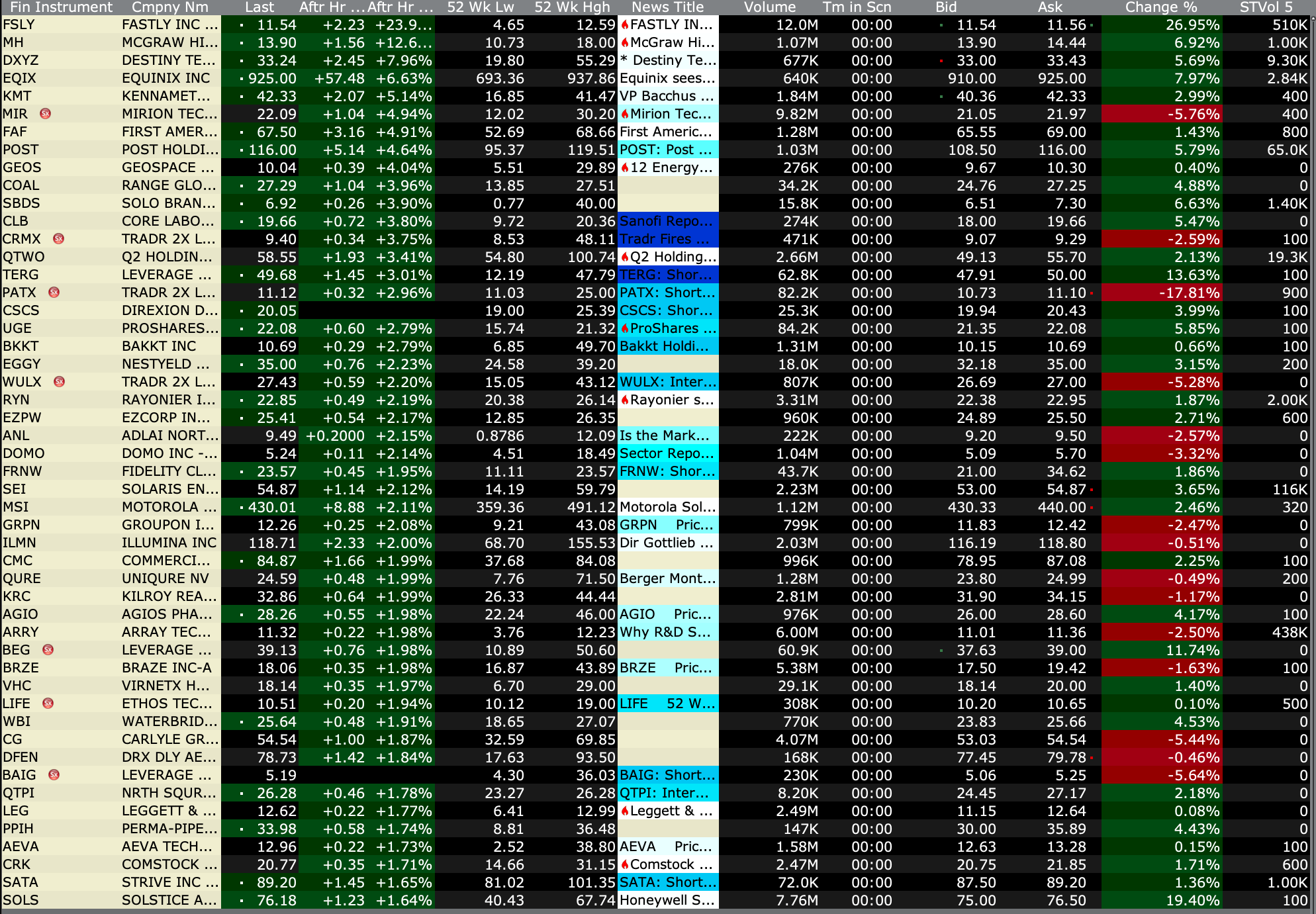

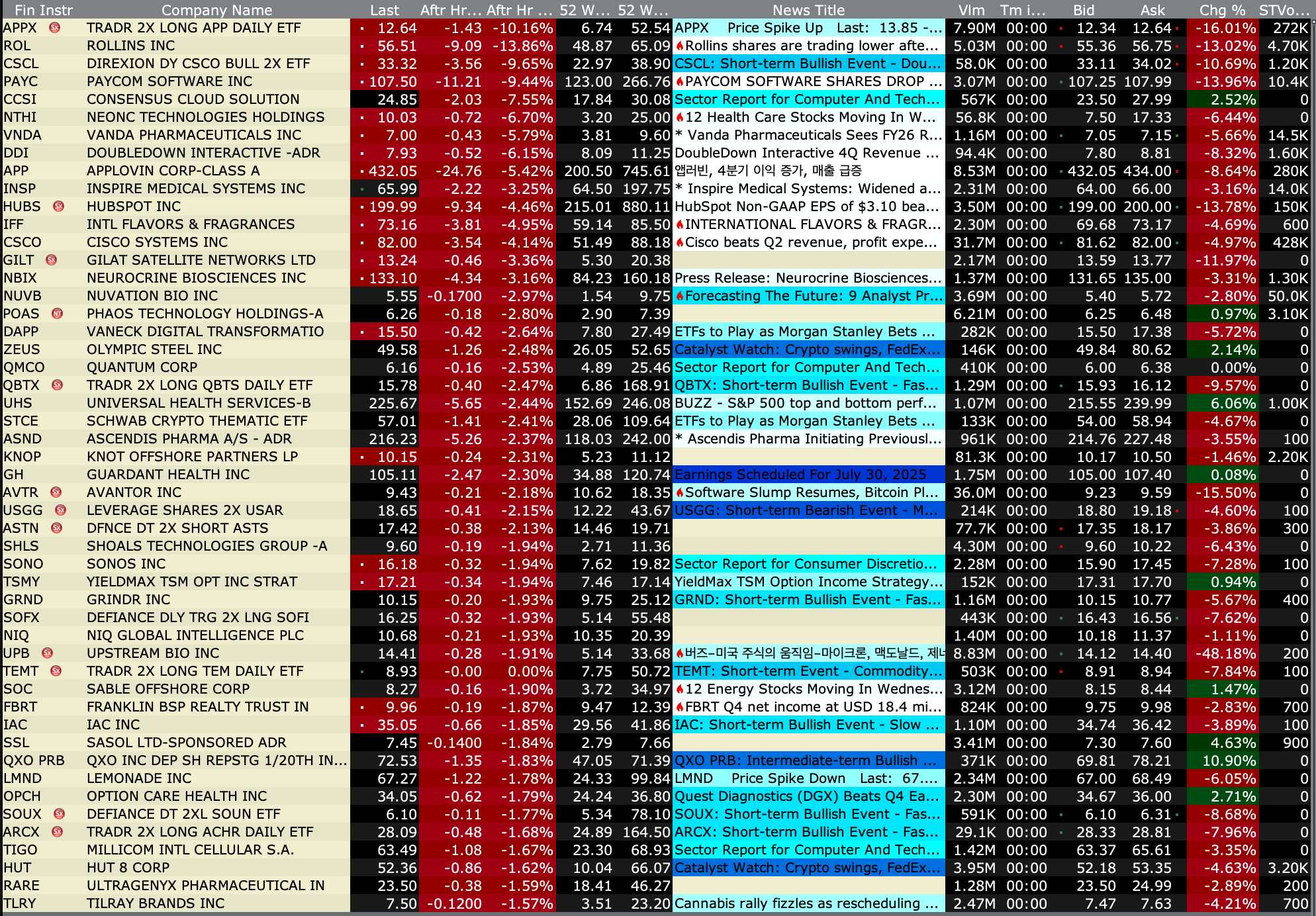

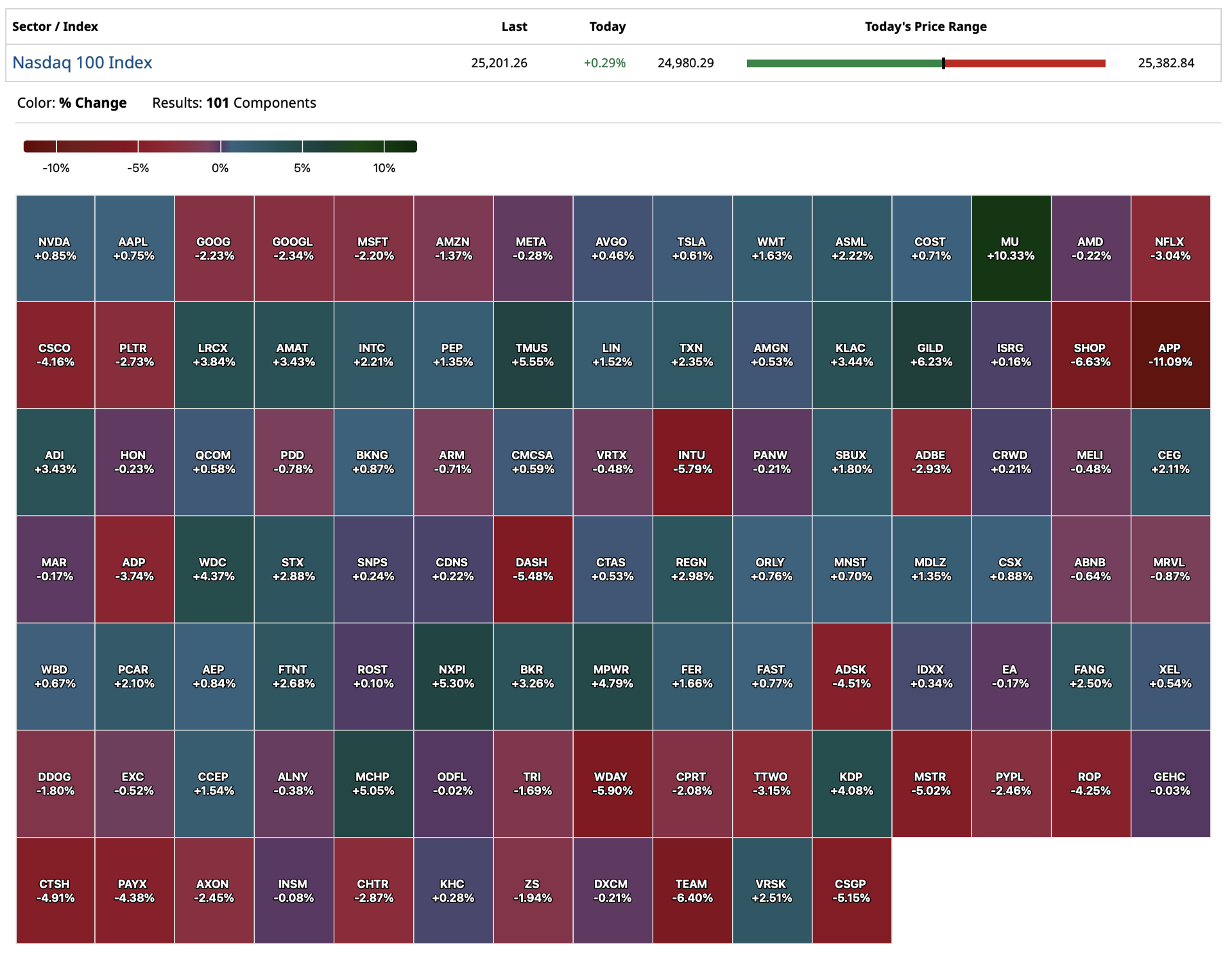

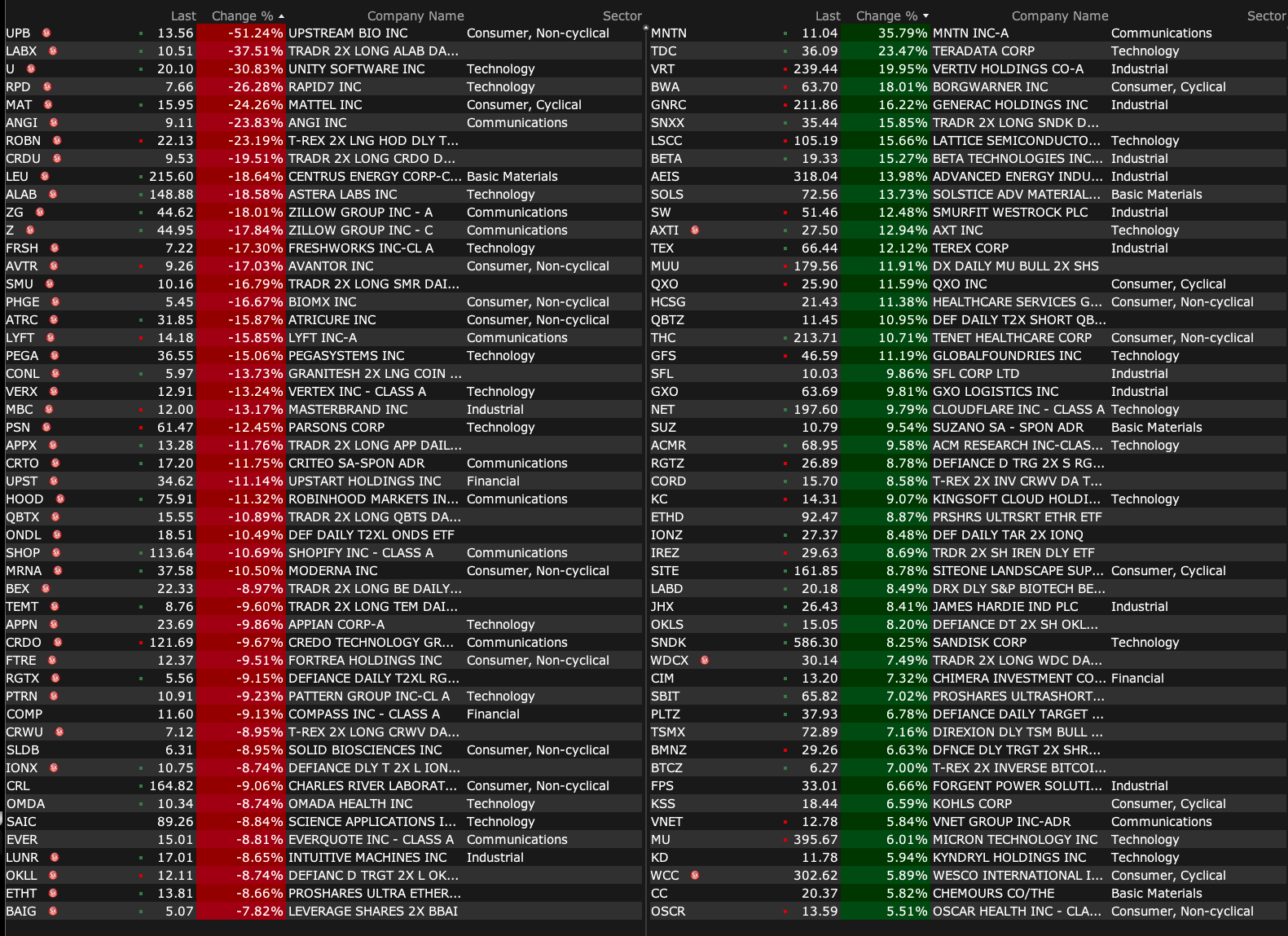

After-Hours Advancers and Decliners

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Feb 11, 2026, 4:40 PM EST

BY Doug Kass · Feb 11, 2026, 4:40 PM EST

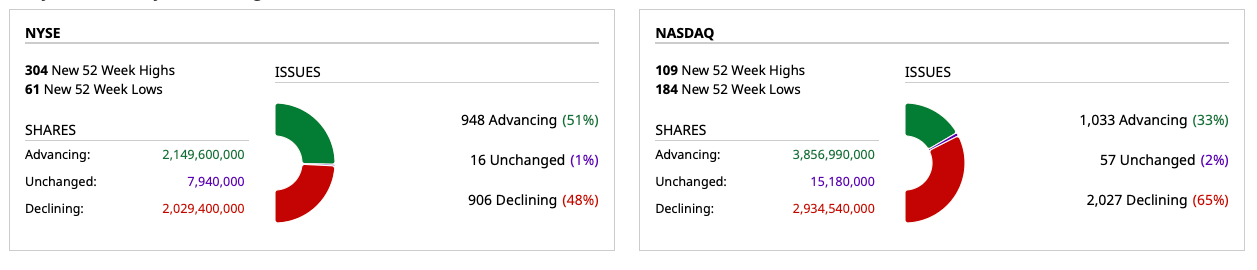

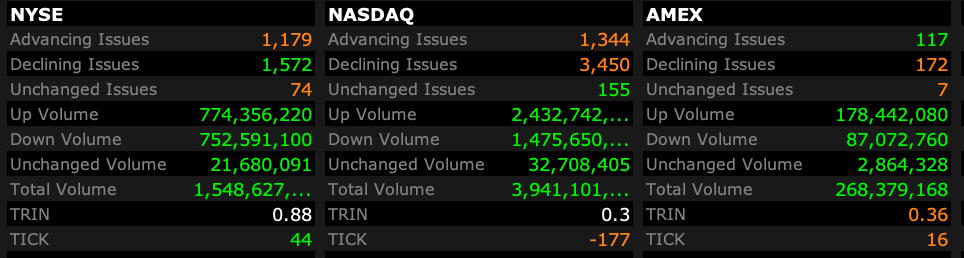

- NYSE volume 5% above its one-month average;

- NASDAQ volume 11% above its one-month average;

- VIX index: down 1.07% to 17.60

BY Doug Kass · Feb 11, 2026, 4:30 PM EST

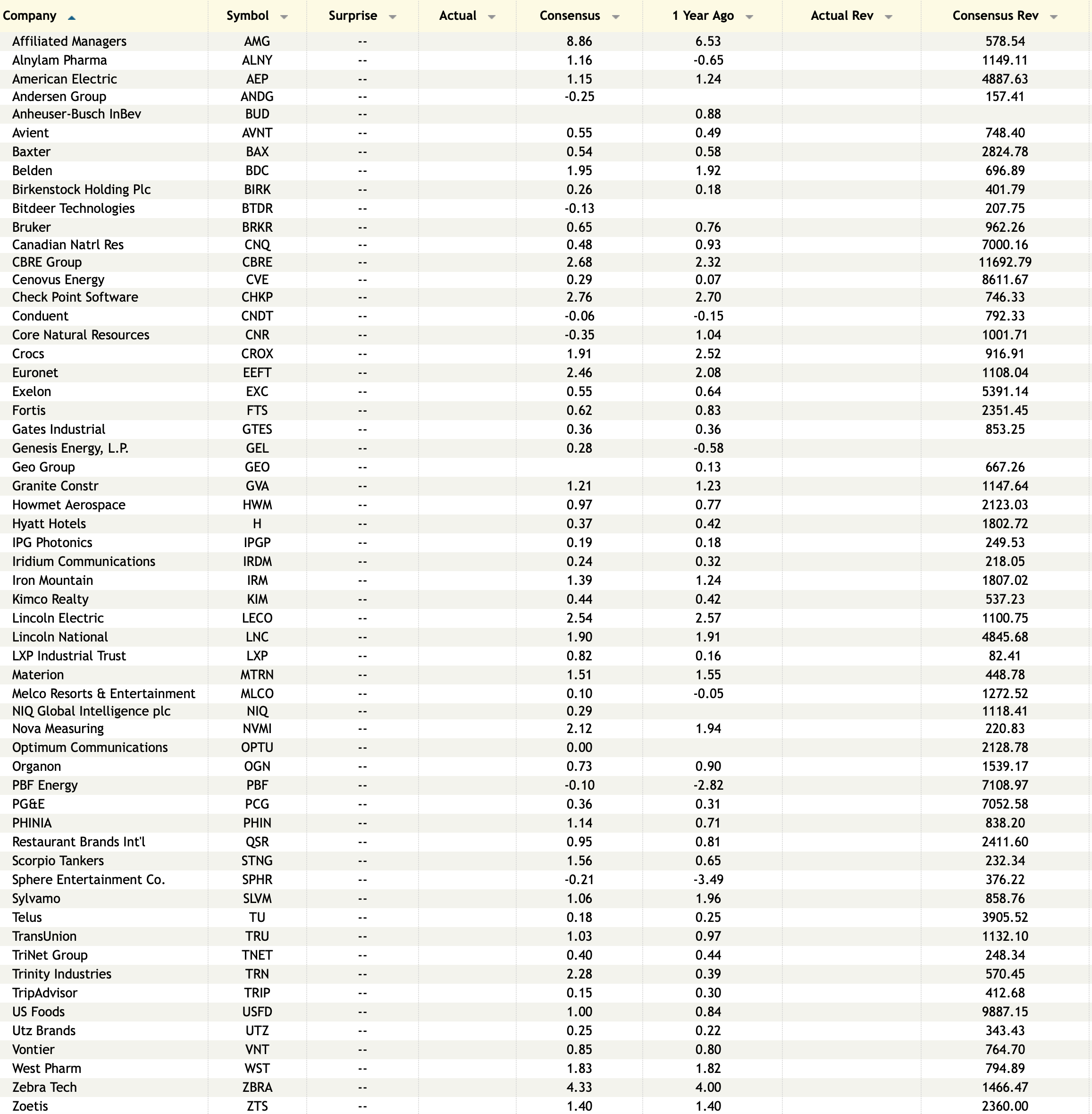

Earnings After the Close Wednesday, Feb. 11

Earnings Before the Open Thursday, Feb. 12

BY Doug Kass · Feb 11, 2026, 3:12 PM EST

The two dumbest things I have done recently were to cover the shorts in (HOOD) and (PLTR) .

BY Doug Kass · Feb 11, 2026, 2:20 PM EST

* Consider this...

BY Doug Kass · Feb 11, 2026, 2:05 PM EST

Mm-mm-memories

Light the corners of my mind

Misty watercolor memories

Of the way we were

Scattered pictures

Of the smiles we left behind

Smiles we gave to one another

For the way we were

- Barbara Streisand The Way We Were

I remember this tune, err the market's emerging profile in prior corrections.

I remember when financials begin to roll over and break down, while consumer staples flourish.

I remember when technology also began to correct during market corrections.

Only memory(ies) — Micron (MU) et al — seem to still seem to be in a sustaining and advancing mode.

It is the laughter we will remember.

The way we were...

BY Doug Kass · Feb 11, 2026, 1:42 PM EST

As of 1:12 PM:

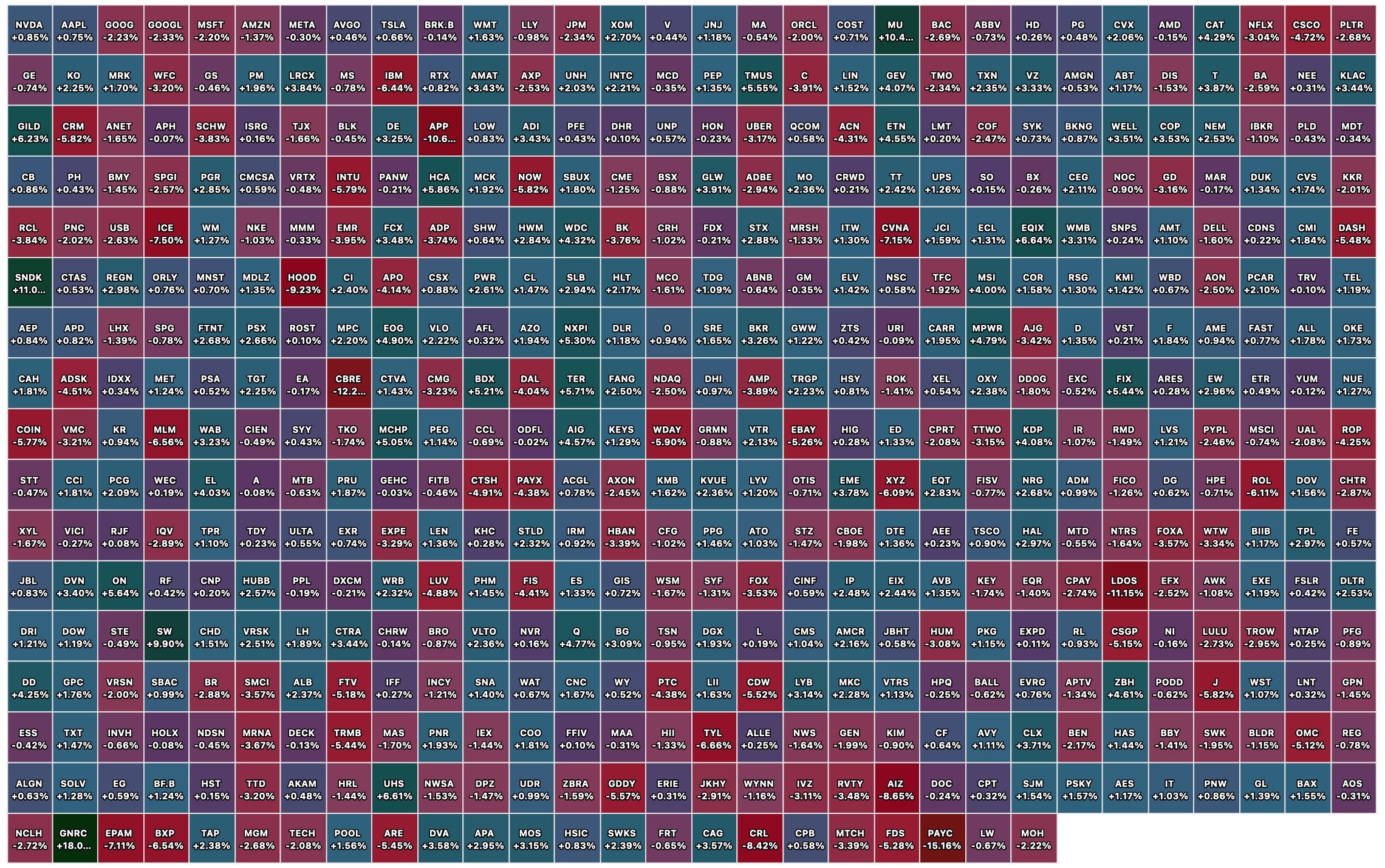

Large-Cap Stock % Advancers

Large-Cap Stock % Decliners

BY Doug Kass · Feb 11, 2026, 1:18 PM EST

With S&P cash +15 handles I am back shorting index calls.

I will be a scale seller on strength this afternoon.

BY Doug Kass · Feb 11, 2026, 12:35 PM EST

I have two research meetings starting at 2:45 p.m. today.

BY Doug Kass · Feb 11, 2026, 12:20 PM EST

- NYSE volume flat to its one-month average;

- Nasdaq volume 20% above its one-month average;

- VIX index: up 0.90% to 17.95

BY Doug Kass · Feb 11, 2026, 11:59 AM EST

Few do detailed work like this anymore:

BY Doug Kass · Feb 11, 2026, 11:40 AM EST

Dougie Kass

STAFF

25 minutes ago

Ludacris Forecast?

BY Doug Kass · Feb 11, 2026, 11:26 AM EST

From Charlie:

BY Doug Kass · Feb 11, 2026, 10:59 AM EST

BY Doug Kass · Feb 11, 2026, 10:45 AM EST

Covered 1/4 of my (GRNY) short (Trade of the Week) under $25.

BY Doug Kass · Feb 11, 2026, 10:31 AM EST

With S&P cash -8 handles (peaked at +50 earlier today) - I have taken in my Index call shorts.

I have no index exposure now.

BY Doug Kass · Feb 11, 2026, 10:15 AM EST

With S&P cash +19 handles I have taken in my Index common shorts done today for a profit.

BY Doug Kass · Feb 11, 2026, 10:13 AM EST

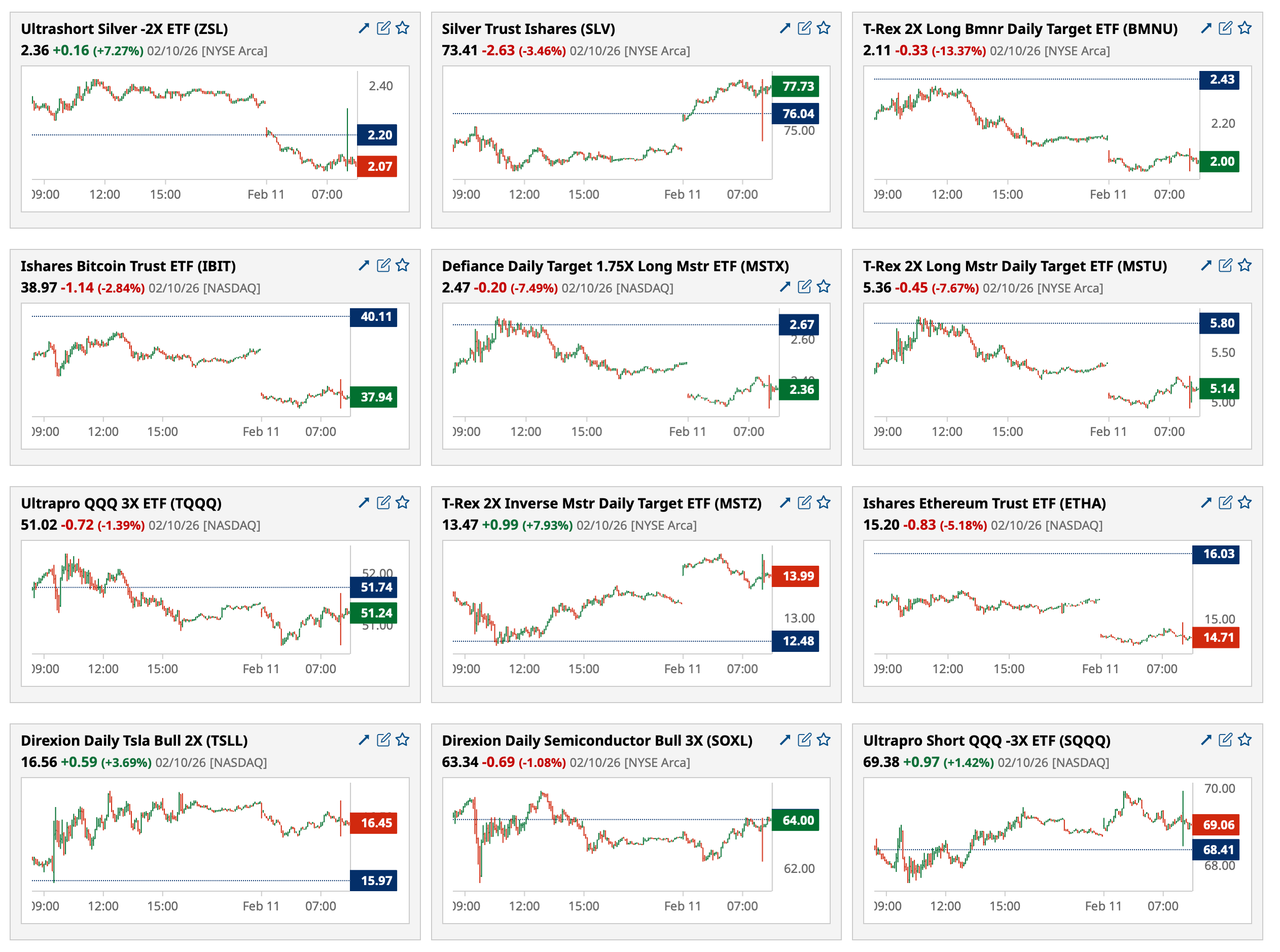

Chart from 9:39 a.m. ET

BY Doug Kass · Feb 11, 2026, 10:10 AM EST

(GRNY) 's constituent holdings are among the highest octane/beta stocks.

In an overbought market this portfolio is what I want to short.

I have moved to large sized today in this exchange-traded fund.

BY Doug Kass · Feb 11, 2026, 10:05 AM EST

With S&P cash +45 handles I am shorting Index calls.

BY Doug Kass · Feb 11, 2026, 10:03 AM EST

Moved to large short (GRNY) at $25.43.

BY Doug Kass · Feb 11, 2026, 9:56 AM EST

From Peter Boockvar:

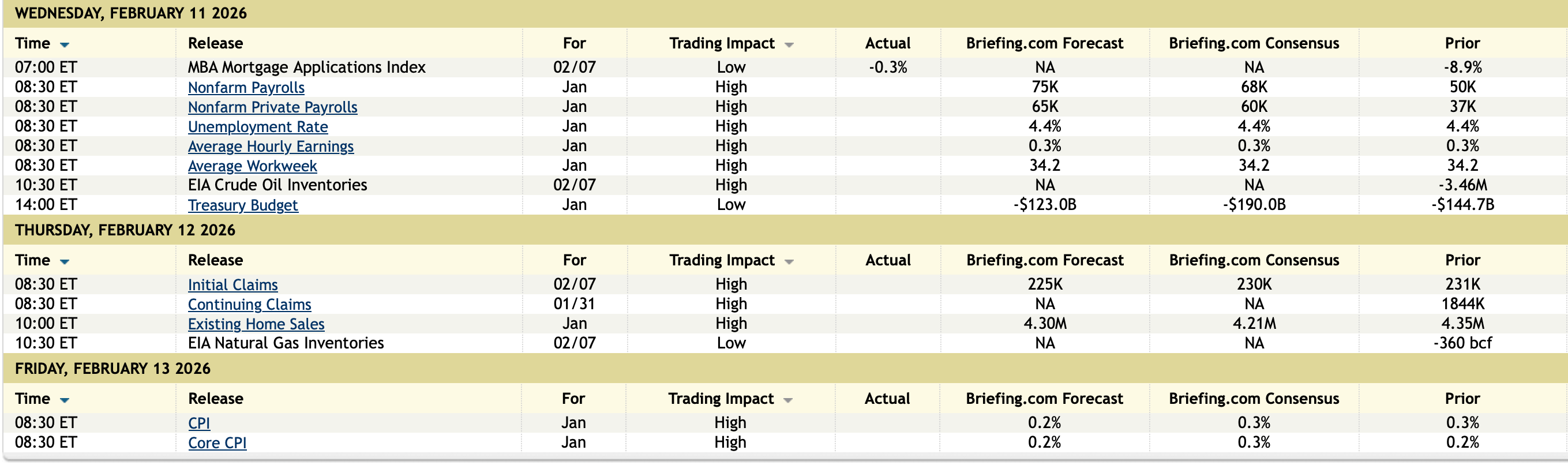

January payrolls jumped by 130k, exactly double the estimate with the private sector contributing 172k of this (govt jobs fell). The two prior months were revised lower by a total of 17k so even incorporating this the upside relative to expectations was notable. The household survey said 528k jobs were added and as it was above the 387k person rise in the labor force, the unemployment rate fell to 4.3% from 4.4%. The all in U6 rate fell to 8% from 8.4% helped too by a drop in those working part time because they can’t find full time work.

It’s important to note here however that about ALL of the job creation came from the private education/heath care sector which contributed 137k jobs (124k came from health/social assistance). Leisure/hospitality added just 1k while professional/business services hired a net 34k (9k of which was temp) and retail added only 1k. Jobs were lost in trade/transport, information, and financial services.

On the goods side, construction added 33k of the 36k, likely helped by data center buildings. Manufacturing hired, finally, by 5k.

The participation rate ticked up by one tenth to 62.5%. Average hourly earnings rose by .4%, one tenth better the expectations but the prior month was revised down by 2 tenths. Versus last year, hourly earnings rose 3.7%. Hours worked were 34.3 vs 34.2 in the month before. Combining the two put average weekly earnings higher by 4.3%, still pretty good.

Bottom line, if I just looked at the headline jobs figure I’d think the labor market is humming. But if I look under the hood, I see that just about all the job growth is still coming from healthcare/social assistance with some lift too in construction. The rest of the economy is reflecting this highly unusual and highly uneven business activity situation.

I will add this, agree with the tariff policy or not, the cost pressures for many small and medium sized businesses that are hurting profit margins is resulting in a slowdown in hiring as they try to recapture those lost margins.

As the Treasury market is solely focused this morning on the headline figure, the 2 yr yield jumped from 3.45% to 3.53%, the 10 yr yield at 4.19% is up from 4.12% while the 30 yr yield is up by 5 bps to 4.82%.

BY Doug Kass · Feb 11, 2026, 9:55 AM EST

From Peter Boockvar:

The market reaction in certain sectors to whatever new AI application is announced believing in disruption, like we saw yesterday with the wealth/asset mgmt stocks, reminds me of exactly what took place in the late 1990’s when anyone announced they were opening up a retail store online and the brick and mortar stocks immediately fell. Yes, Amazon ended up disrupting just about everything but plenty of retailers just added their own direct to consumer websites.

The NY Fed released its quarterly report on household debt and credit and this was said of note and highlighting the splintered US consumer in terms of financial health:

“As household debt levels grow modestly, mortgage delinquencies continue to increase,” said Wilbert van der Klaauw, Economic Research Advisor at the New York Fed. “Delinquency rates for mortgages are near historically normal levels, but the deterioration is concentrated in lower-income areas and in areas with declining home prices.”

And, “Aggregate delinquency worsened in Q4 2025, with 4.8% of outstanding debt in some stage of delinquency. Transitions into early delinquency were mixed with mortgages and student loans increasing, while all other debt types held steady. Transitions into serious delinquency ticked up for credit card balances, mortgages, and student loans while auto loans and HELOC decreased slightly.”

While the average 30 yr mortgage rate held at 6.21%, purchase applications fell again by 2.4% w/o/w after dropping by 14.4% last week. Affordability is still the number one challenge and either wages need to accelerate and/or home prices need to fall in order to improve this situation. Refi’s were up 1.2%.

To some notable earnings comments.

From Marriott and whose stock popped 8.5% yesterday:

“December global RevPAR rose 2.8%, showing the strongest monthly y/o/y growth since February, led by strong leisure demand, particularly for our luxury and resort hotels. By region, fourth quarter RevPAR was again strongest in APAC, which continues to benefit from double digit rooms growth as well as solid macroeconomic growth in many countries.”

“In the US and Canada, fourth quarter RevPAR was around flat. Luxury again saw solid growth, which was offset by declines in the select service tier. Leisure transient RevPAR rose 2% in the quarter, while Group RevPAR increased 1%. These gains were offset by a 3% decline in business transient RevPAR, largely due to a meaningful decline in government RevPAR in the quarter.”

From Coca Cola, a stock we own and was down 1.5% yesterday:

“While unit case volume was flat in 2025, we ended the year with better momentum as volume improved each month during the fourth quarter.”

“Starting with North America. We delivered strong results, despite continued macroecononic pressure on lower income consumers.”

From Hasbro which jumped 7.5% yesterday:

“Right now we continue to see kind of a tale of two cities. The top 20% of households in terms of wealth are really driving a lot of demand and are staying pretty resilient. The lower quintiles of kind of wealth and income, their pennies are pinched. And so we’re trying to appeal to both.”

From SAIA, the trucker and which fell 7% yesterday:

We saw in the NFIB small business index the rise in worries about higher insurance costs. SAIA said, “As we well know, accident related costs continue to rise due to increased litigation costs and settlement values, as well as general inflation, and can develop sometimes unexpectedly over several years. Regrettably, this unexpected need for reserve increases was related to the accidents that happened years ago.”

“Mix headwinds continue to impact our results, with slight decreases in weight per shipment and length of haul compared to the fourth quarter of 2024. Additionally, revenue per shipment, excluding fuel surcharge, decreased .5% compared to last year.”

They are hopeful on volumes, and said this about the overall demand environment, “I think it’s a little bit of everything. I think it’s a little bit more of a positive end of the year, which is good. I think there’s maybe some structural market sort of influences here. But I think in total, the tenor might be just a bit more positive, right? And I think that’s good. Now I will caution just by saying, look, we’re seeing it and hearing it a bit in customer conversations. I’d like to see it more in volumes, too, right? So some of that will develop through the quarter. We think it will but that’s still until we actually see it in the results.”

From Dupont who rallied 5% yesterday and this was their lay of the land for them:

“Underpinning our organic growth is a mixed macro environment. Market indicators for Healthcare & Water Technologies continue to expect mid single digit growth in both spaces on increasing medical procedures to support an aging and growing population and strong global water demand.”

“Overall, automotive demand is about flat in 2026 with weakness in the US and Europe. However, we continue to expect EV builds to significantly outpace overall builds.”

“In construction, after years of decline, market stabilization is expected with flattish demand y/o/y. We are off to a good start to the year.”

From Ferrari, of course catering to the very upper end and whose stock was up 10% yesterday:

“The momentum for our brand remains strong with a solid order book, which extends towards the end of 2027, and the net order intake, supporting further visibility, notwithstanding the persistent uncertainty in the global environment. In addition, residual values are stable and solid, as evidenced by the recent auctions, which achieved strong valuations.”

Thanks to the big rally in industrial metals prices, China’s January PPI continues to be less negative, down by 1.4% y/o/y, the smallest drop since July 2024. CPI ex food and energy saw prices up .8% y/o/y vs 1.2% in the three prior months. With the consumer dealing with still falling home prices, and its dampening wealth effect, price stability in this stat should be welcome.

BY Doug Kass · Feb 11, 2026, 9:45 AM EST

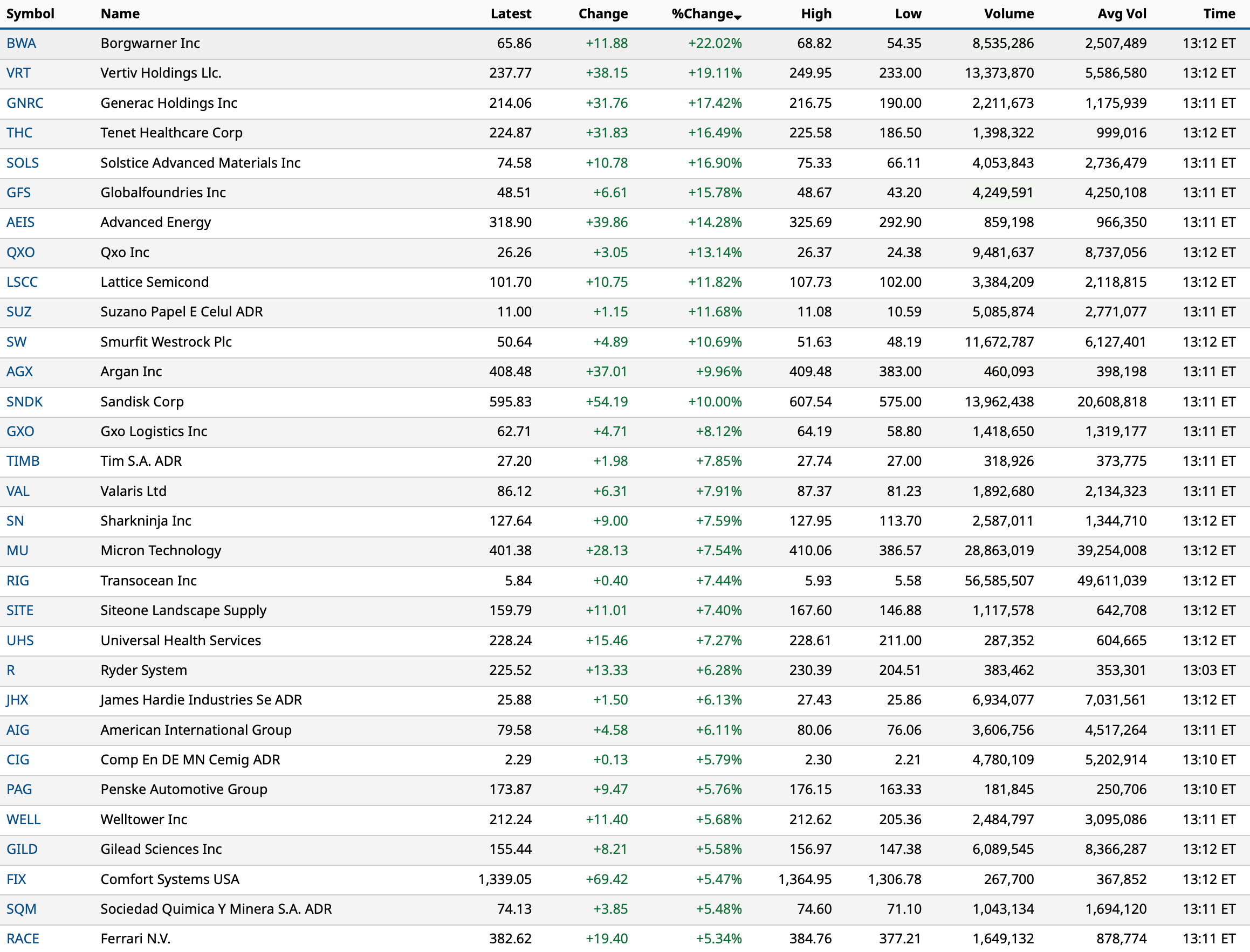

-TDC +21% (earnings, guidance)

-VRT +18% (earnings, guidance)

-NET +13% (earnings, guidance)

-HNGE +12% (earnings, guidance)

-LSCC +12% (earnings, guidance)

-SHOP +11% (earnings, guidance)

-QXO +7.2% (acquires Kodiak Building Partners from Court Square Capital Partners for ~ $2.25B)

-SUZ +7.2% (earnings, guidance)

-GNRC +6.8% (earnings, guidance)

-FRMI +5.7% (received $500M financing commitment from MUFG Bank)

-OTLY +5.6% (earnings, guidance)

-GLDD +4.7% (to be acquired by Saltchuk Resources at $17.00/shr or $1.5B valuation)

-NRGV +4.5% (enters Strategic Framework Agreement with Crusoe for Deployment of Crusoe Spark Modular AI Factory Units to Deliver Crusoe Cloud)

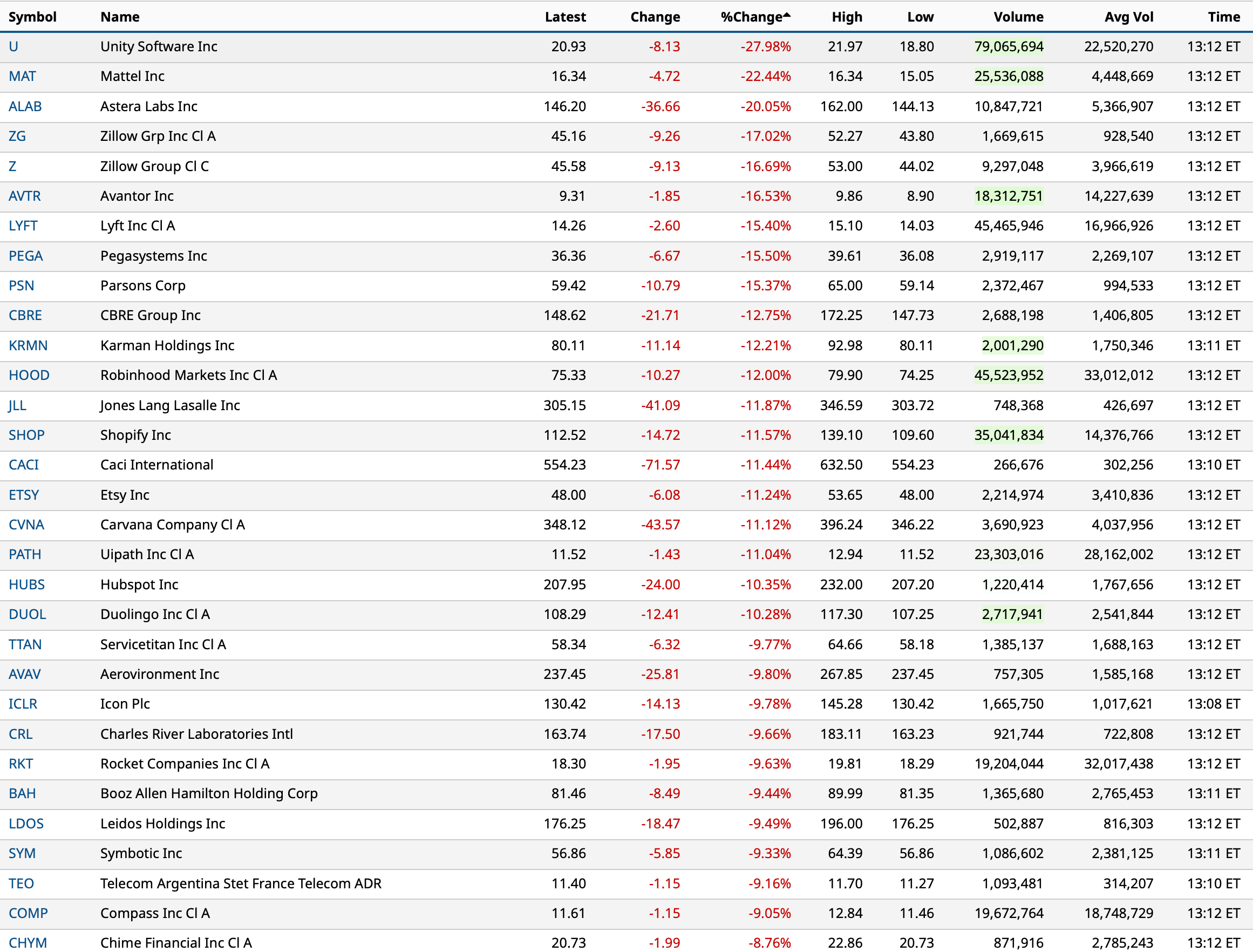

-MAT -28% (earnings, guidance)

-U -26% (earnings, guidance)

-UPB -23% (Phase 2 VALIANT Trial of Verekitug for Treatment of Severe Asthma data)

-MBC -21% (earnings, guidance)

-LYFT -16% (earnings, guidance)

-AVTR -12% (earnings, guidance)

-ALAB -10% (earnings, guidance; grants Amazon Rights to Acquire 3.26M Shares via Warrant at Exercise $142.82/shr)

-HOOD -10% (earnings, color)

-MRNA -9.9% (receives Refusal-to-File Letter from U.S. FDA for Investigational Seasonal Influenza Vaccine, mRNA-1010 citing lack of "adequate and well-controlled" study with a comparator arm)

-KHC -6.6% (earnings, guidance)

-HUM -6.2% (earnings, guidance)

-Z -5.4% (earnings, guidance)

-TMUS -5.2% (earnings, guidance)

-DUOL -5.1% (TMUS offers AI live translation on calls)

-CTGO -4.5% (prices $50M Underwritten Offering of 1.7M Shares and Pre-funded Warrants at $24.95/unit)

-R -3.8% (earnings, guidance)

-SN -3.4% (earnings, guidance; announce share buyback)

-APP -3.0% (lower in sympathy with U)

-THC -3.0% (earnings, guidance)

BY Doug Kass · Feb 11, 2026, 9:20 AM EST

I will be shorting Index calls on the opening if futures continue to be strong (+40 handles).

BY Doug Kass · Feb 11, 2026, 9:19 AM EST

BY Doug Kass · Feb 11, 2026, 9:15 AM EST

BY Doug Kass · Feb 11, 2026, 9:10 AM EST

BY Doug Kass · Feb 11, 2026, 9:00 AM EST

On the gap in futures higher I am adding to my very small Index short:

* (SPY) $695.32

* (QQQ) $614.81

BY Doug Kass · Feb 11, 2026, 8:50 AM EST

BY Doug Kass · Feb 11, 2026, 8:40 AM EST

9:30 a.m.: Fed Bank of Kansas City President Schmid (Non-Voter) speaks on monetary policy and the economic outlook before the Economic Forum of Albuquerque, in Albuquerque, N.M.;

10:15 a.m.: Fed Vice Chair for Supervision Michelle Bowman (Voter) participates in "Supervision and Regulation" discussion before virtual Keefe, Bruyette & Woods 33rd Annual Winter Financial Services Conference, Wash-ington, DC (Livestream available. No text. Q&A from moderator);

4:00 p.m.: Fed Bank of Cleveland President Hammack (Voter) participates in Leadership Dialogue, "Exploring Leadership, Economic Policy, and Career Pathways in Public Service" Leadership Dialogue hosted by the OhioState University John Glenn College of Public Affairs, in Columbus, OH

11:30 a.m.: Treasury hosts a $69 billion; 17-Week Bill Auction; 2:00 p.m.: Federal Budget Balance (January); 1:00 p.m.;Treasury hosts a $42B 10-Year Note Auction

BY Doug Kass · Feb 11, 2026, 8:25 AM EST

From JPMorgan:

US: Futs are flat ahead of NFP with the market having less conviction in a strong print after the Retail Sales miss and weaker high-frequency data. Bond yields are down 1bp across the curve and USD is weaker for the 4th consecutive session. Cmdtys are rallying led by Energy, Copper, and Precious Metals. Pre-mkt, Mag7 names are mostly lower, but on low magnitude; Discr / Energy / Indu / Mat all higher pointing to a potential broad-based cyclical rally if TMT returns are muted. AI ex-Mag7 is seeing a bid, too. Today’s macro data focus is on the NFP release but watch Mtge App given the strength of the recent Homebuilders bid.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Yesterday’s Retail Sales print and subsequent yield curve flattening have put the market on alert for a potential narrative shift. We wrote the following in the CPI Scenario Analysis note that we published yesterday and reposted below:

Given the weaker than expected Retail Sales prints and multiple clients pointing to high-frequency data, including weekly ADP, as indicators that NFP will miss to the downside, this CPI print has taken on heightened importance. While this week’s data releases may still show a Goldilocks environment, there is the risk of a stagflationary reading. My colleague Mark Whitworth flags today’s (Feb 9) move in Rates, where you have a strong bull flattening, as the market expressing a view that the macro data is going to turn softer and is adding duration ahead of the next batch of risk events. Further, steepeners had been a consensus trade, so some unwind into a more uncertain macro data environment makes sense. In Equities, we are seeing a rebound in Software accompanying a reboot of AI and weakness in Momentum (shorts covered, longs sold). Where from here? We agree that a hawkish print is more likely than a dovish print, but we do not see the market reacting strongly to a stagflationary print, e.g., Cyclicals sold, Staples sold, strong rebalance into things like Secular Growth / MegaCap Tech / Healthcare.

Putting it together, this is what I am thinking, do let me know if you disagree:

· NFP (inline / higher) / CPI (hawkish) – BULLISH. This was the market narrative entering this week and is aligned with the US Mkt Intel view.

· NFP (inline / higher) / CPI (dovish) – GOLDILOCKS. Look for Cyclicals / Reflationary sectors / sub-sectors to lead higher with support from MegaCap Tech. If the yield curve bull flattens, this would engage higher beta plays and induce further squeezing.

· NFP (weaker) / CPI (hawkish) – STAGFLATION. Negative for stocks. Turn to Secular Growth to outperform as indices decline; relative value trade likely the way forward in Equities. Commodities become the best asset class.

· NFP (weaker) / CPI (dovish) – MILDLY BEARISH. think the trading environment looks similar to the Feb 9 session, where the market expresses a desire for Defensive assets but one where the fundamental story remains intact, for now, so the broadening theme continues to work. If late-Feb / March macro prints were to continue this trend, calls for rate cuts would spike; currently, June is showing ~59% chance of a 25bp cut and a repeat of this data over the next 3 weeks likely takes that towards 100%. It is unclear whether pricing in a full rate cut with 2.5 – 3 months of macro data ahead of that cut is enough to reignite the bull rally. The increase in market breadth would be great for stock pickers but likely means that the index is stuck in a very tight range.

NFP SCENARIO ANALYSIS – the full Mkt Intel note is here

Feroli’s full NFP preview is here. He sees 75k jobs being added and the unemployment rate (U.3) holding at 4.4%. For Average Hourly Earnings, he sees +0.3% MoM and +3.6% YoY.

The following scenario analysis is NOT A PRODUCT OF JPM RESEARCH, this is a trading desk view from JPM US Market Intelligence.

· [5%] Above 110k. SPX is down 0.5% – 1%

· [20%] Between 90k – 110k. SPX gains 0.25% to 1%

· [40%] Between 60k – 90k. SPX gains 0.25% – 0.75%

· [30%] Between 30k – 60k. SPX loses 0.25% to gains 0.5%

· [5%] Below 30k. SPX is down 0.5% to 1.25%

· WHAT ARE OPTIONS PRICING? For options expiring on February 11, the market is pricing ~1.2% move, as of market close on Feb 6.

· US MKT INTEL ON NFP – Real-time data points to slightly higher downside risk but we see an in line print supporting the markets after a week of turbulence. The key remains the unemployment rate given the significant downshift in population growth. Similar to implied vol, we cannot directly observe the real-time NFP break-even, but we think it is ~30k jobs vs. ~250k in 2023. A step-down in the unemployment rate would be positive for stocks subject to how much the yield curve adjusts. As of Friday’s close, the bond market is pricing ~55bp of cuts this year. We think the print falls in the Goldilocks zone but one that is too hot will trigger a repricing of the yield curve higher and the elevated bond vol likely produces a down for stocks and one that is too cool will have the market on edge that the Fed is late to resuming its easing cycle and with Powell unlikely to cut before his term as Fed Chair ends, means that first cut would be in June.

BY Doug Kass · Feb 11, 2026, 8:15 AM EST

BY Doug Kass · Feb 11, 2026, 8:00 AM EST

BY Doug Kass · Feb 11, 2026, 7:50 AM EST

"Spend each day trying to be a little wiser than you were when you woke up. Day by day and at the end of the day — if you live long enough — like most people, you will get out of life what you deserve."

- Charlie Munger

Growing old is mandatory, but growing up is optional.

BY Doug Kass · Feb 11, 2026, 7:40 AM EST

BY Doug Kass · Feb 11, 2026, 7:30 AM EST

BY Doug Kass · Feb 11, 2026, 7:20 AM EST

BY Doug Kass · Feb 11, 2026, 7:10 AM EST

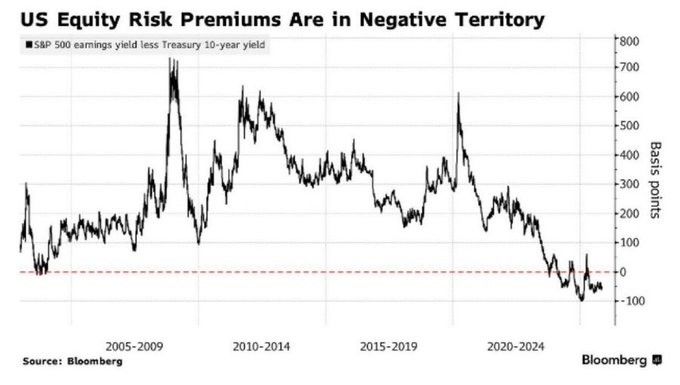

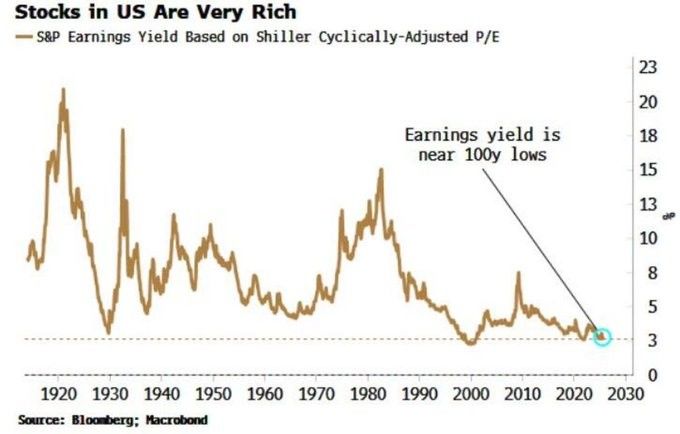

At the core of my negative market view is that the equity risk premium (ERP) has morphed into an equity risk discount (ERD!).

This means, on a risk-adjusted basis, equities offer a zero return to investors.

It also means that investors embrace the absurd belief that there is more risk in bonds than stocks:

As part of the ERP, the earnings yield (inverse of the P/E ratio) is near a century-year-old low. The only time it was lower was during the dot-com bubble:

This means that, if history prevails, we are likely at a very poor launching pad for future investment returns.

BY Doug Kass · Feb 11, 2026, 7:00 AM EST

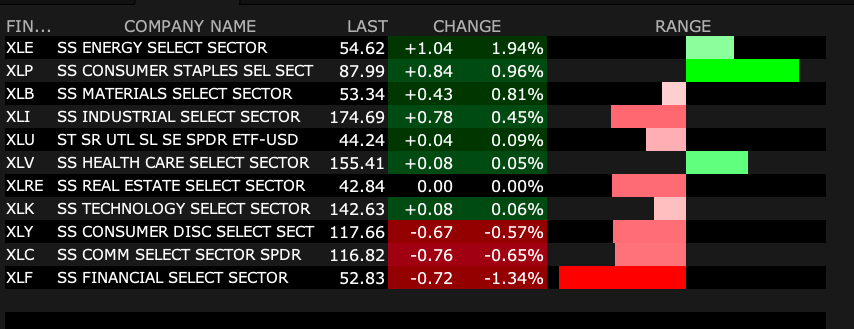

* Technicians have been universally optimistic about financial stocks...

Bonus — Here are some great links:

Last Year's Winners Are This Year's Losers

BY Doug Kass · Feb 11, 2026, 6:45 AM EST

BY Doug Kass · Feb 11, 2026, 6:35 AM EST

Despite protestations from the Mag 7 adherents, tech remains expensive:

BY Doug Kass · Feb 11, 2026, 6:25 AM EST

BY Doug Kass · Feb 11, 2026, 6:15 AM EST

Wolf Street howls about household debt.

BY Doug Kass · Feb 11, 2026, 6:05 AM EST

The S&P Oscillator remains overbought at 2.73% vs. 2.23%.

BY Doug Kass · Feb 11, 2026, 5:55 AM EST

Back shorting the indices last night:

Dougie Kass

Back reshorting indices with s and p futures +19 handles (835 PM):

BY Doug Kass · Feb 11, 2026, 5:49 AM EST