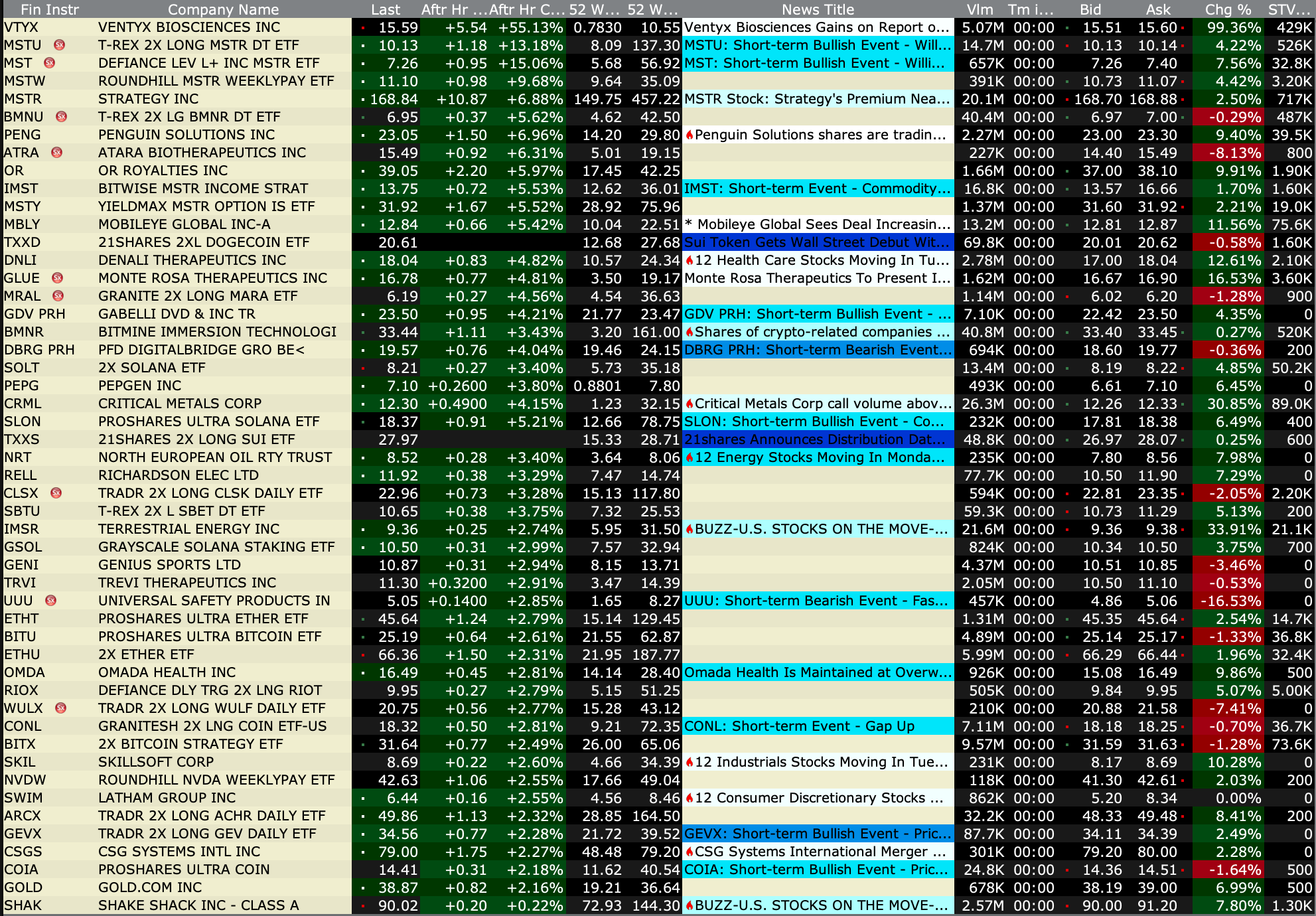

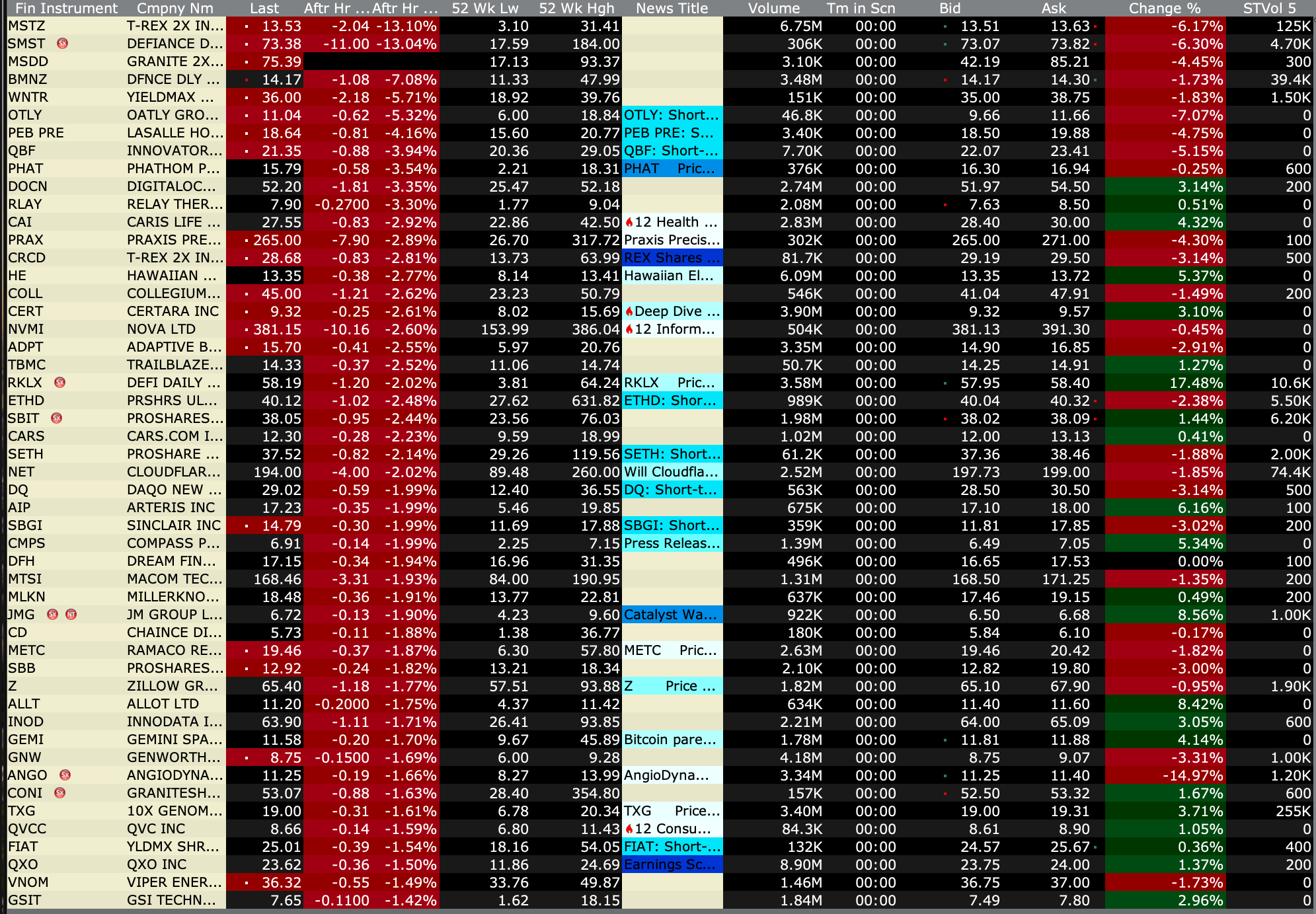

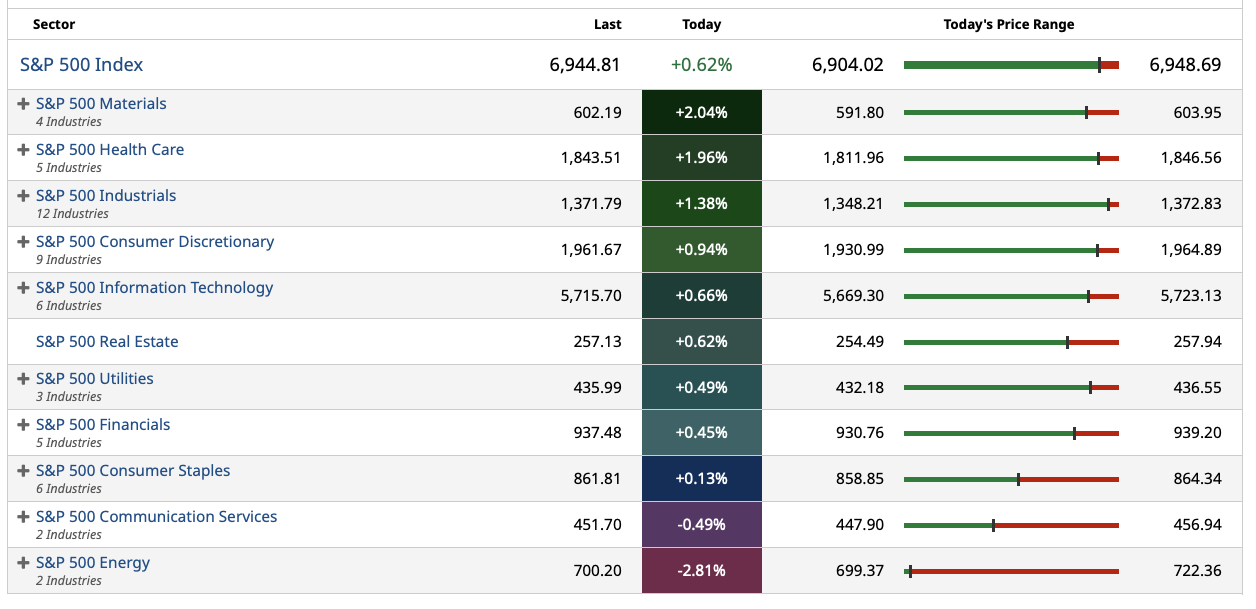

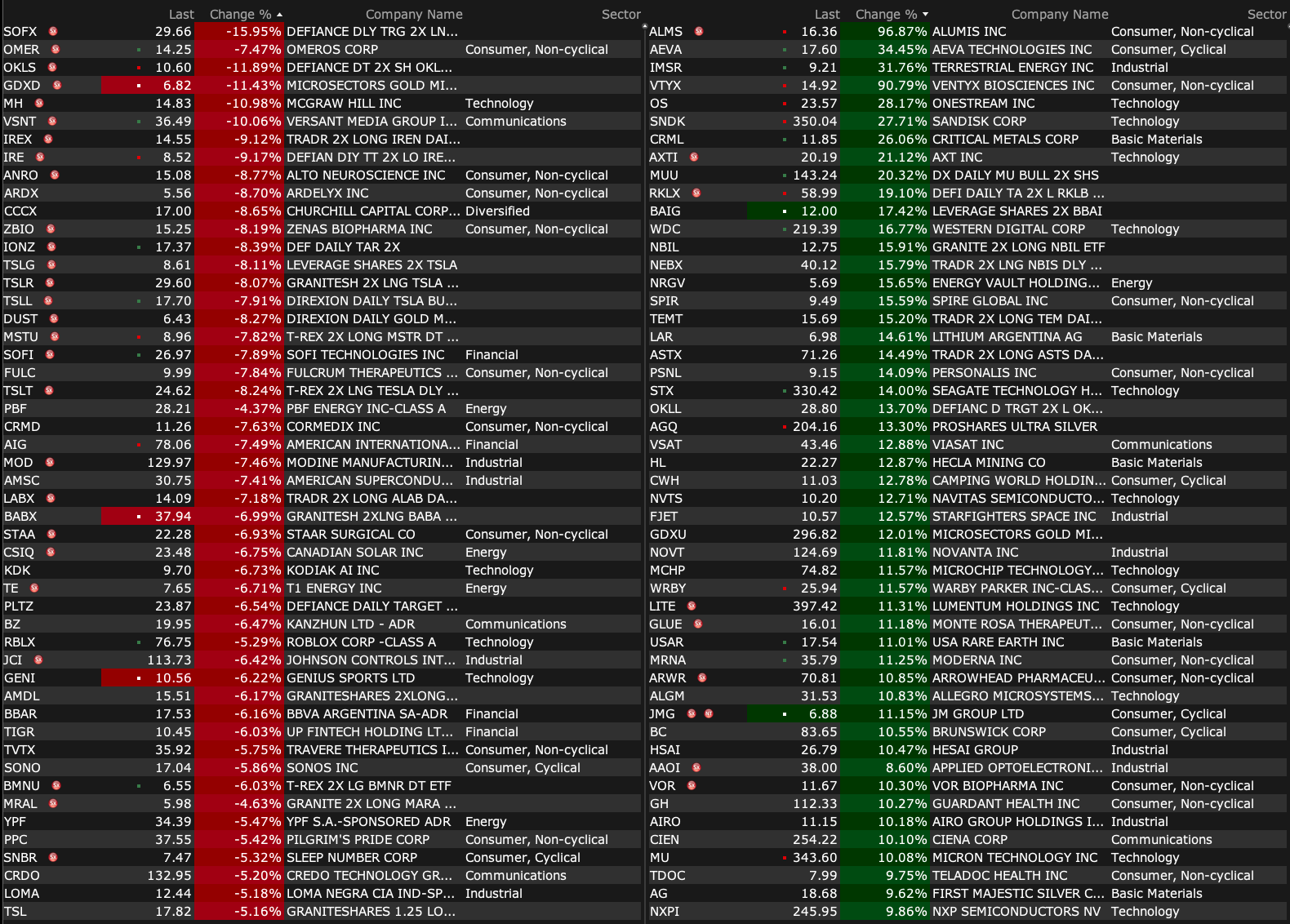

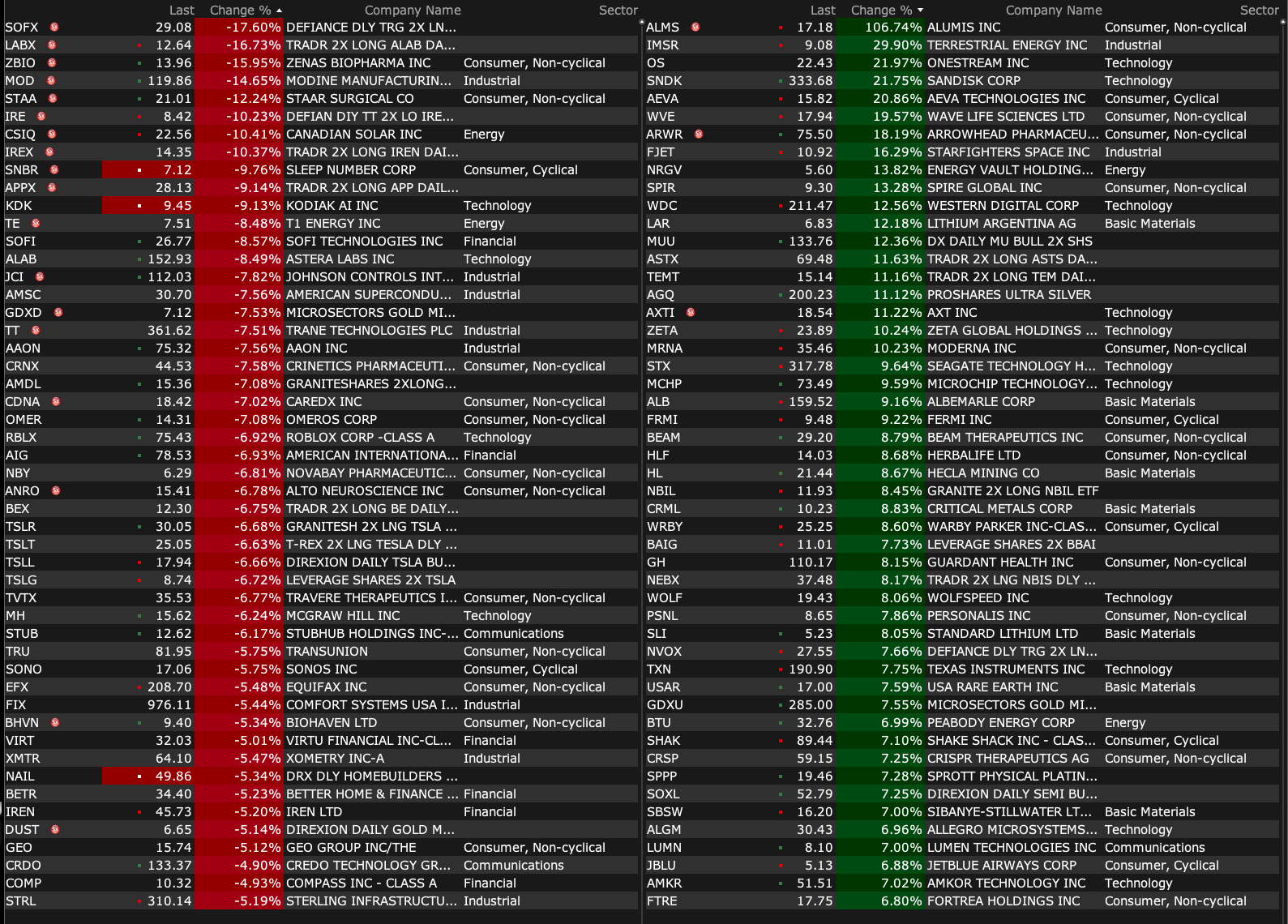

After-Hours Gainers, Losers

After-Hours % Gainers

After-Hours % Losers

BY Doug Kass · Jan 6, 2026, 5:10 PM EST

BY Doug Kass · Jan 6, 2026, 5:10 PM EST

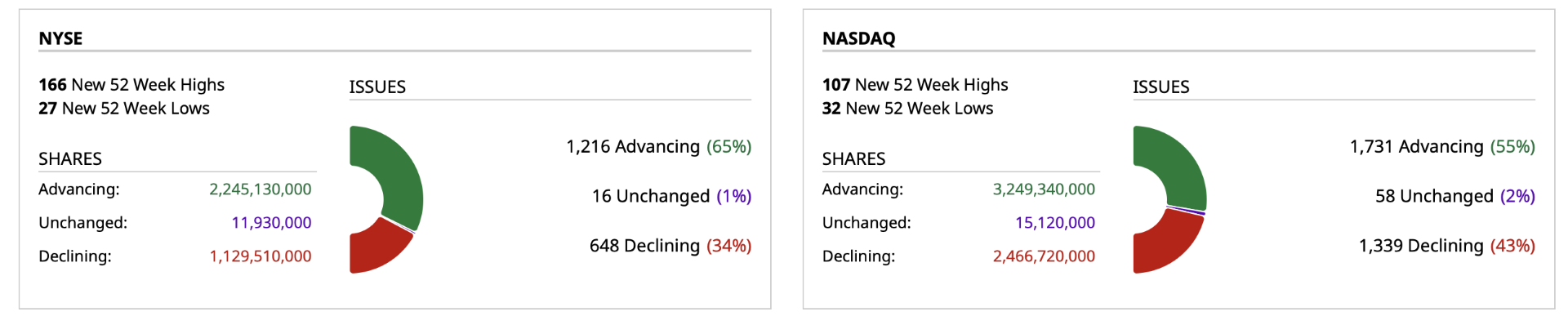

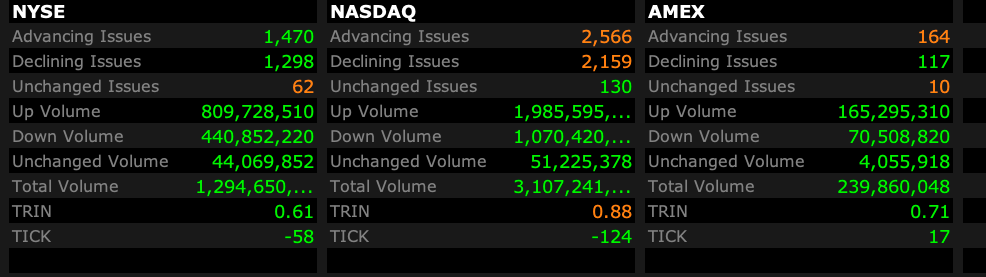

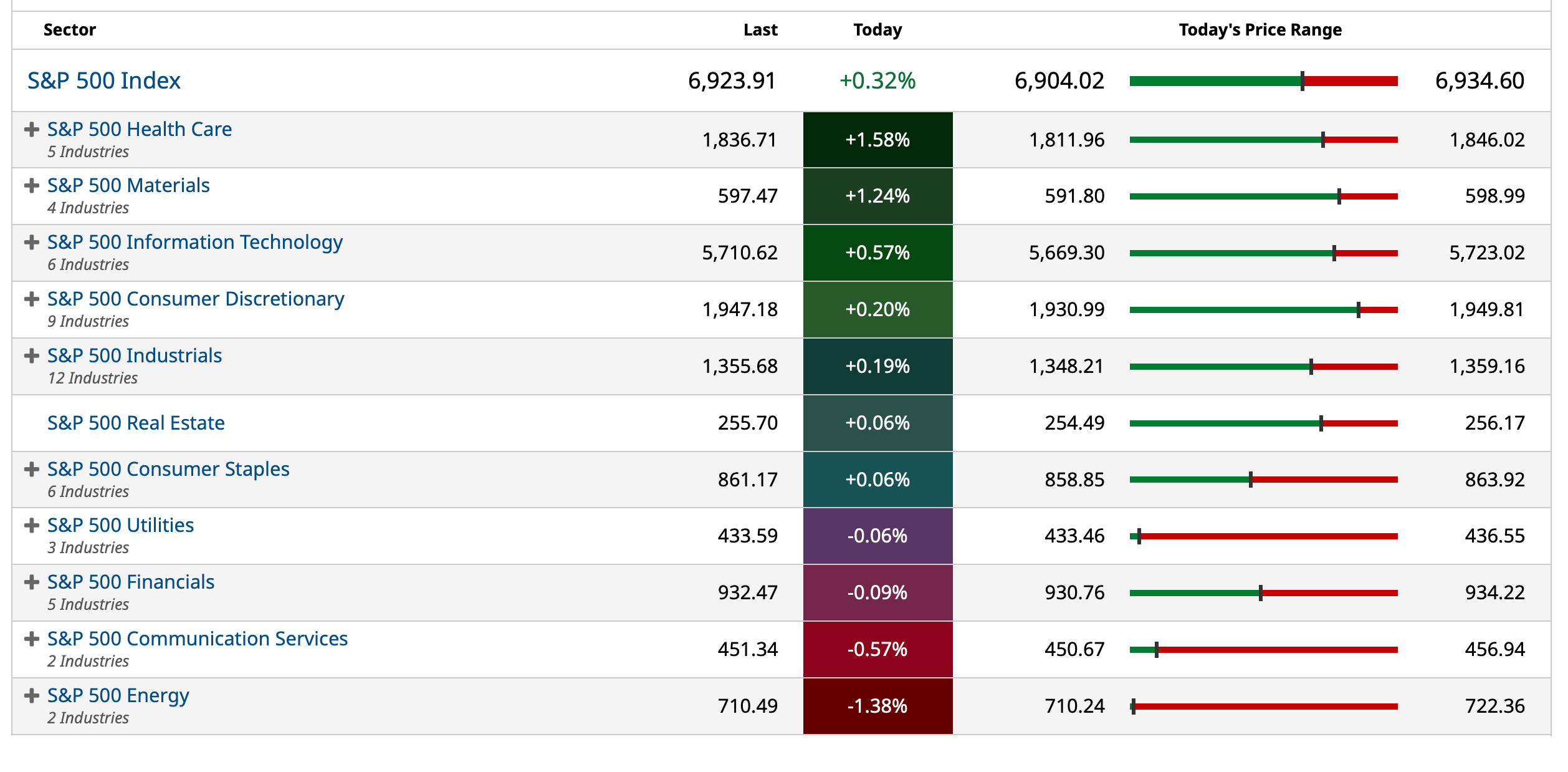

- NYSE volume 21% above its one-month average;

- NASDAQ volume 18% above its one-month average;

- VIX index: down 1.07% to 14.74

BY Doug Kass · Jan 6, 2026, 5:00 PM EST

Wolf Street howls about Japan's central bank's balance sheet.

BY Doug Kass · Jan 6, 2026, 3:33 PM EST

BY Doug Kass · Jan 6, 2026, 2:55 PM EST

Nothing to worry about here..

BY Doug Kass · Jan 6, 2026, 2:44 PM EST

No trades since things.

BY Doug Kass · Jan 6, 2026, 2:33 PM EST

From Randorama on (PEP) (a dog with fleas):

Randy

PepsiCo Announces Industry-First AI and Digital Twin Collaboration with Siemens and NVIDIA

Together, PepsiCo(PEP), Siemens, and NVIDIA will set a new standard for scalable, technically sound digital twin and AI in industrial operations.

BY Doug Kass · Jan 6, 2026, 12:55 PM EST

I have converted my short (SPY) common to short calls.

BY Doug Kass · Jan 6, 2026, 12:02 PM EST

- NYSE volume 26% above its one-month average;

- Nasdaq volume 13% above its one-month average;

- VIX index: up 0.47% to 14.97

BY Doug Kass · Jan 6, 2026, 11:20 AM EST

New multi-week low in (TLT) (and high in intermediate yields).

This means that the equity risk premium (now at a discount) - moves to an even greater discount.

BY Doug Kass · Jan 6, 2026, 10:47 AM EST

BY Doug Kass · Jan 6, 2026, 10:21 AM EST

Here are today's things:

* Added to (SPY) short at $687.82.

* Added to (GS) $952.31 JOET $42.87 and MS $187.53shorts.

* Added to (PEP) $139.74, PG $140.34 and KMB $97.86 longs

BY Doug Kass · Jan 6, 2026, 9:46 AM EST

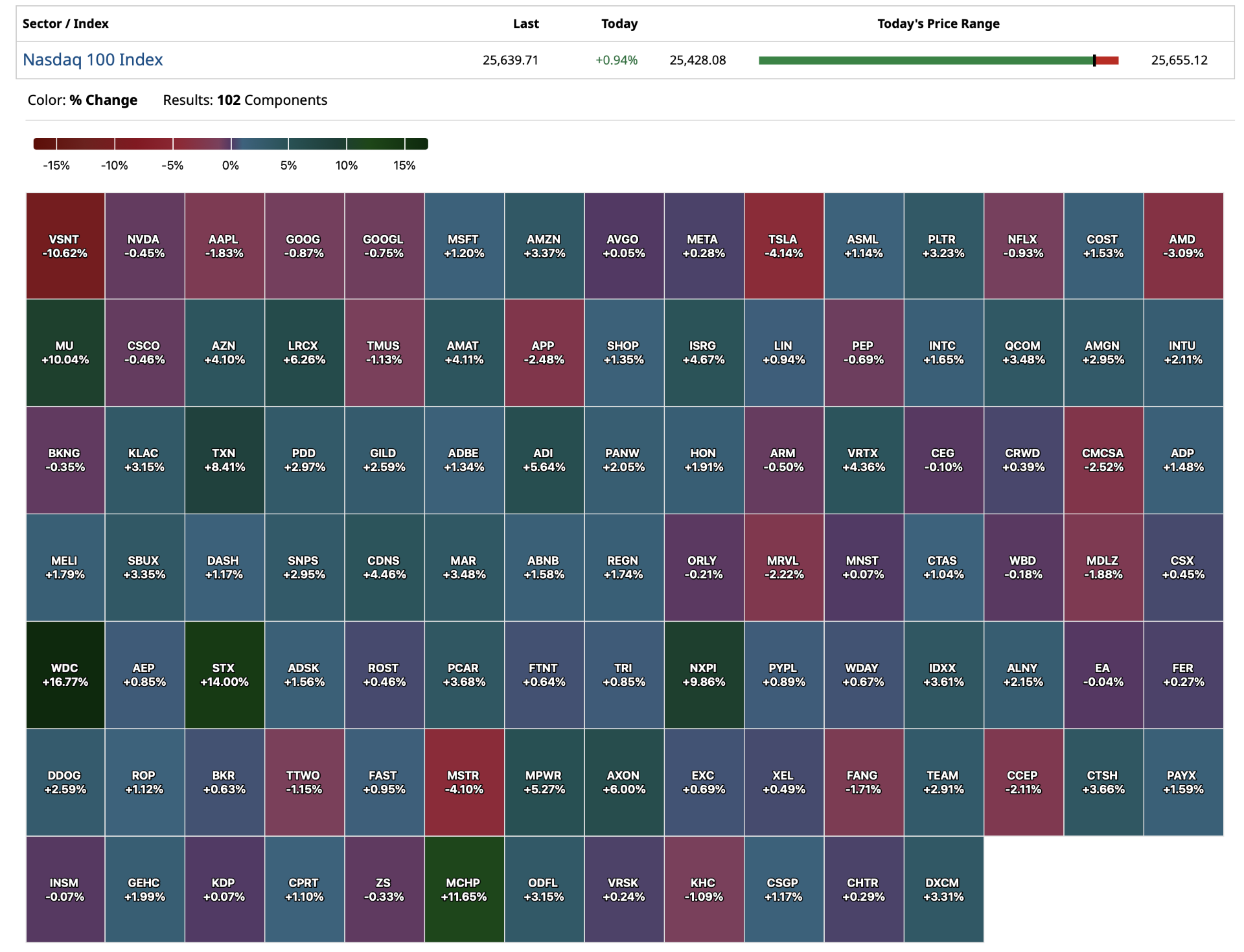

-ALMS +92% (Envudeucitinib delivers leading Skin clearance among next-generation Oral Plaque Psoriasis Therapies in Phase 3 Program)

-CYCN +57% (announces Strategic Agreement with Medsteer and Progress Toward Initiating Phase 2 Proof-of-Concept Study for CYC-126 in Treatment-Resistant Depression in 2H26)

-AZI +35% (Autozi and China Auto Maintenance Parts Alliance forge strategic partnership)

-OS +29% (reportedly buyout firm HG nears deal to take OneStream private)

-AEVA +24% (Aeva and NVIDIA to Integrate 4D LiDAR as Reference Sensor within the NVIDIA DRIVE Hyperion Platform Ecosystem)

-IMSR +19% (executes DOE Agreement for Project TETRA Under Advanced Reactor Pilot Program)

-ARWR +13% (announces Interim Clinical Data on RNAi-based Obesity Candidates Showing Weight Loss in Obese Patients with Diabetes and Improved Measures of Body Composition)

-INVZ +13% (announces integration of its InnovizSMARTer LiDAR with NVIDIA Jetson Orin Nano)

-OCS +11% (granted US FDA breakthrough therapy designation to Privosegtor for treatment of optic neuritis)

-NBP +8.7% (presents positive Givastomig dose expansion from Phase 1b combination study in patients with 1L metastatic gastric cancer)

-HSAI +6.5% (Nvidia said to name Hesai as a new tier 1 supplier for DRIVE Hyperion ecosystem)

-COHU +5.6% (Needham Raised COHU to Buy from Hold, price target: $30)

-ATOS +5.3% (FDA clears study for (Z)-endoxifen in metastatic breast cancer)

-UA +4.9% (Fairfax Financial discloses 22.2% stake v prior disclosed 16.1% stake)

-ANGO +4.3% (earnings, guidance; CEO to retire)

-VST +4.3% (Quantum Capital Group announces sale of Cogentrix to Vistra for ~$4.7B)

-MCHP +4.1% (raises guidance)

-CERT +3.8% (Leerink Partners Raised CERT to Outperform from Market Perform, price target: $13)

-CORZ +3.8% (BTIG Raised CORZ to Buy from Neutral, price target: $23)

-OI +3.7% (Wells Fargo Raised OI to Overweight from Equal Weight, price target: $18)

-RGNT +3.7% (appoints new CEO; GelrinC Establishes Long-Term Durability of Cartilage Repair through Quantitative MOCART Evaluation)

-ALKS +3.3% (Alixorexton Granted Breakthrough Therapy Designation by U.S. FDA for the Treatment of Narcolepsy Type 1)

-BALL +3.1% (multiple broker upgrades)

-AVXL +2.8% (receives FDA feedback on Alzheimer’s disease program; to submit existing data from Phase IIb/III ANAVEX2-73-AD-004 program)

-CRWV +2.3% (extends Its Cloud Platform with NVIDIA Rubin Platform; expected to be among the first cloud providers to deploy the NVIDIA Rubin platform in the second half of 2026)

-SHAK +2.2% (Deutsche Bank Raised SHAK to Buy from Hold, price target: $105)

-AIG -4.6% (appoints Eric Andersen as CEO, effective mid-2026; Peter Zaffino has informed the AIG Board of Directors that he intends to transition to Executive Chair of AIG and retire as CEO)

-DHI -1.5% (Wells Fargo Cuts DHI to Equal Weight from Overweight, price target: $155)

BY Doug Kass · Jan 6, 2026, 9:21 AM EST

BY Doug Kass · Jan 6, 2026, 9:10 AM EST

BY Doug Kass · Jan 6, 2026, 8:55 AM EST

Fed Speakers

8:25 a.m.: Fed Bank of Richmond President Barkin (Non-Voter) will speak at the Raleigh Chamber Economic Forecast 2026, Raleigh,NC (Embargoed text, audience Q&A expected)

Auctions:

11 a.m.: Treasury Announces a 4, 8 and 17-Week Bill Auction;

11:30 a.m.: Treasury hosts a $75B 6-Week Bill Auction

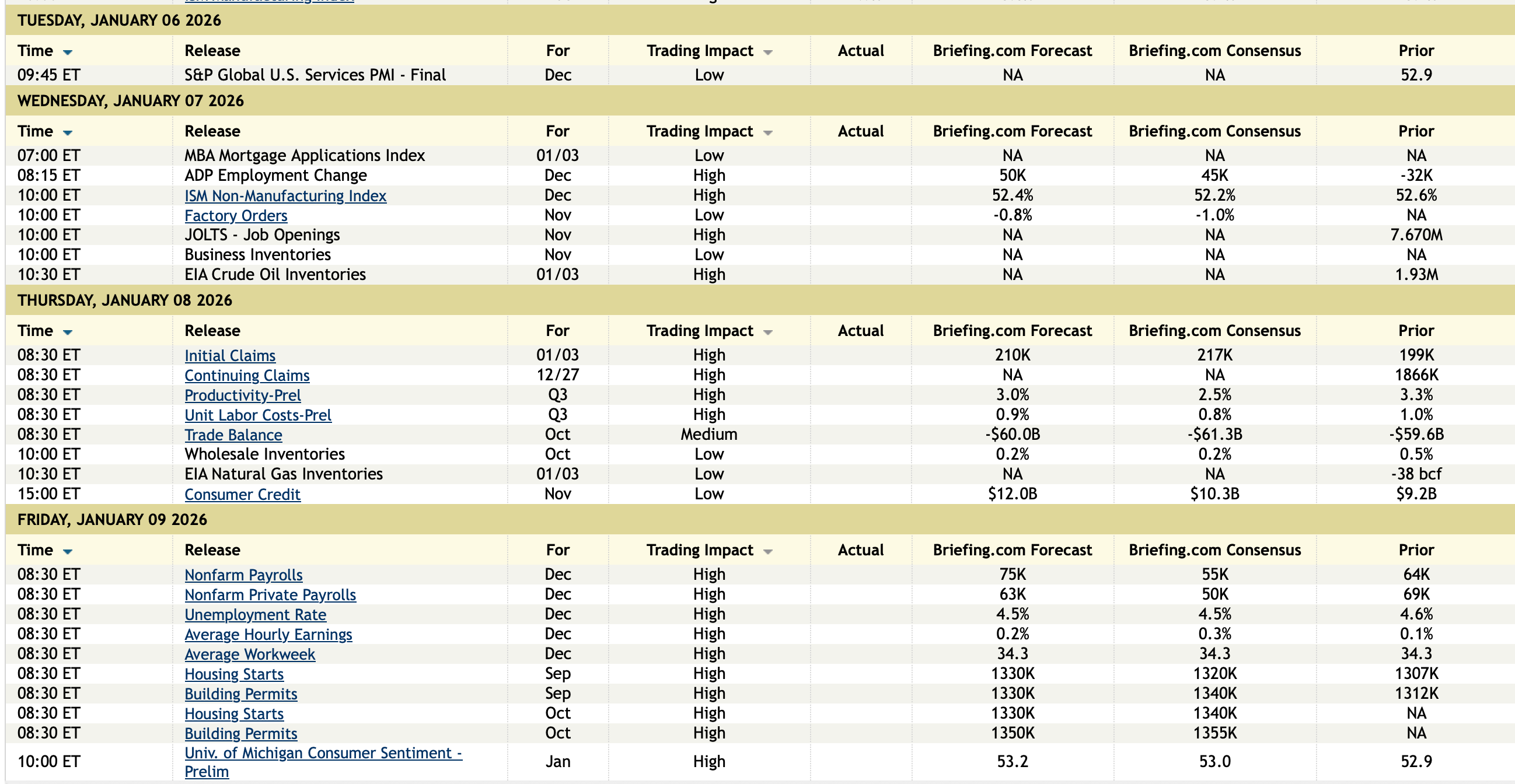

Economic Calendar

BY Doug Kass · Jan 6, 2026, 8:46 AM EST

From Peter Boockvar:

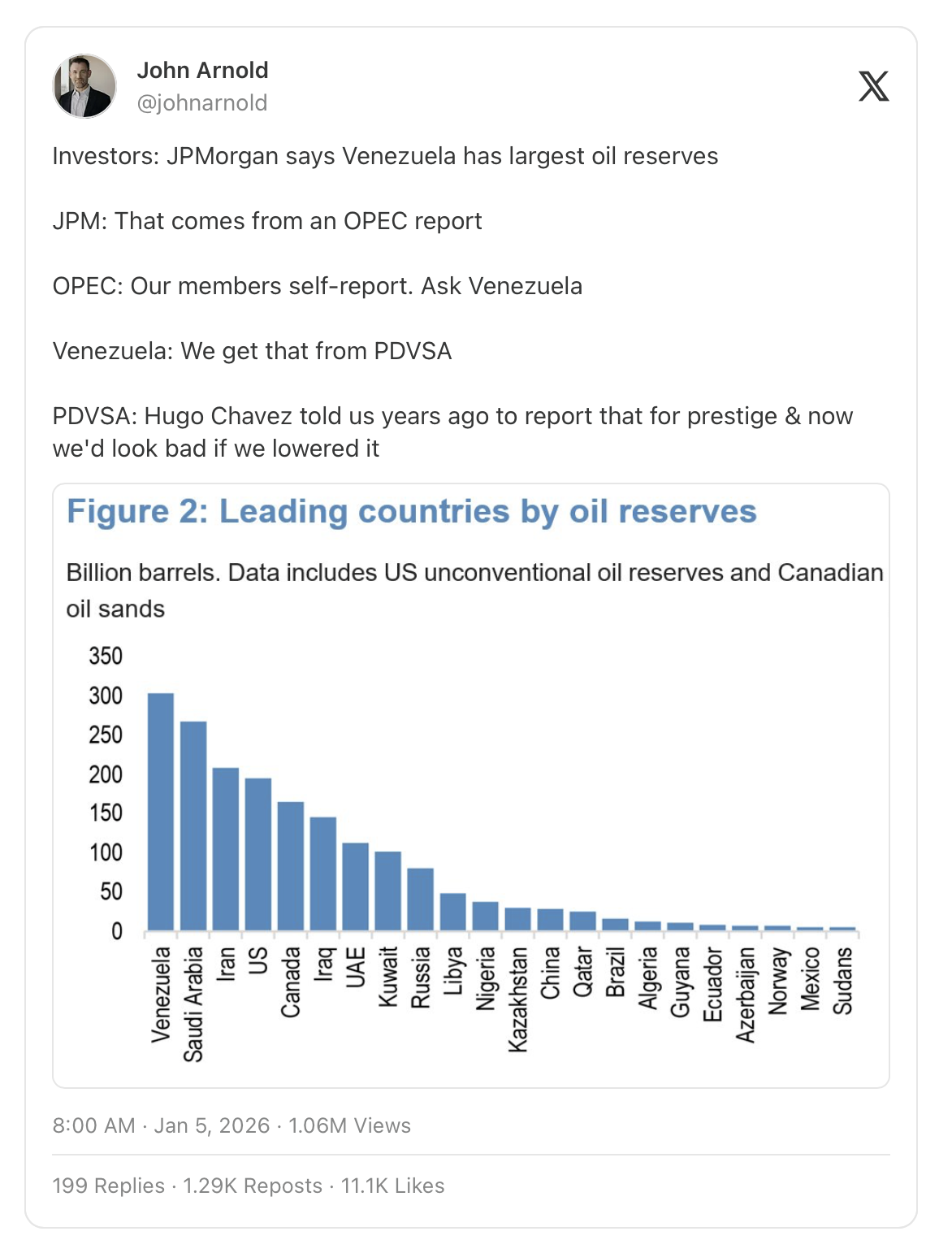

Not that it matters right now as it will take 5-10 years to really ramp up Venezuelan oil production but they might not be the largest holder of global oil reserves. John Arnold, the well known former energy hedge fund manager, yesterday on X basically said the 300 billion barrel reserve claim was made up by Hugo Chavez years ago as it was never independently audited and verified. Here was the tweet,

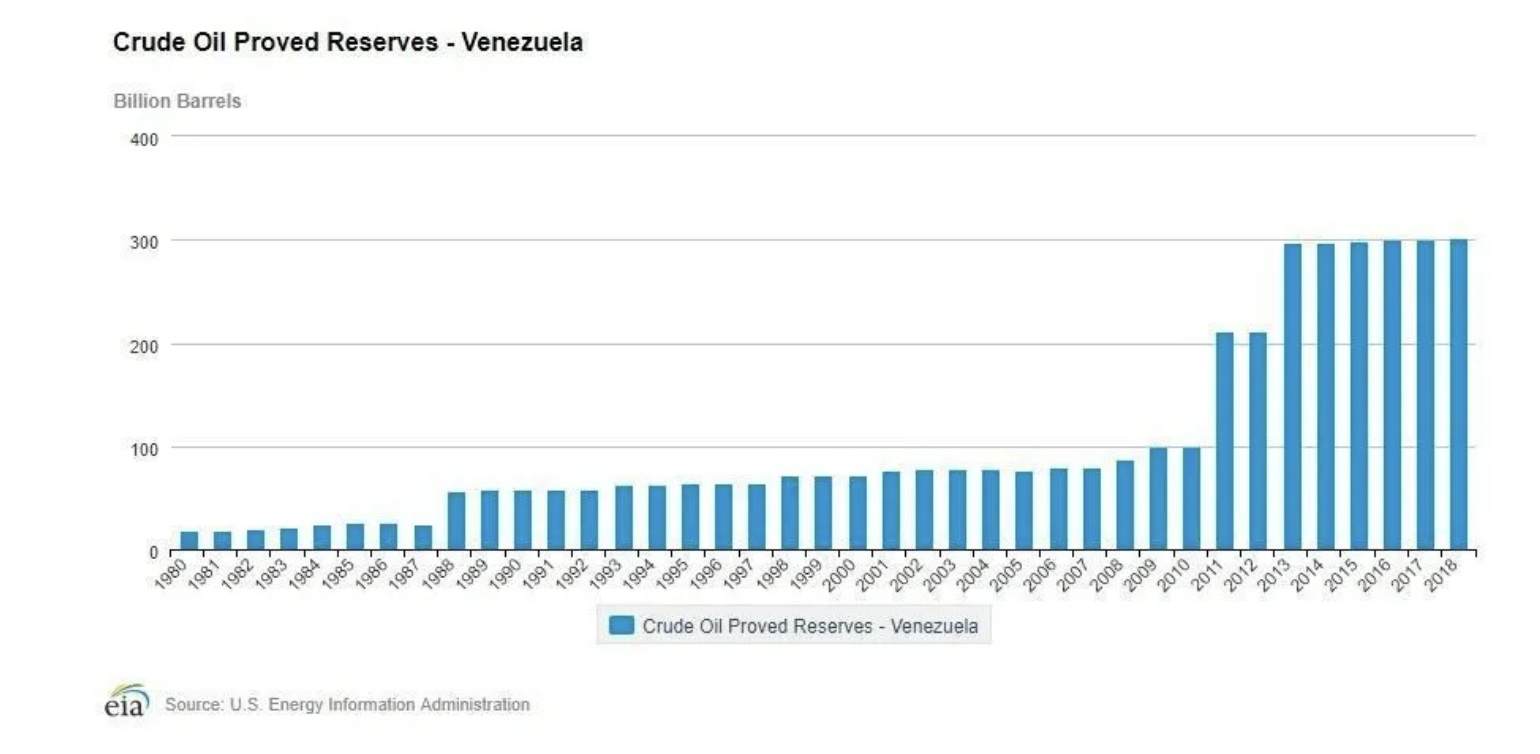

And here is a chart of their stated reserves he also posted. Chavez came to power in 1999 when audited reserves were about 75 billion barrels of reserves. The year he died in 2013, they magically jumped to 300 billion unaudited.

If the 300 billion figure was made up, it would place Saudi Arabia as the biggest holder at about 265 billion barrels, followed by Iran, and Canada at 170 billion according to Wikipedia. The US has about 46 billion according to the EIA so I’m not sure why it’s the 4th largest in the chart above. With respect to Canada, we’re long Canadian Natural Resources which got hit yesterday on the belief that Venezuela heavy, sour would compete with Canadian heavy, sour with US refinery customers but we know this would take years and Canada already has well established pipelines to the refineries, just completed the Trans Mountain pipeline to the west coast of Canada and will likely add more pipeline capacity in order to export more oil to Asia.

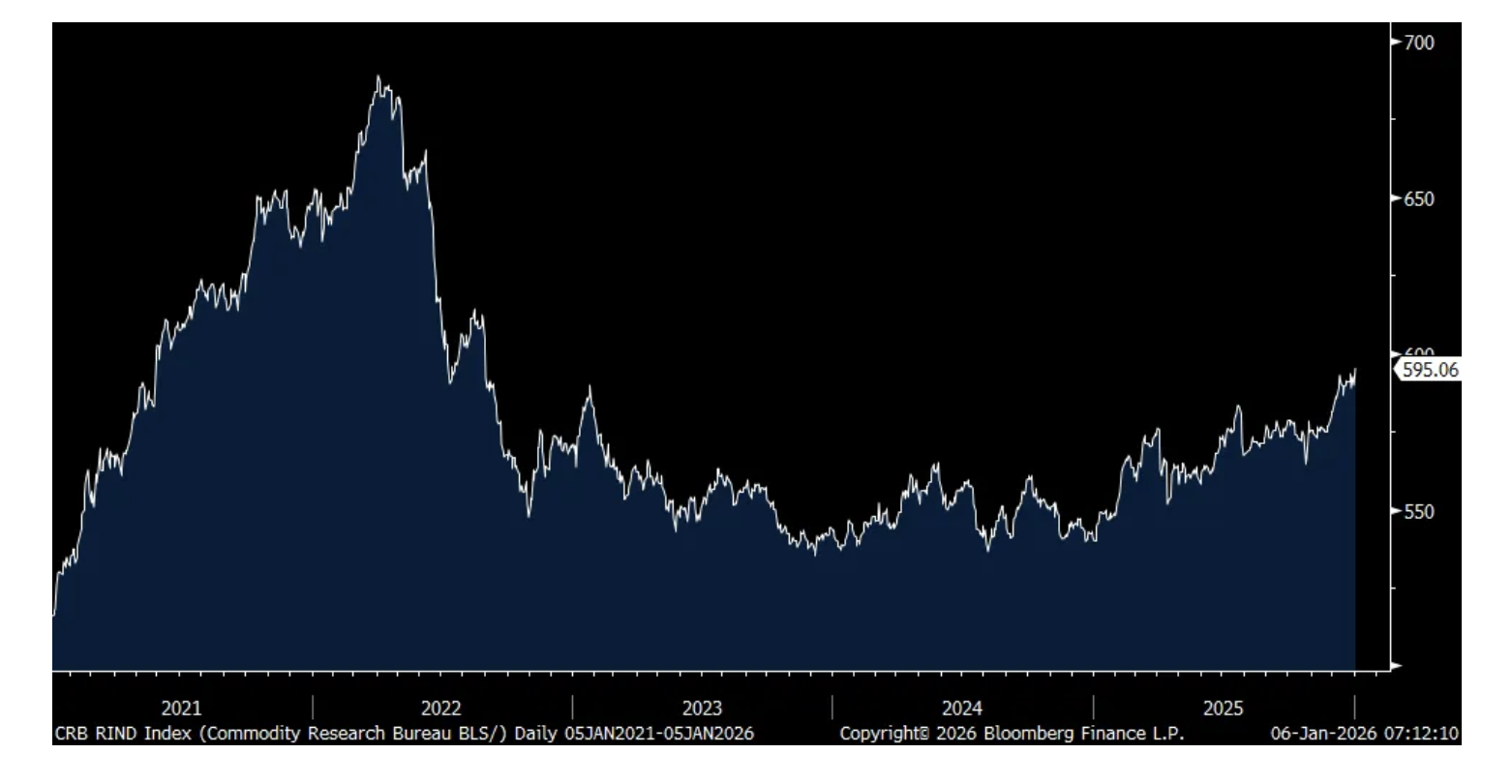

With respect to industrial raw material prices, the CRB raw industrials index yesterday was up 1% to the highest level since August 2022 helped by another record high in copper. Copper that goes into just about everything made, especially the electronics in our hands, the data centers being built and the grids that need to power them.

CRB Raw Industrials Index

Auto sales in the holiday month of December totaled 16.02mm at a SAAR, above the estimate of 15.8mm but below the 16.8mm seen in December 2024 and 16.7mm in December 2019. Cox Automotive estimates that 2026 will give us 15.8mm of vehicle sales and the y/o/y drop would be due to affordability challenges, according to them. Record high car prices and with also the higher cost of keeping a car in terms of insurance and vehicle maintenance, Cox said “The cumulative weight of all these increases has pushed total vehicle ownership cost beyond reach for many middle and lower income households, constraining market access and accelerating the affordability crisis.”

With the price of a car in 2026, tariffs will show up on a lagged basis after some car companies tried to keep a lid on increases last year. Yesterday the head of US sales for Toyota said “Prices are going to go up for us and for our competitors.” With overall vehicle sales still below where they were pre Covid, the CEO of Hyundai Motor America said yesterday too, “What we saw in 2025 is going to bleed into 2026...The way consumers’ mindsets are right now, we’re still dealing with inflation, with negative consumer sentiment.”

More global PMI’s for December are rolling out. Hong Kong’s fell 1 pt m/o/m to 51.9 and Singapore’s slipped to 54.1 from 55.4, still one of the strongest global prints out there. We remain bullish and long stocks in Singapore and some in Hong Kong. India’s final read on its composite index was a solid 57.8.

With the Hang Seng already up 4.2% year to date, S&P Global said this about the Hong Kong PMI, “Growth in both output and new orders was sustained in December, with the respective rates of expansion remaining solid despite easing from November. Notably, the improvement in demand was broad-based, with firms signaling greater sales across domestic and international markets.” I think we’re going to get another year of international stock outperformance relative to the US after many years of underperformance along with EM sovereign bonds relative to developed country bonds.

The final service PMI’s for the Eurozone and UK were revised down from their initial reports to 52.4 and 51.4 respectively, but both holding above 50 and carrying the economies of each in the face of still manufacturing softness.

From S&P Global, ““The eurozone services sector has grown for seven months in a row. The pace of expansion slowed in December, but overall, the picture looks good. Companies have even increased their staffing levels more strongly, and new business indicates that they remain on a growth path. Overall, the recovery in services gained momentum in the fourth quarter, which is a good basis for starting the new year with confidence.”

With the UK they said, “Survey respondents continued to report challenging business conditions, sales headwinds from subdued UK economic prospects, as well as constrained client spending linked to domestic political uncertainty. That said, some firms commented on tentative signs of a recovery in client confidence after a prolonged phase of anxiety in the lead up to the Budget.”

Nothing market moving here but European bourses are in the green this year and we watch too the direction of long term interest rates in the region as they have risen in the face of central bank rate cuts.

With respect to rates in Europe, French CPI in December was up .7% y/o/y as expected. A drop in energy prices helped as services inflation was up 2.2% y/o/y. Goods prices were down .4% y/o/y. German inflation today is expected to be up 2.2% y/o/y.

BY Doug Kass · Jan 6, 2026, 8:40 AM EST

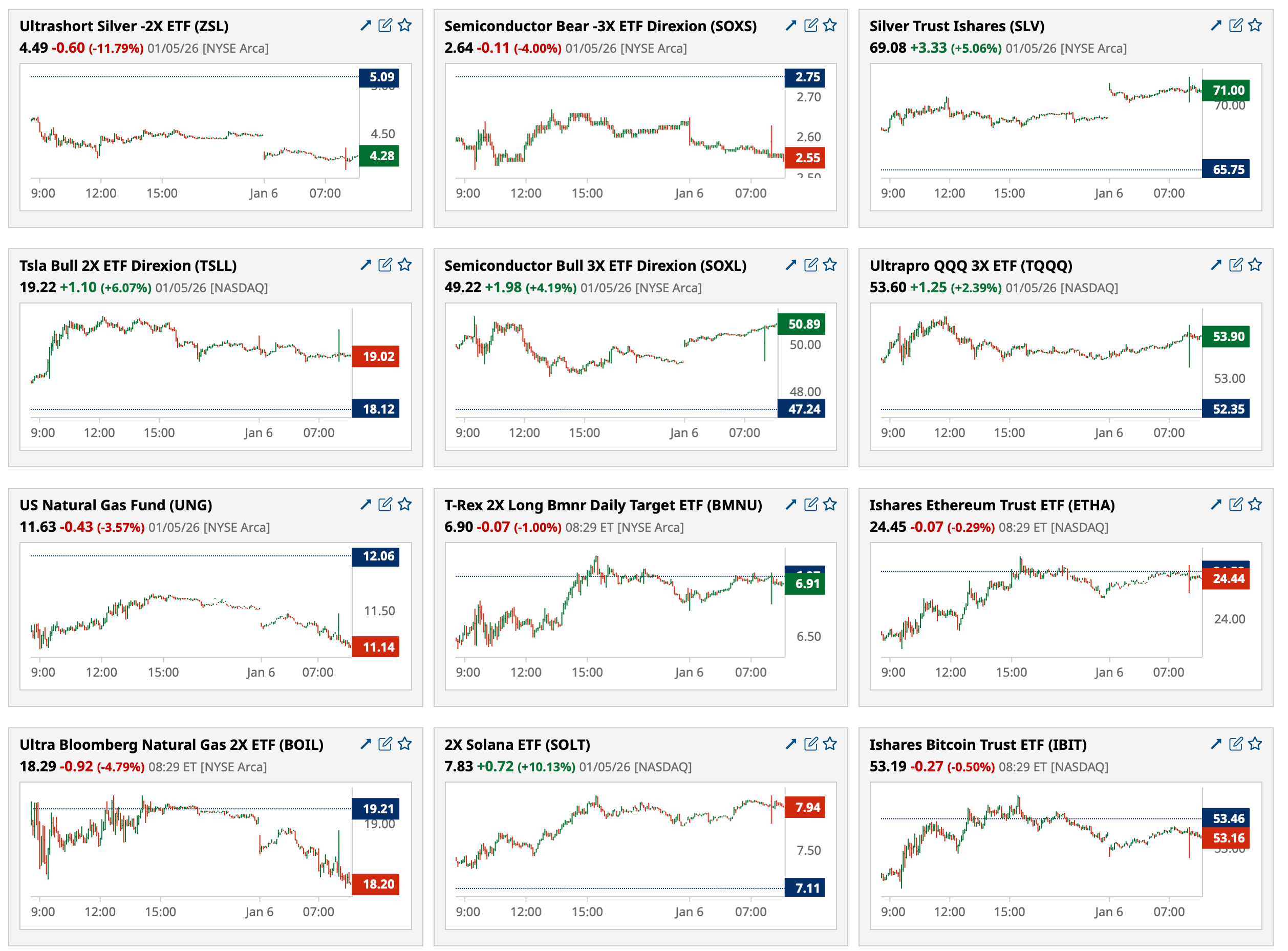

(TLT) is hitting a multi week low today.

BY Doug Kass · Jan 6, 2026, 8:16 AM EST

* Now...

I am adding to my (SPY) short at $687.60.

I plan to move to medium sized on strength.

BY Doug Kass · Jan 6, 2026, 7:30 AM EST

BY Doug Kass · Jan 6, 2026, 7:10 AM EST

From JPMorgan:

US: Futs are flat with RTY underperforming as geopolitics dominate the headlines including a potential US/EU deal that provides a security guarantee for UKR potentially with American soldiers maintaining a presence in UKR. Pre-mkt, Mag7 names are weaker ex-NVDA which is leading Semis higher post-CES presentation. Defensives are leading Cyclicals ex-Energy. Bond yields are higher by 1-2bp with USD also bid.

and...

Yesterday had the feel of a risk-on rally / ‘Everything Rally’. Digging a bit deeper we saw Cyclicals rally at the expense of Defensives. The AI Theme was mixed with a rotation from the Google Ecosystem (JPAIGOOG Index, -3.2%) to the OpenAI Ecosystem (JPAIOPEN Index, -4bp). Given some of the extreme moves yesterday, we may see some mean reversion but think the data this week and then earnings is supportive of a continued bullish run.

POSITIONING INTEL – Prime Time / Monthly Wrap | Strong HF Gains into YE; Positioning Rebounds Modestly

SUMMARY: HF performance ended the year on a high note with strong gains and alpha last month. Globally, HFs were up 2.2% in Dec and +16% for the year (vs. +8% last year, based on our estimates). APAC was the strongest with +3.2% MTD gains while N. America was also strong last month relative to the SPX as HF shorts did well.

In the US, positioning levels rebounded from late Nov lows, but didn’t move a lot in the second half of Dec. Our US Tactical Positioning Monitor’s level ended Dec at +0.4z, 72nd %-tile since 2015 (up from 50th %-tile at end of Nov). HF net leverage has been rising over the past few months and saw around a +1z increase in Dec. HF nets remain near highs across All Strategies and at the 83rd %-tile on a 5yr lookback among Equity L/S funds. As we wrote in our end-of-2025 note (Prime Time | Positioning Trends Still Positive for 2026, but Some Extremes to Watch, Dec 18th), the fact that positioning is still trending higher and HF nets are still elevated are generally positive signs for the market.

HF net flows were a bit mixed last month with buying in EMEA and AxJ vs. selling in Japan. N. America was mixed as we saw strong buying in the first few weeks of Dec before flows turned more negative towards YE. Gross flows were fairly muted and HF gross leverage has been rangebound over the past 6m, though still near long-term highs.

Outside of HFs, CTA positioning rebounded and remains high in Japan (90th %-tile long-term) and Europe (86th %-tile), but less extreme in US (69th %-tile), and HK (65th %-tile). US Equity ETF flows remained positive for a 6th month and Retail investors’ flows in single-stocks were positive, but relatively small as Retail sentiment remained subdued.

In the US, Health Care flows reversed as it was the most net sold sector in Dec (HFs shorted Biotech), after being most bought in Nov (on a combined HF+Retail+ETF basis). On the other hand, Financials was the most bought sector on a combined basis as it performed well and HFs were buyers across industries while ETF flows also turned more neutral, but have yet to ramp up.

Given the focus on Energy / oil, overall HF positioning in the sector remains fairly neutral vs. history in the US (44th %-tile since 2018), but positioning in Oil Services and E&Ps had picked up in the past 2 moths and were near 12m highs. ETF positioning remains very low. CTA positioning in crude oil remains quite low (11th and 16th %-tiles for WTI and Brent).

BY Doug Kass · Jan 6, 2026, 7:00 AM EST

Bonus — Here are some great links:

What's Your Investment Philosophy?

BY Doug Kass · Jan 6, 2026, 6:45 AM EST

Lost in Space (Data Centers In Orbit?) by Doomberg.

BY Doug Kass · Jan 6, 2026, 6:35 AM EST

BY Doug Kass · Jan 6, 2026, 6:25 AM EST

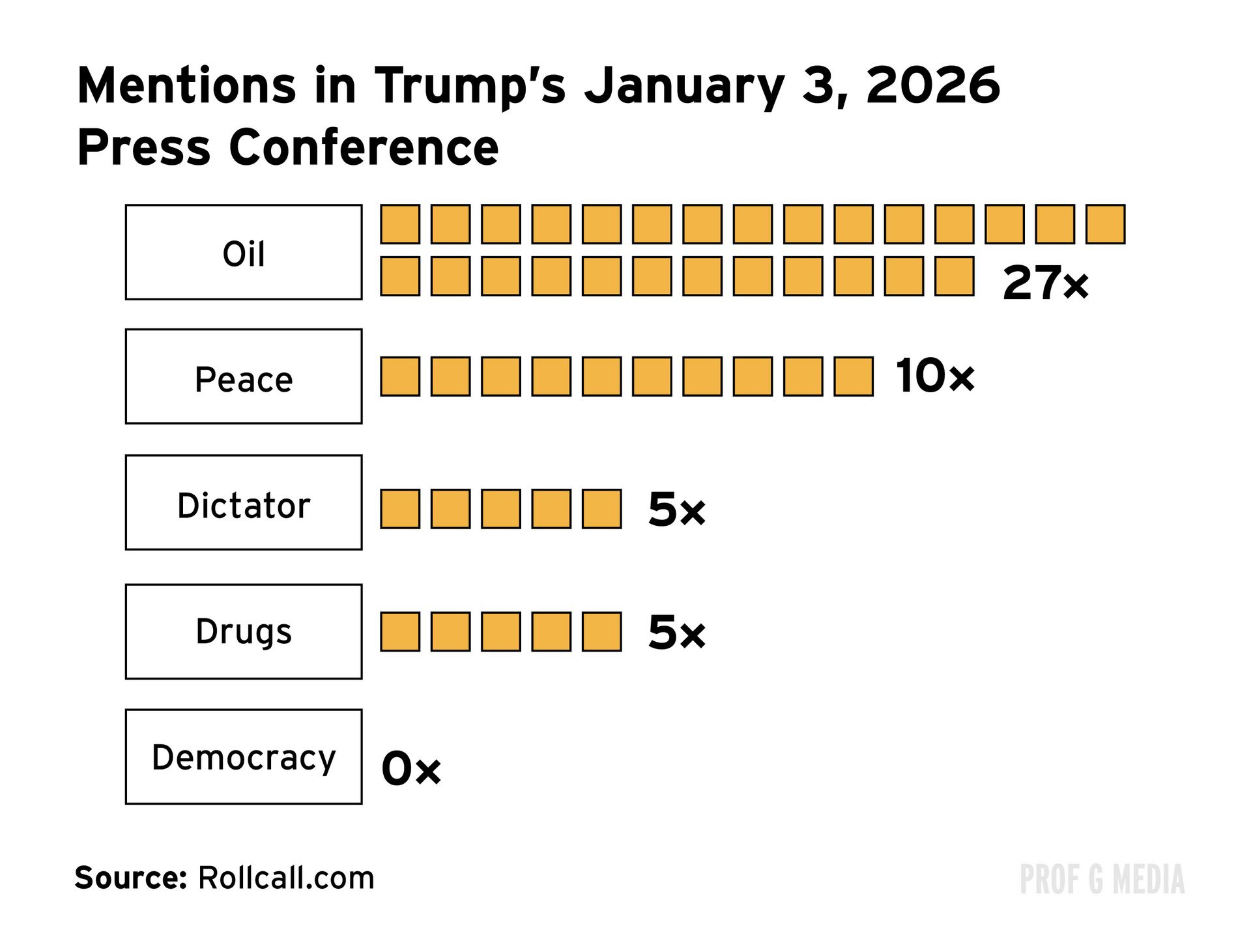

From Professor Scott Galloway:

US Intervention in Venezuela Puts Oil Supply in Focus

On Saturday, January 3, U.S. troops entered Venezuela and, in less than three hours, extracted the country’s president, Nicolás Maduro, and his wife, Cilia Flores. Both were transported to New York City where Mr. Maduro will face drug-trafficking charges.

The operation leaves Venezuela and its $18 trillion in proven oil reserves ostensibly in the hands of its vice president, Delcy Rodríguez — but functionally subject to Trump’s vision for the country.

In a press conference on Saturday, Trump said the U.S. would run Venezuela until a “judicious transition” takes place, without alluding to a specific timeline.

Trump had more detailed plans for Venezuela’s vast oil reserves — believed to be the largest in the world. Namely, U.S. energy corporations will return to the country and fix its broken oil infrastructure. Trump also alluded to a kickback for the U.S. government, stating, “A lot of money is coming outta the ground. We’re gonna get reimbursed for all of that.”

Venezuela has nearly 18% of total global oil reserves, but years of mismanagement has caused the South American nation’s output to drop to only 1% of global oil production.

U.S. oil giants have not publicly agreed to Trump’s plan. Bringing Venezuela’s oil output back to where it was 15 years ago would cost an estimated $110 billion — twice the combined investment of major U.S. oil companies worldwide in 2024.

U.S. energy companies operated in Venezuela once — but it didn’t end well. In 2007, the Venezuelan government seized their operations in a move that Trump has since called “the largest theft of property in the history of our country.”

ExxonMobil and ConocoPhillips refused to accept the terms of the takeover, and the Venezuelan government still owes them billions.

Chevron is the only major U.S. oil company still operating in the country.

According to Politico, the Trump administration has told oil executives that if they want full reimbursement, they must comply with his order to revitalize Venezuela’s petroleum industry.

BY Doug Kass · Jan 6, 2026, 6:15 AM EST

For 28 years I have been writing my Diary.

Sometimes I write something that elicits a very warm response — making it all very worthwhile and satisfying.

Last night I received such an email from Anita Volz Wien, Byron Wien's widow — in response to My 10 Surprises of 2026 (and tribute to Byron):

Doug

Greetings from New York.

Thank you for keeping Byron’s memory alive through his and your surprises. Several friends forwarded them to me and I thought yours were excellent.

Warmest wishes for 2026. Let’s hope we survive the ups and downs of the country and the world.

Anita

Anita Volz Wien

BY Doug Kass · Jan 6, 2026, 6:05 AM EST

Here are Monday's things:

* I reinitiated index shorts:

(SPY) $685.61

(QQQ) $617.68

* I added to my (GRNY) at $25.49 and (JOET) at $42.96 shorts.

* I added to my (CRWV) short at $80.94.

* I added to longs — (PG) at $140.25, (PEP) at $140.51 and (KMB) at $98.98.

* I added to these small financial shorts — (GS) at $944.37, (MS) at $186.54 and (JPM) at $332.39.

BY Doug Kass · Jan 6, 2026, 5:55 AM EST

The S&P Short Range Oscillator rose to a greater overbought at 1.63% vs. 1.34%.

BY Doug Kass · Jan 6, 2026, 5:45 AM EST