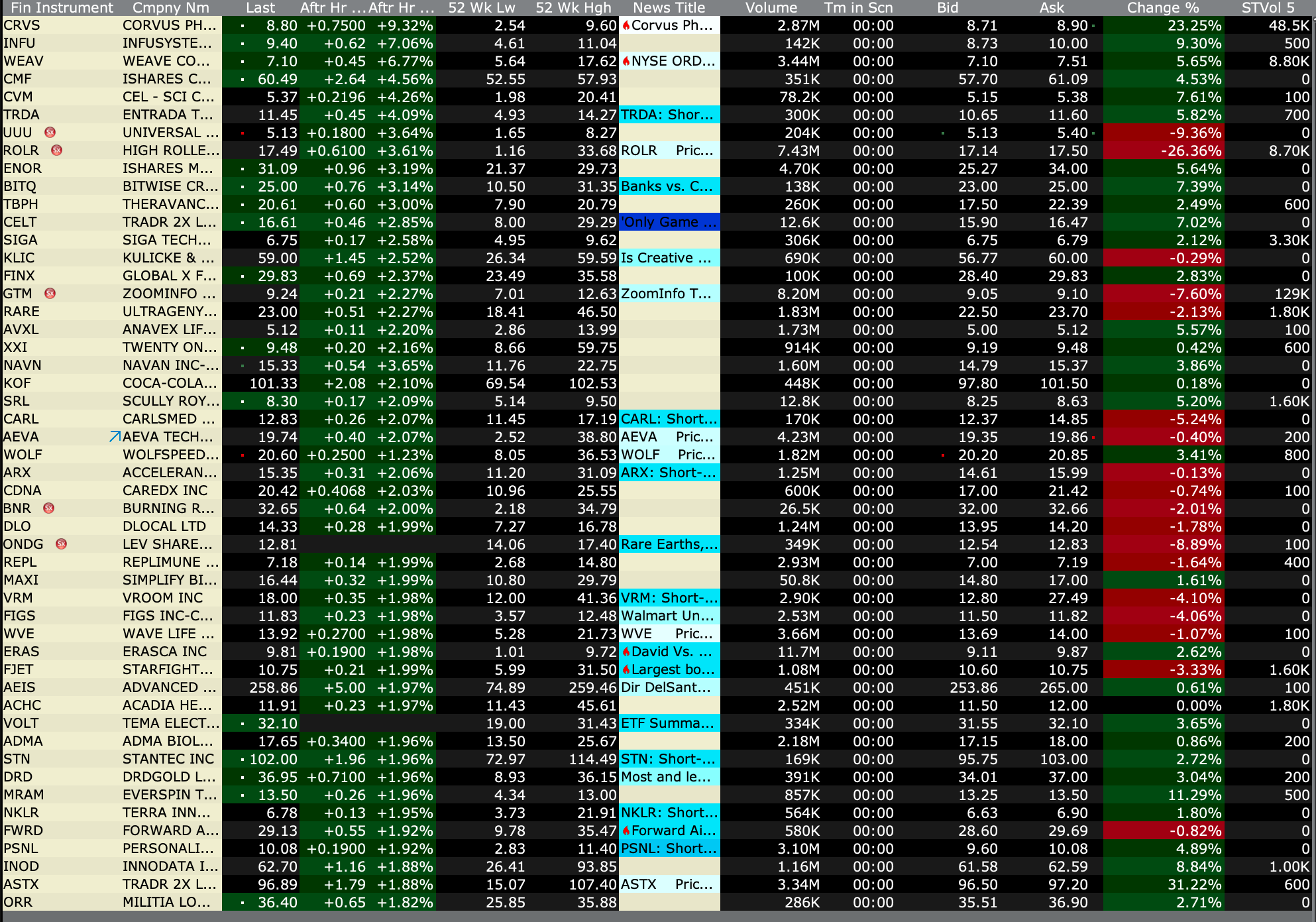

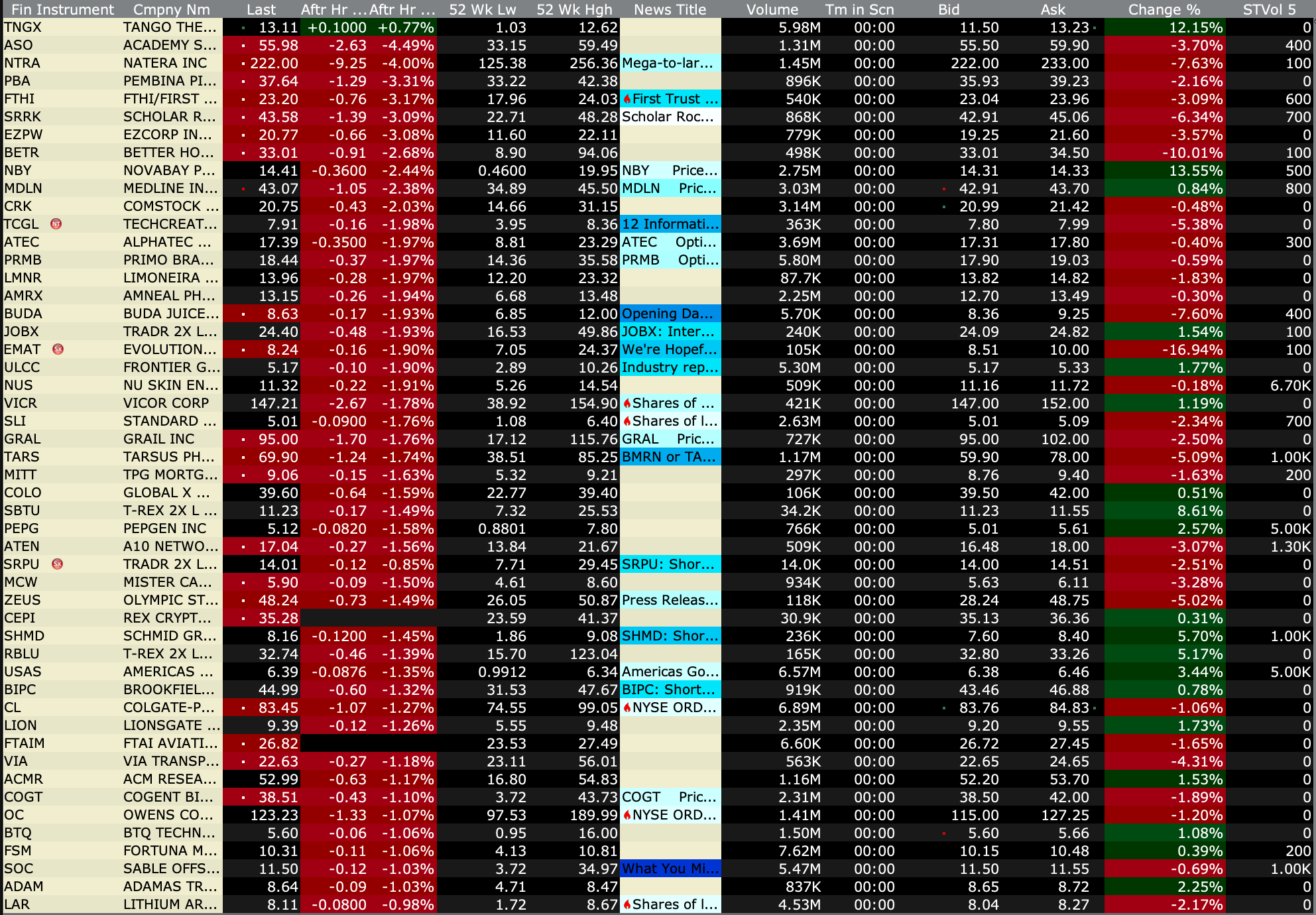

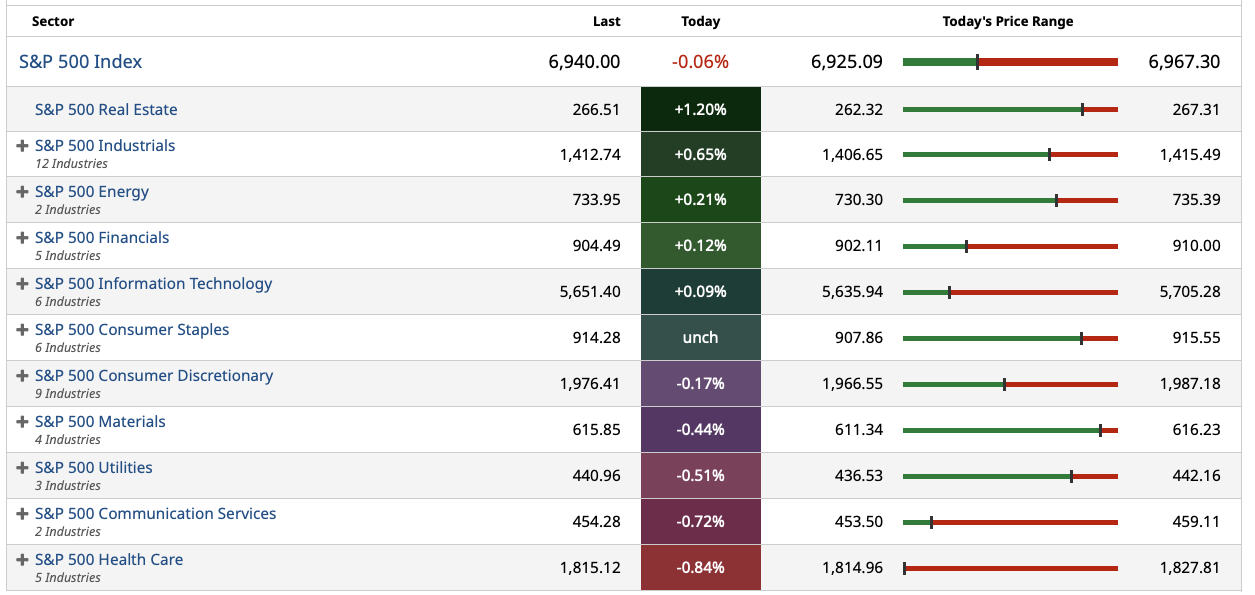

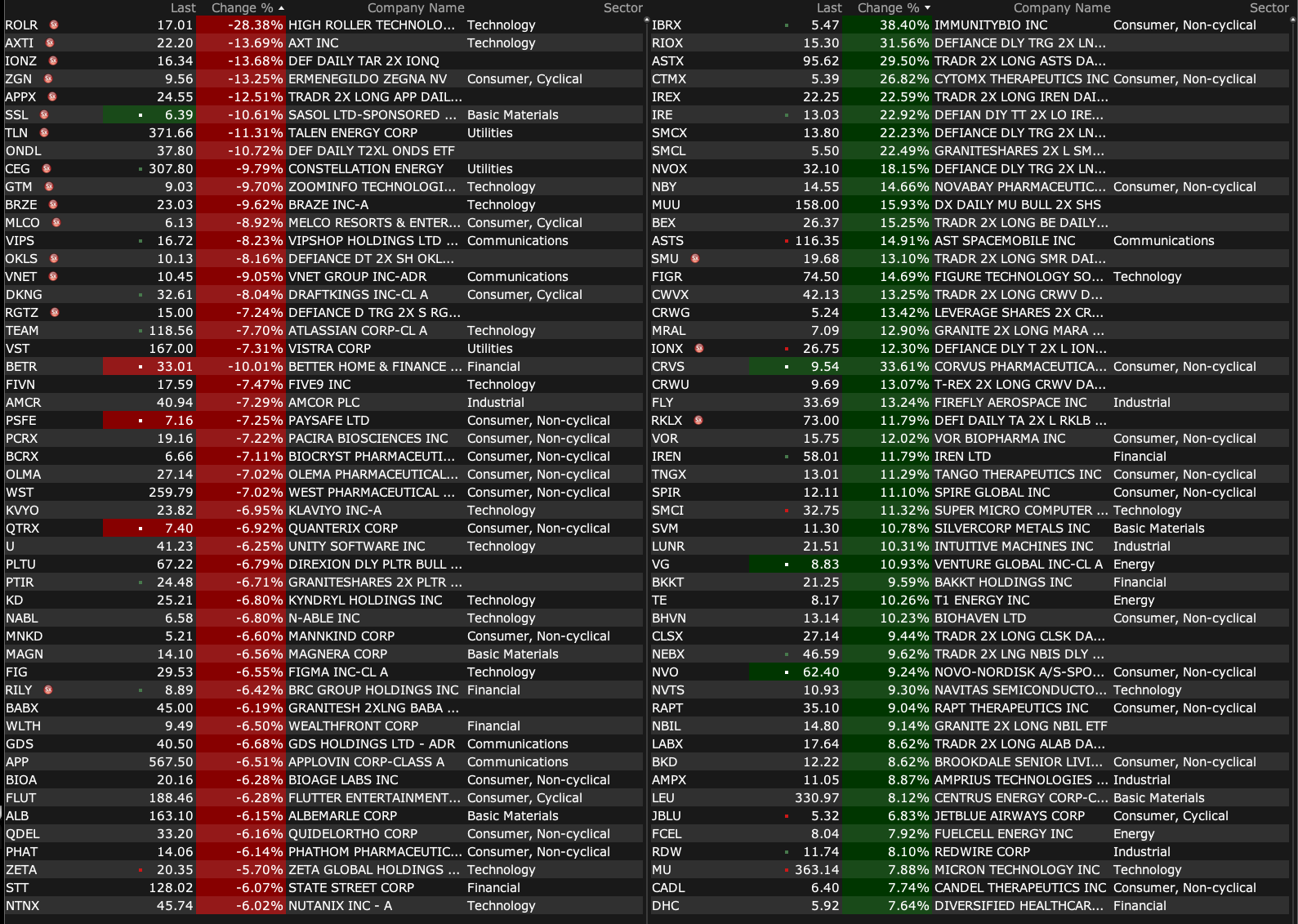

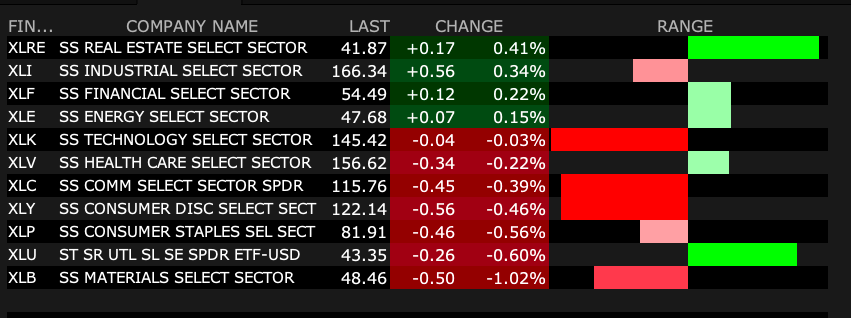

After-Hours Gainers and Losers

After-Hours % Gainers

After-Hours % Losers

BY Doug Kass · Jan 16, 2026, 4:45 PM EST

BY Doug Kass · Jan 16, 2026, 4:45 PM EST

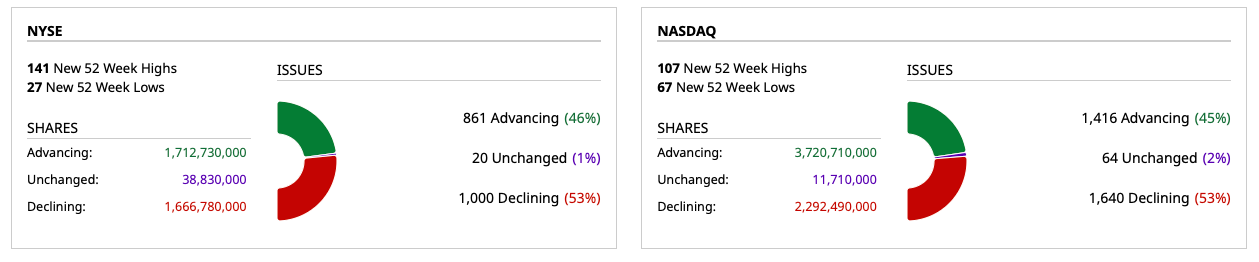

- NYSE volume 22% above its one-month average

- NASDAQ volume 9% above its one-month average

- VIX index: up 0.19% to 15.87

BY Doug Kass · Jan 16, 2026, 4:41 PM EST

I got the fever!

There are only 24 days to Spring Training!! Spring Training Countdown

In keeping with this, let's do a trivia question.

The winner gets a signed book! Amazon.com : doug kass

Which Brooklyn Dodger scout discovered my cousin Sandy Koufax?

And what famous Catholic chapel (in the Vatican) did the Dodger scout speak of when he referenced Sandy's pitching?

No cheating!

BY Doug Kass · Jan 16, 2026, 3:11 PM EST

(TLT) is at the low of the day.

BY Doug Kass · Jan 16, 2026, 2:43 PM EST

Kevin Warsh follows through with Pres. Trump’s view that the U.S. should have the lowest interest rates and cuts the Fed Funds rate to 2% by the end of 2026. At the same time he transfers the Fed’s mortgage holdings to government-sponsored enterprises and the Fed’s coupon holdings to the Treasury in exchange for short-term bills. He works relentlessly to shorten the duration of the Fed’s balance sheet and expresses a goal for 2027 to shrink it. The bond market cheers the more responsible balance sheet management and the 10-year bond rallies to 3.5% but Treasury supply/deficits keep the term premium elevated and the reappearance of inflation risk limits how far the long end can fall and the yield on the long bond remains stubbornly high.

Despite lower short interest rates, housing continues to suffer. After several years of rising prices, home prices are too high to attract adequate demand. Construction volumes suffer and homebuilders are caught with commitment to take delivery of lots from off balance sheet partners that they can’t fulfill. A housing prices war follows and the average new home prices falls 7%. Homebuilder stocks are down by greater than 25%. The resale market remains in the doldrums and volumes fall by 10%. Homebuilders such as Home Depot (HD) and Lowe's (LOW) , real estate brokers and furniture companies all collapse under the weight of lower home prices and slowing sales activity.

BY Doug Kass · Jan 16, 2026, 2:28 PM EST

On the little rally to +12 handles in the S&P, I got much shorter.

BY Doug Kass · Jan 16, 2026, 2:22 PM EST

I added to my (PLTR) short today.

BY Doug Kass · Jan 16, 2026, 2:03 PM EST

Here are today's things:

* Shorted (SPY) at $694.23 and (QQQ) at $624.97.

* Covered SPY at $690.95 and QQQ at $619.98.

* Shorted, covered and shorted SPY calls and QQQ calls.

* Shorted (CVNA) at $462.76, (GS) at $980.00, (MS) at $192.10.

* Shorted more (GRNY) at $25.93, (JOET) at $43.11.

BY Doug Kass · Jan 16, 2026, 1:07 PM EST

With S&P cash +5 handles I am back shorting index calls!

BY Doug Kass · Jan 16, 2026, 12:02 PM EST

- NYSE volume 60% above its one-month average;

- Nasdaq volume 15% above its one-month average;

- VIX index: up 0.57% to 15.93

BY Doug Kass · Jan 16, 2026, 11:30 AM EST

From Peter Boockvar:

Positives,

1) For the week ended 1/10, initial jobless claims fell to just 198k from 207k last week and this lowered the 4 week average to 205k from 212k. In the week prior (1/3) , continuing claims fell back under 1.9mm at 1.884mm from 1.903mm in the week before.

2) While some numbers still seem to be missing, December CPI rose .3% headline and .2% core with the former as expected and the core rate one tenth below expectations as said. The y/o/y gains were 2.7% and 2.6% respectively, unchanged from the prior reads.

3) There was a nice rebound in both the January NY and Philly manufacturing indices to +7.7 for the former and +12.6 for the latter vs -3.7 and -8.8 respectively in the month before. Capital spending plans increased for both.

4) From the Fed’s Beige Book: “Overall economic activity increased at a slight to modest pace in eight of the twelve Federal Reserve Districts, with three Districts reporting no change and one reporting a modest decline. This marks an improvement over the last three report cycles where a majority of Districts reported little change.”

5) With another drop in the average 30 yr mortgage rate to 6.18%, and after the holidays, refi’s spiked by 40% w/o/w and purchase applications were higher by 16% w/o/w.

6) Existing home sales in December totaled 4.35mm, 130k above expectations and a lift from 4.14mm in November. Assume these were closings of contracts signed at the end of the summer into early fall. With the sales lift, months’ supply fell to just 3.3. The NAR said “Inventory levels remain tight,” Yun added. “With fewer sellers feeling eager to move, homeowners are taking their time deciding when to list or delist their homes. Similar to past years, more inventory is expected to come to market beginning in February.”

7) The December NFIB Small Business Optimism index rose .5 pt m/o/m to 99.5 which puts it in line with the 6 month average of 99.4. The NFIB said “2025 ended with a further increase in small business optimism. While Main Street business owners remain concerned about taxes, they anticipate favorable economic conditions in 2026 due to waning cost pressures, easing labor challenges, and an increase in capital investments.” They mentioned taxes because that is now the single most important problem of small business as it jumped by 6 pts m/o/m. Quality Labor was number 2, down 2 pts m/o/m while inflation fell by 3 pts to 12.

8) From Taiwan Semi: “Recent developments in the AI market continue to be very positive...Looking ahead, we observe increasing AI model adoption across consumer, enterprise, and sovereign AI segments. This is driving the need for more and more computation, which supports the robust demand for leading edge silicon. Our customers continue to provide us with their positive outlook. In addition, our customers’ customers, who are many in the cloud service providers, also providing strong signals and reaching out directly to request the capacity to support their business.”

9) December US industrial production rose .4% m/o/m, above the estimate of up one tenth and November was revised up by two tenths. Manufacturing helped with the increase led by machinery and computer/electronics, offsetting a decline in the production of motor vehicles/parts. A 2.6% gain in utility output also lifted the headline figure. Mining production declined.

10) From JP Morgan: “Consumers and small businesses remain resilient. We continue to monitor leading indicators for any signs of stress, and despite weak consumer sentiment, trends in our data are largely consistent with historical norms, and we are not currently seeing deterioration...In terms of the outlook, we expect strong client engagement and deal activity in 2026, supported by constructive market dynamics, which is reflected in our pipeline.”

11) From Citigroup: “the global economy has powered through many shocks over the past few years, creating optimism and confidence that economic growth is poised to continue. With inflation now at normal levels globally, almost every central bank is becoming more accommodating. And while the labor market in the US has softened, capital investment remains strong, especially in tech, and it’s the combination of that CapEx, the health of the consumer, the tax bill benefits from anticipated rate cuts that should be enough to sustain growth. China is relying on exports to grow and compensate for slower domestic consumer demand, and Europe has taken some steps to accelerate its anemic growth, and we’re hopeful that Germany can create a meaningful stimulus.”

12) From Wells Fargo: “Credit performance was strong, and net charge-offs declined 16% from a year ago. The economy and our customers remain resilient, but we continue to closely monitor our portfolios for signs of weakness. In addition to tracking credit metrics in our loan portfolios, such as early stage delinquencies, we also monitor consumer behavior more broadly to help us understand consumer health. For example, we look at things like checking accounts with unemployment flows, direct deposit amounts, overdraft activity, and payment outflows, and we’ve not observed meaningful shifts in trends.”

13) From Bank of America: After going thru loan and charge off data, “Focusing on total net charge-offs, looking forward in the near term, we expect continued stability in total net charge-offs, given the mostly benign consumer delinquency trends and low unemployment data, the continued stability of C&I, and reductions in our commercial real estate exposures.”

14) From Delta: “Top line growth is accelerating on consumer and corporate demand, supporting an outlook for revenue growth of 5% to 7% in the March quarter. The US economy remains on firm footing and consumers continue to prioritize experiences with travel among the top spending categories...Business travel is showing signs of improvement as corporate confidence grows, with the most recent survey of corporate customers indicating that they expect to grow their travel spend this year.”

15) The Bank of Korea held its 7 day repo rate unchanged at 2.5% and hinted that they are now done cutting. “The general view is that rather than making a call on where the next six months are headed, it would be better to wait for more data and decide based on that.”

16) The European Sentix Investor Confidence index improved to -1.8 from -6.2 and better than the estimate of -5. Sentix said “Investors are starting the new year 2026 with slightly more confidence. The Sentix Economic Index for the Eurozone improved by 4.4 points to -1.8 points. This is the highest level since July 2025. In Germany, there is a small silver lining on the horizon at the start of the year. The overall index climbs by 6.3 points to -16.4 points, with the expectations component in particular sending a positive signal with an increase of 6.8 points.”

Negatives,

1) Jay Powell, you are one day closer to your June tee time.

2) In the Beige Book and to the slowdown in hiring we’ve seen in the data, “Employment was mostly unchanged in the most recent period, with eight of the twelve Districts reporting no changes in hiring. Multiple Districts reported an increase in the usage of temporary workers, with one contact reporting this allows them ‘to stay flexible in uncertain times.’ When firms were hiring, it was mostly to backfill vacancies rather than create new positions...Several reports mentioned that fewer workers were switching jobs.”

3) On costs from the Beige Book, “Prices grew at a moderate rate across a large majority of Districts, with only two Districts reporting slight price growth. Cost pressures due to tariffs were a consistent theme across all Districts. Several contacts that initially absorbed tariff-related costs were beginning to pass them on to customers as pre-tariff inventories became depleted or as pressures to preserve margins grew more acute. But contacts in a few industries—like retail and restaurants—were reluctant to pass costs along to price-sensitive customers. Energy and insurance costs continued to be a significant strain on margins. Looking ahead, firms expect some moderation in price growth, but anticipated prices to remain elevated as they work through increased costs.”

4) In the November PPI, core goods prices were up 3.2% y/o/y and that is before the 5% further increase in the CRB raw industrials index since November.

5) The CRB Raw Industrials index rose to the highest since 2022.

6) The Atlanta Fed’s wage tracker saw a slowing to 3.7% from 4% in December. For ‘job stayers’ wages were up 3.5% vs 3.7% in the month before. For those switching, wages grew by 4% vs 4.5% in November.

7) From JB Hunt: “As we move into 2026, the freight market feels fragile. Capacity continues to exit the truckload market, and we are testing the elasticity of supply...Demand in the fourth quarter aligned with expectations, and we continue to see the truckload capacity bubble deflate.” Also, “Most customers view the recent market tightening as temporary or seasonal rather than a structural shift. After several years of mixed signals and forecasting challenges, customers will only acknowledge a structural change after they feel a tighter market for a longer period of time, likely driven by some degree of both reduced capacity and stronger demand.” And, “Inflationary cost pressures continued to impact us in the quarter, but once again were more than offset by solid execution by our people on lowering our cost-to-serve and by driving efficiencies and productivity into our daily work.”

8) From Delta: “Effectively none of our growth in seats will be in the main cabin. They virtually all will be in the premium sector.” The CEO said “We realize that there’s still a fair bit of uncertainty in the environment, particularly on the geopolitical front. We’re not going to project or commit to record earnings until we understand the uncertainties a little bit better.”

9) Good for them but quite the global imbalance, China finished 2025 with a whopping $1.2 trillion trade surplus. Their December trade data well exceeded expectations with exports rising by 6.6% y/o/y, about double the estimate of 3.1%. Imports were higher by 5.7% y/o/y, well more than the estimate of up .9%.

10) ”I can tell your future, look what’s in your hand. But I can’t stop for nothing, I’m just playing in the band” sang Bob Weir.

BY Doug Kass · Jan 16, 2026, 10:50 AM EST

With S&P cash -18 handles (we shorted this morning +22 handles) we will ring the register on the balance of our Index shorts.

I plan to reshort on strength.

BY Doug Kass · Jan 16, 2026, 10:49 AM EST

From Peter Boockvar:

The Bank of Japan is not only in a rate hiking cycle, however glacial, and reducing their QE purchases, they are about to embark on selling its massive holdings of ETFs on Monday of which they own 83 trillion yen of at current market levels (about $500 billion). It will take though 251 years to fully liquidate at the pace they are doing so, 330 billion yen per year. Fortunately for the BoJ, their cost basis is about 37 trillion yen but I hope lessons are learned that the huge intrusion into the markets in order to generate higher inflation that many are so upset about should not be repeated.

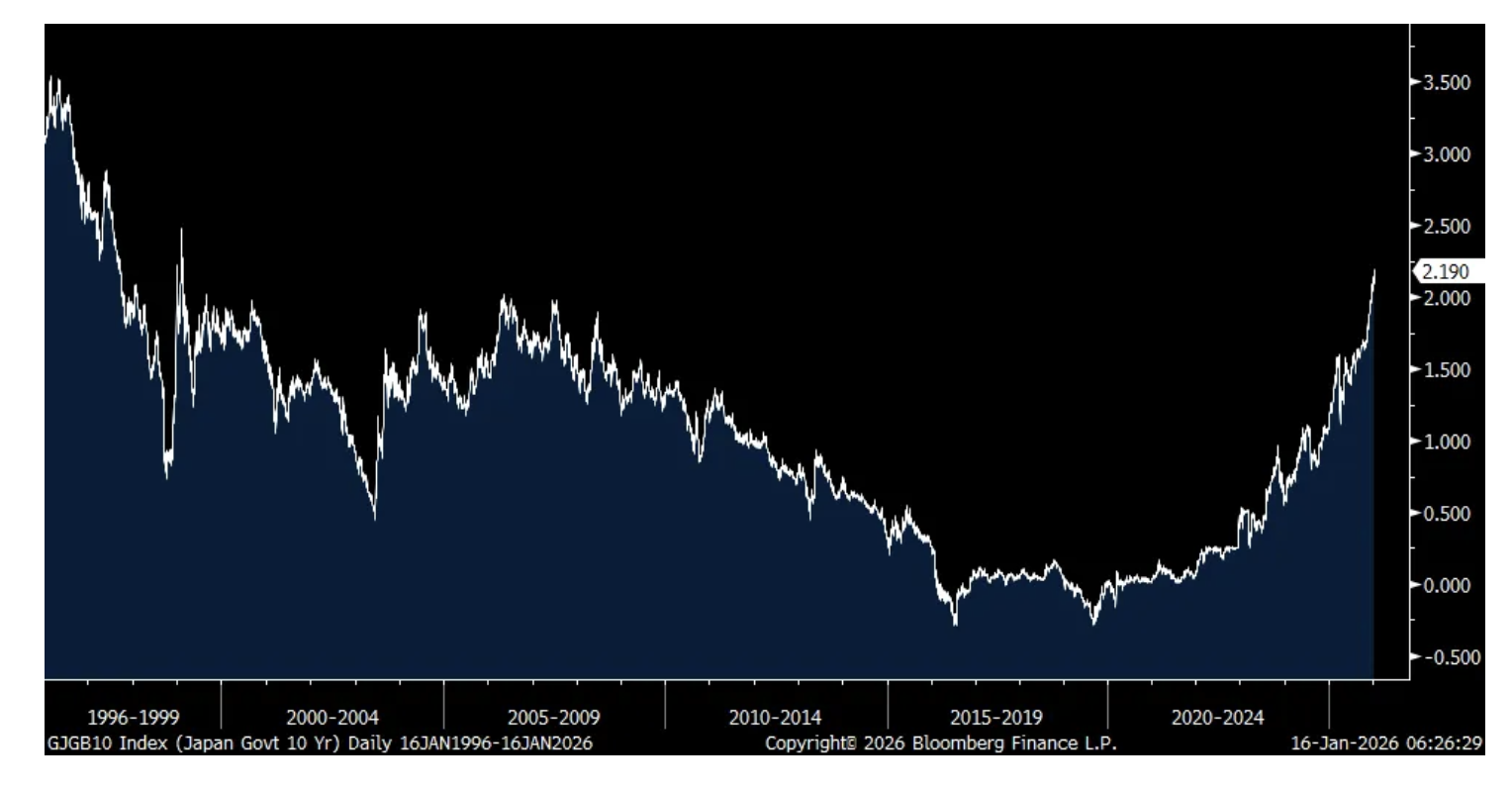

The 10 yr JGB yield by the way is up another 2.7 bps to 2.19%, a fresh 27 year high. The big question for global flows is at what level of yield do the Japanese decide to bring their large amount of overseas money home, especially from the US Treasury market. I don’t know the answer and it’s likely higher than where we are now but we’re quickly heading to that decision time.

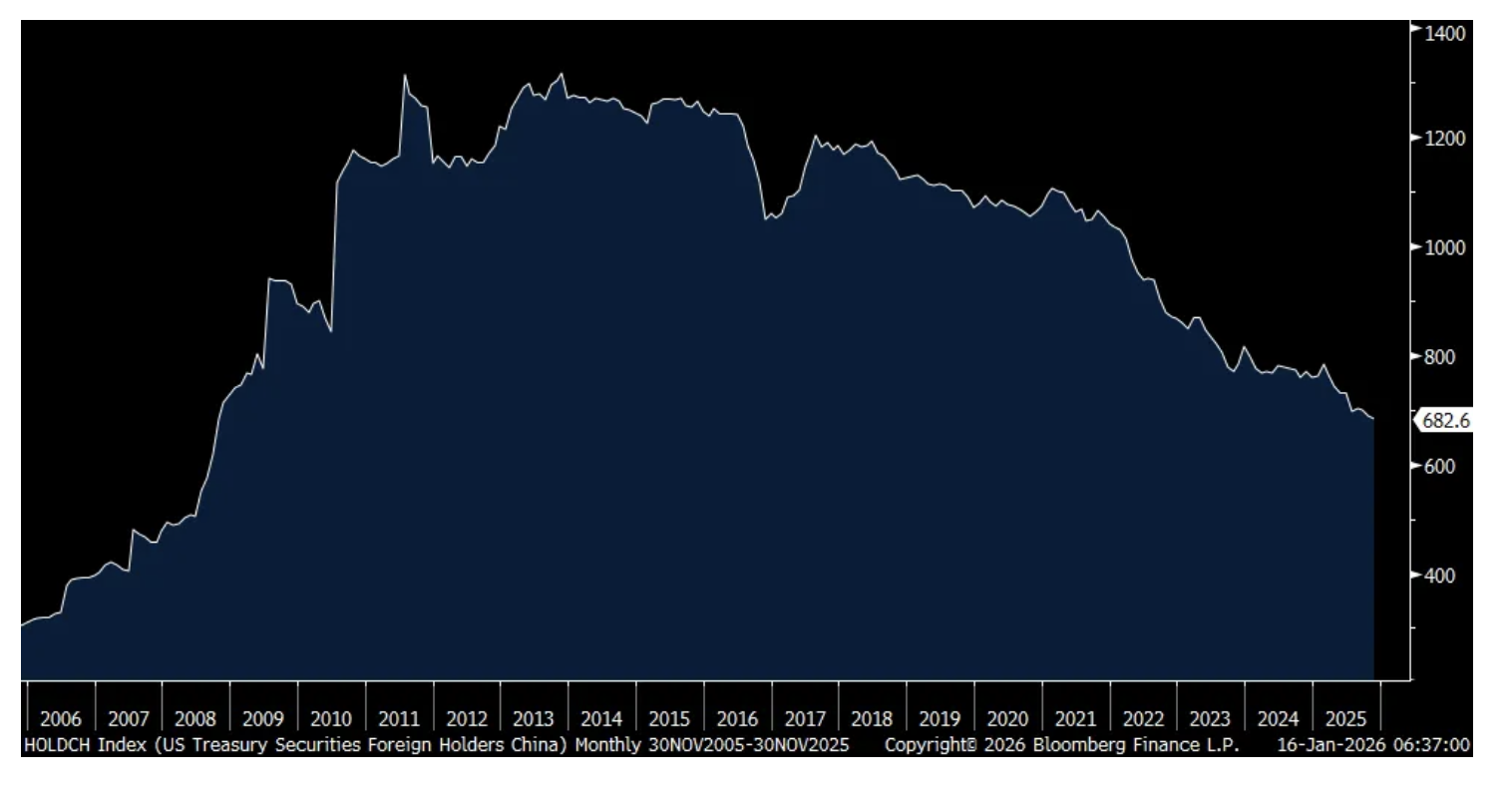

Japan did further add to its US Treasury holdings in November by $2.6b according to last night’s fresh TIC data to $1.2t, the most since 2022. China though continued to sell their holdings, by $6.1b and taking their holdings to $683b, the least since 2008.

Another day of verbal intervention threats also has the yen higher for the 2nd day in three. All something to watch this year I continue to believe.

10 yr JGB Yield

Japanese Holdings of US Treasuries

Chinese Holdings of U.S. Treasuries

In the midst of the recession in the US manufacturing sector, JB Hunt is trading down pre market after missing top line estimates though they beat on the bottom line. They said of note:

“As we move into 2026, the freight market feels fragile. Capacity continues to exit the truckload market, and we are testing the elasticity of supply...Demand in the fourth quarter aligned with expectations, and we continue to see the truckload capacity bubble deflate.” By ‘elasticity’, it was implied that any pick up in demand could lead to a quick rise in pricing.

And they seem ready to push price. “We’re going to be prudent with what the market will give us. Our customers know that we have inflation, and they know that we’re not happy with our margins. Now it’s just down to timing, but we’re not going to wait and sit back and just let all of this season go through without testing exactly what you’re saying (in terms of raising prices).”

“Most customers view the recent market tightening as temporary or seasonal rather than a structural shift. After several years of mixed signals and forecasting challenges, customers will only acknowledge a structural change after they feel a tighter market for a longer period of tome, likely driven by some degree of both reduced capacity and stronger demand.”

“Inflationary cost pressures continued to impact us in the quarter, but once again were more than offset by solid execution by our people on lowering our cost-to-serve and by driving efficiencies and productivity into our daily work.

To some data. The Atlanta Fed’s wage tracker saw a slowing to 3.7% from 4% in December. For ‘job stayers’ wages were up 3.5% vs 3.7% in the month before. For those switching, wages grew by 4% vs 4.5% in November. Some of this is tough comps but also certainly due to the slowdown in hiring.

Atlanta Wage Tracker

BY Doug Kass · Jan 16, 2026, 10:20 AM EST

I covered half my Index shorts when S&P cash went negative.

I plan to reshort on strength.

I am getting a bit more emboldened on the short side - and at some point these wont be short term rentals.

BY Doug Kass · Jan 16, 2026, 10:12 AM EST

With S&P cash +20 handles I am shoring index calls

BY Doug Kass · Jan 16, 2026, 9:45 AM EST

From JPMorgan:

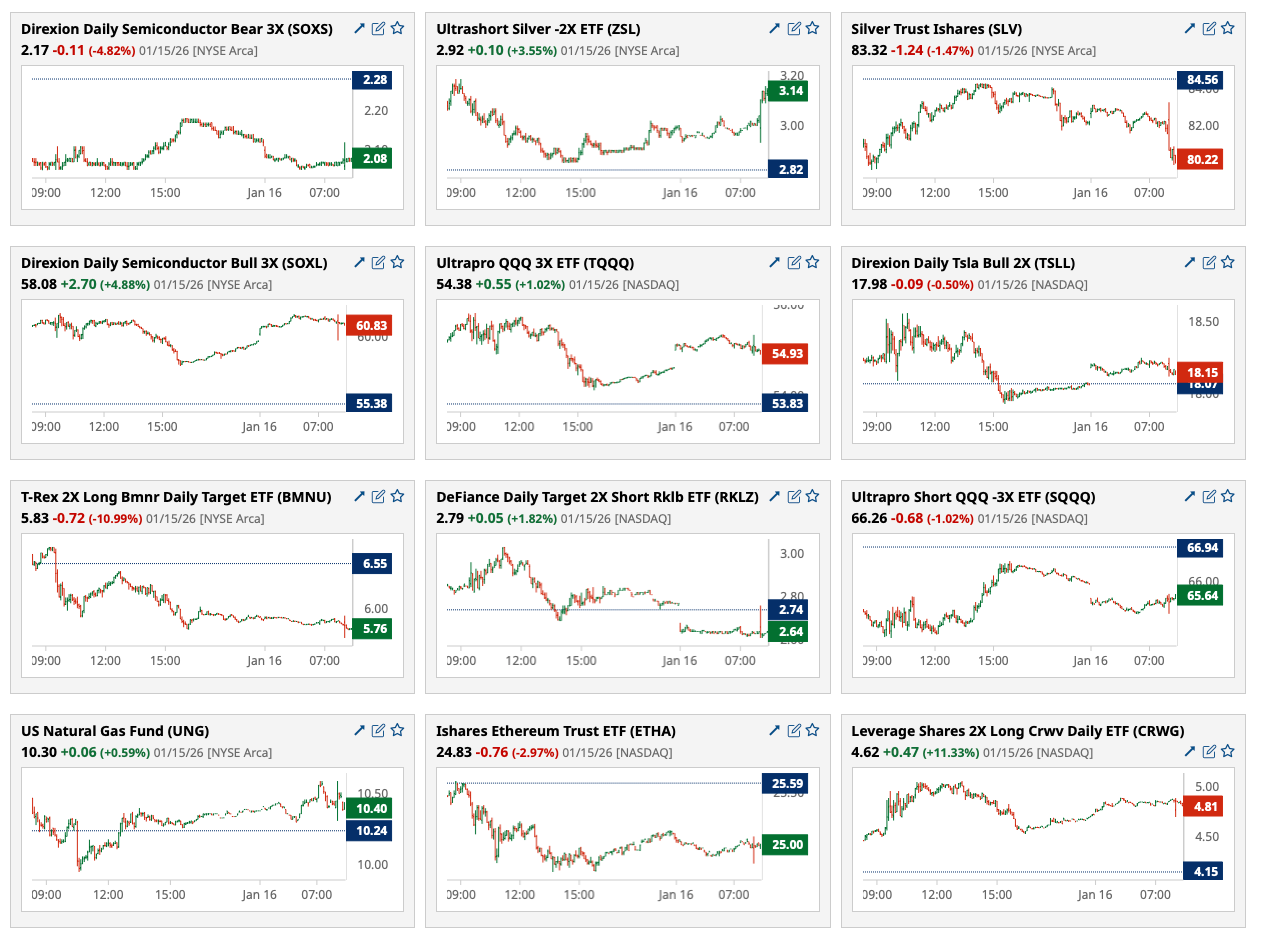

US: Futs are higher led by Tech. Overnight headlines were mostly muted. Pre-market, Mag 7 are mostly higher led by NVDA +1.1%; AI names (AMD +3.2%, AVGO +1.3%, etc.) continued their rally yesterday. Bond yields are unchanged. Commodities are mixed: oil added 1.2%, while silver fell -2.0%; ags are mostly higher.

and..

PM MARKET INTEL EQUITY & MACRO NARRATIVE

Yesterday, market saw some healthy gains with both Tech and Financials rebounding after the weakness so far this week. Pro-cyclical sectors continue to outperform with Industrials adding 0.9% yesterday. Despite the pressure from the upcoming 10% credit card rate cap, large banks earnings so far this week have been robust so far.

Moreover, we had some positive news on labor market: jobless claims fell to the lowest level since the end of November. OIS markets now sees 1.9 rate cut being priced in vs. 2.3 at the beginning of this year. Yesterday, we saw front-end yields rose 5bp with the curve flattened by 6bp amid hawkish labor market data and less-dovish Fedspeakers. Jay Barry tells us that “Though we see little room for front-end rates to move materially higher after the recent sell-off, near-term risks to the long-end of the curve likely skew flatter, and the 10s/30s curve appears too steep to fundamental drivers.”

BY Doug Kass · Jan 16, 2026, 9:40 AM EST

-VERO +300% (holder Madryn Asset Management raises stake)

-ACCL +50% (lockup expiration)

-IBRX +12% (advances First-Line BCG Naive NMIBC Program with Enrollment Exceeding Expectations and Positive Interim Analysis for ANKTIVA Plus BCG)

-ASTS +7.3% (awarded a contract for the Missile Defense Agency Scalable Homeland Innovative Enterprise Layered Defense (SHIELD) indefinite-delivery/indefinite-quantity (IDIQ) contract)

-MU +5.2% (breaks ground on $100B New York memory manufacturing complex)

-ONDS +5.2% (earnings, guidance)

-SNDK +5.0% (sector momentum)

-PLAY +4.8% (Benchmark Company Raised PLAY to Buy from Hold, price target: $30)

-PNC +3.2% (earnings, guidance)

-ABUS -17% (discloses European Patent Office revoked European patent EP 2279254)

-TLN -8.1% (Trump Administration aims to have data centers foot bill for rising power costs)

-QXO -6.9% (prices 31.6M shares at $23.80/share)

-WIT -5.9% (earnings, guidance)

-MOS -4.5% (prelim Q4 production)

-RF -4.4% (earnings, guidance)

-JBHT -3.7% (earnings, guidance)

-HPQ -2.9% (multiple broker downgrades)

BY Doug Kass · Jan 16, 2026, 9:15 AM EST

BY Doug Kass · Jan 16, 2026, 9:10 AM EST

Here are today's premarket things:

* I reshorted (SPY) $694,26

* I shorted (CRWV) $97.38, (GRNY) $25.93, (GS) $980.00 and (MS) $192.21.

BY Doug Kass · Jan 16, 2026, 9:05 AM EST

BY Doug Kass · Jan 16, 2026, 8:45 AM EST

10:50 a.m.: Fed Bank of Boston President Collins (Non-Voter) gives opening and introductory remarks before the Outlook '26 New England Economic Forum, Foxborough, MA (Embargoed text available. No Q&A. No webcast);

11:00 a.m.: Fed Vice Chair for Supervision Bowman (Voter) speaks on the outlook for the economy and monetary policy before the Outlook '26 New England Economic Forum, Foxborough, MA (Text available. Q&A from moderator. No webcast);

3:30 p.m.: Fed Vice Chair Jefferson (Voter) speaks on the economic outlook and monetary policy implementation before the American Institute for Economic Research, Shadow Open Market Committee, and Florida Atlantic University Conference, Boca Raton, FL (Text available. Audience Q&A expected. Webcast available)

BY Doug Kass · Jan 16, 2026, 8:21 AM EST

From Knowledge@Wharton: "The Skills Mismatch Economy: Insights from the Wharton - Accenture Skills Index"

BY Doug Kass · Jan 16, 2026, 7:23 AM EST

BY Doug Kass · Jan 16, 2026, 7:00 AM EST

BY Doug Kass · Jan 16, 2026, 6:45 AM EST

BY Doug Kass · Jan 16, 2026, 6:35 AM EST

* I eliminated my (RACE) long for a loss.

* I further sold off some of these longs: (PEP) and (PG) .

* I added to these shorts: (CVNA) and (JOET) .

BY Doug Kass · Jan 16, 2026, 6:15 AM EST

I am back shorting the indices (common):

* (SPY) $694.33

BY Doug Kass · Jan 16, 2026, 6:05 AM EST

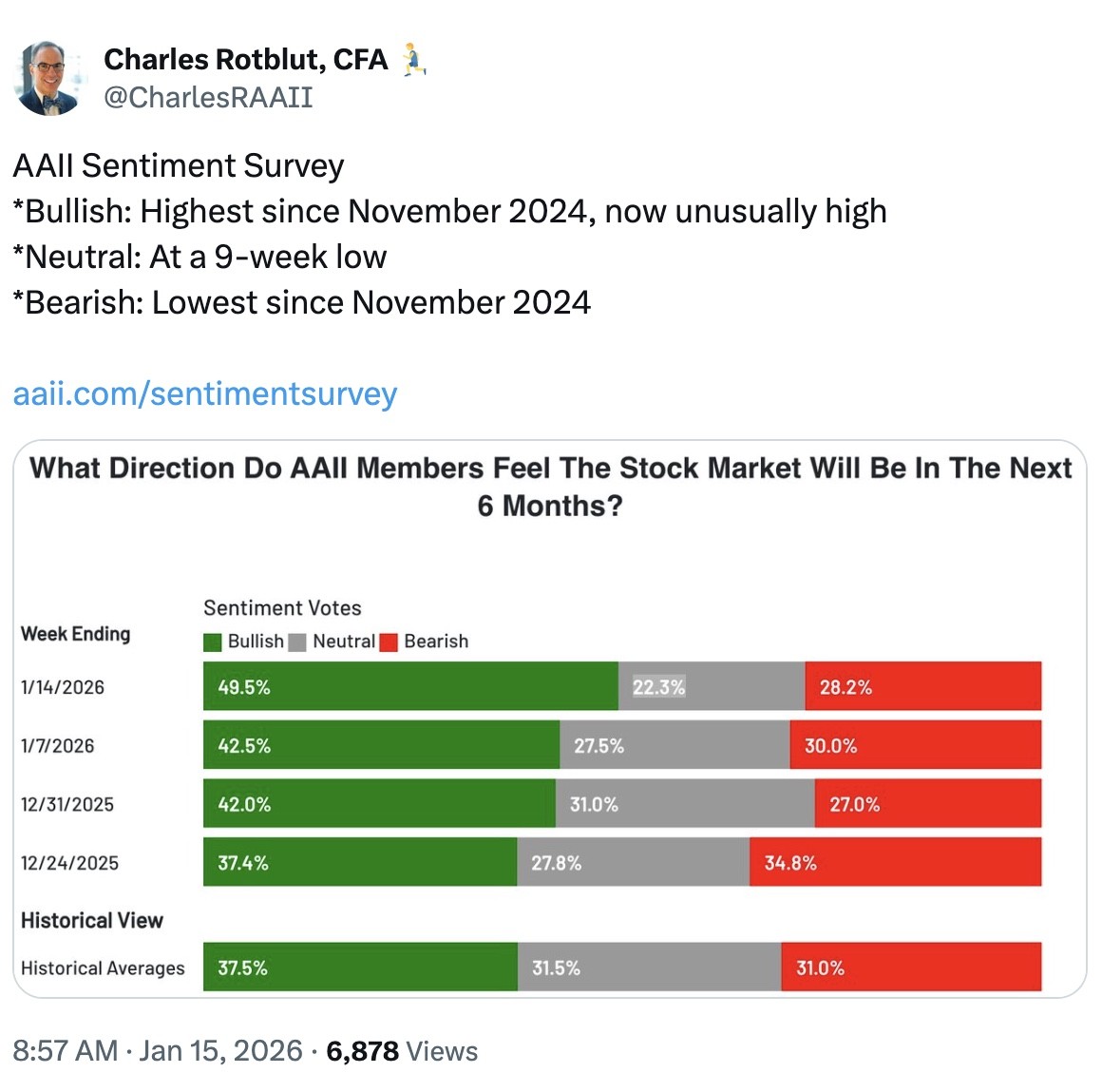

The S&P Short Range Oscillator gapped higher into a greater overbought at 6.39% vs. 4.39%.

More confirmation of an overbought is seen in the AAII Sentiment Survey:

BY Doug Kass · Jan 16, 2026, 5:57 AM EST

BY Doug Kass · Jan 16, 2026, 5:50 AM EST