Howling About CPI

Wolf Street howls about the CPI.

BY Doug Kass · Jan 13, 2026, 4:50 PM EST

Wolf Street howls about the CPI.

BY Doug Kass · Jan 13, 2026, 4:50 PM EST

BY Doug Kass · Jan 13, 2026, 4:40 PM EST

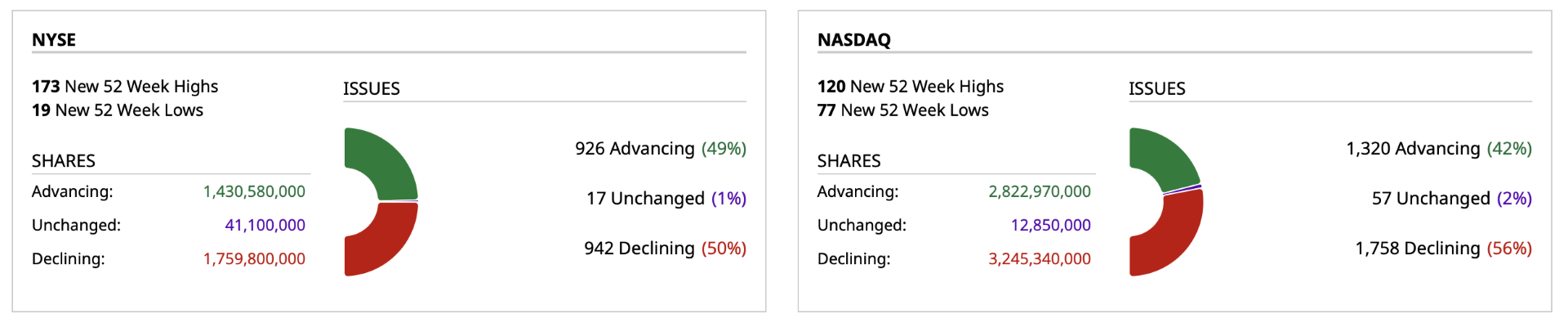

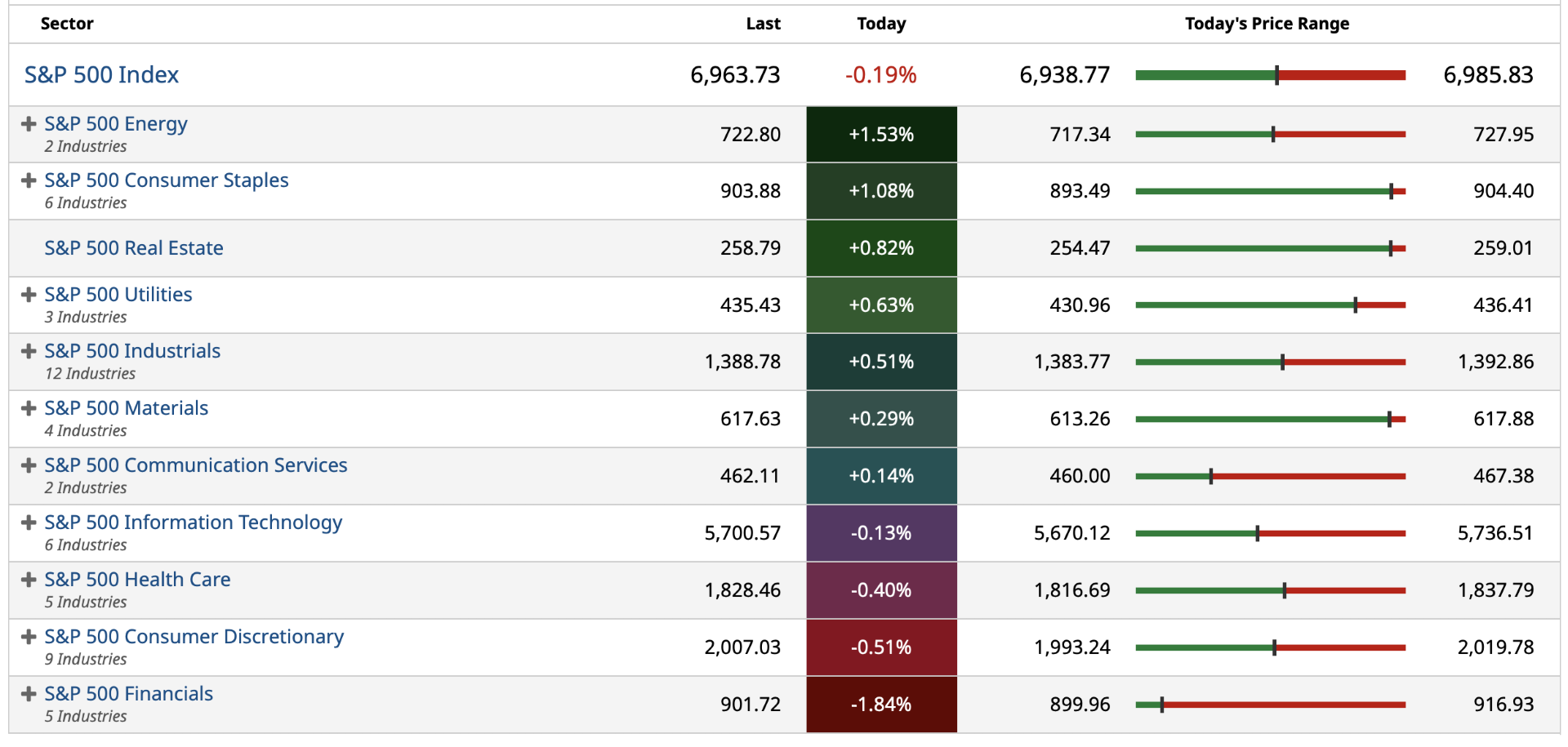

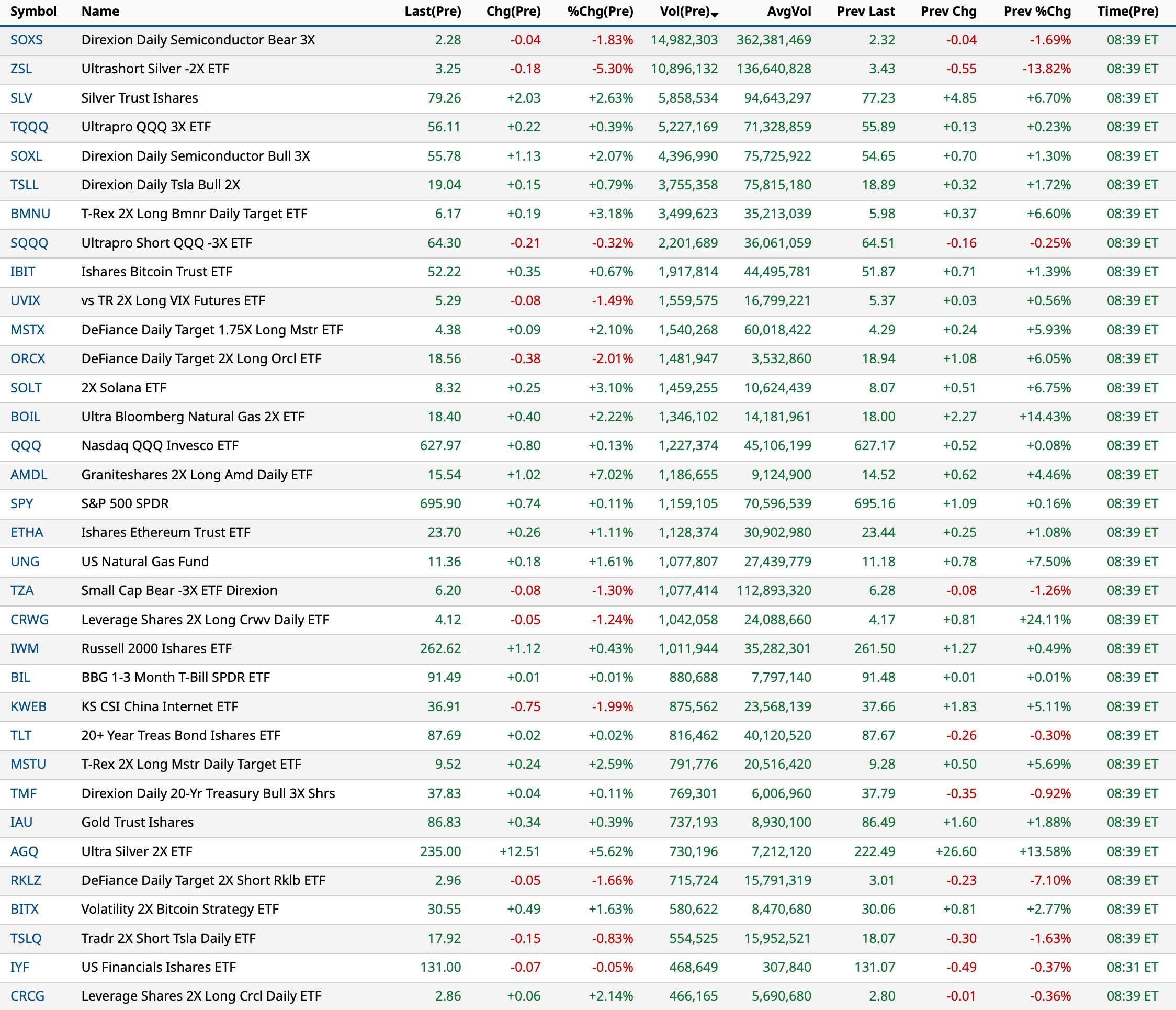

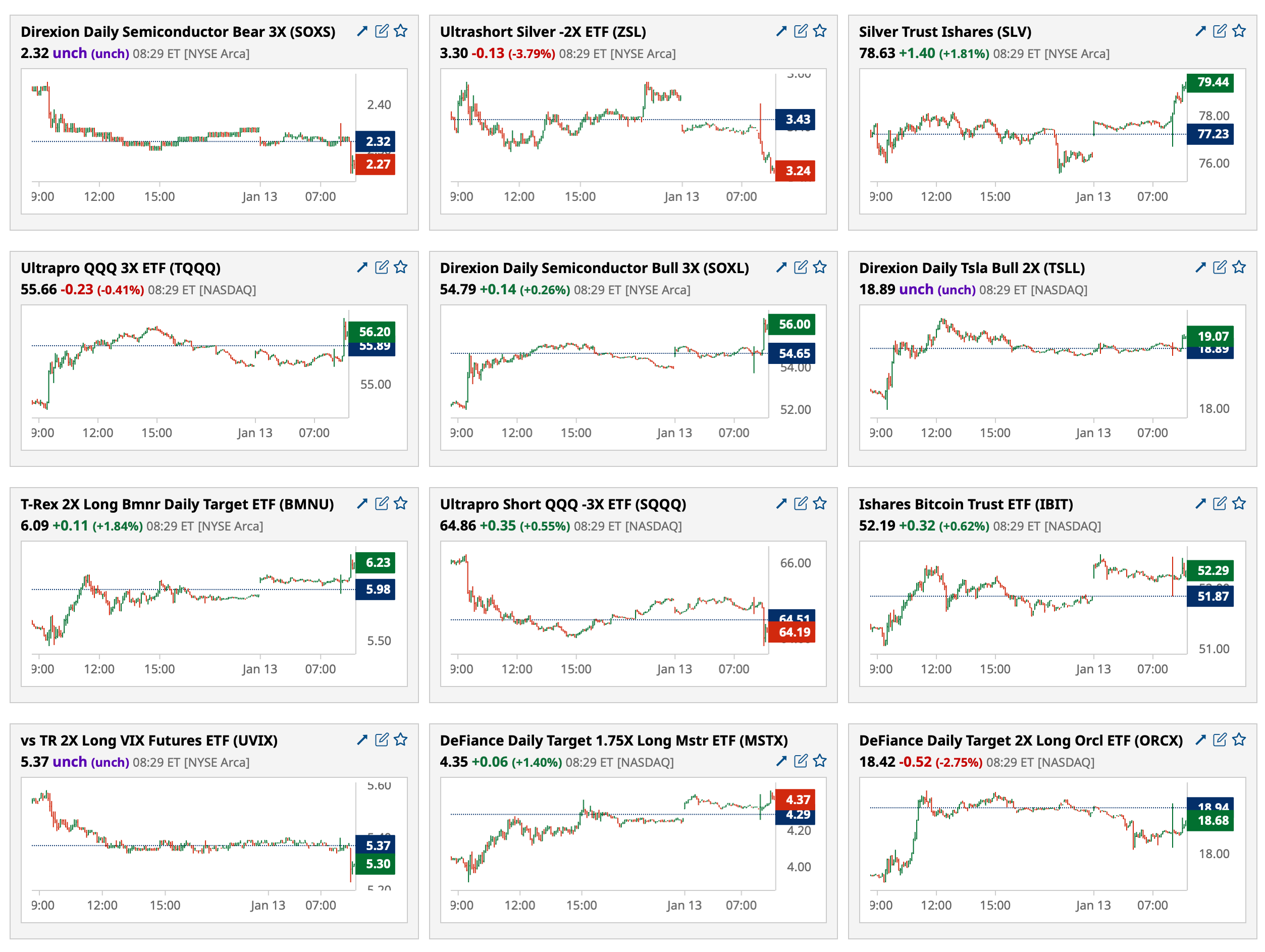

- NYSE volume 7% above its one-month average;

- NASDAQ volume 12% above its one-month average;

- VIX index: up 5.56% to 15.96

BY Doug Kass · Jan 13, 2026, 4:31 PM EST

With S&P cash -14 handles, I am scaling back into index shorts — via short calls.

BY Doug Kass · Jan 13, 2026, 4:02 PM EST

BY Doug Kass · Jan 13, 2026, 3:25 PM EST

More financials on the earnings calendar for pre-open tomorrow morning (Wed. Jan 14th):

BY Doug Kass · Jan 13, 2026, 3:22 PM EST

At 2:28 PM:

BY Doug Kass · Jan 13, 2026, 2:31 PM EST

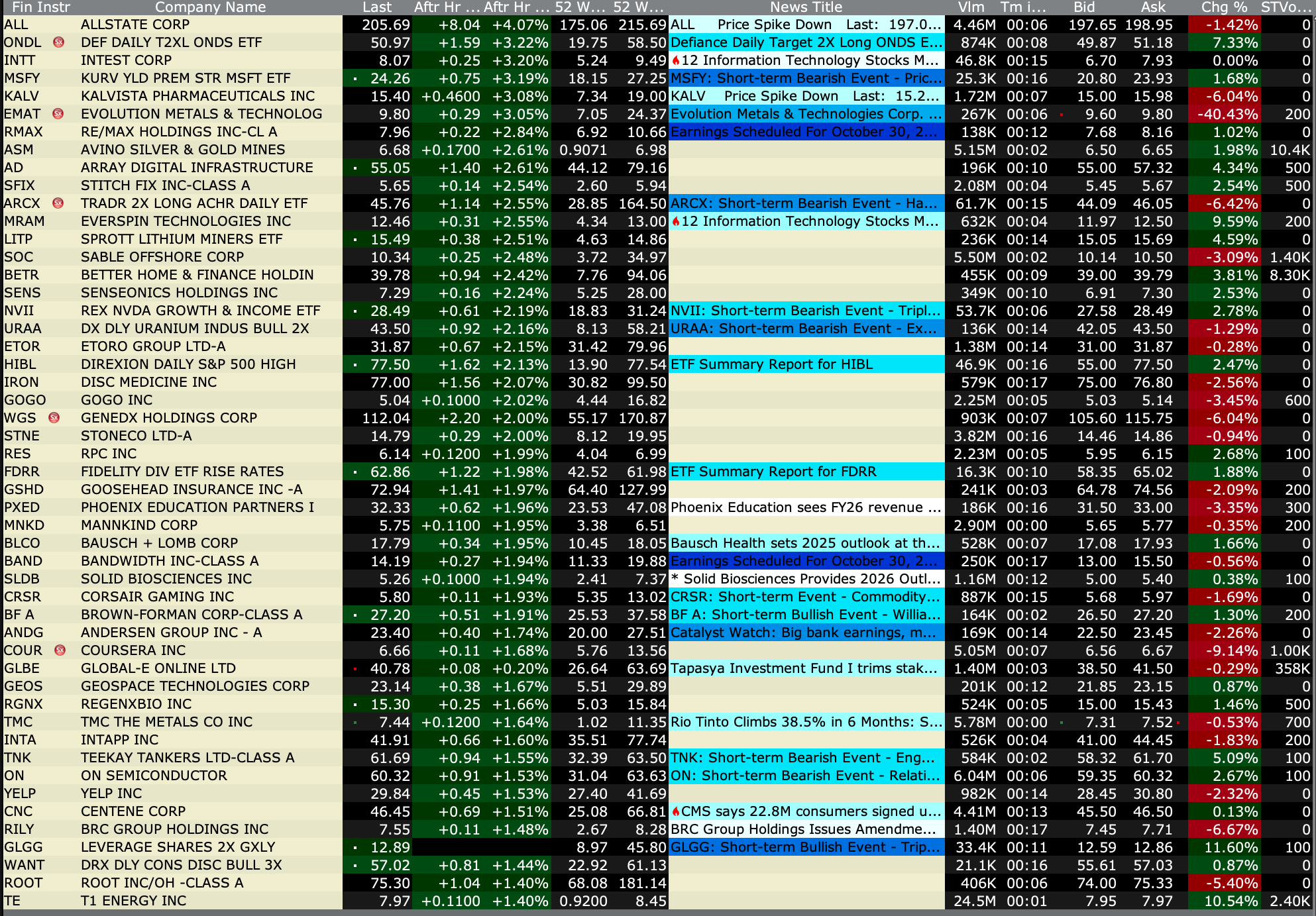

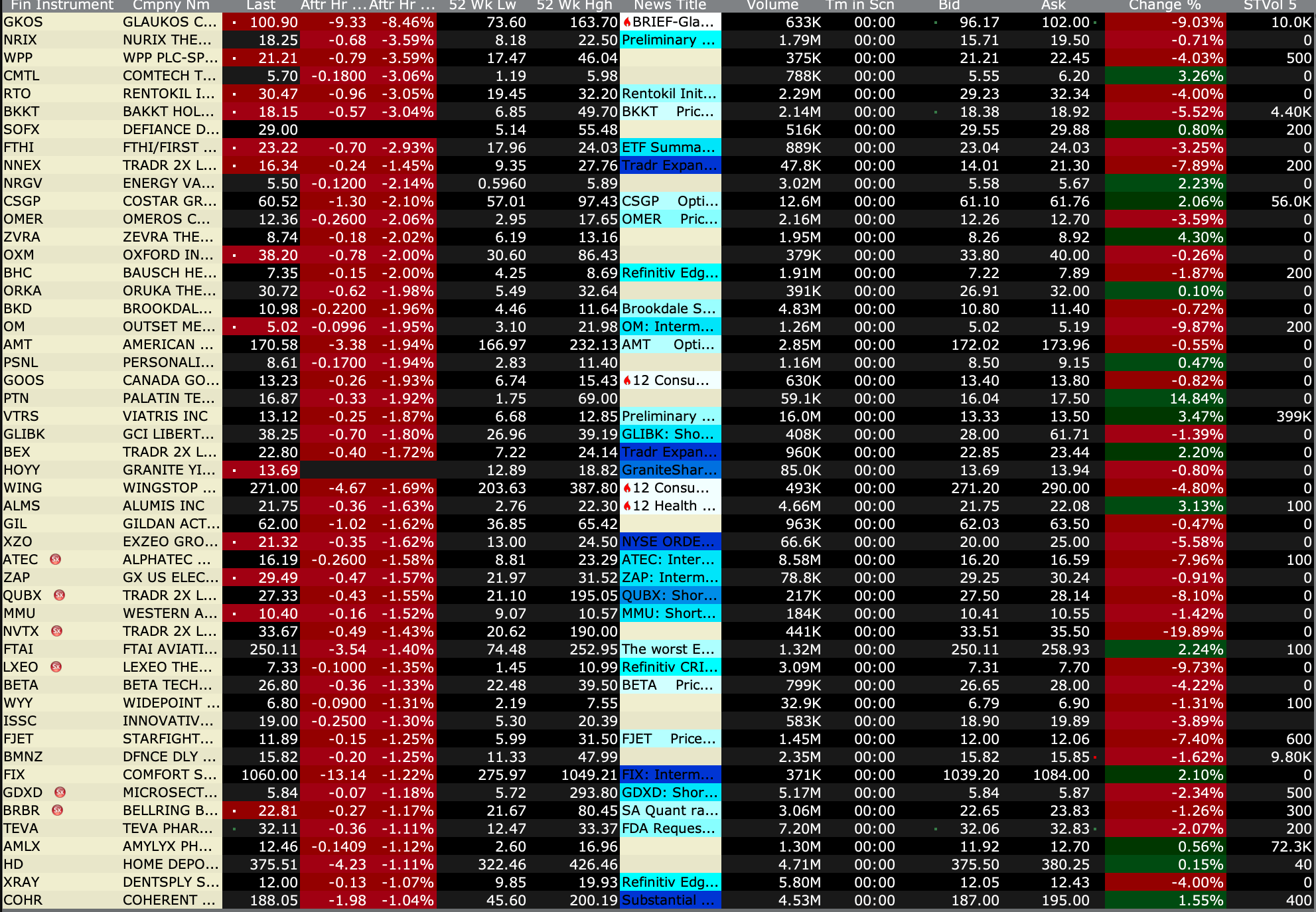

Time and time again I warn about herd-like investor behavior.

Recently (and again in this morning's opener) I cautioned that investor sentiment was growing too optimistic in the financial equity sector of money center banks, regional banks and credit card companies.

That over-confident and bullish view was seen recently in my daily "Charting the Technicals" column (every morning) and in the business media (in which, yesterday, one "talking head" on a noon show proudly proclaimed that she was 10 percentage points overweighted in the financials group).

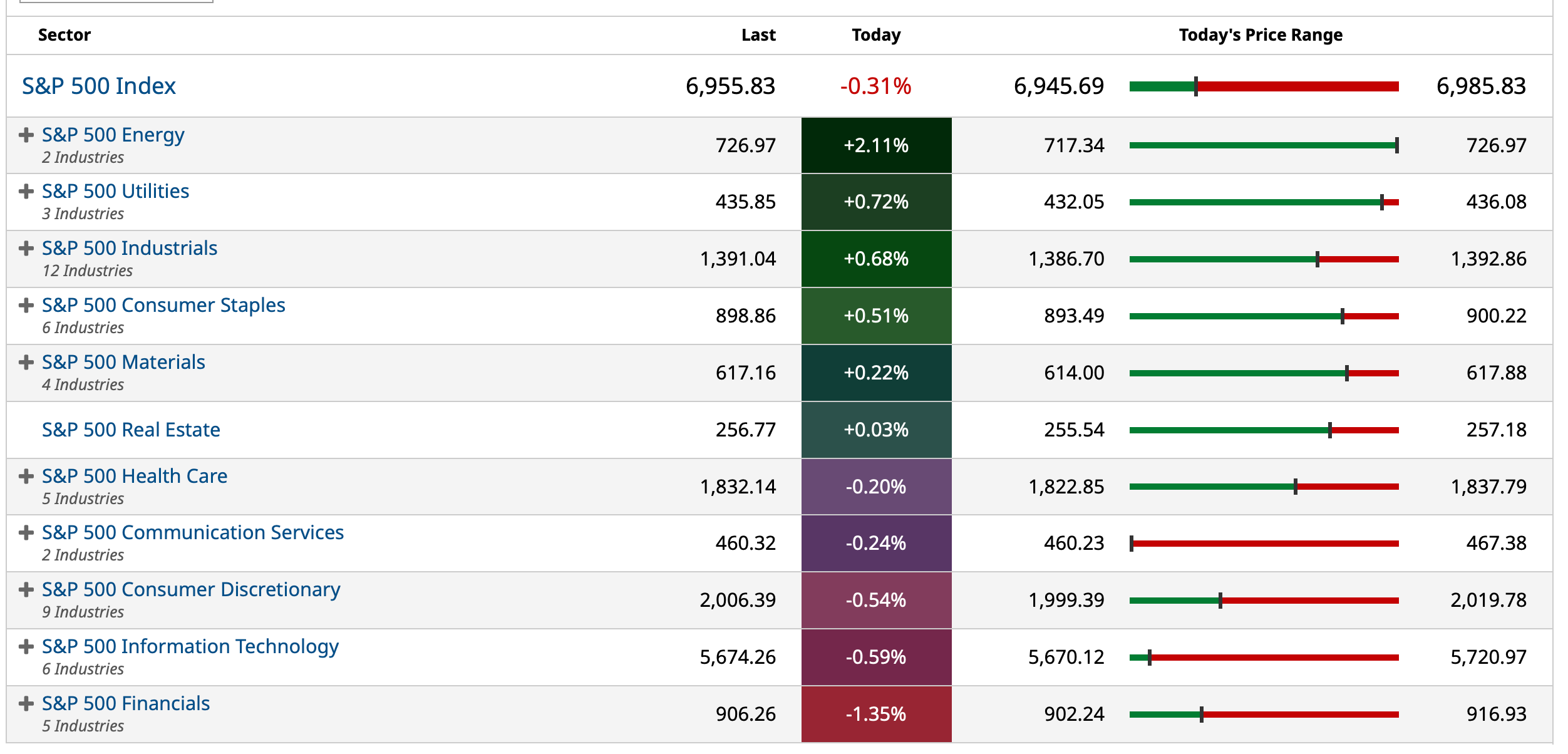

Well, the financials are massive underperformers today:

* (JPM) -$12

* (MS) -$3.50

* (GS) -$10

* (V) -$14

* (MA) -$20

BY Doug Kass · Jan 13, 2026, 2:21 PM EST

PepsiCo (PEP) is up by another +$1.40 today.

The world's fair...

BY Doug Kass · Jan 13, 2026, 1:45 PM EST

My expectation is that 2026 will be an ideal market for opportunistic traders.

But not so great for the buy-and-hold crowd.

BY Doug Kass · Jan 13, 2026, 1:11 PM EST

I averaged up on my (SPY) (call) shorts and have a quick profit.

So, with S&P cash -22 handles, I am covering all of my SPY and (QQQ) call shorts.

I have no index positions on now.

BY Doug Kass · Jan 13, 2026, 1:04 PM EST

With S&P cash -12 handles (a nice rally off of the lows) I am re-shorting (SPY) calls — on a scale with a wide berth.

BY Doug Kass · Jan 13, 2026, 11:39 AM EST

BY Doug Kass · Jan 13, 2026, 11:30 AM EST

BY Doug Kass · Jan 13, 2026, 11:25 AM EST

From Peter Boockvar:

Before I get into the numbers, just a heads up that for some reason I see a dash in the line item for ‘motor vehicle insurance’ which we know has been rising robustly. Maybe a factor in why the core rate was one tenth below the estimate.

December CPI rose .3% headline and .2% core with the former as expected and the core rate one tenth below expectations as said. The y/o/y gains were 2.7% and 2.6% respectively, unchanged from the prior reads. Food prices accelerated to a .7% m/o/m gain for both ‘food at home’ and ‘food away from home’ while energy prices were up .3% m/o/m driven by a 4.4% pop higher in ‘utility gas service’ after three months of declines. Food/beverage prices are up 3% y/o/y while energy costs are up 2.3% y/o/y. Electricity prices in particular were down .1% m/o/m but jumped by 6.7% y/o/y as data center usage juices prices for the rest of us.

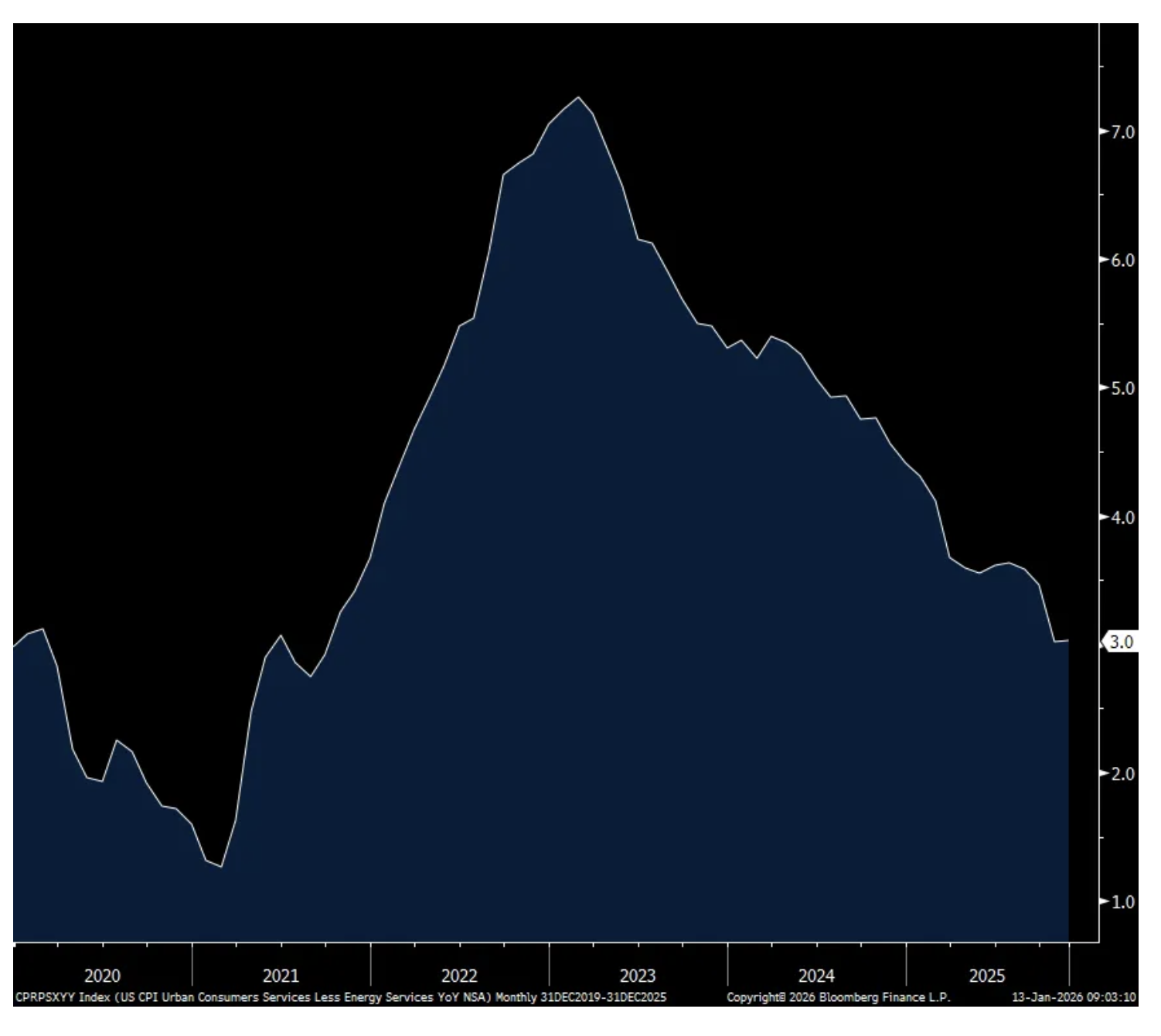

With services, prices here grew .3% ex energy and 3% y/o/y. Rents again led the way as OER was up .3% m/o/m and 3.4% y/o/y. Rent of Primary Residence saw a .3% gain too and up 2.9% y/o/y. Yes, blended rents are rising more like 2-3% in real life but we’re getting closer to reality. Vehicle maintenance costs fell 1.3% m/o/m but still up 5.4% y/o/y. With car insurance, while there was no m/o/m figure, the BLS report did show a 2.8% y/o/y increase and we can thus extrapolate. Airline fares jumped 5.2% m/o/m but still down 3.4% y/o/y. Hotel prices were up 3.5% m/o/m but down 1.8% y/o/y. Medical care costs rose .4% m/o/m and 3.2% y/o/y and remains a steady piece of higher services inflation. CPI is still VERY MUCH undercounting healthcare insurance costs as in the December data it showed a 1.1% m/o/m decline and .5% y/o/y drop. Nowhere I’m aware of is that reality.

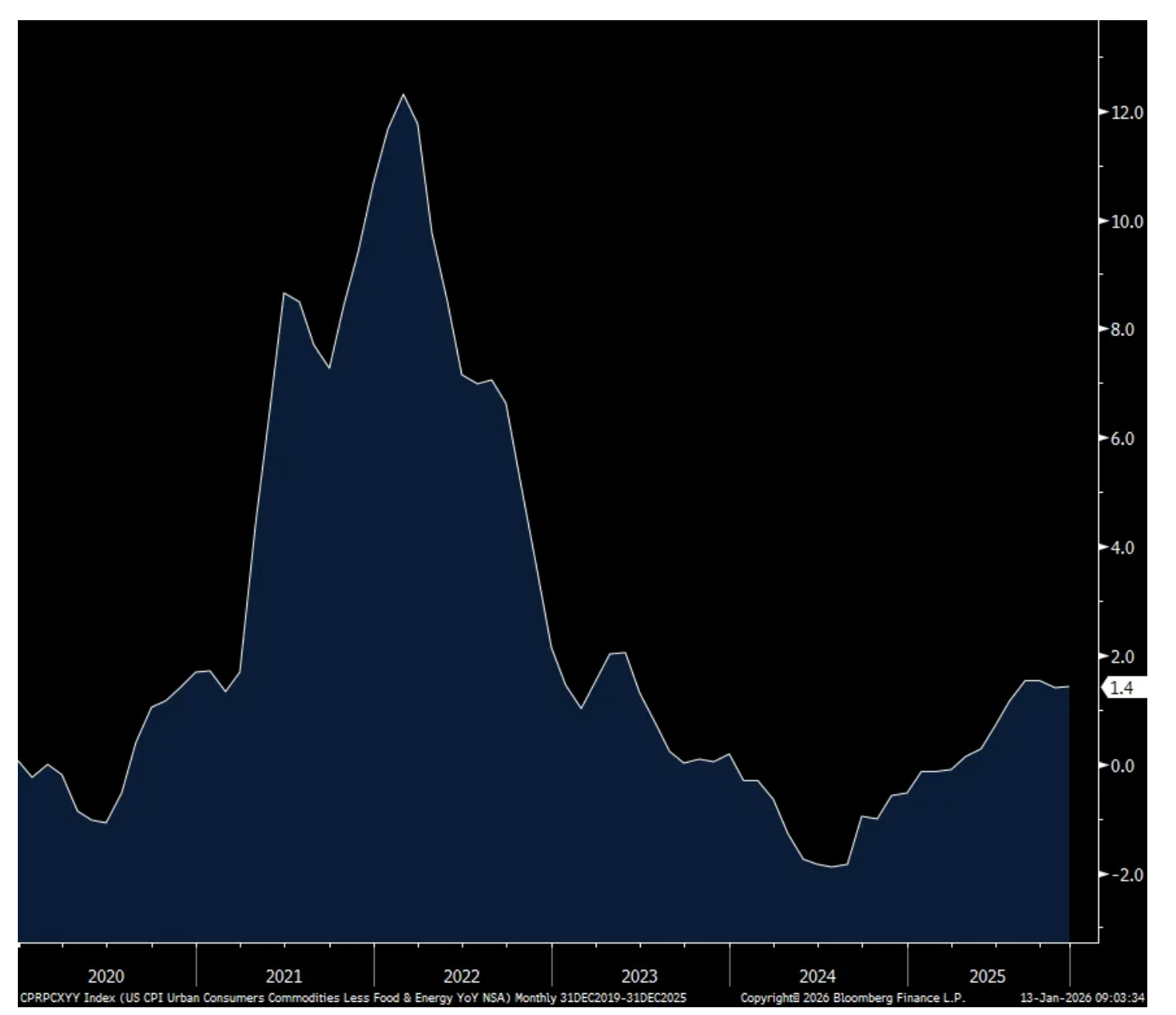

Core goods prices were unchanged m/o/m, though up 1.4% y/o/y. Used car prices kept the m/o/m figure in check as they fell 1.1% but still up 1.6% y/o/y. New car prices were flat vs November and little changed y/o/y. Apparel prices were up .6% both m/o/m and y/o/y. Household furnishings and supplies saw a .5% m/o/m price gain and 3.4% y/o/y with tariffs an big influence here and why they are being scaled back.

The blue pen is where I mark the missing ‘motor vehicle insurance’ m/o/m figure and I’m guessing it was thus not included in the headline/core m/o/m figure.

Bottom line, no real surprises and why the 2 yr inflation breakeven is unchanged. Maybe we’ll read more about the missing ‘motor vehicle insurance’ line. Treasury yields are down a touch post number because of no upside surprises. The 2 yr is down about 1 bp as is the 10 yr and 30 yr yields after 8:29am est.

In the first half of 2026 I do expect a further moderation in rents tempering gains on the service side, but goods price deflation has seemingly ended. Overall, I don’t think Jay Powell is cutting rates again in his remaining 3 FOMC meetings unless the unemployment rate jumps again and/or we see notable deceleration in inflation in the coming months. If correct, the next Fed cut won’t come until June.

Services inflation ex energy y/o/y

Core Goods prices y/o/y

BY Doug Kass · Jan 13, 2026, 11:00 AM EST

From Peter Boockvar:

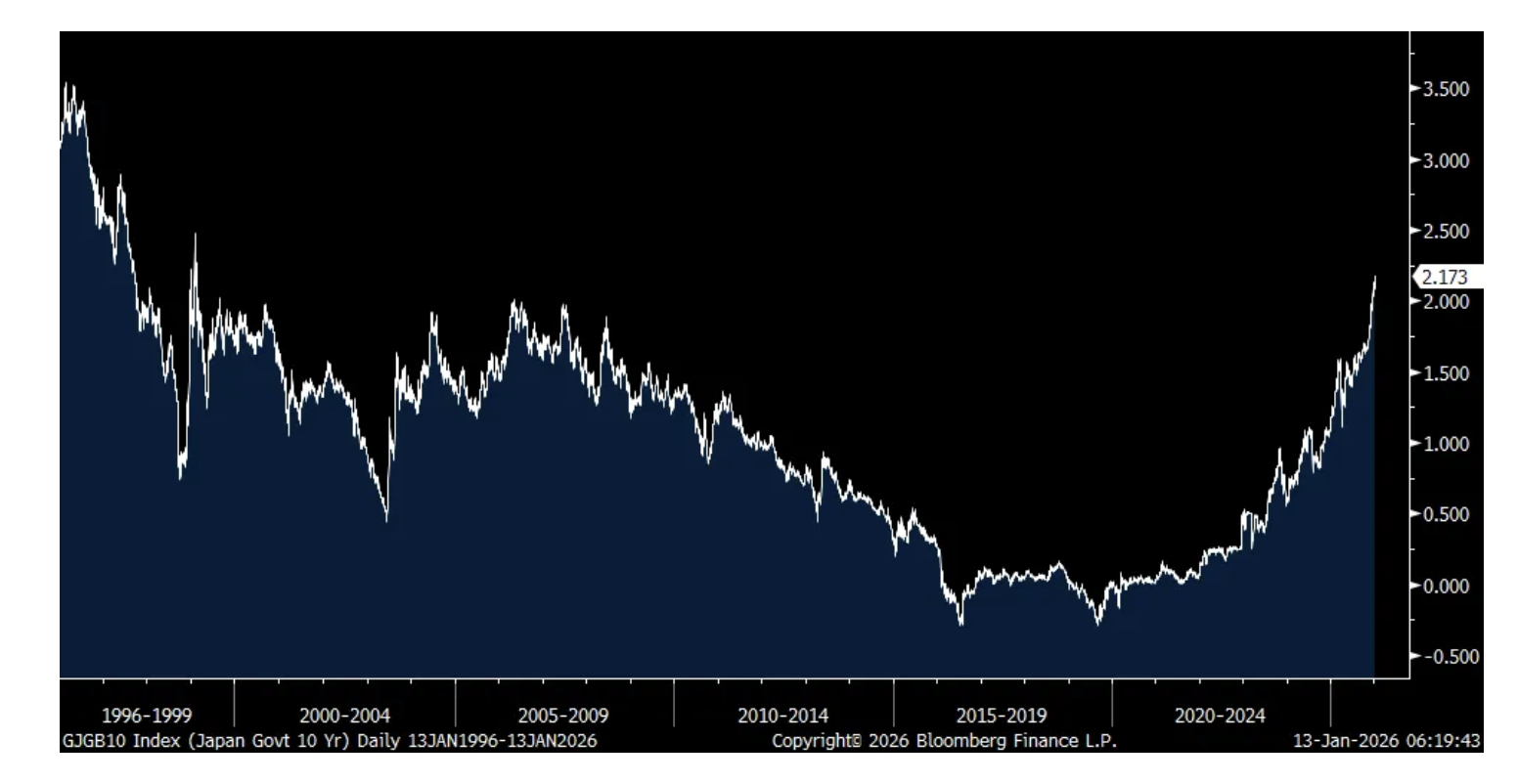

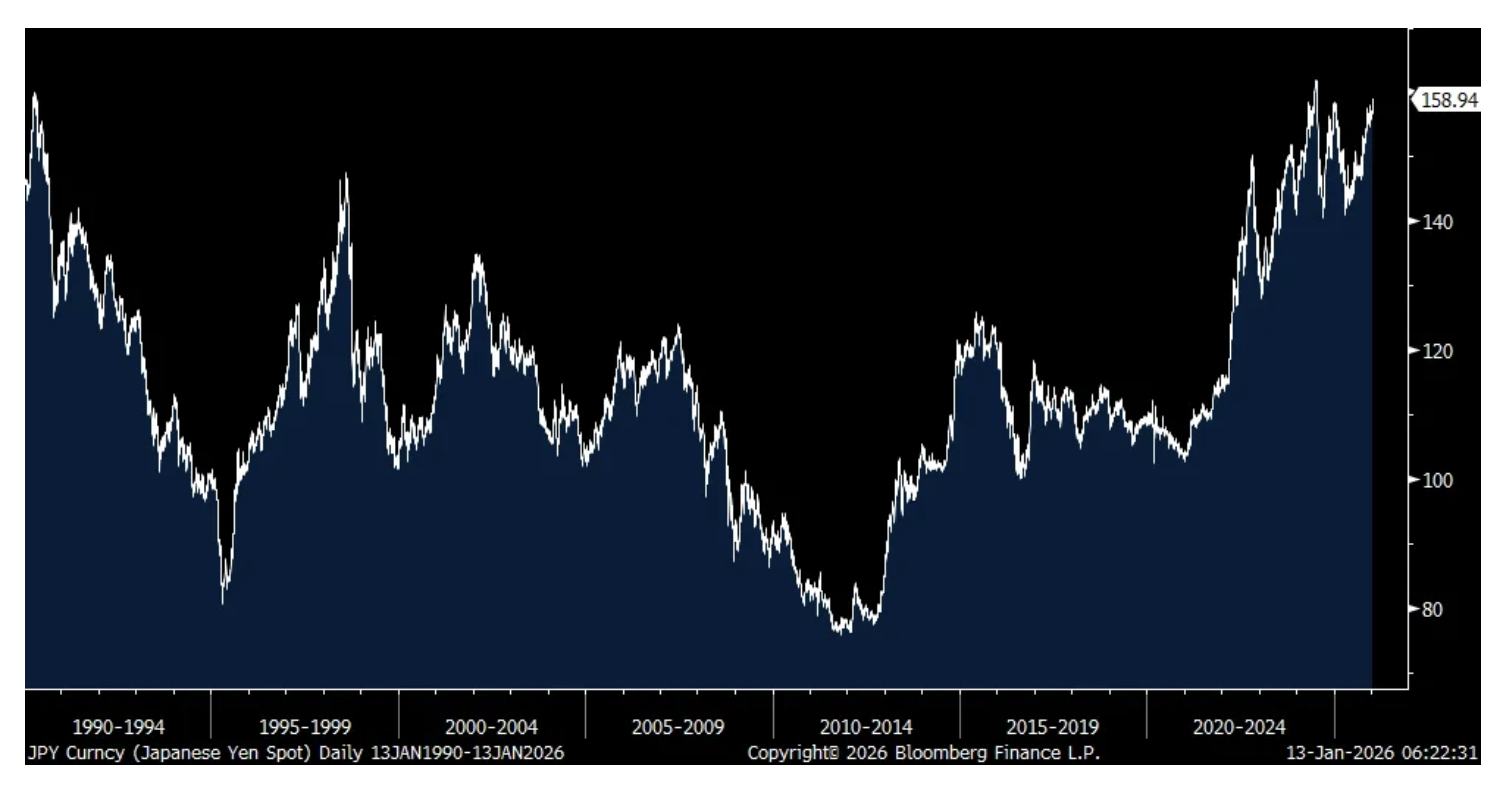

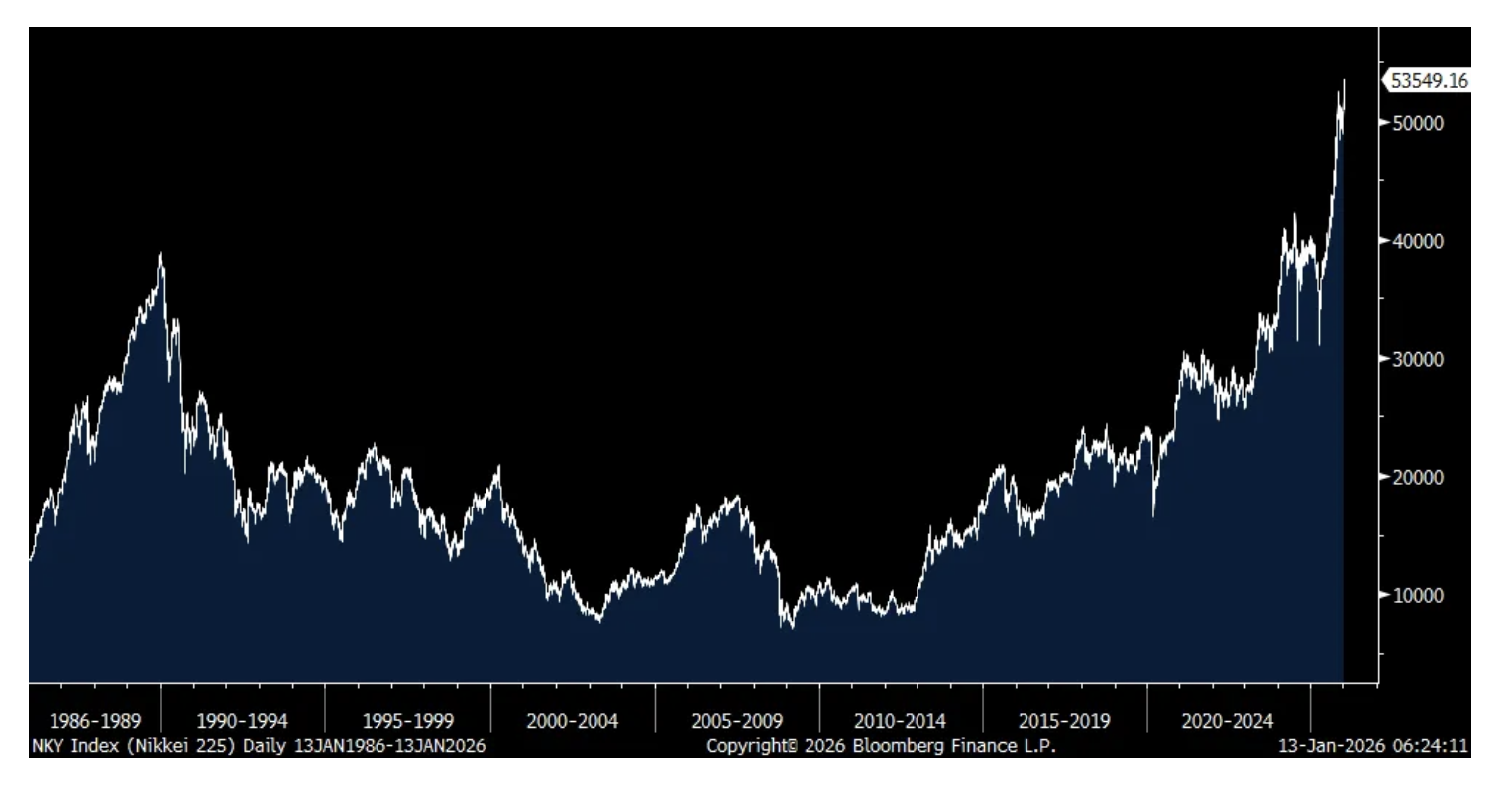

The Takaichi trade is on again. Buy Japanese stocks, sell JGB’s and sell the yen. Talk is that she will call a snap election in coming weeks in order to take advantage of her high approval rating so as to consolidate power within the LDP which has a weaker approval rating than her. The thought is, it will be successful and thus will give her freer reign to pass whatever fiscal initiatives she wants. The Nikkei rallied to another record high. The 10 yr JGB yield jumped 7.6 bps to 2.17%, a fresh 27 yr high. The 30 yr yield was up 9 bps and the 40 yr by 10 bps. These are big moves for the JGB market. The yen is down for the 10th day in the past 11, nearing the weakest level vs the US dollar since 1990 and it triggered a comment not just from the Japanese Finance Minister but thoughts from Scott Bessent as well.

Finance Minister Satsuki Katayama said she had “concerns about the one-way weakening of the yen” and that “Treasury Secretary Bessent shares those concerns.” Long duration sovereign bonds in Europe and the US are lower too with yields up. The US 10 yr yield in particular is back to testing the 4.20% level and the 30 yr 4.85%. Again, something I find to be a really important thing, this rise in long rates globally.

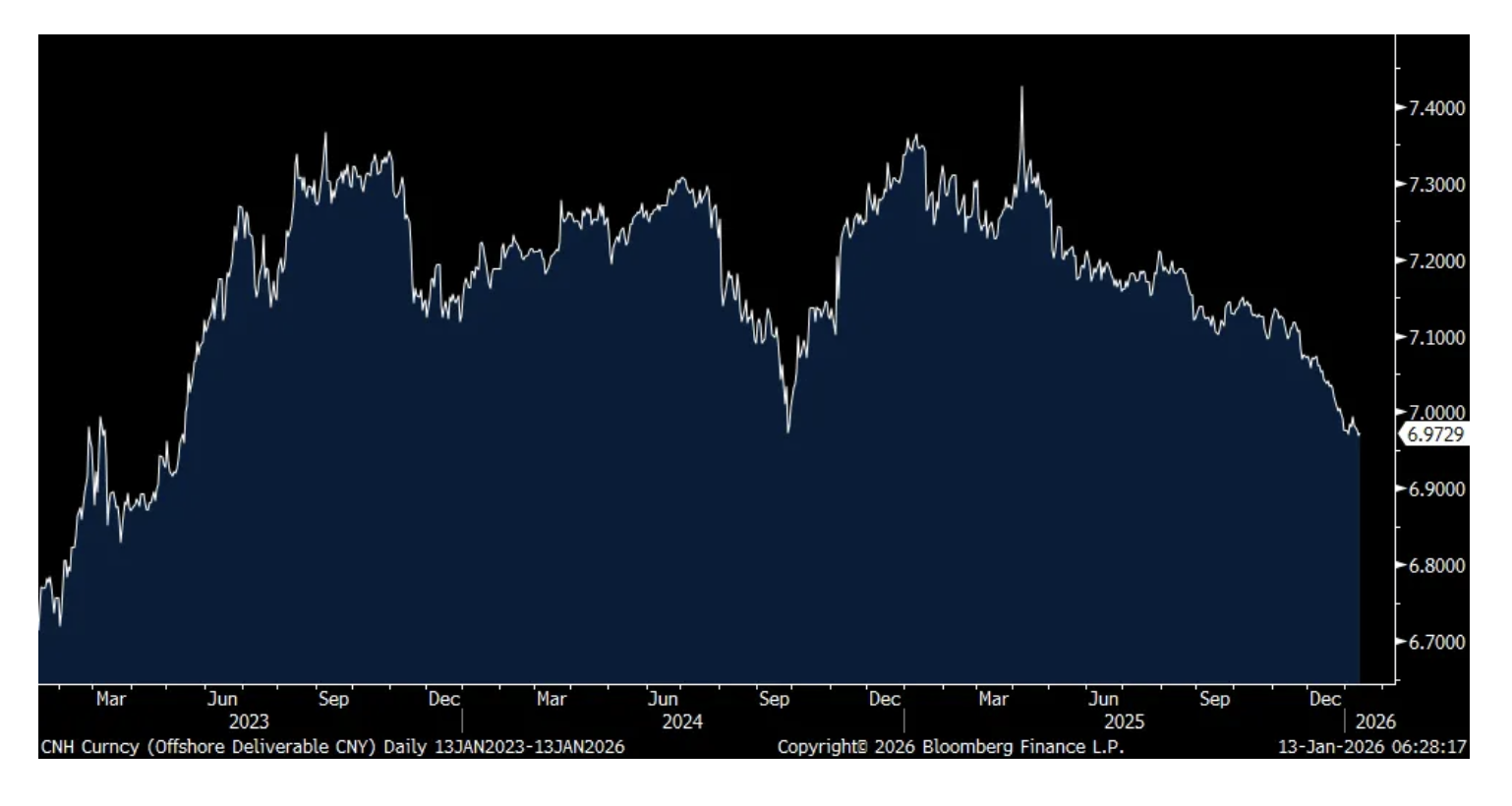

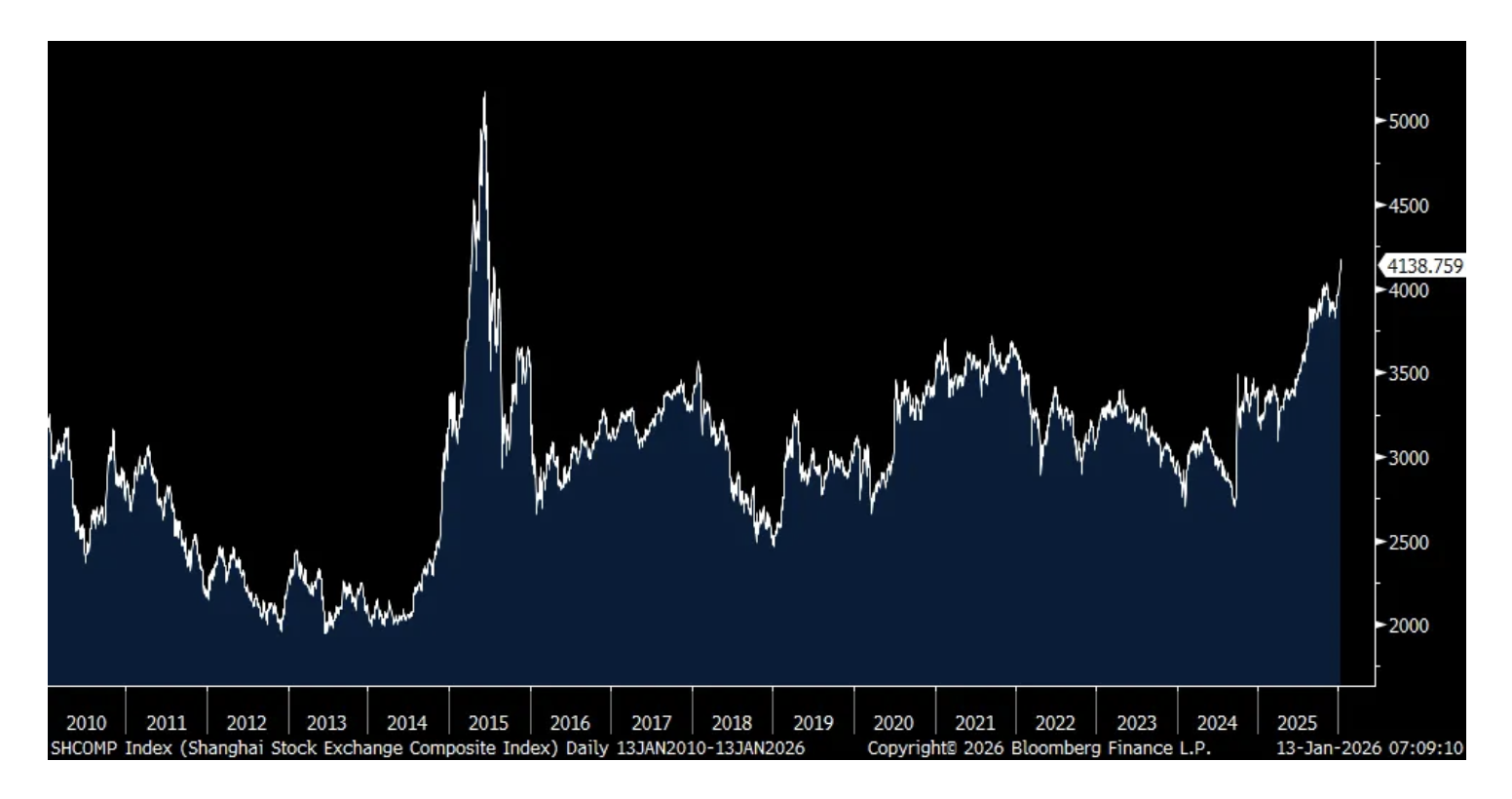

I also continue to think the rally in the Chinese yuan is notable as when it goes up for 13 days in 16 thru Monday (was flat overnight) that is a purposeful desire to have it rally on the part of Chinese officials. This is also an important sea change as it can mark the end of China exporting deflation via its manufacturing exports. Also, the yuan strength has coincided with strength in Chinese stocks where the Shanghai Comp on Monday closed at the highest level since July 2015 before slipping .5% overnight. We continue to own and like some stocks trading in Hong Kong and some in the US that do most of their business there, such as in Macau.

10 yr JGB yield

Yen

Nikkei

Offshore Yuan

Shanghai Comp

The December NFIB Small Business Optimism index rose .5 pt m/o/m to 99.5, which puts it in line with the 6 month average of 99.4. After rising by 4 pts in November, Plan to Hire slipped by 2 pts. Compensation jumped by 5 pts to 31% which matches the highest since last June and Comp plans held at 24% which is the best since late 2024.

After rising to 23% in October a few months after the BBB bill was passed, capital spending plans fell to 19% after a 3 pt drop in November. Plans to Increase Inventory held at -1%.

As for the outlook, it was mixed. Those that Expect a Better Economy rose 9 pts after falling by 5 pts last month. Those that Expect Higher Sales dropped by 5 pts but rose by 9 in the month before. Both are at their 6 month averages. Those that said it’s a Good Time to Expand was unchanged at 13%, also right at its 6 month average.

Higher Selling Prices jumped by 13 pts to 34% in November to the highest since March 2023 but fell back to 30% in December and compares with the 6 month average of 26% and the long term average of half that. Positive Earnings Trends rose 3 pts but at -20% is still around its 6 month average of -21%. The average rate paid on a loan was 8.4%, up 50 bps from November.

The NFIB said “2025 ended with a further increase in small business optimism. While Main Street business owners remain concerned about taxes, they anticipate favorable economic conditions in 2026 due to waning cost pressures, easing labor challenges, and an increase in capital investments.”

They mentioned taxes because that is now the single most important problem of small business as it jumped by 6 pts m/o/m. Quality Labor was number 2, down 2 pts m/o/m while inflation fell by 3 pts to 12. Taxes in particular are a state and local pain point.

Bottom line, nothing market moving here but watching the mood of small business is always important as a reflection of both economic activity but their ability to maneuver through which is always more difficult than bigger businesses that have greater resources and agility.

NFIB

Higher Selling Prices

Delta had mixed results, beating the bottom line but missing the top line. In their release they said “2026 is off to a strong start with top-line growth accelerating on consumer and corporate demand.” Also, “International performance improved significantly from the September quarter, with y/o/y unit revenue growth improving 5 points, driven by Transatlantic and Pacific.”

This was from Jamie Dimon on the macro after another good JP Morgan quarter, “The US economy has remained resilient. While labor markets have softened, conditions do not appear to be worsening. Meanwhile, consumers continue to spend, and businesses generally remain healthy. These conditions could persist for some time, particularly with ongoing fiscal stimulus, the benefits of deregulation and the Fed’s recent monetary policy. However, as usual, we remain vigilant, and markets seem to underappreciate the potential hazards - including from complex geopolitical conditions, the risk of sticky inflation and elevated asset prices.”

BY Doug Kass · Jan 13, 2026, 10:30 AM EST

With S&P cash -27 handles I am moving my Index shorts (thru calls) to small-sized.

BY Doug Kass · Jan 13, 2026, 10:27 AM EST

S&P cash is -6 handles.

Ludacris!

BY Doug Kass · Jan 13, 2026, 10:08 AM EST

I am back shorting (JOET) $43.31 and (GRNY) $25.79.

BY Doug Kass · Jan 13, 2026, 10:05 AM EST

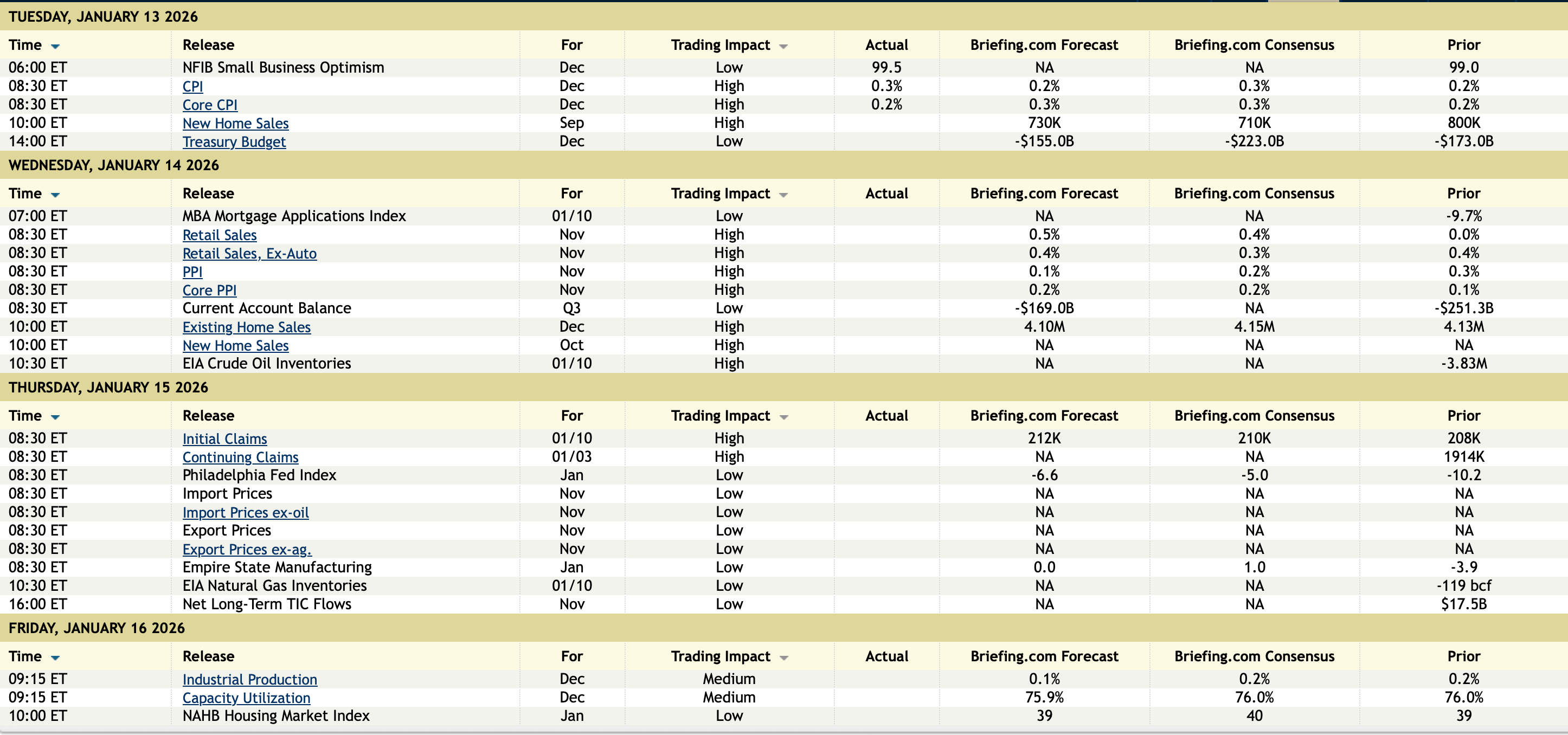

11 a.m.: Treasury Announces a 4 and 8 Week Bill Auction;

11 a.m.: Treasury buyback announcement (liq support);

11:30 a.m.: Treasury hosts a $75B 6-Week Note Auction;

1 p.m.: Treasury hosts a $22B30-Year Bond Auction;

Economic Calendar

BY Doug Kass · Jan 13, 2026, 9:35 AM EST

BY Doug Kass · Jan 13, 2026, 9:20 AM EST

-LHX Department of War (DoW) to invest $1B in planned independently traded Missile Solutions business to significantly increase capacity

-PAR Papa Johns partners with PAR Technology to power POS and OPS transformation

-SLDB FDA Orphan Drug Designation for SGT-212

-KELYA holder Trust K sells entire 3M Class B share stake to Hunt Equity

-RVTY prelim results

-FBIO FDA approval for Zycubo to treat Menkes disease

-ORA 20-year PPA

-OPCH prelim results

-ANIX earnings

-JPM earnings

-CAH raises outlook

-AMD upgrade

-INTC upgrade

-TMCI prelim results

-PDYN prelim results

-LASR prelim results

-THO Loop upgrade

-AMRX prelim results

-TVTX milestone updates

-CING shelf registration

-DAL earnings guidance

-SNPS Piper downgrade

-BK earnings

-NPCE prelim results; FY26 outlook

-ASTS downgrade

BY Doug Kass · Jan 13, 2026, 9:15 AM EST

With S&P futures +18 handles, I am going to make another Ludacris Forecast (that the S&P) moves into negative territory some time during the trading session.

Another Ludacris and, likely, silly forecast!

BY Doug Kass · Jan 13, 2026, 9:10 AM EST

With S&P futures rising by +18 handles after the cooler inflation print (I remain more concerned about cumulative or "stacked" inflation, than the current rate slight moderation in the rate of growth in innflation) I have moved to a large short call (SPY) position.

BY Doug Kass · Jan 13, 2026, 9:00 AM EST

BY Doug Kass · Jan 13, 2026, 8:50 AM EST

* As the herd-like chorus of "first-level thinking" is at near unanimous adoption...

Driving that train

High on cocaine

Casey Jones you better

Watch your speed

Trouble ahead

Trouble behind

And you know that notion

Just crossed my mind

- The Grateful Dead, Casey Jones

Here are the top-10 "group stink" comments that you will (no doubt!) hear in the business media today:

1. Guests and moderators will reduce their market forecasts to the "first level" of thinking — disregarding the complexity of the investment mosaic. It goes something like this... the S&P Index will likely rise by about +10% with S&P profits up low double digits with some modest declines expected in price-earnings ratios.

2. Banks have a noteworthy setup into earnings — with deregulation, an improvement in net interest income (as the yield curve steepens), robust merger and acquisition activity and low relative valuations.

3. The economy is growing in nominal terms at an above-average rate of growth. It is not:

4. The new Fed Chair will grease the economy by lowering interest rates (regardless of sticky inflation). Ergo, the domestic economy will be "running hot."

5. Every single contributor in the business media will be upbeat on the markets. The same guests seen yesterday, will be seen today... and tomorrow. (See #10 below)

6. Guests will universally say that "I can't identify any negatives." There will be no mention of the equity risk discount, a lowly S&P dividend yield of 1.11% (remember, historically 35% of market returns are dividends), the lack of any fiscal discipline (leading to ever higher deficits) and valuations (based on historical metrics) in the 98%-tile.

7. There will be no mention of an overvalued (and record-high) Shiller CAPE Index or how expensive the Buffett Indicator (market valuation relative to GDP) is. These indicators don't count anymore as we are in a new valuation paradigm.

8. There will be no mention of the risks associated with (leveraged) passive products and strategies and changes in market structure. (There are now more ETFs listed than individual stocks.)

9. The gamification of the market will be ignored and not addressed. (Well, I suppose it's normal for 70% of all options traded to have a 24-hour maturity!)

10. Dan Ives and Tom Lee will appear on CNBC in support of the equity market and AI investments. They will be unchallenged.

Cue Bob Weir and The Grateful Dead's "Casey Jones"... there might be some trouble ahead.

BY Doug Kass · Jan 13, 2026, 8:00 AM EST

BY Doug Kass · Jan 13, 2026, 7:30 AM EST

* Technicians are now unanimously bullish...

* I am aggressively expanding my short book

Bonus — Here are some great links:

Fed Independence Is Fading Away, Roll Into Metals

Markets Look Past DC Drama as Bank Earnings and Charts Take Center Stage

BY Doug Kass · Jan 13, 2026, 6:20 AM EST

BY Doug Kass · Jan 13, 2026, 6:05 AM EST

BY Doug Kass · Jan 13, 2026, 5:55 AM EST

The S&P Short Range Oscillator remains overbought at 2.96% vs. 2.62%.

BY Doug Kass · Jan 13, 2026, 5:45 AM EST