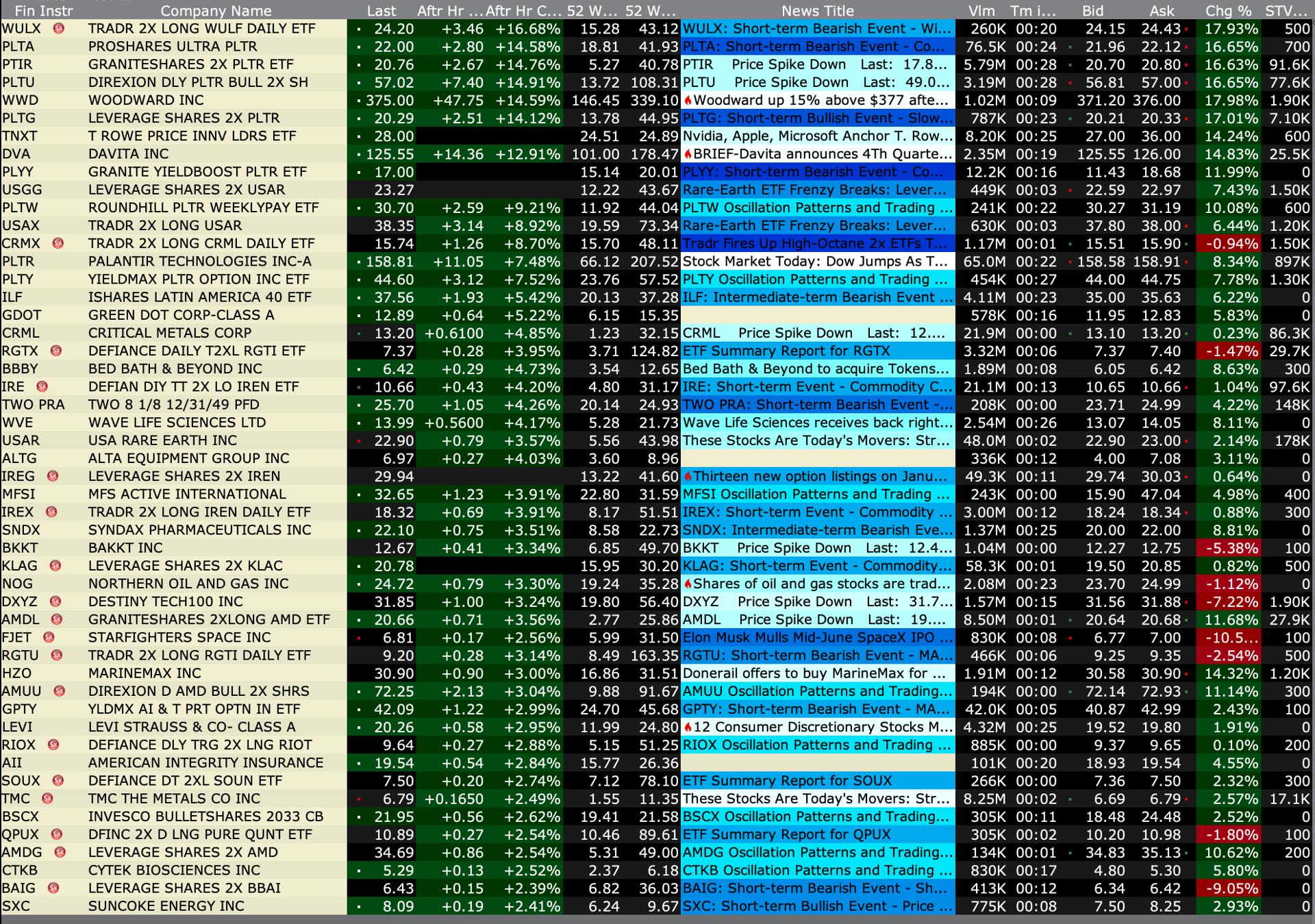

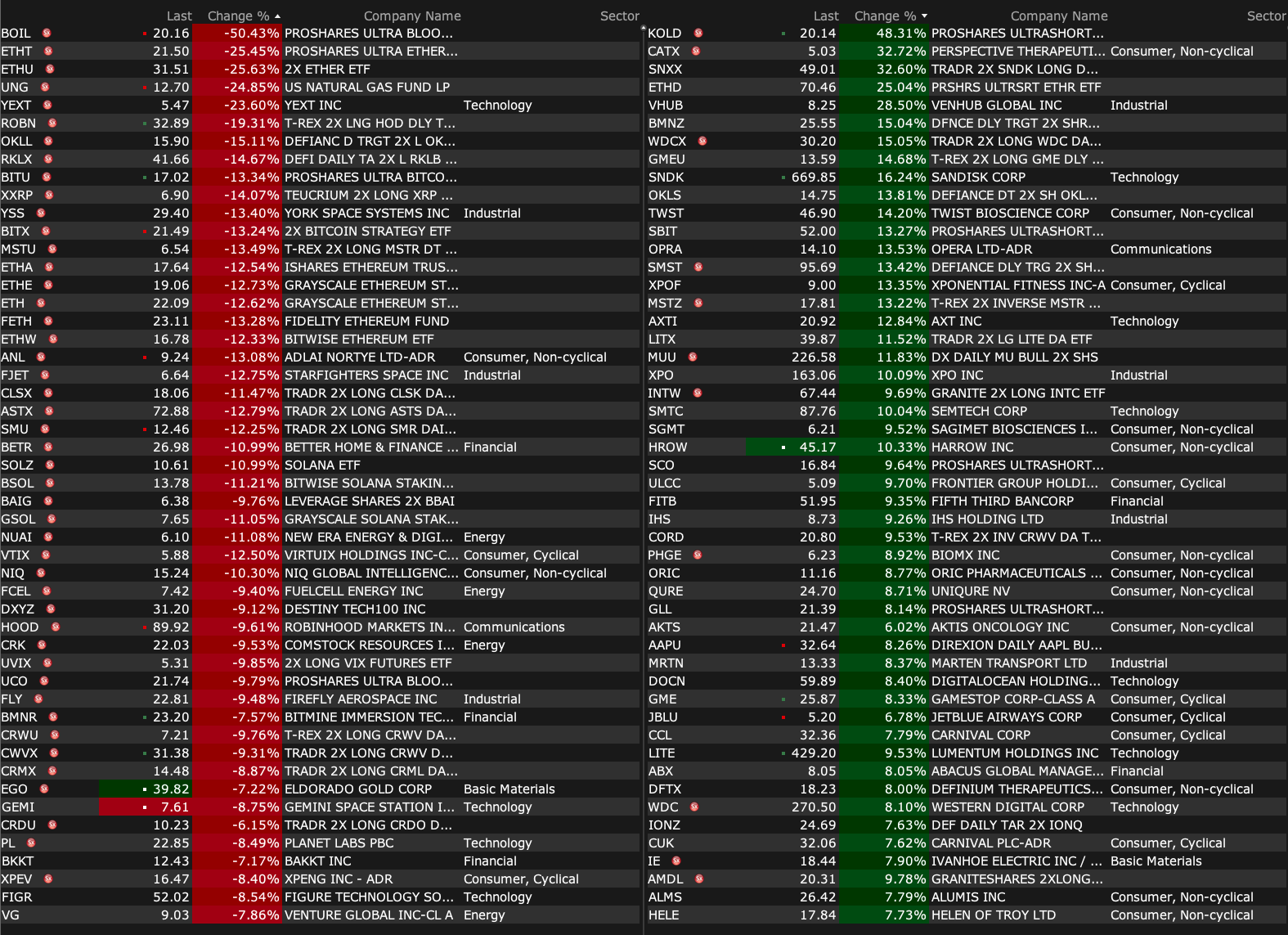

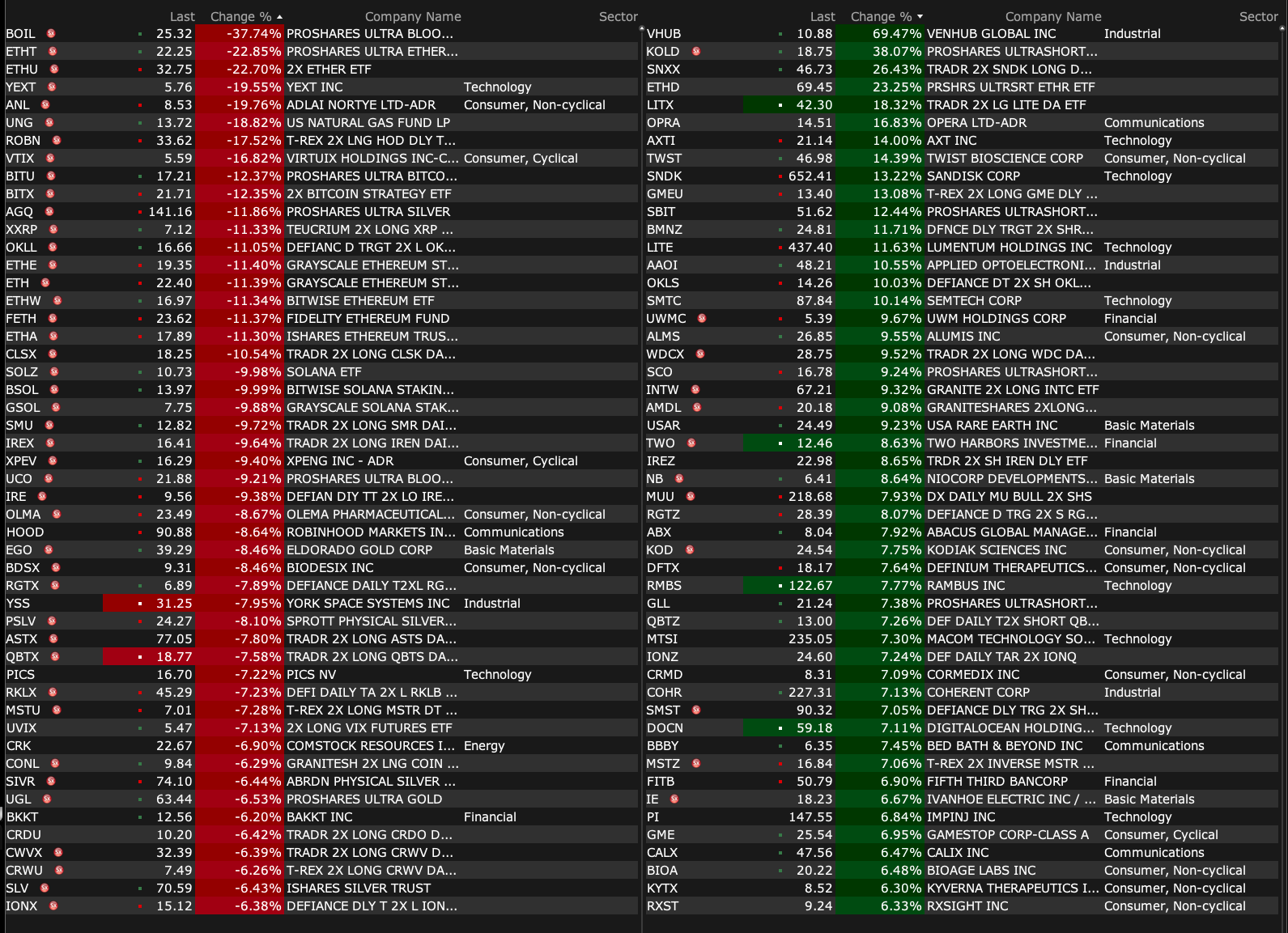

After-Hours Advancers and Decliners

After-Hours % Advancers

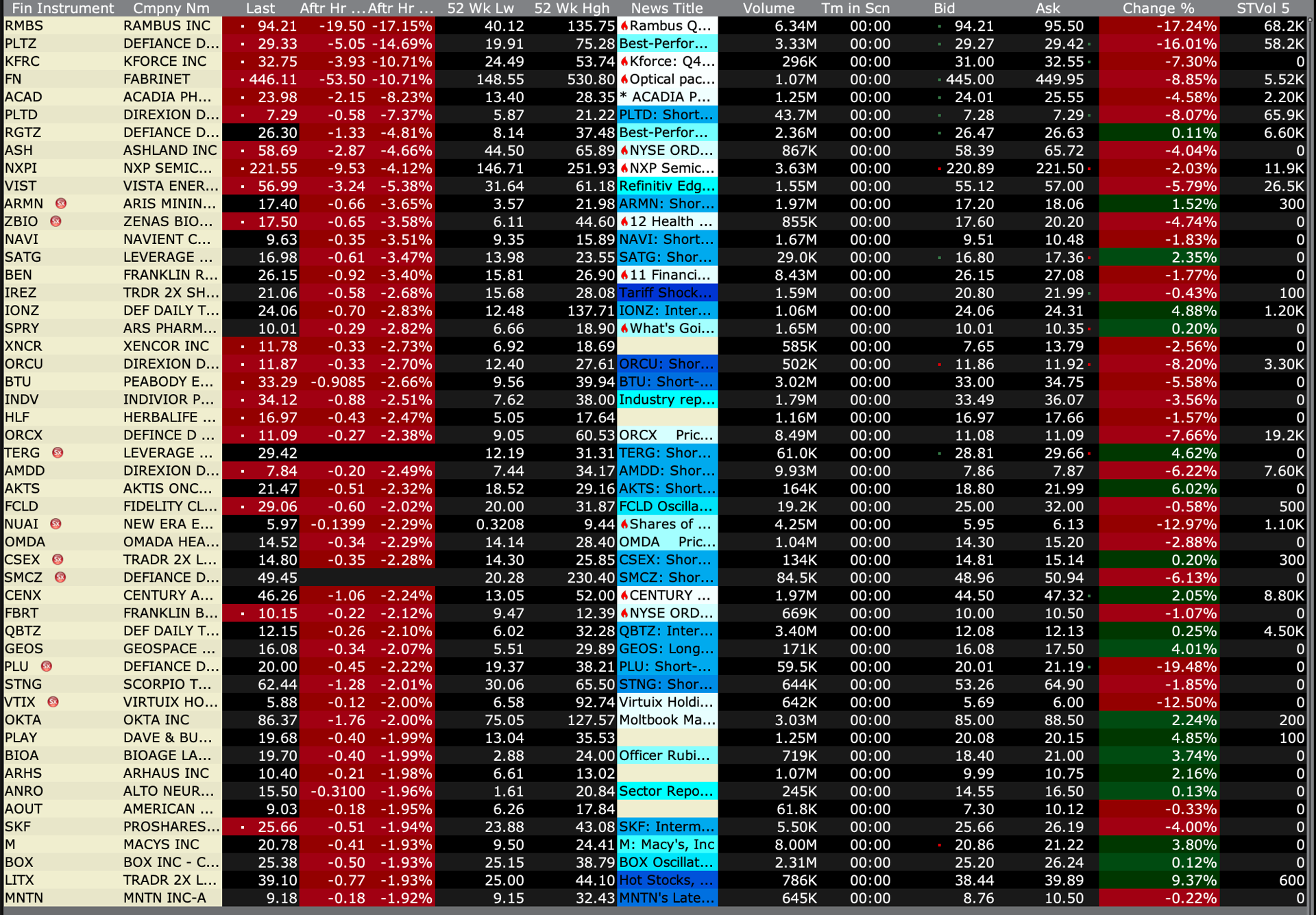

After-Hours % Decliners

BY Doug Kass · Feb 2, 2026, 4:45 PM EST

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Feb 2, 2026, 4:45 PM EST

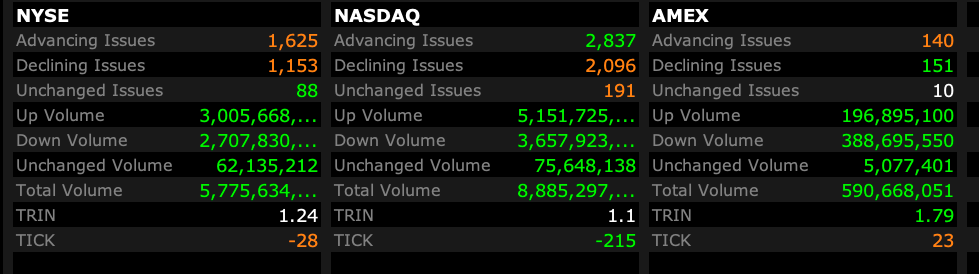

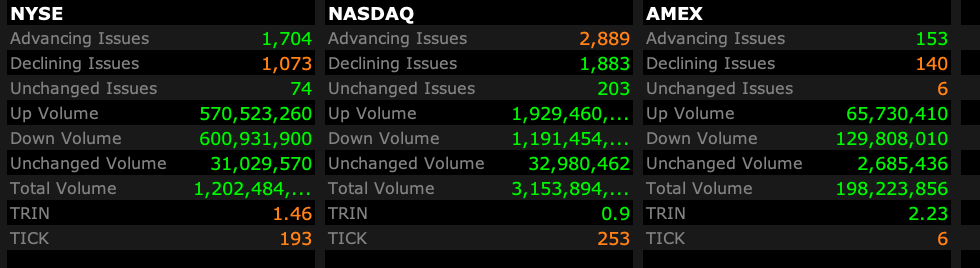

- NYSE volume 17% above its one-month average;

- NASDAQ volume 2% above its one-month average;

- VIX index: down 5.79% to 16.43

BY Doug Kass · Feb 2, 2026, 4:28 PM EST

Proving, I too, can act like a schmuck:

BY Doug Kass · Feb 2, 2026, 3:45 PM EST

Nvidia (NVDA) is nearly -$4/share below my morning short!

Like much of the Mag 7, NVDA is not trading well.

But, PepsiCo (PEP) is! (+$2.78).

BY Doug Kass · Feb 2, 2026, 3:35 PM EST

Here are today's things:

* I shorted index calls on the afternoon ramp.

* I shorted index common:

(SPY) $693.07

(QQQ) $624.20

* I shorted more (JOET) at $42.

* I re-shorted (NVDA) at $190.01.

BY Doug Kass · Feb 2, 2026, 3:30 PM EST

At 2:55 pm:

BY Doug Kass · Feb 2, 2026, 3:20 PM EST

In the last two trading days we have seen some of the wildest price changes in important asset classes that I have seen in decades:

BY Doug Kass · Feb 2, 2026, 3:10 PM EST

My premature cover of my (HOOD) short was one of my biggest errors of the last few months.

BY Doug Kass · Feb 2, 2026, 3:00 PM EST

BY Doug Kass · Feb 2, 2026, 2:45 PM EST

I'm offering out more (JOET) on the short side.

See my comments in the Comments Section.

BY Doug Kass · Feb 2, 2026, 2:35 PM EST

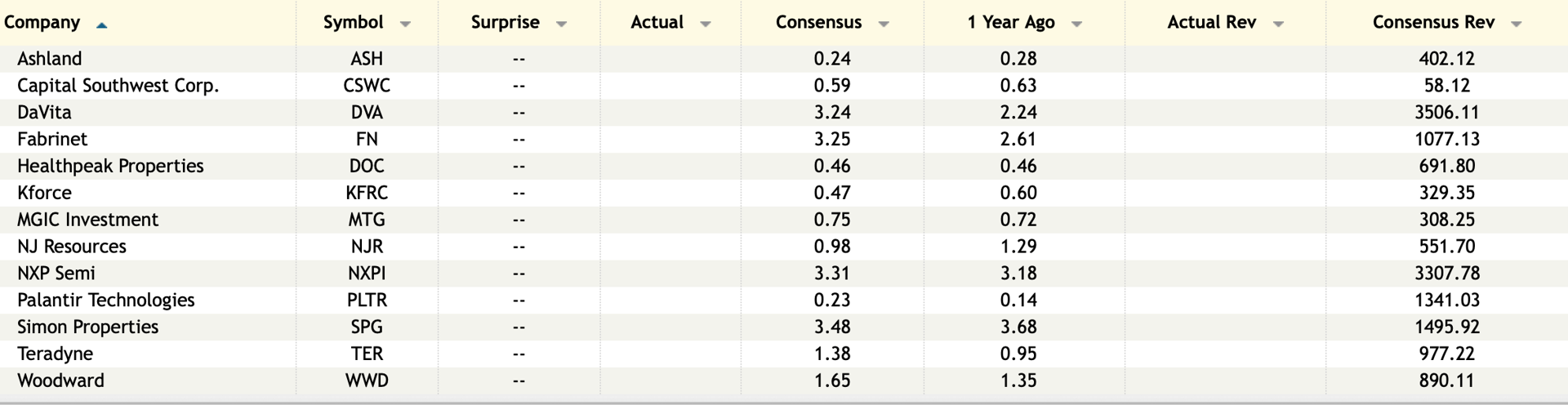

Earnings After the Close Monday, Feb. 2

Earnings Before the Open Tuesday, Feb. 3

BY Doug Kass · Feb 2, 2026, 2:25 PM EST

BY Doug Kass · Feb 2, 2026, 1:56 PM EST

BY Doug Kass · Feb 2, 2026, 1:45 PM EST

I am back short Nvidia (NVDA) at $190.01.

BY Doug Kass · Feb 2, 2026, 1:35 PM EST

BY Doug Kass · Feb 2, 2026, 1:28 PM EST

BY Doug Kass · Feb 2, 2026, 1:00 PM EST

From my pal Charlie Gasparino:

BY Doug Kass · Feb 2, 2026, 12:56 PM EST

BY Doug Kass · Feb 2, 2026, 12:40 PM EST

BY Doug Kass · Feb 2, 2026, 12:28 PM EST

PepsiCo (PEP) is on another run, trading +$2.15 after a near +$5 move on Friday.

Its my "Stock of the Year."

BY Doug Kass · Feb 2, 2026, 12:09 PM EST

From Peter Boockvar:

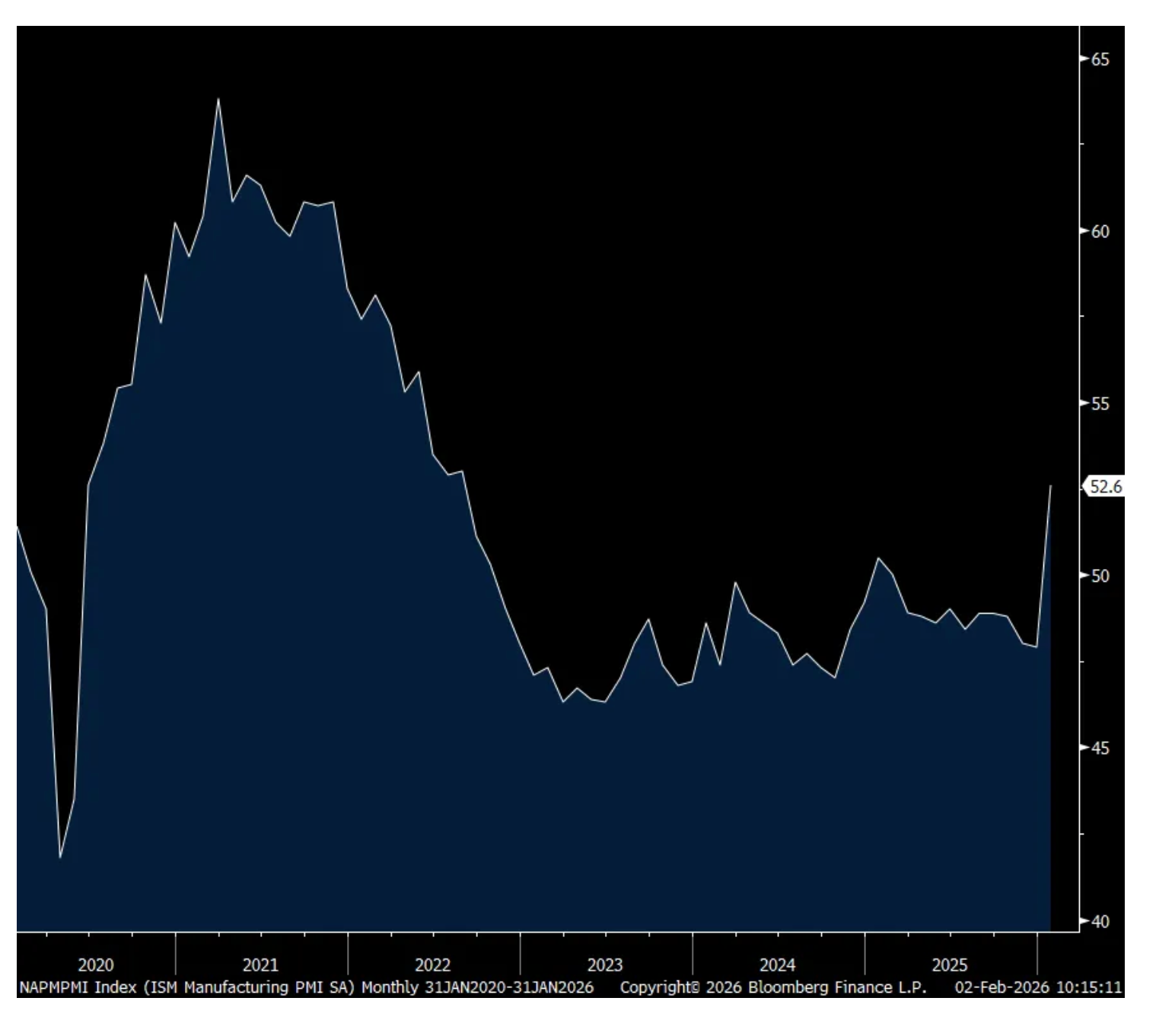

The January ISM manufacturing index rebounded to 52.6 from 47.9 and that was well better than the estimate of 48.5. The increase was led by a 9.7 pt jump in new orders to 57.1 while backlogs too got back above 50 at 51.6. Production (of previously made new orders) stayed above 50 for the 4th month in 5 at 55.9, up 5.2 pts. Inventories were still below 50 at 47.6 and remained very low at the customer level with a print of 38.7, down 4.6 pts m/o/m.

Export orders rose 3.4 pts to 50.2 and imports were up by 5.4 pts to exactly 50. Supplier deliveries showed some slower supply chains with a 54.4 print, up 3.6 pts (goes up when lead times lengthen). Prices paid rose to a 4 month high but up slightly at 59 from 58.5.

With regards to employment, this remained a drag at 48.1, though up from 44.8 in the month before.

Industry breadth got much better too with 9 of 18 sectors surveyed seeing growth vs just 2 in December.

The caveat to all of the above was this commentary from the ISM, “Although these are positive signs for the start of the year, they are tempered by commentary citing that January is a reorder month after the holidays, and some buying appears to be to get ahead of expected price increases due to ongoing tariff issues.”

I’ll add this, also notwithstanding the nice rebound in both the headline print and many of the internals, the commentary below still reflects a very tempered mood in a variety of industries and tariffs are still plaguing business and operations.

“ ‘Hope’ has been word of the year in the Transportation Equipment industry. Unfortunately, all the hope in the world has not materialized into order activity in 2025 or the first half of 2026. Across the board, buyers continue to stand on the sidelines. As we enter 2026, every conversation revolves around hope that the second half of 2026 starts the turnaround. It’s hard to set strategy on hope, but thanks to the uncertainty brought about by this administration, here we are.” [Transportation Equipment]

“Although our volume is low at the moment, the impact on the latest tariff threats on the European Union will have a huge negative impact on our profit for current quoted orders. We will not be able to recover the increase tariffs in our current quotations.” [Machinery]

“Continuing softness in the market, with December orders below average and buyers reluctant to spend despite beneficial tax policies in the U.S. Geopolitical tensions are fueling ‘anti-American’ buyer sentiment, and sales are being lost.” [Machinery]

“Another round of emotionally charged tariffs seems imminent, changing the landscape once more. Movement of custom product out of China continues, but the progress is slow with new qualifications required for transitioned materials and assemblies.” [Computer & Electronic Products]

“Business conditions remain uncertain. Customers are cautious. Broad-based inflation continues. The Supreme Court tariff decision looms.” [Computer & Electronic Products]

“Growing construction markets, data centers and energy projects, are straining the contract labor availability. The trade tariff uncertainty is creating volatility in the supply chain.” [Food, Beverage & Tobacco Products]

“A new year, with new challenges. We are moving manufacturing from China to Mexico — which will now impose tariffs on parts made in China. This push for more of a Mexican supply chain and creates some short-term supply management concerns.” [Chemical Products]

“Confused and uninformed tariff policies continue to plague small companies, making long-term planning pointless. Companies are not making capital commitments beyond 30 days.” [Fabricated Metal Products]

“Business conditions remain soft as we continue to miss sales, orders and profits as result of increased costs from tariffs, continued fallout from the government shutdown, and increased global uncertainty.” [Miscellaneous Manufacturing]

“Business trends moving into 2026 feature many of the headwinds from the third and fourth quarters of 2025. While the ‘plane’ has steadied, there continues to be uncertainty and added costs through our global operations. Tariff impacts on our financial performance last year cannot be overstated, as we had a much smaller EBITDA (earnings before interest, taxes, depreciation and amortization) than previous years. While other inflationary pressures continue to hit the business, tariffs and product costs played a large role. This year, we will continue our multi-country sourcing approach to manufacture and import product from more tariff-friendly countries outside of China. But as we know, nothing is guaranteed with the current administration. We have trimmed costs everywhere inside the business, including on labor and conferences, and reduced our revenue forecast to a much more achievable mark. We’re prepared to battle throughout the year for higher profitability.” [Apparel, Leather & Allied Products]

ISM Mfr’g

BY Doug Kass · Feb 2, 2026, 11:35 AM EST

Jeffries on GOOGL and AMZN:

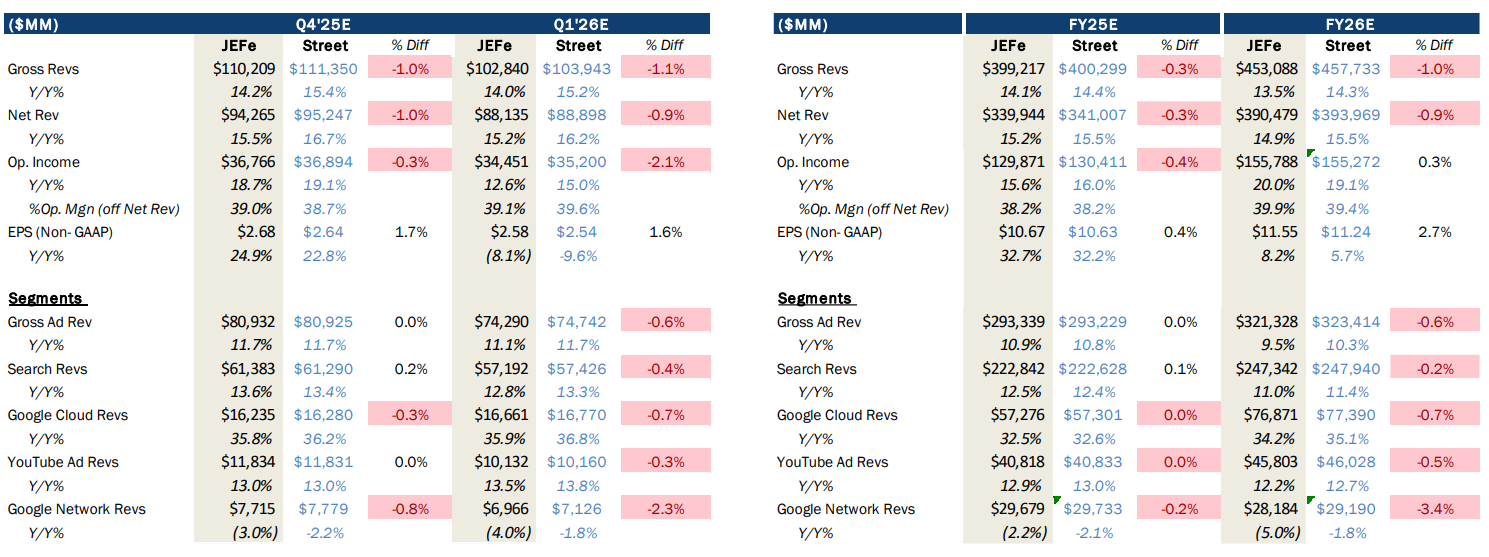

GOOGL (Buy / $400 PT / Thill) – GOOGL is trading at a 15yr high multiple heading into 4Q. Our ad survey shows healthy demand w/ 80% at/above plan and GOOGL leading spend growth at +6.6% Y/Y. YouTube remains fastest growth channel w/ spend up ~8% Y/Y. Our Cloud checks suggest strong revs w/ hyper-growth RPO. We raise our Cloud rev. #s to +36% Y/Y, in line w/ consensus and a 2pt acceleration vs. 3Q. We expect the strong momentum in ads and cloud to support a grind higher in shares and model 4Q/’26 EPS slightly ahead of the Street.

AMZN (Buy / $300 PT / Thill) – Brent likes the 4Q setup w/ stock trading at 13x NTM EV/EBITDA [25% discount to internet large cap avg 13.7x ǀ below 10Y avg ~17x]. Top-line fundamentals look constructive in 4Q w/ accelerating AWS momentum, resilient consumer spend, and stabilizing macro / tariff risks. AWS is primed for re-acceleration w/ backlog growth jumping in 4Q against the easiest comp of the year [4Q24 +14% vs. 29% high in 1Q]. We expect mid-20s, accelerating from +22% in 3Q. Brent remains +ve and we expect $$$ to rotate to AMZN trading at a 30%+ discount to WMT and 25%+ to peers. AMZN is Brent’s close 2nd to META.

BY Doug Kass · Feb 2, 2026, 10:58 AM EST

- NYSE volume 13% above its one-month average;

- Nasdaq volume 12% above its one-month average

- VIX index: down 3.73% or 16.79

BY Doug Kass · Feb 2, 2026, 10:55 AM EST

Selling more Amazon (AMZN) at $244.87.

BY Doug Kass · Feb 2, 2026, 10:24 AM EST

With S&P cash +31 handles, I have moved to medium-sized Index short.

BY Doug Kass · Feb 2, 2026, 10:18 AM EST

With S&P cash +20 handles I am moving (up) to small sized short the Indices.

BY Doug Kass · Feb 2, 2026, 9:59 AM EST

With S&P cash +6 handles I am shorting Index common and calls.

BY Doug Kass · Feb 2, 2026, 9:56 AM EST

Disney's (DIS) shares are down $8/share (to a multi month low) after the EPS release. (Earnings-Report.pdf)

I continue to avoid Disney based on (among other things previously written):

* AI is likely to make inroads into the Disney franchise

* Legacy and former blockbuster franchise movies (Marvel et al) are losing popularity.

* Streaming vulnerability as media companies consolidate (and build up critical mass)

* Sky high admissions prices to theme parks that are exposed to a consumer spending decline.

BY Doug Kass · Feb 2, 2026, 9:45 AM EST

BY Doug Kass · Feb 2, 2026, 9:35 AM EST

-AQST +39% (US FDA Issued Complete Response Letter for Anaphylm; Believes it can rapidly resolve deficiencies and expects to resubmit as early as 3Q26)

-HAIN +12% (to sell North American snacks business to Snackruptors)

-CATX +11% (prices 39.6M shares at $3.79/shr and 6.6M warrants at $3.79/unit in $175M underwritten offering of common stock)

-HROW +9.4% (affirms FY25 Rev $270-280M v $275Me; MELT-300 program on track for NDA submission in first half of 2027)

-TWST +7.1% (earnings, guidance)

-NSSC +5.7% (earnings; raises dividend)

-MLTX +5.4% (announces FDA Fast Track Designation for Sonelokimab Palmoplantar Pustulosis (PPP))

-ORCL +3.9% (discloses up to $20B equity distribution agreement; files to sell 100M depositary shares representing Series D mandatory convertible preferred stock)

-PLTR +2.1% (William Blair Raised PLTR to Outperform from Market Perform)

-RVTY +2.0% (earnings, guidance)

-YEXT -22% (CEO Withdraws Non-Binding Acquisition Proposal; Company Intends to Repurchase $150M of Stock through Self-Tender Offer)

-PHAR -16% (receives Complete Response Letter from U.S. FDA for sNDA for Joenja (leniolisib) in children aged 4 to 11 years with APDS)

-MSTR -7.5% (discloses it acquired 855 BTCs at average purchase price $87,974 During Period January 26, 2026 to February 1, 2026; BTC weakness)

-CTRA -4.4% (confirms to combine with Devon Energy)

-EQT -3.9% (weakness followingdvn DVN/CTRA deal)

-APTV -3.1% (earnings, guidance)

-DVN -3.1% (CTRA to combine with Devon Energy)

-HUM -3.1% (Morgan Stanley Cuts HUM to Underweight from Equal Weight, price target: $174)

-FRHC -3.0% (said to consider selling debt in USD and CNY)

-HESM -2.3% (earnings, guidance)

-DIS -2.2% (earnings, guidance)

-TSLA -2.1% (reports Jan New Car Registrations across Europe)

BY Doug Kass · Feb 2, 2026, 9:15 AM EST

12:30 p.m.: Fed Bank of Atlanta President Bostic (Non-Voter) participates in moderated conversation on monetary policy before theAtlanta Rotary Club, Atlanta, GA (Audience Q&A expected. No media Q&A. No embargoed text. Livestream at https://youtube.com/ )

BY Doug Kass · Feb 2, 2026, 9:05 AM EST

BY Doug Kass · Feb 2, 2026, 8:55 AM EST

BY Doug Kass · Feb 2, 2026, 8:50 AM EST

From Peter Boockvar:

One more thing on Kevin Warsh and why I think he’s the right person for this job. It’s his experience in markets working for Stan Druckenmiller and his knowledge of them before he even got to the Fed. I saw Kevin speak about 10 years ago and he told a story when he first got to the Fed in 2006 and arrived at his office at the Eccles Building for the first time. He requested a Bloomberg terminal so that he could follow the markets but immediately learned that there was just one in the entire building. Until one was eventually hooked up for him about three weeks later, he used Yahoo Finance to get his market quotes which at the time was not providing him credit default swap markets. I’ll add that it was in 2006 that the credit markets started to show shaky legs when market signals started to emanate that something was going on.

The market knowledge and having an ear out for market messaging and signals is also why I’ve always appreciated the opinions of other market savvy former Fed officials like Richard Fisher (ran a hedge fund), Robert Kaplan (Goldman Sachs alum and now back), for sure my former boss Larry Lindsey (macro/market consulting firm for 25 years) and a current one Beth Hammack (Goldman Sachs alum) because they were not interested in running monetary policy just by econometric modeling and instead integrated a broader matrix of knowledge which markets were an important part of.

I bring this up in part because I heard Fed Governor Stephen Miran on CNBC’s Money Movers on Friday who when asked about what he thinks about the rising price of gold (outside of Friday’s selloff), he said the increase was “not informative” to him. As a monetary metal for thousands of years, ignoring what gold does is a mistake I firmly believe and it is not an answer that Kevin Warsh or the others I mentioned would have ever given. It reminded me of the Ron Paul questioning of Ben Bernanke back in 2011.

Miran in the interview also said he wasn’t paying attention to the jump in the December PPI as in his eye’s inflation is only if it passes on to the consumer. Tell that to the businesses having to eat the cost pressures.

This all said, Kevin will still be subject to economic circumstances, a full committee of colleagues and the next time things hit the fan there will be an extraordinary pressure to ‘do something’, especially from you know who. And as Mike Tyson once said “Everyone has a plan until they get punched in the mouth.”

Before I get to the earnings calls, I want to hit on oil prices again where I’ll repeat that a barrel at around $60 is one of the cheapest assets in the world. Yes, because I’m talking my book but if I’m right and it does rise from here, it would complicate the job of Kevin Warsh in the few years to come.

In the FT a few weeks ago there was an article on oil companies that are looking abroad for exploration opportunities because of the dwindling basins in US shale. Something I’ve been hitting on where about 85% of all non-OPEC+ global supply came from US shale over the past 15 years and this is thus a big deal.

Here were some quotes from the article that is helping to make my point. “ ‘The Permian has been a massive wealth creator for America, but we’ve drilled the best prospects and are running out of inventory,’ said Bryan Sheffield, who founded Parsley Energy before selling it.’ “ The shale boom was a technological wonder but “The expansion phase appears to have peaked, though, with the US Energy Information Administration forecasting a y/o/y flattening of production at 13.6mm barrels a day this year and a fall to 13.2mm barrels in 2027, as US drillers cut costs and slow output amid weak crude prices.”

The article also quotes an analyst at market intelligence firm Welligence, “There’s no expectation of material growth in US shale, and some foresee gradual decline starting in the near term.”

This from the CEO of Continental Resources quoted in the article, “We do know there is a real and recognized degradation in the inventory quality of the US conventional resources...adding that US oil production was set to plateau, prompting operators to look abroad.” Now of course over time more oil will be found around the world that will replace US shale but there will be a mismatch in timing I believe.

The earnings calls still reflect a very mixed bag for the US economy.

From American Express, obviously heavily exposed to the upper income consumer, and down by 1.8% Friday:

“Retail spending continued to show good momentum in the quarter, up 10%. And spending at luxury retail merchants was up 15%, reflecting the continue strength of our customer base.”

“Growth in airline and lodging spend was largely stable and restaurant spending was up 9% once again this quarter. Our dining assets are driving high levels of engagement, with spend at US Resy restaurants by US consumer customers up by more than 20%. Momentum from younger customers also continued. As of Q4, Millennial and Gen Z customers now make up the largest share of US consumer spending, and they remain the fastest growing cohort.”

“International also delivered another very strong quarter, with spend up 12% FX adjusted. Growth remains broad based across consumer and business customers and across geographies.”

“Looking at the first three weeks of January, we continue to see good momentum in spend trends.”

“Our credit performance throughout the year was remarkably strong and stable. Delinquency rates were flat throughout the year, and write-off rates remained best in class. Notably, both delinquency and write-off rates are still below 2019 levels. In 2026, we expect credit metrics to remain generally stable with some seasonal variation in provision across quarters.”

From Colgate Palmolive, the maker of toothpaste, toothbrushes, soap, deodorant and pet food, up 6% Friday as consumer staples start to trade better, a favorite group of mine for 2026:

“Emerging markets where we have significant exposure continue to perform ahead of developed markets.”

“We delivered improved momentum on our business in Q4 in terms of organic sales growth and market share, and we have seen stabilization of category growth rates as we exit 2025. But we still face significant uncertainty, while category growth may have stabilized, growth rates remain low. This is difficult in itself, but also could lead to higher levels of promotion and other competitive activity.”

“Foreign exchange is favorable right now, but has been a negative impact for eight of the past 10 years. The geopolitical environment, including tariffs, is volatile, particularly in Latin America, and the US market remains sluggish. While we think trends will improve, we’re not building in a big rebound.”

“Overall, it seems like the categories have stabilized at the lower rate than our historical assumptions...We’re seeing a lot of month-to-month swings in the US, which you can see in the scanner data, obviously, plus we continue to see downward pressure on inventories as categories slow.”

“The volume is particularly more acute an issue in the US, where we’ve seen on our core categories some of the volumes go negative. Our anticipation is that will get a little better. But as I mentioned, we’re not assuming the US will get significantly better at least in the next couple of quarters.”

From Equity LifeStyle Properties and this was on their manufactured home business where they lease lots to people that buy the homes:

“First quarter growth in manufactured home rent is 5.8% at the midpoint of their guidance.” According to ELS, “There’s about 7 million manufactured homes in the country that house about 18 million people.

These are some that are still feeling the inflation pain.

From Schneider National, the trucking company and whose stock plunged 10% Friday:

“When we provided an update last quarter, October results and marketing conditions were supportive of the finishing 2025 at approximately $.70 of EPS. However, November and much of December were materially more challenged than our guidance contemplated, reflecting a very truncated peak season and poor weather conditions throughout the Midwest.”

“We saw momentum as we exited the year, which we believe is a direct result of supply attrition in our industry in the last several months. We believe, we’re in the early inning of normalizing market conditions, in part due to the various regulatory actions being taken, Importantly, these actions are not only driving capacity to exit the market at an accelerated rate, but the ability to backfill new entrants is also increasingly diminished. We expect the full impact will likely be measured in quarters, not months. Still, the last several years have proved to be a challenging backdrop, and we are not satisfied with our results.”

From LyondellBasell Industries, the chemicals company and whose stock fell 1.9% Friday:

The CEO mentioned “some of the most challenging market conditions I have seen in my career.”

“2025 was another exceptionally challenging year with industry margins remaining deeply depressed across all of our core businesses. Industry margins were approximately 45% below historical averages, even worse than the largely difficult conditions we saw in 2024.”

“Several factors are pressuring margins. These include global trade disruptions, low demand for durable goods, a lower oil-to-gas ratio, ongoing global capacity additions, and in Europe, increased competition from imports and structurally higher energy costs.”

Deckers Outdoors popped 20% Friday and they said this:

“Global HOKA and UGG performance was exceptional, with revenue increasing by 18% and 5% versus last year, respectively, and each brand delivering balanced growth across DTC and wholesale.”

“From a regional perspective, HOKA and UGG collectively drove third quarter revenue increases of 15% in international markets, reflecting continued momentum from the first half, and 5% in the US.”

If you’ve made it this far with today’s note, I’ll be quick with all the January manufacturing PMI’s that came out ahead of the US ISM. Everyone in Asia saw a print north of 50.

Taiwan 51.7 vs 50.9

China 50.3 vs 50.1

India 55.4 vs 55

Japan 51.5 vs 50

Vietnam 52.5 vs 53

South Korea 51.2 vs 50.1

Thailand 52.7 vs 57.4

Australia 52.3 vs 51.6

Indonesia 52.6 vs 51.2

Malaysia 50.2 vs 50.1

The final Eurozone manufacturing index at 49.5 was little changed with the initial print a few weeks ago of 49.4 but that was up from 48.8 in the month before and vs 49.6 in November. The UK index was revised up a touch to 51.8 vs 50.6 in December.

Nothing moving on any of these figures but at least in Asia we now have some modest manufacturing growth, the same in the UK and the Eurozone is trying to stabilize.

The US ISM is expected to remain below 50 at 48.5 and I hope this doesn’t mean that US manufacturers are losing market share with the rest of the world.

BY Doug Kass · Feb 2, 2026, 8:30 AM EST

One more thing on Kevin Warsh and why I think he’s the right person for this job. It’s his experience in markets working for Stan Druckenmiller and his knowledge of them before he even got to the Fed. I saw Kevin speak about 10 years ago and he told a story when he first got to the Fed in 2006 and arrived at his office at the Eccles Building for the first time. He requested a Bloomberg terminal so that he could follow the markets but immediately learned that there was just one in the entire building. Until one was eventually hooked up for him about three weeks later, he used Yahoo Finance to get his market quotes which at the time was not providing him credit default swap markets. I’ll add that it was in 2006 that the credit markets started to show shaky legs when market signals started to emanate that something was going on.

The market knowledge and having an ear out for market messaging and signals is also why I’ve always appreciated the opinions of other market savvy former Fed officials like Richard Fisher (ran a hedge fund), Robert Kaplan (Goldman Sachs alum and now back), for sure my former boss Larry Lindsey (macro/market consulting firm for 25 years) and a current one Beth Hammack (Goldman Sachs alum) because they were not interested in running monetary policy just by econometric modeling and instead integrated a broader matrix of knowledge which markets were an important part of.

BY Doug Kass · Feb 2, 2026, 8:00 AM EST

From Gary Marcus:

OpenClaw (a.k.a. Moltbot) is everywhere all at once, and a disaster waiting to happen

BY Doug Kass · Feb 2, 2026, 7:50 AM EST

BY Doug Kass · Feb 2, 2026, 7:40 AM EST

BY Doug Kass · Feb 2, 2026, 7:30 AM EST

BY Doug Kass · Feb 2, 2026, 7:20 AM EST

BY Doug Kass · Feb 2, 2026, 7:10 AM EST

cjsolus

Feels like the market is finally digesting what was to me a very important bump in the PPI numbers Friday that the Wolf howled about, coupled with NVDA having issues with Open AI all of a sudden (Huang has also privately criticized what he has described as a lack of discipline in OpenAI’s business approach and expressed concern about the competition it faces from the likes of Alphabet’s Google and Anthropic, the WSJ said.), the Great Orange wonder making moves to have a conflict once again in the middle east, Japan's interest rates going thru the roof and oh yeah as well as the ever discounted gov't shutdown which last time reeked a bit of havoc on a lot of things most importantly gov't statistics reporting and lets not forget social distress and deaths by gov't hands in the streets of America....

Oh and I forgot the Warsh Effect...God only knows what this nomination means ..I believe higher interest rates in the long run...

Oh and it seems the Bitcoin flight to quality asset class is showing its true colors and this so called flight to safety blah blah that it was built on is seemingly not sustaining that hype... may the greater value added asset win!!

I think Doug said it succinctly the other day..."That was the first shot over the bow!!" with the dip last week....

The excess in the market is beginning to leak out.... IMHO

BY Doug Kass · Feb 2, 2026, 7:00 AM EST

BY Doug Kass · Feb 2, 2026, 6:45 AM EST

BY Doug Kass · Feb 2, 2026, 6:35 AM EST

* And the market is not broadening...

We are now up by more than +$10 in our Russell short of 10 days ago.

From 1/22:

I have moved to medium-sized short (IWM) (from small sized) at $270.41.

Position: Short IWM M

By Doug Kass Jan 22, 2026 9:38 AM EST

From 1/21:

I have taken an initial short position in the Russell index:

* (IWM) at $267.86

Position: Short IWM (S)

By Doug Kass Jan 21, 2026 3:35 PM EST

BY Doug Kass · Feb 2, 2026, 6:25 AM EST

BY Doug Kass · Feb 2, 2026, 6:15 AM EST

I was busy last night:

Dougie Kass

I covered my short index calls by buying S&P futures -34 handles at around 6:30 PM on Sunday evening.

Now delta neutral (I had shorted the rally off the lows late Friday, as posted.)

Dougie Kass

Sold futures for a 30 handle profit (bought -34 and sold -4) and back shorting SPY at $691.30 (8:05PM)

Dougie Kass

Covered SPY $688.85 - for a very quick (10 minutes!) profit. (8:15PM)

This should be some night!

BY Doug Kass · Feb 2, 2026, 6:05 AM EST

The S&P Short Range Oscillator has slipped (slightly) back into an oversold for the first time in several weeks — standing at -0.31% vs. 1.00%.

BY Doug Kass · Feb 2, 2026, 5:55 AM EST

More statistically insignificant pablum:

BY Doug Kass · Feb 2, 2026, 5:45 AM EST