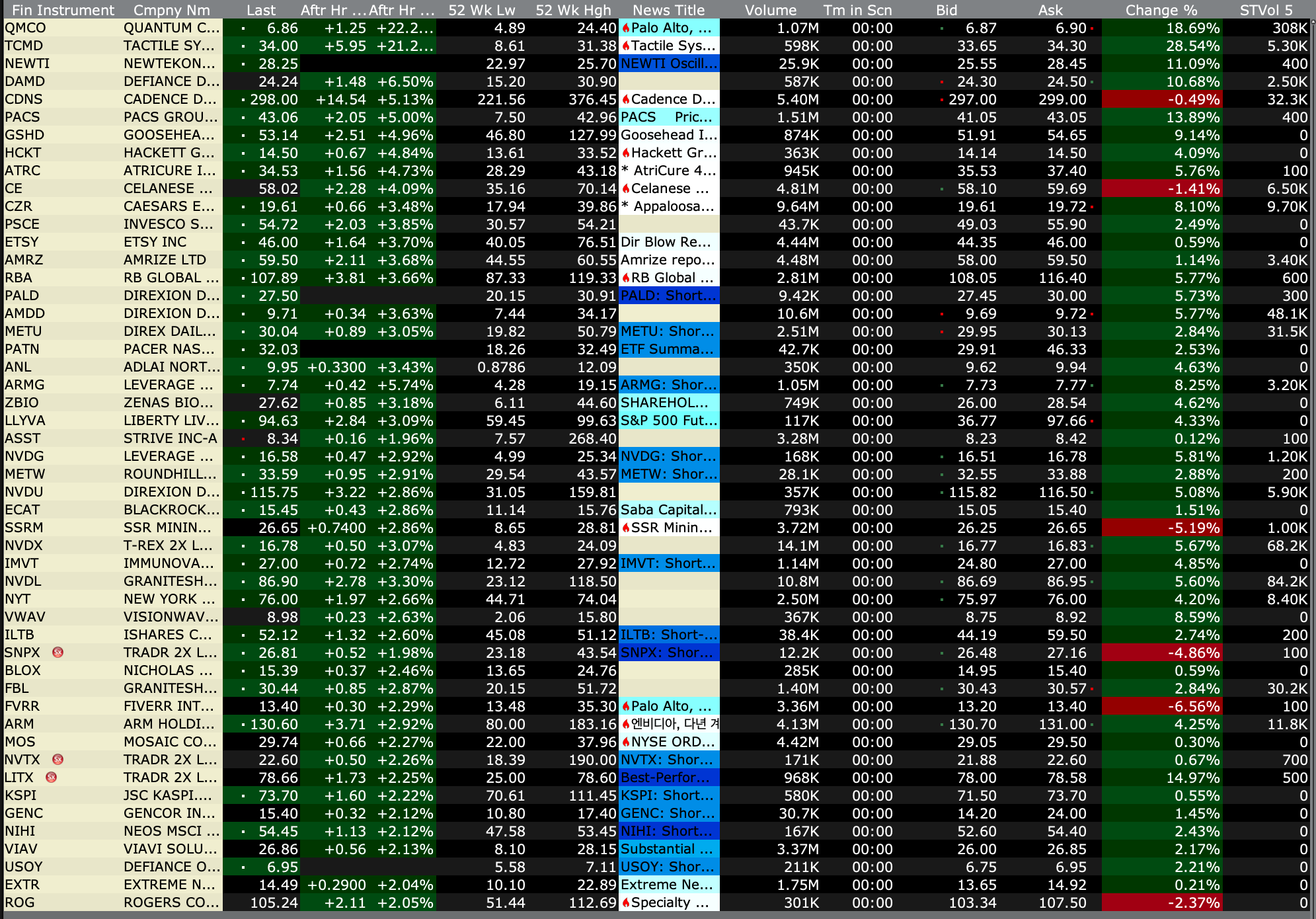

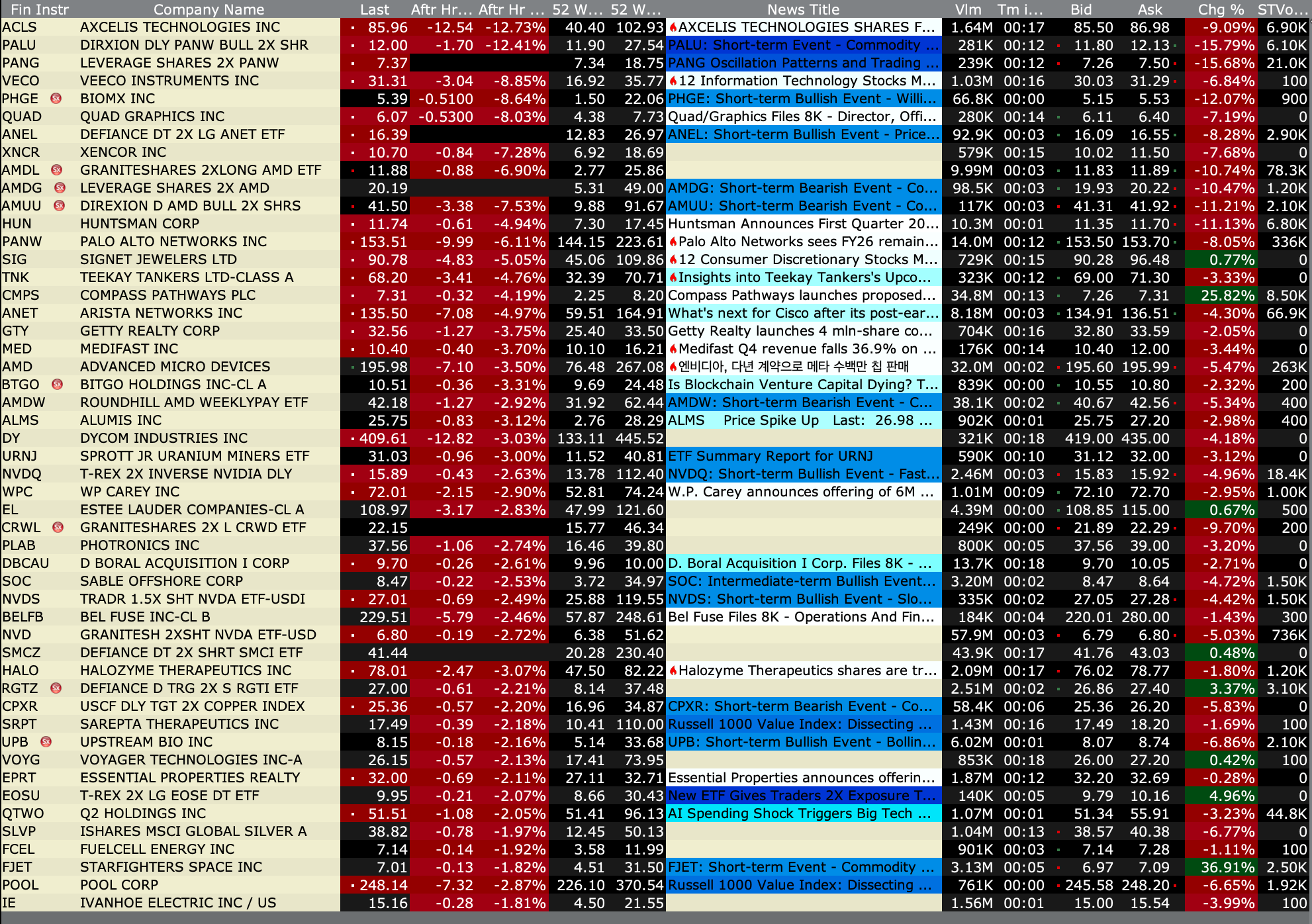

After-Hours Advancers and Decliners

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Feb 17, 2026, 4:45 PM EST

BY Doug Kass · Feb 17, 2026, 4:45 PM EST

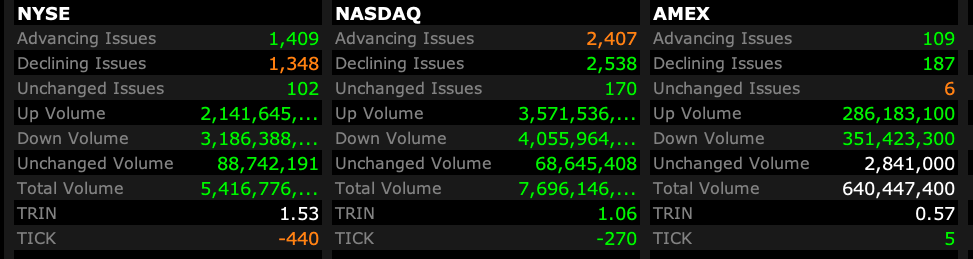

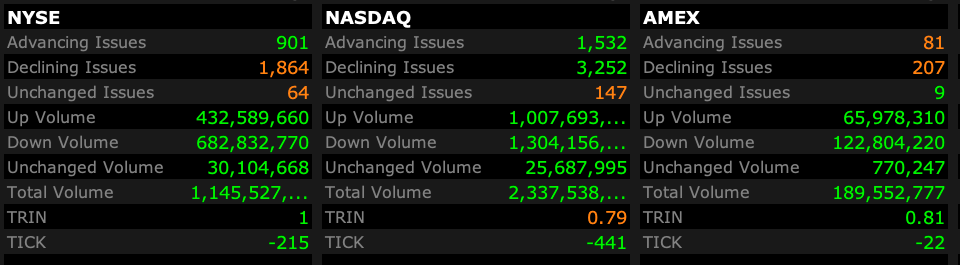

- NYSE volume 5% below its one-month average;

- NASDAQ volume 15% below its one-month average;

- VIX index: down 4.29% to 20.29

BY Doug Kass · Feb 17, 2026, 4:30 PM EST

Berkshire Hathaway reduces its Apple (AAPL) holdings from 238.21 million to 227.92 million shares.

BY Doug Kass · Feb 17, 2026, 4:16 PM EST

With S&P cash selling off and up by less than +10 handles I am taking in all of my short index calls (which I was scaling into on strength) for a small profit — as I am just plum tired out from trading.

And that is saying something!

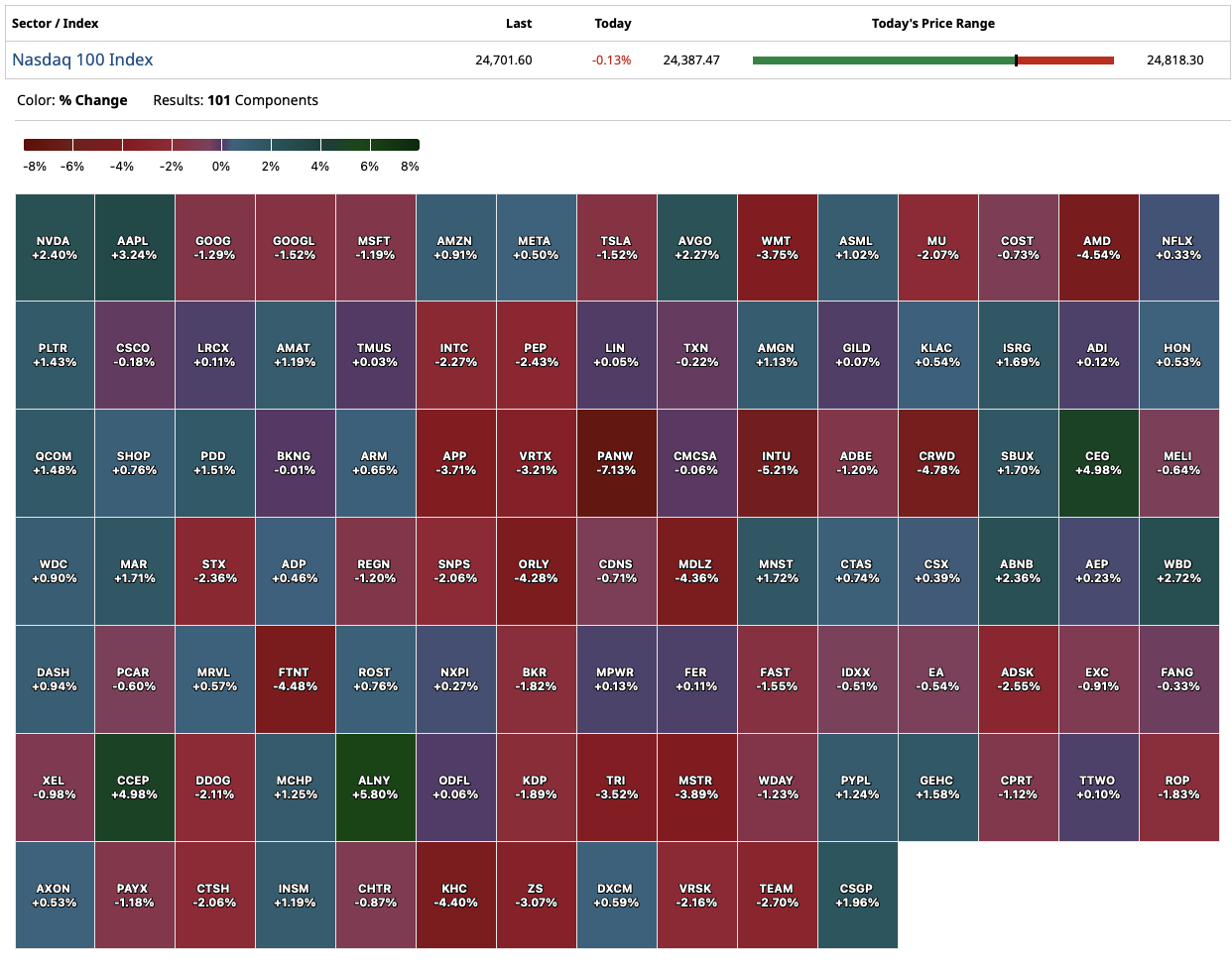

BY Doug Kass · Feb 17, 2026, 3:35 PM EST

BY Doug Kass · Feb 17, 2026, 3:29 PM EST

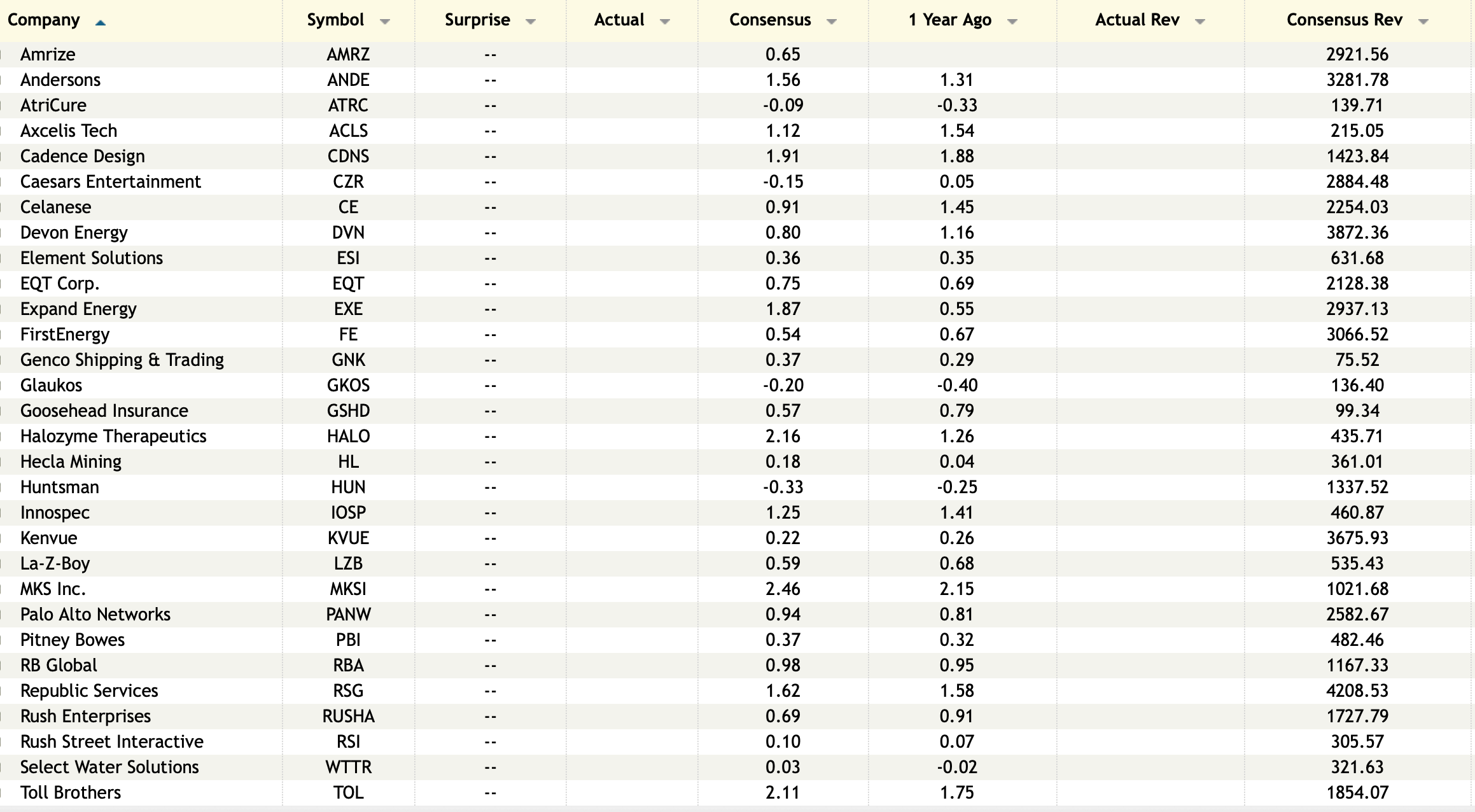

Earnings After the Close Tuesday, Feb. 17

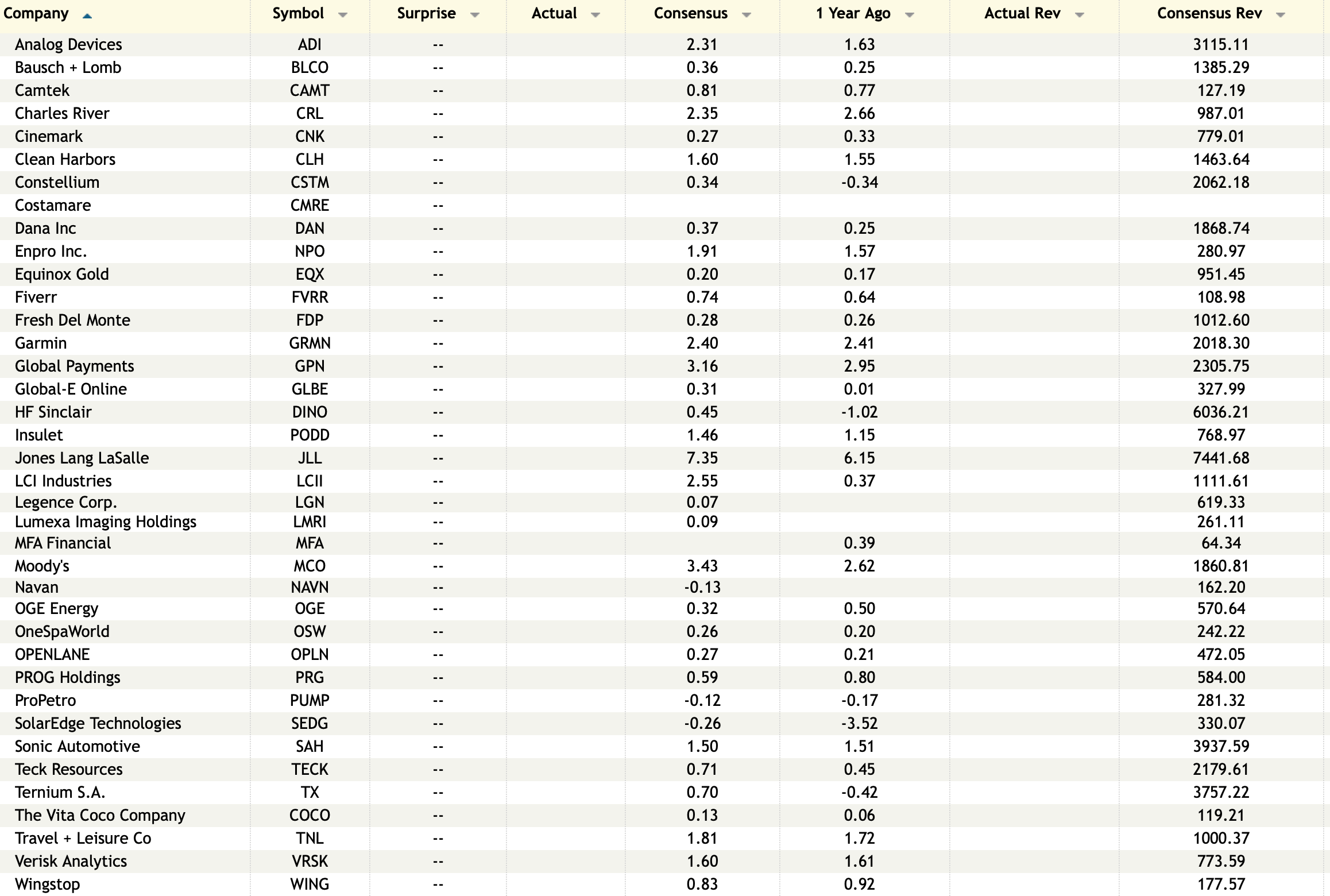

Earnings Before the Open Wednesday, Feb. 18

BY Doug Kass · Feb 17, 2026, 3:16 PM EST

Thus far there has been 5-6 different market trends today.

Blame the player and not the game.

Maximize your trading success within the constraint of the market's volatility!

BY Doug Kass · Feb 17, 2026, 2:30 PM EST

With S&P cash +19 handles (and well off the day's lows) we are back shorting index calls.

BY Doug Kass · Feb 17, 2026, 2:03 PM EST

BY Doug Kass · Feb 17, 2026, 2:00 PM EST

PepsiCo (PEP) (my favorite stock for 2026) is finally selling off (-$5 to $161 today).

We had been steadily selling the rip and finally liquidated the entire position at $167.45 approximately 12 days ago:

PepsiCo (PEP) was my top stock pick for 2026.

It already has been!

I am entirely out of my (PEP) long at $167.45.

Position: None

By Doug Kass Feb 5, 2026 2:37 PM EST

I would be a buyer under $155.

BY Doug Kass · Feb 17, 2026, 1:32 PM EST

S&P cash is now -17 handles and I have taken in my short index calls for another profit.

From about two hours ago:

With S&P cash +9 handles, I am getting more serious on my index short.

Position: Short SPY calls (S), QQQ calls (S)

By Doug Kass Feb 17, 2026 11:35 AM EST

I currently have no index positions (long or short).

I would re-short on strength...

BY Doug Kass · Feb 17, 2026, 1:22 PM EST

BY Doug Kass · Feb 17, 2026, 1:14 PM EST

BY Doug Kass · Feb 17, 2026, 12:55 PM EST

I am re-shorting (JOET) partially because of this strategy disadvantage:

BY Doug Kass · Feb 17, 2026, 12:30 PM EST

I'm re-shorting (GRNY) at $24.77 and (JOET) at $42.44.

BY Doug Kass · Feb 17, 2026, 12:12 PM EST

With S&P cash +9 handles, I am getting more serious on my index short.

BY Doug Kass · Feb 17, 2026, 11:35 AM EST

- NYSE volume flat to its one-month average;

- Nasdaq volume 17% below its one-month average;

- VIX index: up 8.07% to 22.91

BY Doug Kass · Feb 17, 2026, 11:30 AM EST

With S&P cash up by +4 handles, I am back shorting index calls.

Starting very small, given the market's volatility and lack of predictability.

BY Doug Kass · Feb 17, 2026, 11:15 AM EST

From Peter Boockvar:

The February NY manufacturing index, the first industrial figure out for February, was +7.1 vs +7.7 in January and about as expected. This compares with the six montha average of +4.2 and I’ll compare the internals too with the 6 month average to smooth out the very volatile nature of the figures.

New orders at +5.8 compares with its six month average of +.9. Backlogs rebounded to positive territory at 9.1 vs the half yr average of -5.1. Inventories rebounded too to +7.1 vs +1.6.

With employment, it was +4 vs +2.1 while the workweek went positive at 2.1 vs -.3.

Delivery time rose to 4 and vs the six month average of 1.6 (the higher it goes, the longer the lead time, slower supply chain). Prices paid at 49.1 is vs 48 for the half yr average. Prices received at 22.2 is one pt below the six month average.

Looking six months ahead, confidence was 34.7 vs 26.8 for the half yr average. Capital spending plans at 18.2 is almost three times the six month average and hopefully the tax bill is helping to lift CapEx plans outside of data centers.

Bottom line, whether inventory induced in terms of the need to restock or something more with end demand, hopefully we’re trying to carve out a bottom in manufacturing because its been a long three years for those in this sector.

The February NAHB home builder sentiment survey remained well below 50 at 36, down 1 pt m/o/m and 2 pts below the estimate. It was last above 50 in April 2024. The Present Situation remained unchanged at 41 but the Future Outlook fell 3 pts to 46. Notwithstanding the drop in mortgage rates, Prospective Buyers Traffic fell another 2 pts to just 22, highlighting that the price of a home is even more important than the cost of funding right now, especially in terms of coming up with a down payment.

The NAHB said “Persistent affordability challenges, including high housing price-to-income ratios and elevated land and construction costs, helped push builder confidence lower for the second straight month to start the year.”

Also, “While the majority of builders continue to deploy buyer incentives, including price cuts, many prospective buyers remain on the sidelines. Although demand for new construction has weakened, remodeling demand has remained solid given a lack of household mobility.”

Again, when talking about the US economy, it is so important to slice and dice the components because of the narrow contribution we’re seeing in terms of growth. Housing, all in, makes up somewhere in between 15-18% of US GDP according to the NAHB and this key area of business activity remains tough.

BY Doug Kass · Feb 17, 2026, 11:05 AM EST

From Peter Boockvar:

I’m going to steal a line from the commodities guru Jeff Currie to describe what we’re now seeing in the stock market but expand it past just commodities. It’s the ‘revenge of the old economy.’ It’s those stocks that can’t be GenAI’d out of business (or perceived to be) and instead use it to improve the efficiency of their respective companies. Regardless of whose LLM will be the best, regardless of what software subscription a business will end up using, the average person will still have to eat and drink food and beverages. They will still need garbage bags to dispose of trash. They will still need tin foil to hold food in the fridge. They will of course still be using tissues and toilet paper. While snacks for lower income consumers have become more discretionary and thus impacted by spending habits, chances are people are still going to eat cookies and pretzels, drink coffee and buy pet food for their furry loved ones.

Also, getting a manufactured good from point A to point B will still need a ship, truck, plane and/or train. Yes, maybe the brokerage end will be impacted but the physical delivery won’t. I don’t believe yet that we will be transported from place to place via a Star Trek like GenAI model so getting on a plane will still be necessary with respect to travel. While AI is making music, nothing will replace the demand for seeing a live artist on stage. Until robots start excelling in sports, the demand to watch humans perform on the field/ice/court, etc... will not be disrupted. Go US Women’s Hockey Team! Fixing a car still needs parts and labor (maybe a robot one day), GenAI can only help in determining what’s wrong.

You get the point and I’ll reiterate my bullish and long stance on my two favorite groups as we entered 2026, that being oil and gas stocks and consumer staples stocks, not pricey WMT and COST, but the product/food makers.

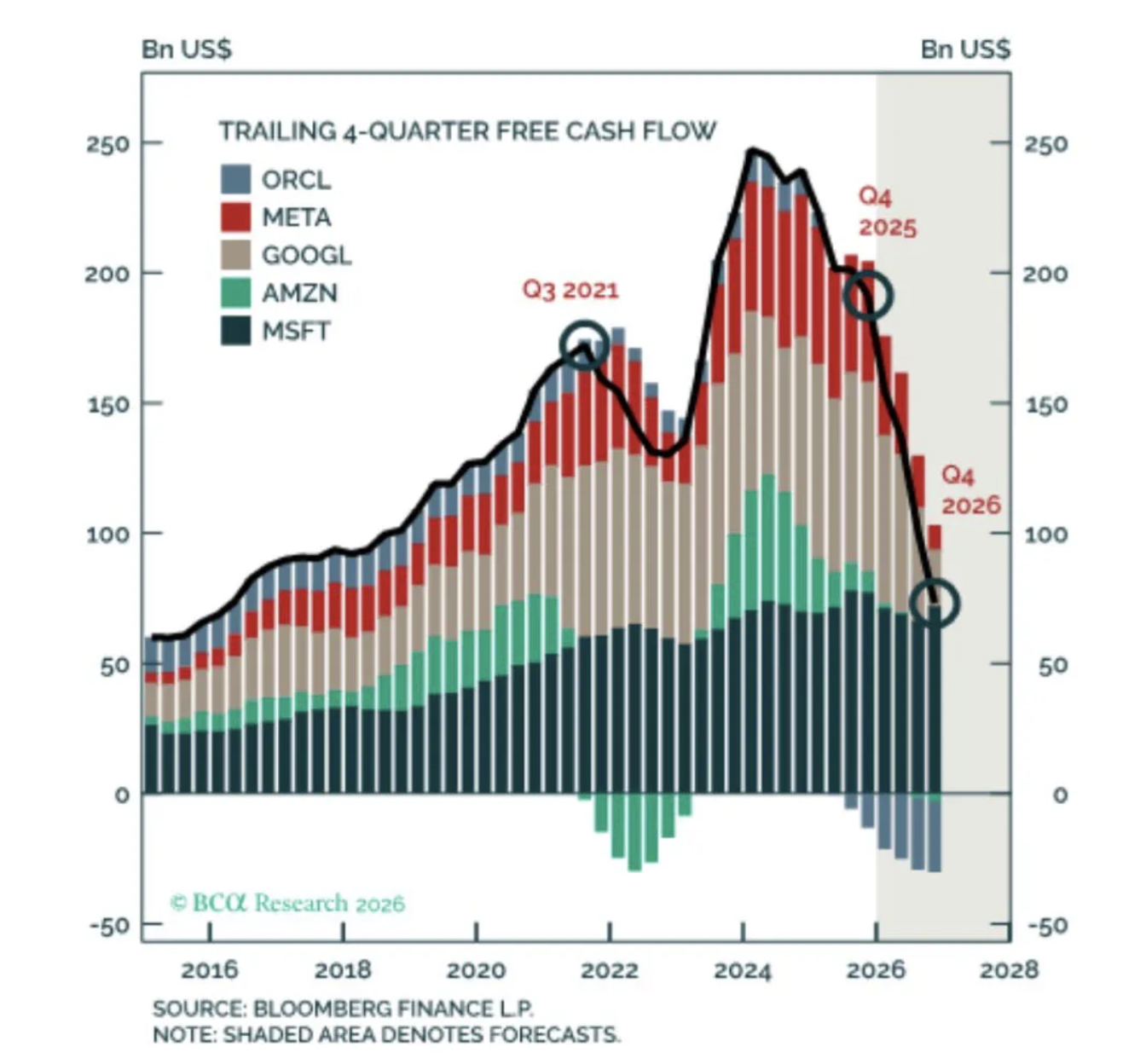

I’ve argued the Mag 7+ trade is over in terms of its market dominance and a key reason is that the free cash flow generating power of these businesses is shrinking because of the enormity of their Cap Ex. This was a great chart I found on X from BCA Research’s Peter Berezin.

With respect to whether international markets can continue to have their day, both absolutely and relative to the US, the key is whether they can take advantage of the moment and Make Their Economies Great Again. Specifically with Europe, when I saw this FT article last week headlined “EU Urged to Enact Regulation ‘Big Bang’,” I want to believe that it’s possible. The piece said “Europe needs a ‘big bang’ moment in which EU capitals set aside national interests and finally tackle the regulatory inertia that has left the continent trailing the US and China, the president of the European Council has said.”

“As he prepared to chair a crucial EU summit on competitiveness, Antonio Costa told the FT that Europe’s problems were as much down to the dead hand of national regulators as Brussels’ over-regulation. ‘We need to give a new political impetus. We need to do in 2026 on competitiveness what we have done last year on defense,’ the former Portuguese prime minister said, referring to agreements on increasing defense spending and pooling procurement.”

Europe, this is your chance. Don’t blow it. I continue to hold what I believe are cheap stocks there even after the rally.

The business model of online travel could certainly get disrupted. Expedia stock fell 20% over the past two weeks due to these fears and they said this of note in last week’s earnings call:

They are not impacted just yet. “In the fourth quarter, we exceeded our expectations, growing bookings and revenue by 11% and expanding our margins by four points. Booked room nights were up 9%, including high single digits in the US and low double digits in EMEA and the rest of the world.”

“Consumer spending remained healthy, with longer booking windows and lengths of stay relative to 2024.”

“Turning to our outlook. Our guidance reflects strong bookings momentum as we enter Q1, while remaining appropriately cautious given ongoing macro uncertainty.”

“as GenAI changes how travelers do trip discovery, it opens up new growth opportunities for us. We’re working with all the major platforms to capture traveler demand, ensuring our brands show up prominently in GenAI searches and function effectively with agentic browsers...I actually think that AI search opens up even more possibilities to reach more travelers.”

The next two businesses will not be impacted by GenAI but still have to manage the macro environment given to them and their own execution.

From Wendy’s, whose stock fell 8% on Thursday as McDonald’s talked about their success with McValue but rallied back by 3% on Friday after they released numbers:

“Starting with the fourth quarter, while results were in line with our expectations, we know that we have a lot of work to do to improve performance...As we shared on our last earnings call, we expected fourth quarter systemwide sales to be down significantly, and they were. Global systemwide sales declined 8.3%, driven by our US business, where marketing spend was down significantly as a result of front end loaded ad spending in 2025 and sales trends throughout the year.”

“The decline in US same restaurant sales was driven by a decrease in traffic, partially offset by a higher average check.”

On the inflation they see, “our outlook for labor inflation of approximately 4%, and a commodity cost increase of approximately 4%, reflecting the continued inflation in beef prices, as well as investments to improve the quality of our products, including upgraded chicken fillets and new buns.”

From Advanced Auto Parts, up 1% yesterday:

Comps were up 1.1% in Q4 but “top line momentum has lagged original expectations. Our pace of same store sales growth has been impacted in part by external factors that have resulted in a softer consumer spending environment.”

“Following a softer start to the quarter, transactions improved during the last 8 weeks, resulting in positive comparable sales growth over that timeframe.”

“Ticket was positive for the quarter and driven by a combination of better unit productivity and higher average selling prices...SKU inflation came in just under 3%. This was about 100 bps lighter than expected due to successful tariff related negotiations, which were still underway at the start of the quarter.”

“Looking at channel performance, our pro business grew by nearly 4% during the quarter, with sales strengthening throughout the quarter on both a one yr and two yr basis. Trends in DIY remain volatile, leading to a low single digit percent decline in comps. We believe this is largely a continuation of the market trends we have experienced all year. Our core consumer group has been adjusting purchasing habits in response to rising prices.”

UK jobs data and the German ZEW were the two economic figures of note overseas. Payrolls shrunk again in January in the UK for the 5th straight month, not helped by the Starmer/Reeves tax increases. However, down 11k was better than the estimate of -20k and December was revised up sharply to a loss of 6k vs the initial print of -43k. Jobless claims also rose in January. Also, in the 3 months ended December, the UK unemployment rate rose one tenth m/o/m to 5.2% which is the highest since January 2021.

After a 5-4 vote in the most recent BoE meeting, this likely sets them up for a rate cut at their next meeting and a classic case of monetary policy trying to bail out anti-growth fiscal policy. The UK 2 yr gilt yield is lower by almost 2 bps to 3.57% in response while the 10 yr is down by 3 bps to 4.37% as yields in the region fall as well. The British pound is slipping too vs the US dollar by almost .50%.

The February German ZEW investor expectations survey fell to 58.3 from 59.6 and that was 7 pts below the estimate. The Current Situation improved to -65.9 from -72.7 as expected but still well under zero. They said, “The ZEW Indicator remains stable. The German economy has entered a phase of recovery, albeit a fragile one. There are still considerable structural challenges, especially for industry and private investment.”

The move lower in European yields followed a nice rally/lower yields in JGB’s overnight and why US Treasury yields are down as well.

BY Doug Kass · Feb 17, 2026, 10:46 AM EST

With a cannabis rescheduling agreement likely very close I plan to move to medium-sized in (MSOS) on continued weakness.

BY Doug Kass · Feb 17, 2026, 10:32 AM EST

With S&P cash now -52 handles (and -56 handles from where we shorted Index calls a few minutes ago) - we are taking the quick profit.

We now have no Index positions on.

I would reshort strength.

BY Doug Kass · Feb 17, 2026, 10:02 AM EST

With S&P cash +4 handles I am shorting Index calls.

BY Doug Kass · Feb 17, 2026, 9:45 AM EST

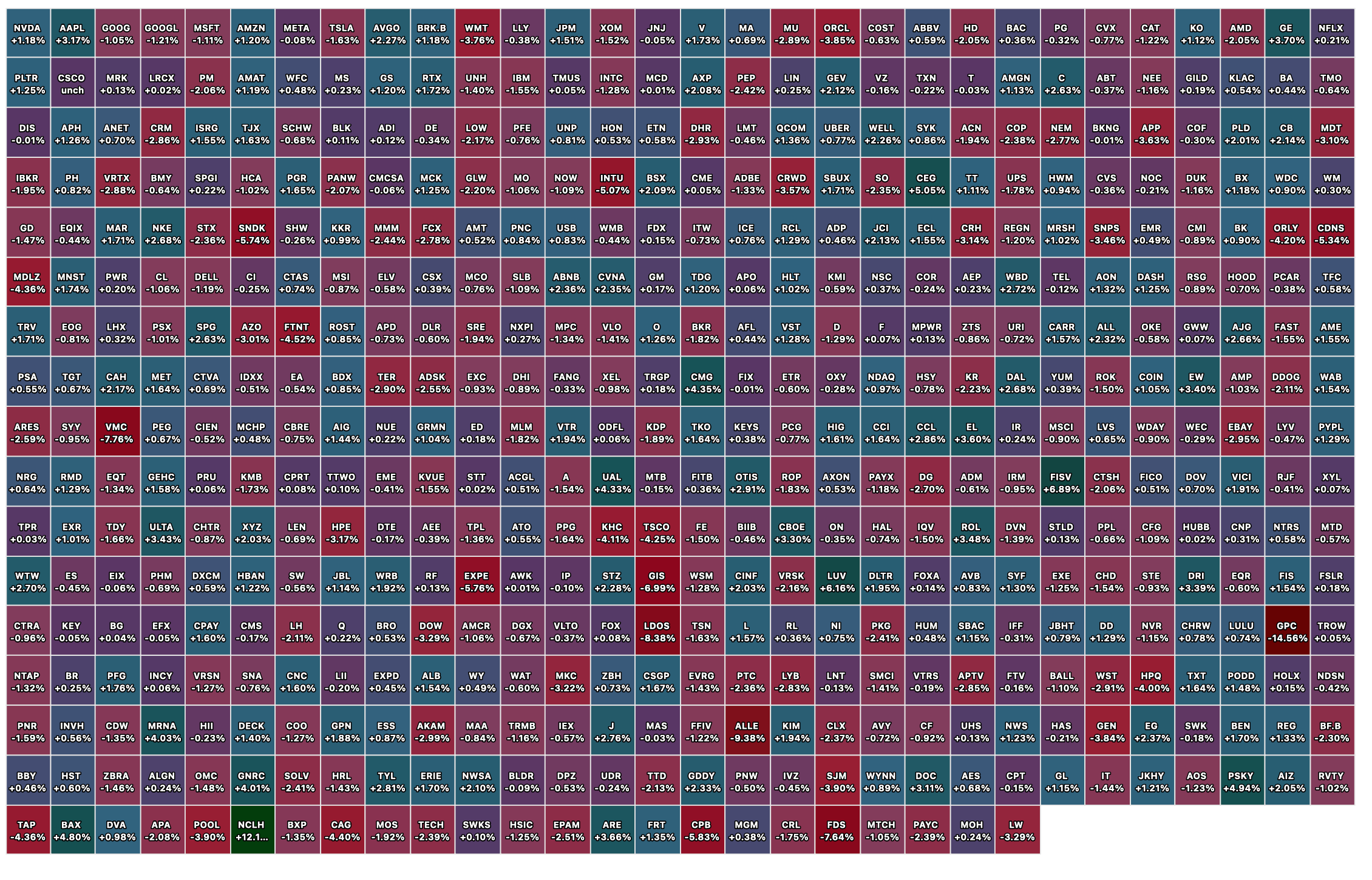

BY Doug Kass · Feb 17, 2026, 9:29 AM EST

BY Doug Kass · Feb 17, 2026, 9:25 AM EST

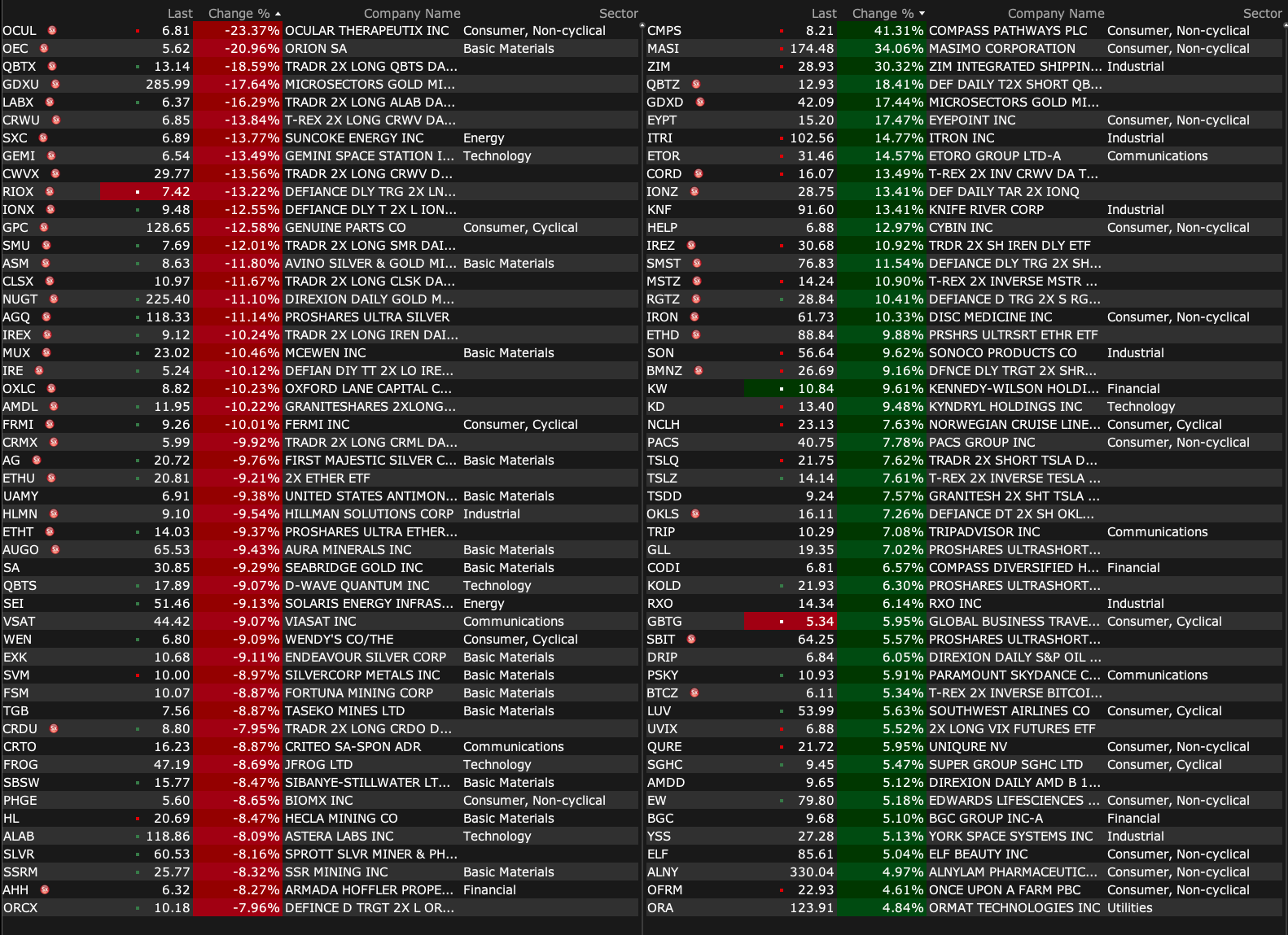

-MASI +36% (confirms to be acquired at $180/shr by Danaher)

-ZIM +35% (confirms to be acquired by Hapag-Lloyd at $35.00/shr in ~$4.2B cash deal)

-CMPS +25% (successfully Achieves Primary Endpoint in Second Phase 3 Trial Evaluating COMP360 Psilocybin for Treatment-Resistant Depression)

-KD +13% (files regulatory report following accounting review)

-ETOR +11% (earnings)

-KW +9.6% (to be acquired at $10.90/shr by consortium in all-cash deal)

-NCLH +6.1% (Activist holder Elliott said to have >10% stake)

-ITRI +4.1% (earnings, guidance)

-PSKY +3.9% (reportedly deal discussions will restart with WBD)

-AVAV +3.5% (JPMorgan Chase and Co Initiates AVAV with Overweight, price target: $320)

-FISV +3.2% (reportedly Activist Jana has built stake and supports CEO Mike Lyons)

-LH +2.8% (earnings, guidance)

-WBD +2.5% (David Faber: Expect Paramount to make final offer above $31.00/shr)

-OCUL -26% (reports results from Landmark SOL-1 Phase 3 Superiority Trial in Wet AMD)

-VMC -8.0% (earnings, guidance)

-DHR -6.0% (acquiring MASI for $180/shr)

-GPC -5.3% (earnings, guidance; confirms plans to separate into Global Automotive and Global Industrial)

-LITE -3.9% (hearing price target raised at Mizuho)

-GIS -3.4% (cuts FY26 guidance)

-MDT -2.5% (earnings, guidance)

BY Doug Kass · Feb 17, 2026, 9:10 AM EST

BY Doug Kass · Feb 17, 2026, 6:51 AM EST

BY Doug Kass · Feb 17, 2026, 6:41 AM EST

BY Doug Kass · Feb 17, 2026, 6:31 AM EST

Nothing to worry about here?

BY Doug Kass · Feb 17, 2026, 6:21 AM EST

BY Doug Kass · Feb 17, 2026, 6:13 AM EST

The S&P Short Range Oscillator got more overbought at 3.60% vs. 2.27%.

BY Doug Kass · Feb 17, 2026, 6:04 AM EST

Wolf Street on delinquency issues.

BY Doug Kass · Feb 17, 2026, 5:57 AM EST