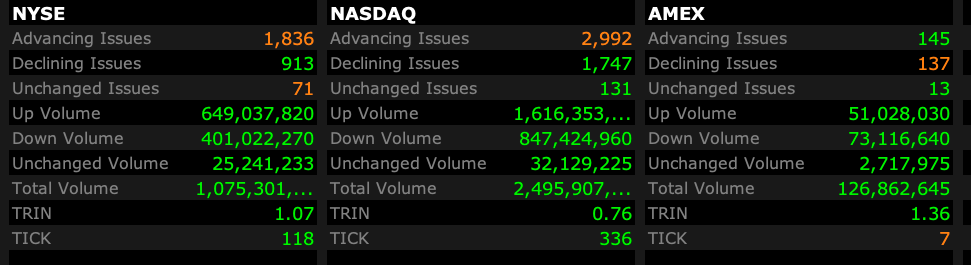

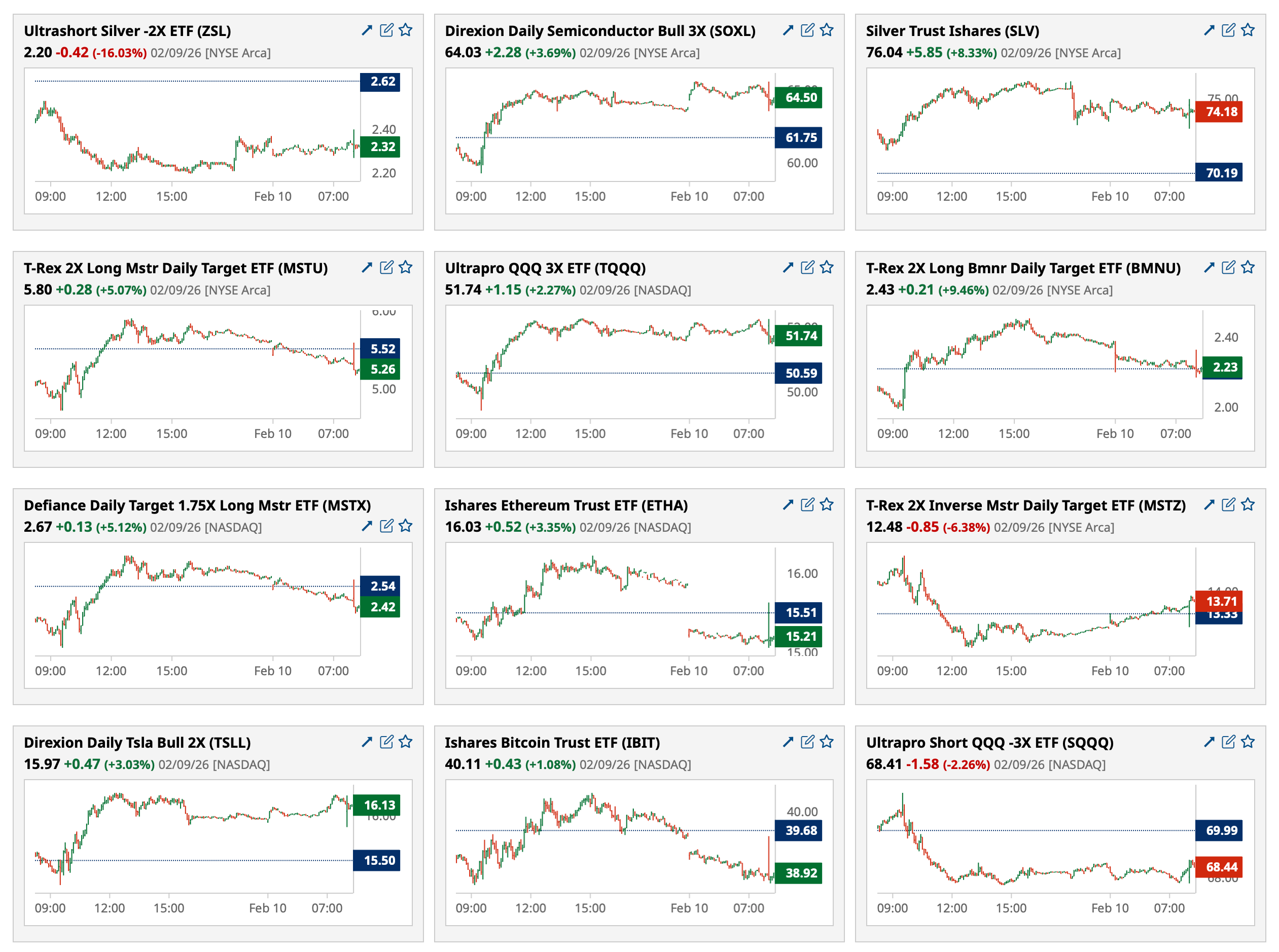

After-Hours Advancers and Decliners

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Feb 10, 2026, 4:55 PM EST

BY Doug Kass · Feb 10, 2026, 4:55 PM EST

BY Doug Kass · Feb 10, 2026, 4:45 PM EST

- NYSE volume 6% below its one-month average;

- NASDAQ volume 7% below its one-month average;

- VIX index: up 2.59% to 17.81

BY Doug Kass · Feb 10, 2026, 4:27 PM EST

Markets usually fall on unexpected news.

Case in point:

BY Doug Kass · Feb 10, 2026, 4:11 PM EST

With S&P cash -26 handles I am covering my short calls put on when equities were well in the black.

BY Doug Kass · Feb 10, 2026, 4:04 PM EST

No trades since shorting index calls.

BY Doug Kass · Feb 10, 2026, 3:43 PM EST

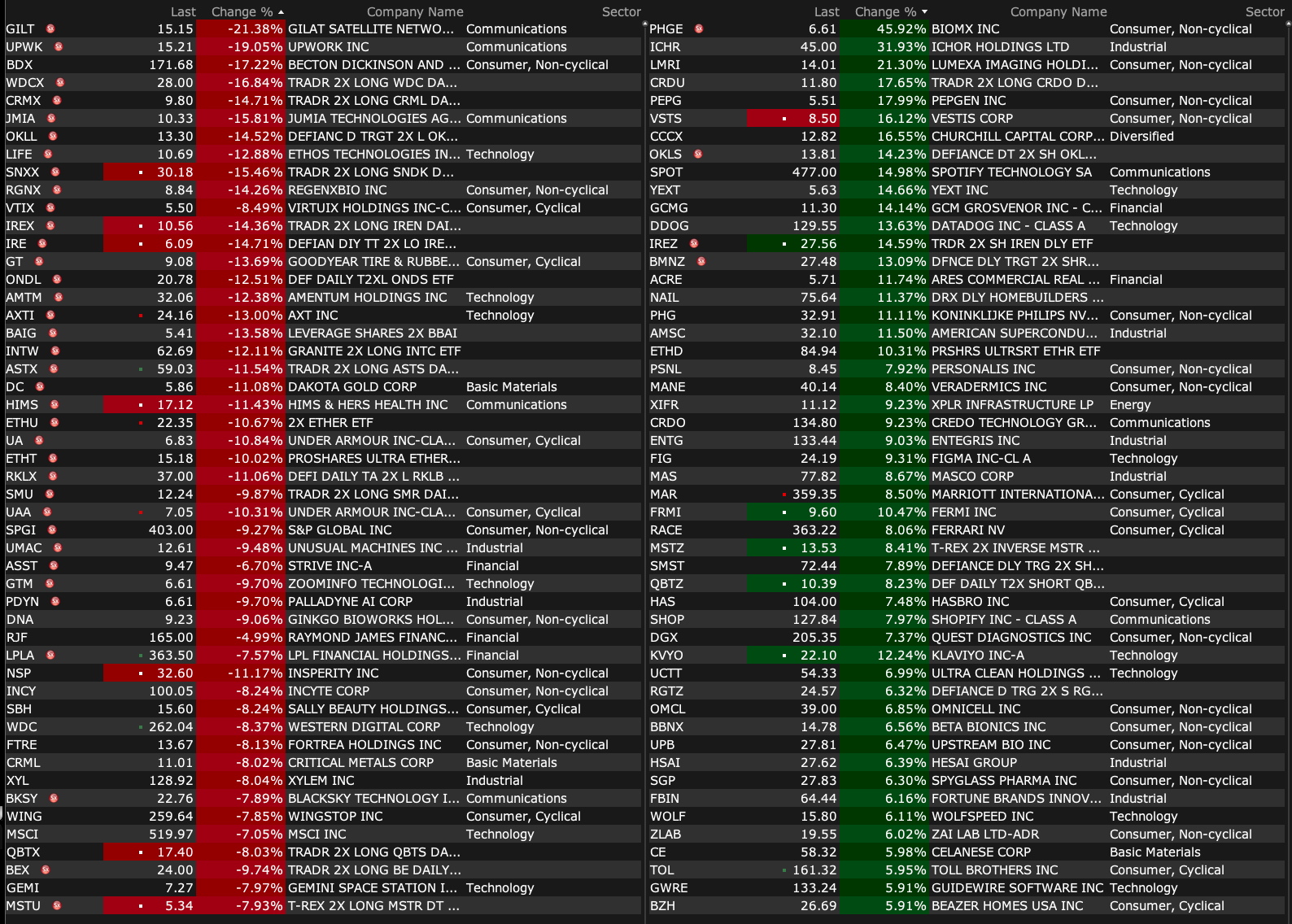

A closer look at the largest % decliners in financials after Altruist announced an artificial intelligence tool that it says can create personalized tax strategies by interpreting financial documents without manual entry.

BY Doug Kass · Feb 10, 2026, 3:07 PM EST

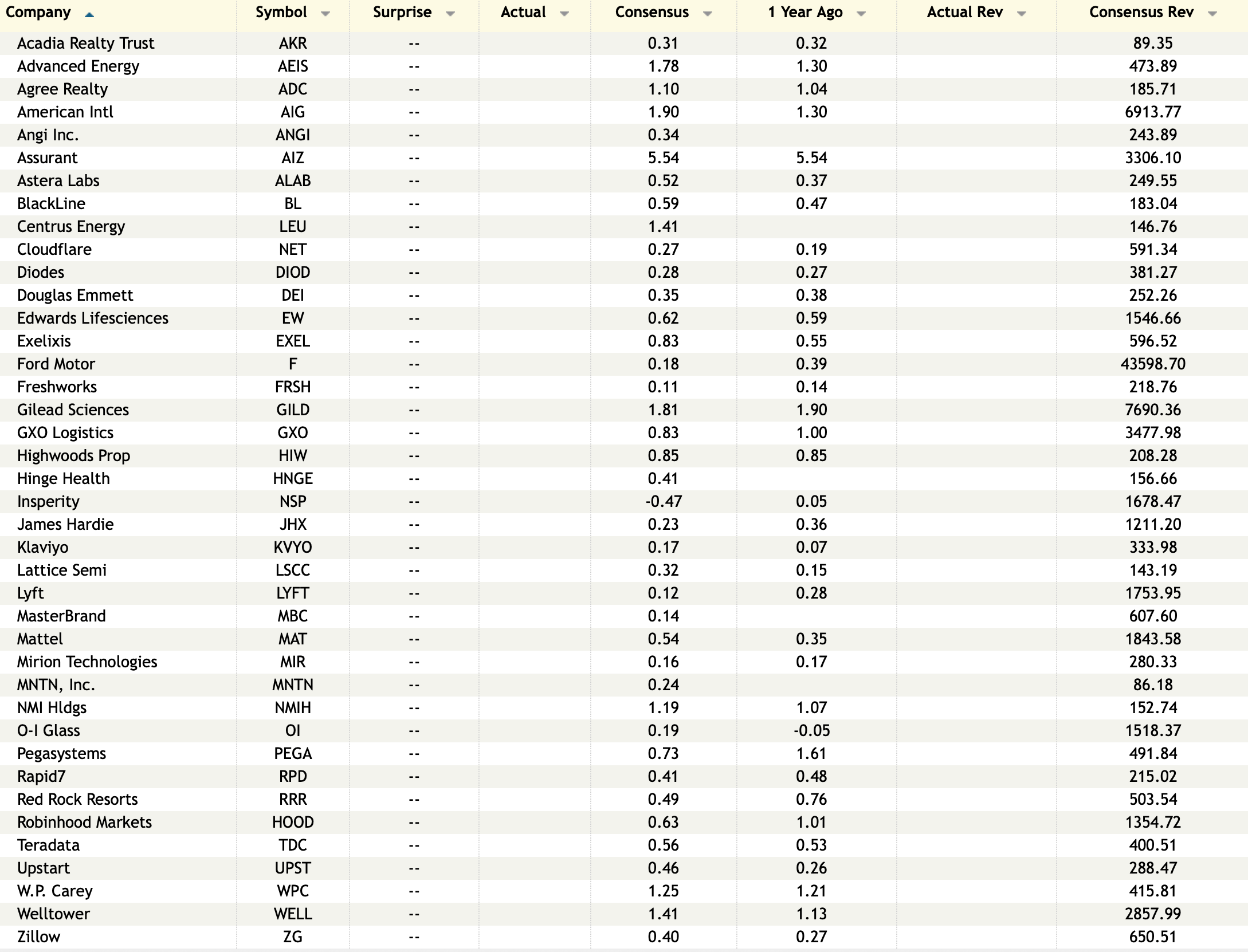

Earnings After the Close Tuesday, Feb. 10

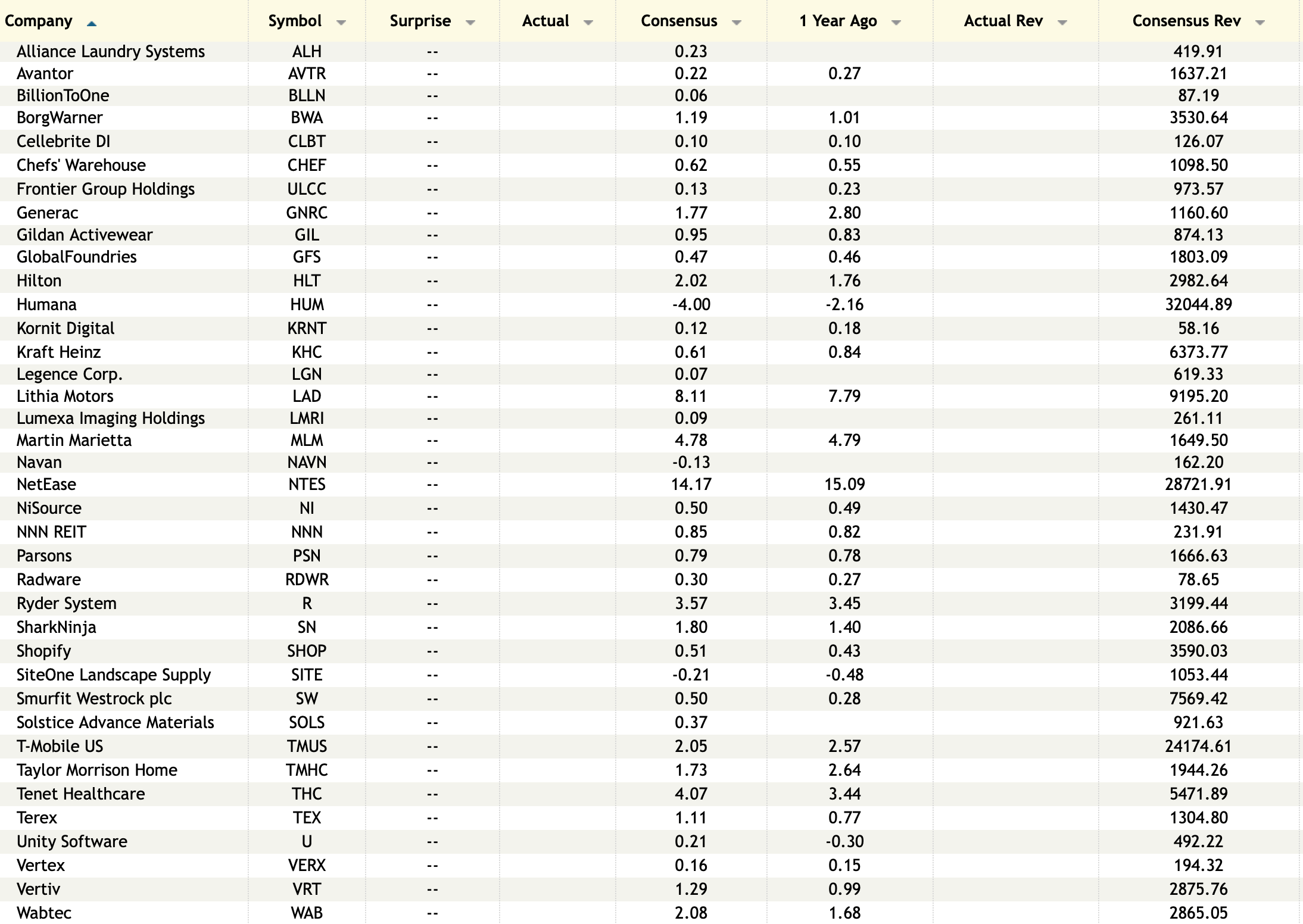

Earnings Before the Open Wednesday, Feb. 11

BY Doug Kass · Feb 10, 2026, 2:44 PM EST

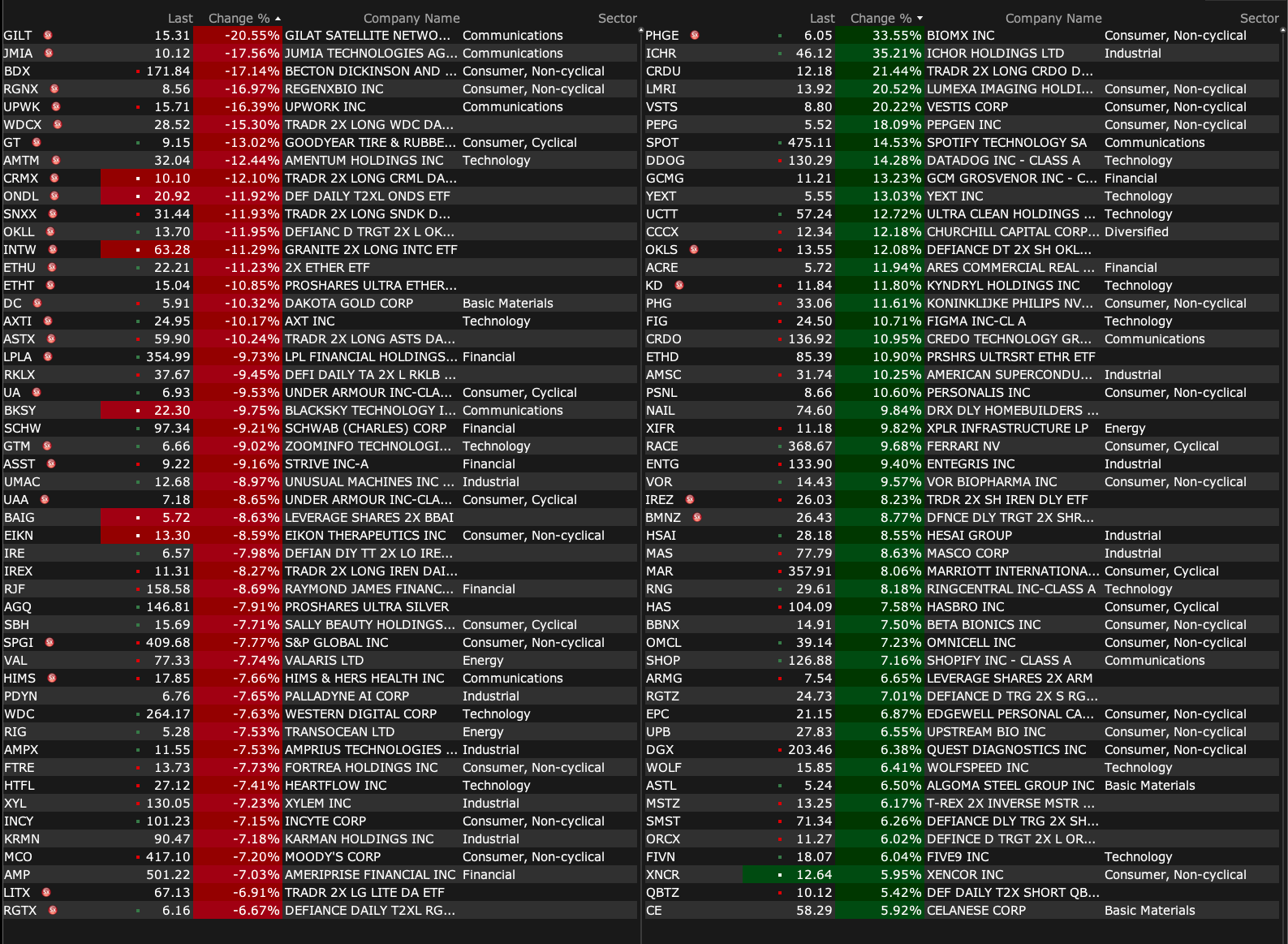

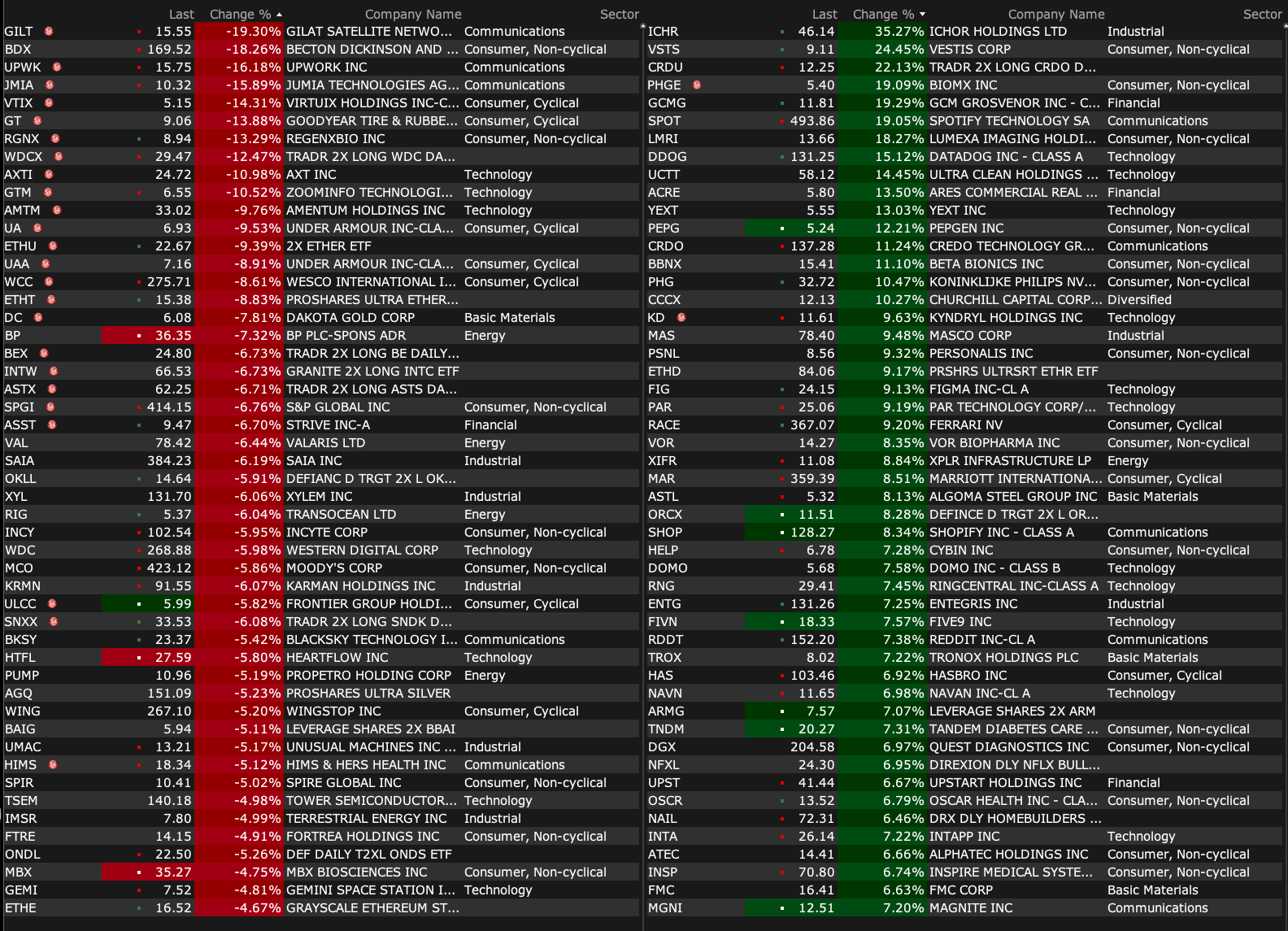

% Movers at 1:30 pm

BY Doug Kass · Feb 10, 2026, 1:38 PM EST

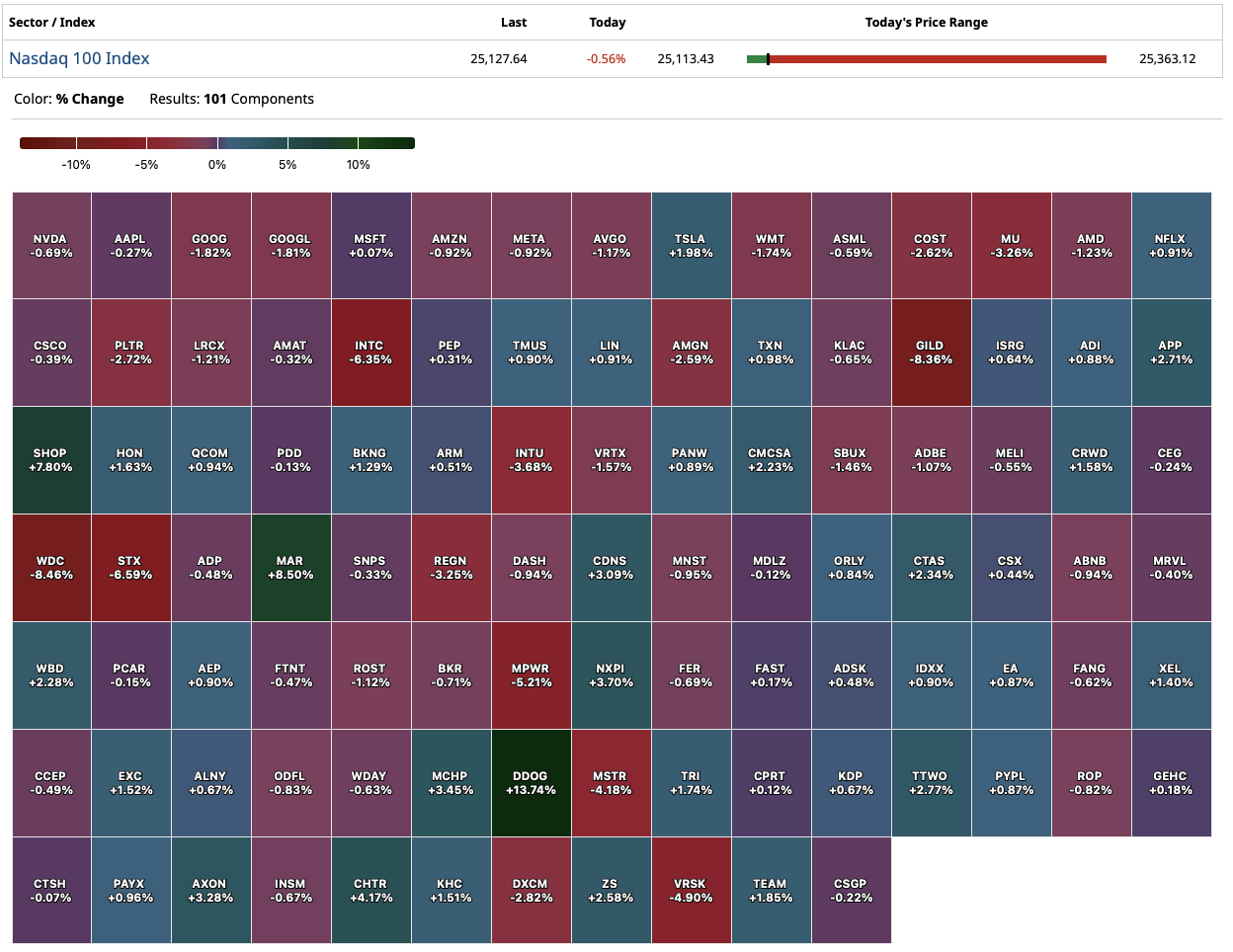

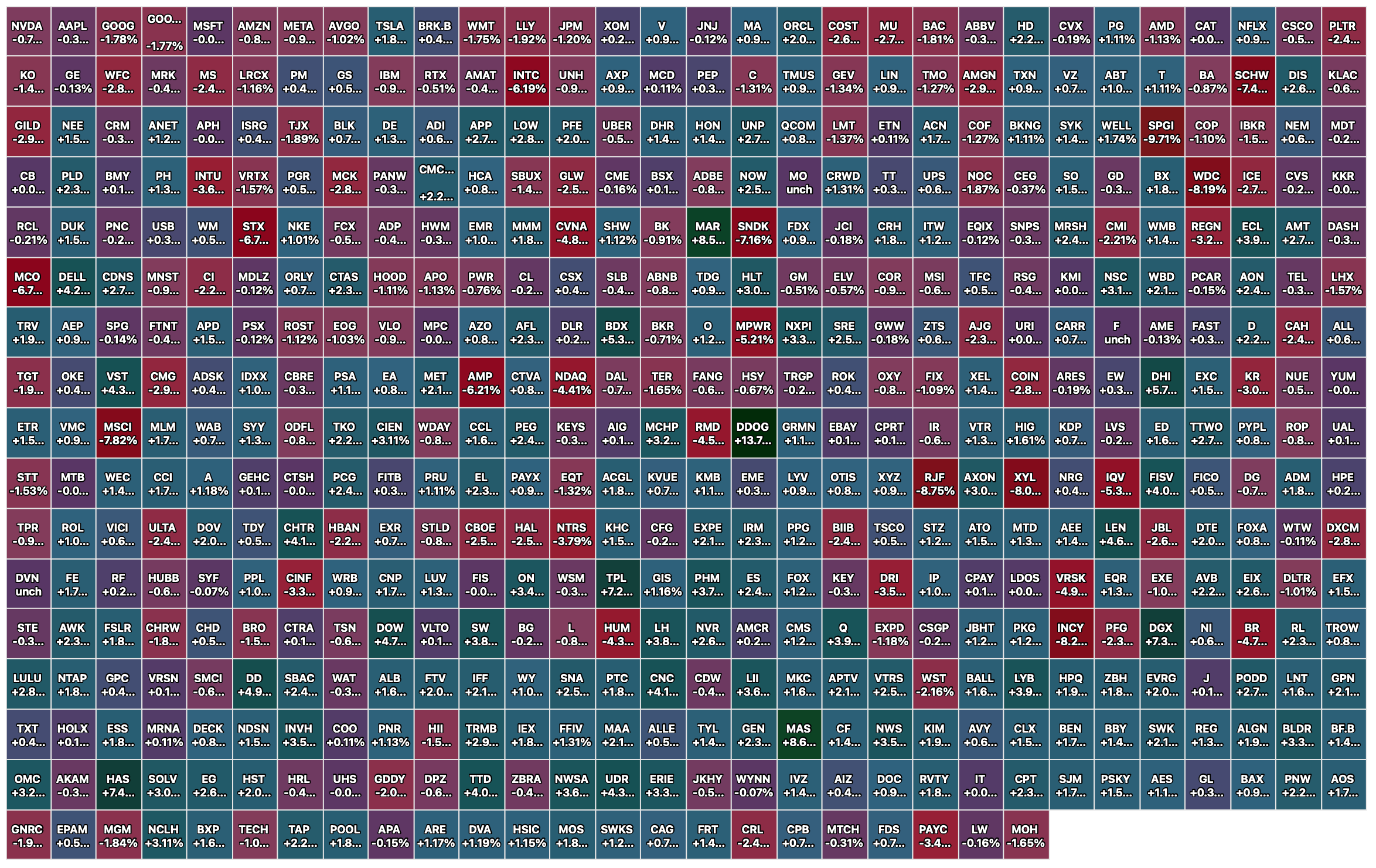

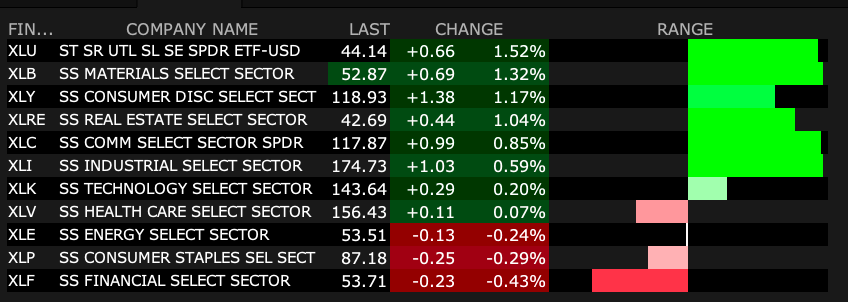

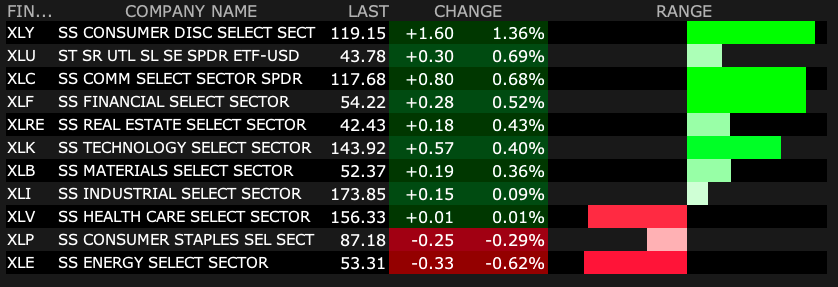

S&P 500 Sectors

Intraday Financials

BY Doug Kass · Feb 10, 2026, 12:58 PM EST

BY Doug Kass · Feb 10, 2026, 12:00 PM EST

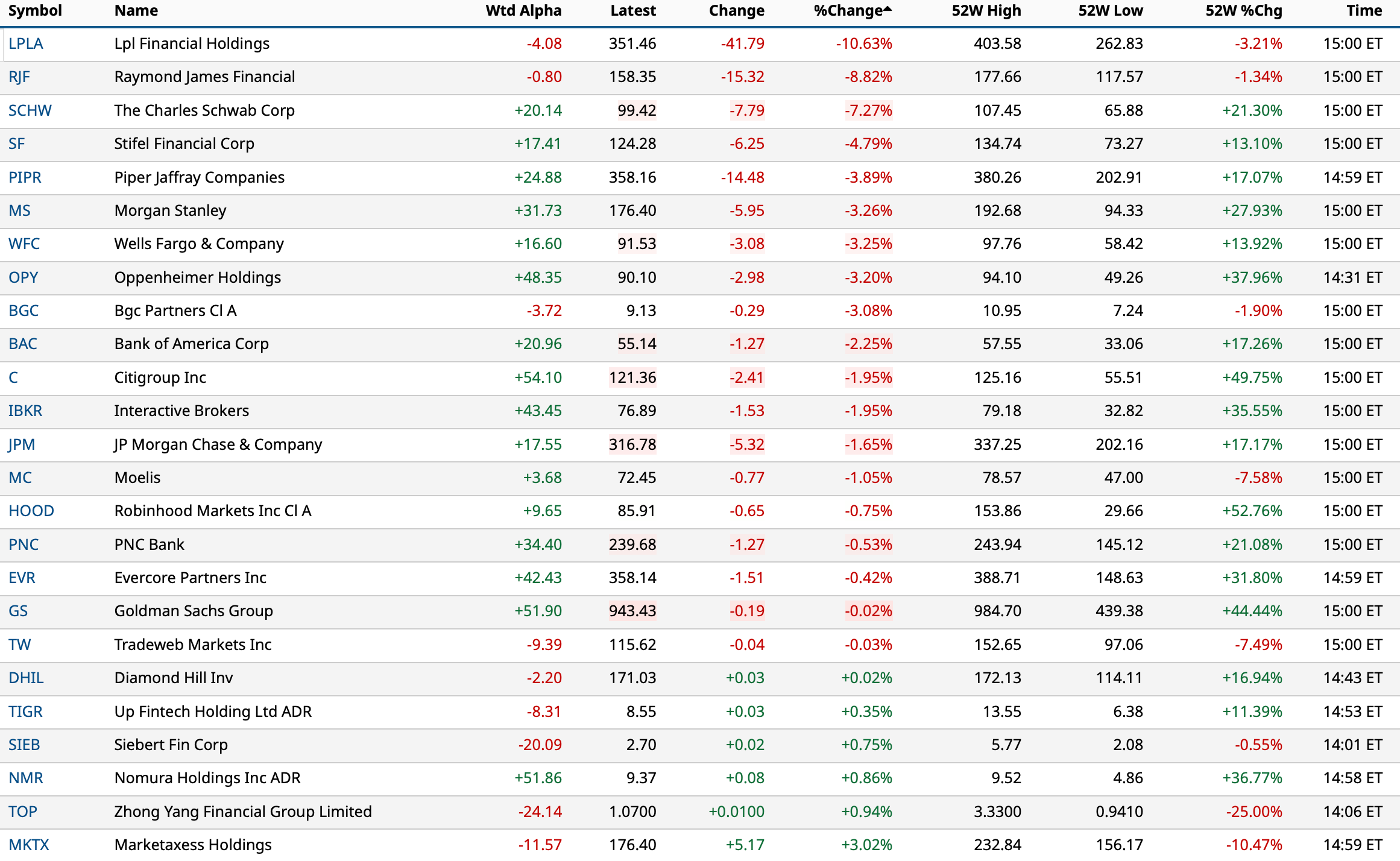

(SCHW)

(MS) and Other Financials

BY Doug Kass · Feb 10, 2026, 11:26 AM EST

- NYSE volume 14% below its one-month average;

- Nasdaq volume 16% below its one-month average;

- VIX index: down 0.75% to 17.23

BY Doug Kass · Feb 10, 2026, 11:10 AM EST

The "programs" continue to pay up for software.

BY Doug Kass · Feb 10, 2026, 11:00 AM EST

I am back short Tesla (TSLA) ($423.78).

BY Doug Kass · Feb 10, 2026, 10:49 AM EST

BY Doug Kass · Feb 10, 2026, 10:45 AM EST

BY Doug Kass · Feb 10, 2026, 10:40 AM EST

Tech (XLK) vs Financials (XLF) at 10:02 AM:

BY Doug Kass · Feb 10, 2026, 10:25 AM EST

With S&P cash +16 handles I am adding to short index calls (and I have converted short index common to short calls).

BY Doug Kass · Feb 10, 2026, 10:17 AM EST

I added to (GRNY) short at $25.30.

I plan to move to large-sized on further strength, given the nature of the exchange-traded funds high octane/beta constituent holdings.

BY Doug Kass · Feb 10, 2026, 9:41 AM EST

I just shorted (QQQ) (to add to my (SPY) short earlier this morning):

* QQQ $615.74

BY Doug Kass · Feb 10, 2026, 9:26 AM EST

-EVMN +93% (EVO301 Phase 2a trial, in moderate-to-severe atopic dermatitis, met primary efficacy endpoint at week 12)

-PHIO +49% (Safety Monitoring Committee (SMC) completed planned safety review for all patients treated with INTASYL compound PH-762 in Phase 1b clinical trial; No dose-limiting toxicities or serious adverse events have been reported for any of the 22 enrolled patients)

-EWCZ +44% (to be taken private by General Atlantic at $5.80/shr cash for EV ~$330M)

-NKTR +24% (new REZOLVE-AD Maintenance Data in Atopic Dermatitis Demonstrate Rezpegaldesleukin Resulted in Durable and New Responses Across Key Disease Measurements with Both Monthly and Quarterly Dosing)

-UNF +18% (said to renew merger discussions with Cintas)

-CRDO +15% (prelim Q3 revenue)

-DDOG +14% (earnings, guidance)

-PSNL +14% (receives Medicare Coverage for NeXT Personal in Lung Cancer Surveillance)

-VELO +14% (qualified as First Additive Manufacturing Vendor for U.S. Army Ground Vehicles)

-SPOT +10% (earnings, guidance)

-RACE +9.1% (earnings, guidance)

-CCO +8.6% (agrees to be acquired by Mubadala Capital and TWG Global for $2.43/shr in cash)

-MAS +7.2% (earnings, guidance)

-OSCR +7.1% (earnings, guidance)

-SNOW +5.3% (higher in sympathy with DDOG)

-U +5.1% (Oppenheimer Raised U to Outperform from Perform, price target: $38)

-MDB +4.9% (higher in sympathy with DDOG)

-ENTG +4.9% (earnings, guidance)

-TRMB +3.4% (earnings, guidance)

-SNAP +2.9% (Arete Capital Partners Raised SNAP to Buy from Neutral, price target: $7.30)

-TSM +2.3% (earnings, guidance)

-HAS +2.2% (earnings, guidance)

-MAR +2.2% (earnings, guidance)

-DD +2.1% (earnings, guidance)

-TECX -38% (discontinues AZD3427 for heart conditions)

-GTM -22% (earnings, guidance)

-MCO -11% (weak S&P Global 2026 outlook)

-HOG -10% (earnings, guidance)

-GT -8.6% (earnings, guidance)

-MORN -8.4% (weak S&P Global 2026 outlook)

-MSCI -6.6% (weak S&P Global 2026 outlook)

-UA -6.2% (CitiGroup Cuts UAA to Sell from Neutral, price target: $6.20)

-FISV -4.4% (earnings, guidance)

-ULCC -4.3% (Deutsche Bank Cuts ULCC to Hold from Buy, price target: $6)

-INCY -4.2% (earnings, guidance)

-HIMS -4.1% (downside momentum)

-KO -3.9% (earnings, guidance)

-SAIA -3.8% (earnings, guidance)

-BP -3.5% (earnings, guidance; suspends share buybacks)

-CRM -3.1% (said to have 'quietly' laid off fewer than 1,000 workers in a new round of cuts)

-ON -3.0% (earnings, guidance)

-WING -2.9% (multiple broker downgrades)

-JMIA -2.4% (earnings, guidance)

-COIN -2.0% (hearing price target cut at JPM)

BY Doug Kass · Feb 10, 2026, 9:18 AM EST

BY Doug Kass · Feb 10, 2026, 9:07 AM EST

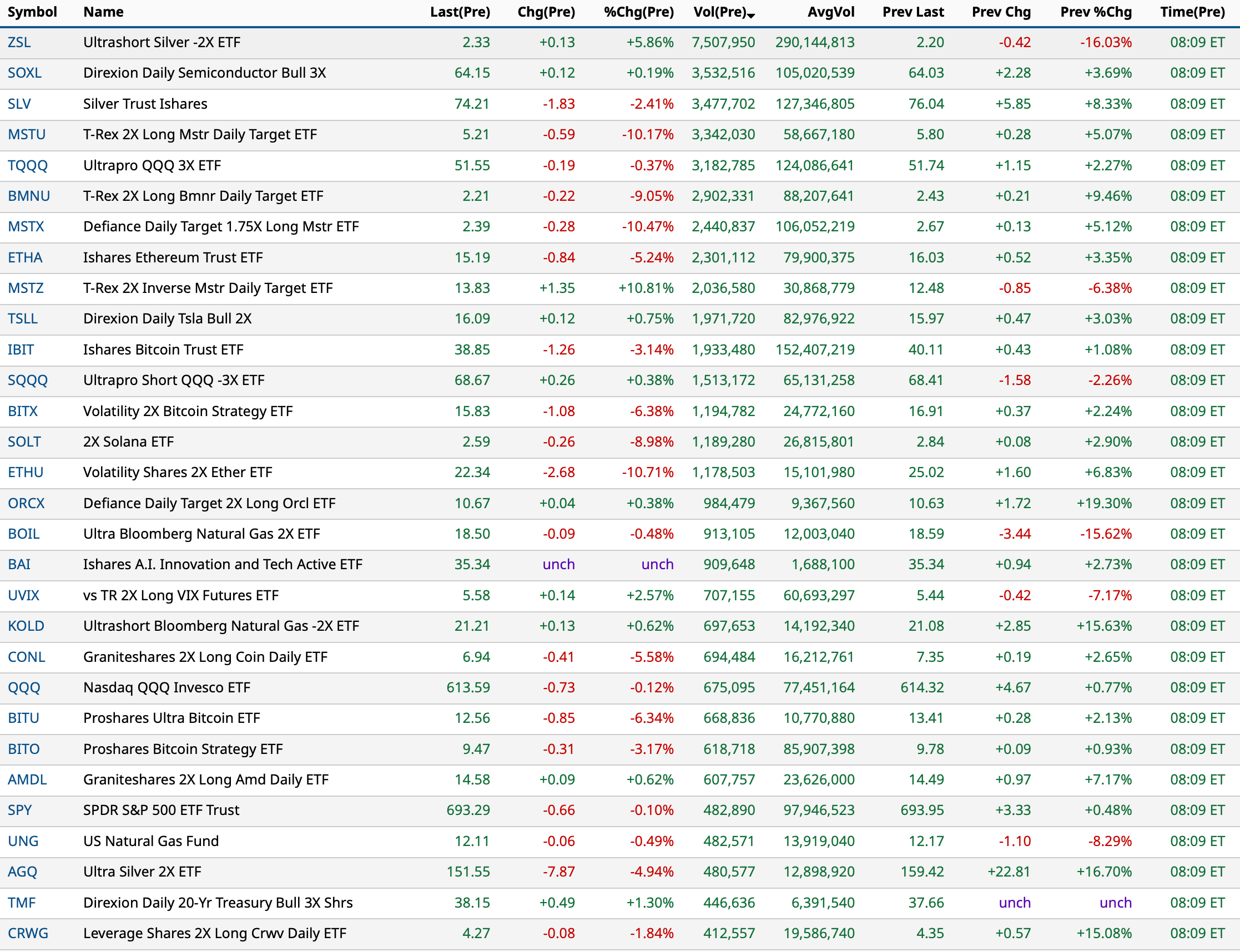

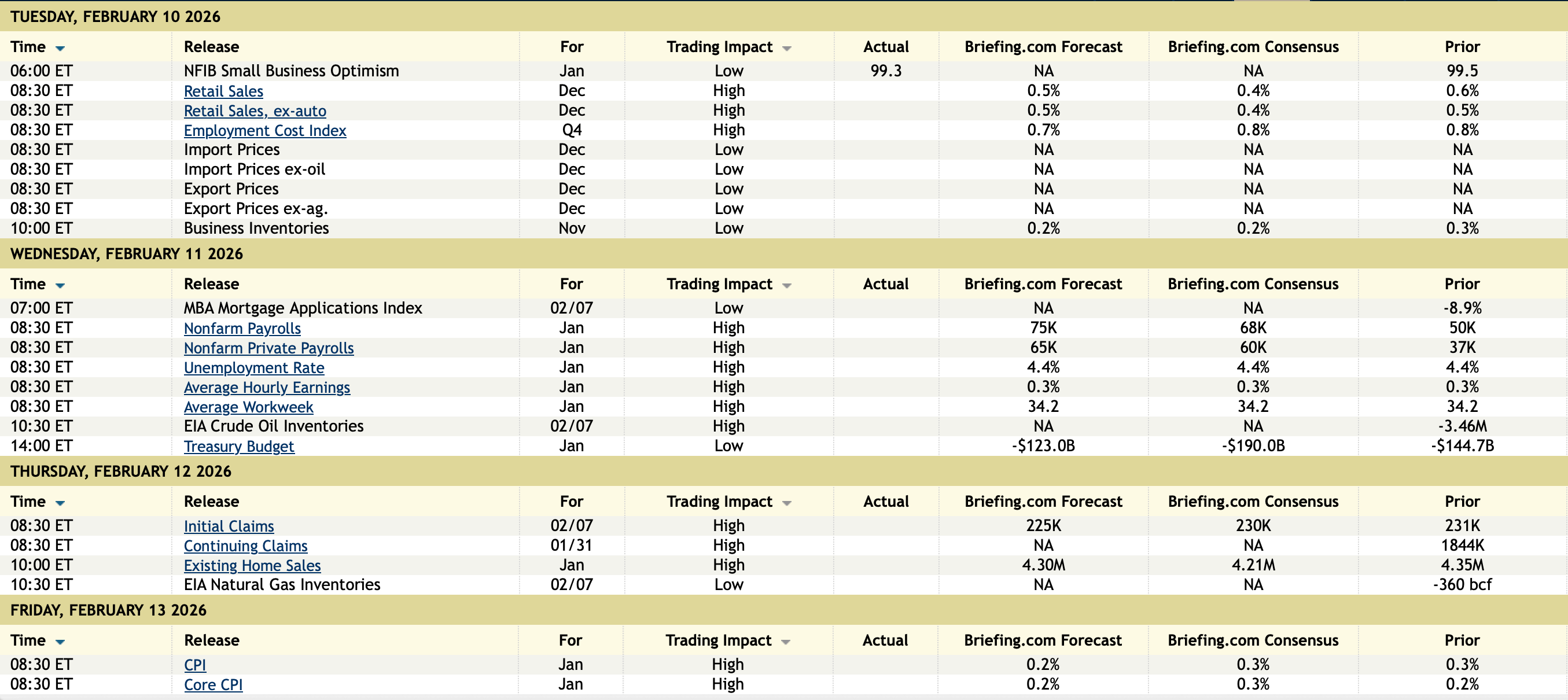

Charts from 8:09 a.m. ET.

BY Doug Kass · Feb 10, 2026, 8:57 AM EST

12:00 p.m.: Fed Bank of Cleveland President Hammack (Voter) speaks on "Banking and the Economic Outlook" before the 2026 Ohio BankersLeague Economic Summit, Columbus, OH (Text available. Q&A expected. Livestream at youtube.com/@ClevelandFed);

1:00 p.m.: Fed Bank of Dallas Pres-ident Logan (Voter) speaks and participates in moderated question-and-answer session before the 2026 Asset Management Derivatives Forum hosted by SIFMA andFIA, Austin, TX (Text available. No audience Q&A. Virtual access available)

11:00 a.m.: Treasury Announces a 4, 8 and 17 Week Bill Auction;

11:30 a.m.: Treasury hosts a $90B 6-Week Bill Auction;

1:00 p.m.: Treasury hosts a $58B 3-Year Note Auction;

2:00 p.m.: Treasury buyback (liq support)

BY Doug Kass · Feb 10, 2026, 8:43 AM EST

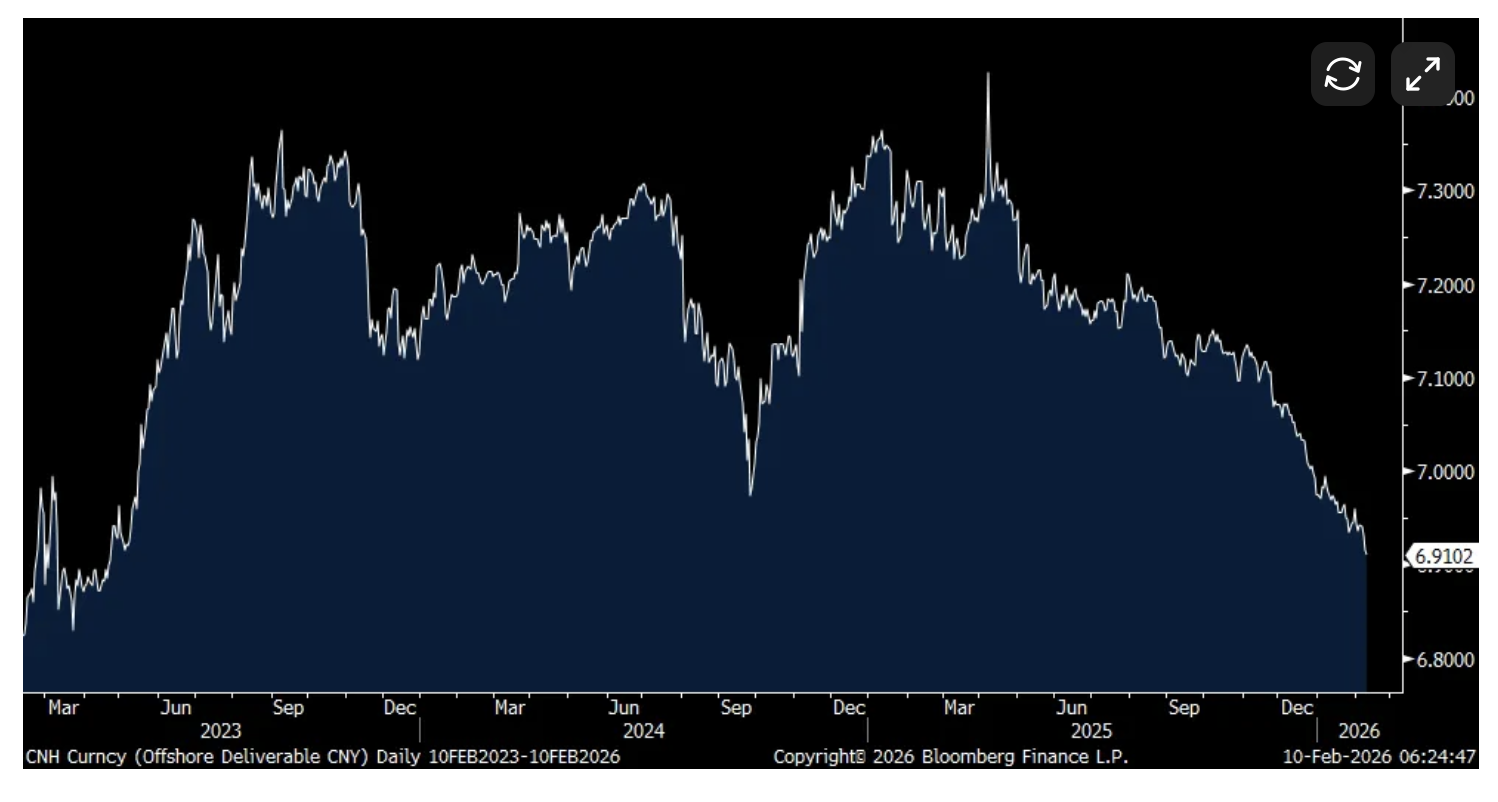

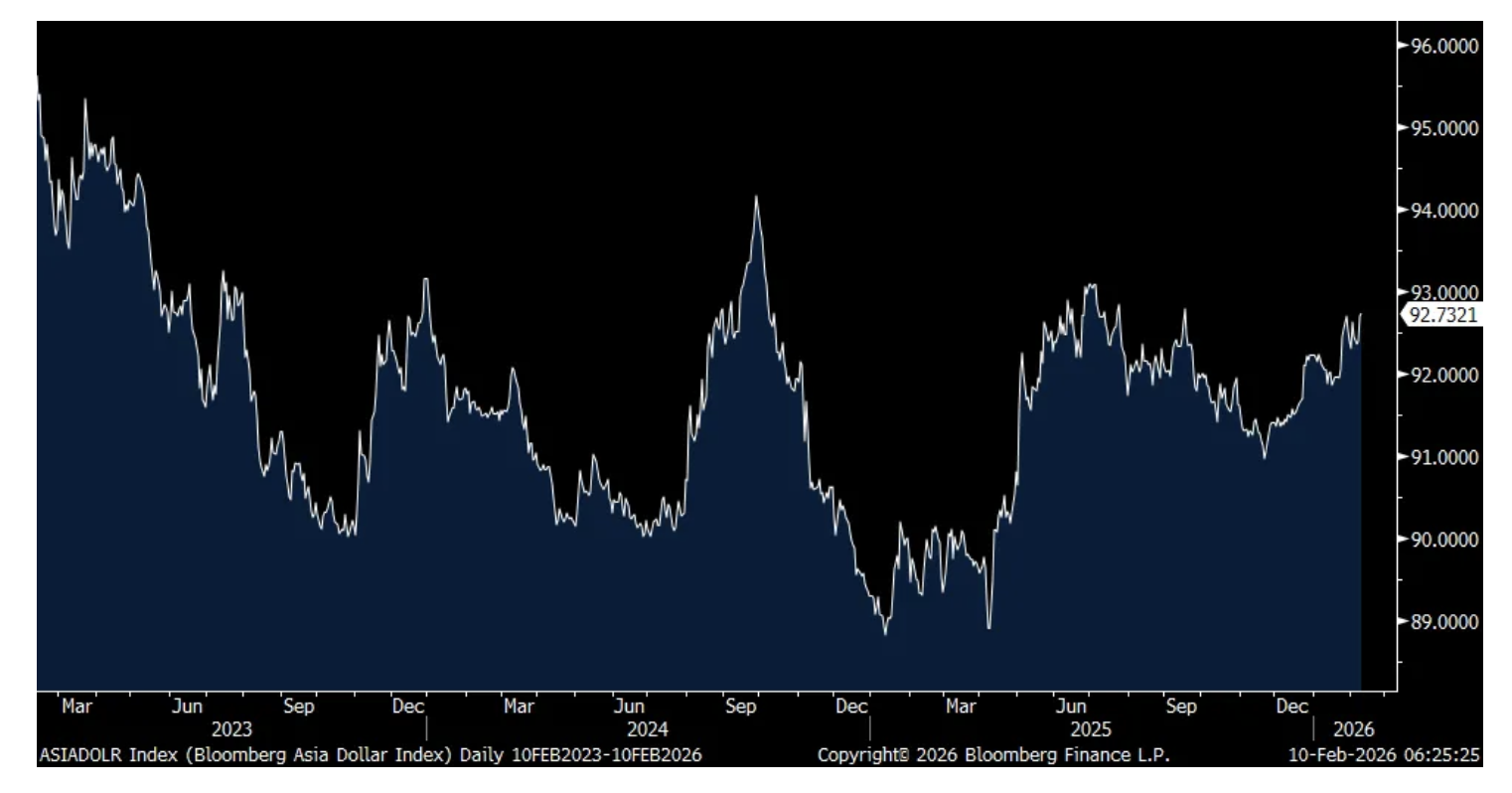

I want to highlight again the continued strength in the Chinese yuan which is now at the strongest level vs the US dollar since May 2023. This is not by accident, this is a concerted effort on the part of Chinese officials to have it strengthen and today’s move follows the story where authorities want banks to lessen their US Treasury holdings which means less foreign capital flows in US dollars. What this move also does is give cover for other Asian currencies to rally, particularly the Japanese yen which is up again with the 2 yr yield at a 30 yr high. And, it also means the Chinese will no longer be exporting deflation.

And if the yen ever gets legs to the upside, it also has major implications for global flows as I mentioned last week when considering the size of Japanese foreign asset holdings, particularly in the US that would lose money with US dollar weakness. I’ll argue again that international stocks and emerging market bonds will benefit again from the perspective of a US investor, as they did last year, to a weakening dollar and we are positioned as such.

Offshore Chinese Yuan (the lower it is, the stronger it is vs USD)

Bloomberg Asia/Dollar Spot index

Before we see CPI on Friday I want to highlight two inflationary trends, one on the downside, one on the upside. Rents continue to recede, mostly in the overbuilt sunbelt states. From the Camden Property Trust earnings call late last week, a stock we own and with an apartment portfolio mostly in the sunbelt states. In the seasonally slow Q4, rental rates “had new leases down 5.3% and renewals up 2.8% for a blended rate of negative 1.6%, which is fairly in line with what we saw in the fourth quarter of ‘24...Renewal offers for first quarter expiration’s were sent out with an average increase of 3% to 3.5% and as expected move-outs to purchase homes remain extremely low at 9.6% for the fourth quarter and 9.8% for the full year of 2025.”

For 2026 full year they expect “market rent growth of approximately 2% for our portfolio...with most of that growth occurring in the second half of the year.”

As I’ve said before, renters need to enjoy the deceleration in rent growth while they can because it won’t last. “On the supply front, it is clear that deliveries in almost all of our markets peaked during 2024 and continued to decline in 2025, setting up 2026 and 2027 to be below average years for new supply. Completions as a percentage of inventory peaked at nearly 4% for our portfolio in 2024 and are expected to be less than 2% this year and closer to 1.5% in 2027.”

UDR, a more coastal focused apartment REIT, expects same store revenue growth of 1.25% this year, down from 2.4% in 2025 but said this, “when demand unexpectedly weakened late in the third quarter, we quickly pivoted to a high-occupancy strategy. These maneuvers positioned the portfolio for a reacceleration of blended lease rate growth in the final months of 2025. This acceleration has continued into early 2026 along with sustained outsized other income growth, low resident turnover, and elevated occupancy.”

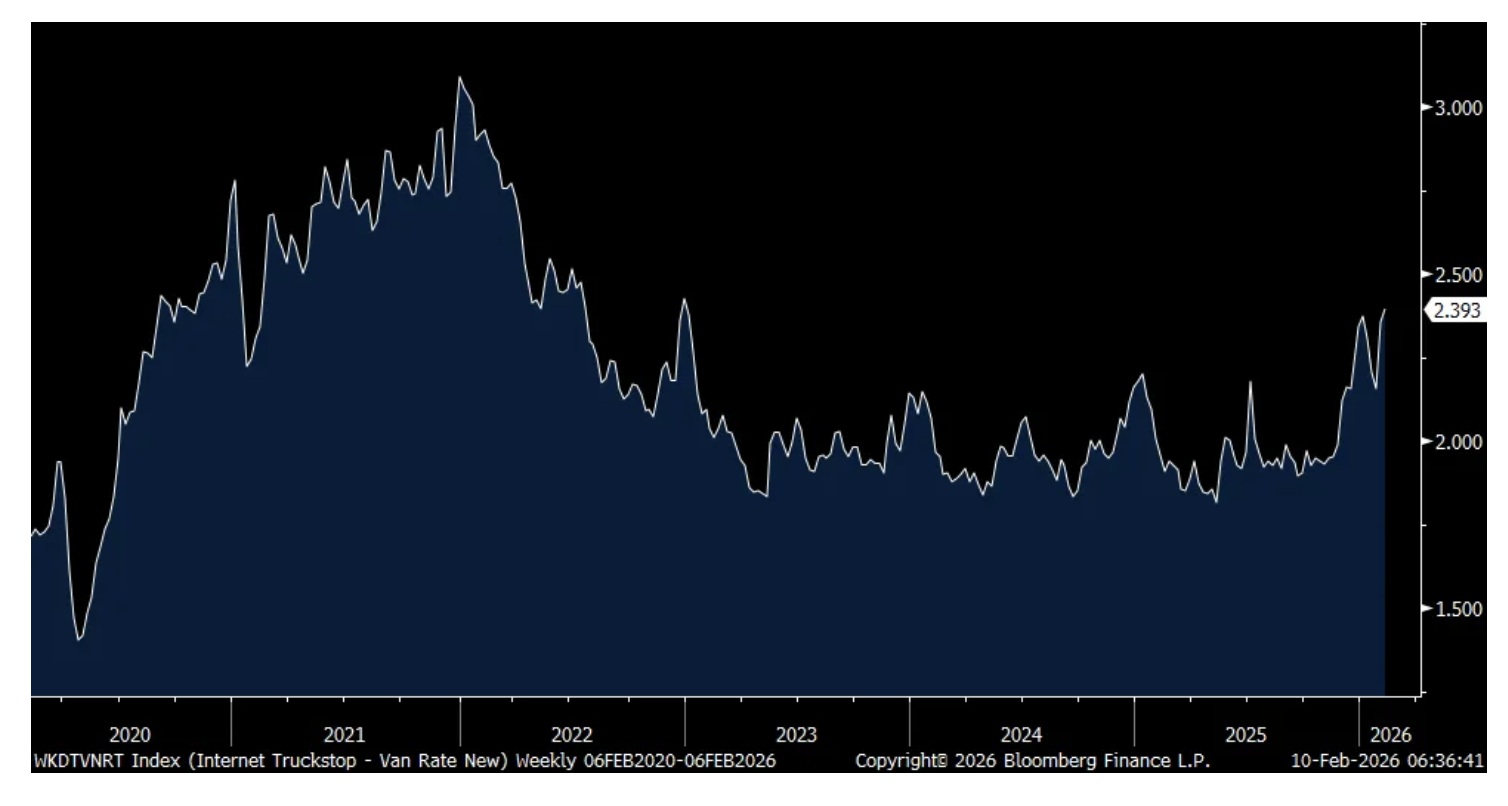

On the flip side, I’ve mentioned the firming up in trucking spot prices that has been cited by a bunch of trucking companies in their earnings reports because of capacity that is leaving the market, rather than due to a pick up in demand. The Internet Truckstop Weekly Van Rate Index as of Friday rose to the highest level since late 2022. So we have core goods prices seen in PPI running higher by about 3% and now we have truck transportation prices shifting higher.

Internet Truckstop Weekly Van Rate Index

The January NFIB Small Business Optimism index fell a touch to 99.3 from 99.5 in December and 99 in November. Plan to Hire slipped 1 pt to 16% which is back to the 6 month average. Reflecting both less demand and supply for labor, Positions Not Able to Fill fell 2 pts to the lowest since July 2020 and 2017 pre Covid. Compensation rose 1 pt to the best since June but comp plans slipped 2 pts.

After jumping by 9 pts last month, those that Expect Better Economy fell by 3 pts to 21% and compares with the 6 month average of 23%. After dropping by 5 pts, those that Expect Higher Sales rose 6 pts. Good Time to Expand rose 2 pts.

Capital spending plans, notwithstanding the tax incentives from the BBB, fell 1 pt to 18%, matching the lowest since 2010. I bolded to emphasize. Plans to Increase Inventory fell 1 pt. Those seeing Higher Selling Prices fell 4 pts to 26% but that is in line with the 6 month average. Positive Earnings Trends dropped 1 pt after rising by 3 last month.

The bottom line from the NFIB, “While GDP is rising, small businesses are still waiting for noticeable economic growth. Despite this, more owners are reporting better business health and anticipating higher sales.”

Labor quality declined as the single most important problem for the 3rd straight month but higher insurance costs rose by 4 percentage points to the most since December 2018. Higher taxes remained the biggest small business problem.

NFIB

In the January Consumer Expectations survey from the NY Fed, one year inflation expectations fell to 3.1% from 3.4% while holding steady further out. Lower home price expectations helped as it did for lower expectations for gas, rent and medical care. They were unchanged for food and higher for the cost of a college education.

Also of note in the survey, “Labor market expectations saw modest improvements with consumers reporting higher expected earnings growth, lower likelihood of a job loss, and higher likelihood of finding a job in the event of a job loss.”

To some earnings calls.

From Sally Beauty, a distributor of beauty stuff to salons and has thousands of stores:

“In our Sally segment (retail), while our customers remained choiceful, they demonstrated overall resilience in a challenging macro environment.”

With their distribution business, “top line results were roughly flat, with both net sales and comp sales down 20 bps to last year, as stylists continued to buy closer to need and seek value. Spending trends softened in tandem with the government shutdown, but rebounded nicely in December. While stylist appointment books were relatively busy, their customers were more cautious in their spending, with some pullback in in add-on services.”

Kering, the owner of Gucci among other brands, is higher by 10% in Paris today as while sales fell 10% last year, they improved in Q4. They said:

“the annual numbers don’t tell the whole story. The critical point is a sequential improvement. We delivered throughout the second half with Q4 showing a clear acceleration.”

“The acceleration in trends was visible across all segments returning to positive territory except for Gucci at group level in Q4.”

“Our conversion rate improved slightly...On the other hand, traffic remains soft.”

In North America specifically, Q4 delivered a 2% comparable growth, maintaining solid momentum with only a 1 point deceleration vs Q3. Despite a 5 point tougher comparison base, the higher end segment performed better and importantly, Gucci was flat in Q4 vs last year, marking the end of the decline in the region.”

Marriott just reported, its stock is rising pre market, and said this in their press release:

“International RevPAR increased 6%, led by EMEA and APAC, benefiting from solid leisure transient and cross border travel. In the US and Canada, RevPAR was roughly flat, reflecting the impact of the extended government shutdown primarily on the business transient segment. Globally, our luxury hotels continued to outperform during the quarter, with RevPAR rising over 6%, and performance moderating down the chain scales.”

From On Semiconductor, which is trading down pre market:

“we are seeing seasonal patterns and are encouraged by improving order trends across our core markets.”

“Automotive inventory digestion is largely behind us. AI data center is increasingly becoming a meaningful growth engine for the company and we believe we have seen the bottom for industrial with global PMI trends pointing to early signs of expansion.”

From Cleveland Cliffs, down 16% yesterday and while they are a big fan of steel tariffs, it’s not yet helping them:

“in 2025, throughout the entire year, we were still exposed to a lot of steel imports, poisoning our domestic market, creating a demand gap that negatively impacted our steel shipments and asset utilization. In response to these challenging conditions, we made difficult decisions on shutting down assets that were dragging us down.”

“Our robust order book is the best confirmation that the business environment has already started to improve. Section 232 tariffs at 50% are, of course, a leading driver of this impact.”

“Automotive is still our core end market. And when domestic production levels of car, trucks, and SUVs remain weak for an extended period, the impacts on us is unavoidable. Vehicle production in the US was down in 2025 for the 3rd consecutive year. But with this new era of policy driven reshoring, the return to pre Covid levels of vehicle production in the US is inevitable.”

BY Doug Kass · Feb 10, 2026, 8:30 AM EST

I am meeting with two company managements between 1:30 PM and 3 PM today.

BY Doug Kass · Feb 10, 2026, 7:50 AM EST

BY Doug Kass · Feb 10, 2026, 7:40 AM EST

* Another false narrative...

Much like Tom Lee said on CNBC yesterday, this morning's Squawk Box guest says $60k is the floor on bitcoin:

I call B.S.

Again.

BY Doug Kass · Feb 10, 2026, 7:30 AM EST

BY Doug Kass · Feb 10, 2026, 7:20 AM EST

Bonus — Here are some great links:

Don’t Confuse Volatility With a Trend Reversal

Call It Whatever You Want, It's A Bull Market

BY Doug Kass · Feb 10, 2026, 7:05 AM EST

BY Doug Kass · Feb 10, 2026, 6:55 AM EST

BY Doug Kass · Feb 10, 2026, 6:45 AM EST

BY Doug Kass · Feb 10, 2026, 6:35 AM EST

Wolf Street howls about Mag 7 employment roles.

BY Doug Kass · Feb 10, 2026, 6:25 AM EST

BY Doug Kass · Feb 10, 2026, 6:05 AM EST

The S&P Short Range Oscillator moved further into overbought at 2.23% vs. 1.76%.

BY Doug Kass · Feb 10, 2026, 5:55 AM EST

I am back shorting indices (common) with S&P futures +14 handles:

* (SPY) $695.50

BY Doug Kass · Feb 10, 2026, 5:45 AM EST