Back Shorting the Indices

A bit after 6 PM I am re-shorting (SPY) at $690.59.

I am a scale seller on strength tonite.

BY Doug Kass · Jan 8, 2026, 6:26 PM EST

A bit after 6 PM I am re-shorting (SPY) at $690.59.

I am a scale seller on strength tonite.

BY Doug Kass · Jan 8, 2026, 6:26 PM EST

BY Doug Kass · Jan 8, 2026, 5:16 PM EST

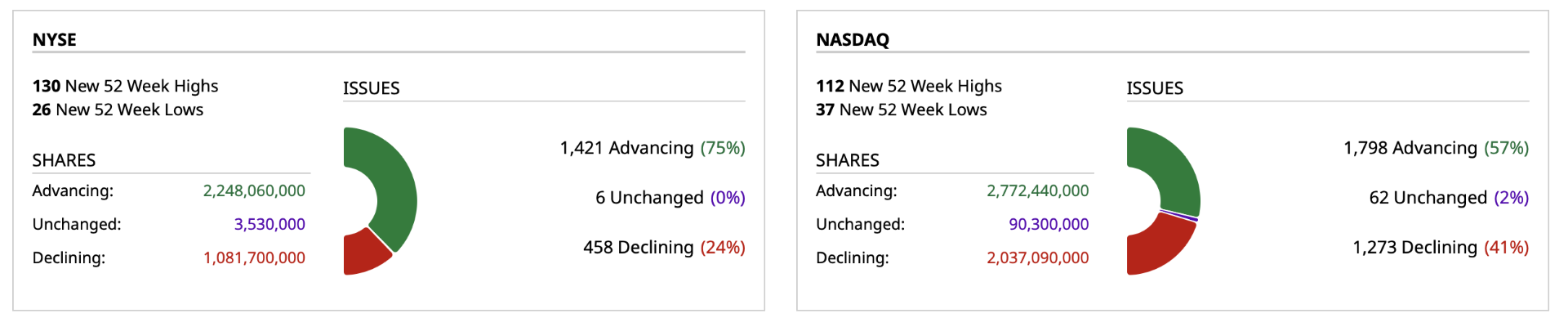

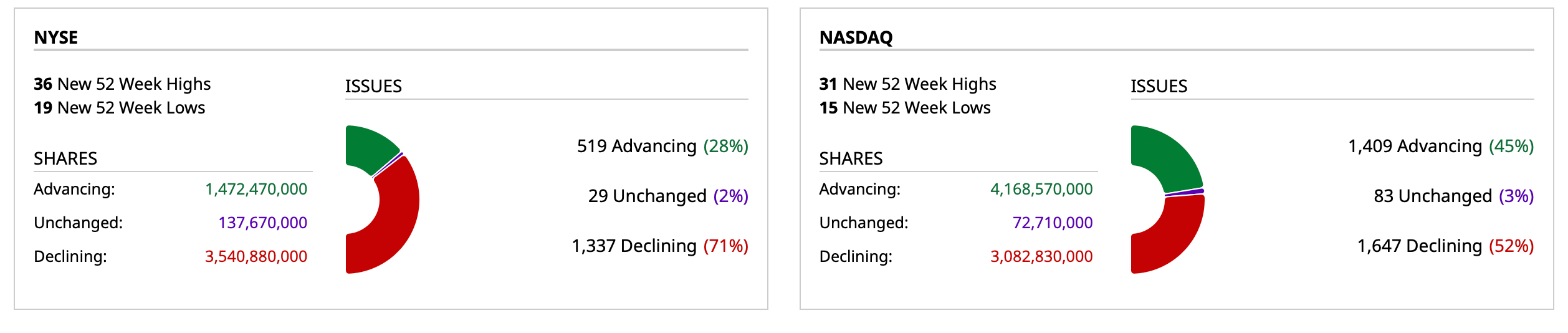

- NYSE volume 13% above its one-month average;

- NASDAQ volume 1% above its one-month average;

- VIX index: up 0.46% to 15.45

BY Doug Kass · Jan 8, 2026, 5:10 PM EST

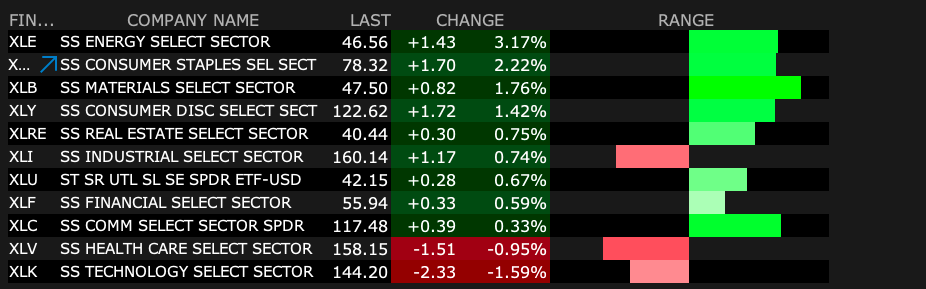

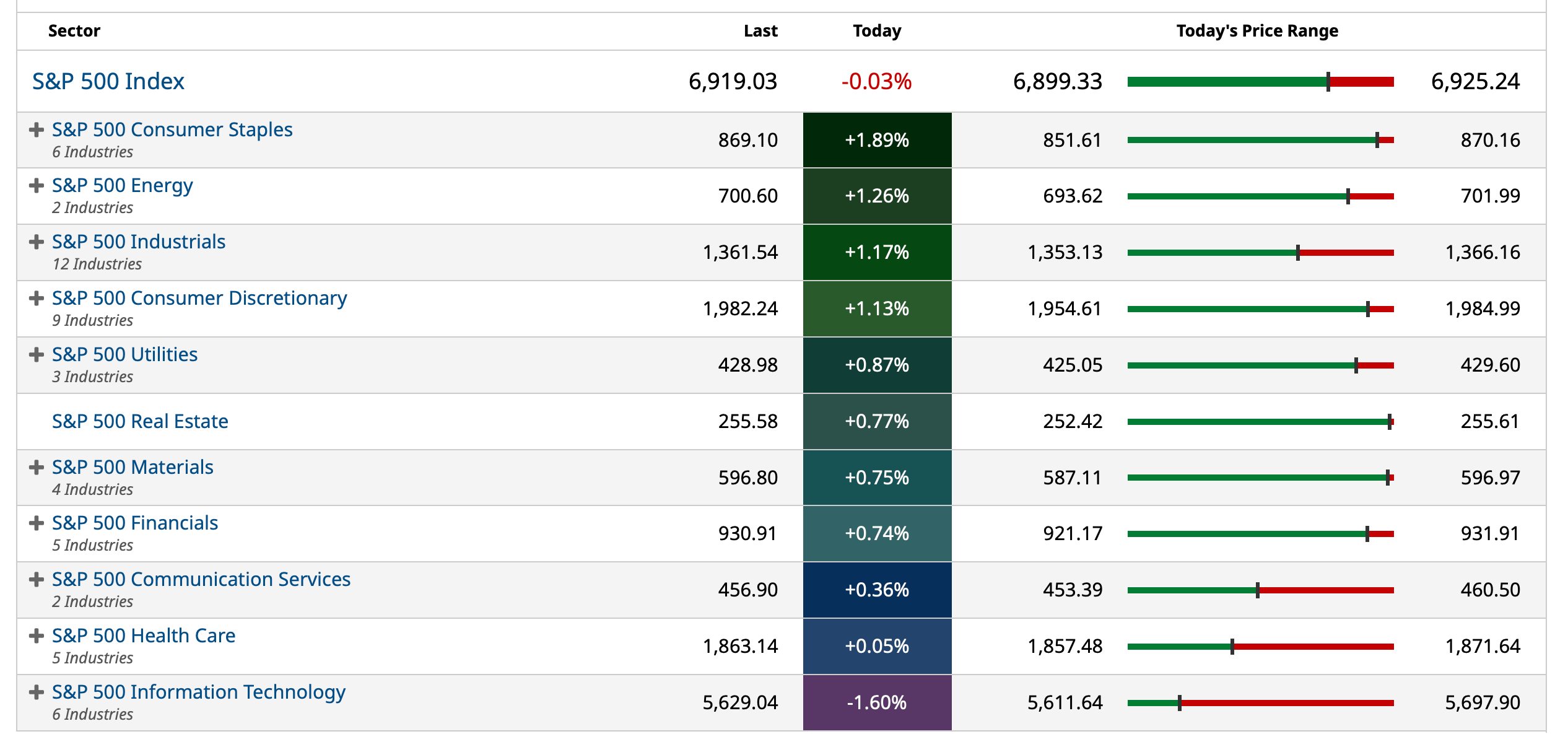

There's been an abrupt change in market leadership consistent with my high-tech cautiousness/concerns (expressed in this morning's chart) — with Staples ( (PG) , (KMB) and (PEP) ) leading the pack.

BY Doug Kass · Jan 8, 2026, 2:37 PM EST

BY Doug Kass · Jan 8, 2026, 1:20 PM EST

No trades since last report.

BY Doug Kass · Jan 8, 2026, 1:09 PM EST

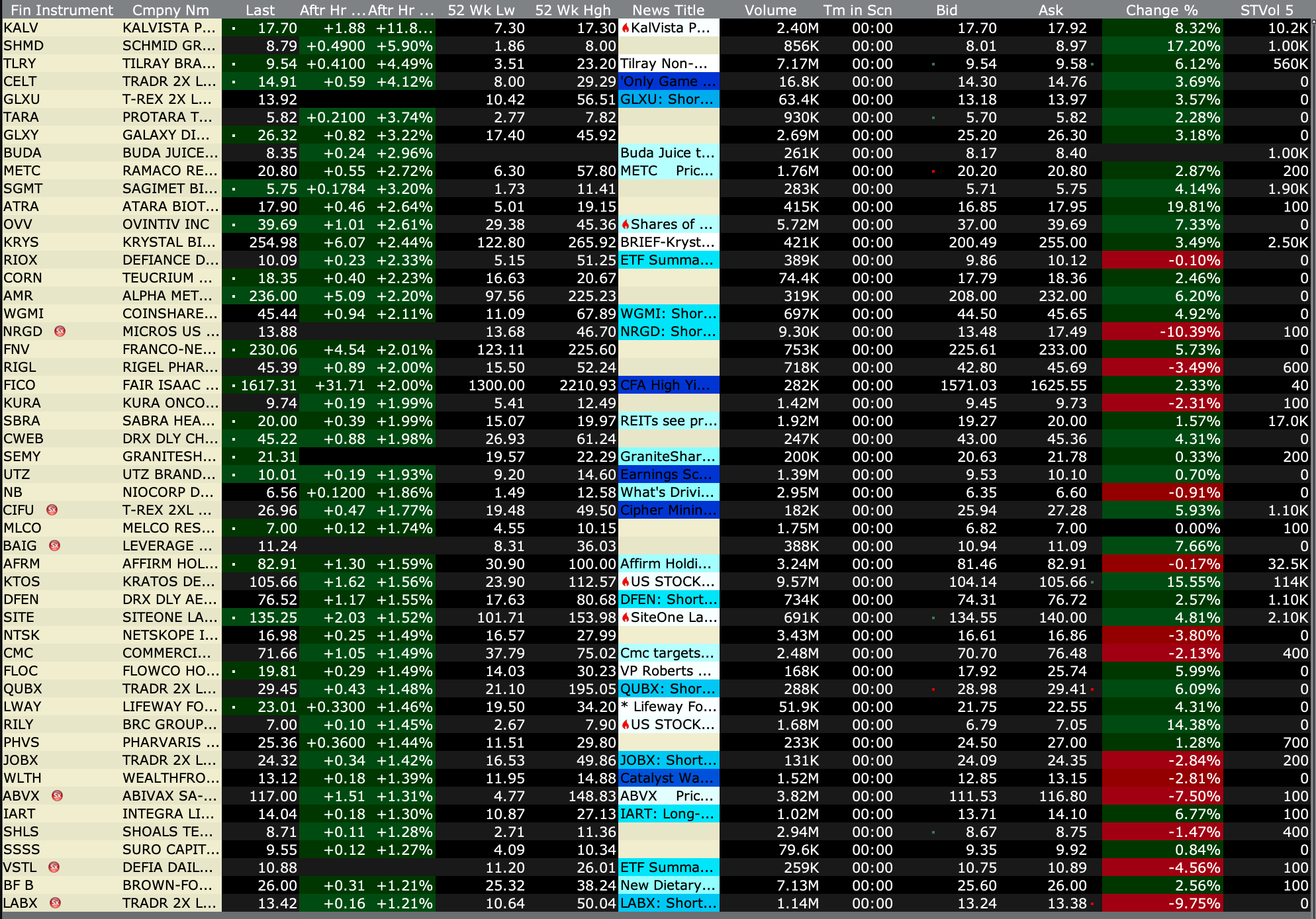

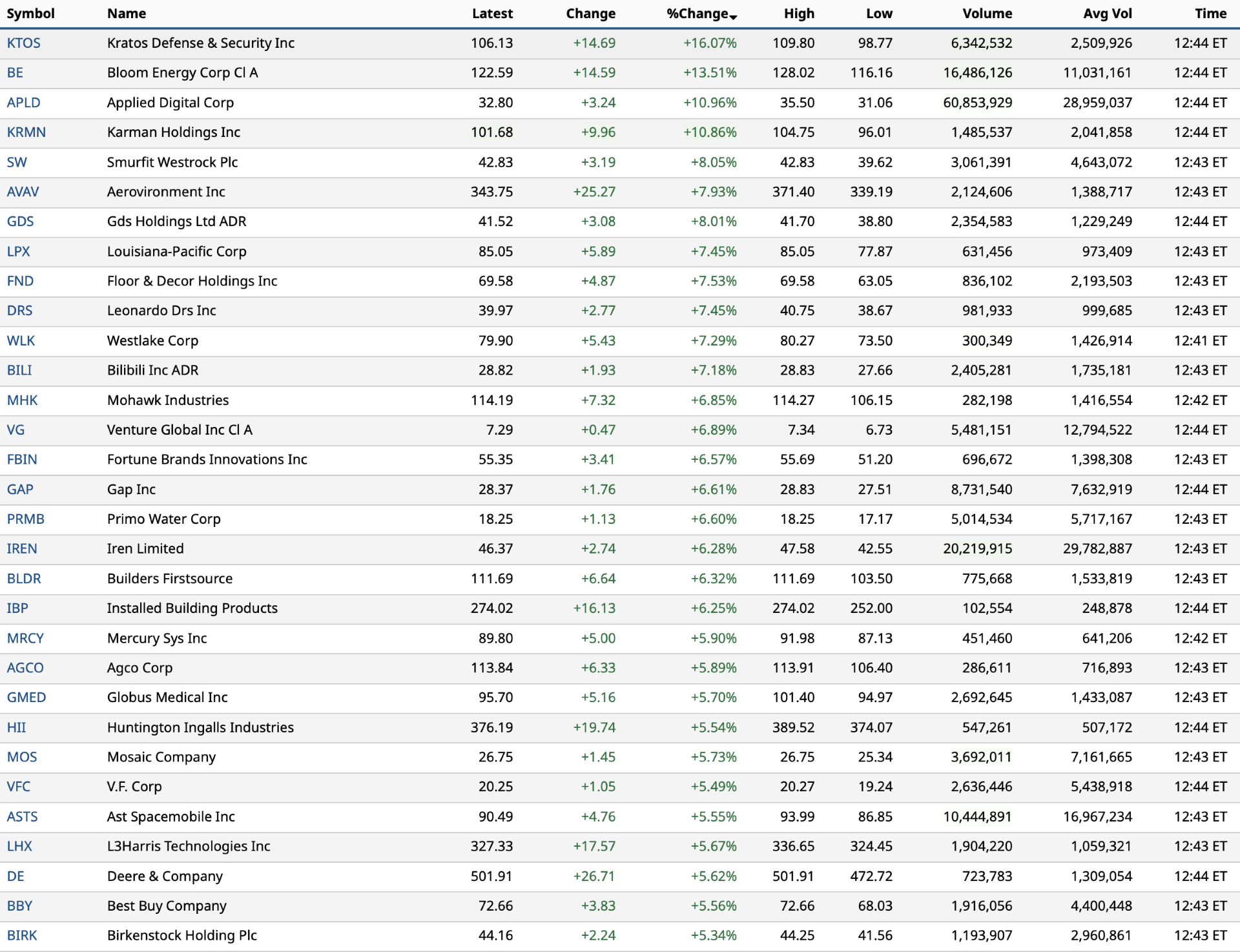

Chart from 10:43 a.m. ET:

BY Doug Kass · Jan 8, 2026, 11:20 AM EST

- NYSE volume 20% above its one-month average;

- Nasdaq volume 4% below its one-month average;

- VIX index: down 0.65% to 15.30

BY Doug Kass · Jan 8, 2026, 10:56 AM EST

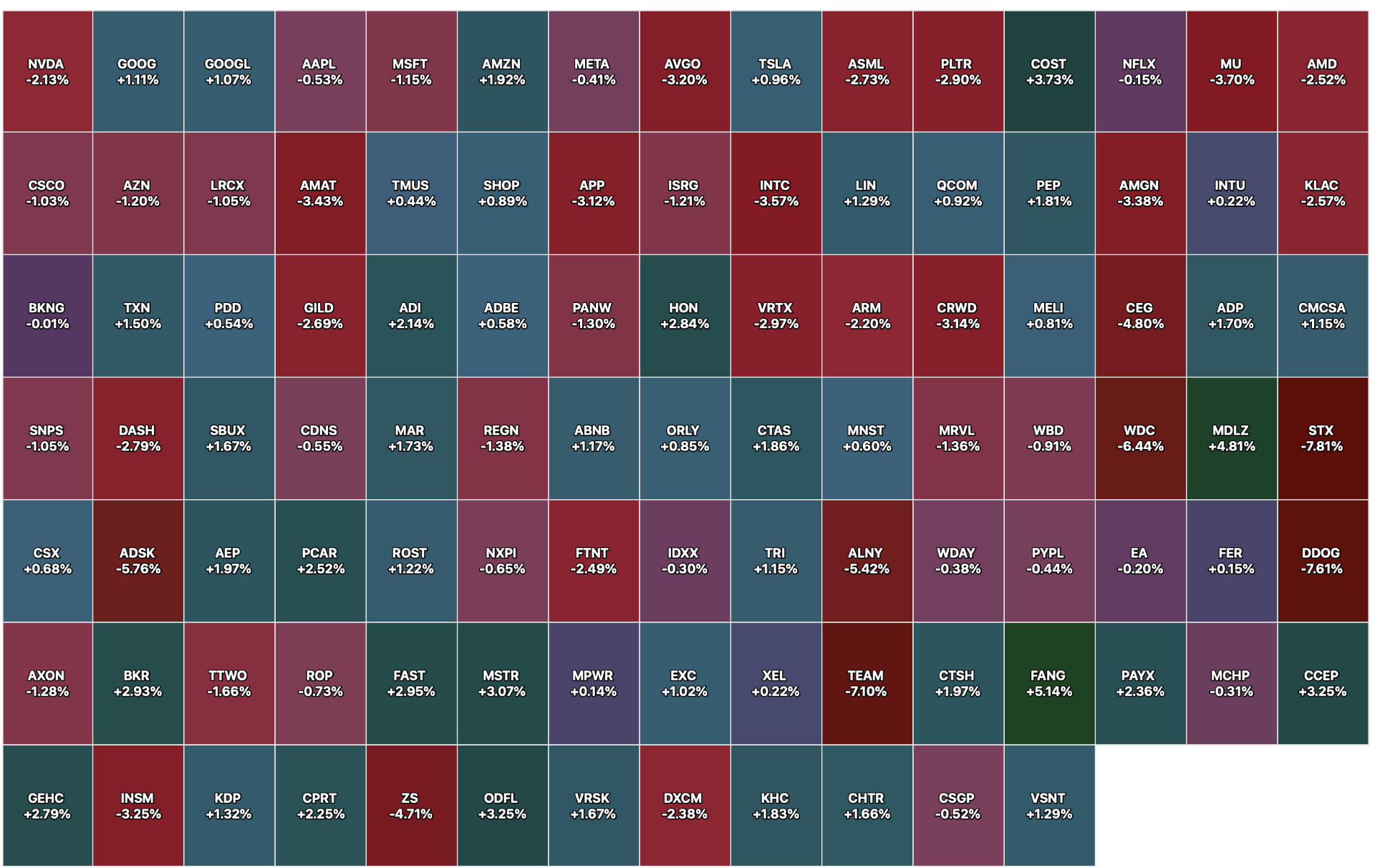

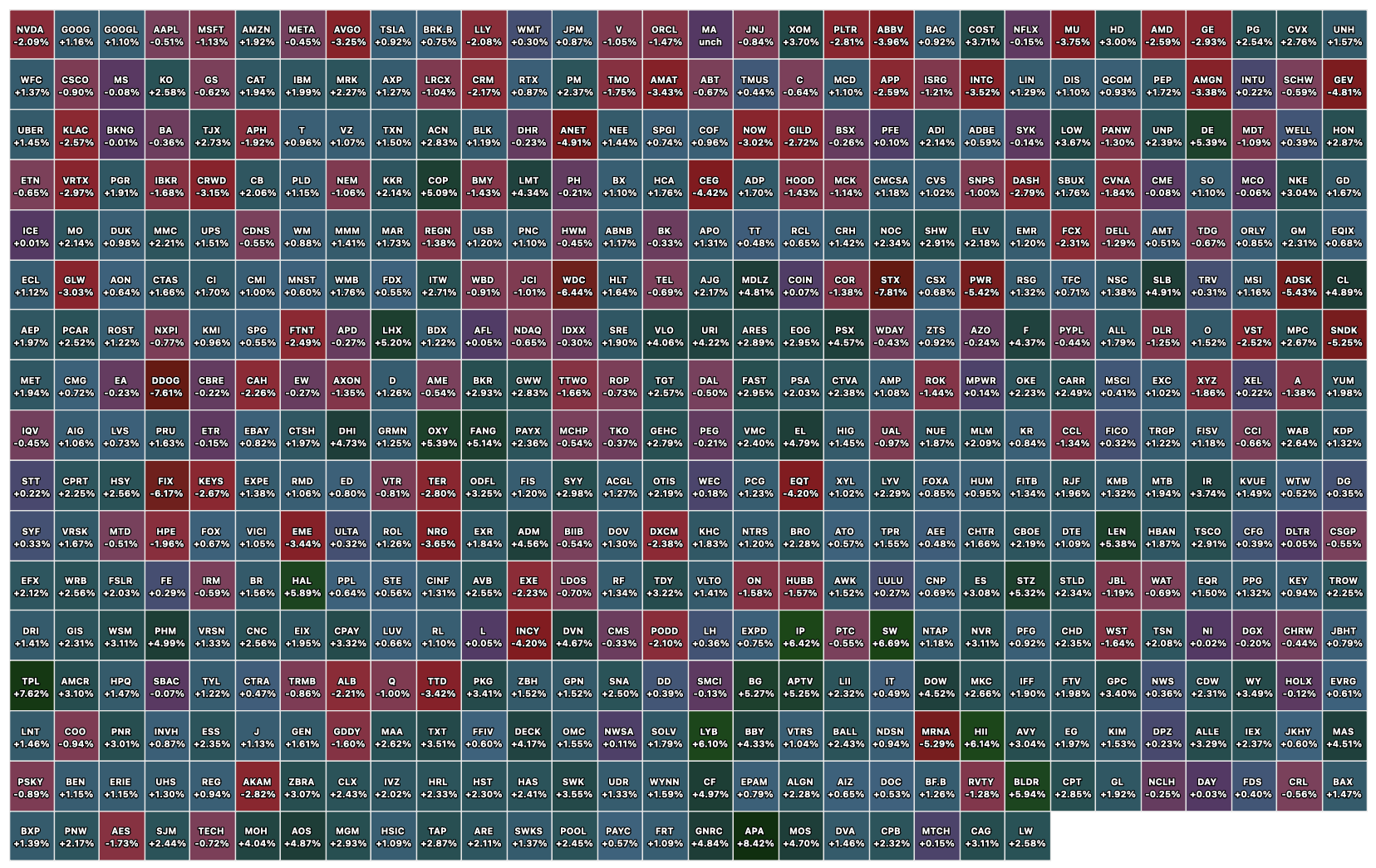

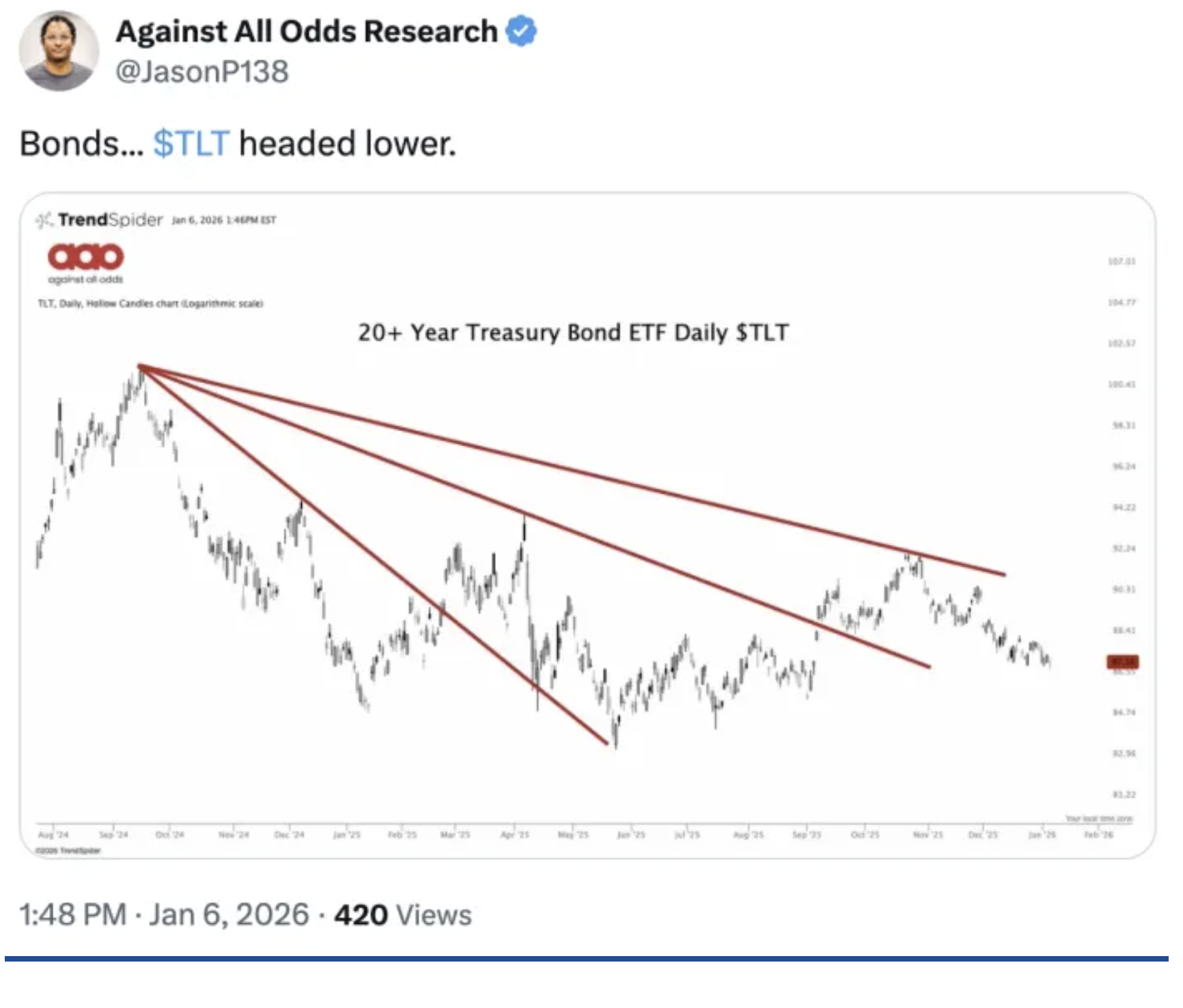

Yesterday I cautioned about interest rates and the technicals of the Magnificent Seven tech stocks -- and I remained concerned.

Here are the two important charts I highlighted on Wednesday:

JAN 7, 2026 6:15 AM EST

JAN 7, 2026 6:30 AM EST

I also expressed these concerns:

JAN 7, 2026 8:00 AM EST

“Successful investing is having everyone agree with you... later.”

- Jim Grant

The last several trading days have been characterized by a further rise in global bond yields (turning the equity risk premium to an even larger discount), large intragroup action, disparate performance in Mag 7/Large-Cap Tech (Apple (AAPL) vs. Amazon (AMZN) yesterday), spastic and casino-like daily moves in individual stocks (e.g. Micron (MU) ) and in precious metals ( (SLV) , (GLD) and (PPLT) ), short squeezes in heavily shorted stocks and extreme bullish investor sentiment (my CNBC Blather Index has 32 CNBC bulls and 1 bear in the last week).

This has all occurred against a backdrop of unsettling geopolitical events and foreign policy that would typically weight on equities — but algorithms and new money into the markets (in a new year) have countered rising geopolitical risks.

As for me, it looks to be the beginning of the end of a maturing bull market.

I have raised my short exposure accordingly.

BY Doug Kass · Jan 8, 2026, 10:28 AM EST

From Peter Boockvar:

I can’t believe I have to go through another quarter of countless earnings calls but here we are. MSC Industrial Direct, a leading distributor of so many products that go right into the manufacturing and industrial end market reported yesterday and its stock fell 4.5%. Here is what they said of note:

“Average daily sales came in at the midpoint of our outlook and increased 4% y/o/y. This was primarily driven by benefits from price of approximately 4.2% that was partially offset by volumes that contracted by 30 bps. The decline in volumes was largely driven by the federal government shutdown, which negatively impacted sales by approximately 100 bps in the quarter. This headwind was felt most in the public sector as seen by a y/o/y decline of 5% in the quarter.”

Sales in this sector lifted when the government reopened. And with respect to raising prices, “we anticipate ongoing benefits from price…So we’re still seeing inflation, not the intense pace that we saw in July and August, but we’re still taking pockets of inflation across the business.”

To get a bit into the weeds here on the impact of tariffs and inflation, “The strongest is seen on the metalworking side, and I think that’s not a surprise for anybody who’s kept track of what’s happening with tungsten. So just to ground everybody, tungsten is a major input into carbide cutting tools, and its supply is controlled by China, and we’ve seen price increases now that exceed 100% on tungsten. So we are taking mid to high single digit price increases from our metalworking suppliers, and we will pass that on starting in mid January.”

“So our exposure is about 15% (to tungsten). We’ll take the first price increase in January. I don’t think we’re done, so I think there will be more inflation passed to us on that. We’re in conversations with our suppliers, so we may see another action needed later on in ’26.”

“Turning to the environment, I would describe demand across the majority of our primary markets as stable. Aerospace remained strong, while some areas of softness remain in automotive and heavy truck. These mixed levels of demand are reflected in the MBI (a manufacturing index) as seen by the recent readings, which remain in contractionary territory.”

From RPM, “the world leader in specialty coatings, sealants and building materials” according to them, who just reported and who missed estimates:

“In the second quarter, sales came in at the lower end of our expectations. The prolonged government shutdown contributed to the trend of longer lead times on construction projects and further pressured already negative consumer sentiment. As a result, sales growth turned negative as the quarter progressed, and earnings declined as we were unable to fully leverage growth investments and overcome temporary margin headwinds from plant and warehouse facility consolidations.”

Helen of Troy just reported too and they said this:

With their Home & Outdoor business, sales fell 6.7% y/o/y “primarily driven by continued competition, lower replenishment orders from retail customers partially due to retailer inventory rebalancing in response to softer demand trends, and decrease in club channel sales in the insulated beverageware category.”

They did mention, similar to MSC, that “these factors were partially offset by the benefit of tariff related price increases” among other things.

Sales in their Beauty & Wellness sector fell .5% y/o/y mostly due to “a decline in Beauty primarily due to softer consumer demand, increased competition, the cancellation of direct import orders from China in response to higher tariffs and lower closeout channel sales” among other factors.

They cut guidance and said “The sales outlook reflects the Company’s view of continued consumer spending softness, especially in certain discretionary categories, as well as its view of increased macro uncertainty, a more promotional environment, and an increasingly stretched consumer.”

Albertson’s fell 6% yesterday after reporting and said this:

“Consistent with what you’ve heard from others, the environment remains mixed and continues to reflect pressure across income segments. At the low end, shoppers are clearly stretched, putting fewer items in the basket each trip and prioritizing essentials while visiting more frequently as they manage their cash flow.”

“Middle income households, which have been relatively resilient, are showing signs of softening with increased price sensitivity and trade down behavior emerging in certain categories. At the high end, spending patterns remain largely stable, but even these customers are becoming more conscious of price and value, reflecting a broader shift towards cautious discretionary spending.” I bolded for emphasis.

Turning to some macro overseas, base pay in Japan in November rose 2% y/o/y vs 2.4% growth in October and 2% in September. While healthy pay growth for the Japanese, it still is running below inflation and why the BoJ is being pressured to hike again. While the data was as expected, we are seeing a drop in JGB yields after a 30 yr bond auction that went ok while the yen is flat.

We did sell our Japanese stocks this week on the belief that Industrial Corporate Japan is facing intense competition from its Chinese peers in a variety of sectors like autos, robotics, industrial automation, and tech. That said, if the Chinese yuan does continue to rally, I think there is a growing possibility the yen could rally vs the US dollar. And, I do applaud Corporate Japan’s actions over the past 10+ years in dramatically improving corporate governance, answering to shareholders and sharply reducing the whole cross share holdings culture of the 1980’s.

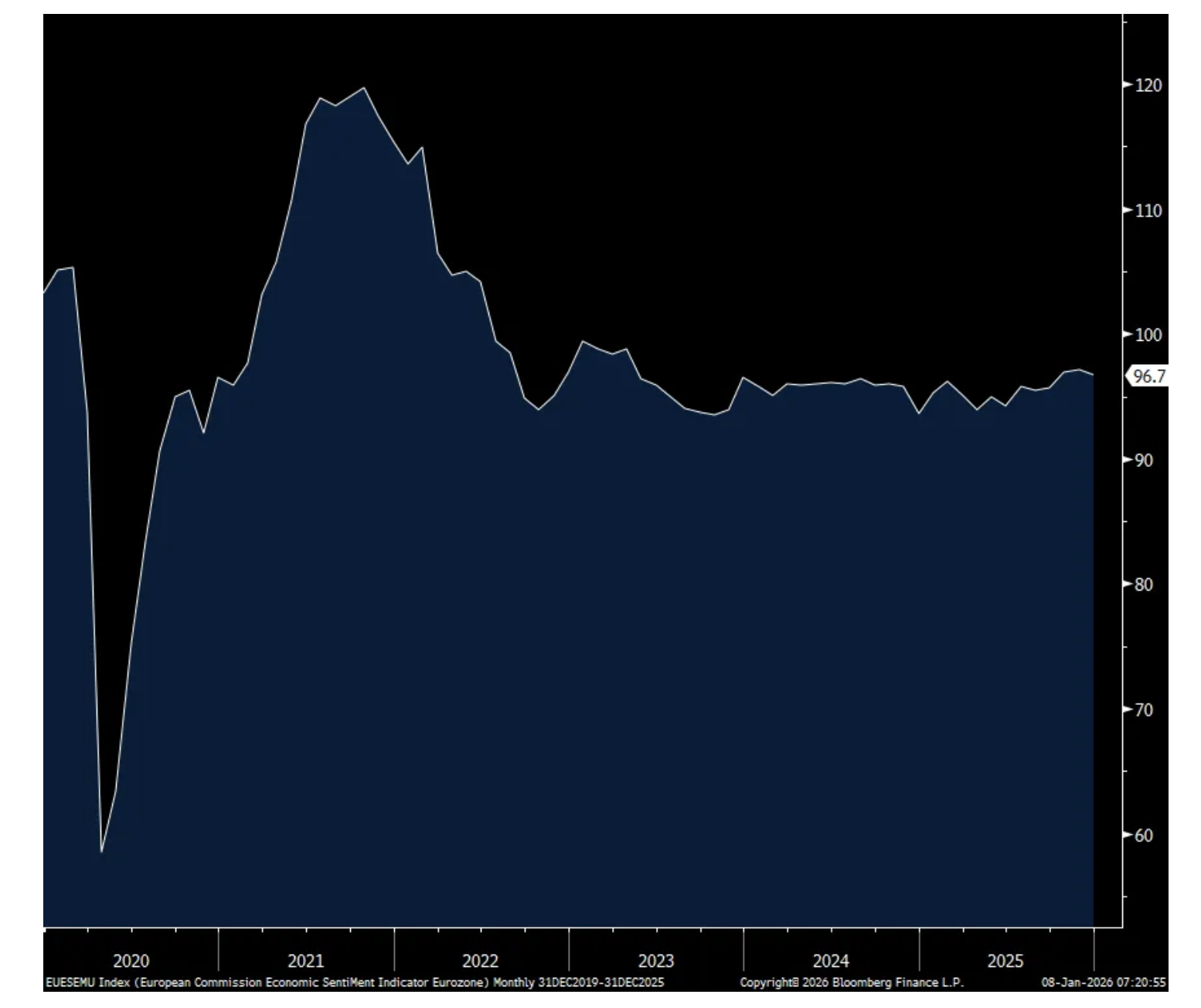

In Europe, the Eurozone December Economic Confidence index fell to 96.7 from 97.1 and vs the estimate of 97.1. This index has basically flat lined over the past 3 ½ years. Component wise, drops in confidence were seen in services, the consumer, retail, partly offset by a less negative read on manufacturing and construction. Nothing market moving here but European bond yields are higher across the board by about 3 bps while stocks are down slightly. The euro is little changed.

Eurozone Economic Confidence Index

Germany saw a big jump in November factory orders of 5.6% m/o/m, well better than the estimate of down 1% and was led by a few big ticket orders. Ex the big orders, new orders grew by .7% from October. We know German manufacturing has been competitively challenged by having higher energy costs and an intense economic rival in China.

BY Doug Kass · Jan 8, 2026, 10:15 AM EST

I covered my (QQQ) short at $619.05 (-$5.00)

I plan to reshort on strength.

BY Doug Kass · Jan 8, 2026, 10:03 AM EST

* Some in the business media reduce market forecasts to a too simplistic and irrelevant equation (Profit Growth Plus P/E Change)

* This as lazy and useless as it is absurd...

BY Doug Kass · Jan 8, 2026, 10:00 AM EST

I moved to very large in (PEP) at $136.56.

BY Doug Kass · Jan 8, 2026, 9:42 AM EST

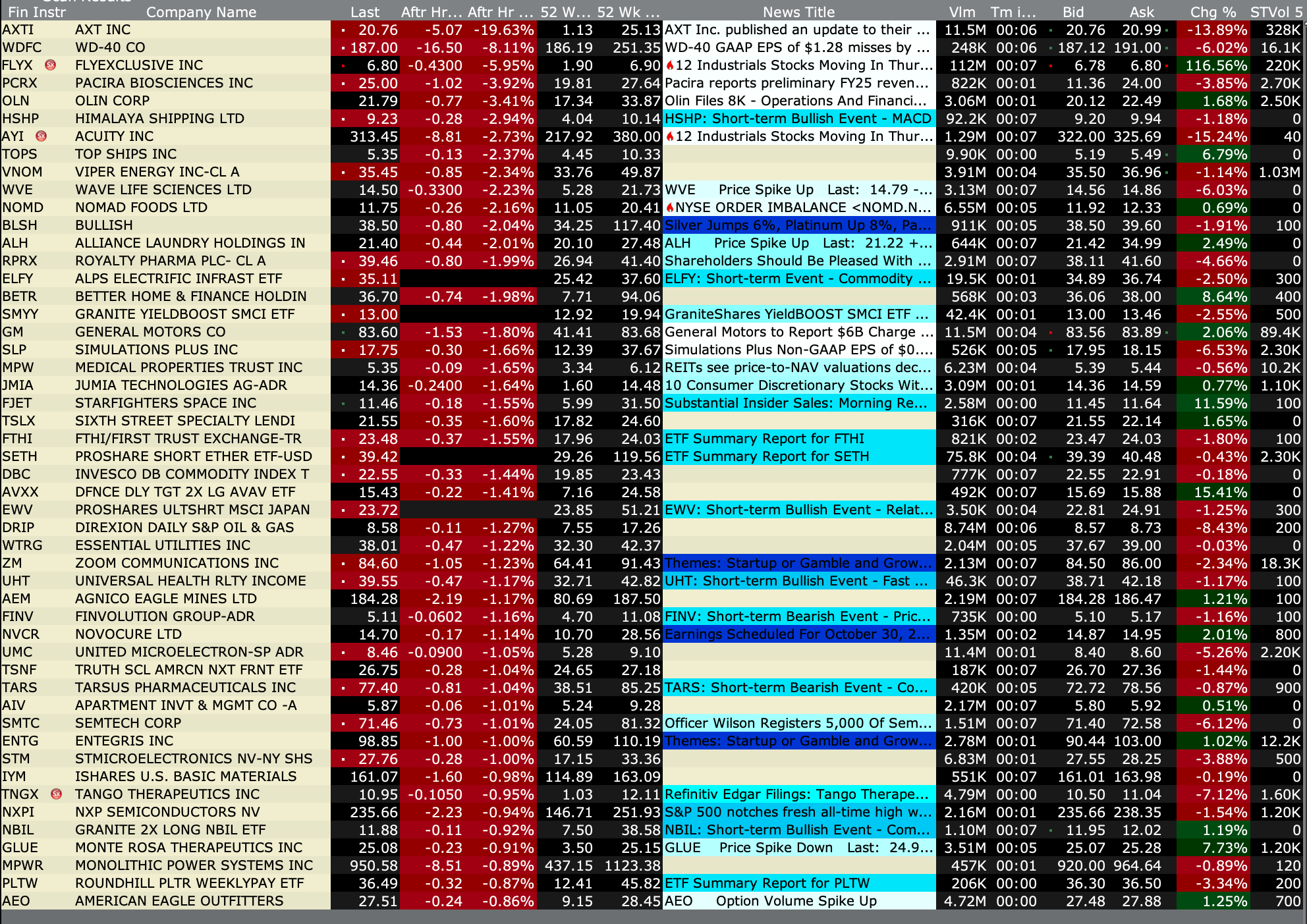

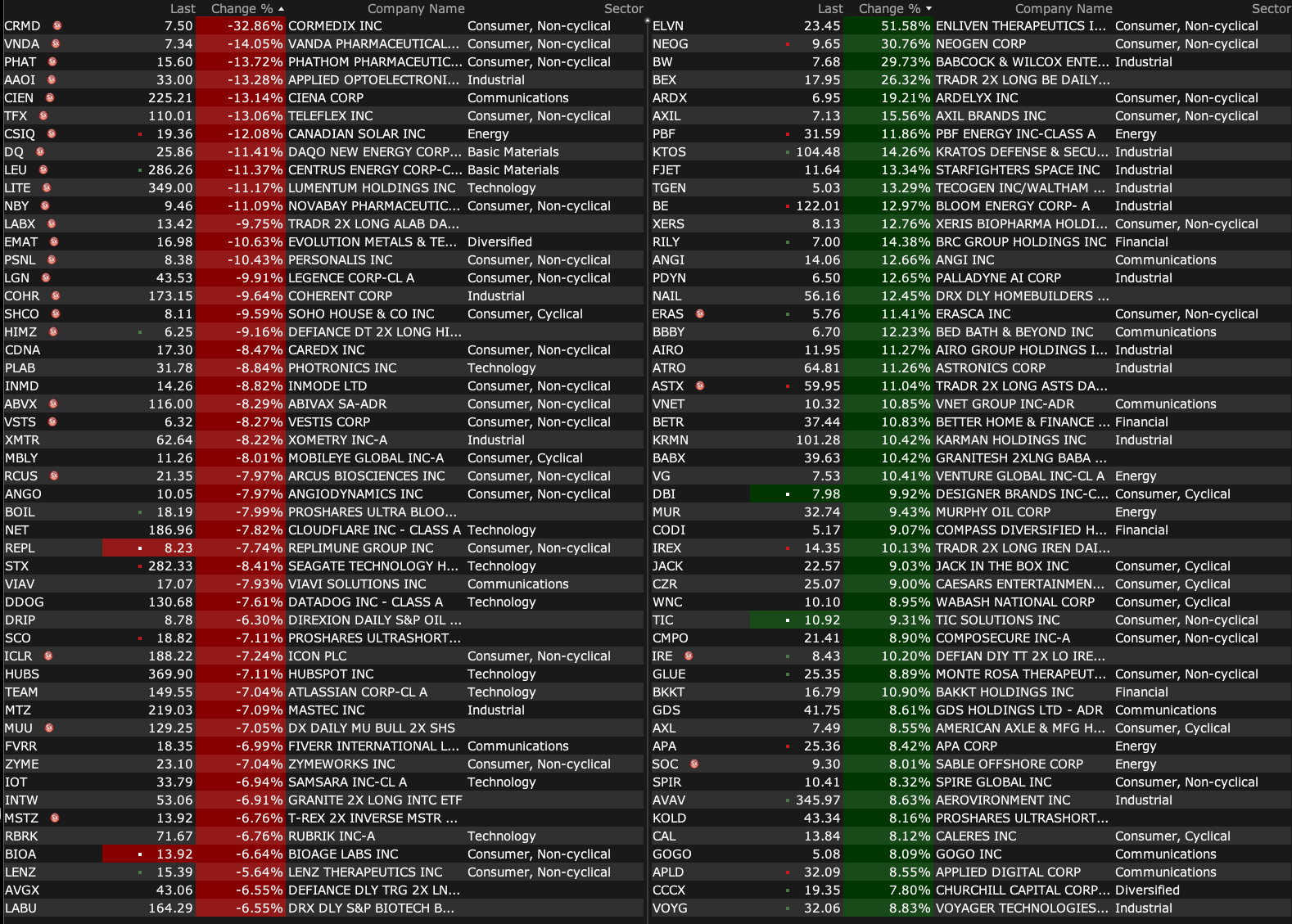

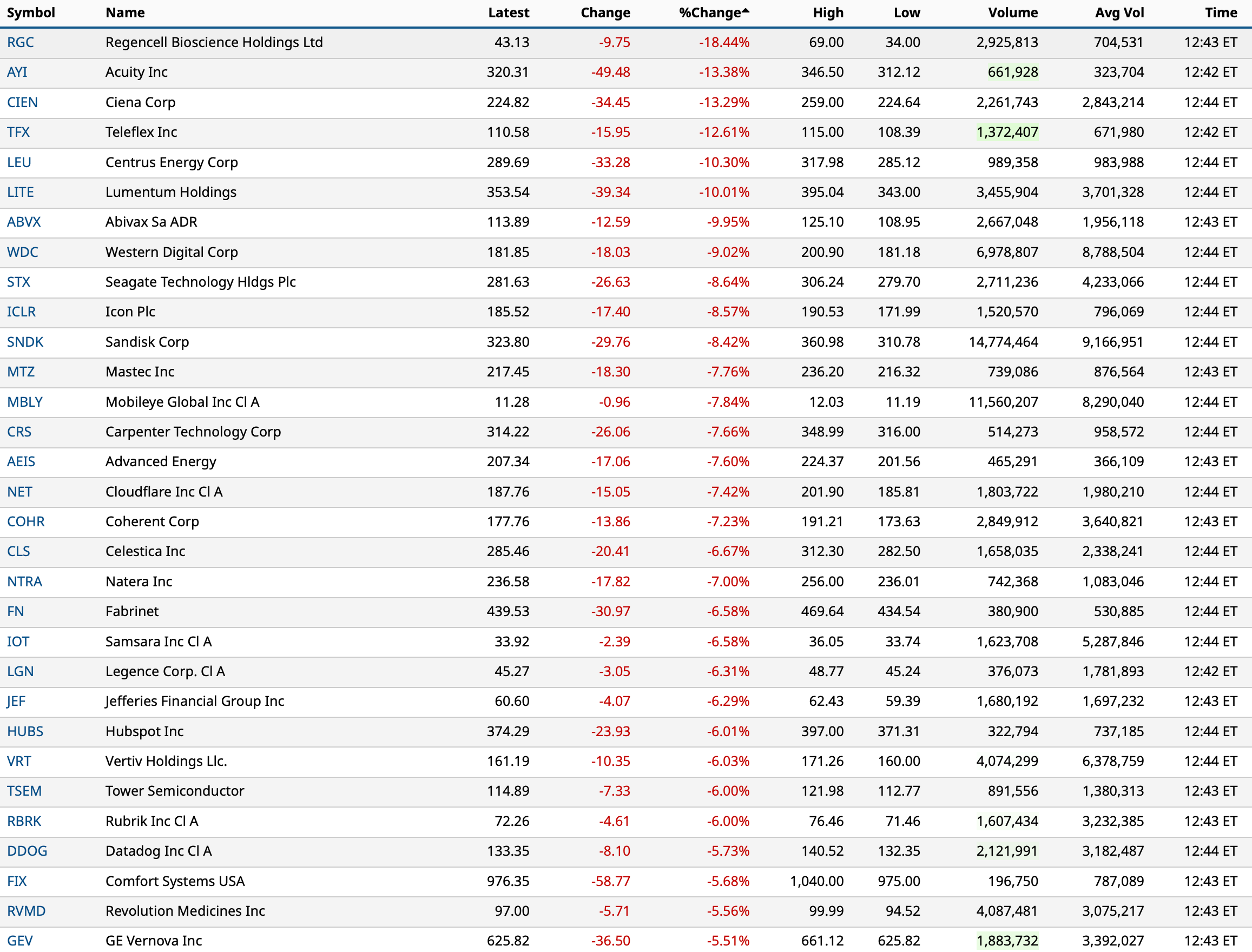

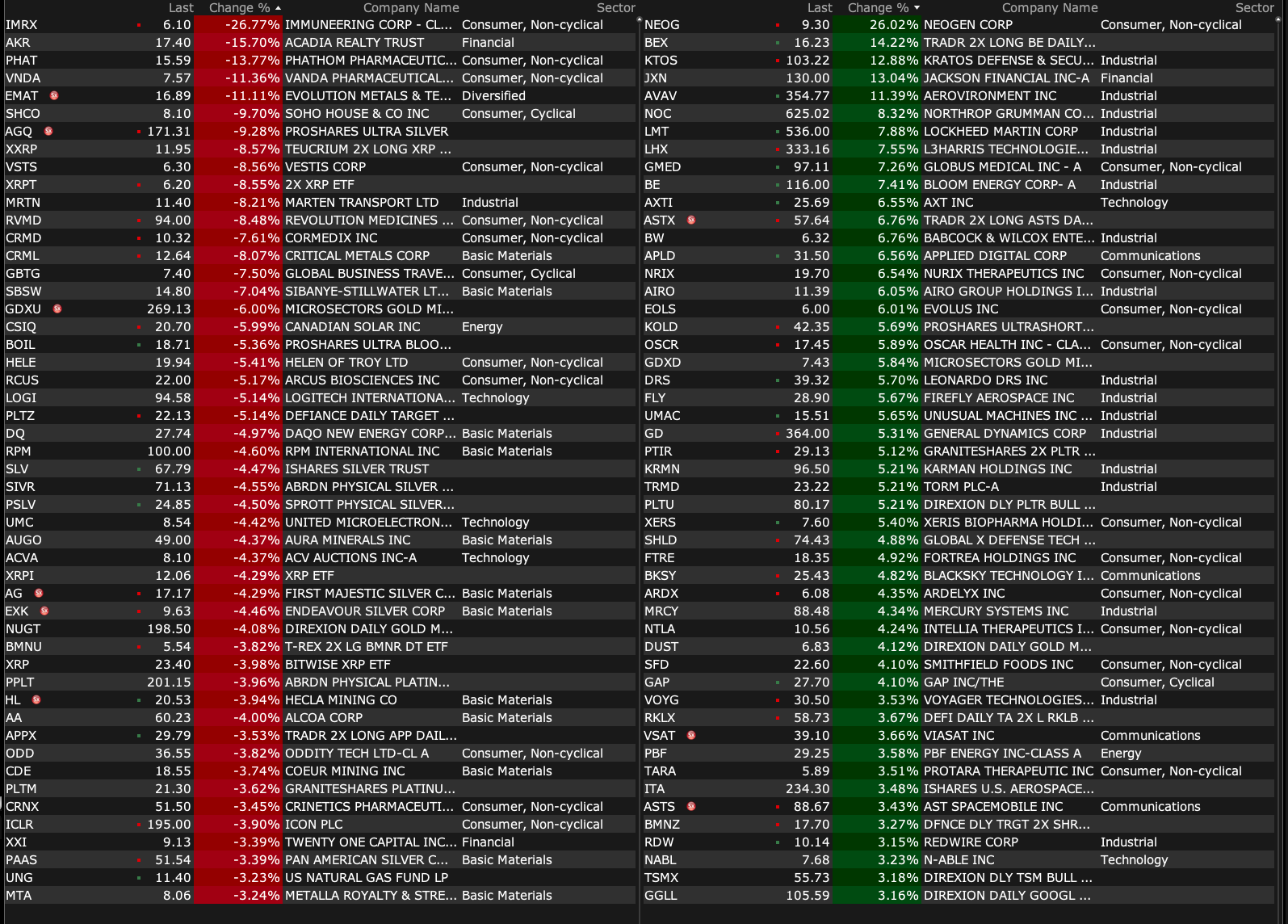

-FLYX +113% (to begin installation of Starlink on its fleet; Installations on flyExclusive's Challenger 350 fleet will begin in early 2026)

-ACON +44% (reports strong Nociscan growth and debt-free balance sheet)

-MLTX +36% (announces positive outcome from Type B Meeting with U.S. FDA with Topline results from SUNRISE-PD Trial expected in 1H26 with plans for BLA submission for SLK in HS in 2H26)

-NEOG +27% (earnings, guidance)

-KTOS +13% (President Trump says he will request increase in US military budget to reach $1.5T in 2027; US FCC said to exempt certain foreign made drones from new government restrictions)

-NOC +8.5% (President Trump says he will request increase in US military budget to reach $1.5T in 2027)

-LMT +7.8% (President Trump says he will request increase in US military budget to reach $1.5T in 2027)

-GMED +7.2% (earnings, guidance)

-KRMN +6.8% (to acquire Seemann Composites and Materials Sciences, Leaders in Advanced Composite Systems for Submarine, UUV/USV and Strategic Naval Surface Platforms for $220M)

-APLD +6.2% (earnings, color)

-GD +5.4% (President Trump says he will request increase in US military budget to reach $1.5T in 2027)

-PBF +5.2% (Piper/Sandler Raised PBF to Overweight from Underweight, price target: $40)

-GAP +4.1% (UBS Raised GAP to Buy from Neutral, price target: $41)

-ARDX +3.3% (earnings, guidance)

-RTX +2.8% (President Trump says he will request increase in US military budget to reach $1.5T in 2027)

-PLTR +2.6% (President Trump says he will request increase in US military budget to reach $1.5T in 2027)

-SHOO +2.5% (Needham Raised SHOO to Buy from Hold, price target: $50)

-STZ +2.3% (earnings, guidance)

-VNDA -11% (receives FDA letter concluding HETLIOZ (tasimelteon) sNDA, for treatment of jet lag disorder, cannot be approved in current form)

-SHCO -9.8% (discloses that buyout partner MCR informed Yucaipa that it will not be able to fund its Closing Commitment in full at or prior to the currently anticipated Closing date)

-CRMD -9.1% (appoints Mike Seckler to the role of EVP & Chief Commercial Officer, effective immediately)

-TFX -9.1% (earnings)

-RVMD -7.5% (AbbVie says not in talks to acquire company, denying earlier press report)

-HELE -5.6% (earnings, guidance)

-SGML -5.2% (Tier1 firm Cuts SGML to Underperform from Neutral, price target: $13 from $11)

-RPM -5.1% (earnings, guidance)

-AA -3.9% (JPMorgan Chase and Co Cuts AA to Underweight from Neutral, price target: $50 from $45)

BY Doug Kass · Jan 8, 2026, 9:25 AM EST

BY Doug Kass · Jan 8, 2026, 9:15 AM EST

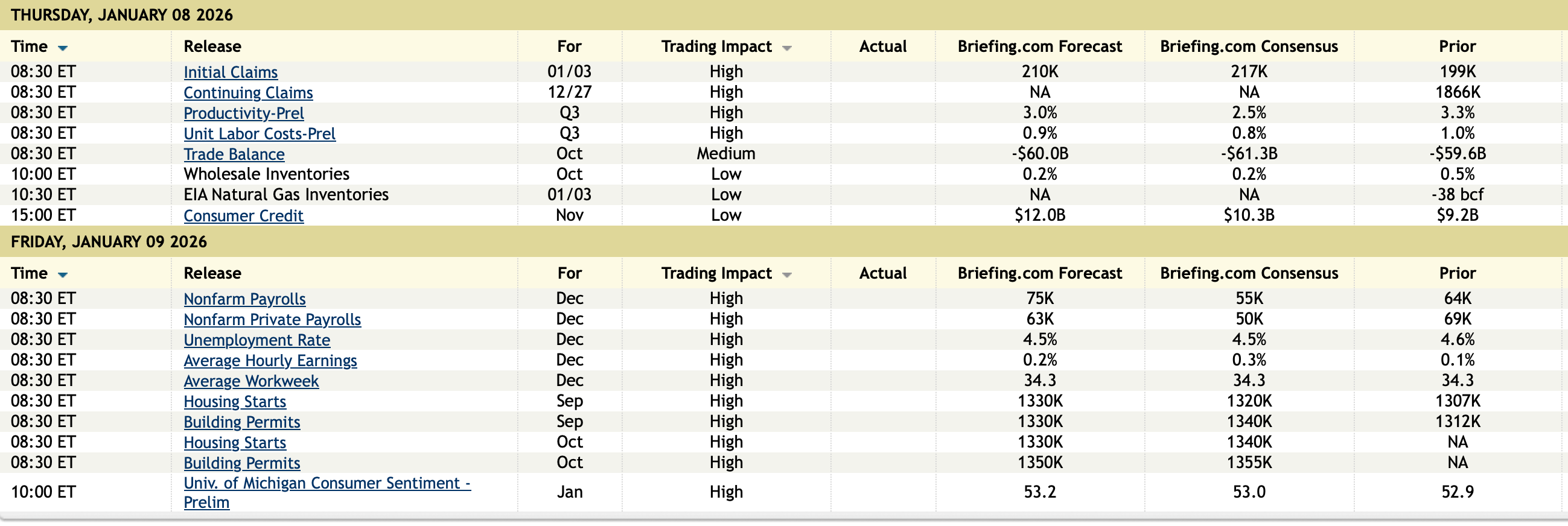

11 a.m.: Treasury announces a 6-Week and 3 and 6 month bill auction;

11:30 a.m.; Treasury hosts an $80 billion 4 and an $80 billion Week Bill Auction;

2 p.m.: Treasury Buyback (liquidity support);

3 p.m.: Treasury inv. class auction data

BY Doug Kass · Jan 8, 2026, 8:55 AM EST

Needham analyst Tom Nikic downgraded Nike (NKE) to Hold from Buy without a price target.

The company's turnaround is progressing slower than expected, the analyst tells investors in a research note. Needham is concerned about Nike's recent level of sell-in in its North America wholesale channel. In addition, China "appears highly problematic," and consensus estimates for the next 12-24 months "look too high," contends Needham.

I am long a small amount of Nike (it's a long-term investment and not a trade). I see no rush to accumulate.

BY Doug Kass · Jan 8, 2026, 8:45 AM EST

* The Trump Administration should not be choosing winners and losers

* Thus far our markets have shrugged off political interference in setting corporate policy — but don't expect this to be a permanent condition

* President Trump's emerging policy directives (cessation of defense company stock buybacks and eliminating institutional purchases of homes) represent a risk to business confidence and the markets

Following the capture of Nicolás Maduro over the weekend, President Trump issued his intentions of eliminating institutional buying of residential real estate and to recommend that defense companies no longer be permitted to buy back their shares.

The later recommendation was particularly interesting — that defense companies were using too much cash on buybacks and dividends at the expense of investing in capital and labor. The president went on to say that defense company executive compensation was far too high:

https://truthsocial.com/@realDonaldTrump/posts/115855387946005468

Agree or disagree, rules/laws should apply to all industries equally. Selective capitalism is a dangerous precedent and slippery slope. And I don't believe the markets will be receptive.

Regardless, we are being told by David Sacks and the current Administration that the AI sector is now part of our national defense and we are at war with China in this regard. They are all doing tons of business with the U.S. government too, directly and indirectly. They are much bigger businesses with more earnings, more employees, and more capacity to invest than the defense contractors, so more important to focus on. Palantir (PLTR) is basically a defense contractor anyway too, look at their book of business.

You want to talk about stock options, buybacks, and executive compensation, look at the tech industry which dwarfs the defense industry by more than several orders of magnitude (thousands of times) in this regard. Look at the list of the wealthiest people in the country, and what that wealth is based on (stock, a lot of it which has come from options).

If there is anyone this policy should apply to, it is the tech guys.

I frankly do not think the president is exactly nuts in this regard, outside of directing this solely at one industry (defense).

I have been out on an island on this one for a while. My view has been NO buybacks for public companies. No stock options for executives. Keep public companies out the market for their own stock, it creates all sorts of perverse incentives, and it is nuts that companies effectively buy the stock their execs are selling, this is as absurd as politicians being able to legally insider trade. Straight equity only (with straightforward accounting).

Dividends are fine. Give dividends the equivalent tax treatment as buybacks if you want. Do all these things, then let’s see if companies start plowing more cashback into their business (capital and labor) as opposed to playing financial engineering games.

I have long made the case that the lack of predictability of Washington policy is an underappreciated market risk.

Yesterday's announcements on defense company buybacks and institutional purchase of homes confirm my concerns.

Those policy intentions are not market friendly.

BY Doug Kass · Jan 8, 2026, 8:04 AM EST

* In the past I have pointed out when technicians join a popular crowd it might be time to fade them.

* In the last few days the "broadening out thesis" and "melt up" have become consensus (see links under "Bonus") — I take the under!

Bonus — Here are some great links:

A Strong Start to the Year as Equity Leadership Broadens

All-Time Highs Everywhere You Look

The Boy Who Cried "Energy Stocks"

The 2026 Outlook (Love when these guys are so confident... ten cuidado!)

BY Doug Kass · Jan 8, 2026, 6:30 AM EST

From Charlie!

BY Doug Kass · Jan 8, 2026, 6:05 AM EST

I have two board meetings today:

11 AM to Noon

2 PM to 4 PM

Thanks for understanding.

BY Doug Kass · Jan 8, 2026, 5:55 AM EST

The S&P Short Range Oscillator moved to 1.19% vs. 2.40% — that's slightly less overbought.

BY Doug Kass · Jan 8, 2026, 5:45 AM EST