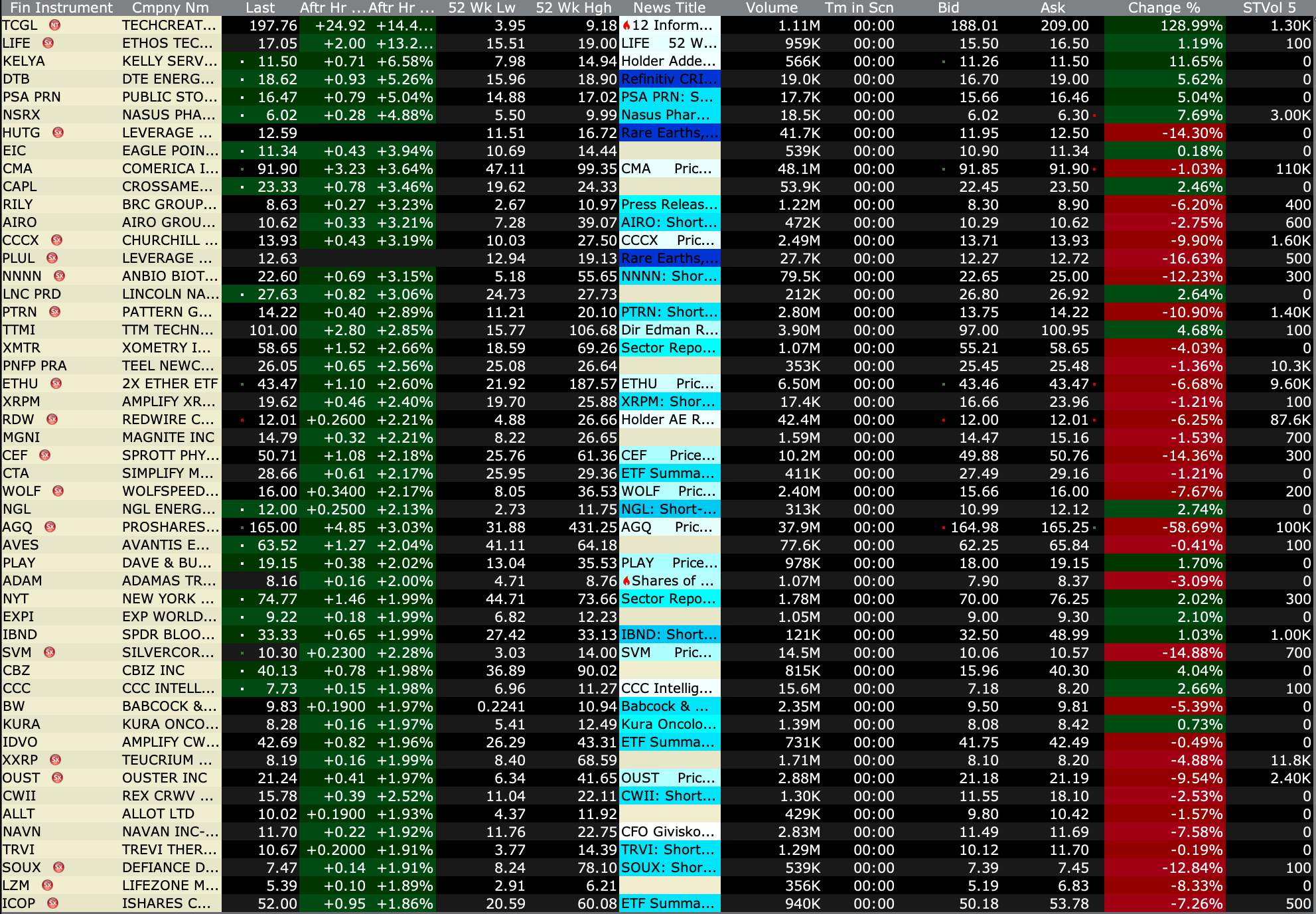

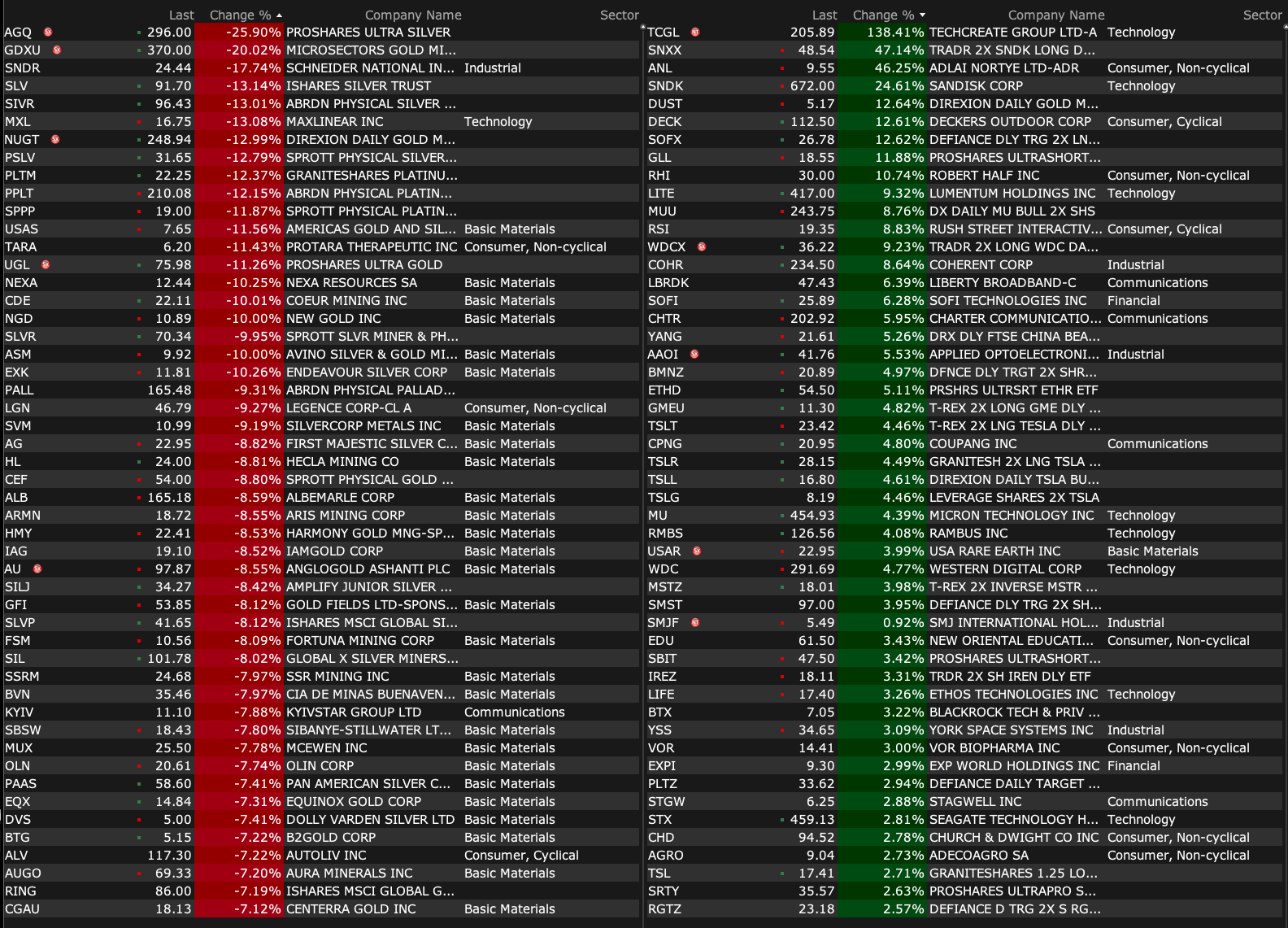

After-Hours Advancers and Decliners

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Jan 30, 2026, 4:45 PM EST

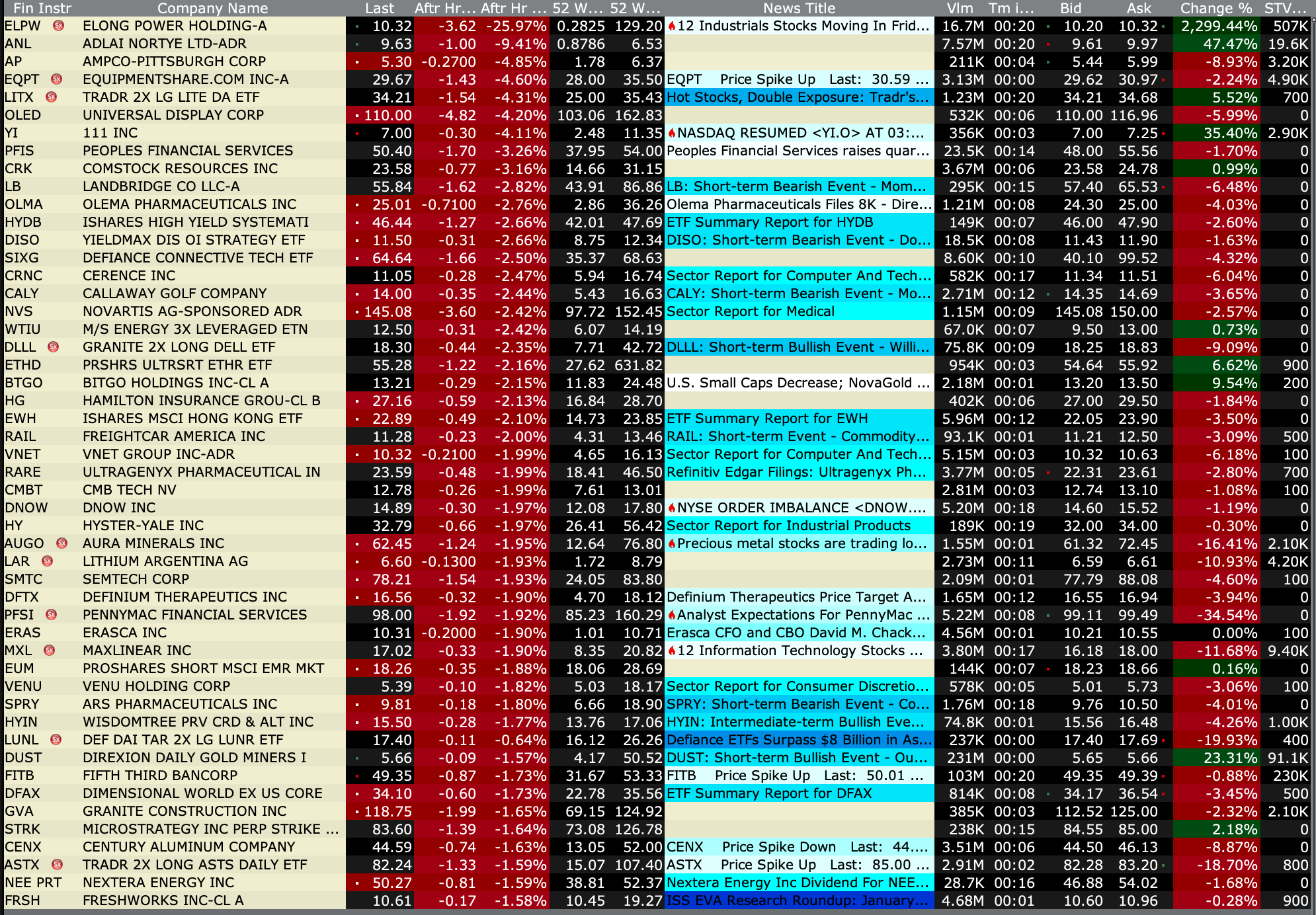

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Jan 30, 2026, 4:45 PM EST

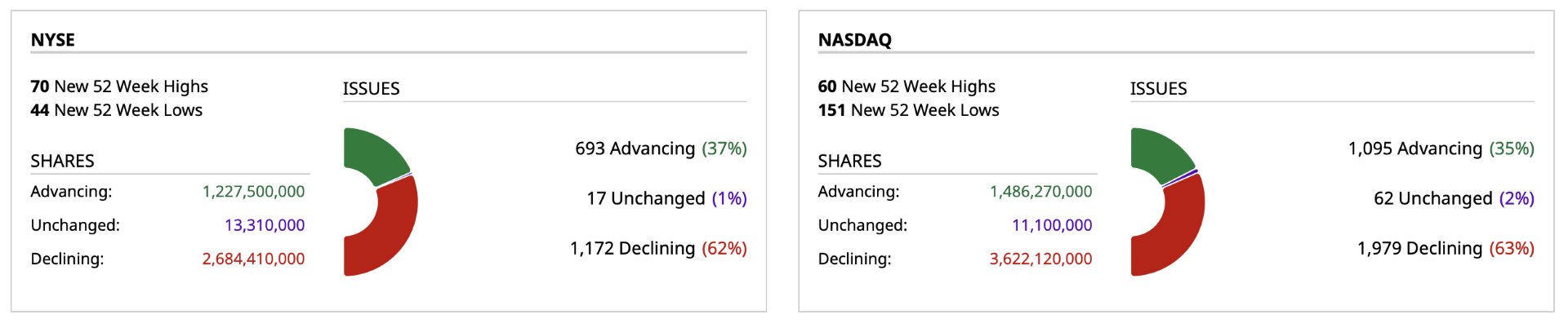

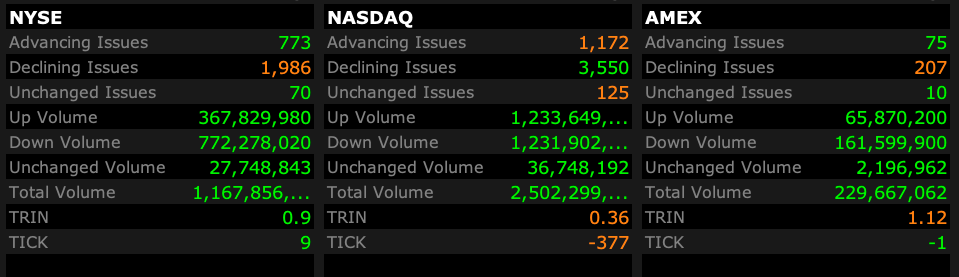

- NYSE volume 28% above its one-month average;

- NASDAQ volume 1% below its one-month average;

- VIX index: up 4.50% to 17.64

BY Doug Kass · Jan 30, 2026, 4:30 PM EST

Thanks for reading my Diary today, all week and over the last 28 years!

I hope my output was valuable.

Enjoy the weekend.

Be safe.

See you back here early Monday morning.

BY Doug Kass · Jan 30, 2026, 4:17 PM EST

With S&P cash -22 handles, I am back shorting index calls

BY Doug Kass · Jan 30, 2026, 4:05 PM EST

(PEP) (+$4.18) is breaking out.

See previous post, "The Pigs Are Flying."

BY Doug Kass · Jan 30, 2026, 3:39 PM EST

BY Doug Kass · Jan 30, 2026, 3:29 PM EST

* PepsiCo's (PEP) shares are up again today — by +$2.83...

A reminder and repost:

* A 4% dividend yield and operating upside at only a 16x forward multiple

"Cheeseburger, Cheeseburger! ... No Orange or Coke Today, Four Pepsi"

In the next few weeks investors will be bombarded with analysts' favorite picks for the coming year. No doubt, the list will include a number of spicy and aggressive names in AI and in other areas. You will not find that character in my annual stock pick.

On the surface it might seem absurd to choose PepsiCo (PEP) — a defensive, consumer staples name to be my stock pick for 2026.

However, my choice is, in part, in anticipation of a (potential) negative return for the S&P 500 and Nasdaq indices for the upcoming 12 months — coupled with a possible turnaround in operations at PepsiCo.

Like many consumer nondurable companies, PepsiCo's shares have been a serial underperformer over the last few years for several reasons:

* Defensive stocks have underperformed in an offensively driven investing backdrop in which large-cap technology have represented the market's leadership.

* Food and beverage equities have suffered from reduced snack consumption (GLP-1 and broader health & wellness pressures) and volume trends have been moribund. PepsiCo, in particular, has faced structural challenges in beverages (Mountain Dew and Gatorade brands).

* Expectations are low.

Elliott Investment Management took a $4 billion stake in PepsiCo back in September and outlined a comprehensive 75-page presentation. Elliotts-Perspectives-on-PepsiCo-Presentation.pdf

As seen in their release, the activist firm proposed a series of changes around the company's Frito-Lay North America operations intended to improve the beverage company's competitiveness and financial performance of Pepsi Foods North America. The recommendations included implementing sharper everyday value through price adjustments, elevating innovation and aggressively lowering operating costs.

Elliott creates a sense of urgency for change at PepsiCo.

Three weeks ago PepsiCo management responded to Elliott and announced some initiatives and financial goals aimed at enhancing shareholder value. The 2026 EPS guidance was better than feared and management plans to improve free cash flow conversion and better operating margins were outlined (an improvement of 100 basis points over the next three years).

Here is the company's guidance: PepsiCo Announces Priorities to Enhance Shareholder Value and Provides Preliminary 2026 Financial Outlook

Elliott Management's response to PepsiCo's December 9 plan:

"We appreciate our collaborative engagement with PepsiCo’s management team and the urgency they have demonstrated."

Here is Morgan Stanley's response to the company's December 9 plan:

Initiatives Focused on Value, Innovation, and Costs/Operations - From Morgan Stanley

PEP highlighted PFNA initiatives to sharpen everyday value, elevate innovation, and aggressively reduce operating costs, many of which were already underway since earlier this year. In terms of value, PEP is implementing sharper everyday value through targeted affordable price tiers by brand and channels aimed at stimulating growth and purchase frequency for its mainstream brands. In terms of innovation, PEP reiterated its focus on permissible, as well as functional offerings with no artificial colors/flavors, simpler ingredients, more protein, as well as fiber and whole grains and the restaging of Lay's and Tostitos, and a Doritos Protein launch in 2026. On the cost side, PEP plans to continue to aggressively reduce operating costs and improve operational excellence (PEP has already closed three manufacturing plants and shut several manufacturing lines this year and is in the process of reducing ~20% of SKUs in the US by early next year), with savings to support investments in A&M and value. PEP noted solid retailer support for its commercial plans, and that it expects shelf space to increase in 1H26.

"You can't get killed falling off the curb."

- Grandma Koufax

Reflecting the well-known product threats, PepsiCo's valuation has rarely been more depressed — at 16x estimated 2027 calendar EPS (down from 24x in 2020 and at a 20% discount to its multi-year mean valuation). The cash flow multiple to enterprise value has fallen from 16x to only 13x in the last five years.

With expectations so low, any surprise to the upside will likely be greeted quite favorably.

It might surprise some, given PepsiCo's market position and history, that the company's market valuation is currently less than $200 billion (or only about 2x 2026 sales).

PepsiCo recently increased its dividend by +5% to $5.69/share — providing a healthy dividend yield of 4%.

A reasonable price target of 18x 2027 projected EPS (still about 10% below peers Procter & Gamble (PG) and Coca-Cola (KO) produces a $165 share objective (vs. current share price of around $143). If achieved, this is a possible return in excess of +20%.

Here is a summary of three recent sell side upgrades (in price targets):

PepsiCo price target raised to $164 from $155 at BofA BofA analyst Peter Galbo raised the firm's price target on PepsiCo to $164 from $155 and keeps a Neutral rating on the shares. Entering 2026, the largest unresolved question for staples remains consumption growth and valuations remain dispersed across the group, but "there feels little to get them off the sidelines in '26 until fundamentals signal a greater turning of the tide," the analyst tells investors in a year-ahead note for the consumer staples group.

PepsiCo price target raised to $170 from $165 at Citi Citi analyst Filippo Falorni raised the firm's price target on PepsiCo to $170 from $165 and keeps a Buy rating on the shares. The firm adjusted targets in the beverages, household and personal care sector as part of its 2026 outlook. Citi is shifting from a bullish stance on the non-alcoholic beverage space throughout 2025 toward favoring the household and personal care names. It sees improving fundamentals for the group due to the cycling of inventory destocking and easier consumption compares.

PepsiCo upgraded to Overweight from Neutral at JPMorgan JPMorgan analyst Andrea Teixeira upgraded PepsiCo to Overweight from Neutral with a price target of $164, up from $151. The firm believes the company's "accelerated agenda" of innovation and marketing spending will drive strong productivity savings. This should position PepsiCo to drive high-single-digit total shareholder return in 2026, which benchmarks well against its high-quality peers, the analyst tells investors in a research note. Meanwhile, JPMorgan says the shares are trading a "steep discount" relative to the group.

Position: Long PEP and PG

By Doug Kass Dec 29, 2025 2:50 PM EST

And this:

* Though it is still early in the year, one of my surprises — that a basket of consumer staples (PEP) , (KO) , (PG) and (KMB) will materially outperform the Mag 7 by a decisive amount in 2026 — appears to be developing...

The AI bubble bursts as the circular financing deals unwind (or are pushed out) — AI capital spending slows abruptly as return on investment concerns emerge as power generation and grid modernization are bottlenecks. Depreciation charges and lower demand wrecks havoc with consensus AI 2026-27 earnings per share expectations. Another big AI surprise would be if China decides to flood markets with inexpensive AI models — pressuring the ultimate and expected robust ROI forecasts (which are already in question by some skeptics).

OpenAI's Sam Altman finds a place to live right next door to Sam Bankman-Fried. His effort to make OpenAI too big to fail, fails. ChatGPT turns out to at best be a commodity large language model purveyor. It becomes obvious to all that its recent $500 billion-plus valuation can’t be supported. Without an ability to do a down round without losing face, OpenAI loses all access to capital. Ultimately, a consortium of its customers and suppliers takes it over to modify its business plan and reduce the cash burn.

With Altman tossed to the curb (or worse), the prosecutions begin.

OpenAI’s problems pushes a deeply committed (to OpenAI) Softbank to the verge of collapse.

Nvidia shares fall by -40% as CoreWeave (CRWV) is driven into bankruptcy.

A basket of defensive consumer nondurable equities (PEP) , (KO) , (PG) and (KMB) materially outperform the Mag 7 by a decisive amount.

The shares of (boring and previously hapless) PepsiCo outperform most other staples and 90% of the S&P Index after a much better skein of organic unit growth and as its core business is rationalized.

- Kass, 10 Surprises for 2026

BY Doug Kass · Jan 30, 2026, 2:25 PM EST

With S&P cash -26 handles I am back shorting index calls.

But, given that its the last day of the month, I will sell with a wide berth on a scale higher.

BY Doug Kass · Jan 30, 2026, 2:08 PM EST

“Games are won by players who focus on the playing field — not by those whose eyes are glued to the scoreboard.”

-Warren Buffett

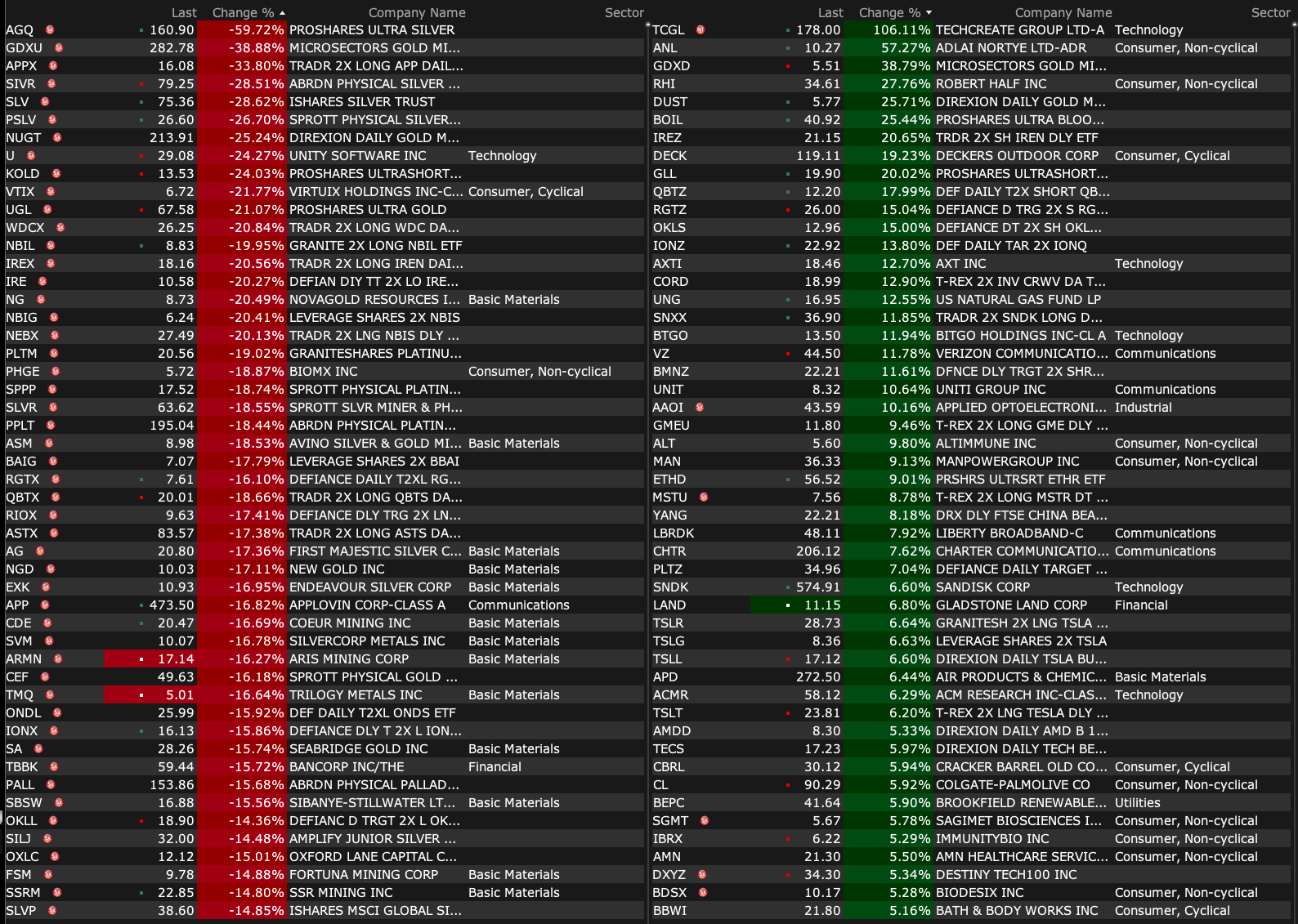

I have rarely heard such gloating about the investment performance of funds heavily weighted or leveraged to equities and precious metals as this week.

Today's dramatic declines were inevitable.

As to where we go from here in gold, silver and platinum — I really have no clue.

Unlike many "talking heads" who confidently answer every question under the sun, I prefer the three words:

"I don't know."

As to where we go in the stock market... as I warned in yesterday's closer, Thursday's weakness may have been the first shot across the bow.

Or not.

BY Doug Kass · Jan 30, 2026, 1:55 PM EST

For several weeks I have made the argument against the broadening thesis:

Despite the robust rise in the averages (especially from the morning lows), I would note that the Russell is not crowing!

(IWM) is, in fact, down on the day (-$1.10).

Position: Short IWM (M)

By Doug Kass Jan 26, 2026 11:35 AM EST

Today (IWM) is -$5.

BY Doug Kass · Jan 30, 2026, 1:45 PM EST

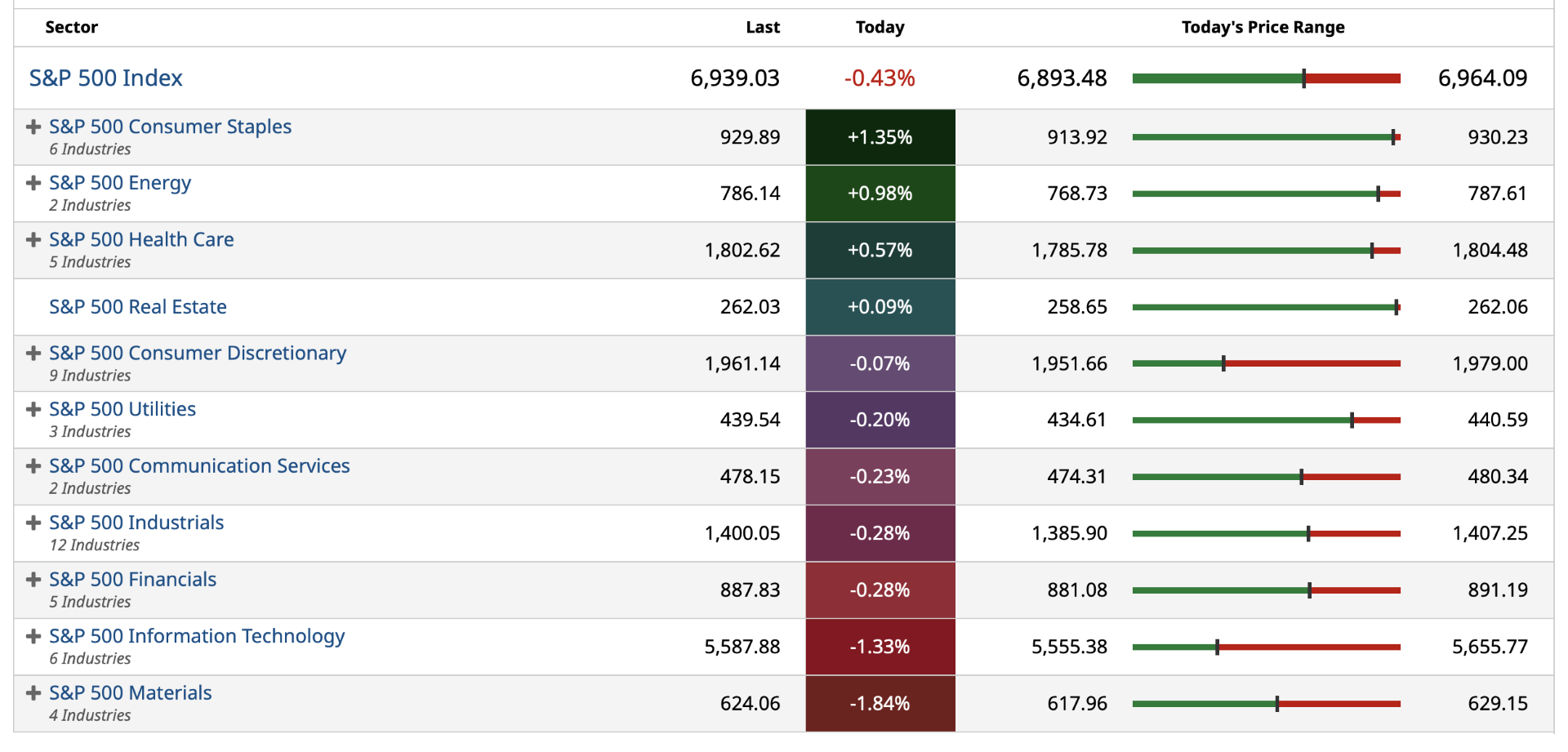

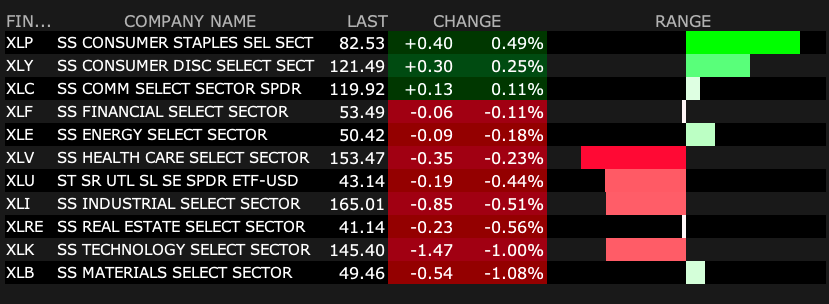

Consumer Staples remains strong today.

In keeping with my Surprises.

BY Doug Kass · Jan 30, 2026, 1:32 PM EST

From Barron's:

He’s Wall Street’s Biggest Showman. Should You Trust Him?

Dan Ives has gone mainstream as Wall Street’s highest-profile stock analyst. Less well known is his growing set of overlapping business interests.

BY Doug Kass · Jan 30, 2026, 1:05 PM EST

* Billionarie Ron Lauder, Kevin Warsh's father in law, has given large sums of money to Republican candidates

* Included in that was a $5 million donation to President Trump's Super PAC, MAGA Inc in March, 2025

This was one of the reasons I predicted this a month ago:

President Trump's choice for Fed Chair was leaked last night and, as suggested in our !0 Surprises for 2026, it is Kevin Warsh:

Trump expected to nominate Kevin Warsh for Federal Reserve chair | CNN Business

From two weeks ago:

Kevin Warsh follows through with Pres. Trump’s view that the U.S. should have the lowest interest rates and cuts the Fed Funds rate to 2% by the end of 2026. At the same time he transfers the Fed’s mortgage holdings to government-sponsored enterprises and the Fed’s coupon holdings to the Treasury in exchange for short-term bills. He works relentlessly to shorten the duration of the Fed’s balance sheet and expresses a goal for 2027 to shrink it. The bond market cheers the more responsible balance sheet management and the 10-year bond rallies to 3.5% but Treasury supply/deficits keep the term premium elevated and the reappearance of inflation risk limits how far the long end can fall and the yield on the long bond remains stubbornly high.

Despite lower short interest rates, housing continues to suffer. After several years of rising prices, home prices are too high to attract adequate demand. Construction volumes suffer and homebuilders are caught with commitment to take delivery of lots from off balance sheet partners that they can’t fulfill. A housing prices war follows and the average new home prices falls 7%. Homebuilder stocks are down by greater than 25%. The resale market remains in the doldrums and volumes fall by 10%. Homebuilders such as Home Depot (HD) and Lowe's (LOW) , real estate brokers and furniture companies all collapse under the weight of lower home prices and slowing sales activity.

By Doug Kass Jan 16, 2026 2:28 PM EST

Position: None

By Doug Kass Jan 30, 2026 5:55 AM EST

BY Doug Kass · Jan 30, 2026, 12:40 PM EST

BY Doug Kass · Jan 30, 2026, 12:23 PM EST

With S&P cash -36 handles I have covered my (SPY) shorts and collapsed the balance of my position.

BY Doug Kass · Jan 30, 2026, 11:33 AM EST

I'm back in the office.

BY Doug Kass · Jan 30, 2026, 11:28 AM EST

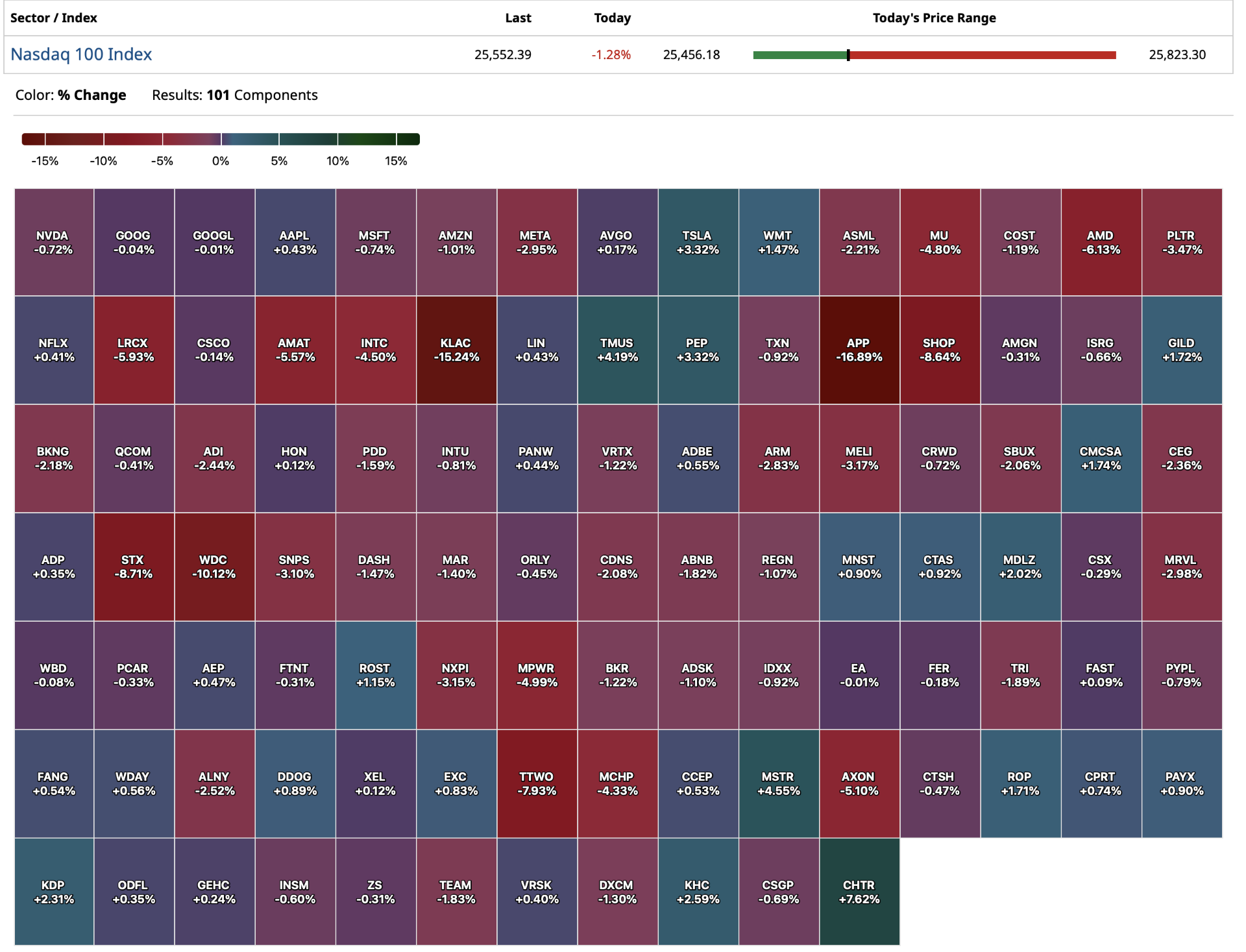

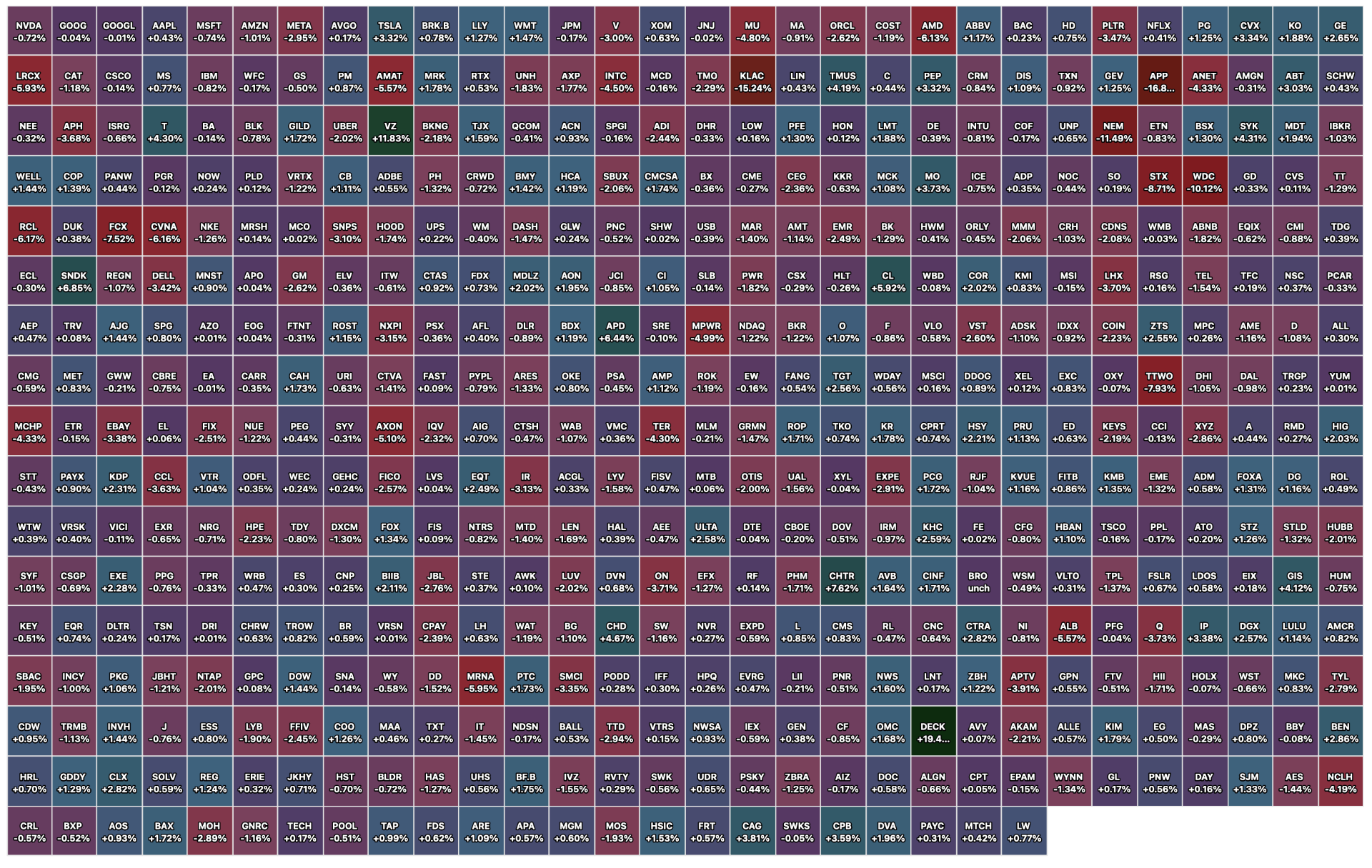

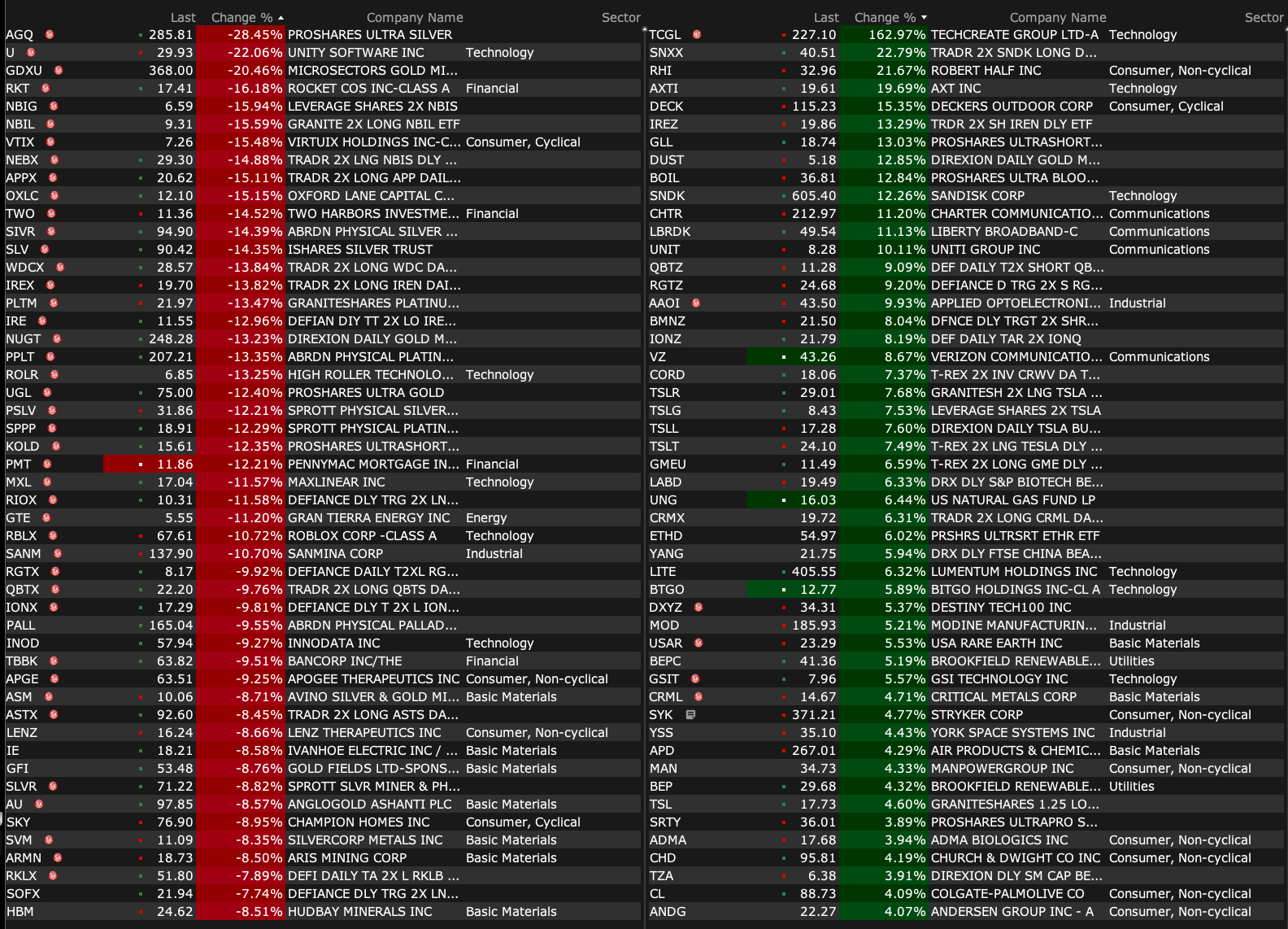

A look at earnings reporting stocks that gapped up/down as of 10:49 a.m.

BY Doug Kass · Jan 30, 2026, 11:20 AM EST

BY Doug Kass · Jan 30, 2026, 11:02 AM EST

-SNDK +24% (earnings, guidance)

-DECK +13% (earnings, guidance)

-RSI +13% (momentum)

-LITE +8.5% (higher in sympathy with SNDK; hearing price target raised at Morgan Stanley)

-CHTR +8.4% (earnings, guidance)

-RHI +8.3% (earnings, guidance)

-SOFI +6.7% (earnings, guidance)

-COHR +6.5% (higher in sympathy with SNDK; hearing price target raised at Morgan Stanley)

-WDC +5.0% (earnings, guidance)

-AAOI +4.0% (higher in sympathy with SNDK)

-CL +3.3% (earnings, guidance)

-VZ +2.7% (earnings, guidance; announces share buyback program)

-SYK +2.0% (earnings, guidance)

-PFSI -22% (earnings)

-CVCO -15% (earnings)

-BZH -12% (earnings)

-APPF -8.3% (earnings, guidance)

-KLAC -7.1% (earnings, guidance)

-ALV -6.6% (earnings, guidance)

-GSIT -4.4% (earnings, guidance)

-DLB -3.7% (earnings, guidance)

-DXC -3.2% (earnings, guidance)

-GDS -3.1% (announces Private Placement of US$300M convertible preferred shares to A Chinese Institutional Investor)

BY Doug Kass · Jan 30, 2026, 9:13 AM EST

BY Doug Kass · Jan 30, 2026, 8:55 AM EST

1:30 p.m.: Fed Bank of St. Louis President (Voter in 2025; Non-Voter in 2026) speaks about the economy and monetary policy at the University of Arkansas Business Forecast Luncheon (Audience questions expected);

5 p.m.: Fed Vice Chair for Supervision Bowman (Voter) speaks on "Monetary Policy and Supervision and Regulation" before the SW Graduate School of Banking at SMU Cox: 161st Assembly for Bank Directors, Oahu, HI (Virtual access available)

BY Doug Kass · Jan 30, 2026, 8:40 AM EST

BY Doug Kass · Jan 30, 2026, 8:25 AM EST

I will be out most of the morning on routine medical appointments.

Less and shorter posts can be expected.

BY Doug Kass · Jan 30, 2026, 7:45 AM EST

BY Doug Kass · Jan 30, 2026, 7:30 AM EST

With S&P futures -21 handles (an hour ago it was -65 handles), I am back putting on some index shorts.

BY Doug Kass · Jan 30, 2026, 7:13 AM EST

* Where is Alan Abelson's pal Abe Briloff when we need him?

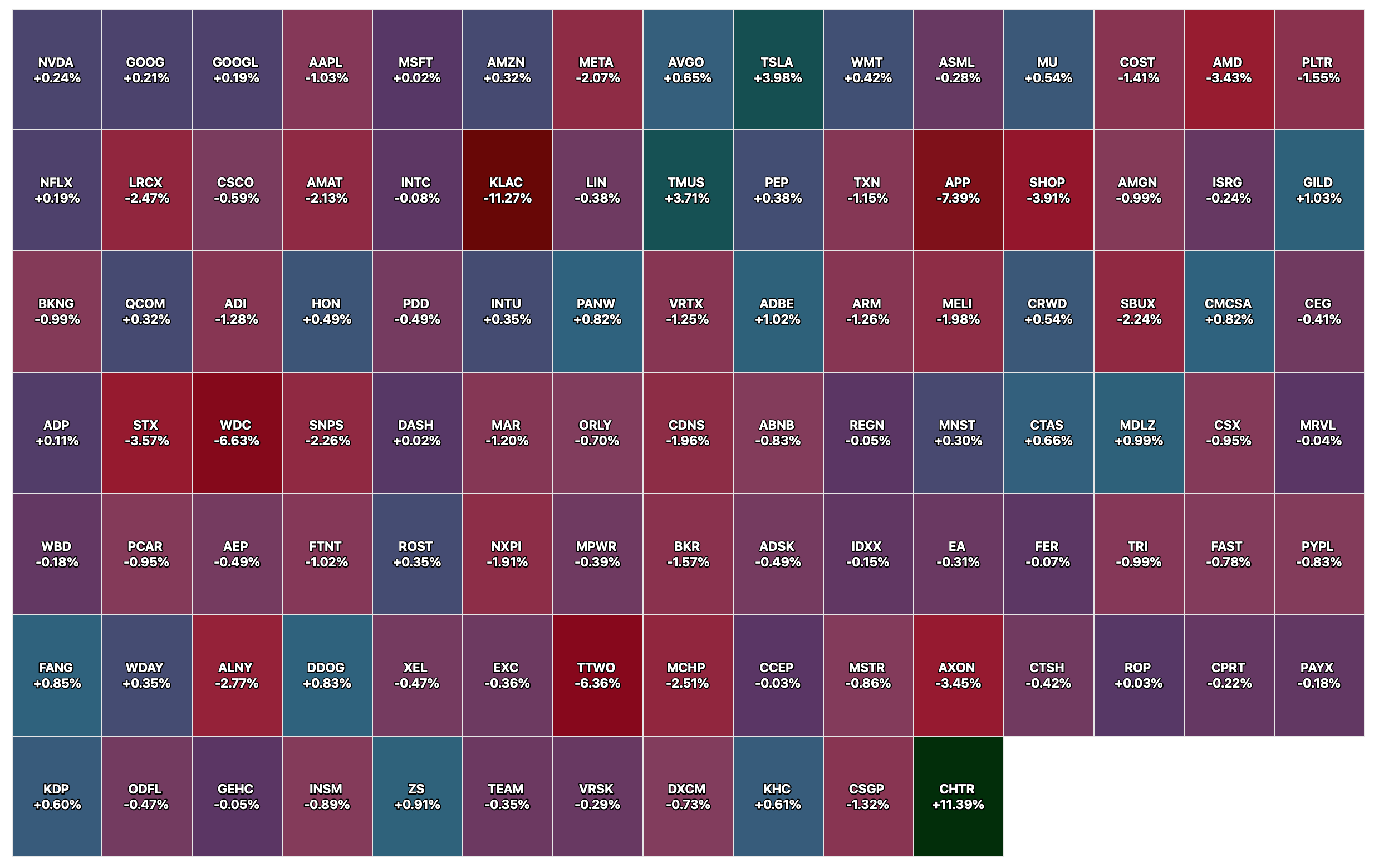

The Microsoft (MSFT) problem is OpenAI.

The company disclosed OpenAI is about half of their remaining performance obligations.

There is a reasonable and growing possibility that OpenAI is going the way of Netscape. My two cents, the line about GDP impact from Nadella is backdoor begging to the government again to bail OpenAI out and effectively bail out Microsoft in the process.

It could be that Microsoft has bet on the wrong horse. Expect to hear similar begging from Oracle (ORCL) and others is my guess. I guess they all think digging holes and filling them back up is a productive use of money?

Then there is this — if you look at its balance sheet, Microsoft may be in a negative cash position now. Not sure what credit you give to “non marketable equity investments.” Then there is the debt and lease liabilities plus we know they have these off-balance sheet vehicles as well.

I am not sure exactly what this all adds up to, while they are producing almost no operating cash flow.

Meta Reports Fourth Quarter and Full Year 2025 Results

Where is Abe Briloff when we need him?

BY Doug Kass · Jan 30, 2026, 7:00 AM EST

BY Doug Kass · Jan 30, 2026, 6:45 AM EST

Phil D. Gapp

* Hat tip to Wally Deemer...

BY Doug Kass · Jan 30, 2026, 6:35 AM EST

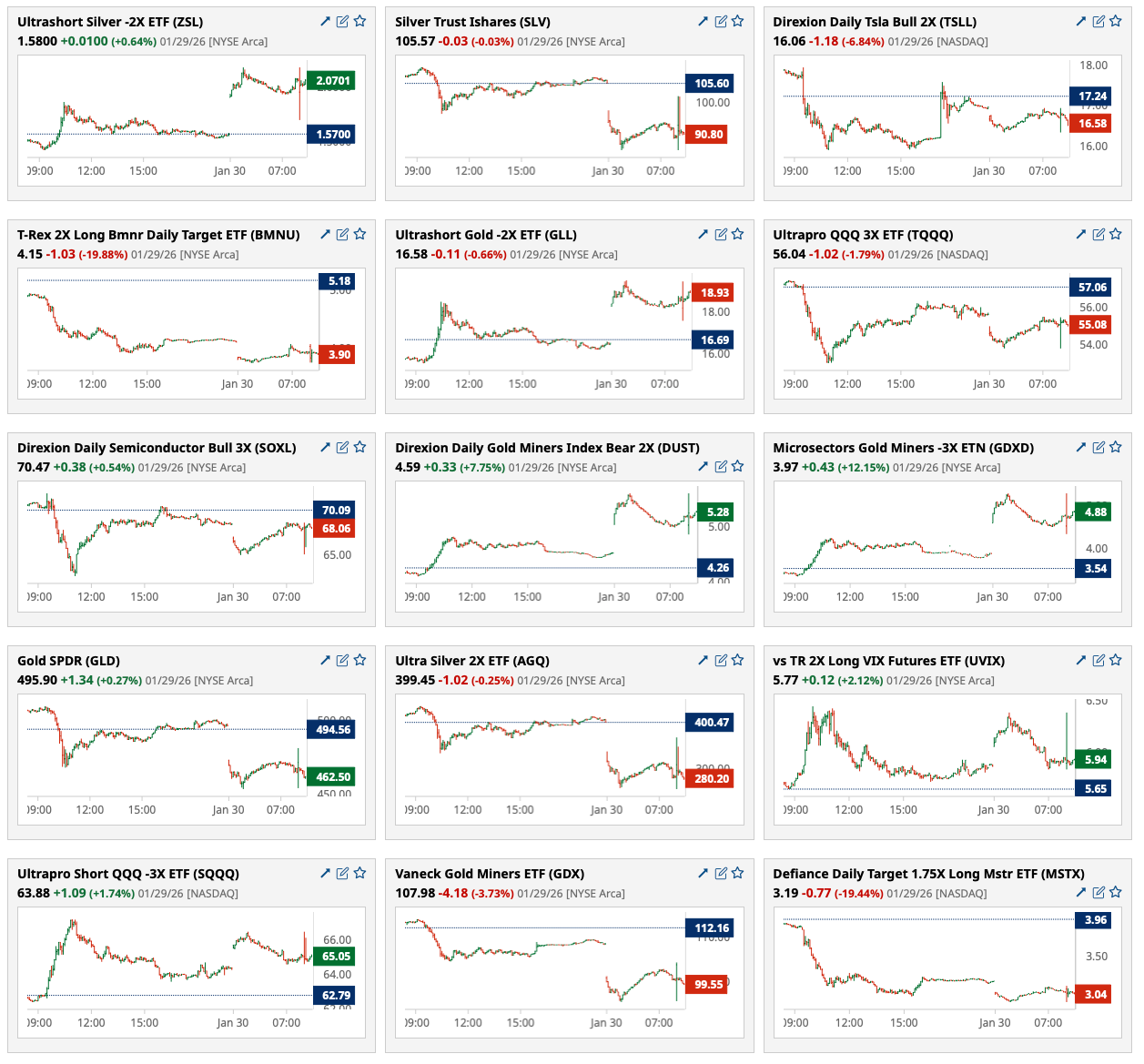

This morning the metals market is getting destroyed:

* Gold -$280 (-5%)

* Silver -$16 (-14%!)

* Platinum -$390 (-15%!)

* Palladium -$245 (-12%!)

From a week ago:

I have maintained a proprietary (read: my own!) technical momentum model.

That model, for the first time, says to sell gold.

That said, I am not shorting GLD - not my style.

But bookmark this post!

Position: None

By Doug Kass Jan 22, 2026 10:23 AM EST

From yesterday:

The price of gold is falling today after a dramatic rise.

(GLD) was trading at $510 and is now $478.

From my 10 Surprises for 2026 Doug's Daily Diary - TheStreet Pro:

There is no place to run, no place to hide — most asset classes fall in the 2026 Bear Market.

Position: None

By Doug Kass Jan 29, 2026 10:46 AM EST

BY Doug Kass · Jan 30, 2026, 6:25 AM EST

BY Doug Kass · Jan 30, 2026, 6:15 AM EST

BY Doug Kass · Jan 30, 2026, 6:05 AM EST

President Trump's choice for Fed Chair was leaked last night and, as suggested in our !0 Surprises for 2026, it is Kevin Warsh:

Trump expected to nominate Kevin Warsh for Federal Reserve chair | CNN Business

From two weeks ago:

Kevin Warsh follows through with Pres. Trump’s view that the U.S. should have the lowest interest rates and cuts the Fed Funds rate to 2% by the end of 2026. At the same time he transfers the Fed’s mortgage holdings to government-sponsored enterprises and the Fed’s coupon holdings to the Treasury in exchange for short-term bills. He works relentlessly to shorten the duration of the Fed’s balance sheet and expresses a goal for 2027 to shrink it. The bond market cheers the more responsible balance sheet management and the 10-year bond rallies to 3.5% but Treasury supply/deficits keep the term premium elevated and the reappearance of inflation risk limits how far the long end can fall and the yield on the long bond remains stubbornly high.

Despite lower short interest rates, housing continues to suffer. After several years of rising prices, home prices are too high to attract adequate demand. Construction volumes suffer and homebuilders are caught with commitment to take delivery of lots from off balance sheet partners that they can’t fulfill. A housing prices war follows and the average new home prices falls 7%. Homebuilder stocks are down by greater than 25%. The resale market remains in the doldrums and volumes fall by 10%. Homebuilders such as Home Depot (HD) and Lowe's (LOW) , real estate brokers and furniture companies all collapse under the weight of lower home prices and slowing sales activity.

By Doug Kass Jan 16, 2026 2:28 PM EST

BY Doug Kass · Jan 30, 2026, 5:55 AM EST

The S&P Short Range Oscillator remains modestly overbought at 1.00% vs. 1.45%.

BY Doug Kass · Jan 30, 2026, 5:45 AM EST