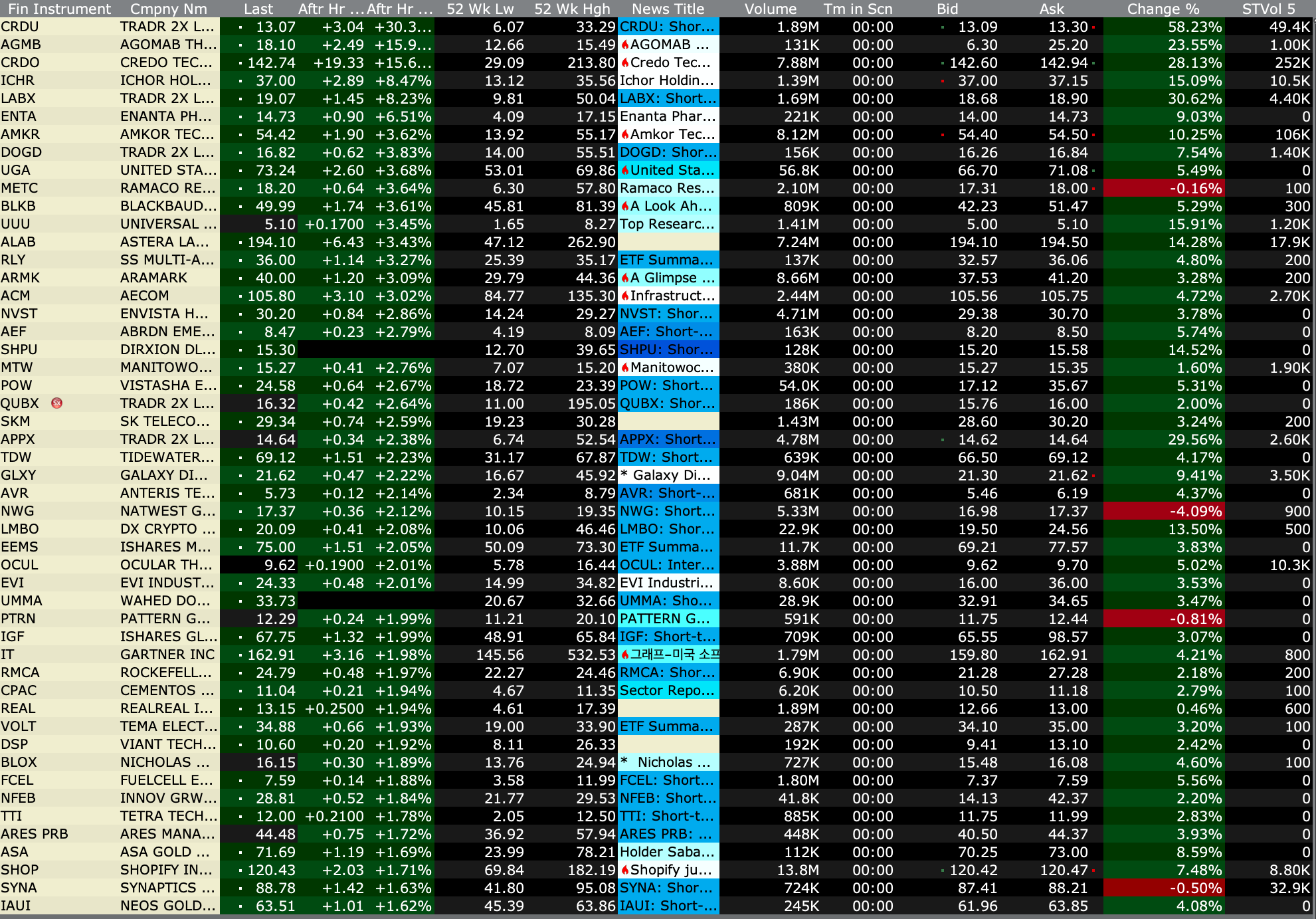

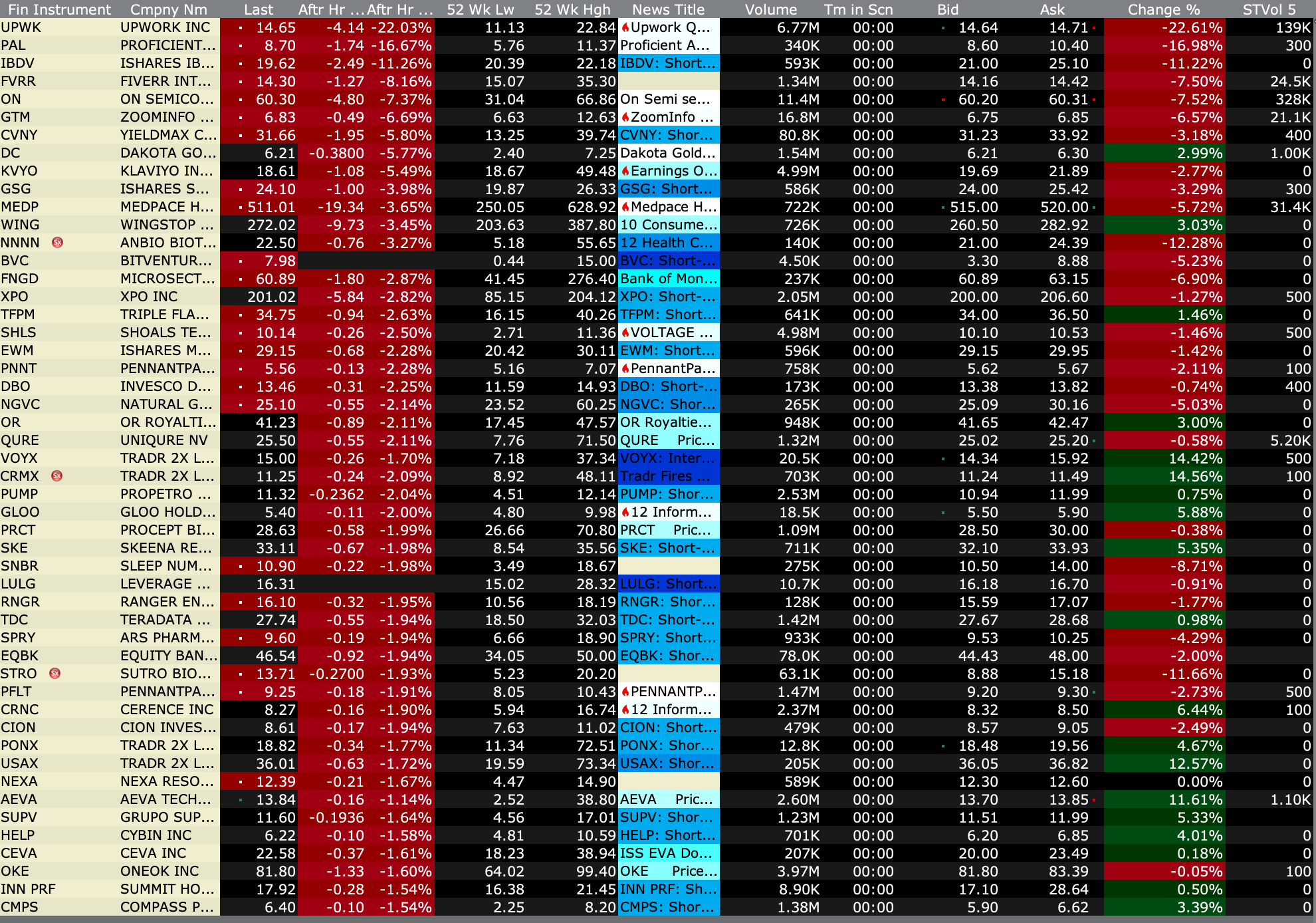

After-Hours Advancers and Decliners

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Feb 9, 2026, 4:55 PM EST

BY Doug Kass · Feb 9, 2026, 4:55 PM EST

BY Doug Kass · Feb 9, 2026, 4:42 PM EST

BY Doug Kass · Feb 9, 2026, 3:47 PM EST

BY Doug Kass · Feb 9, 2026, 3:35 PM EST

I have a brief 3:30 research call.

Back at the close.

BY Doug Kass · Feb 9, 2026, 3:25 PM EST

BY Doug Kass · Feb 9, 2026, 3:16 PM EST

BY Doug Kass · Feb 9, 2026, 3:10 PM EST

* More "info"...

BY Doug Kass · Feb 9, 2026, 2:25 PM EST

BY Doug Kass · Feb 9, 2026, 2:15 PM EST

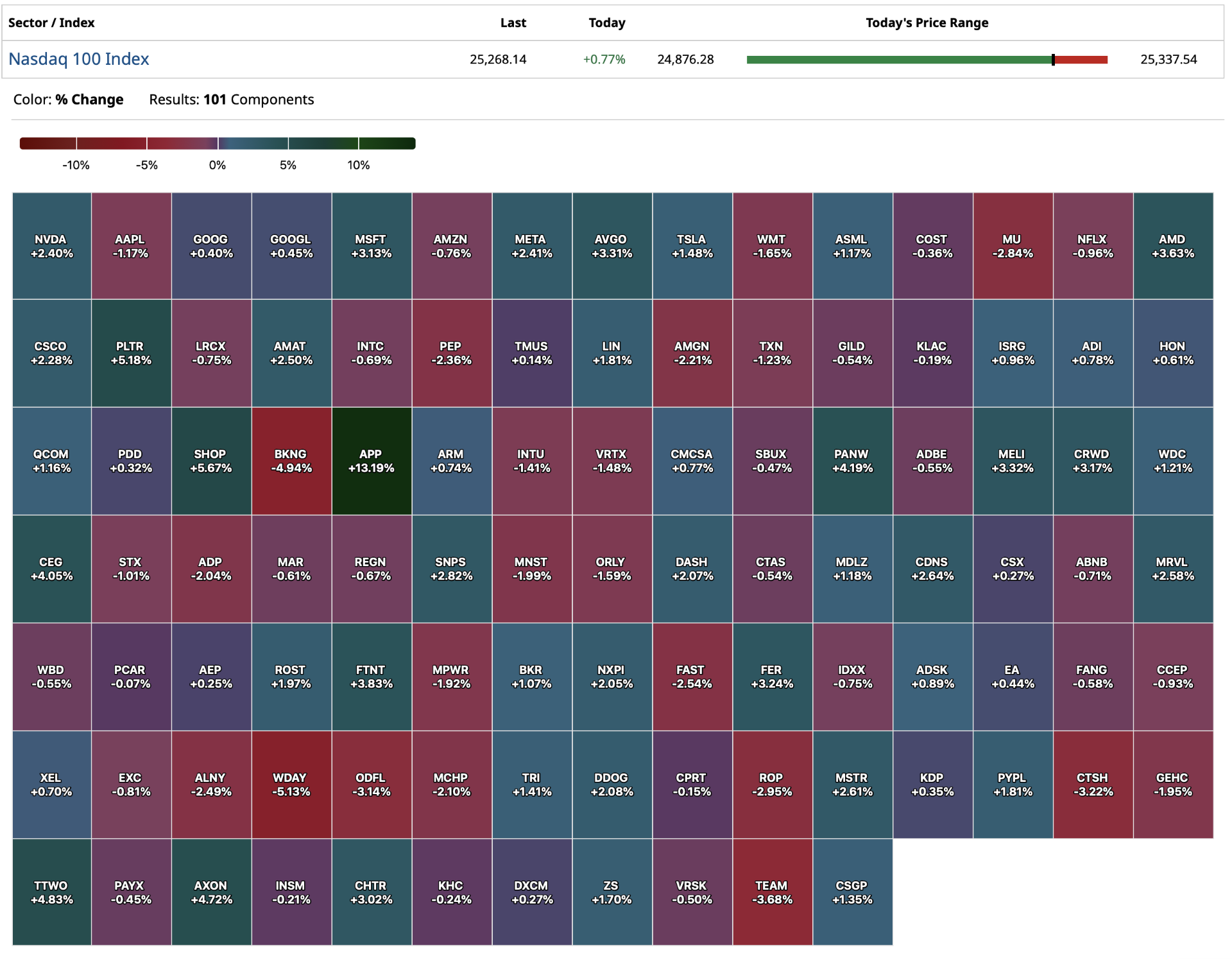

Wolf Street howls about software stocks.

BY Doug Kass · Feb 9, 2026, 2:00 PM EST

BY Doug Kass · Feb 9, 2026, 1:50 PM EST

With S&P cash +38 handles, I have moved to medium-sized short index calls.

Moved my VVS short common (in the indices) to short calls.

BY Doug Kass · Feb 9, 2026, 1:30 PM EST

It appears that a speculator on Polymarket (prediction market) just bet $100,000 that the U.S. will attack Iran in the next day,

If he is correct, he will win $4 million dollars!

BY Doug Kass · Feb 9, 2026, 1:21 PM EST

BY Doug Kass · Feb 9, 2026, 12:35 PM EST

BY Doug Kass · Feb 9, 2026, 11:43 AM EST

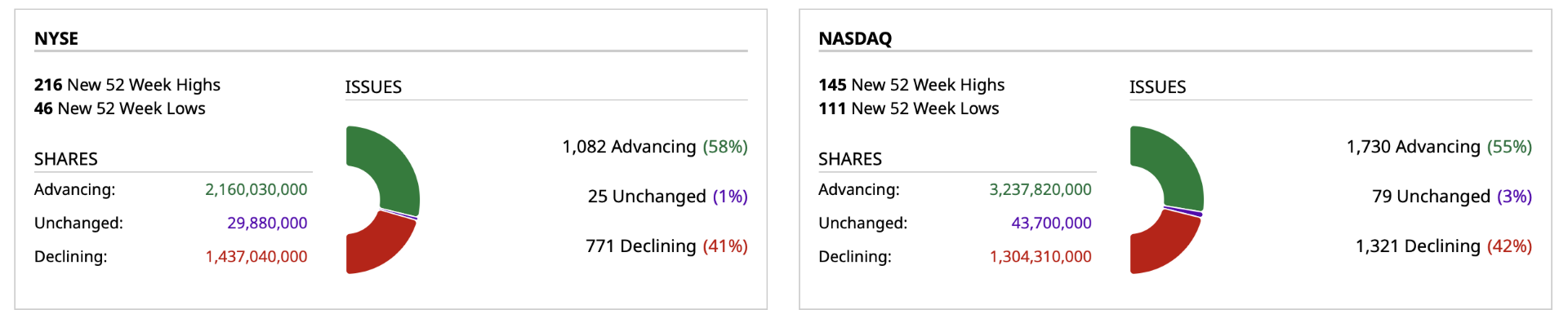

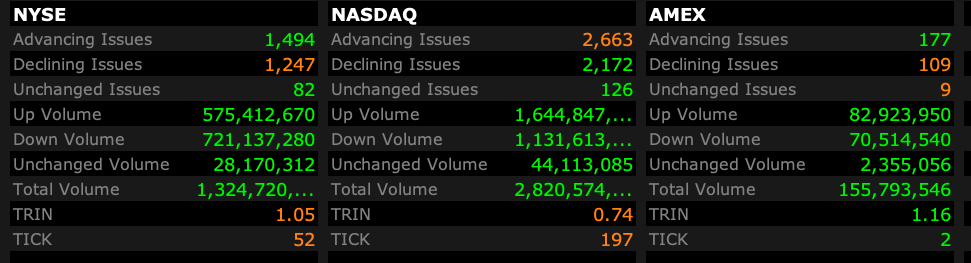

- NYSE volume flat vs its one-month average;

- Nasdaq volume 10% below its one-month average;

- VIX index: down 2.87% to 17.25

BY Doug Kass · Feb 9, 2026, 11:25 AM EST

The Mag 7 transformation from capital light to capital intensive will, well intensify in the time ahead:

BY Doug Kass · Feb 9, 2026, 10:49 AM EST

From Peter Boockvar

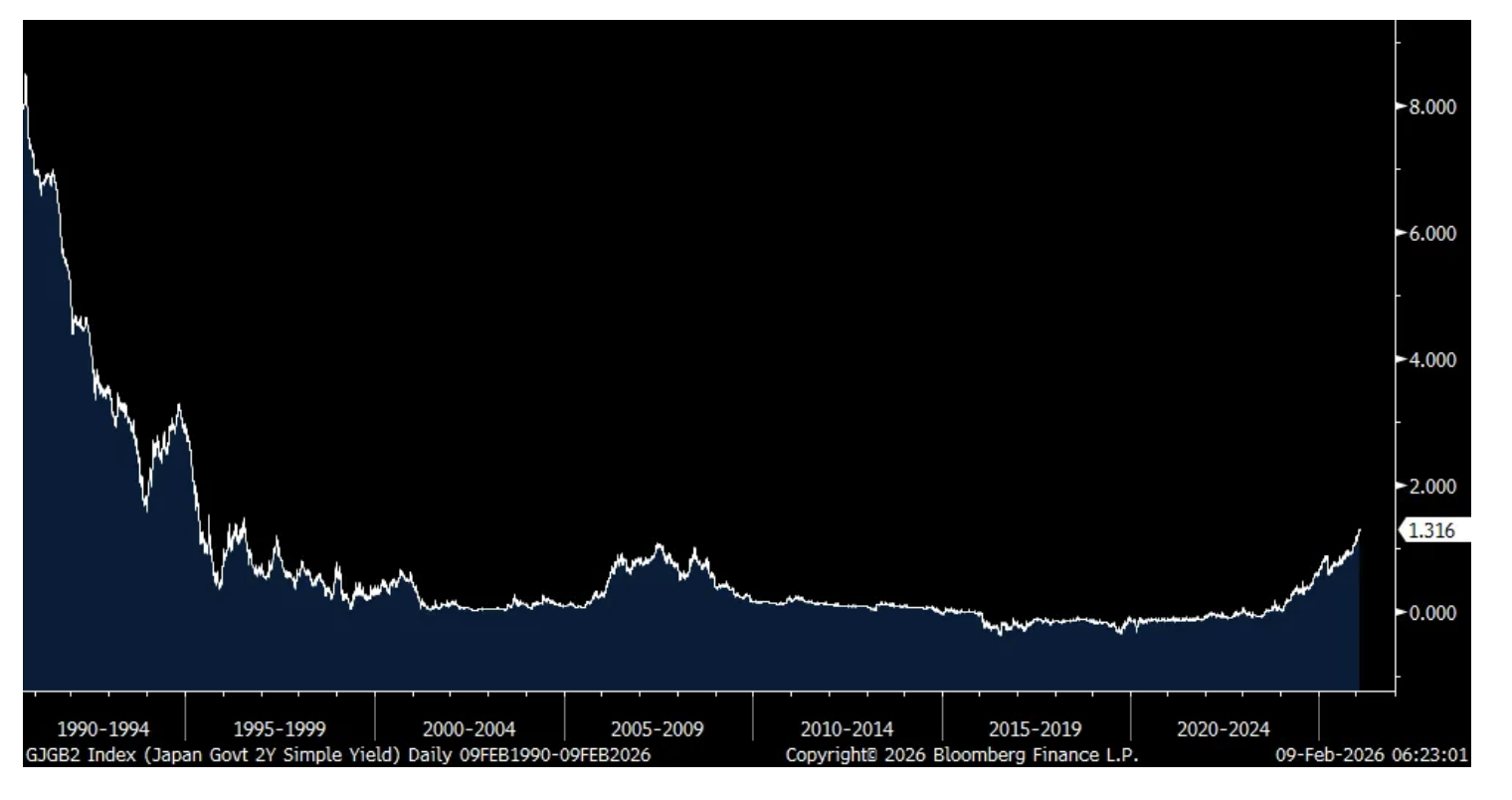

The popularity of Japanese Prime Minister Takaichi Sanae gave the LDP their largest majority position in parliament ever and the Nikkei responded in kind with a record high close, up 4% on the day, while JGB yields closed mostly higher (up for the 2s and 10s but little changed for 30s and 40s) as did the yen. We’ve already seen what initial policy initiatives will be implemented as another round of fiscal stimulus comes so no surprises from that perspective but the margin of victory was certainly impressive. The problem though with short term Keynesian policies is that it never is lasting in impact as policy permanency is a more effective driver of long term economic growth but we’ll see. She is a political rock star in Japan and will have free reign for now. I do expect more rate hikes from the Bank of Japan here as well as inflation remains the main concern of the Japanese populace. The 2 yr JGB yield closed up by 3 bps to 1.32%, a fresh 30 year high. Yes, 30 years.

2 yr JGB Yield

Global yields are higher in response but US Treasuries are being impacted by two other things also. One, Bloomberg is reporting that “Chinese regulators have advised financial institutions to rein in their holdings of US Treasuries, citing concerns over concentration risks and market volatility, according to people familiar with the matter. Officials urged banks to limit purchases of US government bonds and instructed those with high exposure to pare down their holdings, the people said, asking not to be identified discussing private deliberations. The directive doesn’t apply to China’s state holdings of US Treasuries.”

The second thing was the comments from Treasury Secretary Bessent yesterday on Maria Bartiromo’s Sunday Morning Futures where he said with respect to the Fed’s balance sheet under the new incoming Fed Chair Warsh, “I wouldn’t expect them to do anything quickly if they move to an ample (reserves) regime policy, and that does require a larger balance sheet. So, I would think that they’ll probably sit back, take at least a year to decide what they want to do.”

This follows comments on Friday from my former boss Larry Lindsey on CNBC when he said the Fed will NOT be shrinking their balance sheet from here but Warsh instead will just be more judicious when utilizing QE again and most likely only ‘in case of emergency.’ I’m not sure if this is the reason why gold is back above $5,000 but for those who sold a few Friday’s ago thinking Warsh was going to be a hawk under all circumstances, that will not be the case.

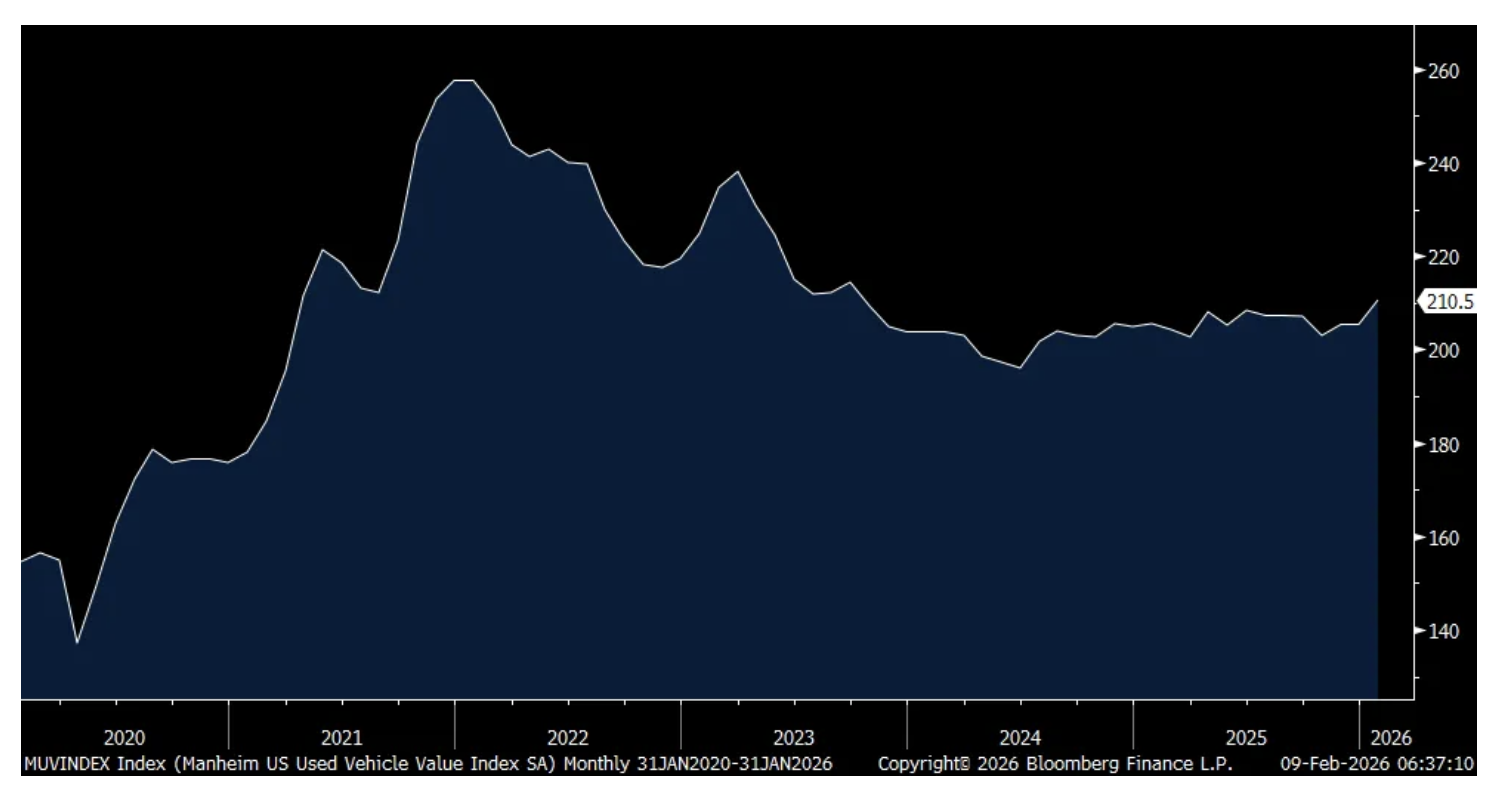

January CPI comes out on Friday and this is what Manheim said about its January wholesale used vehicle value index, with used cars being a key component of the goods portion of inflation. Its index was up 2.4% both m/o/m and y/o/y. “We had planned for a stronger January from a pricing perspective, but wholesale values moved even faster than we expected on the back of strong retail demand, driving the MUVVI to its highest reading since September 2023. With tax refund season officially starting last week, we are expecting that more consumers will be getting refunds - and that the size of those refunds will hit a new record...The spring bounce for wholesale markets looks like it started early this year, and stronger tax refunds and lower used supply may keep it running for longer than typically seen.”

Manheim Wholesale Used Vehicle Index

I’ve cited the LSTA Leveraged Loan Index many times over the past few weeks and learned Friday that software bank loans makes up 13% of the index which is about double the second largest sector allocation.

From Strategy:

“I understand the market conditions for today’s call is challenging...some of you bought Bitcoin or MSTR in the last year. This is your first downturn. My advice is to hold on. Remember the fundamentals that caused you to buy Bitcoin. It’s because Bitcoin is the digital transformation of capital, or maybe it’s the hardest and most ethical form of money, or because you believe in a non-sovereign, censor resistant store of value. None of these fundamentals have changed. They didn’t change in the last year. They haven’t changed in the last 18 years.”

I’ll add, one thing it has proven not be over the 18 years of its existence is to be digital gold. Maybe one day but not yet.

And remember the time when Bitcoin was supposed to be this anti-establishment like asset out of the regulatory hands of government and central banks?

From Michael Saylor on the call, “And so, when you consider the fundamentals of digital capital, you have to start with the most important regulator in the entire world, and that is the President of the United States. We have a Bitcoin President and he’s intent upon making America the Bitcoin superpower, the crypto capital of the world and the leader in digital assets. I don’t think you can underestimate the importance of having support for the industry and digital capital at the very top of the political structure.”

“Capital Hill has embraced Bitcoin. We’ve got bipartisan consensus that the US should embrace digital assets, should embrace digital capital, should be a leader. That is not a debate. No one’s saying that there’s one party in favor of digital capital, another party against it. That’s a big deal. So, although the political process is complicated, the fact that we have moved from an asset, which was a scary speculative thing, and maybe illegitimate, to a legitimate asset that most reasoned politicians and regulators and policymakers believe they need to move constructively with.”

From Simon Property’s earnings call that I finally got around to:

“I think the tariffs are clearly having an effect on retailers. So it is definitely putting more pressure on them, and it’s not the big guys...you put Costco and Walmart, and of course Amazon aside, and then you have the rest of us, okay? And the rest of us are feeling the pinch.”

“Retailers dealt with it successfully this year. But with the tenant, full impact will really be ‘26.”

“the most important thing is traffic is up, sales are up. The retailers that don’t make it, even though I could sit here and blame tariffs, they’re not highly productive retailers.”

From Under Armour, a stock we own with a real turnaround taking place I believe:

“North America is beginning to turn the corner. We believe the December quarter marks the bottom of the reset. Traffic yet remains soft, but underlying indicators are improving. We continue efforts to strengthen our premium online position, even amid a promotional environment.”

From AutoNation whose comps fell 10% for new vehicles:

“Relative to the fourth quarter, the industry faced tougher sales comparisons to last year when post-election sales surged, driving a Q4 2024 light vehicle SAAR of 16.7 million. Also, the sales in this year’s 4th quarter were negatively impacted by the strong pull-ahead earlier in the year as consumers reacted to the tariff announcements and purchased vehicles prior to the exploration of government incentives for electric-related powertrains. We felt these impacts across most brands, with the biggest impact in premium luxury.”

Used unit sales fell 5% “with growth in units higher in the $40,000 price point more than offset by declines in lower priced, used unit sales...Average retail prices were up about 3% for the quarter and 1% for the year.”

On the consumer, “we’ve seen significant compound growth in monthly payments that have basically been driven by a combination of average transaction price, but also some differences in charged APR. I think there will be some relief in charged APR as we get further into this year...but there’s no doubt that affordability is front of mind.” They forecast the new car market to be down “somewhere between 2% and 5% for the year.”

“Our credit and performance metrics are improving, with average FICO scores on originations of 696 for the full year 2025 compared to 678 a year ago and 623 in 2023. 30 days delinquency rates at year end of 2.7% were largely stable as a percentage of the portfolio and in line with our expectations...we do expect delinquency rates to continue to normalize as the portfolio continues toward full maturity, with delinquency rates migrating to the 3% range.”

From Affirm:

On their consumer, “So the one liner answer is the consumer we see today is quite healthy. So they’re able and willing to pay us back. They’re borrowing money. Obviously the growth numbers are out there in the sprint. ..We don’t always say yes to a loan. So it’s a little bit selective but we feel pretty good about both the demand and the ability and willingness to repay.”

From Microchip Technology, down 2% Friday in a big up tape and down more this morning after announcing a convertible note offering:

“We are seeing recovery in most of our end markets. Automotive, industrial, communication, data center, aerospace and defense and consumer are all looking better. The strongest sales performance last quarter was in the aerospace and defense and in our networking, data center solutions and licensing business units.”

They are though experiencing some supply constraints. “We’re running into challenges on certain kind of substrates on very advanced nodes. These challenges were isolated to specific areas, but are now starting to spread more broadly. Our customer requests for expedited shipments have increased significantly from a couple of quarters ago, pointing to some customers’ inventories running low.”

To the overseas data, the February Sentix Eurozone Investor Confidence index rose to +4.2 from -1.8. That’s the best level since last July. Sentix referred to this gain as “showing a silver lining for the Eurozone economy.” And, “Despite discussions about a gas shortage, the investors surveyed by Sentix are also extremely confident about the German economy.” Nothing market moving here but the investor mood music in Europe is getting better.

Sentix

Thanks to shipments of tech products, Taiwan’s exports in January skyrocketed by 70% y/o/y which was above the estimate of up 57%. Exports of electronic products spiked by 60% and were higher by 130% for information and communication products. Shipments to the US were up by 152% y/o/y.

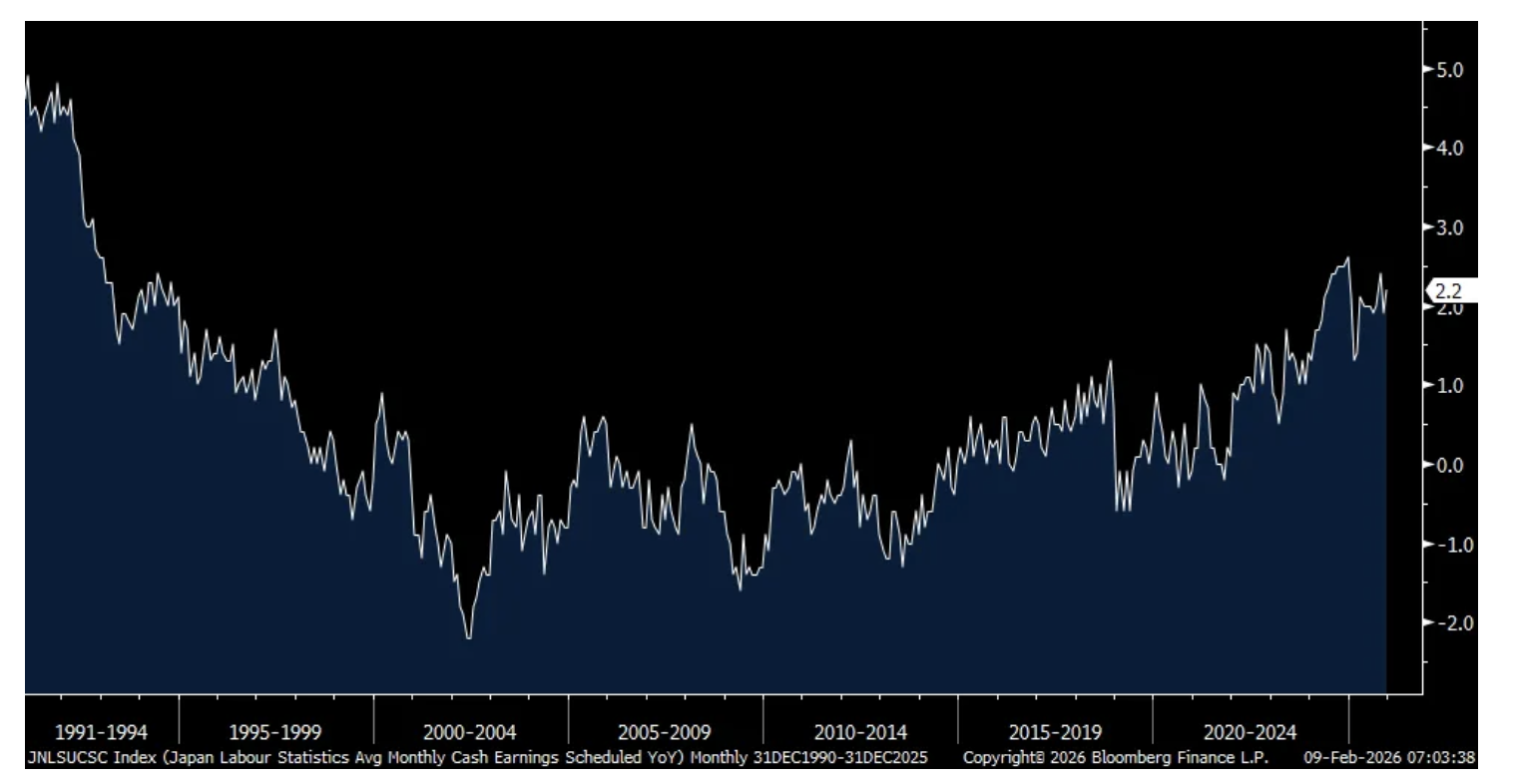

Back to Japan to finish up, base pay in December rose 2.2% y/o/y which is still just running in place with inflation though still at near the best pace since the 1990s.

Base Pay in Japan in December y/o/y

BY Doug Kass · Feb 9, 2026, 10:30 AM EST

Shorted more (GRNY) at $25.01.

BY Doug Kass · Feb 9, 2026, 9:59 AM EST

With S&P cash +2 handles I am re-initiating a short in Index calls.

BY Doug Kass · Feb 9, 2026, 9:54 AM EST

Randy

4 minutes ago

Microsoft (MSFT) downgraded by Melius from Buy to Hold.

BY Doug Kass · Feb 9, 2026, 9:48 AM EST

BY Doug Kass · Feb 9, 2026, 9:20 AM EST

BY Doug Kass · Feb 9, 2026, 9:15 AM EST

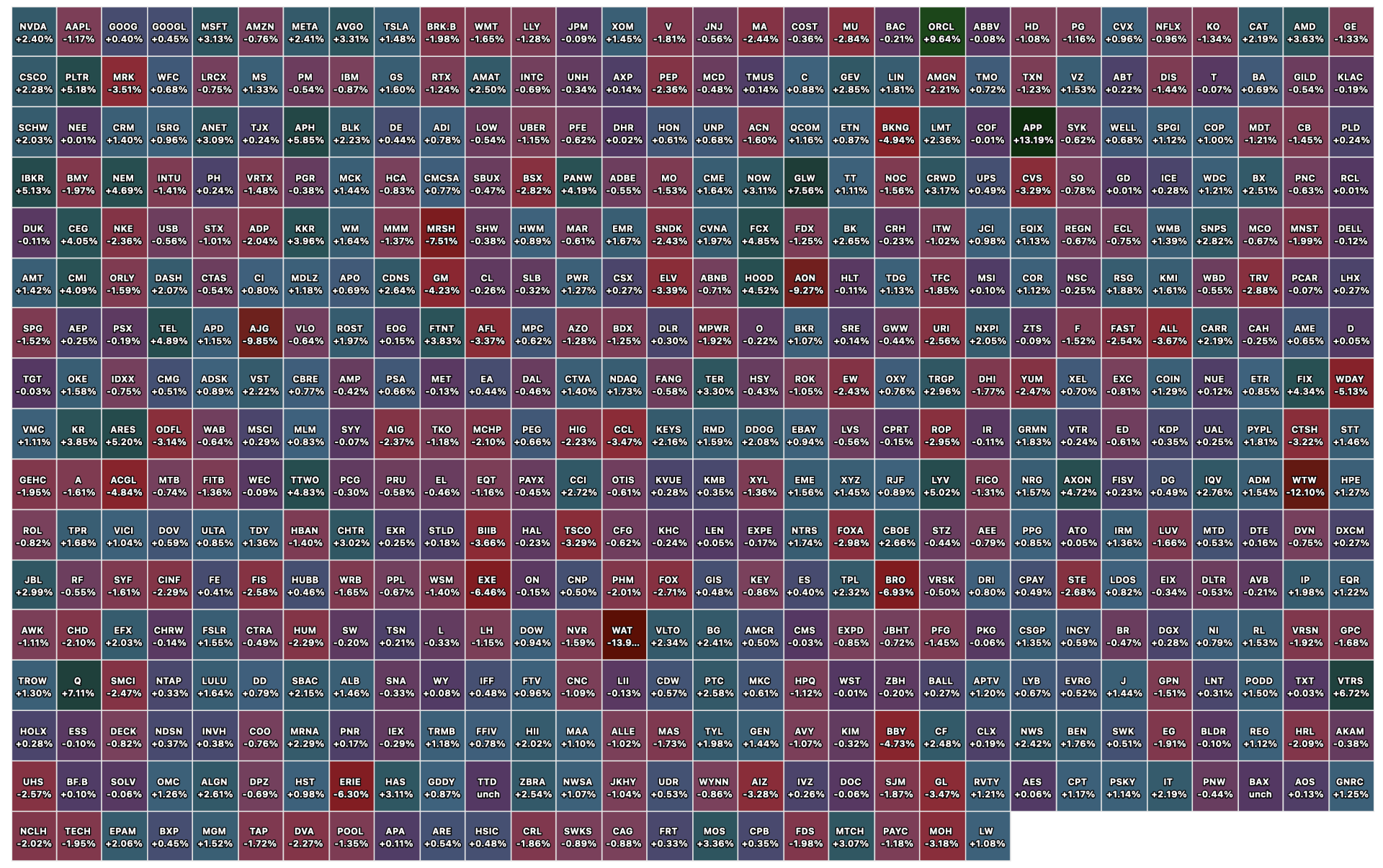

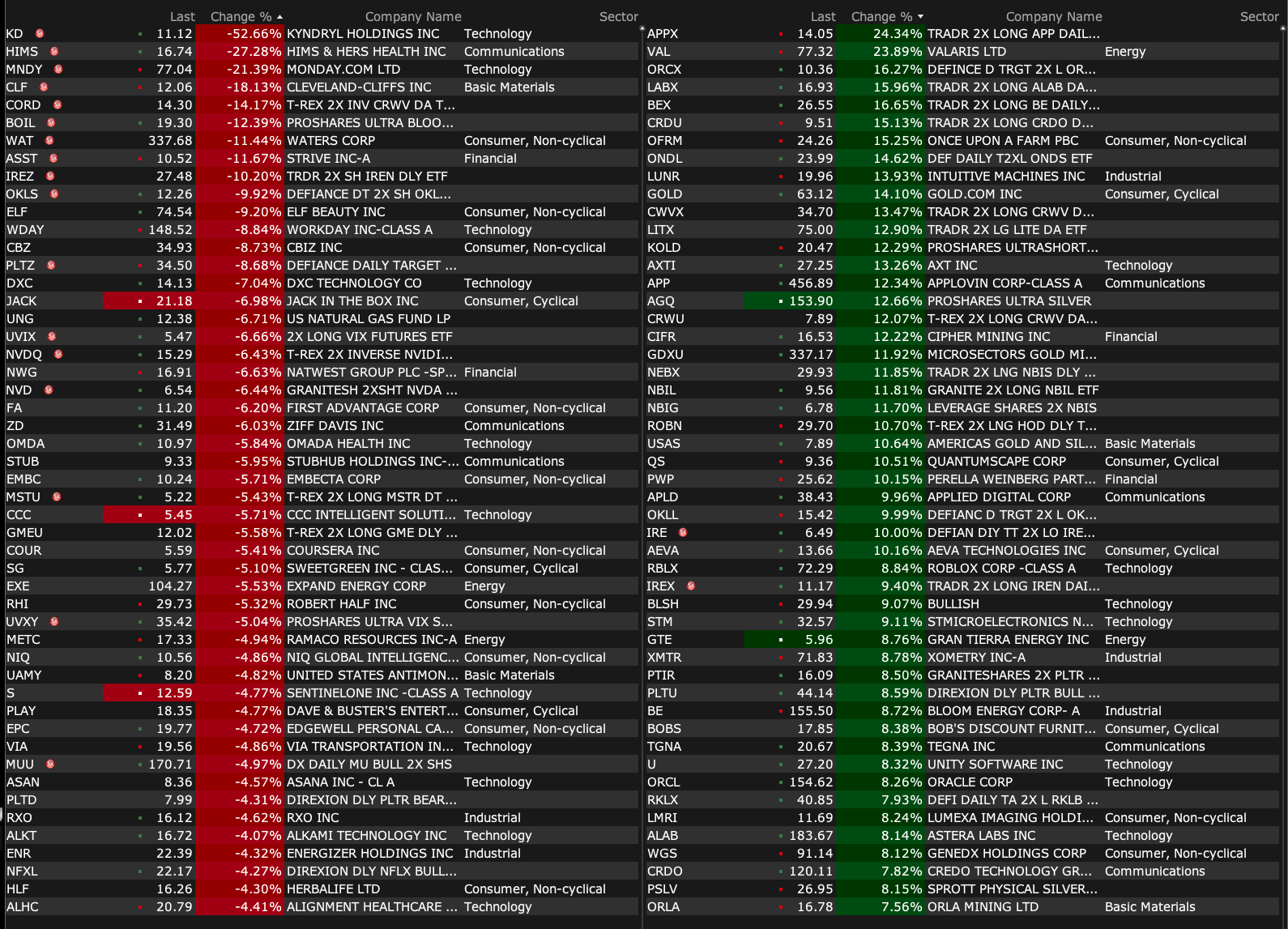

-VAL +21% (to be acquired by Transocean in $5.8B all-stock deal)

-MNTS +20% (Momentus and NASA Partner to Advance In-Orbit Servicing and Space Operations)

-TGNA +8.8% (President Trump backs deal with Nexstar)

-OFRM +7.8% (strength following IPO)

-STM +7.7% (expands partnership with AWS on cloud and AI data centers)

-KR +7.4% (affirms FY25 outlook; confirms former Walmart U.S. Head Greg Foran as its new CEO)

-XTIA +5.6% (guidance)

-NVO +5.2% (Novo Nordisk takes legal action against Hims & Hers to protect patients from unsafe, knock-off Wegovy and Ozempic)

-ORCL +4.7% (DA Davidson Raised ORCL to Buy from Neutral, price target: $180)

-LPTH +3.2% (awarded $9.6M purchase order for Cooled Infrared Cameras from Existing Defense Customer)

-RBLX +3.1% (ROTH Raised RBLX to Buy from Neutral, price target: $84)

-FRMI +3.0% (receives 6 Siemens Energy SGT-800 gas turbines at Port of Houston)

-SOFI +2.6% (Citizens JMP Securities Raised SOFI to Market Outperform from Market Perform, price target: $30)

-APO +2.3% (earnings; Schroders and Apollo announce strategic partnership)

-LLY +2.2% (acquires Orna Therapeutics to advance cell therapies for up to $2.4B in cash)

-KD -43% (earnings, guidance; announces CFO transition)

-HIMS -22% (Novo Nordisk takes legal action against Hims & Hers to protect patients from unsafe, knock-off Wegovy and Ozempic)

-PGY -20% (earnings, guidance)

-MNDY -15% (earnings, guidance)

-WAT -13% (earnings, guidance)

-JAZZ -10% (downside momentum)

-WDAY -5.7% (appoints Co-Founder Aneel Bhusri as CEO, effective immediately; affirms FY26 outlook)

-UVV -5.4% (earnings; appoints new CFO)

-BDX -3.9% (earnings, guidance)

-CLF -3.2% (earnings, guidance)

BY Doug Kass · Feb 9, 2026, 9:03 AM EST

11 a.m.: NY Fed 1-Year Inflation Expectations (January); 11 a.m.: Treasury buyback announcement (liq support); 11:30 a.m.: Treasury hosts an $89 billion 3 and a $77 billion 6-Month Bill Auction;

11:30 a.m.: Federal Reserve Board of Governors Meeting: Review and determination by the Board of Governors of the advance and discount rates to be charged by the Federal Reserve Banks;

1:30 p.m.: Fed Board Governor Waller (Voter) participates in "Digital Assets"discussion before the Global Interdependence Center Summit: "The Dollar and Continued U.S. Exceptionalism," La Jolla, CA;

2:30 p.m.: Fed Board Governor Miran (Voter) participates in conversation before event hosted by Boston University, Boston, MA (No text. Q&A from moderator. Webcast here;

3:15 p.m.: Fed Bank of Atlanta President Bostic (Non-Voter) participates in moderated conversation on monetary policy and the economic outlook before the Top Producer Summit, Nashville, TN (Audience Q&A expect-ed. No media Q&A. No embargoed text. Livestream at www.agweb.com);

5:00 p.m.: Fed Board Governor Miran (Voter) participates in WBUR Podcast: "Is Business Broken?," Boston, MA(No text. Q&A from moderator. Webcast here.

BY Doug Kass · Feb 9, 2026, 8:56 AM EST

* Friday's reversal and ramp was inexplicable to me...

If one is bearish (as I have been), Friday's reversal from the Thursday night lows in stock futures (S&P futures bottomed at -45 handles during the evening) to closing Friday's regular session by almost +130 handles was more than frustrating as there were no clear catalysts to account for the rise.

The large AI spend was already out at 4:10 PM when Amazon's (AMZN) released its outsized AI spend for 2026 ($180 billion).

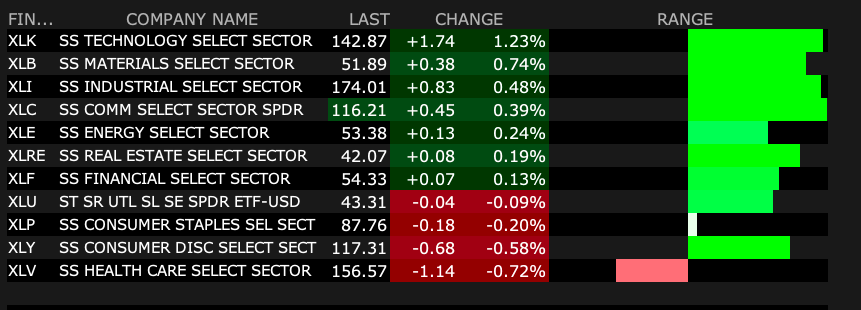

Friday's advance was significantly aided by a handful of stocks:

Regardless, the VIX had its largest daily decline since the April lows:

I didn't tear my hair out, but I did throw a hard object into my stock screen — and early Friday evening I employed some risk management and reduced my index shorts (just in time for this morning's weakness).

Color me confused and pissed off.

I did send emails to four masters of the hedge fund universe, asking for an explanation of Friday's reversal and strength throughout the regular trading session.

Quite frankly, none of them had a real clue.

I would have typically, with one eye on The Super Bowl last night, shorted (SPY) / (QQQ) with the S&P showing early Sunday evening strength. But with the magnitude of Friday's rally, I had no confidence in that strategy.

Of course, today (at least in the early going) — and as mentioned above — futures are negative.

And I am even more pissed off... but still solidly bearish in view.

BY Doug Kass · Feb 9, 2026, 8:00 AM EST

BY Doug Kass · Feb 9, 2026, 7:30 AM EST

BY Doug Kass · Feb 9, 2026, 7:15 AM EST

Bonus — Here are some great links:

BY Doug Kass · Feb 9, 2026, 7:00 AM EST

BY Doug Kass · Feb 9, 2026, 6:50 AM EST

BY Doug Kass · Feb 9, 2026, 6:40 AM EST

BY Doug Kass · Feb 9, 2026, 6:30 AM EST

Last night's futures market was volatile after Friday's large ramp, with S&P futures up by as much as 25 handles and down by over 30 handles.

Now -15 handles.

BY Doug Kass · Feb 9, 2026, 6:20 AM EST

From my old pal and the legendary Fidelity portfolio manager, George Noble:

BY Doug Kass · Feb 9, 2026, 6:10 AM EST

The S&P Short Range Oscillator was briefly in an oversold but has moved back to an overbought at 1.76% vs. -0.44%.

BY Doug Kass · Feb 9, 2026, 6:03 AM EST