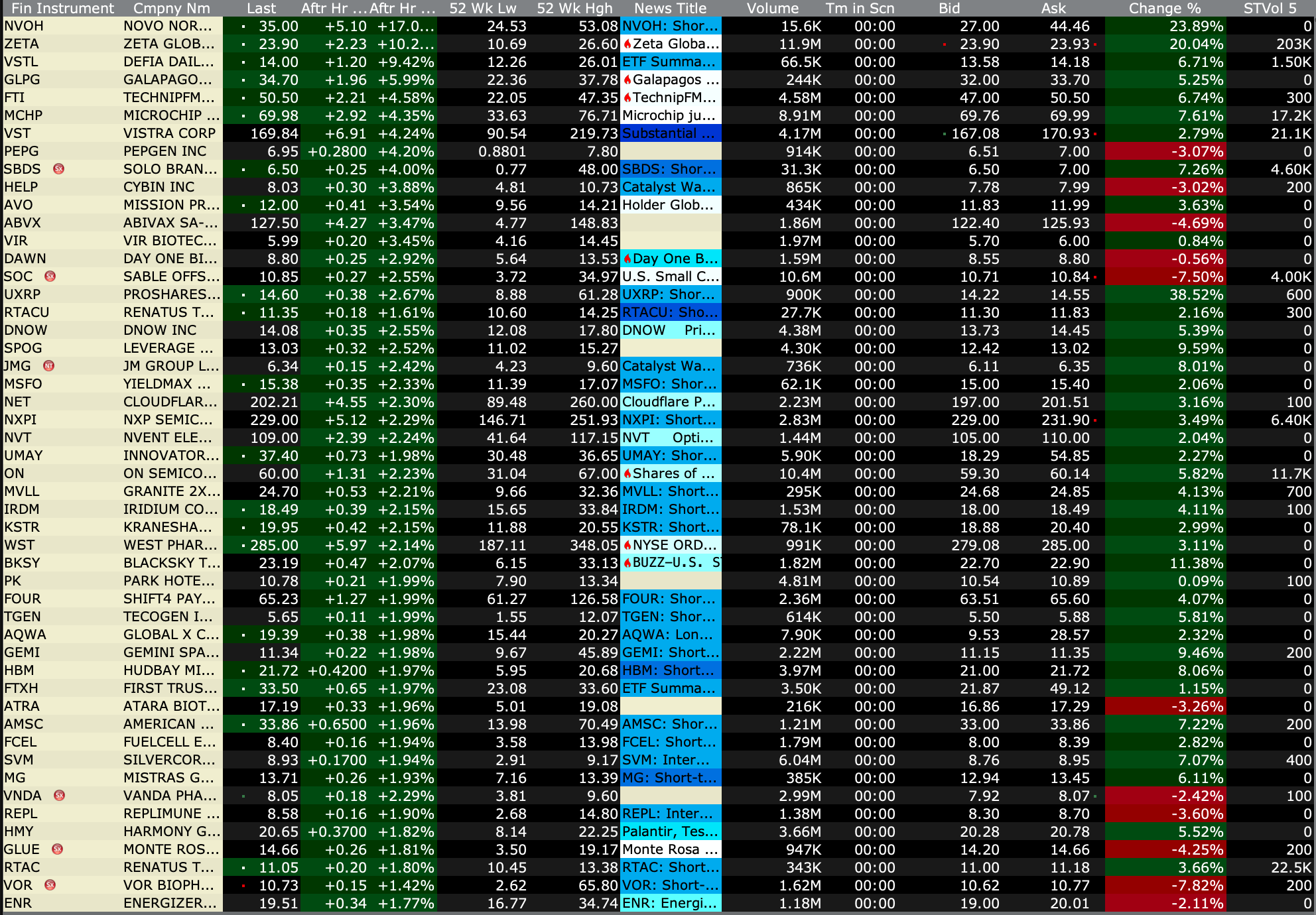

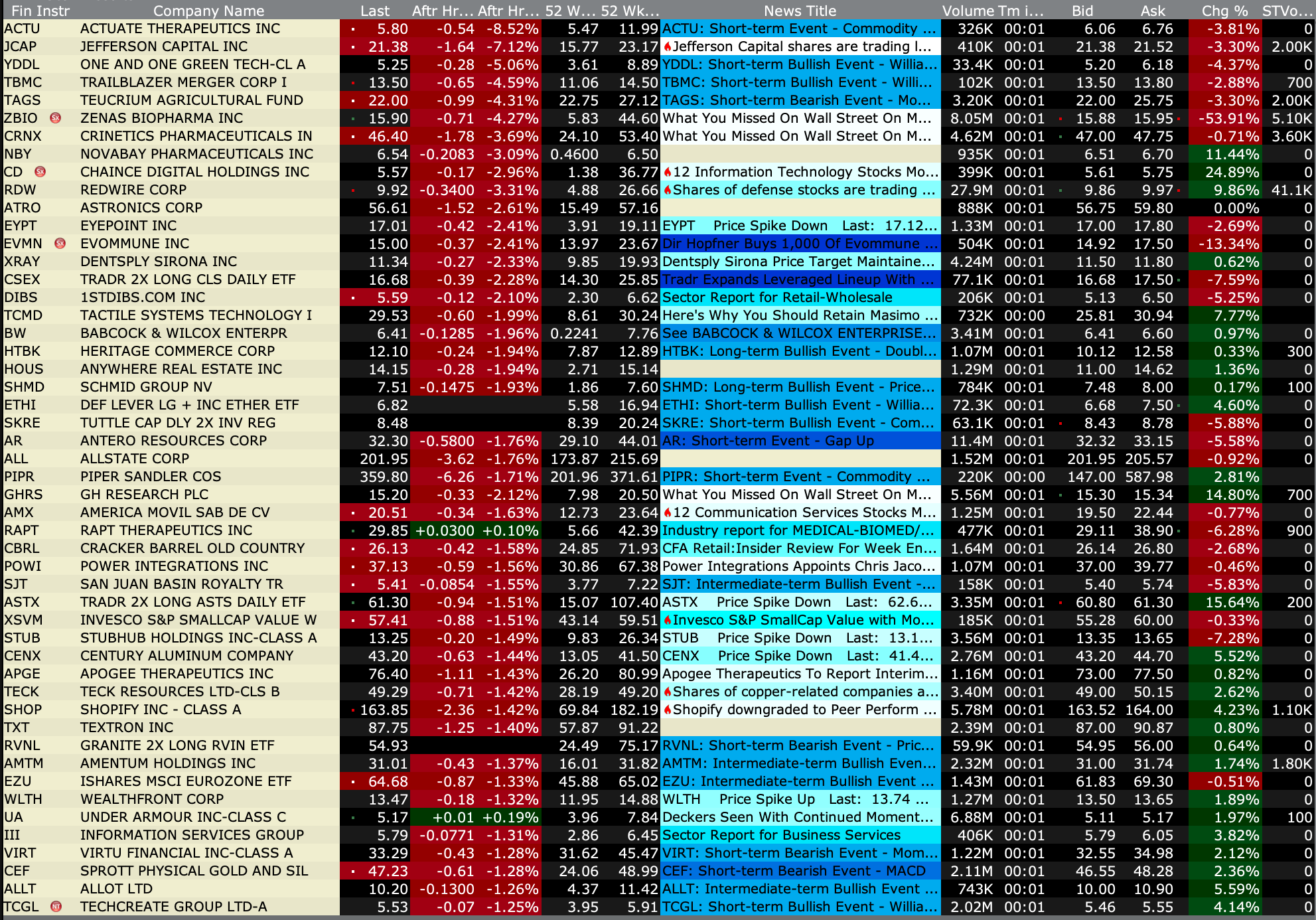

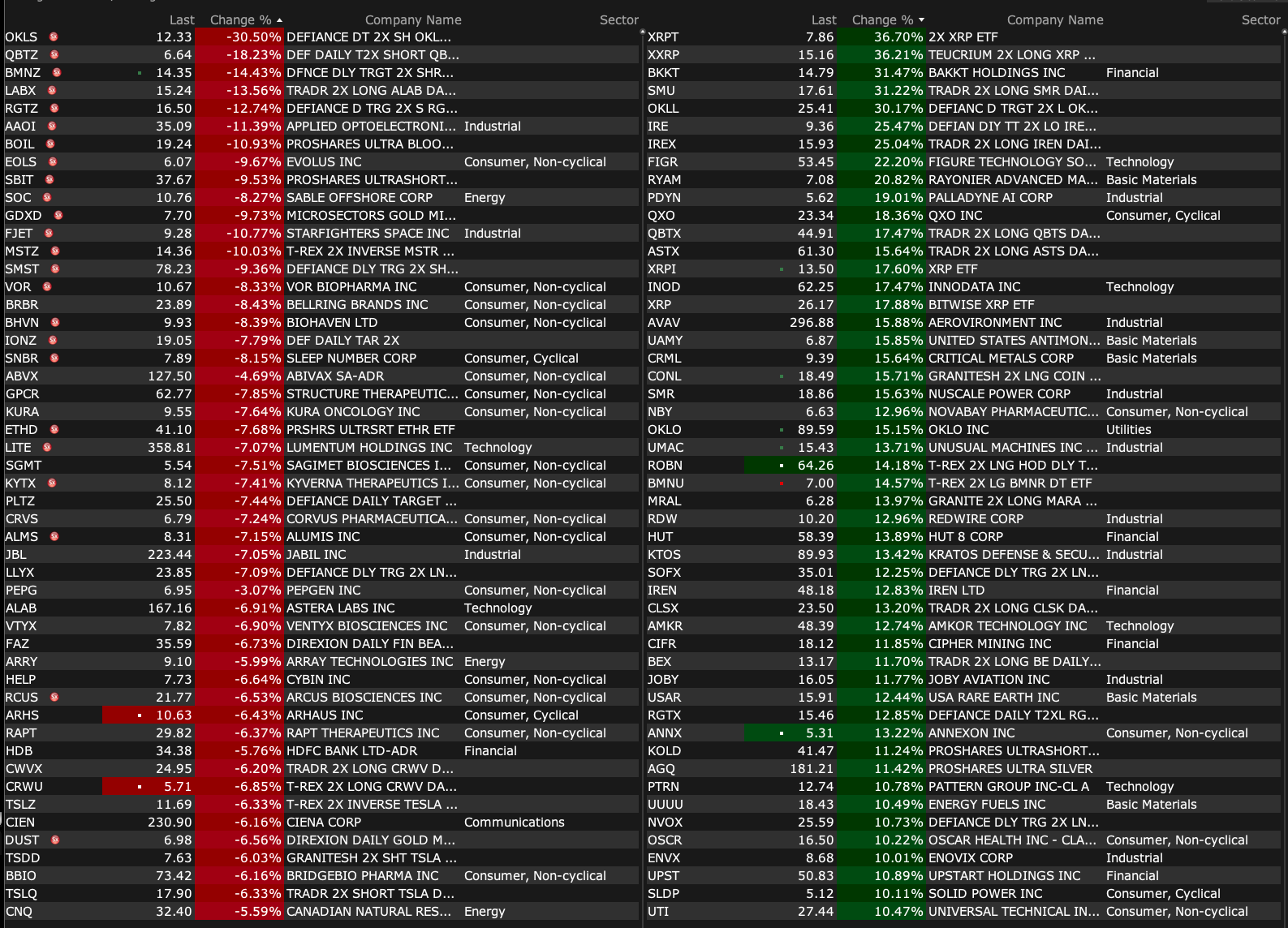

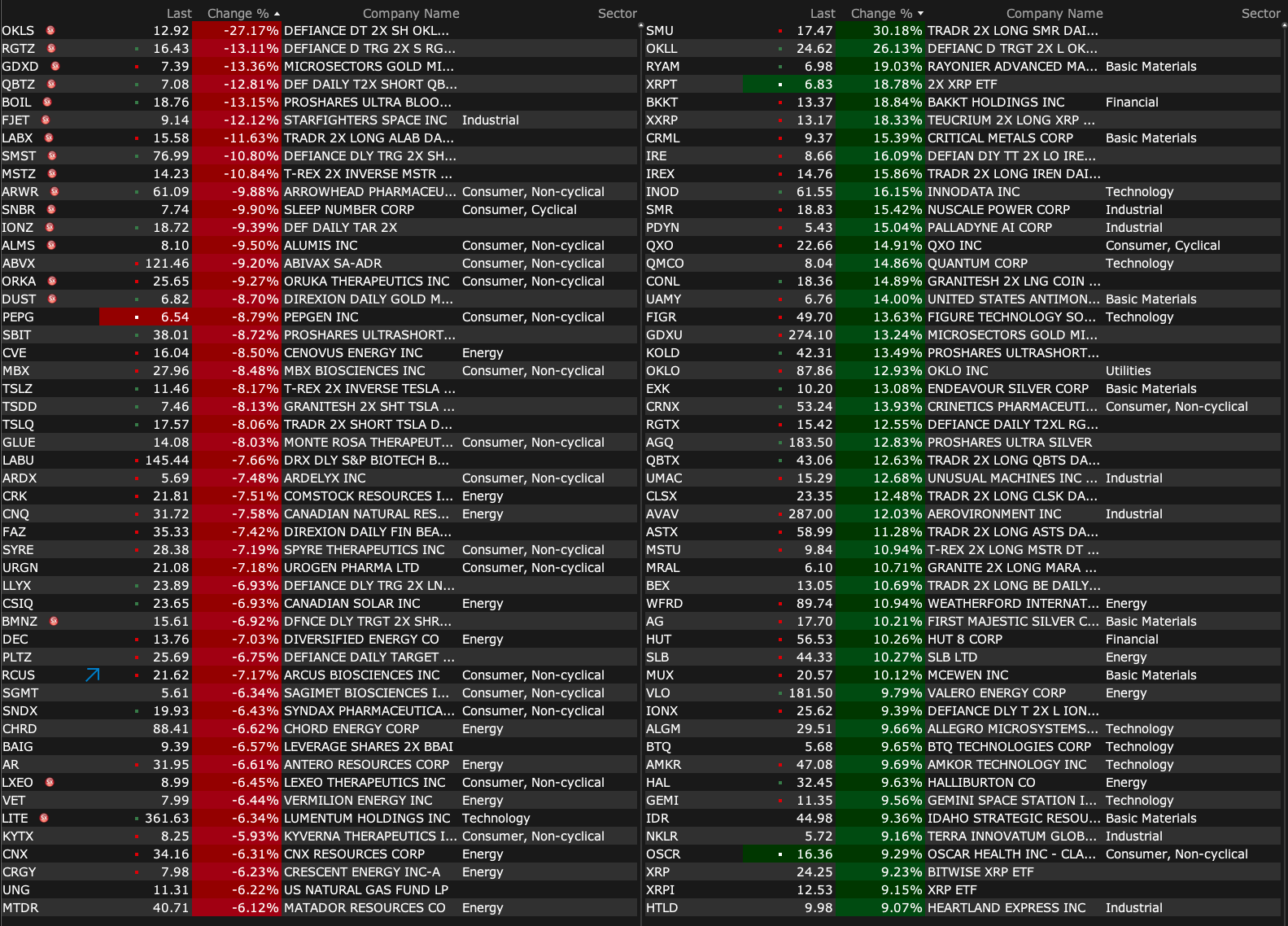

After-Hours Gainers, Losers

After-Hours % Gainers

After-Hours % Losers

BY Doug Kass · Jan 5, 2026, 4:50 PM EST

BY Doug Kass · Jan 5, 2026, 4:50 PM EST

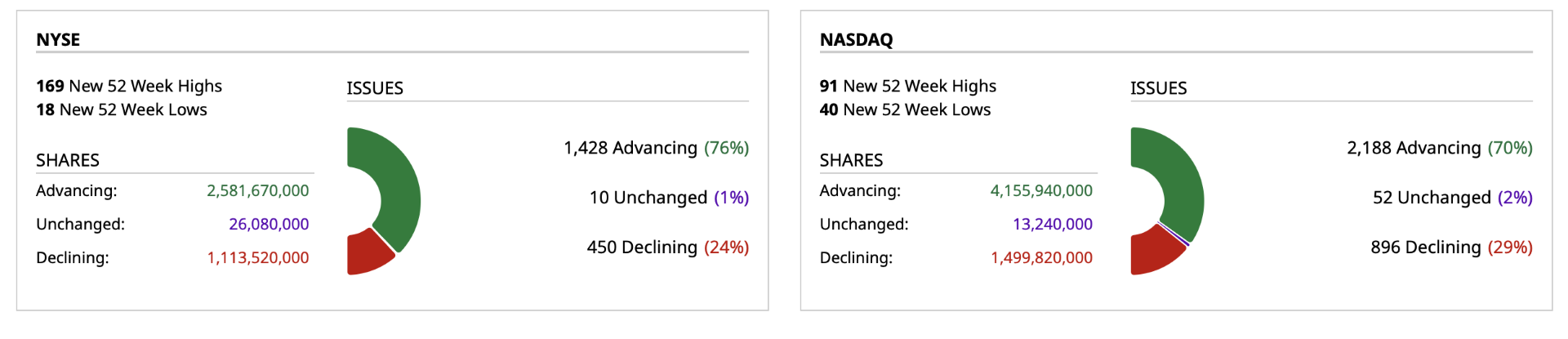

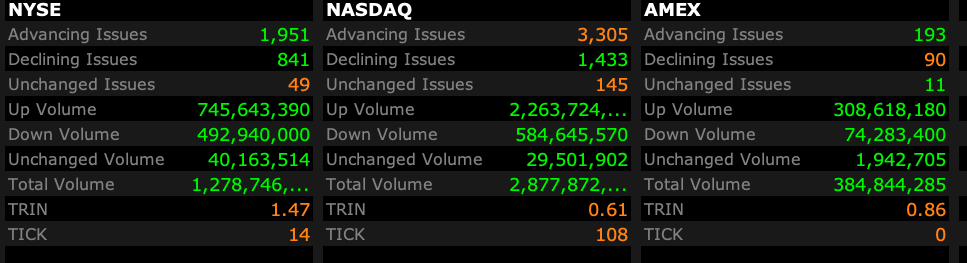

- NYSE volume 34% above its one-month average;

- NASDAQ volume 16% above its one-month average;

- VIX index: up 2.69% to 14.90

BY Doug Kass · Jan 5, 2026, 4:37 PM EST

The Wall Street Journal has confirmed the large bet that Maduro would be dethroned, which I mentioned in my column.

A Mystery Trader Made $400,000 Betting on Maduro’s Downfall - WSJ

BY Doug Kass · Jan 5, 2026, 3:49 PM EST

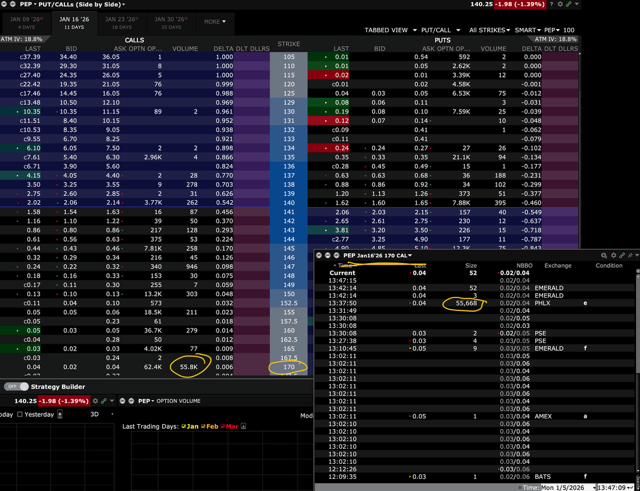

Someone just purchased 55k $170 (PEP) calls for Jan. 16, 2026:

BY Doug Kass · Jan 5, 2026, 2:10 PM EST

Half of the male population between 18 and 50 have a sports betting account. Nearly one quarter of the sports bettors say they are addicted. And one in five persons with a gambling addiction attempt suicide. Wagering on the next Federal Reserve Chairman, Pres. Trump's next tweet, whether the next pitch is a strike or a ball (or how many home runs NY Yankee Aaron Judge will hit, who will score the first Super Bowl point, etc.), invites corruption into every aspect of American life.

More professional teams and college teams are embroiled in "fixes." The shares of Robinhood (HOOD) , Caesars (CZR) , Flutter (FLUT) , MGM Resorts (MGM) , Draft Kings (DKNG) and other companies involved in gambling and predictive markets fall in half — as regulatory authorities begin to place new restrictions on the space.

A deteriorating equity market results in massive retail trading losses - from leveraged ETFs, zero-days to expiration options, etc.

Calls for regulatory action (on leveraged ETFs and zero dated options) grow louder as YOLO and HODL become OHNO.

- Doug Kass My 10 Surprises of 2026

An item that broke over the weekend where it appears a relative newcomer to Polymarket made a $30k wager on “Maduro out by Jan 31, 2026” and made about 13x his money overight.

I am not sure if this is accurate but there is a degree of transparency at Polymarket, there is a receipt, which I posted below.

This is being reported by some legit media outlets. Here’s Yahoo!, for one. Fortune also covered, as have others.

BY Doug Kass · Jan 5, 2026, 2:04 PM EST

I added to my (NKE) , (PG) , (PEP) , and (KMB) longs this morning.

BY Doug Kass · Jan 5, 2026, 1:21 PM EST

Back in the office.

Getting my sea legs back.

BY Doug Kass · Jan 5, 2026, 12:45 PM EST

From Peter Boockvar:

Quite the extraordinary weekend and it wasn’t just in Venezuela, what is going in Iran too is highly noteworthy. It’s always a good day when a despot goes down but I’ll leave the geopolitics/legalities to others. I did think this piece from my friend Tracy Shuchart laid out the real reasons why we did what we did with Maduro and it wasn’t because of drugs and maybe something other than oil.

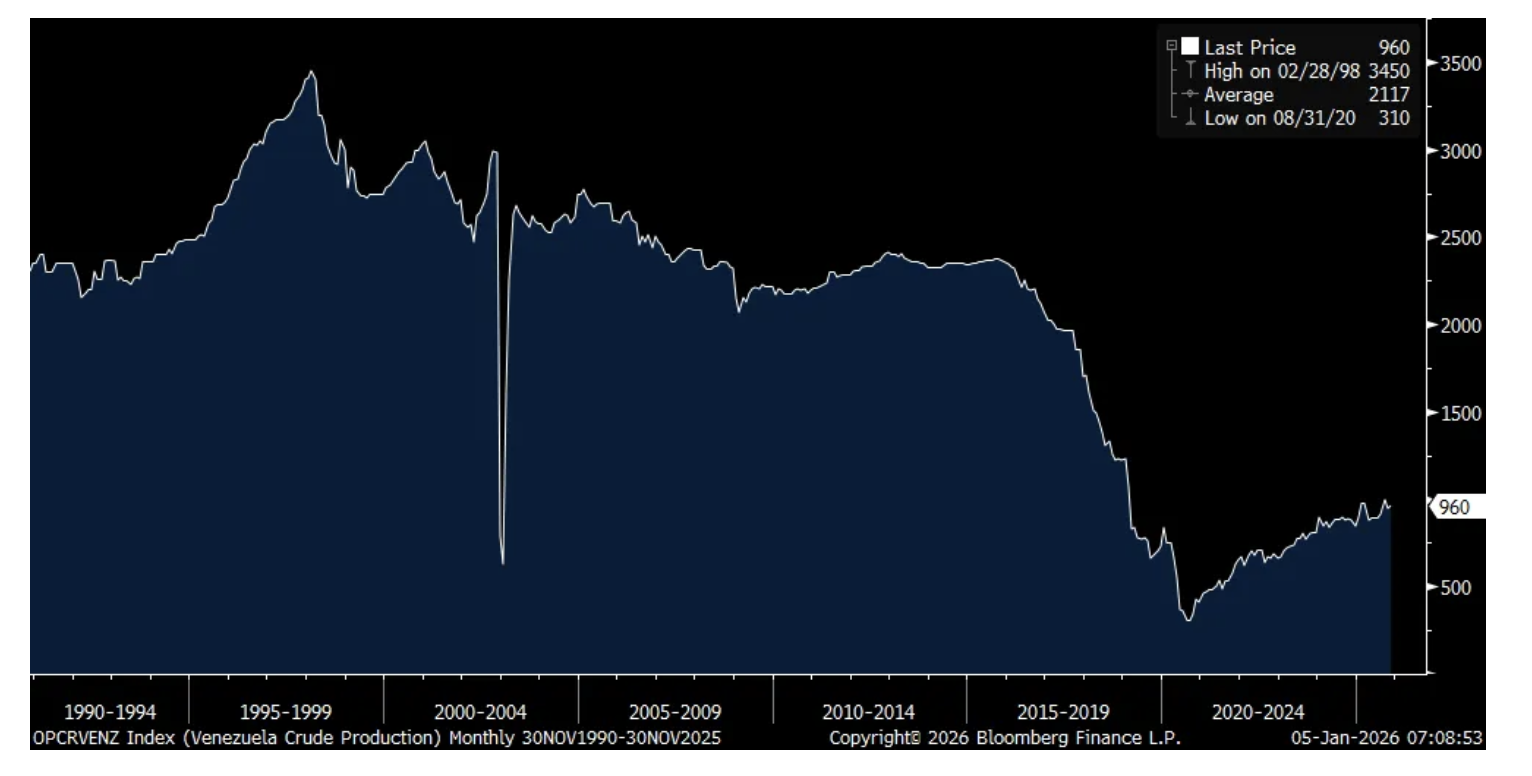

With respect to oil, we know that Venezuela has the world’s largest reserve base of about 300 billion barrels but there is one thing to have it and another to lift it out of the ground. I’m sure you read about all the stats over the weekend and I will lay out what I read too here. Off a current production level of about 960k barrels per day (could dip from here before it reaccelerates upon the placement of a stable government), it could take between 3-5 years and about $10 billion of investment per year to bring production back to about 2mm barrels and possibly up to 10 years to get Venezuelan production back to 3mm barrels, where Venezuela was pre Hugo Chavez.

With global crude demand rising by about 1mm barrels per day, the world will grow into any increase in Venezuelan oil production and in the context of a world that currently produces about 105 million barrels per day, an increase in Venezuelan oil production over the coming 10 years shouldn’t have that much of an impact on global supply and demand, though we’ll of course take more supply.

Also to think about, Venezuela is a member of OPEC+ and OPEC+ can of course tweak overall production quotas to manage what comes from Venezuela in the coming years. OPEC+ over the weekend said they will keep quota levels unchanged for Q1 and said it’s too early to compute what could change with Venezuela. As OPEC+ production levels have not kept pace with the recent quota increases, it appears that Saudi Arabia and the UAE are really the only two members with spare capacity currently anyway.

US refiners rely heavily on heavy, sour crude and will benefit from buying that which Venezuela produces in the coming years but which takes a higher breakeven cost relative to some light, sweet basins around the world. US refiners currently get most of this type from Canada.

Bottom line, the Venezuela news does not change my view point that in the coming few years, the price of oil is dirt cheap and we remain long oil and natural gas stocks. What happens past the next few years, we’ll reaccess then.

Venezuelan Oil Production since 1990

What the political turn in Venezuela also means, after the recent election in Chile and what Javier Milei is currently doing in Argentina, South America is showing signs of shifting away from the failed economic policies of democratic socialism which some in the US delusionally believe they can somehow recreate and generate a different outcome. A big election is coming this October in Brazil where Lula’s economic policies will be put to the election test. We’re long stocks in Brazil, as well as local currency bonds there, in addition to owning positions in other emerging markets that I believe will have another good year. Interestingly, it is not the emerging market countries that the world is getting increasingly worried about rising debts and deficits this time. It’s the developed world’s sovereign bonds that are being questioned.

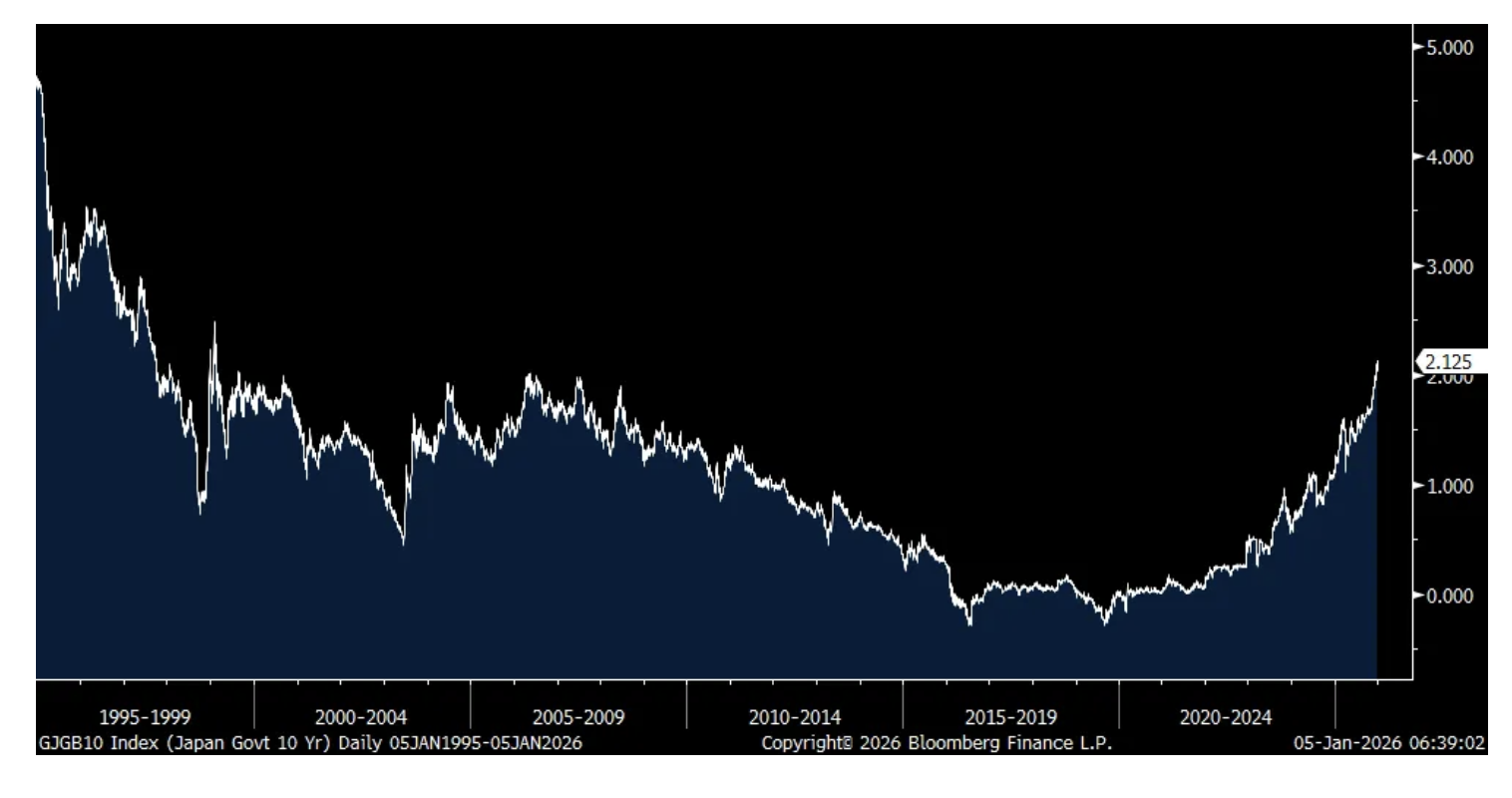

Speaking of which, as the new year gets underway, Japanese bond yields continue higher, again. The 10 yr yield was up by another 6 bps to 2.13%. February 1999 was the last time this yield on this maturity was seen. I continue to believe at some point this will really matter for global bond yields and money flows with Japanese savers and financial institutions big holders of foreign assets and the largest foreign holder of US Treasuries in particular.

Helping to lift yields, as the 2 yr yield was also higher by 2.3 bps to 1.20%, were these comments from BoJ Governor Ueda overnight. “We will keep raising rates in line with improvement in the economy and inflation. The appropriate adjustment of monetary easing will lead to the achievement of stable inflation target and longer-term economic growth.” The yen is a touch higher but still does not trade well in light of the dramatic rise in yields.

I do think this changes though this year, along with other Asian market currencies in light of the move higher in the Chinese yuan which I mentioned on Friday. After rising in 9 out of the last 10 days, it’s down slightly today.

10 yr JGB Yield

I’m shifting gears to the AI data center buildout and its inflationary implications. Yes, we’re currently seeing it from the electricity cost perspective but we’re about to see it from a rise in the prices of devices. The Weekend FT had a piece titled “Chip shortages threaten 20% rise in consumer electronics prices.” It said, “Consumers should prepare for price increases this year of as much as 20% for smartphones, computers and home appliances, analysts and manufacturers have warned, as AI demand drives up the cost of memory chips used in electronics.”

“Consumer electronics makers including Dell, Lenovo, Raspberry Pi and Xiamoi have warned that chip shortages were likely to add to cost pressures and force them to raise prices, with analysts forecasting increases of 5 to 20%.”

“Market researcher TrendForce forecast average Dram prices, including for HBM chips, would rise between 50% and 55% in the fourth quarter of 2025 from the previous quarter.”

I’ll add this, at some point this ends badly for Dram/HBM prices because this inherently boom/bust business will eventually add too much supply but at least for now, we’ll be paying more.

Overall for inflation this year, in the first half I do expect a continuation of service price disinflation because of slowing rents, though an inflection higher in the 2nd half. On the goods price side, that will be the offset to the upside.

https://www.ft.com/content/1f471189-2277-4d5d-822b-78eba6060755

China’s private sector focused services PMI was little changed in December at 52 vs 52.1 in November. RatingDog said “In terms of sub-components, demand for services showed divergence in December. While the new orders index continued the growth trend seen since early 2023, the pace of growth slowed compared to the previous month due to a renewed fall in new export business. New export business returned to contraction following a brief improvement in November, primarily due to reduced tourist numbers, particularly from Japan.”

Vietnam, gaining some manufacturing share from China, saw its December exports jump by 24% y/o/y vs the estimate of up 14%. Their economy grew by 8.5% in Q4, above the forecast of 7.7% and I believe this remains one exciting growth story. We’re still long and positive on Vietnamese stocks.

BY Doug Kass · Jan 5, 2026, 12:30 PM EST

- NYSE volume 58% above its one-month average;

- Nasdaq volume 19% above its one-month average;

- VIX index: up 1.79% to 14.77

BY Doug Kass · Jan 5, 2026, 11:50 AM EST

From Peter Boockvar:

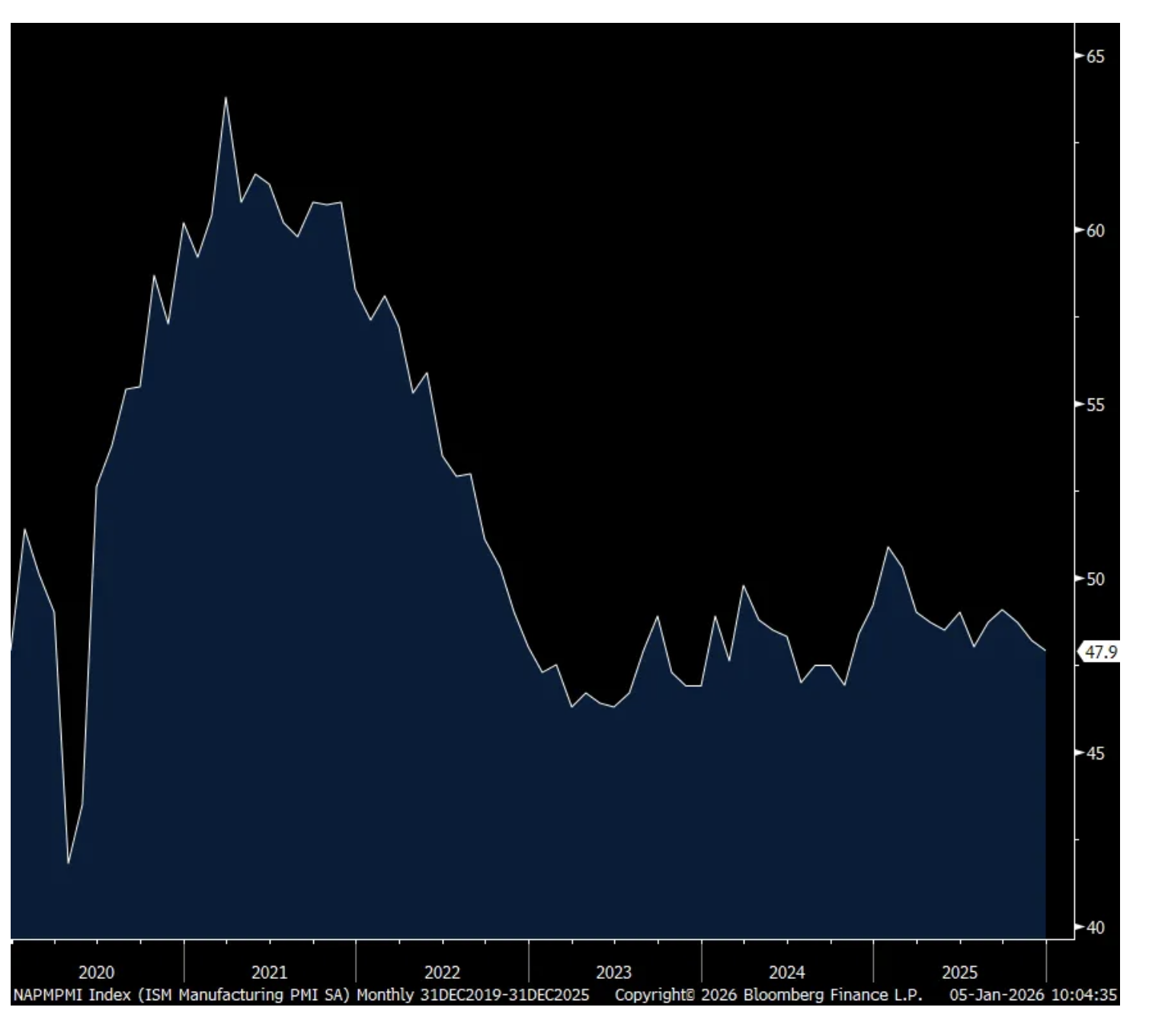

US manufacturing remained under pressure in December as seen in the ISM index print of 47.9 vs 48.2 in November and below the estimate of 48.4. This index has been above 50 just twice since the fall of 2022.

New orders were 47.7 vs 47.4 in the month before and backlogs remained well under 50 at 45.8, though up from 44. Inventories fell 3.7 pts m/o/m to 45.2 while those at the customer level sits at just 43.3. Export orders are still in contraction at 46.8 and was last above 50 in February. Imports came in at only 44.6.

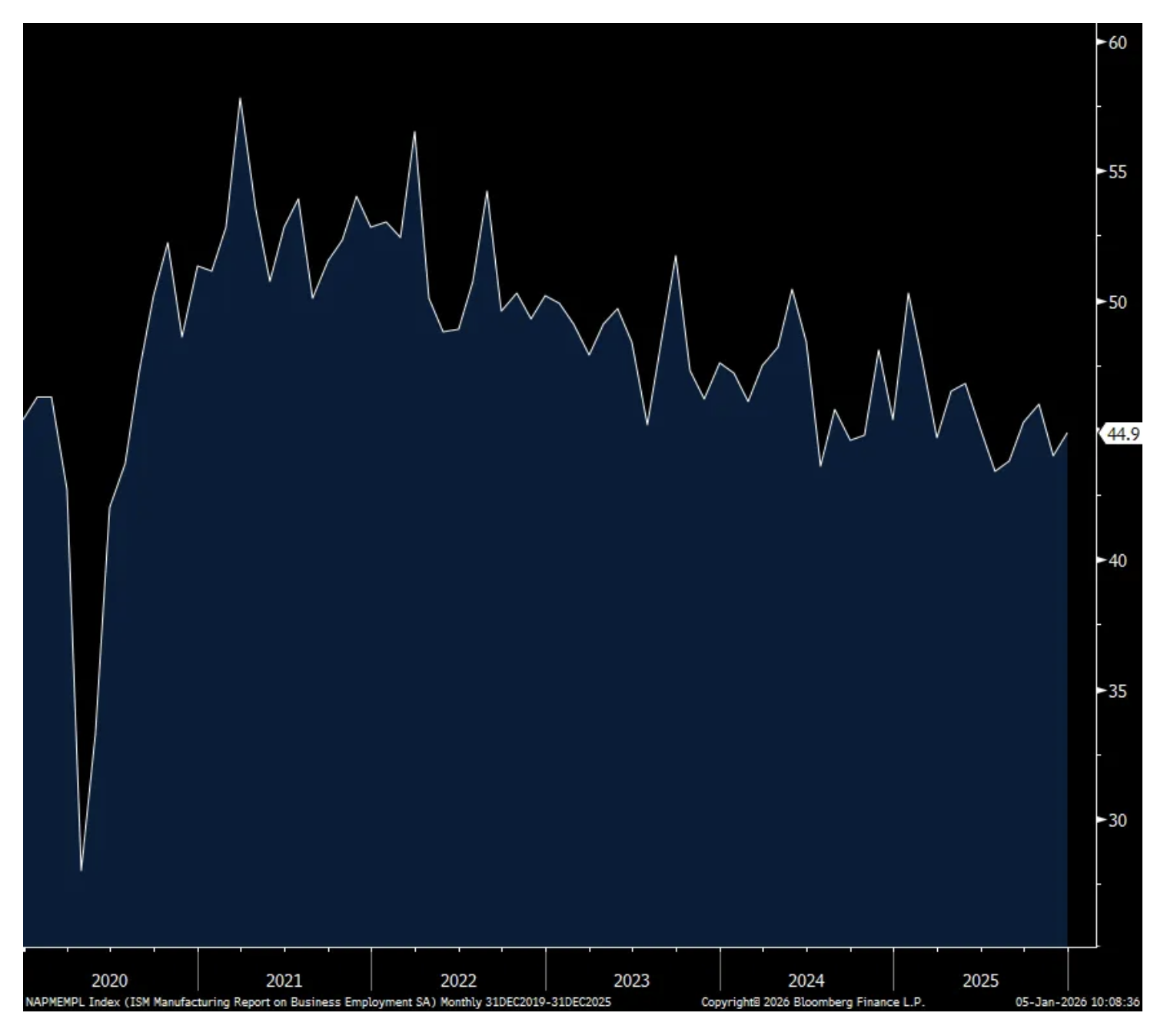

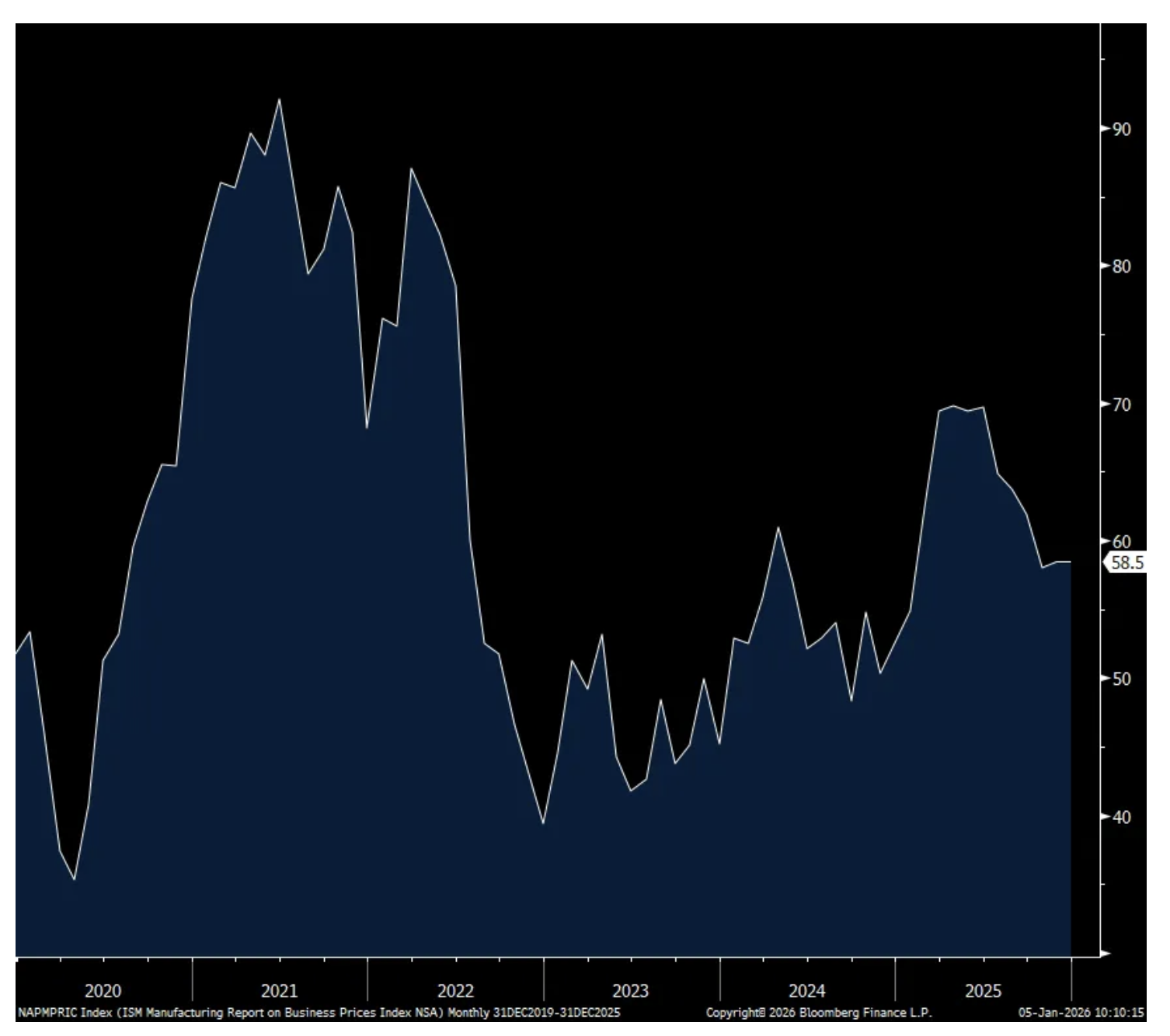

Employment at 44.9 was last seen above 50 back in January. Supply chains saw no stresses, though this gauge rose 1.5 pts to back above 50 at 50.8. Prices paid were unchanged at 58.5 and thus still well above 50, though below its mid year highs. ISM this on inflation, “The Prices Index reading continues to be driven by increases in steel and aluminum prices that impact the entire value chain, as well as tariffs applied to many imported goods.”

In terms of industry breadth, just 2 saw its business expand vs 15 that contracted. The ISM said “Looking at the manufacturing economy, 85 percent of the sector’s gross domestic product (GDP) contracted in December, compared to 58 percent in November, and the percentage of manufacturing GDP in strong contraction (defined as a composite PMI® of 45 percent or lower) increased to 43 percent, compared to 39 percent in November.”

With new orders, “For every positive panelist comment about new orders, 1.3 comments indicated concern about near-term demand, driven by tariff costs and other uncertainties.” On employment, “Companies continued to focus on accelerating staff reductions due to uncertain near- to mid-term demand. The main head-count management strategies remain layoffs and not filling open positions.”

Bottom line, while tariffs are not a headline topic of discussion anymore, it still is a major drag on the manufacturing sector. See below the quotes from a variety of companies in many sectors.

“Winding up the year with mixed results. It has not been a great year. We have had some success holding the line on costs; however, real consumer spending is down and tariffs are ultimately to blame. I hope for some return to free trade, which is what consumers have ‘voted for’ with their spending.” [Chemical Products]

“Trough conditions continue: depressed business activity, some seasonal but largely impacted by customer issues due to interest rates, tariffs, low oil commodity pricing and limited housing starts.” [Machinery]

“Things are quieter regarding tariffs, but prices for all products remain higher. Our costs have increased, so we have increased prices for our customers to compensate. Margins have deteriorated, as full pass through (of cost increases) is not possible.” [Computer & Electronic Products]

“Things are not improving in the transportation equipment market. Many customers are ordering for 2026, but those orders are 20 percent to 30 percent below their historical buying patterns. Some large fleets are still completely on hold for 2026, with zero capital expenditures money available to fleet budgets. Truck rental utilization, which is a good benchmark for the health of the economy, is still below historically stable levels. The general mood of the industry is that the first half of 2026 will be another bust, and we’re now hoping things pick up in the second half, even as the North American truck fleet continues to age.” [Transportation Equipment]

“In the current environment, our company is struggling with customer orders and financially overall. Our senior leaders are struggling to focus our business and get the company on track with quality products. In November, layoffs impacted about 9 percent of our workforce, affecting all locations in the U.S. and Europe.” [Machinery]

“Orders continue to drop for most of our businesses. Many plants are not running near full capacity. Make to order being utilized where possible.” [Chemical Products]

“Order levels have continued to decline: We had a bad October, an awful November and a dismal December. January and February don’t look too good, as bookings are down 25 percent compared to the first two months of 2025.” [Fabricated Metal Products]

“Morale is very low across manufacturing in general. The cost of living is very high, and component costs are increasing with folks citing tariffs and other price increases. It’s cold in our area of the country, absenteeism is worse around the holidays, and sales were lower than we expected for November. So, things look a bit bleak overall.” [Electrical Equipment, Appliances & Components]

“Global logistics remains sensitive to geopolitical shifts. Tariffs are influencing equipment pricing and procurement strategies. Large-scale data center programs are absorbing and reducing availability of resources for other sectors.” [Food, Beverage & Tobacco Products]

“2025 revenue was down 17 percent due to tariffs. The lost revenue has inhibited our ability to offer bonuses to employees or create and hire for new positions.” [Miscellaneous Manufacturing]

ISM Mfr’g

Employment

Prices Paid

BY Doug Kass · Jan 5, 2026, 11:30 AM EST

* This is my 24th year of Surprise Lists

* My Surprise List reverts back to only 10 Surprises in 2026 from 15 Surprises in 2025

* Though precious metals and equities rise early in the year, "there is no place to run, no place to hide" for most of the year

* The President resigns, the U.S. economy moves toward recession and today's leveraged market structure (passive management dominance that "worships at the altar of price") contribute to, and then accelerate, the collapse in most asset classes

- Martha Reeves The Vandellas "Nowhere To Run"

"Concentrate on finding a big idea that will make an impact on the people you want to influence. The Ten Surprises, which I started doing in 1986, has been a defining product. People all over the world are aware of it and identify me with it. What they seem to like about it is that I put myself at risk by going on record with these events which I believe are probable and hold myself accountable at year-end. If you want to be successful and live a long, stimulating life, keep yourself at risk intellectually all the time."

-- Byron Wien

The creator of the annual Surprise List, Byron Wien, remains in my thoughts after his passing several years ago.

Two years ago, in preparation for the assembly of that year's Surprise List of my predictions for the year ahead, I paid homage to my dear pal.

Byron Wien, Wall Street Seer of the Unexpected, Dies at 90 - The New York Times

Here was my tribute to Byron on TheStreet Pro. May his memory be a blessing.

Without further ado, here are my 10 Surprises for 2026:

I won't bury the lede.

Pres. Trump, like The Godfather's Michael Corleone, becomes a wartime President — initially with no opposition in his Cabinet or in Congress (and without a wartime consigliere like Tom Hagen to smooth things over!)

”Goddamn it, if I had a wartime consigliere... a Sicilian...“ |The Godfather

After attacking Venezuela and failing to learn the expensive lessons of regime change attempts with Iraq and Afghanistan, Pres. Trump sees his popularity plummet. Like Corleone, Trump grows more unhinged and the Administration's rhetoric against Mexico's President (Claudia Sheinbaum Pardo) becomes more heated. Pres. Trump gives the Mexican President an ultimatum as an attack on that country is openly discussed on Truth Social. Other regimes, like that of Cuba's Miguel Diaz-Canel's (whose security forces are behind the protection of Venezuela's President Maduro), are also highlighted by the Administration as possible targets early in the year. With the cover of U.S. aggression, Russia becomes more aggressive against Ukraine (there is no peace) and China invades Taiwan in late Summer.

Separate from geopolitics the Epstein files uncover a deeper (and unsavory) relationship with Pres. Trump.

A week long investigative report entitled "Trump First (Not America First") by The Washington Post discloses how much the Trump family has profited from his Presidency. President Trump's base is fractured — his popularity moves to unprecedented and low depths as the Marjorie Taylor Greene-led America First movement permeates both political parties.

Several high-level Trump Administration resignations are announced in the first half of 2026. A number of senior Republican Senators and Congressman distance themselves from the President.

By mid-year impeachment is openly discussed. Surprisingly, four women — Marjorie Taylor Greene, Elise Stefanik, Alexandria Ocasio-Cortez and Elissa Slotnick — emerge as the leaders of their respective political parties. Georgia's Congresswoman Marjorie Taylor Greene doesn't disappear — just the opposite occurs. Greene becomes the titular leader of the "America First" movement of the Republican Party, which is at odds with MAGA:

The "America First" movement gains ever more prominence and popularity within the Republican Party. Marjorie Taylor Greene overtakes Vice President JD Vance in the polls as the likely next Republican Presidential Nominee. New York Congresswoman Alexandria Ocasio-Cortez takes a large lead in the polls to be the next Democratic Presidential Nominee. Michigan Sen. Elissa Slotnick becomes the leading moderate in the Democratic party.

New York Congresswoman Elise Stefanik (who, after stepping down from Congress, breaks with Pres. Trump and announces that she plans to run for Sen. Schumer's NY Senate Seat), becomes another important leader in the "America First" faction of the Republican Party, joining the growing ranks of her party who finally split ranks with Pres. Trump.

Another woman is in the limelight — as First Lady Melania Trump begins divorce proceedings against Pres. Trump. (This was a surprise last year that was wrong....) The divorce settlement is nearly $1 billion, calling further attention to how Trump has profited from his presidency. Pres. Trump unexpectedly resigns under the intense political, social (Epstein) and mainstream media pressure citing his deteriorating health as the reason.

Despite all of the Administration's woes (and that of the domestic economy), the Democratic Party fails to offer a coherent alternative message as the Party remains hostage to the Left. (New York City Mayor Zohran Mamdani, Senator Bernie Sanders and Congresswoman Alexandria Ocasio-Cortez denounce the apprehension of Venezuela President Maduro.)

In a surprise (considering all of the above factors adversely impacting Republicans), the Democratic Party (barely) wins a narrow majority in the House. The U.S. economy weakens as the year proceeds. By year's end unemployment rises above 5% and the consumer price index is back near 4%.

The 2026 deficit approaches a staggering $2.5 trillion (and U.S. debt exceeds $40.5 trillion).

A recession in 2027 appears likely.

Equities (led by the Magnificent Seven tech stocks) succumb to slowing economic and corporate profit growth, the reappearance of inflation, questionable foreign and domestic policy, growing political uncertainties, emerging "problems" for the hyperscalers (as AI capital spending plans are reduced) and elevated valuations.

The K-shaped economy's weakness in the lower income cohort spreads into the middle and upper middle class as the cumulative (or stacked) inflation since Covid finally has an impact — causing a spending freeze. With the outlook for global economic growth dissipating, consumer and business sentiment plummets. BNPL and credit defaults rise and auto repossessions increase dramatically.

Drawdowns in the global equity markets and a moribund housing market contribute to a negative "wealth effect" and an air pocket with the high end consumer as the investor optimism of 2023-25 is abandoned.

There is no place to run, no place to hide — most asset classes fall in the 2026 Bear Market.

Precious metals, commodities and crypto currencies all collapse (after a strong start early in the year) — in Martha Reeves' Revenge.

Bottom line: After starting the year positively, the S&P Index drops by more than 20% in 2026 — with three separate drops of -10%.

Kevin Warsh follows through with Pres. Trump’s view that the U.S. should have the lowest interest rates and cuts the Fed Funds rate to 2% by the end of 2026. At the same time he transfers the Fed’s mortgage holdings to government-sponsored enterprises and the Fed’s coupon holdings to the Treasury in exchange for short-term bills. He works relentlessly to shorten the duration of the Fed’s balance sheet and expresses a goal for 2027 to shrink it. The bond market cheers the more responsible balance sheet management and the 10-year bond rallies to 3.5% but Treasury supply/deficits keep the term premium elevated and the reappearance of inflation risk limits how far the long end can fall and the yield on the long bond remains stubbornly high.

Despite lower short interest rates, housing continues to suffer. After several years of rising prices, home prices are too high to attract adequate demand. Construction volumes suffer and homebuilders are caught with commitment to take delivery of lots from off balance sheet partners that they can’t fulfill. A housing prices war follows and the average new home prices falls 7%. Homebuilder stocks are down by greater than 25%. The resale market remains in the doldrums and volumes fall by 10%. Homebuilders such as Home Depot (HD) and Lowe's (LOW) , real estate brokers and furniture companies all collapse under the weight of lower home prices and slowing sales activity.

The AI bubble bursts as the circular financing deals unwind (or are pushed out) — AI capital spending slows abruptly as return on investment concerns emerge as power generation and grid modernization are bottlenecks. Depreciation charges and lower demand wrecks havoc with consensus AI 2026-27 earnings per share expectations. Another big AI surprise would be if China decides to flood markets with inexpensive AI models — pressuring the ultimate and expected robust ROI forecasts (which are already in question by some skeptics).

OpenAI's Sam Altman finds a place to live right next door to Sam Bankman-Fried. His effort to make OpenAI too big to fail, fails. ChatGPT turns out to at best be a commodity large language model purveyor. It becomes obvious to all that its recent $500 billion-plus valuation can’t be supported. Without an ability to do a down round without losing face, OpenAI loses all access to capital. Ultimately, a consortium of its customers and suppliers takes it over to modify its business plan and reduce the cash burn.

With Altman tossed to the curb (or worse), the prosecutions begin.

OpenAI’s problems pushes a deeply committed (to OpenAI) Softbank to the verge of collapse.

Nvidia shares fall by -40% as CoreWeave (CRWV) is driven into bankruptcy.

A basket of defensive consumer nondurable equities ( (PEP) , (KO) , (PG) and (KMB) ) materially outperform the Mag 7 by a decisive amount.

The shares of (boring and previously hapless) PepsiCo outperform most other staples and 90% of the S&P Index after a much better skein of organic unit growth and as its core business is rationalized.

With so many positioned on the same side of the (bullish) boat, retail investors begin to liquidate from equity funds — reversing the experience of the last few years. The movie of the last decade (of inflows) goes into reverse in 2026 — it's October 1987 (portfolio insurance was to blame) all over again. More than one quarter of the listed ETFs close during the year due to "indifference."

Yes, they “owe it to themselves,” but they also have paid themselves very little interest. With inflation a continuing problem the deficit situation comes to a head. Japanese 10-year rates cross 3% and the yen falls to 200. Facing the possibility of spiraling inflation and a collapsing currency, Japan organizes a global central bank intervention to stabilize the yen. The situation remains precarious at year end setting up for a possible crisis in 2027.

Valuation opacity, a compression in exit multiples and unrealistic net asset value marks (mark to model delays volatility but doesn't remove it) in private equity come into focus in 2026. The greatest problems are companies tied to commercial real estate and Saas companies. There are a number of high-profile bankruptcies in notable private equity portfolios.

A market for stranded LP interests trading at deep discounts becomes widely followed. Further, the IPO market continues to not be a viable exit for most holdings. Gated redemptions become common place. Apollo (APO) , TPG (TPG) , KKR (KKR) and Ares (ARES) each fall by 30%.

After reviewing a possible initial public offering with bankers, the government determines the current corporate structures can’t be reconciled with an IPO and without risking enormous litigation from legacy investors. So, the administration simply nationalizes them – thereby moving the litigation risk away from the enterprises.

Bill Ackman commences litigation that will keep him busy until 2035. The IPOs are ultimately successful and the biggest issuances of all time.

In the rapidly eroding 2026 equity market landscape, Warren Buffett's cash hoard at Berkshire Hathaway (BRK.A) (BRK.B) becomes a valuable gift to Greg Abel. Greg Abel announces that Berkshire Hathaway will begin to whittle down its investment portfolio as the future direction of the company is to purchase full ownership in companies (and not in making minority equity investments).

By the end of 2026, Berkshire Hathaway eliminates its entire holdings in Apple (AAPL) and Bank of America (BAC) . Berkshire Hathaway's shares disappointing recent performance (following Warren Buffett's "retirement") is reversed. The share price rises modestly in 2026 as the major indices drop significantly.

Half of the male population between 18 and 50 have a sports betting account. Nearly one quarter of the sports bettors say they are addicted. And one in five persons with a gambling addiction attempt suicide. Wagering on the next Federal Reserve Chairman, Pres. Trump's next tweet, whether the next pitch is a strike or a ball (or how many home runs NY Yankee Aaron Judge will hit, who will score the first Super Bowl point, etc.), invites corruption into every aspect of American life.

More professional teams and college teams are embroiled in "fixes." The shares of Robinhood (HOOD) , Caesars (CZR) , Flutter (FLUT) , MGM Resorts (MGM) , Draft Kings (DKNG) and other companies involved in gambling and predictive markets fall in half — as regulatory authorities begin to place new restrictions on the space.

A deteriorating equity market results in massive retail trading losses — from leveraged ETFs, zero-days to expiration options, etc. Calls for regulatory action (on leveraged ETFs and zero dated options) grow louder as YOLO and HODL become OHNO.

Many (including myself) have predicted that Pres. Trump’s second-term would be filled with unexpected, extreme and controversial policies that go much further than anything in his first term. Based on the last six months no one has been disappointed!

In early 2026, in a move that stuns even his own party, Pres. Trump in an attempt to stabilize his dwindling poll numbers, a weakening U.S. economy and a sharp drop in stock prices, "rewards" (his words) the country's economy in the hopes of furthering his bull market narrative — by abolishing short-selling in all individual U.S. equities (futures are still allowed to be shorted).

The president markets his Executive Order by stating "that you either own a stock or you don’t," prompting a very short-lived and violent rally in global markets. However, very soon after the announcement, his plan backfires as he fails to realize the enormous and leveraged hedges that exist in today's market. Those hedges are forced to be unwound in anticipation of the implementation of the Executive Order to eliminate equity shorts.

The decline in stocks quickly accelerate as Citadel, Susquehanna and Goldman Sachs (GS) (in particular) grow ever more aggressive in selling out their large hedged books. Market makers and quant strategies hedged books are ruined — their liquidation of their hedges add even more fuel to the avalanche of selling.

Global equities decline by more than -10% in the ensuing two months.

BY Doug Kass · Jan 5, 2026, 10:11 AM EST

* Only about 35% of my 2025 surprises proved accurate - a relatively weak showing

"A second argument is made that there are just too many question marks about the near future; wouldn't it be better to wait until things clear up a bit? You know the prose: 'Maintain buying reserves until current uncertainties are resolved,' etc. Before reaching for that crutch, face up to two unpleasant facts: The future is never clear; you pay a very high price in the stock market for a cheery consensus. Uncertainty actually is the friend of the buyer of long-term values."

-- Warren Buffett, Forbes (1979)

"The missing step in the standard Keynesian theory (is) the explicit consideration of capitalist finance within a cyclical and speculative context... finance sets the pace for the economy. As recovery approaches full employment... soothsayers will proclaim that the business cycle has been banished (and) debts can be taken on. But in truth neither the boom nor the debt deflation... and certainly not a recovery can go on forever. Each state nurtures forces that lead to its own destruction."

-- Hyman Minsky

"Every new beginning comes from some other beginning's end."

-- Seneca the Elder

I wrote in "Prelude First Movement" that I would be grading the surprises for 2025 that I unveiled a year ago.

In 2025 35% of my Surprises were on target. In 2024 less than one third of my Surprises proved prescient. In 2023 four of my first five most important surprises were accurate. (Nine out of my 15 Surprises were correct, a 60% success rate -- tying my best year ever.) As a means of reference, my worst hit rate was in 2013 when only 20% of my Surprises occurred. My best was over 60% in 2018. Below is a report card of my 10 Surprises for 2024:

Was it Iran? Was it the FBI? Was it the CIA, the NSA or just the deep state? No one finds out. The election is a big problem for many powerful vested interests and the swamp doesn't want to let itself get drained. Is the Secret Service even capable of protecting President Trump?

During the early Summer, Donald and Melania Trump announce their intention to divorce. It is revealed that a separation agreement was conceived several years ago. By the end of 2025, it is revealed that President Trump has been having a relationship (with a Democrat!). He publicly declares his desire to get remarried but divorce settlement negotiations with Melania extend and delay the divorce... and his fourth marriage.

Wrong!

National protests and demonstrations emerge and demands from a wide array of members of both the Republican and Democratic parties (including conservatives and liberals) call for "ousting" Elon Musk, an unelected official, from playing such a dominant role in the U.S. government.

Bernie Sanders, taking the Senate's mantle of opposition to Musk, tweets about Elon Musk's and other billionaires' outsized role in the government: "The precedent set in the last few months should upset every American who believes in our democratic form of government. In 2024, just 150 billionaire families spent almost $2 billion to purchase political candidates. Since the election in November, Elon Musk, Jeff Bezos and Mark Zuckerberg got $300 billion richer and are now worth $1 trillion combined. It appears that from now on no major legislation can be passed without the approval of Elon Musk, the wealthiest person in our country. That's not Democracy, it's Oligarchy. We must fight for an economy that works for all, not just the few. Elon Musk is an unelected official that is essentially acting a the President of the United States. We must pass legislation that changes this!"

Funded by George Soros, the law firm Boies, Schiller & Flexner launches a suit restricting the role of unelected officials without official positions in the Administration (like Elon Musk and Vivek Ramaswamy). The suit ends up going to the Supreme Court but is unresolved by year-end.

Reading the room (and increasingly uncomfortable with Musk's notoriety), President Trump begins to be openly critical of Musk and finally abandons him entirely.

Musk lashes out and retaliates by forming his own party and has a nervous breakdown. Separately, Tesla makes little progress in "full self driving." The U.S. government takes away the $7,500 tax credit, competition from China intensifies, unit sales drop by double digits and Tesla's profits collapse. In addition, an "accounting issue" (related to warranties) is uncovered by a short-oriented research boutique. All these factors cause the shares of (TSLA) to drop to $100/share.

Elon Musk's non-Tesla investments suffer from reduced U.S. government support.

Musk grows ever more unhinged throughout 2025 - his mother attempts a family intervention.

Right! The love fest between Trump and Musk did not last long and TSLA shares are slightly higher despite meaningful disappointments.

Starting with immigration, the U.S. southern border is simply shutdown at the beginning of his term and at least 2.5 million undocumented people are deported. There is a high-profile crackdown on a few employers. Jobs for the undocumented become harder to secure. Further, the various federal support and benefit programs for the undocumented becomes unavailable. Fewer jobs and benefits and the constant risk of being deported cause an additional 1.5 million people to self-deport. The economic implications are very inflationary for U.S. wages -- contributing to much higher inflation (see below). Certain industries like hotels and restaurants are particularly challenged to retain adequate labor. Low-end retail suffers, as the customers have fled the U.S. and low-end apartments develop vacancies.

President Trump takes back his "Drill, Baby, Drill" campaign promise. U.S. oil production continues to fall as shale basins top out and drillers focus on free cash flow. The price of oil rises to $85/barrel by mid-2025, aiding to inflationary pressures.

Right on immigration. Wrong on the price of oil.

However, an across-the-board 10% tariff is instituted - further contributing to additional inflationary pressure.

The bond vigilantes come out of hibernation and are ubiquitous next year.

Inflation reaccelerates and rises to above 4% by year-end 2025 (the yield on the 10 year Treasury note exceeds 5.5%) - the Administration considers price controls.

The Federal Reserve pauses in its rate cutting course and eventually reverses policy and tightens. President Trump attacks the Fed and seeks Jay Powell's resignation. Powell stands firm as Fed Chairman.

The U.S. economy enters a recession in late 2025/early 2026 following a continued weakening of the economies of the European Union and China.

Right on tariffs. Wrong on the Fed.

100% Right.

In contrast, the Democratic party grows more liberal (with California Governor Gavin Newsom temporarily taking up the party's de facto mantle of leadership). But, with Newsom moving further to the left (and going even softer on crime policies in his state), California's Governor falls in the polls by year-end and is no longer considered a party leader. The Democratic party appears rudderless, without any clear front runner.

This lays the groundwork for more Republican party political wins in 2026.

Former Vice President Kamala Harris leaves the political scene and accepts a professorship at Stanford University's Law School. Late in the year, Harris announces a plan to reenter politics but it is quickly rebuffed by the Democratic National Committee.

Right on the Democratic Party moving to the left. Wrong on Trump growing more moderate.

* With AI data centers so power-intensive and the AI arms race continuing apace - our nation's supplies of electricity prove inadequate. Power outages become common place and consumers' utility bills soar. With the need for the construction of new natural gas-driven power stations natural gas prices double (contributing to further inflationary pressure). A pissed off public demands action. In order to subsidize lower prices for households, large taxes are placed on AI data centers.

* As the year progresses it becomes clear that there is no material killer app or related revenue stream that is derived from the use of Generative AI. Focus shifts from being directed to consumers to helping corporations cut costs. This transition benefits tech integrators and consultants to the detriment of hyperscalers - the later ultimately recognizes that there is not an adequate revenue stream and scale back their capital outlays and budgets.

Nvidia's (NVDA) "day in the sun" abruptly ends and the share price falls to between $50-$75 in a matter of days as it grows clear that double and tripling ordering buoyed the company's past reported top and bottom lines. The view that other manufacturers "over earned" produces a contagion and a setting in which large cap stocks like Microsoft and other hyperscalers' share suffer similarly.

Wrong. (Maybe I was a year early?)

Though it is many years away from commercial use, the hype/hope cycle takes on a different subject and character. One of the important impacts will be to eventually hack proof of work crypto currencies including bitcoin. In time and if hacked, bitcoin becomes nearly worthless - and bitcoin collapses in price to under $25,000 in the late Summer. Most other secondary and tertiary crypto currencies fall to zero.

The collapse in cryptocurrency prices causes fear of financial contagion - and equities fall by nearly -7% in one month.

Right.

The technology-laden Nasdaq drops by over 20%. But the equal-weighted S&P Index RSP only declines by 5%.Under the weight of AI disappointment, higher interest rates, rising inflation and lower economic growth - financial and technology stocks are among the largest losers.

The Indexes close at their yearly low on the last day of 2025.

Wrong.

The Ukraine war is settled and there is peace in Israel. Israel and Saudi Arabia announce a new (and friendly) accord.

Wrong on Ukraine. Right on Israel.

Inflicting $250 billion -$500 billion in damages (roughly 10-times worse than Hurricane Katrina in 2005), the property and casualty industry is unprepared for such a catastrophic storm. With insufficient reserves and a move to forestall financial contagion, one of the top 10 property and casualty companies is bailed out by the U.S. government. The multi-year move to move away from globalization and towards reshoring in the U.S. backfires as another natural disaster (Covid being the first in early 2020) wrecks and disrupts supply chains in our country and causes another inflationary spike (already abetted by the wage inflation incurred from the deportation policy of the new Administration)).A dramatic reset higher in natural disaster insurance pricing harms home prices across the country -- serving to contain the rise in commodities and finished goods inflation. But with consumers questioning the value of their largest asset (their homes) coupled with a mortgage rate over 8%, consumer confidence collapses.

Wrong.

College football team takeover activity is initiated by Mark Lasry's Avenue Capital Group, which acquires 51% of Notre Dame University's football team for $700 million.

Blackstone purchases a majority interest in the largest and most valuable public sector's football team, the Ohio State University (for $1.5 billion, an offer that the school's trustees deem too large to turn down!), Kohlberg Kravis purchases more than half of (public) University of Alabama's football team for almost $1 billion.

Then, in a shocking move, billionaire investor and Pittsburgh native, David Tepper, acquires all of Carnegie Mellon University for an undisclosed amount.

But Wharton alum and Apollo CEO Marc Rowan is rebuffed in his attempt to have Apollo buy The University of Pennsylvania. Apollo settles on the purchase of 51% of Penn's football team for $175 million.

Senator Elizabeth Warren exclaims, "Isn't it enough that our country's billionaires own professional football teams!"

Even President Trump is irate. Soon thereafter, Congressional legislation prohibiting the acquisition of any private University is proposed and introduced into law.

Partially right.

The Google case is decided in late 2025 with significantly adverse effects on both Apple and Google — the shares of both plummet. The Trump Administration, appalled by the audacious acquisitions of some of the leading U.S. universities' football teams (and then by audacious attempts of private equity to acquire entire universities!) reacts by introducing regulatory and imposing strict capital actions against the private equity industry. Blackstone, Kohlberg Kravis and Apollo fall under the weight of these efforts.

Wrong.

Berkshire Hathaway eliminates its entire stake in Apple (AAPL) - selling all of its shares by mid-year.

Wrong. Though Berkshire dramatically reduced its stake in Apple.

* The LA Dodgers and New York Yankees meet again in the World Series. This time the Yankees sweep the Dodgers.

* Yankee Global Enterprises LLC (which is majority owned by the Steinbrenner family) sells a portion of the New York Yankees to Blackstone.

* Bill Belichick never coaches the University of North Carolina football team - as he is offered and accepts a NFL head coaching position.

* Deion Sanders leaves the University of Colorado and, he too, becomes an NFL head coach - replacing Mike McCarthy of the Dallas Cowboys.

* The heavily favored Super Bowl contender, the Kansas City Chiefs, get blown out in the first round of the NFL Playoffs. Shortly thereafter, similar to the famous 1973 wife swap It's 50th anniversary of Yankees' most insane swap ever of New York Yankees pitchers Fritz Peterson and Mike Kekich, Kansas City Chiefs' Patrick Mahomes and Travis Kelce switch partners ((Patrick Mahomes marries Taylor Swift and Travis Kelce marries Brittany Mahomes).

Wrong.

Next up, my 10 Surprises for 2026!

BY Doug Kass · Jan 5, 2026, 8:55 AM EST

* This is my 24th year of compiling my Surprise List!

* Nothing is more obstinate than a fashionable consensus.

* My Surprise List recognizes that, over the course of time, conventional wisdom is often wrong — as a society and as investors, we are consistently bamboozled by appearance and consensus.

* The real purpose of this endeavor is a practical one — that is, to consider positioning a portion of my portfolio in accordance with outlier events, with the potential for large payoffs on small wagers/investments.

* In Prelude #1 I discuss the history of my Annual List, why I embark on this exercise and some of the lessons I have learned (hint: the importance of thinking creatively and independently)...

"In this age of infinite distraction, when the entitled elect themselves, the party accelerates and the brutal hangover is inevitable."

-- Dr. Michael Burry (he profited from "The Big Short"), 2012 UCLA Commencement Speech

"Never make predictions, especially about the future."

-- Casey Stengel (also short in stature)

"Those who are easily shocked should be shocked more often."

-- Mae West (she liked only two types of men — long and short)

"You are neither right nor wrong because the crowd disagrees with you. You are right because your data and reasoning are right."

-- Legendary value investor Ben Graham (who in the short term recognized the market was a voting machine, not a weighing machine)

"Timid men prefer the calm of despotism to the tempestuous sea of liberty." [Think: Central-bank intervention!]

-- Thomas Jefferson (Founding Father and long of stature)

It's that time of the year again!

I will shortly be unveiling my 10 Surprises for 2026.

I've never walked the same path in my investment career that others have found comfortable, and I'm not going to start now. You see, I find beauty in a variant view. It's satisfying intellectually, analytically and financially, at least when you're correct. There's something special about adopting a non-consensus view and watching it become reality, despite protests from many corners. This notion forms the basis for my annual list.

The purpose of my annual list is to get readers to think more deeply about a variety of issues. As The Dude says in The Big Lebowski: "Yeah, well, you know, that's just, like, my opinion, man."

This year brings more out-of-consensus surprises.

By means of background and for those new to TheStreet Pro (formerly Real Money Pro), 24 years ago I set out and prepared a list of possible surprises for the coming year, taking a page out of the estimable Byron Wien's playbook. Byron was a longtime friend of mine who we lost in late 2023. Byron originally delivered his list while chief investment strategist at Morgan Stanley, then Pequot Capital Management, and finally at Blackstone.

It takes me about four weeks of thinking and writing to compile and construct my annual list. I typically start with about 40 surprises, which are accumulated during the months leading up to my annual column on the subject. I cull the list to come up with my final surprises that make it in print. The preparation of my list, as it was this year, often is not completed until the early hours before publication.

I often speak to, and get input from, some of the wise men and women whom I know in the investment and media businesses (you can probably guess some of their names — two of "the three stooges" (I am the third!) are among those that help most in the constructing of my list). My other go-to source are brilliant hedge-hogger pals who think out of the box and have successfully navigated many market and economic cycles.

I always have associated the moment of writing the final draft, in the weekend before publication, of my annual list with a moment of lift, of joy, and hopefully with the thought of unexpected investment rewards in the new year. This year is no different. I think this year's list is pretty intriguing and many of the surprises have a good chance of occurring!

I set out as a primary objective for my list to deliver a critical and variant view relative to consensus that can provide alpha or excess returns. The publication of my annual list is in recognition that economic and stock market histories have proven that more often than generally thought, consensus expectations of critical economic and market variables may be off-base.

History demonstrates that inflection points are relatively rare and that the crowds often outsmart the remnants. In recognition, investors, strategists, economists and money managers tend to operate and think in crowds. They are far more comfortable being a part of the herd rather than expressing — in their views and portfolio structure — a variant or extreme vision.

It is important to emphasize that these are not forecasts. Rather, they are events with a greater than a 50% chance of occurring that are deemed deeper outlier events, with a probability of 25% or less, relative to consensus expectations. In other words, my Surprises are anti-"Group Stink."

Confidence is the most abundant quality on Wall Street as, over time, stocks climb higher. Good markets mean happy investors and even happier investment professionals.

The factors stated above help explain the crowded and benign consensus that every year seems to begin with, whether measured by economic, market or interest-rate forecasts. But an outlier's studied view can be profitable and add alpha.

Consider the course of interest rates and commodities in 2014, which differed dramatically from the consensus expectations. And consider my outlier view in late 2014 that the drop in oil prices would fail to help the economy and that OPEC would come close to dissolution and oil prices would plummet. An investor could have done quite well by following that message of avoiding energy stocks over the last few years. Or consider the value of my surprise that in 2019 the Federal Reserve would reverse its stance and cut rates, leading to a 2.25% yield on the 10-Year U.S. note. That surprise was in marked contrast to the almost universal view that the Fed would tighten and interest rates would rise.

To a large degree, the business media perpetuates group-think and coddles investors, often into a false sense of security. Consider the preponderance of bullish talk in the financial press. All too often the opinions of guests who failed to see the crippling 2007-2009 drama are forgotten and some of the same, and previously wrong-footed talking heads are paraded as seers in the media after continued market gains in recent years. Memories, it seems are short, especially of a media kind. Nevertheless, if a criterion for appearances was accuracy, there would have been few available guests in 2009-2010 or in 2025 qualified to appear on CNBC, Bloomberg and Fox Business Network.

***

Abba Eban, the Israeli foreign minister in the late 1960s and early 1970s, once said that the consensus is what many people say in chorus but do not believe as individuals.

GMO's James Montier, in an excellent essay published several years ago, made note of the consistent weakness embodied in consensus forecasts:

"Economists can't forecast for toffee... They have missed every recession in the last four decades. And it isn't just growth that economists can't forecast; it's also inflation, bond yields, unemployment, stock market price targets and pretty much everything else... If we add greater uncertainty, as reflected by the distribution of the new normal, to the mix, then the difficulty of investing based upon economic forecasts is likely to be squared!"

"I'm astounded by people who want to 'know' the universe when it's hard enough to find your way around Chinatown."

-- Woody Allen

"Let's face it: Bottom-up consensus earnings forecasts have a miserable track record. The traditional bias is well-known. And even when analysts, as a group, rein in their enthusiasm, they are typically the last ones to anticipate swings in margins."

-- UBS (Top 10 Surprises for 2012)

There are five important and core lessons I have learned over the course of my investing career that form the foundation of my annual surprise lists:

Again, it's important to note that my surprises are not intended to be predictions, but rather events that have a reasonable chance of occurring despite being at odds with the consensus. I call these "possible-improbable events." In sports, betting my surprises would be called an "overlay," a term commonly used when the odds on a proposition are in favor of the bettor rather than the house.

The real purpose of this endeavor is a practical one — that is, to consider positioning a portion of my portfolio in accordance with outlier events, with the potential for large payoffs on small wagers/investments.

Since the mid-1990s, Wall Street research has deteriorated in quantity and quality due to competition for human capital at hedge funds, brokerage industry consolidation and a rapid decline in institutional commission rates. It remains, more than ever, maintenance-oriented, conventional and group-think — or group-stink, as I prefer to call it. Mainstream and consensus expectations are just that and, in most cases, they are deeply embedded into today's stock prices.

It has been said that if life were predictable, it would cease to be life, so if I succeed in making you think, and possibly position, for outlier events, then my endeavor has been worthwhile.

Nothing is more obstinate than a fashionable consensus, and my annual exercise recognizes that, over the course of time, conventional wisdom is often wrong. As a society and as investors, we are consistently bamboozled by appearance and consensus.

Ayn Rand put it well:

"You can ignore reality, but you cannot ignore the consequences of ignoring reality."

Too often, we are played as suckers, as we just accept the trend, momentum and/or the superficial-as-certain truth without a shred of criticism. Just look at those who bought into:

But enough of the rant.

In the second movement of the Prelude to My 10 Surprises for 2026, I will issue a report card on my top 2025 surprises.

BY Doug Kass · Jan 5, 2026, 7:30 AM EST

Bonus — Here are some great links:

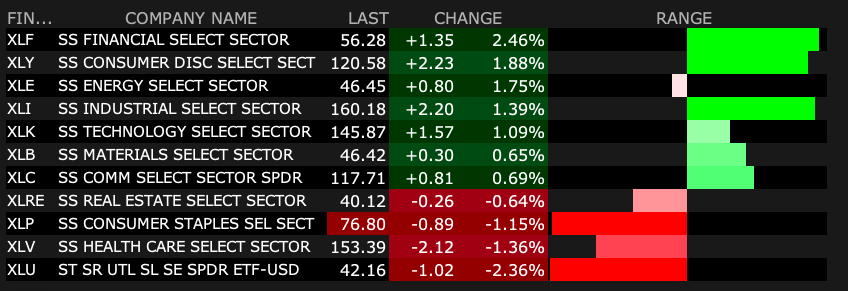

Before You Call a Top, Check the Sectors

Five Charts That Will Define The Markets This Year

BY Doug Kass · Jan 5, 2026, 6:45 AM EST

I'm not surprised the market is up tonight but my bottom line it should end tomorrow lower on the day.

I say that because I think the world is a risker place.

But could be very positive.-- you can't tell now.

What you know now is our fiscal condition is going to be worse as we pursue a guns and butter approach (I added the following tweet):

The President at the same time can be praised and criticized.

BY Doug Kass · Jan 5, 2026, 6:15 AM EST

BY Doug Kass · Jan 5, 2026, 6:05 AM EST

Back shorting the indices:

* (SPY) $685.10

* (QQQ) $616.95

BY Doug Kass · Jan 5, 2026, 5:55 AM EST

The S&P Short Range Oscillator remains overbought at 1.34% vs. 0.34%.

BY Doug Kass · Jan 5, 2026, 5:47 AM EST