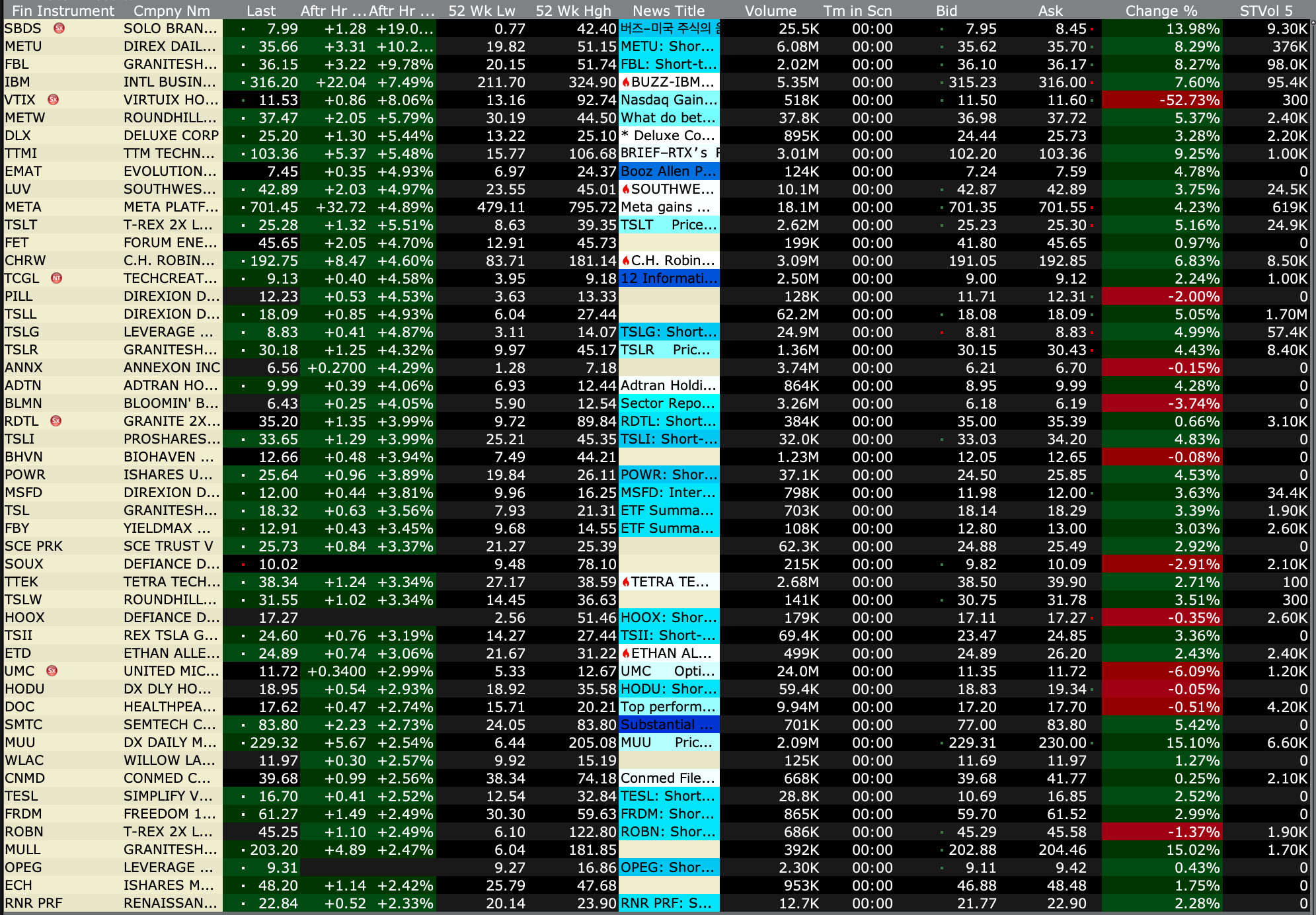

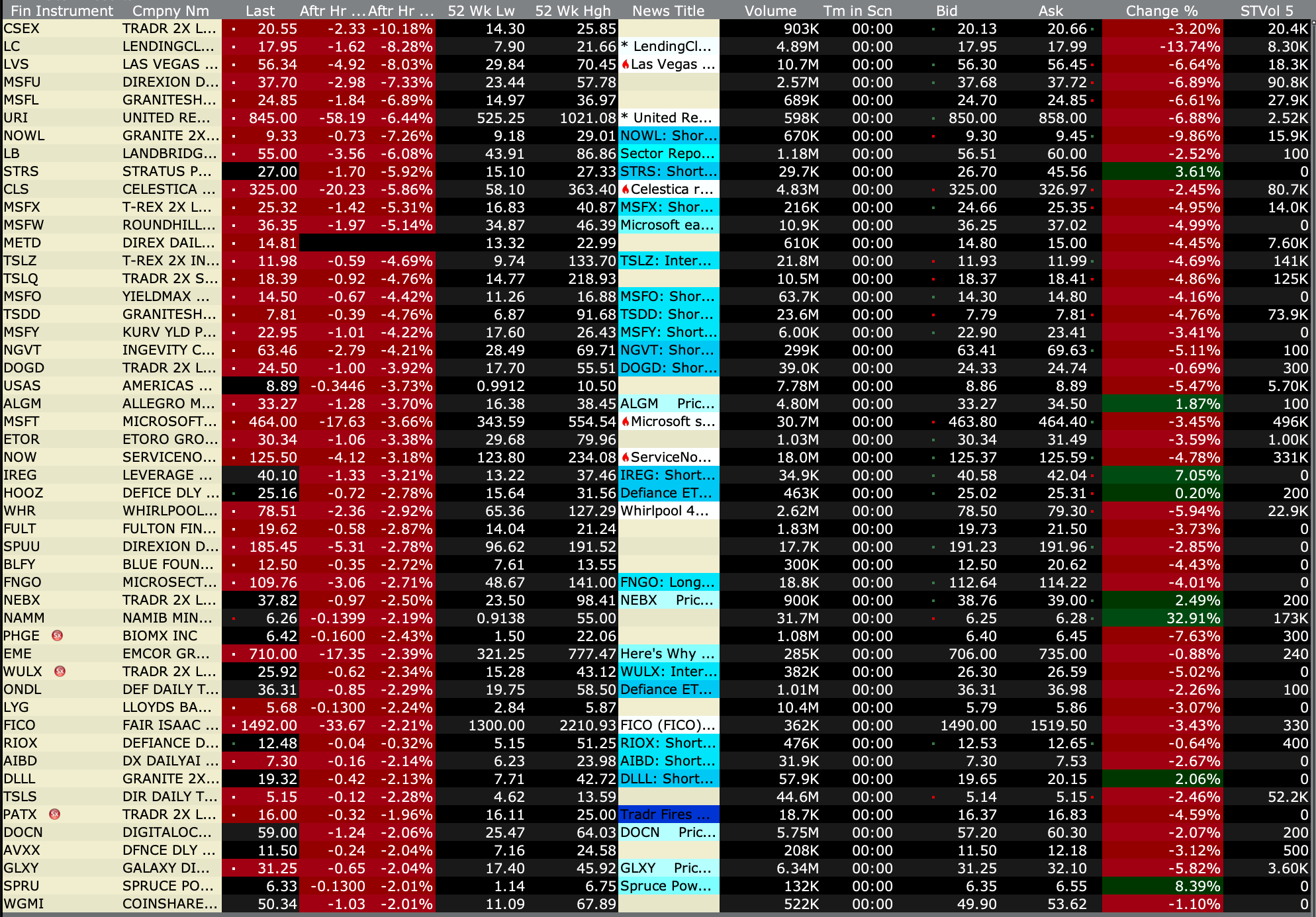

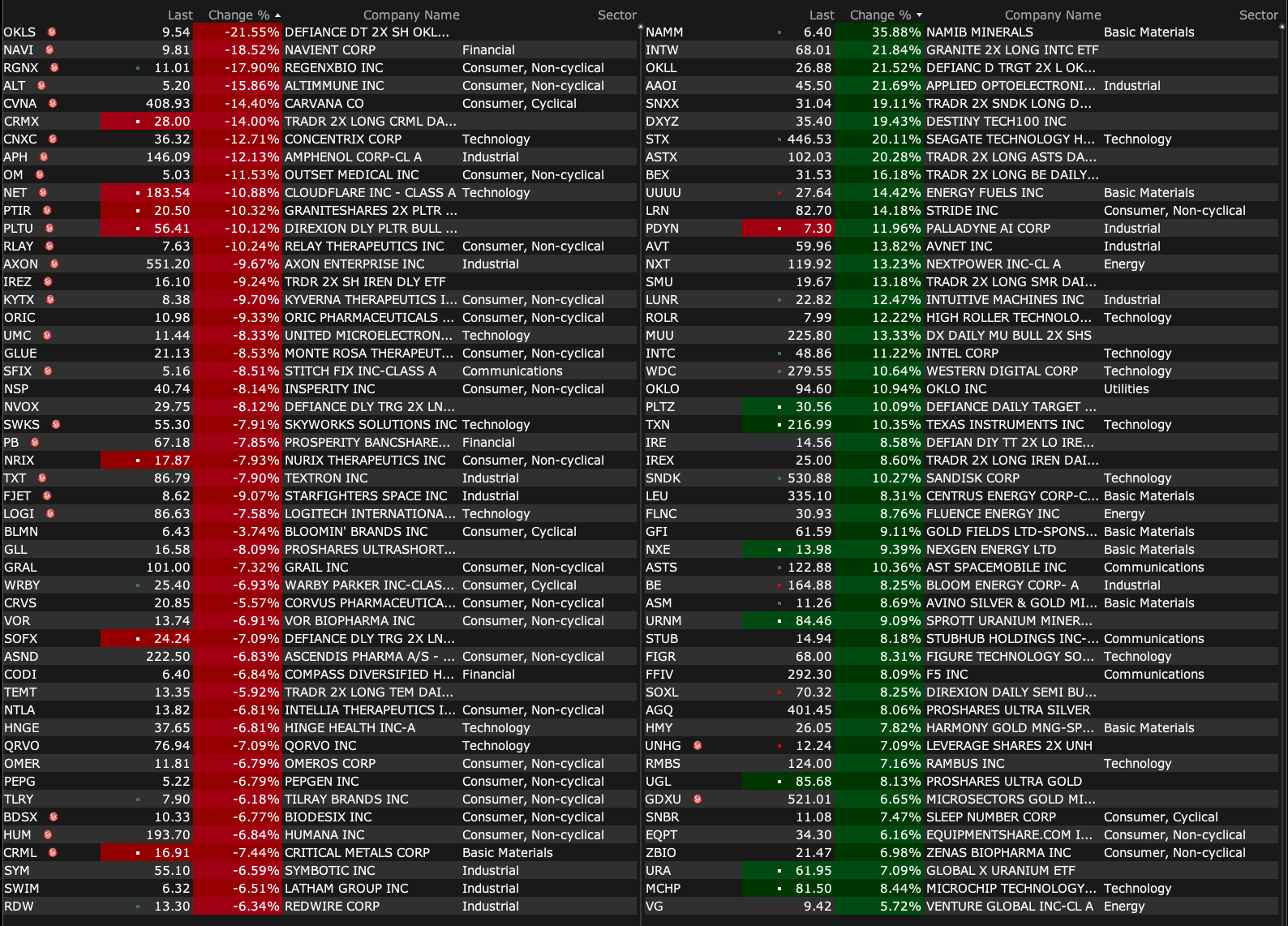

After-Hours Gainers and Decliners

As of 4:25 pm:

After-Hours % Gainers

After-Hours % Decliners

BY Doug Kass · Jan 28, 2026, 4:50 PM EST

As of 4:25 pm:

BY Doug Kass · Jan 28, 2026, 4:50 PM EST

BY Doug Kass · Jan 28, 2026, 4:37 PM EST

BY Doug Kass · Jan 28, 2026, 3:49 PM EST

BY Doug Kass · Jan 28, 2026, 3:34 PM EST

Wolf Street howls about the Fed's statement.

BY Doug Kass · Jan 28, 2026, 2:57 PM EST

From Peter Boockvar:

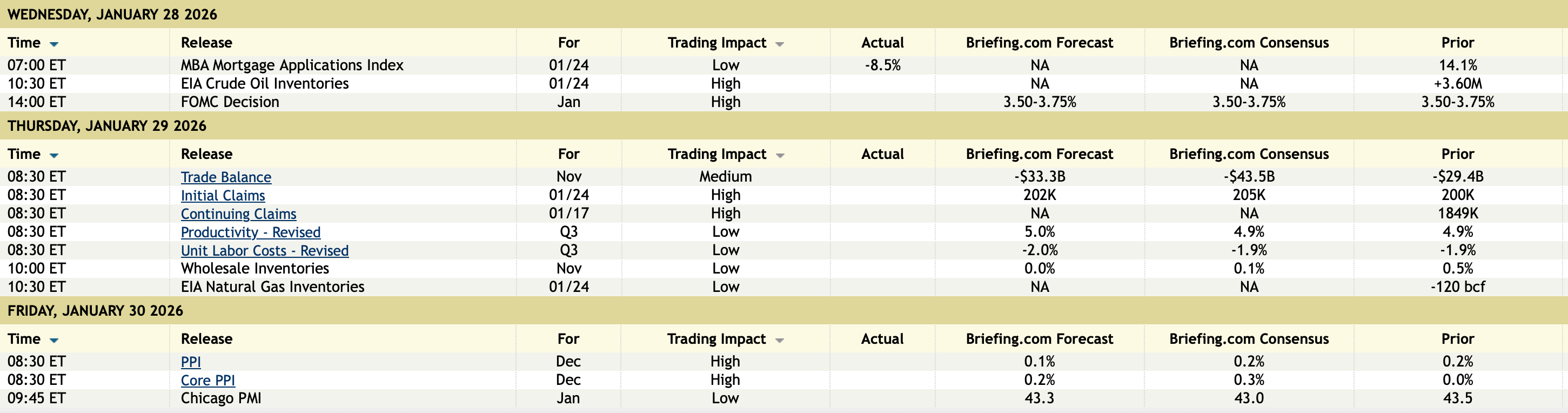

The FOMC upgraded its view on the US economy by saying that it “has been expanding a solid pace.” The December statement referred to growth as “moderate.” Also, on the labor market it said “the unemployment rate has shown some signs of stabilization” compared to “the unemployment rate has edged up through September.” Of course with more data in hand relative to the shutdown inhibited data access in December, consider this a more fresh view of their thinking.

The commentary on inflation remained about the same saying it “remains somewhat elevated.”

Voting for a cut not surprisingly was Stephen Miran and Chris Waller, each wanting 25 bps lower. Interesting that Miran didn’t vote for 50 bps.

Bottom line, in a way it doesn’t really matter what the statement says or what Powell thinks at his presser because we know there is limited time left with this regime. How then the next Fed Chair will vote and corral members along his line of thinking will be most interesting. That said, as outside of Waller and Miran, the rest of the voting committee seems very intent on sitting still right now.

I’ll argue again, unless the rate of inflation takes another leg down and/or the unemployment rate moves much higher from here, Jay Powell is done cutting interest rates at his final two meetings and his colleagues seem to agree at least for now.

The 2 yr, 10 yr and 30 yr yields are dead flat with where they were at 1:59pm est. The March meeting has just a 12% chance of a cut and the April meeting is priced at 32%. Through the end of the year, 45 bps more of cuts are priced in, thus 100% chance of one more and an 80% chance of an additional one thereafter with the first one most likely in June.

BY Doug Kass · Jan 28, 2026, 2:28 PM EST

So interesting:

Amazon axes 16,000 jobs as it pushes AI and efficiency

Amazon (AMZN) whacking more heads.

This follows a cut of 14K in October, the closure of its gaming unit and shutting down its Amazon-branded grocery stores and cashier-less stores, among other things.

We have seen similar stuff out of Microsoft (MSFT) and others.

Despite all the noise about Covid over-hiring (which was five years ago!) and AI-driven efficiency gains (which is all BS, in my view), the real reason is they all see the hit coming on the P&L from the AI investments and are now scrambling to get costs out elsewhere.

The whole thing is a black hole. All of the money going into all the wrong places.

BY Doug Kass · Jan 28, 2026, 2:15 PM EST

Financials are at day's lows.

I'm stepping up my shorting.

BY Doug Kass · Jan 28, 2026, 2:06 PM EST

BY Doug Kass · Jan 28, 2026, 1:13 PM EST

Here are today's things:

* I day traded a small-sized amount of indices ( (SPY) and (QQQ) ) for a profit.

* On the morning strength (+15 S&P handles), I added to my short index calls.

* Shorted more (JOET) at $43.06 and (GRNY) at $25.74.

* Covered some of my (REZI) short at $33.58.

* Halved my (AMZN) long at $246.58.

BY Doug Kass · Jan 28, 2026, 1:00 PM EST

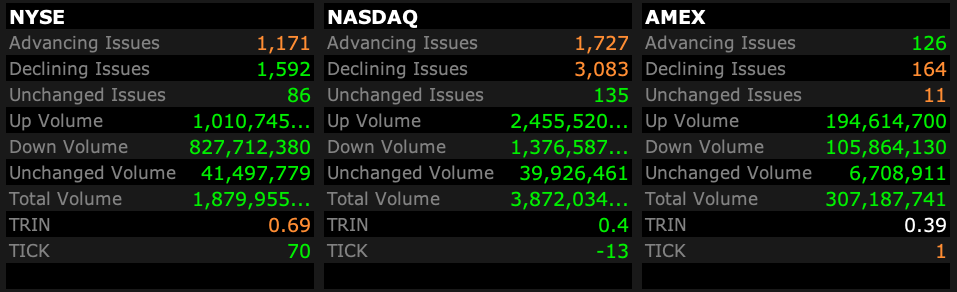

1. Yields up again, (TLT) at day's low, following yesterday's weakness

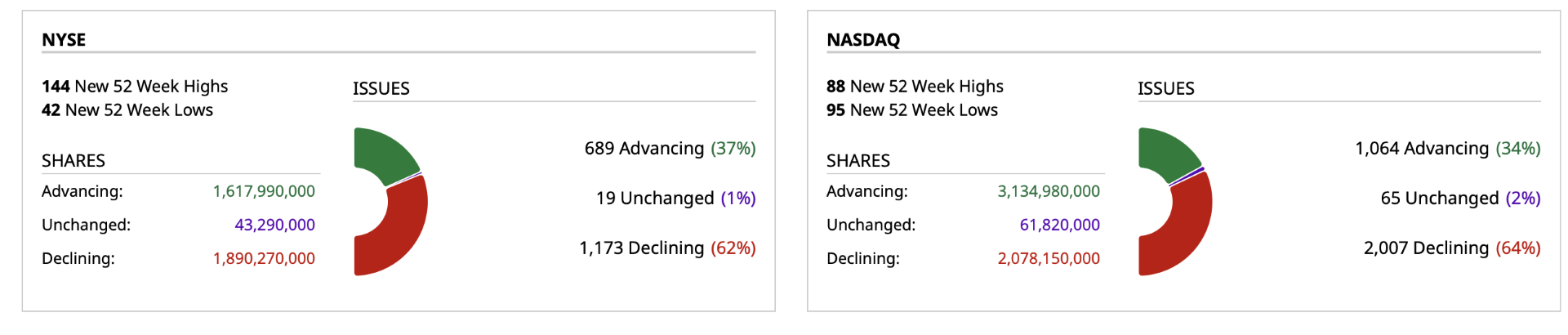

2. The broadening of the advance is now reversing — breadth on NYSE and Nasdaq continues to stink (and (IWM) lower on the day)

3. Financials also continuing recent weakness — (JPM) makes a new multi-week low

4. The magnitude of the precious metals advance continues apace today — is something broken?

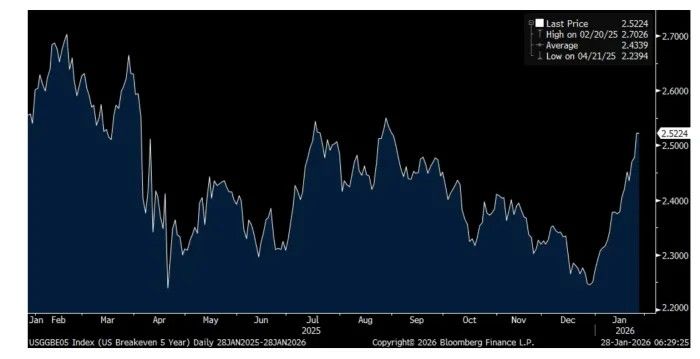

5. Inflation breakevens ripping:

5-Year Inflation Breakeven

BY Doug Kass · Jan 28, 2026, 12:45 PM EST

I'm adding to (JOET) and (GRNY) shorts.

BY Doug Kass · Jan 28, 2026, 12:29 PM EST

BY Doug Kass · Jan 28, 2026, 11:35 AM EST

BY Doug Kass · Jan 28, 2026, 11:15 AM EST

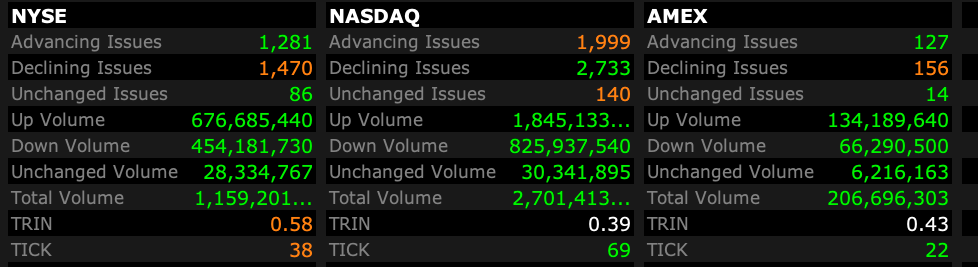

- NYSE volume 2% above its one-month average;

- Nasdaq volume 5% below its one-month average;

- VIX index: up 2.02% to 16.68

BY Doug Kass · Jan 28, 2026, 11:00 AM EST

I halved my Amazon (AMZN) long on this morning's strength.

BY Doug Kass · Jan 28, 2026, 10:40 AM EST

Kdog88

2 minutes ago

Dollar weakness is driving precious metals to the moon, and IMO propping up US stocks. Look out below IF the dollar makes a strong reversal. The big question: is the US dollar permanently impaired and is the death spiral just starting?Dougie….a newly minted 🤣 US penny for your thoughts?

Dougie Kass

STAFF

Just Now

I am lost.The factors I look at no longer work.I am thinking about Hare Krisha

BY Doug Kass · Jan 28, 2026, 10:10 AM EST

Moved to medium-sized short the indexes - on this morning's strength.

Ludacris Day?

BY Doug Kass · Jan 28, 2026, 9:52 AM EST

From Peter Boockvar:

I wonder if the FOMC will talk about the dollar index at a 4 yr low and many emerging market currencies rallying too. I wonder if they will discuss the ever rising price of gold as it is a monetary metal after all. I wonder too if they will mention what is going on with industrial material prices? Below is a 20 yr chart of the change in CPI and the CRB raw industrials index. I wonder if the sharp rise in inflation expectations in the TIPS market this year will be contemplated. The 2 yr inflation breakeven has gone from 2.32% to 2.71% over the past 4 weeks. The 5yr breakeven has gone from 2.25% to 2.52%. Will they discuss amongst themselves the sharp rise in JGB yields and what the potential global implications are flow wise?

There will be offsets too of course. The modest pace of hiring, why and what’s the cause. Rents should further decelerate this year but goods prices are curling higher (core goods prices in PPI up more than 3% y/o/y). Interesting times.

Balancing all of the above, I’ll argue again that unless the inflation rate takes another leg down and/or the unemployment rate takes another leg up, Jay Powell and Co are done raising rates and the next one we’ll get will wait until June with the new Fed Chair, assuming he/she has the votes.

CRB Raw Industrials index in orange/US CPI rate of change in white

2 yr Inflation Breakeven

5 yr Inflation Breakeven

What I find also interesting and please reflect any thoughts on this move is the downturn in leveraged loan prices this week. I mentioned the LSTA leveraged loan index on Monday and will do again today because there hasn’t been an uptick in the index since January 13th and it closed yesterday at the lowest level since May 2025.

LSTA Leveraged Loan Index

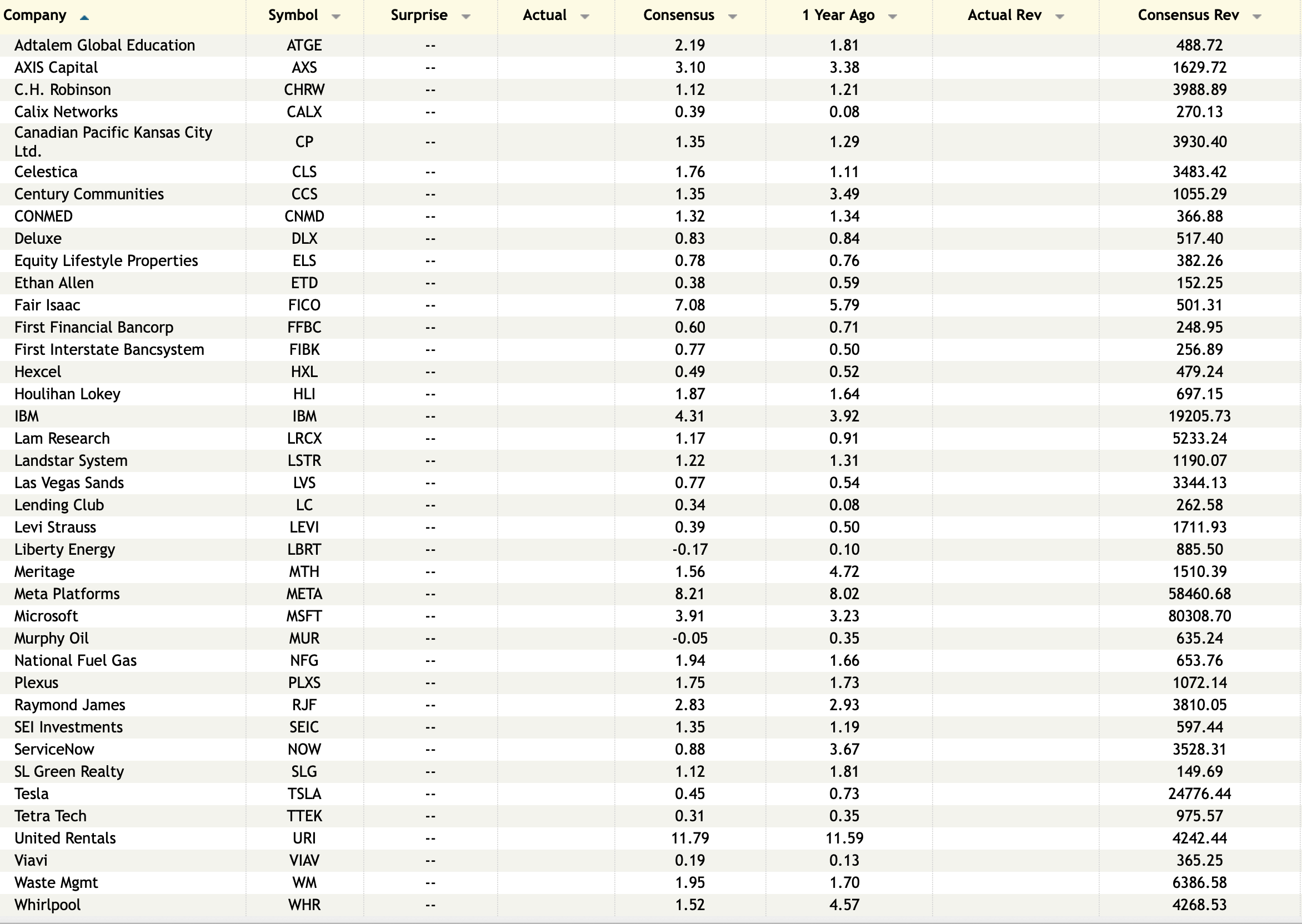

To some important earnings calls.

From Texas Instruments and whose stock is up about 9% pre-market:

“The overall semiconductor market recovery is continuing, and we are well positioned with inventory and capacity to meet immediate customer demand.”

By end market, “the industrial market was up high teens y/o/y, with recovery continuing broadly across sectors and was down mid single digits sequentially. The automotive market increased upper single digits y/o/y and was down low single digits sequentially. Data center grew around 70% y/o/y and mid single digits sequentially. Personal electronics declined upper teens y/o/y and mid teens sequentially. Lastly, communications equipment declined low single digits y/o/y and mid teens sequentially.”

More on the lift in some sectors, “we are seeing a little bit of a pickup in orders, including in industrial, and I can’t tell you why. We’ll have to see how it plays out. But we have seen some noise in the last several months on some issues regarding a certain supplier, and sometimes we all know about the memory shortages. So I don’t know what makes the customers order more. We’ll just have to look and see. I do want to remind us all, that earlier in 2025, I would say the first half of ‘25, we saw a pickup of industrial and then it kind of comes down. We will want to see how sustainable this wake up in orders is.”

From UPS which was little changed yesterday after an initial jump:

“In 2025, we operated through a very dynamic macro-environment, including significant change in global trade policies and increasing geopolitical concerns.” They certainly did.

“In 2026, growth in the US small package market excluding Amazon is expected to be up low single digits. Outside the US, export volume growth is expected to be subdued, partly due to the tough comparisons coming from the boost of tariff front running in 2025.”

For the international segment, “We expect the dynamic environment we experienced in 2025 will continue in 2026, primarily due to the tariff and de minimis policy changes that will continue to drive changes in trade lane mix.”

From PPG Industries, the paint and coatings company that goes on a lot of stuff:

“Results for our Global Architectural Coatings segment improved sequentially each quarter of 2025, with organic sales growth of 2% in the fourth quarter as project related sales in Mexico recovered sequentially and retail sales were strong. Overall demand in Europe remained mixed.”

“Performance coatings segment organic sales grew 3% in the quarter as strong results in aerospace coatings and protective and marine coatings were partially offset by lower automotive refinish coatings demand, reflecting customer order patterns that were weighted toward the first half of the year.”

“Industrial coatings segment organic sales grew 4% y/o/y due to share gains.”

They said their full 2026 guidance “is based on current global economic activity, and FX rates, ongoing soft global industrial production, and mixed demand across the various regions where we operate.”

From GM which had a big day, up 9%:

“In the United States, we achieved our highest full year market share in a decade. In fact, 2025 was our fourth consecutive year of market share growth, and we continue to deliver with low inventory, low incentives, and strong pricing.”

With the tariff impact, the gross impact in 2025 was $3.1 billion. “For the full year, we were able to offset more than 40% of these gross tariff costs through a combination of go-to-market actions, footprint adjustments, and cost reduction initiatives.” Tariffs though will still cost them in 2026. “For Q1, we expect the gross tariff impact to be in the $750 million to $1 billion range.” They look again to offset about 40% of that.

“For the industry, we expect total US SAAR to be in the low 16 million unit range for the year.” I’ll add that it is still below the 17mm+ pre Covid.

From LVMH, down 7% in Paris today:

“Organic growth slightly negative on the year, but positive in the second half.”

“The results of the group are solid in a rather challenging, disrupted climate, economically, from the geopolitical standpoint, but we’ve managed to get through this period. 2026 won’t be simple either, but one thing at a time.”

“What can we say briefly about 2026? The outlook? I always say that in our businesses I am optimistic in the medium term. But short term, it’s very difficult to provide a serious forecast. So many events and the pace of decisions taken left and right in the various countries. It’s extremely difficult to control all these geo economic impacts on our companies. One thing I’m sure of is that the desire for high quality products goes hand in hand with growing living standards in the world.”

“Cognac and indeed spirits in general were down, and that is because of the specific circumstances in the US.”

“Fashion & leather goods enjoyed a significant improvement starting in Q3, driven by local customers and a resumption of growth in Asia, a less strong basis of comparison for Japan and some areas of improvement.”

“On watches & jewelry, there was a significant acceleration in H2.”

“Perfumes & cosmetics were stable with a very sustained innovation policy.”

From American Airlines that traded down 7% yesterday:

They mentioned the negative impact of the government shutdown on business in November and December but “following softer than expected bookings late in the fourth quarter, bookings strengthened meaningfully in January.”

“Premium continued to outperform main cabin throughout the quarter, a trend that has remained consistent all year, underscoring the strength of the premium customer and demand for the premium products we offer.”

“Our international entities performed in line with the guidance we provided in October.” Europe was strong, Latin America soft and while Pacific was down a touch y/o/y, it “showed sequential improvement from the third quarter.”

From Sysco, the food distributor and whose stock popped by 11%:

“Sysco’s 140 bps of local case growth improvement was delivered in an environment where traffic to restaurants per black box, declined more than 200 bps y/o/y and a similar decline q/o/q.”

“The declining foot traffic to restaurants per black box has negatively impacted our national chain restaurant customers, as can be seen in our results, as volume with these customers was down y/o/y.”

To some economic data, mortgage applications fell 8.5% all because of a 16% drop in refi’s w/o/w with the uptick in mortgage rates. Purchases were flat w/o/w.

Australia reported its December CPI and it rose 3.8%, up from 3.4% in November and 2 tenths above expectations. The hawkish RBA Governor Bullock will not be cutting rates again anytime soon and maybe she even hikes. Yields though fell in Australia following a drop in JGB yields after the Japanese 40 yr bond auction went pretty well. At least one day of calm in their markets.

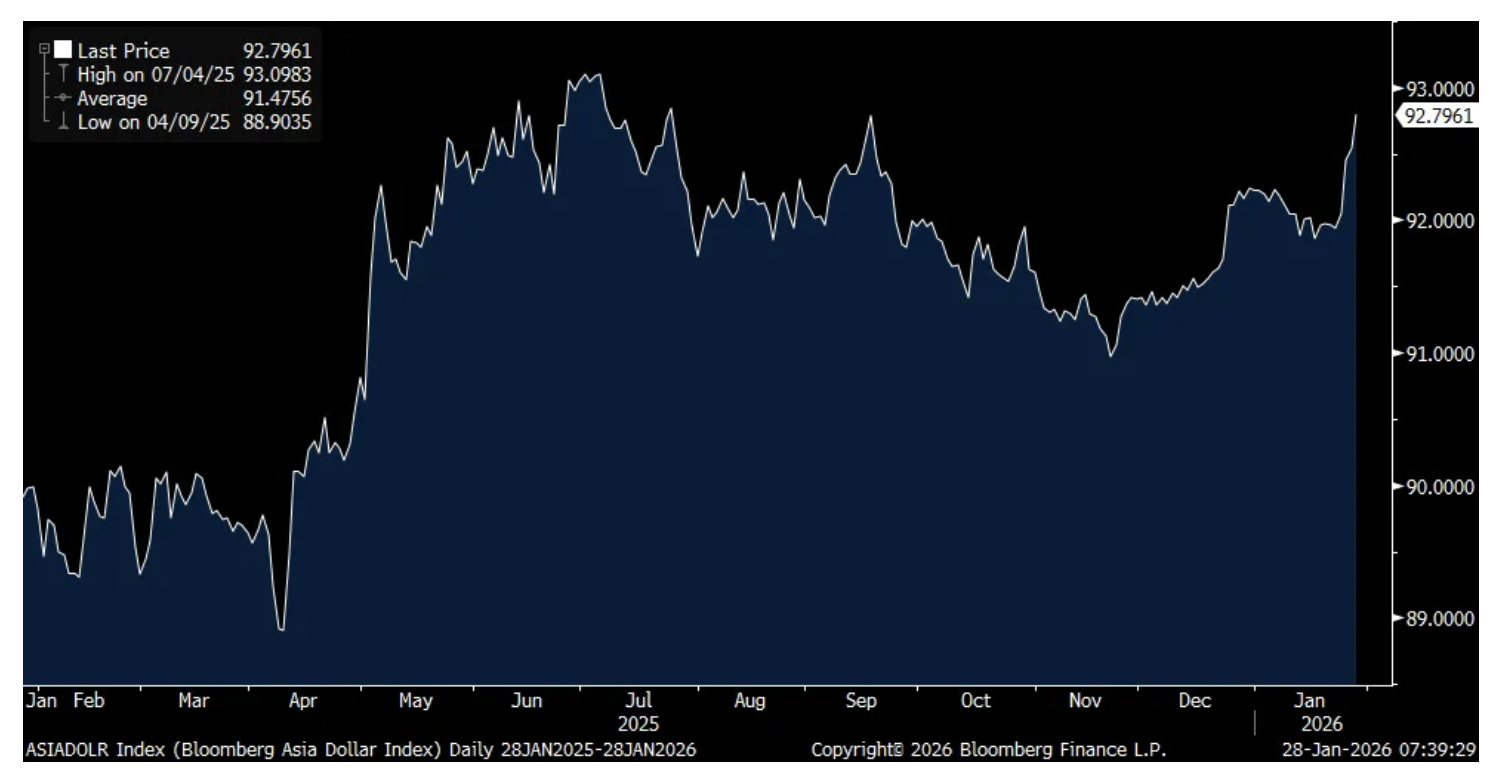

While down slightly today, I will argue again that the rally in the Chinese yuan this year to the highest level since May 2023 is a really big deal and gives cover to other Asian currencies to rally, especially the Japanese yen. Today the Bloomberg Asia Dollar index is rallying to the best level since last July.

Asia Dollar Bloomberg Spot Index

BY Doug Kass · Jan 28, 2026, 9:50 AM EST

(Though not a timing tool), for the first time since the 1997-2000 dot.com bubble the Dr. Shiller's (I have lectured in his Yale University class in the past) Cyclically Adjusted Price to Earnings Ratio (Cyclically adjusted price-to-earnings ratio) has hit 41.00:

BY Doug Kass · Jan 28, 2026, 9:35 AM EST

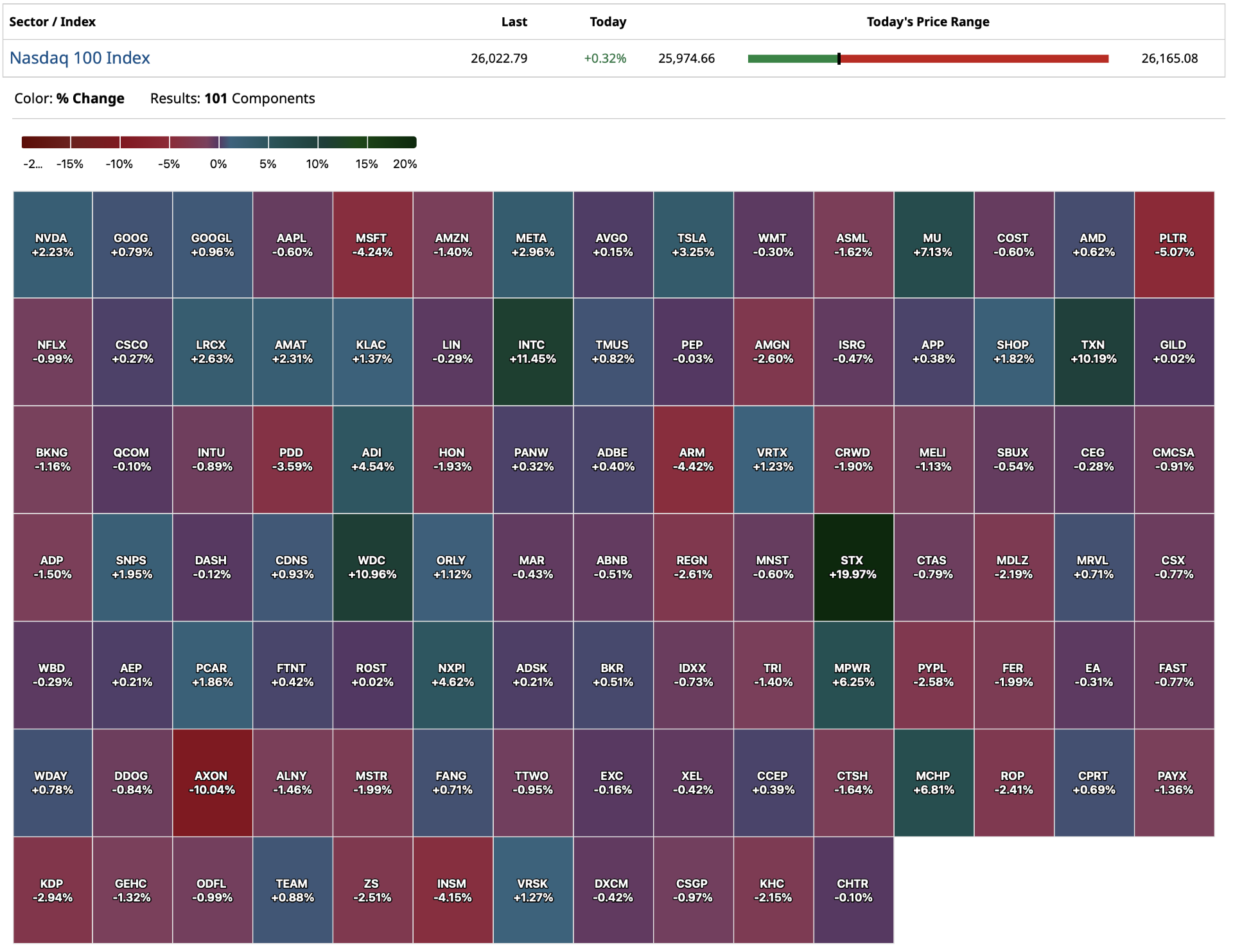

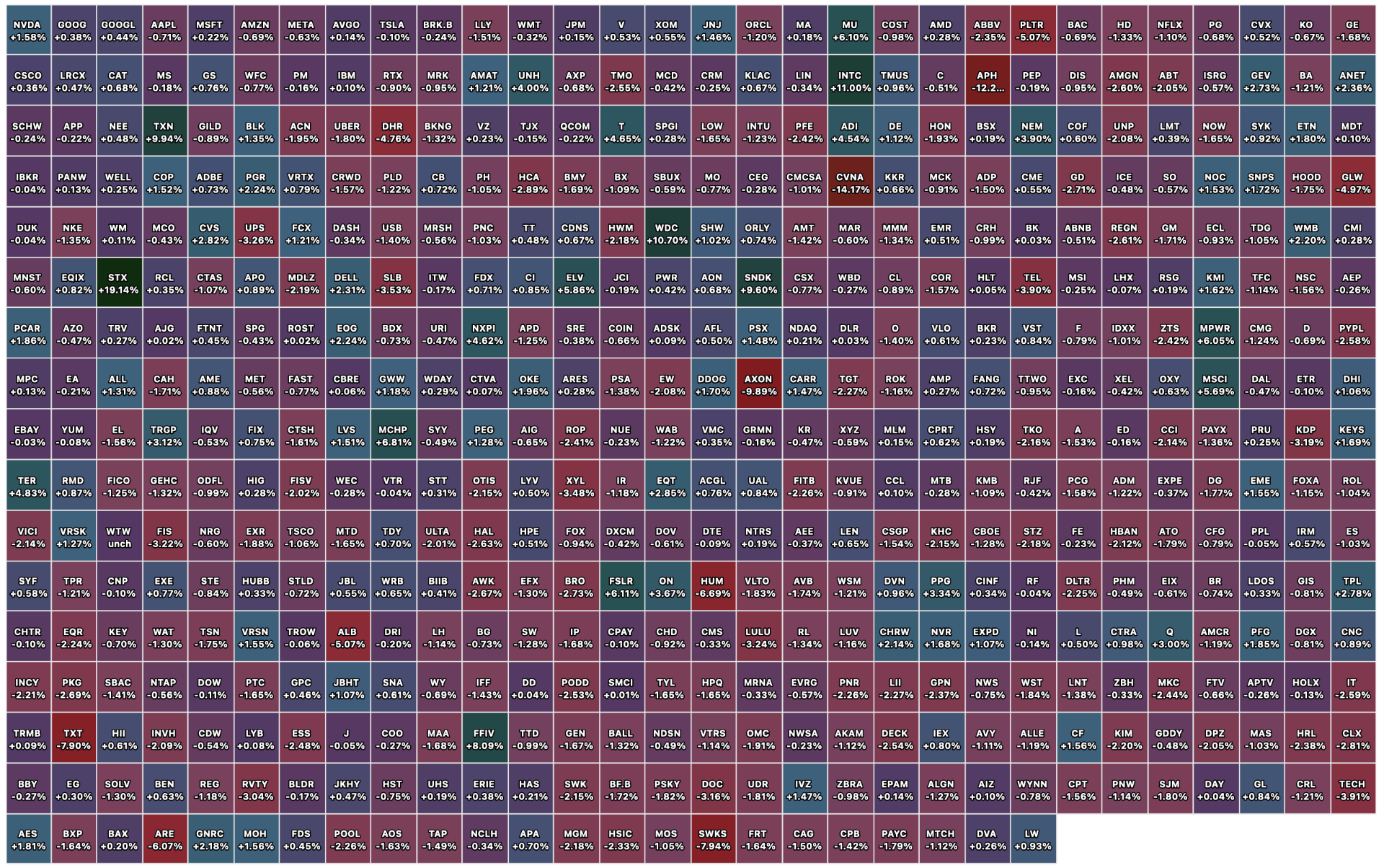

-PDYN +51% (awarded contract of undisclosed amount by the Air Force Research Laboratory)

-LRN +23% (earnings, guidance)

-STEL +14% (to be acquired by Prosperity Bancshares in $2.0B cash-stock deal; earnings)

-AI +13% (said to consider merger with Automation Anywhere)

-NXT +11% (earnings, guidance)

-STX +9.5% (earnings, guidance)

-WIX +9.3% (authorizes 2-year, $2B share repurchase program)

-NVMI +8.1% (momentum)

-ATEX +7.8% (FCC Chairman Carr announces Vote to Expand 900 MHz Broadband to 10 MHz scheduled for Wednesday, February 18, 2026)

-SBUX +6.8% (earnings, guidance)

-TXN +6.7% (earnings, guidance)

-EDU +6.5% (earnings, guidance)

-EAT +6.0% (earnings, guidance)

-ASML +5.0% (earnings, guidance)

-CRCL +3.6% (Mizuho Securities Raised CRCL to Neutral from Underperform, price target: $77 from $70)

-T +2.7% (earnings, guidance)

-ALHC +2.1% (positive mention on CNBC)

-RGNX -34% (US FDA placed a clinical hold on its investigational gene therapy, RGX-111 for treatment of MPS I, also known as Hurler syndrome)

-APH -12% (earnings, guidance)

-ENVB -12% (files to sell 328K shares at $4.41/shr in $1.5M registered direct offering)

-QRVO -9.8% (earnings, guidance)

-ALT -8.6% (prices 17.0M shares in direct offering for gross proceeds $75M)

-BMI -8.4% (earnings, guidance)

-ELV -6.2% (earnings, guidance)

-OTIS -5.8% (earnings, guidance)

-TEVA -4.4% (earnings, guidance)

-TXT -3.5% (earnings, guidance)

-DHR -3.0% (earnings, guidance)

-GLW -3.0% (earnings, guidance)

-VFC -2.4% (earnings, guidance)

-GEV -2.2% (earnings, guidance)

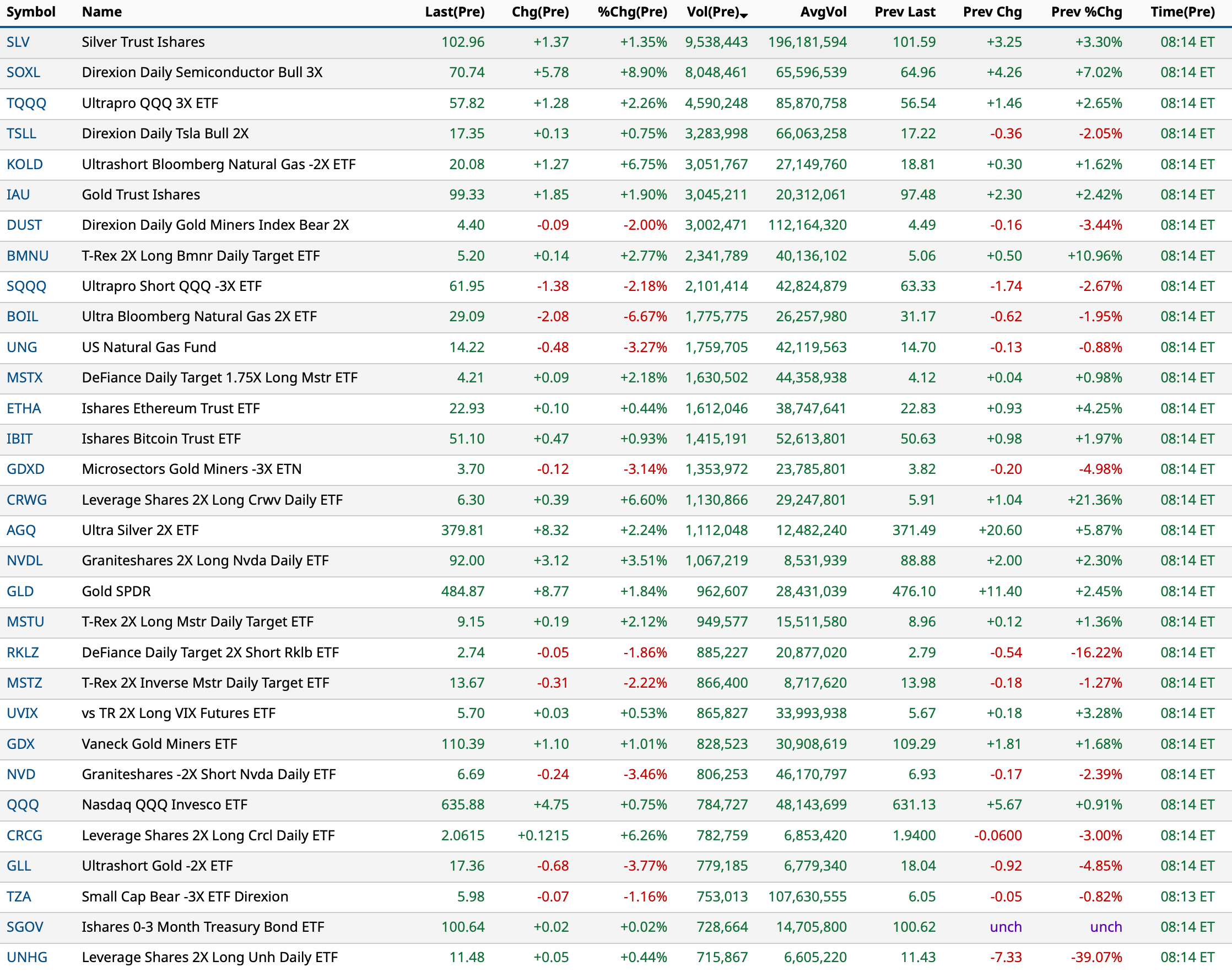

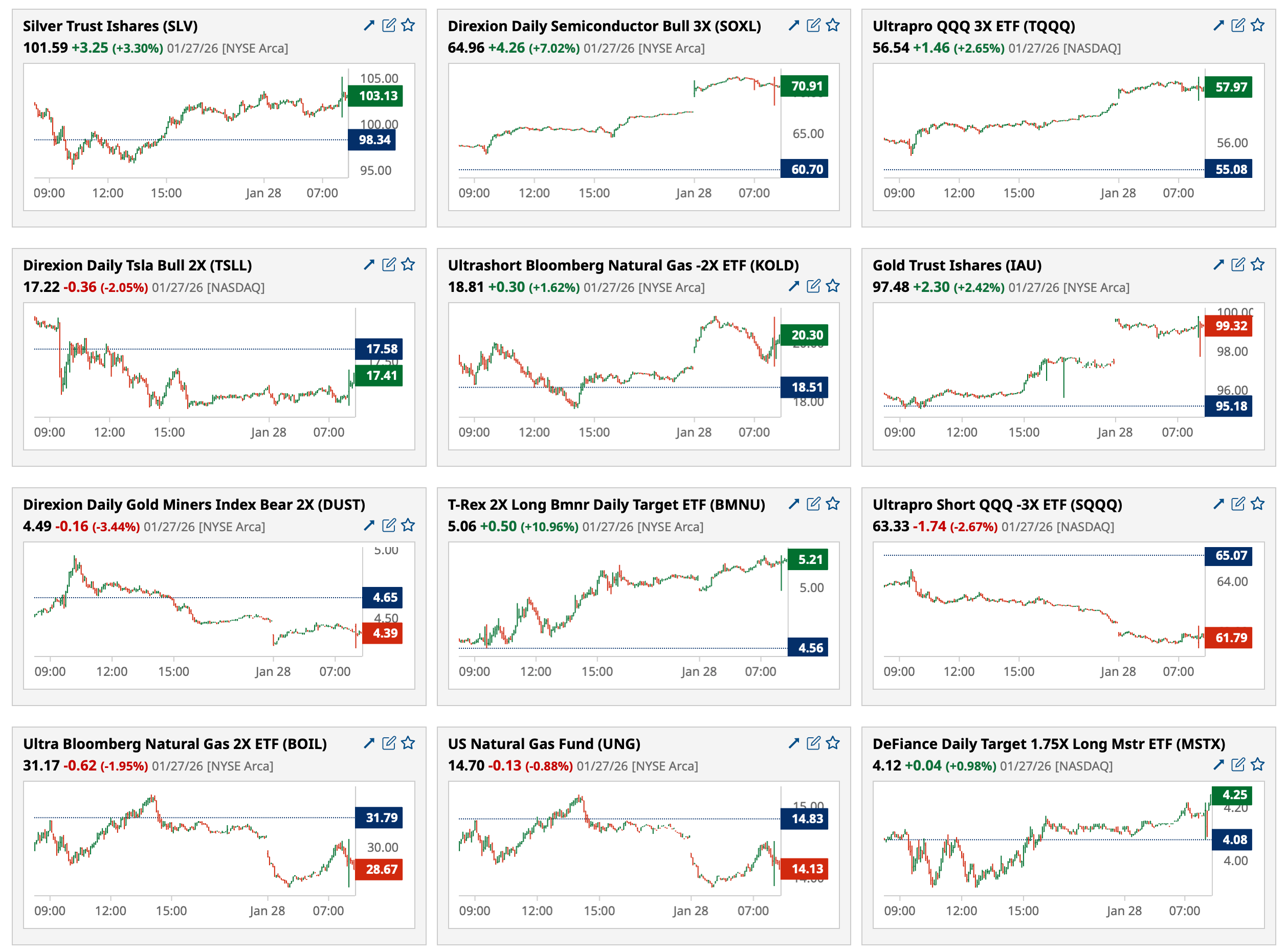

BY Doug Kass · Jan 28, 2026, 9:09 AM EST

BY Doug Kass · Jan 28, 2026, 9:00 AM EST

Charts from 8:14 a.m.

BY Doug Kass · Jan 28, 2026, 8:52 AM EST

BY Doug Kass · Jan 28, 2026, 8:42 AM EST

11:30 a.m.: Treasury hosts a $30B 2-Year FRN Auction;

11:30 a.m.: Treasury hosts a $69B 17-Week Bill Auction

BY Doug Kass · Jan 28, 2026, 8:25 AM EST

It seems that everyone sees everything as positive these days.

Here I respond to Jim Cramer's constructive take of the U.S. dollar:

BY Doug Kass · Jan 28, 2026, 7:40 AM EST

BY Doug Kass · Jan 28, 2026, 7:30 AM EST

BY Doug Kass · Jan 28, 2026, 7:20 AM EST

From JPMorgan (check out pro/con discussion of AI below):

US: Futs are rallying, led by Tech as overnight earnings (ASML, SK Hynix, STX, TXN) boost the group and help fuel the AI trade, perhaps pausing the broadening theme. Pre-mkt, Mag7 / Semis are bid led by AMD (+2.3%), AVGO (+1.4%), and NVDA (+1.6%). Cyclicals are leading Defensives as Fins/Indu/Mats outperform and Staples lag. Bond yields and USD are flat, leading to a muted (based on recent price action) response in cmdtys with gold +1.7% and silver +0.4% as the Energy complex is under pressure (natgas -8%) with Ags maintaining a bid. Today’s macro focus is on the Fed release with the market looking to see if the Fed identifies growth or inflation as the biggest risk but with no moves expected and 3x Mag7 earnings releases, Fed shaping up to be a non-event.

and...

· AI, CLIENT CONVO – increasingly, we are having conversations about the efficacy of AI and whether AI can deliver value in FY26. This discussion had multiple facets:

o Is cost-cutting enough to drive ROI? AI Bulls likely say Yes whereas AI Bears point to cost cutting being the equivalent of being long a put option. In both cases, people agree that we have yet to see meaningful revenue generation or innovation driven from AI. From a theoretical valuation perspective, while AI could expand margins via cost-cutting, if a company went with zero humans and is not growing revenue while it is taking its variable costs asymptotically to zero how much would you pay for that company?

o Does the Anthropic / Accenture deal give you more or less confidence that positive ROI gains are imminent? AI Bulls argued that this accelerates adoption since AI tools will advanced more quickly than companies are able to utilize. AI Bears will say that if a consulting firm has to tell you the value then there is limited value.

o Do we see investors begin to punish companies that “overspend” on AI? If yes, are we at-risk a capex rebalance? AI Bulls will say that there is a very long runway as we see the world build infrastructure that will drive value for the balance of the century. AI Bears argue that reactions to earnings releases in 2026 will begin to reflect a reality that C-suites of public companies need to figure out a revenue-generative use for AI tools.

o AI / AI Tools vs. AI Infrastructure – Both? A less flippant answer is that it makes sense to diversify, and we continue to see client interest in ex-US AI plays which is driving macro interest in China Tech, Korea, and Taiwan. US Mkt Intel likes a combination of Mag7 (JP1BMAG7 Index), Core AI (JPAICORE Index), AI Data Centers / Powers (JP11DCEN Index), and TMT-focused AI (JPAITMT Index).

o Is the productivity gain, alone, worth buying more AI names? AI Bulls will argue that the uptick in productivity will rival that witnesses in the 1990s which should keep US GDP above-trend into the 2030s. AI Bears will point to the potential offset that using more AI reduces brain activity and could increase productivity at the cost of intelligence / innovation, per an MIT study.

BY Doug Kass · Jan 28, 2026, 7:10 AM EST

BY Doug Kass · Jan 28, 2026, 7:00 AM EST

Bonus - Here are some great links:

This Is Not What a Healthy Bull Market Looks Like

3 Silver Charts You Have Not Seen

The Bears Need To Do This ASAP

BY Doug Kass · Jan 28, 2026, 6:45 AM EST

BY Doug Kass · Jan 28, 2026, 6:35 AM EST

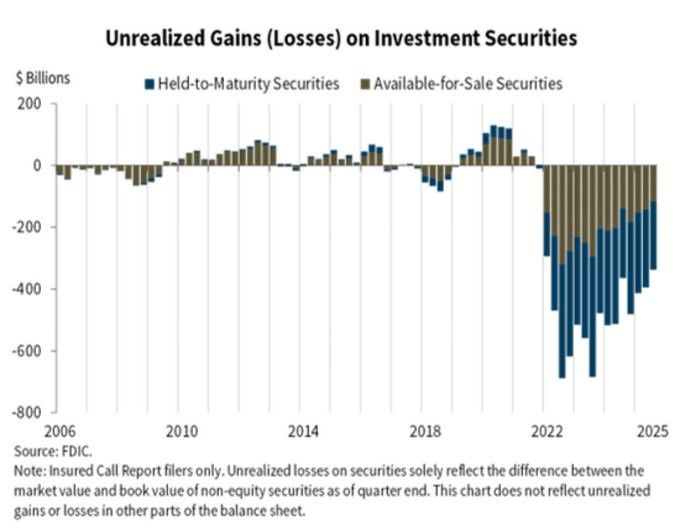

Accumulated bank securities' (unrealized) losses of nearly $340 billion:

I continue to avoid financials.

BY Doug Kass · Jan 28, 2026, 6:25 AM EST

From Quoth The Raven:

"The End Of The Monetary Road": Larry Lepard On Gold, Silver & Bitcoin

BY Doug Kass · Jan 28, 2026, 6:15 AM EST

Chart of the Day

BY Doug Kass · Jan 28, 2026, 6:05 AM EST

BY Doug Kass · Jan 28, 2026, 5:55 AM EST

The S&P Short Range Oscillator stands at 2.18% vs. 2.26% — still overbought.

BY Doug Kass · Jan 28, 2026, 5:45 AM EST