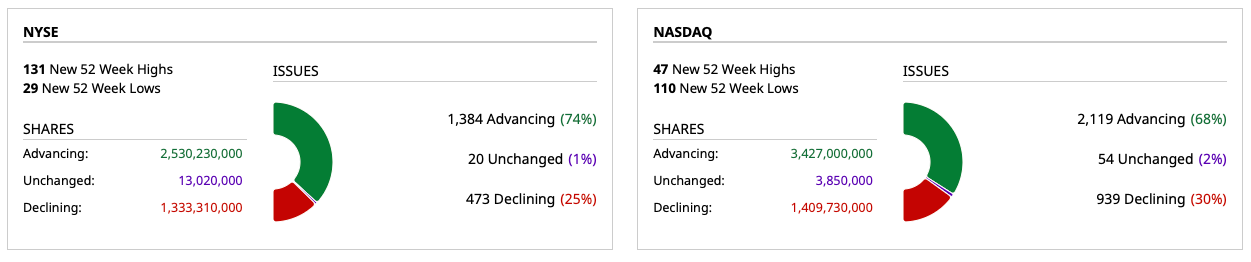

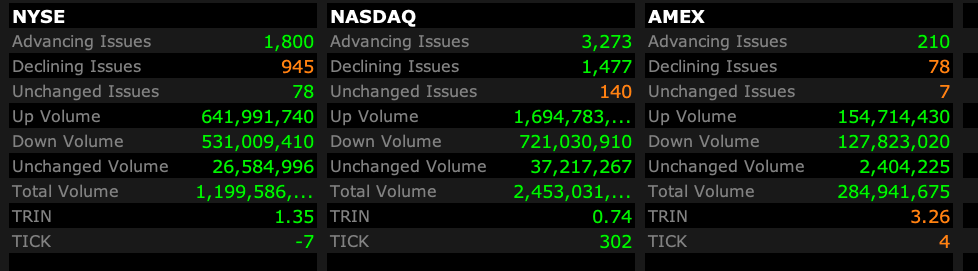

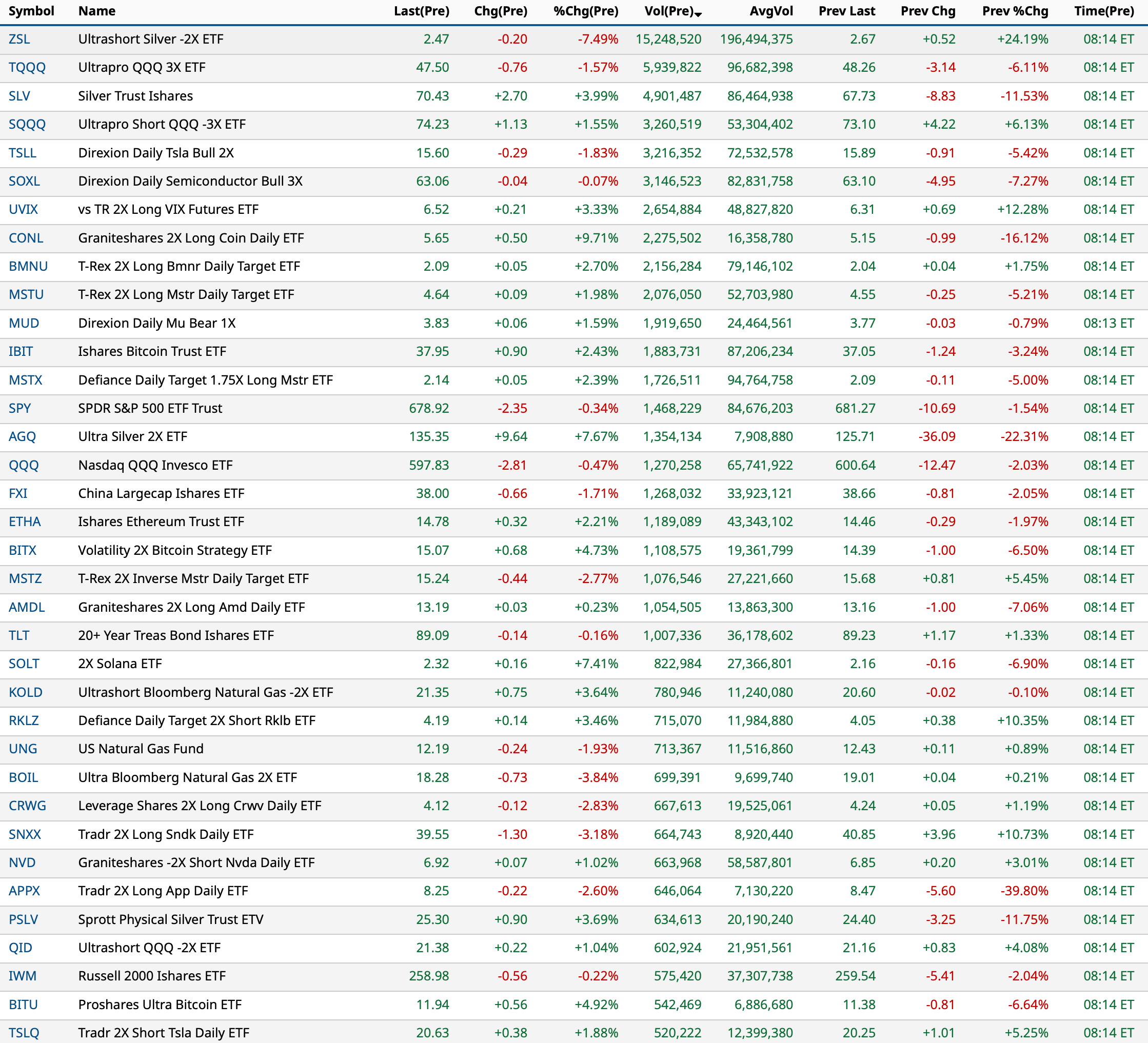

Friday's Closing Market Stats

Closing Breadth

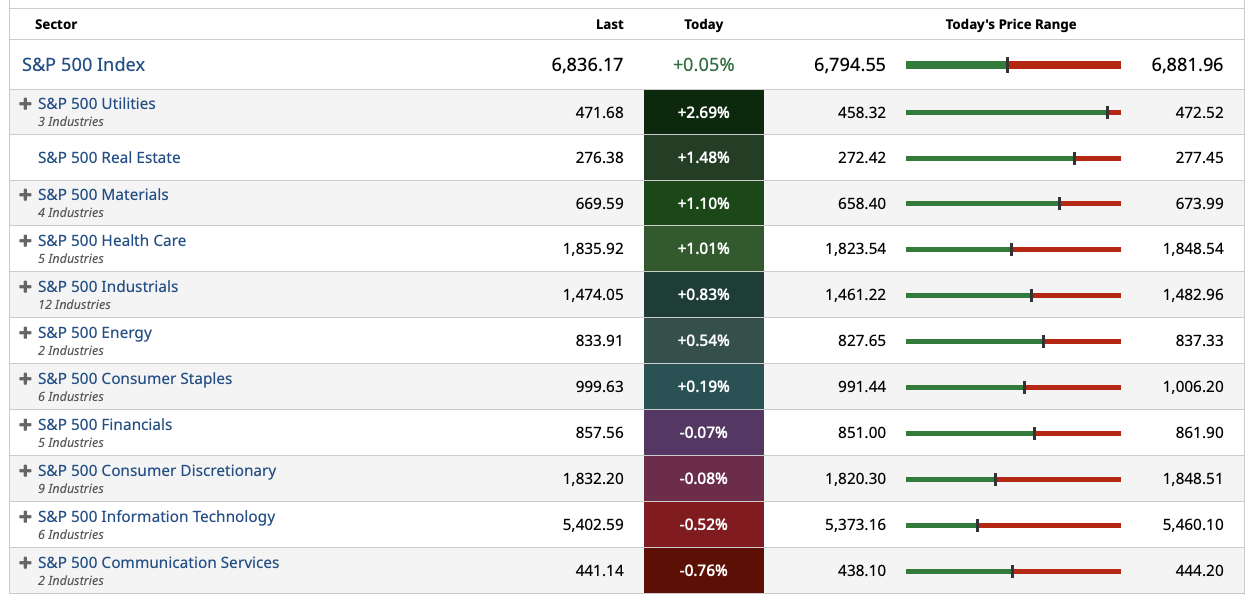

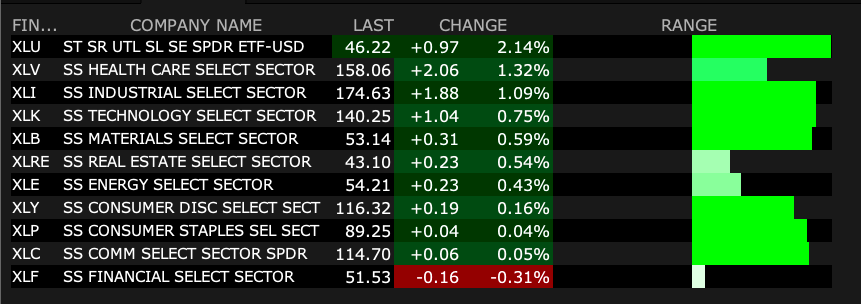

S&P 500 Sectors

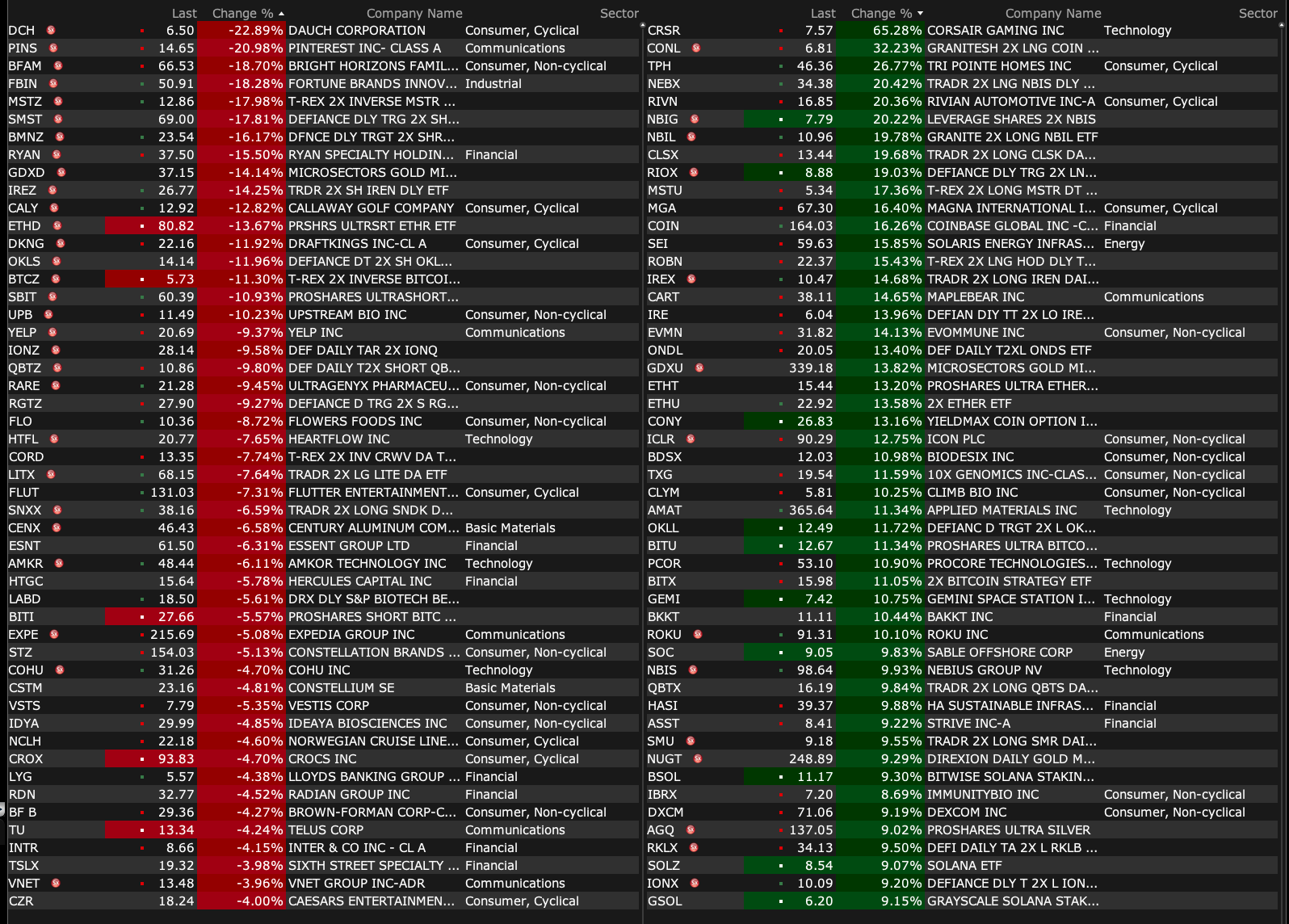

% Movers

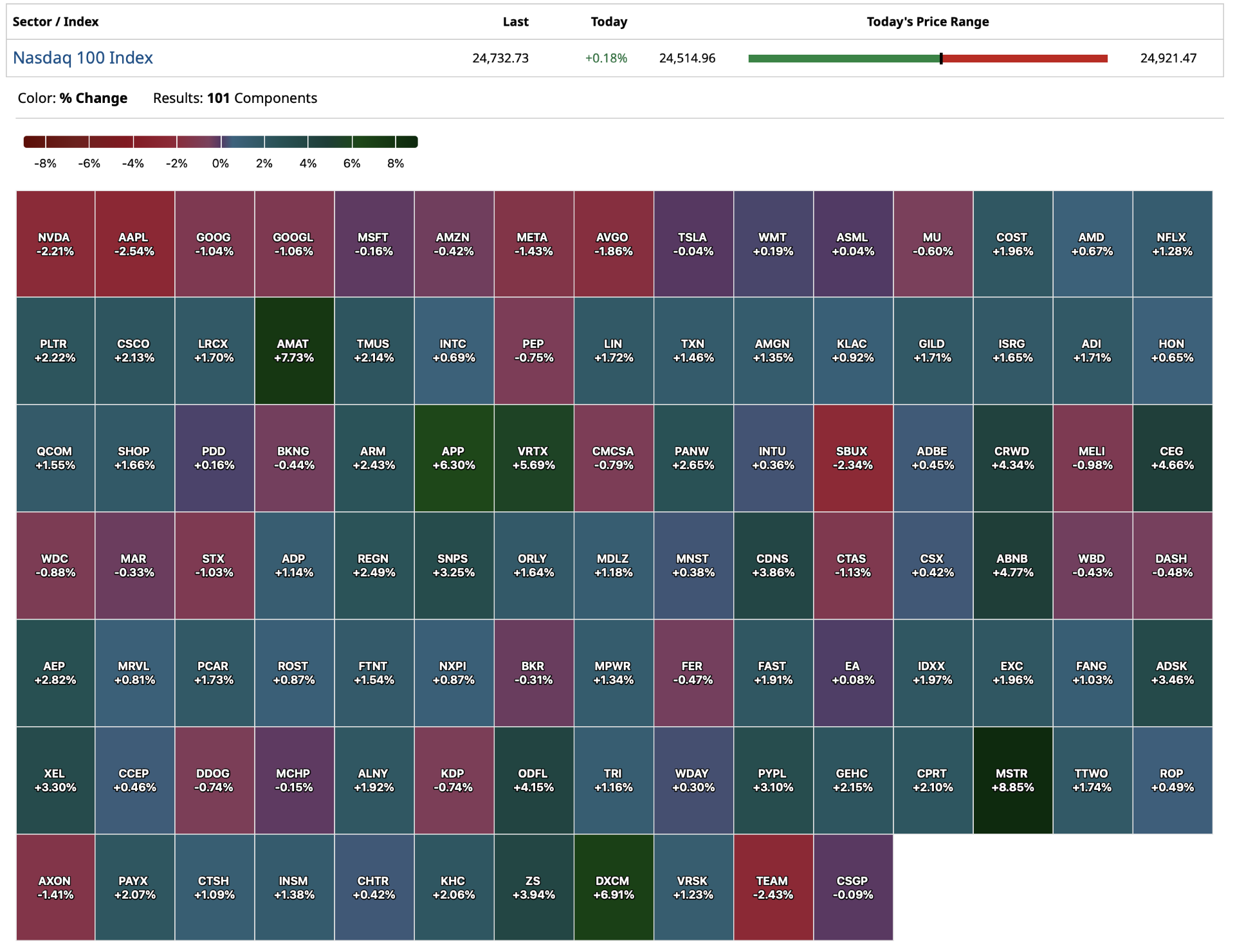

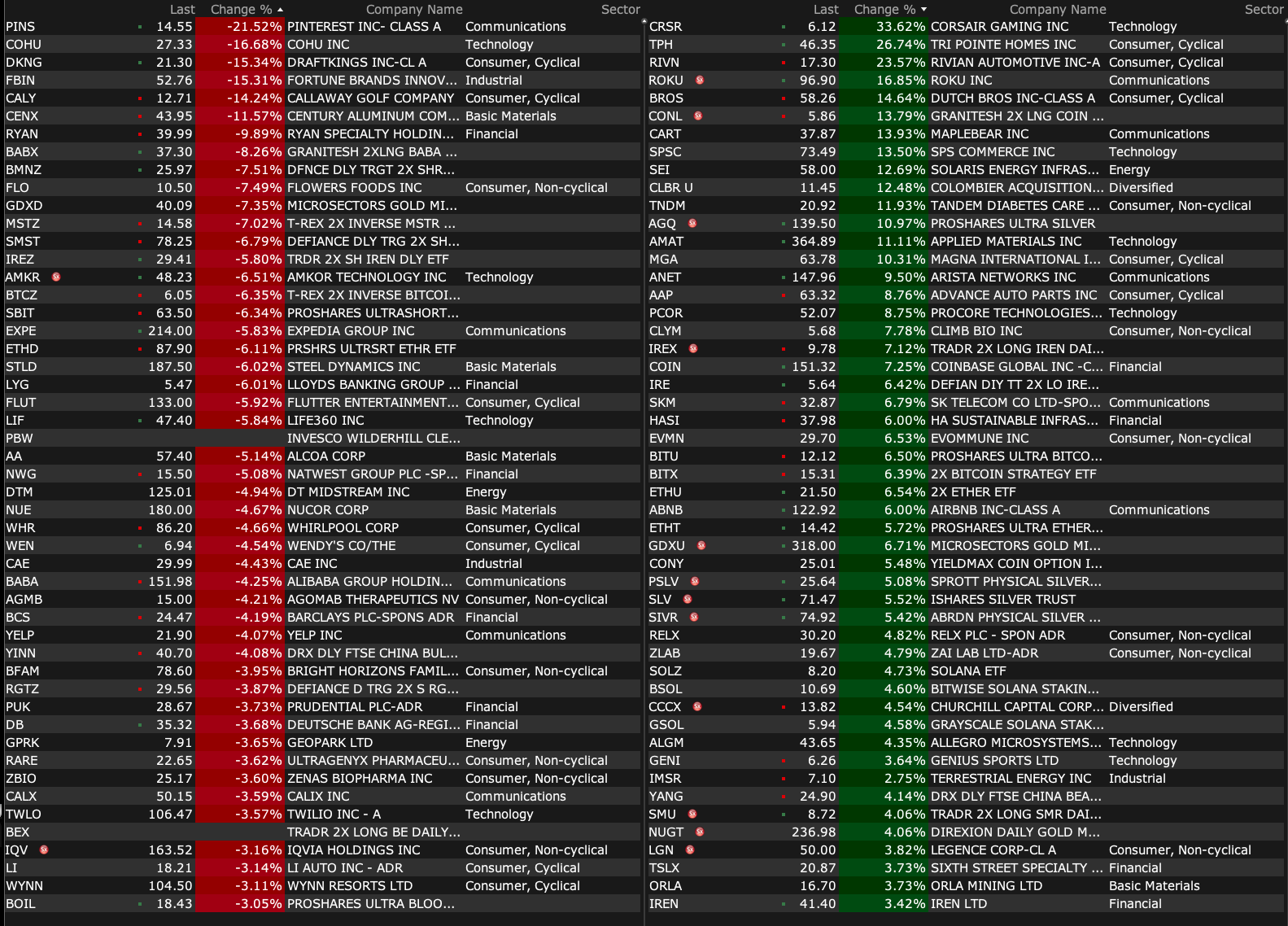

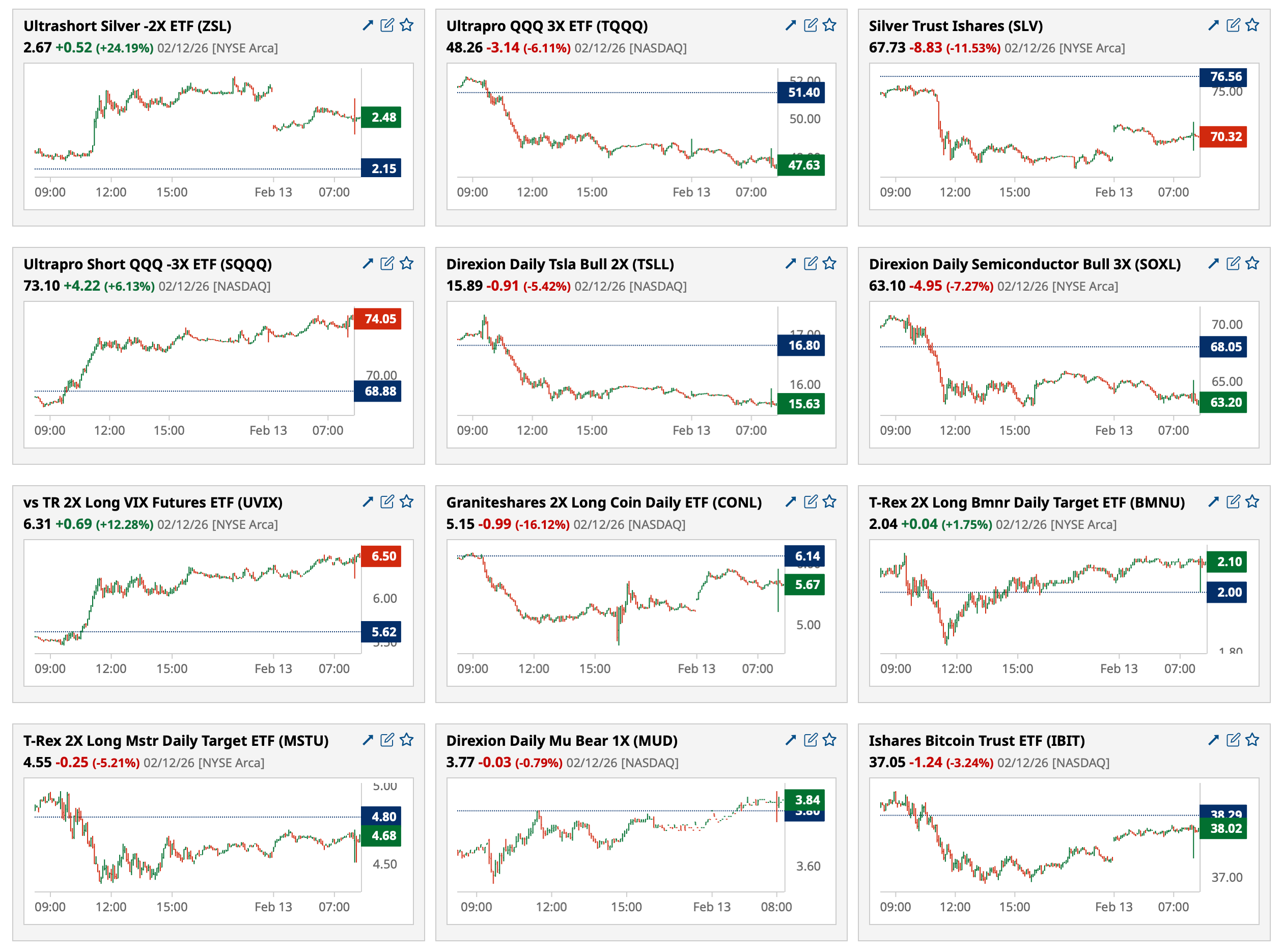

Nasdaq 100 Heat Map

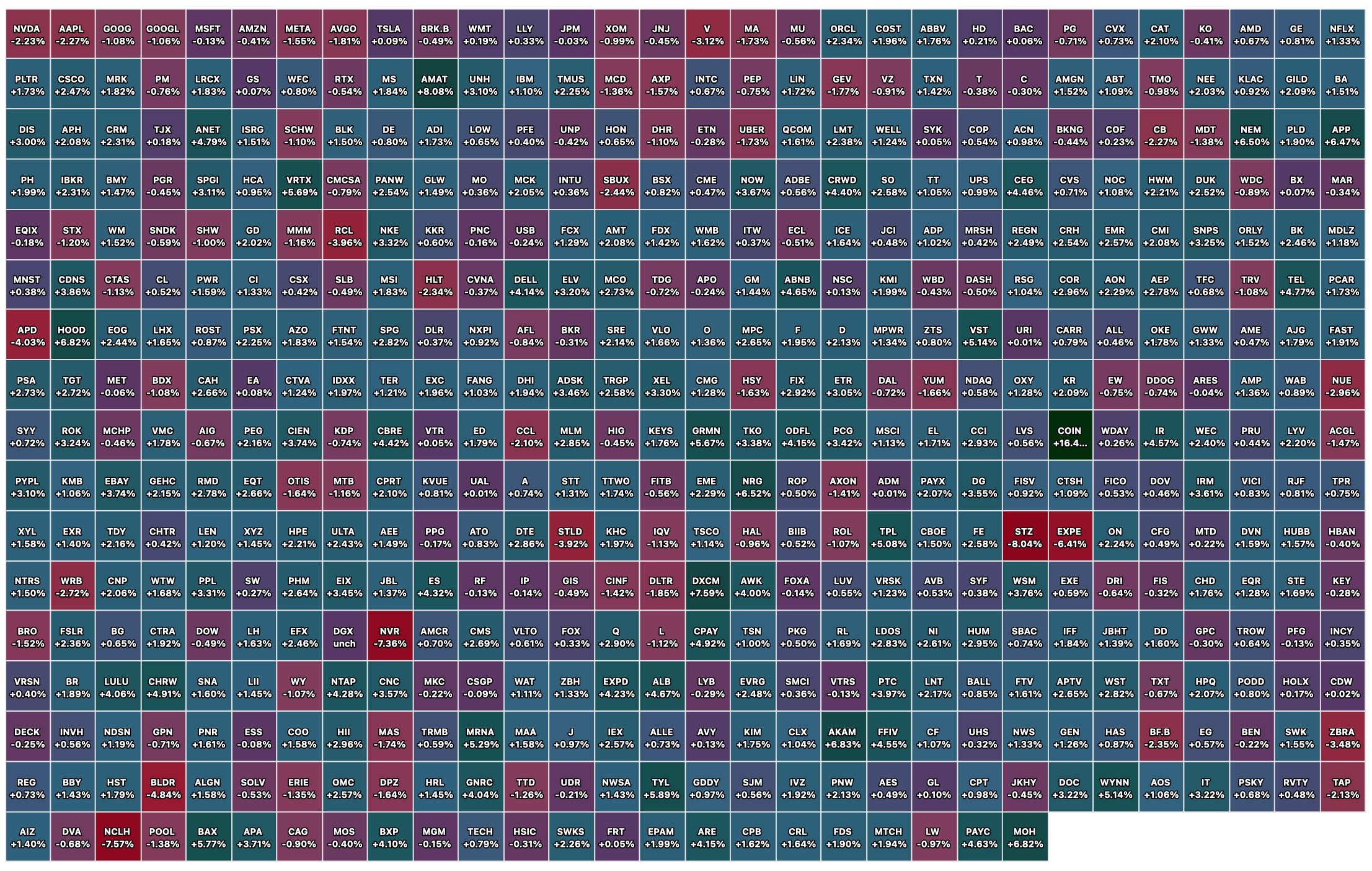

Closing S&P 500 Heat Map

BY Doug Kass · Feb 13, 2026, 4:27 PM EST

BY Doug Kass · Feb 13, 2026, 4:27 PM EST

maircampbell

Somebody help me with Apple. I read the news the other day about Siri not being ready, but this take out seems overdone to me? Thoughts? I'm trying to remember why Dougie hasn't liked Apple for a while, but I can't. Thanks

Dougie Kass

sluggish top and bottom line growth in last five years

expensive given above

it's been a capital allocation play, but net cash has been depleted

buyback is much less accretive to EPS after share price increase of the last few years - given sluggish top/bottom cagr,

berkshire will likely announce more sales

over owned

who is the marginal buyer?

Randy

Technically the charts are ugly on multiple time frames. Best to be hoped technically is that it is going through sideways consolidation. Worst is instead it has begun a downtrend in a tough market.

BY Doug Kass · Feb 13, 2026, 3:20 PM EST

I'm adding further to (MSOS) and (MSOX).

I would like to ultimately be medium sized on any further weakness — so, working as a scale buyer lower.

BY Doug Kass · Feb 13, 2026, 3:10 PM EST

With S&P cash +22 handles (and -20 handles from when, on average, I shorted index calls), I just took off my short Index calls — for a profit.

I have no index positions now.

BY Doug Kass · Feb 13, 2026, 3:00 PM EST

The S& P index has retreated from the highs (losing half the gains) — now up by only +!9 handles.

I am taking in my large-cap trading short rentals ( (TSLA) , (CAT) and (MU) ) for small gains — looking forward to a long weekend.

BY Doug Kass · Feb 13, 2026, 2:55 PM EST

I should never have covered my short...

BY Doug Kass · Feb 13, 2026, 2:26 PM EST

BY Doug Kass · Feb 13, 2026, 1:50 PM EST

I added to Tesla (TSLA) short at $420.20.

BY Doug Kass · Feb 13, 2026, 12:48 PM EST

Back short overbought (very high RSI) Micron (MU) at $416.13.

Not for home gamers, just being transparent.

BY Doug Kass · Feb 13, 2026, 12:35 PM EST

BY Doug Kass · Feb 13, 2026, 12:23 PM EST

With S&P cash +39 handles, I am back shorting index calls.

I am working on a scale, starting very small and adding into strength.

BY Doug Kass · Feb 13, 2026, 12:08 PM EST

Here are the today's things:

* Bought (SPY) and (QQQ) common in premarket (against short Index calls):

SPY $679.61

QQQ $599.05

* When regular trading commenced, I collapsed the long index common with the short index calls.

* Covered my speculative short basket from earlier in the week in the whoosh lower this morning.

* Covered some (GRNY) at $24.54.

* Covered some (JOET) at $42.08.

* Shorted (CAT) at $782.31.

* Added to (MSOS) at $3.92 and (MSOX) at $2.91 longs.

* Added to (NFLX) long at $76.04.

BY Doug Kass · Feb 13, 2026, 12:03 PM EST

Yesterday in the Comments Section Slamen1313 requested a list of longs and shorts in my hedge fund, Seabreeze Partners.

Here you go!

Longs: (MSOS) , (MSOX), (UNH) , (NKE) , (JOE) , (KMB) , (PG) , (PEP) , (NFLX)

Shorts: (CAT) , (CVNA) , (SNBR) , (TSLA) , (SGHC), (CHGG) , (RICK) , (MPTI) , (FXLV), (WOOF) , (RILY) , (JOET) , (GRNY)

(Note: This is not a complete list. It only includes equities I have previously disclosed.)

BY Doug Kass · Feb 13, 2026, 11:50 AM EST

Kernen interviews the Secretary of the Treasury Scott Bessent.

BY Doug Kass · Feb 13, 2026, 11:35 AM EST

(KMB) continues to trade well - up by about +10% off the lows I am holding on to my holdings.

BY Doug Kass · Feb 13, 2026, 11:08 AM EST

- NYSE volume 2% above its one-month average;

- Nasdaq volume 9% below its one-month average;

- VIX index: down 3.22% to 20.15

BY Doug Kass · Feb 13, 2026, 11:03 AM EST

Adding small to (MSOS) and (MSOX) (new position, leveraged MSOS) longs.

BY Doug Kass · Feb 13, 2026, 10:37 AM EST

From Peter Boockvar:

Headline consumer price inflation in January rose .2% m/o/m with a core rate higher by .3% vs expectations for .2% and .3% for each. Versus last year, gains were 2.4% and 2.5% respectively vs 2.7% and 2.6% in December. Lower energy prices of 1.5% m/o/m and flattish y/o/y helped to cap the headline print while food prices were up .2% and 2.8% y/o/y. Electricity prices in particular were down .1% m/o/m but still up 6.3% y/o/y because of you know why. Prices for ‘food at home’ were up .2% after a .7% monthly rise in December and are up 2.1% y/o/y but lagging the gains in ‘food away from home’ where prices were up 4% y/o/y and also .2% m/o/m.

Services inflation ex energy continues to be where most of the inflation is with prices rising .4% m/o/m and 2.9% y/o/y. Owners Equivalent Rent moderated to a .2% m/o/m gain and to 3.3% y/o/y and Rent of Primary Residence was up .2% m/o/m and 2.8% y/o/y (both getting closer to reality on a blended basis). Medical care costs continued their steady rise, up .3% m/o/m and 3.2% y/o/y. However, the price of health insurance fell 1% m/o/m and 2.2% y/o/y. That is NOT reality. Motor vehicle insurance costs fell by .4% m/o/m after the BLS left out the December print. They are now little changed y/o/y on tough comparisons. Fixing a vehicle is still costly, up 4.9% y/o/y and up one tenth m/o/m. As capacity has been right sized in the airline industry, airfare fares jumped by 6.5% m/o/m and by 2.2% y/o/y. That was offset though by.a .5% drop in hotel prices and lower by 3.2% y/o/y.

Core goods prices were flat m/o/m while up 1.1% y/o/y. Lower used car prices of 1.8% m/o/m was a key reason (though will likely reverse higher soon based on what Manheim is saying). New car prices were little changed, up .1% m/o/m and .4% y/o/y. Apparel prices rose .3% m/o/m and 1.7% y/o/y. Thanks to tariffs, the cost of household furnishing and supplies continue higher, up by .3% m/o/m and 3.8% y/o/y led by a jump in applicance prices.

Bottom line, CPI is now up 26% since February 2020 as the US consumer deals with the level rather than rate of change in this figure and why we know there is such a differential in the finances of the US consumer. As what this means for the Fed, it all depends on what one thinks about what the right REAL rate should be. According to the median dot plot, the long run REAL rate should be 1%. Well, with the fed funds rate currently at about 3.65%, one cut would essentially take us there if one uses CPI, and maybe two if PCE is their thing which we know it is. And that is what the bond market is pricing in, along with a 40% chance of a 3rd cut which theoretically would assume a further deceleration of inflation and/or the belief in a lower REAL rate because the labor market is weak.

BY Doug Kass · Feb 13, 2026, 10:10 AM EST

With S&P cash -37 handles I am taking off my speculative basket (short), which included high-beta names such as (MU) and (CAT) - for a quick and good profit.

BY Doug Kass · Feb 13, 2026, 9:47 AM EST

* As free cash flow is plummeting...

I decided to ask the AI about itself.

In this case, I asked Google Gemini about Google’s financials.

Below is the question, and then the response.

I guess not half bad, but not half bad can be very misleading and very wrong.

Specifically with regard to Gemini’s answer about the depreciation drag on earnings per share, a full and correct answer would include the notion that if the company keeps spending the $175 billion-$185 billion in capital expenditures over the four-to-six year depreciation period, it will have $175 billion-$185 billion of annual depreciation.

A full and correct answer would also include the notion that the four-to-six year depreciation period is controversial and a fair bit of CAPEX may depreciate more quickly in practical economic real use and value terms. A reasonably thoughtful human would then think through what this means for future earnings and then also cash flow, and other related things like the ability to buy back stock.

For what it's worth, Google’s earnings before interest, taxes, depreciation, and amortization in Q4 was about $42 billion. Run rate quarterly CAPEX for next year is $45 billion. Seems to be there is a good chance it turns into a no or negative cash flow business depending on a few things, which is probably why the company just went to market with a $32 billion 100-year bond offering, which Gemini should have also mentioned, but needed to be prompted to do so because it is unable to think through the logical implications of all the CAPEX on its own:

I said:

Last quarter google had $6 billion of depreciation and guided to $175 billion-$185 billion of CAPEX for 2026. what does this mean for Google's future reported earnings?

Gemini said:

That $175 billion–$185 billion figure is a massive escalation—it’s essentially Google "doubling down" on the AI arms race. For context, they spent roughly $91 billion in 2025, so they are planning to nearly double their capital intensity in a single year.

While CAPEX (Capital Expenditure) doesn't hit the income statement all at once, it creates a "depreciation tail" that will weigh on reported earnings for years to come. Here is the breakdown of what this means for Google's financial future:

1. The "Depreciation Drag" on EPS

When Google buys a $40,000 H100 GPU or builds a $2 billion data center, that cost is spread out over its useful life (typically 4–6 years for servers).

2. Operating Margin Squeeze

Google’s operating margins have been healthy (low 30s), but the 2026 guidance suggests a period of "digestion."

3. Free Cash Flow (FCF) vs. Reported Earnings

This is where the real "pain" is felt.

4. The "ROI" Clock is Ticking

The market’s negative reaction to this guidance (the stock dropped ~7% post-earnings) signals that investors are moving from "AI excitement" to "AI accountability."

I said:

Why did Google just sell debt?

Gemini said:

Alphabet (Google) just executed a massive $32 billion debt sale (the largest in its history) on February 9-10, 2026, for several strategic reasons that align perfectly with that aggressive $175 billion–$185 billion CAPEX guidance you mentioned.

Here is why they are tapping the debt markets now:

1. The "AI Arms Race" Cash Gap

While Google is a "cash cow," its 2026 spending plan ($175 billion+) is so large that it is expected to outpace its organic cash generation.

2. Financing $37 Billion in Acquisitions

In their Q4 earnings report, Google confirmed they expect to close two major acquisitions in 2026: Wiz and Intersect, for a combined $37 billion.

3. The "Century Bond" (A Bold Financial Flex)

One of the most talked-about parts of this debt sale was a 100-year "century bond" issued in British Pounds (Sterling).

BY Doug Kass · Feb 13, 2026, 9:45 AM EST

BofA analyst Shaun Kelley lowered the firm's price target on DraftKings to $30 from $37.50 and keeps a Neutral rating on the shares after the company reported Q4 revenue below expectations and gave revenue guidance of $6.5B-$6.9B, which implies 7%-14% growth and is below the firm's estimate of $7.0B and the Street's $7.3B. While the guidance is likely conservative, it's also low enough to reinforce concerns on prediction market cannibalization, the analyst tells investors.

BY Doug Kass · Feb 13, 2026, 9:33 AM EST

From Peter Boockvar:

My ability to comment on CPI at 8:30am est will depend on my WiFi connection on my flight.

Aluminum prices are down about 1% in London on the story that the Administration is looking into pulling back on the wide breadth of its tariffs on aluminum and steel and the derivative use of them in packaging, parts, etc... due to the major disruptions the tariffs have caused. Another realization that a more narrow use of tariffs is the better way to go rather than the scattershot path, especially for things we don’t make here and never will.

Because he’s a known hawk, the 2 yr JGB yield and the yen are not responding but Naoki Tamura, a BoJ member, said today in so many words that he wants to raise rates again soon. “It is quite possible that, as early as this spring, the price stability target of 2% can be judged to have been achieved if it’s confirmed with a high certainty that wage growth this year will be in line with the target for the third consecutive year.”

I give him credit for pushing back on the idea that 2%+ inflation should be considered price stability as he said “many households are struggling with the increased cost of living, and many firms are struggling with higher input prices, and I personally do not think it can be claimed that Japan is experiencing price stability as defined.”

We can continue to point to a continued fall in home prices in China in weighing down on the mood of the Chinese consumer from a wealth perspective. Both new and existing home prices fell again in January with the former down 3.3% y/o/y and the latter lower by 6.2%, though the m/o/m decline moderated from the prior month. Shanghai was the only tier 1 city that saw a new home price gain. After contracting for years now, at some point home prices will stop going down and that is when there will be an all clear on the Chinese consumer because of the massive level of personal savings they have accumulated outside of the real estate they own.

Nothing like live entertainment and AI won’t replace that. Sphere Entertainmentstock was up 22% yesterday. They said this of note and it’s not just concerts:

“the Wizard of Oz at Sphere has been both a critical and commercial success, with over 2.2 million tickets now sold and approximately $290 million in ticket sales.”

“we also saw revenue growth in concert residencies and exosphere advertising and sponsorship.”

Wynn Resorts is trading down pre-market because of its Macau results and said this:

“Demand for our product in Las Vegas remained healthy across the board with drop, handle, and ADR all up y/o/y. While RevPAR was slightly below last year, the overall results reflect our ability to balance stronger ADRs with modestly lower occupancy in order to optimize the performance of the building.”

“More recently, demand in Boston has remained healthy into February aside from specific days impacted by poor weather.”

“Shifting to Macau. This quarter was all about significant volume growht but unusually low hold in both VIP and mass...Momentum in Macau has persisted into the first quarter with volumes in January just above those we saw in Q4.”

From Hermes, which rallied by 2.5%:

To this question, “What is your perspective on demand around the world because we see that the middle class is not showing up as much in this aspirational client base?

“Hermes has got a large number of clients all around the world and we have a lot of people in the middle class that can afford Hermes products. If we didn’t serve the middle class, we would only have 15 stores around the world...So when we set up in a country is because we believe that there’s a middle class that can afford and wants our products. Now we set up these stores in areas where we had aspirational clients, not always middle class by the way,”

“We have people in the middle class that shop in our stores and buy our products. So the middle class is not struggling all around the world...And then in the United States, we have a very broad customer base, which allowed us to have this plus 18%.”

From US Foods, benefiting from the staples trade, good numbers and jumped 11%:

Good numbers came in spite “a softer macro environment.”

“Let’s turn to broader industry trends. Chain restaurant foot traffic, as published by BlackBox, was down 2.8% for the fourth quarter, and decelerated 230 bps from the third quarter. Our chain business was down approximately 3.4%. Headwinds from the government shutdown, winter storms in December, and a challenged lower income and younger demographic affected industry demand. We were not immune to these events as they impacted the volume acceleration we were seeing coming out of the third quarter.”

“Our 2026 case growth was strong in January until the widespread storms and weather related closures at the end of the month and beginning of February.”

From Restaurant Brands, the owner of Burger King, Popeyes, and Tim Horton’s and was down by 6% yesterday:

With Tim Horton’s, “We started the year amid macro uncertainty and weaker consumer sentiment in Canada. Yet Tim’s delivered solid performance...with comparable sales in Canada growing 2.8%, outperforming the broader Canadian QSR industry by nearly two points.”

Burger King grew comps by 2.6% in Q4 and seemed to have gained some market share while Popeye’s was down 3.2% for the year.

“Burger King US saw approximately 7% commodity inflation in 2025 , largely due to beef, which increased over 20% for the full year.”

From Anheuser, up 4% yesterday:

“While near-term demand across many CPG categories was impacted by a constrained consumer environment and unseasonable weather, we continue to invest in our stragegic priorities.”

“Our megabrands and premium portfolio grew ahead of our overall business. The growth of our Beyond Beer and non-alcohol beer portfolios accelerated.”

In the US, “While industry volumes were below trend in 2025, we are encouraged by the start to 2026, Beer industry volumes and revenues grew in January and later this year.”

From Mohawk Industries, the maker of carpet and other flooring products:

“Across our markets, commercial demand remained stable, though continued weakness in housing turnover and sluggish new home construction in the US impacted our volume.”

“The fourth quarter reflected a continuation of macroeconomic factors our industry has faced since the second half of 2022. With weak consumer confidence, many large discretionary investments such as home renovations continue to be postponed. Housing turnover in our major regions remains at historical lows due to affordability challenges and economic uncertainty. While 2025 US existing home sales did not improve, sales in December increased over the prior year.”

Applied Materials is up sharply pre market and they said this:

“Our strong performance and outlook for 2026 and beyond are fueled by the acceleration of investments in AI computing.”

“The race to build out AI infrastructure is driving unprecedented spending on semiconductors, semiconductor manufacturing capacity, and research and development.”

BY Doug Kass · Feb 13, 2026, 9:20 AM EST

-TPH +27% (to be acquired by Sumitomo Forestry at $47.00/shr in $4.5B deal)

-IMUX +26% (oversubscribed private placement of up to $400M to accelerate commercial transition; funding to complete phase 3 ENSURE trials in relapsing MS)

-RIVN +22% (earnings, guidance)

-ROKU +15% (earnings, guidance)

-BROS +14% (earnings, guidance)

-SPSC +13% (earnings, guidance)

-CART +12% (earnings, guidance)

-MGA +12% (earnings, guidance)

-AMAT +11% (earnings, guidance)

-AAP +9.4% (earnings, guidance)

-PCOR +8.8% (earnings, guidance)

-ANET +7.9% (earnings, guidance)

-ABNB +5.8% (earnings, guidance)

-COIN +5.0% (earnings, guidance)

-IR +4.3% (earnings, guidance)

-EBS +2.3% (receives U.S. FDA Approval for NARCAN Nasal Spray Multipacks sNDA)

-PINS -21% (earnings, guidance)

-COHU -18% (earnings, guidance)

-FBIN -16% (earnings, guidance)

-DKNG -15% (earnings, guidance)

-BIO -14% (earnings, guidance)

-CALY -14% (earnings, guidance)

-OKYO -6.9% (prices 10.8M shares at $1.85/share)

-EXPE -6.8% (earnings, guidance)

-BABA -5.5% (US expected to add Alibaba and other to list of firms allegedly aiding China's military as soon as Friday, Feb 13th)

-WEN -5.5% (earnings, guidance)

-YELP -4.3% (earnings, guidance)

-KALU -2.6% (speculation President Trump could lower steel tariffs)

-WYNN -2.5% (earnings, color)

-VALE -2.3% (earnings)

BY Doug Kass · Feb 13, 2026, 9:10 AM EST

BY Doug Kass · Feb 13, 2026, 8:55 AM EST

BY Doug Kass · Feb 13, 2026, 8:41 AM EST

BY Doug Kass · Feb 13, 2026, 8:22 AM EST

Good sale of Amazon (AMZN) nine days ago at $237+:

At $237.14 I have sold the balance of my (AMZN) long.

Position: none.

By Doug Kass Feb 4, 2026 10:55 AM EST

BY Doug Kass · Feb 13, 2026, 8:00 AM EST

* We had sold our DKNG last June at about $40/share (last sale $21!)

* Another bet gone bad...

DraftKings (DKNG) gave disappointing guidance — and its shares got schmeissed in late Thursday trading, falling by -$4/share (or -14%) to a new 52-week low:

Half of the male population between 18 and 50 have a sports betting account. Nearly one quarter of the sports bettors say they are addicted. And one in five persons with a gambling addiction attempt suicide. Wagering on the next Federal Reserve Chairman, Pres. Trump's next tweet, whether the next pitch is a strike or a ball (or how many home runs NY Yankee Aaron Judge will hit, who will score the first Super Bowl point, etc.), invites corruption into every aspect of American life.

More professional teams and college teams are embroiled in "fixes." The shares of Robinhood (HOOD) , Caesars (CZR) , Flutter (FLUT) , MGM Resorts (MGM) , Draft Kings (DKNG) and other companies involved in gambling and predictive markets fall in half — as regulatory authorities begin to place new restrictions on the space.

- Doug Kass My 10 Surprises of 2026

BY Doug Kass · Feb 13, 2026, 7:45 AM EST

* Bill Ackman buys (META) shares before reading the company's 10-K

Bill Ackman reveals stake in Meta, says it has 'deeply discounted valuation'

From Kakashii:

BY Doug Kass · Feb 13, 2026, 7:30 AM EST

From earlier in the week:

(GRNY)'s constituent holdings are among the highest octane/beta stocks.

In an overbought market this portfolio is what I want to short.

I have moved to large sized today in this exchange-traded fund.

Position: Short GRNY L

By Doug Kass Feb 11, 2026 10:05 AM EST

BY Doug Kass · Feb 13, 2026, 7:15 AM EST

BY Doug Kass · Feb 13, 2026, 7:05 AM EST

BY Doug Kass · Feb 13, 2026, 6:55 AM EST

* And another Surprise (of my 10 Surprises for 2026) might become realized — even sooner than expected...

From Gary Marcus:

Breaking: OpenAI is probably toast

From my 10 Surprises for 2026:

The AI bubble bursts as the circular financing deals unwind (or are pushed out) — AI capital spending slows abruptly as return on investment concerns emerge as power generation and grid modernization are bottlenecks. Depreciation charges and lower demand wrecks havoc with consensus AI 2026-27 earnings per share expectations. Another big AI surprise would be if China decides to flood markets with inexpensive AI models — pressuring the ultimate and expected robust ROI forecasts (which are already in question by some skeptics).

OpenAI's Sam Altman finds a place to live right next door to Sam Bankman-Fried. His effort to make OpenAI too big to fail, fails. ChatGPT turns out to at best be a commodity large language model purveyor. It becomes obvious to all that its recent $500 billion-plus valuation can’t be supported. Without an ability to do a down round without losing face, OpenAI loses all access to capital. Ultimately, a consortium of its customers and suppliers takes it over to modify its business plan and reduce the cash burn.

With Altman tossed to the curb (or worse), the prosecutions begin.

OpenAI’s problems pushes a deeply committed (to OpenAI) Softbank to the verge of collapse.

Nvidia shares fall by -40% as CoreWeave (CRWV) is driven into bankruptcy.

A basket of defensive consumer nondurable equities ( (PEP) , (KO) , (PG) and (KMB) ) materially outperform the Mag 7 by a decisive amount.

The shares of (boring and previously hapless) PepsiCo outperform most other staples and 90% of the S&P Index after a much better skein of organic unit growth and as its core business is rationalized.

BY Doug Kass · Feb 13, 2026, 6:45 AM EST

What, me worry?....

BY Doug Kass · Feb 13, 2026, 6:35 AM EST

BY Doug Kass · Feb 13, 2026, 6:25 AM EST

Nothing could possibly go wrong here:

BY Doug Kass · Feb 13, 2026, 6:15 AM EST

and...

US commercial real estate and the financial sector: the year of truth? - Flossbach von Storch RI

BY Doug Kass · Feb 13, 2026, 6:05 AM EST

I closed out the balance of my index shorts in the whoosh lower late yesterday afternoon, at the close of trading:

Dougie Kass

I covered my Index call shorts at the close of trading today.

BY Doug Kass · Feb 13, 2026, 5:55 AM EST

The S&P Short Range Oscillator remains in overbought — at 2.27% vs. 3.50%.

BY Doug Kass · Feb 13, 2026, 5:45 AM EST