My Highest Short Exposure in Months

This afternoon I took my short exposure to the highest level in several months.

BY Doug Kass · Jan 12, 2026, 4:56 PM EST

This afternoon I took my short exposure to the highest level in several months.

BY Doug Kass · Jan 12, 2026, 4:56 PM EST

BY Doug Kass · Jan 12, 2026, 4:45 PM EST

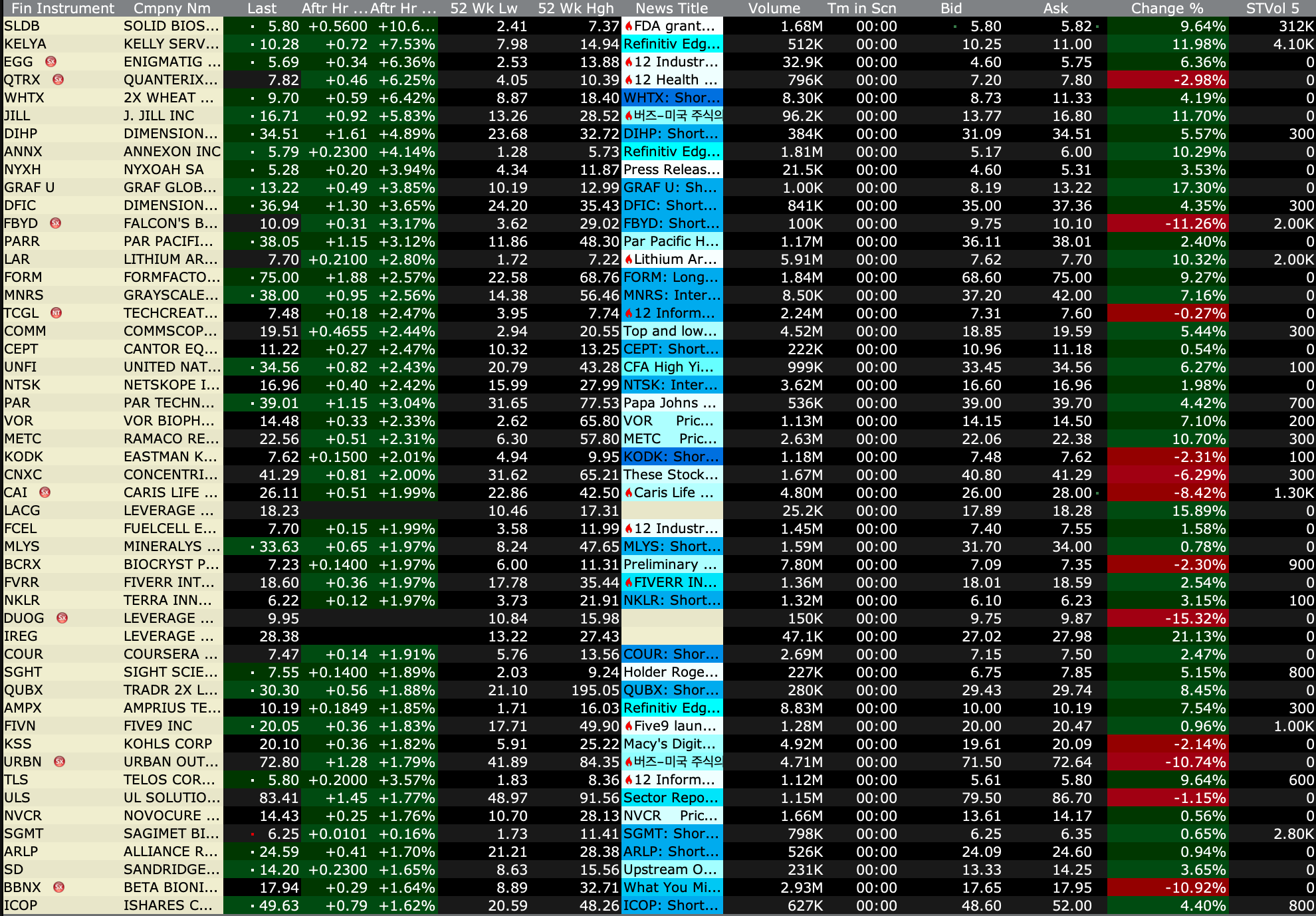

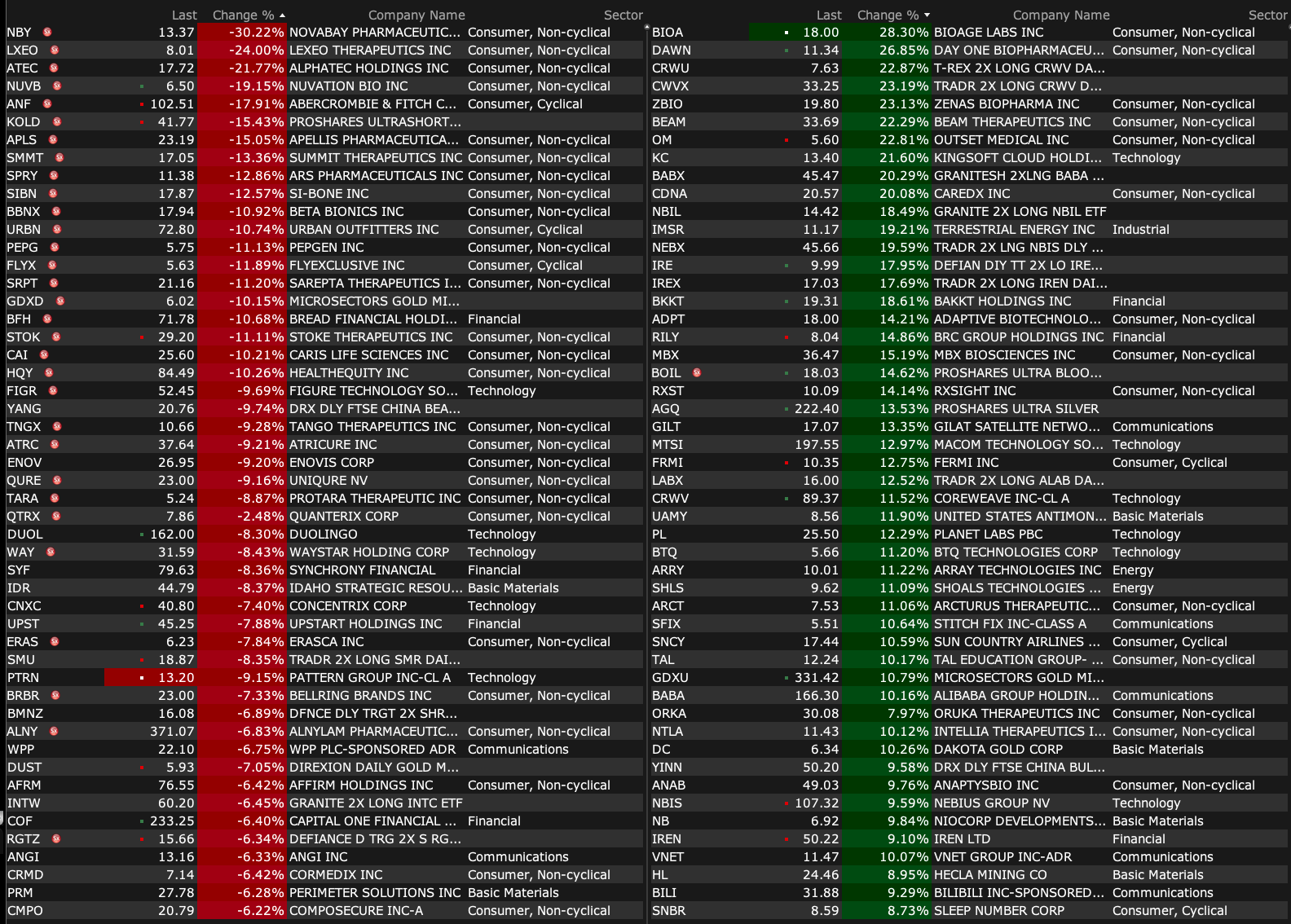

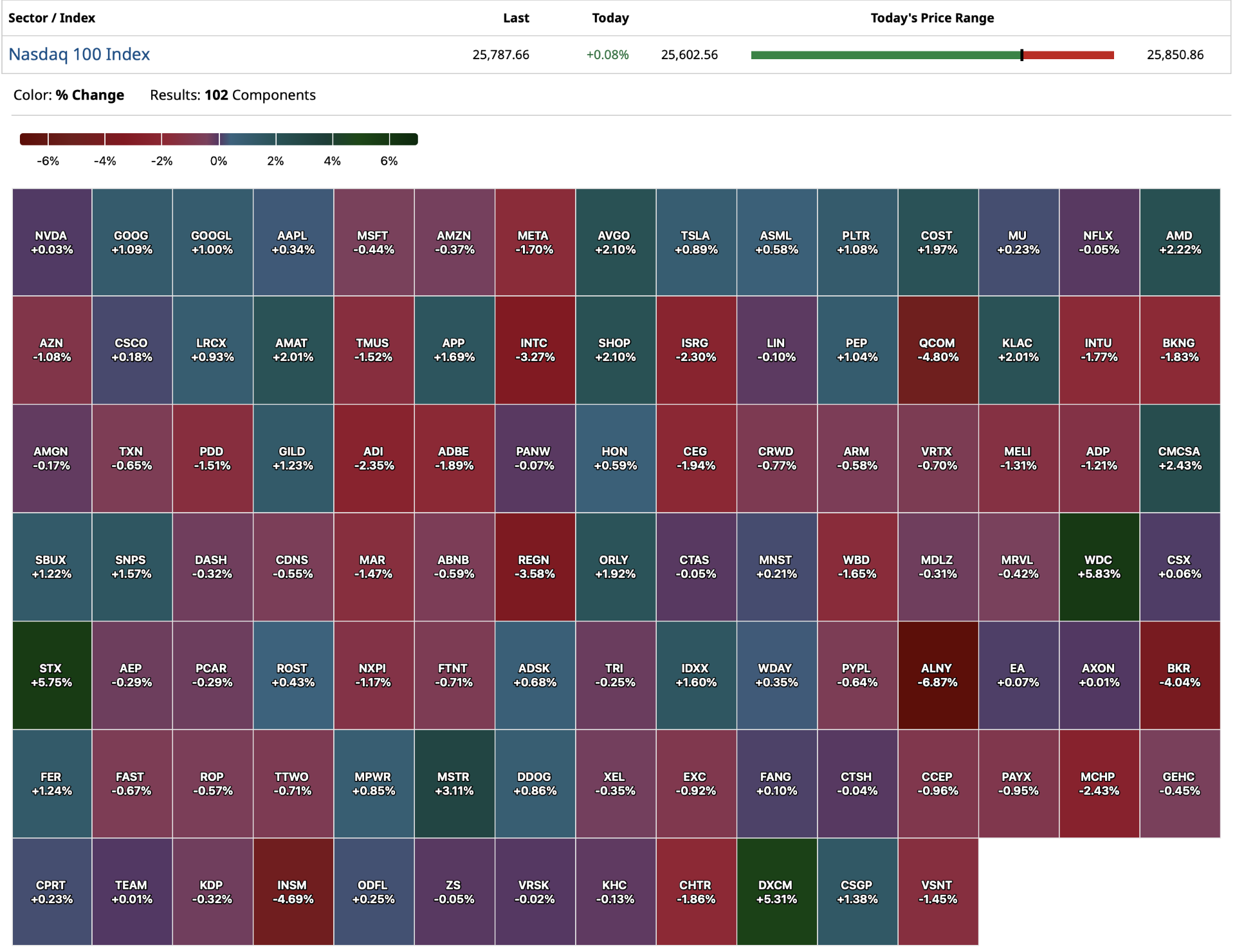

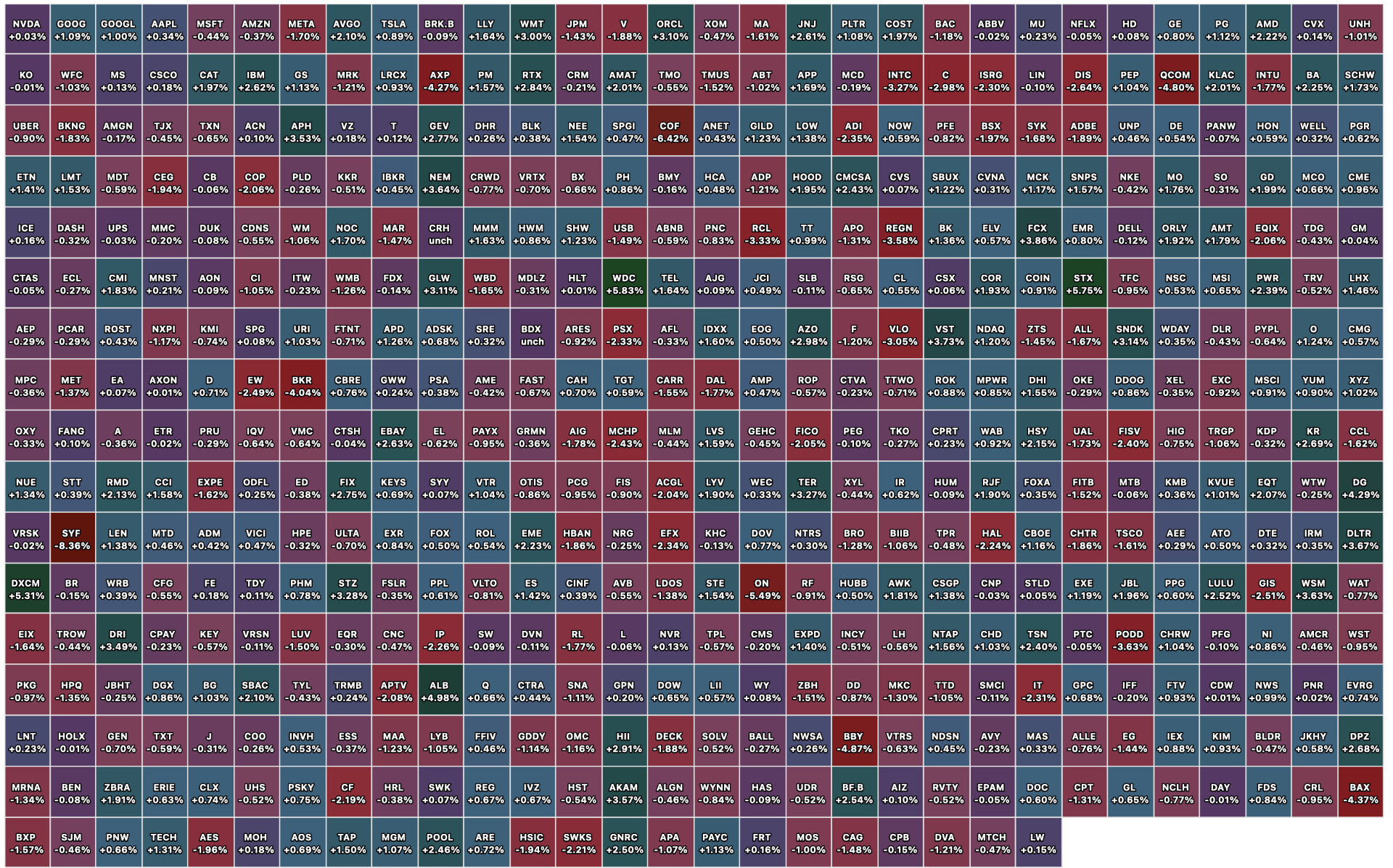

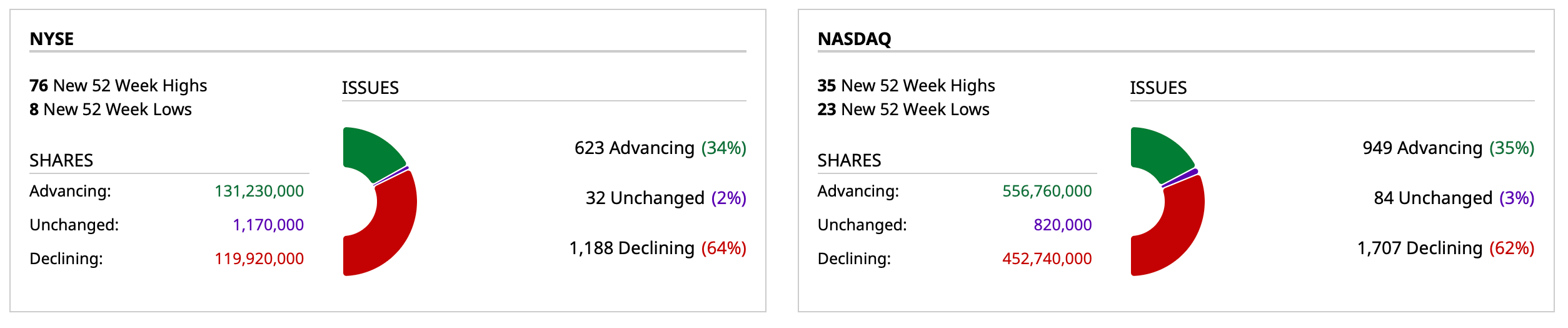

- NYSE volume 4% above its one-month average;

- NASDAQ volume 14% above its one-month average;

- VIX index: up 4.14% to 15.09

BY Doug Kass · Jan 12, 2026, 4:26 PM EST

I am leaving early for a medical appointment — as mentioned earlier today.

BY Doug Kass · Jan 12, 2026, 3:00 PM EST

glow1615

Not a political post, just putting on my MAGA/Trump whisperer hat:

It seems the market is catching the rhythm of Trump histrionics. Start with prognostications of an apocalypse in the overnight futures trading...followed by, calmer heads entering the arena and thanking the "Orange Man Bad" panic stricken for their morning's discounted purchases...climaxing in, the market yawns at yet another non-event, event.

There is no doubt that Trump is impatient and chaotic in his governing style. Is that really surprising? He is a businessman/effusive salesperson and loathes the bureaucratic process. He's about closing "deals". Of course we all know, " the devil is in the details". He has espoused support for issues that were previously the centerpiece of the Democrat's platform. Conservatives are puzzled as to how tariffs and scaring off cheap labor became the centerpiece of their platform. You would hope both parties could get behind rooting out "waste, fraud and abuse" , since both have claimed it as a goal , in the past. I thought we all agreed that the government having fewer employees was a "good thing". You know, more people pulling the cart than being in the cart. What i have found is "we'll see" is probably the most accurate and thoughtful market call to so many of Trump's policy declarations. Market pundits used to say, "the market hates uncertainty"....seems that trading proverb can be put to rest for the time being as well.

Good luck to all.

BY Doug Kass · Jan 12, 2026, 2:37 PM EST

From Peter Boockvar:

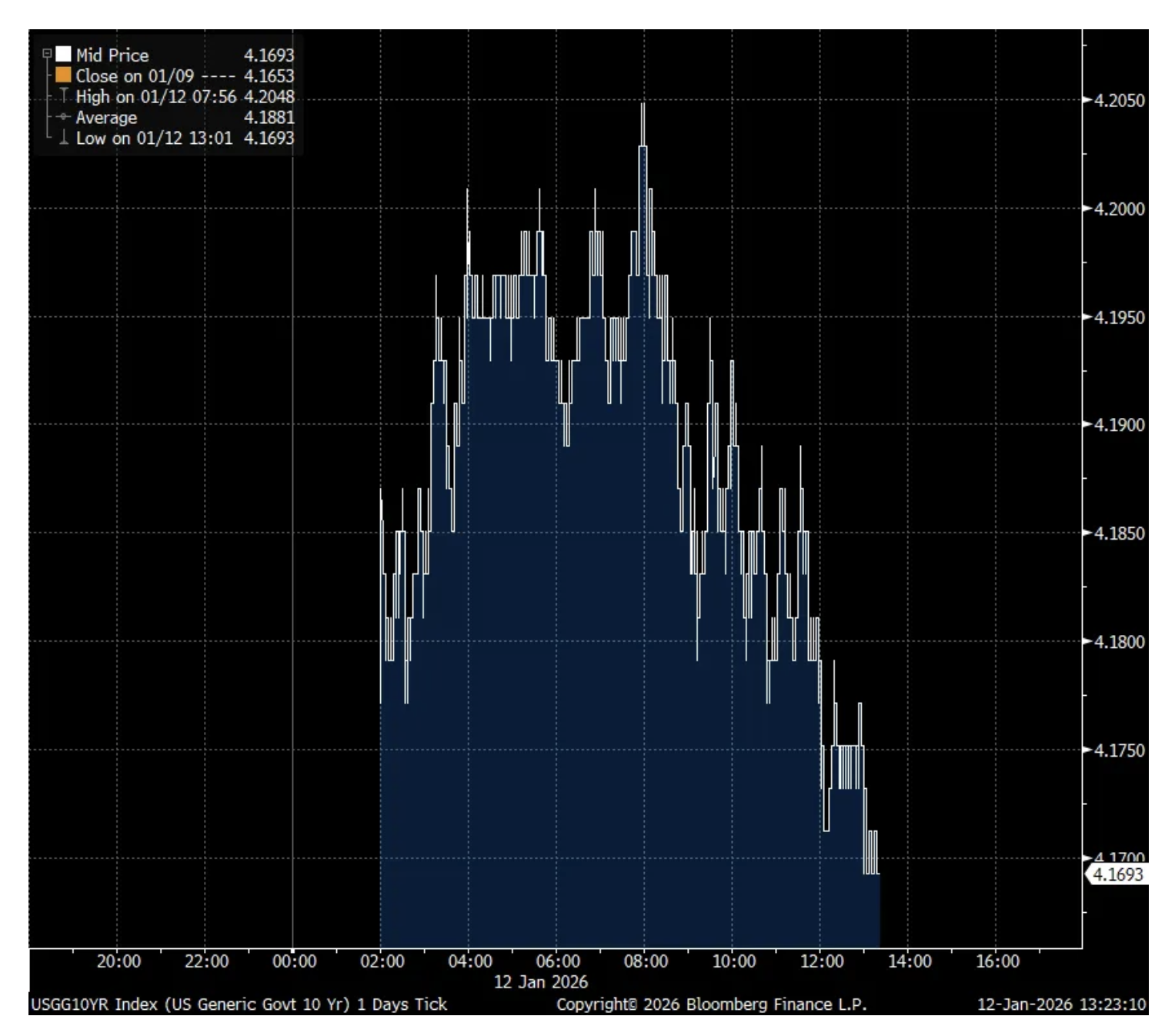

The heightened drama with the Federal Reserve and its current Chair did not impact the 10 yr note auction which was pretty good. The yield of 4.173% was below the when issued pricing of 4.18%. The bid to cover of 2.55 was about spot on with the previous 12 month average. Direct and indirect bidders took down about 94% of the auction, above the one year average of about 90%. After touching 4.20% this morning, the 10 yr yield has backed off to 4.17%.

Bottom line, who once said that “May you live in interesting times”? Because we certainty do.

Intraday 10 yr yield

BY Doug Kass · Jan 12, 2026, 1:50 PM EST

BY Doug Kass · Jan 12, 2026, 1:31 PM EST

BY Doug Kass · Jan 12, 2026, 1:00 PM EST

Homebuilder St. Joe Co. (JOE) breaks out to a high and staples continue to be well bid.

BY Doug Kass · Jan 12, 2026, 12:49 PM EST

Bernstein lowered the firm's price target on Zillow (Z) to $95 from $105 and keeps an Outperform rating on the shares. The firm says it remains constructive on the name despite the price target change.

I remain short Z.

BY Doug Kass · Jan 12, 2026, 12:15 PM EST

With S&P cash +6 handles I have moved close to large-sized short (SPY) calls.

I also added to (QQQ) short calls.

BY Doug Kass · Jan 12, 2026, 12:06 PM EST

Back in the office.

BY Doug Kass · Jan 12, 2026, 11:56 AM EST

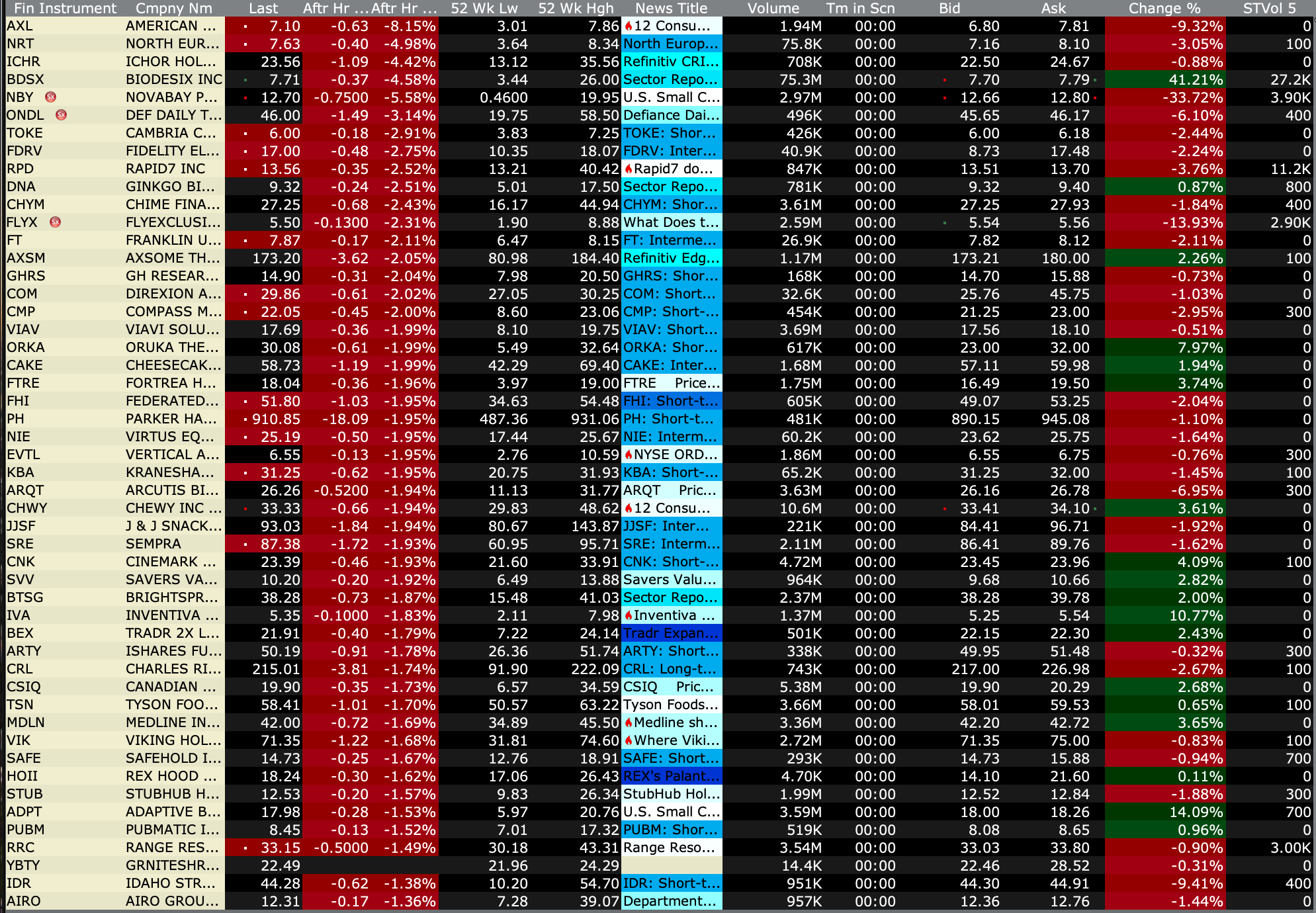

- NYSE volume 21% above its one-month average;

- Nasdaq volume 18% above its one-month average;

- VIX index: up 6% to 15.34

BY Doug Kass · Jan 12, 2026, 11:18 AM EST

From Peter Boockvar:

I’ll let the price of gold (up $96), silver (up $4.5), platinum (up $78), the value of the US dollar (DXY down .4%) and US Treasuries (10 yr yield up 3 bps) speak to the criminal targeting of Jay Powell, at least today.

It’s one of those unusual things, that feeling of sadness when someone passes that you’ve never personally met. But sometimes a virtual connection is made from a distance when something they do just resonates. The Grateful Dead/Dead & Company and things in between were that for me. I always loved these words written and sang by Bob Weir in Cassidy and seems so fitting now:

“Fare thee well now. Let your life proceed by its own design. Nothing to tell now. Let the words be yours, I’m done with mine.”

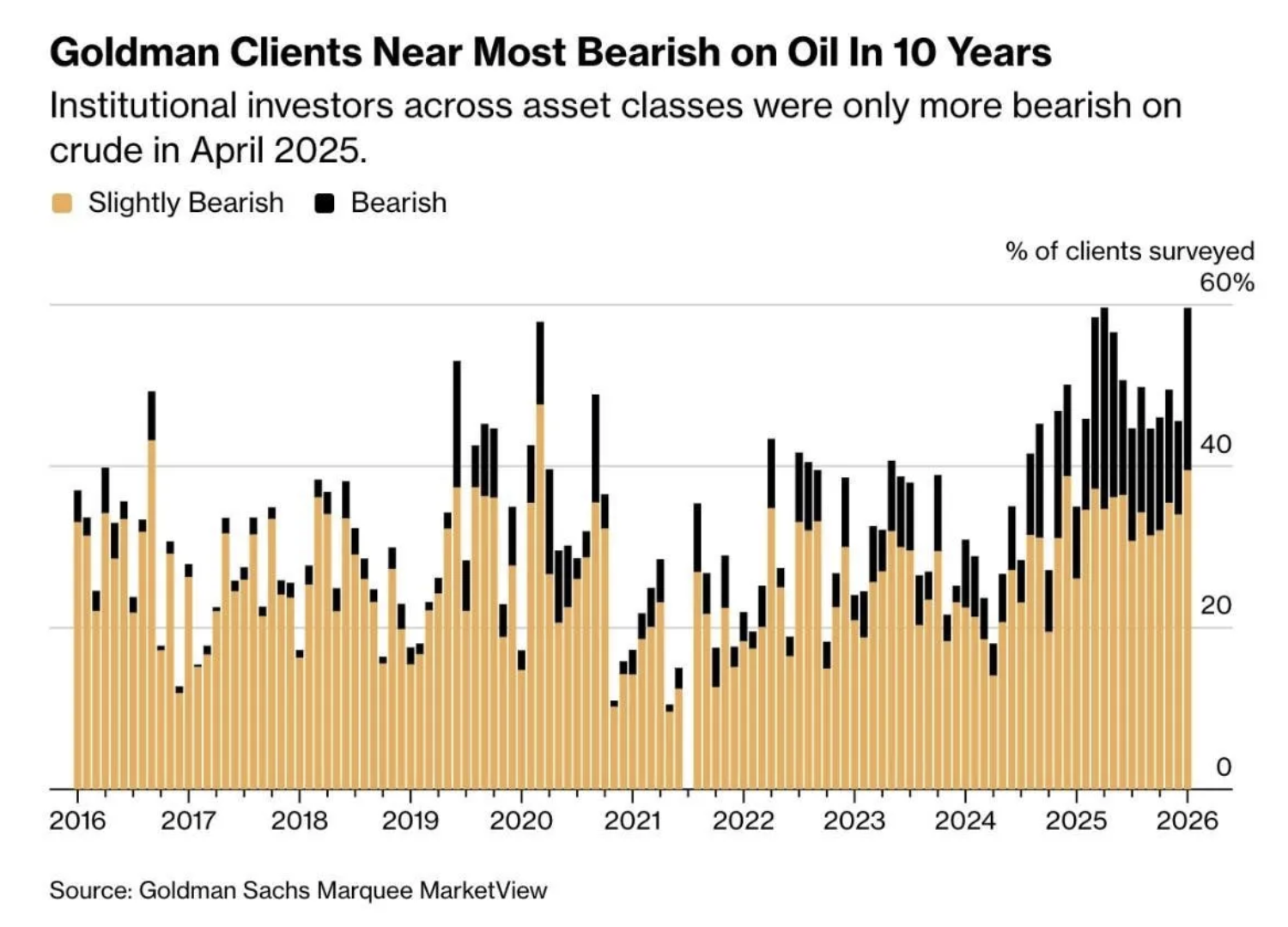

As a bull on oil and gas stocks, from a sentiment perspective I was encouraged from a contrarian standpoint to see this chart from Goldman Sachs a few days ago highlighting the high level of bearishness.

I’m going to add this to my list of bullish factors I incorporate into my analysis and here are the rest:

1)More on sentiment, the net speculative long positions in crude oil according to Friday’s CFTC data for the week ended last Tuesday is just off 15 year lows, an historically good contrarian take.

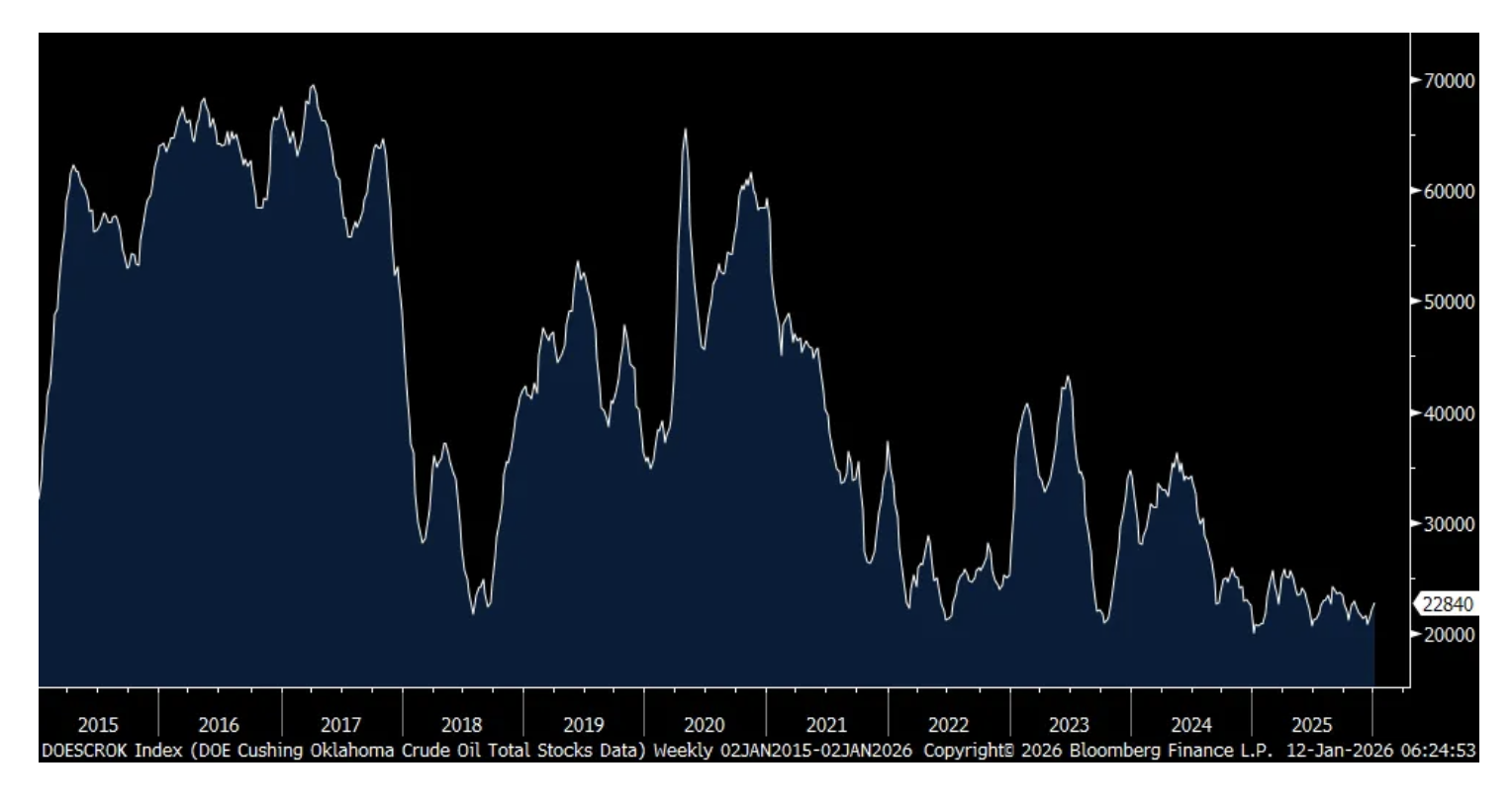

2)While there is all the talk about a glut of oil inventories, it seems to be mostly on the water. Inventories in Cushing are at 10 yr lows.

3)At least over the next year plus, the futures curve is flat as a pancake, not a sign of any short term gluts.

4)While there will be an increase in Venezuelan supply in the coming years, however slow it will take, however much it will cost, all to get back to where they were more than a decade ago, eventually, along with incoming supplies from Guyana and Brazil, there seems to be little talk about the plateau in US shale oil production. US shale accounted for about 85% of non-OPEC+ oil supply over the past 15 years and this production, at least geologically for now, is in the process of rolling over. My friend Tracy Shuchart in a piece over the weekend said “The Permian Basin, which carries the entire US production story, requires 400,000 barrels per day of new production additions annually just to offset base declines from existing wells. You’re not growing production in this environment. You’re running in place, and increasingly you’re falling behind.”

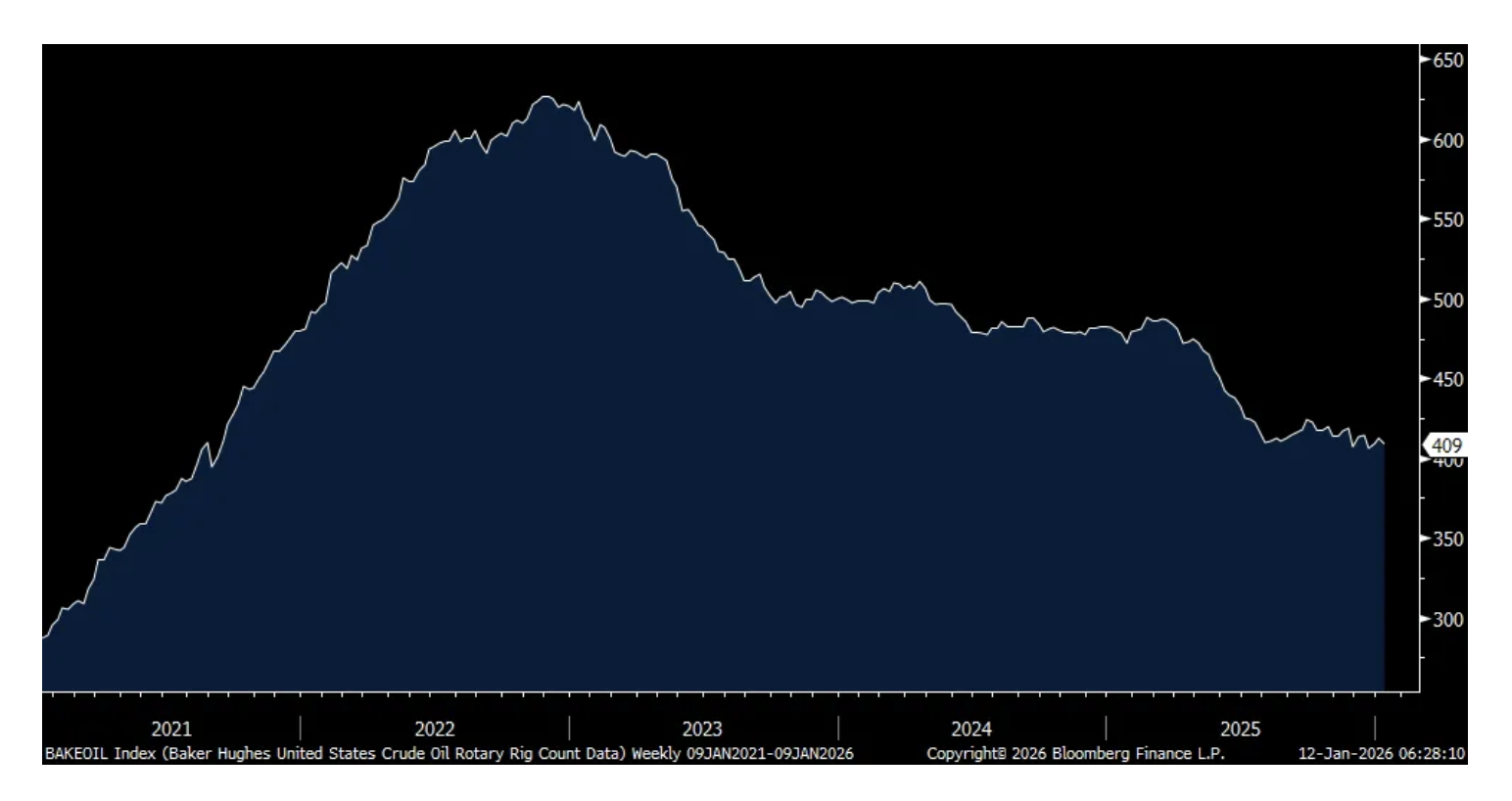

5)The US oil rig count is at a 4 ½ yr low. More than half of US shale basins lose money around $50 a barrel.

6)A lot of talk about reduced China demand for oil due to the ever growing EV presence, which is true, but did you know that of the 1.4 billion people in China that only about 400,000 have been on a plane? Demand for jet fuel and other petro products, especially for petrochemicals, will continue for years. And, the demand from India, the Middle East, Africa and other emerging areas will only continue higher keeping oil demand steady at 1-1.5mm barrels per day, easily absorbing new Venezuelan oil supply in coming years.

7)Even the IEA is now admitting that oil demand won’t peak until at least 2050 up from tomorrow, I say sarcastically because they’ve been mostly wrong in their belief that the world was on the cusp of using less fossil fuels.

8)EV’s are losing the VHS/Betamax battle with hybrids and ICE vehicles, thus pushing further out the demand for fossil fuels.

9)I don’t think Saudi Arabia wants oil prices any lower and that’s reflected in OPEC+’s desire to hold quota’s unchanged in Q1. And the quota increases seen so far over the past year have not been matched by coincident increases in oil production, evidence that there isn’t much spare capacity left, seemingly just in Saudi Arabia and the UAE.

10)Free Iran, a big question with what comes next of course.

Net Spec Long Position in Crude Oil Futures

Cushing, Oklahoma Crude Oil Inventories

US Crude Oil Rig Count

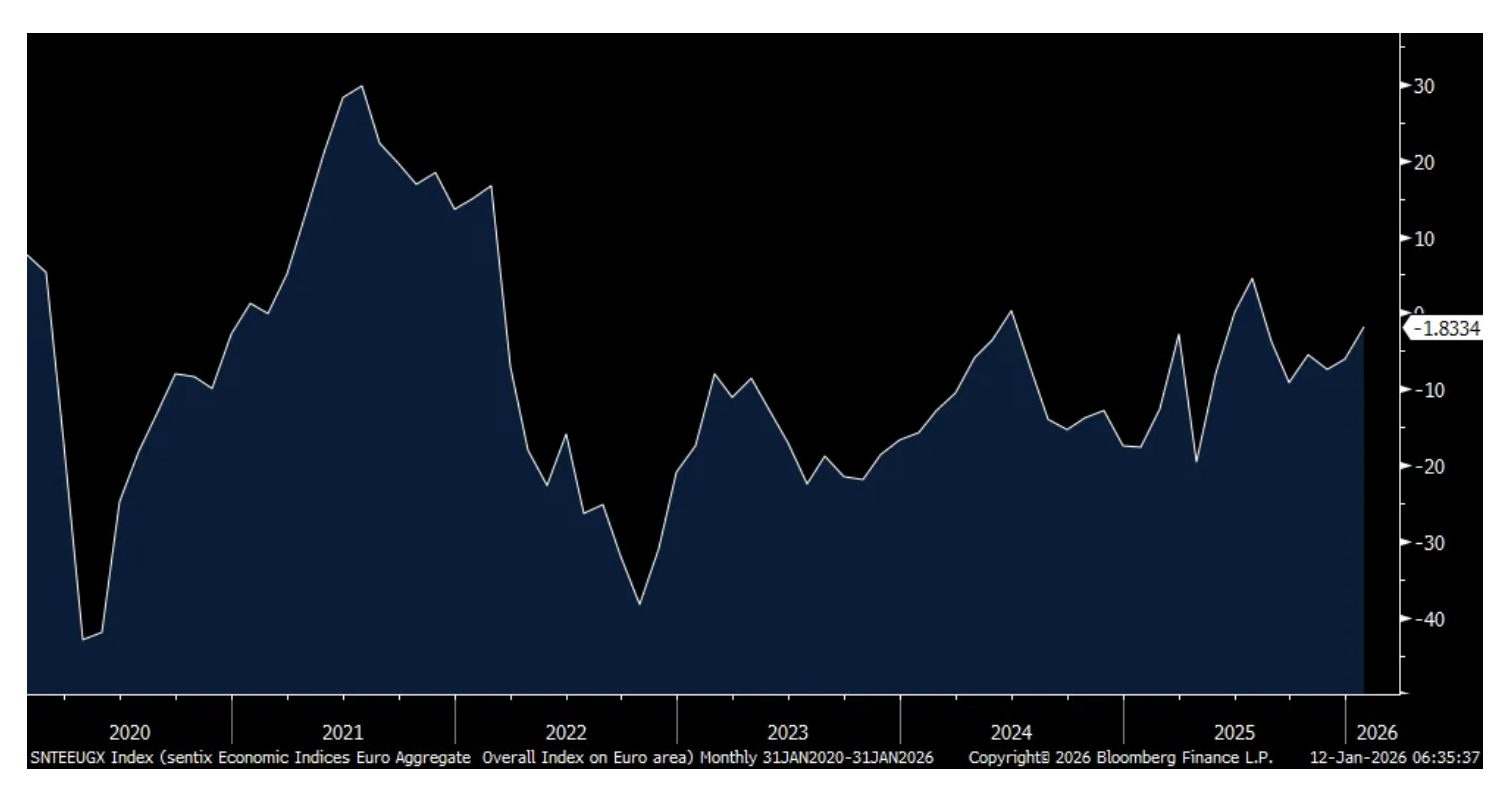

Not much going on overseas data wise. The European Sentix Investor Confidence index improved to -1.8 from -6.2 and better than the estimate of -5. Sentix said “Investors are starting the new year 2026 with slightly more confidence. The Sentix Economic Index for the Eurozone improved by 4.4 points to -1.8 points. This is the highest level since July 2025. In Germany, there is a small silver lining on the horizon at the start of the year. The overall index climbs by 6.3 points to -16.4 points, with the expectations component in particular sending a positive signal with an increase of 6.8 points.” Nothing market moving but the world can certainly use quicker economic growth in Europe, particularly from its biggest contributors, Germany and France.

Sentix

BY Doug Kass · Jan 12, 2026, 10:10 AM EST

With S&P cash only -6 handles I am back adding to my SPY short calls.

BY Doug Kass · Jan 12, 2026, 10:02 AM EST

Sold my (QQQ) long at $625.55

BY Doug Kass · Jan 12, 2026, 9:53 AM EST

With S&P cash -17 handles (rallying smartly from the morning low's) I have sold out my (SPY) common at $692.58.

Meeting bound!

BY Doug Kass · Jan 12, 2026, 9:52 AM EST

"To expect the unexpected shows a thoroughly modern intellect."

-Oscar Wilde

This is why I have done my Surprises List for the last 28 years:

JAN 5, 2026 10:11 AM EST

* This is my 24th year of Surprise Lists

* My Surprise List reverts back to only 10 Surprises in 2026 from 15 Surprises in 2025

* Though precious metals and equities rise early in the year, "there is no place to run, no place to hide" for most of the year

* The President resigns, the U.S. economy moves toward recession and today's leveraged market structure (passive management dominance that "worships at the altar of price") contribute to, and then accelerate, the collapse in most asset classes

- Martha Reeves The Vandellas "Nowhere To Run"

"Concentrate on finding a big idea that will make an impact on the people you want to influence. The Ten Surprises, which I started doing in 1986, has been a defining product. People all over the world are aware of it and identify me with it. What they seem to like about it is that I put myself at risk by going on record with these events which I believe are probable and hold myself accountable at year-end. If you want to be successful and live a long, stimulating life, keep yourself at risk intellectually all the time."

-- Byron Wien

The creator of the annual Surprise List, Byron Wien, remains in my thoughts after his passing several years ago.

Two years ago, in preparation for the assembly of that year's Surprise List of my predictions for the year ahead, I paid homage to my dear pal.

Byron Wien, Wall Street Seer of the Unexpected, Dies at 90 - The New York Times

Here was my tribute to Byron on TheStreet Pro. May his memory be a blessing.

Without further ado, here are my 10 Surprises for 2026:

I won't bury the lede.

Pres. Trump, like The Godfather's Michael Corleone, becomes a wartime President — initially with no opposition in his Cabinet or in Congress (and without a wartime consigliere like Tom Hagen to smooth things over!)

”Goddamn it, if I had a wartime consigliere... a Sicilian...“ |The Godfather

After attacking Venezuela and failing to learn the expensive lessons of regime change attempts with Iraq and Afghanistan, Pres. Trump sees his popularity plummet. Like Corleone, Trump grows more unhinged and the Administration's rhetoric against Mexico's President (Claudia Sheinbaum Pardo) becomes more heated. Pres. Trump gives the Mexican President an ultimatum as an attack on that country is openly discussed on Truth Social. Other regimes, like that of Cuba's Miguel Diaz-Canel's (whose security forces are behind the protection of Venezuela's President Maduro), are also highlighted by the Administration as possible targets early in the year. With the cover of U.S. aggression, Russia becomes more aggressive against Ukraine (there is no peace) and China invades Taiwan in late Summer.

Separate from geopolitics the Epstein files uncover a deeper (and unsavory) relationship with Pres. Trump.

A week long investigative report entitled "Trump First (Not America First") by The Washington Post discloses how much the Trump family has profited from his Presidency. President Trump's base is fractured — his popularity moves to unprecedented and low depths as the Marjorie Taylor Greene-led America First movement permeates both political parties.

Several high-level Trump Administration resignations are announced in the first half of 2026. A number of senior Republican Senators and Congressman distance themselves from the President.

By mid-year impeachment is openly discussed. Surprisingly, four women — Marjorie Taylor Greene, Elise Stefanik, Alexandria Ocasio-Cortez and Elissa Slotnick — emerge as the leaders of their respective political parties. Georgia's Congresswoman Marjorie Taylor Greene doesn't disappear — just the opposite occurs. Greene becomes the titular leader of the "America First" movement of the Republican Party, which is at odds with MAGA:

The "America First" movement gains ever more prominence and popularity within the Republican Party. Marjorie Taylor Greene overtakes Vice President JD Vance in the polls as the likely next Republican Presidential Nominee. New York Congresswoman Alexandria Ocasio-Cortez takes a large lead in the polls to be the next Democratic Presidential Nominee. Michigan Sen. Elissa Slotnick becomes the leading moderate in the Democratic party.

New York Congresswoman Elise Stefanik (who, after stepping down from Congress, breaks with Pres. Trump and announces that she plans to run for Sen. Schumer's NY Senate Seat), becomes another important leader in the "America First" faction of the Republican Party, joining the growing ranks of her party who finally split ranks with Pres. Trump.

Another woman is in the limelight — as First Lady Melania Trump begins divorce proceedings against Pres. Trump. (This was a surprise last year that was wrong....) The divorce settlement is nearly $1 billion, calling further attention to how Trump has profited from his presidency. Pres. Trump unexpectedly resigns under the intense political, social (Epstein) and mainstream media pressure citing his deteriorating health as the reason.

Despite all of the Administration's woes (and that of the domestic economy), the Democratic Party fails to offer a coherent alternative message as the Party remains hostage to the Left. (New York City Mayor Zohran Mamdani, Senator Bernie Sanders and Congresswoman Alexandria Ocasio-Cortez denounce the apprehension of Venezuela President Maduro.)

In a surprise (considering all of the above factors adversely impacting Republicans), the Democratic Party (barely) wins a narrow majority in the House. The U.S. economy weakens as the year proceeds. By year's end unemployment rises above 5% and the consumer price index is back near 4%.

The 2026 deficit approaches a staggering $2.5 trillion (and U.S. debt exceeds $40.5 trillion).

A recession in 2027 appears likely.

Equities (led by the Magnificent Seven tech stocks) succumb to slowing economic and corporate profit growth, the reappearance of inflation, questionable foreign and domestic policy, growing political uncertainties, emerging "problems" for the hyperscalers (as AI capital spending plans are reduced) and elevated valuations.

The K-shaped economy's weakness in the lower income cohort spreads into the middle and upper middle class as the cumulative (or stacked) inflation since Covid finally has an impact — causing a spending freeze. With the outlook for global economic growth dissipating, consumer and business sentiment plummets. BNPL and credit defaults rise and auto repossessions increase dramatically.

Drawdowns in the global equity markets and a moribund housing market contribute to a negative "wealth effect" and an air pocket with the high end consumer as the investor optimism of 2023-25 is abandoned.

There is no place to run, no place to hide — most asset classes fall in the 2026 Bear Market.

Precious metals, commodities and crypto currencies all collapse (after a strong start early in the year) — in Martha Reeves' Revenge.

Bottom line: After starting the year positively, the S&P Index drops by more than 20% in 2026 — with three separate drops of -10%.

Kevin Warsh follows through with Pres. Trump’s view that the U.S. should have the lowest interest rates and cuts the Fed Funds rate to 2% by the end of 2026. At the same time he transfers the Fed’s mortgage holdings to government-sponsored enterprises and the Fed’s coupon holdings to the Treasury in exchange for short-term bills. He works relentlessly to shorten the duration of the Fed’s balance sheet and expresses a goal for 2027 to shrink it. The bond market cheers the more responsible balance sheet management and the 10-year bond rallies to 3.5% but Treasury supply/deficits keep the term premium elevated and the reappearance of inflation risk limits how far the long end can fall and the yield on the long bond remains stubbornly high.

Despite lower short interest rates, housing continues to suffer. After several years of rising prices, home prices are too high to attract adequate demand. Construction volumes suffer and homebuilders are caught with commitment to take delivery of lots from off balance sheet partners that they can’t fulfill. A housing prices war follows and the average new home prices falls 7%. Homebuilder stocks are down by greater than 25%. The resale market remains in the doldrums and volumes fall by 10%. Homebuilders such as Home Depot HD and Lowe's LOW, real estate brokers and furniture companies all collapse under the weight of lower home prices and slowing sales activity.

The AI bubble bursts as the circular financing deals unwind (or are pushed out) — AI capital spending slows abruptly as return on investment concerns emerge as power generation and grid modernization are bottlenecks. Depreciation charges and lower demand wrecks havoc with consensus AI 2026-27 earnings per share expectations. Another big AI surprise would be if China decides to flood markets with inexpensive AI models — pressuring the ultimate and expected robust ROI forecasts (which are already in question by some skeptics).

OpenAI's Sam Altman finds a place to live right next door to Sam Bankman-Fried. His effort to make OpenAI too big to fail, fails. ChatGPT turns out to at best be a commodity large language model purveyor. It becomes obvious to all that its recent $500 billion-plus valuation can’t be supported. Without an ability to do a down round without losing face, OpenAI loses all access to capital. Ultimately, a consortium of its customers and suppliers takes it over to modify its business plan and reduce the cash burn.

With Altman tossed to the curb (or worse), the prosecutions begin.

OpenAI’s problems pushes a deeply committed (to OpenAI) Softbank to the verge of collapse.

Nvidia shares fall by -40% as CoreWeave (CRWV) is driven into bankruptcy.

A basket of defensive consumer nondurable equities ( (PEP) , (KO) , (PG) and (KMB) ) materially outperform the Mag 7 by a decisive amount.

The shares of (boring and previously hapless) PepsiCo outperform most other staples and 90% of the S&P Index after a much better skein of organic unit growth and as its core business is rationalized.

With so many positioned on the same side of the (bullish) boat, retail investors begin to liquidate from equity funds — reversing the experience of the last few years. The movie of the last decade (of inflows) goes into reverse in 2026 — it's October 1987 (portfolio insurance was to blame) all over again. More than one quarter of the listed ETFs close during the year due to "indifference."

Yes, they “owe it to themselves,” but they also have paid themselves very little interest. With inflation a continuing problem the deficit situation comes to a head. Japanese 10-year rates cross 3% and the yen falls to 200. Facing the possibility of spiraling inflation and a collapsing currency, Japan organizes a global central bank intervention to stabilize the yen. The situation remains precarious at year end setting up for a possible crisis in 2027.

Valuation opacity, a compression in exit multiples and unrealistic net asset value marks (mark to model delays volatility but doesn't remove it) in private equity come into focus in 2026. The greatest problems are companies tied to commercial real estate and Saas companies. There are a number of high-profile bankruptcies in notable private equity portfolios.

A market for stranded LP interests trading at deep discounts becomes widely followed. Further, the IPO market continues to not be a viable exit for most holdings. Gated redemptions become common place. Apollo (APO) , TPG (TPG) , KKR (KKR) and Ares (ARES) each fall by 30%.

After reviewing a possible initial public offering with bankers, the government determines the current corporate structures can’t be reconciled with an IPO and without risking enormous litigation from legacy investors. So, the administration simply nationalizes them – thereby moving the litigation risk away from the enterprises.

Bill Ackman commences litigation that will keep him busy until 2035. The IPOs are ultimately successful and the biggest issuances of all time.

In the rapidly eroding 2026 equity market landscape, Warren Buffett's cash hoard at Berkshire Hathaway (BRK.A) (BRK.B) becomes a valuable gift to Greg Abel. Greg Abel announces that Berkshire Hathaway will begin to whittle down its investment portfolio as the future direction of the company is to purchase full ownership in companies (and not in making minority equity investments).

By the end of 2026, Berkshire Hathaway eliminates its entire holdings in Apple (AAPL) and Bank of America (BAC) . Berkshire Hathaway's shares disappointing recent performance (following Warren Buffett's "retirement") is reversed. The share price rises modestly in 2026 as the major indices drop significantly.

Half of the male population between 18 and 50 have a sports betting account. Nearly one quarter of the sports bettors say they are addicted. And one in five persons with a gambling addiction attempt suicide. Wagering on the next Federal Reserve Chairman, Pres. Trump's next tweet, whether the next pitch is a strike or a ball (or how many home runs NY Yankee Aaron Judge will hit, who will score the first Super Bowl point, etc.), invites corruption into every aspect of American life.

More professional teams and college teams are embroiled in "fixes." The shares of Robinhood (HOOD) , Caesars (CZR) , Flutter (FLUT) , MGM Resorts (MGM) , Draft Kings (DKNG) and other companies involved in gambling and predictive markets fall in half — as regulatory authorities begin to place new restrictions on the space.

A deteriorating equity market results in massive retail trading losses — from leveraged ETFs, zero-days to expiration options, etc. Calls for regulatory action (on leveraged ETFs and zero dated options) grow louder as YOLO and HODL become OHNO.

Many (including myself) have predicted that Pres. Trump’s second-term would be filled with unexpected, extreme and controversial policies that go much further than anything in his first term. Based on the last six months no one has been disappointed!

In early 2026, in a move that stuns even his own party, Pres. Trump in an attempt to stabilize his dwindling poll numbers, a weakening U.S. economy and a sharp drop in stock prices, "rewards" (his words) the country's economy in the hopes of furthering his bull market narrative — by abolishing short-selling in all individual U.S. equities (futures are still allowed to be shorted).

The president markets his Executive Order by stating "that you either own a stock or you don’t," prompting a very short-lived and violent rally in global markets. However, very soon after the announcement, his plan backfires as he fails to realize the enormous and leveraged hedges that exist in today's market. Those hedges are forced to be unwound in anticipation of the implementation of the Executive Order to eliminate equity shorts.

The decline in stocks quickly accelerate as Citadel, Susquehanna and Goldman Sachs GS (in particular) grow ever more aggressive in selling out their large hedged books. Market makers and quant strategies hedged books are ruined — their liquidation of their hedges add even more fuel to the avalanche of selling.

Global equities decline by more than -10% in the ensuing two months.

BY Doug Kass · Jan 12, 2026, 9:30 AM EST

BY Doug Kass · Jan 12, 2026, 9:13 AM EST

11:30 a.m.: Treasury hosts a $77B 6-Month Bill Auction;

1 p.m.: Treasury hosts a $58B 3-YearNote Auction;

1 p.m.: Treasury hosts a $39B 10-Year Note Auction;

1 p.m.: Treasury hosts a $86B 3 Month Bill Auction

12:30 p.m.: Fed Bank of Atlanta President Raphael Bostic (Non-Voter) moderates a discussion at event hosted by the Rotary Club of Atlanta (Audi-ence Q&A expected. No media Q&A. No embargoed text. Livestream.

12:45 p.m.: Fed Bank of Richmond Presi-dent Barkin (Non-Voter) will speak at the North Carolina Bankers Association Economic Forecast Forum, Durham, NC (Text (repeat of Jan. 6), audience Q&A expect-ed);

6 p.m.: Fed Bank of New York President Williams (Voter) gives keynote before the C. Peter McColough Series on International Economics event organized by the Council on Foreign Relations, NYC (Virtual access available. Text and moderated Q&A expected)

BY Doug Kass · Jan 12, 2026, 9:03 AM EST

BY Doug Kass · Jan 12, 2026, 8:47 AM EST

Bonus — Here are some great links:

The End of Tech Dominance? New Kids in Town

BY Doug Kass · Jan 12, 2026, 7:19 AM EST

I have a busy day.

I have a research meeting from 10 AM to 11:30 AM.

In the afternoon, for a few hours, I have to deal with a continuing medical issue of a family member.

Thanks for understanding.

BY Doug Kass · Jan 12, 2026, 6:45 AM EST

BY Doug Kass · Jan 12, 2026, 6:35 AM EST

There are some important points in this post:

BY Doug Kass · Jan 12, 2026, 6:25 AM EST

I have covered my medium-sized short (SPY) calls (put on Friday afternoon) with long SPY common stock at $689.40 (-$4.70) — as the options market is not yet open!

I have also covered my small short (QQQ) calls (also put on Friday afternoon) with long QQQ common stock at $621.33 (-$5.35).

Essentially I have a buy write on now.

BY Doug Kass · Jan 12, 2026, 6:15 AM EST

(QQQ) s are now +$6.81. I'm taking a small short call position.

Position: Short QQQ calls (VS)

By Doug Kass Jan 9, 2026 2:52 PM EST

and...

With S&P cash +43 handles and the S&P at an all-time high I am more aggressively shorting SPY calls.

Position: Short SPY calls (M)

By Doug Kass Jan 9, 2026 11:56 AM EST

BY Doug Kass · Jan 12, 2026, 6:05 AM EST

Wolf Street howls about the President's attack on the Fed Chair.

BY Doug Kass · Jan 12, 2026, 5:55 AM EST

BY Doug Kass · Jan 12, 2026, 5:45 AM EST