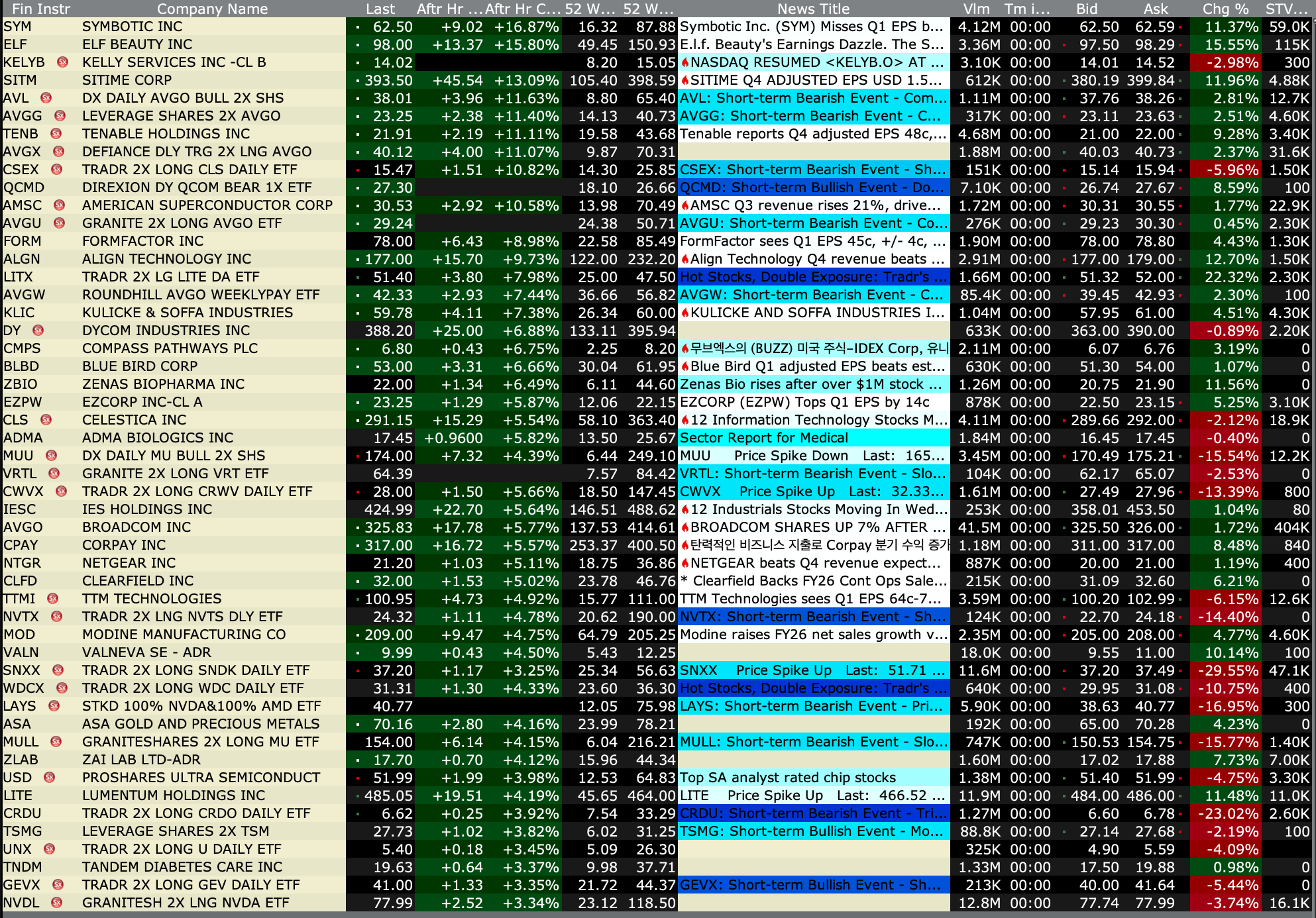

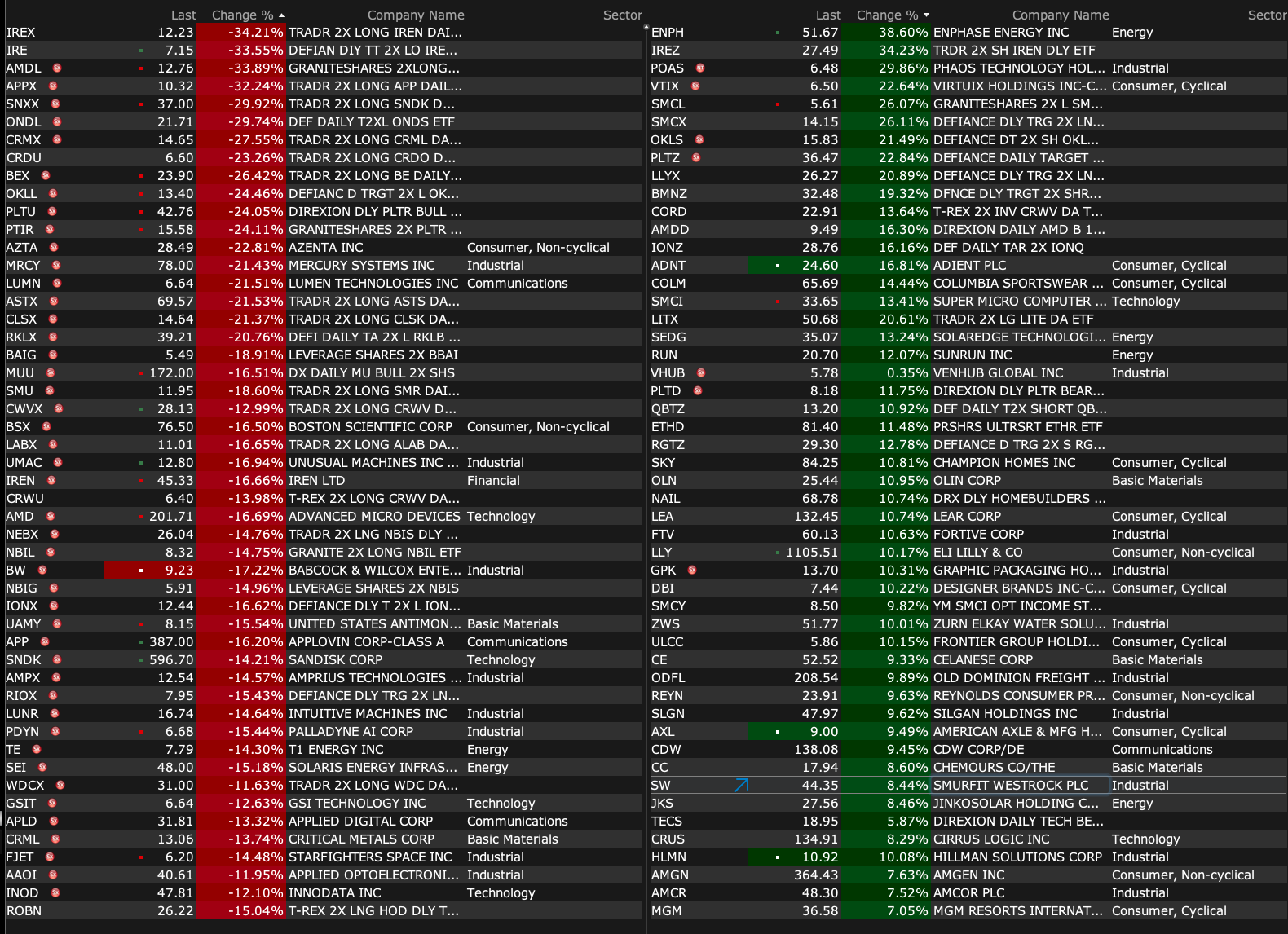

After-Hours Advancers and Decliners

After-Hours % Advancers

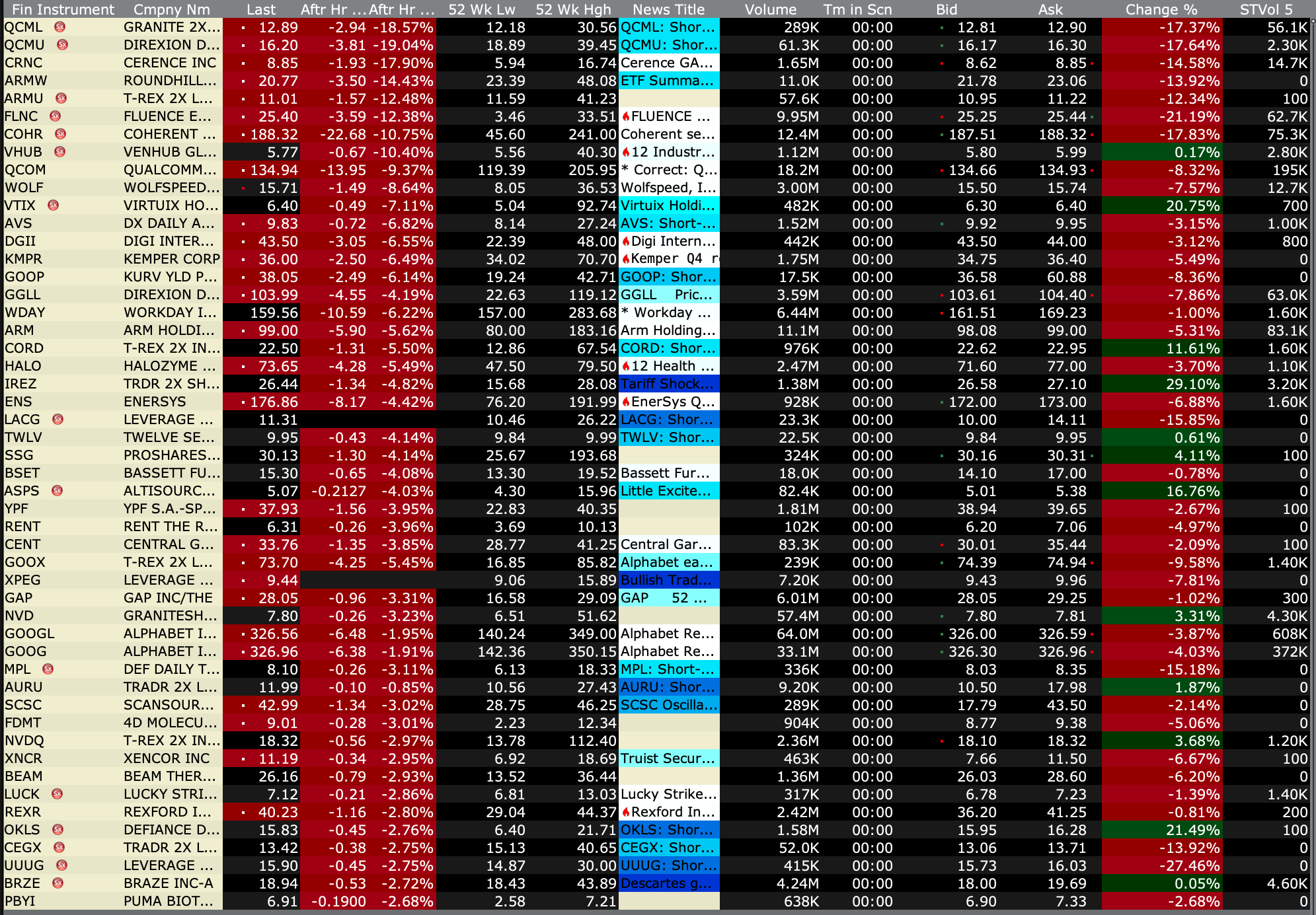

After-Hours % Decliners

BY Doug Kass · Feb 4, 2026, 4:45 PM EST

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Feb 4, 2026, 4:45 PM EST

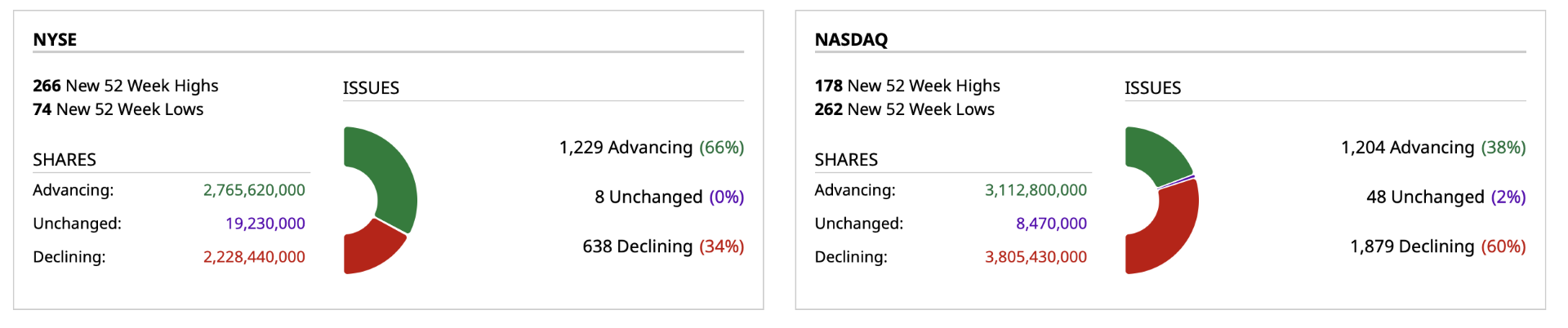

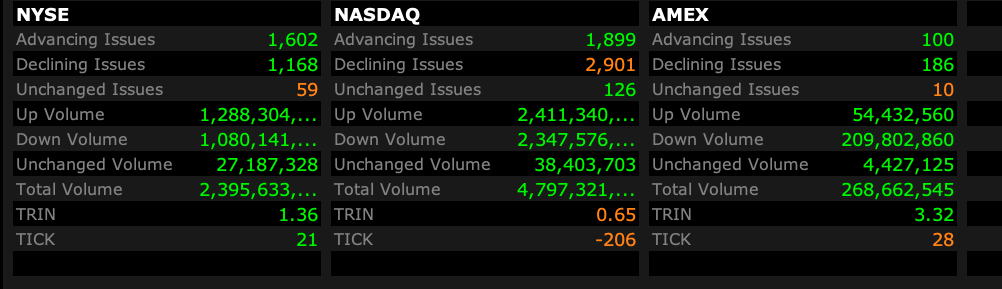

- NYSE volume 48% above its one-month average;

- NASDAQ volume 24% above its one-month average;

- VIX index: up 3.56% to 18.64

BY Doug Kass · Feb 4, 2026, 4:27 PM EST

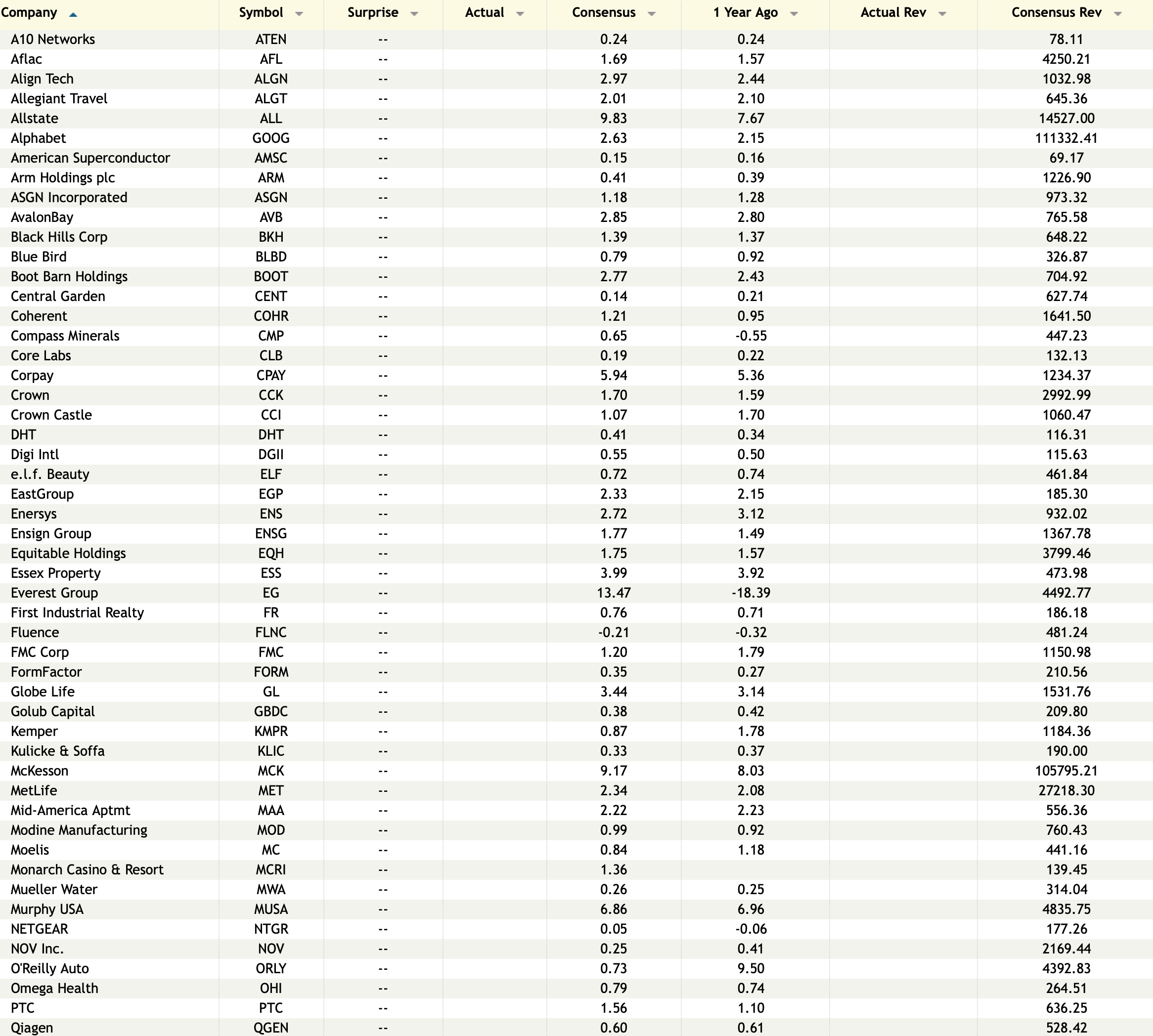

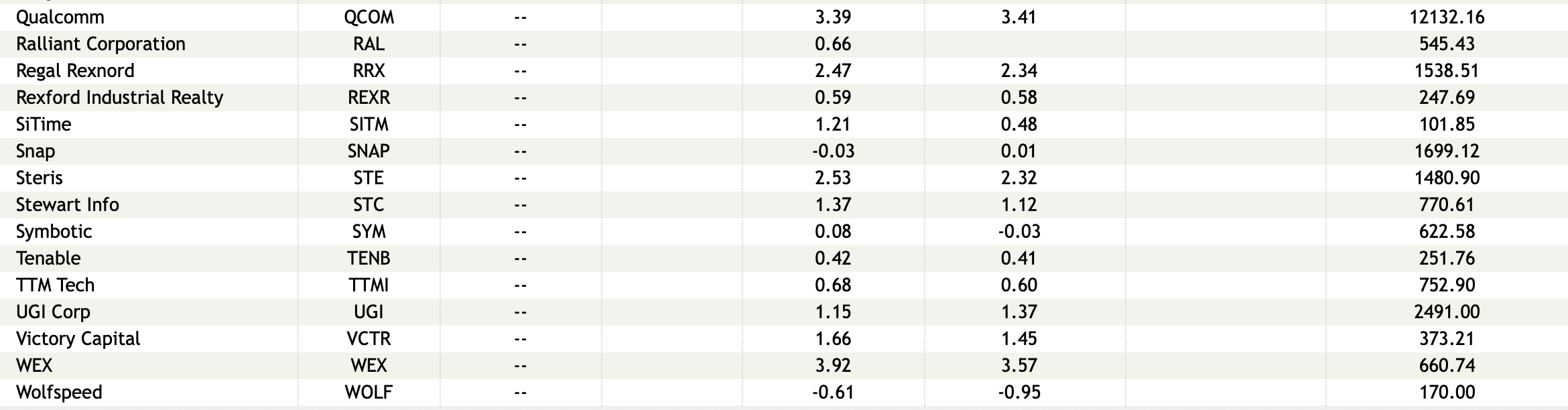

Earnings After the Close Wednesday, Feb. 4

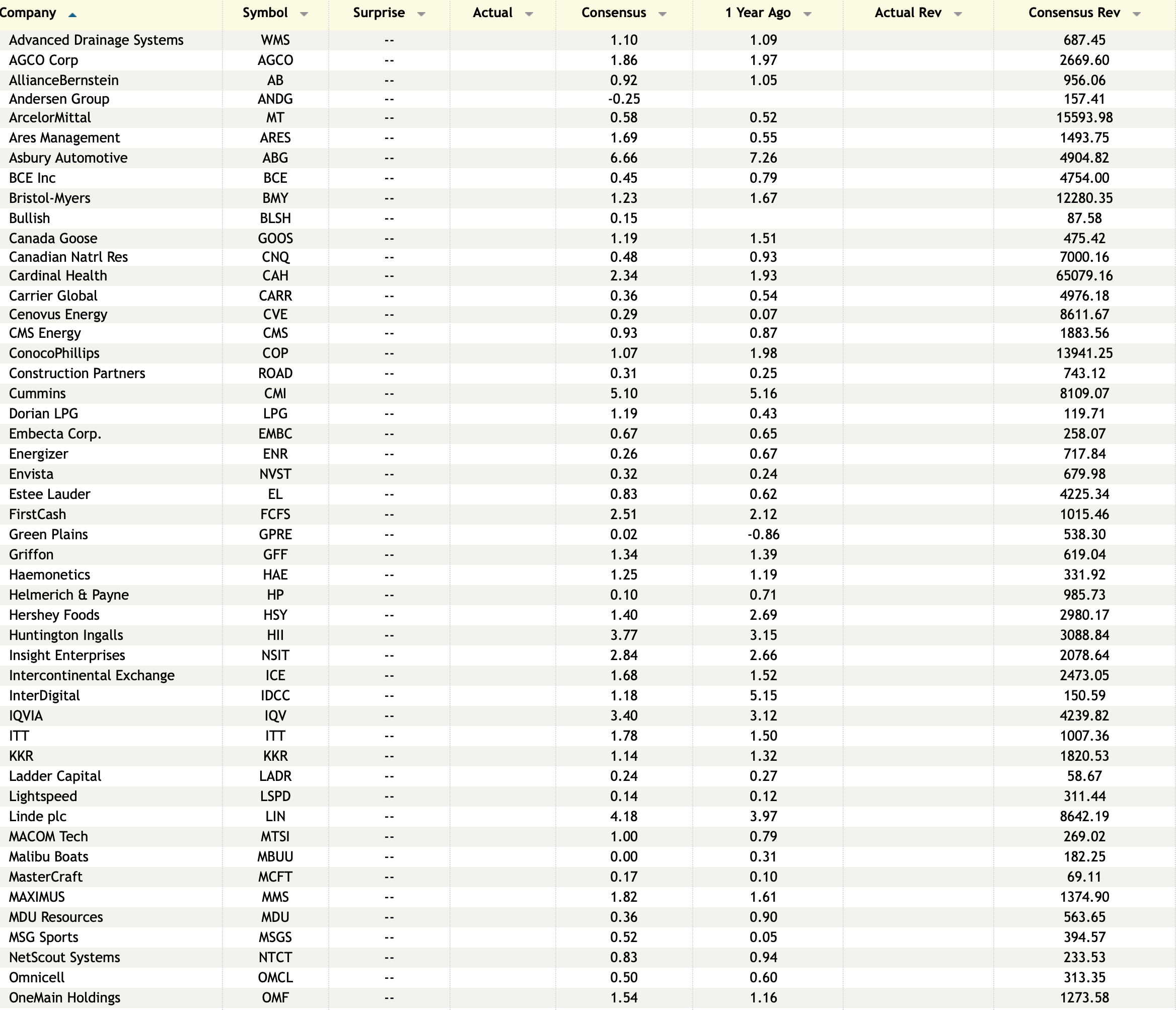

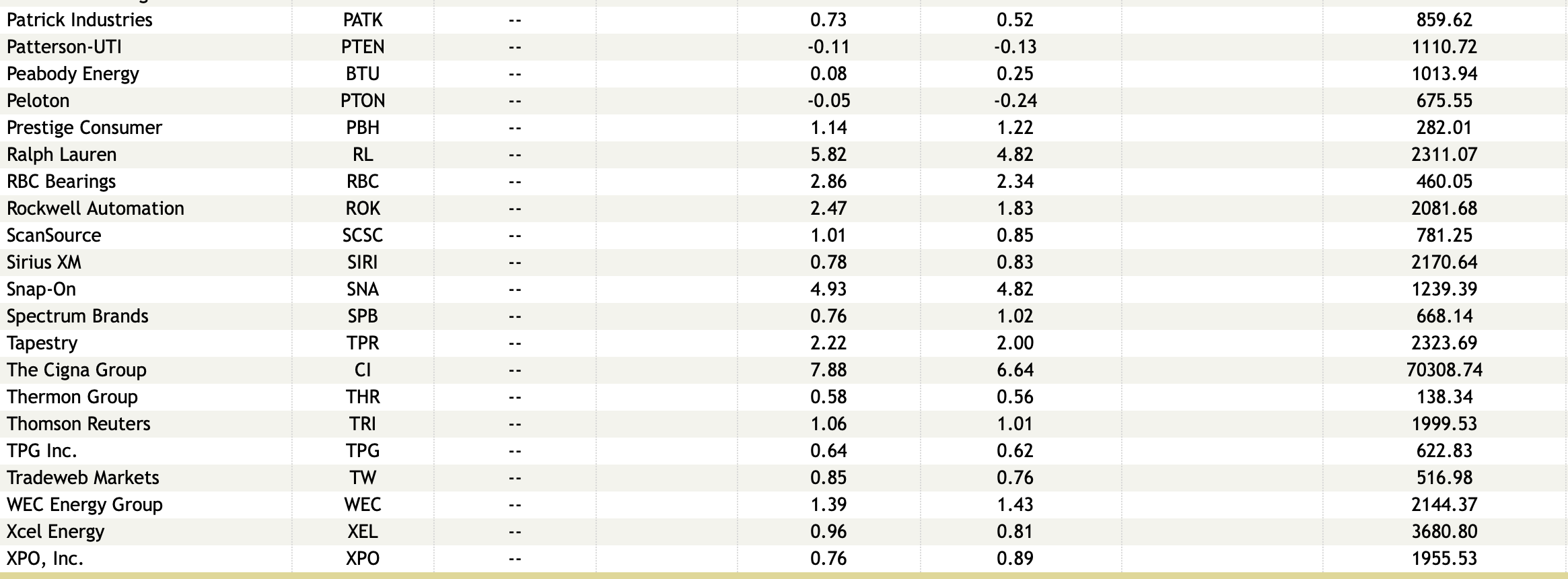

Earnings Pre Open Thursday, Feb. 5

BY Doug Kass · Feb 4, 2026, 3:32 PM EST

Others are hearing what I am hearing on a (possible) cannabis rescheduling announcement.

BY Doug Kass · Feb 4, 2026, 3:12 PM EST

Wolf Street howls about job revisions.

BY Doug Kass · Feb 4, 2026, 3:06 PM EST

From my perch, this is as comical as Tom Lee's optimistic projections:

BY Doug Kass · Feb 4, 2026, 2:30 PM EST

I have covered my (REZI) short ($35.71) for a small profit.

BY Doug Kass · Feb 4, 2026, 1:50 PM EST

I have covered the balance of my Carvana (CVNA) short at $369.25 (-$41) for a profit.

I plan to re-short on strength.

BY Doug Kass · Feb 4, 2026, 1:41 PM EST

I have covered my CoreWeave (CRWV) short at $83.06 for a profit.

I plan to re-short on strength.

BY Doug Kass · Feb 4, 2026, 1:35 PM EST

I just covered my Zillow (Z) short at $56.18 for a profit.

I shorted Zillow in December at about $70 share:

I am short Zillow.

From my friends at BTIG:

December 17, 2025

Zillow Group, Inc. (ZG) Neutral

GOOG Test of Sponsored For-Sale Listings in Mobile Still Going

--------------------------------------------------------------

### What You Should Know:

A Google (GOOG, Not Rated) test placing for-sale home listings at the top of mobile search results sparked concern last weekend that it could be mounting a challenge to ZG & CoStar's (CSGP, Neutral) Homes.com. The test appeared to run afoul of industry advertising rules & by yesterday nobody we spoke to was able to surface the listings anymore, leading to speculation that the test had been pulled & sparking some relief for ZG. We were able to surface the mobile for-sale listings test in a search conducted this morning, w/listings still including data from the same platform as before along w/sponsored links paid for by brokers. This saga may not be over just yet...While scary, this isn't relevant to near-term estimates & we are not contemplating any related impact to numbers.

Position: Short Z VS

By Doug Kass Dec 17, 2025 10:40 AM EST

BY Doug Kass · Feb 4, 2026, 1:30 PM EST

I have covered my Freedom Holdings (FRHC) at $113.95 (-$7) for a nice gain in the last month.

BY Doug Kass · Feb 4, 2026, 1:25 PM EST

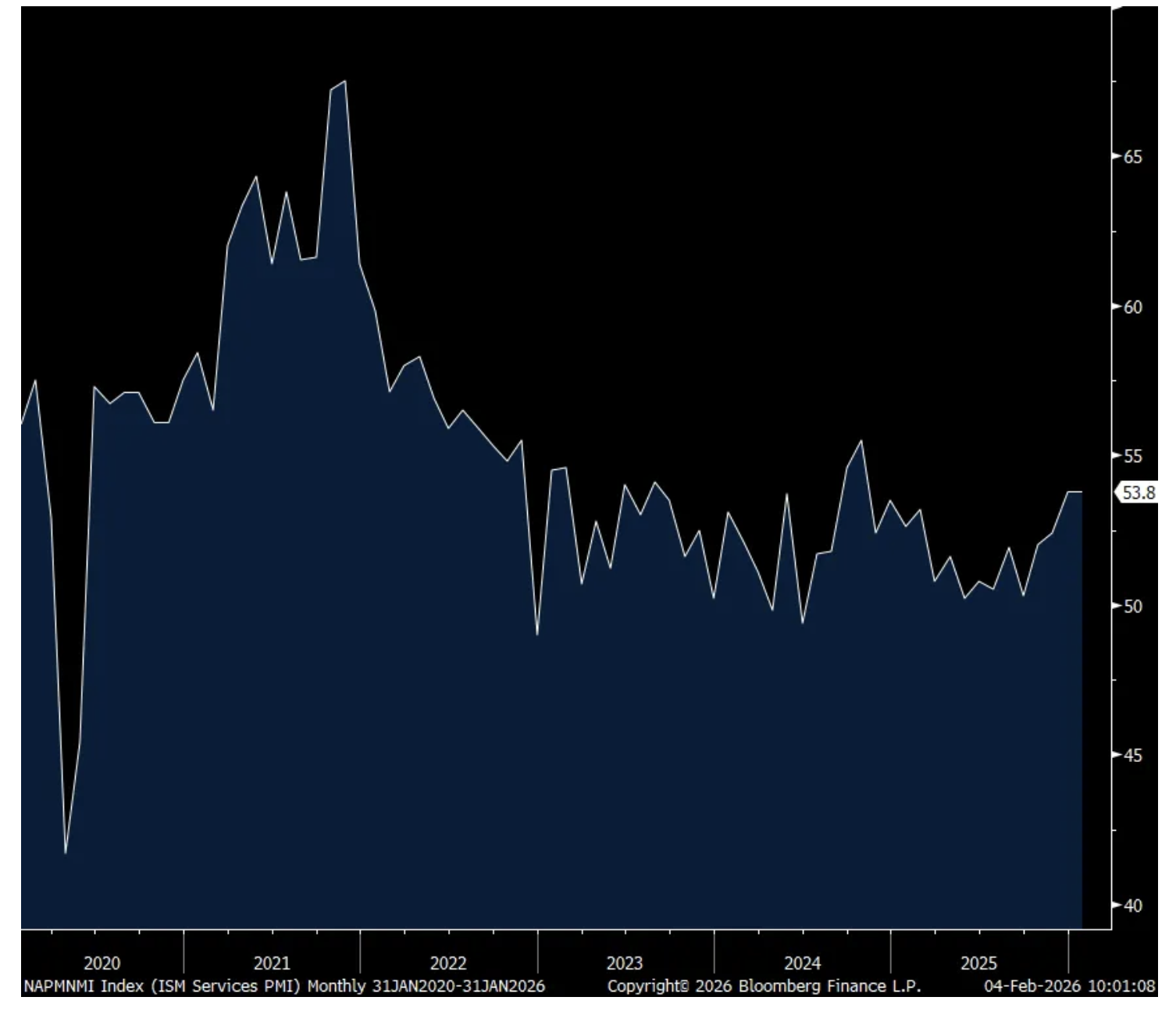

From Peter Boockvar:

The January ISM services index was unchanged m/o/m at 53.8, though a touch above the estimate of 53.5 (December was revised from 54.4). The business activity component lifted to 57.4 from 55.2 and 3 pts above the 6 month average.

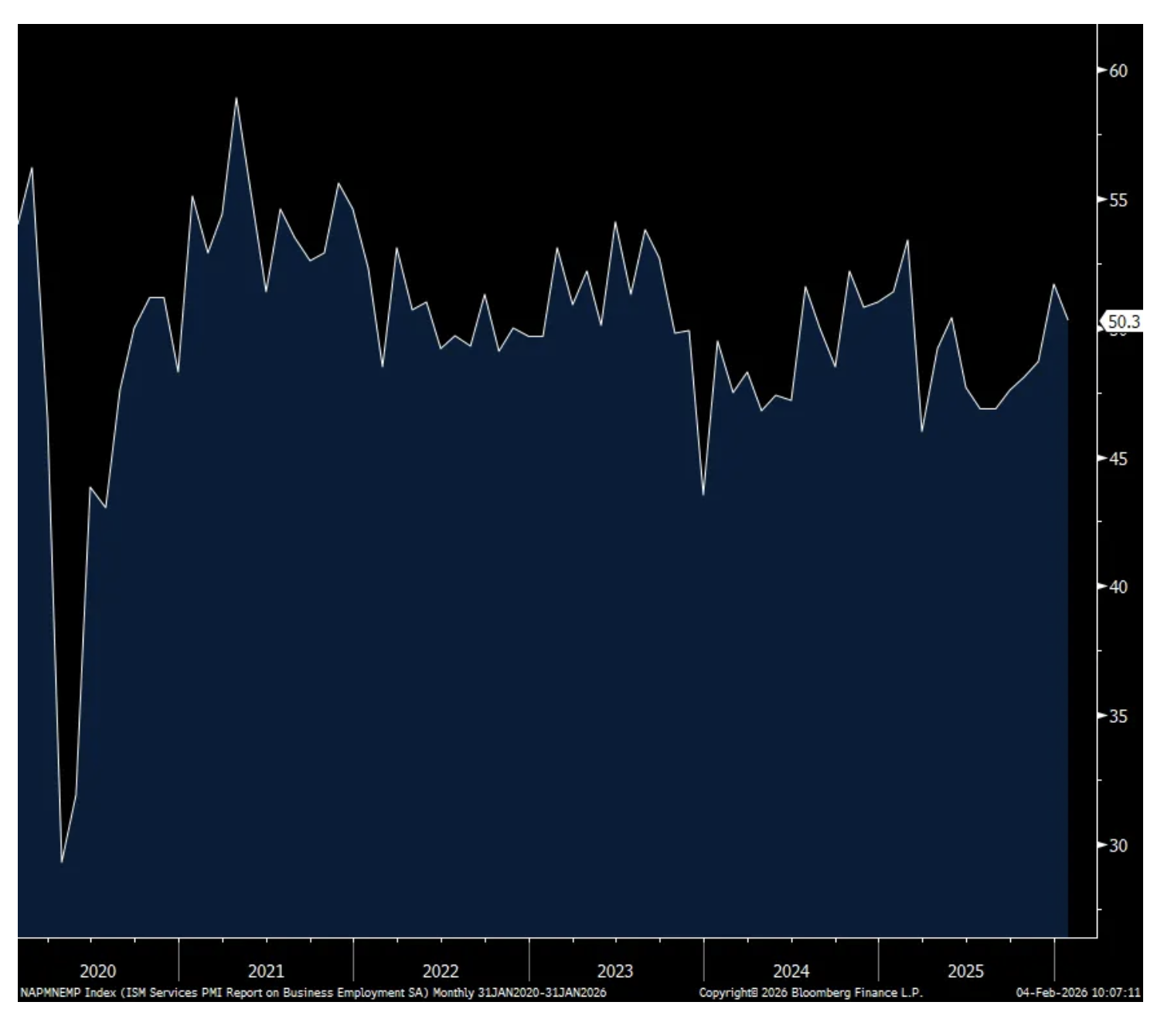

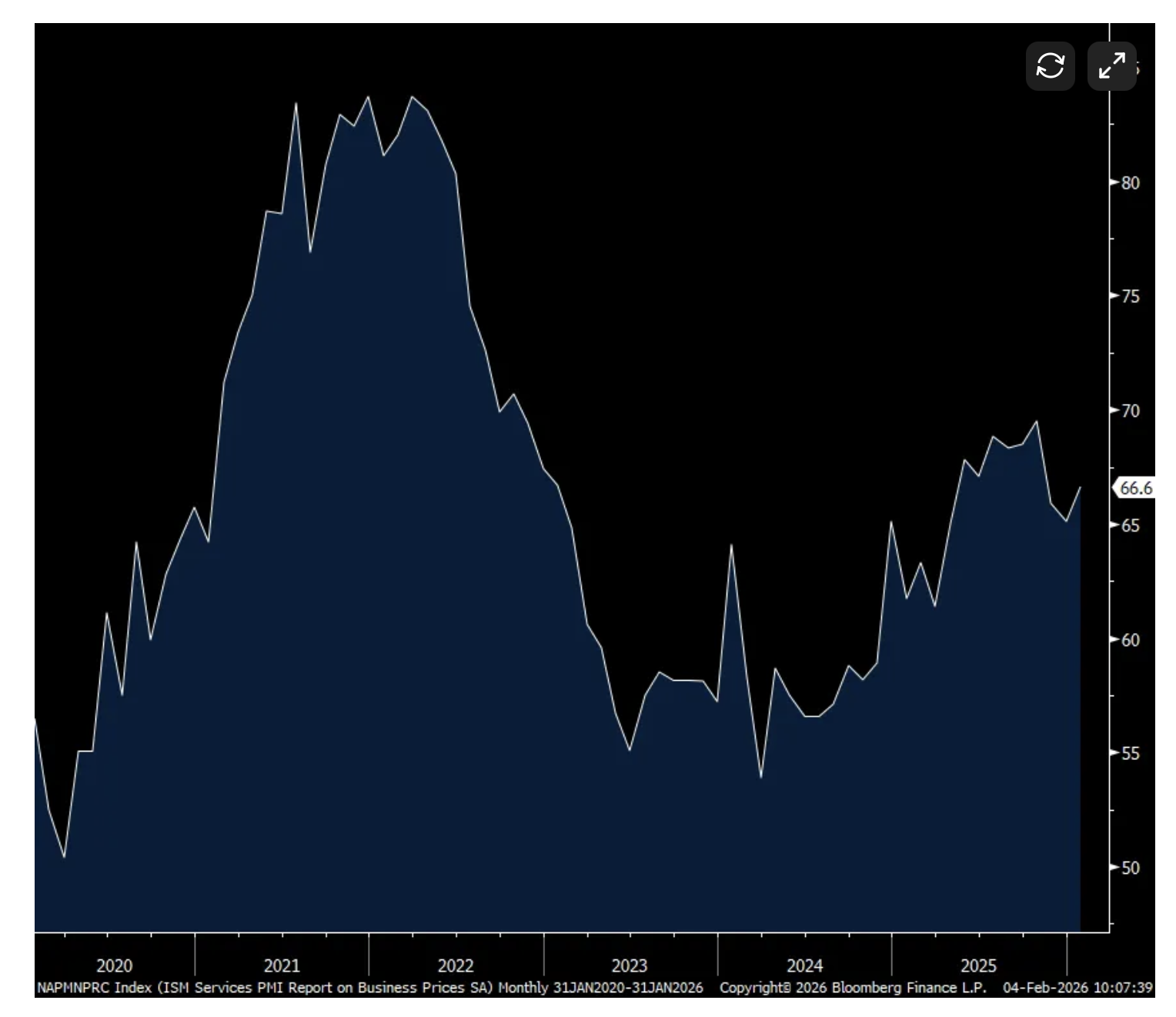

New orders slipped 3.4 pts but after rising by 3.7 pts last month. Backlogs are still below 50 at 44, exactly where the half yr average is at. Inventories took a big dive, down 9.1 pts to 45.1. Employment was down 1.4 pts to 50.3, though holding above 50 for a 2nd month after a string of below 50 prints. That said, just 5 of 18 industries added new workers. Supplier deliveries reflect longer lead times. Finally, prices paid rose 1.5 pts m/o/m to 66.6, remaining well above 50. There are now 17 industries paying higher prices of 18 asked up from 15 in December.

Industry breadth remained the same with 11 of 18 sectors reporting growth and 5 seeing a contraction.

ISM said this of note, “There was more respondent commentary in January on tariff impacts and uncertainty, potentially the result of annual contract renewals and geopolitical tensions. Gasoline and diesel fuel continued to be cited as commodities down in price. With the highest Business Activity and Supplier Deliveries index readings since October 2024, indicating higher business activity levels and slower supplier deliveries, whether pricing increases will stick or expand needs to be closely watched.”

The comments below were mixed.

“The uncertainty of U.S. tariff policies continues to affect our purchasing. The proliferation of AI is affecting how we purchase services, particularly getting more value out of service contracts and taking a harder look at risk.” [Accommodation & Food Services]

“Pending surge in new capital investments of our customers, specifically in data centers, combined cycle power, and nuclear market sectors. Expect significant business growth in 2026, both in the domestic U.S. and globally.” [Construction]

“Our business has stayed pretty consistent over the past few months.” [Finance & Insurance]

“AI data center construction is expected to cause constraints in the IT market and availability. We haven’t seen delays on IT equipment yet but expect them in the coming months.” [Health Care & Social Assistance]

“Still slow but more optimistic.” [Management of Companies & Support Services]

“Overall business is slow coming out of the end of year and holidays.” [Other Services]

“Supply chain is steady. Prices are leveling off.” [Public Administration]

“Solid holiday performance across most units. January is even better. Consumers are still buying discretionary goods.” [Retail Trade]

“Typical slow start. A lot of busy activity quoting, reports and the like.” [Transportation & Warehousing]

“Data centers are causing large spikes in requirements. Suppliers are challenged by capacity and tariffs. Therefore, this is both an exciting and challenging time in the industry.” [Utilities]

Bottom line, the service sector continues to carry the US economy, and certainly helped by the construction of data center buildings and everything that includes, as it usual does but under the hood remains an uneven picture. Treasury yields are at the highs of the day but didn’t respond much to the number.

ISM Services

Employment

Prices Paid

BY Doug Kass · Feb 4, 2026, 1:15 PM EST

I have covered my (GRNY) short at $24.18 (-$0.82).

I plan to re-short strength.

BY Doug Kass · Feb 4, 2026, 12:55 PM EST

Here are today's things:

* I covered my (ARKK) short at $70.36.

* I initiated a (HOOD) long at $83.45.

* I added to (MSOS) at $4.02.

* I sold out of my (AMZN) long at $237.14.

BY Doug Kass · Feb 4, 2026, 12:45 PM EST

BY Doug Kass · Feb 4, 2026, 12:35 PM EST

I'm adding to (MSOS) at $4.00.

BY Doug Kass · Feb 4, 2026, 12:22 PM EST

BY Doug Kass · Feb 4, 2026, 12:14 PM EST

BY Doug Kass · Feb 4, 2026, 11:50 AM EST

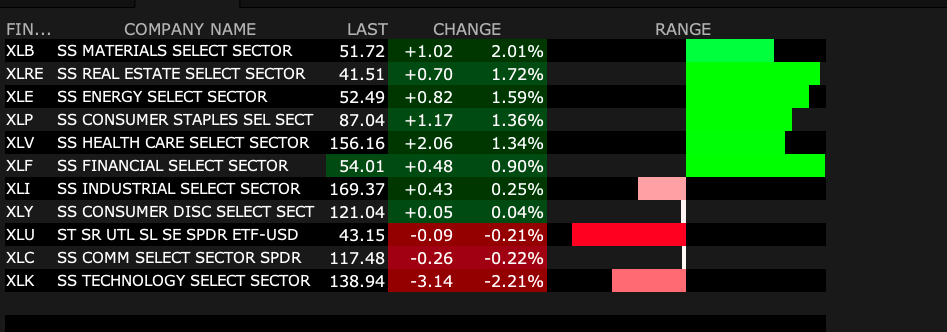

Tech (XLK) vs Financials (XLF) at 11:20 a.m.:

BY Doug Kass · Feb 4, 2026, 11:40 AM EST

I have covered my (ARKK) short (-$3) at $70.36 for a profit.

BY Doug Kass · Feb 4, 2026, 11:33 AM EST

"It's and easy game, if you can control your emotions." - Warren Buffett

BY Doug Kass · Feb 4, 2026, 11:20 AM EST

At $237.14 I have sold the balance of my (AMZN) long.

BY Doug Kass · Feb 4, 2026, 10:55 AM EST

(ARKK) is down a quick -$10 and I have covered some at $71.23.

I had recently mentioned this name as one of my favorite shorts:

Favorite Long: None

Favorite Short: (GRNY) / (ARKK) (it's a tie!)

Position: Short GRNY (M), ARKK (VS)

By Doug KassJan 29, 2026 7:10 AM EST

BY Doug Kass · Feb 4, 2026, 10:51 AM EST

I have moved to medium-sized long in (HOOD) under $80/share.

BY Doug Kass · Feb 4, 2026, 10:46 AM EST

Covering some (CVNA) (-$29) at $381.10.

BY Doug Kass · Feb 4, 2026, 10:36 AM EST

From Peter Boockvar:

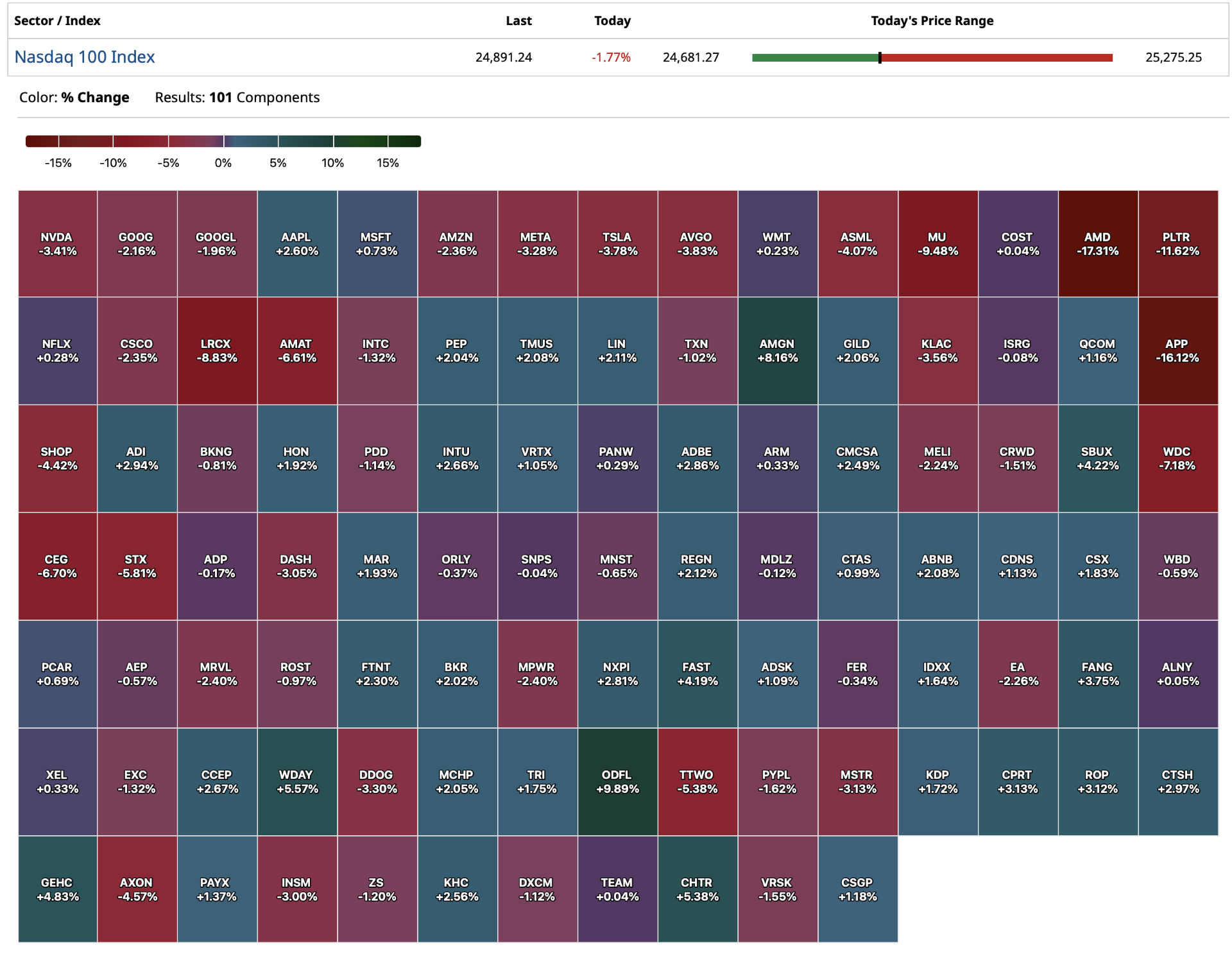

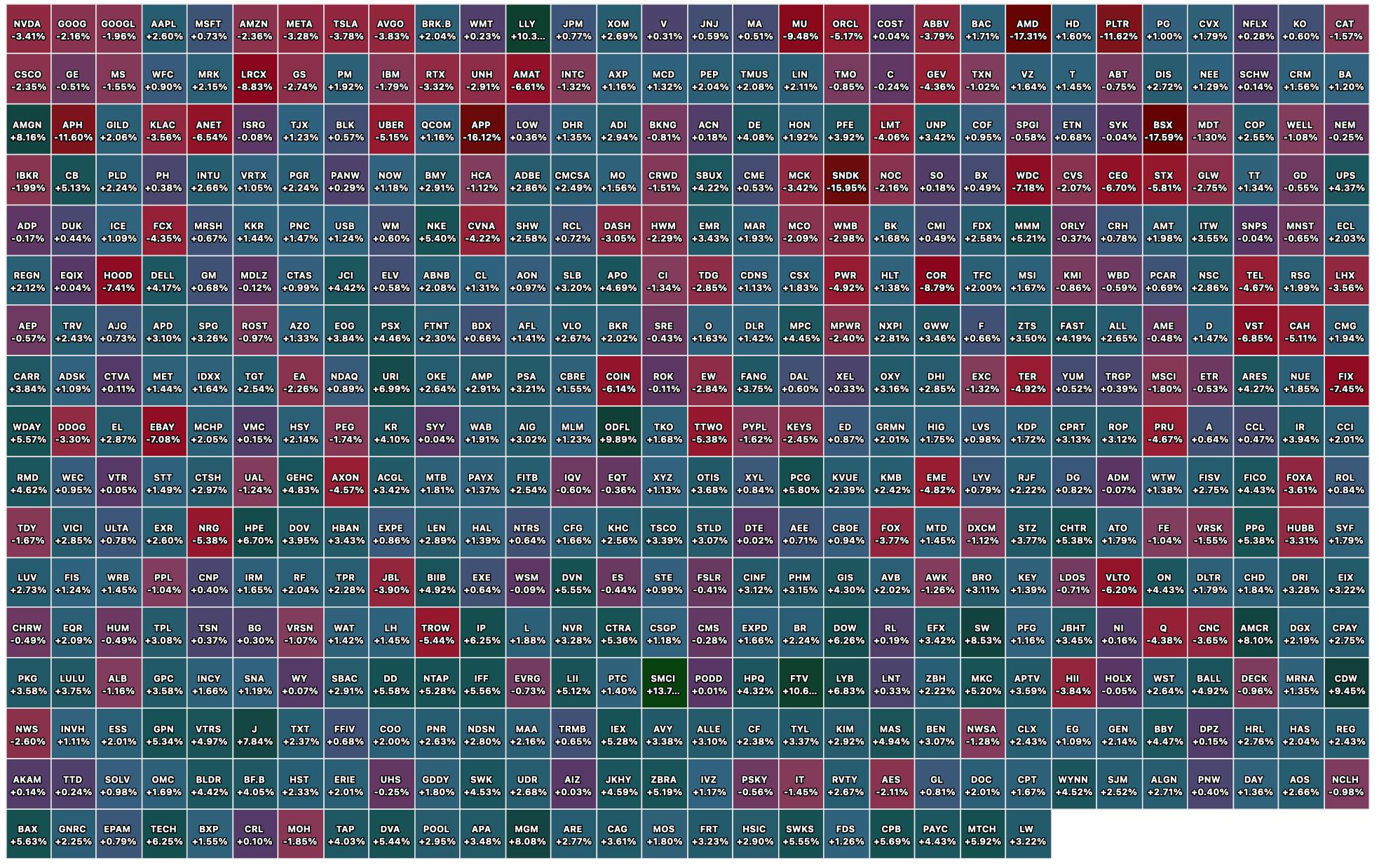

I’ve been asking out loud for weeks what is going on in the private credit space as seen with the sharp drop in the LSTA Leveraged Loan index and BDC (business development company) stocks (already weak because of dividend cuts due to lower interest income on their floating rate debt they hold). Well, we finally seem to be getting our answer. Barclays estimates that about 20% of the BDC market has loans tied to the software space and we of course see what is going on. I saw a quote in a Bloomberg article from someone at Raymond James that thinks that 20% figure is even too low. “If your software business is in healthcare, the fund classifies it as a healthcare exposure. The software exposure is meaningfully higher than it looks.” Yes, the Anthropic news yesterday resulted in more broad based selling in the space but this selling started before yesterday.

Separately but tied to GenAI, so many bells are ringing on the waning dominance of the AI tech trade and the Too Big To Fail business of OpenAI which I marked them with that moniker back in September. Oracle’s huge exposure to them, margin compression and balance sheet stresses, Open AI’s growing competition from Gemini, among others, questions about the Nvidia/OpenAI relationship, Google’s TPU growing competition with Nvidia’s GPUs along with increased competition from AMD and others, Coreweave’s stock down by half, Broadcom falling 20% from its peak, AMD getting hammered today, Meta having reported two phenomenal quarters in a row but whose stock peaked back in August as investors focus on their massive spend, Microsoft yesterday closing at its lowest level since last May, down 24% from its October top and the increasing intensity of the competition from China both on the AI side but also on the chip side.

Bottom line, something I said back in late November, the GenAI tech trade is no longer a one way ride. We’ve transitioned it from ‘buy everything’ to ‘not everyone can win.’ I believe we are losing this trade in terms of its ability to carry the market but luckily so far investors have found other things to buy and that includes other parts of the S&P 500, small and mid cap and for sure international stocks. Can this last, I don’t know because of the huge concentration of the group but I hope so. I continue to believe that a port in the storm is the beaten up consumer staples stocks, both in food and consumer products, and we are positioned as such in a bunch of them, along still with commodities because of supply issues.

As we saw with the internet buildout, eventually the real benefits accrued to the users of the technology and the businesses built on top of it rather than the builders of the infrastructure and maybe that pivot is about to happen?

Shifting gears, no pun intended, US vehicle sales in January were weak, totaling just 14.85mm vs the estimate of 15.2mm. That compares with 15.6mm in January 2025 and 16.84mm in January 2020 right before you know what. Affordability still an issue here too with record high vehicle prices.

On why we still own platinum (after selling a bunch of silver) is that hybrids are winning the EV war and they use more platinum in each vehicle battery than an ICE vehicle uses platinum. A story in Nikkei News today, “Toyota Motor plans to make around 30% more hybrid vehicles in 2028 compared with current production levels and expand their manufacture significantly in the US, as consumers react to countries cutting incentives to buy pure electric vehicles. The world’s biggest carmaker by sales expects to produce 6.7 million hybrid vehicles globally in two years time, up from a planned 5 million hybrid and plug-in hybrids in 2026, according to suppliers familiar with Toyota’s plans.” About 40% of the demand for platinum comes from the auto sector (vs 80% for palladium) and the three largest producers of the metal are South Africa, Russia and Zimbabwe.

From Pepsi, a stock we own in consumer staples industry and which rallied 5% yesterday:

“Following extensive consumer feedback around affordability limitations and subsequent market tests on sharper price points during the second half of 2025, we have begun offering greater affordability on certain packages of iconic brands (such as Lay’s, Tostitos, Doritos and Cheetos). These initiatives aim to improve the purchase frequency of our brands with consumers.”

Selective price cuts in these products is meant to drive demand. “We think that for some consumers, low and middle income consumers, the biggest friction they have today in our category for faster penetration is affordability. So, we have been testing multiple ways to give them affordability. So, this will be a very surgical, very focused on particular brands, particular formats, particular channel investment. And from the tests that we’ve done at scale in multiple markets, this has very good ROI for us.”

On the macro with their consumer, “clearly a middle and low income consumer that continues to be stretched and choiceful, and that we have to earn being part of their basket every day. I think that’s how we’re thinking about it for the US. Internationally, we’re seeing different parts of the world behaving differently, but we’re optimistic about Mexico…We’re seeing positive trends in China. Again, I’m referring to our business and the surroundings of our business rather than larger macros. And we’re seeing a positive situation in the Middle East. We’re seeing a good consumer there as well. A bit weaker in Western Europe. And then Brazil kind of neutral.” Those are their bigger markets.

From Madison Square Garden Entertainment, another stock we own and where live events are still in high demand:

“These results were led by another record setting year for the Christmas Spectacular in its 92nd holiday season run. This quarter’s results also reflected growth across virtually every other aspect of our business. That included bookings, sponsorships, and suites, as well as the various revenue streams related to the Knicks and Rangers.”

“From a demand standpoint, the majority of concerts across our portfolio of venues were again sold out during the second quarter. In terms of in-venue spending, merchandise per caps at concerts were up in the quarter, while food and beverage per caps were down, both of which we primarily attribute to the mix of events.”

From Capri Holdings, the owner of Michael Kors and Jimmy Choo, and whose stock dropped by 13% yesterday:

The top line seemed to be ok relative to expectations (Jimmy Choo outperforming Kors), though still fell y/o/y, but it was the margin squeeze from tariffs that drove the stock lower. “Now looking at total company margin performance. Gross margin of 60.8% declined 230 bps. Underlying gross margins expanded by 70 bps due primarily to better full price sell throughs and a reduction in promotional activity. This was offset by higher than anticipated tariffs based on the sales mix of new product.”

Paypal plunged by 20% along with a management shakeup. These were some macro comments:

“in the fourth quarter, online branded checkout TPV (total payment volume) grew 1% on a currency neutral basis, down from 5% in the third quarter. The four point deceleration was more than we expected and was concentrated in three main areas, each contributing roughly a point or so to the slowdown.”

“First, US retail weakness. We saw pressure across our retail merchant portfolio, particularly among lower and middle income consumers. While part of this can be attributed to macro factors and a K shaped economy, it’s also clear that we need to do more to win with key merchants, particularly during high volume shopping periods.”

“Second, international headwinds, particularly in Germany, which is one of our largest markets. Our German growth has moderated due to macroeconomic softness, normalization of our long standing market leadership position, and competition from alternative payment methods.”

“Third, deceleration in several high growth verticals, specifically in travel, ticketing, crypto and gaming, categories that had strong growth in the fourth quarter of ’24 and continuing through much of ’25.”

From NXPI Semiconductors, with its heavy industrial exposure and down 4.5% yesterday due to softer than expected auto related sales:

“The year was a tale of two halves, with the first half of the year exhibiting weaker demand trends, while in the second half of the year, demand began to accelerate in support of our long term revenue growth model.”

Their auto business was flat y/o/y “due to slower inventory digestion of direct customers in the first half of 2025. With the inventory digestion behind us, the second half performance aligns with our long term outlook.”

Their industrial and IoT end market saw flat revenues too y/o/y. Mobile grew 6% while communication infrastructure dropped by 24%.

Illinois Tool Works rallied almost 6% as their business seems to be stabilizing. They said of note:

“Starting with the top line, organic growth of 1.3% marked our best quality performance of the year. Overall, Q4 demand improved.”

From WW Grainger on how they are dealing with tariffs:

“In the fourth quarter, we remained engaged in active dialogue with our supplier partners and took modest price increases in November to help offset continued cost pressure. These actions were on top of the price increases in May and September, when we began to pass through tariff related costs. In January of this year, we passed further price in response to previously delayed tariff inflation and to offset annually negotiated cost increases with our suppliers, which were largely in effect as of February 1st.”

On their business outlook, “In the US, we anticipate continued demand pressure as tariff related price increases weigh on market volumes, and while we expect industry specific tailwinds in certain areas of the economy will persist, many of these green shoots are outside of core MRO product categories.”

From Chipotle, trading down pre-market:

Comps fell 2.5% in Q4 with “a dynamic consumer backdrop, with our guests placing heightened focus on value and quality and pulling back on overall restaurant spending.”

“we anticipate cost of sales inflation to be higher in the first half of the year, and we’ll step down to the low to mid single digit range in the second half of the year as we lap elevated beef costs. This results in full year cost of sales inflation in the mid single digit range.”

They see wage inflation “in the low single digit range.”

They are taking a margin hit “I would anticipate pricing to be in that 1% to 2% range, while inflation will be closer to that 3% to 4% range.”

Should the Fed cut because of slower consumer price inflation or not because of still higher level cost inflation eaten here by Chipotle? I say the latter as a kid who puts his hands over his/her eyes and think they are invisible, less consumer price inflation doesn’t mean we don’t have an inflation issue still.

Some stats on their customer, “the guest skews younger, a little more higher income, is typically a digital native” and they like “clean food, clean ingredients, high protein.” As for the demo, “60% of our core users are over $100,000 a year in income, in average household income.” Thus 40% are making less and are more subject to financial pressures.

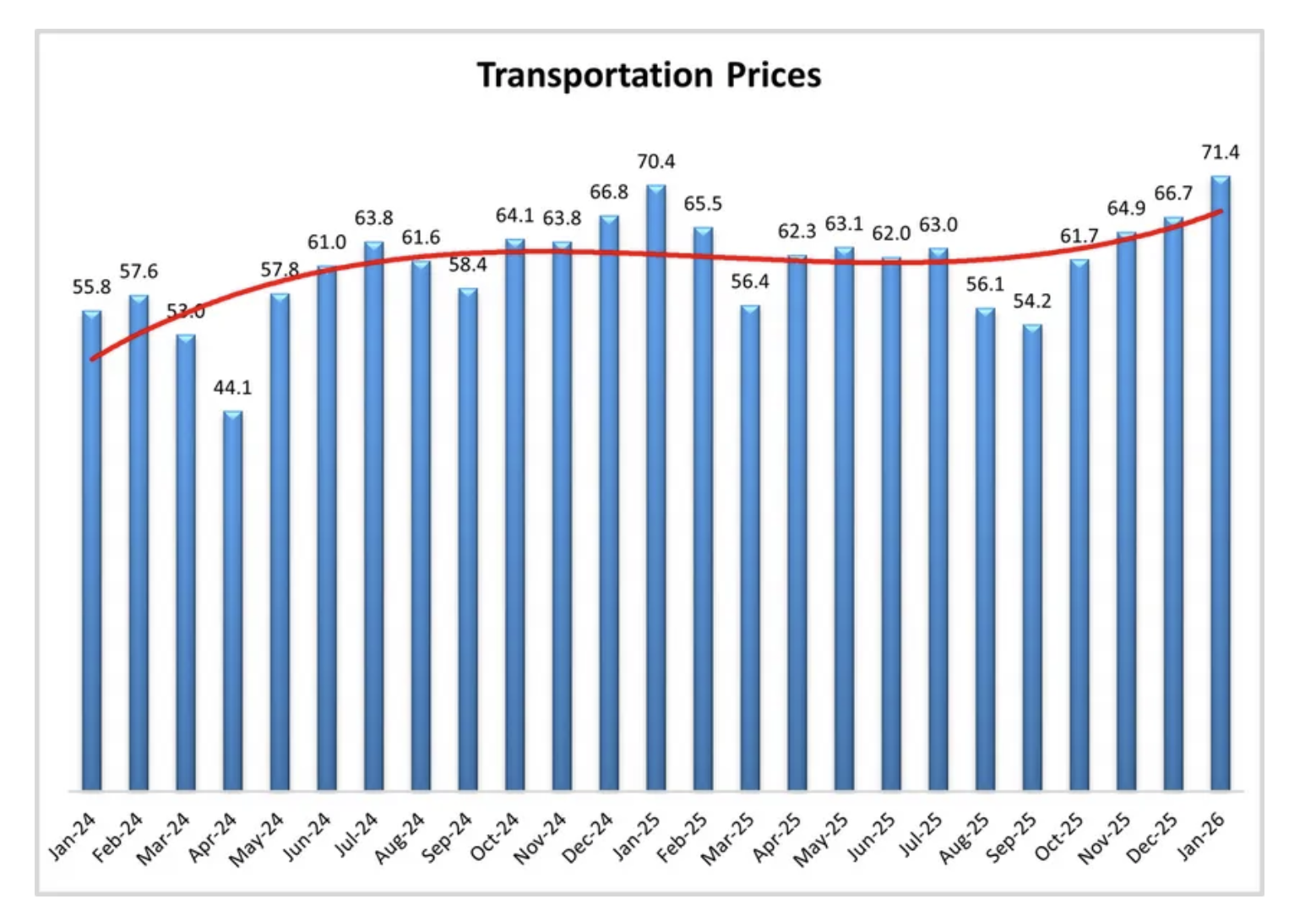

Again shifting gears, to the trucking stocks and its boost to the DJ Transportation Index. What I’ve highlighted here a few times over the past few weeks when listening to the earnings calls of some truckers, capacity is leaving the industry quickly and prices are firming up even though volumes aren’t changing much. Yesterday the Logistics Managers index for January said “This continued tightening led to another increase (+4.8) in transportation prices, which at 71.4 is expending more quickly than any time since April of 2022.”

While the average 30 yr mortgage rate was little changed w/o/w, purchase applications fell by a sharp 14.4% while refi’s were lower by 4.7%. Listening to the earnings calls of some home builders the last few weeks, affordability issues still are a major factor, notwithstanding the drop in mortgage rates over the past year.

Some more January PMI’s, mostly focused on services:

Singapore 56.8 vs 54.1

Hong Kong 52.3 vs 51.9

China services 52.3 vs 52

Japan services 53.7 vs 51.6

Australia services 56.3 vs 51.1 (no wonder why they hiked rates)

Eurozone services 51.6 vs 52.4

UK services 54 vs 51.4

European bonds are getting a lift after headline CPI in January rose 1.7% as expected vs 2% in the month before. The core rate was higher by 2.2%, one tenth less than expected. Inflation is still being driven by services where prices rose 3.2% y/o/y. The inflation in Europe is very mixed country wise with Germany reporting January CPI up 2.1% while in France prices rose .4%. How does a central bank conduct policy in an economic situation like this?

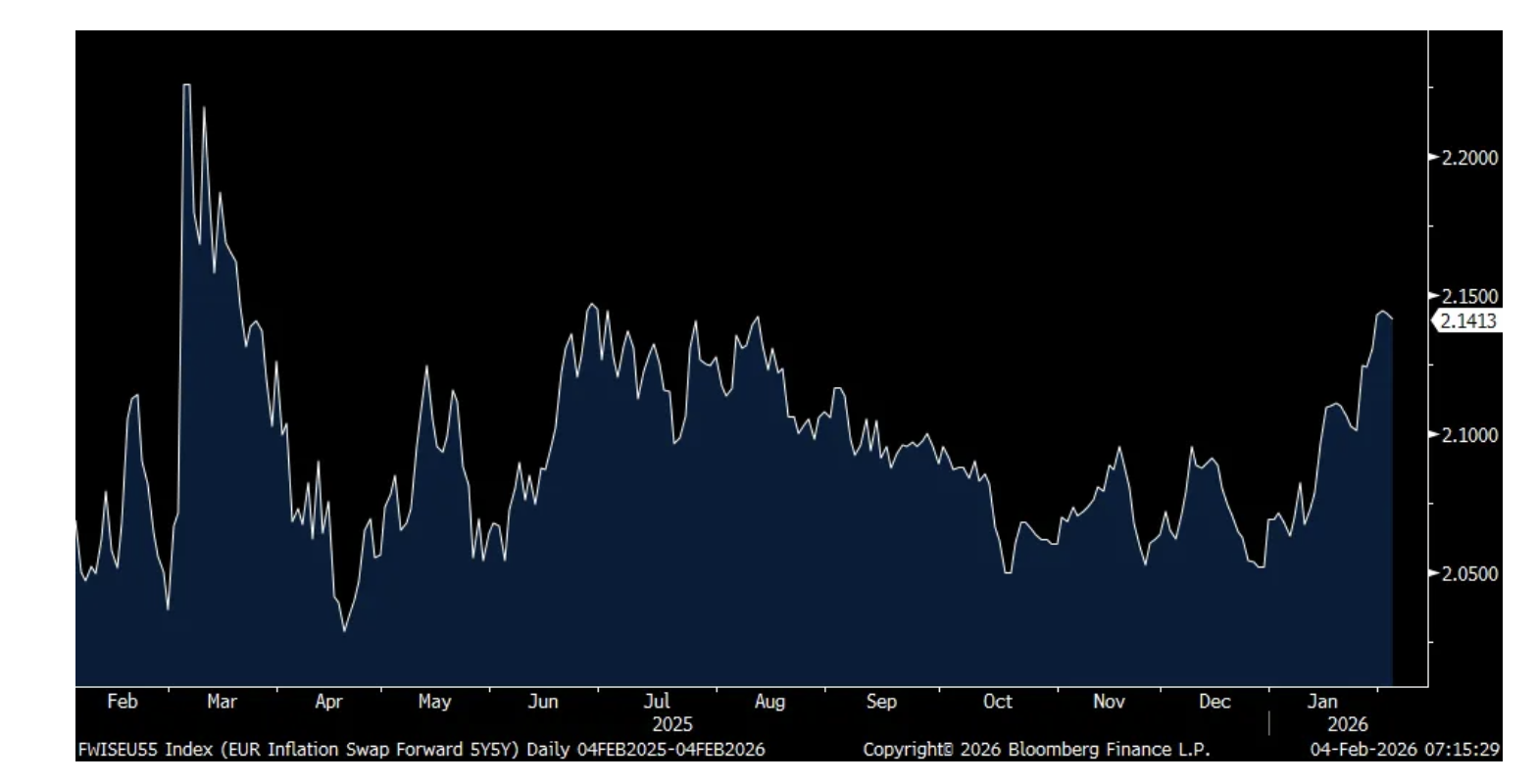

The 5 yr 5 yr euro inflation swap is unchanged at 2.14%, just off the highest since last summer, and with a deposit rate at 2%, the ECB has it about right. That said, after 200 bps of rate cuts, long term interest rates remain elevated with the German 30 yr yield yesterday touching a 15 yr high.

5 yr 5 yr Euro Inflation Swap

BY Doug Kass · Feb 4, 2026, 9:35 AM EST

From Peter Boockvar:

ADP said 22k private sector jobs were added in January, about half the estimate of 45k and down from 37k in December, revised from the initial print of 41k. Hiring of 30k for very small companies sized between 1-19 employees offset shedding of 30k for those slightly bigger with 20-49 workers. Medium sized businesses up to 499 employees added 41k while those bigger than that lost 18k.

Sector wise was mixed. In services, again education/health services drove most of the employment, adding 74k. Leisure and hospitality added 4k, financial services 14k and trade/transportation/utilities 4k. Lost jobs were seen in information (by 5K), professional/business services (by 57k) and other services (by 13k).

On the goods side, manufacturing cut another 8k, offset by a 9k person increase in construction hiring.

With respect to pay, ‘job stayers’ saw an increase of 4.5% vs 4.4% in December. For ‘job changers’ wages rose 6.4% vs 6.6% in the month before. ADP said “wage growth has remained stable.”

Smoothing out the figures, the 3 month average private sector job gain is 44k vs the 6 month average 48k and the 12 month average of 23k. This compares with 64k on average in 2024 and 106k in 2019. Everyone has their explanation for the slowdown in hiring. Is it more the supply side with population growth now barely rising? Likely in part. Is it the demand side that is slackening? Likely in part.

Treasury yields didn’t move much on the data.

BY Doug Kass · Feb 4, 2026, 9:11 AM EST

BY Doug Kass · Feb 4, 2026, 8:50 AM EST

12:00 p.m.: FedBank of Richmond President Barkin (Non-Voter) speaks before the Rotary Club of Aiken Economic Sympo-sium, Graniteville, DC (Repeat of Feb. 3 speech. Audience Q&A expected. No livestream);

6:30 p.m.: FedBoard Governor Cook (Voter) speaks on monetary policy and the economic outlook before the Economic Club of Miami, Miami, FL (text available. Q&A from moderator. Webcast here.)

11:30 a.m.: Treasury hosts a $69B 17-Week Bill Auction;

2:00 p.m.: Treasury buyback (liq support)

BY Doug Kass · Feb 4, 2026, 8:38 AM EST

I believe even our subscribers who have been extremely optimistic investors (regarding AI) might now realize why I have written 171 columns in the "More Tales From Nvidia" series.

BY Doug Kass · Feb 4, 2026, 8:00 AM EST

BY Doug Kass · Feb 4, 2026, 7:50 AM EST

BY Doug Kass · Feb 4, 2026, 7:40 AM EST

BY Doug Kass · Feb 4, 2026, 7:30 AM EST

BY Doug Kass · Feb 4, 2026, 7:20 AM EST

If you are going to panic, panic early.

George Noble with a brilliant Spaces from last night.

A must listen:

Zach Marx, Nobody Special, David Nicoski, and Eric Carter | AI Bust Coming, Software is a Disaster.

BY Doug Kass · Feb 4, 2026, 7:10 AM EST

BY Doug Kass · Feb 4, 2026, 7:00 AM EST

Bonus — Here are some great links:

What’s Going On With the Dollar?

Stocks Exist Outside the United States

BY Doug Kass · Feb 4, 2026, 6:45 AM EST

BY Doug Kass · Feb 4, 2026, 6:35 AM EST

BY Doug Kass · Feb 4, 2026, 6:25 AM EST

I would continue to avoid BDCs and publicly traded private equity firms:

BY Doug Kass · Feb 4, 2026, 6:15 AM EST

The S&P Short Range Oscillator moved into a greater overbought at 1.95% vs. 0.38%.

BY Doug Kass · Feb 4, 2026, 6:05 AM EST

BY Doug Kass · Feb 4, 2026, 5:55 AM EST

I am taking a small long rental in (HOOD) based on the oversold in premarket (under $87)

Low confidence trade.

BY Doug Kass · Feb 4, 2026, 5:46 AM EST