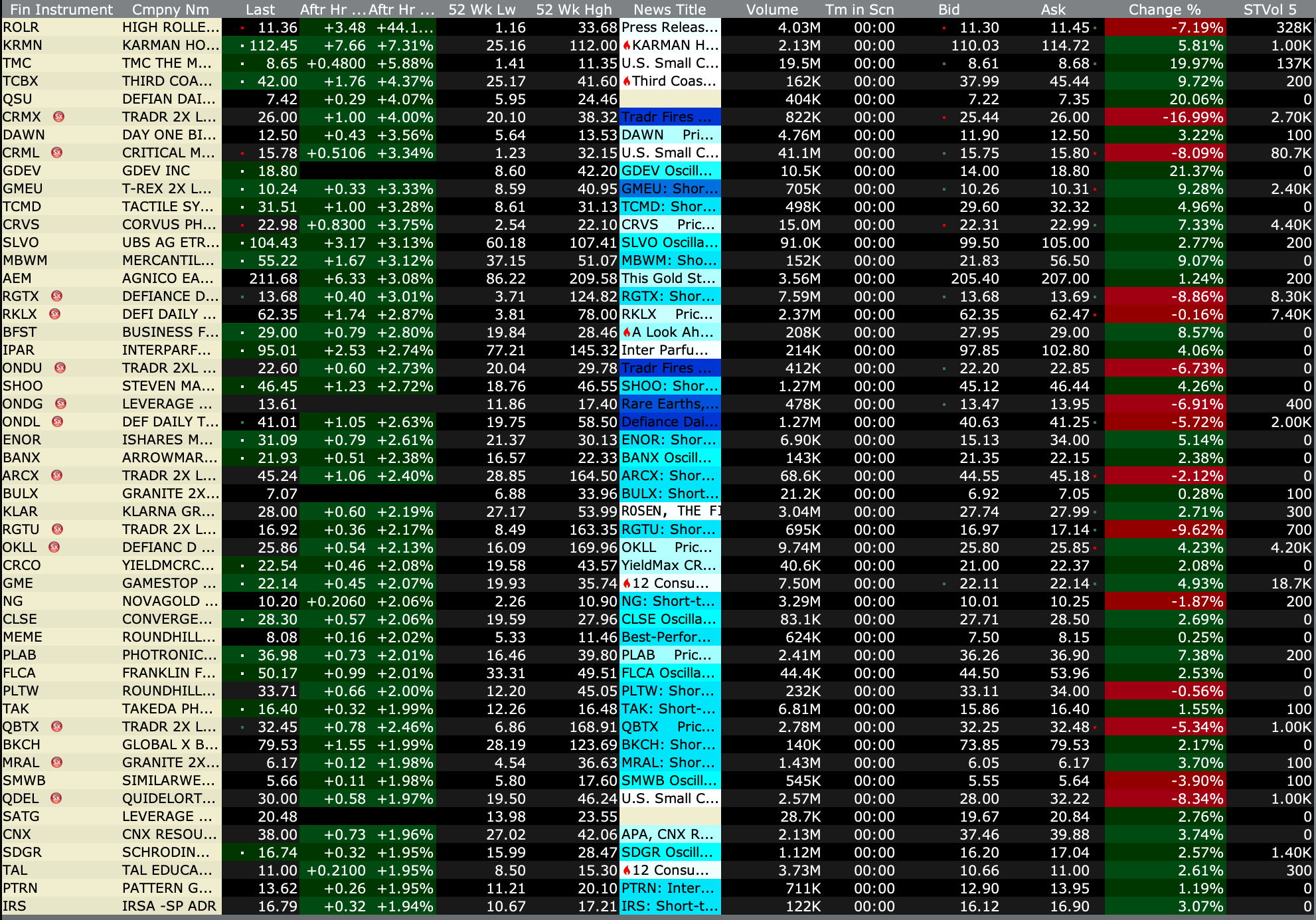

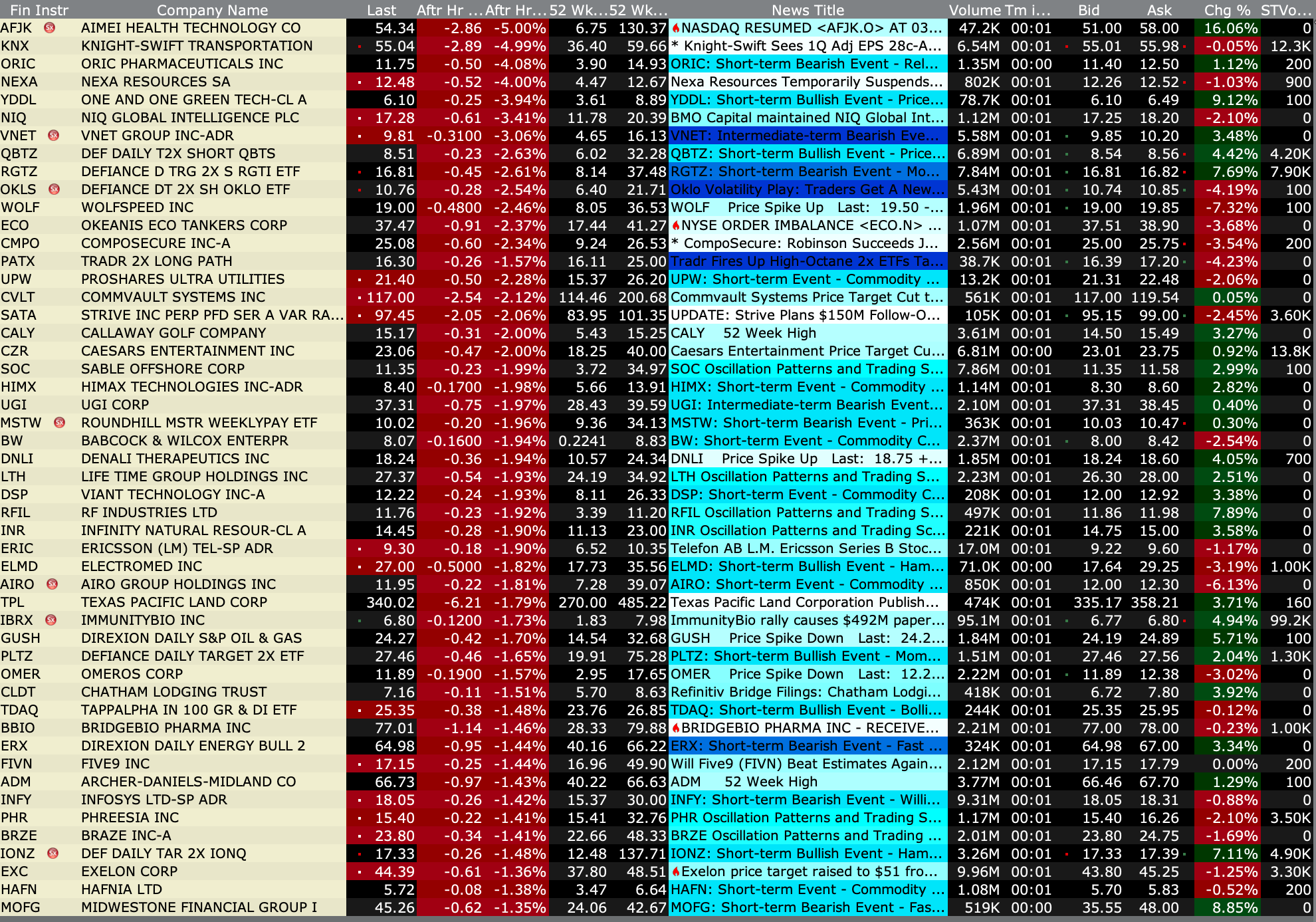

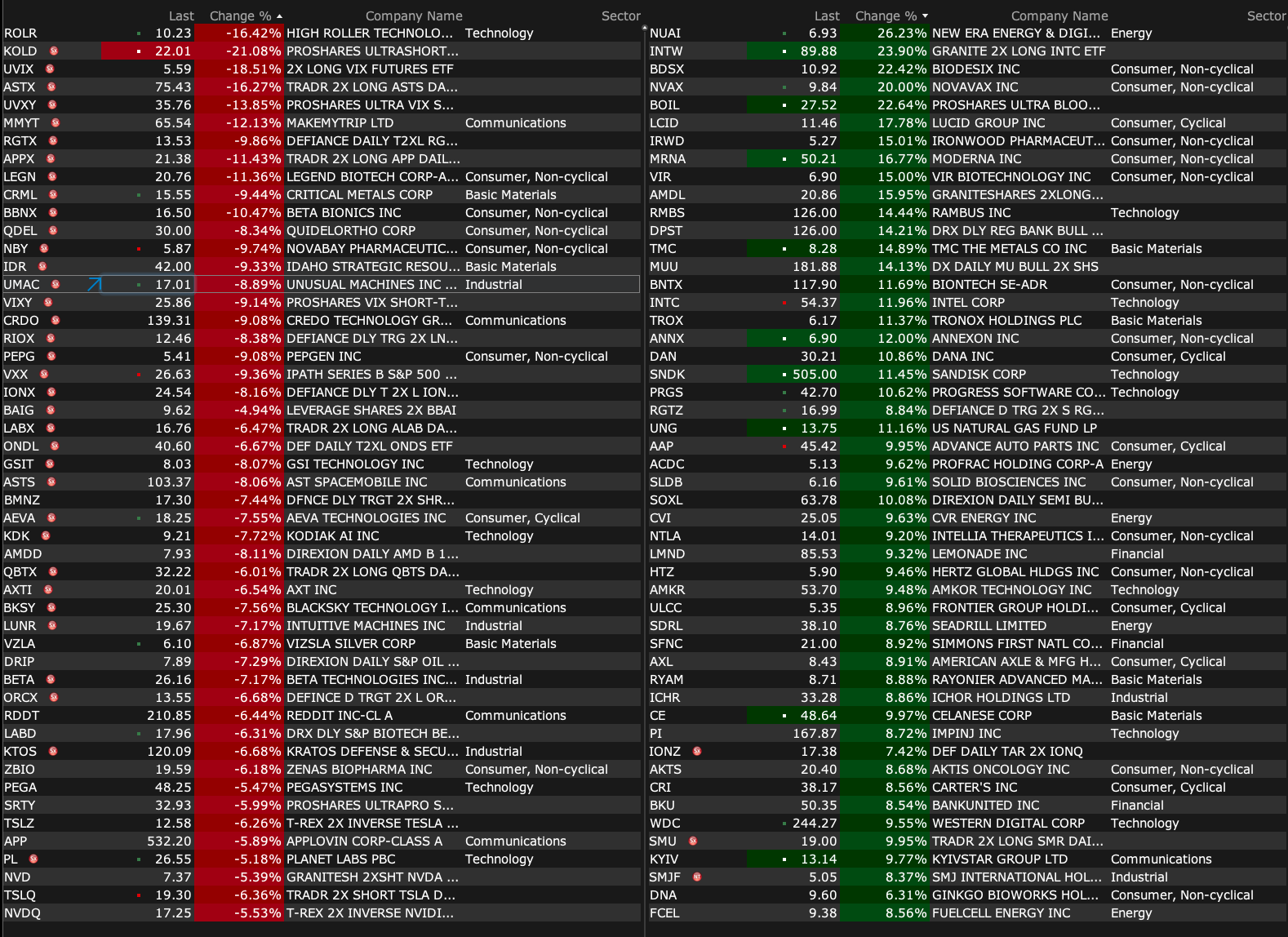

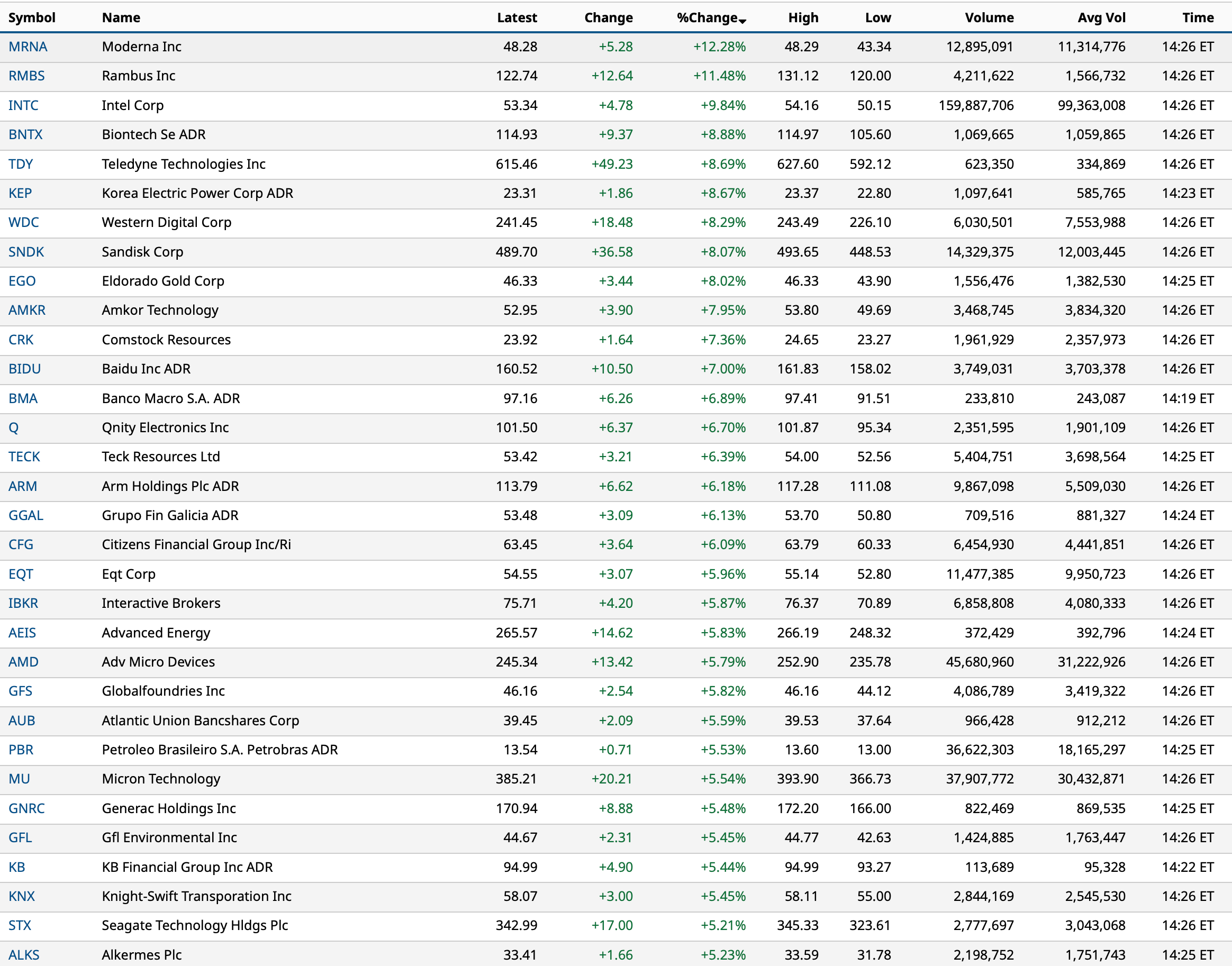

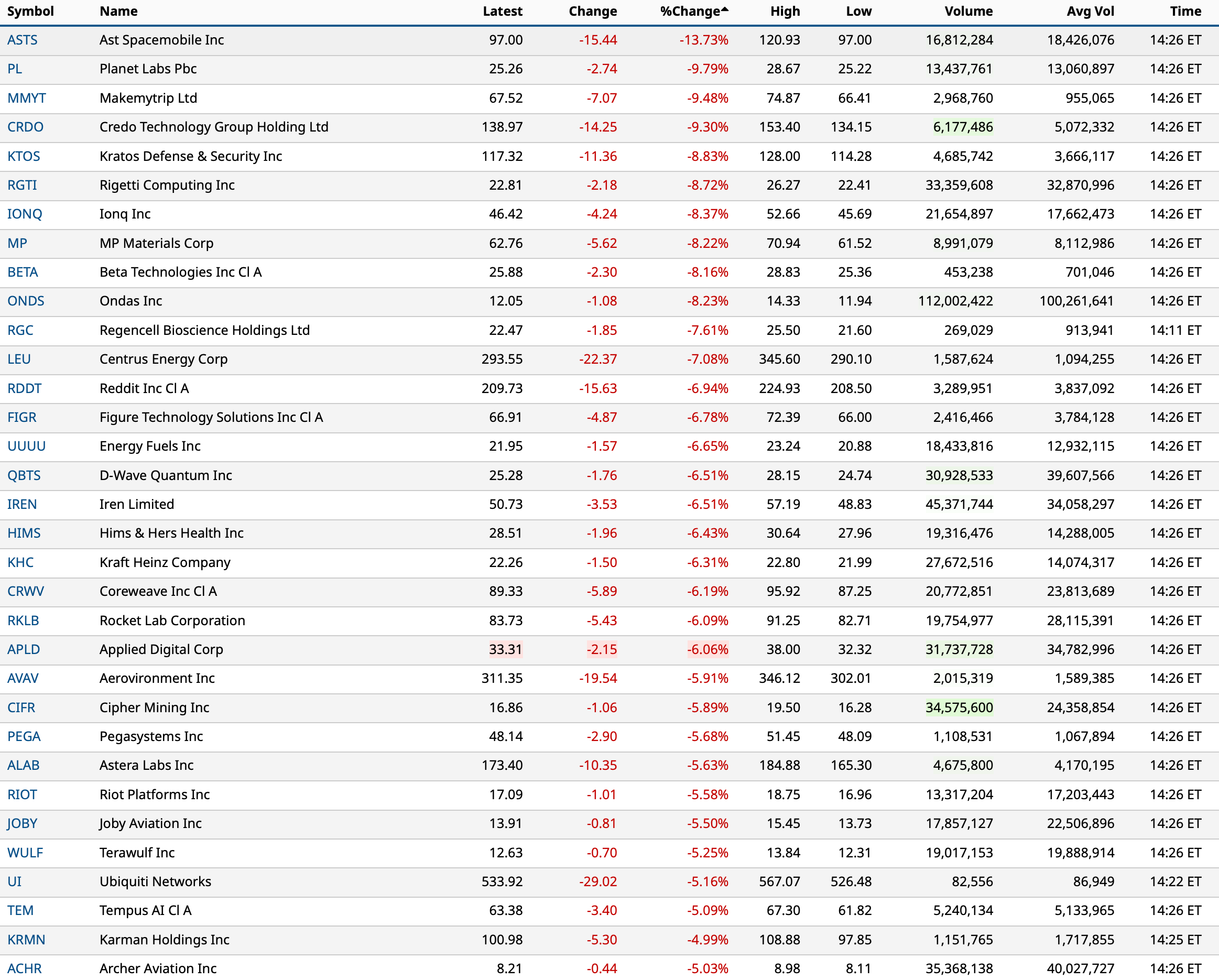

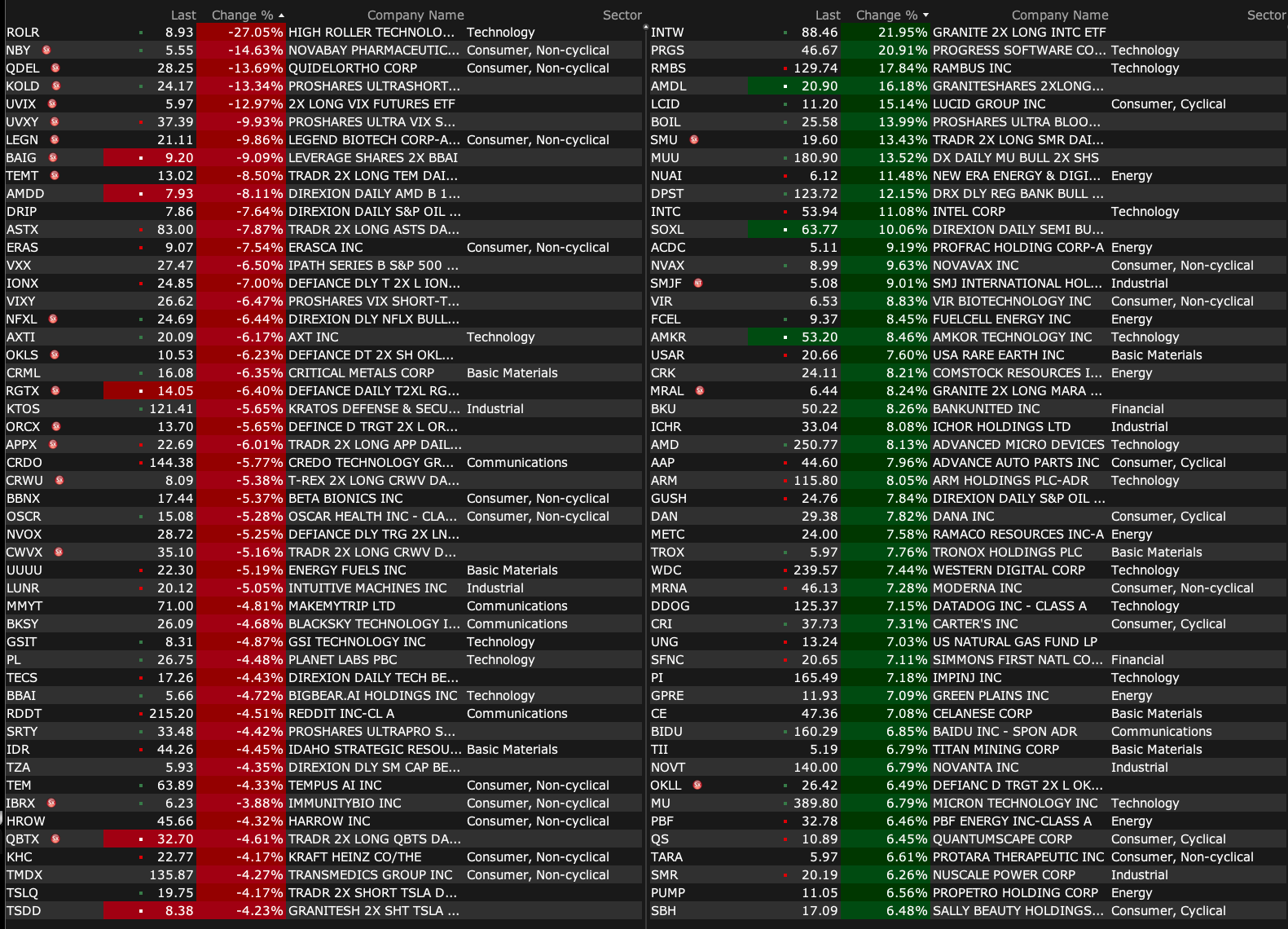

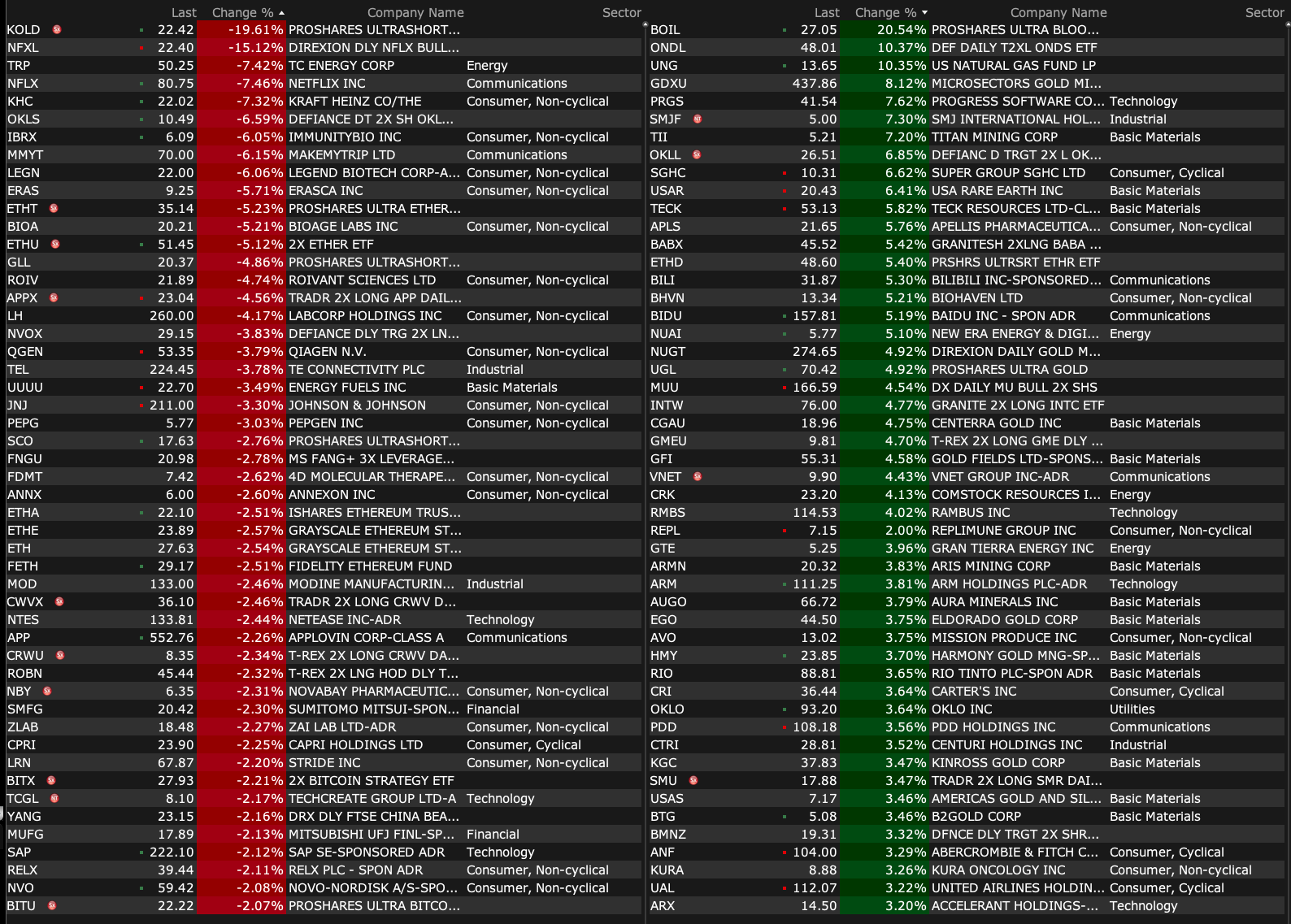

After-Hours Gainers and Decliners

After-Hours % Gainers

After-Hours % Decliners

BY Doug Kass · Jan 21, 2026, 4:45 PM EST

BY Doug Kass · Jan 21, 2026, 4:45 PM EST

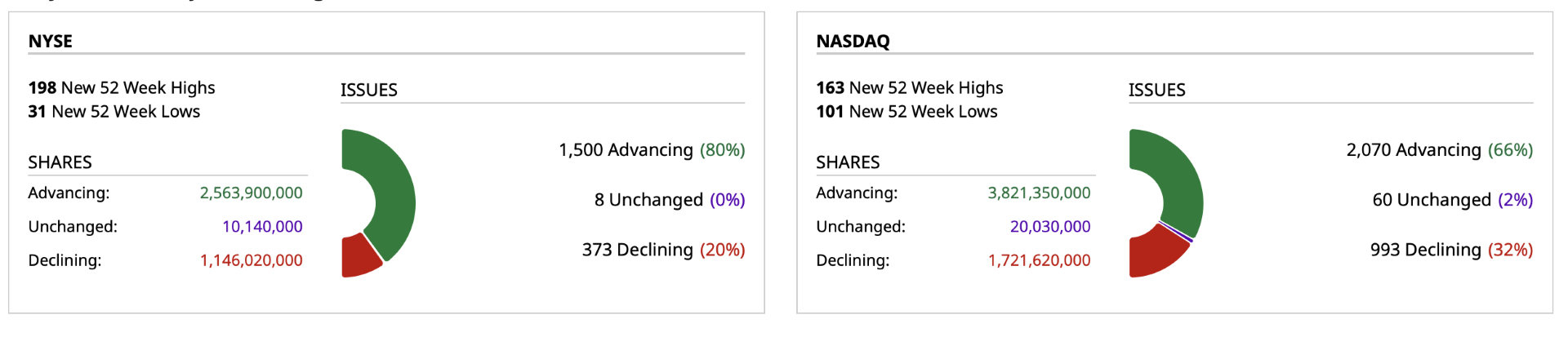

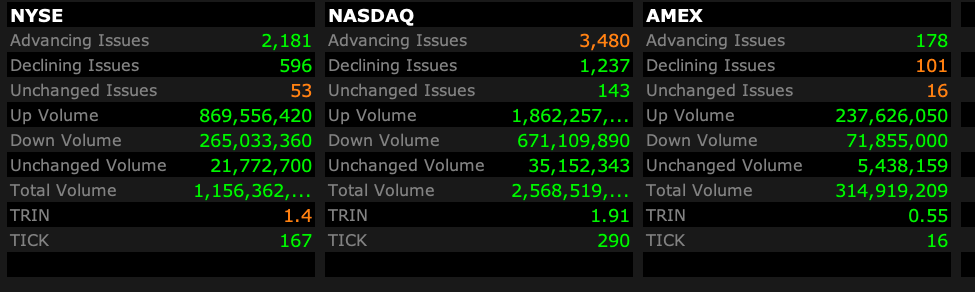

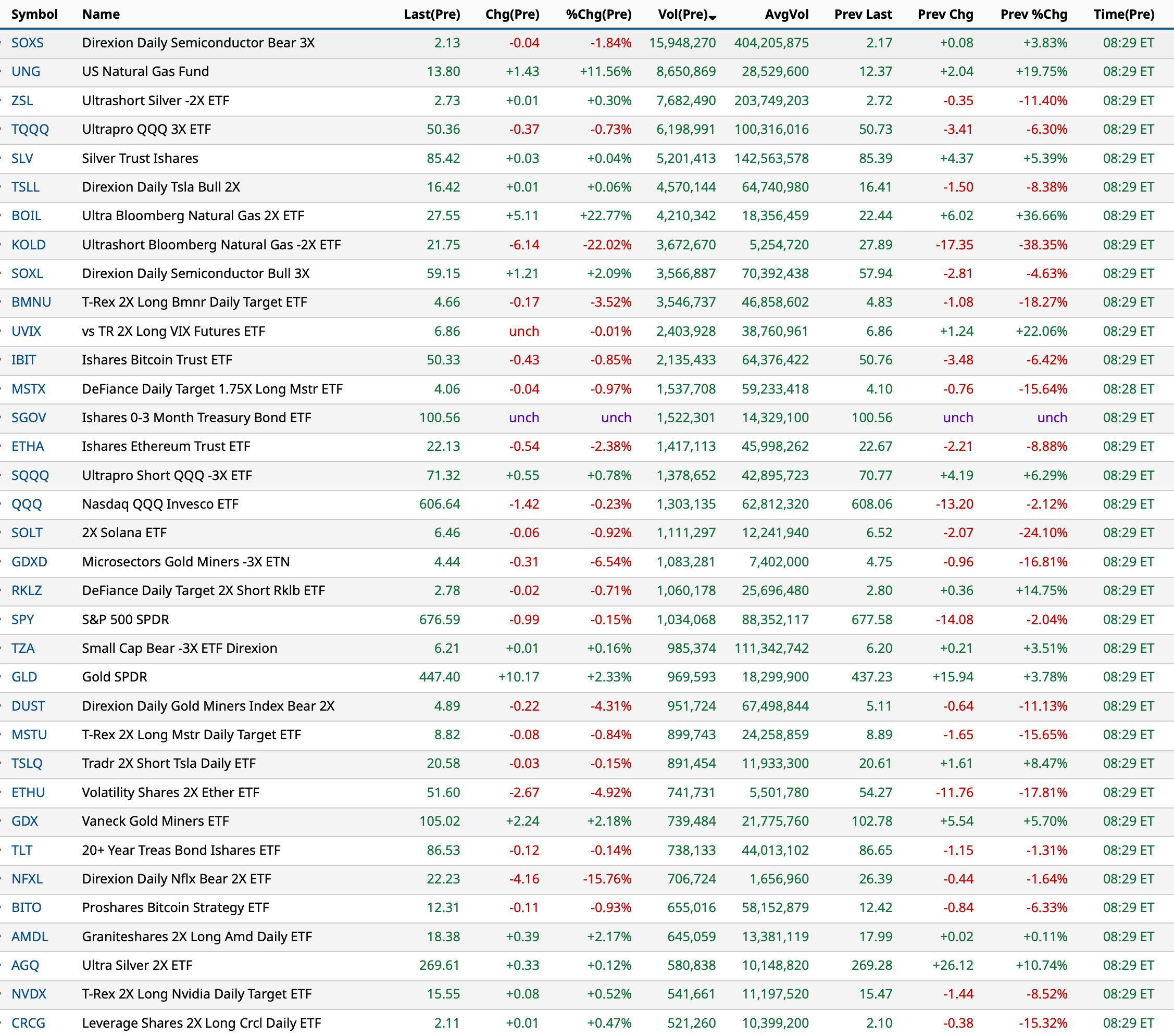

- NYSE volume 24% above its one-month average

- NASDAQ volume 12% above its one-month average

- VIX index: down 15.48% to 16.98

BY Doug Kass · Jan 21, 2026, 4:27 PM EST

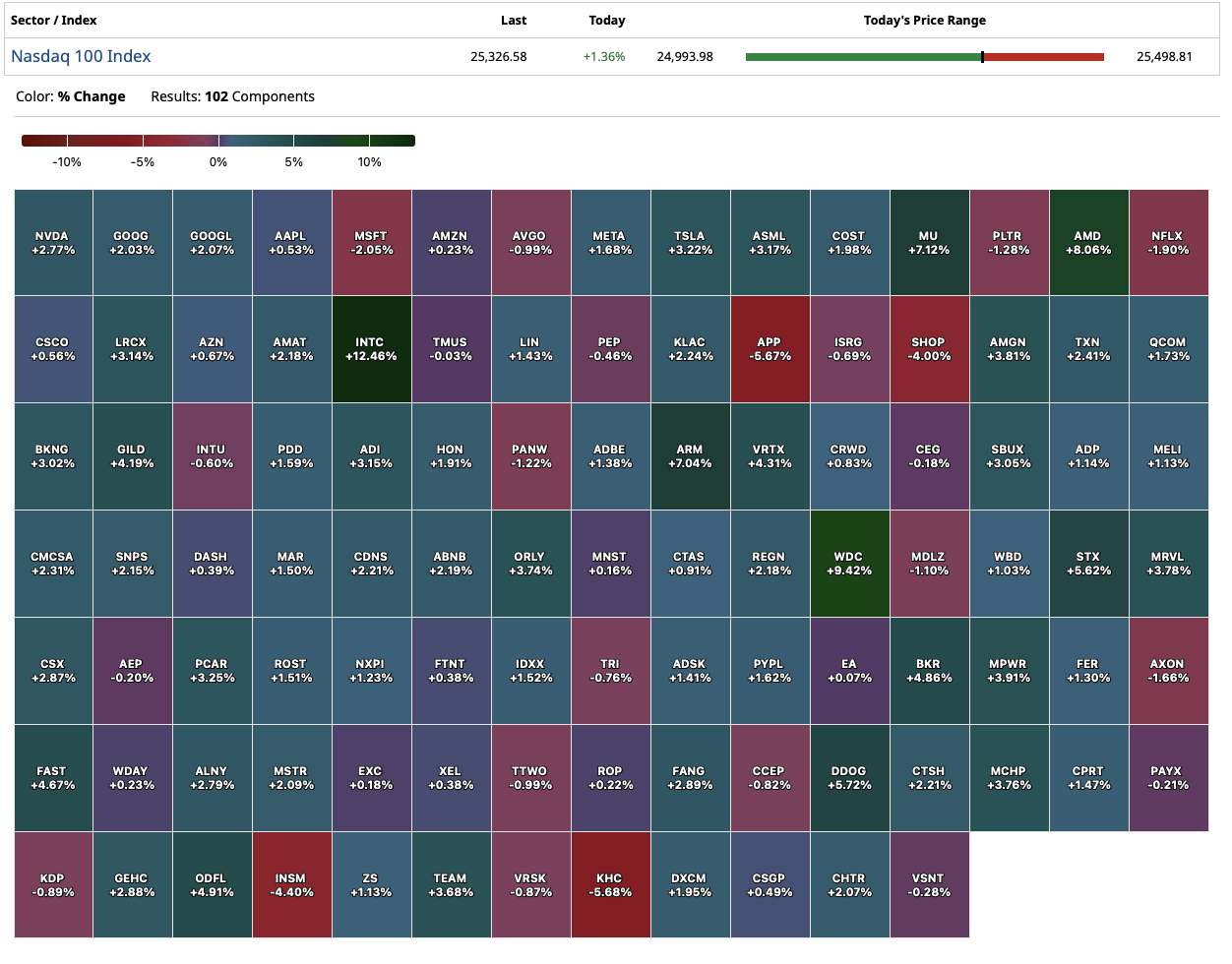

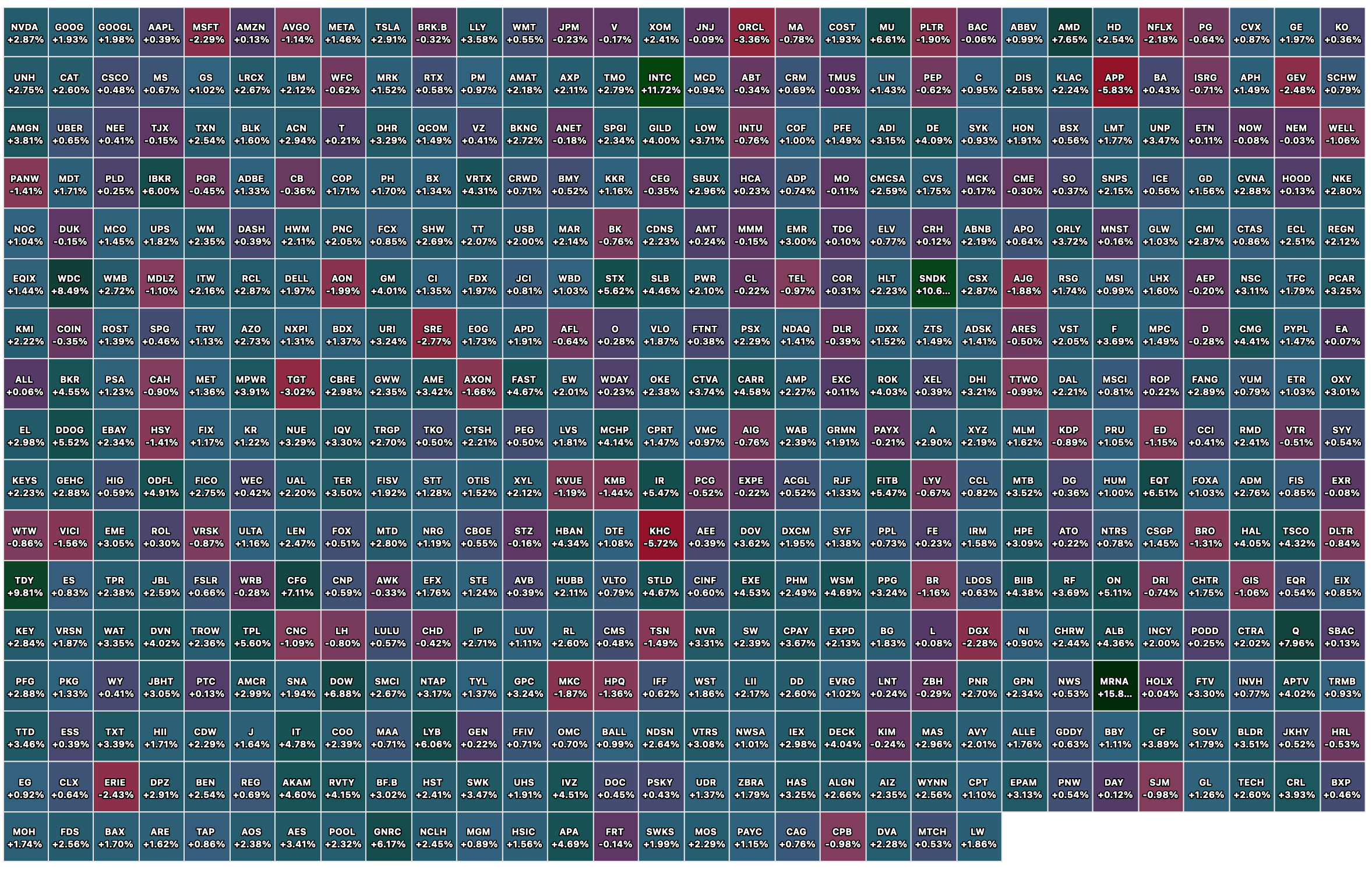

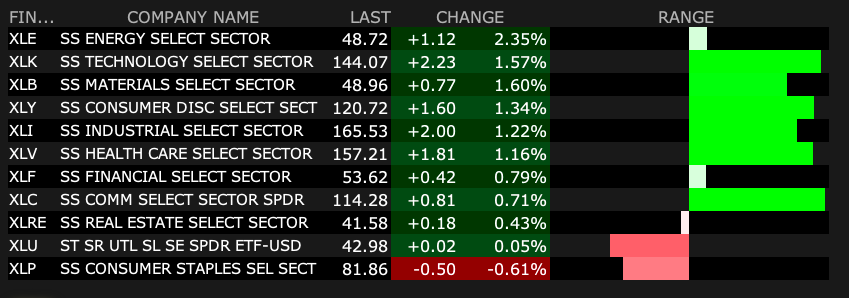

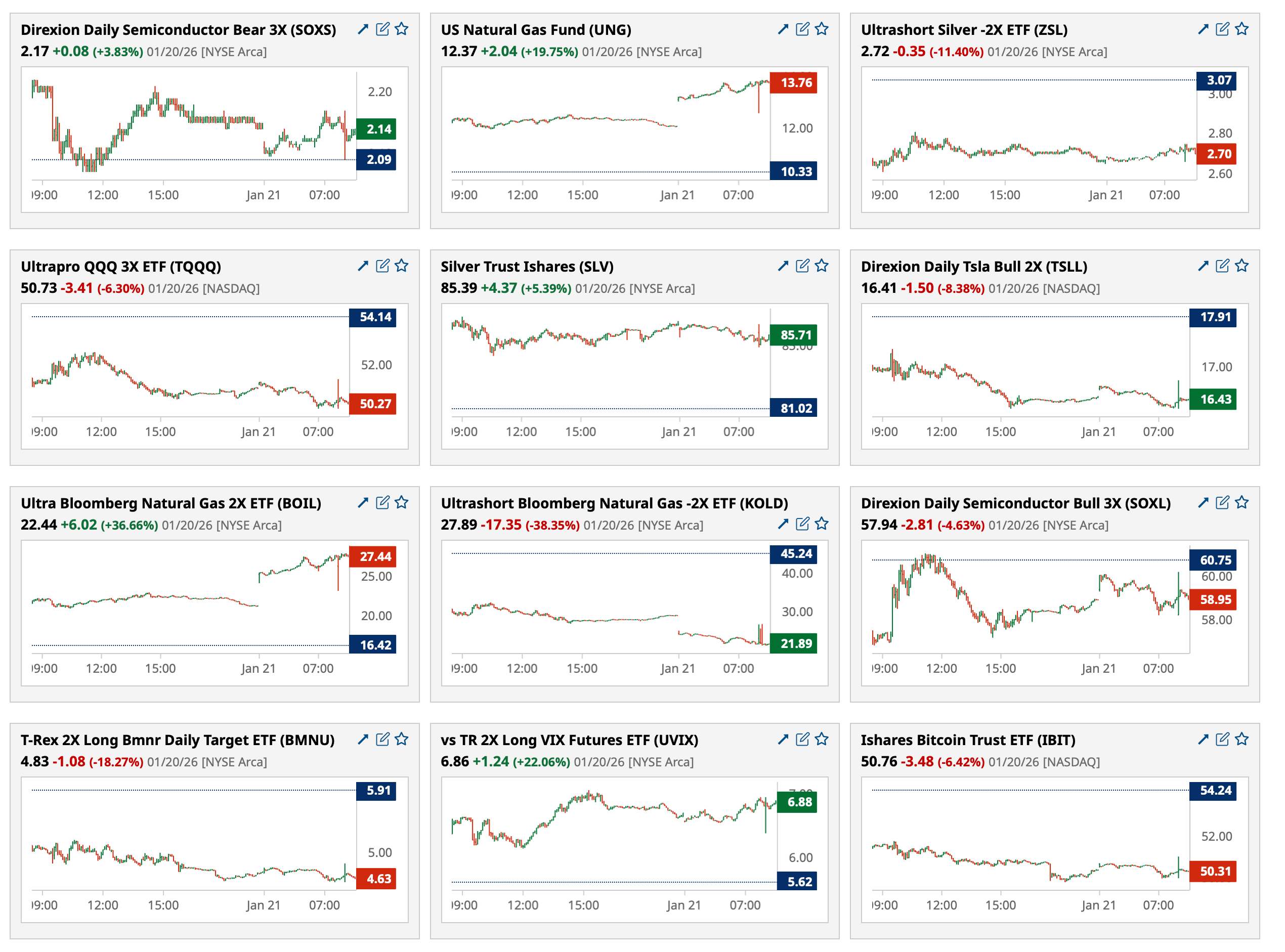

Look at the intraday charts of the Tech ETF (XLK) and compare it to the Financials ETF (XLF) below.

While XLK retraced half the gain, the XLF retraced almost all of the noon Trump Greenland/tariff news:

BY Doug Kass · Jan 21, 2026, 4:20 PM EST

BY Doug Kass · Jan 21, 2026, 4:02 PM EST

BY Doug Kass · Jan 21, 2026, 3:58 PM EST

I have taken an initial short position in the Russell index:

* (IWM) at $267.86

BY Doug Kass · Jan 21, 2026, 3:35 PM EST

BY Doug Kass · Jan 21, 2026, 2:50 PM EST

This is a great tweet and it makes me nostalgic.

It is a video of my appearance at Berkshire Hathaway's Annual Meeting a decade ago with Charlie Munger and Warren Buffett:

BY Doug Kass · Jan 21, 2026, 1:00 PM EST

With S&P cash +29 handles (it was +75 handles only 45 minutes ago!) I am taking in all my short index calls.

I plan to re-short on strength.

This is an ideal trading market, but not so great for the buy-and-hold crowd.

PS: I have a routine annual physical today at 2 PM.

BY Doug Kass · Jan 21, 2026, 12:01 PM EST

Equities fall from comments in Davos that Greenland will not negotiate with President Trump.

BY Doug Kass · Jan 21, 2026, 11:50 AM EST

(XLK) vs. Financials (XLF) as of 11:21 AM:

BY Doug Kass · Jan 21, 2026, 11:42 AM EST

- NYSE volume 13% above its one-month average;

- Nasdaq volume 8% below its one-month average;

- VIX index: down 12.99% to 17.48

BY Doug Kass · Jan 21, 2026, 10:52 AM EST

I'm shorting (JOET) again.

BY Doug Kass · Jan 21, 2026, 10:16 AM EST

With S&P cash +53 handles I have sold my long indexes:

* (SPY) $682.55

* (QQQ) $ 612.55

BY Doug Kass · Jan 21, 2026, 10:07 AM EST

With S&P cash +46 handles I am aggressively shorting Index calls.

BY Doug Kass · Jan 21, 2026, 9:54 AM EST

BY Doug Kass · Jan 21, 2026, 9:50 AM EST

From Peter Boockvar:

JGB’s are rebounding after a brutal day and a rough few years. Understand that the rise in JGB yields really started in the summer of 2023 when the BoJ ended yield curve control, further lifted by a reduction in BoJ bond purchases, rising inflation and with the BoJ slow crawling interest rate increases but it’s now clear that debts and deficits matter in the eyes of bond investors and the demand for long duration exposure continues to wane.

Helping the rally today was the Japanese Finance Minister speaking in Davos on Bloomberg TV, “I’d like everyone in the market to calm down.” She also said “Since last October, our fiscal policy has consistently been responsible and sustainable, not expansionary, and the numbers clearly demonstrate that.”

After spiking by 37 bps over the past two days, the 30 yr JGB yield is lower by 14 bps. The 10 yr yield is down by 7.4 bps after rising by 17 bps this week. The yen is up slightly.

As global rates rise around the world, when looking at the US Treasury market, foreign ownership is at about 30% of the market vs 50% 15 years ago and I expect that percentage to continue to drop. Reasons will be continued diversification out of the US dollar and global competition with yields.

I will argue again too that the rally in the Chinese yuan to the highest level since May 2023, which is not by accident, is one of the biggest things to happen year to date for a few reasons. Number one, it creates an umbrella for other Asian currencies to rally which in turn makes US dollar assets like Treasuries less attractive. Number two, along with the anti-involution policies now being implemented in China, China exporting deflation around the world is over.

The world is changing big time in front of our eyes, the direction of global trade flows is morphing and diversifying and investors need to have a global lens when investing in the coming 5-10 years as it’s not going to be just about the US, the S&P 500 and the Mag 7. At the same time, gold is now becoming the most important global reserve currency. It’s up another $100 and we remain positive and long.

Fastenal was down 2.6% yesterday and they said this of note yesterday:

“We achieved double digit growth in Q4 with daily sales up just over 11%, and we continue to gain market share despite a sluggish industrial economy.”

“Looking at the broader operating environment in the fourth quarter, the US economy continued to send mixed signals, especially in the industrial sector. While some areas showed resilience, others faced continued headwinds that impacted demand and supply chains.”

“US PMI and industrial production remained mixed in Q4, with heavier manufacturing segment showing relative weakness. PMI average was in the low 48s for the quarter, while industrial production was close to flat compared to last year, although with some improvement late in the quarter.”

“Turning now to pricing...We implemented targeted price adjustments across select product categories, bringing our y/o/y price increase impact to approximately 3% for the quarter on matched product. These actions were designed to offset higher input costs, which they did, while remaining competitive in a challenging environment.”

From DR Horton, down 1.8% yesterday:

“New home demand remains impacted by affordability constraints and cautious consumer sentiment.”

“We increased our sales incentives during the first quarter, and we expect incentives to remain elevated in fiscal 2026, with a level dependent on demand, changes in mortgage interest rates, and overall market conditions.”

To a question on the impact on demand in response to the recent drop in rates (which has since reversed up), “As we enter into the spring and the first two weeks, really too early to tell what we’re going to see as far a trajectory into the spring, but when we see those kind of rates, moves in rates, and hovering right around 6%, it does spur some activity in our sales offices.”

By the way, mortgage applications lifted w/o/w with purchases up 5.1% and refi’s jumped 20.4% with the drop in rates. We’ll of course see what the reaction is to the reversal higher.

From MMM, down 7% yesterday:

“The macro remains soft and largely unchanged from Q3, but due to our strong execution, we’ve outperformed.”

“General industrial, safety and electronics, collectively about 65% of our business, came in better than expected, with exceptional y/o/y strength in the second half in electrical markets, aerospace and self contained breathing apparatus, all of which were up low double digits. Abrasives, industrial adhesives and tapes and electronics were all up mid single digits.”

“Auto and auto aftermarket remained soft as expected, while our consumer segment and roofing granules business were weaker than expected.”

From Fifth Third Bank, up 2% yesterday:

“Fourth quarter average loans increased 5% y/o/y, driven by 7% growth in consumer loans and 7% growth in middle market and business banking C&I loans.”

“Net charge-offs were 40 bps for the quarter, the lowest level in the past seven quarters.’

“Industry loan growth continues to be concentrated in lending to non-depository financial institutions, which represented approximately 60% of total industry loan growth and virtually all non-real estate and non-consumer related loan growth in the second half of 2025.”

But Fifth Third only has modest exposure to lending into this space.

On corporate loan growth this year, “Wild card here at the end of the day is going to be what - for lack of a better term - we’re calling chronic postponement syndrome internally, which is the tendency for our clients to postpone really large capital investments in the face of uncertainty. So they all feel, I think on balance, I don’t think they feel the same or better about ‘26 than they did about ‘25. And I think they’re all excited about tax reform. Rates have been helpful, but they really have been sort of south to the accumulated increase in costs, more than anything else in terms of the business. But they want to believe that they’re making multiyear investments into an environment where the rules of the road are going to be stable.”

“And so the question really is going to be, do they feel like they have that stability, or do they feel like there’s a risk that the window closes to make those investments? Or do we just continue to deal with this chronic postponement syndrome as a drag on broader utilization and C&I activity? So that’s sort of where we are.”

Overseas, the December UK CPI was higher by 3.4% y/o/y, one tenth above the estimate and up from 3.2% in the month before and the upside was led by airfares and tobacco. The core rate at 3.2% though was one tenth below expectations and is unchanged with November. Services inflation remains the pain point with an increase of 4.5% y/o/y. Bottom line, the UK economy remains in a stagflationary economic situation with only modest growth and still sticky inflation.

The 10 yr UK inflation breakeven was little changed in response but at 3.1% is at the highest level since October.

Also out of the UK, the January CBI industrial orders index rose a touch to -30 from -32 but obviously deeply negative. CBI said this:

“Manufacturers are finding conditions extremely tough, with output and orders falling again. Many firms report seeing customers delay decisions, order only what they strictly need, or hold back from committing altogether, leaving order books thin and confidence fragile.

“At the same time, cost pressures – from rising wages, high energy prices and taxes – are squeezing margins and weighing on competitiveness, pushing firms to plan price rises even as demand remains subdued.”

BY Doug Kass · Jan 21, 2026, 9:35 AM EST

BY Doug Kass · Jan 21, 2026, 9:05 AM EST

BY Doug Kass · Jan 21, 2026, 9:00 AM EST

11:30 a.m.: Treasury hosts a $69B 17-Week Bill Auction;

1 p.m.: Treasury hosts a $13B 20-Year Bond Auction

BY Doug Kass · Jan 21, 2026, 8:55 AM EST

BY Doug Kass · Jan 21, 2026, 8:45 AM EST

* Though it is still early in the year, one of my surprises — that a basket of consumer staples ( (PEP) , (KO) , (PG) and (KMB) ) will materially outperform the Mag 7 by a decisive amount in 2026 — appears to be developing...

The AI bubble bursts as the circular financing deals unwind (or are pushed out) — AI capital spending slows abruptly as return on investment concerns emerge as power generation and grid modernization are bottlenecks. Depreciation charges and lower demand wrecks havoc with consensus AI 2026-27 earnings per share expectations. Another big AI surprise would be if China decides to flood markets with inexpensive AI models — pressuring the ultimate and expected robust ROI forecasts (which are already in question by some skeptics).

OpenAI's Sam Altman finds a place to live right next door to Sam Bankman-Fried. His effort to make OpenAI too big to fail, fails. ChatGPT turns out to at best be a commodity large language model purveyor. It becomes obvious to all that its recent $500 billion-plus valuation can’t be supported. Without an ability to do a down round without losing face, OpenAI loses all access to capital. Ultimately, a consortium of its customers and suppliers takes it over to modify its business plan and reduce the cash burn.

With Altman tossed to the curb (or worse), the prosecutions begin.

OpenAI’s problems pushes a deeply committed (to OpenAI) Softbank to the verge of collapse.

Nvidia shares fall by -40% as CoreWeave (CRWV) is driven into bankruptcy.

A basket of defensive consumer nondurable equities ( (PEP) , (KO) , (PG) and (KMB) ) materially outperform the Mag 7 by a decisive amount.

The shares of (boring and previously hapless) PepsiCo outperform most other staples and 90% of the S&P Index after a much better skein of organic unit growth and as its core business is rationalized.

- Kass, 10 Surprises for 2026

Yesterday, in a day in which the S&P Index fell by -1.80%, a package of staples (PEP, PG, KO and KMB) were conspicuous winners:

* (PEP) +$1.08

* (PG) +$2.54

* (KMB) +$2.17

* (KO) +$1.31

By contrast, the components of Mag 7 stumbled badly and were conspicuous losers:

* (TSLA) -$18.02

* (AAPL) -$8.52

* (AMZN) -$7.69

* (NVDA) -$7.23

* (MSFT) -$4.52

* (GOOGL) -$9.16

* (META) -$15.09

Since September, Mag 7 stocks (compromising a package of popular "generational compounders" are flat and are massively underperforming:

BY Doug Kass · Jan 21, 2026, 8:05 AM EST

BY Doug Kass · Jan 21, 2026, 7:43 AM EST

Bonus — Here are some great links:

Global Breadth Will Not Let Go

What Worked and What Didn't In Trump's 1st Year of 2nd Term

BY Doug Kass · Jan 21, 2026, 6:45 AM EST

BY Doug Kass · Jan 21, 2026, 6:35 AM EST

BY Doug Kass · Jan 21, 2026, 6:25 AM EST

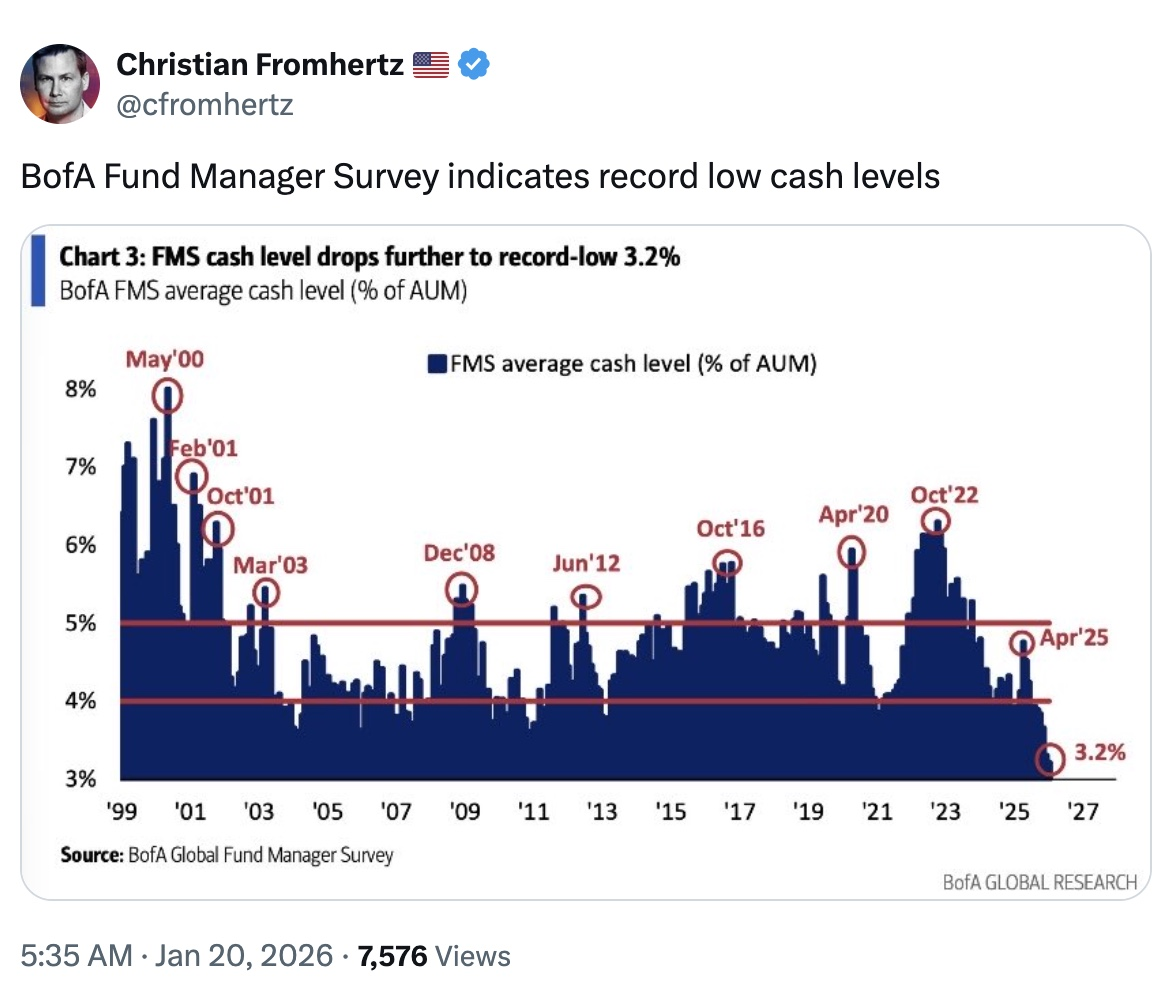

In the past I have called BS to the "cash on the sidelines" argument — usually promulgated by the bullish cabal late in bull market cycles. Here

I also called BS to the manner in which cash on the sidelines was computed.

This morning I call BS to the notion that investors are defensive and "the market is climbing a wall of worry."

The BofA Fund Manager Survey indicates record low cash levels:

BY Doug Kass · Jan 21, 2026, 6:05 AM EST

The S&P Short Range Oscillator fell to 2.54% vs. 5.11%.

BY Doug Kass · Jan 21, 2026, 5:55 AM EST

In the early going S&P futures are +23 and Nasdaq futures are +82.

I sold out my index long rentals for a quick profit:

* (SPY) $679.62

* (QQQ) $609.75

From late yesterday (4:01 PM):

I added to my trading long rental in the indices (and currently plan to hold overnight):

* (SPY) at $676.81

* (QQQ) at $607.31.

Position: Long SPY common (S/M), QQQ common (S/M); Short SPY calls (S), QQQ calls (S)

By Doug Kass Jan 20, 2026 4:01 PM EST

BY Doug Kass · Jan 21, 2026, 5:45 AM EST