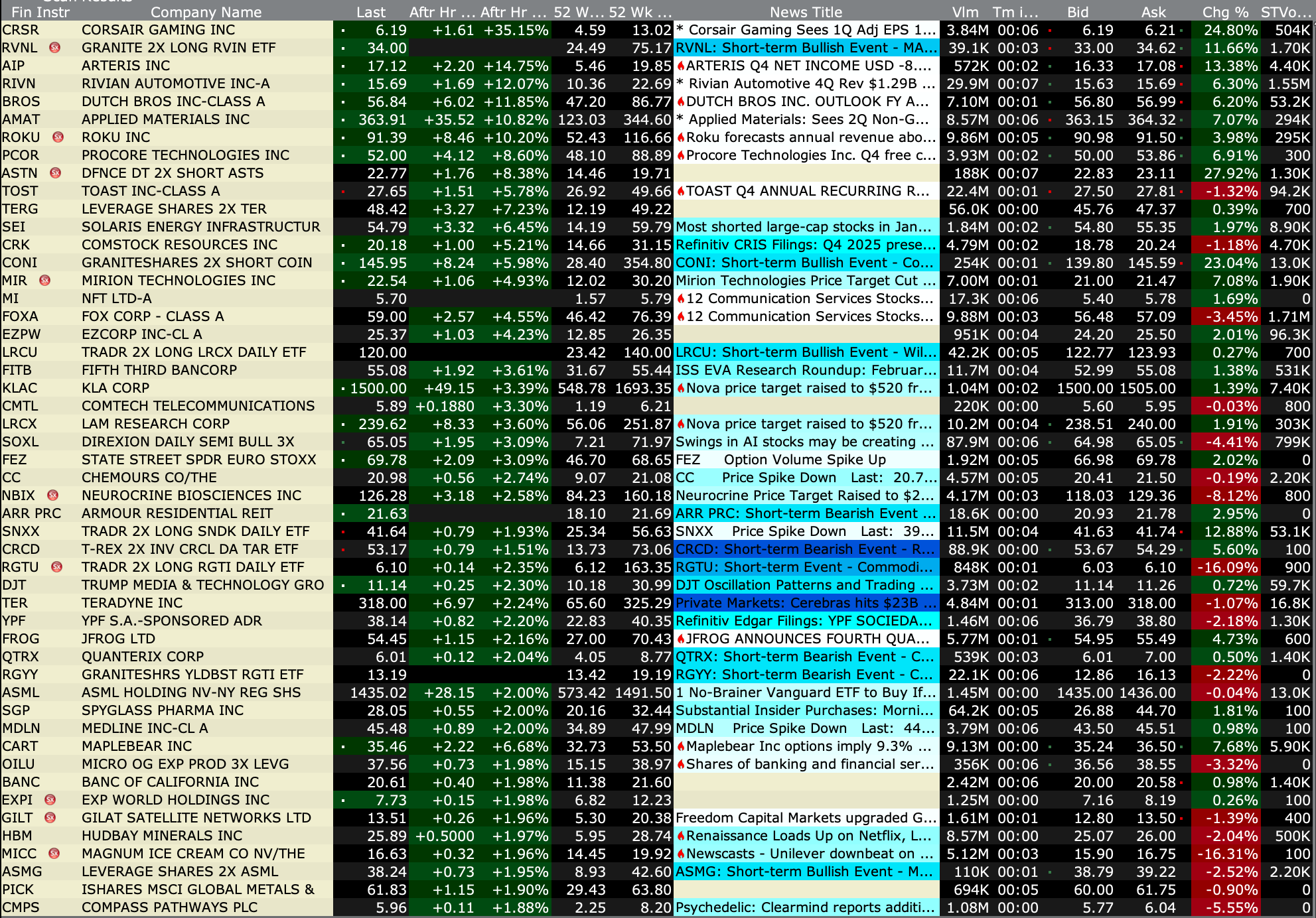

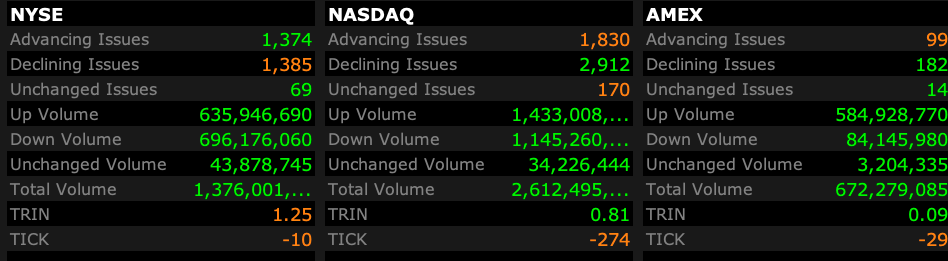

After-Hours Advancers and Decliners

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Feb 12, 2026, 4:35 PM EST

BY Doug Kass · Feb 12, 2026, 4:35 PM EST

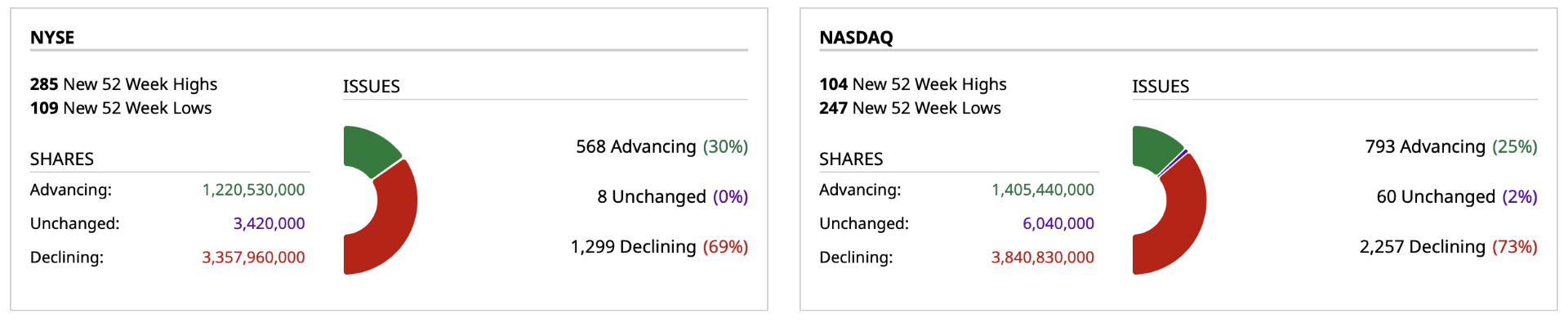

- NYSE volume 30% above its one-month average;

- NASDAQ volume 4% below its one-month average;

- VIX index: up 18.30% to 20.88

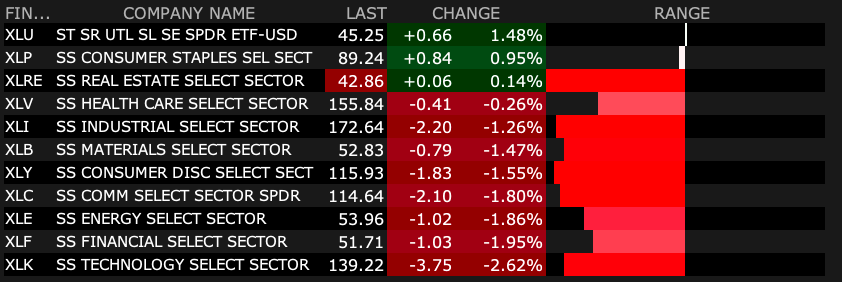

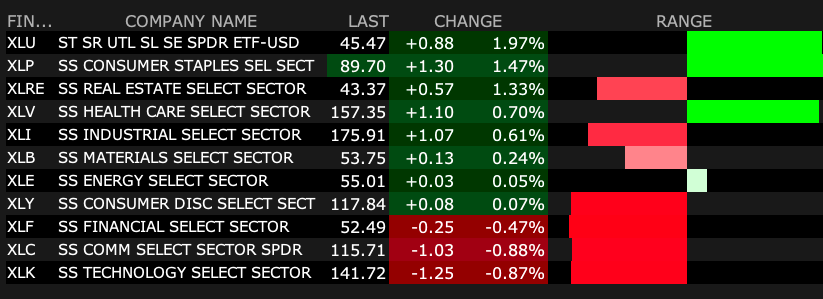

S&P 500 Sector ETFs

BY Doug Kass · Feb 12, 2026, 4:16 PM EST

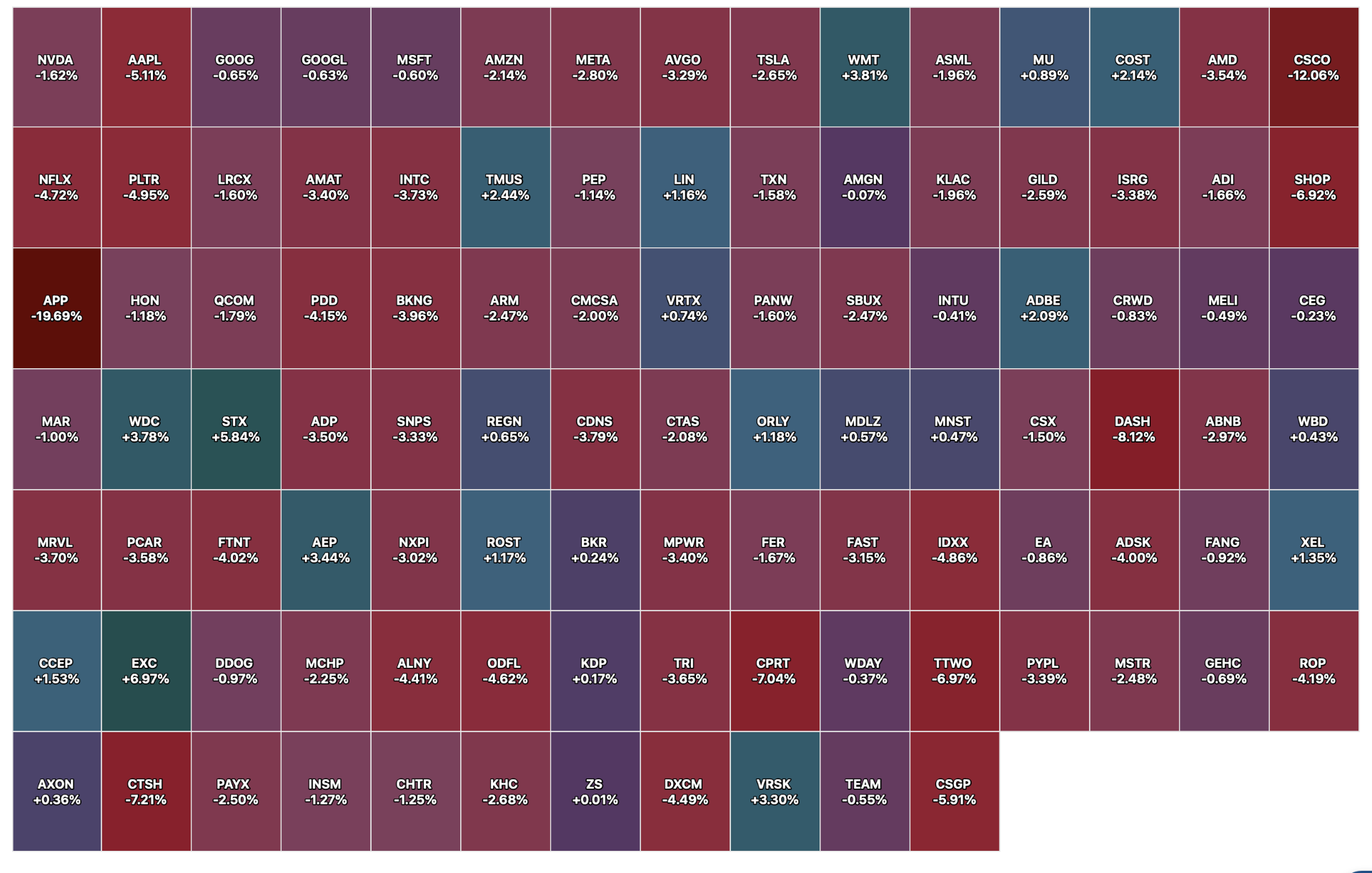

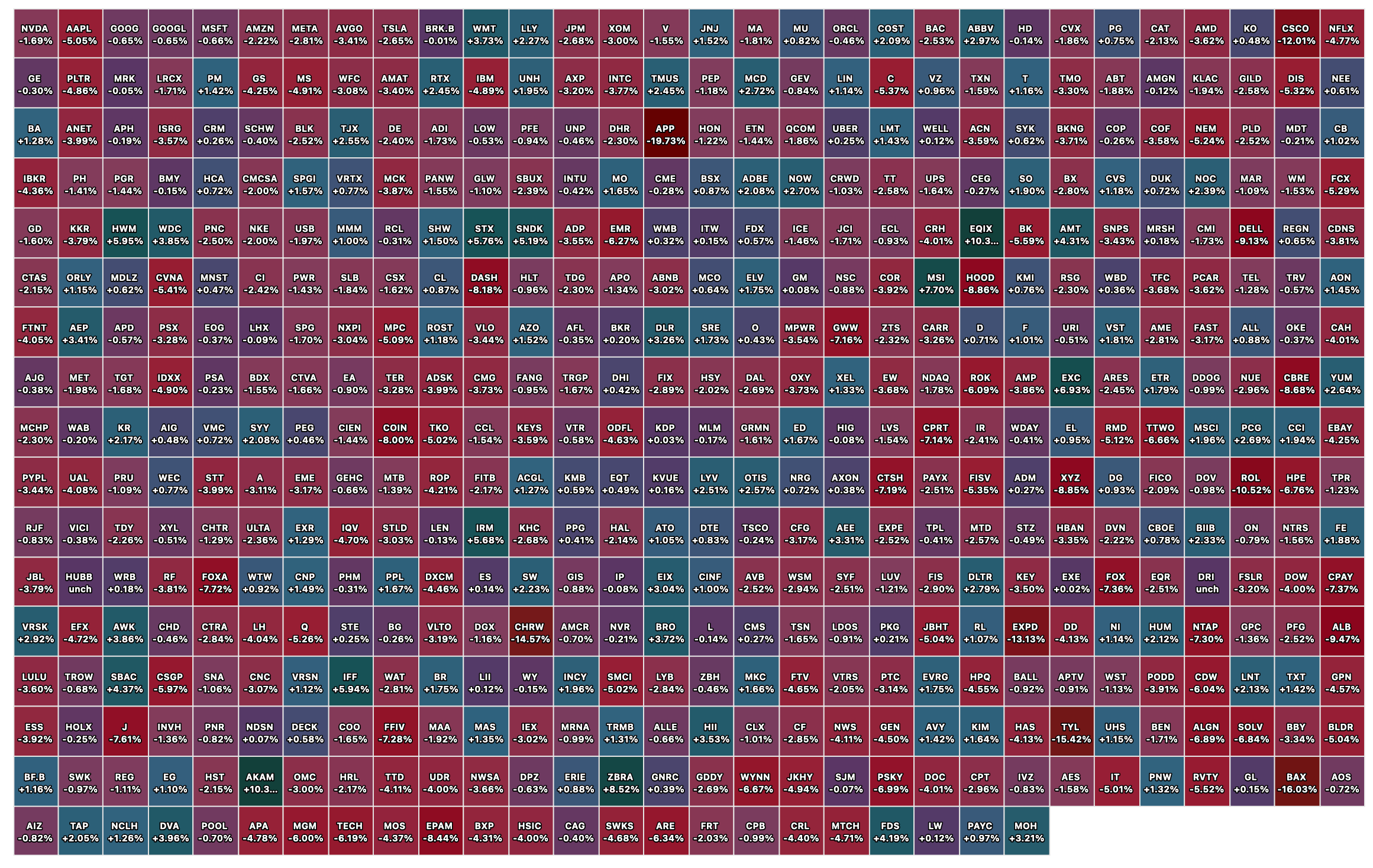

Large-Cap Stock % Advancers

Large-Cap Stock % Decliners

BY Doug Kass · Feb 12, 2026, 2:54 PM EST

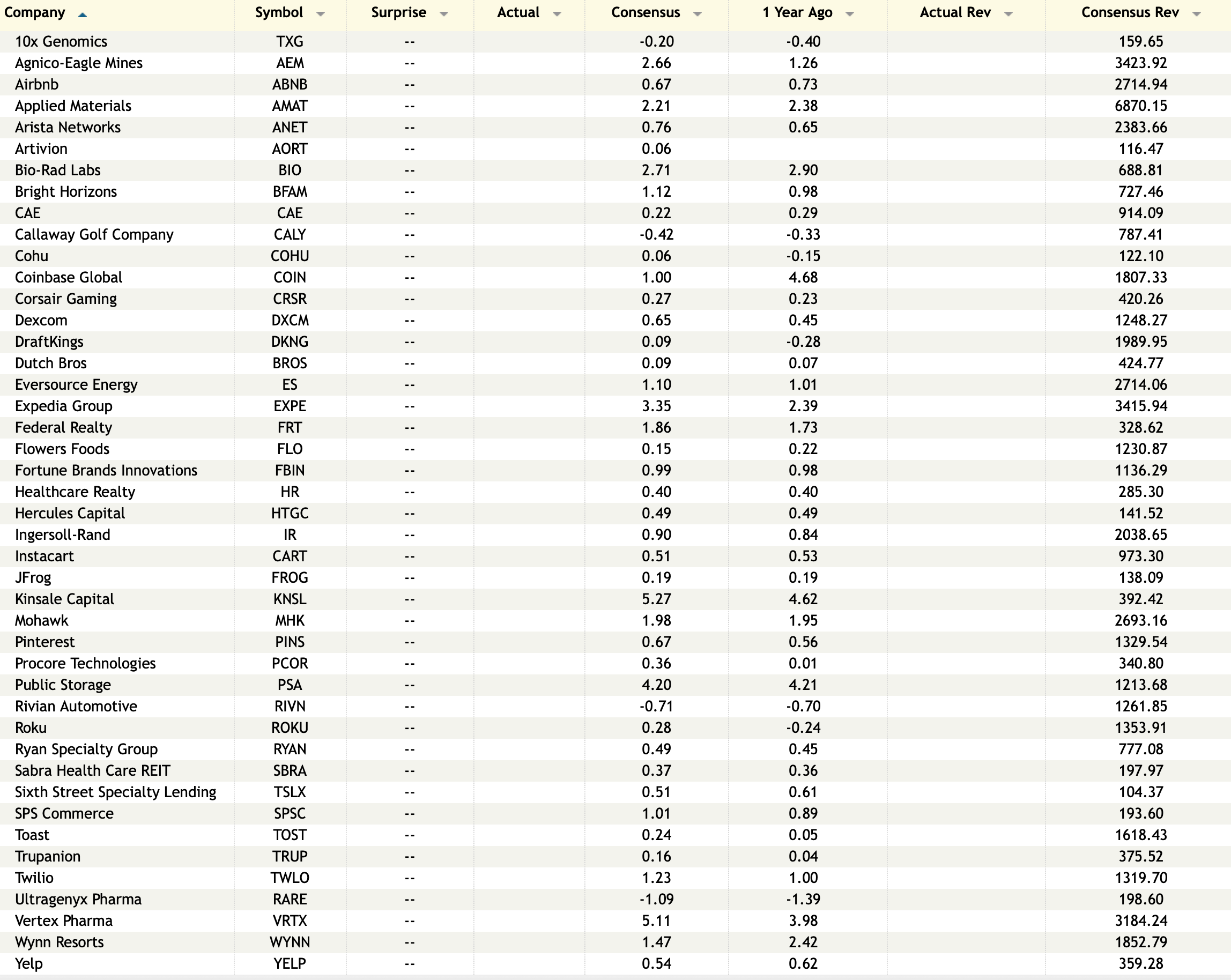

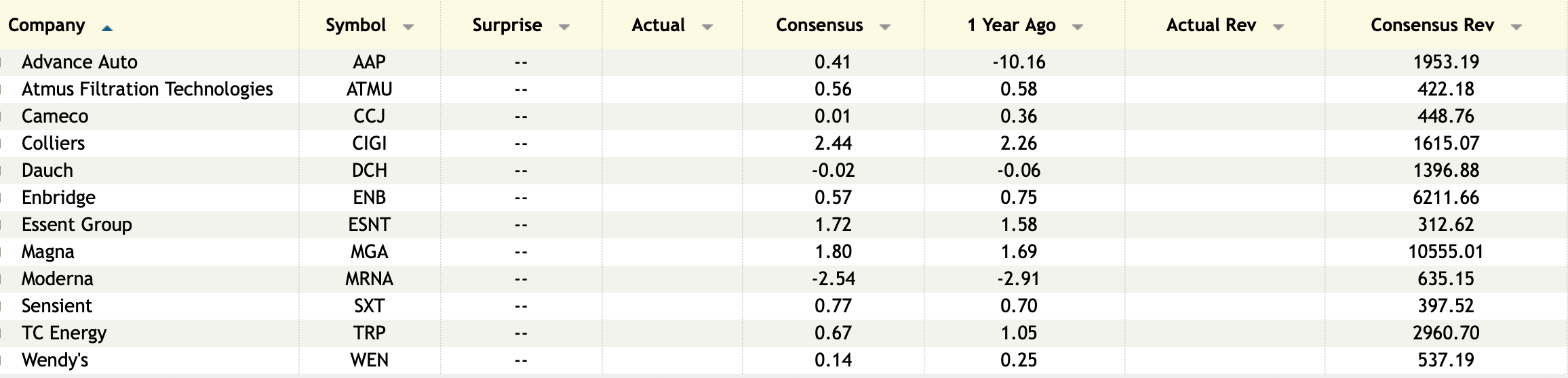

Earnings After the Close Thursday, Feb. 12

Earnings Before the Open Friday, Feb. 13

BY Doug Kass · Feb 12, 2026, 2:38 PM EST

As of 1:20 pm:

BY Doug Kass · Feb 12, 2026, 1:45 PM EST

As of 1:19 pm:

BY Doug Kass · Feb 12, 2026, 1:35 PM EST

No trades since last report.

I will be out most of the afternoon.

BY Doug Kass · Feb 12, 2026, 12:26 PM EST

I have no current plans to cover any shorts today.

BY Doug Kass · Feb 12, 2026, 11:11 AM EST

BY Doug Kass · Feb 12, 2026, 10:47 AM EST

From Peter Boockvar:

Important private credit read/McValue seems to be working

With the growing set of eyes on the private credit space because of worries about software exposure, I recommend you read this Q4 report from Lincoln International (ht Bloomberg article and YH) where it said “Slowing EBITDA growth led to the lowest q/o/q growth in private company enterprise values in 2025; could this be a sign of things to come in 2026?”

This is what particularly stood out to me, “While the covenant default rate remained flat since Q3 at 3.2%, amendment activity increased 13% quarter-over-quarter, with maturity extension and covenant holiday activity increasing 14% and sponsor infusion activity increasing 31%. Conversely, repricing amendment activity, often a sign of positive company performance, increased just 6%. This trend suggests that although lenders and sponsors remain supportive of portfolio companies, the signs of distress amongst underperforming portfolio companies are growing.”

And, “The covenant default rate is only one measure of stress and, to dig deeper into the health of the direct lending market, Lincoln did an analysis of PIK activity and determined that 11% of loans valued by Lincoln paid PIK interest in 2025. Importantly, this represents any magnitude of PIK interest (i.e., it may be a small partial PIK toggle or a full PIK election). The 11% represents an increase from 7% in 2021.”

Further on this, “Further analysis showed that, of the 11% of loans with PIK interest, Lincoln determined that 58% of those companies had “bad PIK” interest, meaning these companies did not pay any PIK interest at initial transaction close (including loans that had a PIK toggle that was not utilized at inception), but now had some component of PIK interest, up 1% from Q3 and 23% since Q4 2021. Putting this all together, of the total population of loans in Lincoln’s proprietary private market database, 6.4% of loans had “bad PIK”, an increase from 6.1% in Q3 and 2.5% in Q4 2021. This “bad PIK” percentage can be viewed as a “shadow default rate” or a proxy for situations wherein there may have otherwise been a default if not for a PIK election given such elections are often made due to liquidity tightness. As further corroboration that this cohort of loans with bad PIK may be experiencing stress, the average increase in loan-to-value (LTV) was 36.7%, increasing from a healthy 39.4% at inception to 76.1% today, further demonstrating the stress of these borrowers.”

The Lincoln Private Market Index Ends the Year with its Slowest Quarter of Growth in 2025

I want to mention again this continued rally in the Chinese yuan where the offshore rate is now below 6.90 vs the US dollar. It’s up for the 8th day in 9 and this is the longest weekly winning streak in 13 years. This is purposeful and again, this is the end, for now I believe, of China exporting deflation via its excess but highly efficient and high tech manufacturing production and this story below also highlights the steps Chinese officials are taking to make that happen.

Bloomberg News reported that “China Bans Below Cost Car Sales to End Prolonged Price War.” The article said “In a final set of guidelines released Thursday, the State Administration for Market Regulation effectively banned automakers from selling vehicles below their total cost of production. That includes not just a company’s factory floor expenses, but administrative, financial and sales overheads.” The anit-involution campaign has been taking place over the past six months but it seems like it’s getting more serious.

From McDonald’s:

A big focus on the call on providing value to its customers. “We’ve listened to customers and adjusted along the way with a relentless focus on delivering leadership in value and affordability...Together with McValue and exciting marketing, we gained share with low income consumers in December, and we’ve seen a meaningful increase in our value and affordability scores.”

US comps grew 6.8% in Q4 “driven by positive check and guest count growth. While some of the performance is attributable to easier prior y/o/y comparisons, it largely reflects the success of value, menu and marketing initiatives that supported steady improvement in our baseline momentum.”

That said, “We believe the underlying assumptions for our 2026 outlook are prudent and reflect our expectations that the QSR industry environments in the US and across many markets will remain challenging.”

Mattel got smashed by 25% yesterday and said this of note:

“the growth in the US was less than anticipated, which impacted our full results relative to expectations. 2025 was marked by uncertainty in US trade dynamics that affected retailer ordering patters for much of the year.”

“After two challenging quarters where US retailers delayed orders, there was a significant acceleration in orders through most of the fourth quarter. December, however, ended up growing less than anticipated in the US and our full year results finished below expectations. The challenge was specific to the US, while our international business performed in line with expectations, with growth in every region in the quarter.”

I’ll ask this, why exactly do we have tariffs on imported toys that we will never make here?

“what we saw in December was a more promotionally driven environment and a price sensitive consumer looking for deals. And we reacted on a timely basis.”

From Hilton, up about .50% yesterday, after rising by 3% yesterday on the Marriott report:

“strong international performance and solid group demand were offset by softer US government demand and weaker international inbound into the US.”

“Positive trends continued into early 2026 with group leading, including strong in-month group bookings, solid leisure demand and continued business transient improvement.”

They think 2026 will be better than 2025 “driven by continued strength in EMEA, improvement in APAC, and an improvement in the US driven by stronger economic conditions, major events, easier comps and continued limited supply.”

James Hardie, the maker of building products for residential construction and repair/remodel, jumped 6% yesterday and said this of note:

“Current market conditions remain mixed due to the category’s exposure to the new construction end market in the southern region...So, new construction activity, it’s challenging across most of our regions, with Texas, the West, and the Southeast showing the greatest softness out there given their scale, and our exposure to these markets.”

“I’ll start with Texas, because Texas is so significant for us and for the country. It’s about 26% of national closings out there. So what we’re seeing in Texas is builders, for the the most part, have been tightly managing inventory. After significant volume declines in Q3, we have seen some signs of normalization early in the calendar year. The recent weather has created short term production delays, and we’re seeing most builders remain conservative, pacing starts to sales.”

“In repair and remodel, we have seen demand stabilize at the current low levels...It’s choppy, but it’s stabilizing. We’re not seeing it get any worse, which is good. We’re seeing sentiment improving across all our regions, West, South, Midwest, and Northeast, particularly where there’s aging housing stock, which makes a lot of sense.”

From Martin Marietta Materials, down 6% yesterday:

“Looking ahead, our 2026 shipment guidance of 2% growth at the midpoint reflects a balanced macro environment in which we expect sustained infrastructure investment and accelerating momentum in data centers and energy to offset continued softness in private non-residential and residential construction”

Infrastructure investment they reference is related to the Infrastructure Investment and Jobs Act “and robust DOT budgets in Martin Marietta states underpinning a multi year pipeline of projects.”

“Spending on data center construction remains exceptionally healthy and continues trending upwards...Whether the solution is natural gas, onshore wind, grid-scale storage, or nuclear, nearly all pathways require the essential aggregates we provide.”

From Ryder, up 2% yesterday:

Earnings in fleet management fell “reflecting weaker market conditions in rental and used vehicle sales...Rental demand increased sequentially, but only in line with historical seasonal trends and not indicating any improvement in market conditions. Rental demand this quarter was below prior year.”

Revenue in their ‘dedicated’ division fell “due to lower fleet count, reflecting the prolonged freight downturn.”

“In terms of market assumptions, we’re expecting modest US economic growth in 2026 and no meaningful change in freight market conditions. Our outlook also assumes US Class 8 production declines 4% in 2026.”

From Cisco, down 7% pre-market because of margin pressure as the top line was fine:

“In Q2, total revenue growth accelerated to 10% y/o/y, with product revenue up 14% driven by robust demand for AI infrastructure and campus networking solutions.”

In response to “the recent significant increases in memory prices across the market...we have already announced price increases and will continue to monitor market trends and make additional adjustments as necessary.”

Also, “we are revising contractual terms with channel partners and customers to address evolving component prices.” And, they want to “negotiate favorable terms and secure supply to fulfill current and future demand.”

Quantifying the margin hit, “Non-GAAP product gross margin was 66.4%, down 130 bps y/o/y, primarily driven by negative impacts from mix and higher memory costs, partially offset by productivity improvements.”

To data overseas of relevance, Japan said its January PPI rose 2.3% y/o/y as expected but still highlighting the pricing pressures still very much alive there. Nothing market moving but the 2 yr JGB yield is sitting at 30 yr highs in anticipation for more BoJ rate hikes. Yields in 10s were unchanged but fell for 30s and 40s. The yen is little changed while the Nikkei finally took a rest, flat on the day.

The UK economy in Q4 rose just 1% y/o/y and one tenth q/o/q with modest consumer spending and a rise in government spending y/o/y. There was a decline in exports offset by higher business investment y/o/y, though fell q/o/q. There is enormous political pressure on the Starmer government and his poll numbers are very weak. They thought they can tax their way out of the budget pressures and its only made things worse. Cheap stocks though still are widespread in the UK market and we own some.

BY Doug Kass · Feb 12, 2026, 10:15 AM EST

I will be out much of the afternoon at business meetings.

BY Doug Kass · Feb 12, 2026, 10:05 AM EST

I am re-shorting (JOET) and (GRNY)

BY Doug Kass · Feb 12, 2026, 9:55 AM EST

BY Doug Kass · Feb 12, 2026, 9:45 AM EST

11:00AM: Treasury announces a 3 and 6 month and a 6 & 52 Week Bill Auction;

11:00AM: Treasury Announces a TIPS and Bond Auction;

11:30AM: Treasury hosts a $105B 4 and a $95B 8 Week Bill Auction;

1:00PM: Treasury hosts a $25B 30-Year Bond Auction

BY Doug Kass · Feb 12, 2026, 9:35 AM EST

I am short Super Group (SGHC).

Today Spruce Capital Management issued a short report.

Super Group (SGHC) Limited - Spruce Point Capital Management LLC

BY Doug Kass · Feb 12, 2026, 9:20 AM EST

From Peter Boockvar:

After jumping to 232k last week (revised up by 1k), initial claims fell to 227k (4k above the estimate). This brings the 4 week average to 220k from 213k as a print of 199k drops out. Continuing claims lifted by 21k w/o/w to 1.862mm, 12k more than anticipated.

I should just copy and paste my bottom line over the past year because it still is the same. The pace of firing’s, as measured here, remains muted while the rate of hiring’s (outside of healthcare/social assistance and data center construction) has slowed.

BY Doug Kass · Feb 12, 2026, 9:15 AM EST

Upside:

-FSLY +41% (earnings, guidance)

-CGNX +24% (earnings, guidance)

-MH +19% (earnings, guidance)

-PRCH +19% (earnings, guidance)

-CROX +15% (earnings, guidance)

-BBIO +14% (reports Positive Phase 3 Topline Results for Oral Infigratinib with the First Statistically Significant Improvements in Body Proportionality in Achondroplasia)

-EQIX +13% (earnings, guidance)

-SPHR +13% (earnings)

-ZBRA +13% (earnings, guidance; approves additional $1B share buyback)

-TYRA +9.2% (higher following BBIO drug data)

-APRE +7.6% (strengthens Global Patent Portfolio in DNA Damage Response (DDR) Cancer Therapeutics)

-SNDK +6.7% (momentum)

-BTU +5.0% (President Trump: Coal power generation to be up about 25-30% this year)

-LNC +4.9% (earnings)

-HWM +4.8% (earnings, guidance)

-OSCR +3.8% (Raymond James Raised OSCR to Outperform from Market Perform, price target: $18)

-WST +3.6% (earnings, guidance)

-CBRE +3.4% (earnings, guidance)

-ZTS +3.0% (earnings, guidance)

-BUD +2.9% (earnings, guidance)

-TRU +2.5% (earnings, guidance; raises dividend)

-ADI +2.1% (Barclays Raised ADI to Overweight from Equal Weight, price target: $375)

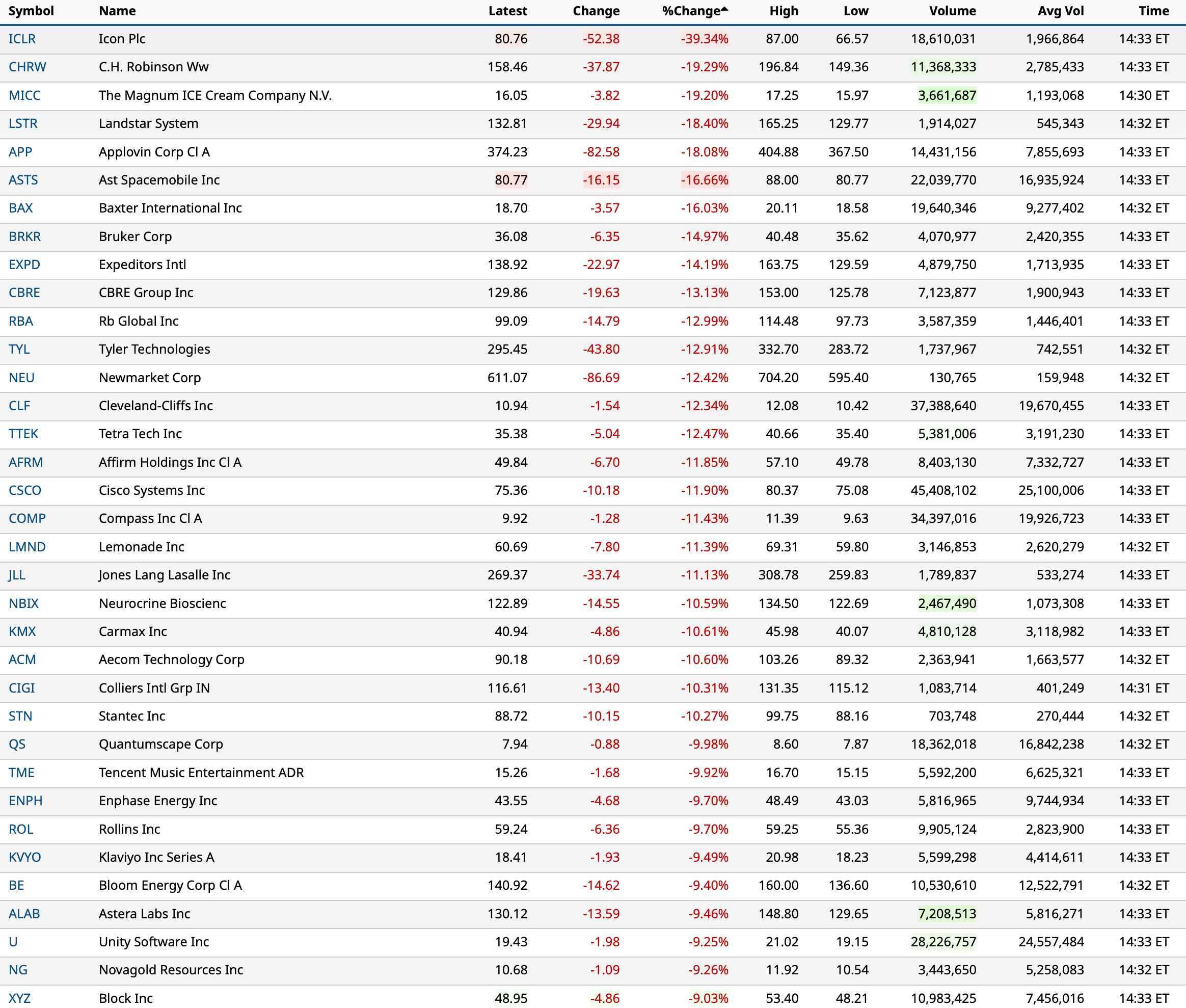

Downside:

-MCRB -21% (cutting workforce ~30% to focus on early-stage live biotherapeutic programs in Inflammatory and immune diseases)

-ROL -14% (earnings)

-BAX -12% (earnings, guidance)

-INSP -12% (earnings, guidance)

-PAYC -11% (earnings, guidance)

-ASTS -10% (offers $1B of Convertible Senior Notes Due 2036)

-CHKP -7.6% (earnings, color)

-CSCO -7.4% (earnings, guidance)

-TYL -7.1% (earnings, guidance)

-BMRN -6.2% (downside pressure following BBIO reporting Positive Phase 3 Topline Results for Oral Infigratinib with the First Statistically Significant Improvements in Body Proportionality in Achondroplasia)

-NVMI -5.6% (earnings, guidance)

-ASND -5.3% (downside pressure following BBIO reporting Positive Phase 3 Topline Results for Oral Infigratinib with the First Statistically Significant Improvements in Body Proportionality in Achondroplasia)

-LEG -5.2% (earnings, guidance)

-SNY -4.6% (names Belén Garijo as CEO)

-TRIP -4.2% (earnings)

-PPC -3.8% (earnings)

-MESO -3.1% (provided data presented at the February 2026 Tandem Meetings of the American Society for Transplantation and Cellular Therapy (ASTCT) and the Center for Blood and Marrow Transplant Research (CIBMTR))

-QTWO -3.1% (earnings, guidance)

-QSR -2.1% (earnings, guidance)

-RGTI -2.1% (hearing TD Cowen Cuts RGTI to Hold from Buy)

BY Doug Kass · Feb 12, 2026, 9:05 AM EST

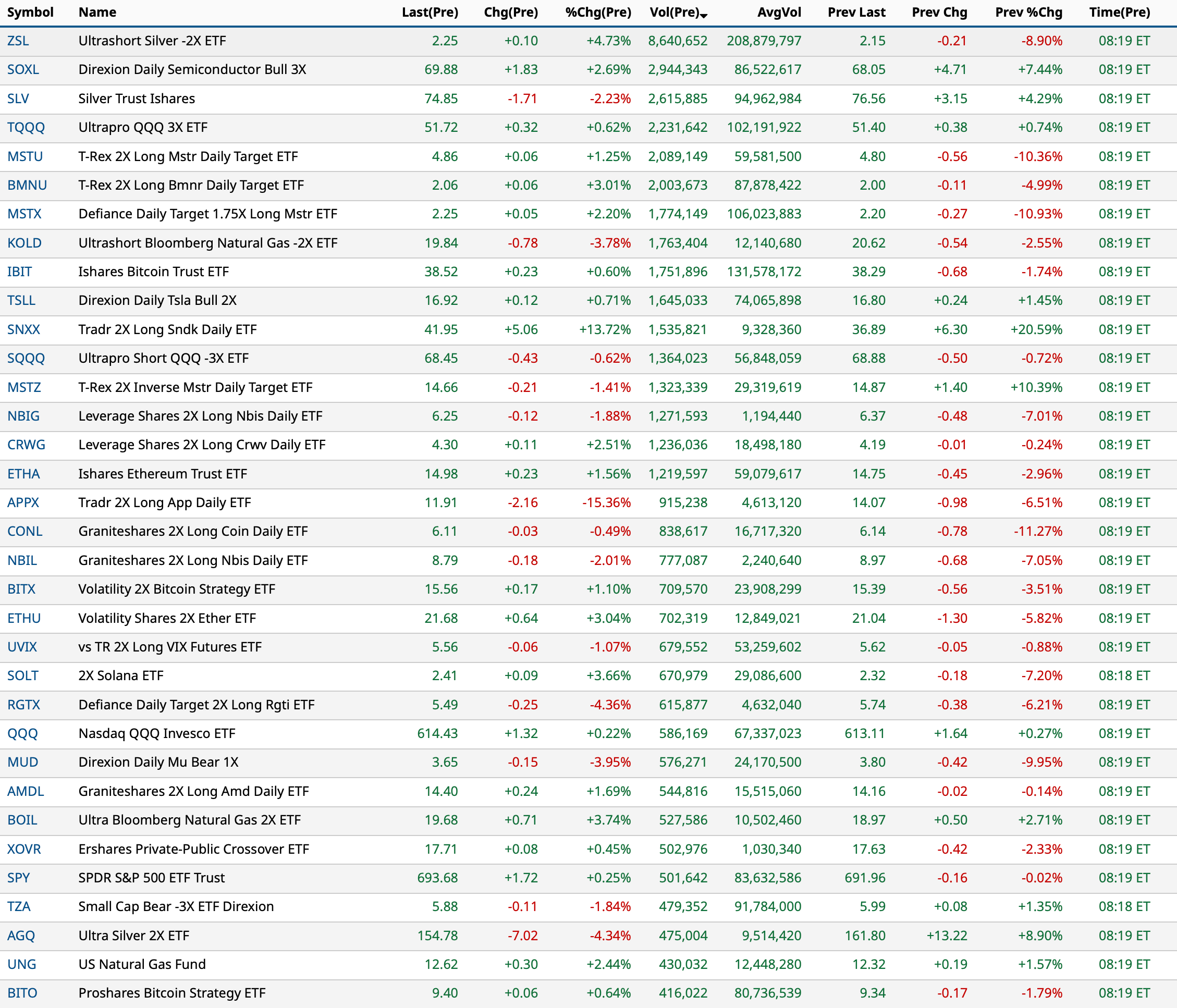

As of 8:19 AM:

BY Doug Kass · Feb 12, 2026, 8:56 AM EST

At 8:43 AM:

BY Doug Kass · Feb 12, 2026, 8:50 AM EST

BY Doug Kass · Feb 12, 2026, 8:34 AM EST

I have shorted a basket of speculative and high-beta equities this morning.

Names are withheld to protect the innocent.

Most investors should not short, but I post this for the purpose of giving you all a sense of the rising degree of my market pessimism.

BY Doug Kass · Feb 12, 2026, 8:21 AM EST

BFF Johnny The Greek vs. Neil The Real Deal

Johnthegreek

Wages rising at twice the rate of inflation. You heard it here first. Unemployment down.

Phenomenal job report bodes well for future gains. Once we start collecting on and stopping waste, fraud and abuse, this will only add to optimism. Construction way up. Job numbers will continue to rise as factories continue their expansion. I will continue to buy significant dips cautiously.

I don’t believe these important points are stressed enough on this platform. There is good news out there.

Dougie Kass

BY Doug Kass · Feb 12, 2026, 7:41 AM EST

BY Doug Kass · Feb 12, 2026, 7:30 AM EST

BY Doug Kass · Feb 12, 2026, 7:10 AM EST

"We've long felt that the only value of (stock) forecasters is to make fortune tellers look good. Even now, Charlie and I continue to believe that short-term market forecasts are poison and should be kept locked up in a safe place, away from children and also from grown-ups who behave in the market like children."

- Warren Buffett

"Crypto really looks like it is bottoming because the fundamental situation is positive... Banks are embracing crypto, there are regulatory bills coming that are favoring crypto. Crypto has alot of tailwinds."

- Tom Lee

Riddle me this...

Tom Lee's (BMNR) has retreated from $161 to under $20 in the last year.

Crypto bull Tom Lee appears daily on CNBC — yet he is NEVER challenged by show hosts.

He has previously said that bitcoin was bottoming on CNBC and elsewhere at $105k, $95k, $85k, $75k and $65k.

BY Doug Kass · Feb 12, 2026, 7:00 AM EST

BY Doug Kass · Feb 12, 2026, 6:45 AM EST

BY Doug Kass · Feb 12, 2026, 6:35 AM EST

Cramer, Cramer, Cramer? Bueller? - Ferris Bueller's Day Off (1/3) Movie CLIP (1986) HD

The shares of Salesforce (CRM) have declined from $327 to $185 — hitting a 52-week low on Wednesday (-$9/share or -4%).

But Dan Ives sees (another) opportunity:

BY Doug Kass · Feb 12, 2026, 6:25 AM EST

What could go wrong?

A financial platform or a casino?

BY Doug Kass · Feb 12, 2026, 6:15 AM EST

BY Doug Kass · Feb 12, 2026, 6:05 AM EST

Wolf Street howls about HELOCS.

BY Doug Kass · Feb 12, 2026, 5:55 AM EST

The S&P Short Range Oscillator is getting more overbought at 3.50% vs. 2.73%.

BY Doug Kass · Feb 12, 2026, 5:45 AM EST

The embedded tweet could not be found…

The embedded tweet could not be found…