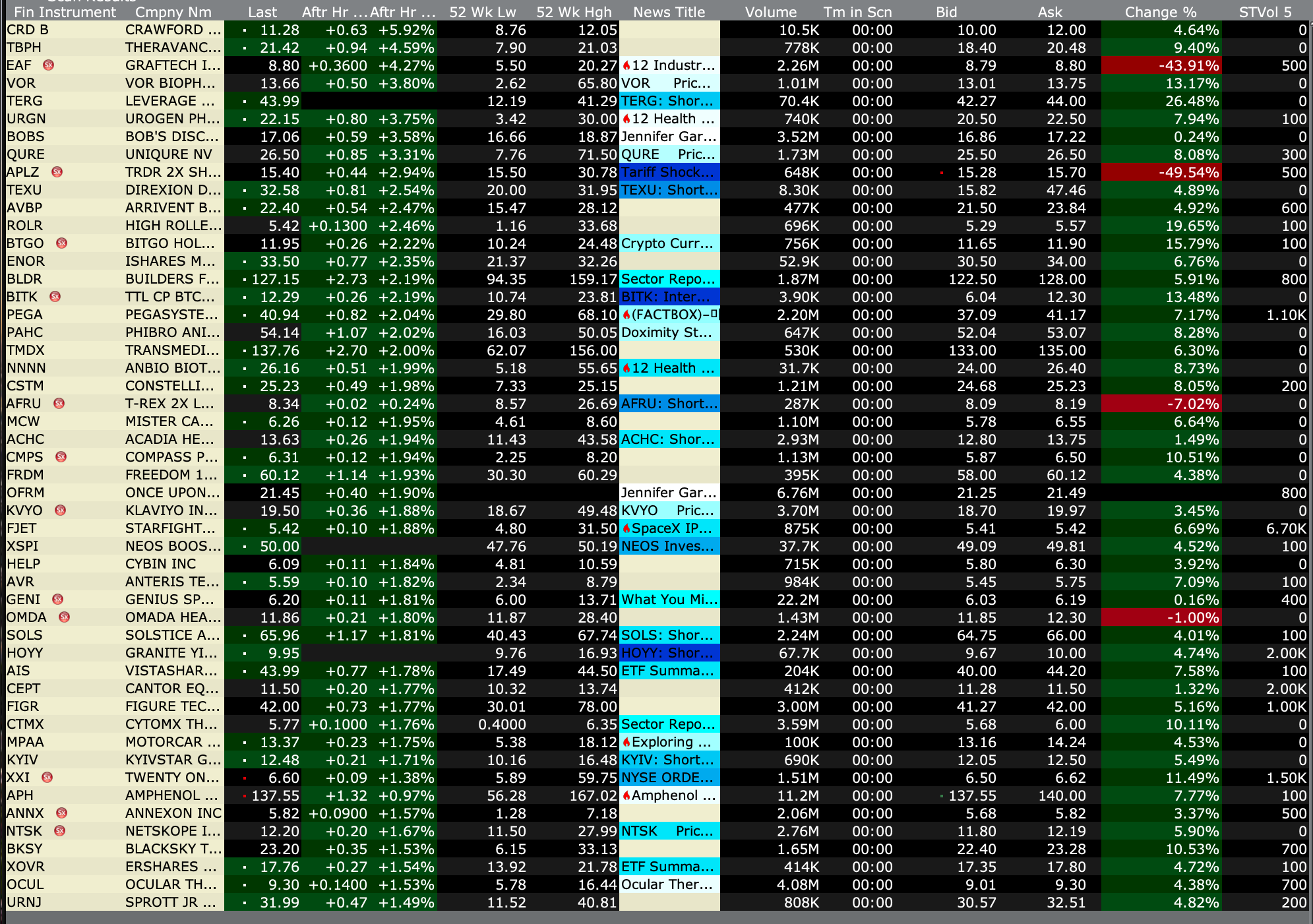

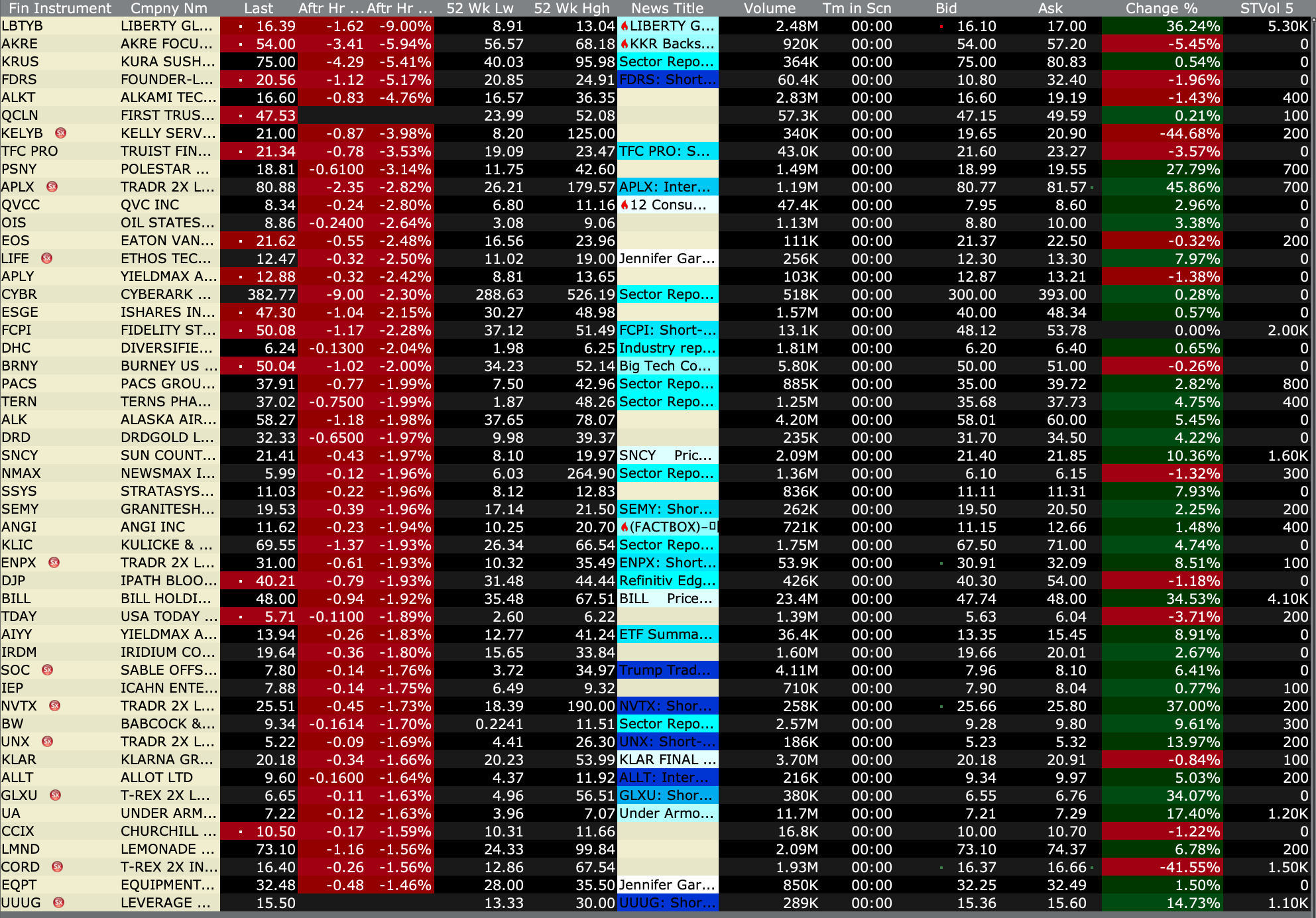

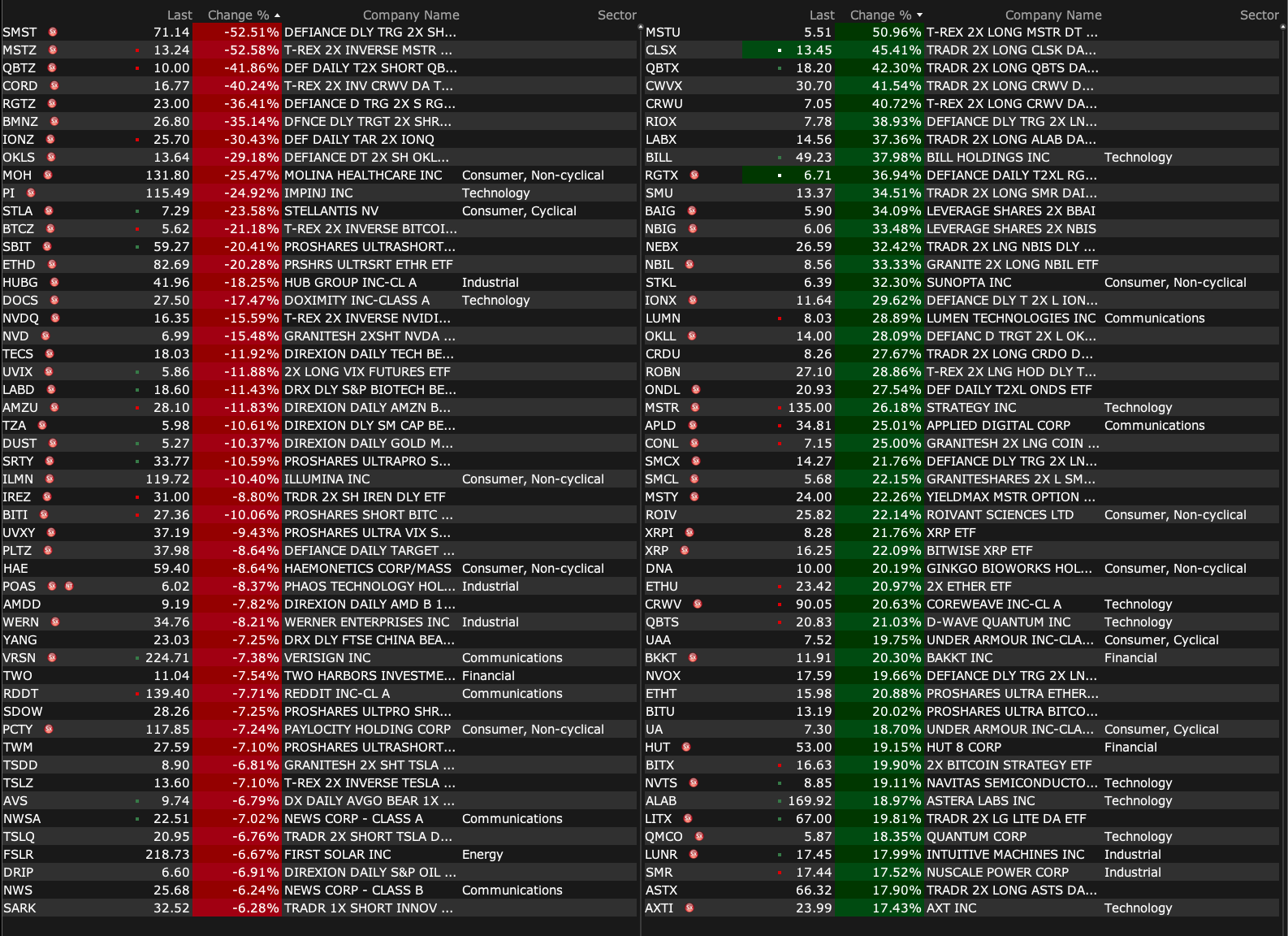

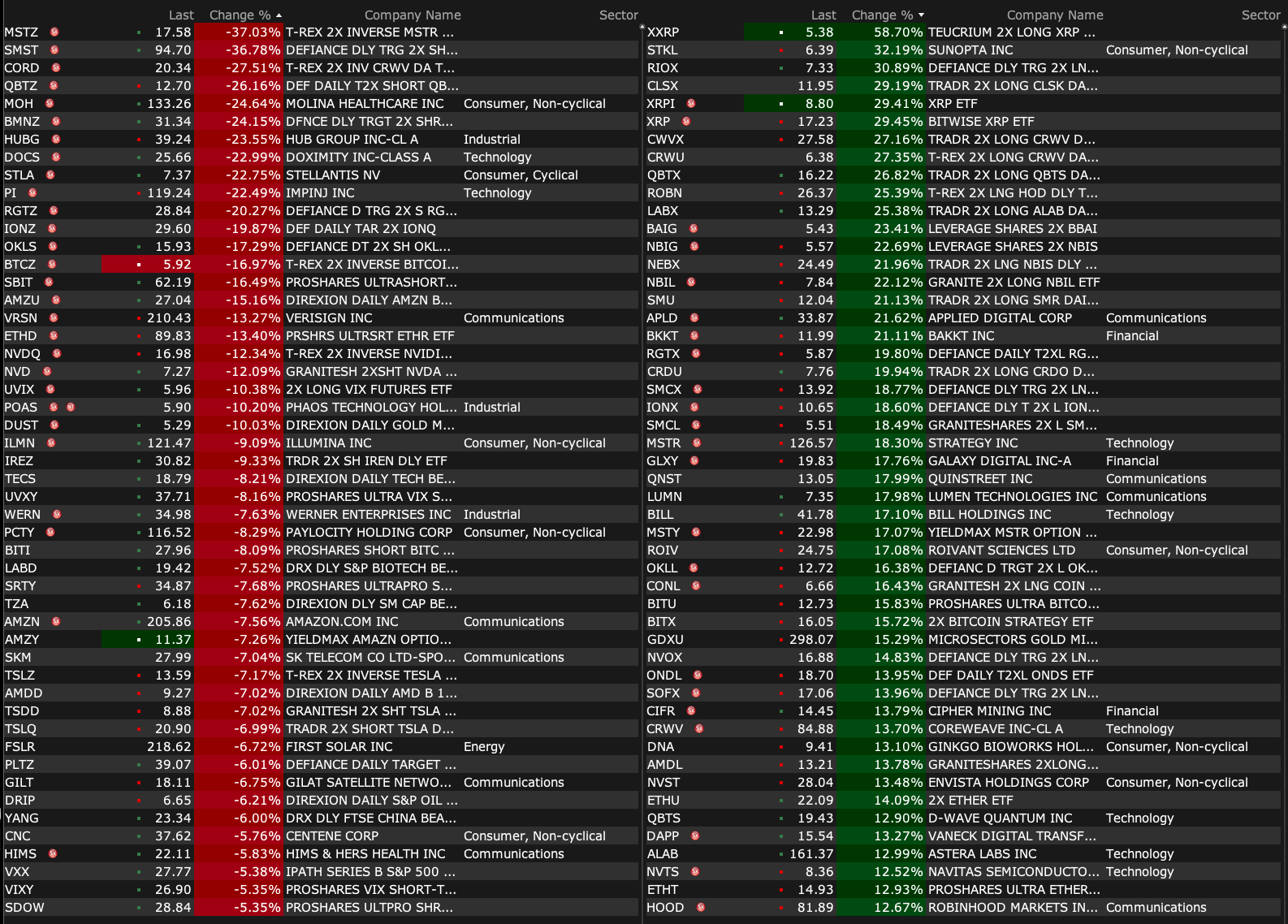

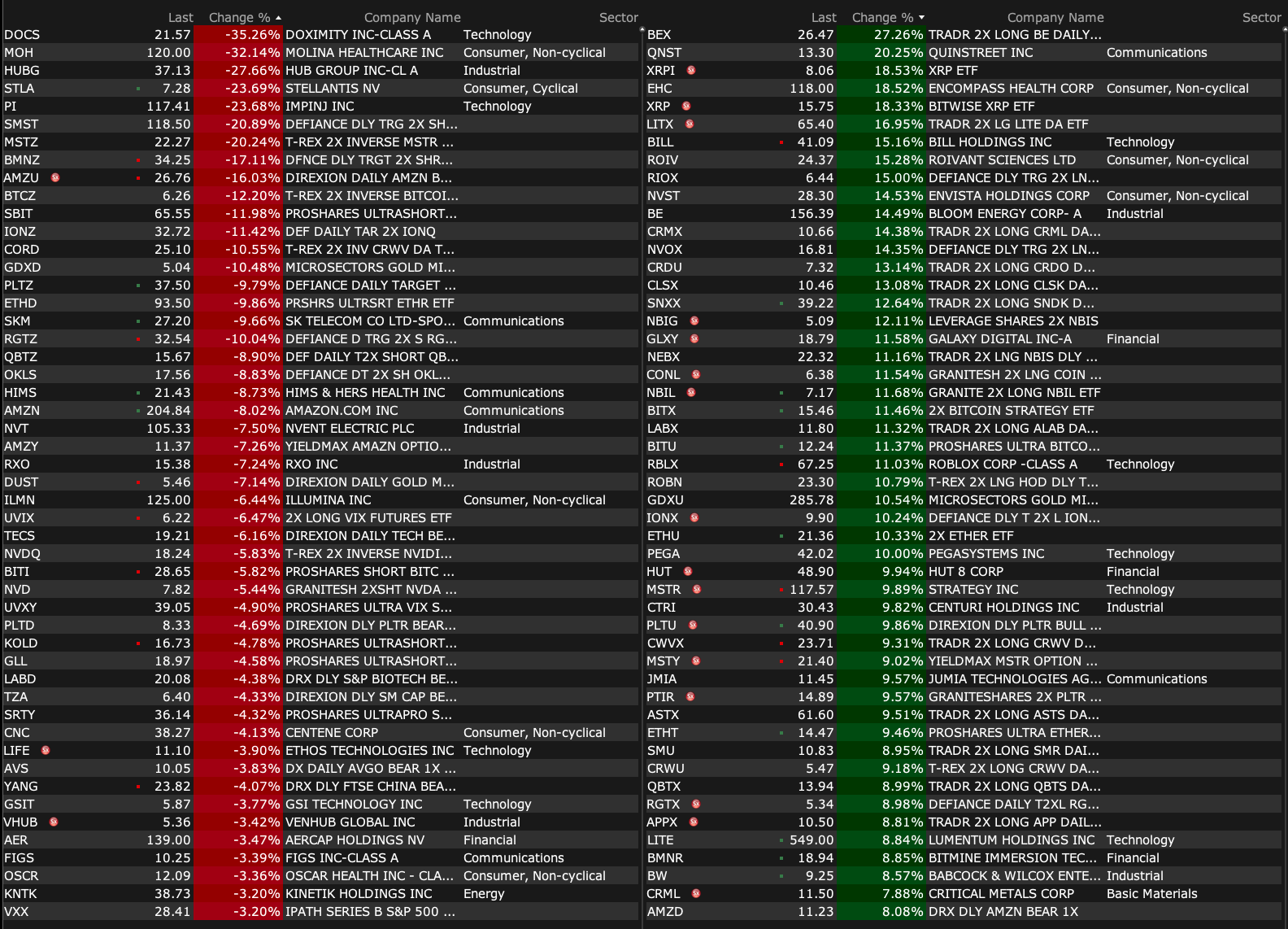

After-Hours Gainers and Decliners

After-Hours % Gainers

After-Hours % Decliners

BY Doug Kass · Feb 6, 2026, 4:50 PM EST

BY Doug Kass · Feb 6, 2026, 4:50 PM EST

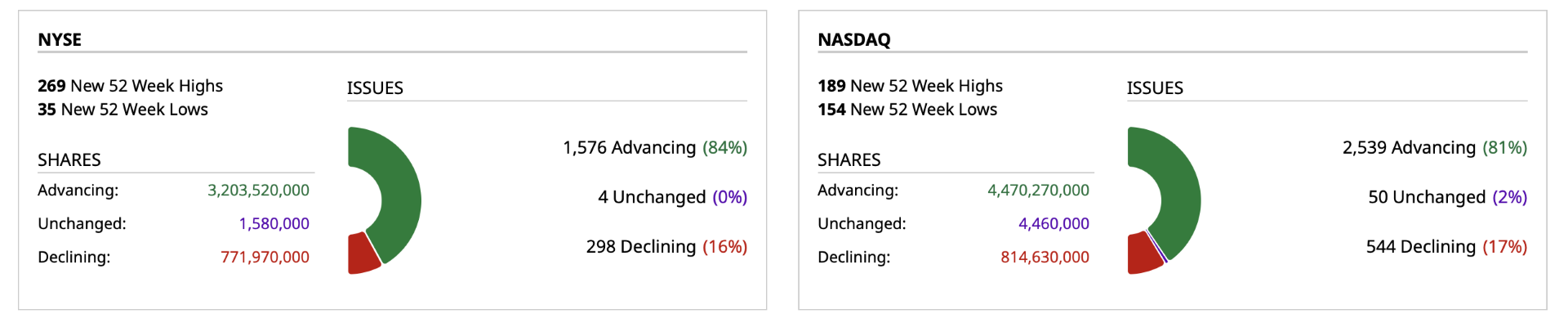

- NYSE volume 11% above its one-month average;

- NASDAQ volume 2% below its one-month average;

- VIX index: down 18.56% to 17.73

BY Doug Kass · Feb 6, 2026, 4:29 PM EST

"Just one more thing."

- Lt. Columbo

Jensen Huang is an extraordinary CEO.

But taking his unqualified and ebullient comments on face value without any critical probing (whatsoever) says much about the state of our business media (losing its value) and the state of market participants (perhaps losing their heads).

The risks of execution, availability of feedstock (energy sources) and the uncertainty of ROIC and the timing of those possible returns on large amounts of capital spend are totally being ignored. (In my 175 issues of "More Tales" I have outlined some bona-fide professional opinions that cast a lot of doubt on Nvidia's (NVDA) CEO optimism).

It is as if the ever-rising stock market is the sole indicator that the returns will be there and justify current prices.

BY Doug Kass · Feb 6, 2026, 3:45 PM EST

I will close the week with these pearls of wisdom from Charlie Munger:

BY Doug Kass · Feb 6, 2026, 3:30 PM EST

BY Doug Kass · Feb 6, 2026, 3:10 PM EST

I am leaving early today to attend to some personal stuff.

Thanks for reading my Diary today and all week.

Enjoy the weekend.

Be safe.

BY Doug Kass · Feb 6, 2026, 2:55 PM EST

Why would anyone not already plugged into their investment in OpenAI and/or reliant on OpenAI as a customer be willing to give them fresh capital at this point — especially at a massive and likely stepped up valuation?

If the Middle East guys do it, my gut is the only reason would be arm twisting from the current Administration as a backdoor way to try and help bail the thing out for the time being (re the implications for the U.S. equity market and economy).

They may enjoy lighting oil and natural gas on fire out there but they do not enjoy burning money.

Those guys are not dumb. I cannot imagine what the investment case is now. Share losing, burning money, high-cost architecture, questionable management at best, no real business model, reliant on continual funding with massive dilution on the come, etc.

There is zero reason I can think of for fresh capital to come in at a massive stepped up valuation at this point.

Granted, there is really zero reason for existing customers/investors to keep piling in too, other then to keep the flywheel spinning, which cannot go on forever. It is really no different than a heroin addict chasing another high with larger and larger doses. You know how it ends.

Getting sober is always the better choice, as painful as it can be.

BY Doug Kass · Feb 6, 2026, 2:40 PM EST

Wolf Street howls about rising used car prices and what it portends for inflation.

BY Doug Kass · Feb 6, 2026, 2:28 PM EST

With S&P cash +101 handles, I have moved to medium-sized short the indices.

BY Doug Kass · Feb 6, 2026, 12:00 PM EST

I am re-shorting (GRNY) at $24.71 and adding to (JOET) short .

I'm also scaling into more index common shorts with cash +93 handles.

BY Doug Kass · Feb 6, 2026, 11:25 AM EST

- NYSE volume 18% above its one-month average;

- Nasdaq volume 5% above its one-month average;

- VIX index: down 14.15% to 18.69

BY Doug Kass · Feb 6, 2026, 11:20 AM EST

(QQQ) $604.02

(SPY) $686.12

BY Doug Kass · Feb 6, 2026, 10:45 AM EST

With S&P cash +83 handles, I am about to reshort the indexes.

BY Doug Kass · Feb 6, 2026, 10:39 AM EST

No trades since last report.

BY Doug Kass · Feb 6, 2026, 10:30 AM EST

(MU) has been downgraded by a well-regarded small tech research boutique.

BY Doug Kass · Feb 6, 2026, 9:32 AM EST

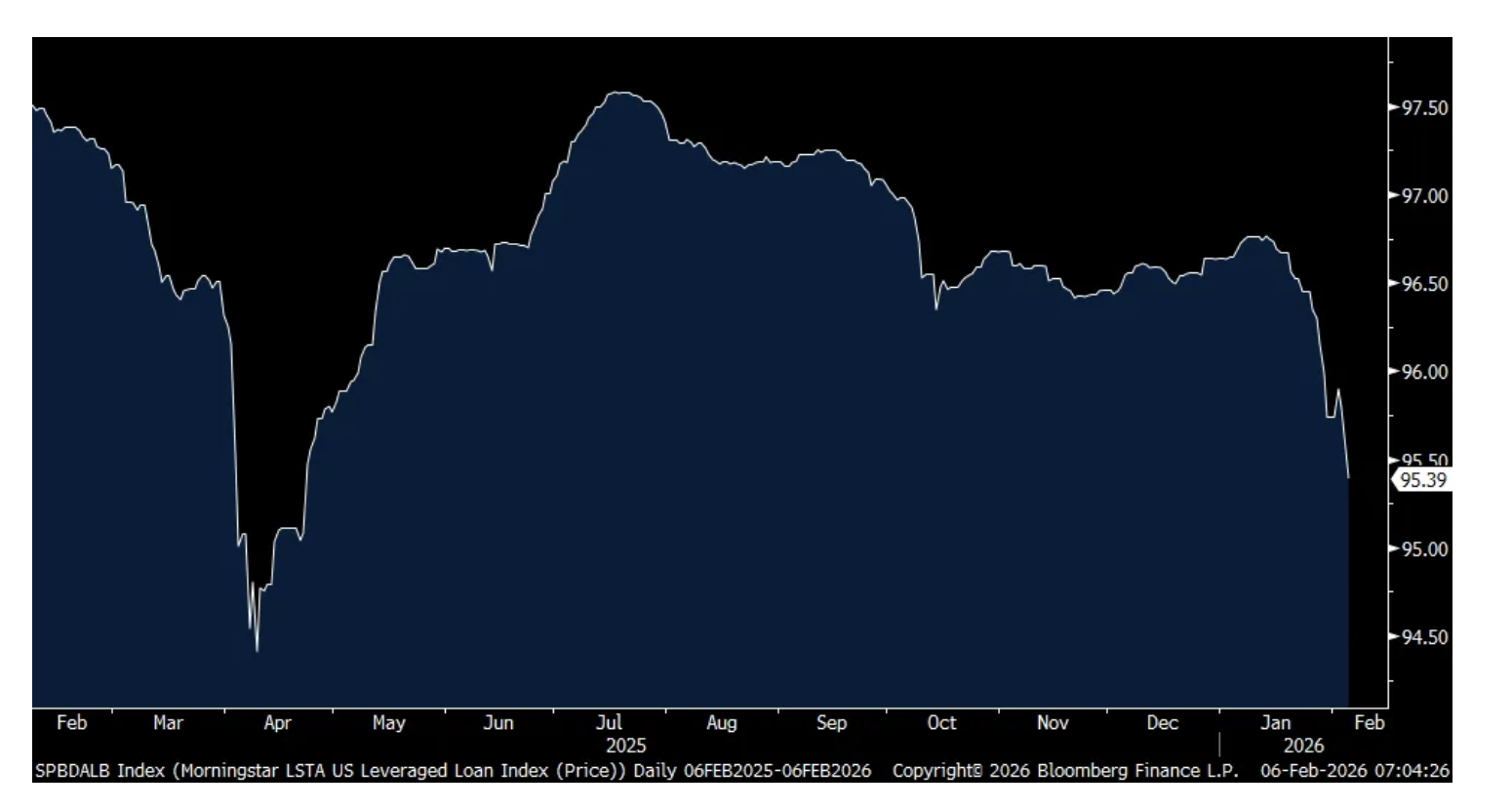

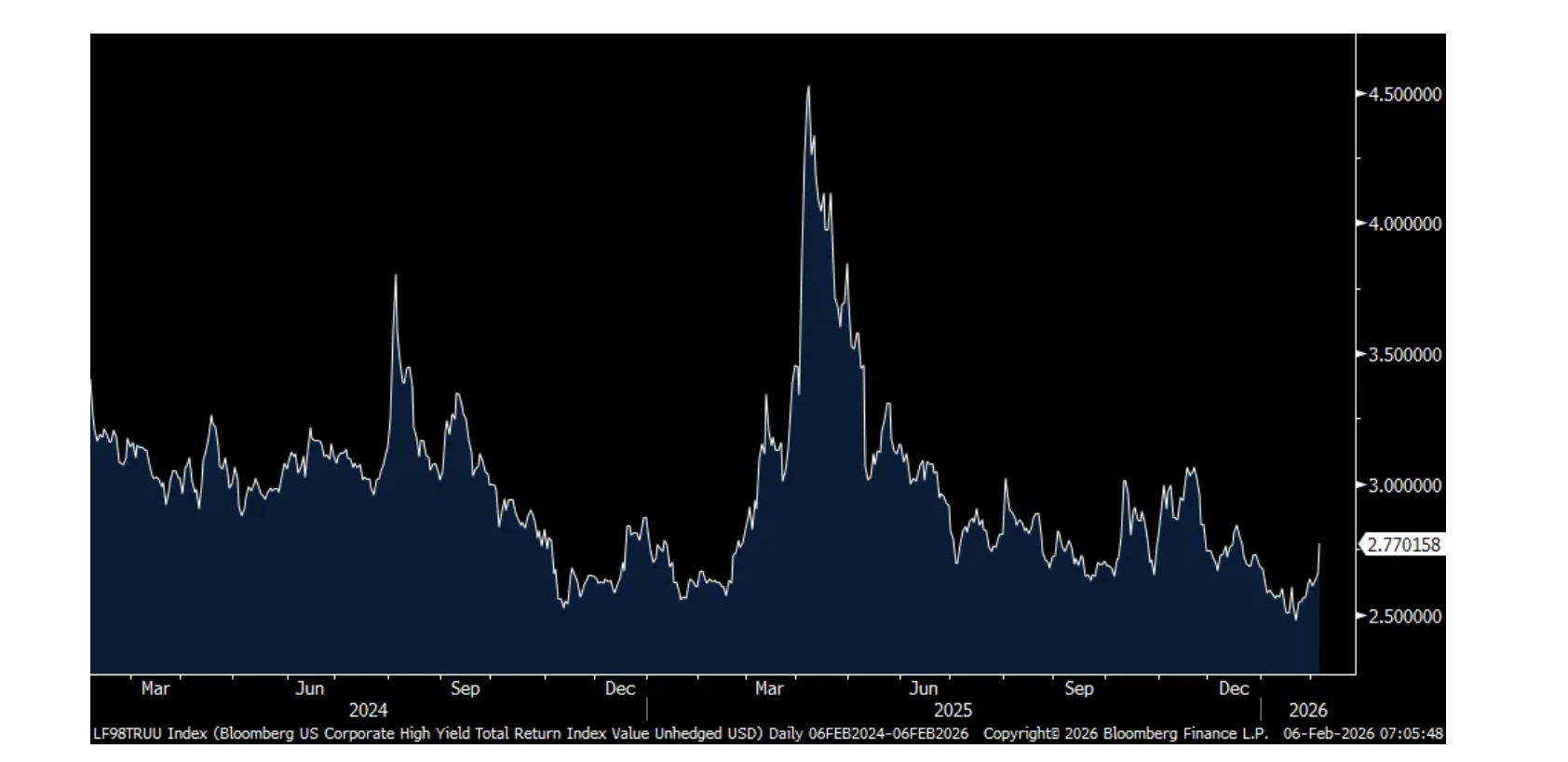

From Peter Boockvar:

Here is an updated chart on the LSTA leverage loan index as of yesterday’s close. Understand that leveraged loans are just one piece of the overall private credit space but at least a metric here for us to gauge market pricing. With respect to high yield, spreads have curled up over the past week as seen below but still remain historically low at just 277 bps over.

LSTA Leveraged Loan Index

High Yield spread to US Treasuries

To the earnings calls, lets start with what was said of note from the private equity/credit firms that reported earnings. The rest, a continued mix bag of business activity. I will add one thought, I was never a fan of private equity/credit tapping retail investors and the wealth management industry for capital as there just didn’t seen to be a natural fit in terms of time horizons. Pension funds, insurance companies and endowments have the long term view on investments and that was a good match for privates. Retail does not I believe and I watch closely to what level of redemptions now occur because if they do increase, it will raise the cost of capital for everyone else in the private industry.

I will also channel Josh Harris (who runs the PE firm 26North Partners) on this who agrees with me as he said yesterday at a Wall Street Journal conference that this is “not going to end well...People don’t understand the duration. They don’t understand that some of these structures may not be liquid when things go wrong - and that’s exactly when they need the money.”

From KKR, down 5% yesterday and by 13% this week:

“We are seeing much greater bifurcation across our industry. It is becoming harder to generalize about asset classes and easier to distinguish between firms that are well positioned and those that are not.”

“So I would say the recent volatility speaks to new anxiety for the market around potential disruption risks, but it is not new anxiety for us. So we’ve been focused on AI driven competition and disruption risk for the last several years…To give you a sense of the number because I’m sure people are wondering, software is about 7% of our AUM and that is with, I would say, a highly inclusive definition of software. And so our concentration is well below our industry, well below broad equity and credit indices. In the market right now, as you know, this happens when there’s this much emotion all at once is painting everything with one brush. We would just caution that not all software investments are the same.”

From Ares Management, lower by 11% yesterday:

Defending their loan book, “As evidenced by our strong fund performance, our investment portfolios continue to exhibit solid fundamentals, and our credit portfolios generated attractive return premia over the traded market equivalents...Loan-to-value ratios are near historical lows in the 40% range, interest coverage continues to strengthen, and q/o/q non-accruing loan trends are generally flat, while remaining well below historical average levels.”

Notwithstanding my concerns and after saying they are seeing still good demand from institutional investors, “We also continue to see strong demand from individual investors. Despite over $300 billion in private market gross inflows from the wealth channel over the past three years, the average allocation to private markets for individual investors remains unchanged at approximately 3% to 4%, primarily due to rising overall market values. As a result, we believe that there are meaningful opportunities for private market allocations in the wealth channel to move towards the much higher allocations that we see among institutional investors.”

On their software exposure, “Across our firm, we have a highly diversified portfolio of investments in software companies, which are nearly all senior loans and represent about 6% of our total AUM and less than 9% of what we consider private credit AUM, inclusive of real asset lending but excluding liquid credit...Our software portfolio is highly diversified across many subsectors with a very small percentage of the portfolio that we deem to have high risk of AI disruption. We lend at lower loan to value on software which are in the high 30% range compared to mid-40s LTV on the rest of the portfolio...As a result we see no change to our earnings growth outlook from AI risks in our existing portfolio and our business can naturally adapt to the risks and opportunities as they’re presented.”

From Blue Owl, down 3.5% yesterday:

“In credit, the fourth quarter was marked by a high level of debate and discussion about the health of the private credit markets. The fact of the matter is the trends we observed within Blue Owl’s credit portfolios remained strong and did not align with the headlines or investor fears. The sentiment seems to be echoed broadly by other asset managers and banks alike across broader credit markets.”

To the question about its software lending, “Tech lending has worked, continues to work, and to get very direct right to your answer, no. We don’t have red flags. In point of fact, we don’t have yellow flags. We actually have largely green flags. The tech portfolio continues to be the most pristine amongst all of our portfolios. Amongst all of our subsectors. I appreciate we’re all looking forward, but remember these are loans that are on average 30% of the value of the enterprise at time of acquisition, or LTV, with huge equity cushions.”

The CEO further defended software companies and their relevance in the age of GenAI but also said “there are certain parts of software that are vulnerable and they are. We’ve studied our portfolios very carefully. We do not see any meaningful exposure to those more susceptible areas.”

Amazon’s $200b of CapEx will be 25% of revenue vs 18% in 2025, 13% in 2024 and 9% in 2023. AWS grew revenue by 24% y/o/y which is “the fastest we’ve seen in 13 quarters.” That spend will be “predominantly in AWS because we have very high demand, customers really want AWS for core and AI workloads, and we’re monetizing capacity as fast as we can install it.” And will all this CapEx pay off? “we see strong return on invested capital. Obviously strong demand for these services and we continue to like the investments in this area.”

On the price of the AI buildout, “Another challenge is cost. I’ve said this many times, but if we want AI to be used as expansively as companies want, we have to make the cost of inference lower. A significant impediment today is the cost of AI chips. Customers are starving for better price performance, and typically and understandably, the dominant early leaders aren’t in a hurry to make that happen. They have other priorities. It’s why we’ve built our own custom silicon and Trainium and it’s really taken off.”

I guess that was Jassy’s dig at Nvidia.

On retail, “We continue to see strong customer response to everyday essentials and grocery. In 2025, everyday essentials grew nearly twice as fast as all other categories in the US, representing one out of every three units sold in our store.”

From Hershey and whose stock rallied 9% in a tough tape:

“The retail environment for US snacking remained steady during the fourth quarter, as consumers continued to spend selectively, prioritizing products that offer either emotional or functional value. Retail takeaway for the US confectionary category accelerated in 2025, reflecting durable consumer demand. For the year, Confection was the third fastest growing US snacking category behind only nutritional bars and meat snacks.” We own Conagra as a play on meat snacks as they own Slim Jim.

Hershey’s salty snack business saw revenue growth of 15.6% in the quarter y/o/y. “On the salty side of the business, I think it’s really important to be in the right places in the category: permissible, better-for-you, portion control. Those are areas that continue to leverage growth. Consumers are willing to pay for that. That’s where the growth is, and that’s where our brands area positioned in the category.”

On pricing, which they’ve taken a bunch of over the past few years to offset higher cocoa prices, “the deflationary momentum on cocoa takes future pricing pressure down.”

From Ralph Lauren, down 4.5% yesterday but seemed to have a good quarter and we know they have an upper income consumer:

“on the outlook for Q4, we saw continued broad based global momentum across regions and channels behind our brand and our business through and coming out of holiday. So, we took up our Q4 outlook based on this continued momentum, notably in North America, where, despite a pretty volatile, choppy environment, we continue to drive solid, high quality balanced growth across channels this past quarter. Asia also really strong momentum behind our businesses across markets in that region.”

“underlying demand remains healthy and our core consumer continues to be resilient and we expect a healthy solid underlying growth trend for Q4.”

‘While the consumer has proven more resilient than we initially anticipated this year, we remain somewhat cautious on the North American operating environment due in part to further consolidation across the broader wholesale channel, including recent developments at Saks.”

“We continue to expect Europe to grow at the high end of mid single digits…And we now anticipate Asia to grow mid-teens, up from our prior outlook of a high single to low double digit increase.”

From Tapestry, up 10% in a rough tape yesterday and catering to upper income spenders with strength in Coach (revenue up 25%) offsetting weakness at Kate Spade (sales down 14%):

“we powered global growth through compelling experiences, delivering double digit gains in North America, Greater China and Europe, significantly outpacing the industry and growing market share in each of these regions.”

From Asbury Automotive Group, the owner of auto dealerships and whose stock fell 7% yesterday:

“The beginning of January was good until we got hit by the weather. And so that pullback that we saw in October, November was not there the first few weeks in January, but after the weather hit us, it impacted us pretty big. As you know, that storm came in through Texas and it basically just followed our path of where we have stores all the way to the Northeast.”

“On the ground, we noticed a pullback in consumer spending in parts and service.”

From Cummins, down 10% yesterday:

“For our markets, we expect continued weakness in first half demand in our North America heavy and medium duty truck markets, but anticipate other markets, particularly power generation, to remain strong throughout the year.”

To data overseas, Vietnam reported strong export data with them rising 30% y/o/y, above the estimate of 25.5%. I continue to be positive on Vietnam’s economy and stock market and on To Lam, its head of government, a real free market reformer who is also cutting the government bureaucracy. This is a very exciting emerging economy.

The Reserve Bank of India held its repo rate unchanged at 5.25% as expected. We’re positive and long Indian stocks too. Interesting that this came up in the press conference with regards to their FX reserves, “there is no reduction in our holdings of US Treasuries” even though the dollar amount has fallen to a 5 yr low so there clearly has been.

BY Doug Kass · Feb 6, 2026, 9:30 AM EST

I just sold out my (HOOD) trading long rental at $77.40 (+$4.70 on the day)

The shares traded last night under $70/share (where I bought) - reducing my average and reducing my loss.

But a loss, nonetheless.

BY Doug Kass · Feb 6, 2026, 9:21 AM EST

-QNST +22% (earnings, guidance)

-RVSN +19% (advancement to next phase of collaboration with Israel Railways)

-ROIV +18% (earnings; Unit Priovant announces Positive Phase 2 Results for Brepocitinib in Cutaneous Sarcoidosis)

-BE +14% (earnings)

-BILL +14% (earnings, guidance)

-DAVE +14% (reports prelim Q4 revenue)

-RBLX +11% (earnings, guidance)

-MSTR +9.7% (earnings)

-UI +8.6% (earnings)

-RDDT +7.8% (earnings, guidance)

-PIPR +7.5% (earnings)

-CMND +7.0% (enters development agreement with Polyrizon to apply proprietary intranasal hydrogel technology for optimized MEAI formulation)

-MP +4.3% (US confirms to have signed 11 new bilateral critical mineral frameworks or MOUs with countries)

-GEN +3.9% (earnings, guidance)

-UA +3.2% (earnings, guidance)

-TM +2.0% (earnings, guidance)

-DOCS -35% (earnings, guidance)

-MOH -31% (earnings, guidance)

-HUBG -29% (earnings, guidance)

-STLA -26% (announces €22.2B in charges to “largely reflect the cost of over-estimating the pace of the energy transition”; guidance)

-EAF -24% (earnings, guidance)

-PI -23% (earnings, guidance)

-AOSL -14% (earnings, guidance)

-COTY -13% (earnings, guidance)

-NWL -12% (earnings, guidance)

-AMZN -8.0% (earnings, guidance)

-ILMN -5.7% (earnings, guidance)

-CNC -4.9% (earnings, guidance)

-CBOE -4.2% (earnings, guidance)

-UNM -4.0% (earnings, guidance)

-NWSA -2.9% (earnings)

-PM -2.3% (earnings, guidance)

BY Doug Kass · Feb 6, 2026, 9:20 AM EST

10:00 a.m.: U of Michigan Sentiment; U of Michigan Current Conditions; U of Michigan Expectations; U of Michigan 1-Year Inflation; U of Michigan 5-10 Year Inflation (February-Preliminary);

10:30 a.m.: ECRI Weekly Index of Economic Activity (w/e 1/30);

3:00 p.m.: Consumer Credit (December)

12:00 p.m.: Fed Vice Chair Jefferson (Voter) speaks on the economic outlook and supply-sideinflation dynamics before the Brookings Institution, Washington, DC (Text available. Q&A from moderator. Webcast at connect.brookings.edu/)

BY Doug Kass · Feb 6, 2026, 9:05 AM EST

BY Doug Kass · Feb 6, 2026, 8:45 AM EST

I just sold my (IBIT) (bitcoin) at $38.21.

In at $35.72 last night.

BY Doug Kass · Feb 6, 2026, 8:31 AM EST

* My Barron's interview of four months ago called attention to the risks associated with large AI cap spend...

"The further a society drifts from the truth, the more it will hate those that speak it."

- George Orwell

To think how many times I have had to defend my skeptical position regarding several of the "Generational Compounders" (in the Mag 7) over the last year on Twitter, FIN TV (and in the business media), in our Comments Section and elsewhere.

"I think the monkeys at the zoo should have to wear sunglasses so they can't hypnotize you."

- Jack Handey, Saturday Night Live

I have repeatedly written that many of the Mag 7 had morphed from having attractive capital-light profiles to problematic (read: uncertainty of the timing and the returns from massive AI capital spending) capital-heavy (and intensive) profiles.

I made these observations in an interview I had with Barron's Randy Forsyth in October 2025:

Meta Stock Took a Dive. It’s the Poster Child for the Debate Over AI Spending.

All eyes were on the parade of earnings reports from the technology behemoths this past week. But what grabbed the markets’ attention were the implications of their massive capital investments in artificial intelligence on their balance sheets and cash-flow statements.

At the center of this debate was Meta Platforms, which plunged 11% on Thursday after reporting a miss on earnings but, more importantly, said it was pushing full-speed ahead on AI data centers, projecting $71 billion in spending, up from $69 billion previously. Moreover, the company said that capital expenditures “will be notably larger in 2026 than 2025.”

All of which is absorbing increasing amounts of megatechs’ cash flow. As Doug Kass of Seabreeze Partners observes, the so-called hyperscalers have morphed from being “capital light” to capital-intensive operations. In the process, they have had to turn to external financing for their ambitious AI buildouts.

In fact, Meta brought this year’s biggest investment-grade corporate bond deal to market, totaling some $30 billion, the latest in a parade of recent data-center borrowing. Bank of America tallies $75 billion of AI-related public debt offerings in the past two months.

And that doesn’t count other financings, including Meta’s creative off-balance-sheet funding of its Louisiana data center, described by colleague Adam Levine in last week’s Tech Trader column. That includes a $38 billion loan tied to Oracle’s data centers, on top of $18 billion of public bonds issued by the company, led by world’s second-richest person, Larry Ellison.

Putting numbers to Kass’ point, BofA credit strategists Yuri Seliger and Sohyun Marie Lee write in a client note that capital spending by five of the Magnificent Seven megacap tech companies (Amazon.com, Alphabet, and Microsoft, along with Meta and Oracle) has been growing even faster than their prodigious cash flows. “These companies collectively may be reaching a limit to how much AI capex they are willing to fund purely from cash flows,” they write.

Read the rest of the Barron's column here:

Meta Stock Took a Dive. It’s the Poster Child for the Debate Over AI Spending. - Barron's

Importantly, the unprecedented AI spend soaking up and most of the large free cash flow generation means that there is a reduced amount of money available for company buybacks (that have buoyed share prices of the Mag 7 constituents).

The uncertainty and risks introduced and associated with the outsized capital spend are simply not valuation friendly.

We sold our last Mag 7 long, Amazon (AMZN) , two days ago at $237.50, and have no current intention of returning to large-cap technology.

See my "More Tales of Nvidia" series, which is comprised of 174 columns, written over the last 15 months, that has cautioned, among other things, about the returns from the massive AI spend.

BY Doug Kass · Feb 6, 2026, 7:31 AM EST

BY Doug Kass · Feb 6, 2026, 7:00 AM EST

Bonus — Here are some great links:

BY Doug Kass · Feb 6, 2026, 6:45 AM EST

BY Doug Kass · Feb 6, 2026, 6:25 AM EST

BY Doug Kass · Feb 6, 2026, 6:15 AM EST

Wolf Street howls about bitcoin and Strategy.

BY Doug Kass · Feb 6, 2026, 6:05 AM EST

The S&P Short Range Oscillator dipped back into oversold at -0.44% vs. 1.01%.

I have no index positions on currently.

BY Doug Kass · Feb 6, 2026, 5:55 AM EST

Dougie Kass

I purchased a small trading long rental in bitcoin - via IBIT at $35.72

Dougie Kass

I just sold half of my IBIT at $37.26

BY Doug Kass · Feb 6, 2026, 5:45 AM EST