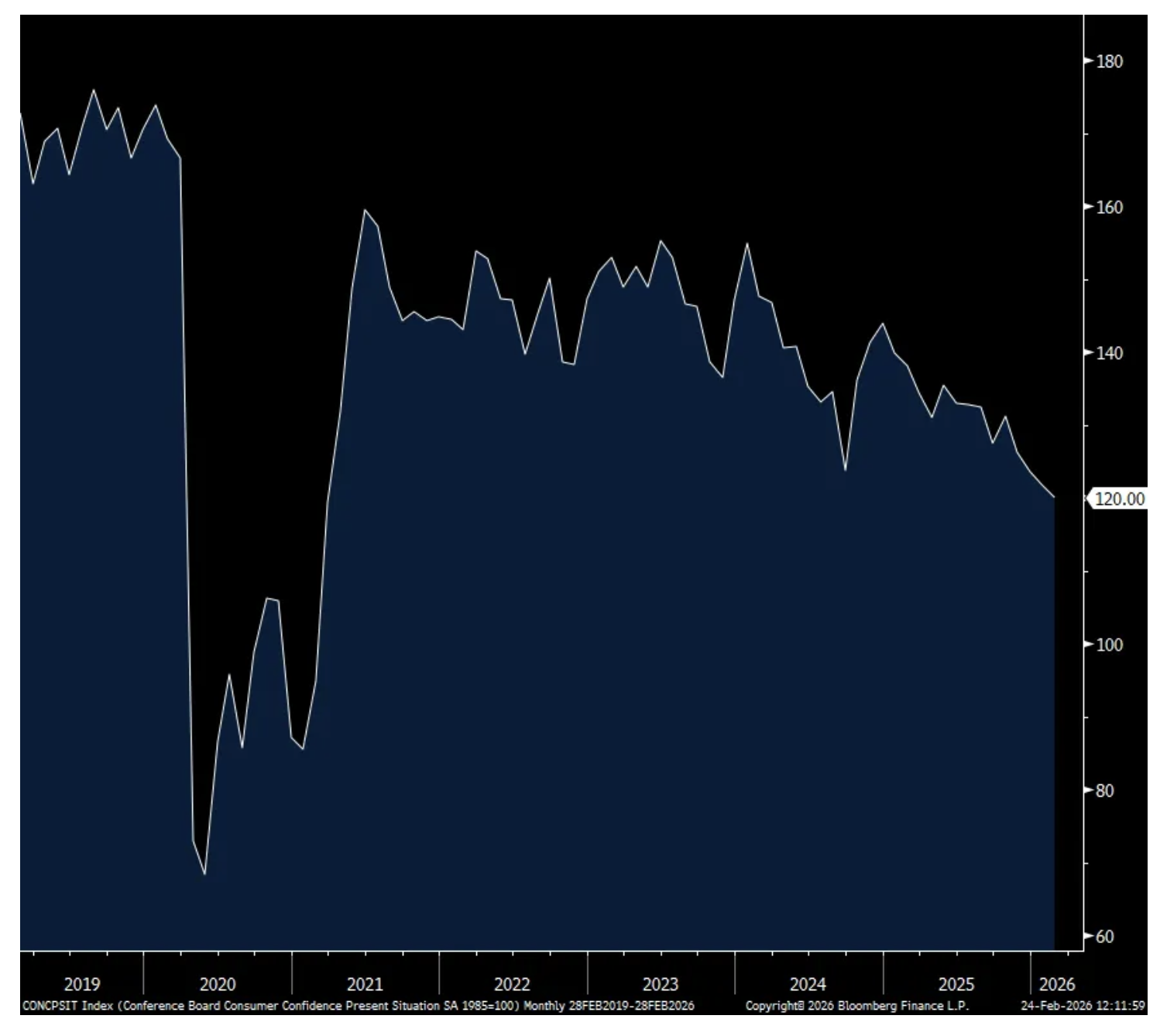

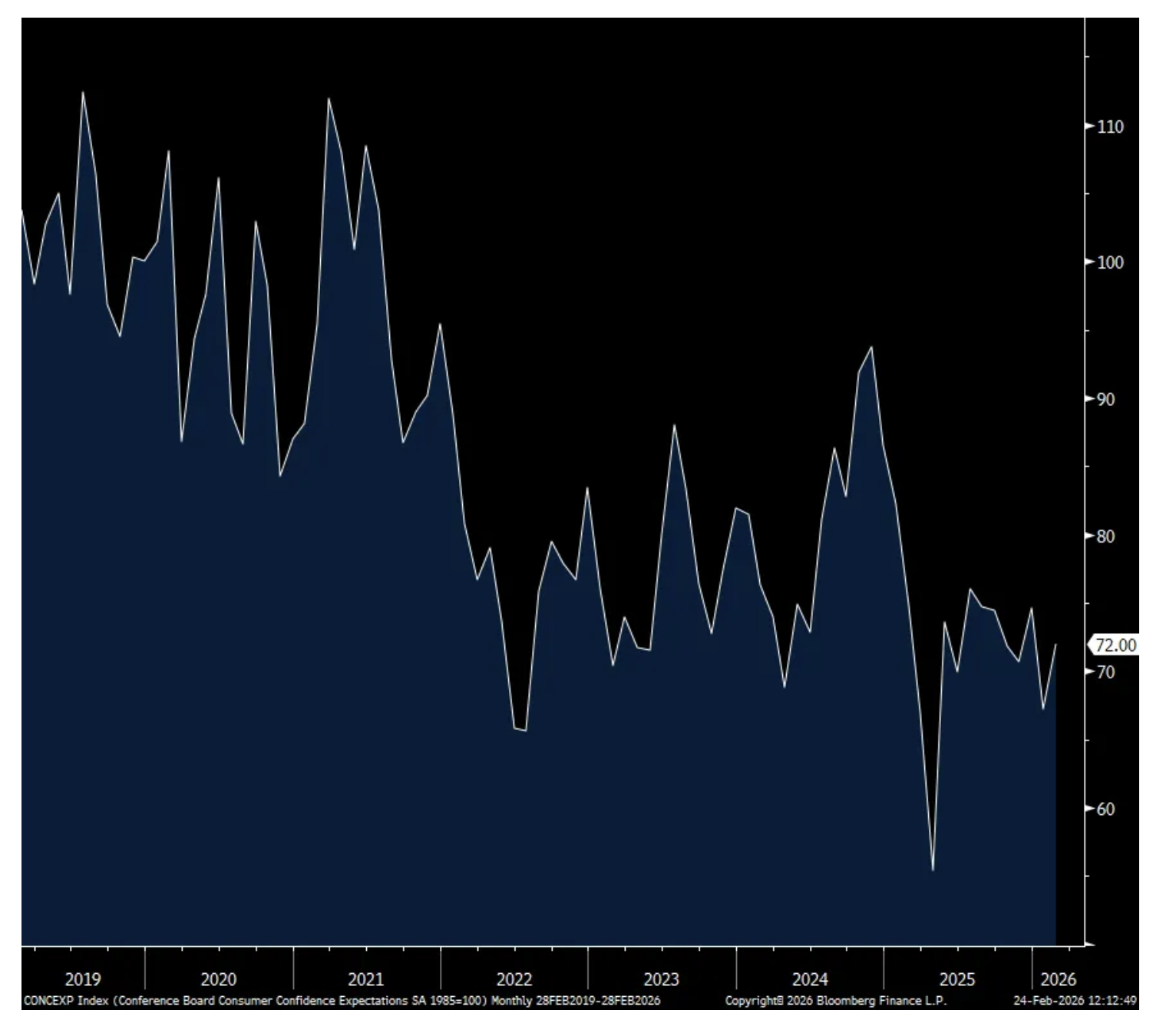

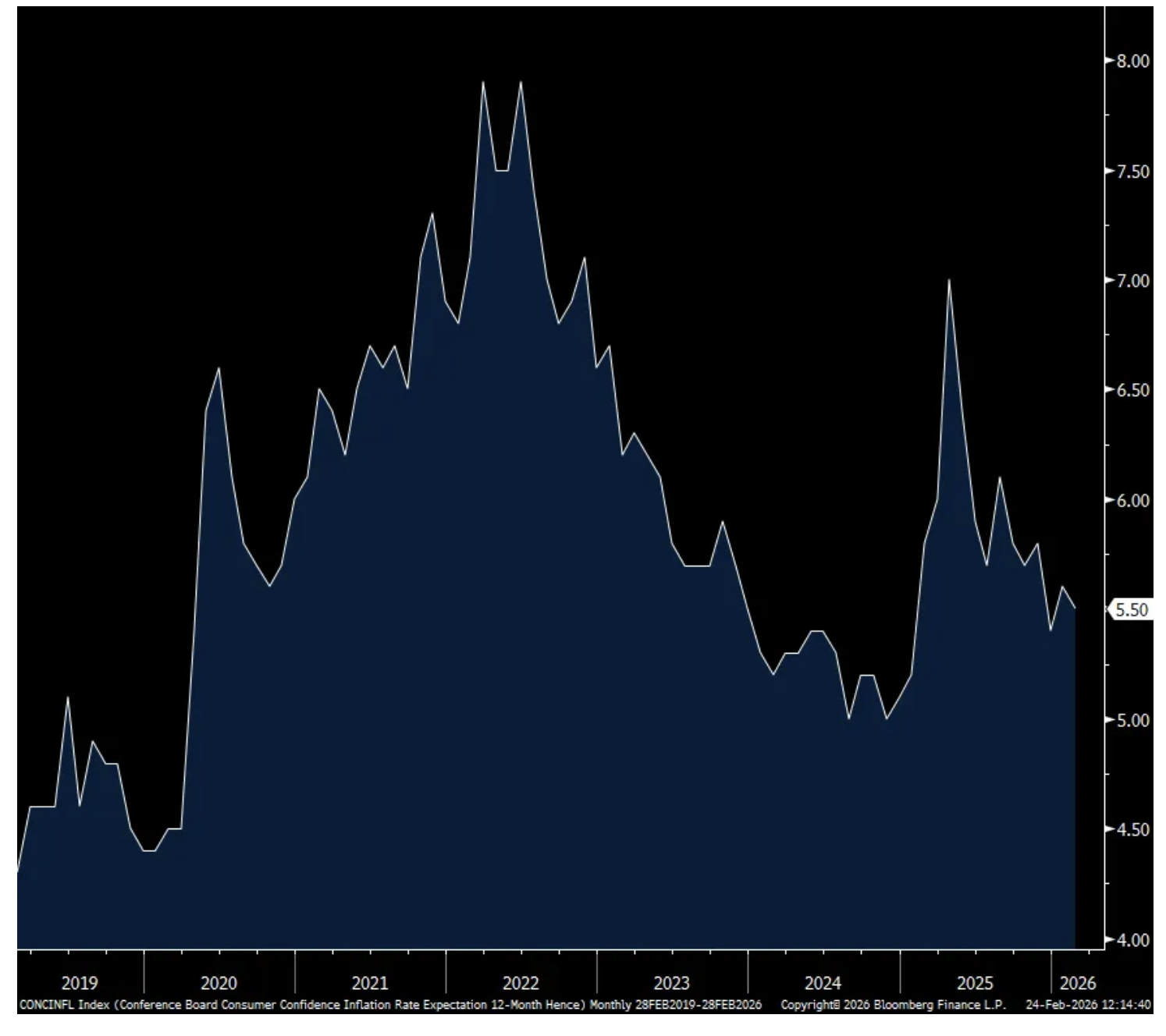

The February consumer confidence index from the Conference Board was 91.2, above the estimate of 87.1 and up from 89 in the month before and vs 94.2 in December. The m/o/m gain was all in the Expectations component which was up almost 5 pts while the Present Situation fell to the lowest level since March 2021. One year inflation expectations were 5.5% vs 5.6% in January and 5.4% in December. It got as high as 7% last year right after the tariff news in April.

The answers to the labor market questions were mixed. Those that said jobs were Plentiful rose 2.2 pts to a 3 month high but those that said they were Hard to Get rose 1.6 pts to the highest since February 2021. Looking out 6 months, off the lowest level since last April, those expecting ‘more jobs’ lifted slightly. Income expectations were little changed.

Spending intentions fell a touch for autos and homes and were up for major appliances.

Demographically, those under 35 were the most optimistic while “By income, confidence on a six-month moving average basis continued to dip for most brackets.”

The bottom line from the Conference Board, “Four of the five components of the index firmed. Nonetheless, the measure remained well below the four year peak achieved in November 2024.” This of course is something we’re well aware of with the very differentiated consumer depending on their level of income.

Present Situation

Expectations

One yr Inflation Expectations

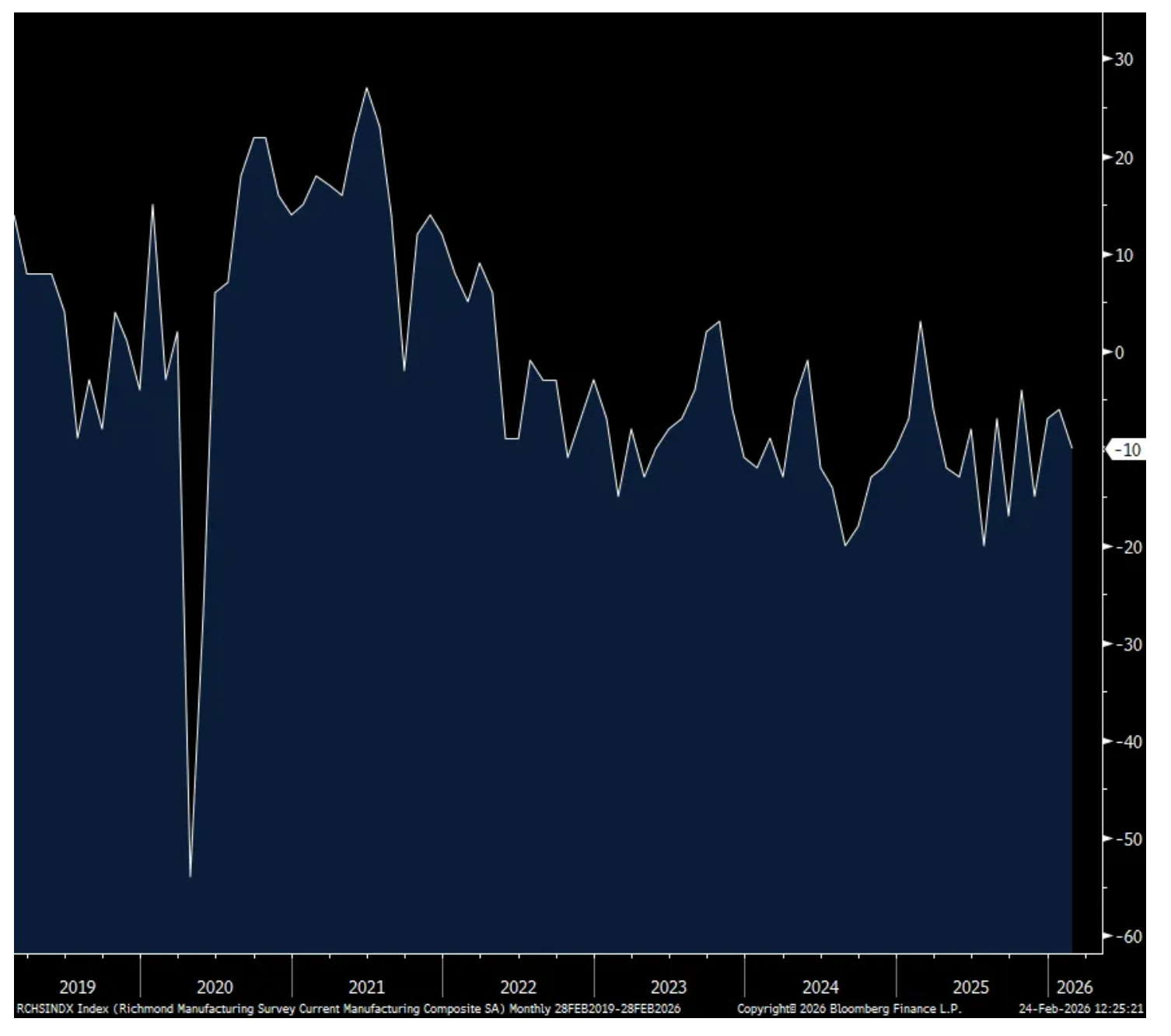

Finally, the Richmond manufacturing survey for February which fell to -10 from -6 and follows a flat read in Dallas and positive ones in NY and Philly. The ISM will reconcile next week all the regional surveys, and it’s expected to print above 50 for the 2nd month in a row. There are signs of a manufacturing bottom but the lift right now is more seemingly related to some inventory build rather than signs seen yet of end demand improvements. That though was not seen in this Richmond survey as it was more a continuation of weak orders.

Richmond Mfr’g

BY Doug Kass · Feb 24, 2026, 1:40 PM EST

On the afternoon advance (S&P cash is now +53 handles) I have moved from very small to small-sized short index calls.

BY Doug Kass · Feb 24, 2026, 1:21 PM EST

I have a conference call from 1 PM to 2:30 PM.

BY Doug Kass · Feb 24, 2026, 12:54 PM EST

With S&P cash +43 handles I am selling another tranche of index calls (short).

But taking baby steps and still very small sized.

BY Doug Kass · Feb 24, 2026, 12:05 PM EST

- NYSE volume 10% below its one-month average

- NASDAQ volume 4% below its one-month average

- VIX index: down 5.76% to 19.80

BY Doug Kass · Feb 24, 2026, 11:20 AM EST

With S&P cash +42 handles, I am (very slowly at first) re-shorting index calls.

BY Doug Kass · Feb 24, 2026, 11:10 AM EST

BY Doug Kass · Feb 24, 2026, 10:50 AM EST

BY Doug Kass · Feb 24, 2026, 10:40 AM EST

"Stanford and Harvard just dropped one of the most unsettling papers on AI agents I've read in a long time. It's called "Agents of Chaos." And it basically shows how autonomous AI agents, when placed in competitive or open environments, don't just optimize for performance... They drift toward manipulations, coordination failures and strategic chaos. This isn't a benchmark flex paper. It's a systems-level warning."

https://x.com/alex_prompter/status/2026226107104817207

BY Doug Kass · Feb 24, 2026, 10:25 AM EST

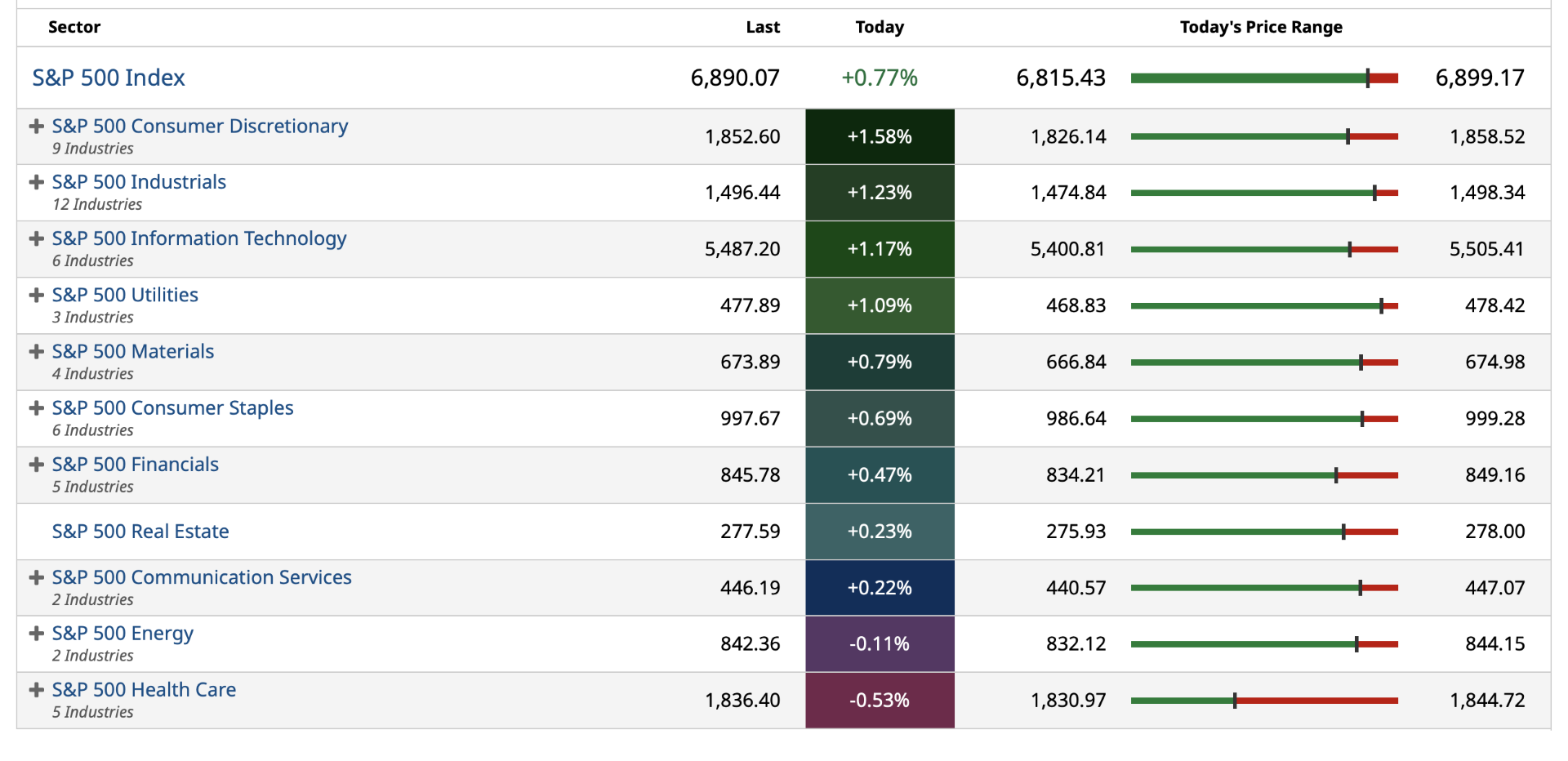

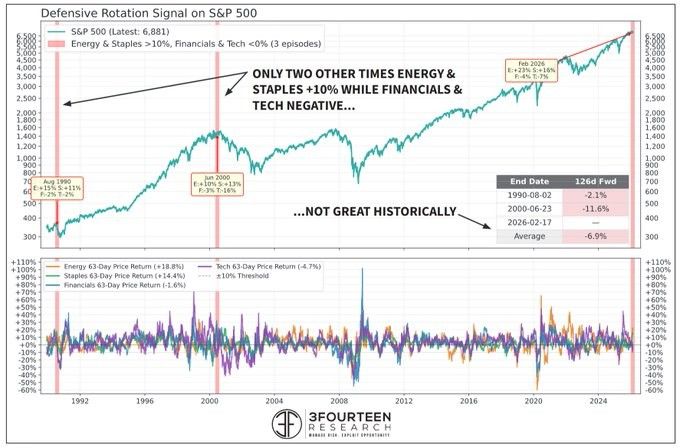

* Violent rotation (from tech/financial to staples), private equity concerns and disruptive AI tools — were the major market themes yesterday

* Over history, leadership changes are typically market unfriendly

* 'Ruby or Manic' Tuesday? To be honest I am clueless whether there will be follow thru today in "the market without memory"

* Mick Jagger had the ticket — as yesterday don't matter when its gone

* So I will continue to trade opportunistically — shorting the rips and covering the dips

* A few more days like Monday would be more conclusive evidence, that, in technical terms, the U.S. stock market is making an important top

"Employment's down

He tells me in his bedroom voice

"C'mon, honey, let's go make some noise"

Time, it goes so fast (when you're having fun)

It's just anther manic Monday

I wish it was Sunday'

Cause that's my fun day

My I don't have to run day"

- The Bangles, Manic Monday

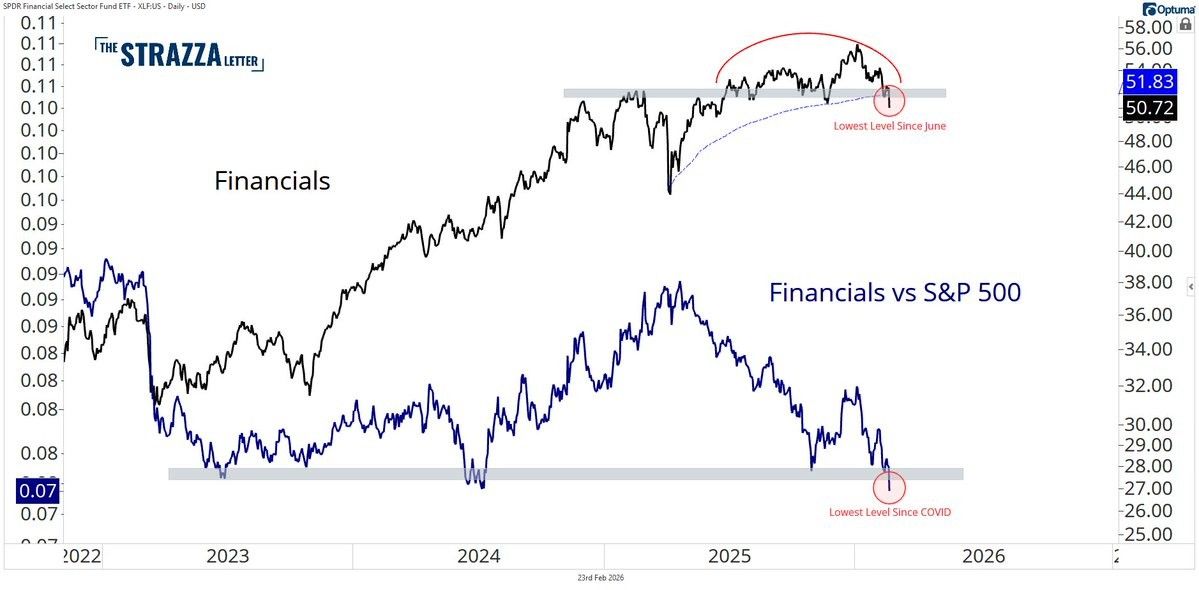

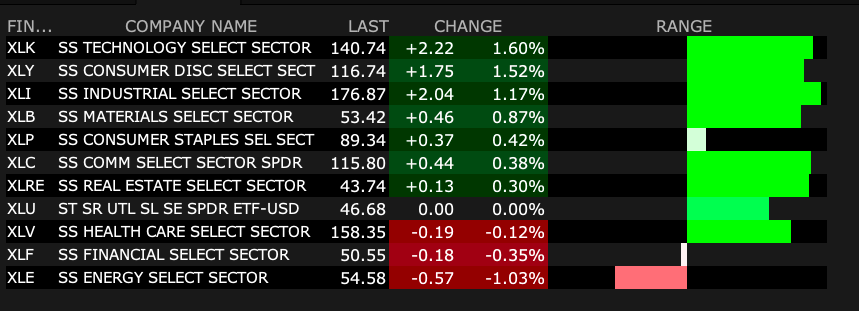

Yesterday's price action was brutal with plenty of rotation (away from technology and financial and towards defensive, consumer staples).

Historically, leadership changes are market unfriendly. As seen in the chart below, financials and technology were down by over 1% on Monday while energy and staples were higher. Over the last 60-65 trading days, energy and staples are up by more than 10%, while financials and technology are negative. There have been only two times in history that these two events have occurred — in 1990 (Desert Storm) and in 2000:

Contributing to the exaggerated moves were the machines and algos (a move that I predicted in my 10 Surprises for 2026). Add to this was Anthropic's potential disruption of the sagging software sector and threat to cybersecurity firms that hit IBM (IBM) , CrowdStrike (CRWD) , Palo Alto (PANW) and others where it hurts.

A shift in market structure resulted in passive products and strategies producing a movie in reverse as compared to what we have witnessed over the last five years.

This has been a constant warning and market concern of mine. I described it, yesterday, as the The Revenge of the Nerds:

* 2026 is already becoming a surprising year...

* Though it is still early in the year, one of my surprises — that a basket of consumer staples ( (PEP) , (KO) , (PG) and (KMB) ) will materially outperform the Mag 7 by a decisive amount in 2026 — appears to be developing...

The AI bubble bursts as the circular financing deals unwind (or are pushed out) — AI capital spending slows abruptly as return on investment concerns emerge as power generation and grid modernization are bottlenecks. Depreciation charges and lower demand wrecks havoc with consensus AI 2026-27 earnings per share expectations. Another big AI surprise would be if China decides to flood markets with inexpensive AI models — pressuring the ultimate and expected robust ROI forecasts (which are already in question by some skeptics).

OpenAI's Sam Altman finds a place to live right next door to Sam Bankman-Fried. His effort to make OpenAI too big to fail, fails. ChatGPT turns out to at best be a commodity large language model purveyor. It becomes obvious to all that its recent $500 billion-plus valuation can’t be supported. Without an ability to do a down round without losing face, OpenAI loses all access to capital. Ultimately, a consortium of its customers and suppliers takes it over to modify its business plan and reduce the cash burn.

With Altman tossed to the curb (or worse), the prosecutions begin.

OpenAI’s problems pushes a deeply committed (to OpenAI) Softbank to the verge of collapse.

Nvidia shares fall by -40% as CoreWeave (CRWV) is driven into bankruptcy.

A basket of defensive consumer nondurable equities ( (PEP) , (KO) , (PG) and (KMB) ) materially outperform the Mag 7 by a decisive amount.

The shares of (boring and previously hapless) PepsiCo outperform most other staples and 90% of the S&P Index after a much better skein of organic unit growth and as its core business is rationalized.

- Kass, 10 Surprises for 2026

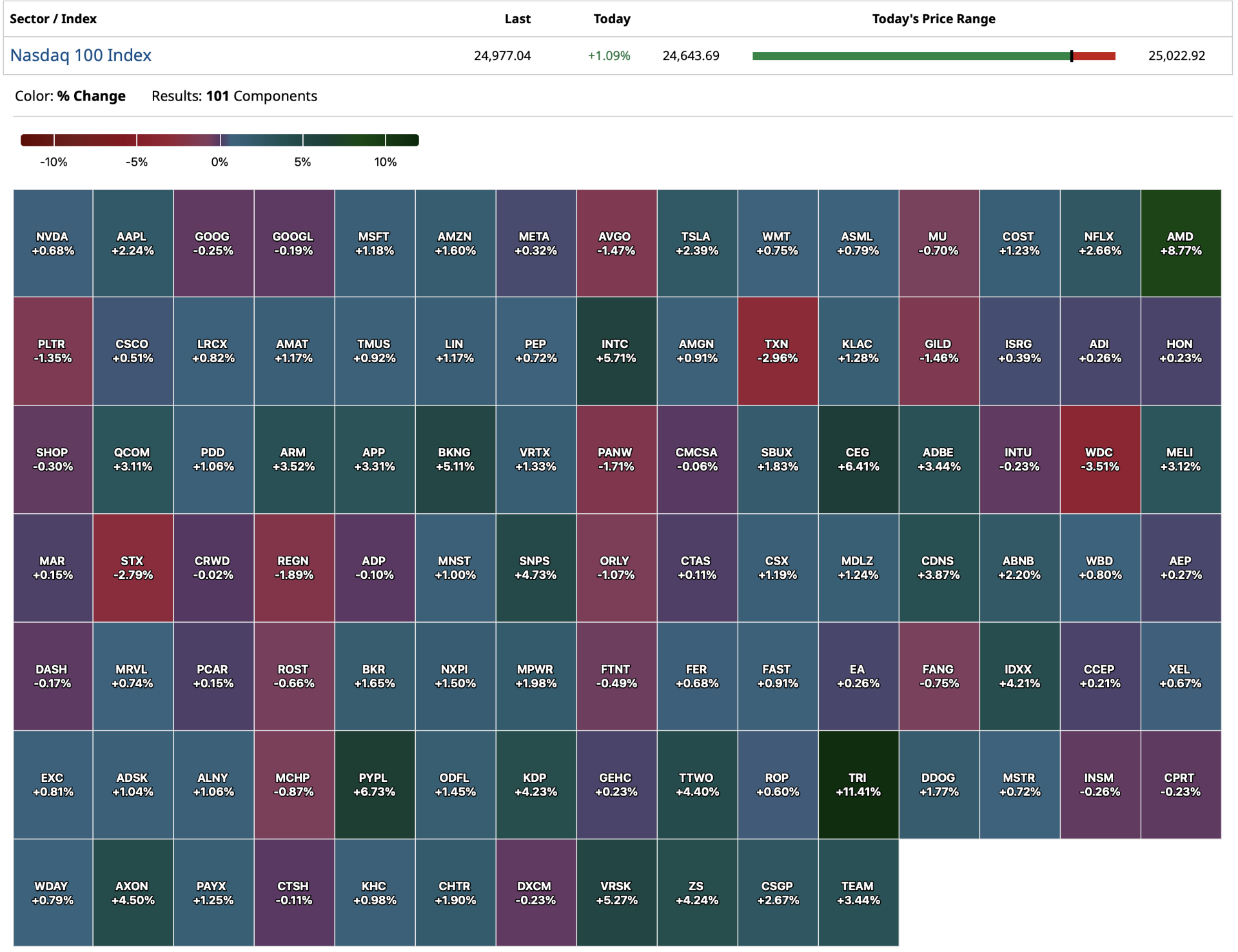

Today, in a day in which the S&P index is -1%, a package of staples (PEP, PG, KO and KMB) are conspicuous winners:

* (PEP) +$2.37

* (PG) +$3.16

* (KMB) +$1.57

* (KO) +$0.33

By contrast, the components of Mag 7 are stumbling badly and are conspicuous losers:

* (TSLA) -$10.70

* (AAPL) +$2.20

* (AMZN) -$5.71

* (NVDA) +$0.35

* (MSFT) -$11.43

* (GOOGL) -$2.20

* (META) -$11.66

By Doug Kass Feb 23, 2026 11:50 AM EST

The financial space suffered as much as technology as concerns that AI will destabilize financial intermediaries and the tail of private equity worries boiled over. The later, was also a part of my Surprise List:

Valuation opacity, a compression in exit multiples and unrealistic net asset value marks (mark to model delays volatility but doesn't remove it) in private equity come into focus in 2026. The greatest problems are companies tied to commercial real estate and Saas companies. There are a number of high-profile bankruptcies in notable private equity portfolios.

A market for stranded LP interests trading at deep discounts becomes widely followed. Further, the IPO market continues to not be a viable exit for most holdings. Gated redemptions become common place. Apollo (APO) , TPG (TPG) , KKR (KKR) and Ares (ARES) each fall by 30%.

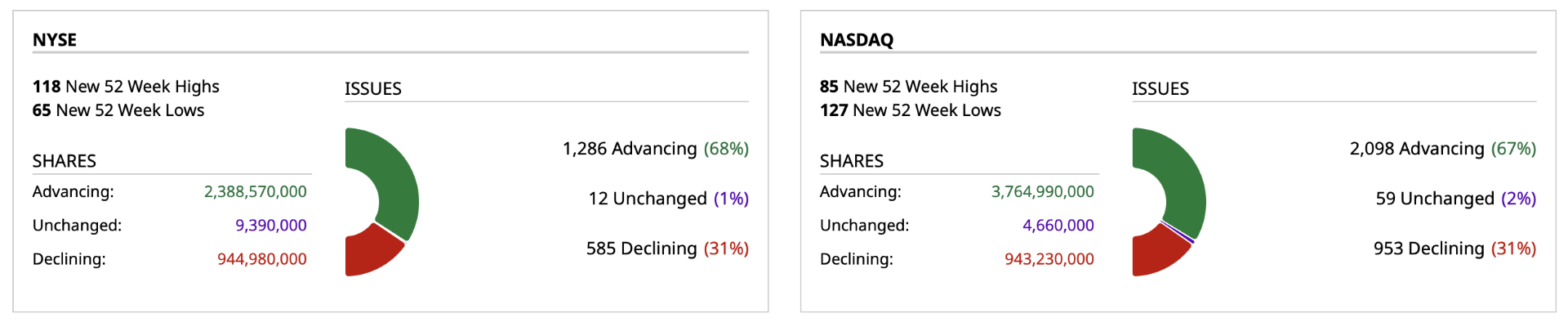

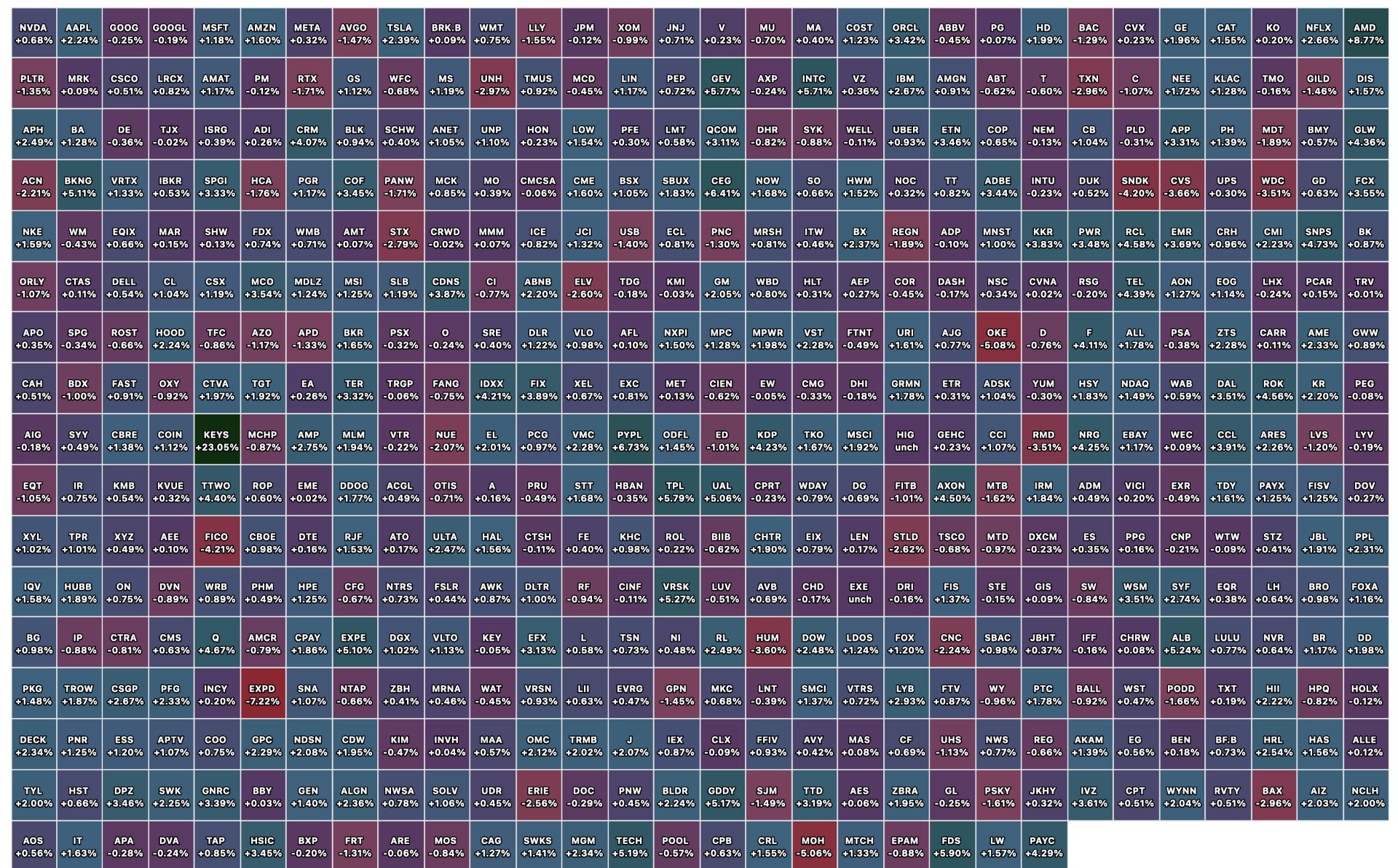

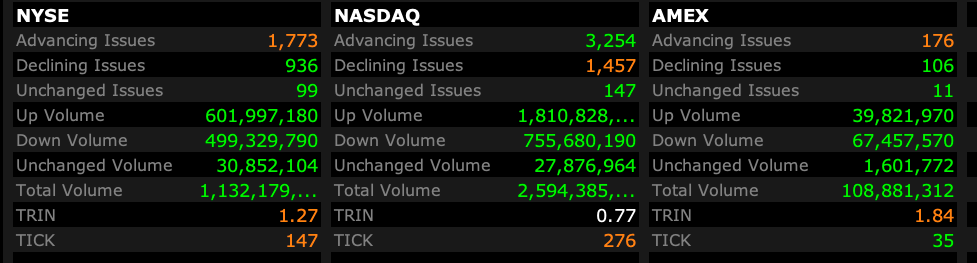

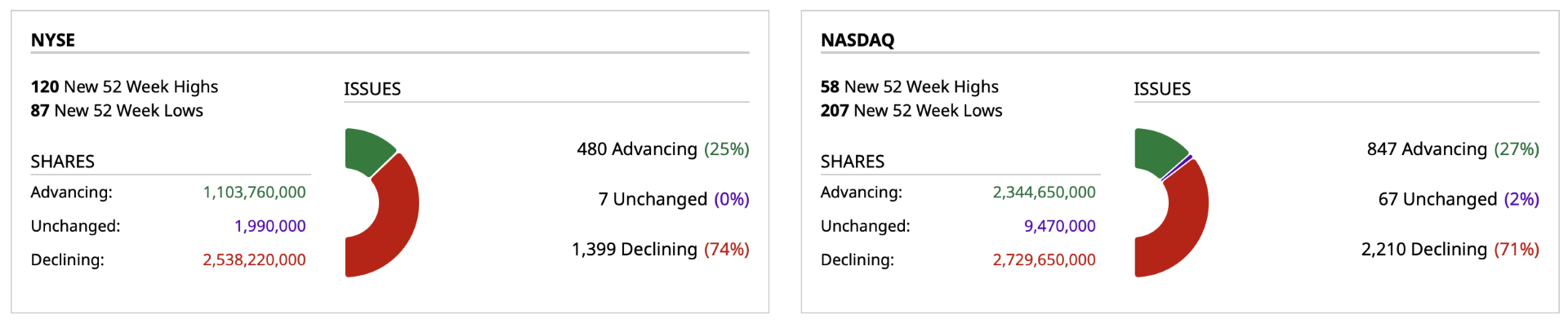

Market breadth was overwhelmingly negative — though falling far short of a 80% down day (h/t Wally Deemer):

As I write this its already 6 AM, what to do next?

Six o'clock already, I was just in the middle of a dream

I was kissin' Valentino by a crystal-blue, Italian stream

But I can't be late, 'cause then I guess I just won't get paid

These are the days when you wish your bed was already made

- The Bangles, Manic Monday

Unfortunately it is unclear to me as the market without memory seems to have a different chapter day after day — sometimes hour after hour.

Tactically, I continue to successfully short the rips and cover the dips, trying to capture alpha in an unpredictable market. (You might recall, late in the morning, the S&P cash index actually turned positive for a brief period of time (at which point we re-shorted)).

She would never say where she came from

Yesterday don't matter if it's gone

While the sun is bright or in the darkest night

No one knows, she comes and goes

- The Rolling Stones, Ruby Tuesday

While there exists a possibility of a Ruby Tuesday, I am inclined to expect more volatility with limited upside today. But this is a guess as there is nothing scientific behind the "forecast."

A few more days like Monday would be more conclusive evidence, that, in technical terms, the U.S. stock market is making an important top.

Regardless of market direction I will continue to report my trading moves in real time.

I continue to see equities, from an intermediate view, to be under pressure with continued volatility — ideal for opportunistic traders but not so great for the buy-and-hold crowd.

I hope this helps.

BY Doug Kass · Feb 24, 2026, 9:25 AM EST

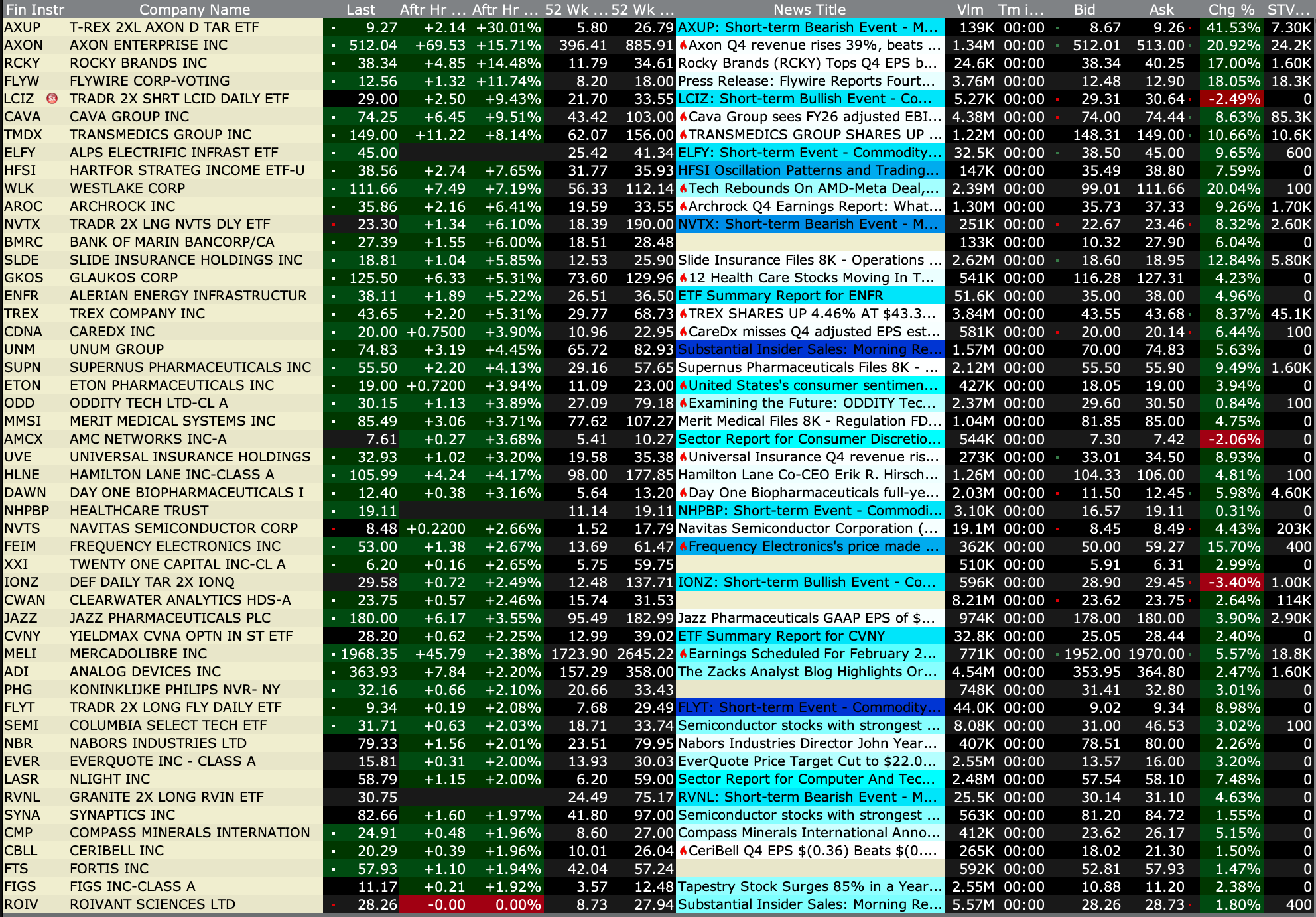

Upside:

-VIR +34% (Astellas and Vir Biotechnology Announce Global Strategic Collaboration to Advance PSMA-targeting PRO-XTEN® Dual-masked T-Cell Engager VIR-5500 for the Treatment of Prostate Cancer; earnings)

-LRMR +33% (US FDA Grants Breakthrough Therapy Designation for Nomlabofusp in Friedreich’s ataxia (FA) and Reiterates Planned BLA Submission in June 2026)

-PVLA +31% (Phase 3 SELVA Clinical Study of QTORIN 3.9% Rapamycin Anhydrous Gel (QTORIN rapamycin) in Microcystic Lymphatic Malformations Met Primary Endpoint)

-CLVT +24% (earnings, guidance)

-SGHC +23% (earnings, guidance)

-THR +18% (CECO to merge with Thermon Group Holdings in $2.2B stock and cash deal)

-HTCR +14% (authorizes $2M share repurchase program)

-KEYS +14% (earnings, guidance)

-AMD +9.8% (AMD and Meta Announce Expanded Strategic Partnership to Deploy 6 Gigawatts of AMD GPUs)

-PLBY +7.3% (reports prelim Q4 revenue)

-INTU +7.2% (signs multi-year partnership with Anthropic to bring custom AI agents to mid-market businesses on the Intuit platform and highly personalized experiences for consumers and businesses)

-FRPT +5.2% (Morgan Stanley Raised FRPT to Overweight from Equal Weight, price target: $90 from $71)

-ANET +5.0% (hearing Goldman raises price target)

-FIS +3.0% (earnings, guidance)

-RAL +3.0% (reportedly activist investor Irenic has built a stake, pushing for cost cutting and accelerated share buyback)

-MBOT +2.9% (Tampa General Hospital is the First Health System in Florida to Adopt the LIBERTY Endovascular Robotic System)

-HD +2.6% (earnings, guidance)

-QCOM +2.5% (multiple broker upgrades)

-KDP +2.1% (earnings, guidance)

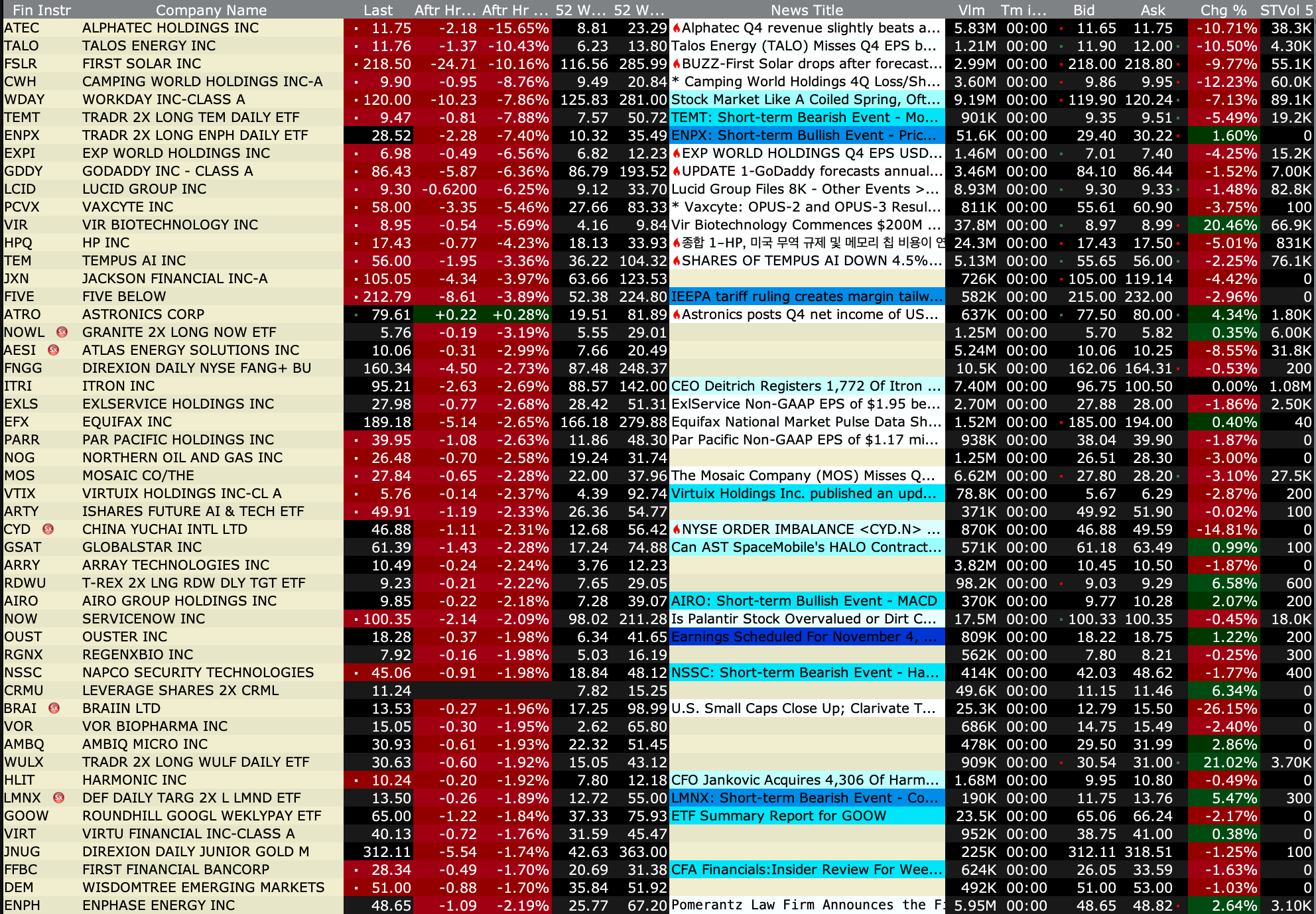

Downside:

-FULC -14% (announces 12-Week Results from the 20 mg Dose Cohort of the Phase 1b PIONEER Trial of Pociredir in Sickle Cell Disease; earnings)

-WHR -11% (announces ~$800M common stock offering; files automatic mixed shelf of an indeterminate amount)

-ZD -11% (earnings)

-GOSS -10% (Barclays Cuts GOSS to Underweight from Overweight, price target: $0.30)

-UCTT -9.1% (earnings, guidance)

-HIMS -6.5% (earnings, guidance)

-AS -6.2% (earnings, guidance)

-PLNT -5.6% (earnings, guidance)

-KYNB -5.2% (announces data from the Investigator-Sponsored Phase 1b/2 Study of FG-3246 in Combination with Enzalutamide in Patients with Metastatic Castration Resistant Prostate Cancer to Be Presented at ASCO GU 2026)

-PAY -4.6% (earnings, guidance)

-NVO -3.0% (reportedly Novo Nordisk to cut Ozempic list price by 34% to $675/month and Wegovy prices by 50% to $675/month, effective from Jan 2027)

-KTOS -2.6% (earnings, guidance)

-FWRG -2.1% (earnings, guidance)

BY Doug Kass · Feb 24, 2026, 9:15 AM EST

From Peter Boockvar:

I know the stock market is taking the attitude that GenAI is going to disrupt just about everything but I do know that for every horse and buggy maker that went out of business there are a lot more bank tellers today than imagined when the ATM machine was first invented, to use some examples. Rather than an AI driven dystopian future that some are writing about, I’m still sticking to the belief that technology will ALWAYS end up creating more new jobs than it destroys and this time won’t be different. That said, technological obsolescence is always real, something that will never change and why I prefer investing in businesses that most likely won’t get disrupted and instead will benefit from productivity enhancing technology. I like boring, unexciting companies, especially now.

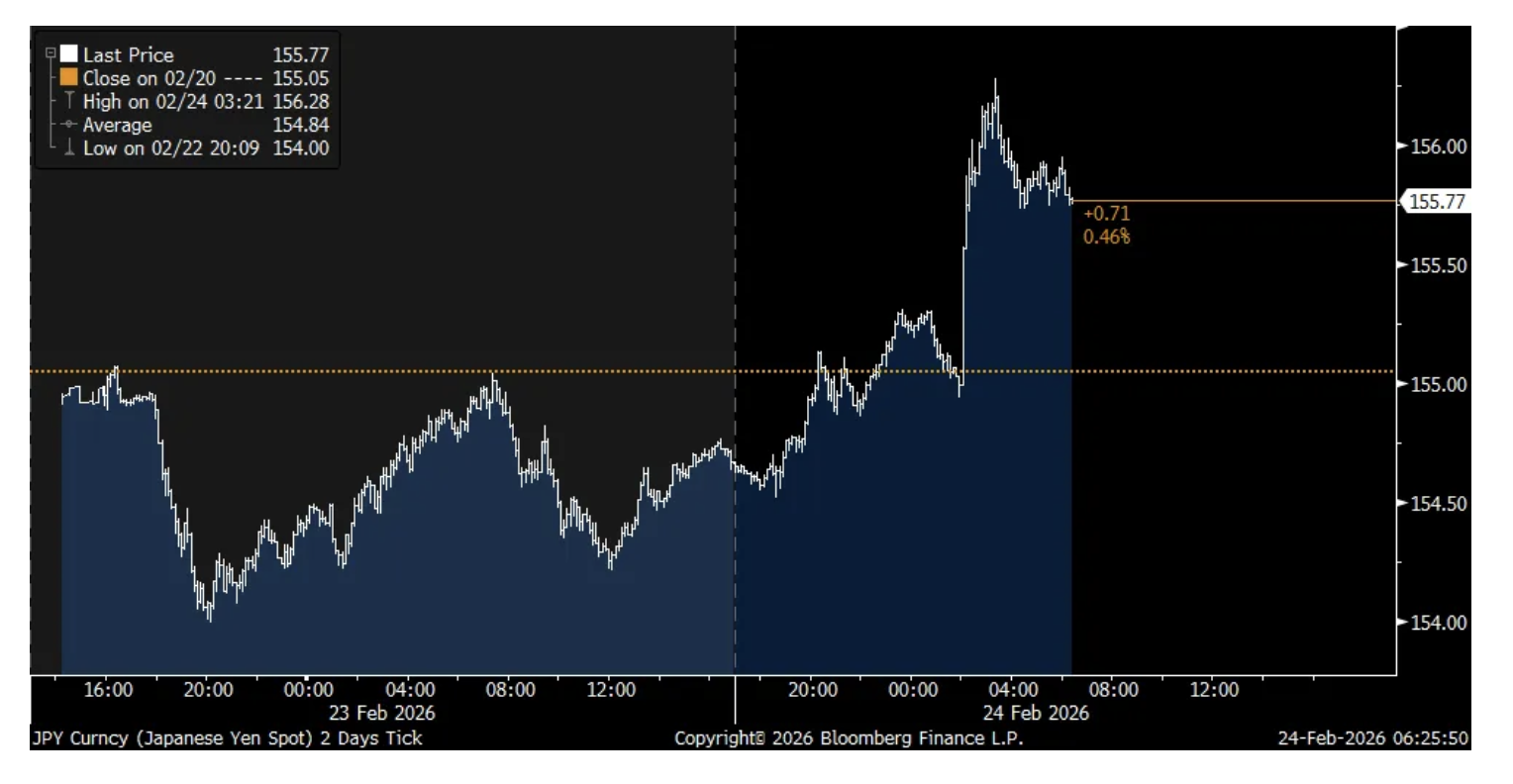

The key factor as to why Sanae Takaichi is the Japanese Prime Minister is because the populace was unhappy with inflation and blamed her predecessor for it. Rather than taking this message to heart and giving a blessing to the Bank of Japan in dealing with it via interest rates, she supposedly told BoJ Governor Ueda last week when they met for a coffee talk that she wouldn’t like more rate increases. This story comes from Mainichi newspaper “citing unidentified people.”

In response, the yen is down almost 1%, which in turn helps to lift inflation. The 2 yr yield fell 4 bps to 1.22% and by 3-5 bps for the 10s, 30s and 40s.

2 day chart in Yen and you can see reaction

Everything I’m reading points to a nice lift in travel and consumer spending behavior in China during their Lunar New Year holiday. According to the South China Morning Post “An 8.6% increase in Lunar New Year spending is a rare bright spot in Chinese efforts to bolster domestic demand.” That gain covers the first four days that they have data on but said “The nine-day holiday, which finished Monday, also set records for domestics and overseas travel.” As we own some of the Macau casino stocks, visitation there totaled about 1.55 million over the 9 days, according to figures out, which compares with 1.31 million in the 8 days last year. So on average, about 172k vs 164k in the year before, an increase of around 5%.

What the Chinese economy now needs to really unleash the Chinese consumer with their massive pile of savings is for home prices to stop going down. I talk about this because the Chinese consumer has global economic ramifications as they love to travel around the world and spend money and also some key US brands have a large presence there, as we know.

After a lift in the February NY and Philly manufacturing indices well into positive territory, the Dallas regional survey was around the flat line at +.2 vs -1.2 in January. Something that sticks out in the internals was the jump in ‘finished goods inventories’ to +8.9 from -12.2 and that is the first print above zero since last August which tells me that at least right now, most of the improvement we’ve seen in some manufacturing stats/surveys has to do with inventory building more so than a lift in end demand, at least right now.

Disappointingly was the negative print in Capital Expenditures for the first time since last April and they also fell in the 6 month outlook.

Here were some notable comments with tariffs still a factor. And this was the most upsetting quote from a company in the Fabricated Metal Product sector, “We do not have debt, [and we] own our property. But we are closing our family business, active since 1958, because customers [either] are not buying or [are not] paying on time. Solid production demand in first half [of 2026], expected to slow a bit in second half.”

This quote from a company in the Transportation Equipment sector highlights my main concern with the impact of tariffs:

“The new tariffs are killing small-to-medium-sized manufacturing firms in several instances. One such example is the importation of tungsten. We purchase tungsten carbide from a U.S. firm, but they have no option but to purchase their raw materials from China, so the [tariff] costs get passed on to us. Our competitors in Ireland and Sweden are able to purchase the material from China with no tariffs involved. So, they can manufacture at lower prices and export to the U.S. U.S. manufacturing firms like us cannot compete under these circumstances.”

Here were some others of note:

Computer and electronic product manufacturing

Extreme volatility in the price of silver has affected us, but we have been able to pass price increases through to customers. In spite of the AI sound and fury in the stock market, the “real economy” continues to chug along. Our customers continue to place regular orders and have accepted price increases averaging 5-6 percent over last year.

Availability dried [up], and prices increased significantly. Larger orders that need multiple management approval are difficult to manage since prices and availability are unpredictable. Prices tend to increase without notice; in some cases, twofold.

Machinery manufacturing

Business remains strong, and we are receiving many new large opportunities.

The floodgates have opened! What we’ve been praying for and hoping for is finally coming to fruition. We look to be firing on all cylinders this year and making up for lost time.

Nice and steady which is good.

Paper manufacturing

Continued depressed demand.

Printing and related support activities

It’s just crazy how little demand is out there right now. We are seeing some uptick in quoting, and we will soon start to get jobs that normally occur in the spring and summer. We blame it all on the chaos and lack of consistency coming out of the federal government.

Transportation equipment manufacturing

While we and our customers are seeing positive market signs, they are not large enough or consistent enough to instill any degree of confidence.

Consumer confidence for large purchases is still weak.

Beverage and tobacco product manufacturing

Our sales got off to a surprisingly strong start this year, which has us playing catch-up. That, along with a planned shutdown for a week in January for annual maintenance, has us scrambling right now. Whether these strong sales continue for the year or are just an anomaly is unknown, but we are treating this as a trend that will last for most of the year.

Home Depot is trading up about 3% pre-market with slightly better than expected comps and said this on their business:

“For the fourth quarter, our results were largely in-line with our expectations, reflecting the lack of storm activity in the third quarter and ongoing consumer uncertainty and pressure in housing. Adjusting for storms, underlying demand was relatively stable throughout the year.”

From Domino’s Pizza and whose stock rose 4% yesterday:

“Before I highlight our great 2025 and look ahead to 2026, I want to provide my perspective on the QSR Pizza category in the US. There seems to be a narrative out there that pizza is a challenged and declining category. That is just not true. Looking back to 2019, you’ll find a category that has generally grown approximately 1% to 2% per year, including last year, 2025. I am confident QSR Pizza will continue to grow at this historical rate in 2026 and beyond.” So am I as a consistent consumer of pizza.

“Despite a challenging macro environment that impacted the entire restaurant industry...We grew both our carryout and delivery businesses again this year in the US...We also drove positive order counts in both our US and International businesses.”

“And in a year when customers continued to seek value, we innovated with our Best Deal Ever promotion.”

In response to the bifurcated consumer out there, “certainly in QSR, there’s been a lot of stuff written about the lower income cohort declining. That is not something that’s happened in Domino’s. We grew that. We grew all income cohorts in Q4 and for the full year.”

From Freshpet, up 5% yesterday:

“Our data suggests that despite the macroeconomic headwinds we experienced last year and continue to see today, the total addressable market for Freshpet continues to grow and is now up to 36 million households compared to the 33 million households we announced at CAGNY last year. These figures reflect consumers’ ongoing interest in treating their pets as valuable family members and the growth is driven in part by the ongoing generational transition to younger consumers for whom pets and high quality food are of greater interest than previous generations.”

“Our fastest growing buyer group is our ultra buyers, who make up nearly 500,000 households and spend over $1,100 a year on Freshpet. Overall, we are not seeing trade down, and we are not seeing loyal customers buying us less often. We are continuing to win with new dog households, the next generation dog owners, Millennial and Gen Z, and believe our omnichannel strategy will drive further growth with these cohorts.”

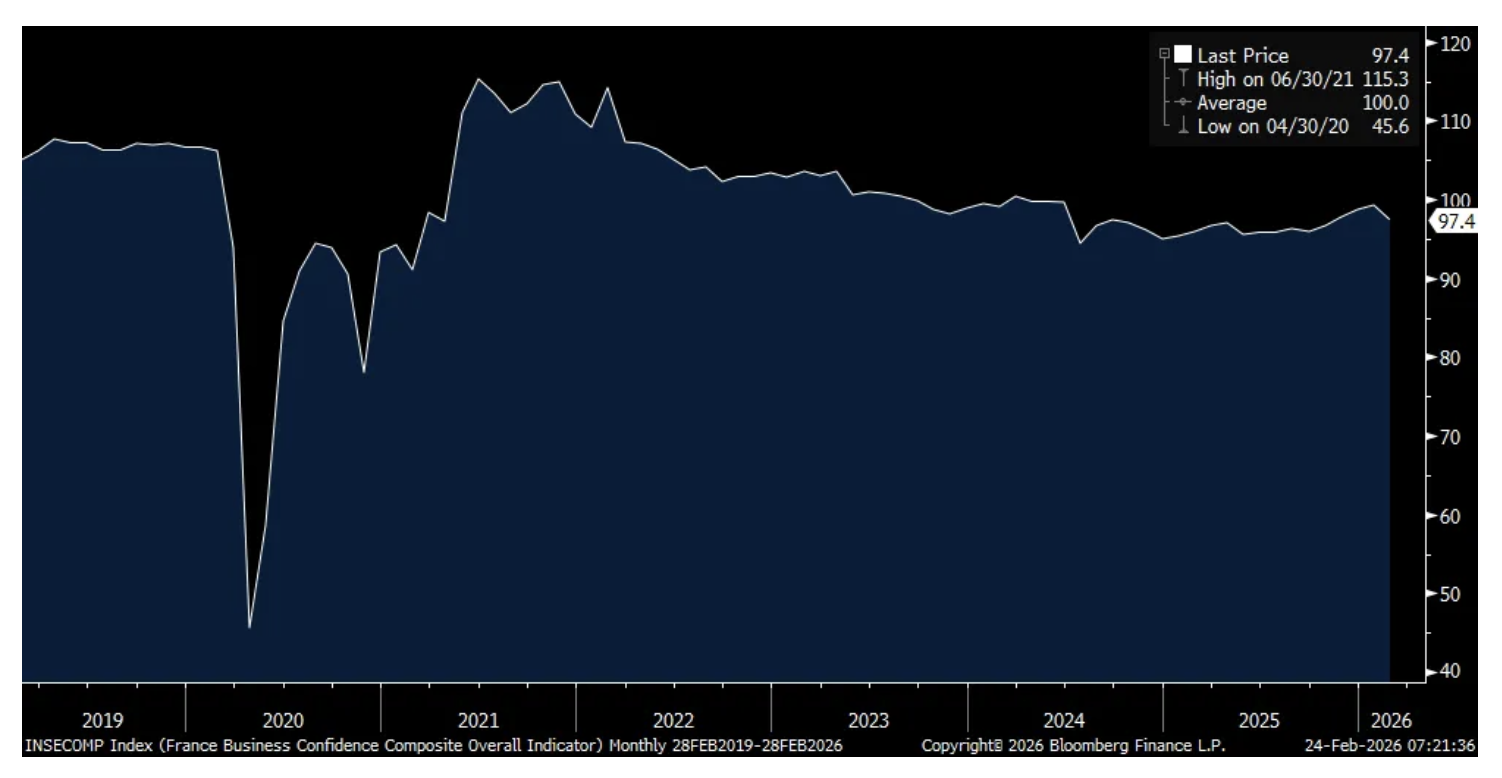

To some overseas data, French business confidence in February slipped by 2 pts to 97 and vs the estimate of no change. That’s the lowest since October but has pretty much flat lined over the past two years. Manufacturing gave back the January 3 pt rise while services, retail and employment each fell too m/o/m. Construction was the only thing that was unchanged. Nothing market moving here but highlights the relatively stagnant French economy.

French Business Confidence

BY Doug Kass · Feb 24, 2026, 9:00 AM EST

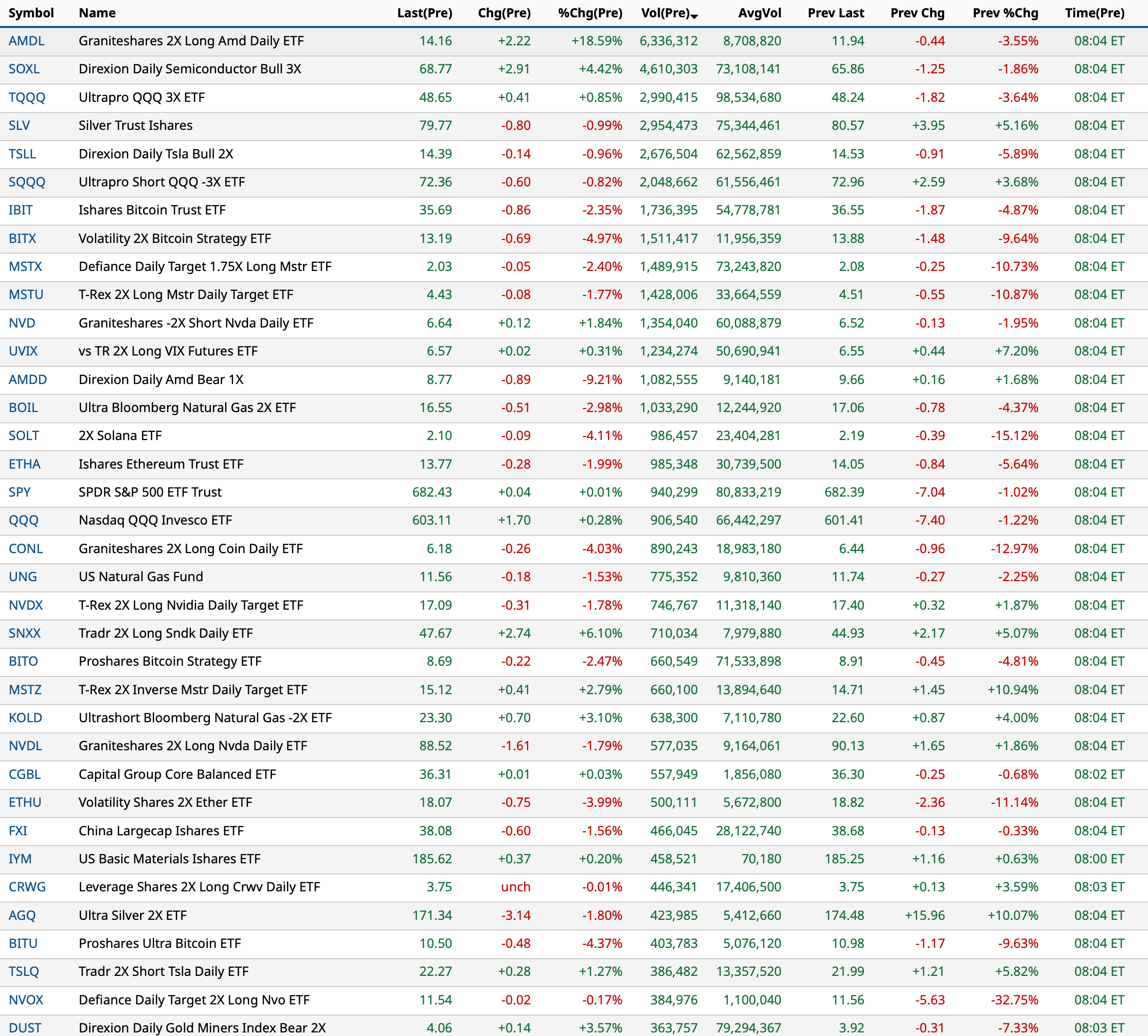

As of 8:04 AM:

BY Doug Kass · Feb 24, 2026, 8:50 AM EST

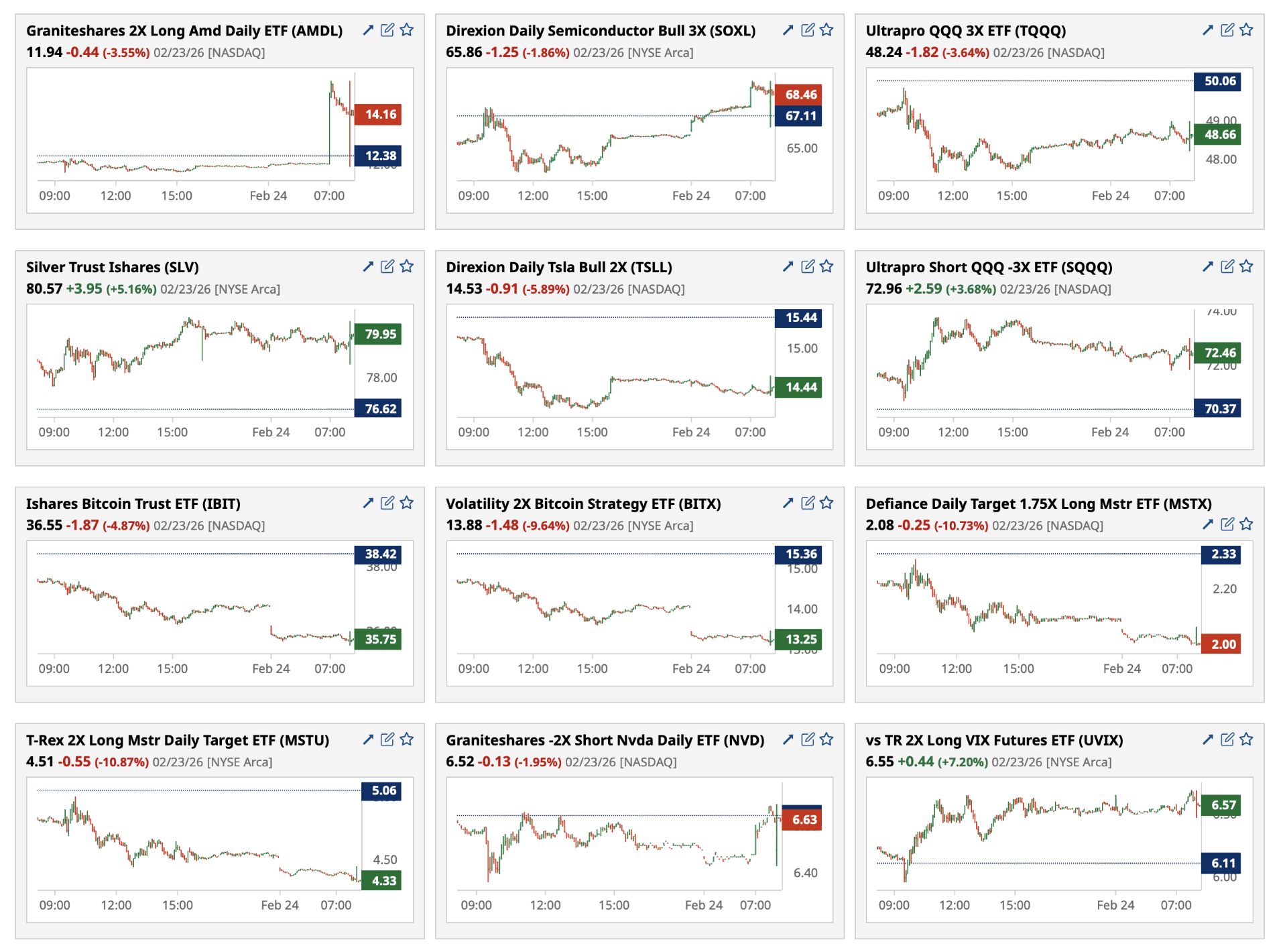

% Movers at 8:26 AM:

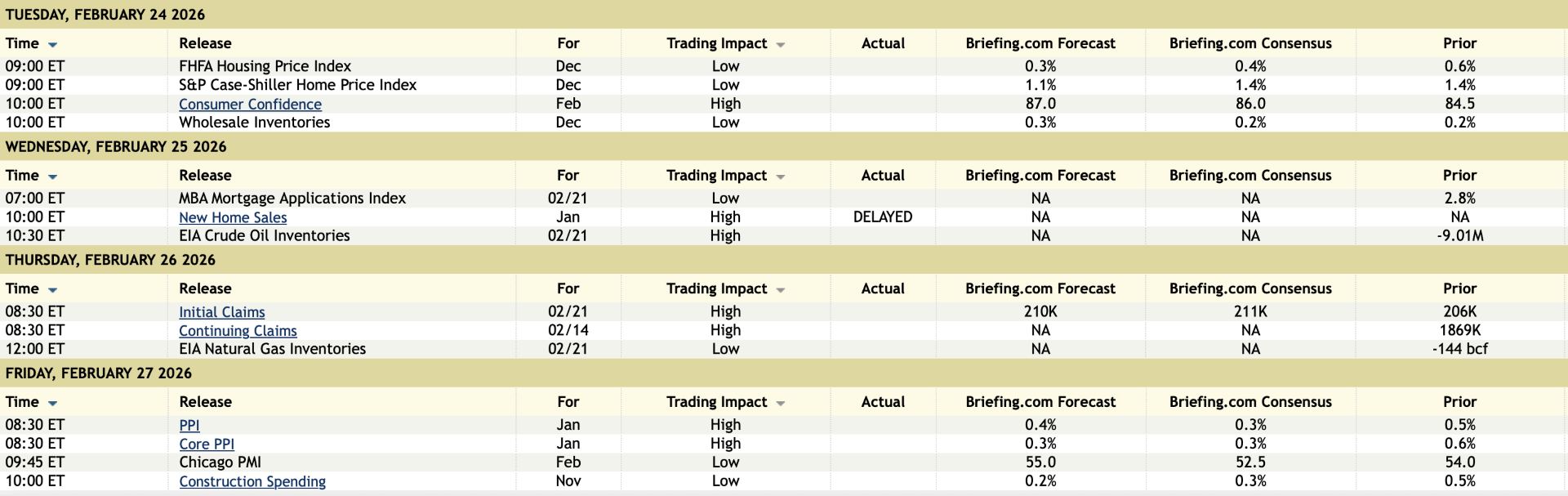

BY Doug Kass · Feb 24, 2026, 8:40 AM EST

11:00AM: Treasury Announces a 4 and 8 Week Bill Auction

11:30AM: Treasury hosts a $90B 6-Week Bill Auction

1:00PM: Treasury hosts a $69B 2-Year Note Auction

8:00AM: Fed Bank of Chicago President Goolsbee (Non-Voter) speaks and participates in moderated question-and-answer session before the 42nd National Association for Business Economics (NABE) Economic Policy Conference, "The Great Realignment: Navigating AI, Demographic, and Geo-Economic Change," (Embargoed text TBD. Livestream here

9:00AM: Fed Bank of Atlanta President Bostic (Non-Voter) participates in conversation on monetary policy, the economic outlook and personal reflections before event hosted by Marketplace, Atlanta, GA (No audience Q&A. No embargoed text. Livestream here).

9:00AM: Fed Bank of Boston President Collins gives opening remarks before the "Technology-Enabled Disruption: Shaping the Future of Finance and Payments" conference at the Federal Reserve Bank of Boston, Boston, MA (Other details TBA).

9:15AM: Fed Board Governor Waller (Voter) speaks on technology before the "Technology-Enabled Disruption: Shaping the Future of Finance and Payments" conference at the Federal Reserve Bank of Boston, Boston, MA (Livestream here. Text available. Q&A from moderator).

9:35AM: Fed Board Governor Cook (Voter) speaks on "Artificial Intelligence and Productivity" before the National Association for Business Economics (NABE) 42nd Annal Economic Policy Conference, "The Great Realignment: Navigating AI, Demographic, and Geo-Economic Change, Washington, DC (Webcast here. Text available of introductory remarks. Q&A from moderator and audience).

3:15PM: Fed Bank of Richmond President Barkin (Non-Voter) and Federal Reserve Bank of Boston President Susan Collins (Non-Voter) participate in panel discussion before the "Technology Enabled Disruption: Shaping the Future of Finance and Payments" conference at the Federal Reserve Bank of Boston, Boston, MA (Livestream available)

BY Doug Kass · Feb 24, 2026, 8:30 AM EST

BY Doug Kass · Feb 24, 2026, 8:18 AM EST

BY Doug Kass · Feb 24, 2026, 8:01 AM EST

BY Doug Kass · Feb 24, 2026, 7:11 AM EST

BY Doug Kass · Feb 24, 2026, 7:01 AM EST

BY Doug Kass · Feb 24, 2026, 6:41 AM EST

The S&P Short Range Oscillator slipped back to only a modest overbought — now standing at 1.03% vs. 3.81%.

BY Doug Kass · Feb 24, 2026, 5:55 AM EST

BY Doug Kass · Feb 24, 2026, 5:45 AM EST