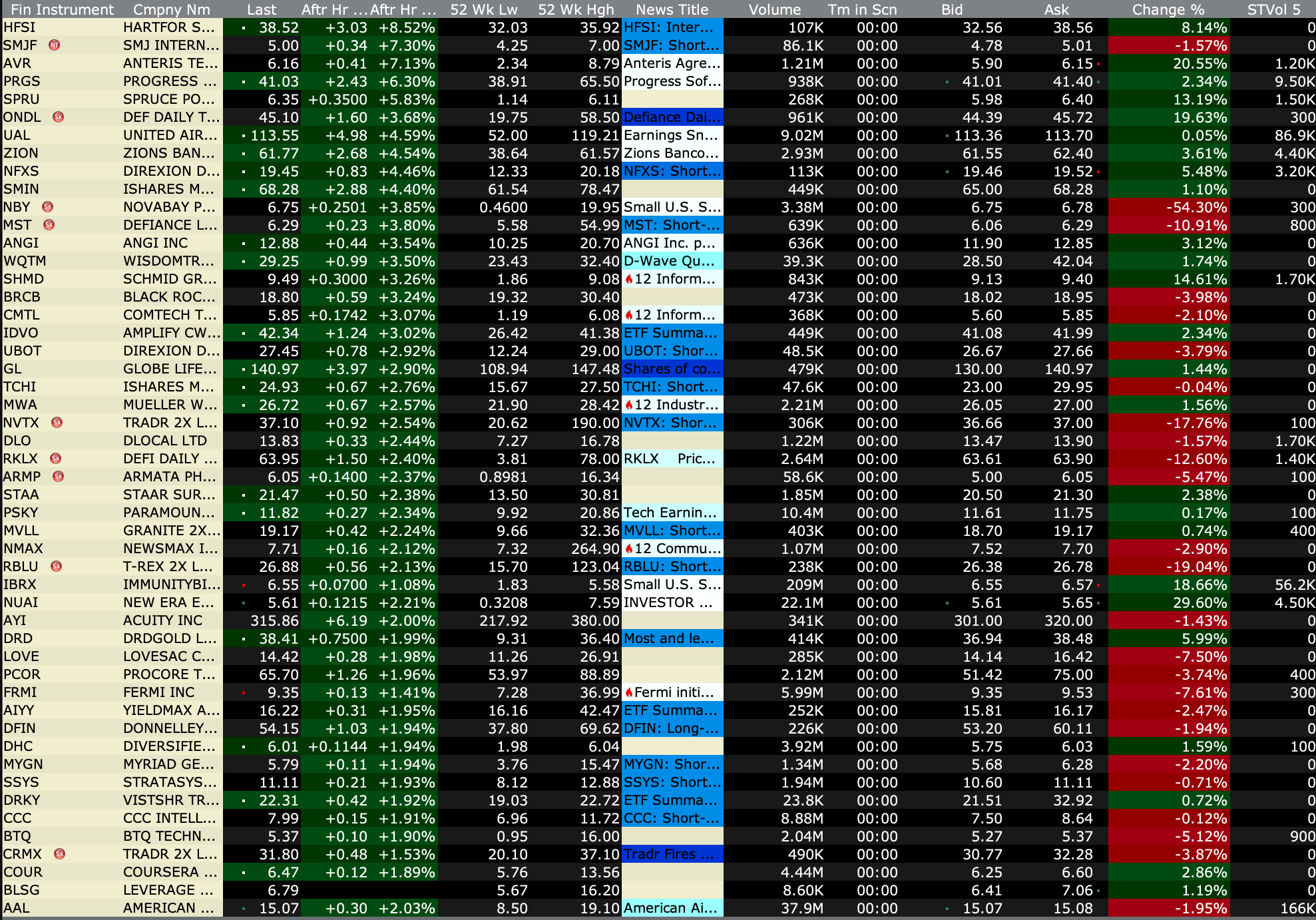

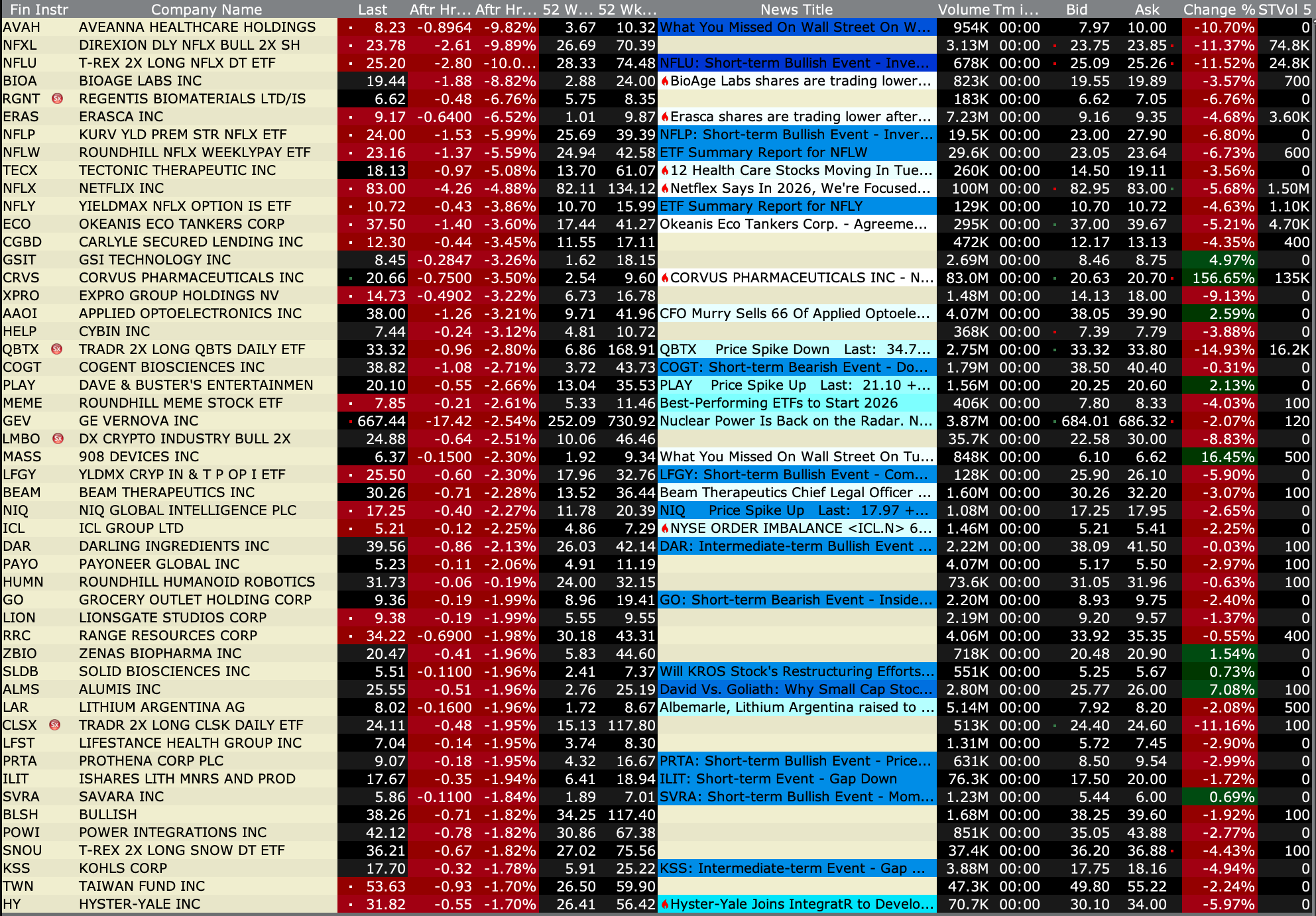

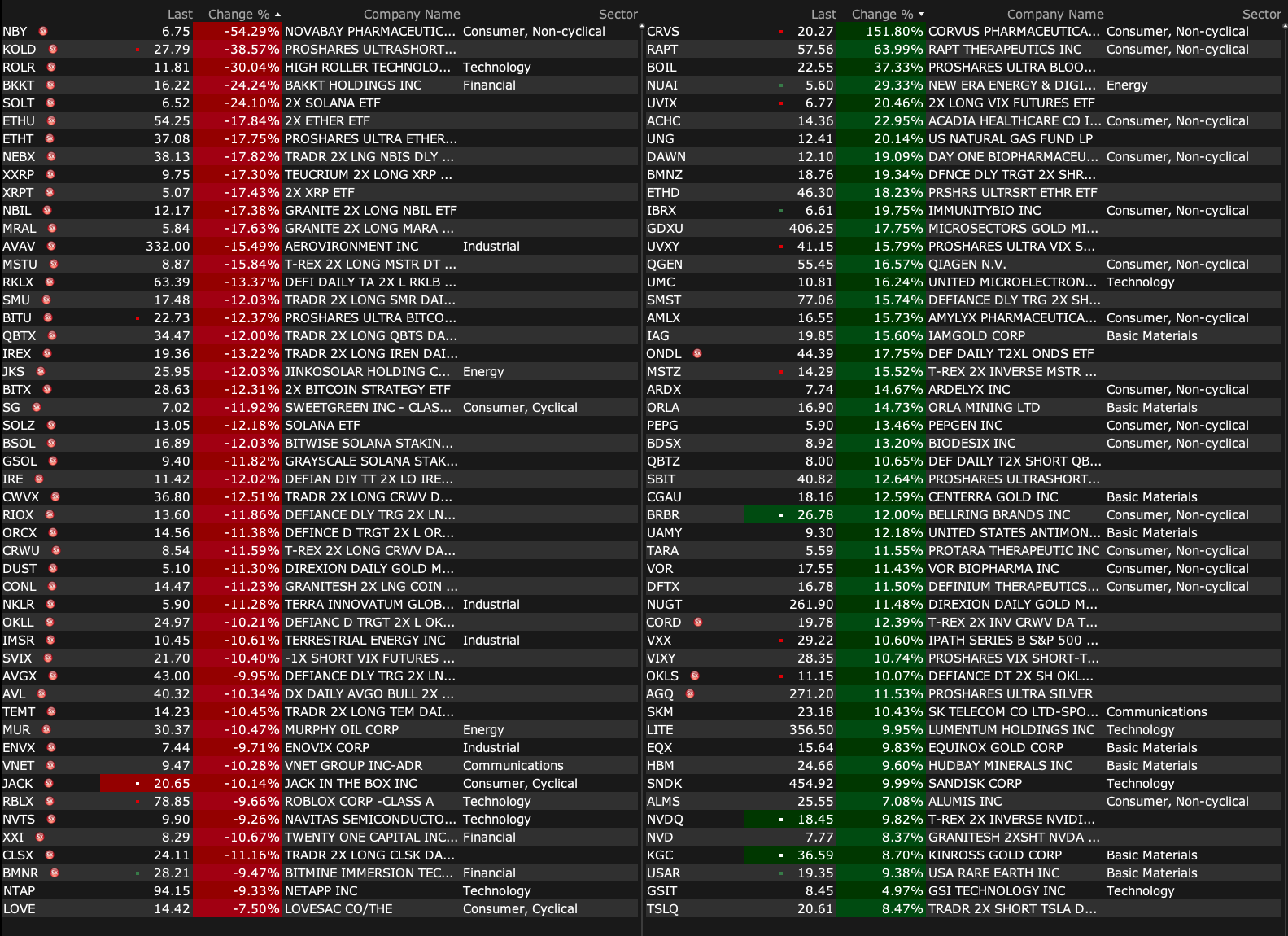

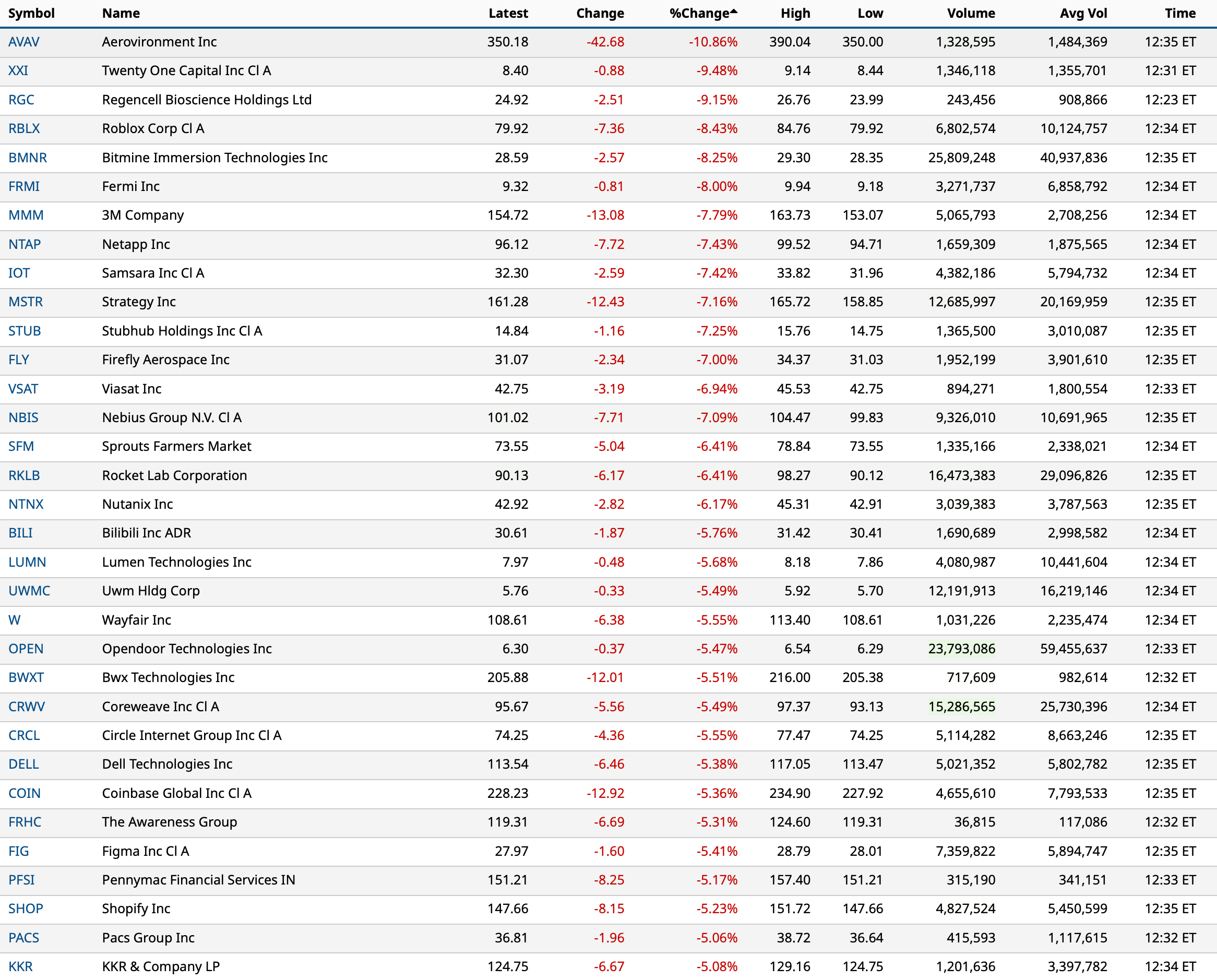

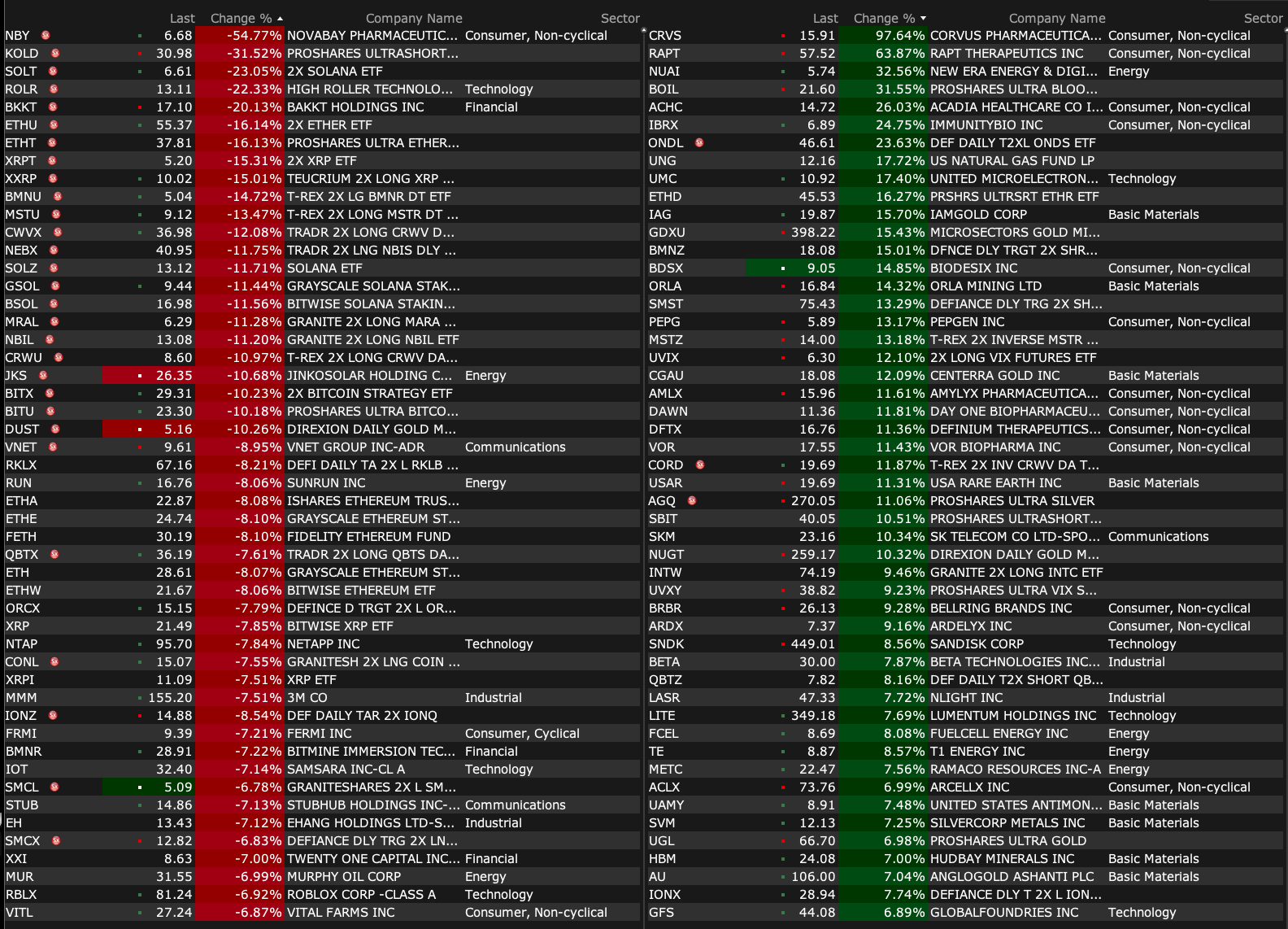

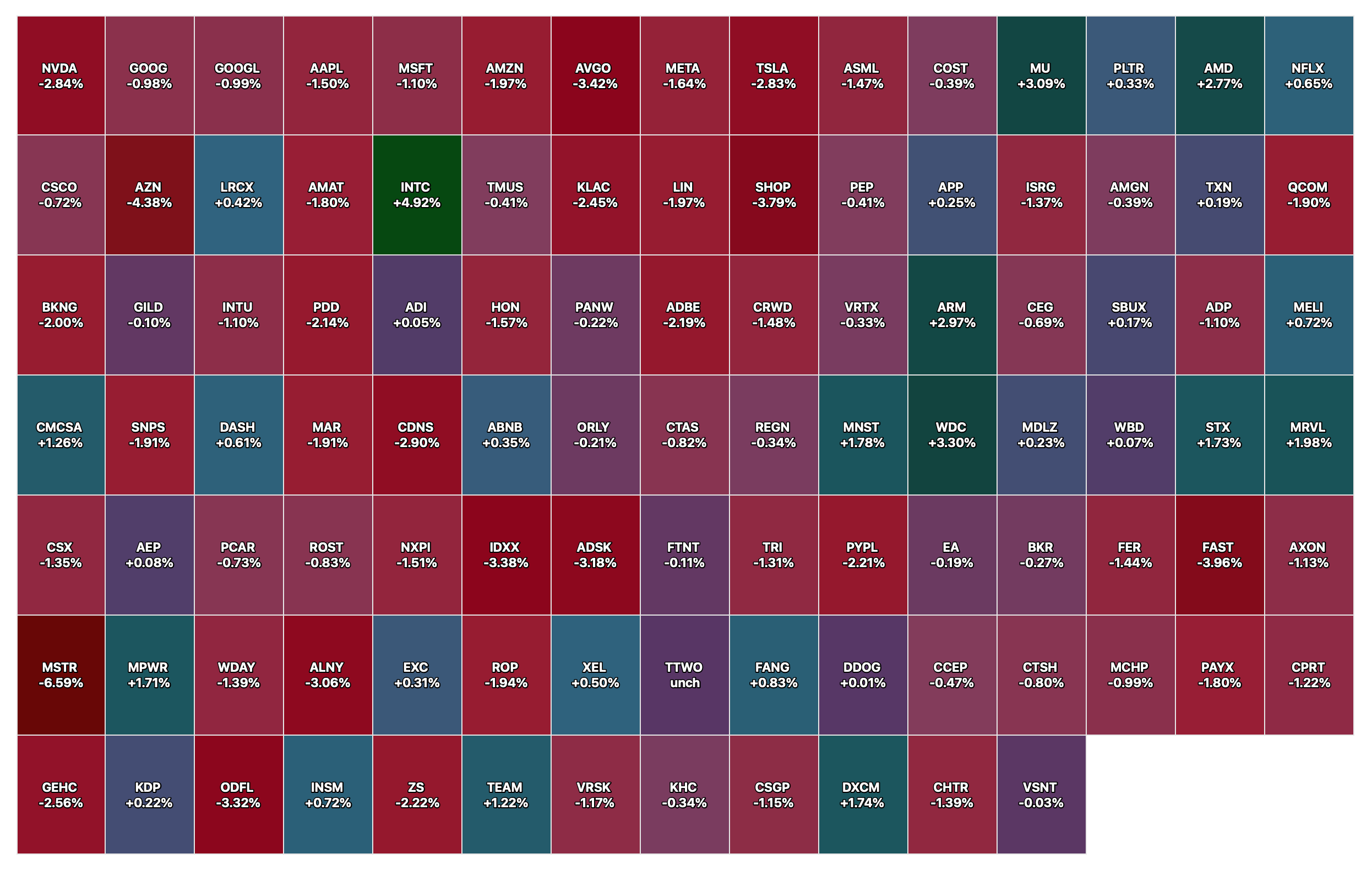

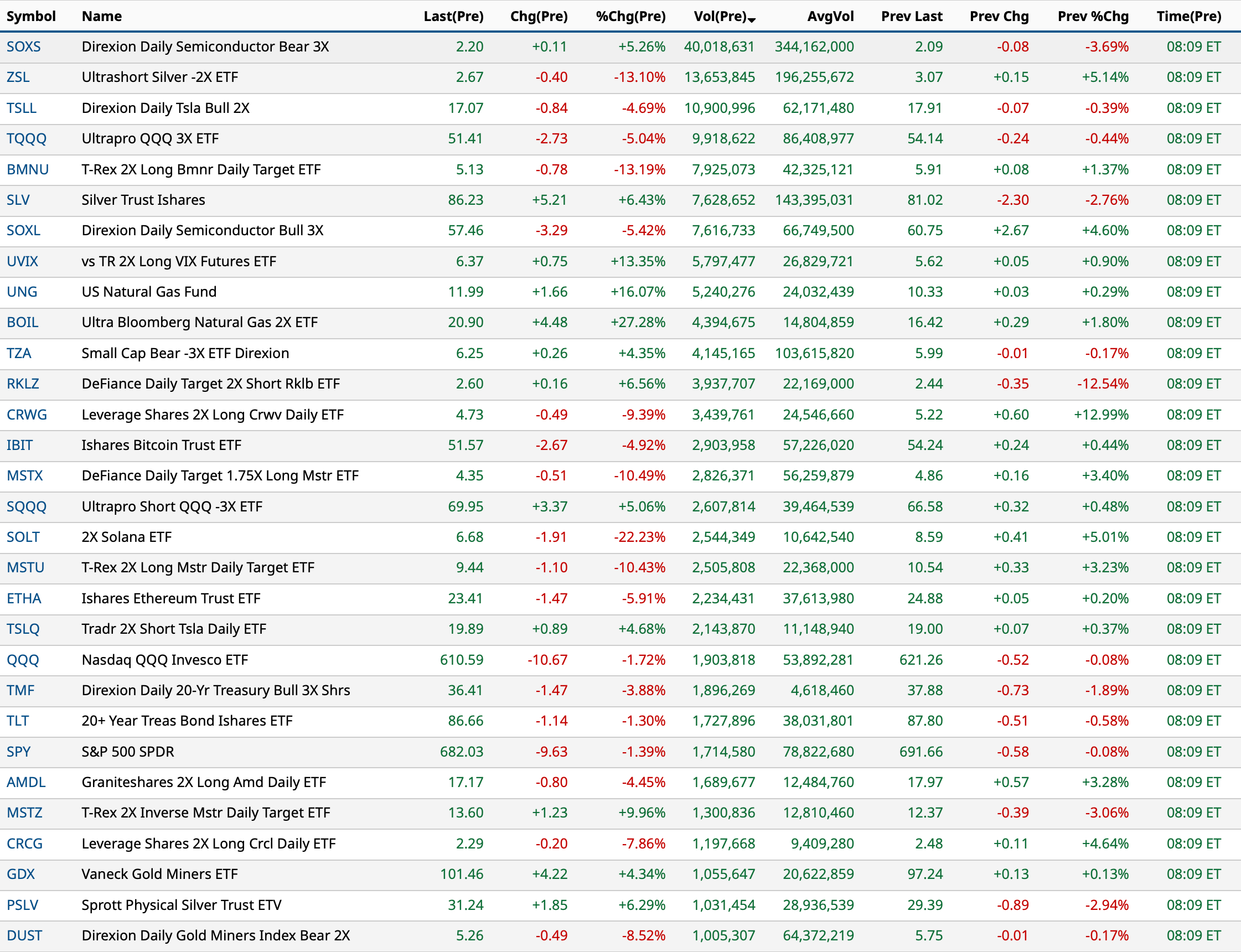

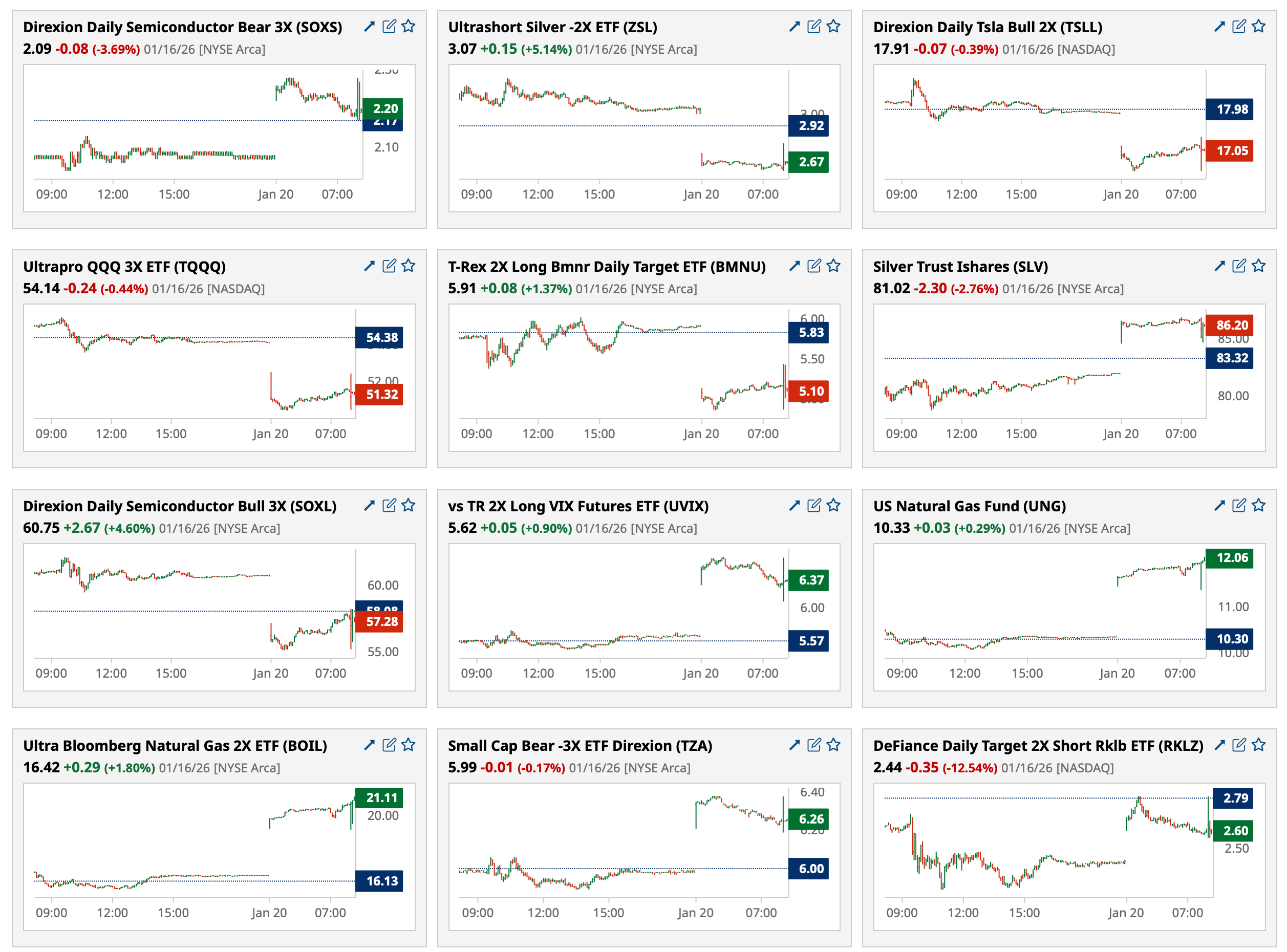

After-Hours Gainers and Decliners

After-Hours % Gainers

After-Hours % Decliners

BY Doug Kass · Jan 20, 2026, 4:45 PM EST

BY Doug Kass · Jan 20, 2026, 4:45 PM EST

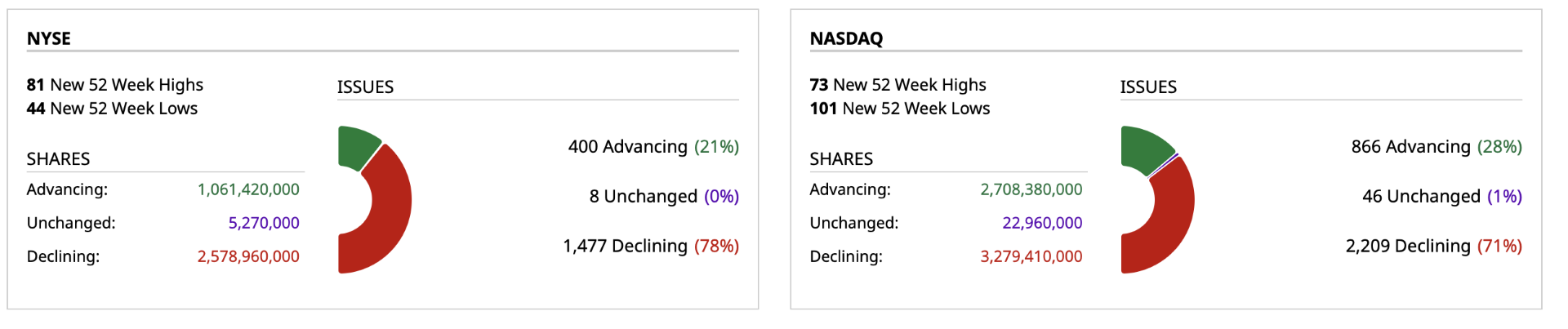

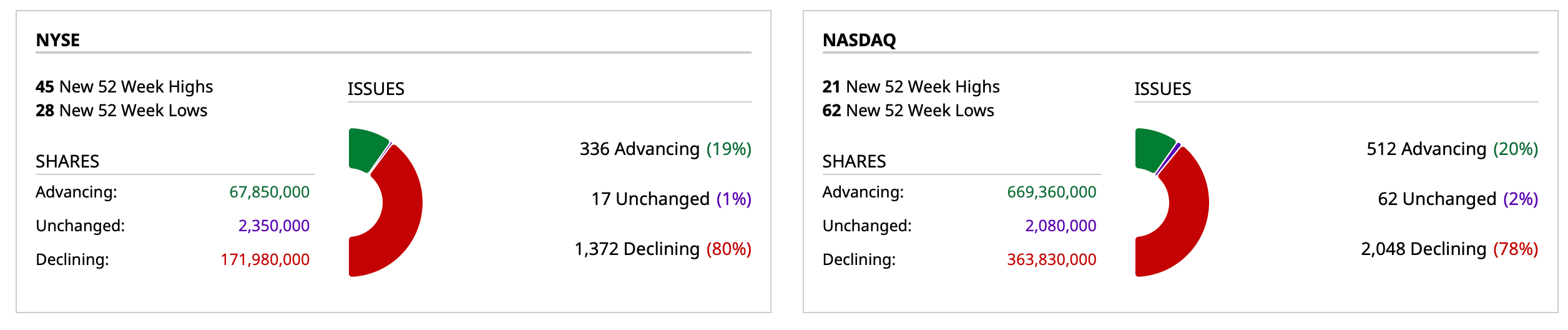

- NYSE volume 19% above its one-month average

- NASDAQ volume 16% above its one-month average

- VIX index: up 6.95% to 20.15

BY Doug Kass · Jan 20, 2026, 4:26 PM EST

I added to Netflix (NFLX) at $82.84 (-$5), moving from very small to small-sized (an investment and not a trade).

Though guidance was weak, the company is notoriously a conservative guider.

More tomorrow.

BY Doug Kass · Jan 20, 2026, 4:17 PM EST

I added to my trading long rental in the indices (and currently plan to hold overnight):

* (SPY) at $676.81

* (QQQ) at $607.31.

BY Doug Kass · Jan 20, 2026, 4:01 PM EST

From "Meet" Bret Jensen:

Bret Jensen

Really solid hour interview conducted by Steve Eisner from the Big Short this week with a senior professor and AI expert from NYU. Quite interesting take that LLMs are never going to get us to AGI. Other technologies might eventually to do so. He has numerous intriguing takes on the current state of AI development. It was well worth an hour of my time to listen to. If this professor is right, the NASDAQ probably trading for half its current trading level a year or two from now.

Gary Marcus on the Massive Problems Facing AI & LLM Scaling | The Real Eisman Playbook Episode 42

BY Doug Kass · Jan 20, 2026, 3:40 PM EST

We have been ahead of the curve regarding concerns about JGB yields:

* A must read and nowhere discussed on Fin TV....

Position: None

By Doug Kass Dec 1, 2025 7:25 AM EST

Wolf Street howls about exploding Japanese government bond (30 year) yields:

BY Doug Kass · Jan 20, 2026, 3:30 PM EST

From Charlie!

BY Doug Kass · Jan 20, 2026, 3:25 PM EST

With S&P cash -140 handles, I took a very small short-term trading long rental in (SPY) at $677.58.

I will likely be out by the close.

BY Doug Kass · Jan 20, 2026, 3:07 PM EST

I added small to (AMZN) at $229.91 (-$9) after selling some recently above $240.

BY Doug Kass · Jan 20, 2026, 3:02 PM EST

I covered my (AMH) short at $31.98 for a profit.

BY Doug Kass · Jan 20, 2026, 2:58 PM EST

I just covered my (JOET) at $42.29 and (GRNY) at $25.29 shorts.

BY Doug Kass · Jan 20, 2026, 2:46 PM EST

I covered these shorts just now:

* (GS) at $940.30 (-$23)

* (MS) at $181.54 (-$7.50)

BY Doug Kass · Jan 20, 2026, 2:42 PM EST

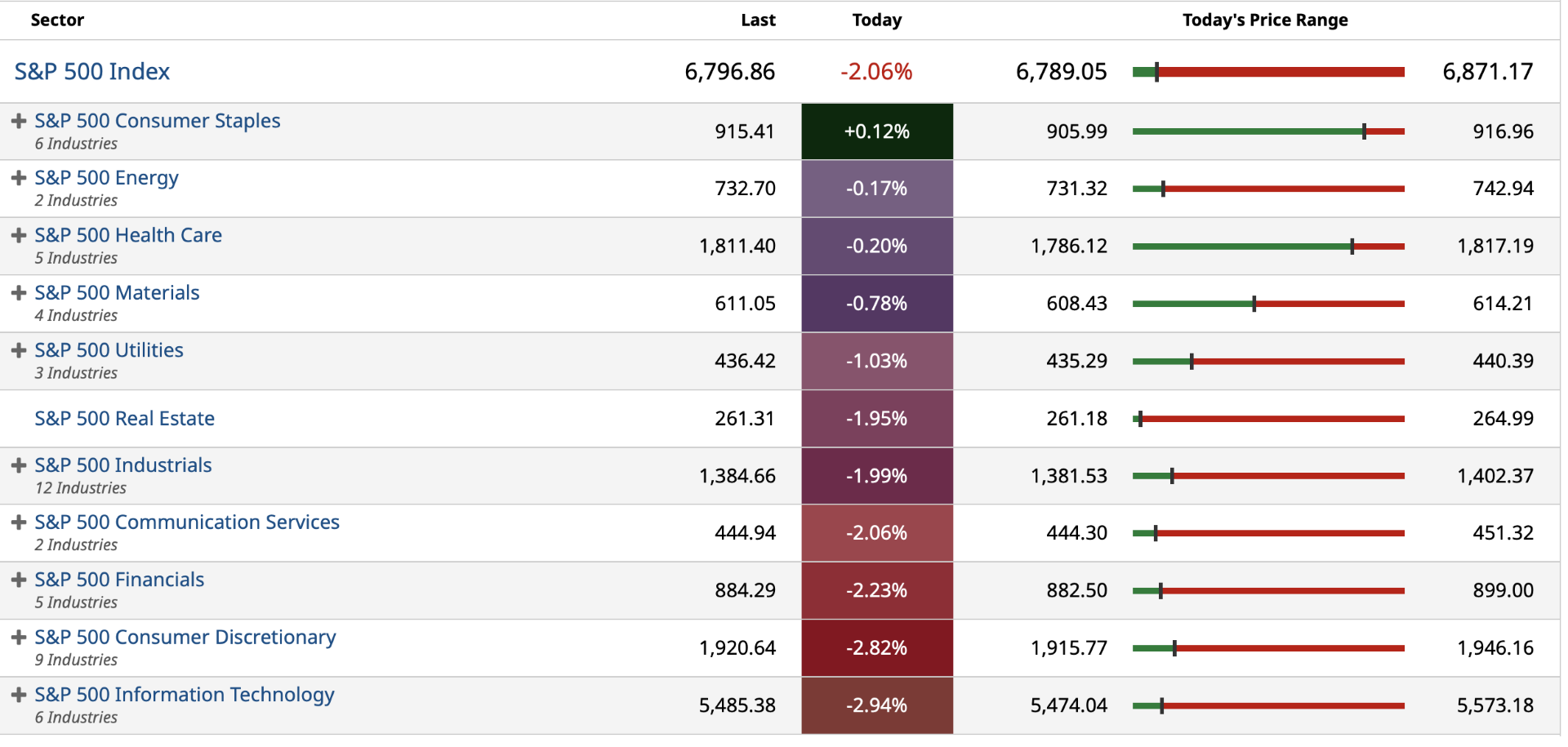

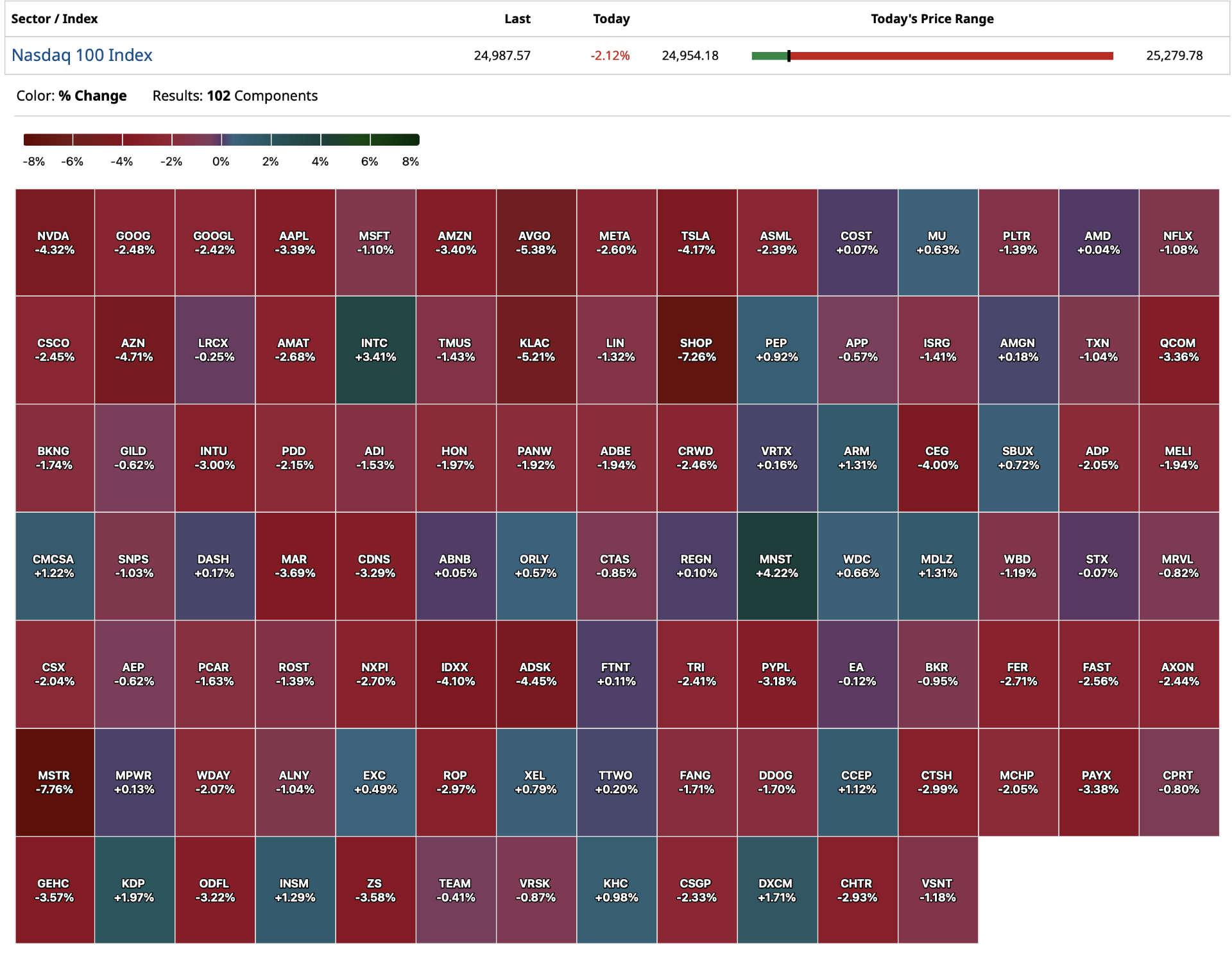

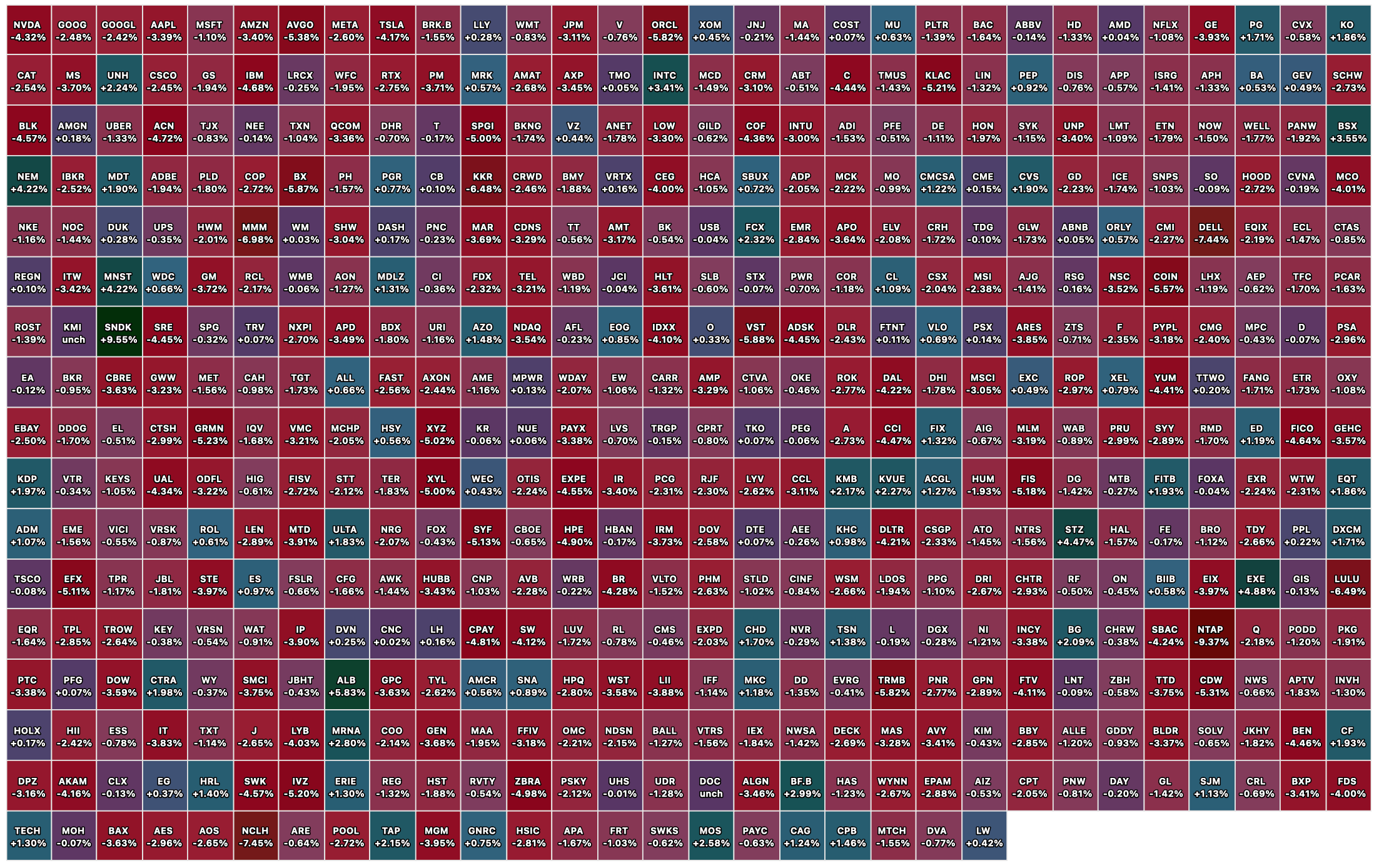

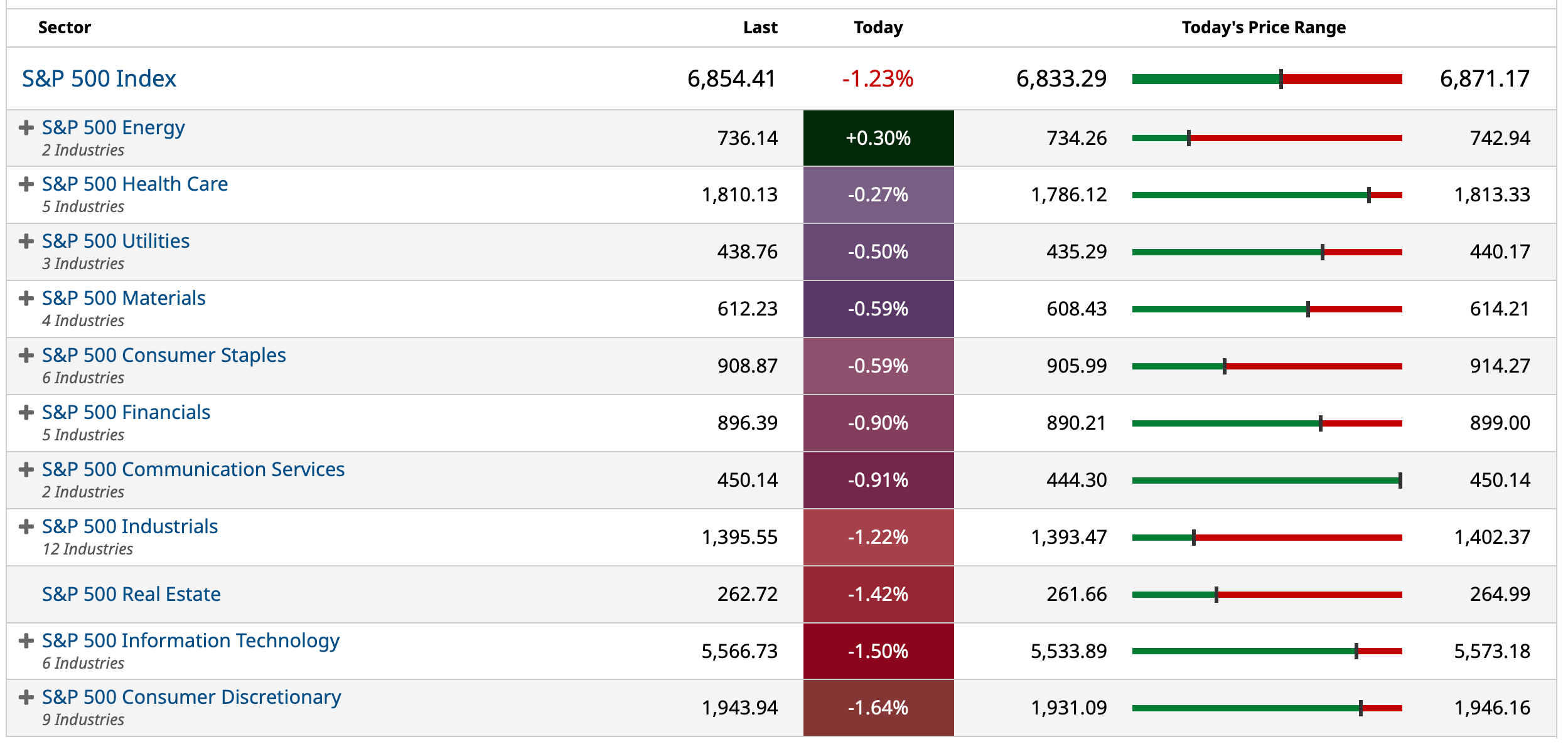

With financials seemingly leading each downtick, here is a look at six large names intraday:

BY Doug Kass · Jan 20, 2026, 2:31 PM EST

Tech (XLK) and Financials (XLF) making simultaneous day lows at 1:38 PM:

BY Doug Kass · Jan 20, 2026, 2:10 PM EST

With S&P futures now down -130 handles, approximately 50 handles lower than where I sold index calls, I am taking in all those index calls for a quick profit.

BY Doug Kass · Jan 20, 2026, 2:05 PM EST

BY Doug Kass · Jan 20, 2026, 12:50 PM EST

BY Doug Kass · Jan 20, 2026, 12:40 PM EST

I have a business lunch at 12:30-2 PM.

BY Doug Kass · Jan 20, 2026, 12:00 PM EST

With S&P cash -80 handles, I am back shorting index calls.

BY Doug Kass · Jan 20, 2026, 11:45 AM EST

- NYSE volume 35% above its one-month average;

- Nasdaq volume 20% above its one-month average;

- VIX index: down 0.48% to 18.75

BY Doug Kass · Jan 20, 2026, 11:30 AM EST

* Any fool can turn a blind eye but who knows what the ostrich sees in the sand

* When the time comes to sell, investors won't want to...

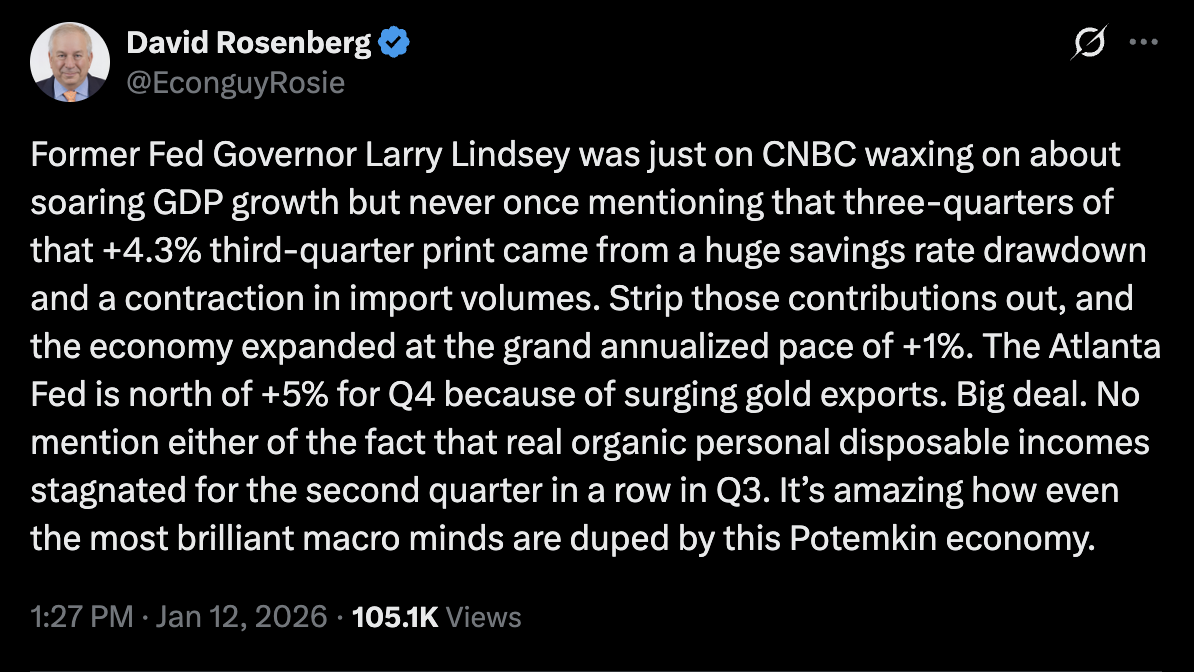

* This morning's opening missive quotes Yogi Berra, Albert Einstein, Warren Buffett, Howard Marks, Larry Fink, David Rosenberg, Voltaire, Jean-Jacques Rousseau, George Orwell, Franklin D. Roosevelt and (last but not least!) Wally Deemer

What follows is a combination of my recent correspondences with Seabreeze Partners' investors and timely articles I have written on TheStreet Pro:

In my hedge fund, we remain slightly net short in exposure (out of respect for the stock market's upward momentum) but plan to add to that exposure if our fundamental concerns appear to be developing (and if stock price action begins to confirm my ursine outlook).

The equity of a company is fundamentally a claim on assets - representing the residual value of an asset or business after all liabilities are paid off. This is the shareholder's stake, a "leftover" amount in the accounting equation:

Calculating shareholders' equity or what truly belongs to a holder of equity is relatively easy to compute and is objective.

What is more difficult, however, is what that equity is worth - this is the subjective part of investing.

This is where my hedge fund, Seabreeze Partners, disagrees with the consensus - we question what the multiplier should be on earnings.

- Wally Deemer, Introduction to his new book When the Time Comes to Buy You Won't Want To (Volume II)

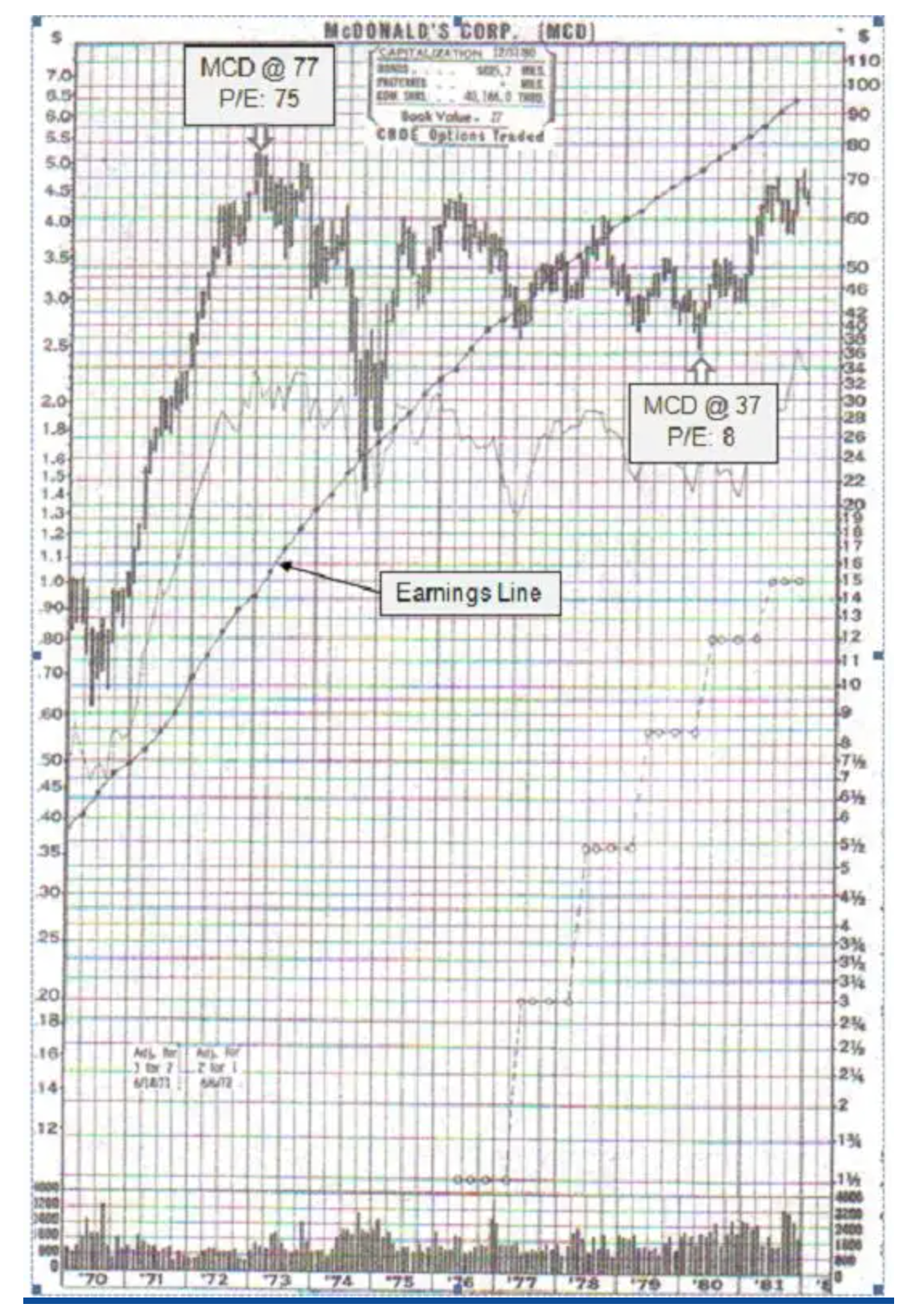

The investment mosaic is so much more complicated than simply taking an S&P profit expectation and multiplying it by a multiple — as Wally Deemer's extreme example of McDonalds' (MCD) share price performance during and after the collapse of The Nifty Fifty era (1972-1980) shows.

The share price of McDonald's during the decade of the 1970s (when I was at Putnam Management Company) provides a vivid and extreme blueprint of a market (and consensus) being very wrong about the value accorded one of the most popular stocks. This illustration will better explain why we see as the risks associated with currently elevated valuations.

From 1972-1980, McDonald’s growth in earnings per share compounded by an extraordinary +25% per year. Yet, its price-to-earnings ratio dropped from 75x to only 9x and its share price declined by more than -50%!

- Wally Deemer, When The Time Comes to Buy You Won't Want To (Volume II)

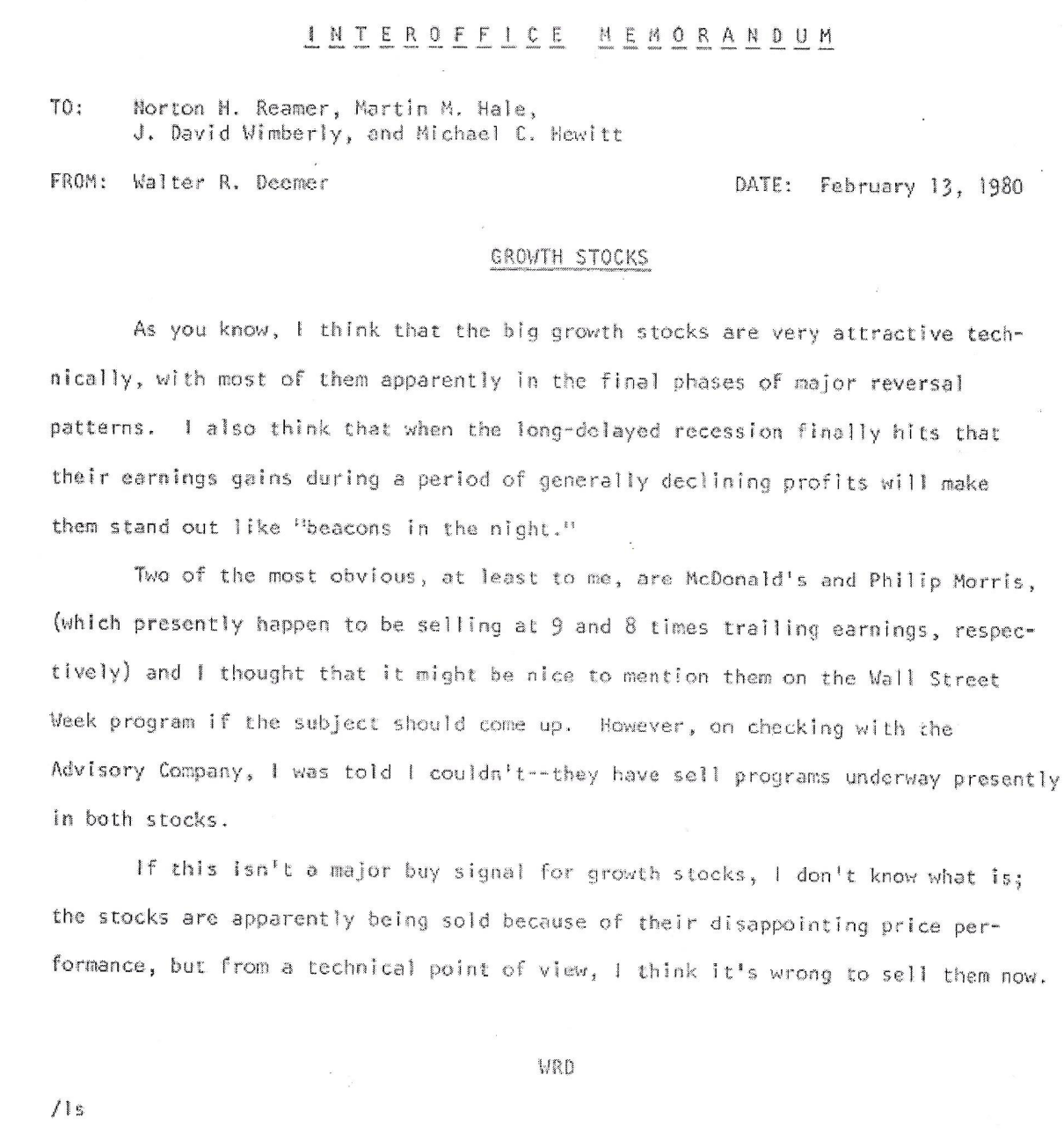

Here is a memo from Wally (my associate at Putnam) in 1980:

And here is the McDonald's chart from the 1970s:

While the S&P Index is not anywhere as overvalued as McDonald's was in 1972 (when MCD possessed a 75x price earnings multiple), as noted previously, we believe the markets are materially overpriced at current valuations.

We see a Bull Market in Group Stink with a herd-like chorus of "first level thinking" at a near unanimous pitch and adoption today – somewhat like the peak in “The Nifty Fifty” so clearly expressed by a 77x multiple in McDonalds’ ’stock price in 1972.

To paraphrase Wally, when it’s time to sell (McDonalds in 1972) or perhaps the S&P Index in 2026, investors won't want to....

"We have now sunk to a depth at which restatement of the obvious is the first duty of intelligent men."

- George Orwell

Seabreeze is slightly net short for the multitude of reasons mentioned in our previous commentary to investors and on TheStreetPro:

* We reject the generally positive consensus expectations for U.S. economic growth:

"We have learned that we cannot live alone, at peace: that our own well-being is dependent on the well-being of other nations far away. We have learned that we must live as men, not as ostriches, nor as dogs in the manger. "

- Franklin D. Roosevelt

Increasingly (and importantly), errant Administration policy could begin to adversely impact economic alliances and contribute to a downturn in global economic activity.

Domestically, we believe there is a growing possibility that the current K-shaped economy's weakness in the lower income cohort spreads into the middle and upper middle class as the cumulative (or stacked) inflation since Covid finally has an impact — causing a spending freeze. With the outlook for global economic growth dissipating, consumer and business sentiment could plummet. BNPL (buy now pay later) and credit defaults would then rise and auto repossessions could increase dramatically.

Drawdowns in the global equity markets and a still moribund housing market may contribute to a negative "wealth effect" and an air pocket with the high end consumer as investor optimism of 2023-25 is abandoned.

* We also reject the notion that the new Fed Chair will grease the economy (and run it "hot") by lowering interest rates. We disagree on several counts: we see inflation remaining sticky and we don't think the new Chair will have a cooperative Committee.

* The equity risk premium — which has historically been an excellent forecaster of future equity returns — is now a discount. This means that the market is pricing more risk in bonds than in stocks!

* Historical valuation metrics are at about the 97%-tile. Indicators like the Buffett Ratio, Shiller CAPE and Price/Sales are at all-time overvalued readings. We strongly disagree with the many investors who believe we are in a new valuation paradigm. From Howard Marks:

* Dividends typically account for a bit more than 35% of the total return of stocks. The S&P Dividend Yield is now at a multi-decade low of 1.12% — contributions from dividends are modest — likely leading to substandard returns for an extended period of time.

* The composition of equity returns remains out of balance with a small number of large-cap technology stocks (highly dependent on the AI trade) contributing to overall returns. As noted in 170 "More Tales From Nvidia" columns, I am far less optimistic regarding the overall value of and return on investment prospects for the outsized AI capital expenditures - for society and as it relates to the productivity of individual companies.

* Margin debt, like valuations, is at a record high — inflating the indexes by borrowed money. Any reversal in market sentiment could trigger an unwind of this leverage, which could cascade in a market dominated by passive products and strategies that worship at the altar of price and momentum. The recent unwind in the leveraged cryptocurrency markets might foreshadow what may happen in equities in 2026.

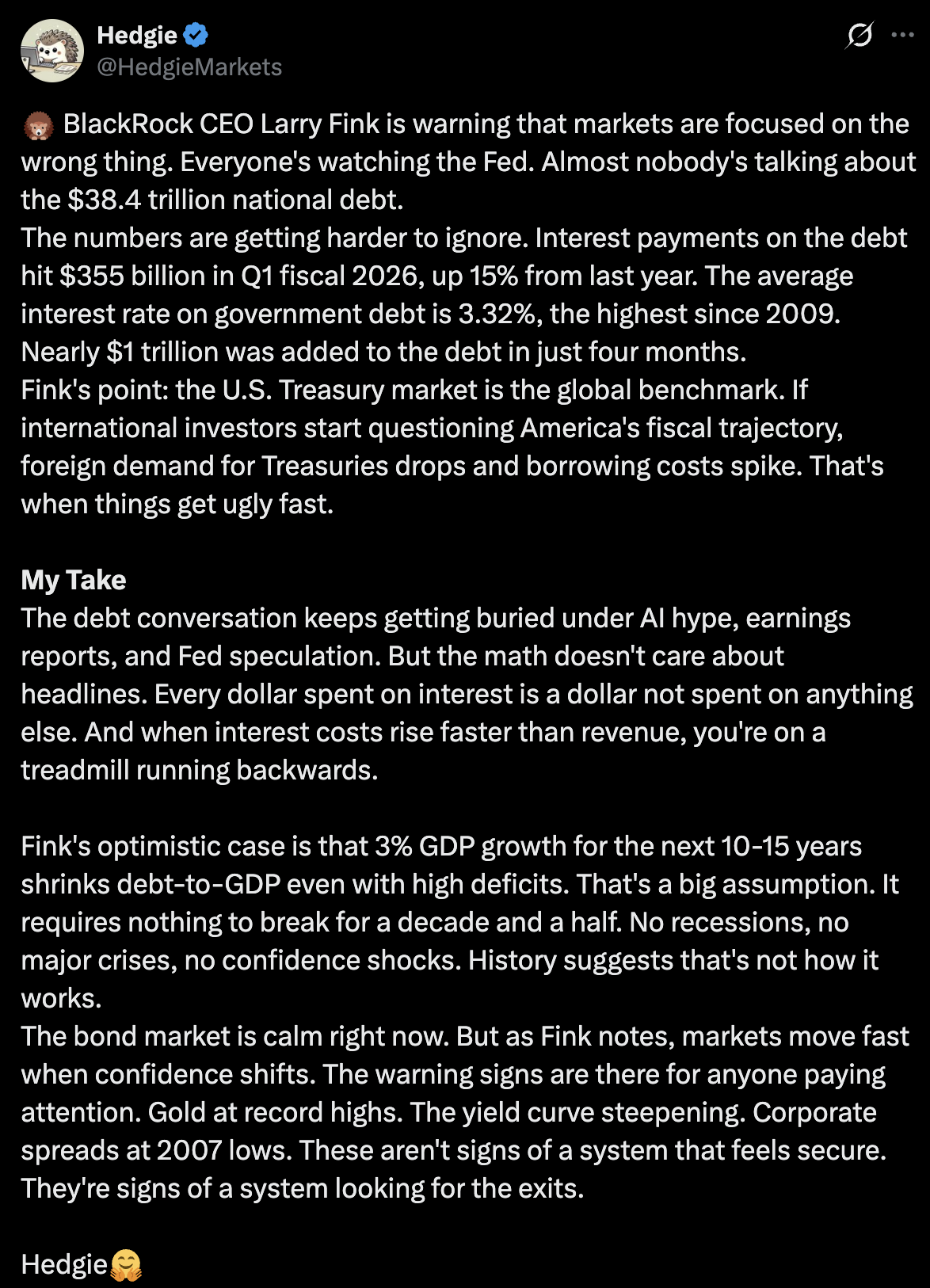

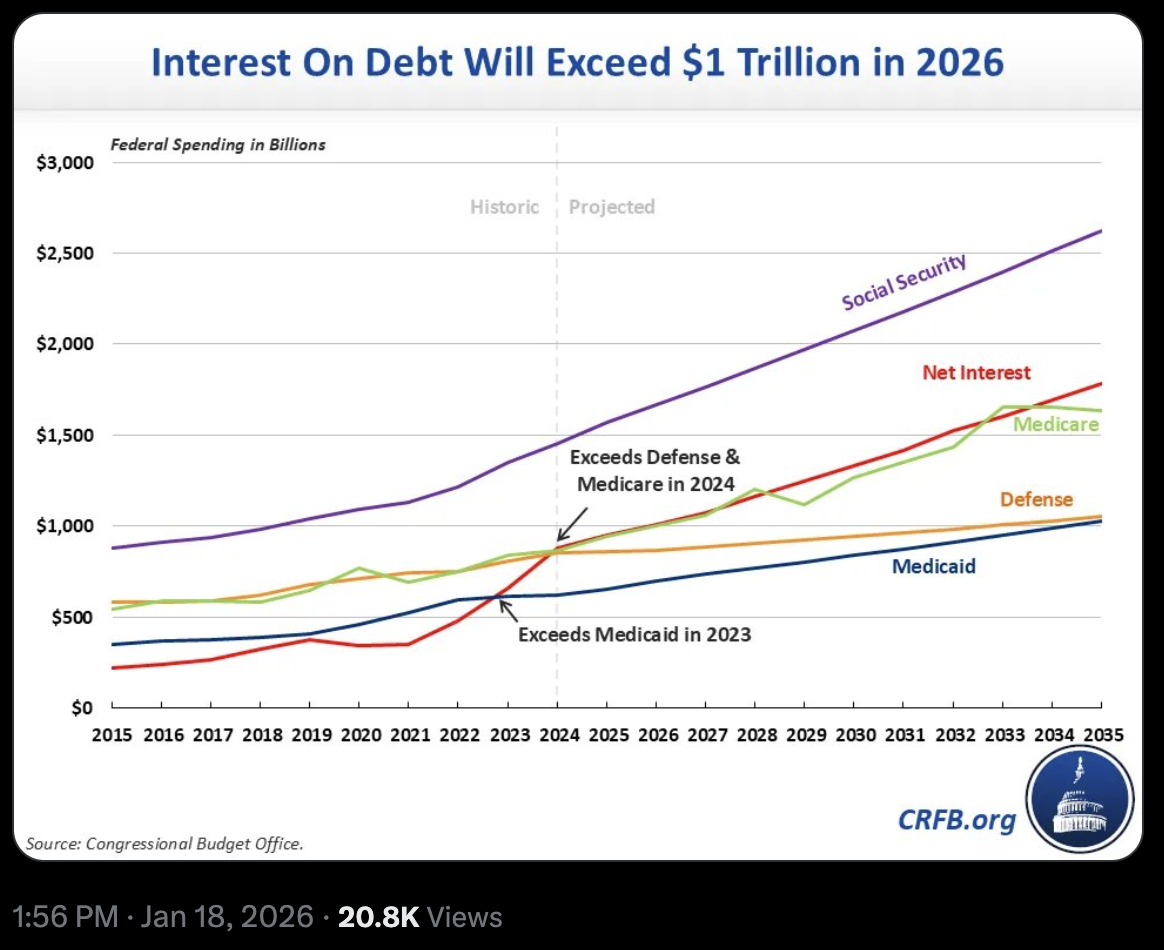

* Neither political party is acting in a fiscally responsible manner. A feckless approach to our deficit is producing a steady march higher in our national debt:

* I recently mentioned reading my friend Andrew Ross Sorkin's new book 1929: Inside the Greatest Crash in Wall Street History-and How It Shattered a Nation.

I couldn't help but see the similarities between then and now. The 1920s did not end well as our society lost sight of the value of regulations: wise rules are a source of abundance, well-regulated markets/systems attract users and investors, removing the constables patrolling our financial markets is potentially dangerous and U.S. capital markets became the world's largest not despite regulation, but because of it.

* There are large risks associated with (leveraged) passive products and strategies, the proliferation of ETFs (today there are more ETFs than individual stock listings!), changes in market structure and in a leveraged crypto currency investing base. The gamification of the market is being ignored and is not being addressed by market participants and by regulators. (It is abnormal and symptomatic to the degree of speculation going on today that 70% of all options traded have only a 24-hour maturity!)

* Wall Street strategists are unanimously bullish - on average they are forecasting a +11% return for 2026. They are nearly always bullish, so their opinions should be taken accordingly — and with a grain of salt. We believe they are failing to consider the growing list of negatives, some of which we discuss today.

"I must seem like an ostrich who forever buries its head in the relativistic sands in order not to face the evil quanta."

- Albert Einstein

A famous philosopher, baseball player Yogi Berra famously once said that "the future ain't what it used to be."

As I noted in a recent monthly commentary to Seabreeze's limited partners - Warren Buffett warned about a too ebullient mindset in November 1999, only four months before the dot.com bubble burst:

Once a bull market gets underway and once you reach the point where everybody has made money no matter what system he or she followed, a crowd is attracted into the game that is responding not to interest rates and profits but simply to the fact that it seems a mistake to be out of stocks. In effect, these people superimpose an I-can't-miss-the-party factor on top of the fundamental factors that drive the market. Like Pavlov's dog, these "investors" learn that when the bell rings - in this case, the one that opens the New York Stock Exchange at 9:30 a.m. - they get fed. Through this daily reinforcement, they become convinced that there is a God and that He wants them to get rich.

Voltaire also put it well when he wrote:

"History never repeats itself. Man always does."

Delusions swing between extremes, like pendulums. Delusions of grandeur and unending wealth give place to delusions of unending gloom. One is as unreal as the other. Today we seem to be close to an extreme in speculative activity and valuations. Unfortunately, history teaches us that the unsustainable cannot be sustained as, ultimately, with panic and pain, bubbles burst.

When I look at today's valuations I am reminded of (a twist) of something written by Jean-Jacques Rousseau:

"History never deceives us; it is we who deceive ourselves."

For what we have learned from history is that we haven't learned from history:

In summary, perhaps the S&P Index in 2026 has some resemblance to McDonald's share price overvaluation in 1972 — when a top was made in McDonald's (and investors were willing to pay 75x EPS). At that time (like today), everyone was all in the investing pool in the belief that equities were a buy on every dip and would never fall.

While we certainly don't think that today's stock market is as extremely overvalued as McDonald's was 53 years ago, there is a message in the comparison (and a twist of Wally Deemer's mantra):

"When the time comes to sell, most won't want to."

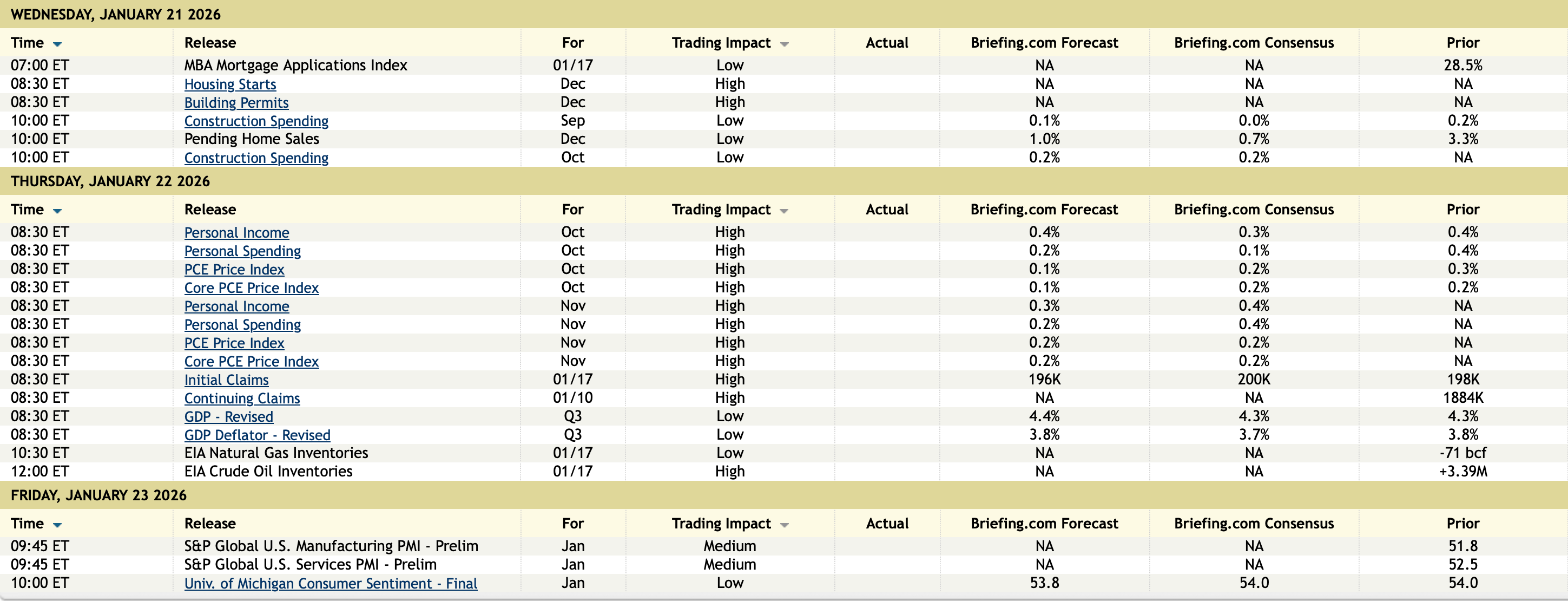

BY Doug Kass · Jan 20, 2026, 10:00 AM EST

From Peter Boockvar:

In light of another tariff threat over the weekend, today would be the ideal day to get a ruling from the Supreme Court on the use of IEEPA so we can all know what will be allowed and prohibited for the sake of clarity. While also being used as a geopolitical weapon rather than in dictating terms of trade, it is every business and household that is put under a cloud of uncertainty when it comes to providing and consuming goods and services in terms of pricing and costs. It is no wonder the pace of job creation, particularly via small and medium sized businesses, has slowed since April as companies do their best to contain costs in order to mitigate cost pressures and cloudy visibility elsewhere.

To some, the success or failure of the use of tariffs (outside of the hoped for reshoring as a result) comes down to whether there is a rise in consumer price inflation but it’s also important to see the extent companies are dealing with producer price inflation and the hit to margins if cost increases can’t be passed on. Regardless of the outcome, there is still higher costs that need to be absorbed somewhere and mitigation efforts, including a slowdown in hiring, that gain in importance. The Fed’s Beige Book highlighted this last week the continued flow through of tariff/tax increases.

This is not meant to be a political discourse (I prefer lower taxes and deregulation as the way to make the US a more competitive place to do business by the way). This is strictly a discussion on taking the world as it is as an investor in markets as I have to quantify the real world impact of policy regardless in as an objective perspective as possible. That is all I am trying to do.

To the debate on who is eating the tariffs, the German Kiel Institute released a report yesterday that said “Contrary to US government rhetoric, the cost of US import tariffs are not borne by foreign exporters. Instead, they hit the American economy itself. Importers and consumers in the US bear 96% of the tariff burden.”

Here is what the study covered. “The research team analyzed more than 25 million shipment records covering a total value of almost four trillion US dollars in US imports. The findings are clear:

They homed in on trade with Brazil and India after the tariff increases on each to 50%. “Again, the data show that foreign exporters did not lower their prices to offset the additional tariffs. Had exporters absorbed the tariffs, their US prices would have fallen relative to other markets - but this was not the case.”

“We compared the Indian exports to the US with shipments to Europe and Canada and identified a clear pattern. Both export value and volume to the US dropped sharply, by up to 24%. But unit prices - the prices Indian exporters charged - remaned unchanged. They shipped less, not cheaper.“ I bolded for emphasis.

I’ll add one more thing on the tariff pass through debate on prices. The more I hear from companies, the more I believe that the pass through will play out over a multi year process. For example, if I’m company ABC and my costs just went up by 20%, in most instances I can’t immediately go raise prices by that amount, there is no way the market could absorb that so quickly. Maybe I can get away with 4-5% at a clip which means that in order to recapture margin, I might take price over a multi year time frame, in addition to having to possibly eat some of it.

I’ll let the markets speak from here with the price of gold, silver and other metals continuing their rise. The US dollar is weaker and US yields are much higher. Also impacting US yields, and global ones too, is another rise in JGB yields after the Japanese PM set February 8th for their early election and after an expected consolidation of power within the LDP, the focus is on the fiscal stimulus package that will be implemented. How many times have I said that this rise in JGB yields will at some point matter? Many and I guess it now does. Japan also had a 20 yr bond auction that reflected softer demand relative to the 12 month average.

From an investing standpoint, I’m still comfortable owning international stocks and bonds, denominated in local currencies in anticipation of continued pressure on the US dollar, along with commodities as the world shifts into multipolar regimes. There are still cheap, value stocks in the US too that we own, including beaten up consumer staple stocks. I remain bearish on long duration sovereign bonds.

With respect to oil in particular, in case you didn’t see this story from Friday, Harold Hamm the founder of Continental Resources “said he’s about to shut down his company’s drilling in North Dakota’s Bakken for the first time in decades because of low crude prices” reported Bloomberg News. He said in a phone interview, according to the article, “There’s no need to drill it when margins are basically gone.”

Bloomberg estimates that $58 a barrel is the essential breakeven cost wise with room for a small profit in the Bakken. And with the higher costs of oilfield equipment like pipe, drilling gear and generators, “A lot of people are assessing their activity in all the basins” said Hamm.

As bulls on oil, this is the supply response that eventually will reset prices higher.

After hearing from JB Hunt last week, Cass Freight released its December shipments data and they fell 3.2% m/o/m seasonally adjusted and are down 7.5% y/o/y. They said “The three winter storms which hit the Midwest in the first two weeks of December slowed the highway network and created some pent-up demand that was still evident in the spot market in the first half of January.”

Also, “Holiday consumer spending data suggest retail inventories destocked in recent months as freight shipments across modes were below spending trends.”

And finally from them and on tariffs, “While the soft volume environment persists, after considerable destocking in Q4 ‘25, we think the Supreme Court decision on IEEPA tariffs could provide a positive catalyst for freight demand.” And as JB Hunt alluded to on their call, any improvement in freight demand will likely lead to higher trucking prices as a lot of capacity has left the market over the past few quarters.

Positively from a worldwide container shipping perspective, global shippers are beginning to ship product again through the Red Sea and Suez Canal as Maersk said last Thursday. “This decision follows a continued stabilization of conditions in and around the Red Sea, including the Suez corridor, as well as improved stability and reliability in the region” the company said in a release. This should further cool container shipping costs.

The January ZEW investor confidence index in the German economy improved to 59.6 from 45.8 and that was above the estimate of 50. The Current Situation remained deeply negative but less so at -72.7 from -81. That was 3 pts above the forecast.

From ZEW, “Despite the announcement of additional tariffs by the US last weekend, export-oriented industries are experiencing, in some cases, significant improvements. In particular, the balances of the steel and metal industry as well as of the mechanical engineering have increased by 18.2 and 22.7 points, respectively. The balance for the automotive industry rose by 16.5 points to minus 5.5 points. The balances for the chemical and pharmaceutical industries and electrical engineering have also improved by 12.4 and 14.0 points, respectively. These results are in line with the figures for industrial production in November 2025, which turned out significantly better than expected and a surprisingly strong increase in orders. In addition, the Mercosur agreement is likely to have improved the outlook for export-intensive industries. However, the unpredictable US trade policy continues to be an additional burden on the German export economy.”

Responding to geopolitics and JGB yields, the euro is higher as are European sovereign bonds yields while stocks are lower.

In the UK, payrolls fell by 43k, about double expectations of a decline of 20k. In the 3 months ended November saw an unemployment rate of 5.1%, unchanged m/o/m. Private payroll growth is slowing with a 3.6% y/o/y gain through November, down from 3.9% in October. Notwithstanding the soft data, the British pound and gilt yields are also responding more to the Greenland tariff threats and the rise in long term global bond yields with both higher.

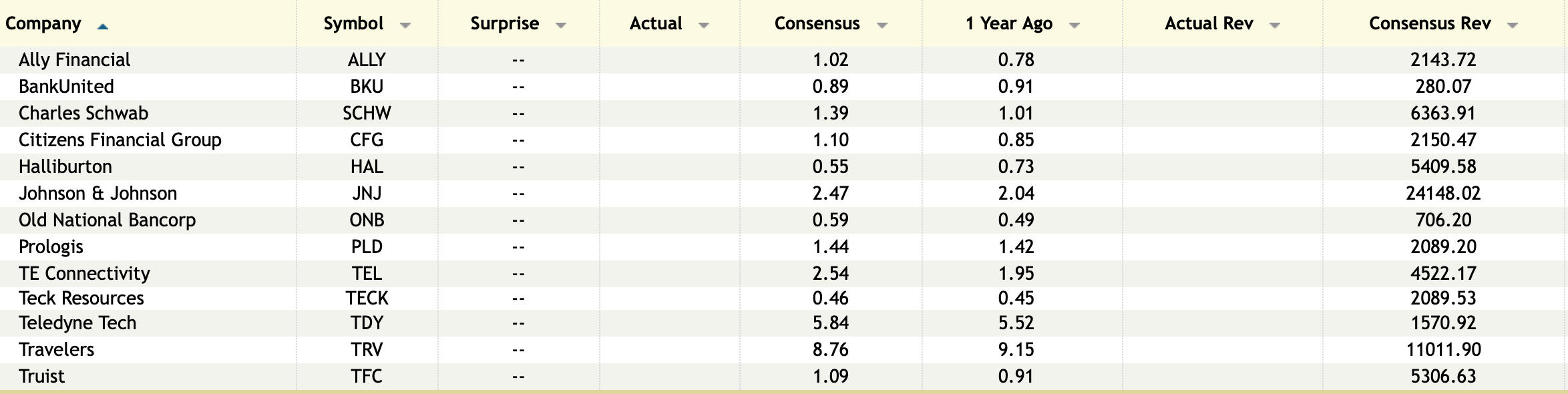

I’ll end with an earnings comment from DR Horton:

“Affordability constraints and cautious consumer sentiment continue to impact new home demand. We expect our sales incentives to remain elevated in fiscal 2026, the extent to which will depend on the strength of demand during the spring, changes in mortgage interest rates and market conditions throughout the year.”

BY Doug Kass · Jan 20, 2026, 9:30 AM EST

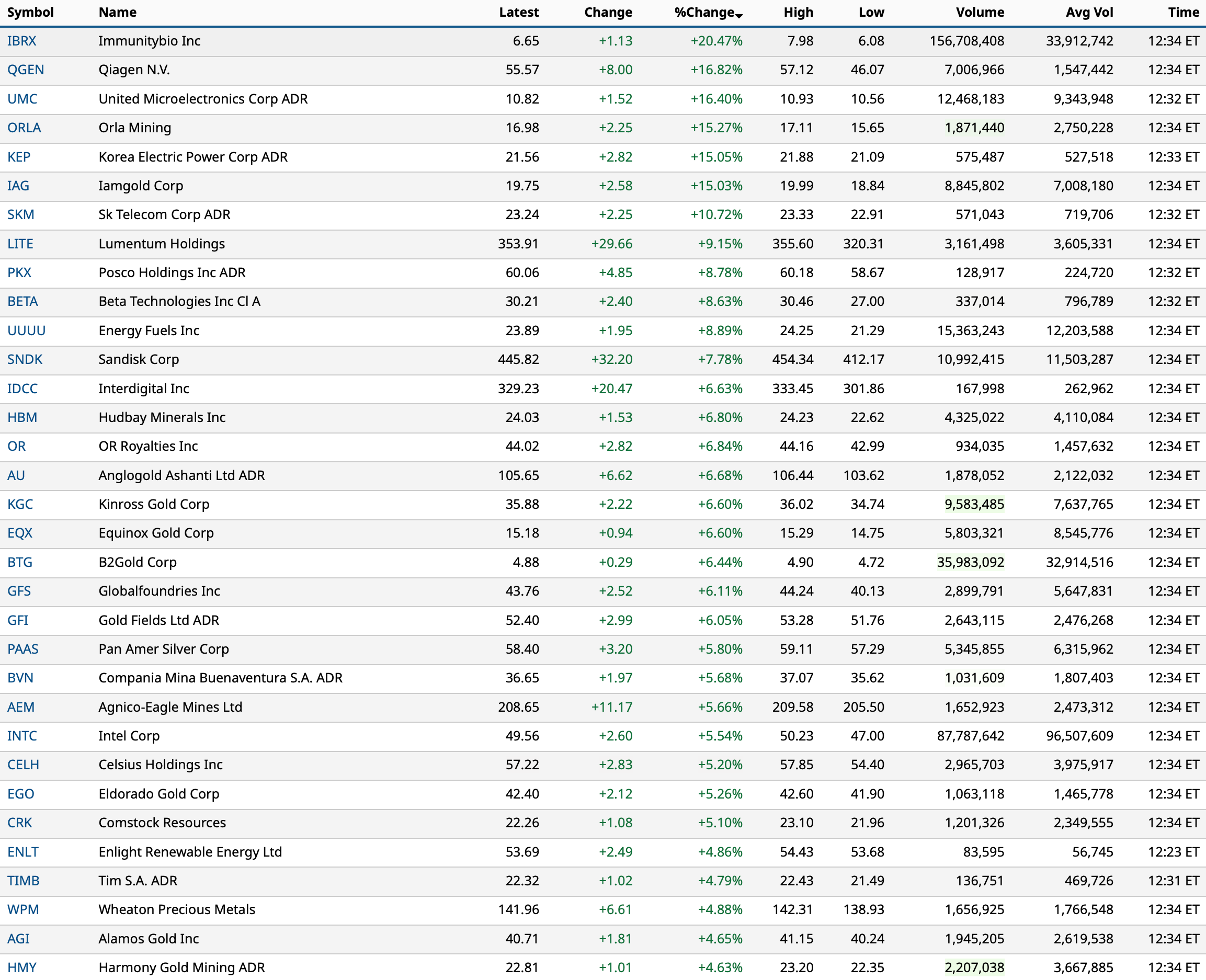

BY Doug Kass · Jan 20, 2026, 9:05 AM EST

-IBRX +20% (to resubmit sBLA for ANKTIVA in BCG-unresponsive papillary NMIBC)

-HL +7.4% (precious metals miner strength)

-AG +6.5% (precious metals miner strength)

-NVAX +6.0% (discloses license agreement with Pfizer to research, develop, and commercialize the Matrix-M Technology for use in vaccine products in at least one and up to two infectious diseases)

-AEM +3.9% (precious metals miner strength)

-ISOU +3.9% (commences winter drilling at Laroque East uranium project)

-NEM +3.0% (precious metals miner strength)

-PEBO +3.0% (earnings)

-NOW +2.4% (OpenAI signs deal to integrate AI agents into ServiceNow software)

-NBY -14% (entered an ATM Sales Agreement with Virtu for sale of up to $100M of shares)

-FAST -6.3% (earnings, guidance)

-CIEN -6.0% (Tier1 firm Cuts CIEN to Neutral from Buy, price target: $260)

-MMM -4.0% (earnings, guidance)

-MUR -3.7% (announced results from the Civette exploration well in Block CI-502 offshore Côte d’Ivoire)

-AMZN -2.5% (CEO: Seeing some sellers passing along tariffs and others are absorbing it)

-APP -7.0% (CapitalWatch issues short report alleging money laundering)

-SPWR -5.8% (earnings, guidance)

BY Doug Kass · Jan 20, 2026, 8:57 AM EST

Chart from 8:24 a.m. ET:

BY Doug Kass · Jan 20, 2026, 8:45 AM EST

11 a.m.: Treasury Announces a 4 and 8 Week Bill Auction;

11:30 a.m.: Treasury hosts a $89B 3 and a $77B 6-Month Bill Auction;

1 p.m.: Treasury hosts a $50B 52-Week Bill Auction;

1 p.m.: Treasury hosts an $85B 6-Week Bill Auction

11:30 a.m.: Federal Reserve Board of Governors Closed Board Meeting: Review and determination by the Board of Governors of the advance and discount rates to be charged by the Federal Reserve Banks.

BY Doug Kass · Jan 20, 2026, 8:36 AM EST

rolf thrane

3 minutes ago

No Clear Off-Ramp

Donald Trump continues to assert that the United States should acquire or control Greenland. While the rhetoric is persistent, military intervention is not a realistic option, notwithstanding public posturing.

There are numerous constraints, but one in particular stands out: it is highly unlikely that U.S. military leadership would support or execute an order to invade or coerce the territory of a NATO ally. I will not expand further on this point, both because this is not a political forum and because I naturally carry personal bias, having been born and raised in Denmark.

That said, the broader European reaction is best understood through precedent and deterrence. Trump’s continued framing of Greenland as something to be bought or won triggers deep resistance across Europe—not only in Denmark, but far beyond it. The underlying concern is obvious: what comes next? If Greenland can be pressured, why not Guadeloupe, Martinique, or French Guiana?

The Danes will not back down. Nor is there a compelling reason for Emmanuel Macron to do so. Macron’s legacy is very much at stake; he has no interest in appearing to have been bullied by the United States. On the contrary, there is growing sentiment within Europe that this is a moment to draw a firm line.

That is where the European Union Anti-Coercion Instrument comes into play. This EU law explicitly allows the Union to respond collectively when a non-EU country attempts to pressure or economically coerce a member state. If Trump were to impose retaliatory tariffs or other coercive trade measures against Europe, the EU would have little practical choice but to invoke it—not doing so would render the instrument meaningless.

Some European leaders increasingly view this confrontation not only as a risk, but as an opportunity to reinforce Europe’s strategic autonomy. In Denmark, Lars Løkke Rasmussen appears willing to take this issue head-on, in part because it strengthens his statesman profile and potentially positions him for a future return to the premiership. By contrast, the sitting prime minister, Mette Frederiksen, has so far taken a more cautious, lower-visibility approach.

The result is a standoff with no obvious or rapid off-ramp. De-escalation is possible, but it is unlikely to be quick, and it will almost certainly require a reframing of objectives rather than pressure tactics. As it stands, the incentives on all sides point toward persistence rather than retreat.

BY Doug Kass · Jan 20, 2026, 8:26 AM EST

BY Doug Kass · Jan 20, 2026, 8:10 AM EST

It is important to recognize that investment strategists (at JPMorgan and elsewhere) are not anticipatory, they are reactive:

From JPMorgan:

US MKT INTEL – We are Tactically Bullish but with near-term caution, meaning stay long but hedge. This section also includes color on variables shaping markets, including geopolitics, gov’t funding deadline, and housing. The Monetization Menu is unchanged except for adding downside hedges.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

We remain Tactically Bullish but with near-term caution. Our bullish framework is focused on (i) resilient macro growth; (ii) positive earnings growth; and (iii) a thawing trade war. This framework is now being challenged as the trade war may re-ignite but it is too early to suggest that the macro story deteriorates rapidly enough to flip bearish. We also think it is too early to abandon US assets and think it better to hedge downside, especially if we see a Trump pivot coming out of Davos.

· US MKT INTEL VIEW – Beginning with the macro landscape, we are of the view that the aggregate US Consumer is in a stronger position than is commonly thought. This household strength is basis for a US economy that may continue to grow above-trend and will be supported by fiscal tailwinds and still strong corporate sector. Next, earnings growth is expected to be robust with 14.4% EPS growth expected for the SPX, if you average consensus top-down ($305.57) and bottom-up ($310.50) estimates. This compares to 12.5% EPS growth expected for FY25 and 7.8% for FY24.

o The primary risks include (i) a US kinetic conflict; (ii) another inflation peak; (iii) weakness in small/medium businesses that leads to heightened unemployment; and (iv) AI fatigue / significant rotation away from US TMT.

BY Doug Kass · Jan 20, 2026, 8:00 AM EST

Today the "talking heads" on the Fin TV shows will tell us they sold down their portfolios on Thursday afternoon.

BY Doug Kass · Jan 20, 2026, 7:50 AM EST

BY Doug Kass · Jan 20, 2026, 7:40 AM EST

From Quoth the Raven:

BY Doug Kass · Jan 20, 2026, 7:30 AM EST

BY Doug Kass · Jan 20, 2026, 7:20 AM EST

Raise your hands if you want to listen to a bunch of blowhards at Davos on the business TV platforms today?

I thought so... very few hands.

Raise your hands if you want to make some money today.

I thought so... a lot of hands.

Well, let's get going!

BY Doug Kass · Jan 20, 2026, 7:10 AM EST

BY Doug Kass · Jan 20, 2026, 7:00 AM EST

* Technicians' super confidence and the absence of bears are signposts of a top...

Bonus — Here are some great links:

A-D Line Suggests Limited Drawdowns

The Deck Is Stacked With Strength

The Big Question for Small Caps

BY Doug Kass · Jan 20, 2026, 6:45 AM EST

BY Doug Kass · Jan 20, 2026, 6:35 AM EST

BY Doug Kass · Jan 20, 2026, 6:25 AM EST

The yield on the 10-year Treasury note is +6 basis points to 4.29%:

BY Doug Kass · Jan 20, 2026, 6:15 AM EST

BY Doug Kass · Jan 20, 2026, 6:05 AM EST

The S&P Short Range Oscillator remains overbought at 5.11% vs. 6.39%.

BY Doug Kass · Jan 20, 2026, 5:55 AM EST

BY Doug Kass · Jan 20, 2026, 5:45 AM EST