Howling About the Capital Spending Boom

Wolf Street howls about the boom in capital spending.

BY Doug Kass · Jan 26, 2026, 5:00 PM EST

Wolf Street howls about the boom in capital spending.

BY Doug Kass · Jan 26, 2026, 5:00 PM EST

BY Doug Kass · Jan 26, 2026, 4:45 PM EST

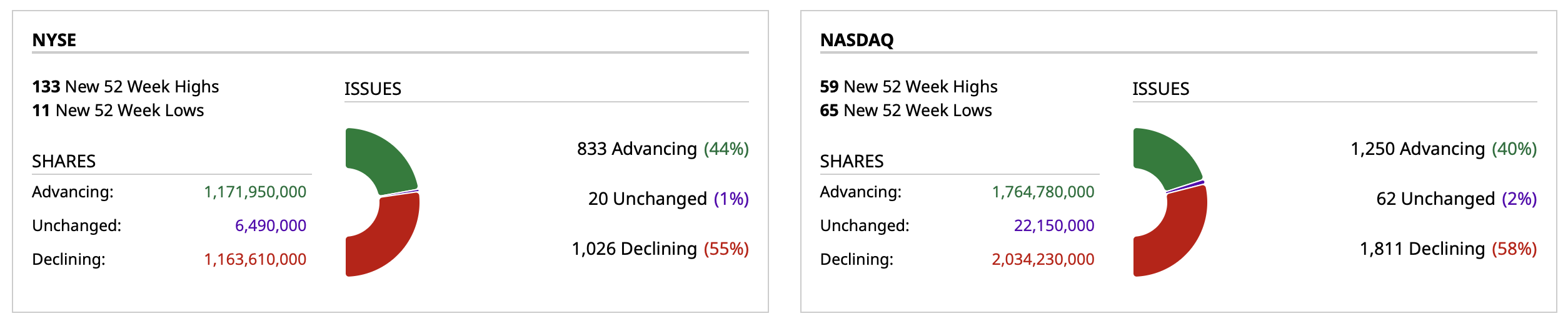

- NYSE volume 2% below its one-month average;

- NASDAQ volume 12% below its one-month average;

- VIX index: up 0.37% to 16.15

BY Doug Kass · Jan 26, 2026, 4:27 PM EST

UnitedHealth (UNH) is coming down hard in the after-hours on this news:

Trump Administration Proposes Keeping Steady the Rates Medicare Pays Insurers

I have added to my small long position at $322.50.

BY Doug Kass · Jan 26, 2026, 4:18 PM EST

Nike (NKE) reports that it is cutting 775 employees as it accelerates "automation" of its domestic distribution centers.

BY Doug Kass · Jan 26, 2026, 3:55 PM EST

BY Doug Kass · Jan 26, 2026, 3:48 PM EST

BY Doug Kass · Jan 26, 2026, 3:33 PM EST

Weak:

BY Doug Kass · Jan 26, 2026, 2:55 PM EST

The S&P Index is now +100 handles off the evening/futures session's lows.

Breadth stinks and there is no broadening out ( (IWM) is lower).

Bears are an endangered species.

I plan to move to medium-sized short (SPY) and (QQQ) into further strength.

BY Doug Kass · Jan 26, 2026, 2:08 PM EST

No trades since last report.

This is a research day.

BY Doug Kass · Jan 26, 2026, 1:59 PM EST

BY Doug Kass · Jan 26, 2026, 12:28 PM EST

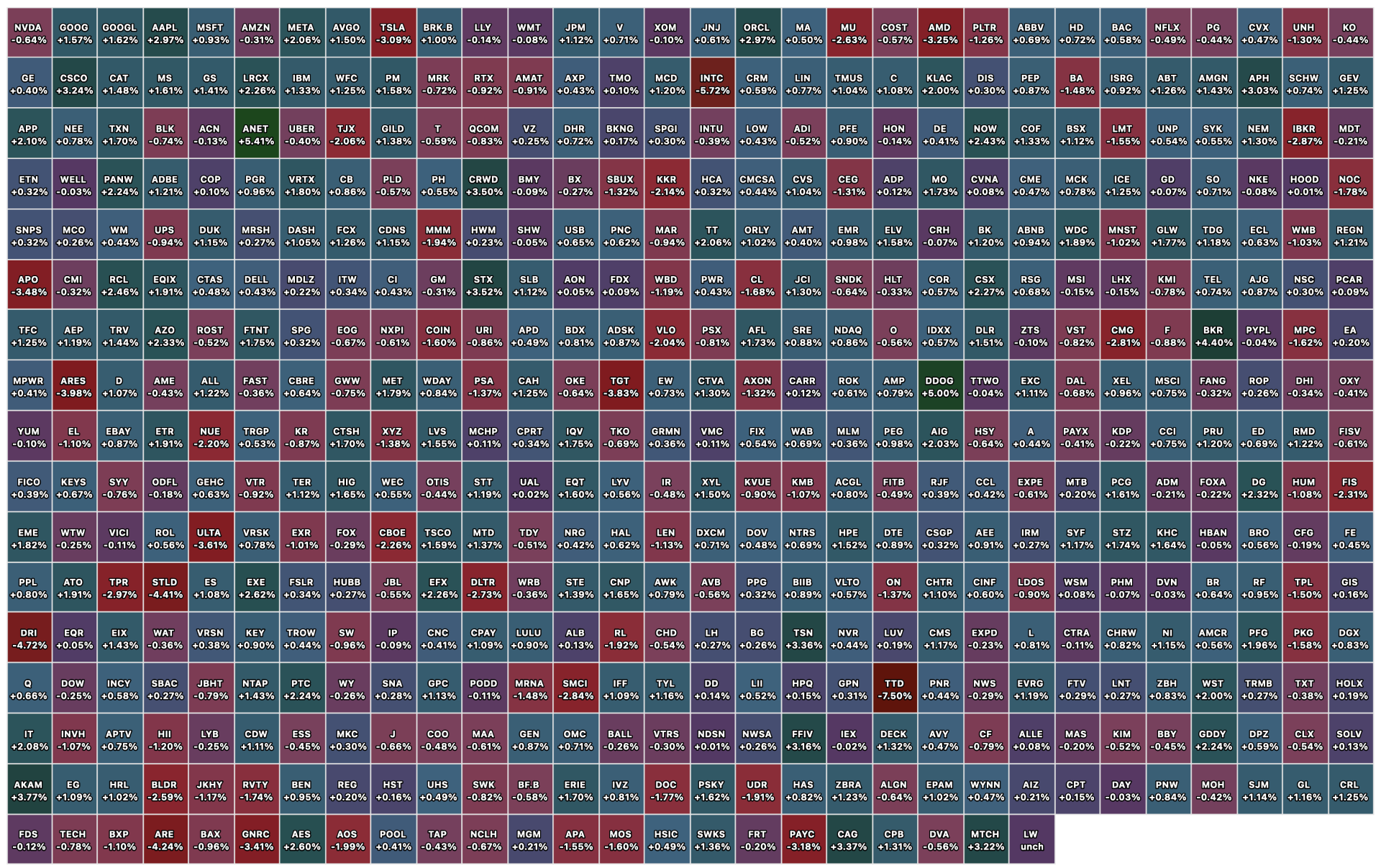

Despite the robust rise in the averages (especially from the morning lows), I would note that the Russell is not crowing!

(IWM) is, in fact, down on the day (-$1.10).

BY Doug Kass · Jan 26, 2026, 11:35 AM EST

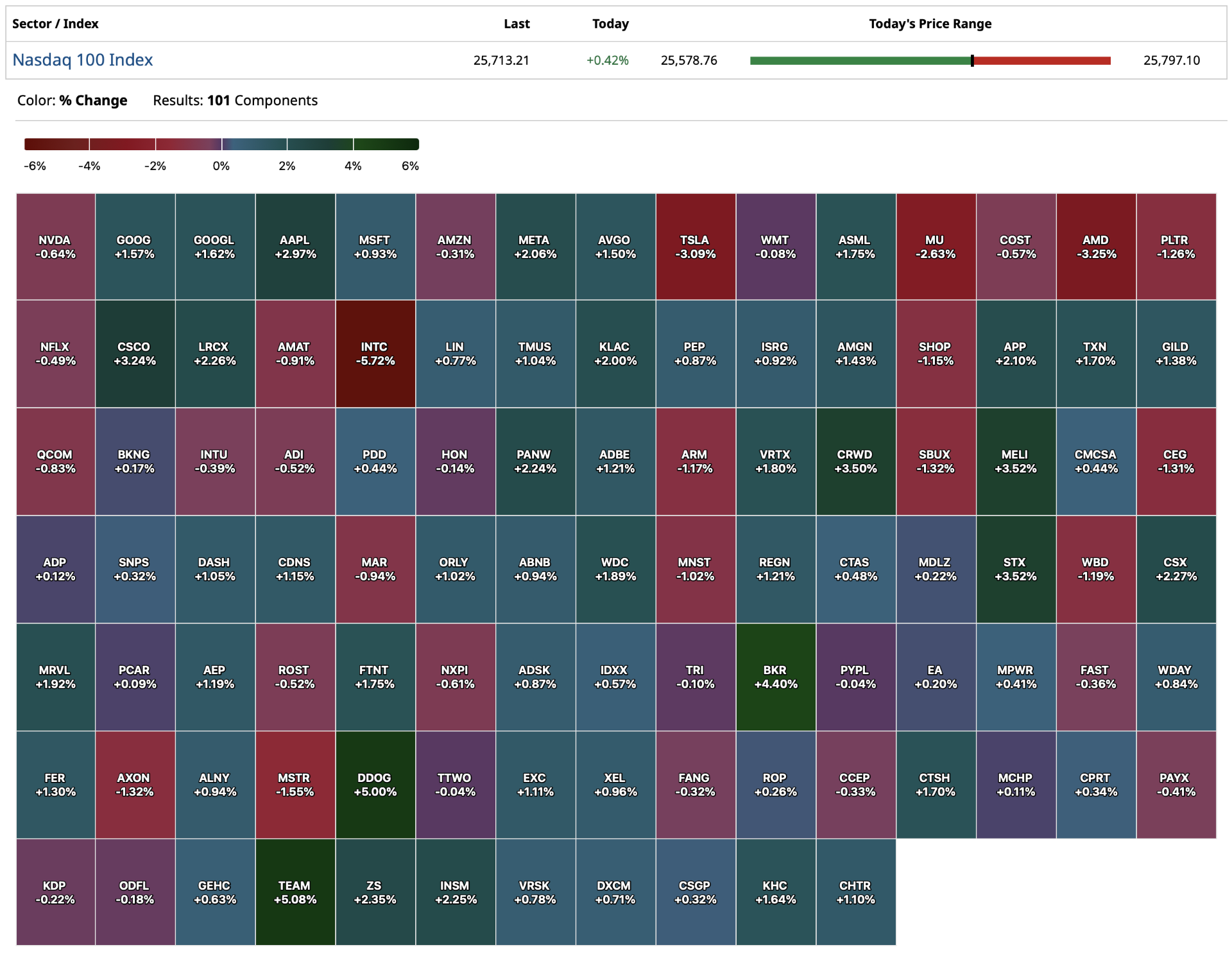

Nvidia's (NVDA) shares are falling a bit after Microsoft (MSFT) announced the launch of MAIA 200, its latest competitive AI chip.

BY Doug Kass · Jan 26, 2026, 11:11 AM EST

- NYSE volume flat compared to its one-month average;

- Nasdaq volume 16% below its one-month average;

- VIX index: down 0.37% to 16.03

BY Doug Kass · Jan 26, 2026, 11:00 AM EST

Adding to Index shorts with S&P cash +31 handles.

Reshorting (JOET) and (GRNY) .

BY Doug Kass · Jan 26, 2026, 10:09 AM EST

* Equities are no longer driven by active investors — as passive investing dominates the investing landscape

* You won't see or read this discourse/observation in the business media this morning...

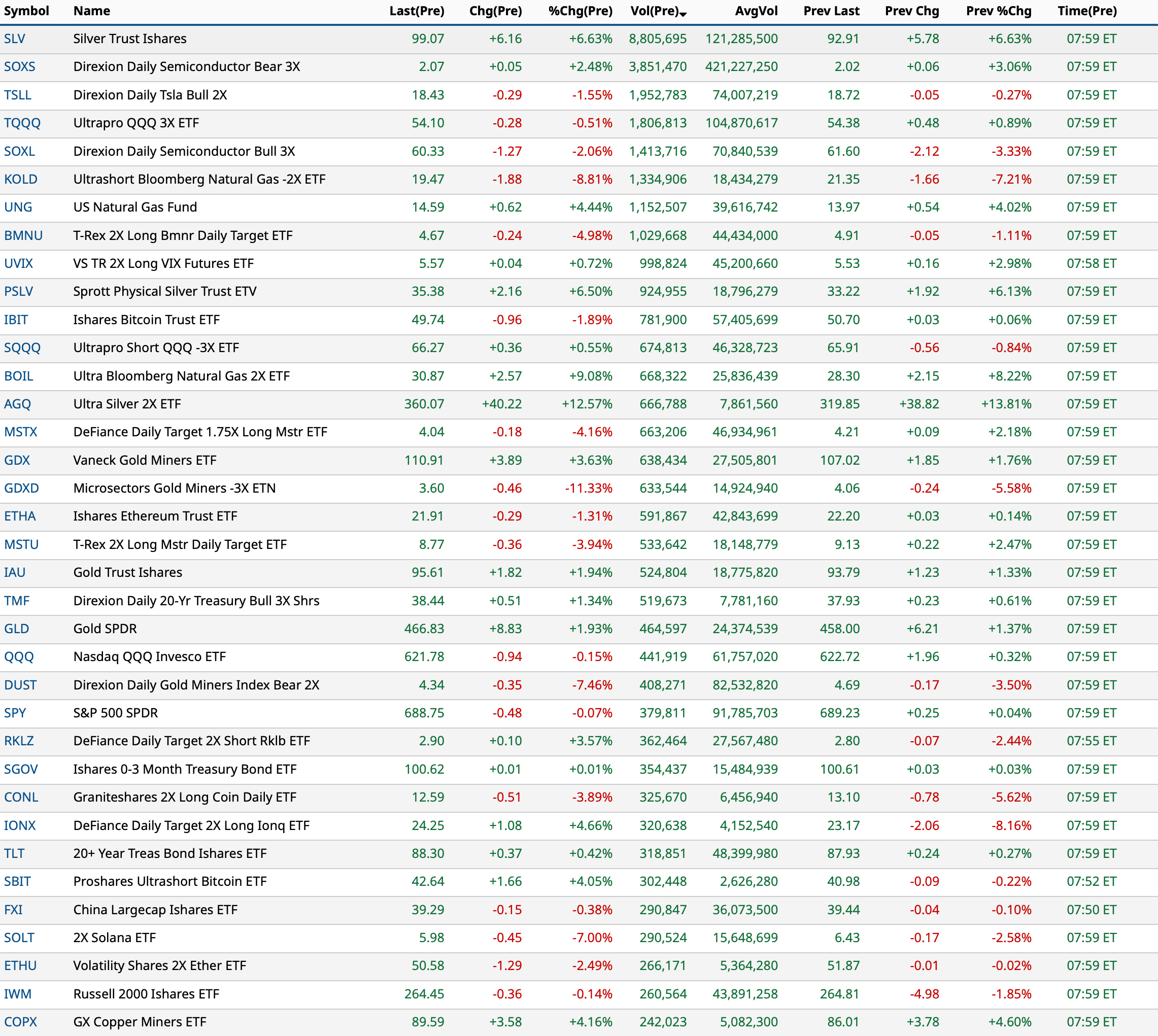

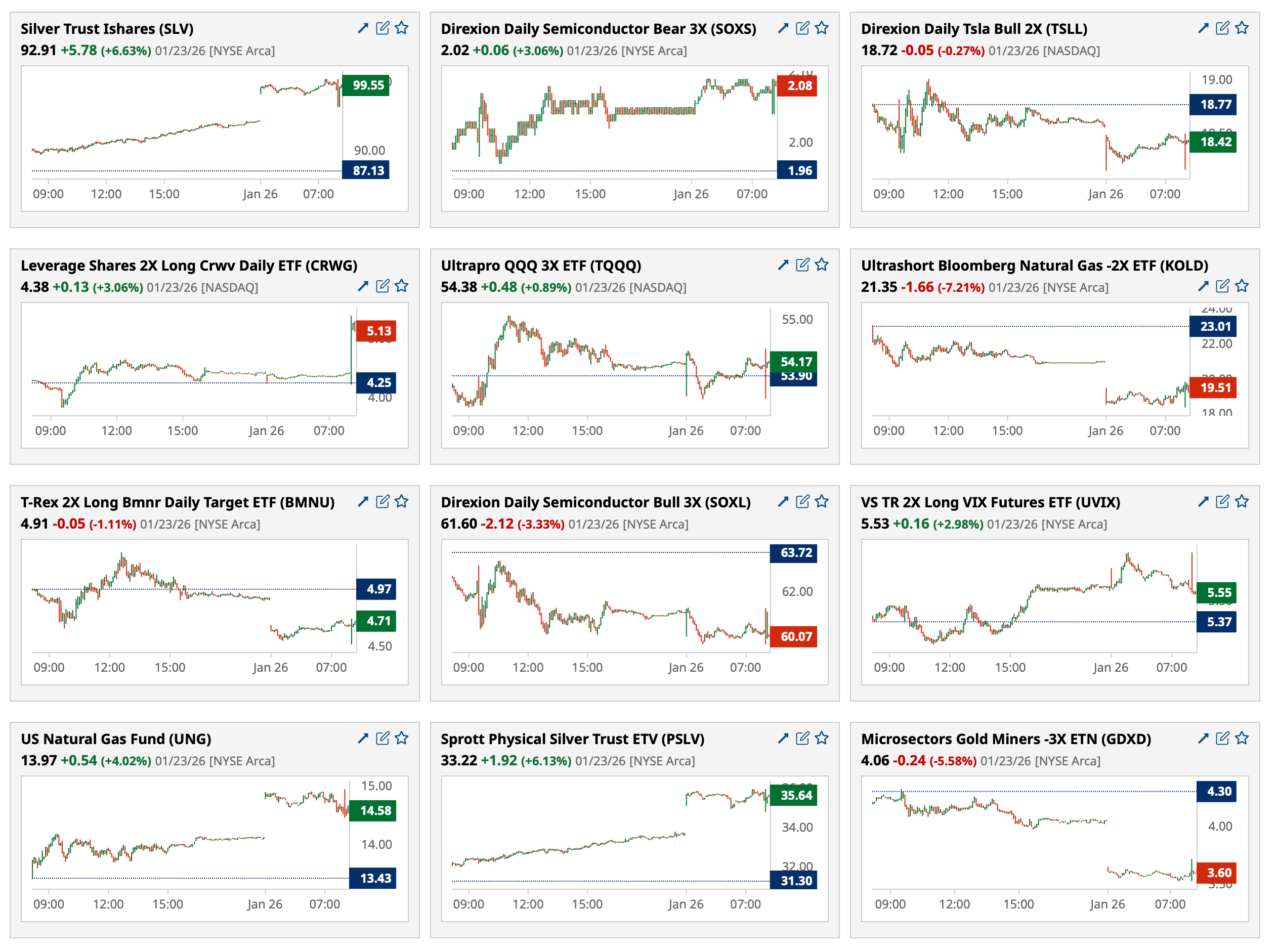

Between the continuing parabolic moves in metals (platinum, silver and gold are materially higher overnight, again) and the disparate sector action on Friday, price movements are unlike anything I have seen in years.

On the second point, the Russell Index (got shellacked, we recently shorted) on Friday — declining by -2.20% ( (IWM) -$6) as (SPY) closed down by only -0.14% and (QQQ) closed up by +0.13%.

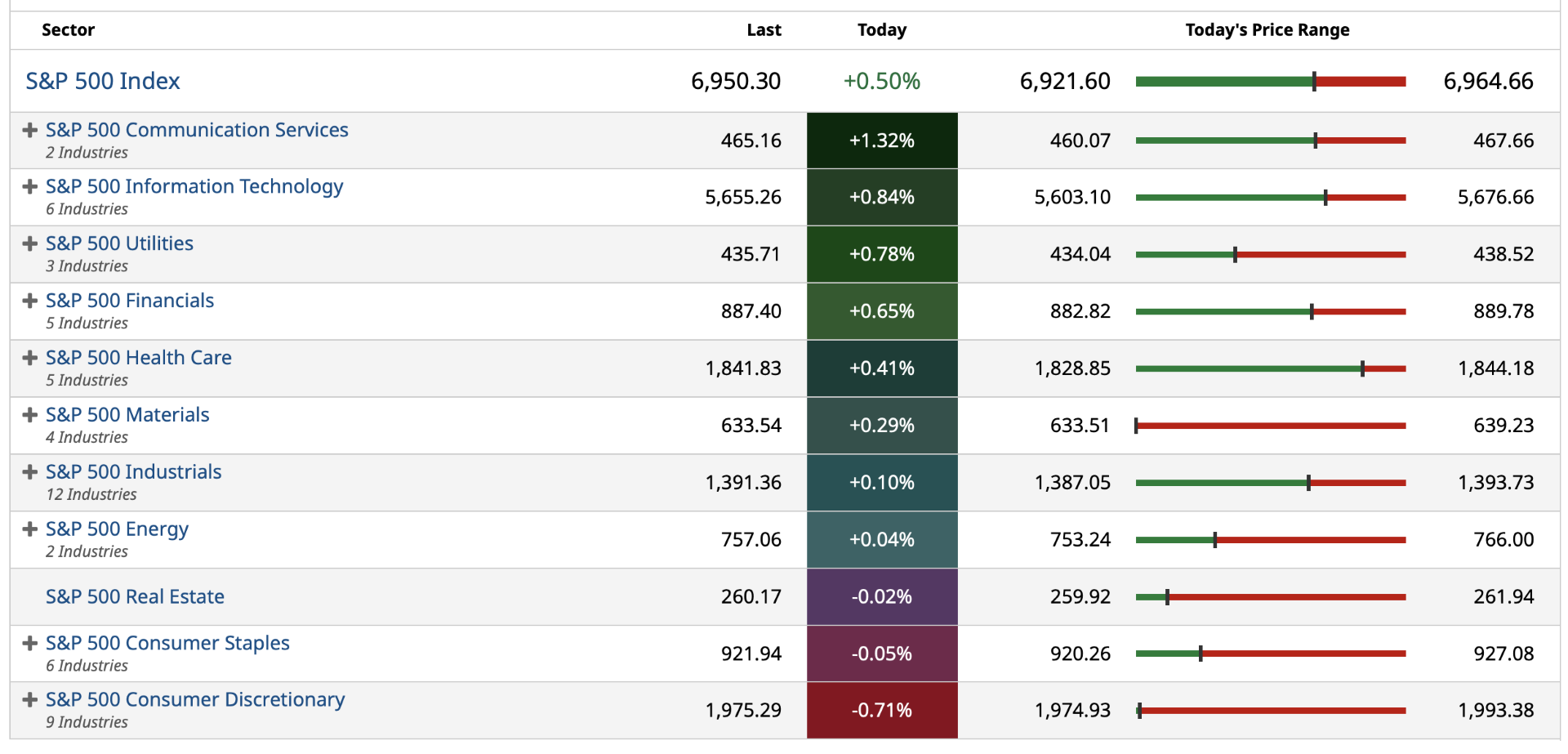

In terms of sector performance, technology was the world's fair ( (AMZN) +$5.59, (MSFT) +$15.56, (META) +$10.24, etc.) but financials spit the bit ( (AXP) -$7.75, (GS) -$36.55, (MS) -$4.31, (JPM) -$6.20, (APO) -$3.43, etc.)

For several years I have cautioned about the perils of market structure — with markets morphing into a voting machine rather than a weighing machine with the proliferation and, now, dominance of passive products and strategies that worship at the altar of price momentum:

Like water in a bathtub that swishes around, group performance changes repeatedly and rapidly.

I am uncertain what this means for the future direction of the markets, but historically weakness in financials portends weakness in the overall market. From my perch, as noted earlier, market participants are underpricing risk/volatility.

But this is something that bullish investment strategists will not point out because it doesn't fit with their bullish narratives.

BY Doug Kass · Jan 26, 2026, 9:30 AM EST

From Peter Boockvar:

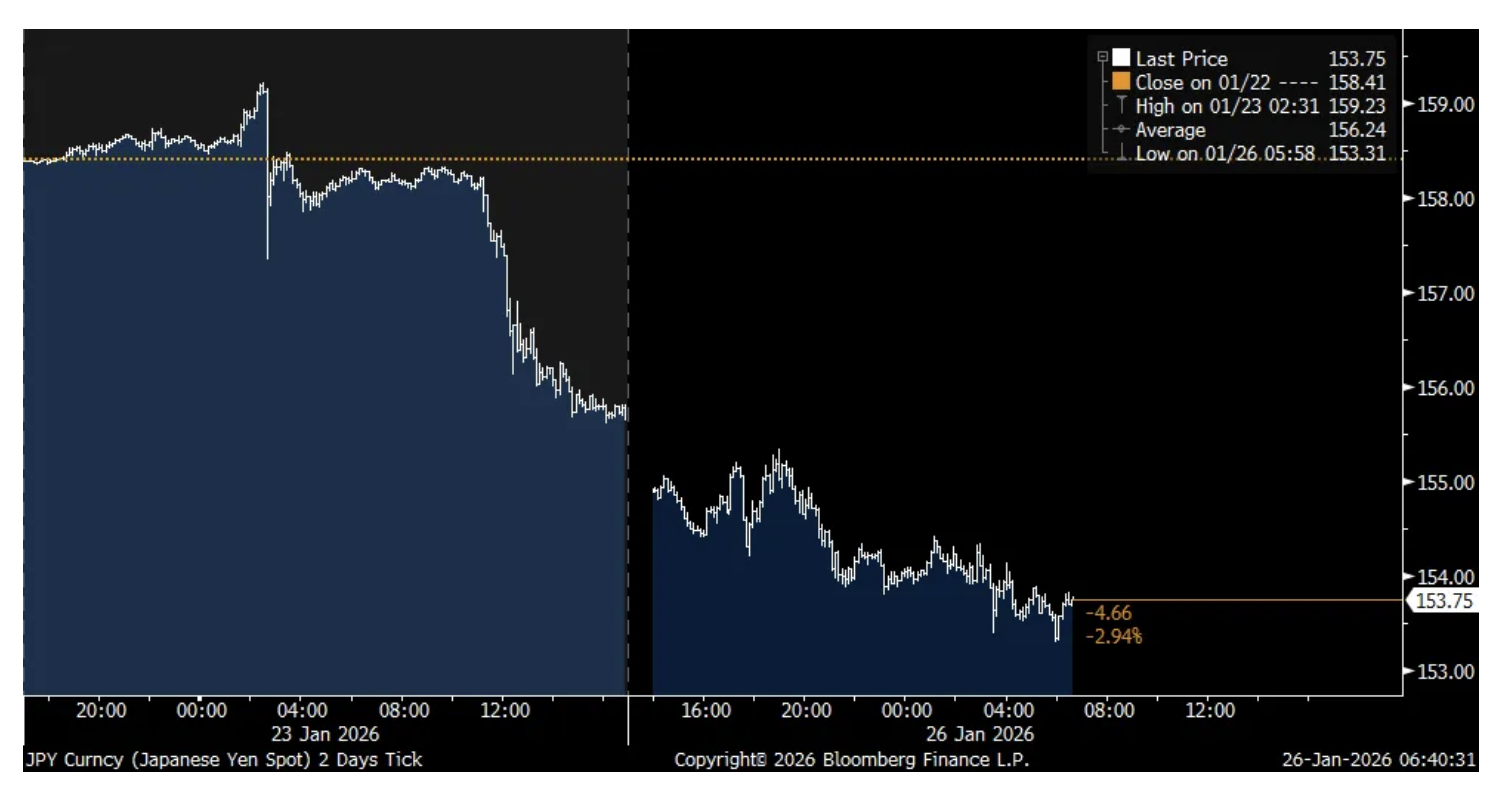

So it seems that about 160 on the yen/dollar cross rate is the line in the sand both for the Japanese and the US. I say the latter, as we’ve already heard for weeks the complaining on the part of the Japanese, because the talk on Friday of the US Treasury making a ‘rate check’ with trading desks which is another way of setting the stage for FX intervention. No confirmation of any intervention though but the signaling was enough to see quite the reversal from Friday night Japanese time to today. See below the intraday moves over the past two trading days.

The US dollar is also weak across the board. The euro is testing the highest level since September 2021. The British pound is just off a level last seen in January 2022. The Aussie$ is at the best level vs the US dollar since February 2023. The Singapore dollar is the strongest vs USD since 2014 and the Chinese yuan continues its rally and is at the highest point since May 2023.

Gold, silver and other metals continue to power higher in response. There are a bunch of major implications here if this US dollar weakness continues. Here are a few possible reactions:

1)The US starts to import inflation.

2)Foreign investors either increase the level of dollar hedging against their US holdings and/or they decide to sell their US asset, like stocks and bonds.

3)Commodity prices further rally.

4)While big US multi-national companies and manufacturers might benefit from a weaker dollar via exports, about 40% of imports are intermediate goods that end up in the finished product (circling this back to possibility #1).

5)A reduced purchasing power of the US dollar could limit US consumer spending.

6)It really complicates the job of the Federal Reserve, even though some of the weakening in the dollar is in anticipation of an easy Fed after Powell leaves.

7)Threatens long term interest rates and they rise in response.

To the incredible run in industrial metals prices by the way, I highly recommend a watch of this presentation given by Robert Friedland (hat tip Luke Groman in his great weekend FFTT piece) a few months ago as to the importance of them and the growing difficulty in procuring them. Robert, if you are not familiar, is probably the greatest metals entrepreneur over many decades with currently multiple Ivanhoe entities.

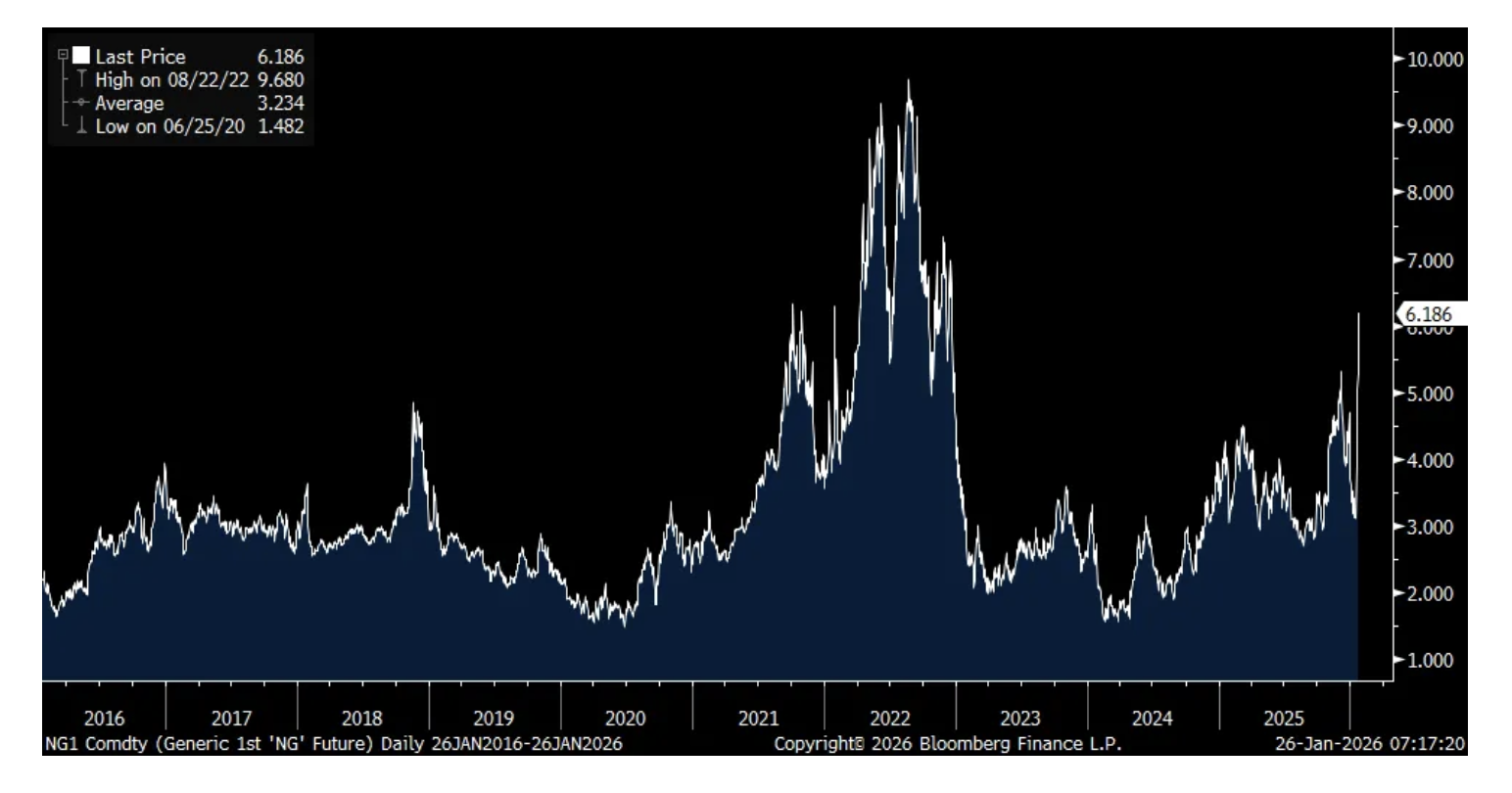

I do expect the industrial/precious metals bull market will widen out to energy and ag and we are positioned as such. Natural gas is today jumping by another 17% to over $6 and is up by 100% over the past 5 trading days for the obvious reason. It’s at a level last seen in December 2022.

Yen intraday

Natural Gas

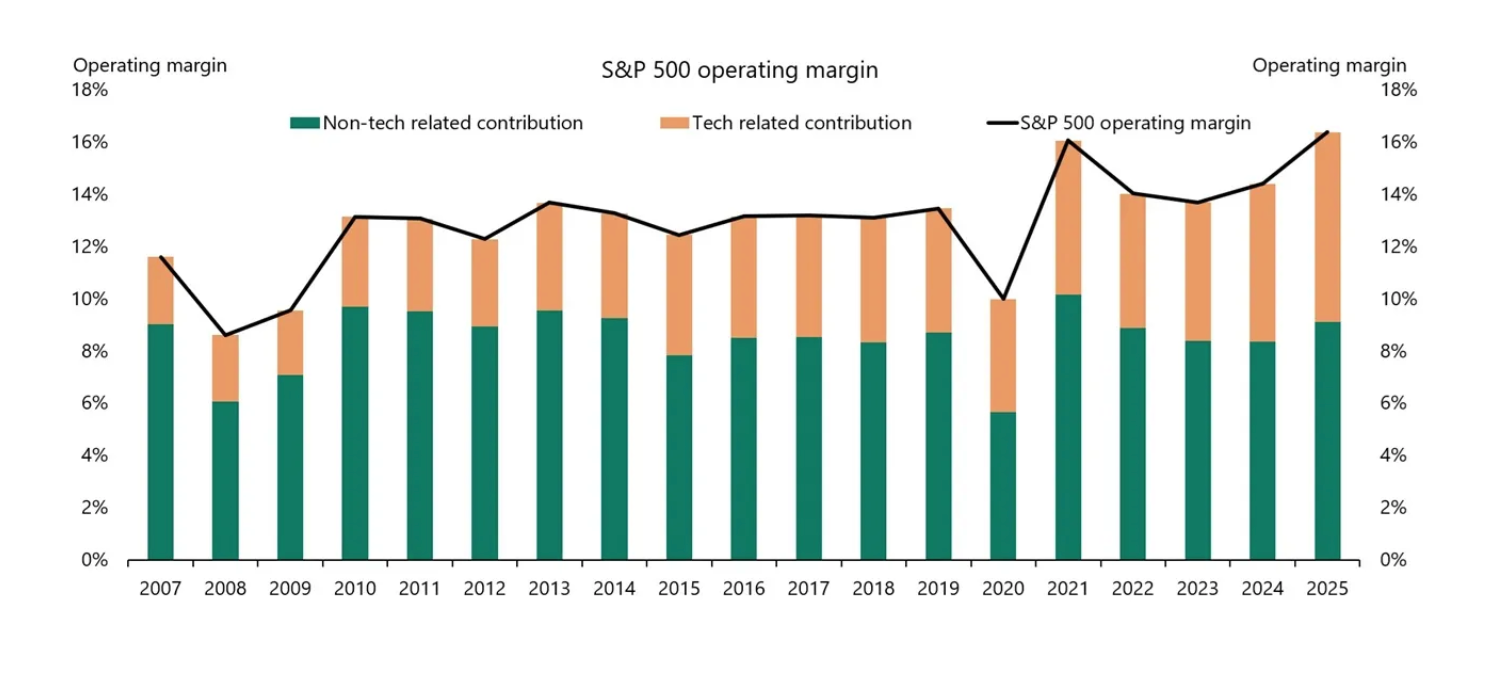

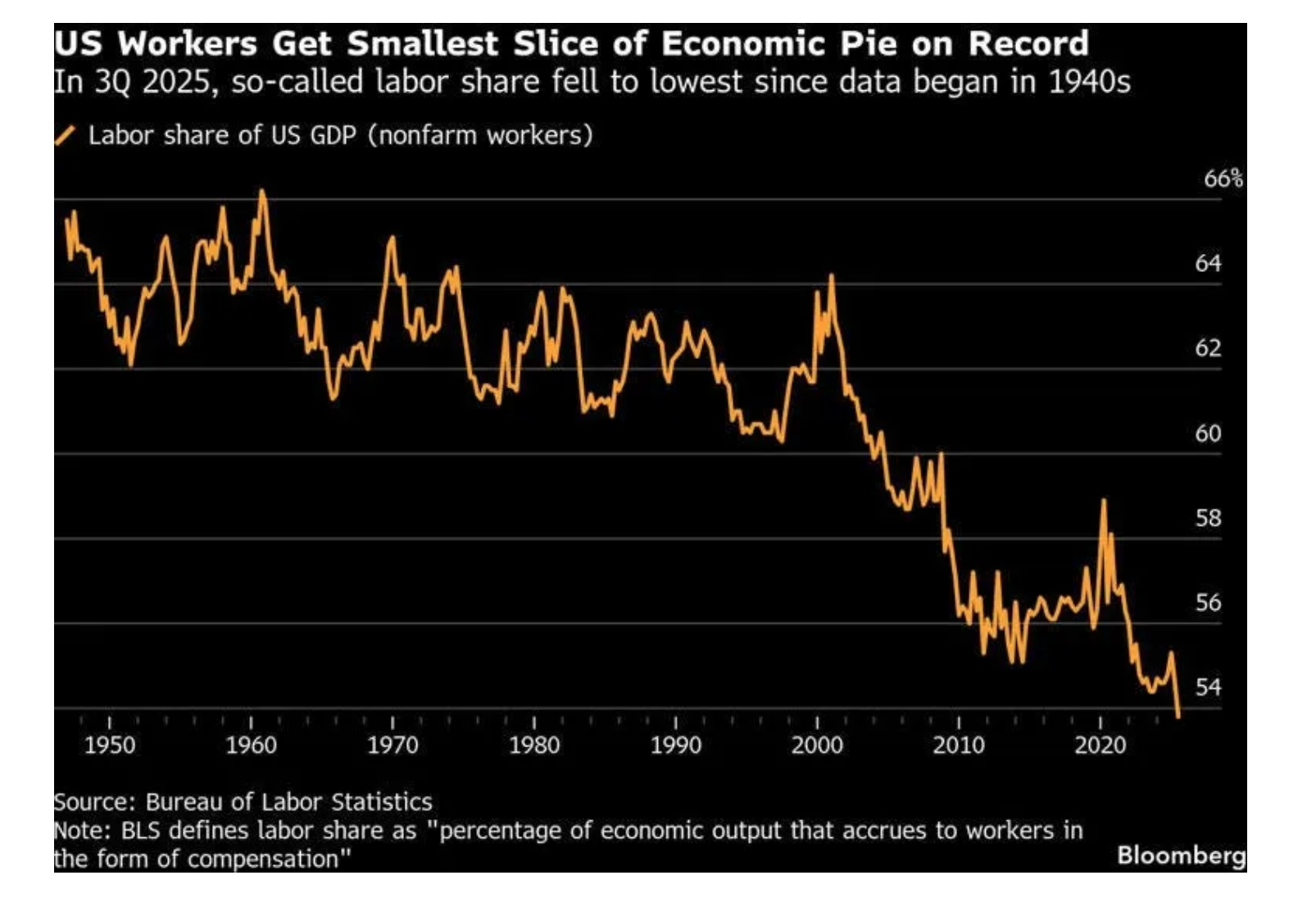

Ahead of a big few weeks of earnings I want to post two charts here. One from Torsten Slok on corporate profit margins and the big influence of big cap tech. The other from my friend Eric Rosen who writes the great Substack twice a week, The Rosen Report. His chart he mentioned a few weeks ago is one from Bloomberg that reflects the low level of labor income relative to GDP and we know that labor costs are a big part of corporate expenses. Both factors have helped to drive corporate profit margins to record highs and always begs the question over how sustainable it is, especially with the growing capital intensity of the tech/Gen AI business.

Keep in mind that when we discuss the valuations on the stock market it is not just a random P/E ratio that reflects it as it’s important too to understand at what level of margin is that multiple based on. Looking at the S&P 500 and with it trading at about 22x 2026 earnings, that is on record high margins making it crucial that margins can sustain themselves. Because if they can’t, the market is much more highly valued than just a 22x multiple. It is also why I like to look at price to sales, among other valuation metrics.

S&P 500 profit margin expansion coming from tech companies

Capital One fell 7.6% Friday and they said this of note on their call:

“The US consumer and the overall macroeconomy remains resilient. The unemployment rate inched up in 2025, but remains pretty low by historical standards. Layoffs and new unemployment claims are low and stable. Wages are still growing in real terms, and consumer spending remains robust. Debt servicing burdens remain stable and close to pre-pandemic levels.”

“Because of the budget bill implemented last summer, consumers will see larger tax refunds this year than last year, and tax withholdings will also be lower in 2026...But I do think we’re still in a period of elevated economic uncertainty. Inflation remains above the Fed’s target. Job creation slowed significantly in the second half of 2025. Some consumers are feeling pressure from the cumulative effects of price inflation, higher interest rates. And many of those relying on the Affordable Care Act for their health insurance will see their premiums going higher quite sharply in some cases. And so I think these uncertainties will hang over the economy and hang over the choices that consumers make.”

On credit quality, “We talked about the improvement in our charge-off rate has steadily improved, really through most of 2025. And in fact, in the fourth quarter, it was 113 bps lower than a year ago. And our front book of new originations continues to perform well. As we look ahead, delinquencies remain the best leading indicator of credit performance. Our card delinquencies improved steadily beginning in the second half of 2024 all the way through the first half of 2025, but we’ve now seen two quarters in which they’ve moved more or less in line with normal seasonality. This has been true both in our legacy Domestic Card portfolio and for Discover. And it suggests that credit is settling out after almost a year of steady improvement.”

Speaking of credit quality, please keep your eye on the LSTA leveraged loan index which closed on Friday at the lowest level since December 2nd. This is coincident with the news that the private credit fund BlackRock TCP Capital Corp (TCPC is the ticker) is taking a big haircut to the NAV of its holdings, by 19%. BlackRock said it “is primarily driven by issuer specific developments during the quarter.”

We should all have our eyes on the performance of private credit in light of the massive expansion of the asset class as there cannot be enough good loans around relative to the huge cash piling into credit manager coffers.

LSTA Leveraged Loan Index

BY Doug Kass · Jan 26, 2026, 9:00 AM EST

BY Doug Kass · Jan 26, 2026, 8:44 AM EST

BY Doug Kass · Jan 26, 2026, 8:37 AM EST

11 a.m.: Treasury buyback announcement (liq support);

11:30 a.m.: Treasury hosts a $89B 3- and $77B 6-Month Bill Auction;

1 p.m.: Treasury hosts a $69 billion 2-Year Note Auction

BY Doug Kass · Jan 26, 2026, 8:20 AM EST

BY Doug Kass · Jan 26, 2026, 8:03 AM EST

With S&P futures back to flat I am adding to my index shorts:

* (SPY) $689.06

* (QQQ) $622.26

BY Doug Kass · Jan 26, 2026, 7:30 AM EST

From JPMorgan:

US MKT INTEL – Tactically Bullish. Color on this week including an update on the consumer, earnings, FX, geopolitics, gov’t shutdown, inflation, macro data, and the retail investor. We make no WoW changes to the Monetization Menu

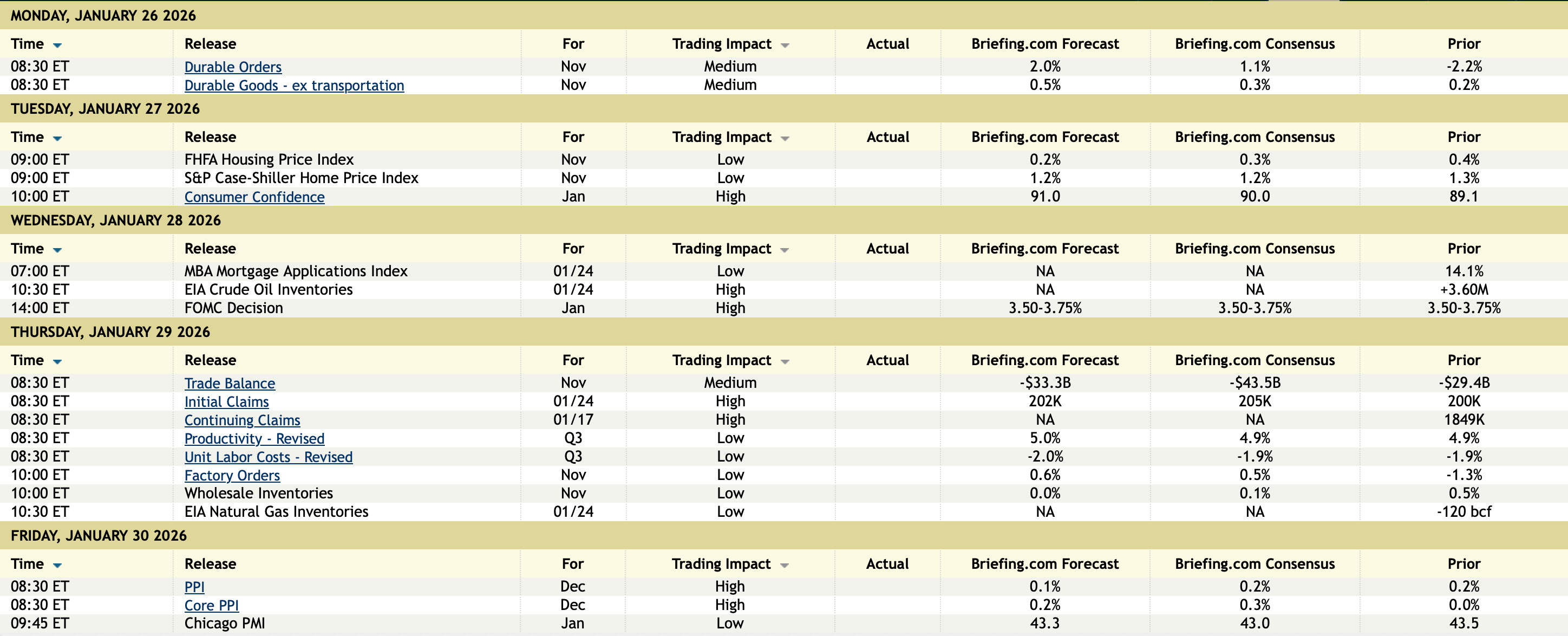

US: Futs are weaker but have retraced much of their overnight lows as geopolitics and USD/JPY roil markets ahead of a significant earnings week, as Mag7 earnings reports kick off this week. DXY falls as USD/JPY sees another significant decline on intervention risk. Bond yields are lower by 1-2bp as the yield curve bull steepens. The FX moves are triggering a surge in gold and silver, up 2% and 6% as PGMs outperform gold; Ags are higher and natgas remains the story within Energy. In Eqy pre-mkt, Mag7 names are mixed, Semis are weaker, but Energy / Materials are higher with their underlying cmdtys. Both Cyclicals (ex-cmdtys) and Defensives are weaker pre-mkt. Today’s macro data focus is on Cap Goods / Durables and regional Fed activity indicators.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

The SPX fell 35bp last week, marking the 3rd loss in 4 weeks as geopolitics dominated the narrative; but, the index is +1% on the year (Equal-weighted SPX is +3.7% YTD). NDX outperformed on the week, with its third consecutive weekly gain; whereas, RTY printed a 32bp loss. With the Fed likely on hold this week, geopolitical tension cooling, and a resilient macro story, the market’s focus shifts back to earnings.

Tactically Bullish. As we move past Greenland, Trump threatened Canada with a 100% tariff if they sign a trade deal with China. This may produce a very short-term overhang to the market, ultimately, we think the market will look through this given (i) expectations for the SCOTUS to halt Trump’s usage of emergency tariffs; (ii) this being viewed as a negotiating tactic ahead of the USMCA renegotiation; and (iii) the recency of Trump’s Greenland pivot likely having investors think that anything that would be a material negative on affordability into the midterms is unlikely to last. US / Canada total trade in Goods and Services is ~$1T

· MONETIZATION MENU (same as the Jan 12 & 22 editions) – (i) We like TMT as a core holding, including Mag7, Semis, China Tech, and AI plays. For AI, we like the Core AI and TMT-focused AI baskets (JPAICORE Index and JPAITMT Index); though we would holder a lower the allocation relative to the balance of Tech. (ii) The US / Global Growth Reboot remains attractive and like holding a combination of Airlines (JP2AIR Index), Cyclicals (JPACYCL Index), Financials (both KRE and XLF), Retailers (JP2RTL Index), and Transports ex-Airlines (JP1BTXA Index). The RTY is another beneficiary of this theme. (iii) International plays are likely to perform at least in line with the SPX and we like China, Japan, and South Korea within APAC, broader Latam including Brazil. (iv) Debasement – this theme was very profitable in 2025 and think that trend continue in the very near-term as geopolitical turmoil renews interest. Within this theme we like gold, silver and their associated miners (GLD, SLV, GDX, SILJ, and XME)

BY Doug Kass · Jan 26, 2026, 7:10 AM EST

BY Doug Kass · Jan 26, 2026, 7:00 AM EST

Bonus - Here are some great links:

IGV v SMH - The Most Oversold Ever

BY Doug Kass · Jan 26, 2026, 6:45 AM EST

BY Doug Kass · Jan 26, 2026, 6:35 AM EST

Friday was one of the wildest days I have witnessed in a long time — from a sector volatility standpoint.

I think the VIX at 16 and change is underpricing risk.

Thinking about how I can get long volatility.

More to come on Friday, this morning...

BY Doug Kass · Jan 26, 2026, 6:25 AM EST

Shorting the indices further:

* (SPY) $688.46

* (QQQ) $621.23

BY Doug Kass · Jan 26, 2026, 6:15 AM EST

BY Doug Kass · Jan 26, 2026, 6:05 AM EST

The S&P Short Range Oscillator remains overbought at 2.91% vs. 4.44%.

BY Doug Kass · Jan 26, 2026, 5:55 AM EST

Dougie Kass

S and P futures have rallied from -56 to -14 Sunday evening.

I am back shorting (SPY) /QQQ common:

BY Doug Kass · Jan 26, 2026, 5:45 AM EST