My Tweet of the Day (Part Five)

BY Doug Kass · Jan 7, 2026, 4:55 PM EST

BY Doug Kass · Jan 7, 2026, 4:55 PM EST

BY Doug Kass · Jan 7, 2026, 4:45 PM EST

BY Doug Kass · Jan 7, 2026, 4:35 PM EST

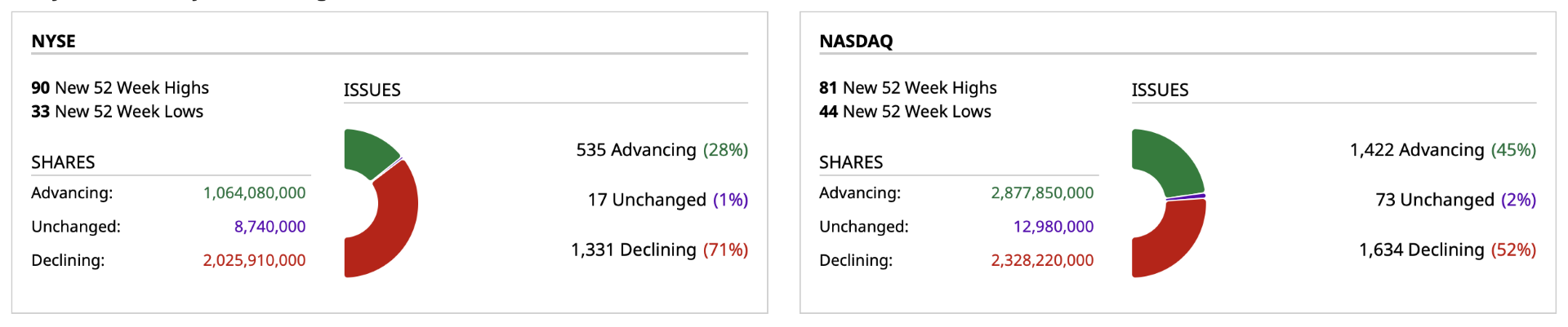

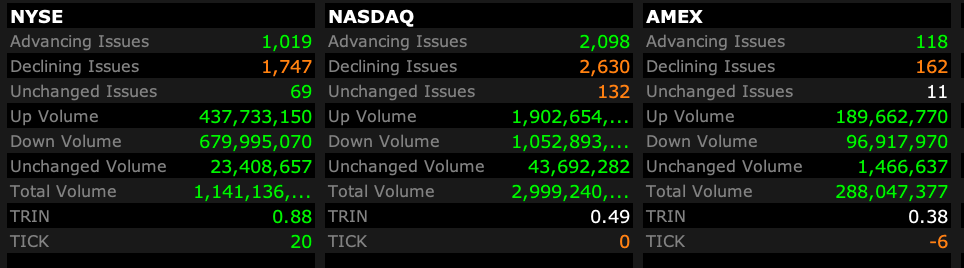

- NYSE volume 18% above its one-month average

- NASDAQ volume 11% above its one-month average

- VIX index: up 4.07% to 15.35

BY Doug Kass · Jan 7, 2026, 4:22 PM EST

BY Doug Kass · Jan 7, 2026, 4:13 PM EST

BY Doug Kass · Jan 7, 2026, 4:01 PM EST

* For JTG!

Here are today's things:

* I shorted (SPY) common and covered for a small profit.

* I shorted more (GRNY) at $25.62 and (JOET) at $43.38.

* I added to my short SPY calls when the market was higher earlier in the morning.

* I shorted more (GS) at $959.01 and (MS) at $187.

* I covered my (JPM) short at $227.95.

* I added to my large (PEP) long at $137.92 and I sold a small amount of calls against the incremental purchase.

* I added to (KMB) at $96.69.

BY Doug Kass · Jan 7, 2026, 3:40 PM EST

Wolf Street howls about the profile of the jobs report this morning.

BY Doug Kass · Jan 7, 2026, 3:00 PM EST

Defense stocks are broadly lower on another Truth Social post that the Administration is prohibiting buybacks by defense companies.

Lockheed Martin (LMT)

Northrop Grumman (NOC)

General Dynamics (GD)

BY Doug Kass · Jan 7, 2026, 2:28 PM EST

A speculative short that I have had in my portfolio — American Homes 4 Rent (AMH) — is getting hit on the Trump news prohibiting institutional purchases of residential homes:

BY Doug Kass · Jan 7, 2026, 1:09 PM EST

Break in!

Blackstone's (BX) shares getting hit on President Trump's statement that he will ban institutions from purchasing homes.

BY Doug Kass · Jan 7, 2026, 1:04 PM EST

I have a business lunch. Back at around 1:30 PM.

BY Doug Kass · Jan 7, 2026, 12:39 PM EST

kenlud

I retired from RBC in 2016. I started my career in 1975. That said, I have never seen such a mass of imponderables in the market.

Navigating them is next to impossible. Political. Economic. Lopsided trading with commensurate gains and losses. One group (AI) absolutely dominating the market.

I will stick with those high yielding Canadian energy names I mention here and though I have taken some nice gains in precious metals I don't plan to either add right now or sell.

Canada's energy industry is the strongest card held in trade talks with the US. There is widespread concern today that it is slowly being withdrawn.

"Carney heads to China next week, seeking new markets and better relations"

BY Doug Kass · Jan 7, 2026, 11:55 AM EST

From Peter Boockvar:

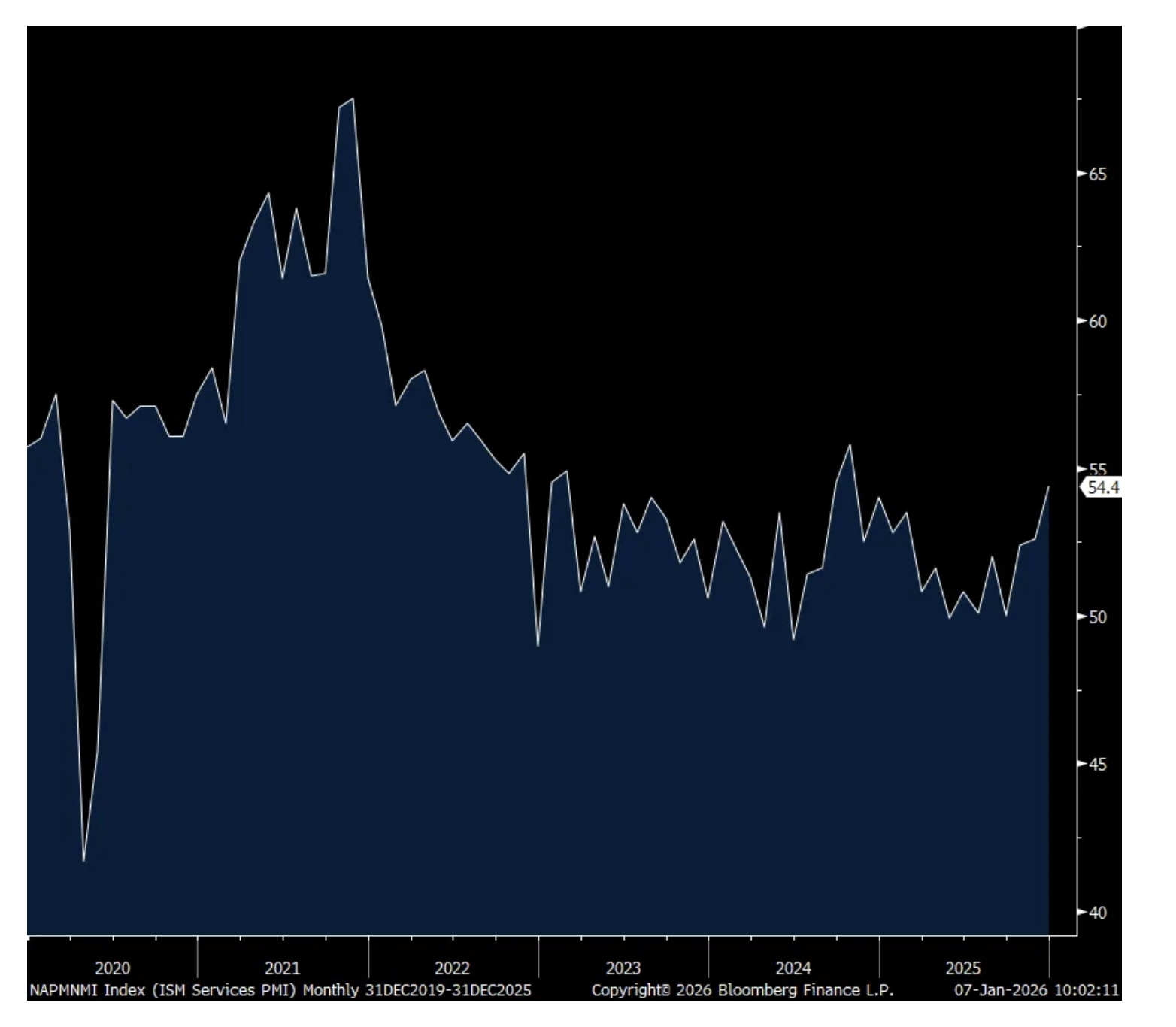

The December ISM services index rebounded to 54.4 from 52.6, above the estimate of 52.2 and the best since October 2024. ISM said “Tariff impacts and seasonality were common themes among panelists’ comments.” While the Business Activity component rose to 56 from 54.5, only 9 industries of 18 saw an increase vs 11 in November.

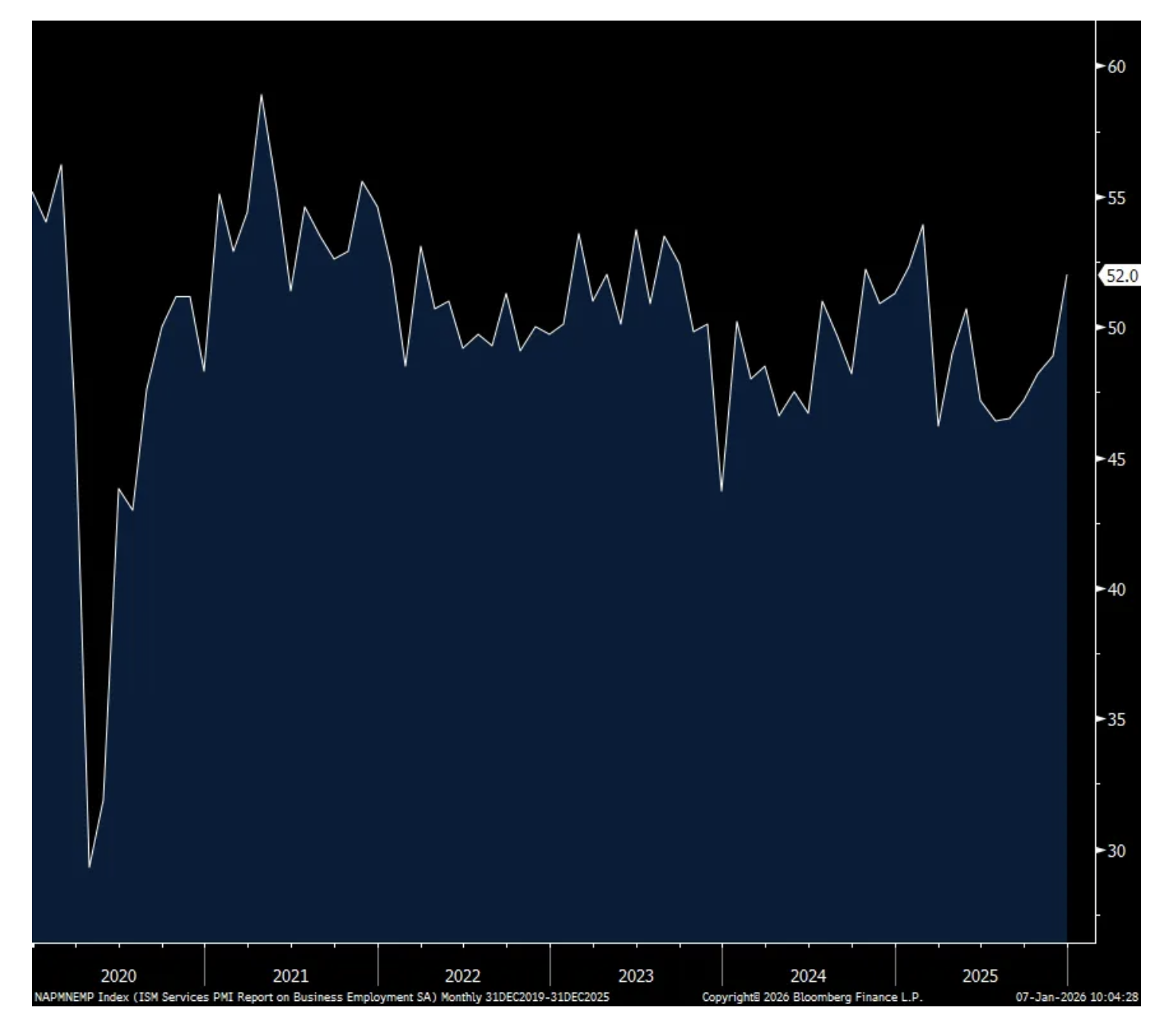

A 5 pt rise in the new orders component to 57.9 helped as did the 3.1 pt increase to back above 50 in the employment component to 52, the first time above 50 since May. What I can’t square here is that only half of the 18 industries surveyed saw a boost to new orders vs 12 in November. On the jobs portion, ISM said “Comments from respondents include: ‘We are now able to hire more qualified people, as the labor market appears to be stabilizing’ and ‘Did a reduction in force of roughly 10 percent as a cost-containment measure.’” Of the 18 industries asked, 7 saw a lift in employment vs 6 in November so still less than half.

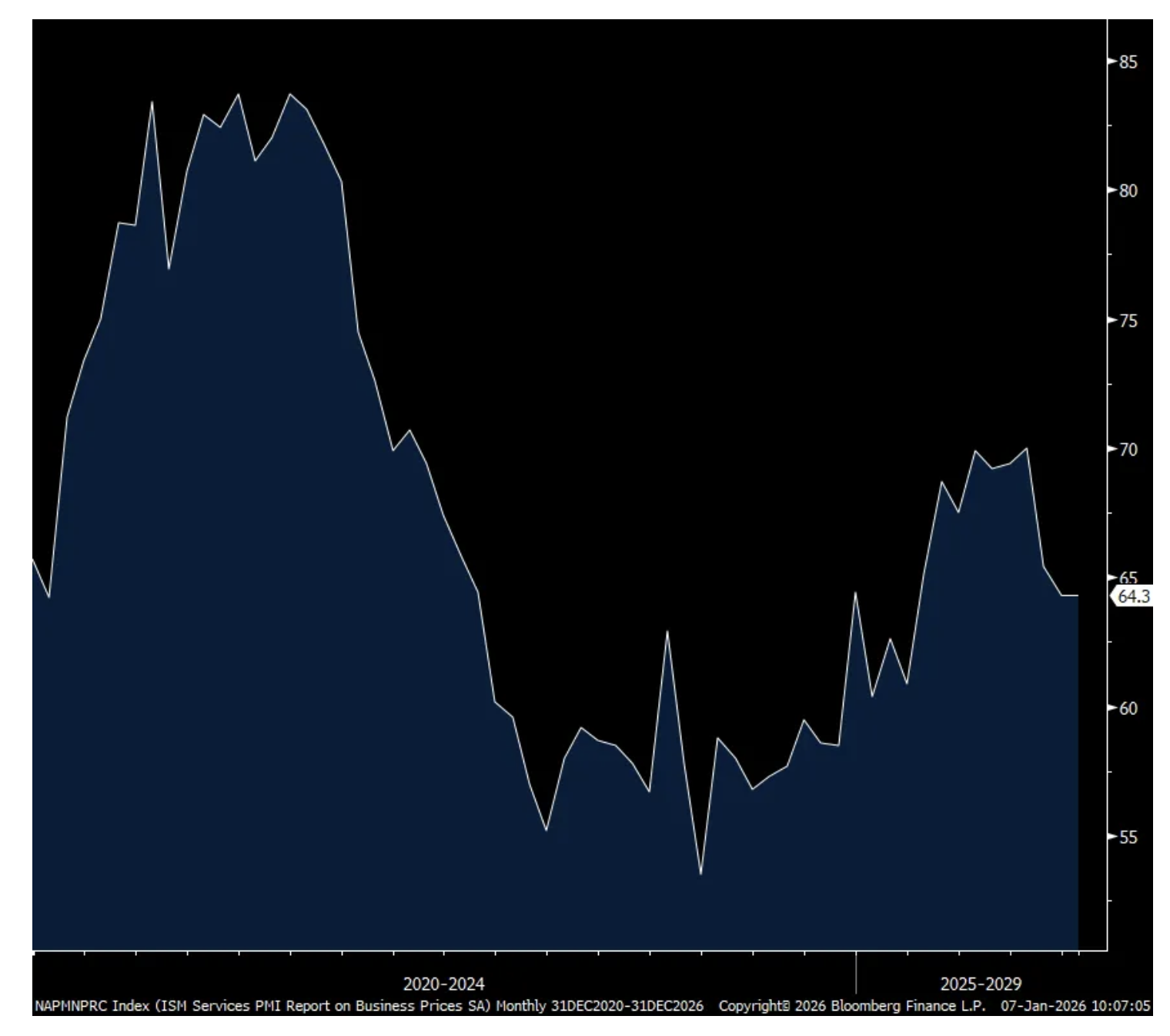

Backlogs remained depressed at 42.6, below the 6 month average of 44.1. Inventories were up a touch at 54.2 but that is the most since October 2024. Supplier Deliveries stayed above 50 at 51.8 which is exactly what the half yr average is. Prices paid fell by 1.1 pts m/o/m to 64.3, still well above 50 but the lowest since March.

The caveat to the headline gain was that just 11 industries of 18 surveyed saw business growth vs 12 in November while 5 saw business declines, the same number in the month before.

Bottom line, the headline gain in the core part of the US economy was good to see but there was some mixed stuff, as mentioned, under the hood with weak industry breadth in terms of growth in key line items and down from November. The industry comments below too were mixed.

The respondent comments:

“We continue to experience higher prices, primarily due to the impact of the administration’s trade and tariff policies. We are disproportionately impacted by importing seafood from Southeast Asia and coffee from South America.” [Accommodation & Food Services]

“In general, business is flat. Value brands are still experiencing higher demand. But premium brands struggle to maintain market share.” [Agriculture, Forestry, Fishing & Hunting]

“Rising labor and staffing shortages across facilities and auxiliary services, increasing regulatory and compliance requirements within the state, continued inflationary pressure on supplies and contracted services, ongoing supply-chain variability for specialized equipment and materials, heightened sustainability expectations and state-led environmental initiatives, fluctuations in enrollment affecting institutional budgets and purchasing volumes, and increased competition and pricing volatility in the regional supplier market.” [Educational Services]

“Overall, business is healthy, most of our purchasing is staying consistent, and we are renewing most contracts as we head into the new year.” [Finance & Insurance]

“Flu cases on the rise; the vaccine is not of much help this year. Respiratory equipment and supplies are seeing a surge in demand.” [Health Care & Social Assistance]

“Annual pricing markups from key service and data providers are higher than they’ve been for many years — gradually drives costs up.” [Information]

“Continuing uncertainty and apprehension regarding tariffs and the resulting impact on pricing.” [Public Administration]

“We expect flat national home prices in 2026, with a forecast of a 0.5-percent increase and a plausible range from a decrease of 3.6 percent to a gain of 4.6 percent. Many metro areas across the country are already posting year-over-year declines, making 2026 the most likely year since 2010 for a modest national price dip.” [Real Estate, Rental & Leasing]

“High business activity due to the holiday season.” [Transportation & Warehousing]

“Year-over-year growth has been coming down for the last three months. Most likely, the government shutdown was a contributor.” [Wholesale Trade]

ISM Services

Employment

Prices paid

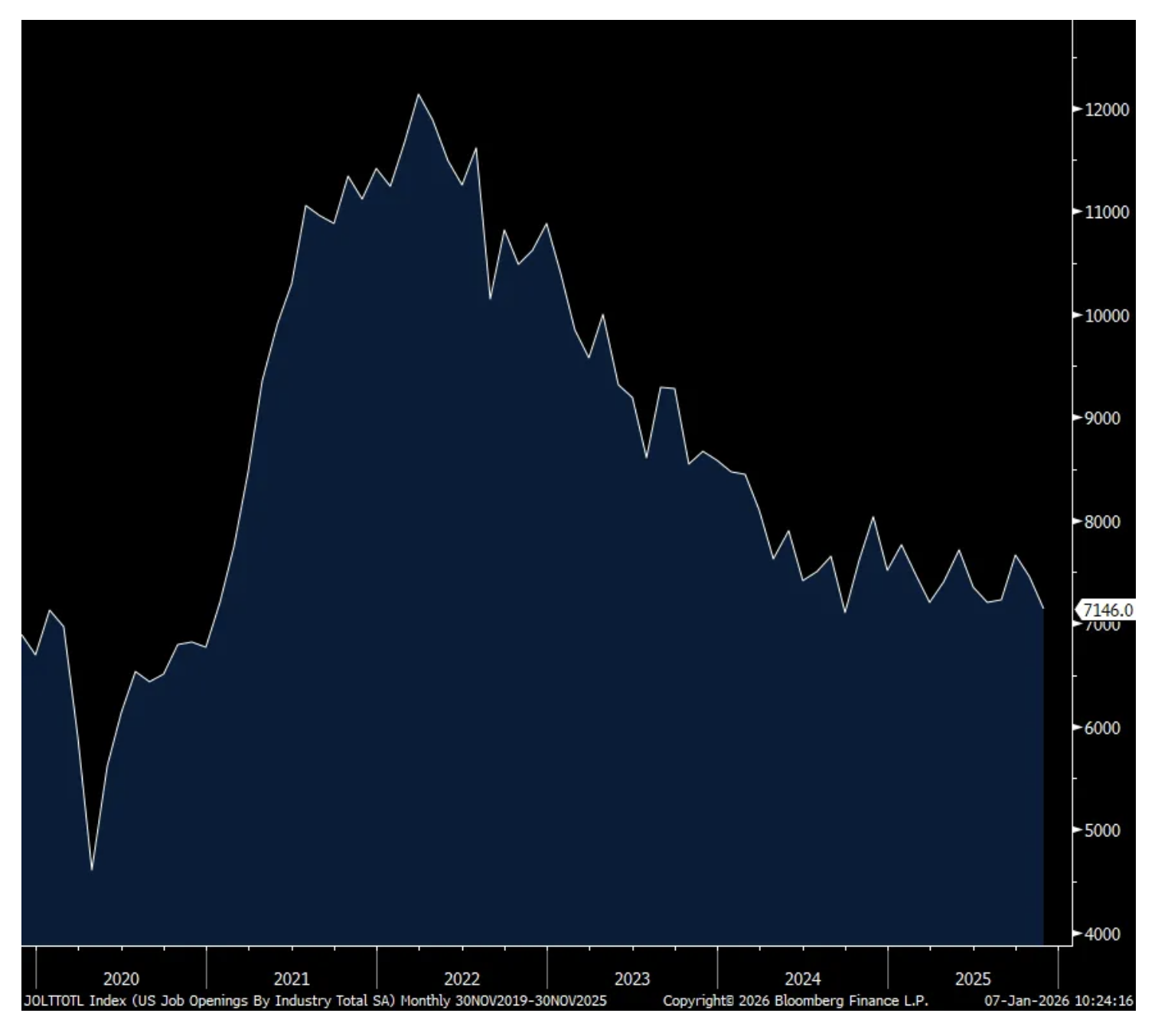

ISM services index rebounds but internals mixed/Job Openings nearing 5 yr low

The December ISM services index rebounded to 54.4 from 52.6, above the estimate of 52.2 and the best since October 2024. ISM said “Tariff impacts and seasonality were common themes among panelists’ comments.” While the Business Activity component rose to 56 from 54.5, only 9 industries of 18 saw an increase vs 11 in November.

A 5 pt rise in the new orders component to 57.9 helped as did the 3.1 pt increase to back above 50 in the employment component to 52, the first time above 50 since May. What I can’t square here is that only half of the 18 industries surveyed saw a boost to new orders vs 12 in November. On the jobs portion, ISM said “Comments from respondents include: ‘We are now able to hire more qualified people, as the labor market appears to be stabilizing’ and ‘Did a reduction in force of roughly 10 percent as a cost-containment measure.’” Of the 18 industries asked, 7 saw a lift in employment vs 6 in November so still less than half.

Backlogs remained depressed at 42.6, below the 6 month average of 44.1. Inventories were up a touch at 54.2 but that is the most since October 2024. Supplier Deliveries stayed above 50 at 51.8 which is exactly what the half yr average is. Prices paid fell by 1.1 pts m/o/m to 64.3, still well above 50 but the lowest since March.

The caveat to the headline gain was that just 11 industries of 18 surveyed saw business growth vs 12 in November while 5 saw business declines, the same number in the month before.

Bottom line, the headline gain in the core part of the US economy was good to see but there was some mixed stuff, as mentioned, under the hood with weak industry breadth in terms of growth in key line items and down from November. The industry comments below too were mixed.

The respondent comments:

“We continue to experience higher prices, primarily due to the impact of the administration’s trade and tariff policies. We are disproportionately impacted by importing seafood from Southeast Asia and coffee from South America.” [Accommodation & Food Services]

“In general, business is flat. Value brands are still experiencing higher demand. But premium brands struggle to maintain market share.” [Agriculture, Forestry, Fishing & Hunting]

“Rising labor and staffing shortages across facilities and auxiliary services, increasing regulatory and compliance requirements within the state, continued inflationary pressure on supplies and contracted services, ongoing supply-chain variability for specialized equipment and materials, heightened sustainability expectations and state-led environmental initiatives, fluctuations in enrollment affecting institutional budgets and purchasing volumes, and increased competition and pricing volatility in the regional supplier market.” [Educational Services]

“Overall, business is healthy, most of our purchasing is staying consistent, and we are renewing most contracts as we head into the new year.” [Finance & Insurance]

“Flu cases on the rise; the vaccine is not of much help this year. Respiratory equipment and supplies are seeing a surge in demand.” [Health Care & Social Assistance]

“Annual pricing markups from key service and data providers are higher than they’ve been for many years — gradually drives costs up.” [Information]

“Continuing uncertainty and apprehension regarding tariffs and the resulting impact on pricing.” [Public Administration]

“We expect flat national home prices in 2026, with a forecast of a 0.5-percent increase and a plausible range from a decrease of 3.6 percent to a gain of 4.6 percent. Many metro areas across the country are already posting year-over-year declines, making 2026 the most likely year since 2010 for a modest national price dip.” [Real Estate, Rental & Leasing]

“High business activity due to the holiday season.” [Transportation & Warehousing]

“Year-over-year growth has been coming down for the last three months. Most likely, the government shutdown was a contributor.” [Wholesale Trade]

ISM Services

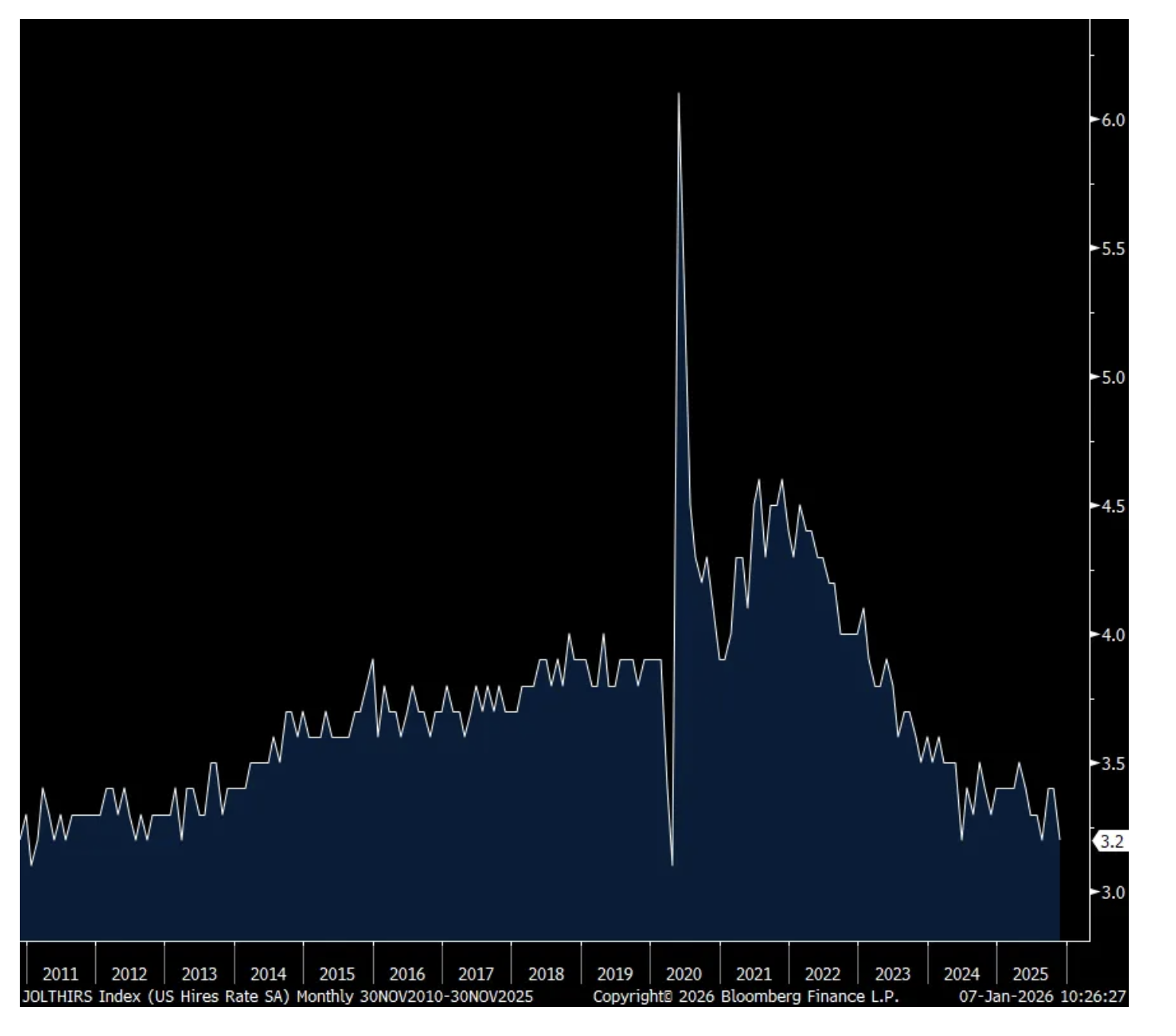

Hiring rate

BY Doug Kass · Jan 7, 2026, 11:39 AM EST

- NYSE volume 21% above its one-month average;

- Nasdaq volume 17% above its one-month average;

- VIX index: up 2.58% to 15.13

BY Doug Kass · Jan 7, 2026, 11:20 AM EST

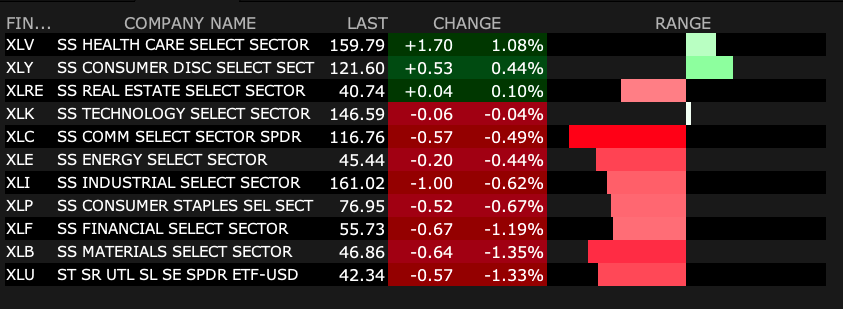

It is my view that financials hit important resistance and are now vulnerable.

NONE

BY Doug Kass · Jan 7, 2026, 10:36 AM EST

Chart from 10 a.m. ET

BY Doug Kass · Jan 7, 2026, 10:29 AM EST

Wolfe Research downgraded JPMorgan Chase to Peer Perform from Outperform; JPM has outperformed since their upgrade alongside their 2025 Outlook (+37% vs. the S&P500 +16%), and while JPM remains a best-in-class franchise, great companies don't always make great stocks. Over the next two-years, they expect JPM's EPS growth to lag peers due asset sensitivity and higher expense growth / weaker operating leverage. Relative valuation vs. peers appears full at ~14x their 2027 EPS (Money Centers ~11x / Regionals ~10x), and while they do not anticipate JPM will see meaningful multiple contraction, they believe EPS growth will ultimately lag peers, prompting their Downgrade to Peer Perform (from Outperform).

BY Doug Kass · Jan 7, 2026, 10:10 AM EST

I covered my (JPM) short at $328.

I plan to reshort on strength.

BY Doug Kass · Jan 7, 2026, 10:00 AM EST

From Peter Boockvar:

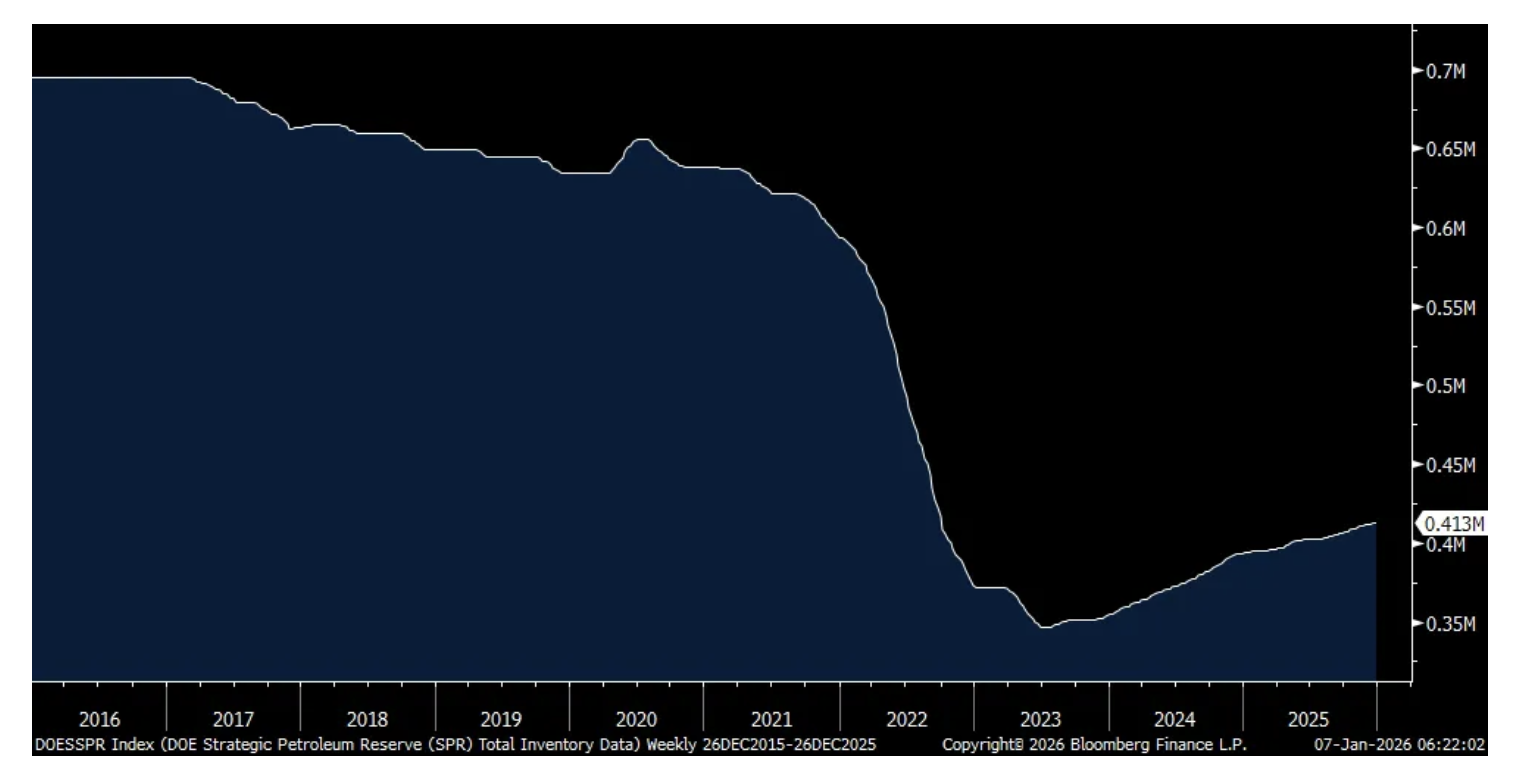

With any barrels of oil we get from Venezuela, I’d recommend we use it to fill the Strategic Petroleum Reserve which remains about 250 million barrels below the peak in 2020 before Biden tapped it to lower prices.

Strategic Petroleum Reserve in barrels

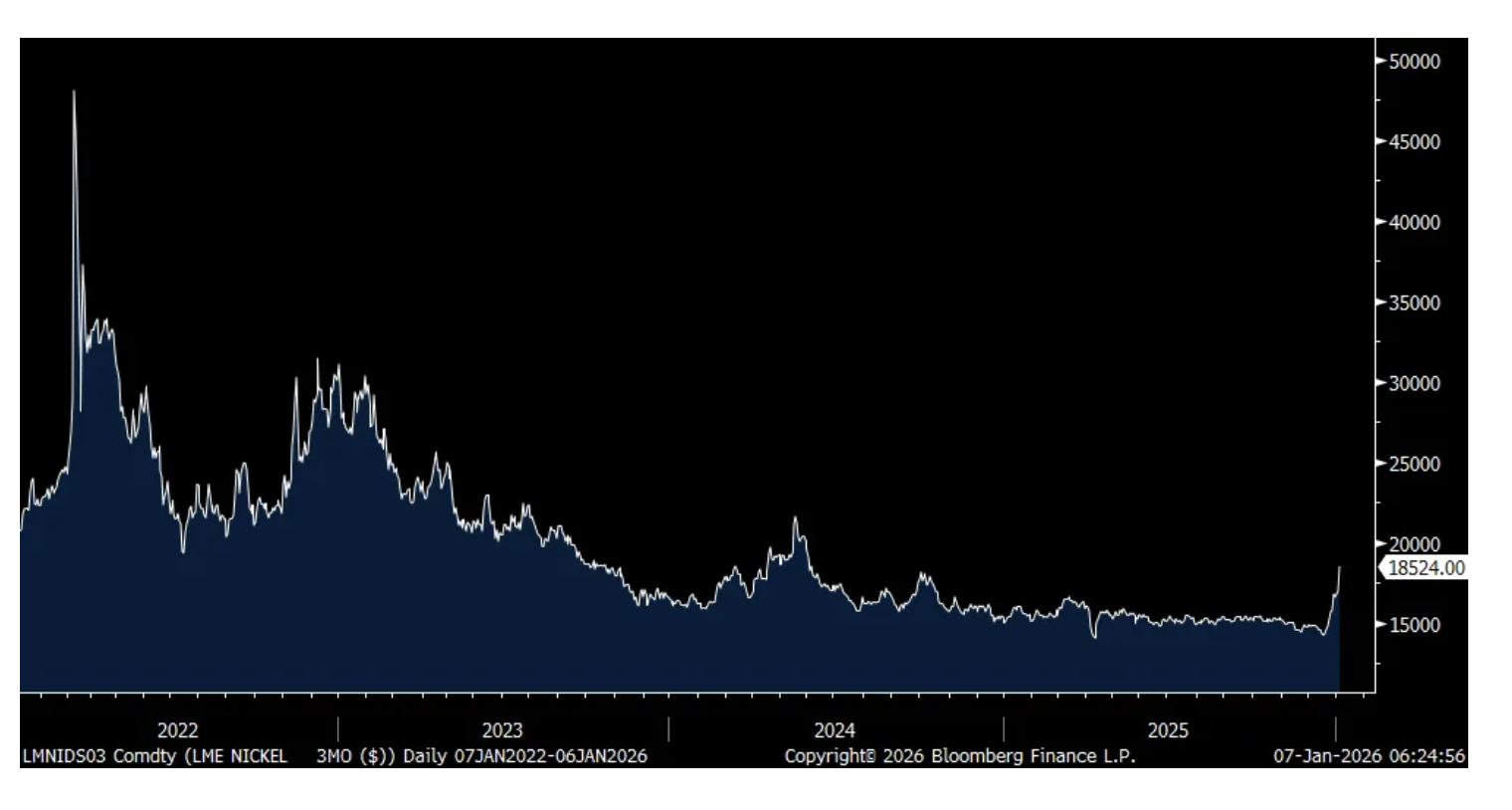

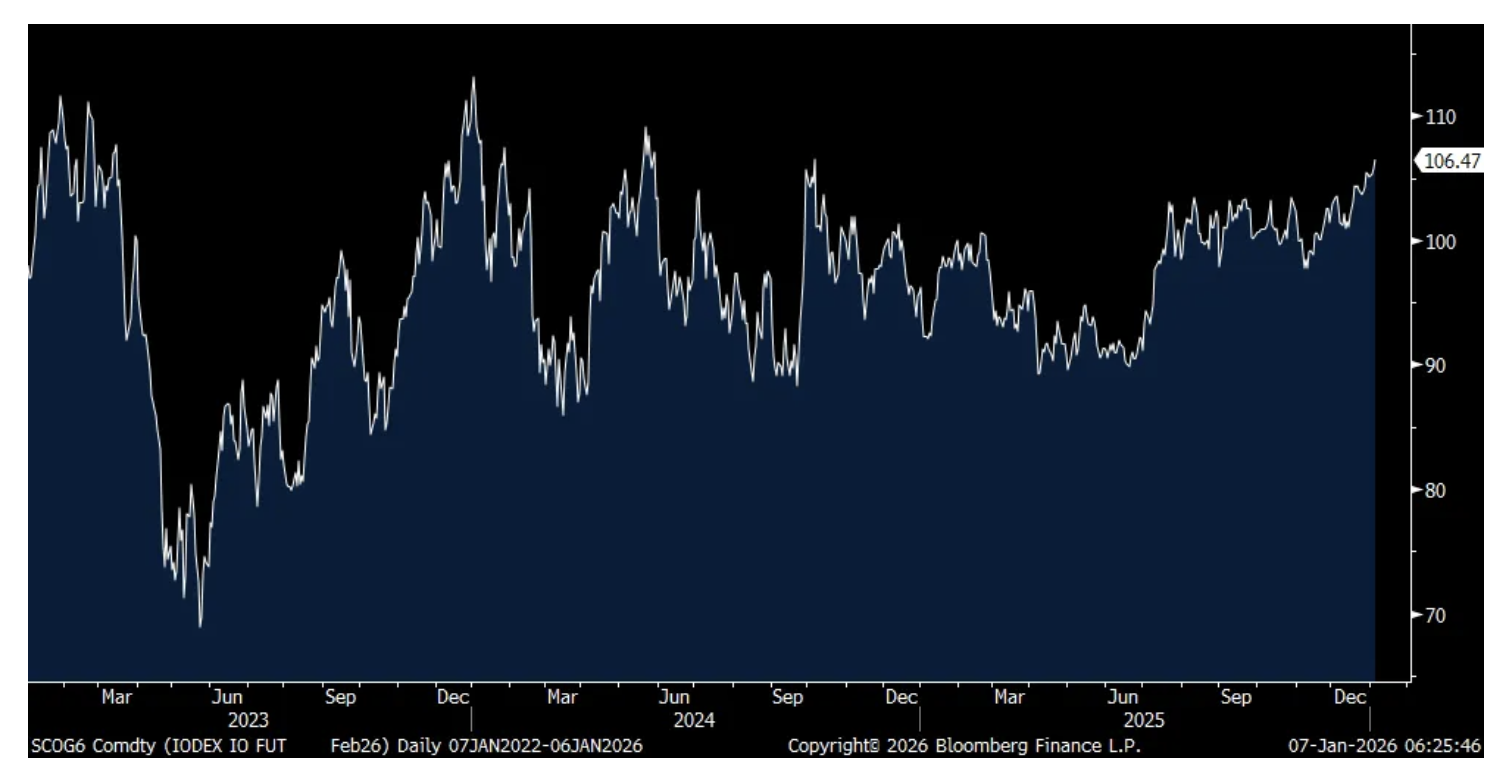

I mentioned Tuesday the highest close Monday in the CRB raw industrials index since August 2022 and which rose another .7% yesterday. Not included is nickel and in case you didn’t see, it rallied by 9% yesterday to the highest level since June 2024. Iron ore this morning is rising to a level last seen in May 2024.

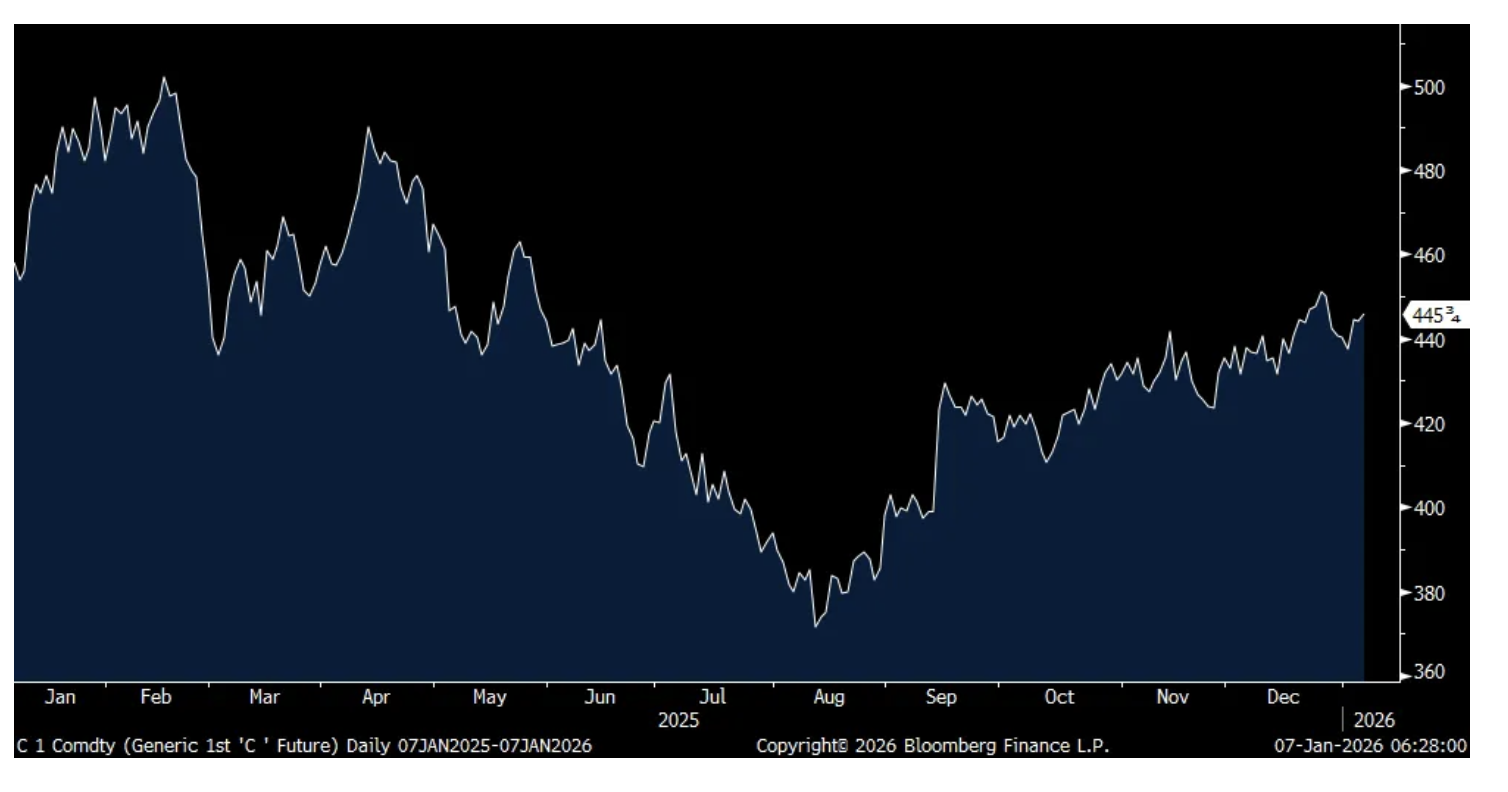

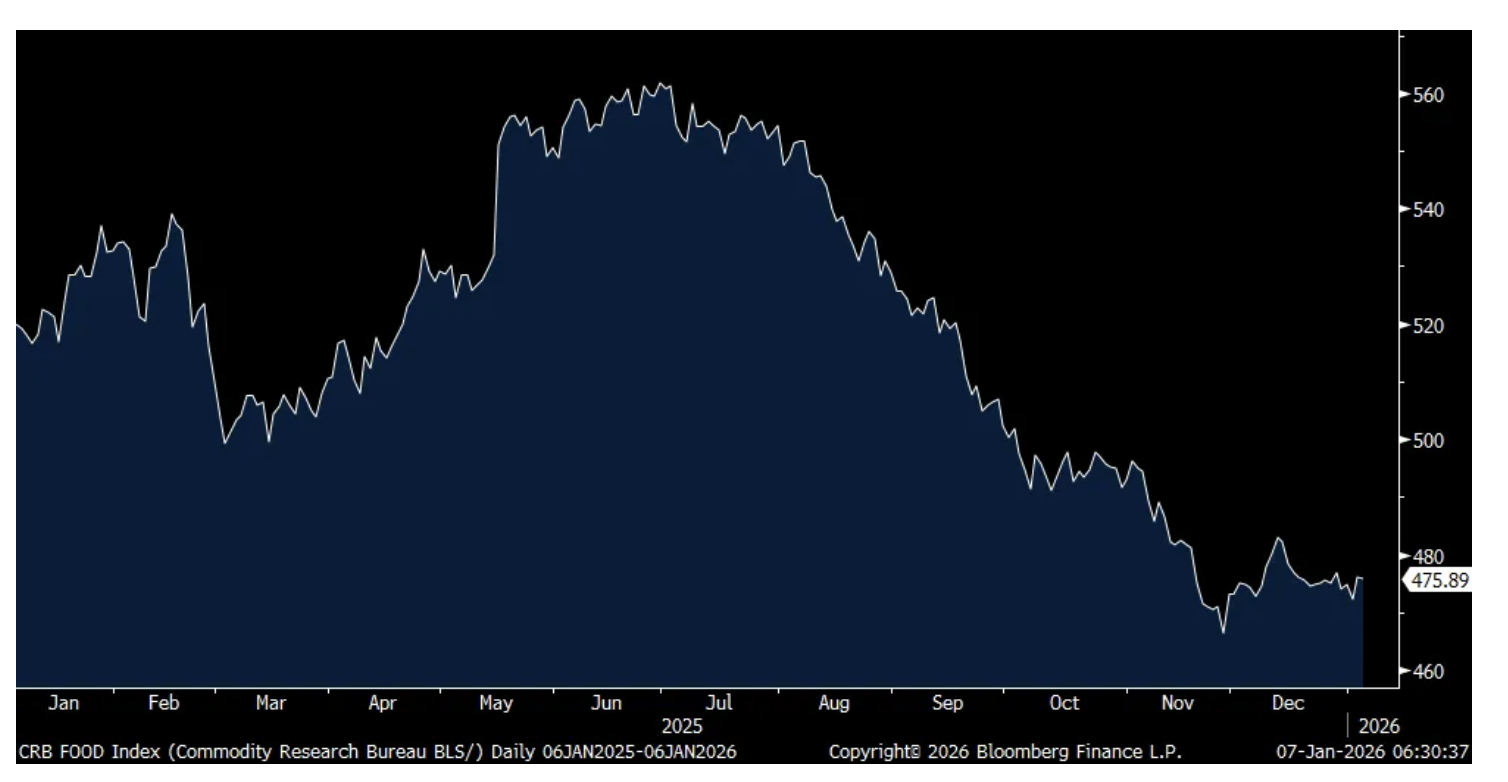

A bull market in industrial metals continues on and I eventually expect it to be joined by energy and agriculture. Corn by the way is just a nickel from the highest since May 2025. Soybeans are well off their November highs though at just over $10 a bushel. Wheat a year ago was $5.40 a bushel vs today’s level of $5.13. The CRB Food Stuff index is 15% off its 2025 peak of 560, currently at 476 as of yesterday’s close helped by the pullback in cocoa.

Our play on ag is owning some of the fertilizer stocks which are depressed but still paying generous dividend yields that are covered by cash flows.

Nickel

Iron Ore

Corn

CRB Food Stuff Index

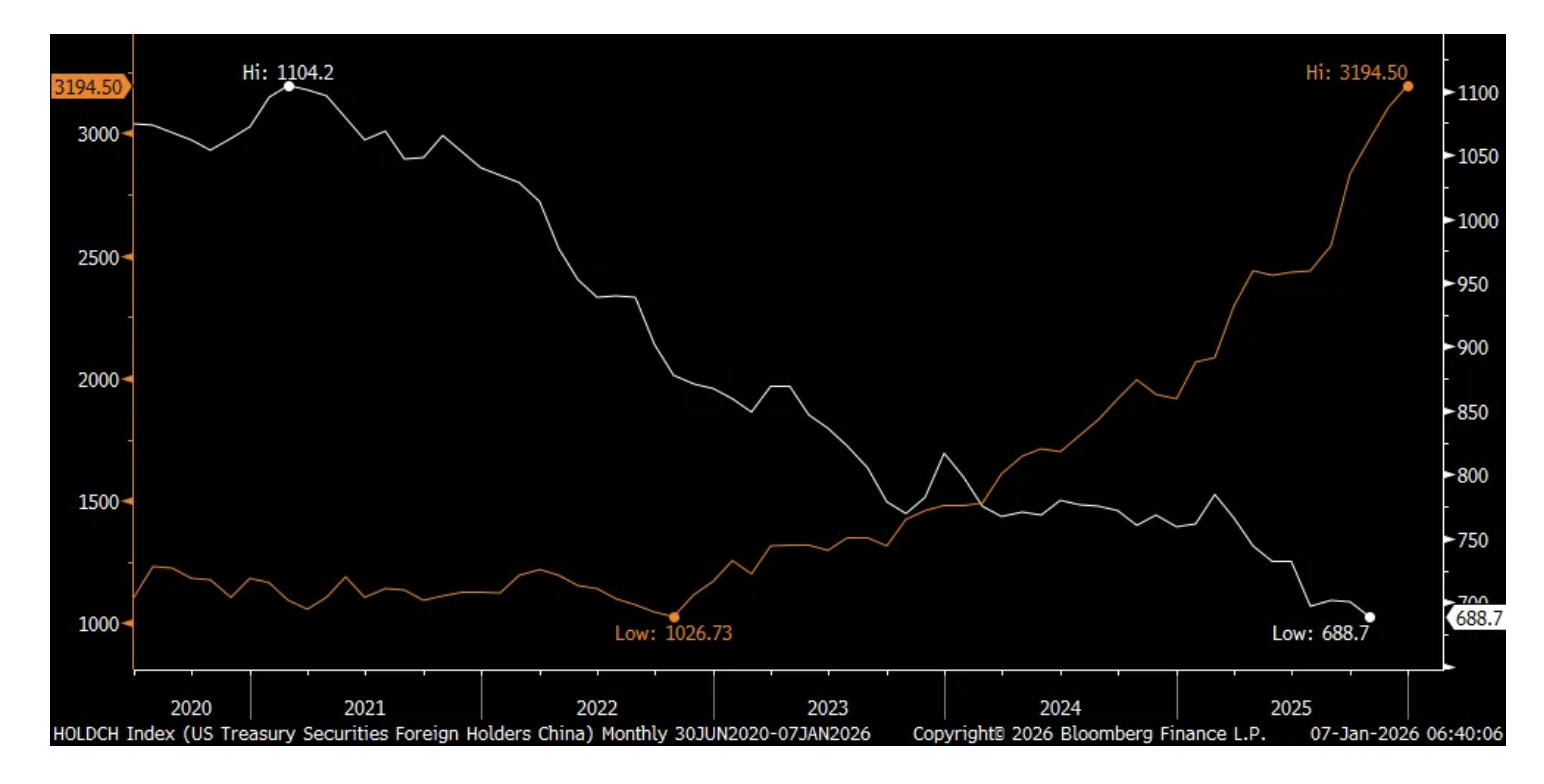

China further increased its holdings of gold in December and it continues to go in the opposite direction of their holdings of US Treasuries.

China gold holdings in orange as of Dec ($ value, tonnage & price)/US Treasury holdings in white as of Oct

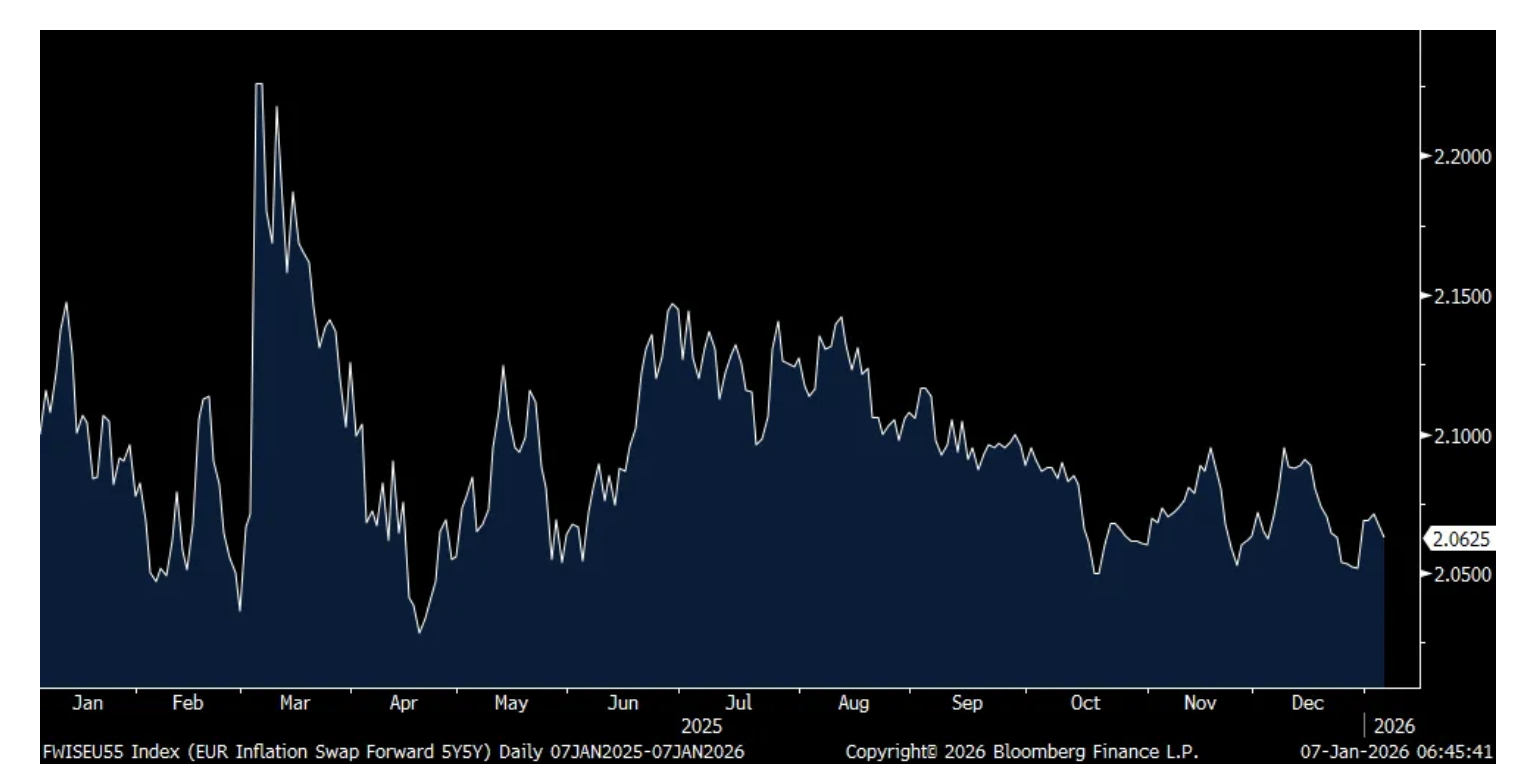

Eurozone December CPI rose 2% headline as expected vs 2.1% in November. The core rate was 2.3%, down one tenth too from November and one tenth less than expected. Lower energy prices has been the main reason for lower inflation as it fell 1.9% y/o/y. Also, non-energy goods prices were up just .4% y/o/y. Services inflation continues to be the pain point as it came in up 3.4% vs 3.5% in November and 3.4% in October.

With the data about as expected and the ECB deposit rate at a REAL rate of zero (though long term rates have risen), the 5 yr 5 yr euro inflation swap is unchanged this morning at 2.06%. Sovereign European bond yields are down across the board by 3-4 bps.

Australia reported its November CPI where the trimmed mean was up 3.2% as expected vs 3.3% in October. With an overnight cash target rate of 3.6%, the RBA will remain on hold with their more hawkish central bank Governor Michele Bullock. The Australian 2 yr yield was unchanged but the 10 yr yield slipped by 3 bps.

5 yr 5 yr Euro Inflation Swap

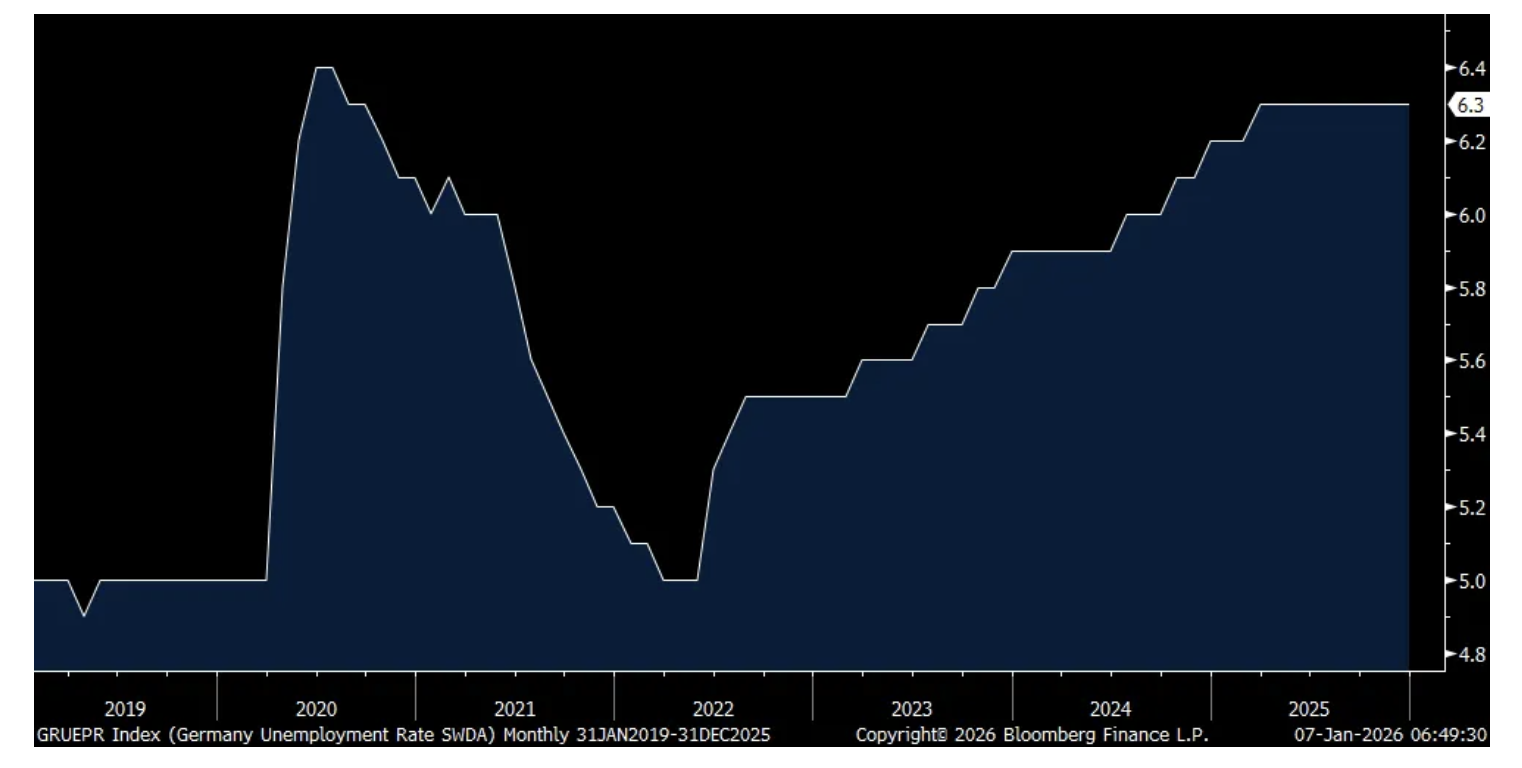

Also out of Europe today was the December German jobs data where the number of unemployed rose by 3k, less than the forecast of up 5k but vs up 1k in November. Their unemployment rate held at 6.3% which matches the highest since July 2020 in response to essentially no aggregate economic growth in the country last year with the main drag in manufacturing as we know. For perspective, it was at 5% in February 2020 pre Covid.

German retail sales in November were soft, down .6% m/o/m vs the estimate of up .2% but mostly offset by a 6 tenths upward revision to October.

German Unemployment Rate

BY Doug Kass · Jan 7, 2026, 9:50 AM EST

Shorted more (GS) (JPM) and (MS) on opening.

BY Doug Kass · Jan 7, 2026, 9:49 AM EST

From Peter Boockvar:

ADP said the private sector added a net 41k jobs in December, under the estimate of 50k and after a job loss of 29k in November. It was mostly businesses sized between 50-499 employees that led the job growth, hiring 34k. Small businesses have sharply slowed down their pace of hiring since April (tariffs to blame in part) but did add 9k in December after shedding 120k in November. Large businesses added just 2k people on net.

The services sector, again, contributed most of the jobs, and again in education/health services (+39k) and leisure and hospitality (+24k). Jobs were added too in trade/transportation/utilities and financial services. Jobs were lost in information and professional/business services. On the goods side, manufacturing lost another 5k while construction and natural resources/mining each added 1k.

With respect to pay, those ‘stayers’ saw a wage gain of 4.4% y/o/y, unchanged with November. ‘Job changers’ saw wage gains of 6.6% y/o/y, up from 6.3% in the month before. Both pretty good but did moderate as 2025 progressed.

Bottom line, smoothing out the monthly noise and we see hiring in the private sector has clearly slowed down. The 3 month average from ADP is now 20k vs the 6 month average 22k, the 12 month average of 51k and the 2024 job gain of 144k.

BY Doug Kass · Jan 7, 2026, 9:25 AM EST

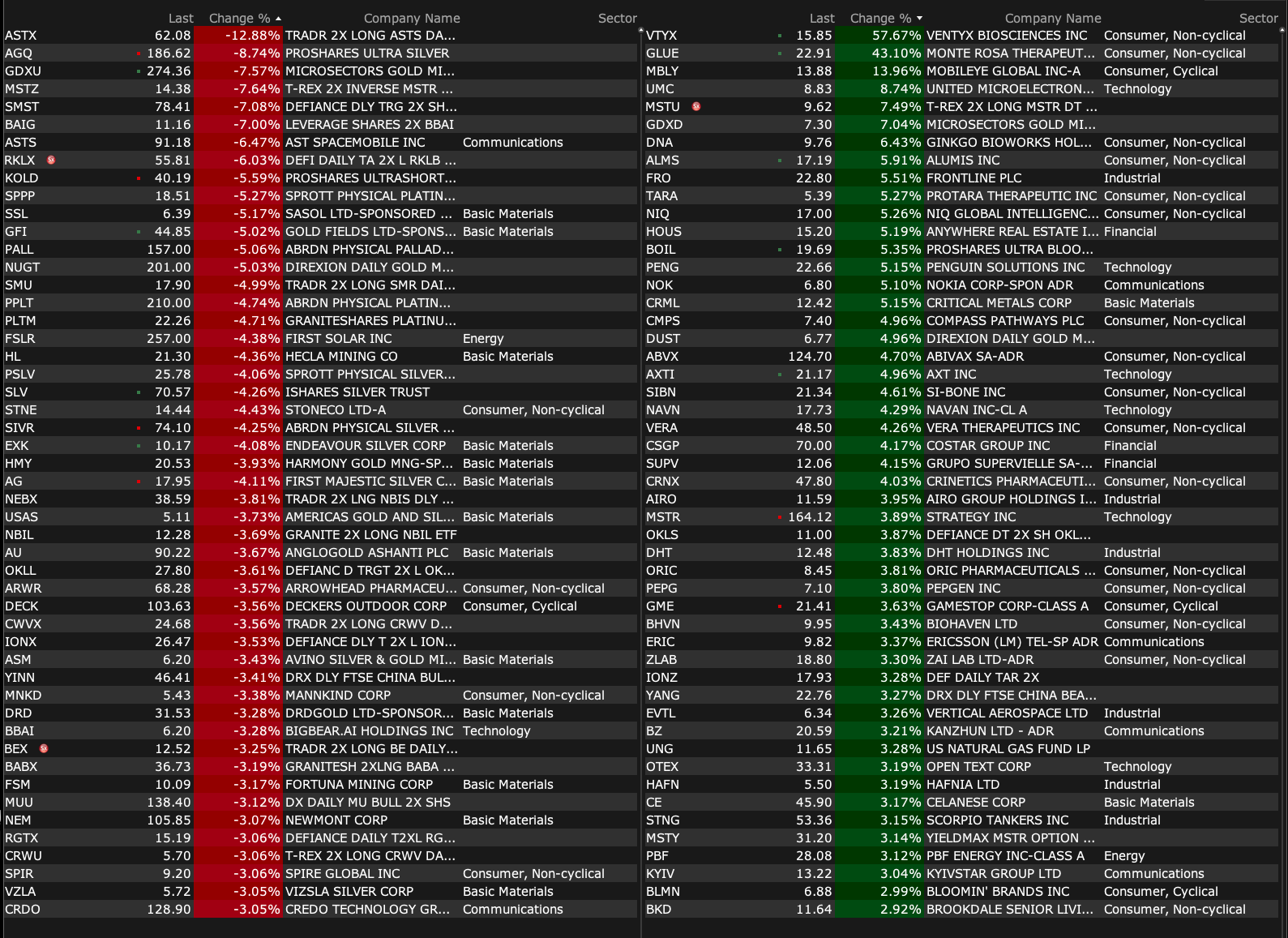

-VTYX +56% (momentum as reportedly company nears deal to be acquired by Eli Lilly for over $1B)

-GLUE +45% (announces Positive Interim Phase 1 Data of MRT-8102 Demonstrating Profound CRP Reductions in Elevated CVD-risk Subjects)

-MBLY +14% (to acquire Mentee Robotics for $900M to accelerate physical AI leadership)

-CDIO +10% (Cardio Diagnostics, Aimil Ltd. and Dr. Lal PathLabs Limited Partner to launch the PrecisionCHD Test in India)

-PENG +5.4% (earnings, guidance)

-VLO +5.2% (sales of Venezuela oil will continue indefinitely; Sanctions will be rolled back as part of agreement between Trump Administration and interim Venezuelan authorities)

-CRML +5.1% (approves, commences construction start-up in Greenland for Tanbreez Pilot Plant & Multi-Use Facilities)

-CSGP +4.2% (guidance; announces share buyback program)

-AIR +3.1% (earnings, guidance)

-INGN +3.1% (launches Aurora CPAP Masks for Obstructive Sleep Apnea in the US)

-VERA +3.0% (US FDA Granted Priority Review to Atacicept BLA for Treatment of Adults with IgA Nephropathy)

-W +2.6% (Barclays Raised W to Overweight from Equal Weight, price target: $123)

-REGN +2.3% (Tier1 firm Raised REGN to Buy from Underperform, price target: $860 from $627)

-EMAT -24% (downside momentum following closure of SPAC merger)

-APOG -14% (earnings, guidance; CFO resigns)

-UNF -5.0% (earnings, guidance)

-CLF -2.0% (Keybanc/Pacific Crest Cuts CLF to Sector Weight from Overweight)

-COMP -2.0% (files to sell $750M in convertible senior notes due 2031; revises guidance)

BY Doug Kass · Jan 7, 2026, 9:14 AM EST

BY Doug Kass · Jan 7, 2026, 8:55 AM EST

BY Doug Kass · Jan 7, 2026, 8:39 AM EST

11:30 a.m.: Treasury hosts a $69 billion 17-Week Bill Auction

4:10 p.m.: Fed Vice Chair for Supervision Bowman (Voter) speaks before the California Bankers Association 2026 Bank PresidentsSeminar (Virtual event. Speech topic, text, Q&A to be announced. Audio feed available)

BY Doug Kass · Jan 7, 2026, 8:20 AM EST

“Successful investing is having everyone agree with you... later.”

- Jim Grant

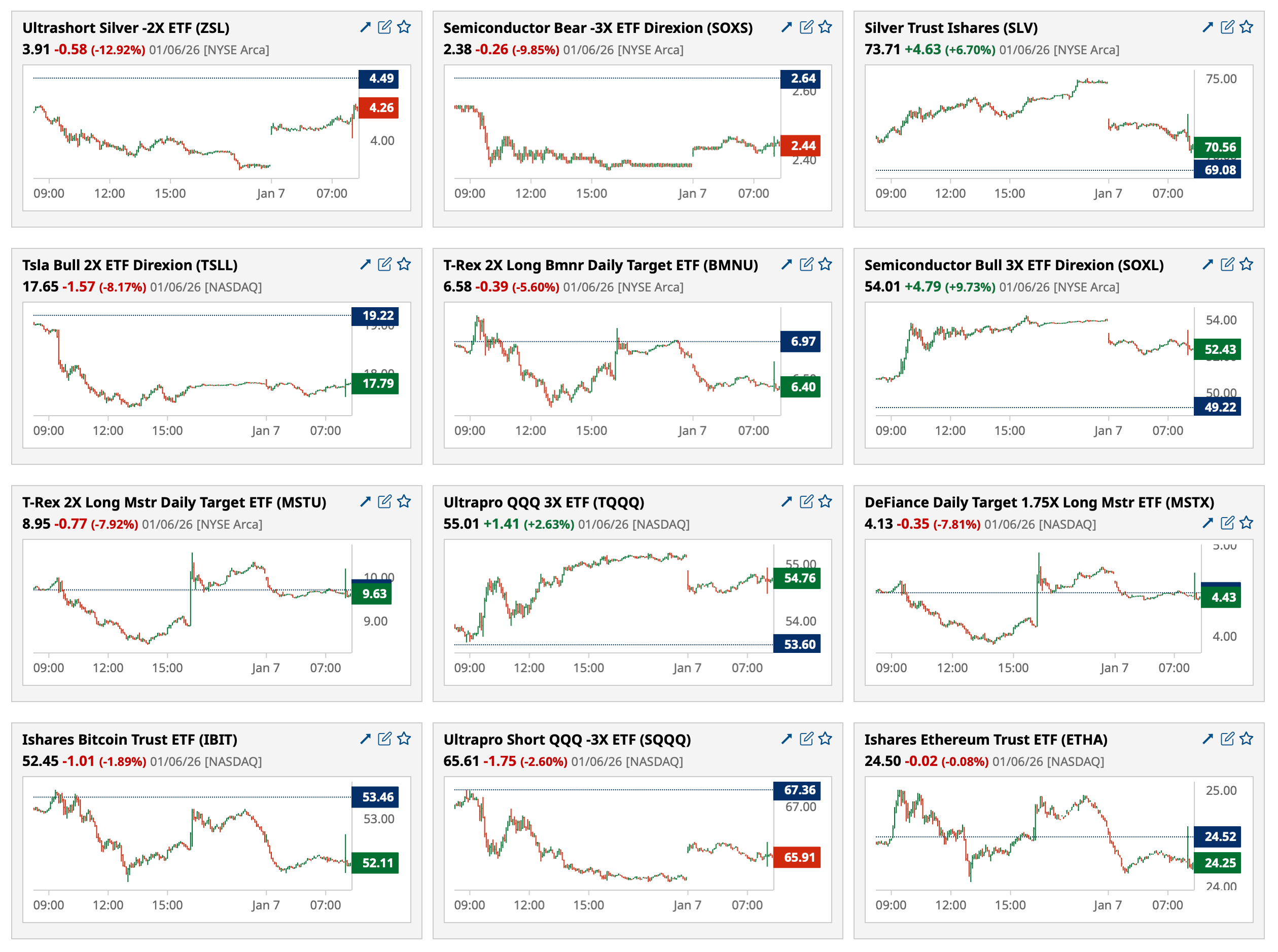

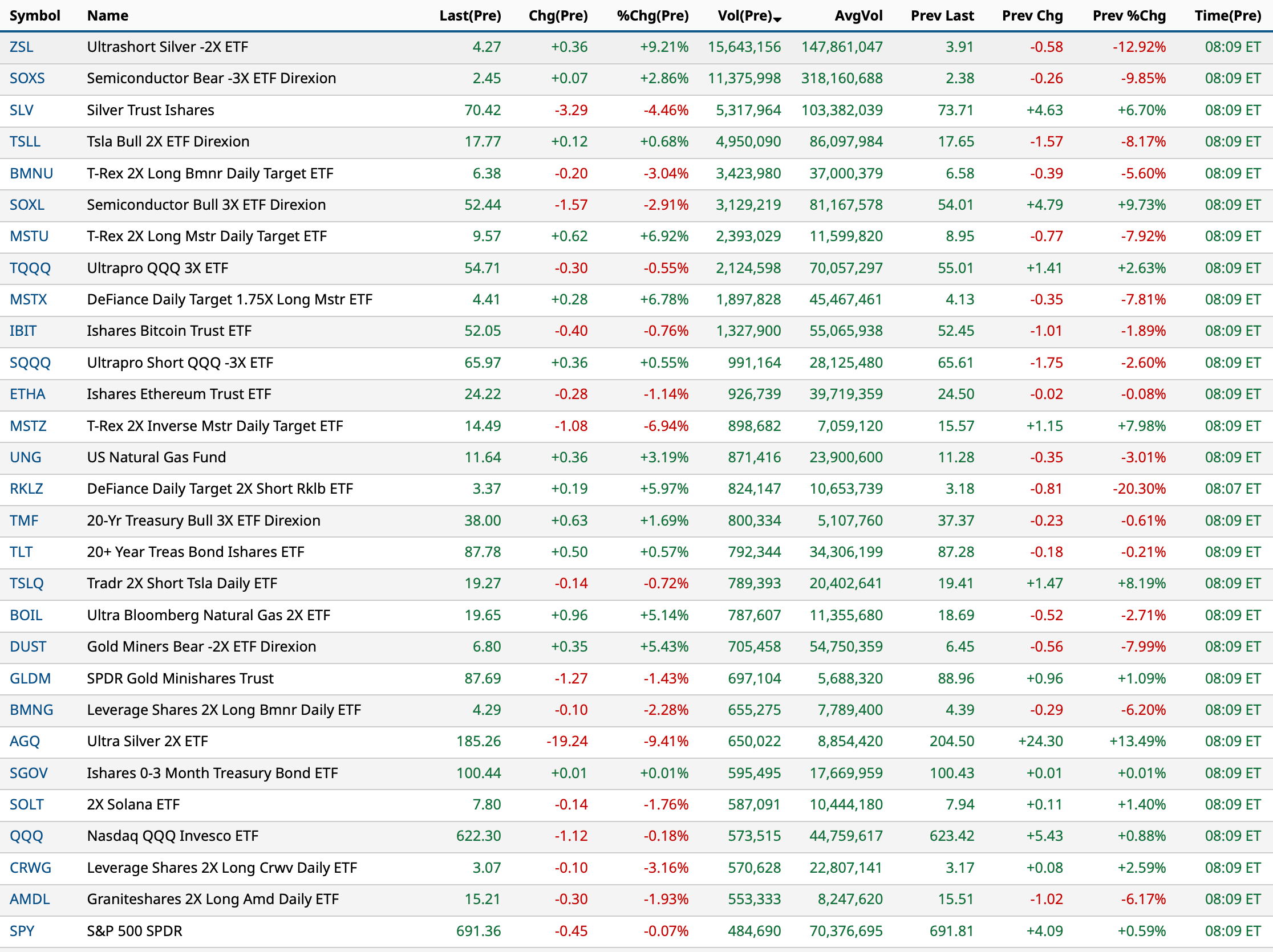

The last several trading days have been characterized by a further rise in global bond yields (turning the equity risk premium to an even larger discount), large intragroup action, disparate performance in Mag 7/Large-Cap Tech (Apple (AAPL) vs. Amazon (AMZN) yesterday), spastic and casino-like daily moves in individual stocks (e.g. Micron (MU) ) and in precious metals ( (SLV) , (GLD) and (PPLT) ), short squeezes in heavily shorted stocks and extreme bullish investor sentiment (my CNBC Blather Index has 32 CNBC bulls and 1 bear in the last week).

This has all occurred against a backdrop of unsettling geopolitical events and foreign policy that would typically weight on equities — but algorithms and new money into the markets (in a new year) have countered rising geopolitical risks.

As for me, it looks to be the beginning of the end of a maturing bull market.

I have raised my short exposure accordingly.

BY Doug Kass · Jan 7, 2026, 8:00 AM EST

BY Doug Kass · Jan 7, 2026, 7:48 AM EST

BY Doug Kass · Jan 7, 2026, 7:25 AM EST

Wolf Street howls about the auto industry's woes.

BY Doug Kass · Jan 7, 2026, 7:15 AM EST

From JPMorgan:

US: Futs are weaker as markets pause ahead of a series of US labor and econ momentum data. Pre-mkt, bond are bid with yields down 2-4bp as the curve flattens; USD is unchanged. TMT is underperforming with most Mag7 and Semis names lower with Energy, HC, and Staples rallying pre-mkt. In cmdtys, Ags are the bright spot as we see some profit-taking in Metals and crude is under pressure as Trump says that Venezuela will send 30mm – 50mm barrels of sanctioned oil to the US where sales proceeds are expected to be split between the two countries.

and...

US MKT INTEL’S NFP SCENARIO ANALYSIS

Feroli’s full NFP preview is here. He sees 75k jobs being added, above the Street’s estimate of 59k; November printed 64k jobs. For the unemployment rate (U.3) he sees 4.6%, above the Street’s estimate; prior print was 4.564% (rounds to 4.6%). For Average Hourly Earnings, he sees +0.3% MoM and +3.6% YoY.

The following scenario analysis is NOT A PRODUCT OF JPM RESEARCH, this is a trading desk view from JPM US Market Intelligence.

· [5%] Above 105k. SPX is down 0.5% – 1%

· [25%] Between 75k – 100k. SPX gains 0.25% to 1%

· [40%] Between 35k – 75k. SPX gains 0.25% – 0.75%

· [25%] Between 0k – 35k. SPX loses 0.25% to gains 0.5%

· [5%] Below 0k. SPX is down 0.5% to 1.25%

· WHAT ARE OPTIONS PRICING? For options expiring on January 9, the market is pricing ~1.2% move, as of market close on Jan 2.

· US MKT INTEL ON NFP – We look for an inline to slightly stronger print. After hitting what was thought to be a soft patch in the economy late summer / Q3, it was thought that we would see hiring resume. Well, the economy never saw that dip with Q3 GDP printing 4.3% and Q2 3.8%. This consumer-led expansion has been peculiar due to a lack of hiring as spending / growth accelerated higher. Now, do we see hiring return adding more support to a stronger than average aggregate consumer? The NFIB Small Business Survey’s Hiring Sub-index has acted as a leading indicator for NFP, typically establishing a trend 1-2 months ahead of the official NFP prints. That sub-index has been trending higher since this summer (see below). This may not be reflected in this week’s print, but we look for the trend to point toward accelerated hiring. It remains to be seen if this resumption in hiring will add an inflationary impulse.

BY Doug Kass · Jan 7, 2026, 7:00 AM EST

BY Doug Kass · Jan 7, 2026, 6:45 AM EST

BY Doug Kass · Jan 7, 2026, 6:30 AM EST

BY Doug Kass · Jan 7, 2026, 6:15 AM EST

Gary Marcus weighs in on Yann LeCun's departure from Meta (META) .

BY Doug Kass · Jan 7, 2026, 6:05 AM EST

BY Doug Kass · Jan 7, 2026, 5:55 AM EST

The S&P Short Range Oscillator is inching up to a further overbought level at 2.40% vs. 1.63%.

BY Doug Kass · Jan 7, 2026, 5:45 AM EST