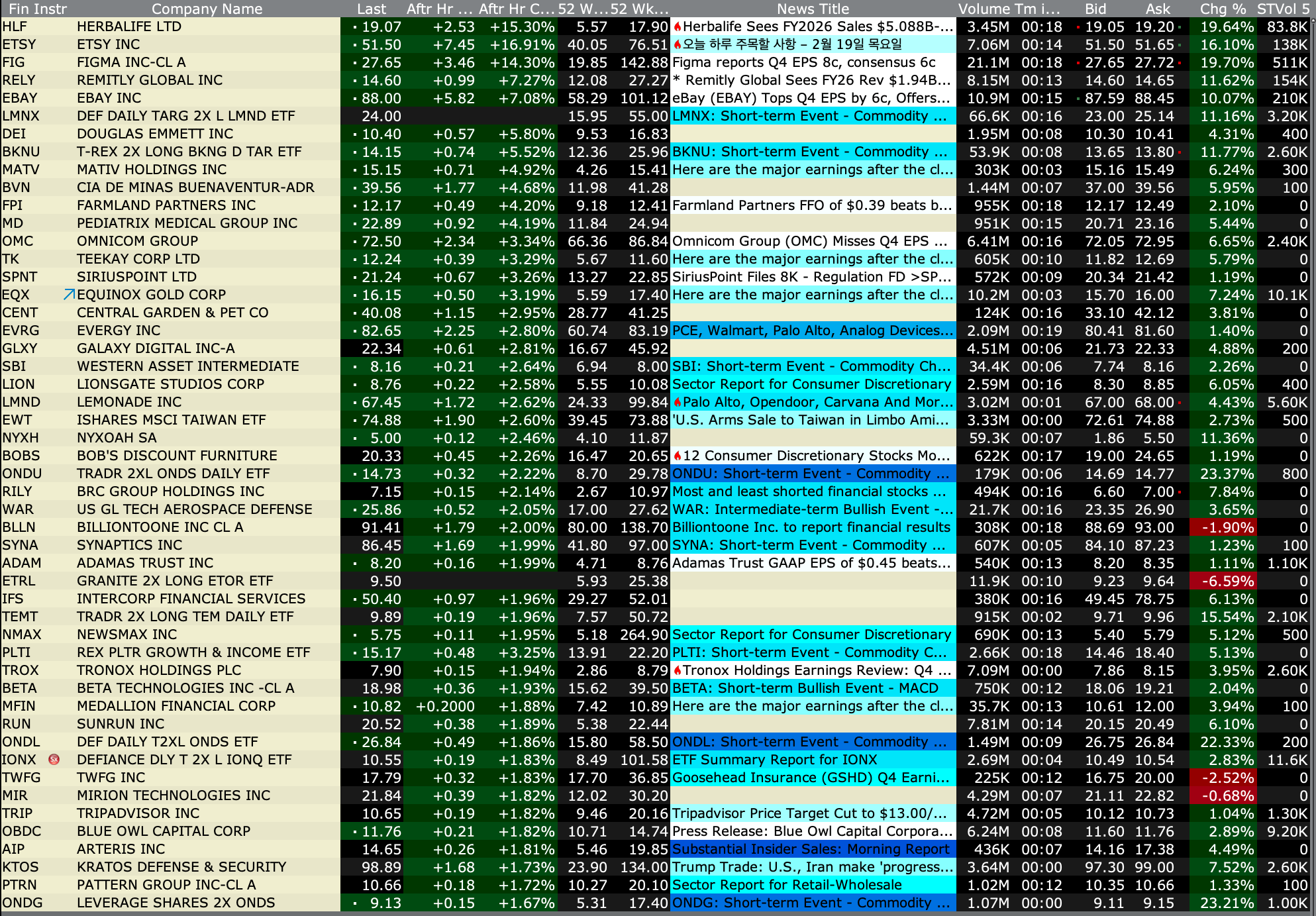

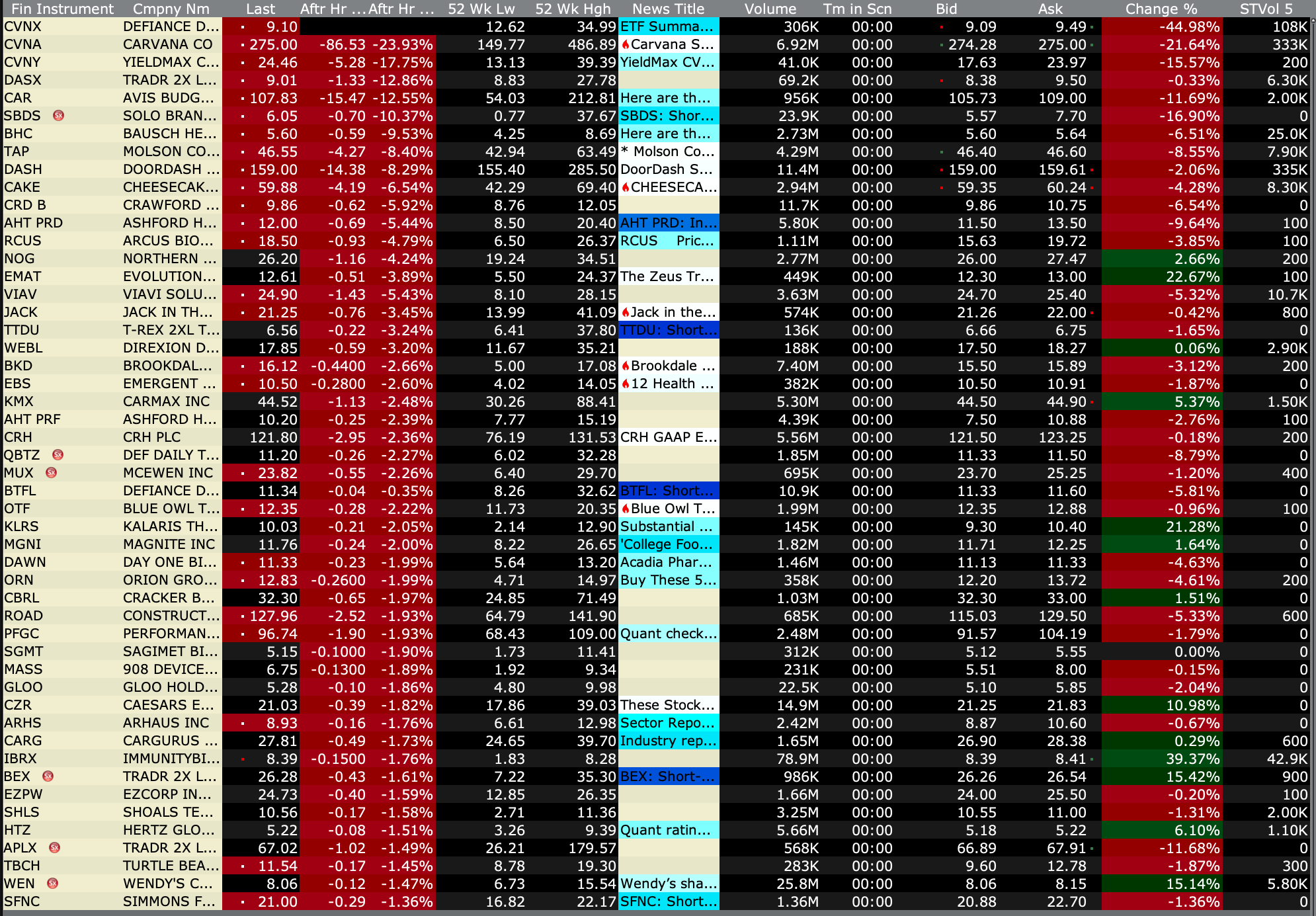

After-Hours Advancers and Decliners

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Feb 18, 2026, 4:45 PM EST

BY Doug Kass · Feb 18, 2026, 4:45 PM EST

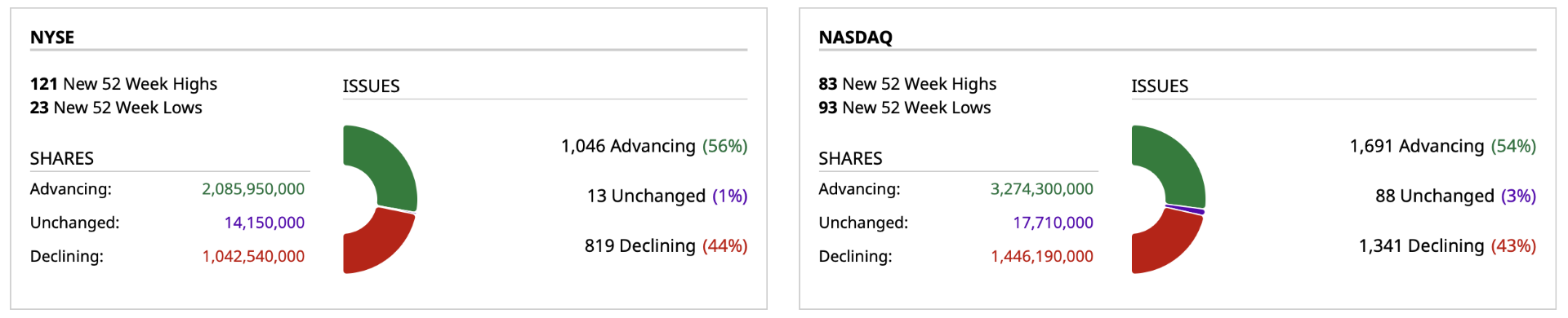

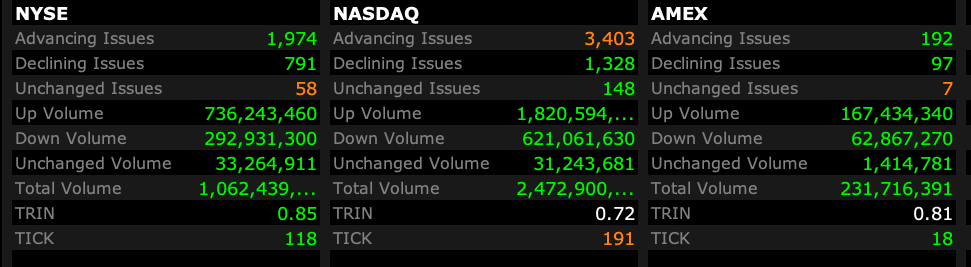

- NYSE volume 15% below its one-month average;

- NASDAQ volume 14% below its one-month average;

- VIX index: down 3.30% to 19.62

BY Doug Kass · Feb 18, 2026, 4:27 PM EST

Carvana (CVNA) just announced quarterly earnings.

Here is the report:

Carvana Announces Record Fourth Quarter and Full Year 2025 Results | Carvana

I am covering my short -$62 at $288.

I plan to re-short on strength.

BY Doug Kass · Feb 18, 2026, 4:14 PM EST

From Peter Boockvar:

If you’re interested in giving yourself a headache in terms of trying to figure out what the Fed does next (even with incoming Fed Chair in a few months), I recommend reading the minutes from the FOMC meeting three weeks ago. I’ll save you some time and an Advil and include quotes here when ‘several,’ ‘many’, ‘most’ members lean in a particular direction. The net result is a committee that is more inclined to wait it out for now with rates. The 2 yr yield is at the high of the day in response, up by 2.5 bps to 3.46% while 10 yr yield is up 2 bps to 4.08%. Both we know though are near one year lows.

On one hand, “In considering the outlook for monetary policy, several participants commented that further downward adjustments to the target range for the federal funds rate would likely be appropriate if inflation were to decline in line with their expectations.”

On the other hand, “Several participants indicated that they would have supported a two-sided description of the Committee’s future interest rate decisions, reflecting the possibility that upward adjustments to the target range for the federal funds rate could be appropriate if inflation remains at above-target levels.”

“Several participants remarked that the ongoing moderation in inflation for housing services was likely to continue to exert downward pressure on overall inflation. Several participants also expected higher productivity growth associated with technological or regulatory developments to put downward pressure on inflation.”

“Most participants, however, cautioned that progress toward the Committee’s 2 percent objective might be slower and more uneven than generally expected and judged that the risk of inflation running persistently above the Committee’s objective was meaningful.”

“Several participants also raised the possibility that sustained demand pressures could keep inflation elevated relative to the Committee’s 2 percent objective.”

“Most participants noted that recent data readings such as those for the unemployment rate, layoffs, and job openings suggested that labor market conditions may be stabilizing after a period of gradual cooling. Almost all participants observed that while the level of layoffs remained low, hiring remained low as well.”

“Participants generally anticipated that the pace of economic growth would remain solid in 2026, though uncertainty about the outlook for growth remained high. Most participants expected growth to be supported by continued favorable financial conditions, fiscal policy, or changes in regulatory policy. Moreover, in light of the strong pace of AI-related investment as well as the higher productivity growth of recent years, several participants judged that ongoing gains in productivity would be supportive of economic growth.”

On the markets, “In their discussion of financial stability, several participants commented on high asset valuations and historically low credit spreads.”

“Several participants highlighted vulnerabilities associated with the private credit sector and its provision of credit to riskier borrowers, including risks related to interconnections with other types of nonbank financial institutions, such as insurance companies, and banks’ exposure to this sector. Several participants commented on risks associated with hedge funds, including their growing footprint in Treasury and equity markets, rising leverage, and continued expansion of relative value trades that could make the Treasury market more vulnerable to shocks.”

BY Doug Kass · Feb 18, 2026, 3:30 PM EST

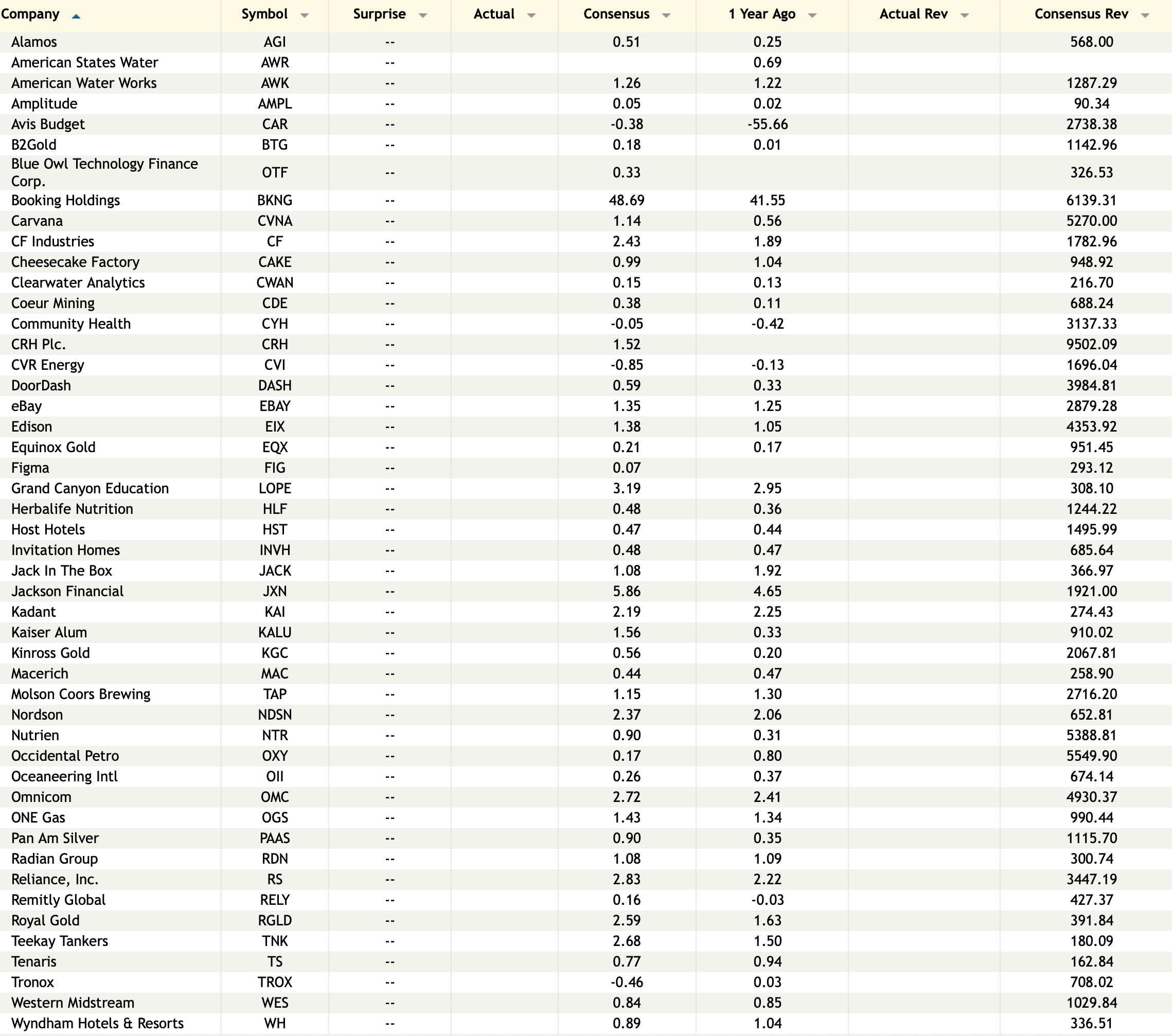

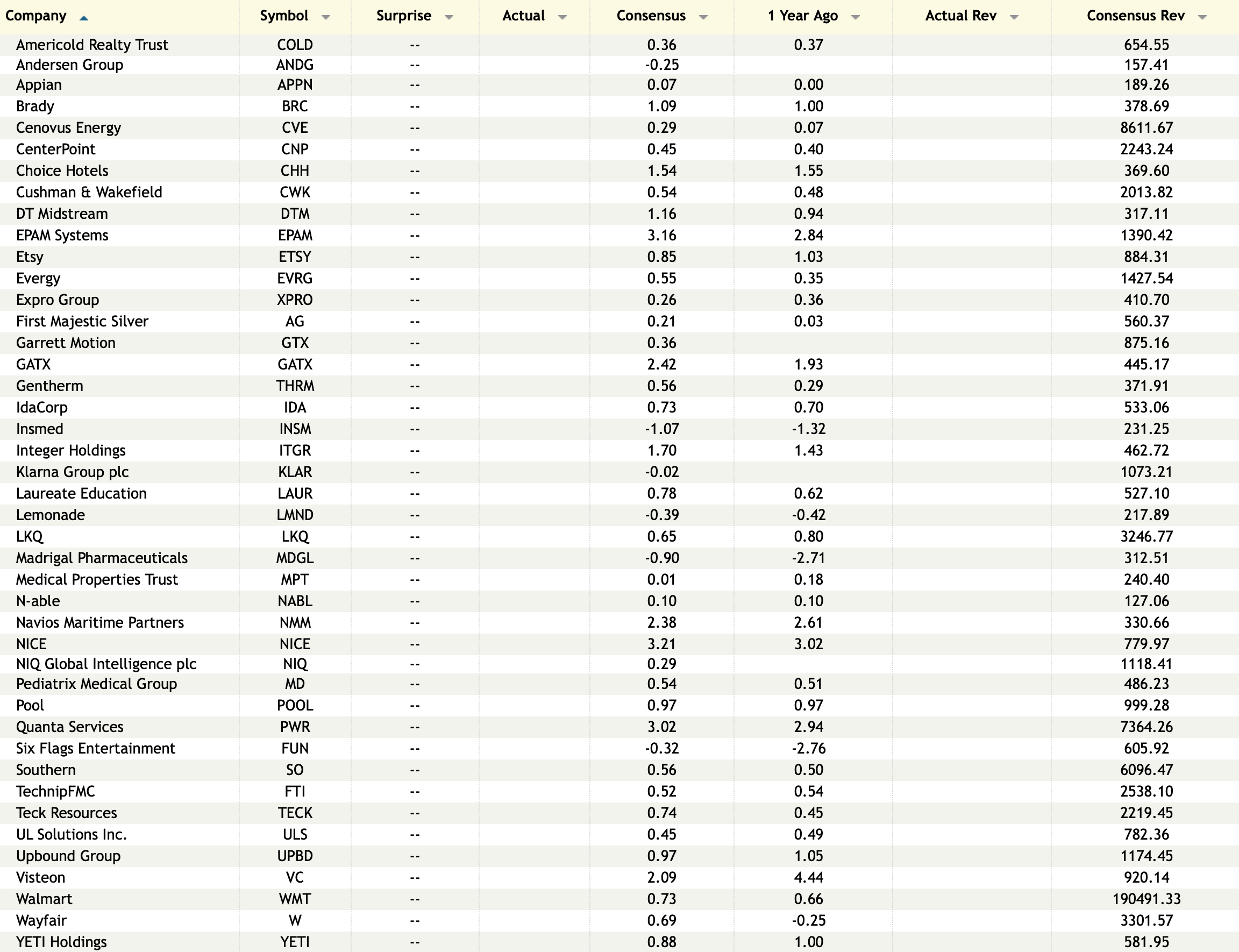

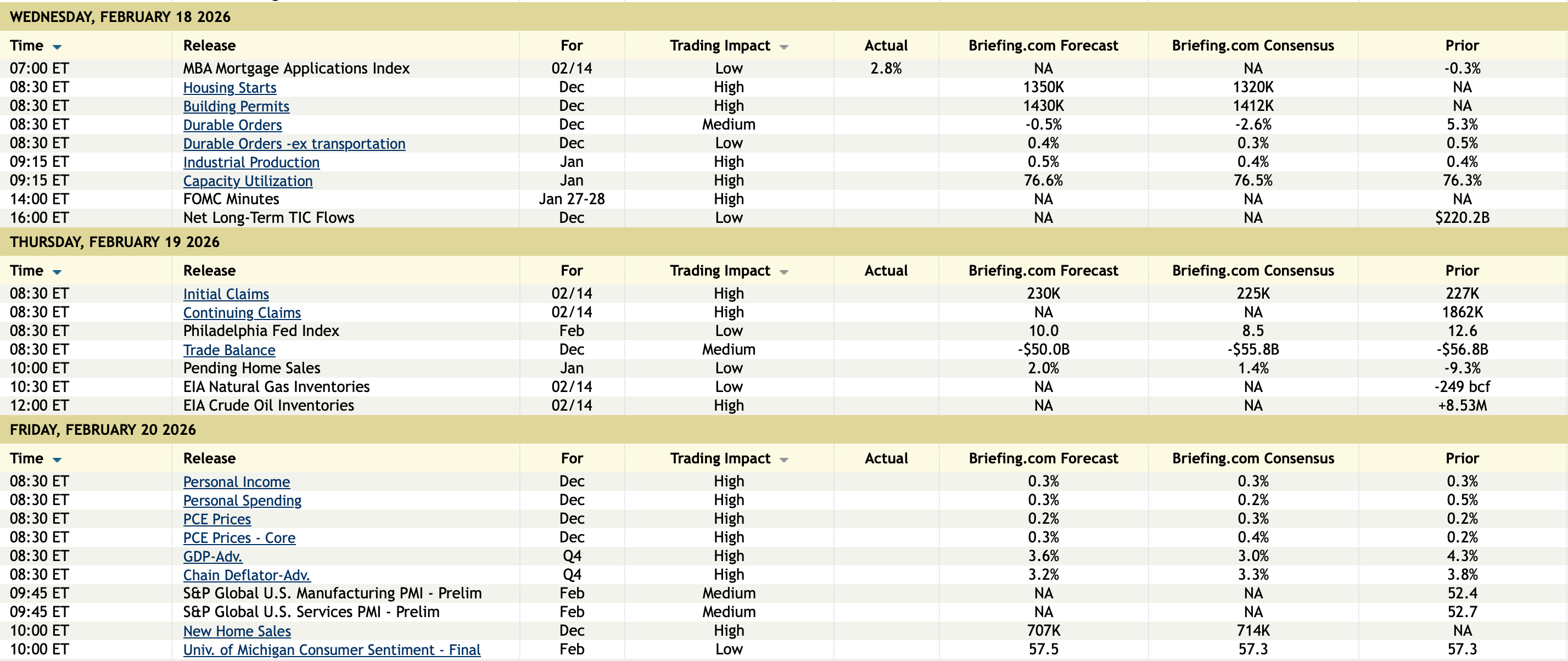

Earnings after the Close Wednesday, Feb. 18

Before the Open Thursday, Feb. 19

BY Doug Kass · Feb 18, 2026, 3:22 PM EST

Wolf Street howls about durable goods orders.

BY Doug Kass · Feb 18, 2026, 2:22 PM EST

BY Doug Kass · Feb 18, 2026, 2:00 PM EST

Given this:

Dougie Kass

Exacta!

After experiencing more than $500k of damage from a frozen pipe on Long Island.... having work being done in Florida house.

A pipe just broke and water is pouring into the first floor.

I might be a bit involved over the next few hours.

At lease I won the exacta.

----

....I have just taken in my index shorts with S&P cash +42 handles (it peaked at +65, where i was shorting)...

Stay tuned.

BY Doug Kass · Feb 18, 2026, 1:50 PM EST

In response to Halftime's upbeat profits outlook:

BY Doug Kass · Feb 18, 2026, 12:40 PM EST

BY Doug Kass · Feb 18, 2026, 12:05 PM EST

- NYSE volume 22% below its one-month average;

- Nasdaq volume 18% below its one-month average;

- VIX index: down 7.20% to 18.83

BY Doug Kass · Feb 18, 2026, 11:20 AM EST

Back shorting ETFs (GRNY) $25.03 and (JOET) $42.83.

BY Doug Kass · Feb 18, 2026, 11:05 AM EST

I have taken a Long Amazon (AMZN) /Short Costco (COST) and Walmart (WMT) pairs trade.

To summarize:

Amazon - Back at around $200 and at a reasonable value level (20x 2027 conservative EPS assumption) with about a 2.5-1.0 upside reward v downside risk. I fully understand the real issue is whether the market will give Amazon time for the investment in data centers to accrue (many large heavily spending tech companies have already experience a contraction in valuations).

WalMart and Costco - Competitors to Amazon, these box retailers seem more than fully priced. In a world of slowing retail expenditures, WMT and COST should not trade twice as expensive as AMZN (who appears capable of +15% to +20% growth over the next two years).

Should equities take a spill I expect Amazon to fall far less than WalMart and Costco.

BY Doug Kass · Feb 18, 2026, 11:05 AM EST

Here are today's things:

* I reestablished Index common and call shorts (with S&P cash +50 handles) into this morning's ramp:

(SPY) $687.69

(QQQ) $607.51

* I added to (MSOS) $3.89 and (MSOX) $2.89 longs

* Pairs trade:

Long (AMZN) $202.98

Short (COST) $1011.87 and (WMT) $128.21

BY Doug Kass · Feb 18, 2026, 10:38 AM EST

* Investors are underpricing risk

* Equities — both fundamentally and from a valuation standpoint — remain somewhere between very overvalued and pornographically overvalued

"Trouble with you

Is the trouble with me

Got two good eyes

But we still don't see

Come round the bend

You know it's the end

The fireman screams

And the engine just gleams

Driving that train

High on cocaine

Casey Jones you better

Watch your speed

Trouble ahead

Trouble behind

And you know that notion

Just crossed my mind..."

- The Grateful Dead Grateful Dead - Casey Jones (Winterland 12/31/78)

What follows is a combination of Daily Diary submissions and my communications with my hedge fund (Seabreeze Partners) Limited Partners:

In past commentary we have noted that, with traditional valuations in the 98%-tile, stock market multiples are materially disconnected from reality and are somewhere between being very overvalued and pornographically overvalued. It remains our strong (but unpopular) conviction that investors are underpricing risk and that today's excessive valuations are a poor launching pad for future investment returns.

We have long been a value investor, rarely chasing price nor compromising our investing disciplines. We are unemotional investors, endorsing (and not deviating from) the strategy of objectively evaluating reward vs. risk and maintaining a "margin of safety" in structuring Seabreeze's portfolio.

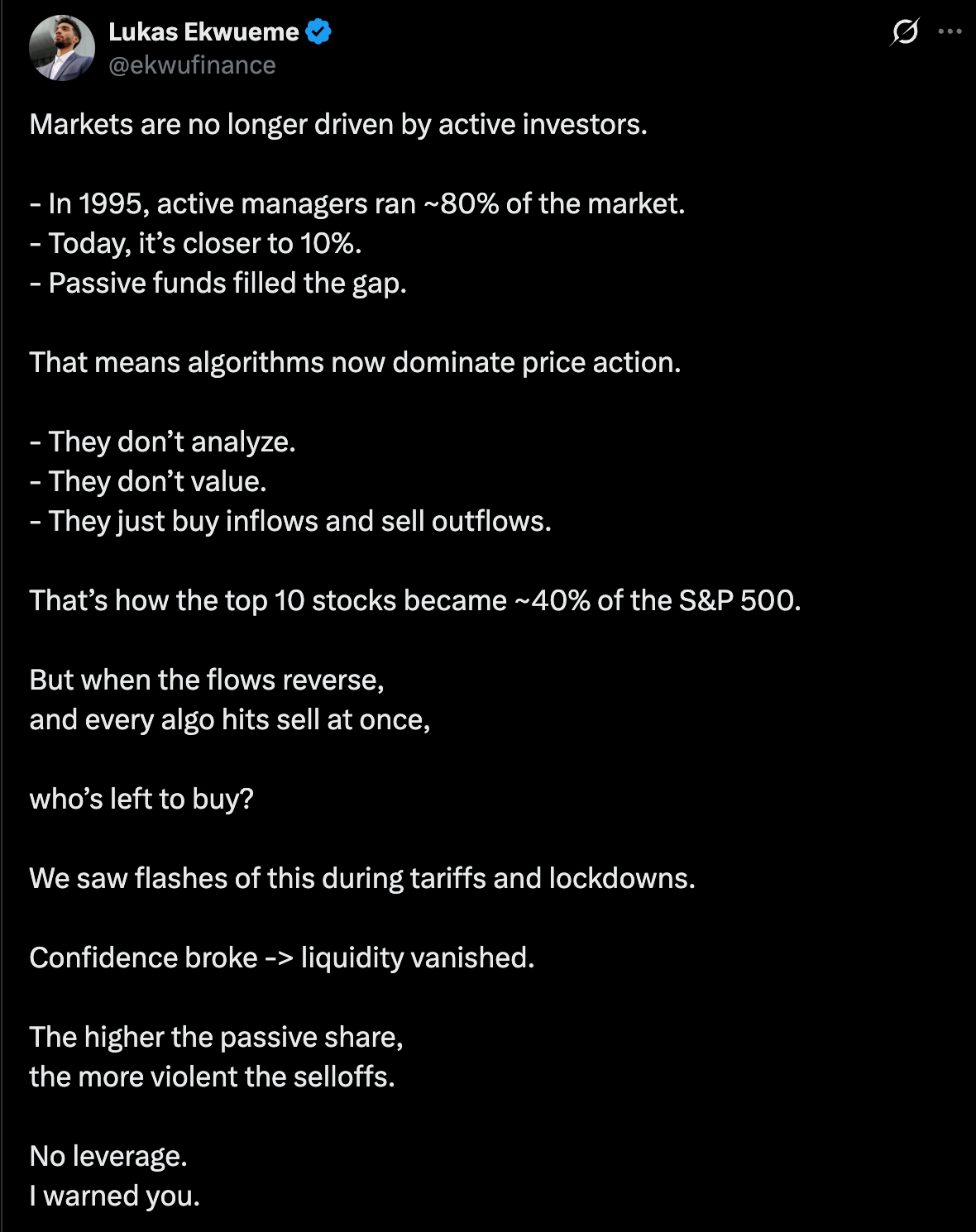

Value investors and investing have become a near obsolete endangered species: redeemed out and/or replaced by pod shops, quantitative products and strategies, index funds and by retail and institutional investors that worship at the altar of price momentum.

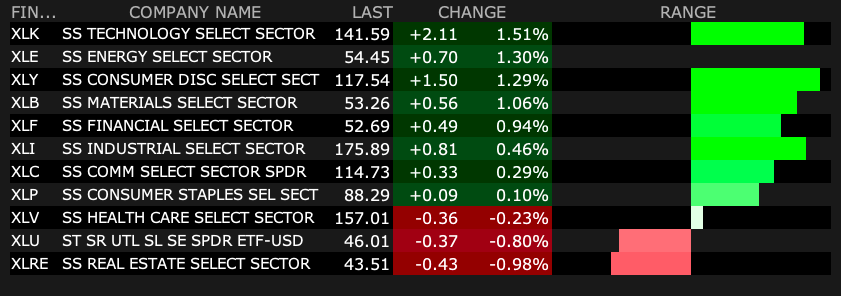

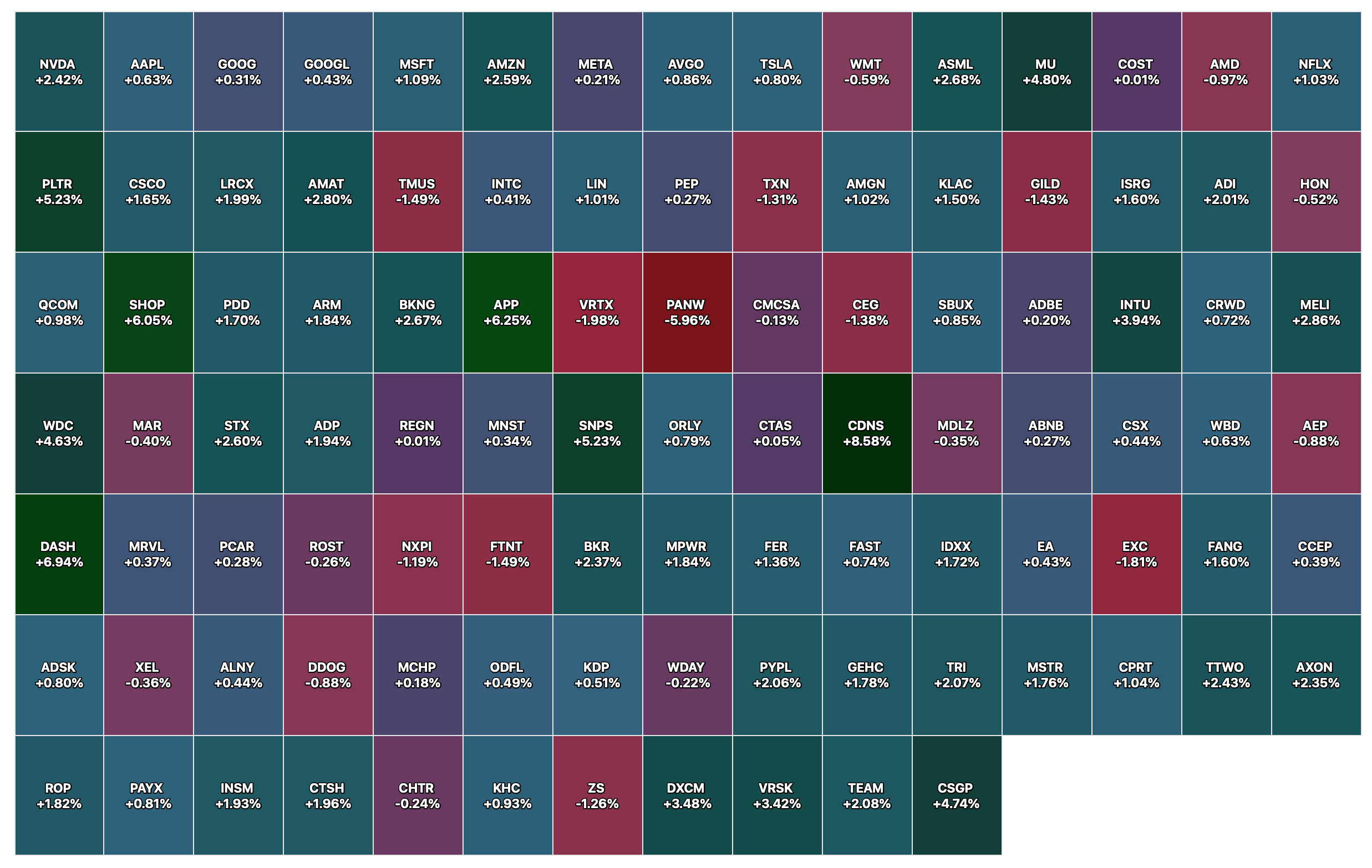

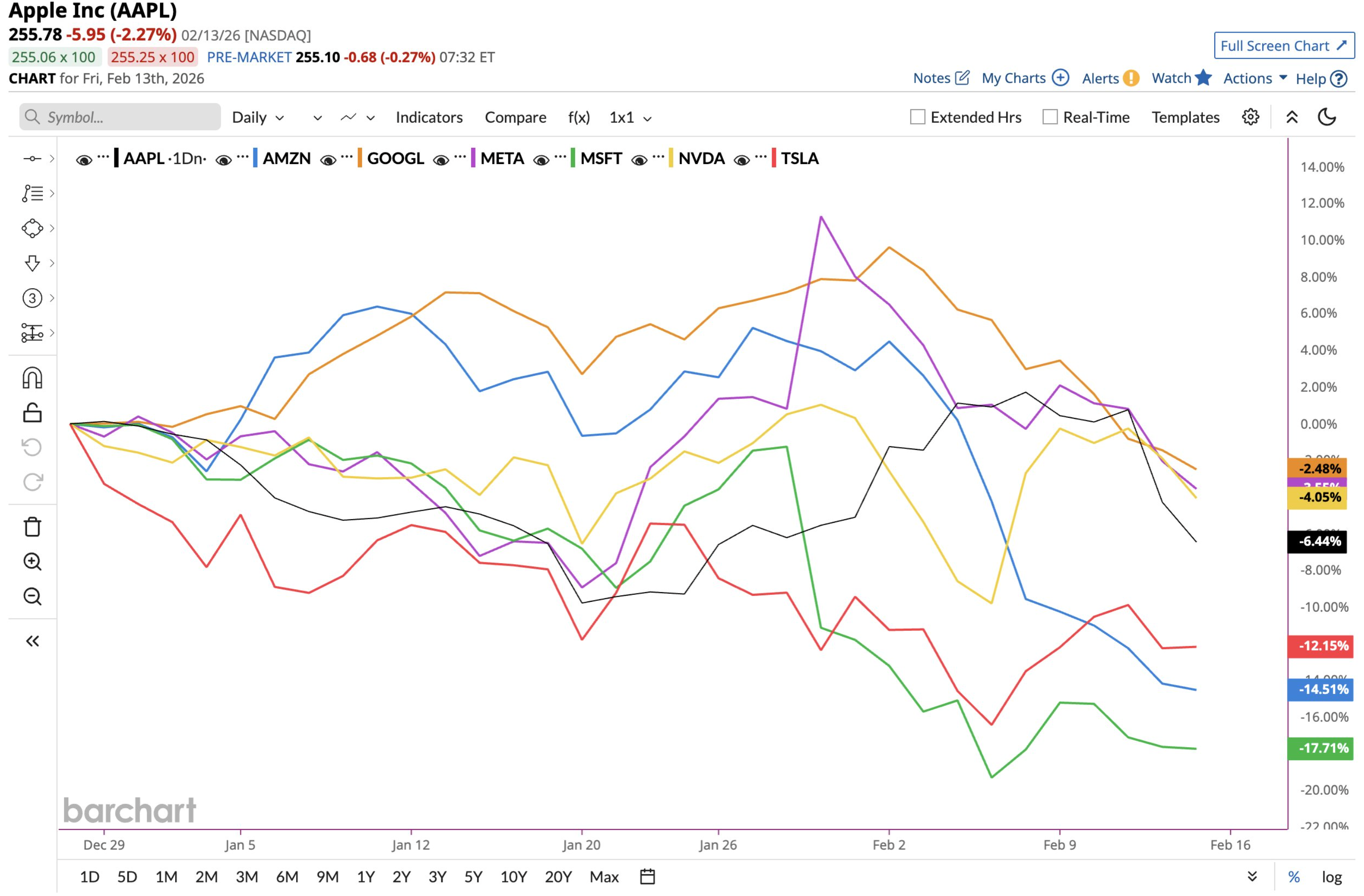

We do not consider the trend away from value investing to be a permanent condition. Indeed, recent price action suggests a change might already be afoot (as previous market leaders (Magnificent Seven) have begun to falter):

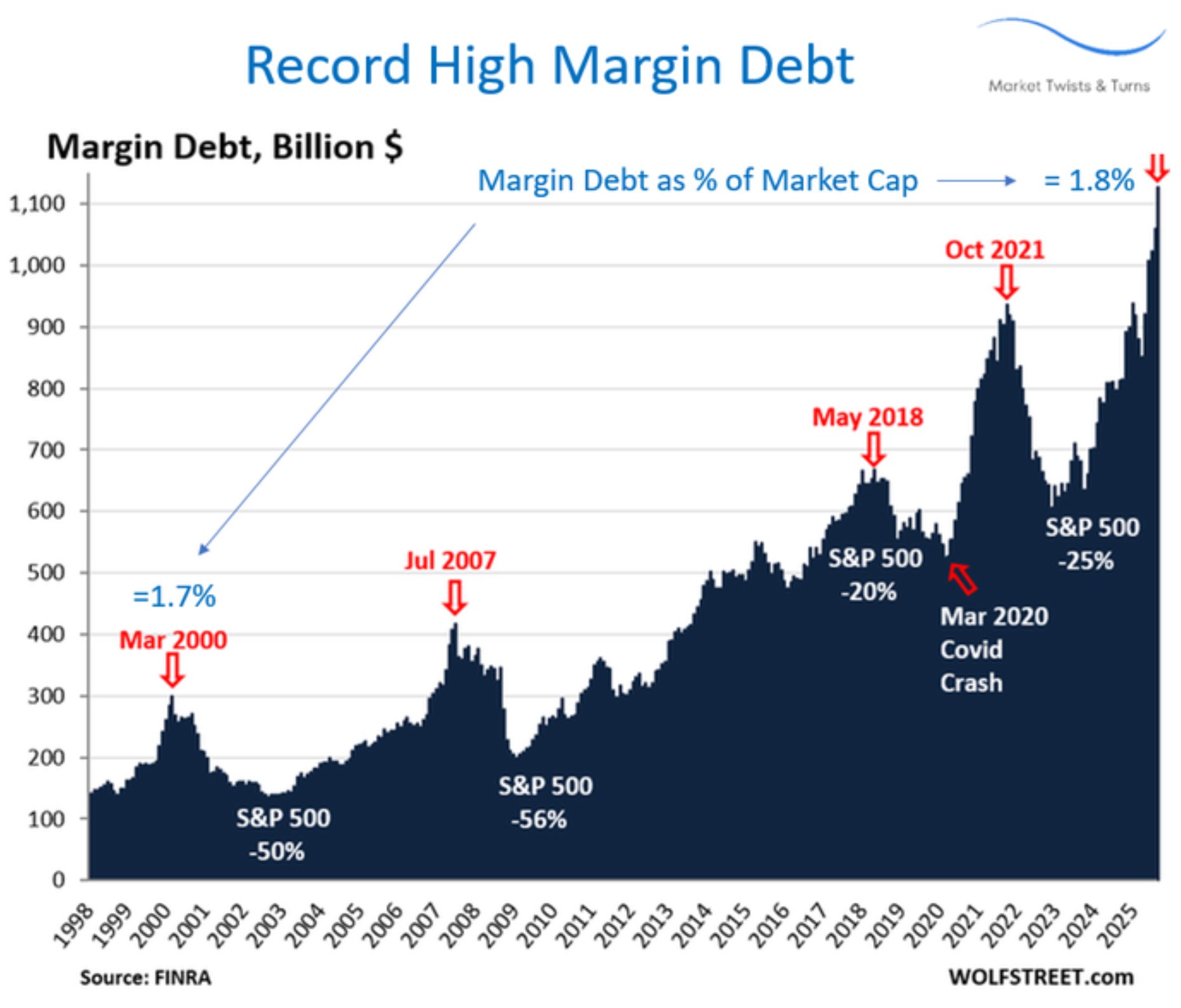

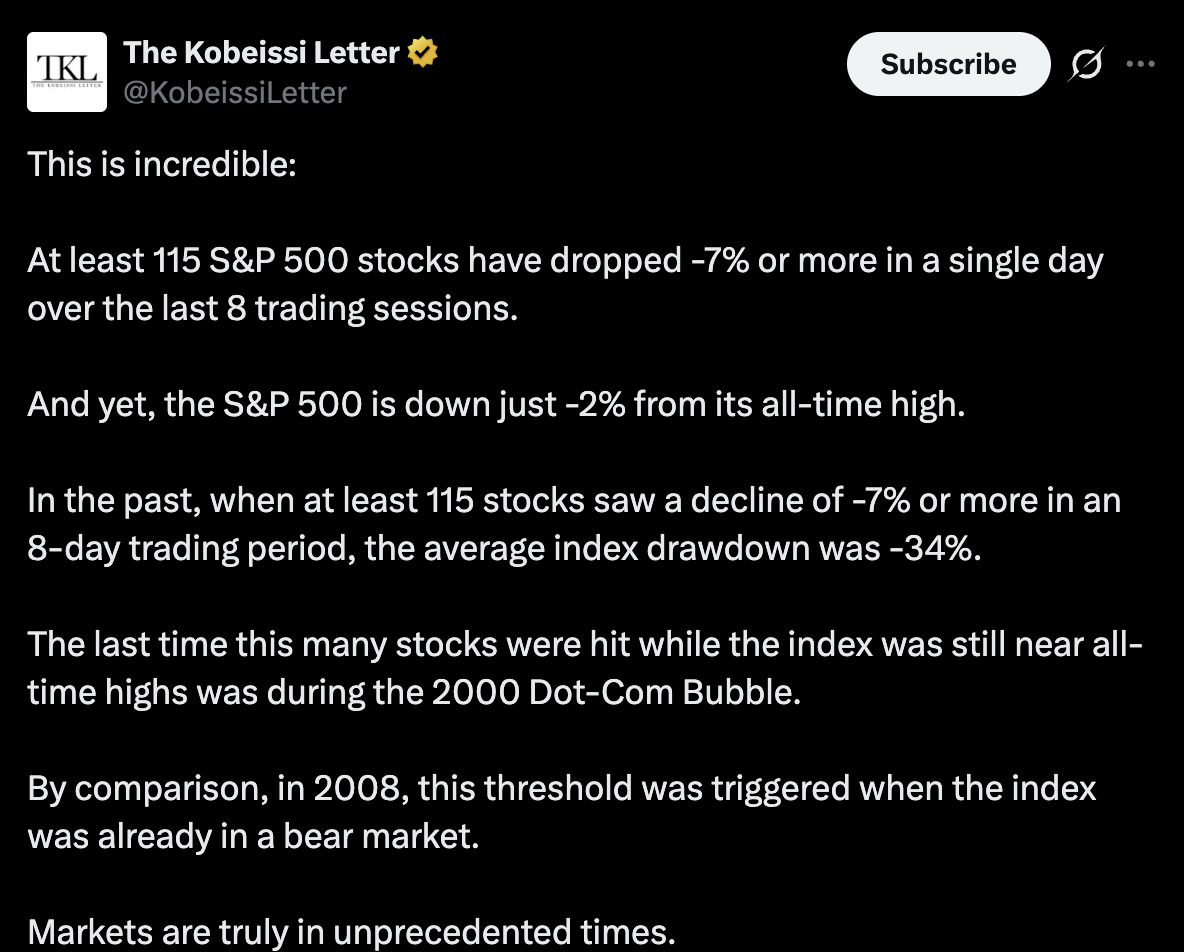

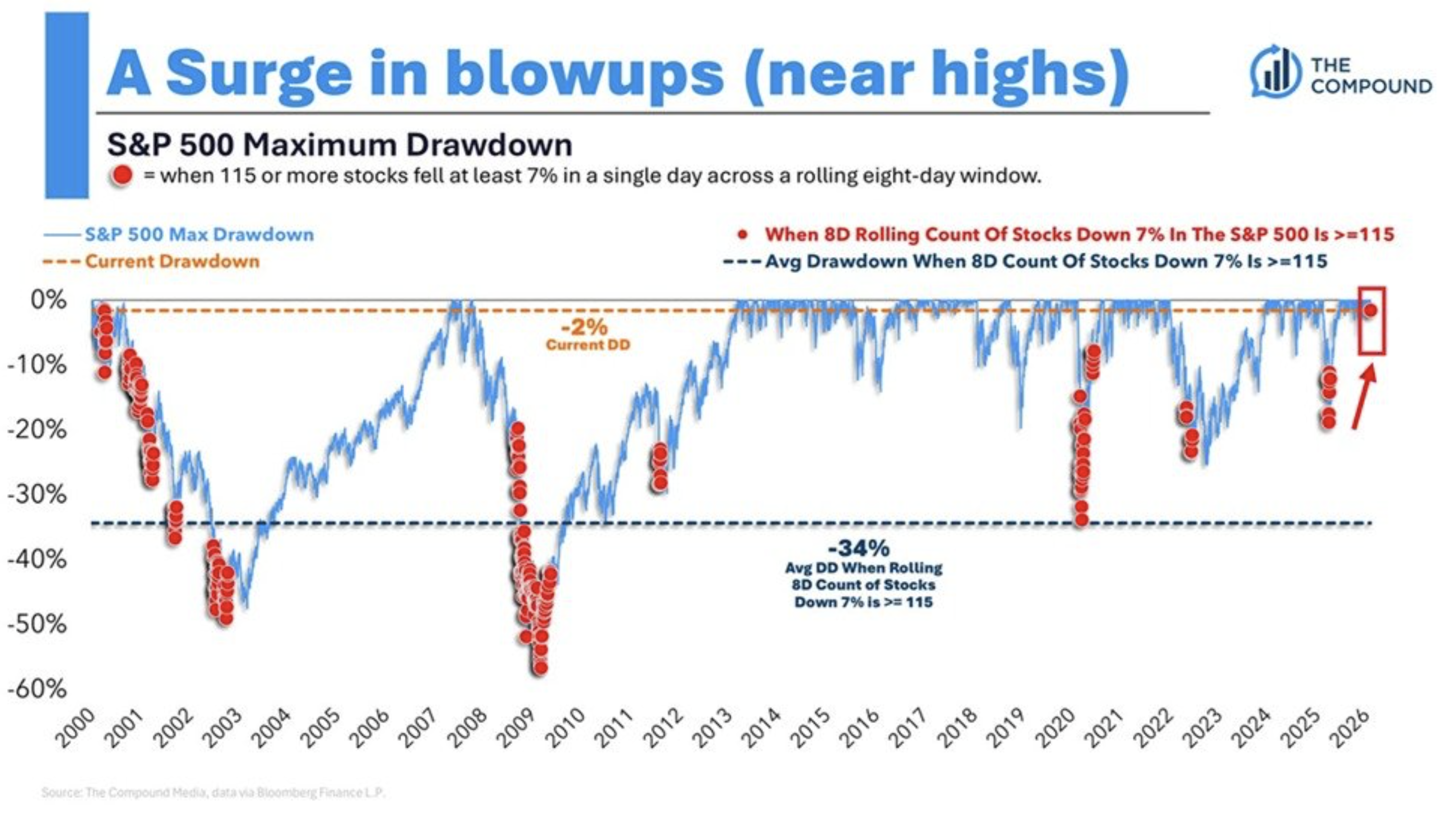

In the extreme, our markets today are looking more like speculative and, even gambling parlors (rather than traditional avenues of investing) than at any time in the last century. What could possibly go wrong with margin debt above the dot-com bubble levels, zero days to expiration (0DTE) options (with 24-hour maturities!) and accounting for 78% of all Nasdaq options volumes when coupled with the CME planning to launch single stock futures?

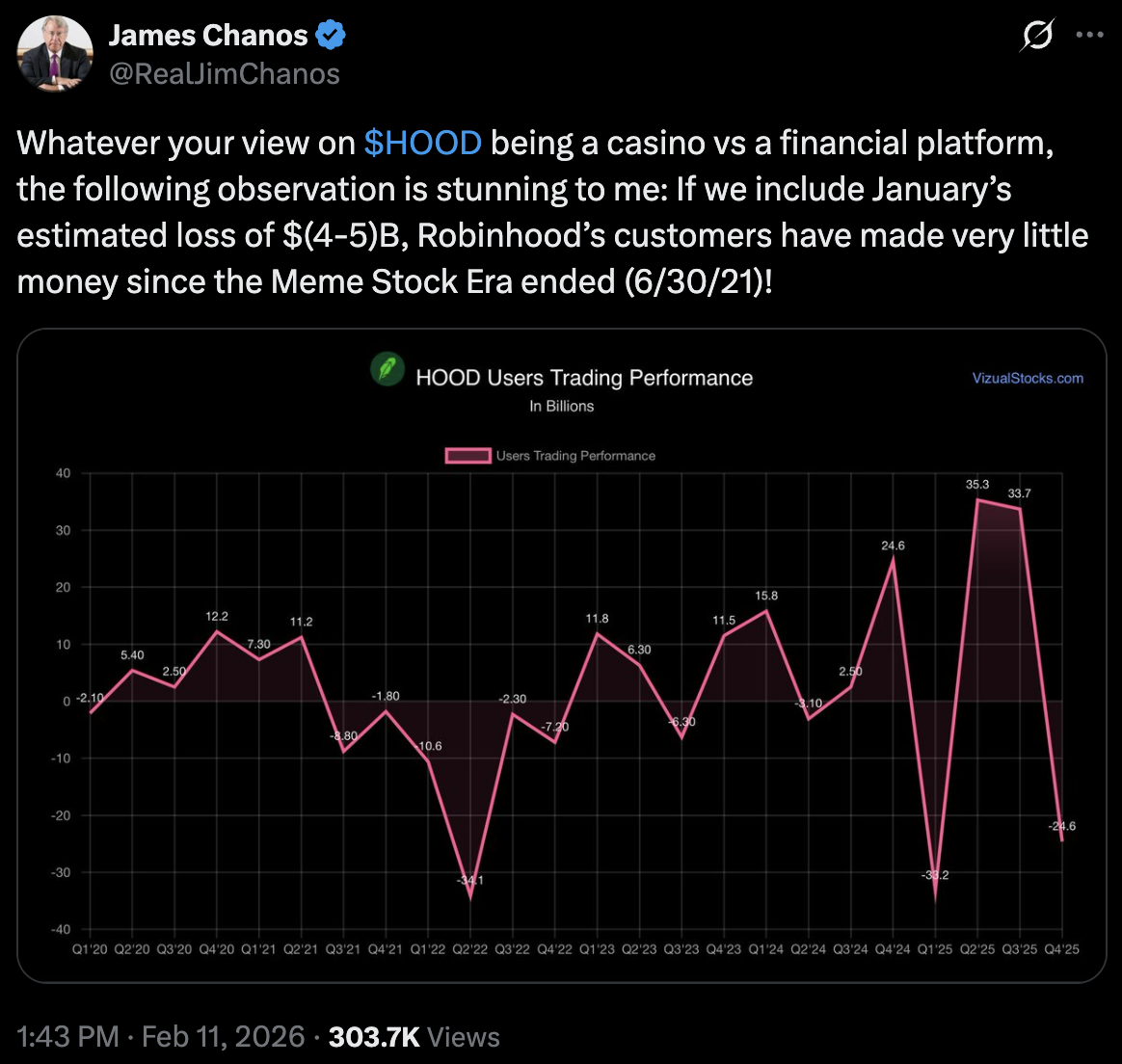

As a template, the popular brokerage website Robinhood (HOOD) (as measured by cumulative customer losses) has become a casino and not a traditional financial platform:

With margin debt, like valuations, at a record high — the equity indices have been inflated by both borrowed money and by the disproportionate role of passive investing (that has led to massive inflows into passive products and strategies). Any reversal in market sentiment could trigger an unwind of this leverage, which could cascade in a market dominated by passive products and strategies.

The recent unwind in the leveraged cryptocurrency markets might foreshadow what may happen in equities over the remainder of the year.

We do not think this ends well and we have growing confidence that we will be able to buy stocks at lower (and more attractive) levels over the next few months.

When and if this time comes, we will not hesitate to buy — but for now we wait patiently for the right pitch.

History has taught us several important lessons — much of which has been lost by the current generation of investors:

Market structure is a little discussed market risk — but it is something that we remain sorely concerned about.

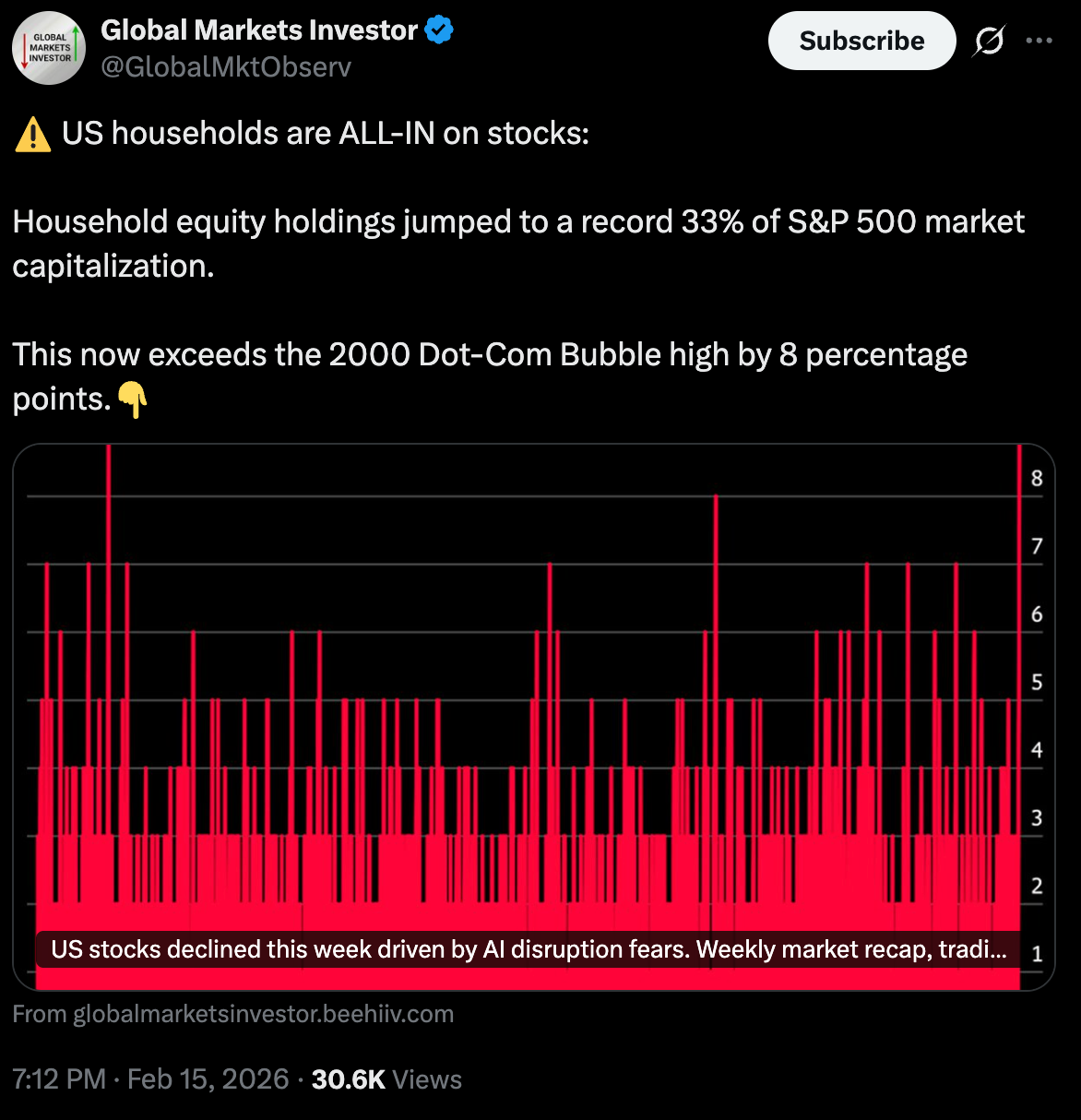

Today investors are all-in on equities:

The decade-long transformation from active portfolio management to passive portfolio management (in which algorithms and machines dominate investment decisions) has contributed to this all-in (long) status. As a result, most investors are now comfortably long (and are ignoring multiple fundamental and valuation concerns).

Passive investment management is agnostic to fundamentals — they know everything about price but very little about value. However, as noted above, the slightest change of momentum lost could lead to an episode of tumultuous selling (think the October 1987 and early 2022 market meltdowns):

Away from market structure, our fundamental concerns — ignored by the majority of investors who have grown momentum-based and influenced — remain very much intact.

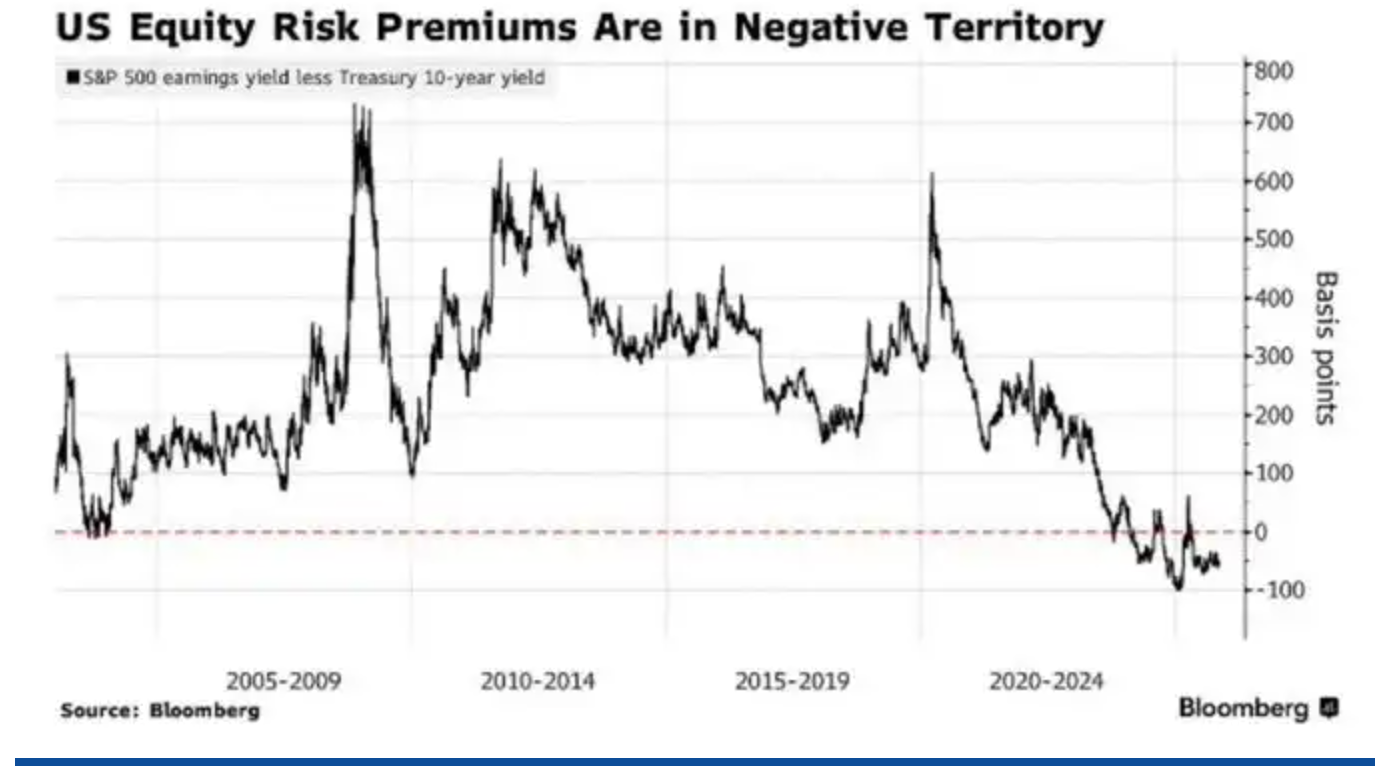

At the core of our negative market view is that the equity risk premium (ERP) has morphed into an equity risk discount (ERD!).

This means, on a risk-adjusted basis, equities offer a zero return to investors.

It also means that investors embrace the absurd belief that there is more risk in bonds than stocks:

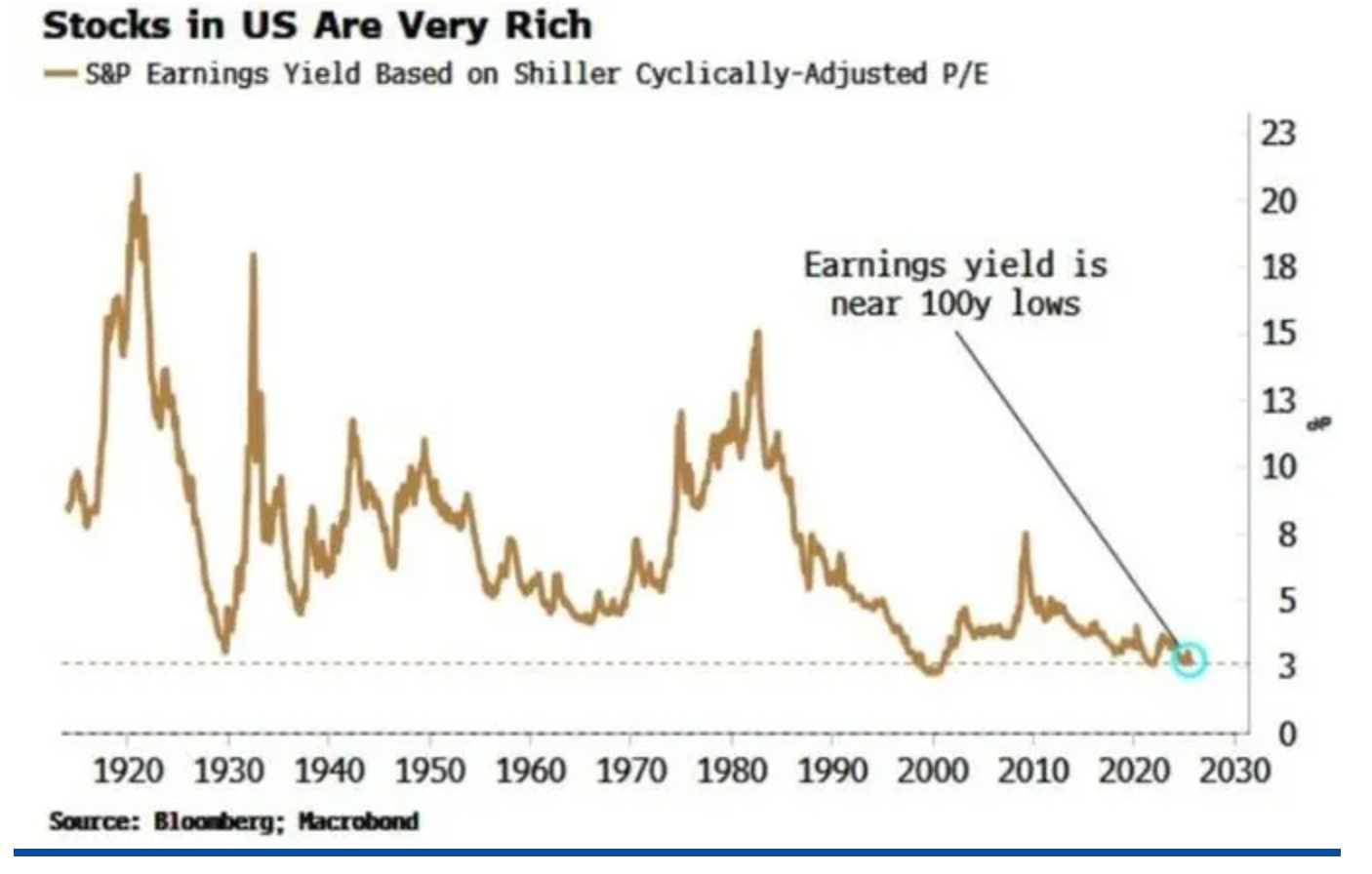

As part of the equity risk premium, the earnings yield (inverse of the P/E ratio) is near a century-year-old low. The only time it was lower was during the dot-com bubble:

Let me end this commentary by repeating some of my fundamental concerns previously discussed:

* We reject the generally positive consensus expectations for U.S. economic growth. Our core concern is that we are in a period of "slugflation" (sluggish domestic economic growth coupled with persistently high inflation):

We have learned that we cannot live alone, at peace: that our own well-being is dependent on the well-being of other nations far away. We have learned that we must live as men, not as ostriches, nor as dogs in the manger.

- Franklin D. Roosevelt

Increasingly (and importantly), errant Administration policy could begin to adversely impact economic alliances and contribute to a downturn in global economic activity.

Domestically, we believe there is a growing possibility that the current K-shaped economy's weakness in the lower-income cohort spreads into the middle and upper-middle class as the cumulative (or stacked) inflation since Covid finally has an impact — causing a spending freeze. With the outlook for global economic growth dissipating, consumer and business sentiment could plummet. BNPL (buy now pay later) and credit defaults would then rise and auto repossessions could increase dramatically.

and...

Economy Is In Recession": Only 181k Jobs Gained For All Of 2025

Drawdowns in the global equity markets and a still moribund housing market may contribute to a negative "wealth effect" and an air pocket with the high-end consumer as investor optimism of 2023-25 is abandoned.

* We also reject the notion that the new Fed Chair will grease the economy (and run it "hot") by lowering interest rates. We disagree on several counts: we see inflation remaining sticky and we don't think the new Chair will have a cooperative Committee.

* As previously noted, historical valuation metrics are at about the 98%-tile. Indicators like the Buffett Ratio, Shiller CAPE and Price/Sales are at all-time overvalued readings. We strongly disagree with the many investors who believe we are in a new valuation paradigm.

From Howard Marks:

* Dividends typically account for a bit more than 35% of the total return of stocks. The S&P Dividend Yield is now at a multi-decade low of 1.12% — contributions from dividends are modest — likely leading to substandard returns for an extended period of time.

* The composition of equity returns remains out of balance with a small number of large-cap technology stocks (highly dependent on the AI trade) contributing to overall returns. We are far less optimistic (than most) regarding the overall value of and return on investment prospects for the outsized AI capital expenditures — for society and as it relates to the productivity and profitability of individual companies.

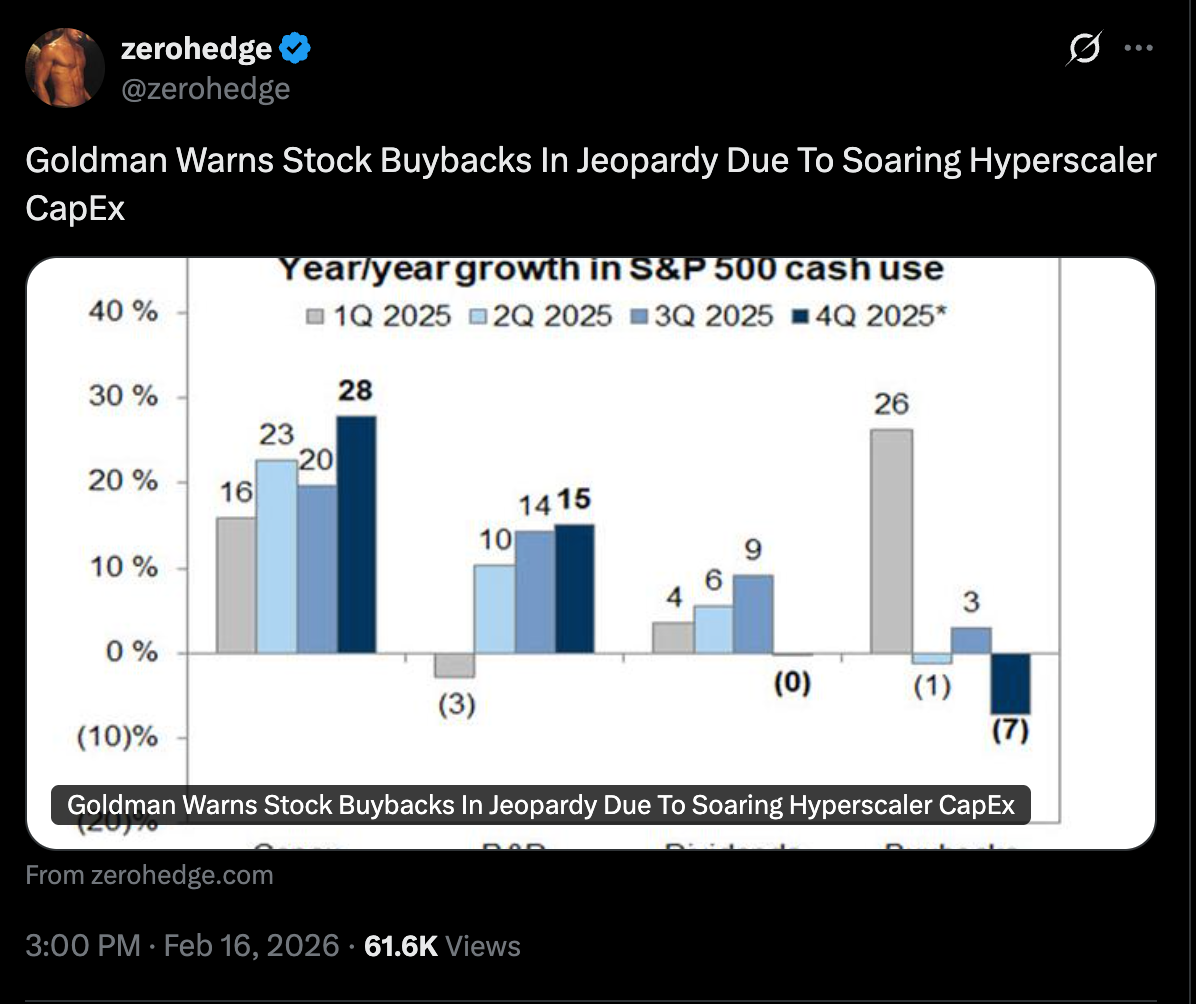

Mag 7 free cash flow is in free fall. So, after buying back over $1 trillion of stock in recent years (dramatically supporting the Nasdaq), the game is over as the unprecedented spend has transformed the hyperscalers from capital light to capital intensive — with attendant and adverse ramifications (on EPS growth and capital allocation strategy):

* Neither political party is acting in a fiscally responsible manner. A feckless approach to our deficit is producing a steady march higher in our national debt:

* I recently mentioned reading my friend Andrew Ross Sorkin's new book 1929: Inside the Greatest Crash in Wall Street History-and How It Shattered a Nation...

I couldn't help but see the similarities between then and now. The 1920s did not end well as our society lost sight of the value of regulations: wise rules are a source of abundance; well-regulated markets/systems attract users and investors; removing the constables patrolling our financial markets is potentially dangerous; and U.S. capital markets became the world's largest not despite regulation, but because of it.

* Wall Street strategists are unanimously bullish — on average they are forecasting a +11% return for 2026. They are nearly always bullish, so their opinions should be taken accordingly — and with a grain of salt.

As previously noted, Warren Buffett warned about a too ebullient mindset in November 1999, only four months before the dot-com bubble burst:

Once a bull market gets underway and once you reach the point where everybody has made money no matter what system he or she followed, a crowd is attracted into the game that is responding not to interest rates and profits but simply to the fact that it seems a mistake to be out of stocks. In effect, these people superimpose an I-can't-miss-the-party factor on top of the fundamental factors that drive the market. Like Pavlov's dog, these "investors" learn that when the bell rings — in this case, the one that opens the New York Stock Exchange at 9:30 a.m. — they get fed. Through this daily reinforcement, they become convinced that there is a God and that He wants them to get rich.

History never repeats itself. Man always does.

- Voltaire

Delusions swing between extremes, like pendulums. Delusions of grandeur and unending wealth give place to delusions of unending gloom. One is as unreal as the other.

Today we seem to be close to an extreme in speculative activity and valuations. Unfortunately, history teaches us that the unsustainable cannot be sustained as, ultimately, with panic and pain, bubbles burst.

When we look at today's valuations we are reminded of (a twist) of something written by Jean-Jacques Rousseau:

History never deceives us; it is we who deceive ourselves.

For what we have learned from history is that we haven't learned from history.

BY Doug Kass · Feb 18, 2026, 9:30 AM EST

-RXT +143% (Rackspace and Palantir announce strategic partnership to help enterprises rapidly deploy and operate Palantir’s Foundry and Artificial Intelligence Platform (AIP) in production)

-TCMD +26% (earnings, guidance)

-MCW +16% (to be taken private by Leonard Green at $7/shr in cash; earnings)

-GRMN +15% (earnings, guidance; announces share buyback program)

-ZEO +15% (signs MOU with Creekstone Energy to Develop 280 MW of Baseload Power for Utah AI Data Center)

-WING +13% (earnings, guidance)

-BIOA +12% (earnings)

-GPN +11% (earnings, guidance)

-GSHD +11% (earnings, guidance)

-MSGS +10% (CFO Victoria Mink to step down)

-PODD +8.0% (earnings, guidance)

-PRG +7.7% (earnings, guidance)

-MRNA +7.3% (U.S. FDA will Initiate Review of mRNA-1010, Investigational Seasonal Influenza Vaccine Submission)

-CE +7.1% (earnings, guidance)

-COCO +7.0% (earnings, guidance)

-ADI +5.7% (earnings, guidance)

-PUMP +4.1% (earnings, guidance)

-OVV +3.9% (agrees to sell its Anadarko assets for $3B cash)

-RIOT +3.6% (Activist holder Starboard said to urge company to speed up shift to data centers)

-MCO +3.5% (earnings, guidance)

-PLTR +3.0% (Rackspace and Palantir announce strategic partnership to help enterprises rapidly deploy and operate Palantir’s Foundry and Artificial Intelligence Platform (AIP) in production)

-SM +2.1% (to sell certain South Texas assets to Caturus Energy, LLC for a cash purchase price of $950M)

-FVRR -23% (earnings, guidance)

-ACLS -14% (earnings, guidance)

-DINO -14% (earnings; CEO Tim Go to take a voluntary leave of absence from his duties)

-RXRX -13% (NVDA exits stake)

-PANW -7.2% (earnings, guidance)

-FIGR -5.7% (prices, upsizes secondary public offering of common stock)

-WPC -3.5% (prices 6M shares for gross proceeds ~$432M)

-POR -3.0% (prices 9.5M shares at $50.70/share)

-SNDK -2.8% (prices 5.8M shares at $545/shr in secondary offering)

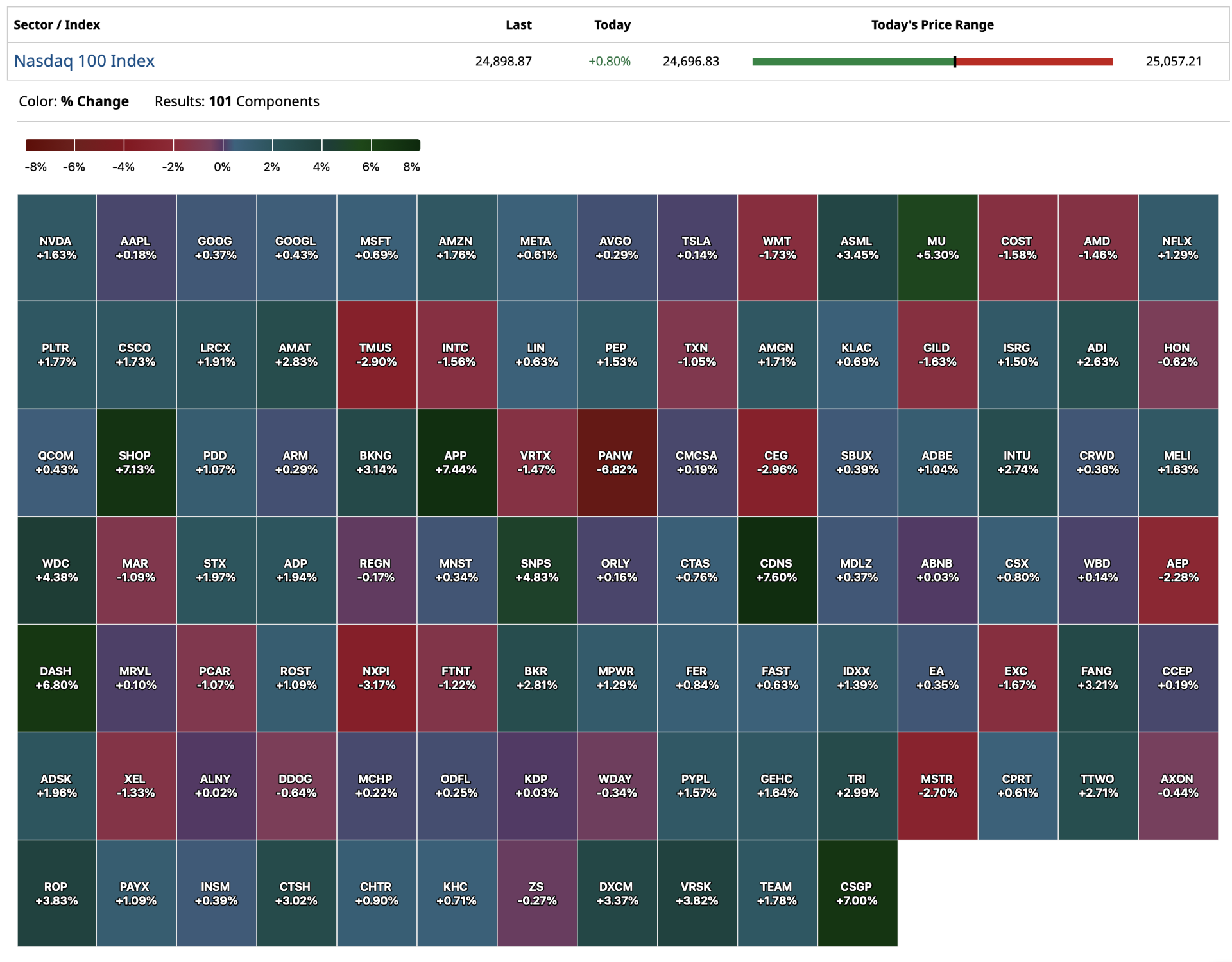

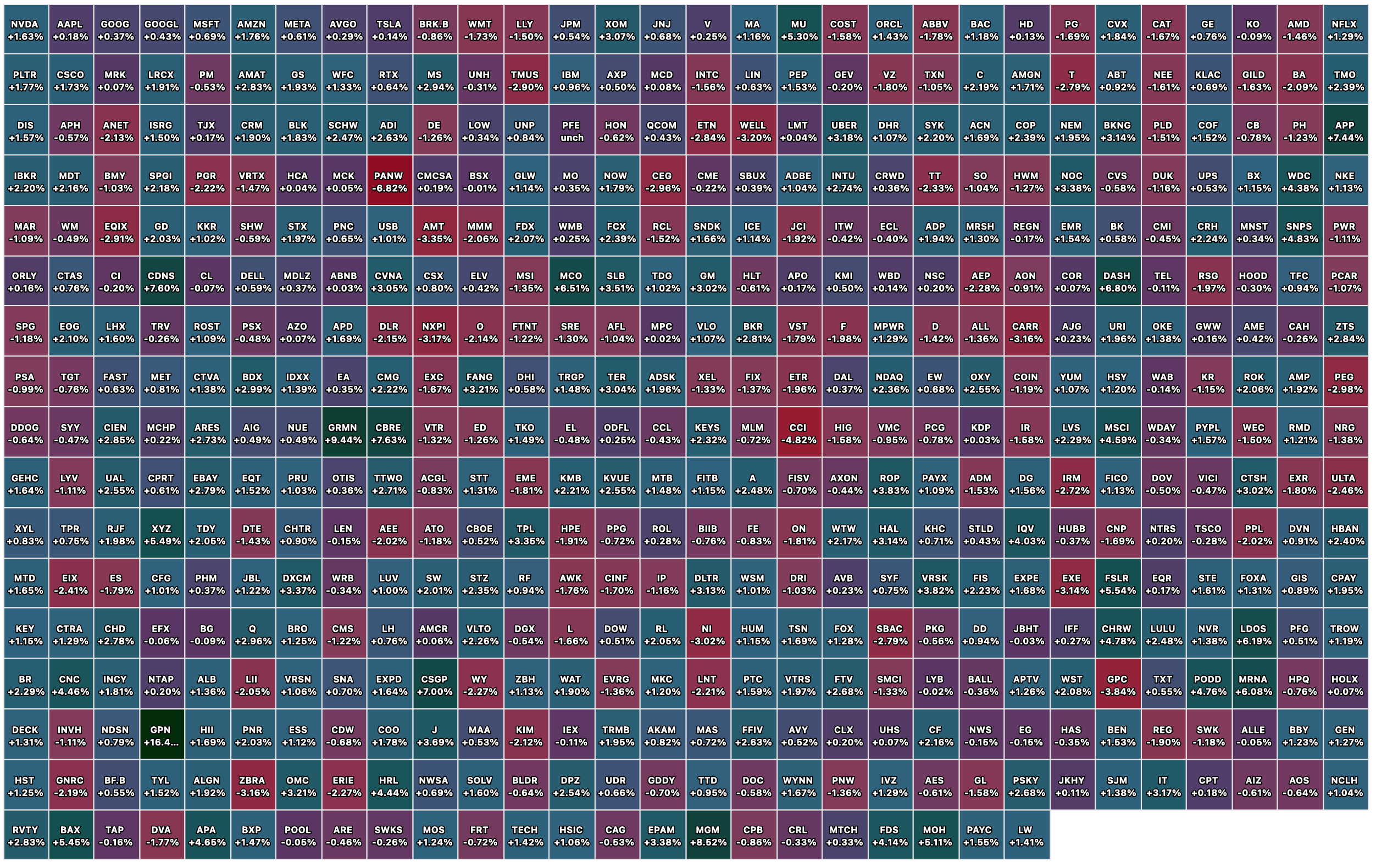

BY Doug Kass · Feb 18, 2026, 9:22 AM EST

BY Doug Kass · Feb 18, 2026, 9:05 AM EST

BY Doug Kass · Feb 18, 2026, 8:50 AM EST

8:30 a.m.: Fed Vice Chair for Supervision Bowman (Voter) speaks before the Banking Outlook Conference: "The Next Horizon inBanking" hosted by the Federal Reserve Bank of Atlanta (No text. Q&A from moderator. No webcast)

1 p.m.: Treasury hosts a $16B 20-Year Bond Auction

BY Doug Kass · Feb 18, 2026, 8:40 AM EST

And my response to Jim:

BY Doug Kass · Feb 18, 2026, 7:15 AM EST

BY Doug Kass · Feb 18, 2026, 7:04 AM EST

BY Doug Kass · Feb 18, 2026, 6:05 AM EST

BY Doug Kass · Feb 18, 2026, 5:55 AM EST

The S&P Short Range Oscillator remains overbought at 3.16% vs. 3.60%.

BY Doug Kass · Feb 18, 2026, 5:45 AM EST