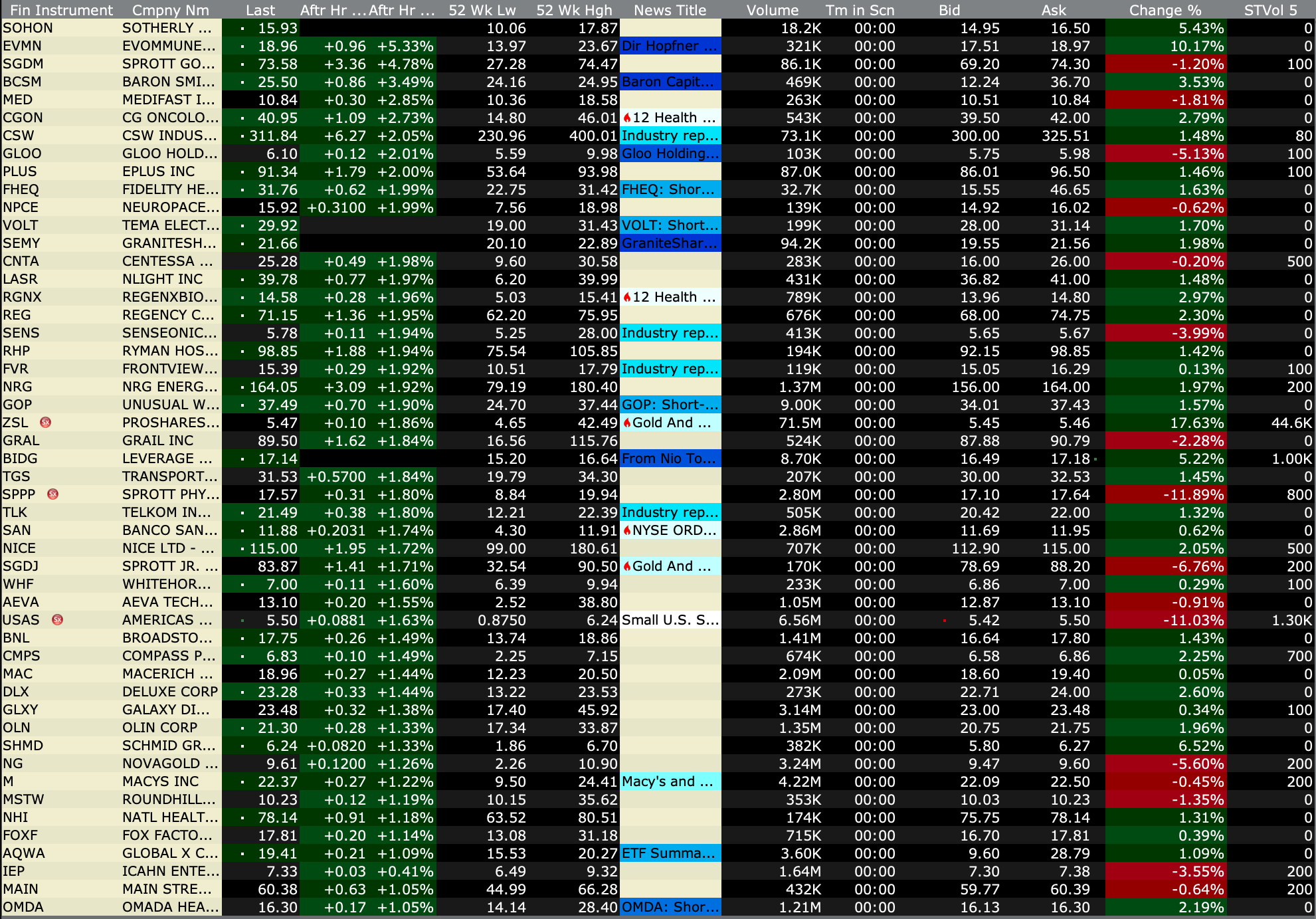

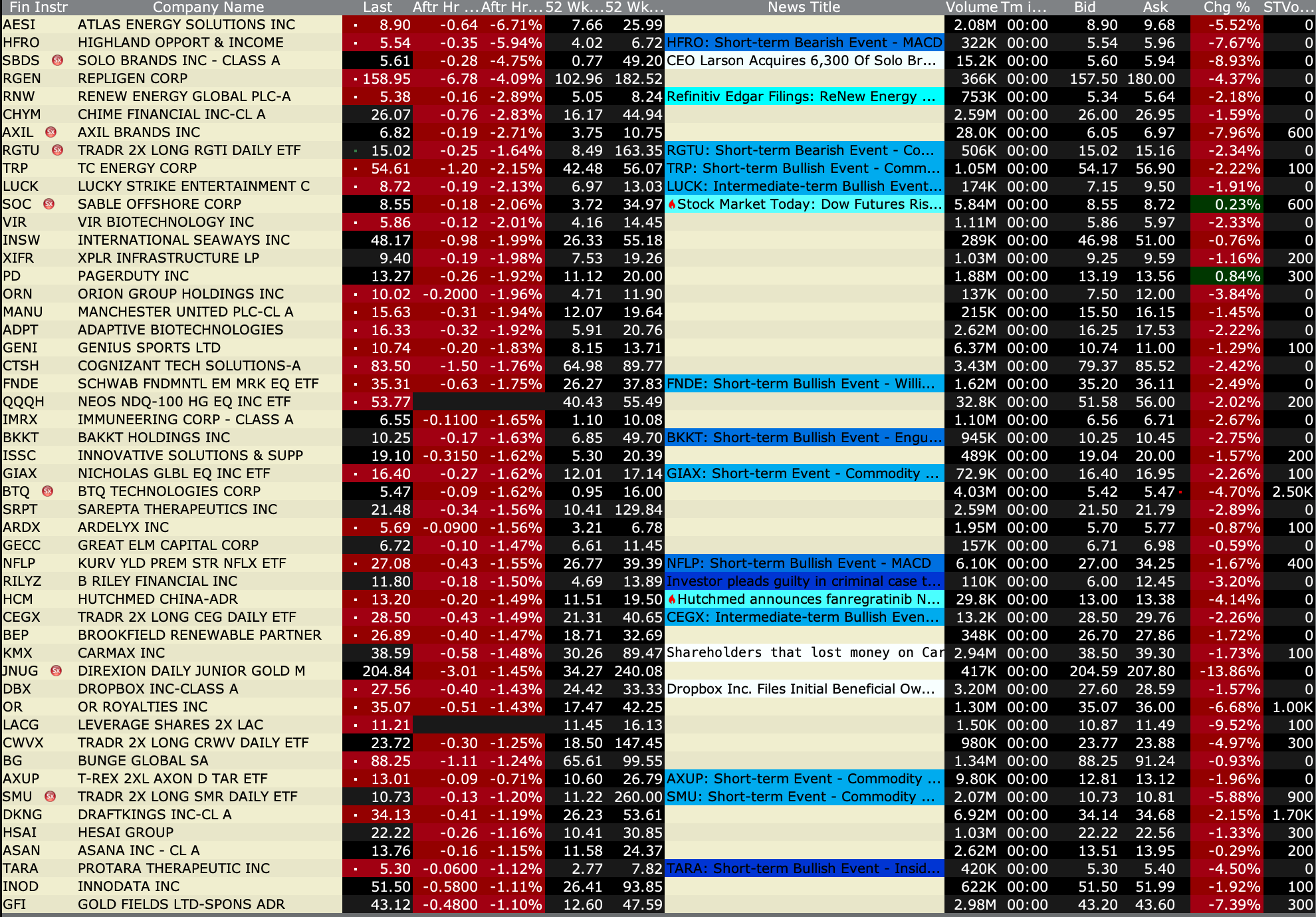

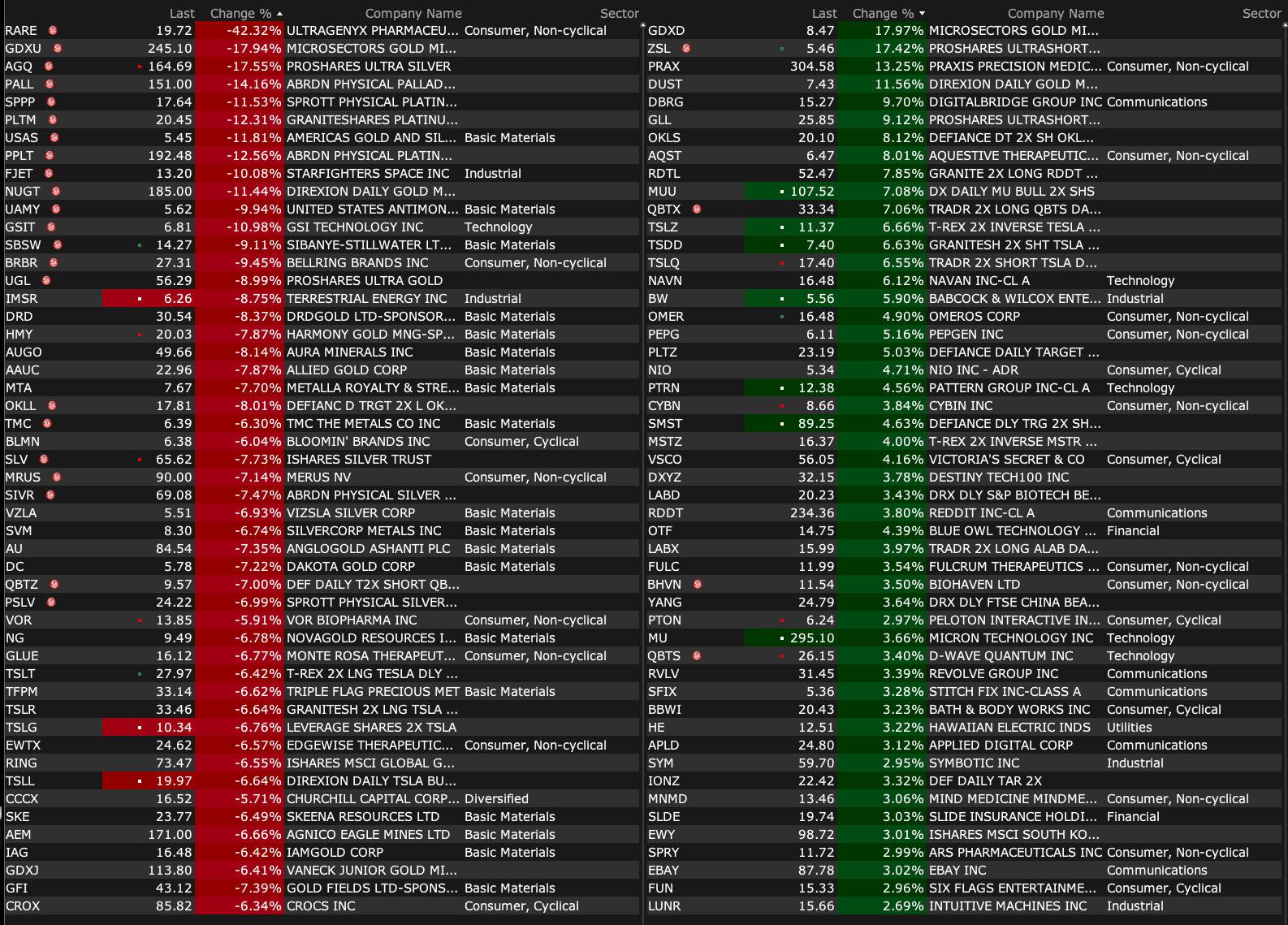

After-Hours Gainers, Losers

After-Hours % Gainers

After-Hours % Losers

BY Doug Kass · Dec 29, 2025, 4:50 PM EST

BY Doug Kass · Dec 29, 2025, 4:50 PM EST

BY Doug Kass · Dec 29, 2025, 4:40 PM EST

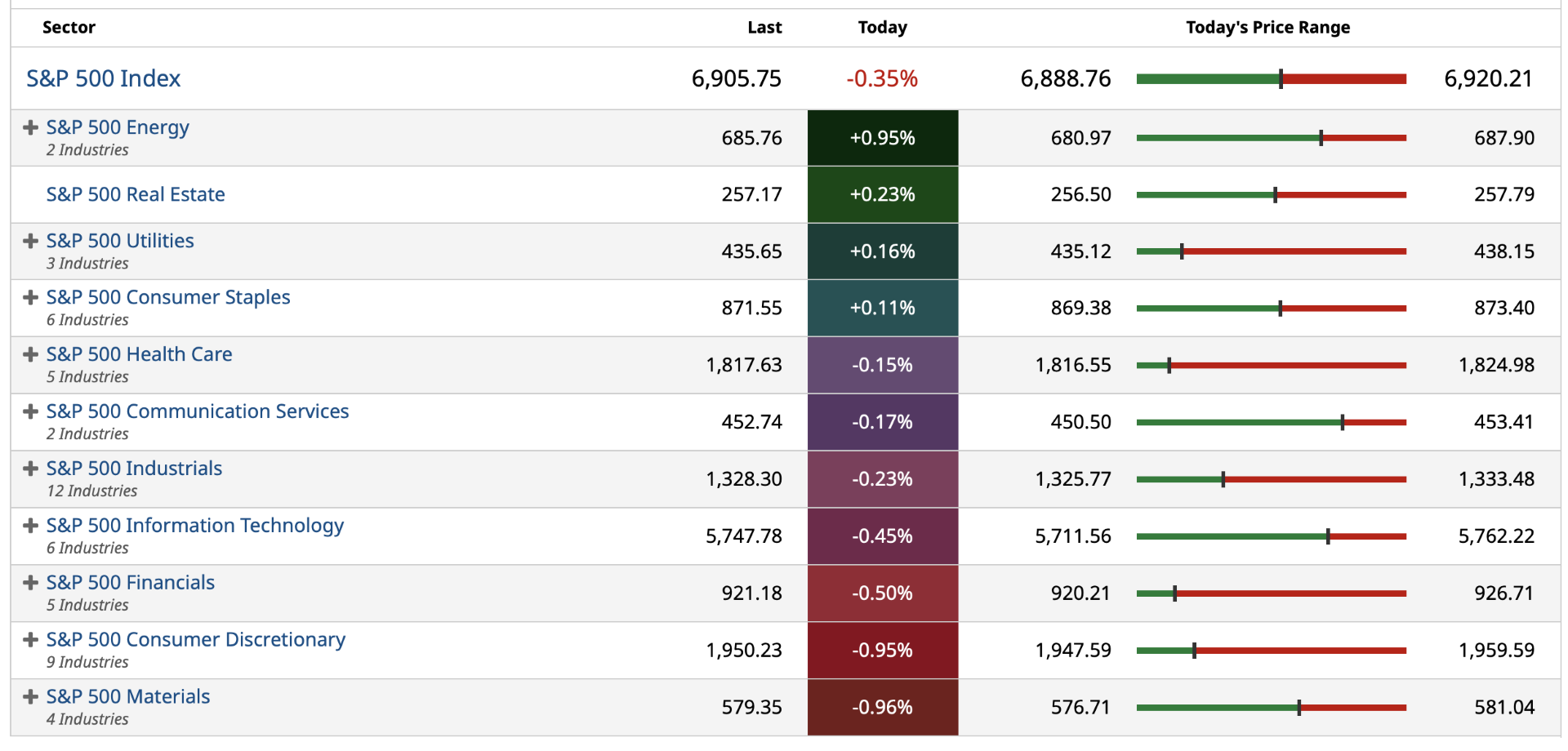

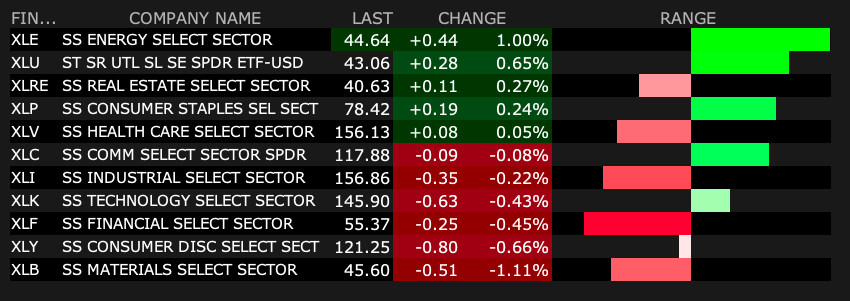

- NYSE volume 25% below its one-month average

- NASDAQ volume 17% below its one-month average

- VIX index: up 4.34% to 14.19

BY Doug Kass · Dec 29, 2025, 4:30 PM EST

Dougie Kass

Reshorted PLTR, FRHC and MSTR (VS) today - low keying it as i placed it only in the Comments Section because I don't want anyone to follow me into this pool of speculative equities (on the short side)...

Dougie Kass

With S&P cash -17 handles I am beginning (baby steps) to reshort Index calls.

I plan to give the market a wider berth than usual given year end on Wednesday afternoon.

BY Doug Kass · Dec 29, 2025, 4:10 PM EST

* A 4% dividend yield and operating upside at only a 16x forward multiple

"Cheeseburger, Cheeseburger! ... No Orange or Coke Today, Four Pepsi"

The Olympia Restaurant: Cheeseburger, Chips and Pepsi - SNL

In the next few weeks investors will be bombarded with analysts' favorite picks for the coming year. No doubt, the list will include a number of spicy and aggressive names in AI and in other areas. You will not find that character in my annual stock pick.

On the surface it might seem absurd to choose PepsiCo (PEP) — a defensive, consumer staples name to be my stock pick for 2026.

However, my choice is, in part, in anticipation of a (potential) negative return for the S&P 500 and Nasdaq indices for the upcoming 12 months — coupled with a possible turnaround in operations at PepsiCo.

Like many consumer nondurable companies, PepsiCo's shares have been a serial underperformer over the last few years for several reasons:

* Defensive stocks have underperformed in an offensively driven investing backdrop in which large-cap technology have represented the market's leadership.

* Food and beverage equities have suffered from reduced snack consumption (GLP-1 and broader health & wellness pressures) and volume trends have been moribund. PepsiCo, in particular, has faced structural challenges in beverages (Mountain Dew and Gatorade brands).

* Expectations are low.

Elliott Investment Management took a $4 billion stake in PepsiCo back in September and outlined a comprehensive 75-page presentation. Elliotts-Perspectives-on-PepsiCo-Presentation.pdf

As seen in their release, the activist firm proposed a series of changes around the company's Frito-Lay North America operations intended to improve the beverage company's competitiveness and financial performance of Pepsi Foods North America. The recommendations included implementing sharper everyday value through price adjustments, elevating innovation and aggressively lowering operating costs.

Elliott creates a sense of urgency for change at PepsiCo.

Three weeks ago PepsiCo management responded to Elliott and announced some initiatives and financial goals aimed at enhancing shareholder value. The 2026 EPS guidance was better than feared and management plans to improve free cash flow conversion and better operating margins were outlined (an improvement of 100 basis points over the next three years).

Here is the company's guidance: PepsiCo Announces Priorities to Enhance Shareholder Value and Provides Preliminary 2026 Financial Outlook

Elliott Management's response to PepsiCo's December 9 plan:

"We appreciate our collaborative engagement with PepsiCo’s management team and the urgency they have demonstrated."

Here is Morgan Stanley's response to the company's December 9 plan:

Initiatives Focused on Value, Innovation, and Costs/Operations - From Morgan Stanley

PEP highlighted PFNA initiatives to sharpen everyday value, elevate innovation, and aggressively reduce operating costs, many of which were already underway since earlier this year. In terms of value, PEP is implementing sharper everyday value through targeted affordable price tiers by brand and channels aimed at stimulating growth and purchase frequency for its mainstream brands. In terms of innovation, PEP reiterated its focus on permissible, as well as functional offerings with no artificial colors/flavors, simpler ingredients, more protein, as well as fiber and whole grains and the restaging of Lay's and Tostitos, and a Doritos Protein launch in 2026. On the cost side, PEP plans to continue to aggressively reduce operating costs and improve operational excellence (PEP has already closed three manufacturing plants and shut several manufacturing lines this year and is in the process of reducing ~20% of SKUs in the US by early next year), with savings to support investments in A&M and value. PEP noted solid retailer support for its commercial plans, and that it expects shelf space to increase in 1H26.

"You can't get killed falling off the curb."

- Grandma Koufax

Reflecting the well-known product threats, PepsiCo's valuation has rarely been more depressed — at 16x estimated 2027 calendar EPS (down from 24x in 2020 and at a 20% discount to its multi-year mean valuation). The cash flow multiple to enterprise value has fallen from 16x to only 13x in the last five years.

With expectations so low, any surprise to the upside will likely be greeted quite favorably.

It might surprise some, given PepsiCo's market position and history, that the company's market valuation is currently less than $200 billion (or only about 2x 2026 sales).

PepsiCo recently increased its dividend by +5% to $5.69/share — providing a healthy dividend yield of 4%.

A reasonable price target of 18x 2027 projected EPS (still about 10% below peers Procter & Gamble (PG) and Coca-Cola (KO) ) produces a $165 share objective (vs. current share price of around $143). If achieved, this is a possible return in excess of +20%.

Here is a summary of three recent sell side upgrades (in price targets):

PepsiCo price target raised to $164 from $155 at BofA BofA analyst Peter Galbo raised the firm's price target on PepsiCo to $164 from $155 and keeps a Neutral rating on the shares. Entering 2026, the largest unresolved question for staples remains consumption growth and valuations remain dispersed across the group, but "there feels little to get them off the sidelines in '26 until fundamentals signal a greater turning of the tide," the analyst tells investors in a year-ahead note for the consumer staples group.

PepsiCo price target raised to $170 from $165 at Citi Citi analyst Filippo Falorni raised the firm's price target on PepsiCo to $170 from $165 and keeps a Buy rating on the shares. The firm adjusted targets in the beverages, household and personal care sector as part of its 2026 outlook. Citi is shifting from a bullish stance on the non-alcoholic beverage space throughout 2025 toward favoring the household and personal care names. It sees improving fundamentals for the group due to the cycling of inventory destocking and easier consumption compares.

PepsiCo upgraded to Overweight from Neutral at JPMorgan JPMorgan analyst Andrea Teixeira upgraded PepsiCo to Overweight from Neutral with a price target of $164, up from $151. The firm believes the company's "accelerated agenda" of innovation and marketing spending will drive strong productivity savings. This should position PepsiCo to drive high-single-digit total shareholder return in 2026, which benchmarks well against its high-quality peers, the analyst tells investors in a research note. Meanwhile, JPMorgan says the shares are trading a "steep discount" relative to the group.

BY Doug Kass · Dec 29, 2025, 2:50 PM EST

BY Doug Kass · Dec 29, 2025, 12:40 PM EST

BY Doug Kass · Dec 29, 2025, 12:12 PM EST

Bored with Bloomberg, CNBC and Fox Business?

Want some tradeable ideas from two friends who are savvy, analytical, humble and take ownership for their losers and don't gloat about their winners?

Well ... check out MRKT CALL with Guy and Dan.

Run, don't walk (at 11 AM) to watch MRKT Call - Monday, December 29th

BY Doug Kass · Dec 29, 2025, 11:20 AM EST

- NYSE volume 12% below its one-month average

- NASDAQ volume 16% below its one-month average

- VIX index: up 6.91% to 14.54

BY Doug Kass · Dec 29, 2025, 10:58 AM EST

* Been active! Phew!

Here are today's things:

* I covered (SPY) and (QQQ) common shorts at $687.64 and $619.85, respectively.

* Back shorting index common SPY at $689.08 and QQQ at $622.33 (then converted to short calls for a profit).

* I shorted (GS) at $907.26 and (MS) at $181.65.

* I shorted more (JPM) at $328.13.

* I added to (KMB) at $101.05 and (PEP) at $143.89.

BY Doug Kass · Dec 29, 2025, 10:11 AM EST

I have converted my index common shorts to call shorts.

BY Doug Kass · Dec 29, 2025, 9:55 AM EST

I am now shorting index calls as well as common — with S&P cash -14 handles.

BY Doug Kass · Dec 29, 2025, 9:52 AM EST

I added to PepsiCo (PEP) at $143.89 and Kimberly-Clark (KMB) at $101.05 longs this morning.

Sidenote: PepsiCo is my 2026 Stock Pick of the Year!

BY Doug Kass · Dec 29, 2025, 9:50 AM EST

With S&P cash rallying off the lows and now only -13 handles I am back shorting the Indices:

* (SPY) $689.08

* (QQQ) $622.33

BY Doug Kass · Dec 29, 2025, 9:44 AM EST

* This morning we consider and take note of the wise words of Yogi Berra, Lt. Columbo, George Orwell, Howard Marks, Dr. Robert Shiller, Warren Buffett and Herman's Hermits...

"We have now sunk to a depth at which restatement of the obvious is the first duty of intelligent men."

- George Orwell

As I prepare my year-end Surprise List, I embrace Yogi Berra's quote (used in the header of this column above) and I would caution how overvalued equities are:

* Every Wall Street strategist is bullish. They are nearly always bullish, so their opinions should be taken accordingly — and with a grain of salt.

* The equity risk premium — which has historically been an excellent forecaster of future equity returns — is now a discount. This means that the market is pricing more risk in bonds than in stocks!

* Historical valuation metrics are at about the 97%-tile. Indicators like the Buffett Ratio, Shiller CAPE and Price/Sales are at all-time overvalued readings.

* Dividends typically account for a bit more than 35% of the total return of stocks. The S&P Dividend Yield is now at a multi-decade low of 1.12% — contributions from dividends are modest — likely leading to substandard returns for an extended period of time.

* The composition of equity returns remains out of balance with a small number of large-cap technology stocks (highly dependent on the AI trade) contributing to overall returns.

* Margin debt, like valuations, is at a record high — inflating the indices by borrowed money. Any reversal in market sentiment could trigger an unwind of this leverage which could cascade in a market dominated by passive products and strategies that worship at the altar of price and momentum. The recent unwind in the leveraged cryptocurrency markets might foreshadow what may happen in equities in 2026.

From Howard Marks:

The above conditions incorporate some of my concerns over the next few years.

After Friday's close we observed some near-term concerns (breadth, volume, participation, unfriendly bonds):

"Just one last thing."

-Lt. Columbo

"I'm Henery The Eighth, I Am! Henery The Eighth, I Am, I am!

I got married to the widow next door,

She's been married seven times before.

And ev'ryone was a Henery,

She wouldn't have Willie or a Sam.

I'm her eighth old man named Henery,

Henery the Eighth, I Am!

Second verse same as the first!"

-Herman's Hermits, "Henry The VIII, I Am" Herman's Hermits "Henry The VIII, I Am" on The Ed Sullivan Show

Much like the last several days...

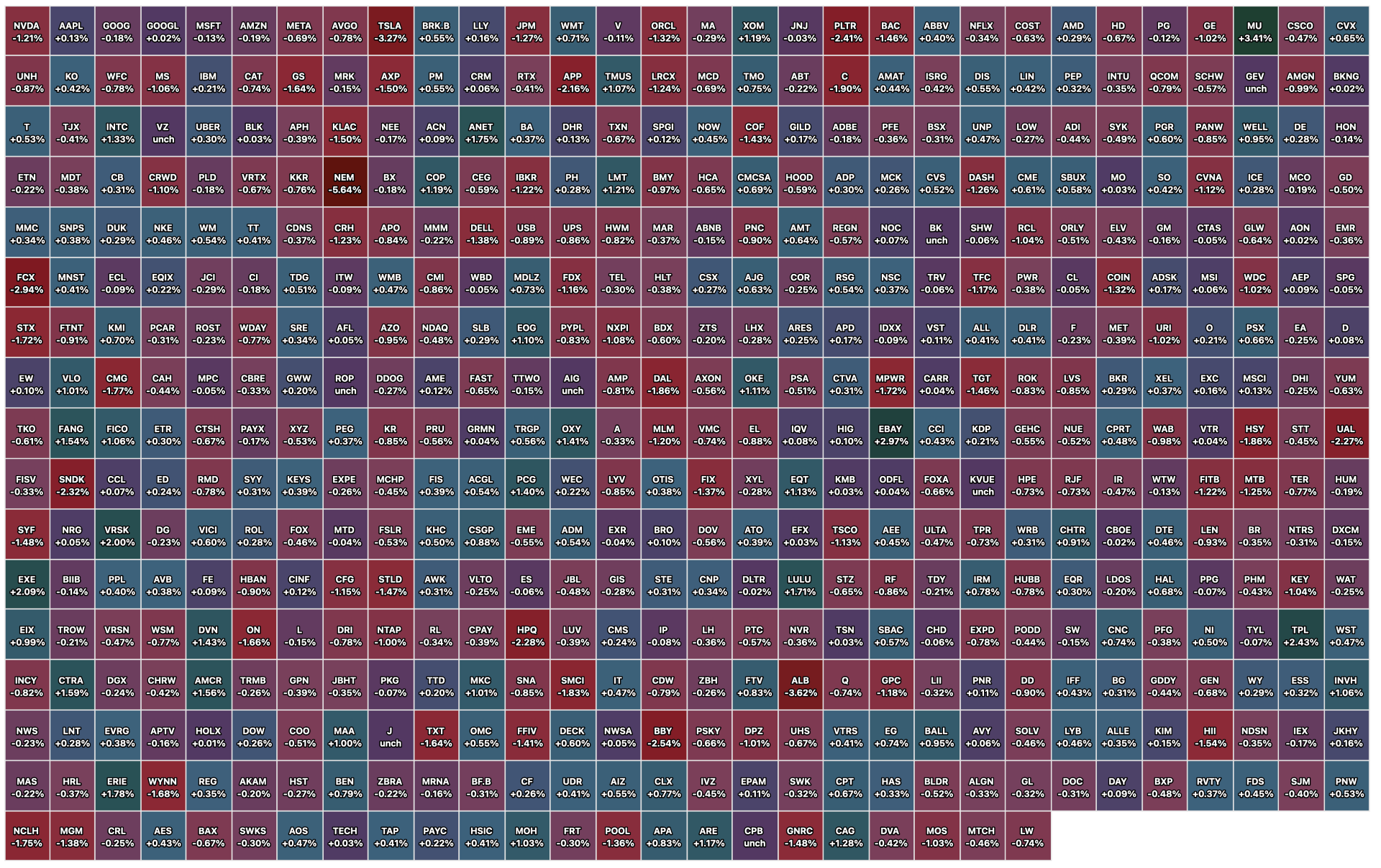

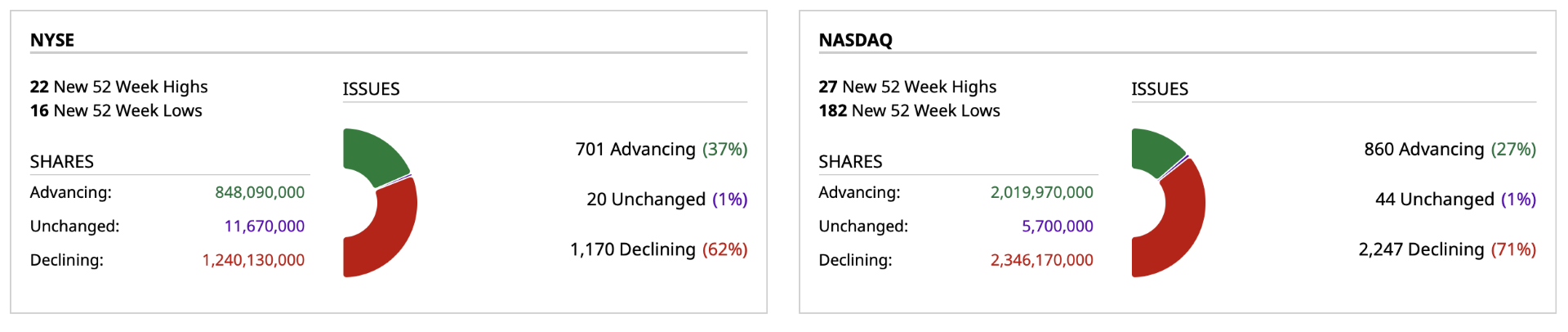

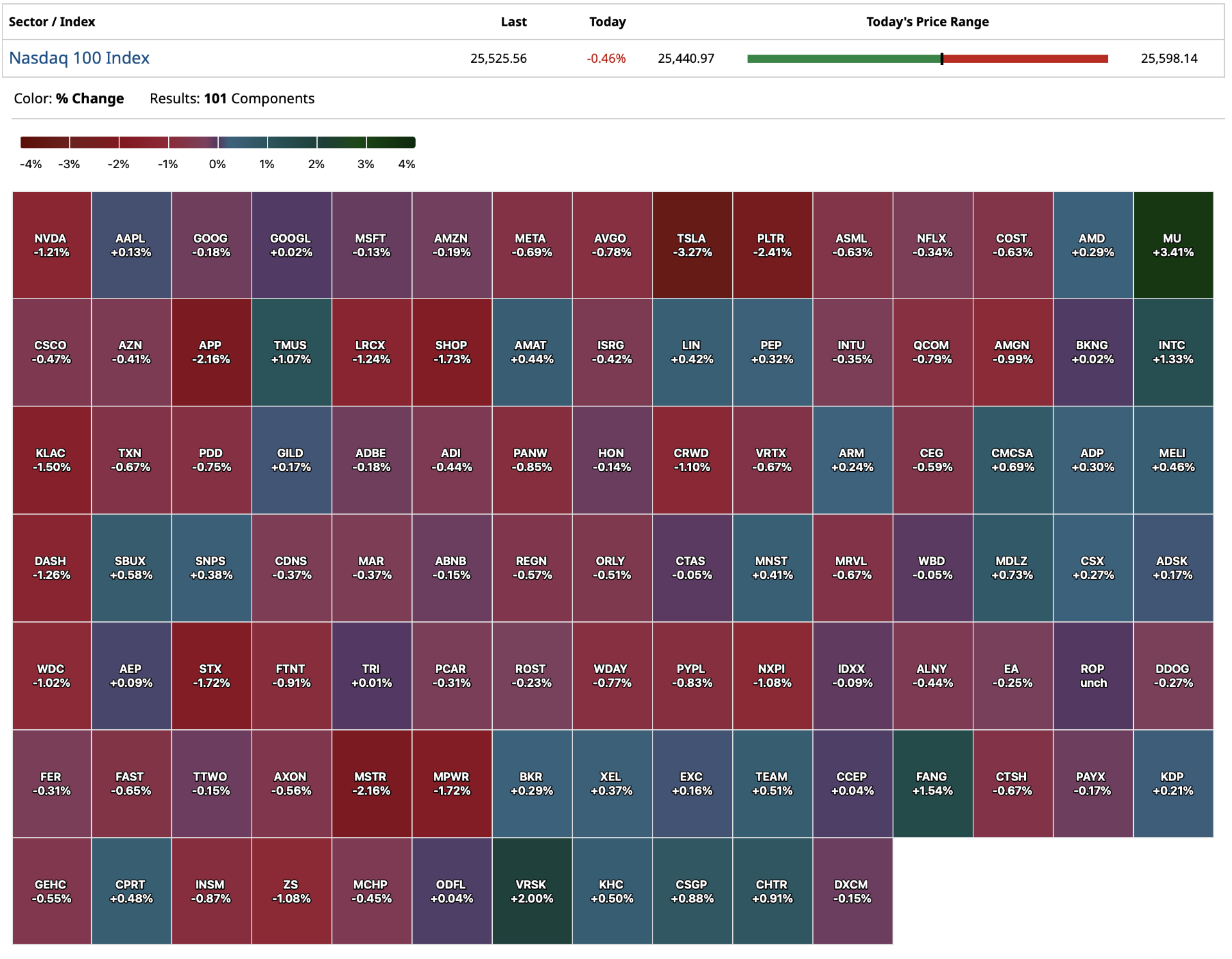

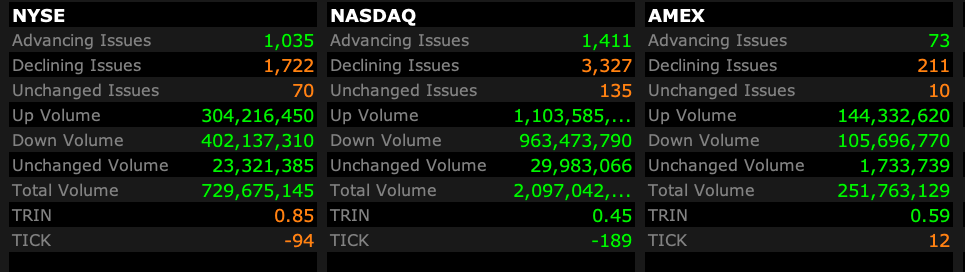

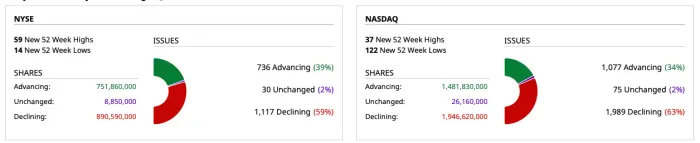

* Market breadth was weak (especially on the Nasdaq where it was two-to-one negative):

* Volume was low - about 40% below the one month average on both the NYSE and Nasdaq.

* Bond prices closed down and near the lows of the day.

Until it does matter.

By Doug Kass Dec 26, 2025 5:05 PM EST

BY Doug Kass · Dec 29, 2025, 9:30 AM EST

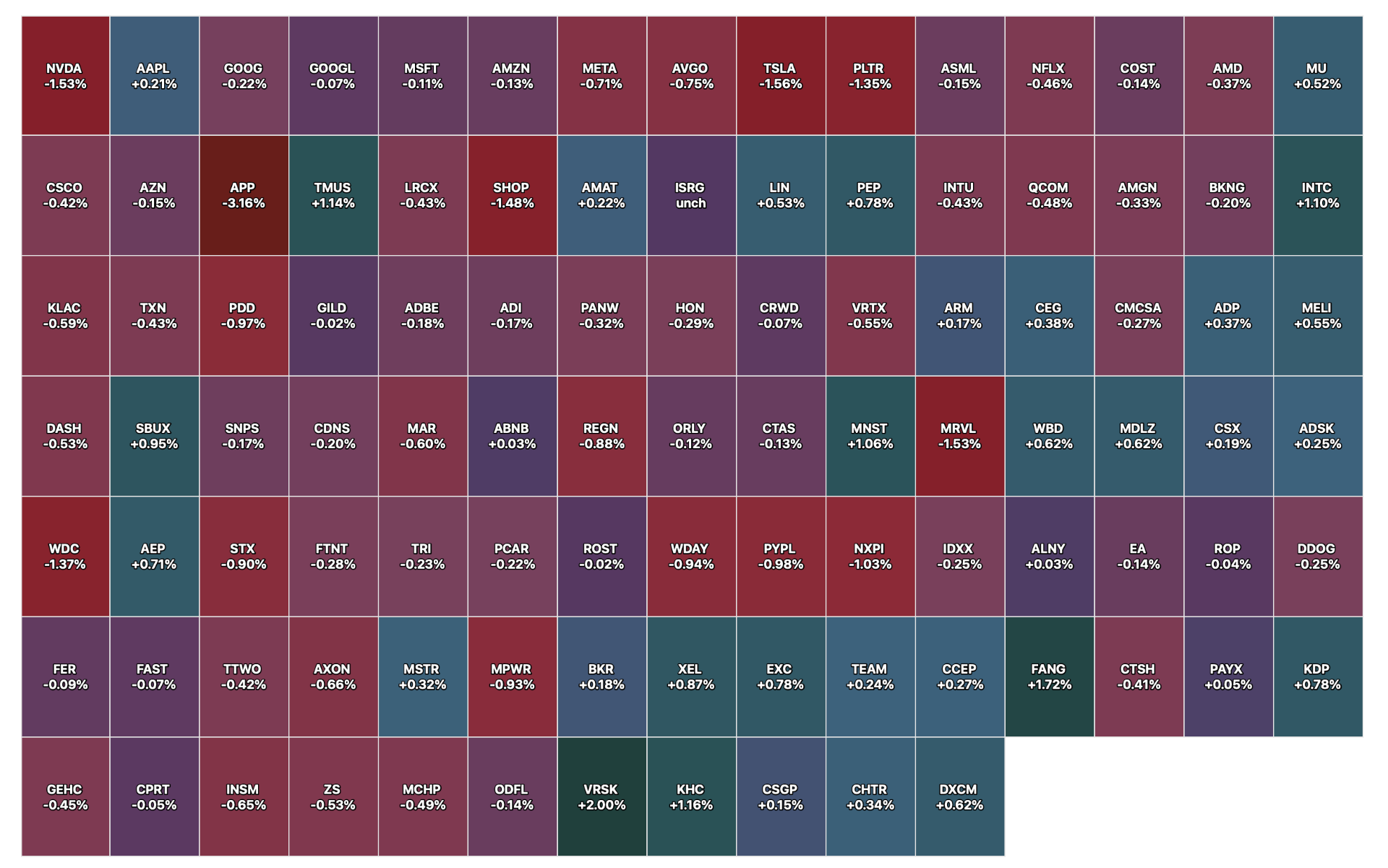

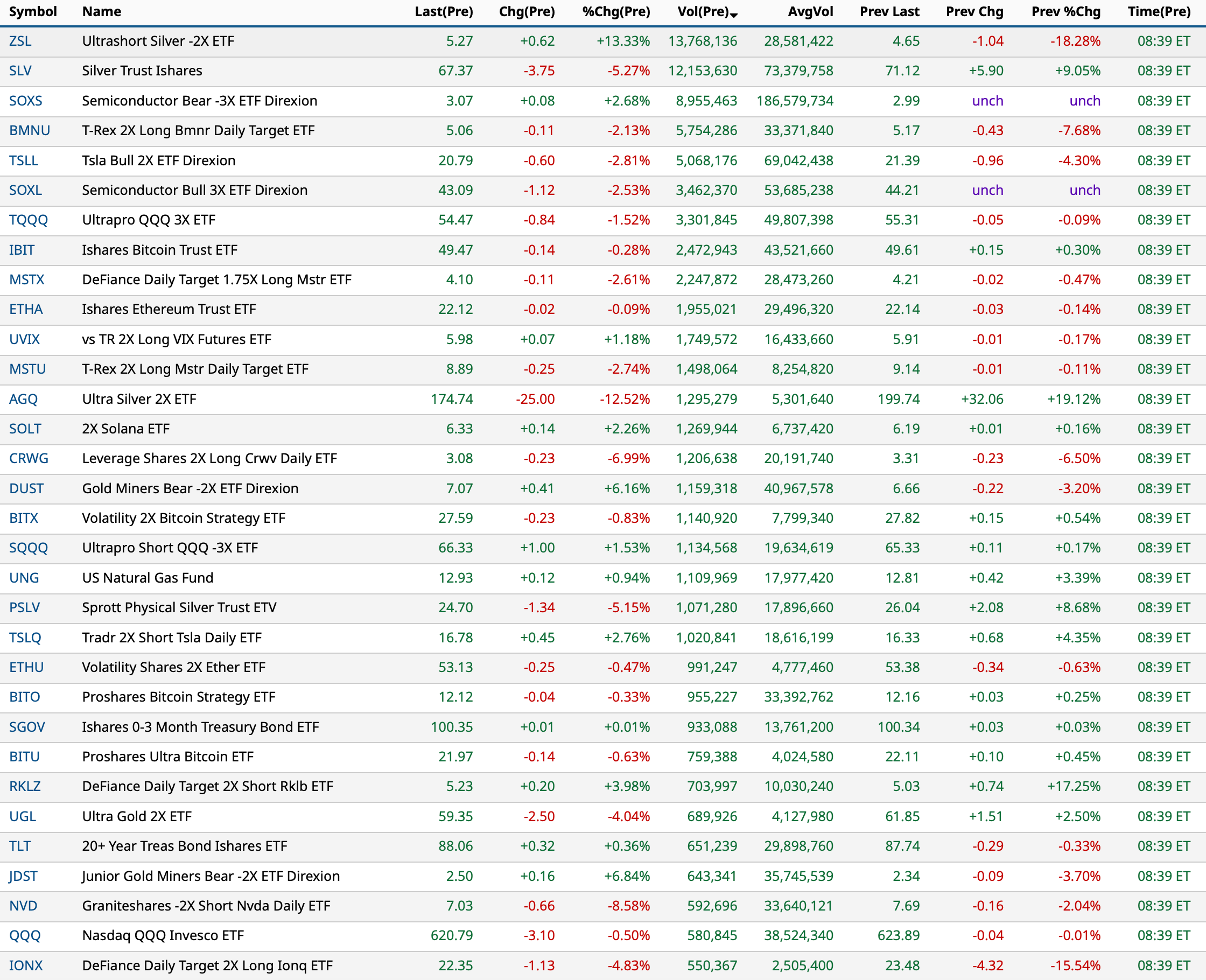

As of 8:39 AM:

BY Doug Kass · Dec 29, 2025, 9:20 AM EST

-DBRG +31% (Softbank acquires DigitalBridge for $4B enterprise value)

-TAOP +14% (relocates headquarters and secures $2M smart elevator contracts)

-PRAX +9.8% (FDA Grants Breakthrough Therapy Designation to Praxis Precision Medicines' Ulixacaltamide for Essential Tremor)

-PHGE +7.5% (announces $3M private placement financing)

-KYIV +3.0% (higher off prospect of potential Ukraine peace agreement)

-CPNG +2.9% (announces customer compensation plan related to previously disclosed data breach)

-INO -7.9% (not currently planning to hold an Advisory Committee meeting to discuss INO-3107 application)

-AXTI -7.7% (prices public offering of 7.1M shares at $12.25 each)

-HL -4.2% (silver stock weakness following silver’s pullback from record high prices)

-CDE -4.0% (silver stock weakness following silver’s pullback from record high prices)

-RARE -3.3% (Phase 3 Orbit and Cosmic studies failed to meet primary endpoints for Setrusumab (UX143) in Osteogenesis Imperfecta)

BY Doug Kass · Dec 29, 2025, 9:10 AM EST

I just took in the balance of my index shorts with S&P futures -31 handles.

BY Doug Kass · Dec 29, 2025, 8:58 AM EST

With S&P futures -33 handles and Nasdaq futures -195 handles I am taking in half of my index shorts (moving from medium to small-sized):

* (SPY) $687.06

* (QQQ) $619.07

BY Doug Kass · Dec 29, 2025, 8:57 AM EST

BY Doug Kass · Dec 29, 2025, 8:55 AM EST

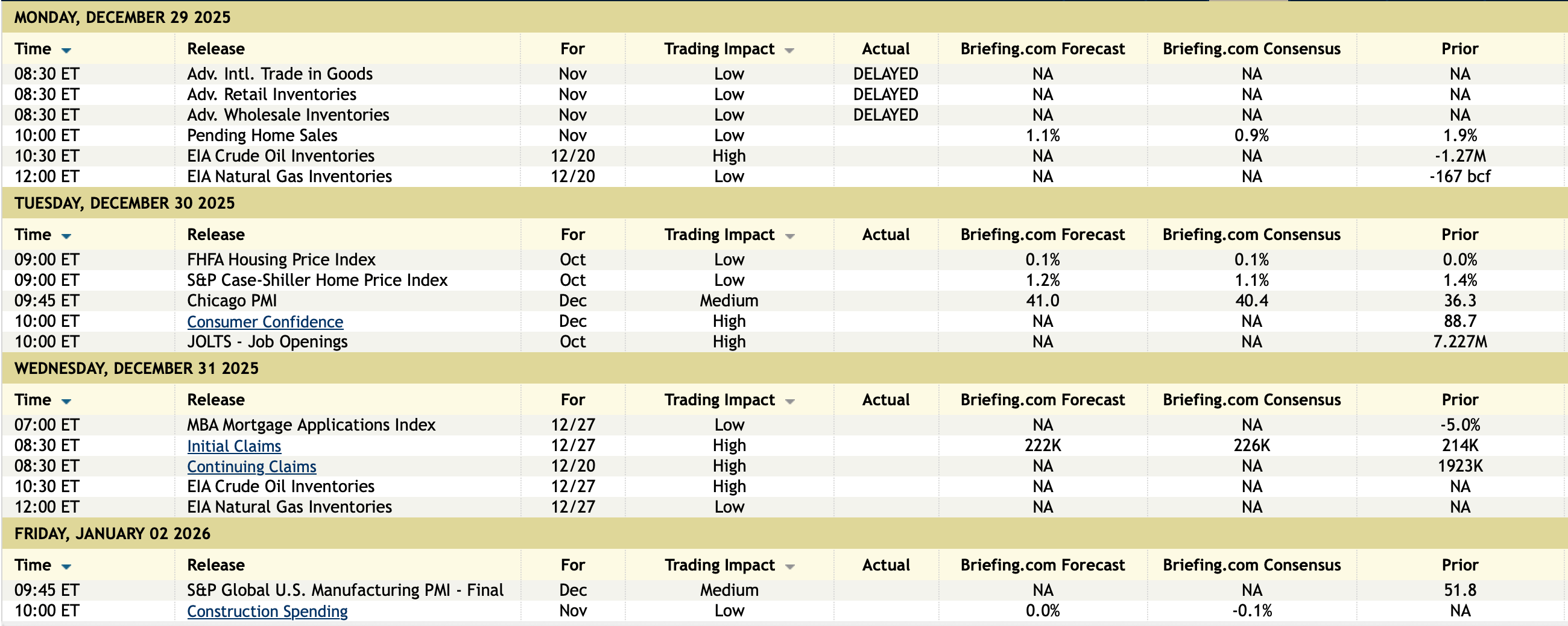

11:30 AM: Treasury hosts an $86B 3 and a $77B 6-Month Bill Auction

10:30 AM: Dallas Fed Manufacturing Activity (December);

BY Doug Kass · Dec 29, 2025, 8:45 AM EST

At 8:11 AM:

BY Doug Kass · Dec 29, 2025, 8:35 AM EST

BY Doug Kass · Dec 29, 2025, 8:25 AM EST

I am shorting (JPM) and (GS) in premarket.

BY Doug Kass · Dec 29, 2025, 8:14 AM EST

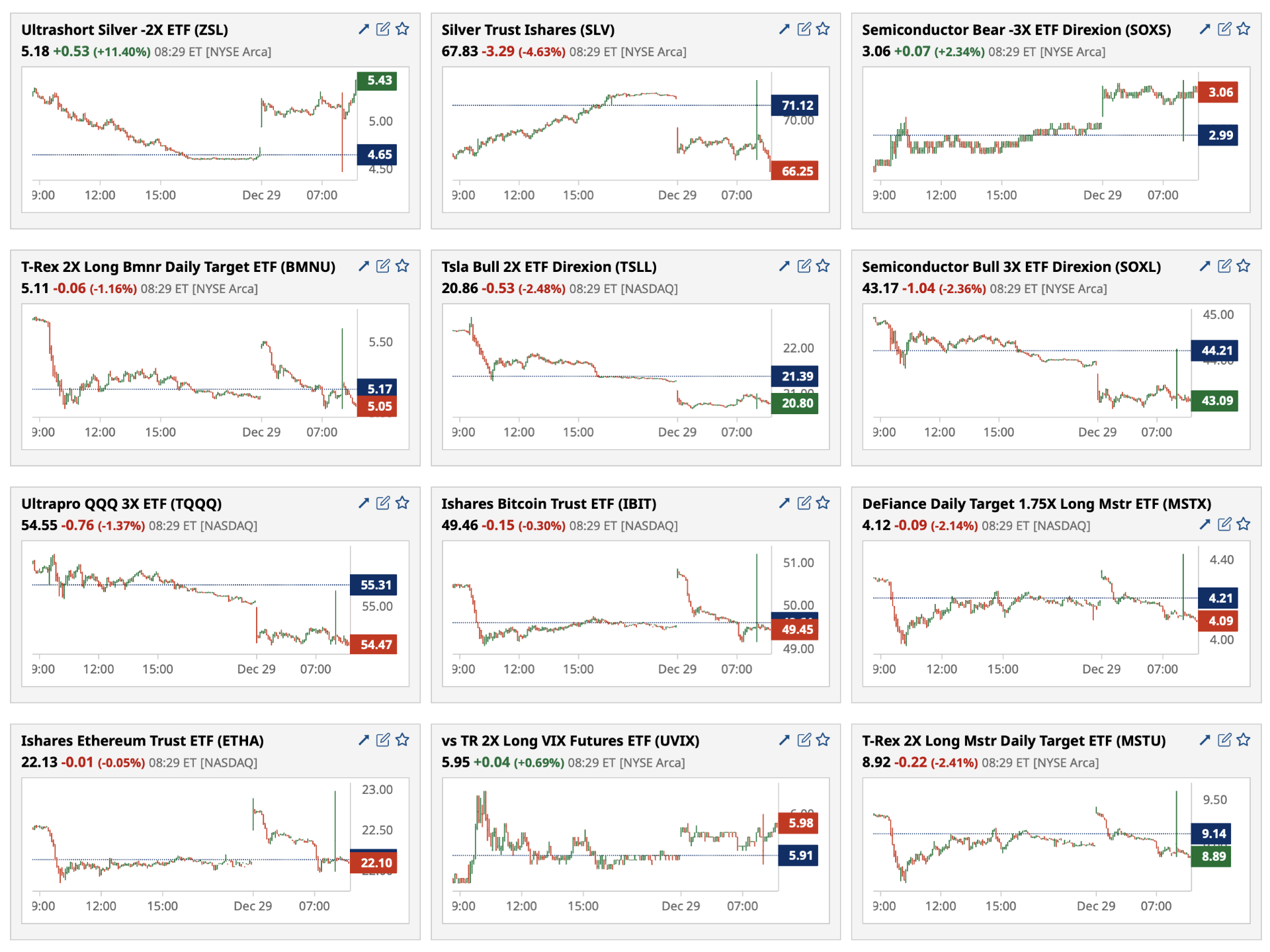

It is remarkable to me that Fin TV has not said a word about what is going on in the precious metals markets:

and...

BY Doug Kass · Dec 29, 2025, 7:50 AM EST

BY Doug Kass · Dec 29, 2025, 7:40 AM EST

BY Doug Kass · Dec 29, 2025, 7:30 AM EST

BY Doug Kass · Dec 29, 2025, 7:20 AM EST

BY Doug Kass · Dec 29, 2025, 7:05 AM EST

BY Doug Kass · Dec 29, 2025, 6:50 AM EST

Bonus — Here are some great links:

Seasonality and the Eight-Month Rally ("Jazzy" Jeff Hirsch)

BY Doug Kass · Dec 29, 2025, 6:35 AM EST

From The Credit Strategist:

Welcome to Kingstown — 2026 Outlook

BY Doug Kass · Dec 29, 2025, 6:20 AM EST

While I made a nice/quick profit, as I suggested (and with (MU) trading another -$4 lower), this short cover will likely be premature:

I covered my Micron (MU) short ($285.19).

I suspect that a month from now, I will view this as a bad cover!

That said, I will take a nice profit (in only a few hours).

From early this morning:

Micron Short

I shorted (MU) in the premarket at $293.70.

Position: Short MU (S)

BY DOUG KASS DEC 26, 2025 9:37 AM EST

Position: None

By Doug Kass Dec 26, 2025 1:43 PM EST

BY Doug Kass · Dec 29, 2025, 6:05 AM EST

Wolf Street howls about first day "pops" of IPOs.

BY Doug Kass · Dec 29, 2025, 5:55 AM EST

The S&P Short Range Oscillator remains slightly overbought at 1.12% vs. 1.80%.

BY Doug Kass · Dec 29, 2025, 5:45 AM EST