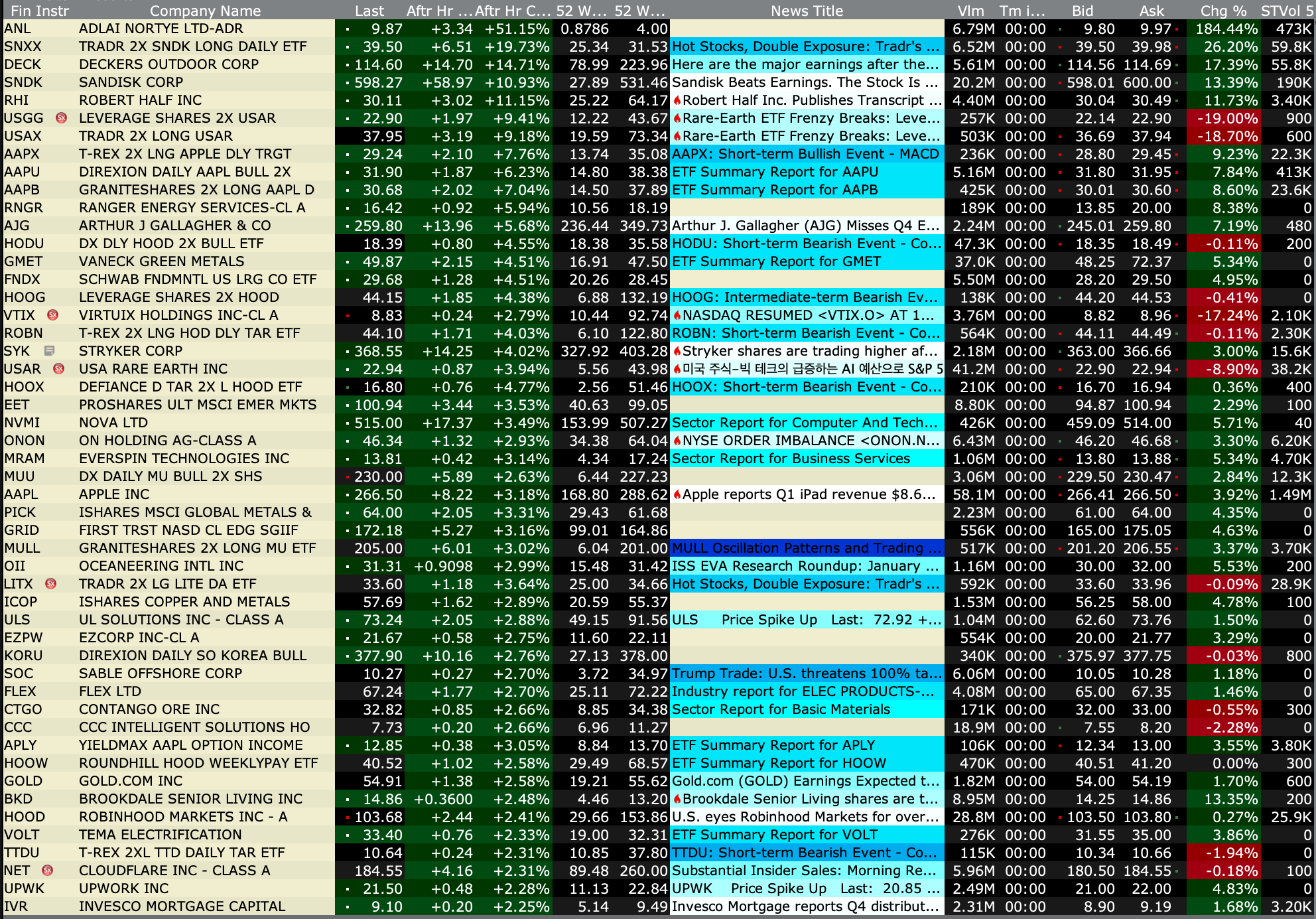

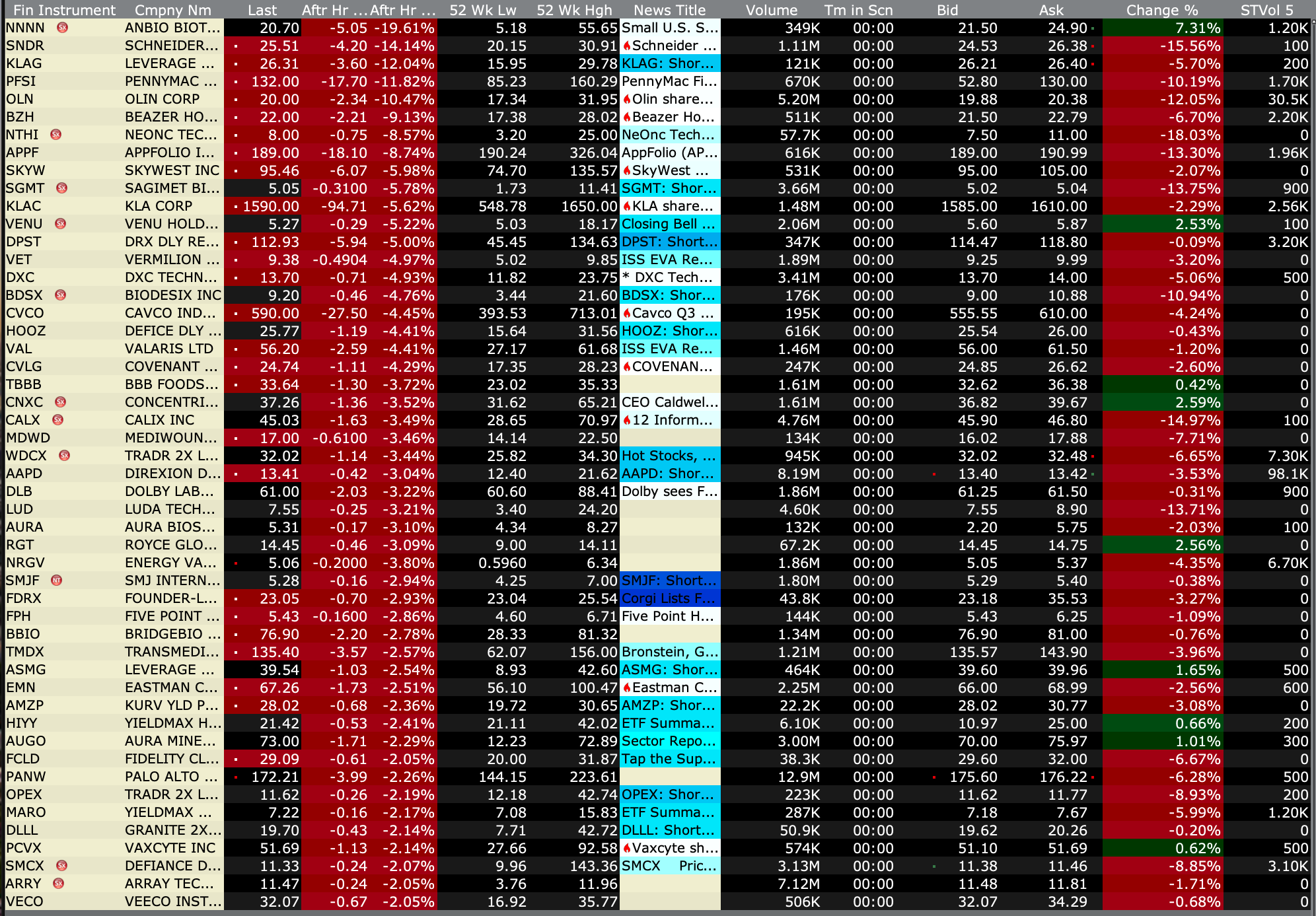

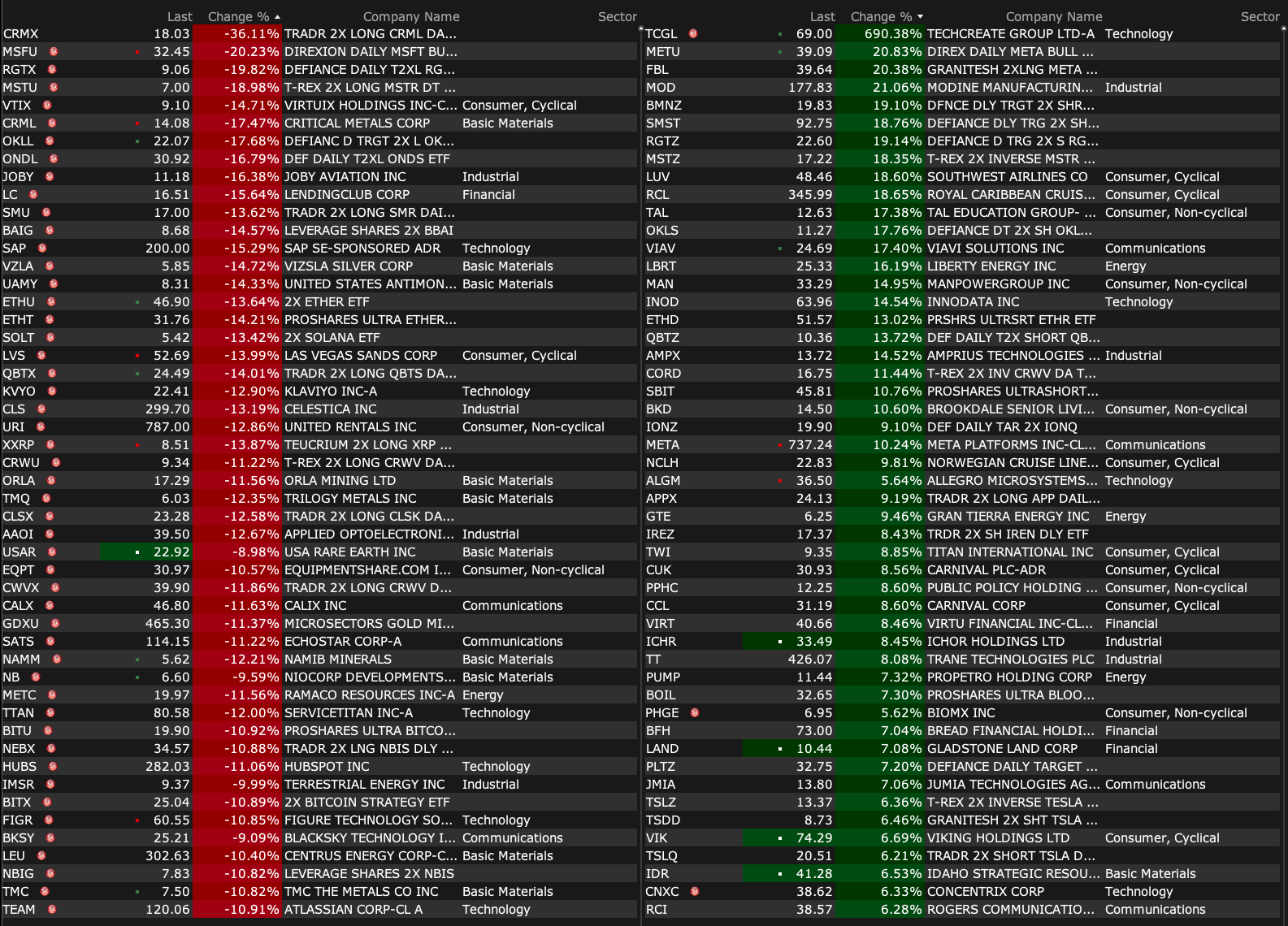

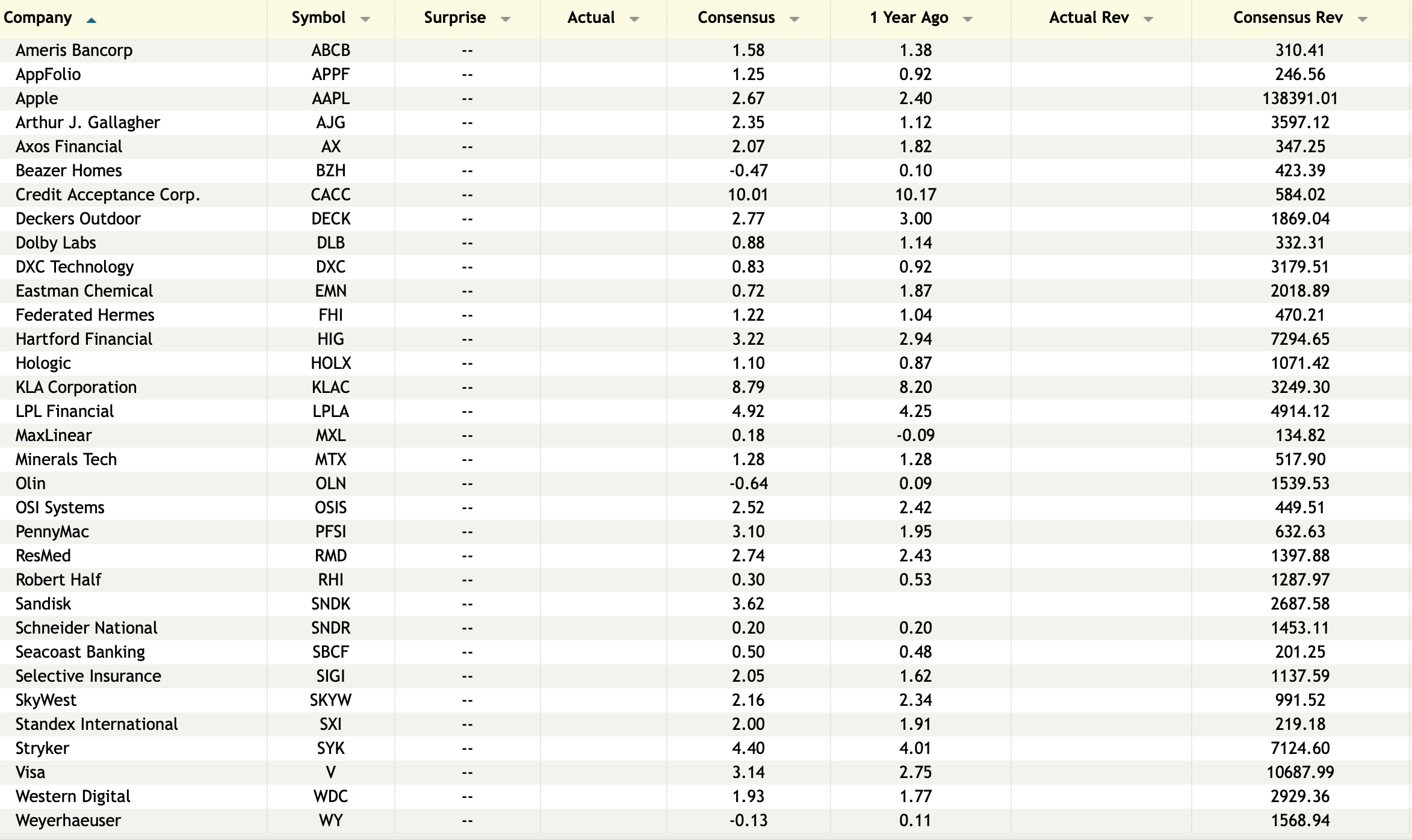

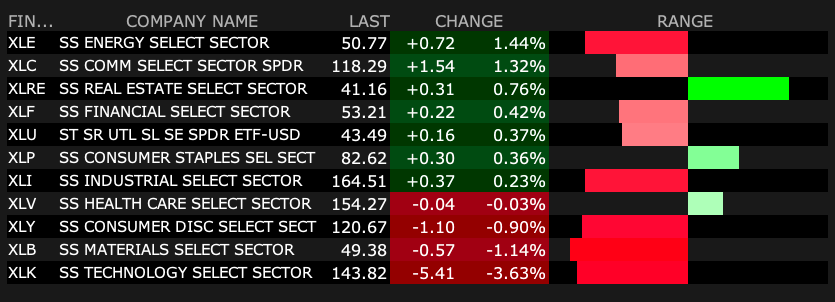

Interesting look at earnings reporting stocks as of 1:30 PM.

Those that gapped up remained up but for Tesla (TSLA) and International Paper (IP) and the majority of those that gapped down are near their lows of the day.

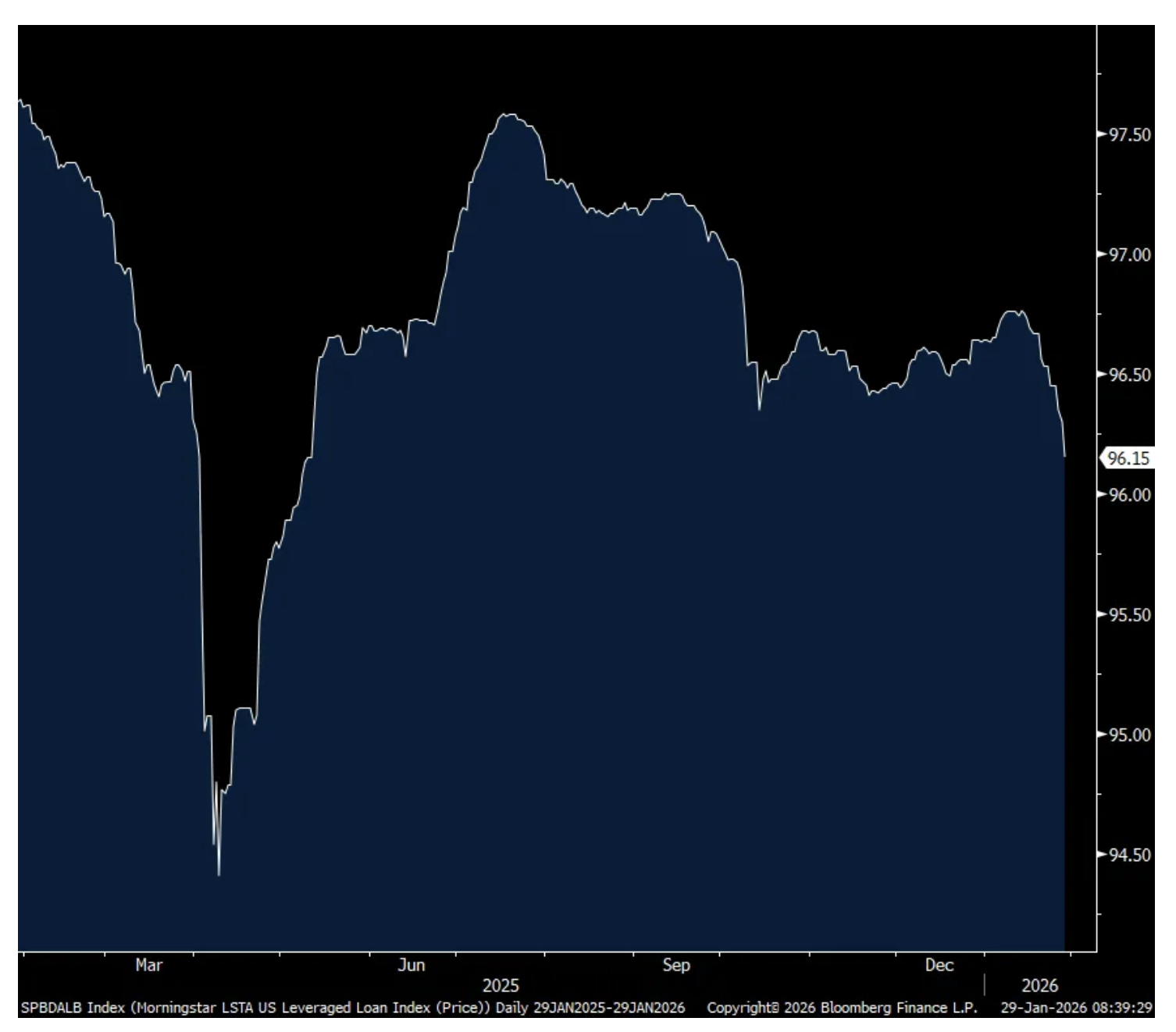

Before I get to the claims data, I want to mention again the LSTA leveraged loan index because something is going on. It closed yesterday at the lowest level since May 2025. I welcome any thoughts on this. It hasn’t seen an uptick since January 13th.

LSTA Leveraged Loan Index

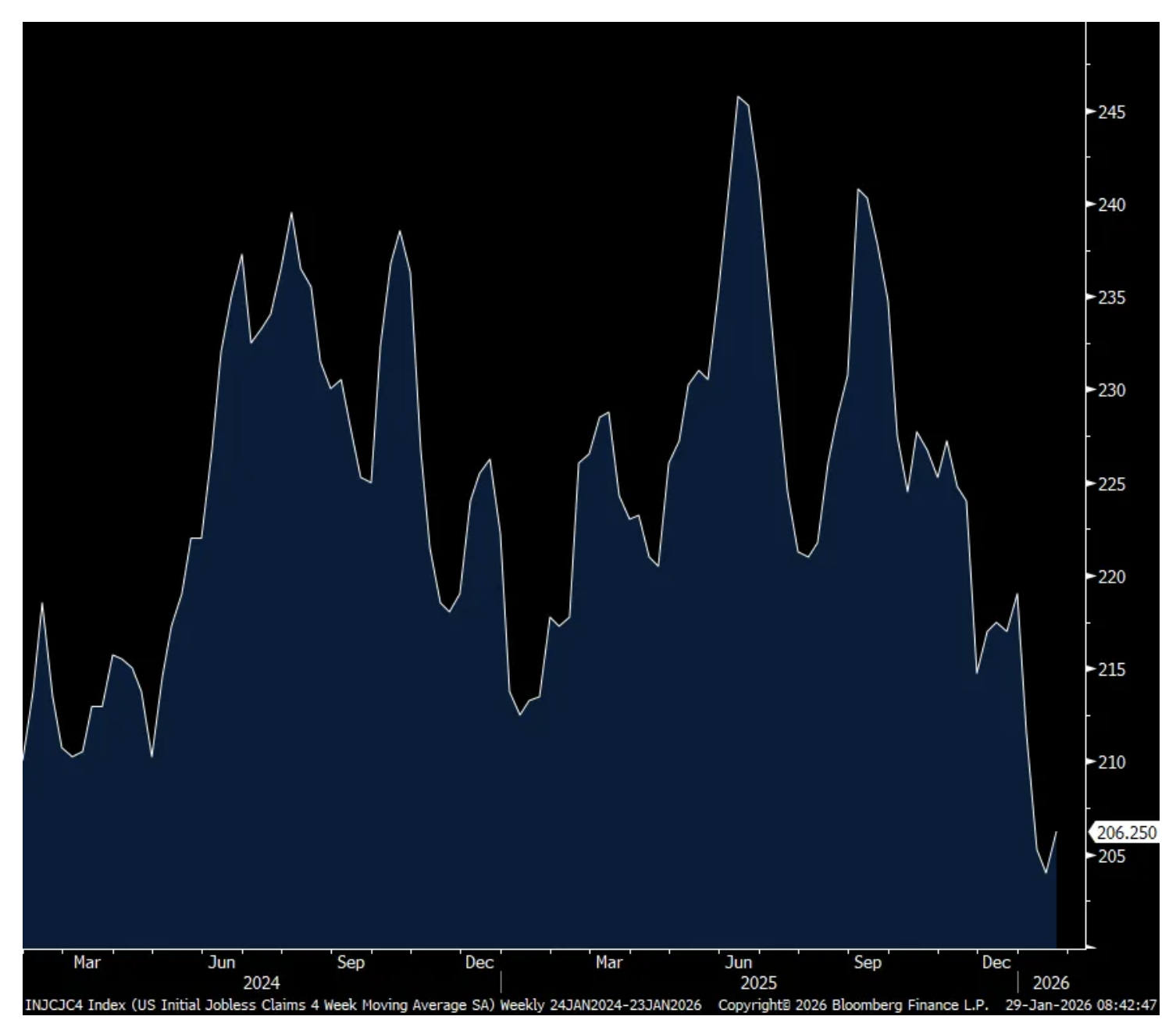

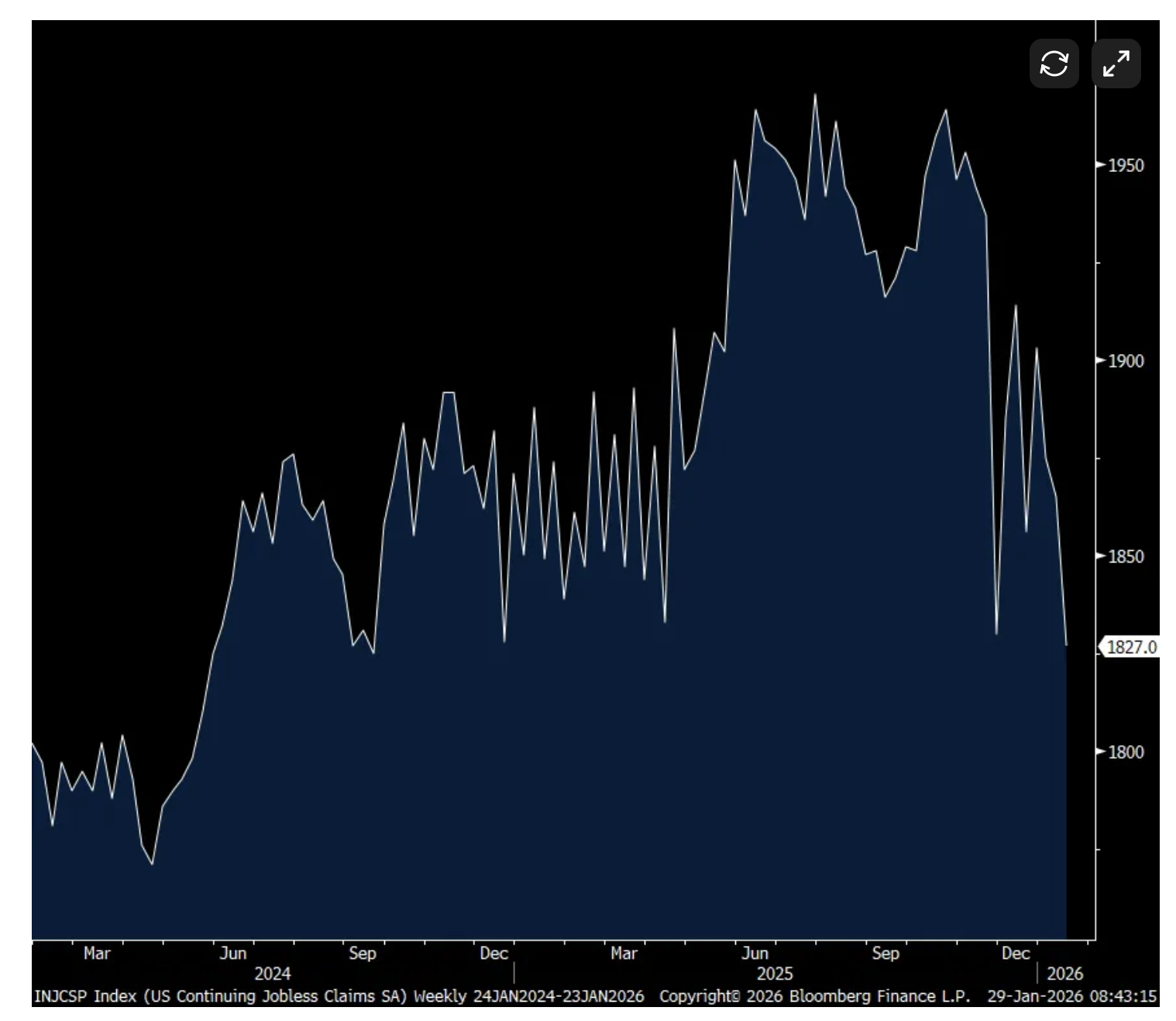

Initial jobless claims were little changed at 209k vs 210k last week and was 4k above the estimate. The 4 week average rose to 206k from 204k. Continuing claims dipped to 1.827mm from 1.865mm and furthering away from the 1.9mm level that has been a lid for now. The question here though is whether people’s claims are expiring and why continuing claims are falling or are people finding new jobs. Considering the slowdown in the overall pace of hiring, I’m leaning to the former.

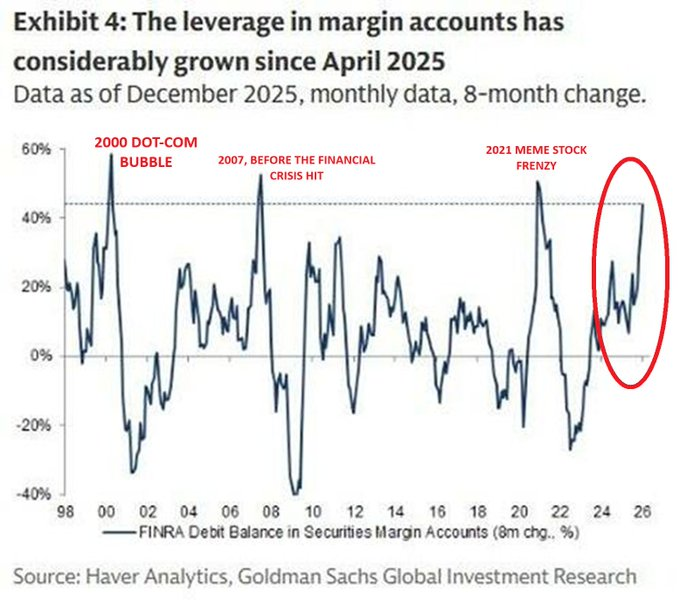

Margin debt now stands at $1.23 trillion - rising by $325 billion over the last 12 months.

Margin debt has increased in eight straight months, surging by +45% since April, 2025.

This is the fastest increase since right before the dot.com bubble burst and in mid-2007 (a month or two before the Great Recession hit and stocks plummeted):

Boockvar on the Investors Intelligence Bulls, ADP on AI

From Peter Boockvar:

Flashing red/Commodities/Earnings and ADP chimes in on AI jobs impact

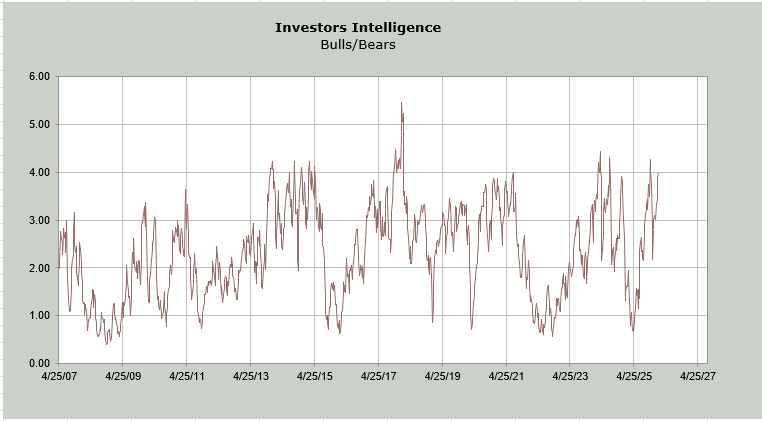

The Investors Intelligence survey is now flashing red with the Bulls back above 60 for the first time in more than a year at 61.5. With Bears at just 15.4, the spread at 46.1 is well above the 40 threshold that I considered stretched. In today’s AAII, Bulls were 44.4, up 1.2 pts w/o/w vs Bears at 30.8, down 1.9 pts. That is not an extreme spread so it’s really II that I’m highlighting today. This is only relevant for the short term but something to take note of.

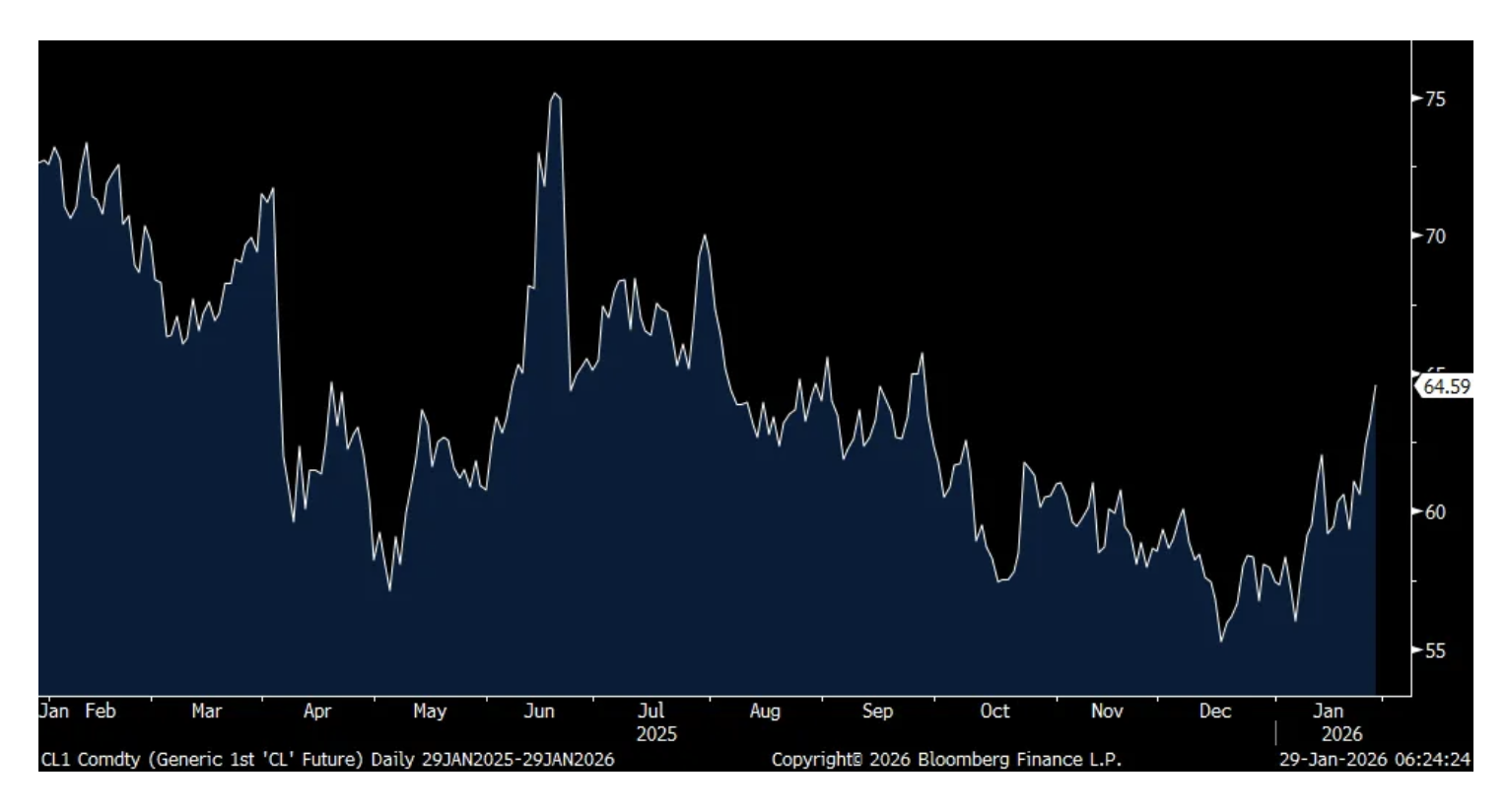

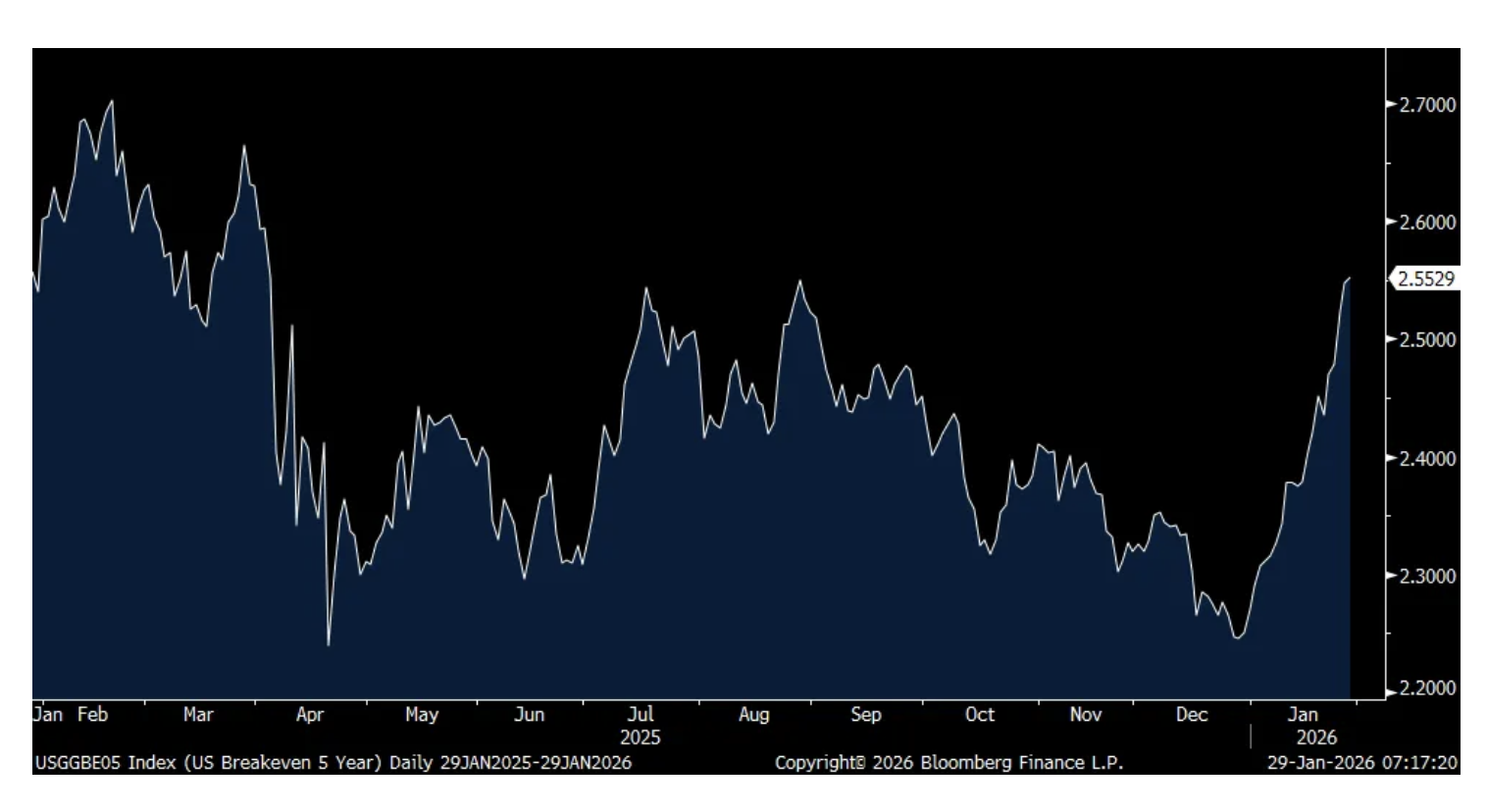

This move in industrial and precious metals continues on and the pace of gains is astonishing to see. The CRB raw industrials index closed yesterday at a fresh 3 ½ yr high, helped by copper. Quietly too, the price of WTI crude oil is rising to the highest level since late September. I continue to believe that a barrel of oil is one of the cheapest assets in the world and it will join the commodity bull market in metals. We remain long. If I’m right, the upcoming new Fed Chair is going to have a real dilemma on his hands. The 5 yr inflation breakeven at 2.55% matches the highest since last April.

CRB Raw Industrials Index

WTI

5 yr Inflation Breakeven

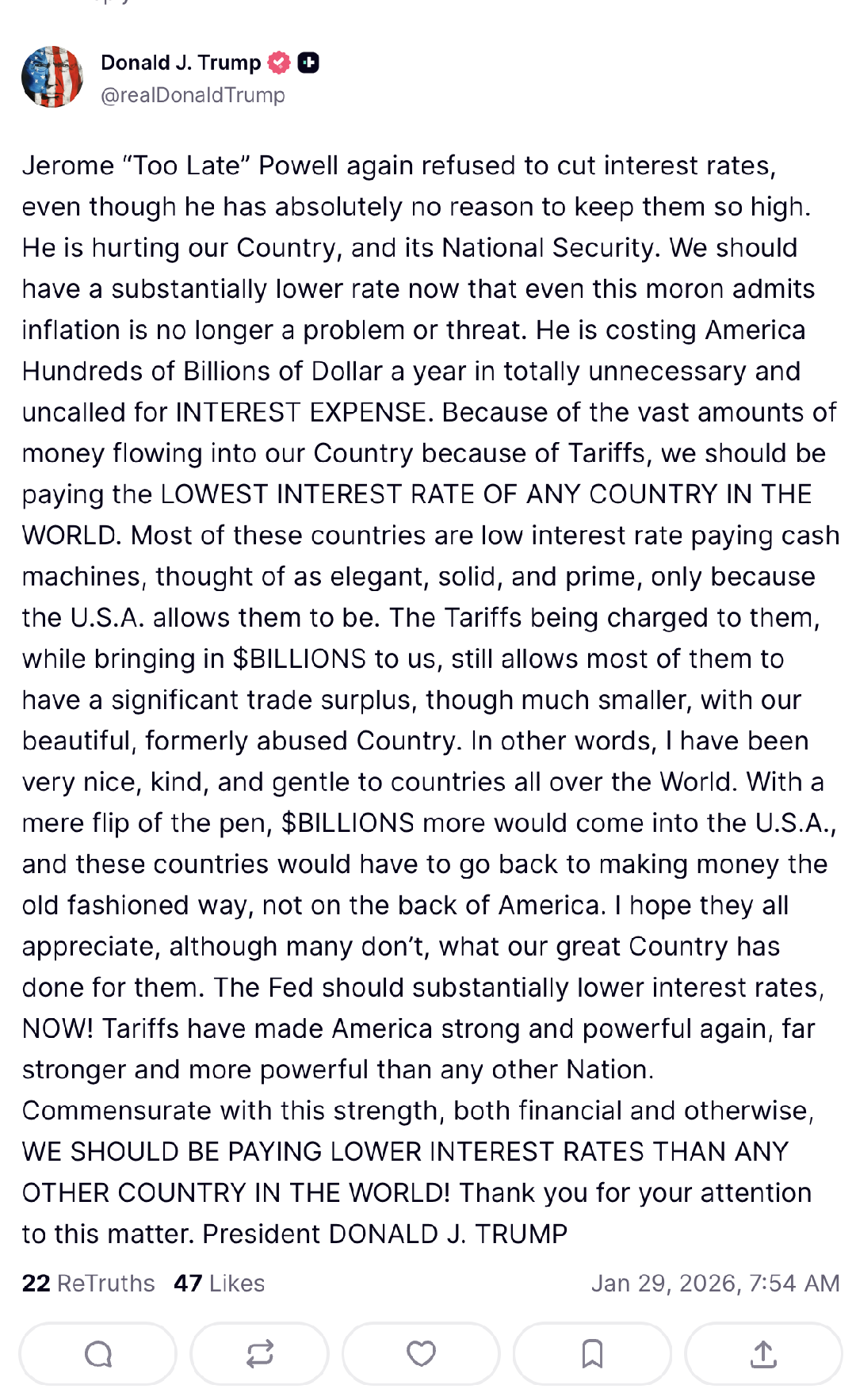

It’s not just the Fed that is sitting tight for now, the Bank of Canada expressed the same sentiments yesterday as they held their overnight rate at 2.25% which is below the rate of inflation. They said “The Bank is committed to ensuring that Canadians continue to have confidence in price stability through this period of global upheaval.”

If you want positive REAL rates of substance, emerging market bonds is where one needs to go and we are long, in local currencies. For example, REAL rates in Brazil are 1100 bps. It’s zero in Europe and Canada, negative in Japan and at just .8% in the US.

The earnings calls still reflects a mixed bag economy. I know some like to look at the headline GDP figure but the major contributions are still coming from the data center buildout, upper income spending and government largesse. There is little to no growth elsewhere.

From Starbucks:

“In the US, where much of our turnaround work has been focused, company operated transaction comps grew y/o/y for the first time in 8 quarters, and we grew transactions across all dayparts in the quarter.” Execution is also dramatically improving in all areas.

With the 4% comp growth in the US, transactions were up 3% and average ticket up by 1%, “driven by a growing mix of espresso and tea-based beverages, alongside the continued rise in the popularity of our cold foam platform.”

“People came back to the brand, and we also drove engagement or more frequency with our existing customers.”

International comps grew by 5%. “Most of our largest international markets, including our company operated businesses in China, Japan, and the UK, contributed to our comp sales performance in the quarter. China continues to showcase strong momentum.”

“while market dynamics can change, we continue to expect coffee prices and tariff pressures to peak in Q2 and find some relief in the back half of the fiscal year.”

From Brinker’s, the owner of Chili’s and Maggiano’s:

Chili’s comps are still robust, up 8.6%, “outpacing the casual dining industry by 680 bps.”

“Q2 results were driven by our world class marketing and brand building that brought guests in and continued improvements in food, service, and atmosphere that brought guests back.”

“Chili’s top line sales growth was driven by price of 4.4%, positive traffic of 2.7%, and positive mix of 1.5%.” Its Margarita of the Month program helped comps.

I’ll add this, casual dining has clearly been outperforming quick service and fast casual because it skews to older customers that have more money.

Maggiano’s is still challenged with a drop in comps of 2.4%.

On the macro, “December didn’t look great. January looked better. Weather stopped everything. We’ll see what happens when we get fully out of the weather, whether the strength that we saw in January restarts.”

This was the response on the ADP earnings call to a question of what the impact of AI is having on the labor market and whether it’s a reason for the slowing pace of hiring:

“I think more of the headlines that I’ve seen actually have been more about sort of corporate realignment following a big hiring period post-pandemic. But in terms of the data we look at, we look at it obviously very closely. We look at it by industry, and about 10 or 12 industry groups. We’re not really seeing anything discernible there. I mean, you look at the labor market situation, certainly the hiring levels are muted, job openings are relatively muted. We’ve been talking about that now for some quarters on this call.”

“What we’ve also been talking about, though, and what we still continue to see is continuing reductions in the level of overall layoffs going on in the job market, and certainly lower layoffs. And across the industry groups, we see a lot of consistency, if you like, in terms of where they’re going and sort of areas that potentially you may think of as being more subject to being at risk with AI. We’re not actually seeing it in those industry verticals. So things like financial services, things like professional services, tech, and so on, we’re actually seeing reasonably healthy growth. So it’s hard to say, but the empirical data does not really point to that happening at this point in time. The future obviously is yet to be determined.”

From Meta who reported another phenomenal quarter (24% revenue growth off a big base) but another eye opening pace of capital spending:

“We ended 2025 strong with more than 3.5 billion people now using at least one of our apps every day. That includes more than 2 billion daily actives each on Facebook and WhatsApp and just shy of that on Instagram.”

“Our business also performed very well, thanks to record breaking holiday demand and AI driven performance gains. We are now seeing a major AI acceleration.”

“In Q4, the total number of ad impressions served across our services increased 18%. Impression growth was healthy across all regions, driven primarily by engagement and user growth, and to a lesser degree, ad load optimizations. The average price per ad increased 6% y/o/y, benefiting from increased advertiser demand, largely driven by improved ad performance.”

“We anticipate 2026 capital expenditures, including principal payments on finance leases, to be in the range of $115 billion to $135 billion, with y/o/y growth driven by increased investment to support our Meta Superintelligence Labs efforts and core business.”

Their previous guide was $110 billion and this new level of spend compares to $70 billion in 2025 and $37 billion in 2024. Relative to the expected 2026 revenue estimate, it’s now up to 52% vs 35% in 2025 and 23% in 2024. In 2021 before the AI spend started, it was 16%. I’ll use the word ‘astonishing’ again.

Microsoft is being weighed down by a slight miss in their Azure growth rate and big exposure to Open AI in terms of their remaining performance obligations (RPOs). “Commercial remaining performance obligation, which continues to be reported net of reserves, increased to $625 billion and was up 110% y/o/y with a weighted average duration of approximately 2 ½ years.” Of this, 45% is tied to OpenAI.

With cloud, “we continue to see strong demand across workloads, customer segments, and geographic regions, and demand continues to exceed available supply.”

“Capital expenditures were $37.5 billion, and this quarter roughly two-thirds of our CapEx was on short lived assets, primarily GPUs and CPUs.”

Their expected CapEx number of about $100b for fiscal yr ended 6/26 is 30% of expected revenue which compares with 23% in fiscal ‘25 and 12% in fiscal ‘22 right before CapEx inflected much higher.

From CH Robinson, the logistics/transportation broker:

“Over the past year, we’ve consistently said that we’re not immune to macroeconomic conditions, but that we are managing them better than we have in the past. The fourth quarter certainly provided a challenging macroenvironment. With weak global freight demand, rising spot costs in trucking, and falling ocean rates all providing headwinds to our business.”

“The Cass Freight Shipment Index declined y/o/y for the 13th consecutive quarter and was the lowest Q4 reading since the financial crisis of 2009. Spot market costs for truckload capacity spiked during the last 5 weeks of the quarter, due to a seasonal decline in capacity, three winter storms, and incremental pressure from the cumulative enforcement of various commercial driver regulations.”

“International freight continues to be impacted by global trade policies, which caused previous front-loading, a dislocation of shipments, and a more pronounced decline in demand after the Q3 peak season. Combined with excess vessel capacity, this caused ocean rates to decline substantially vs a year ago...So, the macro conditions for global transportation companies were difficult in Q4, and we are not impervious to these volume and rate dynamics.”

Overseas, the Swedish Riksbank held its policy rate unchanged at 1.75% as expected. They have negative REAL rates too with December CPI up 2.1% y/o/y and are on hold for now.

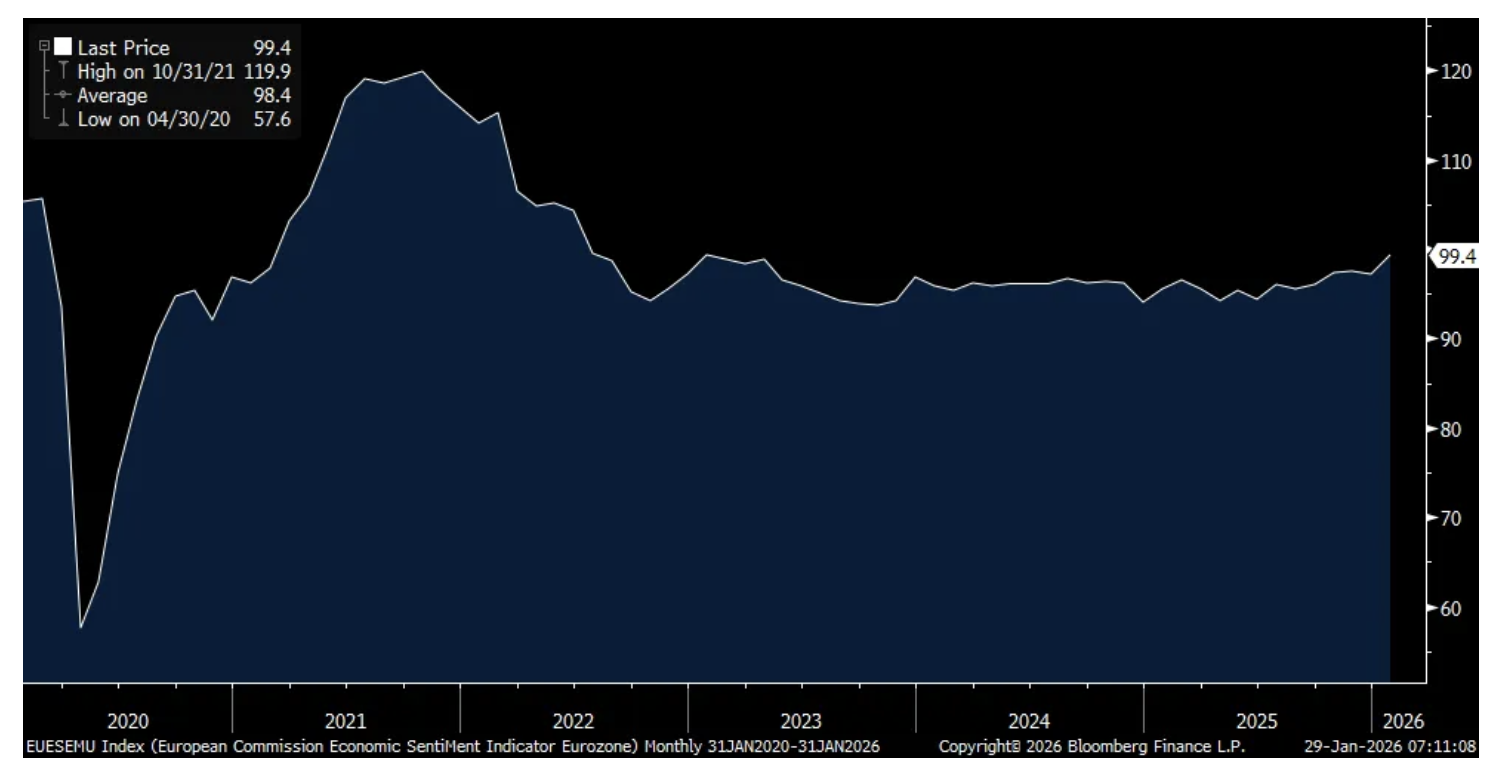

The January Eurozone Economic Confidence index did lift to 99.4 from 97.2 and that was 2.3 pts above expectations with improvements in services and manufacturing. That matches the best level since July 2022. Can the pressure Trump is putting on the region Make Europe Great Again in terms of incentivizing the region to get its economic house in order? We should all hope so and if the case, European stocks can have another good year.

I have bought back (for a nice profit the Index common that I sold early this morning) now back to delta neutral the indexes:

* (SPY) $695.73

* (QQQ) $630.01

From this morning:

Late Wednesday Evening and Early Thursday Morning Trading

I am actively trading the market's growing volatility, opportunistically. (Note: I really don't recommend this sort of frenetic trading for home gamers — it is too hard and time consumptive! I also suspect most won't care to follow this sort of trading, though we do have a number of very active traders as subs).

When S&P futures slipped back to about -18 handles (around 7:05 PM last night) I bought (SPY) and (QQQ) to become delta-equivalent neutral against my short index calls:

* SPY $693.44

*QQQ $632.14

Now S&P futures are +20 handles.

I am back shorting the indices. I am accomplishing this by taking off some of the index longs put on at around 7:05 PM last night:

* SPY $697.63

* QQQ $635.70

Position: Long SPY common (VS/S), QQQ common (VS/S); Short SPY calls (S), QQQ calls (S)

Microsoft report 'solid' but not enough to clear elevated expectations, says RBC

RBC Capital keeps an Outperform rating and $640 price target on Microsoft after its results. The company delivered a solid quarter with revenue, EPS, and operating margins exceeding expectations, but results weren't enough to clear elevated expectations, the analyst tells investors in a research note. RBC adds however that with Al monetization broadening and much of incremental Al capacity already contracted, it sees continued upside in growth and margins.

Microsoft price target lowered to $575 from $630 at Deutsche Bank

Deutsche Bank analyst Brad Zelnick lowered the firm's price target on Microsoft to $575 from $630 and keeps a Buy rating on the shares. The company reported solid fiscal Q2 results, but fell short of "more lofty" market expectations for Azure growth, the analyst tells investors in a research note. The firm updated the company's model post the earnings print.

Microsoft price target raised to $540 from $520 at Stifel

Stifel analyst Brad Reback raised the firm's price target on Microsoft to $540 from $520 and keeps a Buy rating on the shares. Capacity constraints limited Azure upside and it does not appear investors should expect a meaningful Azure acceleration the next few quarters given management's commentary around the need to balance datacenter supply among their own apps, R&D efforts and customer demand, the analyst tells investors. The firm continues to believe the company must get to a point where Azure growth meaningfully outpaces capex growth rates for the stock to effectively re-rate in coming quarters, the analyst added.

Microsoft removed as Top Pick at Morgan Stanley after Q2 report

Morgan Stanley analyst Keith Weiss contends that Microsoft reported "another remarkably strong" fiscal Q2 with its $240B revenue base growing 17% year-over-year, or 15% in constant currency, and EPS excluding a $10B gain from OpenAI up 24% year-over-year, or 21% in constant currency. However, investor focus has narrowed more tightly towards areas seen as the key indicators of GenAI fitness, namely Azure growth and M365 Commercial Cloud, and Azure growth at 38% cc only exceeded company guidance by 1 percentage point, disappointing investors expecting a beat in the 2%-3% range, the analyst added. The analyst removed Microsoft as his Top Pick, but keeps an Overweight rating and $650 price target on the shares.

Microsoft price target lowered to $580 from $640 at Evercore ISI

Evercore ISI lowered the firm's price target on Microsoft to $580 from $640 and keeps an Outperform rating on the shares. Microsoft posted "solid results" with Azure's 38% growth slightly beating expectations, but capacity constraints are slowing acceleration, the analyst tells investors. Capex increased 66% year-over-year and investors are seeking evidence of Azure acceleration from these investments, the analyst added.

Microsoft price target lowered to $550 from $575 at JPMorgan

JPMorgan lowered the firm's price target on Microsoft to $550 from $575 and keeps an Overweight rating on the shares following the earnings report. Microsoft reported revenue and earnings upside, but with slightly less magnitude than in recent quarters, the analyst tells investors in a research note. The firm attributes this to softness in the company's "less-critical" gaming and advertising segments, as well as capacity constraints in Azure.

Microsoft price target lowered to $575 from $625 at Wedbush

Wedbush lowered the firm's price target on Microsoft to $575 from $625 and keeps an Outperform rating on the shares. The firm notes the company delivered results that featured beats across all key metrics as the company is capitalizing on the heightened momentum seen in the AI Revolution reflected in the increased strength it continues to see in its cloud and AI solutions. Microsoft remains a core winner in the IVES AI 30 list, Wedbush adds. The firm believes that any weakness post print represents strong buying opportunities for long-term investors.

Microsoft price target lowered to $641 from $645 at Bernstein

Bernstein analyst Mark Moerdler lowered the firm's price target on Microsoft to $641 from $645 and keeps an Outperform rating on the shares. The firm notes Microsoft delivered solid results and healthy guide, yet the stock was down about 6% aftermarket, as Azure growth slightly missed the buyside expectation. Management stated that Azure could have grown over 40%, but they are constrained by capacity and are prioritizing 1st party apps and R&D over near-term Azure growth. Bernstein thinks this is a hard but necessary decision for the company's long-term value creation.

Microsoft price target lowered to $600 from $650 at Piper Sandler

Piper Sandler analyst Brent Bracelin lowered the firm's price target on Microsoft to $600 from $650 and keeps an Overweight rating on the shares following quarterly results. The firm notes Azure growth and a steady outlook for Q3 once again fell short of investor expectations. While investors remain myopically focused on Azure and capex plus lease growth, management made it clear that its focus remains on the broader platform, which means allocating capacity towards Azure, first-party apps, and internal R&D. Piper remains bullish on Microsoft.

Microsoft price target lowered to $635 from $660 at Citi

Citi lowered the firm's price target on Microsoft to $635 from $660 and keeps a Buy rating on the shares. The firm views the company's earnings report as mixed. Azure posted slight upside with growth slightly slowing as Microsoft makes a capacity allocation decision to prioritize first party services, the analyst tells investors in a research note. Citi slightly reduced Azure estimates following the print but says CoPilot momentum is accelerating.

Microsoft price target lowered to $615 from $630 at Wells Fargo

Wells Fargo lowered the firm's price target on Microsoft to $615 from $630 and keeps an Overweight rating on the shares. While Q2 results are likely to add to debates around Azure capacity constraints, the firm thinks the Q3 guide actually suggests potential for growth to improve in the second half of 2026 and beyond as more capacity comes online

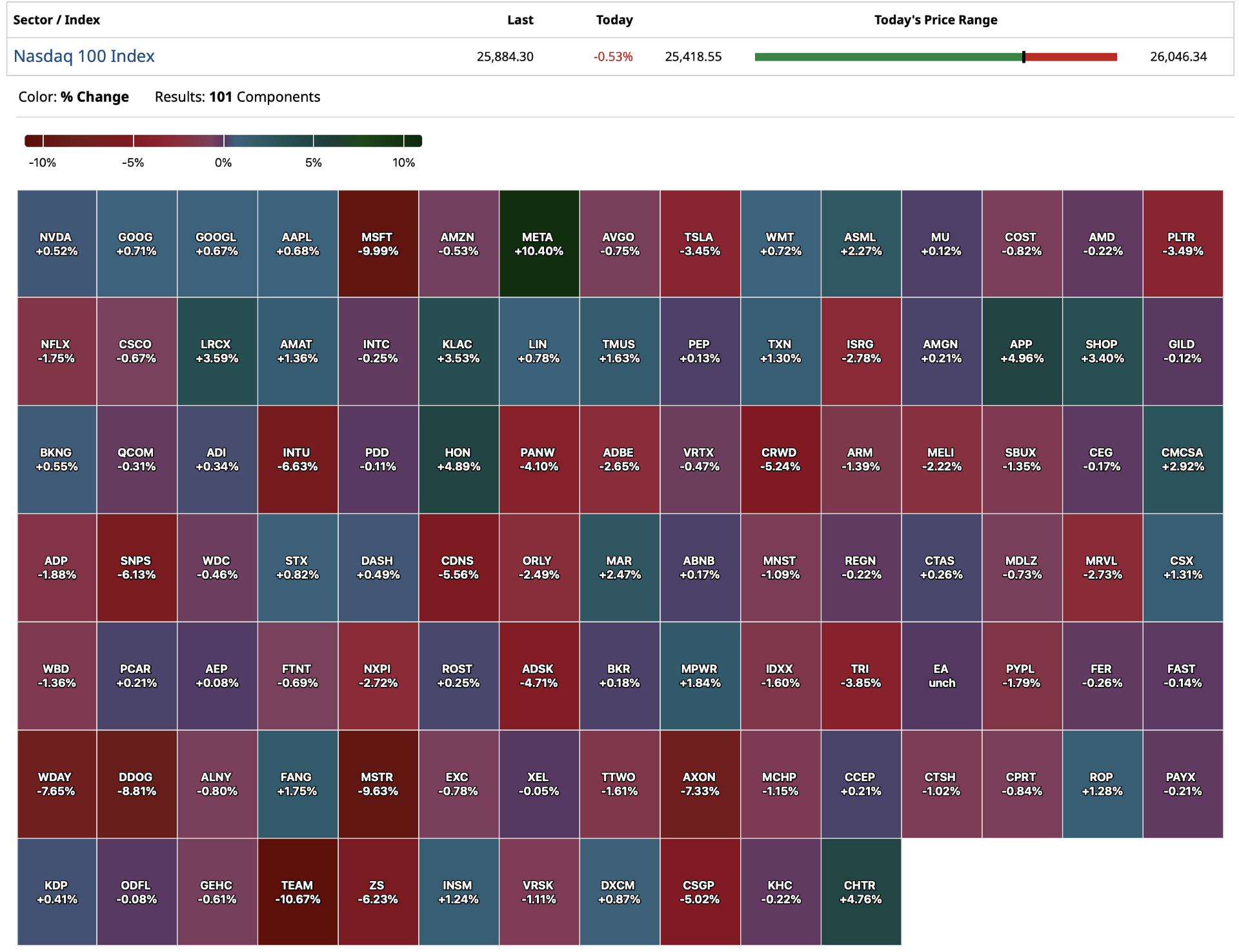

US: Futs are higher, led by Tech, after the first batch of Mag7 earnings. Pre-mkt META +7.9%, MSFT -6.6%, and TSLA +2.8% with AAPL tonight and then AMZN / GOOG next week. Cyclicals are trading higher led by Energy and Industrials and the AI theme also acting well as capex / fundamentals remain supportive of growth. The yield curve is twisting steeper with the USD flat. Cmdtys remain bid across all 3 complexes with WTI (Iranian supply fears) and precious (debasement trade) the most notable. Today’s macro data focus is on jobless claims though given Powell’s comments yesterday, Friday’s PPI is more important.

Following Divine Ms. M's cautionary comments, this just in from fellow stooge Peter Boockvar:

The Investors Intelligence survey is now flashing red with the Bulls back above 60 for the first time in more than a year at 61.5. With Bears at just 15.4, the spread at 46.1 is well above the 40 threshold that I considered stretched. In today’s AAII, Bulls were 44.4, up 1.2 pts w/o/w vs Bears at 30.8, down 1.9 pts. That is not an extreme spread so it’s really II that I’m highlighting today. This is only relevant for the short term but something to take note of.

Notice that first line about the broad GDP impact :

“We are still in the beginning phases of AI diffusion and its broad GDP impact...”

Ohhh.... so now Microsoft is either pretending to be the Red Cross (looking to make charitable contributions to the U.S. economy) OR the company is tacitly begging for even more help from the U.S. government because things are not playing out exactly like they expected with their massive loss-making investments?

Then of course this whole thing (the series of tweets) is just one more way to pump the stock price because otherwise what else is the point of this diatribe on Twitter/X?

Microsoft's shares are trading -$30 in premarket trading.

From one of uber-bullish Dan Ives' daily appearance on CNBC. (Dan has blocked me on Twitter for my critical comments):

"In the last month we have seen 25% accelerating in orders . Investors are underestimating Azure growth as use cases explode. Look I think the stock has a "6" in front of it. This is a table pounder. Investors give MSFT no respect. Its almost like the Rodney Dangerfield of software... Investors are underestimating the company's growth in 2026. That's really the call. The Bears won't win.... I get the concerns but the reality is that demand to supply is 12-1 as it relates to the hyperscaler buildout. As it looks to growth, the Street is underestimating Microsoft's numbers by as much as 20%".

From last week (Dan Ives, again, on CNBC):

"Microsoft is going to be a clear EPS standout next week." (Yes it was, Dan!)

But we do know that sentiment is getting a wee bit frothy. I hesitate to use the word giddy only because the Investors’ Intelligence bulls moved up to 61.5%, which is their first foray over 60% in more than a year. Yet the Bull/Bear ratio only pushed up to 3.99. Am I being fussy? Probably. I have said that when we have 4 to 1 bulls to bears (a ratio over 4.0) we have gotten to giddy.

Late Wednesday Evening and Early Thursday Morning Trading

I am actively trading the market's growing volatility, opportunistically. (Note: I really don't recommend this sort of frenetic trading for home gamers — it is too hard and time consumptive! I also suspect most won't care to follow this sort of trading, though we do have a number of very active traders as subs).

When S&P futures slipped back to about -18 handles (around 7:05 PM last night) I bought (SPY) and (QQQ) to become delta-equivalent neutral against my short index calls:

* SPY $693.44

*QQQ $632.14

Now S&P futures are +20 handles.

I am back shorting the indices. I am accomplishing this by taking off some of the index longs put on at around 7:05 PM last night: