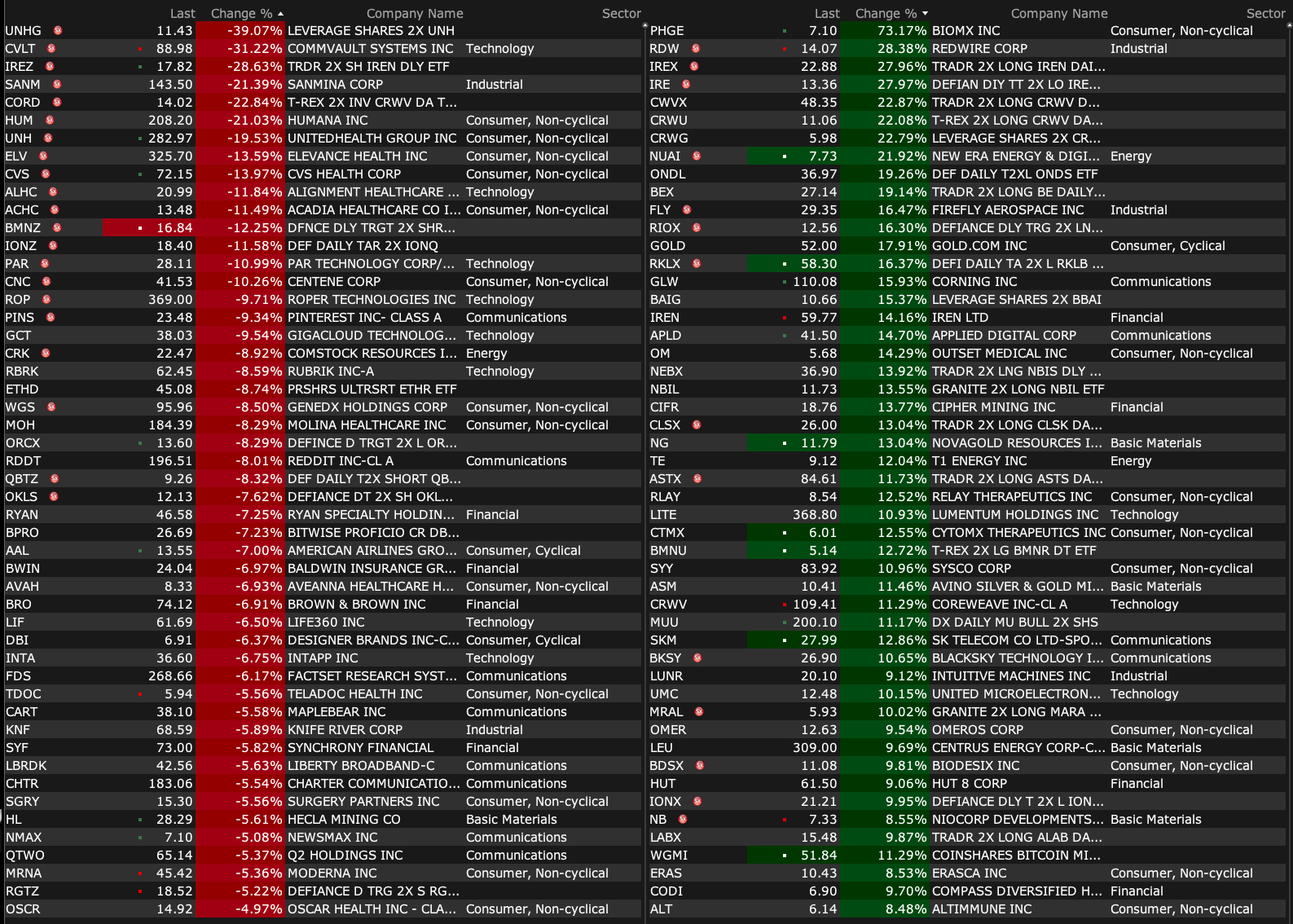

After-Hours Gainers and Decliners

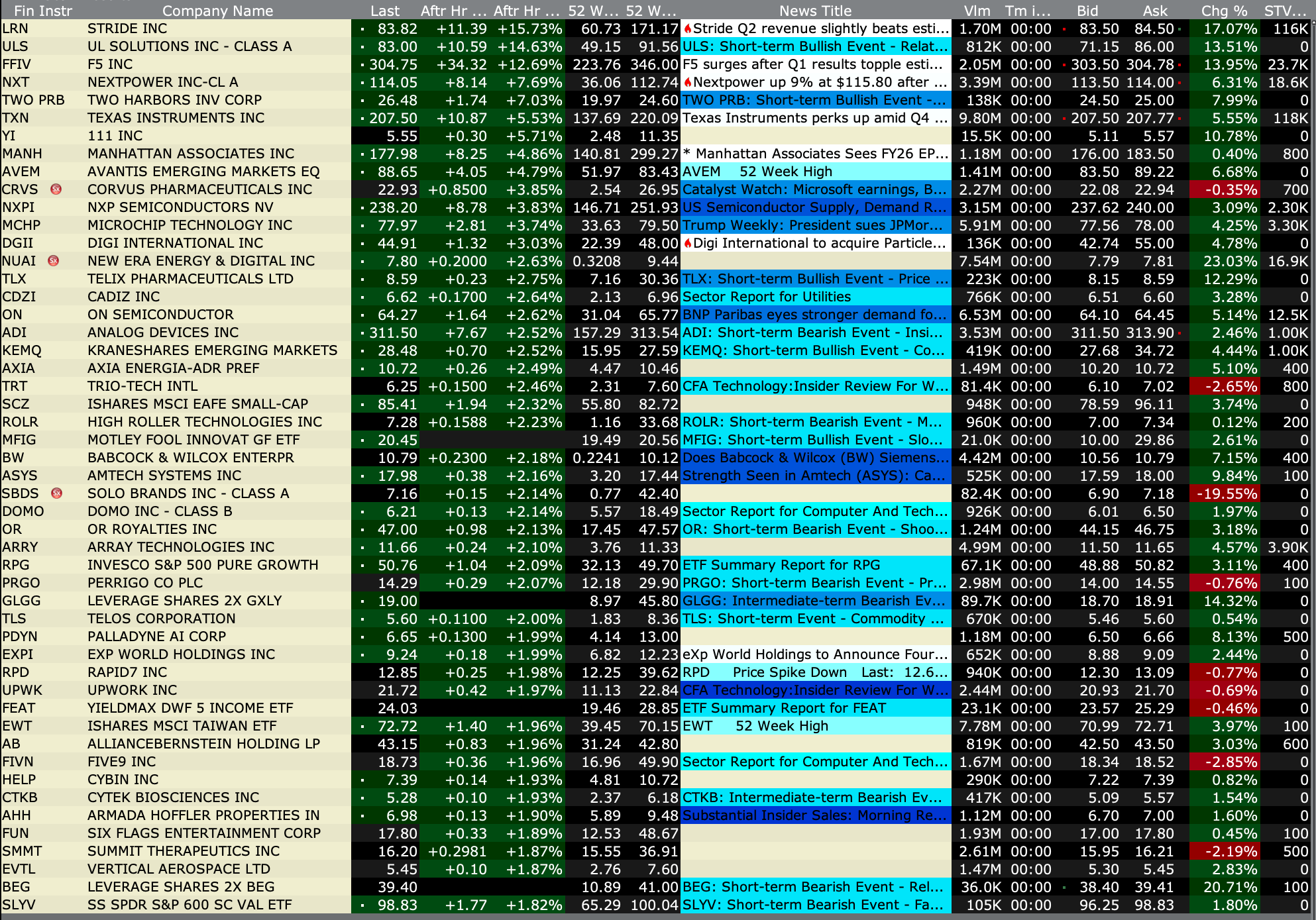

After-Hours % Gainers

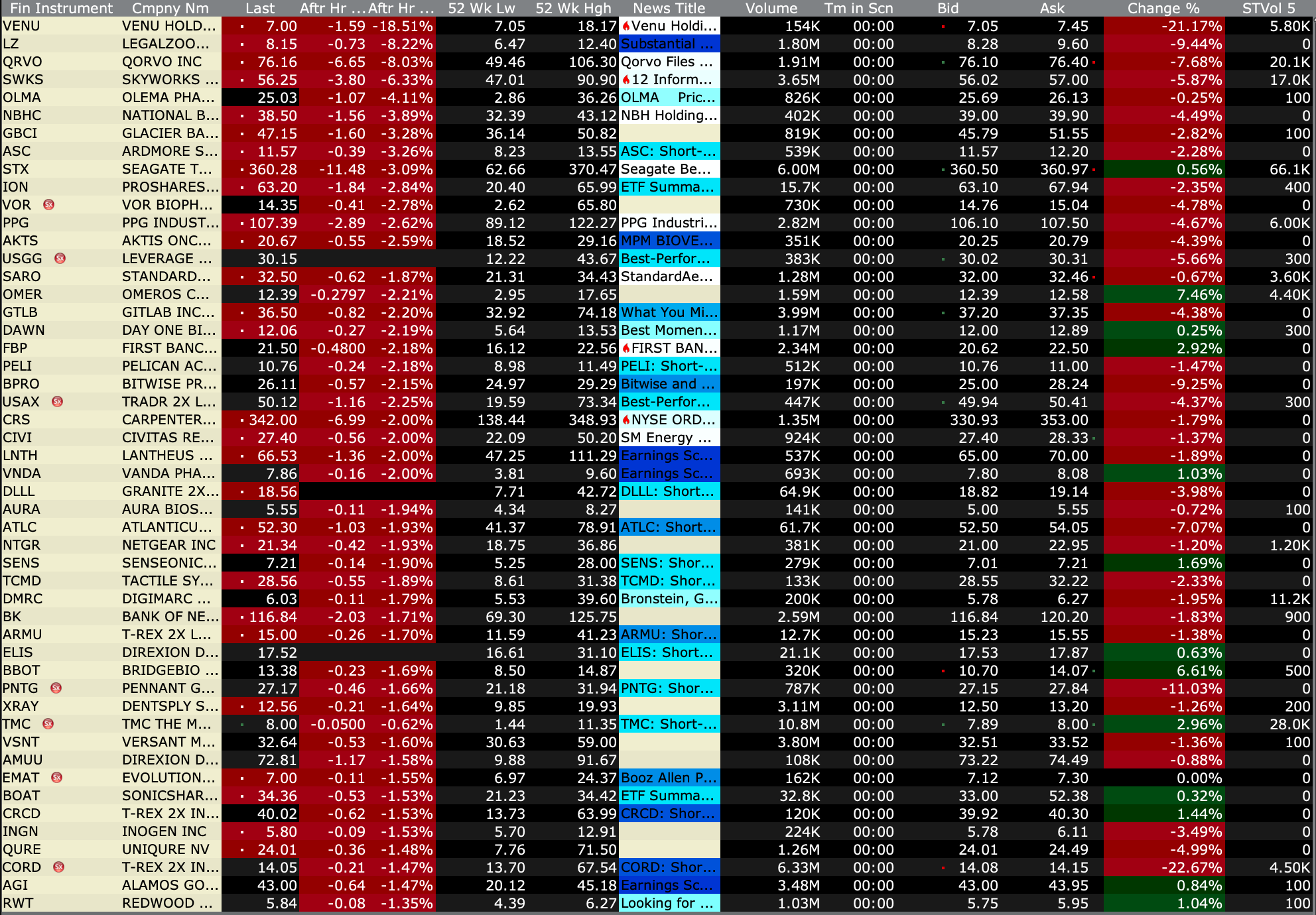

After-Hours % Decliners

BY Doug Kass · Jan 27, 2026, 4:40 PM EST

BY Doug Kass · Jan 27, 2026, 4:40 PM EST

- NYSE volume 8% above its one-month average;

- NASDAQ volume 3% below its one-month average;

- VIX index: up 0.99% to 16.31

BY Doug Kass · Jan 27, 2026, 4:29 PM EST

Thanks for reading my Diary today.

I am leaving early to listen to a tribute to The Grateful Dead's Bob Weir.

Enjoy the evening.

Be safe.

BY Doug Kass · Jan 27, 2026, 3:51 PM EST

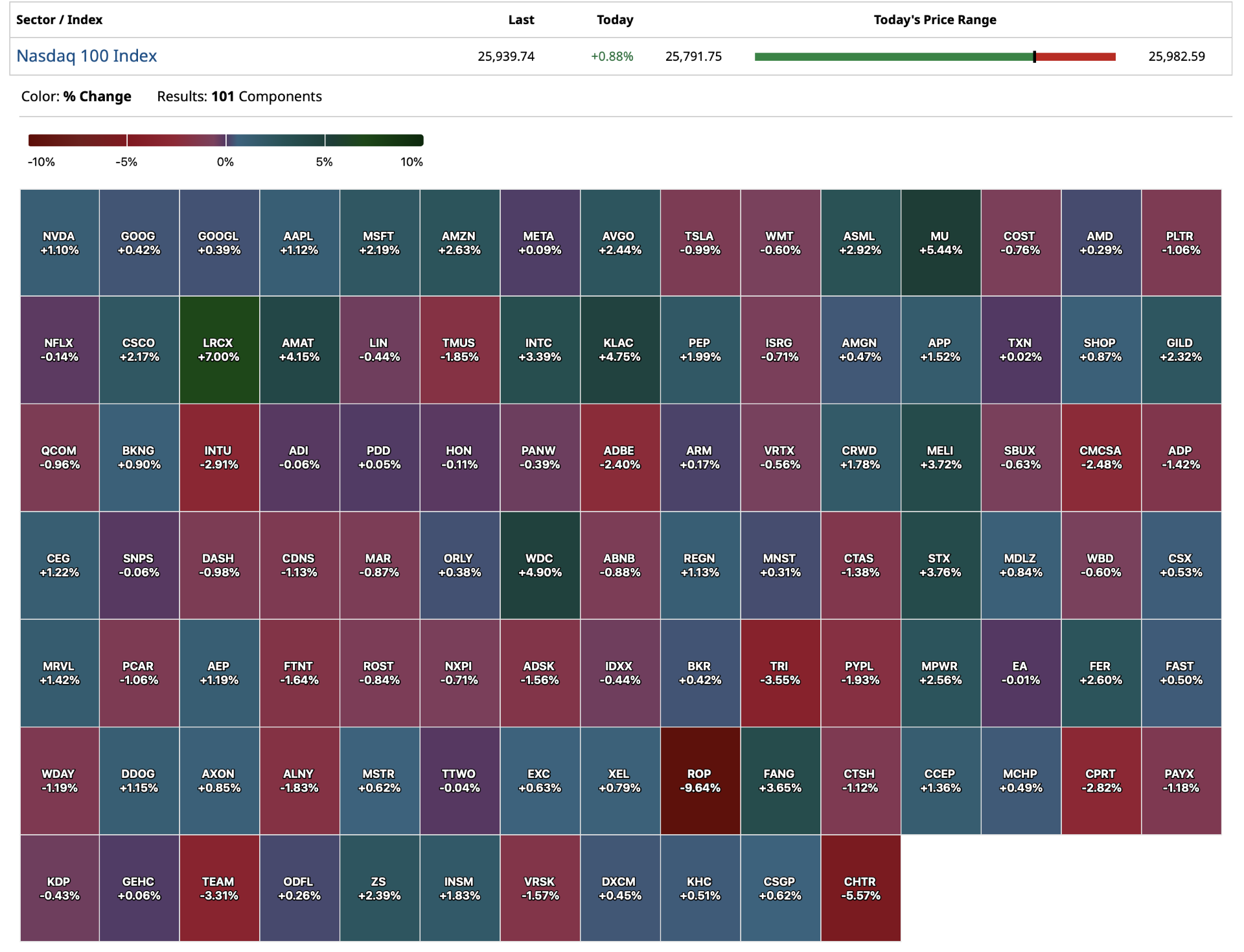

The chart of the day — Micron (MU) :

BY Doug Kass · Jan 27, 2026, 3:46 PM EST

and...

To put how unimportant the UnitedHealth (UNH) purchase was for Berkshire Hathaway — at $1.5 billion the UNH holdings represent the conglomerate's nineteenth largest position!

Warren Buffett Portfolio 2025 & Berkshire Hathaway Holdings

Position: Long UNH (S)

By Doug Kass Aug 15, 2025 1:28 PM EDT

BY Doug Kass · Jan 27, 2026, 3:28 PM EST

BY Doug Kass · Jan 27, 2026, 2:15 PM EST

Jeff G

Interesting info on the ground. All 3 of the manufacturing plants in the Company I work for are effectively shut down due to power prices (Illinois, Maryland, Texas). Either (or all 3):

Other area manufacturing are in the same boat - everywhere. Will have to hit 1Q2026 GDP (ex-power generators), possible shortages of good, inflation, etc. Surprised there isn't more talk about this (I guess keeping track of events in a small corner of Minneapolis is more important....)

BY Doug Kass · Jan 27, 2026, 1:55 PM EST

From Peter Boockvar:

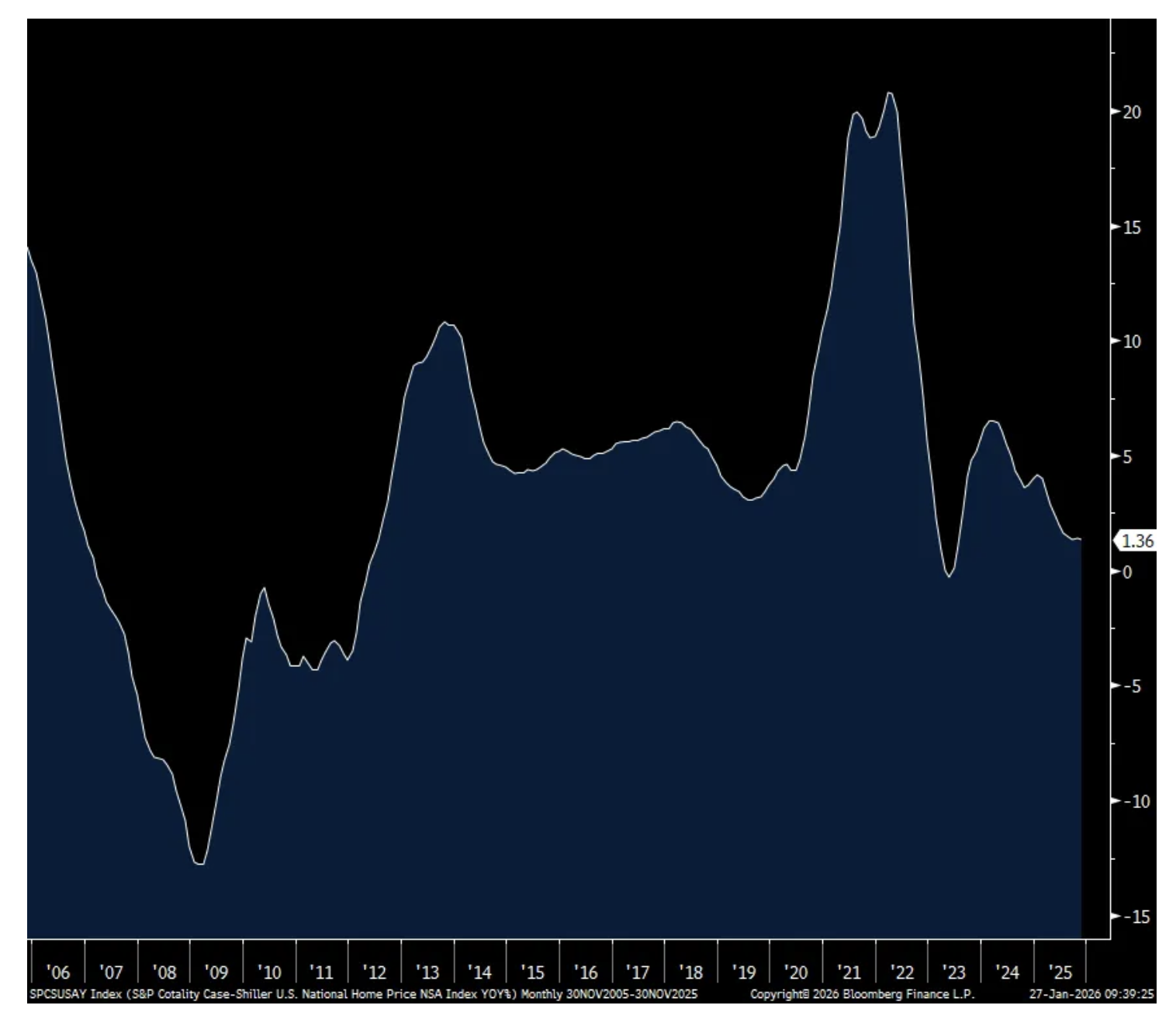

The November national home price index from S&P Cotality rose 1.4% y/o/y, about as expected and a similar pace seen in October. It is though the slowest pace of gain since July 2023 and I think that is a good thing. For all the debate and announced initiatives to spur the number of transactions in the housing market anything that just gooses the demand side without a coincident increase in supply will just further raise home prices that would offset the benefit of lower mortgage rates/fees/whatever. I’d say 25 years of doing so in such an extreme way is enough evidence. Homeowners have enjoyed a tremendous increase in equity in their homes and maybe they can tap that for a new kitchen and/or daily expenses and they won’t like a drop in the value of their home but we need more first time home buyers along with supply in order to increase the number of transactions to unfreeze the market.

In order to do so realistically is to sharply reduce the blockages to new supply, via easier permitting, zoning, etc… but we know that this is done at the local level while the demand side is being tinkered with at the federal level . We also need a period of time where wages/salaries rise much faster than the pace of home price inflation, thus the tempering in price gains is a good thing in the goal to improve affordability and the number of transactions. Also, as I’ve said before too, we need the baby boomers to downside and free up existing home supply but we know that is a tough thing for those that want space for their grandchildren.

As seen, the markets with the most amount of supply had the biggest price declines and in turn hopefully can spur demand, the pace of transactions and the economic activity associated with that. The biggest home price drops took place in Tampa, Dallas, Denver and Phoenix. Tight supply has only led to higher prices in markets like New York, Boston, Minneapolis, and Chicago.

National Home Price Index y/o/y

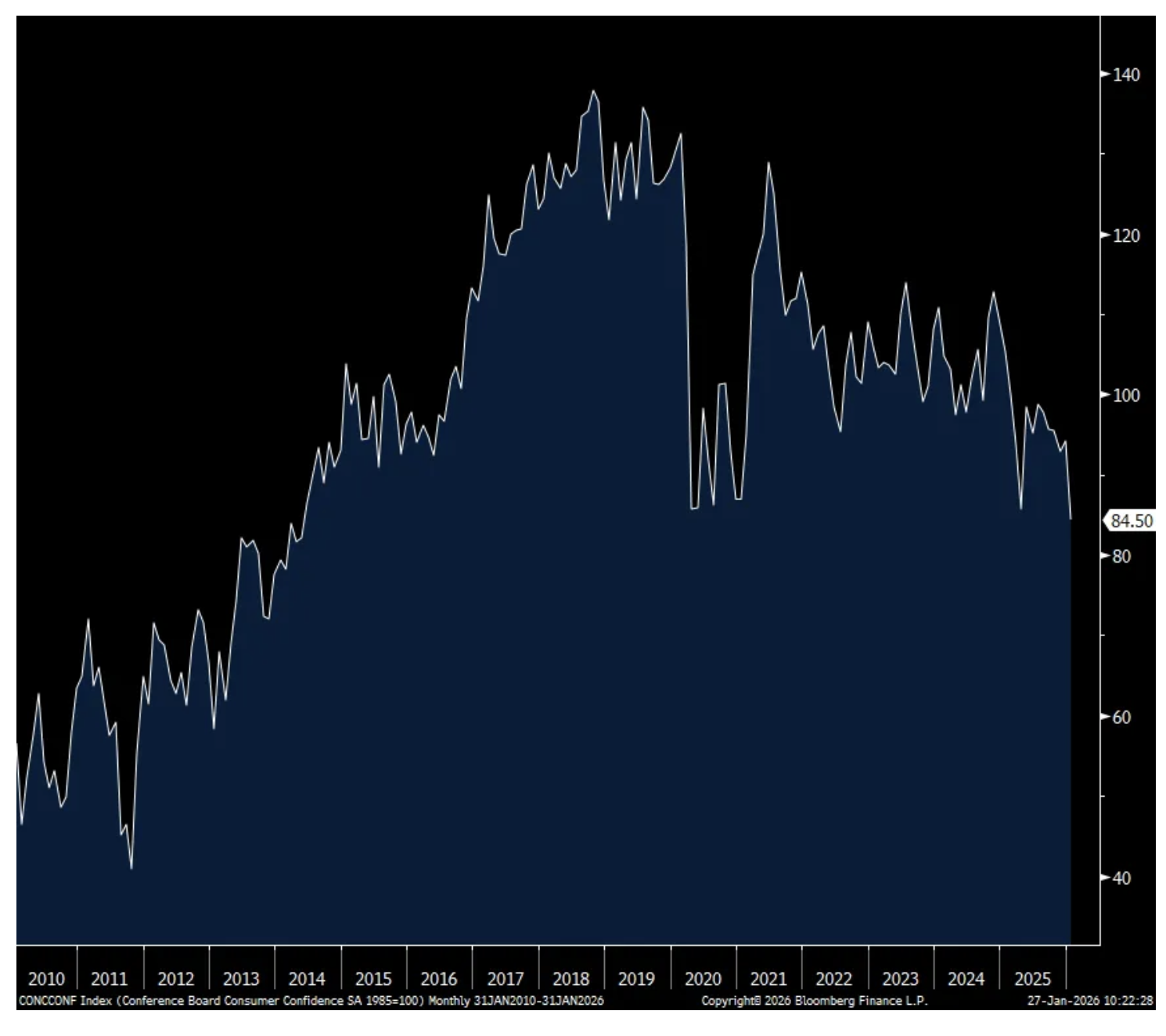

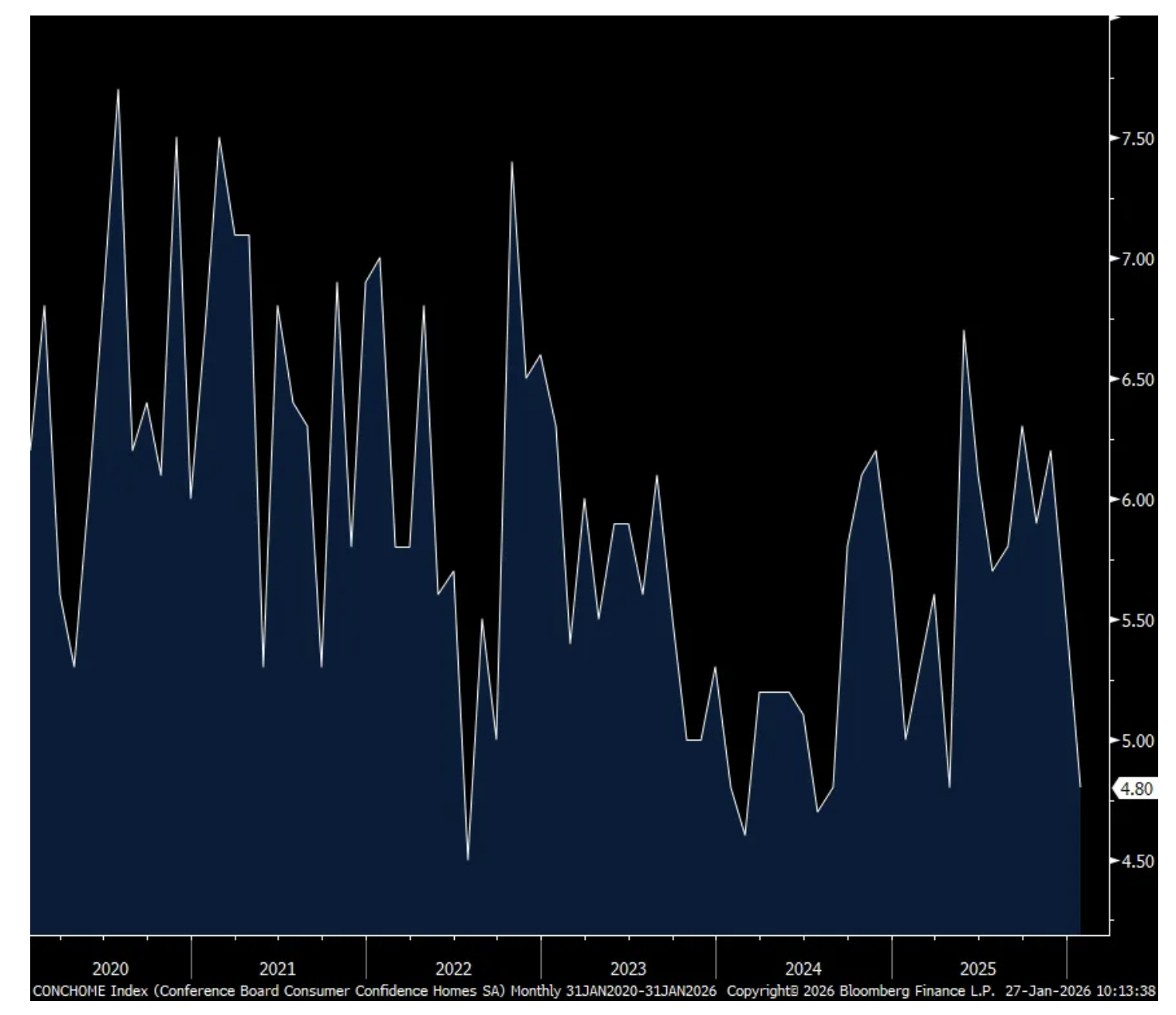

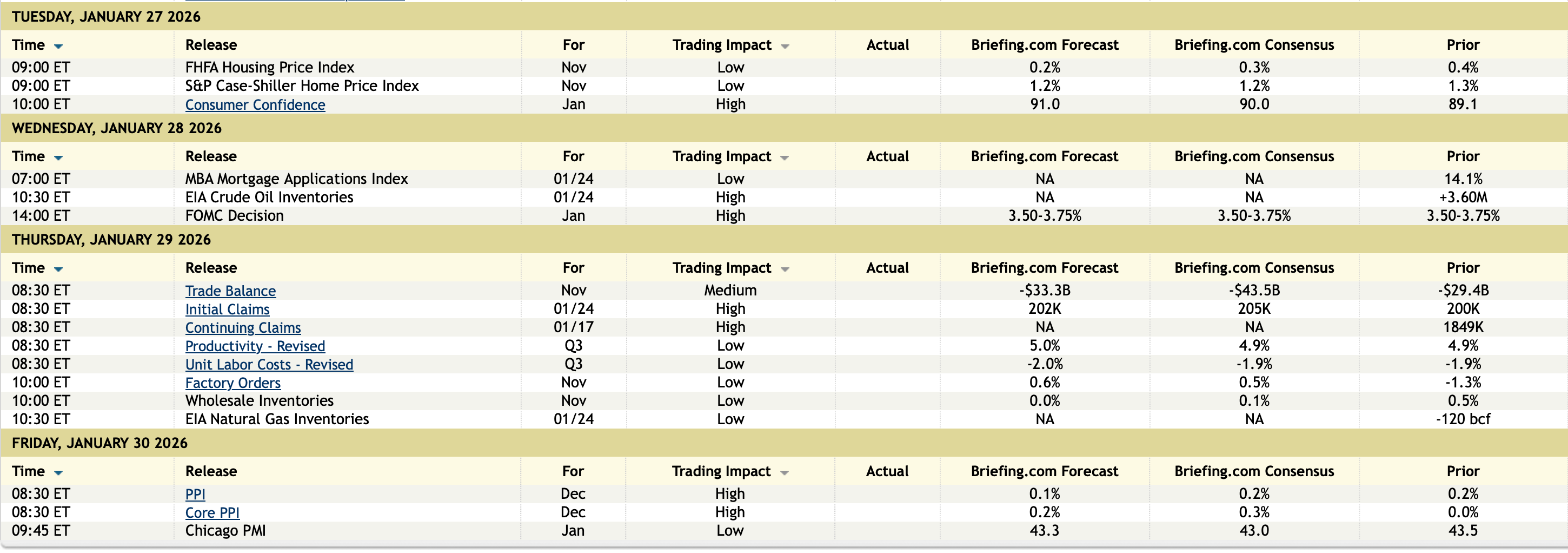

The January consumer confidence index from the Conference Board fell to 84.5, the softest since May 2014, from 94.2 and well below the estimate of 91. The Present Situation fell about 10 pts as did Expectations. One year inflation expectations ticked up to 5.7% from 5.4% and vs 5.8% in the month before that.

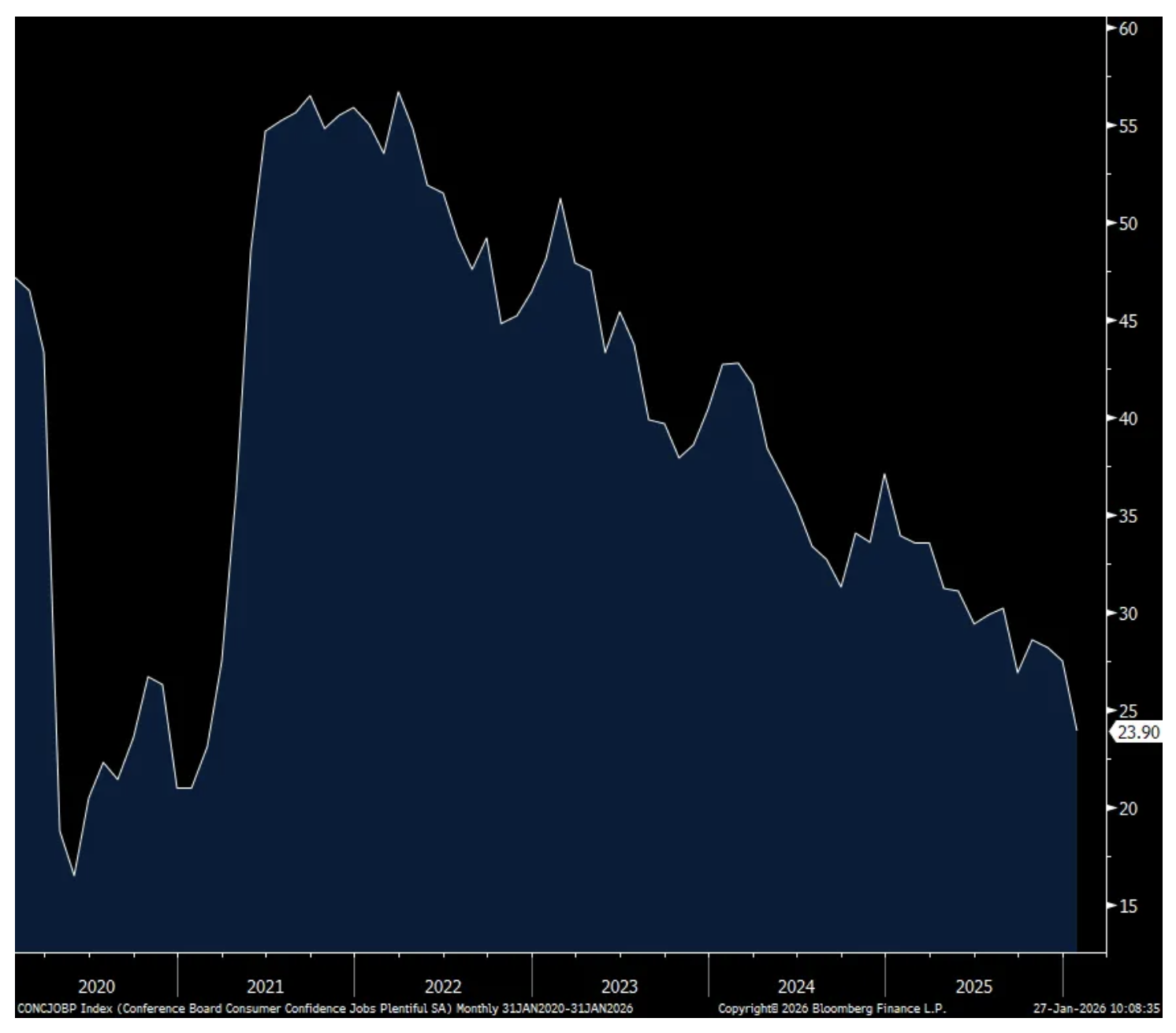

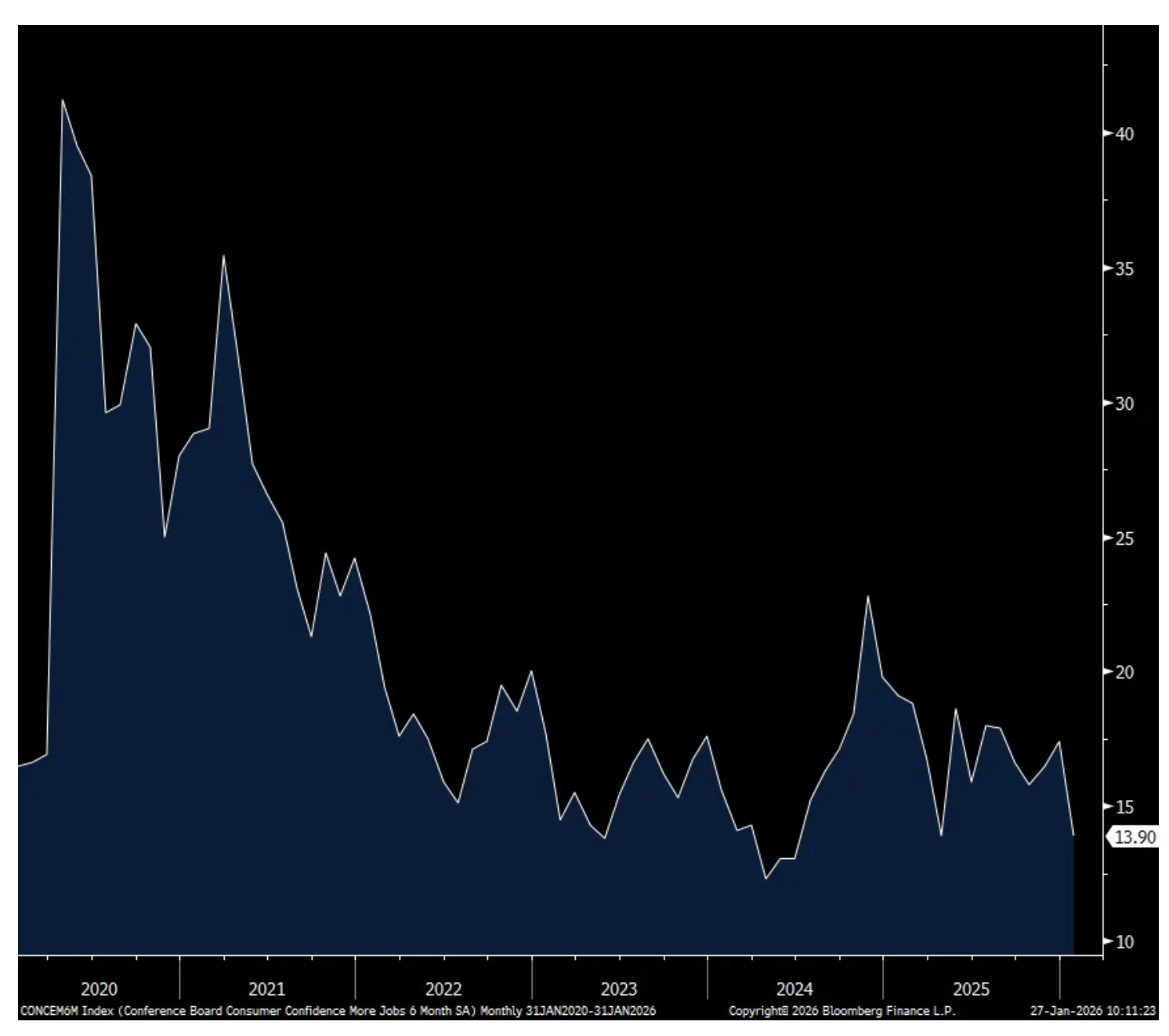

Weakness in particular was seen in the answers to the labor market questions. Jobs Plentiful fell to 23.9 from 27.5 and that is the lowest since February 2021. Those that are Hard to Get rose 1.7 pts to 20.8, the most since February 2021. With respect to the 6 month expectations for the labor market, it deteriorated too. Those that see ‘more jobs’ in the first half this year fell to 13.9 from 17.4 and that matches the lowest since June 2024. Expectations for income softened too.

Spending intentions to buy a home fell to match the lowest since July 2024, notwithstanding the recent dip in mortgage rates. They fell too for vehicles and major appliances.

The bottom line from the Conference Board, “Consumers’ write-in responses on factors affecting the economy continued to skew towards pessimism. References to prices and inflation, oil and gas prices, and food and grocery prices remained elevated. Mentions of tariffs and trade, politics, and the labor market also rose in January, and references to health/insurance and war edged higher.”

My bottom line, inflation levels (not the rate of change that Wall Street cares about) remain the economic pain point and as we debate what the Fed will do this year, I continue to argue that lower inflation should be the main focus because that is the best foundation for a healthy economy that in turn will generate more job growth.

Consumer Confidence

Jobs Plentiful

Hard to Get

More Jobs

Plans to Buy a Home

Lastly, following the negative print from the Dallas manufacturing index yesterday, today’s Richmond’s regional figure was -6 vs -7 in the December.

BY Doug Kass · Jan 27, 2026, 1:40 PM EST

Bond prices slip to the day's lows following the auction results.

BY Doug Kass · Jan 27, 2026, 1:18 PM EST

Not especially rigorous but the tweet is accurate:

BY Doug Kass · Jan 27, 2026, 1:10 PM EST

In reference to the prior column, here is a side-by-side intraday comparison of (XLK) (Tech) vs. (XLF) (Financials) as of 12:25 pm:

BY Doug Kass · Jan 27, 2026, 1:01 PM EST

I have previously mentioned my concern that expectations of large depreciation expenses stemming from the massive AI buildout could adversely impact Mag 7 EPS to be reported shortly.

My old friend Jim Chanos made an additional and important point in a tweet just now:

BY Doug Kass · Jan 27, 2026, 12:54 PM EST

BY Doug Kass · Jan 27, 2026, 12:45 PM EST

BY Doug Kass · Jan 27, 2026, 12:35 PM EST

I continue to avoid financials, having been warning about the sector for several weeks:

Look at the intraday charts of the Tech ETF (XLK) and compare it to the Financials ETF (XLF) below.

While XLK retraced half the gain, the XLF retraced almost all of the noon Trump Greenland/tariff news:

By Doug Kass Jan 21, 2026 4:20 PM EST

BY Doug Kass · Jan 27, 2026, 12:23 PM EST

BY Doug Kass · Jan 27, 2026, 12:10 PM EST

From Peter Boockvar:

I wrote this last week:

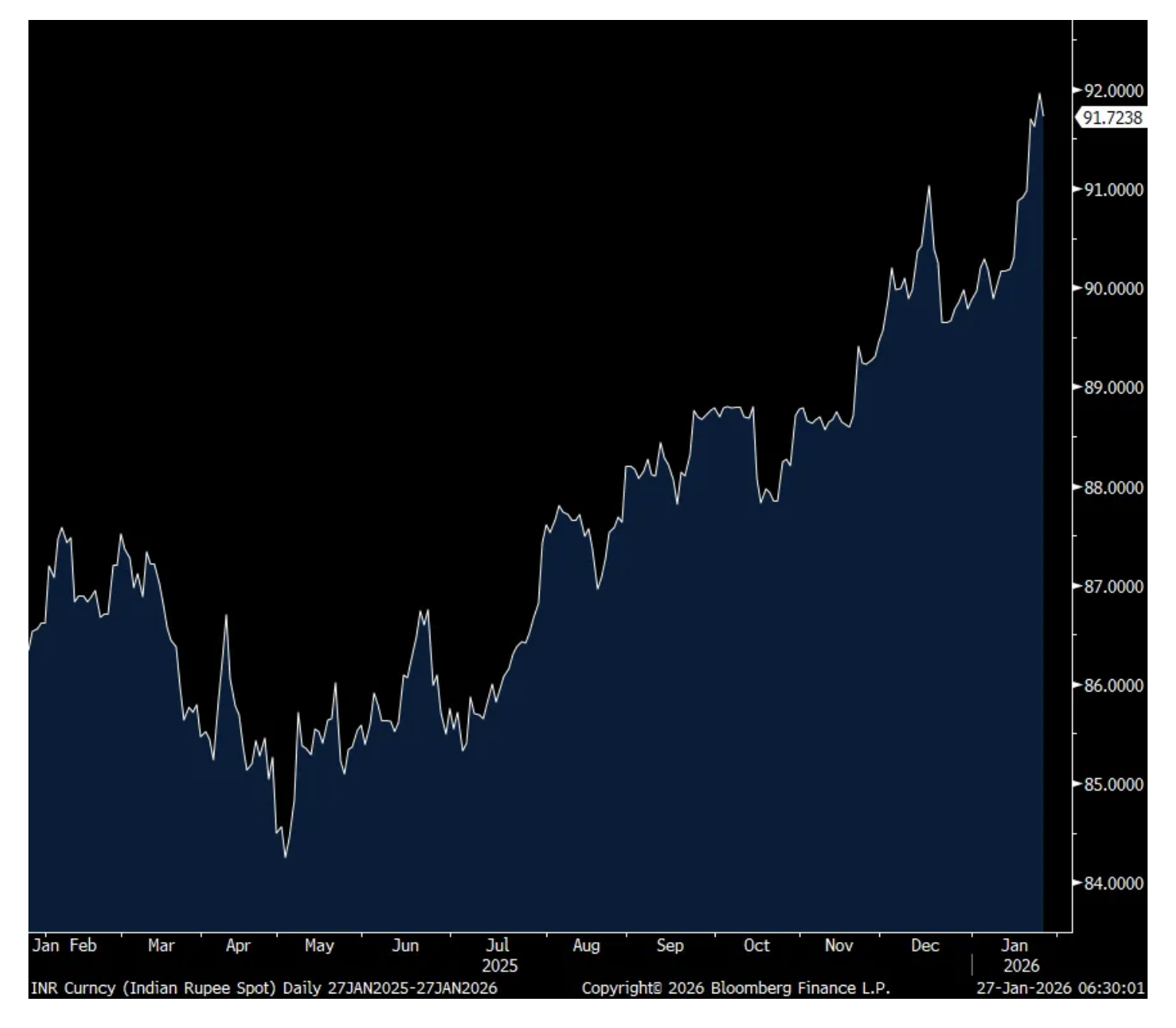

I wanted to quantify the last point and add some more. At the end of 2024 gold made up about 19% of global official reserves. It ended 2025 at 30%. The US dollar’s share is now down to 40% from 50% at the end of 2024. I expect this trend to continue, especially when we see more and more global trade take place in currencies that are not the US dollar. Take the announced deal today between the EU and India where tariffs will fall dramatically. More trade between the two regions will take place in euros and rupees and gold will be the settling currency with any surplus. The rupee has been very weak over the past year but is getting a lift on the deal and is a cheap currency. We are long along with Indian stocks.

The gold rally is not a safety trade, it is reflecting a tectonic shift in where global participants are most comfortable parking their money in preserving value. Also in terms of physically protecting it in light of the continued freeze on half of Russia’s central bank reserves. We remain long gold but acknowledging that at any moment it could be due for a rest after the extraordinary run.

Indian Rupee (the higher, the weaker vs USD)

As we await earnings from the hyperscalers, I continue to think it’s important to pay attention to the intense and growing competition from the Chinese models. The South China Morning Post this morning is reporting that Alibaba says Qwen3-Max-Thinking is its ‘best model so far’, while Moonshot calls Kimi K2.5 the world’s most powerful open-source model. Alibaba Group Holding and Moonshot AI have unveiled their latest flagship artificial intelligence models, narrowing the gap with US industry leaders OpenAI and Google DeepMind.”

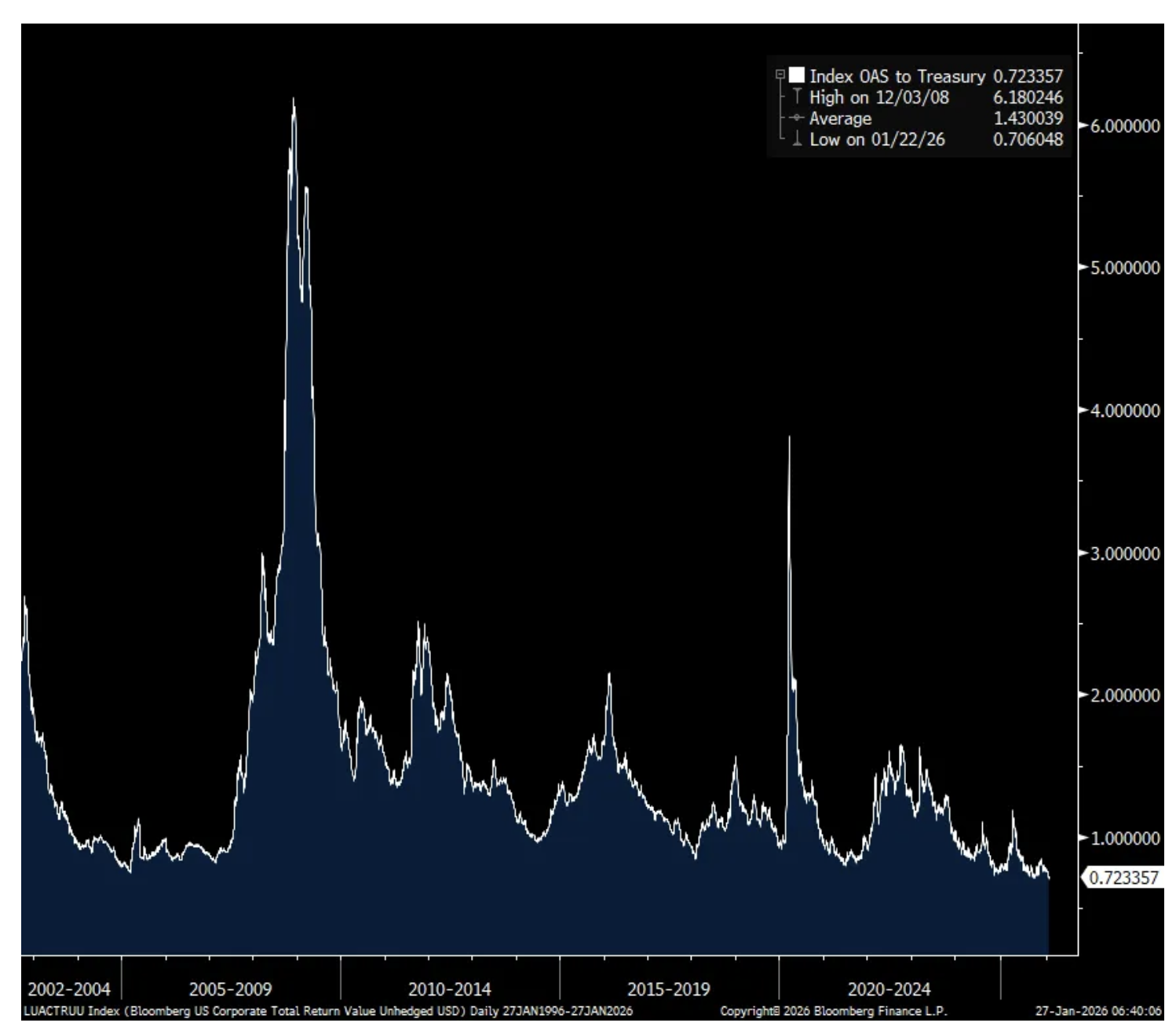

I wanted to point out that on Thursday, the US corporate investment grade bond spread tightened to just 70 bps (closed yesterday at 72 bps). I have data back to 2001 and it’s never been this tight. It says as much about the expensive nature of corporate bonds but also what investors think about holding US Treasuries relative to corporates. I guess would you rather hold the bonds of Coca Cola and Walmart or the US government with the market obviously voting for the former right now.

IG Corporate Bond Spread

BY Doug Kass · Jan 27, 2026, 10:35 AM EST

* The voting machine is overwhelming the weighing machine these days

Equities continued to advance on Monday — and that ascent continues in the futures market this morning.

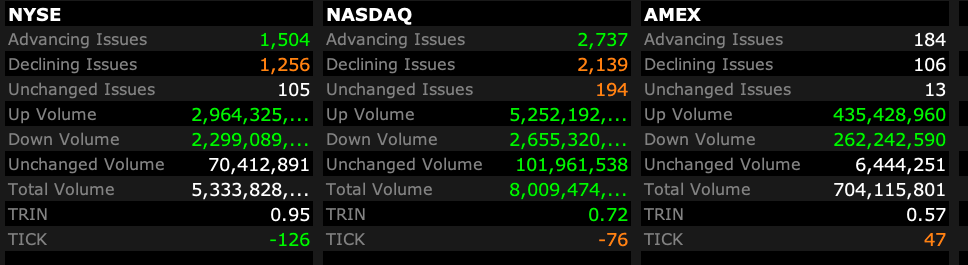

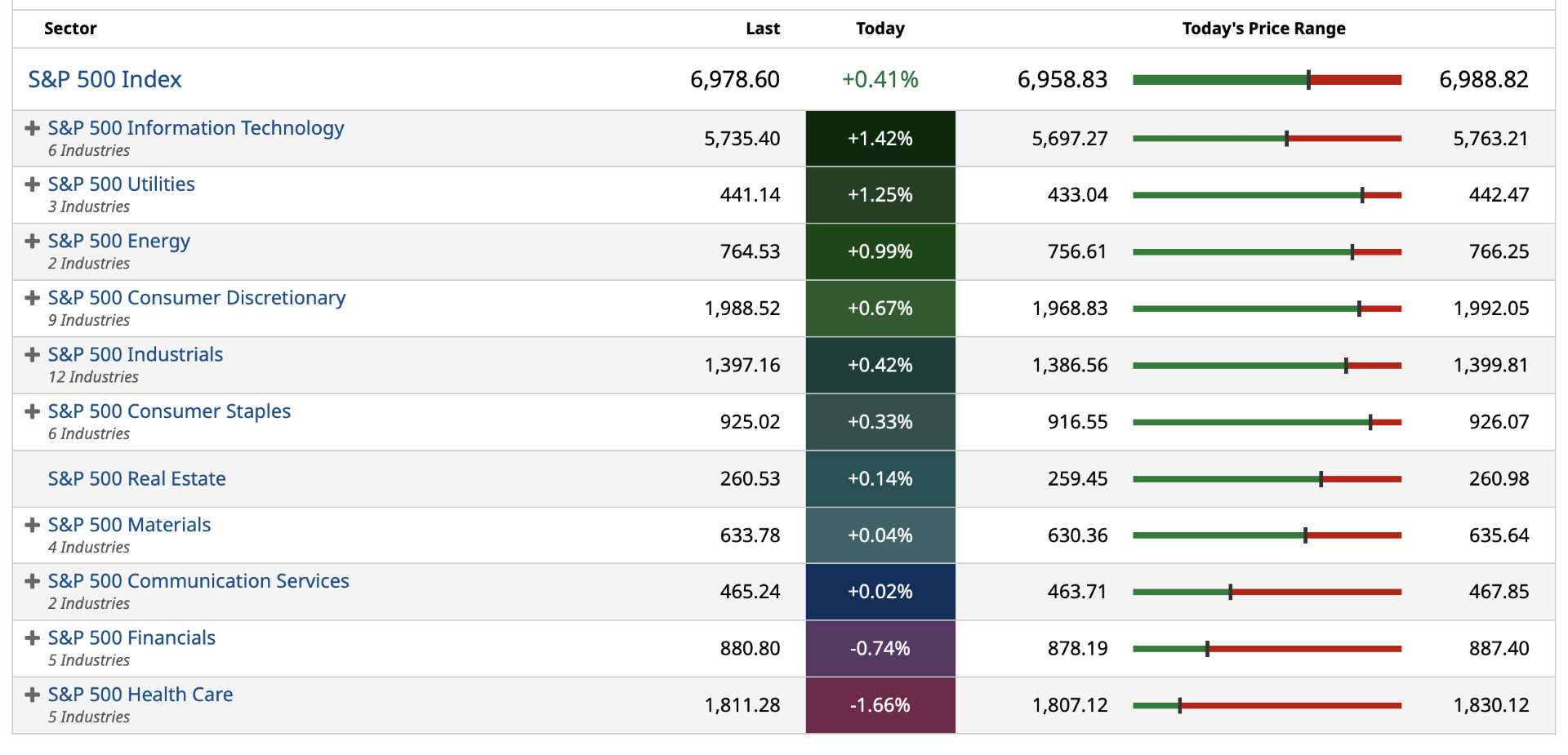

The northerly move seems uninterested and oblivious to uninspiring market breadth:

Nor is the market concerned about fatuous/feckless policy (erratic tariffs, absence of fiscal discipline et al), uncooperative and highly partisan politicians in Washington, D.C. (likely leading to a government shutdown in February), very expensive valuations, a equity risk premium that has become an equity risk discount, parabolic moves in precious metals, a breakout (to the upside) in other commodities (leading, in part, to sticky inflation), evidence of rising levels of speculation, investor complacency, a narrowing in the internals, rising JGB yields, the precarious state of AI capital spending vs. projected returns (on that investment) and a host of other headwinds (often mentioned in my Diary).

Bears are going the way of the flightless and extinct dodo bird - rapidly becoming an endangered species:

The principles of "value investing" and "margin of safety" have become anathema to market participants as the advance in stocks continues to be propelled by the growing dominance of passive products and strategies which are getting massive inflows:

Those products/strategies (stirred by machines and algos) don't think and they have no emotion — they worship at the altar of price momentum.

And stock prices are rising.

As I have previously mentioned in The 'Happy Meals' Won't Last Forever (as illustrated in Wally Deemer's McDonald's (MCD) observation in the 1970s when earnings per share compounded at a +26% annual rate but the price-to-earnings dropped from 77-times to 8-times) history is littered with periods in which high valuations were a poor launching pad for future investment returns:

Bukowski's quote reflects the paradox that smart people, aware of complexity, are prone to doubt. But less-knowledgeable individuals often possess overconfident certainty leading to an imbalance where uninformed voices dominate.

This links to the Dunning-Kruger Effect, where incompetence masks itself.

You might find some of Dunning-Kruger in the business media today... frankly I discover it everyday.

Happy meals won't last forever.

BY Doug Kass · Jan 27, 2026, 9:45 AM EST

Spruce Point Capital Management has issued a "strong sell" on one of my current shorts: Resideo Technologies (REZI) .

Here is their complete analysis. Resideo Technologies, Inc. - Spruce Point Capital Management LLC

BY Doug Kass · Jan 27, 2026, 9:28 AM EST

BY Doug Kass · Jan 27, 2026, 9:20 AM EST

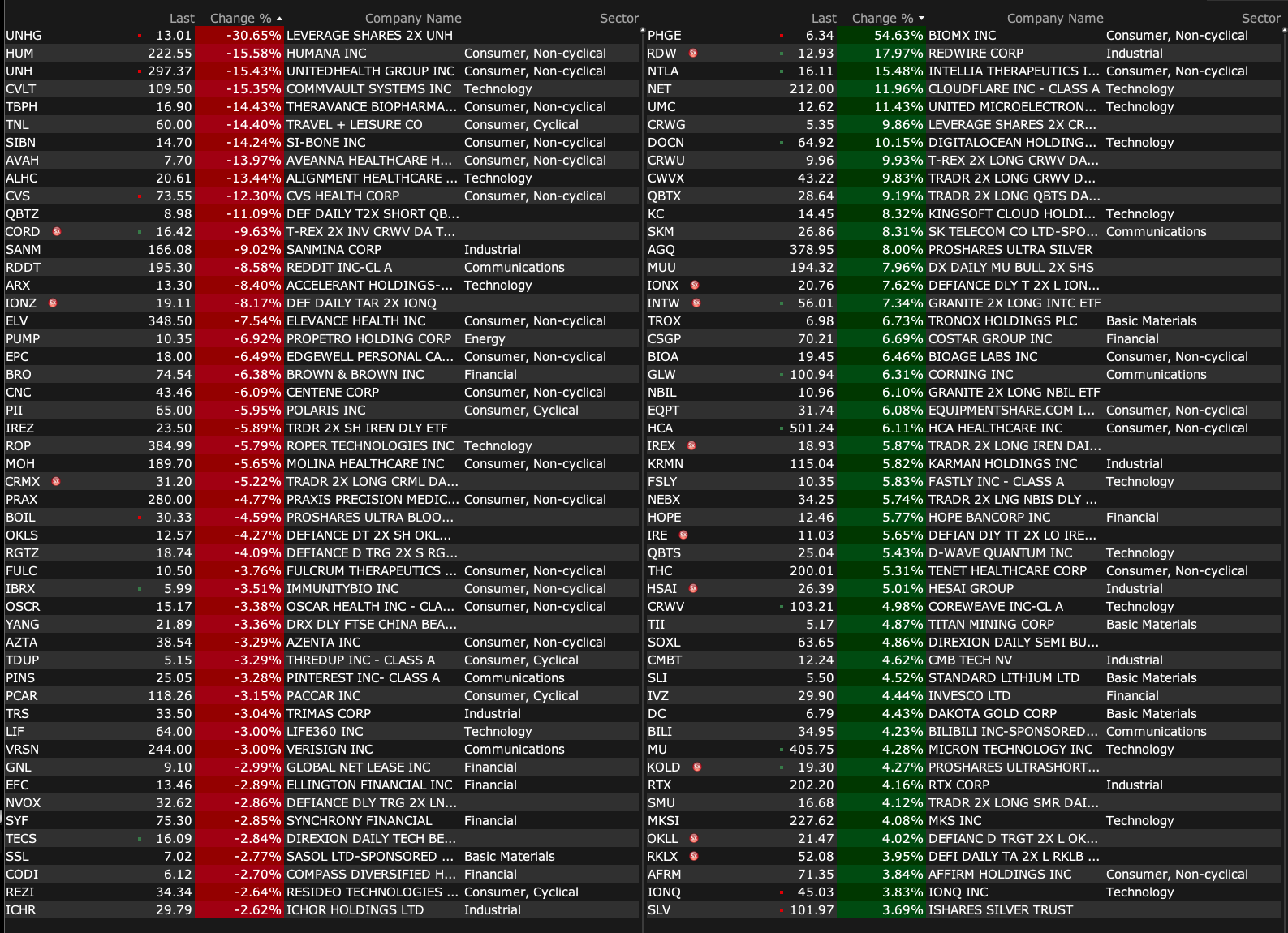

-CYN +36% (triples DriveMod Tugger autonomous vehicle orders in 2025)

-NTLA +19% (US FDA lifts Clinical Hold on MAGNITUDE-2 Phase 3 Clinical Trial of nexiguran ziclumeran (nex-z) in hereditary transthyretin amyloidosis with polyneuropathy (ATTRv-PN))

-RDW +17% (selected for Undisclosed Portion of Missile Defense Agency’s $151B Multi-Vendor SHIELD IDIQ to Support Homeland Defense)

-NET +12% (hearing constructive commentary from RBC on AI workloads)

-KRMN +8.6% (Systima Facility awarded MDA Contract under $151B SHIELD IDIQ)

-CSGP +7.9% (reportedly Third Point to urge Costar restructure operations; hearing BTIG Raised CSGP to Buy from Neutral, price target: $80)

-GLW +7.9% (Corning and Meta confirm multiyear, up to $6B agreement to accelerate US Data Center Buildout)

-HCA +6.3% (earnings, guidance; raises dividend)

-GM +4.1% (earnings, guidance; raises dividend)

-MU +4.0% (confirms to break ground on Advanced Wafer Fabrication Facility in Singapore)

-AFRM +3.7% (Needham Raised AFRM to Buy from Hold, price target: $100; Bolt selects Affirm as embedded Buy Now, Pay Later partner)

-RTX +3.5% (earnings, guidance)

-SYY +3.5% (earnings, guidance)

-AAL +3.4% (earnings, guidance)

-UPS +3.1% (earnings, guidance)

-CRM +2.9% (Unit Computable Insights receives ~$5.6B US Army contract)

-OLOX +2.3% (begins recommissioning of pipeline)

-HUM -15% (CMS and White House will propose .09% average rate increase for Medicare Advantage in 2027, less than analysts expected)

-UNH -15% (earnings, guidance; CMS and White House will propose .09% average rate increase for Medicare Advantage in 2027, less than analysts expected)

-CVLT -14% (earnings, guidance)

-RDDT -8.7% (hearing Cleveland Research Company Cuts RDDT to Neutral from Buy)

-SANM -8.5% (earnings, guidance)

-UI -5.3% (weakness attributed circulation of Hunterbrook report)

-JBLU -4.9% (earnings, guidance)

-PINS -3.4% (announces restructuring plan)

-PII -3.3% (earnings, guidance)

-AA -2.2% (hearing Morgan Stanley Cuts AA to Equal Weight from Overweight, price target: $64)

-PCAR -2.0% (earnings, guidance)

BY Doug Kass · Jan 27, 2026, 9:10 AM EST

(Today's ) things:

* Shorted (SPY) $694.65 and (QQQ) $629.46.

* Added to (GRNY) $25.75 short.

* Added to (UNH) long at $295.14.

BY Doug Kass · Jan 27, 2026, 8:59 AM EST

From JPMorgan:

US: Futs are higher, led by Tech, as geopolitical / headline risk subsides, and the market focuses on earnings as the Fed decision is expected to be a non-event. Equities are poised for another attempt at 7k. Pre-mkt, the yield curve is twisting steeper as JGB-induced vol subsides; USD is flat. Mag7 and Semis are bid as HC is hit on headlines related to Medicare pricing. Cyclicals leading Defensives, driven by Fins / Mats. In cmdtys, precious metals continue to move vertically with gold +1.5% and silver +8%, though PGMs are being sold. Today’s macro focus is on the weekly ADP print, home price data, Consumer Confidence, and regional Fed activity indicators.

· EU/UK: Major markets are mostly higher led by the UK / Italy with SMID-caps / Germany lagging. EU / India signed a free trade agreement. APAC session was positive despite US hiking tariffs on Korea for not approving its trade deal with the US quickly enough. In EU thematics, Momentum / Recession are leading with Quality / Vol lagging. UKX +0.4%, SX5E +0.3%, SXXP +0.3%, DAX -0.1%. CSI -0.0%, HSI +1.4%, NKY +0.8%, ASX +0.9%, KOSPI +2.7%.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Today’s session may offer a further calming of the market as investors shift from headline risk to earnings risk. Trump will have a speech on affordability later today with outstanding threats of 100% tariffs on Canada and an increased tariff on Korea to 25%.

· YESTERDAY’S MACRO DATA (Abiel Reinhart) – Capital goods orders and shipments continued their ascent in the November durable goods report, setting up a decent fourth quarter for equipment investment. Total durable goods orders jumped 5.3%m/m on a lift from aircraft, while ex transportation orders rose 0.5%. For core capital goods—nondefense ex aircraft—orders increased 0.7% and shipments 0.4%, with orders tracking 8.5% saar over 3 months and shipments 9.9%. We see 4Q equipment investment now tracking just over 5%q/q saar, vs our prior forecast of 2.5%. More detail on equipment investment comes with the November trade report later this week, since most tech equipment is imported. Manufacturing surveys suggested continued growth in activity through December and possibly into January.

· TODAY’S MACRO DATA – Keep an eye on the ADP weekly release. If this economy can take some of the outsized spending combine that with a positive outlook, including fiscal support, and convert that to improved hiring then I think the market could explode higher. Capex from TMT will remain supportive to both GDP and to the SPX (assuming we receive expected earnings delivery). Adding hiring would boost consumption that is expected to receive a tailwind from higher than expected tax returns. Separately, housing data, regional Fed activity data, and Consumer Confidence numbers will be release today, too. The housing data is expected to see further price increases which may buttress the homebuilders trade. On Consumer Confidence, Feroli sees a MoM increase from 89.1 to 90.0.

· TRADE – with the threat of a 100% tariff on Canada looming, UK’s Starmer said that the UK will not be forced to choose between the US and China. Comments were made ahead of his trip to China. Should the UK sign, or agree to the framework of a trade deal, this may embolden other countries to push back on the Trump Administration. Part of our tactical hypothesis includes a thawing of the trade war, but this is the type of event that may escalate the trade war. That said, Trump’s focus on affordability, the basis for his speech today, means his response is unclear should the UK push forward with a trade deal with China.

MAG7 EARNINGS PREVIEW: AMZN, GOOG, META, MSFT (MARK SCHILSKY)

· AMZN 25Q4 EARNINGS PREVIEW – The Andy Jassy Show: AMZN remains the most frustrating Internet stock for the most Internet investors, easily. Seemingly, everyone I speak to is long the stock headed into 2026 on a similar thesis of: 1) AWS Revenue growth will accelerate meaningfully – partially due to Anthropic’s continued rapid growth, 2) the stock is genuinely cheap now. It’s literally as cheap as it’s ever been on GAAP P/E, and 3) investors anticipate meaningful Retail margin expansion in the coming years as AMZN leverages the usage of robots. It’s a great, simple pitch. But if I want to be honest, the only KPI that truly matters this quarter is AWS Revenue growth. See today’s Tech Sketch for my full Preview.

· GOOG 25Q4 EARNINGS PREVIEW – The Funding Long: Owning GOOG the past few months has felt like snuggling up inside a warm blanket: cozy and safe. But I worry that we’re veering, short-term, into ‘lazy long’ territory. Buyside estimates for 2027 EPS are not significantly above the Street, so it feels like investors are playing more for continued multiple expansion rather than material earnings beats. That set-up bugs me given that GOOG is now more expensive than MSFT, AMZN and META on 2026 GAAP P/E. See today’s Tech Sketch for my full Preview.

· META 25Q4 EARNINGS PREVIEW – Avocado Toasted: Investor sentiment has soured considerably on META since the Q325 print when it became abundantly clear that Zuckerberg’s foot remains firmly pressed down on the OpEx/capex accelerator. Looking at this quarter specifically, investors’ attention is focused squarely on the 2026 OpEx guide (can’t be bigger than feared) as well the Q126 Revenue guide (needs to show a modest FXN acceleration on an easier comp). All told, I’d characterize investor sentiment on META heading into this print as ‘timid’. See below for my memo laying out investor expectations. Also see Doug’s META Q425 Earnings Preview. Mark’s full note is here.

· MSFT 25Q4 EARNINGS PREVIEW – Too Much SaaS, Not Enough AI: From an investor standpoint, MSFT is currently stuck between a rock (SaaS) and a hard place (OpenAI). In my estimation, they only way they extricate themselves is by meaningfully accelerating Azure growth into the low-to-mid 40’s quickly. We probably don’t get that this quarter, but there’s a real chance we cross the 40 threshold on the guide. But, much of that potential acceleration is out of Satya’s hands. It’s in Sam’s. Mark’s full preview is here.

· JPM’s Internal IT Strategy Team Webinar on the ‘Death of Software’ was HUGE: We had over 900 clients dial-in for last Friday’s Untangling the ‘Death of Software’ Narrative with our IT Strategy Team and Mark Murphy. The last time I was part of a webinar of that scale was DeepSeek Monday. Unfortunately, last Friday’s webinar was not recorded nor are their official notes but feel free to give Mark Murphy a call!

BY Doug Kass · Jan 27, 2026, 8:55 AM EST

BY Doug Kass · Jan 27, 2026, 8:39 AM EST

11 a.m.: Treasury Announces a 4 and 8 Week Bill Auction;

11:30 a.m.: Treasury hosts a $90B 6-Week Bill Auction;

1 p.m.: Treasury hosts a $70B 5-Year Note Auction;

2 p.m.: Treasury buyback (liqsupport)

BY Doug Kass · Jan 27, 2026, 8:30 AM EST

Bonus — Here are some great links:

What Soaring Precious Metals Means for Inflation

BY Doug Kass · Jan 27, 2026, 6:30 AM EST

BY Doug Kass · Jan 27, 2026, 6:05 AM EST

BY Doug Kass · Jan 27, 2026, 5:55 AM EST

The S&P Short Range Oscillator remains overbought at 2.26% vs. 2.91%.

BY Doug Kass · Jan 27, 2026, 5:45 AM EST