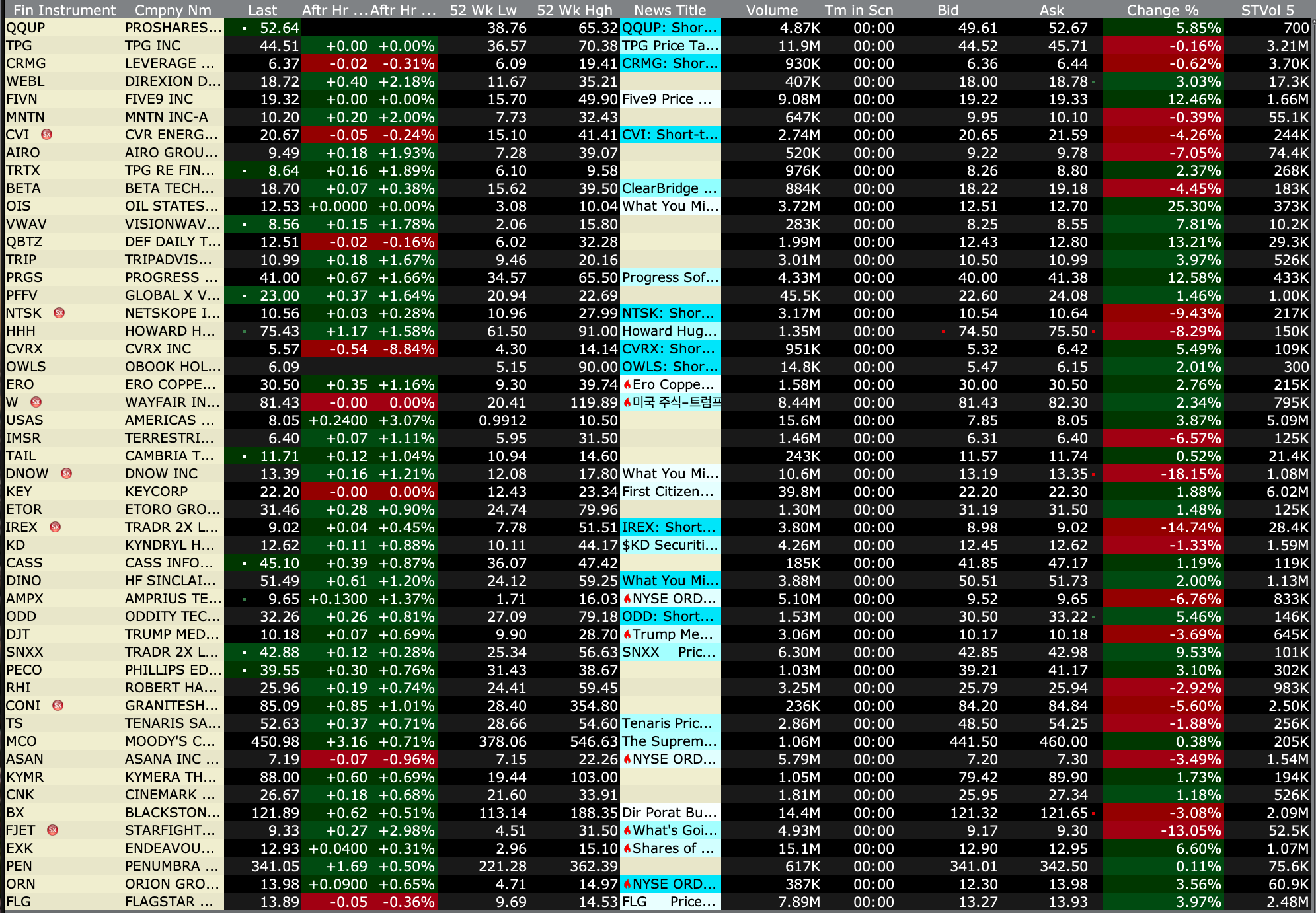

After-Hours Gainers and Decliners

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Feb 20, 2026, 4:50 PM EST

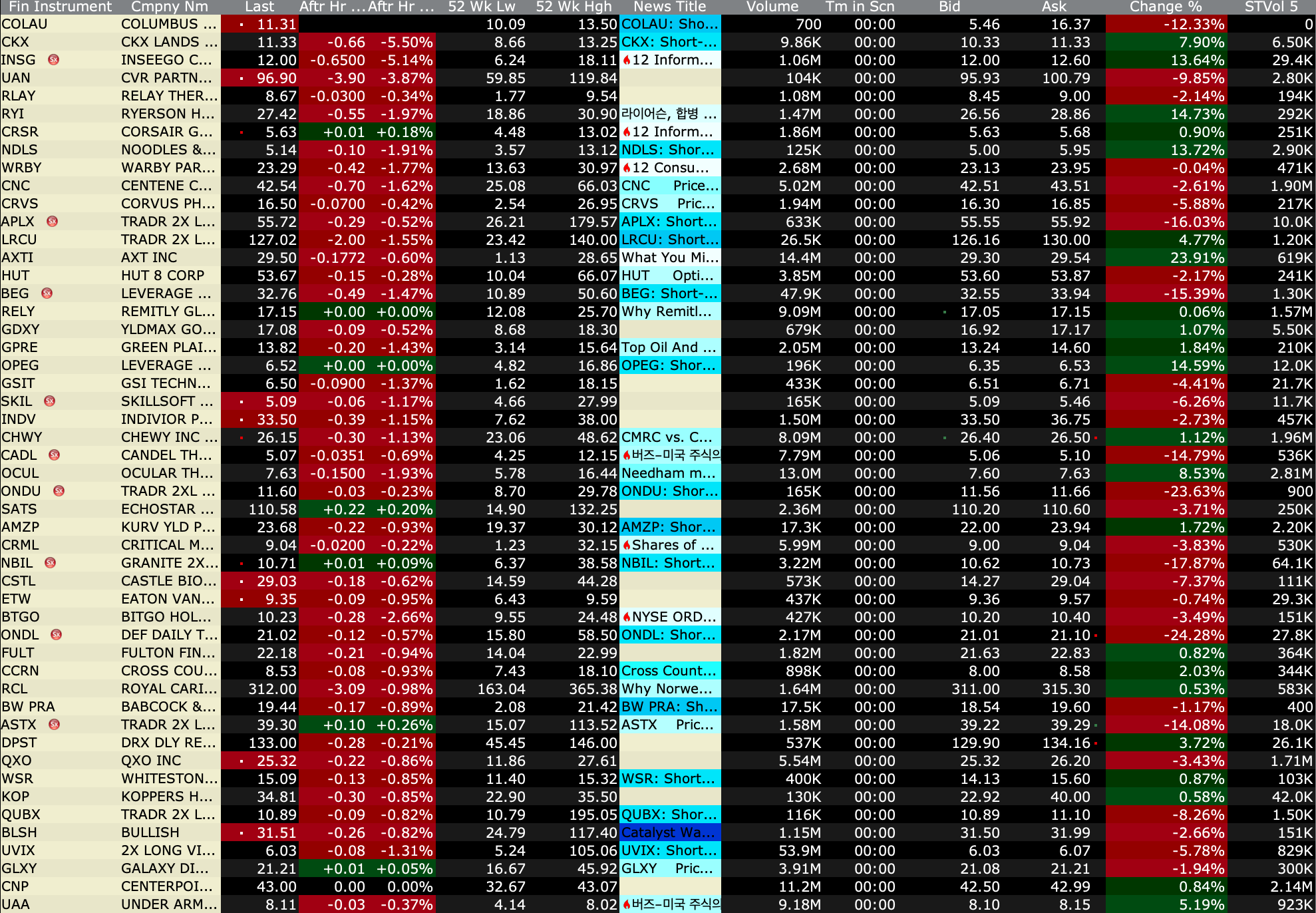

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Feb 20, 2026, 4:50 PM EST

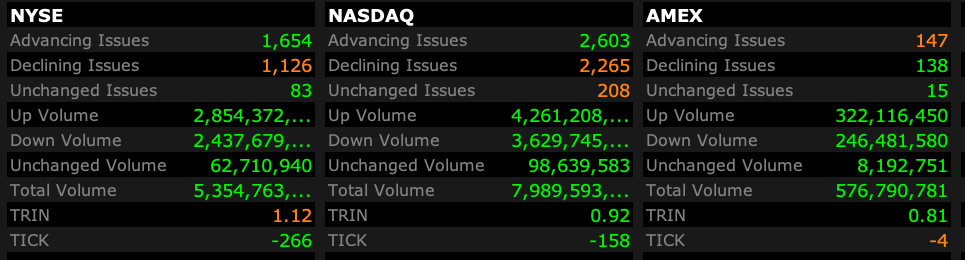

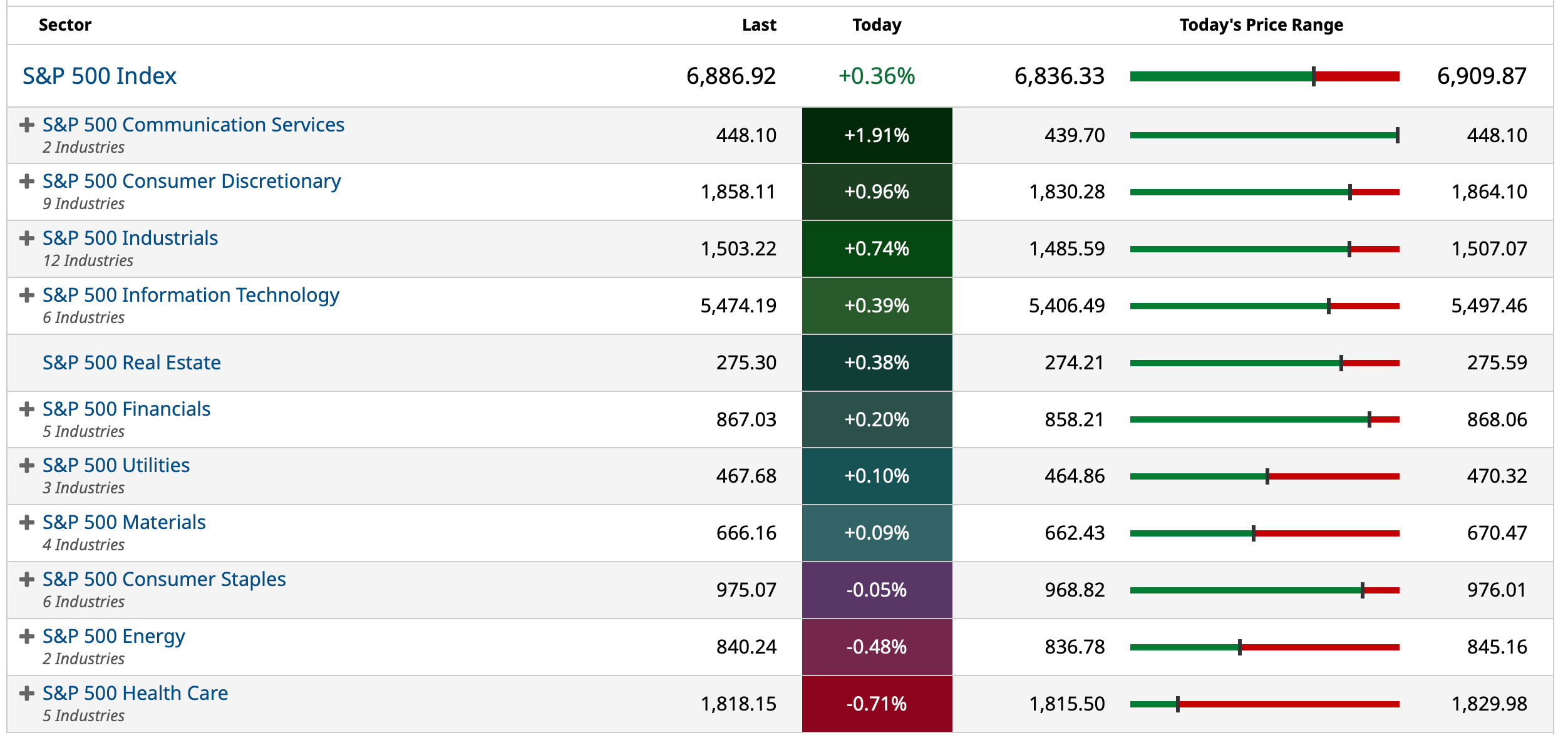

- NYSE volume 2% below its one-month average;

- NASDAQ volume 8% below its one-month average;

- VIX index: down 5.54% to 19.11

BY Doug Kass · Feb 20, 2026, 4:36 PM EST

Some individual cannabis buys this afternoon:

* GLASF $7.43

* (GTBIF) $6.42

* (TCNNF) $6.15

BY Doug Kass · Feb 20, 2026, 3:55 PM EST

I am outta here early.

Thanks for reading my Diary — I hope it was value added.

Enjoy the evening.

Be safe.

BY Doug Kass · Feb 20, 2026, 3:35 PM EST

* That no one in the business media is discussing...

I suspect Blue Owl's loan book is bad but not a disaster.

However, as is often the case with specialty finance companies, the real risk is the loss of funding — because there can be (as is the case now with redemption requests at Blue Owl) a mismatch between the company's maturities and the expectations of investors (and their willingness to fund the company).

Commercial banks take in deposits to fund their investments and loans. While they are subject to a deposit run (like what occurred at SVB), it is rare.

The problem for Blue Owl is that they don't have a retail pipeline (for deposits). So, if they can't sell bonds... they are toast.

BY Doug Kass · Feb 20, 2026, 2:35 PM EST

* George Noble at his best...

BY Doug Kass · Feb 20, 2026, 1:50 PM EST

Wolf Street howls about the Supreme Court decision on tariffs.

BY Doug Kass · Feb 20, 2026, 1:40 PM EST

I have moved to medium-sized (from small sized) (MSOS) at $3.91.

BY Doug Kass · Feb 20, 2026, 1:27 PM EST

BY Doug Kass · Feb 20, 2026, 1:25 PM EST

From Peter Boockvar:

Positives,

1) The Supreme Court said that the presidential use of tariffs cannot be derived from IEEPA. The US economy will get a large tax cut on a variety of goods and services and many small and medium sized businesses get cost pressure relief. The use of tariffs via other sections is fine to use but of course more narrow and hopefully strategic in focus. While the US government loses tax revenues, maybe it can be offset by faster economic growth which generates greater tax receipts but either way we will never tax our way out of our debts and deficits as the problem is on the spending side.

2) Within the Q4 GDP report, stripping out government spending and inventory changes put final sales to private domestic purchases up by 2.4% and averaged 2.5% in 2025. Personal consumption growth of 2.4% was as expected and added 160 bps to GDP growth with spending on healthcare being a big contributor. On the CapEx side and reflecting data center spend, spending on software and R&D added a combined 40 bps and ‘info processing’ added an additional 65 bps. Inventories contributed 20 bps. Another perspective, versus Q4 2024, Q4 2025 GDP growth was up by 2.2% vs 2.3% in Q3, 2.1% in Q2 and 2% in Q1.

3) Distorted by the President’s Day holiday, initial claims fell to 206k from 229k (revised up by 2k) and vs the estimate of 225k. The 4 week average was little changed at 219k vs 220k last week. We’ll further smooth out the holiday with next week’s claims figure. Continuing claims rose 17k w/o/w to 1.869mm and remains below 1.9mm but still elevated.

4) The Philly region saw a print of 16.3, up from 12.6 in January and vs the estimate of 7.5. The internals though were pretty mixed as new orders and backlogs fell as did employment and the workweek. Inventories rose but to just around zero. Delivery times eased and prices paid and received both fell m/o/m. The six month business outlook rose to 42.8 and is back above the six month outlook of 36.3. In contrast to what was seen in the NY survey, capital spending plans fell sharply to 14.4 from 30.3 and that is below the six month average of 22.8.

5) The February NY manufacturing index, the first industrial figure out for February, was +7.1 vs +7.7 in January and about as expected. This compares with the six month average of +4.2. Looking six months ahead, confidence was 34.7 vs 26.8 for the half yr average. Capital spending plans at 18.2 is almost three times the six month average.

6) In the December TIC data, what foreigners did pile into again in 2025 were US stocks but they did so on a hedged basis in a much bigger way relative to the prior years.

7) Non defense capital goods orders ex aircraft (known as core) rose .6% m/o/m in December, twice the estimate and November was revised up to an .8% gain vs the initial print of up .4%. On a y/o/y basis, core orders are now up 7.5%.

8) December housing starts totaled 1.4mm units, about 100k above the estimate and with a rise in both single family and multifamily starts. The single family start figure of 981k in particular is the best since last February but is right in line with the 2 yr average. On the permit side, they fell by 15k m/o/m for single family while rising for multi family (which is very volatile month to month).

9) The MBA said mortgage applications rose 2.8% w/o/w but with the gain all in refi’s, up 7.1% w/o/w.

10) From Walmart: “Sales were strong across each segment of the business and this includes sales of general merchandise, which grew on a global basis and was up low single digits for Walmart US, led by fashion. Fashion was a bright spot for us both in-store and online...The most recent quarter we had like-for-like inflation that was trending a little bit above 1%. That breaks down into food inflation being a little bit less than that, general merchandise inflation being a little bit more than that. That’s generally what our outlook is for the next quarter and the balance of the year. There are some pressures...the maximum fair pricing legislation around drugs. We expect to contribute to about 100 bps headwind for the full year.”

11) From EBAY: On the macro, “In the US, while we faced uncertainty relative to trade policy, consumer demand has remained resilient and we saw broad based strength across categories in Q4. I would say, in contrast, Europe has been more challenged as consumer confidence remains low and retail sales trends are subdued there.”

12) From Klarna: As to their credit exposure and delinquencies, “what we’re seeing is actually stability, not a deterioration.”

13) From Deere: “In earthmoving, double digit y/o/y growth in retail settlements and a growing order bank have prompted us to increase our industry outlooks for both construction and compact construction equipment in North America. In small ag, order activity for mid-size tractors supporting the dairy and livestock production system has remained solid, while order velocity for North American turf equipment and compact uitlity tractors has increased...Global large ag fundamentals, while still challenged, were largely stable over the quarter. This stability has enabled a modest improvement in our net sales forecast for North American large ag this year, as our combined early order program finished better than expected and large tractor order activity has increased. These improvements have helped us to offset softer projections for the South American ag equipment market in 2026.”

14) From Toll Brothers: “Since mid-January, we have seen an increase in overall traffic and sales consistent with the start of the spring selling season. While it is early, we are cautiously encouraged by the increase in activity over the past months. Our strategy of balancing price and pace worked well in the first quarter.” Also, “Our overall incentive remained flat compared to the fourth quarter at 8% of sales price. This is the third consecutive quarter that incentives remained flat on a percentage basis.”

15) From Invitation Homes: in their earnings release they said in Q4 (the slowest seasonal time of the year) , saw renewal rent growth of 4.2% and new lease decline of 4.1% with a blended rent growth pace of 1.8%. For the full year 2025, blended rent growth was 3.1%.

16) From Cheesecake Factory: “While the restaurant industry continued to face a more challenging operating environment, including weather-related impacts, our business remained steady, with revenue for the quarter finishing within our expected range...Industry sales decelerated in the fourth quarter, as reflected by the Black Box casual dining index declining sequentially by 410 bps from the third quarter. The Cheesecake Factory’s comparable sales were negative 2.2% in the fourth quarter, down from .3% in the third quarter, demonstrating relative stability in comparison to the industry sequential declines.” North Italia was soft while Flower Child saw strong comps.

17) From Doordash: “growth in the business continues to be quite strong. And we are seeing that from both existing consumers as well as newer consumers where MAU (monthly average users) growth continues to be strong, order frequency continues to be strong.”

18) From Booking Holdings: “Despite volatility in the broader global markets, the underlying fundamentals of our business are solid. Travel demand remains resilient...Asia continues to be one of the most attractive growth opportunities. Travel demand in the region remains structurally strong, supported by rising incomes and increasing cross border travel.”

19) From Expedia: “In the fourth quarter, we exceeded our expectations, growing bookings and revenue by 11% and expanding our margins by four points. Booked room nights were up 9%, including high single digits in the US and low double digits in EMEA and the rest of the world...Consumer spending remained healthy, with longer booking windows and lengths of stay relative to 2024...Turning to our outlook. Our guidance reflects strong bookings momentum as we enter Q1, while remaining appropriately cautious given ongoing macro uncertainty.”

20) From Vulcan Materials: “Data centers remain the biggest catalyst with over 150 million square feet under construction and another nearly 450 million square feet announced. Over 70% of this activity is occurring within 30 miles of a Vulcan aggregates facility.”

21) Japan’s headline CPI in January rose 1.5% y/o/y vs 2.1% in the prior month with a 2.6% print ex food and energy, both one tenth less than forecasted. The headline figure is downardly influenced by the Japanese government’s attempt to lower fuel costs via tax initiatives and a slower pace food price increases helped too.

22) Also in Japan, the February S&P Global manufacturing PMI rose to 52.8 from 51.5 while services were little changed at 53.8, up .1 pt m/o/m. S&P Global asid, “Manufacturers in particular were boosted by greater demand from overseas clients, with factories seeing the quickest upturn in new export work for 8 years.” And, “firms were more upbeat regarding the outlook, with new product launches, greater demand for technology, and the recent landslide election win by the Takaichi administration all forecast to support growth.”

23) Japan said its exports were up a solid 16.8% y/o/y, above the estimate of 13% and driven by shipments of semi’s and other electronic products thanks to the AI buildout of course. Regionally though exports were mixed, rising by 32% to China (the rush to ship product before the Lunar New Year) , by 30% to the EU while falling by 5% to the US because of a drop in auto shipments.

24) India’s PMI remained solid at 59.3 with manufacturing rising to 57.5 while services were little changed at 58.4.

25) The Eurozone saw a slight lift in its February composite PMI which rose to 51.9 from 51.3 and above the estimate of 51.5. Manufacturing got back above 50 at 50.8 vs 49.5 in January led by Germany while it softened in France. Services were up a touch m/o/m to 51.8 from 51.6. S&P Global said, “It might be premature, but this could be the turning point for the manufacturing sector as the headline PMI increased to growth territory.” Also, “Services growth is continuing at a moderate pace, supporting overall growth in the Eurozone.”

26) The UK composite PMI was 53.9 vs 53.7 with a modest rise in manufacturing to 52 while services at 53.9 fell a hair from 54. S&P Global said “The upturn continues to be led by the service sector but there are signs that manufacturing is regaining momentum to join in the recovery, reporting a surge in export orders of a magnitude not seen since the pandemic.”

27) Also in the UK, January retail sales ex auto fuel rose 2% m/o/m, well better than the estimate of up .3%.

28) The UK CBI industrial orders index for February rose 2 pts m/o/m but is still very negative at -28. The CBI said “The downturn in manufacturing output eased in February after a downbeat period around the turn of the year. However, many firms continue to report consumers holding back amid low confidence and elevated cost pressures.”

29) CPI in the UK in January slowed to a 3% y/o/y rate of change as estimated and down from 3.4% in December led by a drop in fuel prices and food. The core rate though at 3.1% was one tenth above what was anticipated and services inflation remains rather persistent with 4.4% growth.

30) Australia reported its January jobs report that was about as expected and with a one tenth drop in their unemployment rate.

Negatives,

1) The headline and PCE price indexes for December rose by .4% each vs the .3% estimate for both. Versus last year prices are up 2.9% headline and 3% core, also one tenth above expectations for each and vs 2.8% for both in November. Services inflation again is leading the way, up 3% y/o/y ex food and energy but goods prices continue to accelerate after a period of disinflation. Prices here are up 1.7% y/o/y, the quickest since April 2023.

2) December income and spending figures were as expected when including November revisions. Particularly with spending, REAL was up just one tenth m/o/m. Combining the two puts the savings rate at 3.6% which is the lowest since October 2022.

3) Q4 GDP was up just 1.4% q/o/q annualized, half the estimate of 2.8% and 8 tenths of that was due to a 3.6% price deflator vs the forecast of 2.8%. The government shutdown led to a 115 bps drag in federal government spending, partly offset by a 25 bps contribution from state and local spending. Net trade neither added nor took away from growth. Residential construction too was flat.

4) The December trade deficit at $70.3b was about $15b above expectations as imports jumped by 3.6% m/o/m while exports fell by 1.7%. That deficit compares to $53b in November.

5) After a 7.4% drop in December m/o/m, pending home sales fell again in January by .8% m/o/m vs the estimate of a rebound of 2%. This index is now at a record low dating back to when it first started in 2001 and thus below the post-crash low in 2010. We have the pace of existing home sales at the lowest level since the mid 1990’s when the US population was 70 million people smaller. The NAR said, “Improving affordability conditions have yet to induce more buying activity. With mortgage rates nearing 6%, an additional 5.5 million households that could not qualify for a mortgage one year ago would qualify at today’s lower rates. Most newly qualifying households do not act immediately, but based on past experience, about 10% could enter the market—potentially adding roughly 550,000 new homebuyers this year compared with last year.”

6) In the MBA weekly data purchases fell for a 4th straight week notwithstanding the drop in mortgage rates to 6.17%.

7) The February NAHB home builder sentiment survey remained well below 50 at 36, down 1 pt m/o/m and 2 pts below the estimate. It was last above 50 in April 2024. The Present Situation remained unchanged at 41 but the Future Outlook fell 3 pts to 46. Notwithstanding the drop in mortgage rates, Prospective Buyers Traffic fell another 2 pts to just 22. The NAHB said “Persistent affordability challenges, including high housing price-to-income ratios and elevated land and construction costs, helped push builder confidence lower for the second straight month to start the year.” Also, “While the majority of builders continue to deploy buyer incentives, including price cuts, many prospective buyers remain on the sidelines. Although demand for new construction has weakened, remodeling demand has remained solid given a lack of household mobility.”

8) New home sales in December were 15k above expectations at 745k but down from 758k in November and October saw a big downward revision to 656k. Months’ supply was 7.6 vs 7.7 in November and 9 in October.

9) In the monthly December TIC data, foreigners were net sellers of US notes and bonds in December as they continue to shrink their overall holdings relative to the US outstanding debt.

10) Loan growth in the US but narrow. From the Dallas Fed’s Banking Conditions survey, “Loan volume and demand continued to increase in February. The expansion in overall loan volume has been supported entirely by commercial real estate loans; residential real estate, consumer and commercial and industrial loan volumes have been declining since the end of 2025. Credit standards and terms tightened, but loan pricing continued to decline. Overall loan performance deteriorated a touch. Bankers reported increasing general business activity. Their outlooks leaned optimistic. Survey respondents broadly expect sizeable growth in loan demand and business activity six months from now and stable loan performance.”

11) The Architecture Billings Index for January fell to just 43.8 from 47.1 led by a drop in the commercial/industrial component. The chief economist there said “Overall economic conditions remain subdued, with revised 2025 employment data revealing smaller gains than anticipated.”

12) The February US PMI from S&P Global fell to 52.3 from 53 with declines in both manufacturing and services. Remembering that the services component does not include the key sectors like retail and construction, they said this: “A combination of weakened demand, high prices, and adverse weather colluded to dampen business activity in February, resulting in the slowest expansion of output for ten months. Customer demand growth has softened, with orders even falling in factories, curbing jobs growth to a crawl across both manufacturing and services.” This level of their survey equates to 1.5% GDP growth according to them.

13) The final February UoM consumer confidence index was 56.6 vs the initial print of 57.3 and little changed with 56.4 seen in January. Though off the record lows, the level is still depressed. Inflation expectations both one yr and for 5-10 yr time frame, eased one tenth m/o/m to 3.4% and 3.3% respectively. The UoM said, “ About 46% of consumers spontaneously mentioned high prices eroding their personal finances; readings have exceeded 40% for seven months in a row.” And this highlighting the two lane US consumer economy, “A sizable month-to-month increase in sentiment for the largest stockholders was fully offset by a decline among consumers without stock holdings. Similar divergences were seen across income and education, where higher-income or college educated consumers exhibited increases in sentiment while lower-income or less-educated counterparts did not. With their much stronger income prospects and investment porfolios, wealthier and higher-income consumers feel better insulated from any possible risks to the economy.”

14) From Walmart: “In the US, we see the customer choiceful in their spending. Again, this quarter, the majority of our share gains came from households making more than $100,000. For households earning below $50,000, we continue to see the wallets are stretched. And in some cases, people are managing spending paycheck to paycheck. That said, even these households are emphasizing convenience nearly as much as price.”

15) From Wayfair: “My general view is what we’ve been seeing, which is that for the housing market to recover, it’s a little bit of a slow burn. And you’re seeing, like every quarter that goes by, the percentage of mortgages that get refinanced at the current rates keeps ticking up, but it’s a relatively slow process.”

16) From Pool Corp: “In 2025, we estimate that just under 60,000 new pools were built in the US amid single digit decline from last year. This is about half of what we saw at the height of the pandemic and 40% lower than in 2022...While new pool construction remained down, maintenance spending proved resilient.” For 2026, their “outlook assumes new pool construction will stay close to the 60,000 units we saw in 2025. Maintenance revenues should remain resilient...Given that we have not yet observed a positive inflection in discretionary spending trends, we will continue to monitor these dynamics before projecting the timing of any significant recovery. Overall, we expect 2026 to continue to be a challenging market.”

17) From Klarna: This in part is what bothered investors, “faster growth, faster adoption means lower upfront transaction margins and operating profit.” With the growth in its loan portfolios, “The real question is simply, do we want to make more money even if it means slightly less today to make significantly more tomorrow?”

18) From Sonic Automotive: “Fourth quarter new vehicle volume faced headwinds from pull forward consumer demand for electric vehicles ahead of the expiration of the federal tax credit in the third quarter, combined with strong luxury demand in the prior year fourth quarter.” As for pricing this year, the tariff situation is NOT over. To a question asking “are you starting to see indications that the OEMs are planning to push on more more costs? The answer, “Absolutely. They’re lowering margin rebates that we get, they’re pushing - prices are going up. There’s no question that you’re going to see that. They’re not going to sit back and lose billions and billions of dollars. They can’t, it’s just not going to happen. And so it’s going to be really interesting to see the elasticity in new car pricing as we move forward over the next six months.”

19) From La-Z-Boy: “Continued challenging traffic consistent with our industry was partially offset by strong in-store execution, including higher conversion rates, average ticket, and design sales...Within the quarter, same store sales trends were strongest in January, turning positive versus a year ago, until widespread adverse weather slowed traffic in late January and continuing into early February across much of the United States.”

20) From Builders FirstSource: “The housing market remains weak and is characterized by more headwinds than tailwinds as affordability challenges, muted consumer confidence, and depressed commodity prices continue. This was apparent in November and December as our sales fell off more than expected as these cross currents impacted starts and led to a softer Q4.” The commodity prices they are referring to are lumber and oriented strand board (OSB) .

21) From Wingstop: Comps were down by 5.8%, though better than the estimate of down 6.7%, and “which is attributable to the macro pressures our core consumer continued to face...Similar to what we shared on our last call, and as we entered 2026, we expect that the consumer environment to remain choppy with continued pressure on our core consumer.” They expect flat to up low single digit comps this year.

22) From Wendy’s: “Starting with the fourth quarter, while results were in line with our expectations, we know that we have a lot of work to do to improve performance...As we shared on our last earnings call, we expected fourth quarter systemwide sales to be down significantly, and they were. Global systemwide sales declined 8.3%, driven by our US business, where marketing spend was down significantly as a result of front end loaded ad spending in 2025 and sales trends throughout the year...The decline in US same restaurant sales was driven by a decrease in traffic, partially offset by a higher average check.”

23) From General MIlls: “While the company is making meaningful progress in strengthening its remarkability to position the business for long term sustainable growth, this progress has come amid a more challening backdrop. Weak consumer sentiment, heightened uncertainty, and significant volatility have weighed on category growth and impacted consumer purchase patterns, resulting in a slower pace and higher cost of volume recovery than initially expected.”

24) From Booking Holdings: “The booking window in the US remained steady in the fourth quarter, though we continue to see slightly lower ADRs and a slightly shorter length of stay versus the prior year, which may indicate that some consumer segments are continuing to be thoughtful on their discretionary spending.”

25) From Vulcan Materials: “As expected, aggregate units profitability continue to expand and public (sector) demand continue to grow. However, single family residential activity was weaker than we initially anticipated, yielding a full year volume and price at the lower end of our initial expectations.” That public sector demand is coming from highway projects and also other public infrastructure like water, sewer, etc...

26) From Genuine Parts: “despite our overall sales growth in the quarter, we saw weakening of market conditions in Europe and sales below our internal forecasts for US independent owners. There was sequential improvement throughout the year across many areas of the business that are encouraging.”

27) From Advance Auto Parts: Comps were up 1.1% in Q4 but “top line momentum has lagged original expectations. Our pace of same store sales growth has been impacted in part by external factors that have resulted in a softer consumer spending environment...Following a softer start to the quarter, transactions improved during the last 8 weeks, resulting in positive comparable sales growth over that timeframe...Ticket was positive for the quarter and driven by a combination of better unit productivity and higher average selling prices...SKU inflation came in just under 3%. This was about 100 bps lighter than expected due to successful tariff related negotiations, which were still underway at the start of the quarter.”

28) Australia’s services PMI fell 4.1 pts m/o/m to 52.2 while the manufacturing component slipped to 51.5 from 52.3. And this too, “On the price front, the degress to which average cost pressures faced by Australian private sector firms increased intensfied and was substantial in February. Costs facing goods producers rose at the strongest rate in 10 months, as surveyed firms often noted greater supplier prices and paying more for raw materials, including metals. Service providers also saw a faster rise in operating expenses, as higher wage and electricity costs were mentioned by companies on both sectors.”

29) Payrolls shrunk again in January in the UK for the 5th straight month. However, down 11k was better than the estimate of -20k and December was revised up sharply to a loss of 6k vs the initial print of -43k. Jobless claims also rose in January. Also, in the 3 months ended December, the UK unemployment rate rose one tenth m/o/m to 5.2% which is the highest since January 2021.

30) The February German ZEW investor expectations survey fell to 58.3 from 59.6 and that was 7 pts below the estimate. The Current Situation improved to -65.9 from -72.7 as expected but still well under zero. They said, “The ZEW Indicator remains stable. The German economy has entered a phase of recovery, albeit a fragile one. There are still considerable structural challenges, especially for industry and private investment.”

BY Doug Kass · Feb 20, 2026, 1:00 PM EST

Dougie Kass

Ludacris Day?

BY Doug Kass · Feb 20, 2026, 12:35 PM EST

I'm adding further to (MSOS) at $3.98 and MSOX at $2.96

BY Doug Kass · Feb 20, 2026, 12:25 PM EST

I have converted my short index common into short calls.

BY Doug Kass · Feb 20, 2026, 12:20 PM EST

BY Doug Kass · Feb 20, 2026, 12:15 PM EST

BY Doug Kass · Feb 20, 2026, 11:53 AM EST

- NYSE volume 8% above its one-month average;

- Nasdaq volume 8% below its one-month average;

- VIX index: down 1.14% to 20

BY Doug Kass · Feb 20, 2026, 11:35 AM EST

BY Doug Kass · Feb 20, 2026, 11:22 AM EST

I am adding to ETF shorts in (GRNY) at $25.09, (JOET) at $42.75 as well as a number of individual short positions with S&P cash +43 handles.

BY Doug Kass · Feb 20, 2026, 11:11 AM EST

With S&P cash +45 handles I have moved to small sized (from very small sized) short the Indexes.

BY Doug Kass · Feb 20, 2026, 11:01 AM EST

From Peter Boockvar:

The headline and PCE price indexes for December rose by .4% each vs the .3% estimate for both. Versus last year prices are up 2.9% headline and 3% core, also one tenth above expectations for each and vs 2.8% for both in November. Food prices rose .4% m/o/m after no change in November and energy prices were up .2% after a 1.7% jump in the month before.

Services inflation again is leading the way, up 3% y/o/y ex food and energy but goods prices continue to accelerate after a period of disinflation. Prices here are up 1.7% y/o/y, the quickest since April 2023. Still muted but the change in trajectory is what should be watched. I still think rental growth slowing will moderate service prices in coming few quarters but goods prices will continue to rise.

The initial reaction is a 2 bps rise in the 2 yr inflation breakeven to 2.75% but the 5 yr is unchanged at 2.47%. The 2 yr yield at 3.47% is up 2 bps post data while the 10s and 30s are up 1 bp.

I’ll repeat again my belief that Jay Powell is done cutting rates and Kevin Warsh will only give us 1-2 the rest of the year, under current data seen and of course a lot could change with inflation and labor.

December income and spending figures were as expected when including November revisions. Particularly with spending, REAL was up just one tenth m/o/m. Combining the two puts the savings rate at 3.6% which is the lowest since October 2022. Not much cushion for lower to middle income consumers while the upper end saves less with income relative to spending when their stock portfolios rise.

Q4 GDP was up just 1.4% q/o/q annualized, half the estimate of 2.8% and 8 tenths of that was due to a 3.6% price deflator vs the forecast of 2.8%. Personal consumption growth of 2.4% was as expected and added 160 bps to GDP growth. On the CapEx side and reflecting data center spend, spending on software and R&D added a combined 40 bps and ‘info processing’ added an additional 65 bps. Inventories contributed 20 bps.

On the flip side, the government shutdown led to a 115 bps drag in federal government spending, partly offset by a 25 bps contribution from state and local spending. Net trade neither added nor took away from growth. Residential construction too was flat.

Stripping out government spending and inventory changes put final sales to private domestic purchases up by 2.4% and averaged 2.5% in 2025 which is pretty good.

Another perspective, versus Q4 2024, Q4 2025 GDP growth was up by 2.2% vs 2.3% in Q3, 2.1% in Q2 and 2% in Q1.

Bottom line, between the higher than expected price deflator which leads to lower REAL growth and the big drop in federal government spending because of the shutdown, that explains the miss relative to expectations. Elsewhere, no real surprises. Again, about all of US economic growth is coming from data center construction, upper income spending and anyone benefiting from the federal government’s $1.8 trillion deficit and $7 trillion of total annual spending.

BY Doug Kass · Feb 20, 2026, 11:00 AM EST

Cost basis on last (SPY) and (QQQ) common shorts:

* SPY $688.31

* QQQ $608.67

BY Doug Kass · Feb 20, 2026, 10:57 AM EST

S&P cash is now +37 handles and I am back shorting (SPY) common and calls.

BY Doug Kass · Feb 20, 2026, 10:51 AM EST

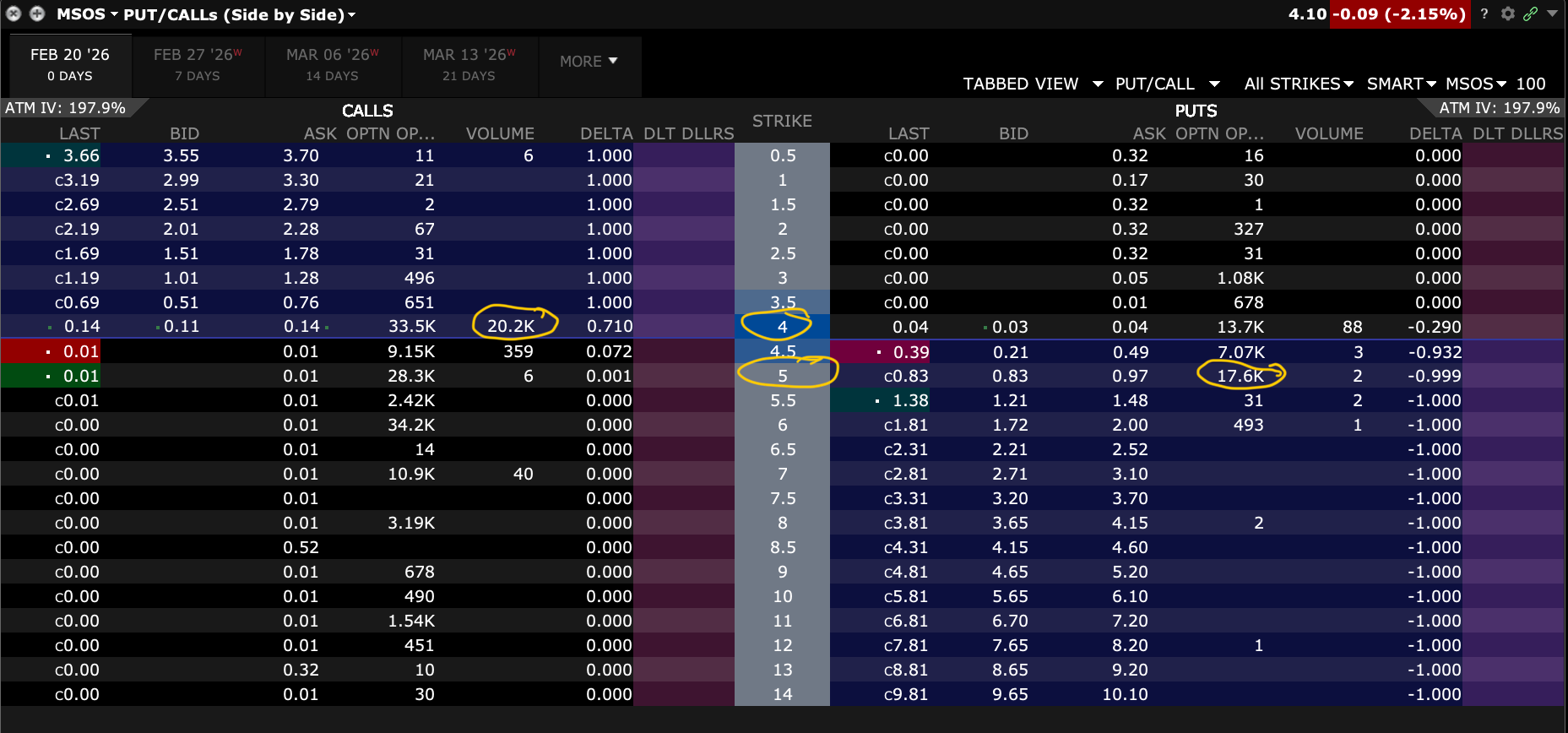

(MSOS) option volume on $4 calls and $5 puts right out of the gate

BY Doug Kass · Feb 20, 2026, 10:50 AM EST

With S&P cash selling off and only +4 handles I have covered all my Index shorts (common and calls) for a quick and nice profit.

BY Doug Kass · Feb 20, 2026, 10:26 AM EST

* (OWL) down by another six percent this morning...

BY Doug Kass · Feb 20, 2026, 10:15 AM EST

I shorted the indexes on the tariff decision gap (+40 handles) in stock prices.

BY Doug Kass · Feb 20, 2026, 10:09 AM EST

One of the speculative investment shorts that I have not disclosed previously in my Diary is Nova Minerals.

Today Spruce Point Capital delivered a negative analysis of NVA:

BY Doug Kass · Feb 20, 2026, 10:00 AM EST

With S&P cash +3 handles I am shorting Index calls (again).

BY Doug Kass · Feb 20, 2026, 9:53 AM EST

From Peter Boockvar:

From a certainty perspective, it would be great for businesses and households to finally hear from the Supreme Court today on tariffs. As the administration has rolled back some tariffs on goods they realize we will never make in the US, I think they secretly want the Court to rule against them as it would be a gigantic tax cut for everyone and help the cost of living challenges for many, especially ahead of the November elections. They can then better focus their tariff strategy on strategic areas of the economy rather than the scattershot approach that was taken.

We’ll of course have to see where some of these private credit issues go (with now full gates up on a retail focused Blue Owl private credit fund) but I will repeat my belief that the new relationship between retail investor and private equity/credit firms are not a good marriage. They just don’t have the same time horizon and liquidity needs. Of course some parts of retail do, those who firmly commit to a 7-10 yr hold, but many don’t and I worry about them getting stuck just as they might need the money.

The Blue Owl Technology BDC (OTF symbol), a different entity from the one that gated yesterday, where software makes up about 70% of their loans defended its portfolio in their earnings call yesterday as its stock fell 2.5%:

“What I want to underscore at the outset is that performance at OTF has been strong, and we expect that to continue.”

Addressing the investor focus on software exposure, “We’ve always liked software and it has been a significant contributor to our performance. We built dedicated technology investing capabilities to match the opportunity and our portfolio remains excellent. Our software borrowers are delivering low to mid teens revenue and EBITDA growth on average, among the strongest across our direct lending strategy.”

In light of the GenAI concerns they did a dive into their borrower companies and “Our analysis confirms the quality of our assets and gives us confidence that our portfolio remains aligned with where the market is going...So, combined with our defensively constructed portfolio of predominantly first lien senior secured loans to private equity sponsored borrowers with LTVs in the low 30s and significant equity cushions, we have a substantial buffer even in periods when equity valuations are pressured, which helps support downside protection and durable earnings.”

“Our underwriting thesis remains focused on sticky mission critical applications where AI serves as an additive layer rather than a replacement.”

Before I get to more earnings calls, I want to swing back to the GenAI trade and highlight again one of the worries of investors, including myself, that isn’t talked about as much as other concerns over the massive spend. That being the growing, intense compeition forming with the Chinese.

In case you didn’t see this piece in the FT titled “Is an AI price war about to begin?”, I’ll give some of the highlights from the article.

“The price of using artificial intelligence is falling. In China, entry-level access to AI models has been marketed for about $3 a month by the country’s hottest AI group Zhipu. Widely seen as one of China’s closest local equivalents to OpenAI, it develops large language models to compete with US systems.”

“In a market where paid plans from US peers are closer to $20 a month depending on tier, and enterprise contracts run into the millions annually, this move by Zhipu amounts to a price war.”

“Markets are pricing a world in which US AI groups maintain outsized control over global AI revenue and dominate the highest margin segments, while global users continue to accept higher price points. But how sustainable is that assumption?”

The article does highlight the advantages that the US models have that includes the “larger existing revenue bases than Chinese peers” among other factors and that “Data security concerns and regulatory scrutiny would probably limit the use of Chinese AI models in the US and parts of Europe, particularly for government workloads.”

“Yet the technological gap between US and Chinese AI models is narrowing. On standardized industry benchmarks, leading Chinese LLMs now operate close to their US counterparts across reasoning, coding and general knowledge tasks. In areas such as mathematical problem solving, the gap has narrowed to low single digit percentage differences, according to Stanford’s 2025 AI index.”

Lastly with this on pricing, “If technology is no longer the binding constraint, competition then shifts to price. OpenAI’s pricing for developers of its flagship GPT-5.2 model is about $1.75 per million input tokens, units used to measure text processed and generated by AI models, and $14 per million output tokens. On Zhipu’s domestic developer platform, its latest flagship language model GLM-5 is priced at about $0.58 per million input tokens and $2.60 per million output tokens. The difference is most striking in output pricing, where it undercuts most US models.”

And to sum up, “Much of the optimism behind US AI stocks rests on the assumption that users will keep paying for incremental performance gains. But as differences narrow, the price of AI may soon be set by the cheapest model that is good enough.”

To more earnings calls.

From Walmart where they used the word ‘choiceful’ again in describing the US consumer:

“Sales were strong across each segment of the business and this includes sales of general merchandise, which grew on a global basis and was up low single digits for Walmart US, led by fashion. Fashion was a bright spot for us both in-store and online.”

“In the US, we see the customer choiceful in their spending. Again, this quarter, the majority of our share gains came from households making more than $100,000. For households earning below $50,000, we continue to see the wallets are stretched. And in some cases, people are managing spending paycheck to paycheck. That said, even these households are emphasizing convenience nearly as much as price.”

“The most recent quarter we had like-for-like inflation that was trending a little bit above 1%. That breaks down into food inflation being a little bit less than that, general merchandise inflation being a little bit more than that. That’s generally what our outlook is for the next quarter and the balance of the year. There are some pressures...the maximum fair pricing legislation around drugs. We expect to contribute to about 100 bps headwind for the full year.”

We know Walmart has a much greater ability to deal with tariffs and other cost pressures relative to its smaller retail peers and a big reason why they continue to take market share.

From EBAY and whose stock was up 3% each of the past two days:

On the categories that contributed strength to sales, “The collectibles category had another standout quarter and was the largest contributor to GMV growth in Q4.”

Also of note, “a notable acceleration in other subcategories like bullion and collectible coins amid unique demand for precious metals in recent months.”

This was an interesting area of growth, “Motors, parts and accessories, or P&A, also finished the year strong...We are seeing a repair over replace trend among consumers maintaining aging vehicles.”

Similar to what Walmart said, “Fashion was also one of the leading contributors to growth in Q4, led by our luxury and preloved apparel focus categories.”

On the macro, “In the US, while we faced uncertainty relative to trade policy, consumer demand has remained resilient and we saw broad based strength across categories in Q4. I would say, in contrast, Europe has been more challenged as consumer confidence remains low and retail sales trends are subdued there.”

Wayfair, the furniture seller, was down 13%, after a jump in the prior two days, on modest guidance. They said this:

“My general view is what we’ve been seeing, which is that for the housing market to recover, it’s a little bit of a slow burn. And you’re seeing, like every quarter that goes by, the percentage of mortgages that get refinanced at the current rates keeps ticking up, but it’s a relatively slow process.”

“So our whole plan is not really premised on how the market turns, because I think that’s a very hard thing to predict.”

From Pool Corp that dropped by 15% yesterday:

“In 2025, we estimate that just under 60,000 new pools were built in the US amid single digit decline from last year. This is about half of what we saw at the height of the pandemic and 40% lower than in 2022...While new pool construction remained down, maintenance spending proved resilient.”

For 2026, their “outlook assumes new pool construction will stay close to the 60,000 units we saw in 2025. Maintenance revenues should remain resilient...Given that we have not yet observed a positive inflection in discretionary spending trends, we will continue to monitor these dynamics before projecting the timing of any significant recovery. Overall, we expect 2026 to continue to be a challenging market.”

From Klarna that crashed by 27%:

This in part is what bothered investors, “faster growth, faster adoption means lower upfront transaction margins and operating profit.”

With the growth in its loan portfolios, “The real question is simply, do we want to make more money even if it means slightly less today to make significantly more tomorrow?”

As to their credit exposure and delinquencies, “what we’re seeing is actually stability, not a deterioration.”

From Deere whose stock jumped by 12% to a record high:

“In earthmoving, double digit y/o/y growth in retail settlements and a growing order bank have prompted us to increase our industry outlooks for both construction and compact construction equipment in North America. In small ag, order activity for mid-size tractors supporting the dairy and livestock production system has remained solid, while order velocity for North American turf equipment and compact uitlity tractors has increased.”

“Global large ag fundamentals, while still challenged, were largely stable over the quarter. This stability has enabled a modest improvement in our net sales forecast for North American large ag this year, as our combined early order program finished better than expected and large tractor order activity has increased. These improvements have helped us to offset softer projections for the South American ag equipment market in 2026.”

To the economic data outside the US of relevance.

Japan’s headline CPI in January roe 1.5% y/o/y vs 2.1% in the prior month with a 2.6% print ex food and energy, both one tenth less than forecasted. The headline figure is downardly influenced by the Japanese government’s attempt to lower fuel costs via tax initiatives and a slower pace food price increases helped too.

Notwithstanding the slightly less than expected figures, the JGB 10 yr inflation breakeven is higher by 3 bps, though the regular 10 yr yield is lower while the 2 yr is unchanged. I still think the BoJ is raising rates again either in March or April to stem the yen weakness and calm the long end of the JGB yield curve.

On to the PMIs where signs are growing for a pick up in manufacturing while price pressures remain elevated.

In Japan, the February S&P Global manufacturing PMI rose to 52.8 from 51.5 while services were little changed at 53.8, up .1 pt m/o/m. S&P Global asid, “Manufacturers in particular were boosted by greater demand from overseas clients, with factories seeing the quickest upturn in new export work for 8 years.” And, “firms were more upbeat regarding the outlook, with new product launches, greater demand for technology, and the recent landslide election win by the Takaichi administration all forecast to support growth.”

To the inflation situation in this survey for Japan, “Underlying data indicated that a quicker rise in expenses at services companies offset a softer increase in prices at manufacturers. At the same time, the rate of output charge inflation hit a 21 month high in the latest survey period. Services companies recorded a steeper rise in selling prices than factories.”

Australia’s services PMI fell 4.1 pts m/o/m to 52.2 while the manufacturing component slipped to 51.5 from 52.3. And this too, “On the price front, the degress to which average cost pressures faced by Australian private sector firms increased intensfied and was substantial in February. Costs facing goods producers rose at the strongest rate in 10 months, as surveyed firms often noted greater supplier prices and paying more for raw materials, including metals. Service providers also saw a faster rise in operating expenses, as higher wage and electricity costs were mentioned by companies on both sectors.”

India’s PMI remained solid at 59.3 with manufacturing rising to 57.5 while services were little changed at 58.4. India’s economy remains an exciting growth story and we are long stocks there.

The Eurozone saw a slight lift in its February composite PMI which rose to 51.9 from 51.3 and above the estimate of 51.5. Manufacturing got back above 50 at 50.8 vs 49.5 in January led by Germany while it softened in France. Services were up a touch m/o/m to 51.8 from 51.6.

Just as we’re seeing signs that US manufacturing is bottoming out (likely inventory builds for now), the same came be said for Europe. S&P Global said, “It might be premature, but this could be the turning point for the manufacturing sector as the headline PMI increased to growth territory.” Also, “Services growth is continuing at a moderate pace, supporting overall growth in the Eurozone.”

On inflation, “Prices pressures in the services sector...has relaxed a bit in February. Costs are still increasing at a high rate but not as fast as the month before while companies increased their prices to their customers at a significantly lower rate than before.” For manufacturers, “input costs rose at the fastest pace since December 2022” and also rose for selling prices.

The UK composite PMI was 53.9 vs 53.7 with a modest rise in manufacturing to 52 while services at 53.9 fell a hair from 54. S&P Global said “The upturn continues to be led by the service sector but there are signs that manufacturing is regaining momentum to join in the recovery, reporting a surge in export orders of a magnitude not seen since the pandemic.”

This was said on prices in the UK, “Meanwhile, average cost burdens increased sharply at private sector businesses in February. Although the rate of input price inflation eased to a three-month low, it remained above the long-run survey average. This was largely due to another steep increase in business expenses across the service economy, which survey respondents mostly attributed to elevated wage pressures. There were also reports of rising raw material costs and technology expenses. Manufacturers additionally commented on higher commodity prices, particularly copper and other metals.”

“In contrast to the weaker trend for overall input cost pressures, prices charged inflation picked up for the third month running in February. The latest rise in average output charges was the sharpest since April 2025, which mainly reflected a steep and accelerated increase in the service economy. Anecdotal evidence cited the impact of higher employment costs and prices charged by suppliers, although some firms noted that competitive pressures had continued to erode margins.”

In the UK in January retail sales ex auto fuel rose 2% m/o/m, well better than the estimate of up .3%.

BY Doug Kass · Feb 20, 2026, 9:45 AM EST

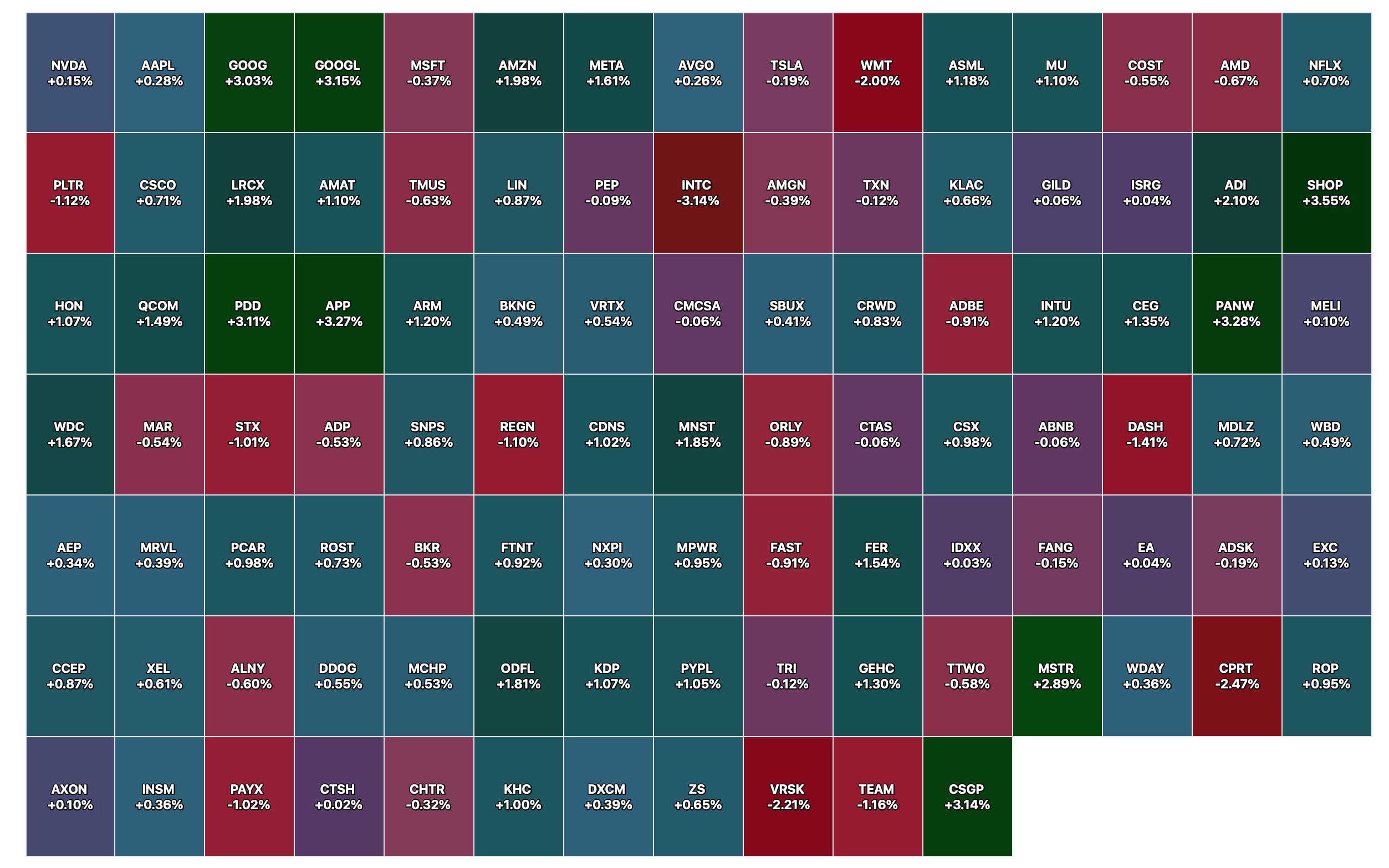

* (AMZN) (long) +$1.00

* (WMT) (short) -$2.60

* (COST) (short) -$8.00

BY Doug Kass · Feb 20, 2026, 9:43 AM EST

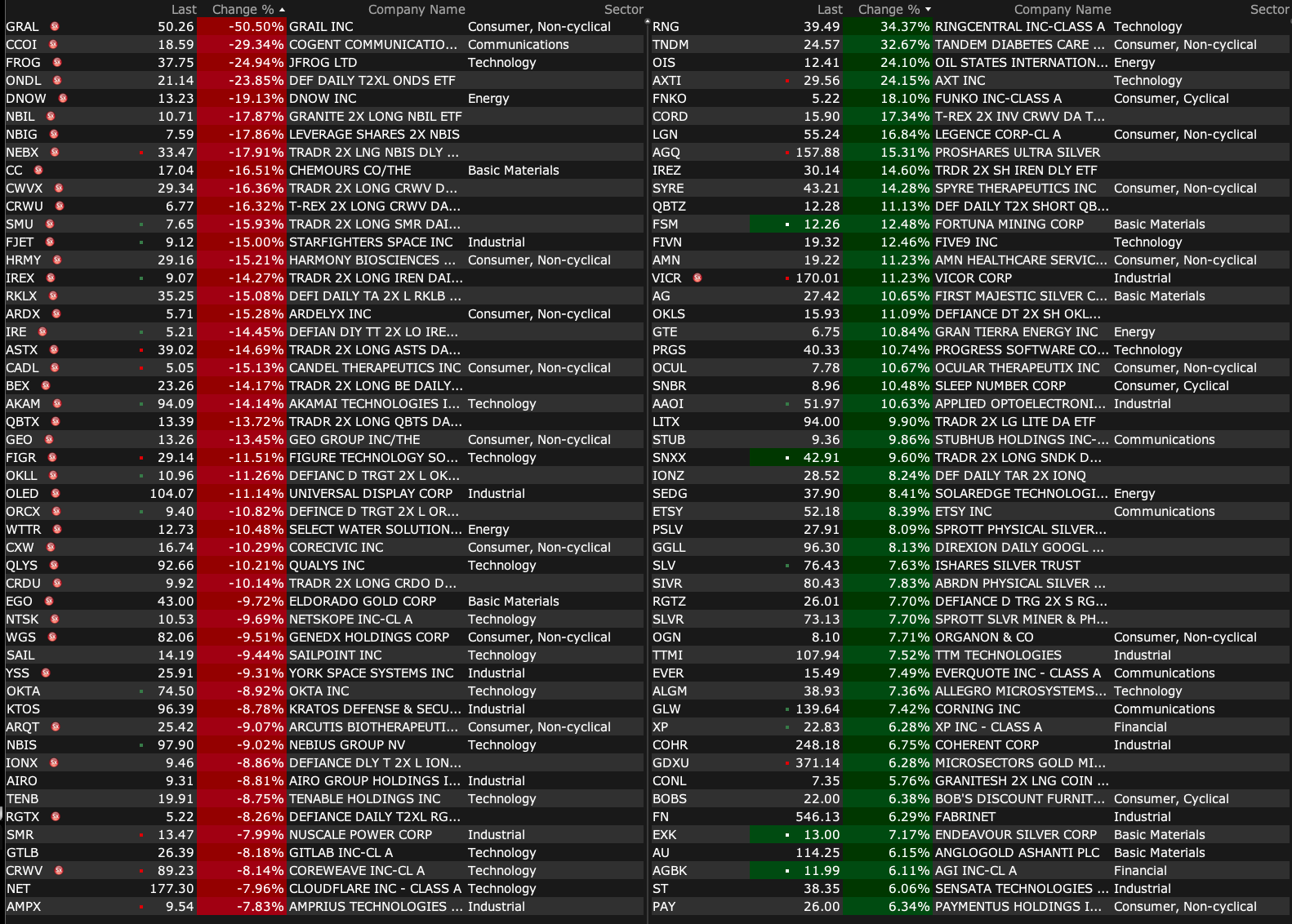

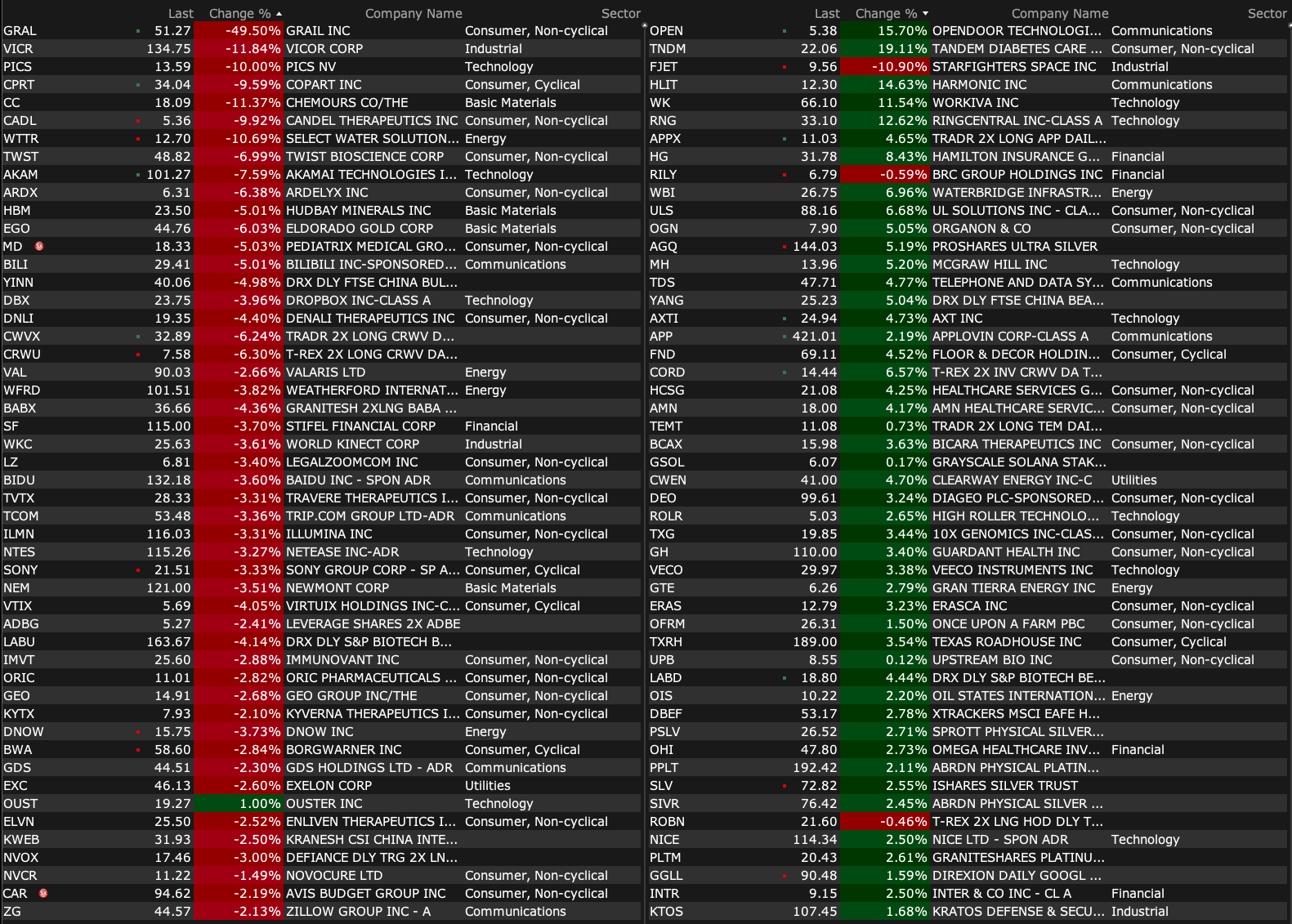

-OPEN +19% (earnings, guidance)

-HLIT +14% (earnings, guidance)

-RNG +14% (earnings, guidance)

-INDI +13% (earnings, guidance)

-TNDM +13% (earnings, guidance)

-WK +12% (earnings, guidance)

-CELH +6.8% (CAGNY conference commentary, color)

-OGN +5.7% (Audit Committee completed independent review and determined no action is required related to timing of purchases of biosimilars from a supplier in prior years)

-TDS +5.4% (earnings, guidance)

-APP +4.8% (planning own company social platform after failing TikTok bid)

-FIX +4.8% (earnings; raises dividend)

-FND +4.6% (earnings, guidance)

-AXTI +3.7% (earnings)

-GH +3.4% (earnings, guidance)

-AD +3.3% (earnings, guidance)

-TXRH +3.3% (earnings, guidance)

-LYV +2.9% (earnings, guidance)

-DCH +2.5% (Jefferies initiates with Buy)

-GRAL -48% (earnings, color)

-INSG -15% (earnings, guidance)

-VICR -13% (earnings)

-CPRT -10% (earnings)

-WTTR -10% (prices 13.7M shares at $12.75/share)

-CC -9.3% (earnings, guidance)

-CADL -8.2% (announces $100M Royalty Funding Agreement with RTW to Support the Potential Launch of Aglatimagene Besadenovec (CAN-2409) in Localized Prostate Cancer; prices 18.3M shares at $5.45/share)

-TWST -6.7% (downside momentum)

-ARDX -6.2% (earnings, guidance)

-EGO -5.7% (earnings, guidance)

-HBM -5.2% (earnings, guidance)

-LZ -4.8% (earnings, guidance)

-WKC -4.1% (earnings, guidance)

-NEM -3.3% (earnings, guidance)

-PPL -2.5% (earnings, guidance)

-RIG -2.5% (earnings)

-CRWV -2.0% (reportedly Blue Owl Capital failed to secure financing for a $4B data center project in Pennsylvania)

-LYB -2.0% (cuts dividend)

BY Doug Kass · Feb 20, 2026, 9:17 AM EST

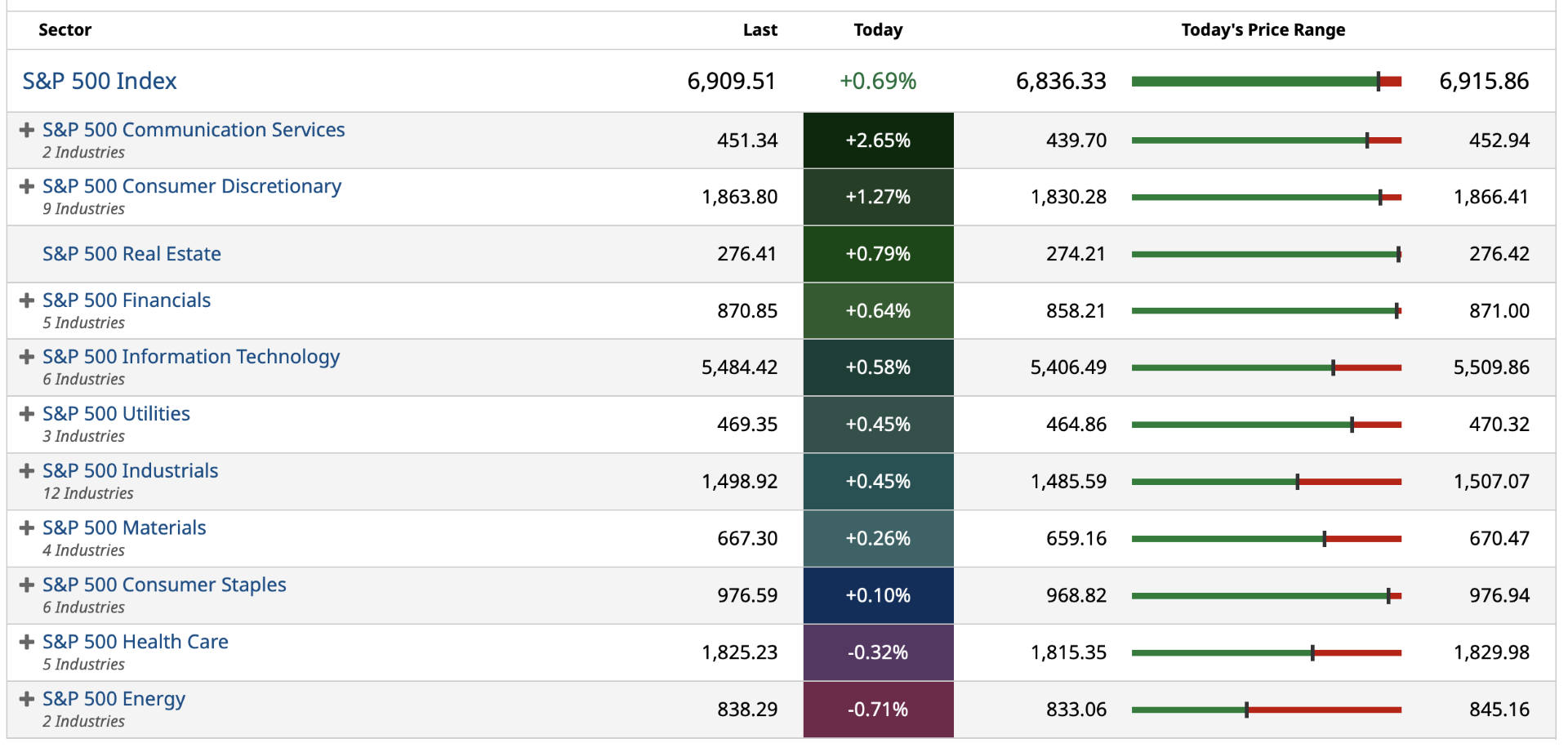

Charts from 8:19 a.m. ET

BY Doug Kass · Feb 20, 2026, 9:09 AM EST

BY Doug Kass · Feb 20, 2026, 8:59 AM EST

9:45 a.m.: Fed Bank of Atlanta President Bostic (Non-Voter) participates in moderated conversation on the economic outlook before event hosted by the Birmingham Business Journal, Birmingham, AL (Audience Q&A expected. No media Q&A. No embar-goed text. Livestream at youtube.com/watch?v=izmOhgLd_b)

1:15 p.m.: Fed Bank of Dallas President Logan (Voter) speaks at the Columbia University and Bank Policy Institute's Conference on Bank Regulation (New York; Audience questions expected);

3:30 p.m.:Fed Bank of St. Louis President Musalem (Non-Voter) appears on Fox Business

BY Doug Kass · Feb 20, 2026, 8:50 AM EST

I added to my (CVNA) short at $334.48 in the wee early morning hours.

Please don't follow me into this risky short!

BY Doug Kass · Feb 20, 2026, 8:43 AM EST

I have covered the balance of my SPY short taken this morning -for a nice and quick profit:

* (SPY) $682.77 (in at $686.72 at 4:10 a.m.)

From earlier:

I took a quick +$2 profit on 3/4 of my (SPY) (short) trade from two hours ago:

* Covered SPY at $684.61

From earlier:

I am back shorting the indices:

* (SPY) $686.72

Position: Short SPY common (VS)

By Doug Kass Feb 20, 2026 5:55 AM EST

Position: Short SPY (VVS)

By Doug KassFeb 20, 2026 6:25 AM EST

BY Doug Kass · Feb 20, 2026, 8:40 AM EST

BY Doug Kass · Feb 20, 2026, 8:28 AM EST

BY Doug Kass · Feb 20, 2026, 8:23 AM EST

From JPMorgan:

US: Futs are higher led by Tech. Pre-market, Mag 7 are all higher; GOOGL added +1.6%. Bond yields are modestly higher; 2y +1.5bp; USD is flat. Commodities are mixed: base metals and oil are lower, while previous metals are rallying. Overnight, a WSJ article wrote that Trump considers an initial limited strike to force negotiation. Today, key macro focus will be PCE, Flash PMIs and SCOTUS opinion day (markets are waiting for possible decision on IEEPA tariffs).

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

SPX has been nearly flat so far this week after last week’s 1.4% selloff and consecutive sessions of de-grossing (Positioning Intel tells us that HF de-grossing spike to 3z in the first week of February and 2z last week). So far this week, we have seen some stabilization in the sector rotation and de-grossing activities. Looking ahead, we will have a number of key macro releases today (PCE, GDP, PMIs) and next week (State of the Union Address, PPI), with three SCOTUS opinion days (markets are expecting potential ruling on IEEPA, see scenario analysis below). NVDA earnings on February 25th remains the most important tech catalyst.

MACRO DATA PREVIEW

· PCE (MIKE HANSON; here) – The team raised their tracking estimate for core PCE to 0.39%, bring the YoY estimate higher from 2.9% previously to 3.1%. He added: “Such an outcome in the data, if realized, would likely reinforce the concern among most FOMC participants (as revealed in the January minutes) that returning to the 2% inflation target could take longer and be more uneven than generally expected. Note that this forecast is conditioned on our December tracking estimate of 0.37% m/m (3.0%oya).”

· GDP (FEROLI; here) – We [Feroli and team] expect that real GDP rose 3.0% q/q saar (2.6% oya) in 4Q25. GDP was driven by consumption growth of 2.5%, continued gains in equipment and IPP investment, inventory building, and another lift from net exports, though smaller than in recent quarters. The government sector should be weak because of the federal government shutdown. There will also be continued weakness in both residential and nonresidential investment. Nominal GDP will have risen around 6.3%, outpacing the 4.0% increase in employee compensation, which should be supportive of decent growth in profits. Those will be released with the second GDP estimate.

· FLASH PMI-SRVCS (FEROLI; here) – We [Feroli and team] expect the February flash services PMI to inch up to 53.0 from 52.7 in January. After an elevated string of prints for much of the second half of 2025 the survey signaled slower growth around the turn of the year. The new business component partially recovered from a dip in December, moving from 51.1 to 53.2 in the January report. The February print could benefit from normalizing weather following winter storm Fern, although temperatures continue to remain unusually cold. While services prices softened overall in January, output prices remain elevated. The employment index jumped to 53.3 from 51.5 in December, mirroring the uptick in payroll growth in private service-providing firms, which marked 136k, the highest since the end of 2024. The backlogs of work in the PMI services report are close to the cycle-high level, which could point to a further increase in employment in the sector.

· FLASH PMI-MFG (FEROLI; here) – We [Feroli and team] look for the February flash manufacturing PMI reading to remain broadly stable from the January print, inching up to 53.0 from 52.4. While both output and new orders rose in the recent report, the gap between the two metrics continues to be wide after reaching its highest in December. This concern is exacerbated by stocks of finished goods, which remain elevated after peaking in November, and comments from the ISM release noted a temporary demand boost from post-holiday replenishment and tariff-driven front loading. Another concerning aspect of the PMI survey has been firming inflation. Output prices rose to 58.5 from 56.3 in December, and input prices ticked up to 62.2 from 61.3. Overall, price indexes remain elevated, albeit lower than the peak seen in the middle of last year. This inflation uptick could take time before being reflected in CPI, as we noted earlier.

BY Doug Kass · Feb 20, 2026, 7:10 AM EST

BY Doug Kass · Feb 20, 2026, 6:55 AM EST

* We re-shorted Carvana near the close on Thursday at $332.40.

BY Doug Kass · Feb 20, 2026, 6:45 AM EST

Remember that Carvana (CVNA) shares fell by -$70/share following the disappointing call.

Between the analysts and the business media, investors seem to have no one on their side.

BY Doug Kass · Feb 20, 2026, 6:35 AM EST

I took a quick +$2 profit on 3/4 of my (SPY) (short) trade from two hours ago:

* Covered SPY at $684.61

From earlier:

I am back shorting the indices:

* (SPY) $686.72

Position: Short SPY common (VS)

By Doug Kass Feb 20, 2026 5:55 AM EST

BY Doug Kass · Feb 20, 2026, 6:25 AM EST

All four company managements were lobbed soft balls in CNBC pre and post IPO interviews:

BY Doug Kass · Feb 20, 2026, 6:15 AM EST

* Blue Owl sells the good debt (in part to an affiliate), leaving the dog poop (that no one will touch) behind in the portfolio

* Riddle me this, Bryn (The Blue Owl Bull)...

Valuation opacity, a compression in exit multiples and unrealistic net asset value marks (mark to model delays volatility but doesn't remove it) in private equity come into focus in 2026. The greatest problems are companies tied to commercial real estate and Saas companies. There are a number of high-profile bankruptcies in notable private equity portfolios.

A market for stranded LP interests trading at deep discounts becomes widely followed. Further, the IPO market continues to not be a viable exit for most holdings. Gated redemptions become common place. Apollo (APO) , TPG (TPG) , KKR (KKR) and Ares (ARES) each fall by 30%.

Kass Diary, 10 Surprises for 2026

From yesterday:

BY Doug Kass · Feb 20, 2026, 6:05 AM EST

I am back shorting the indices:

* (SPY) $686.72

BY Doug Kass · Feb 20, 2026, 5:55 AM EST

The S&P Short Range Oscillator remains overbought at 2.53% vs. 3.18%.

BY Doug Kass · Feb 20, 2026, 5:45 AM EST