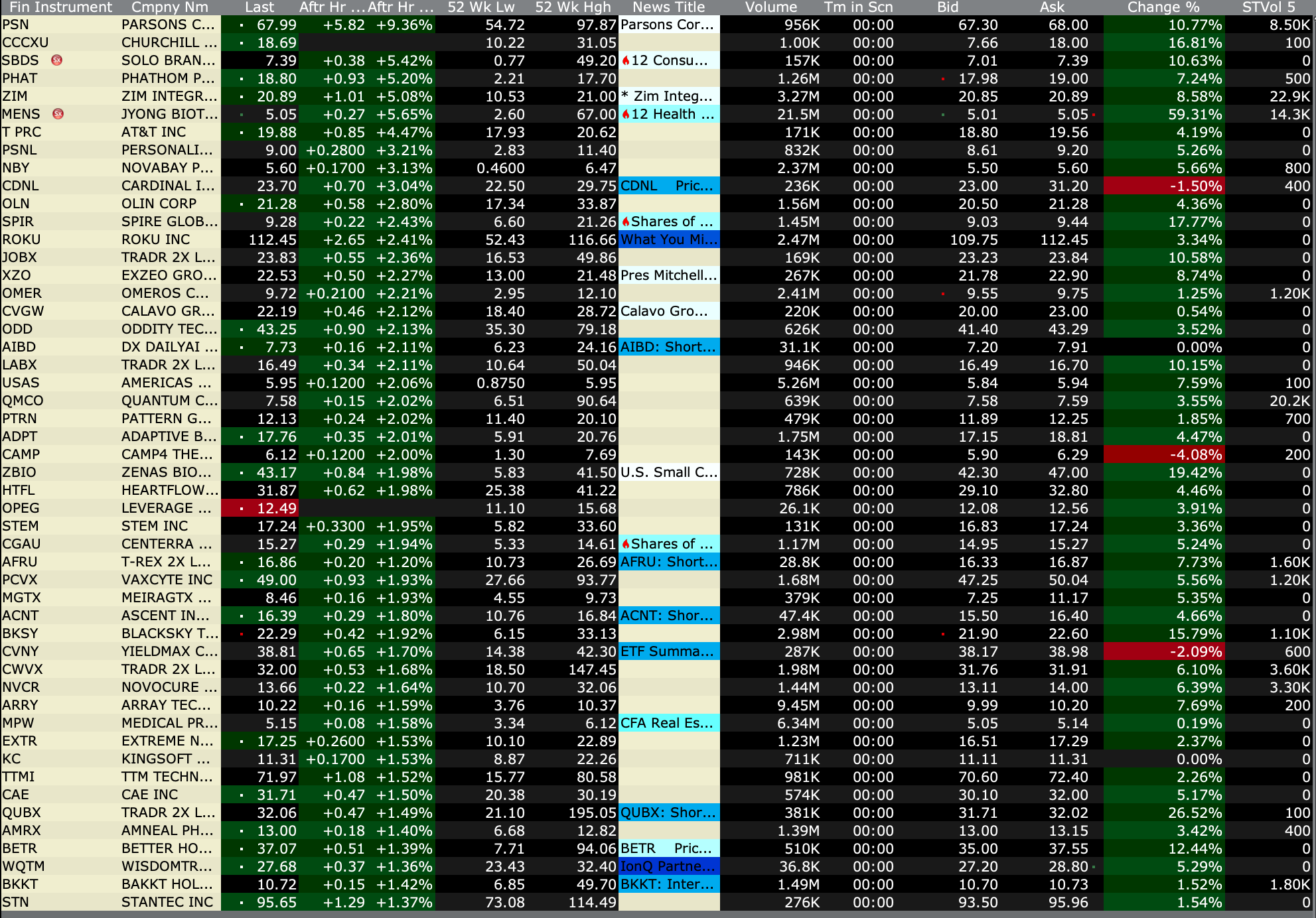

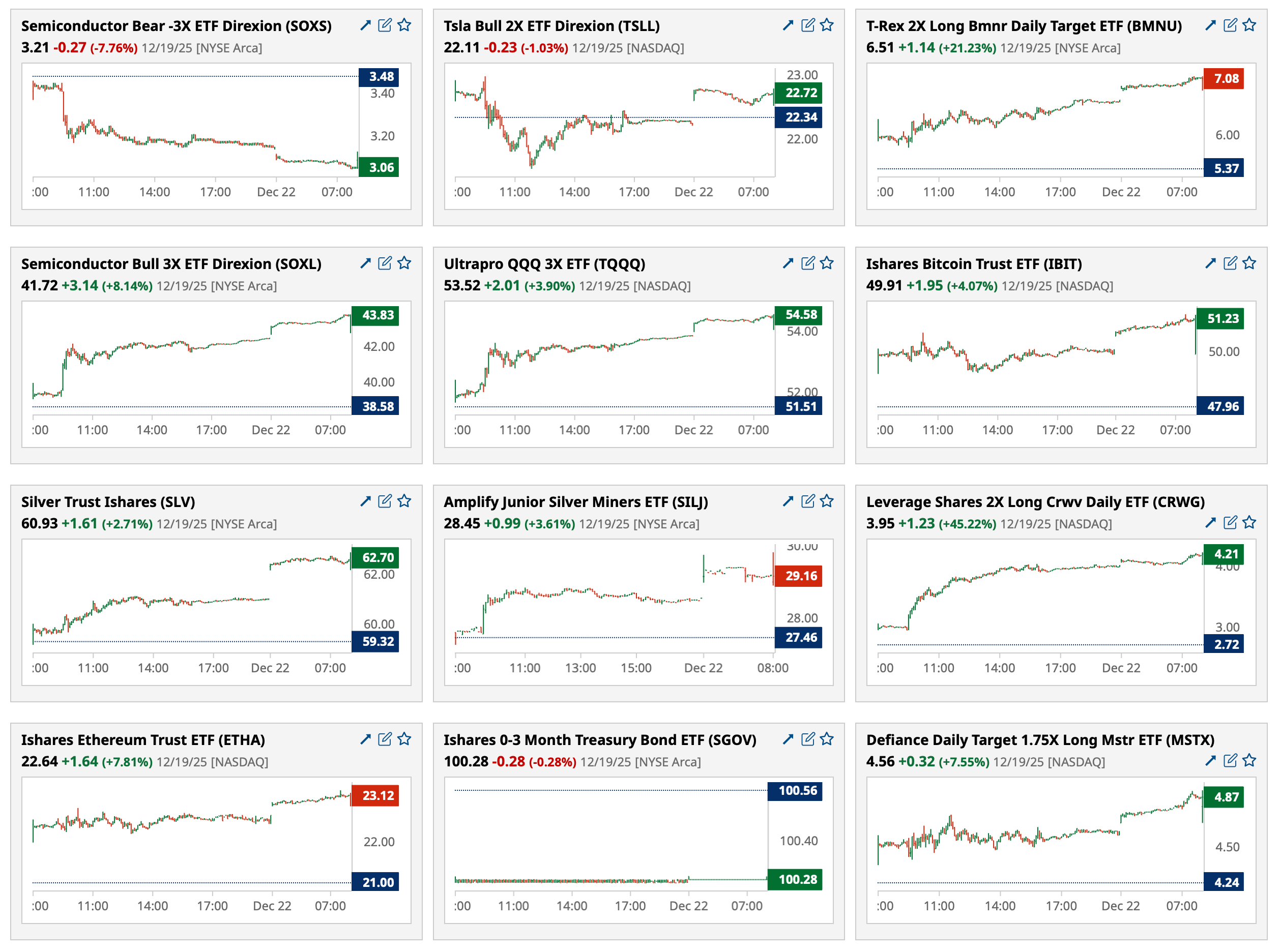

After-Hours Gainers, Losers

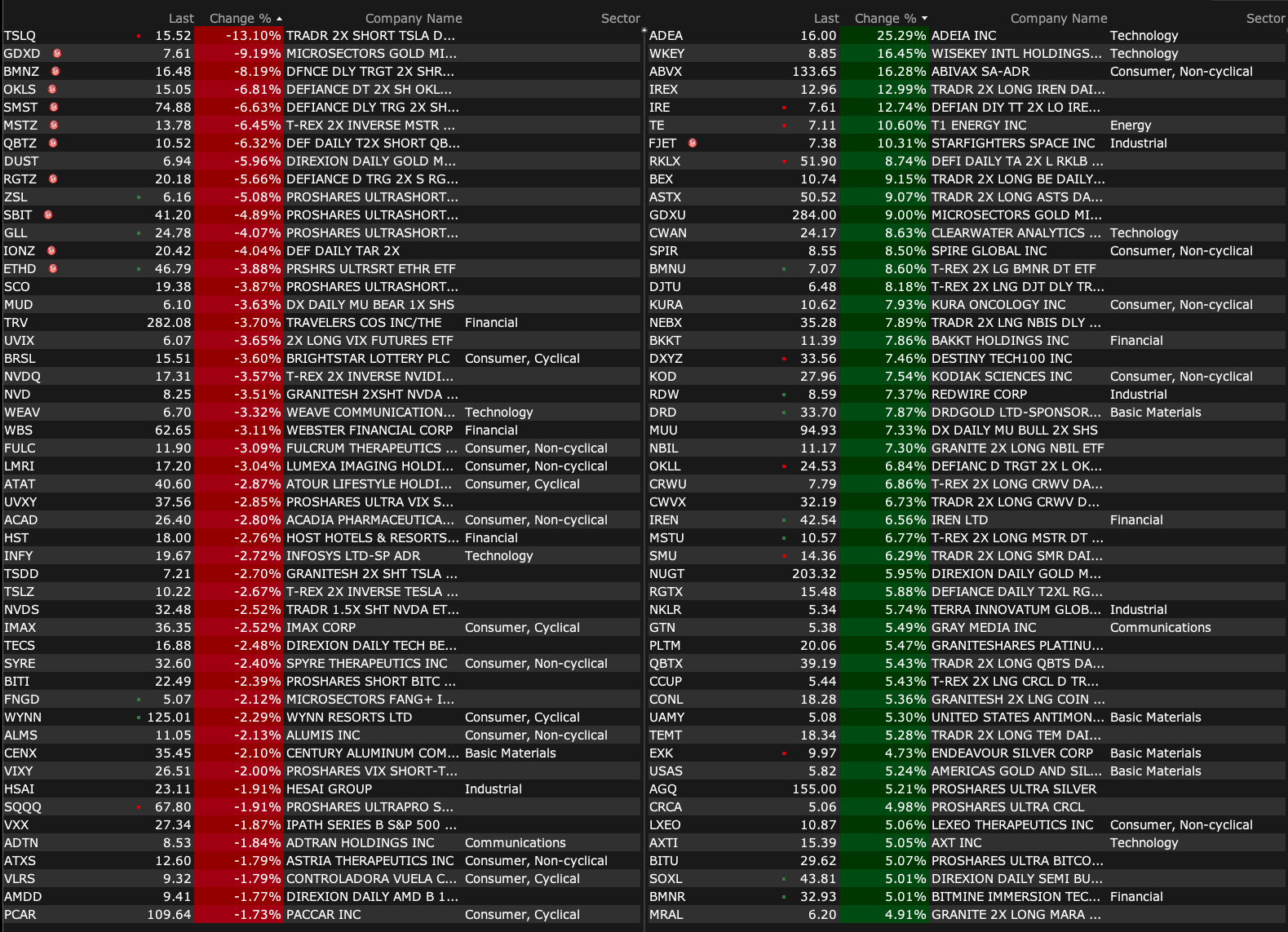

After-Hours % Gainers

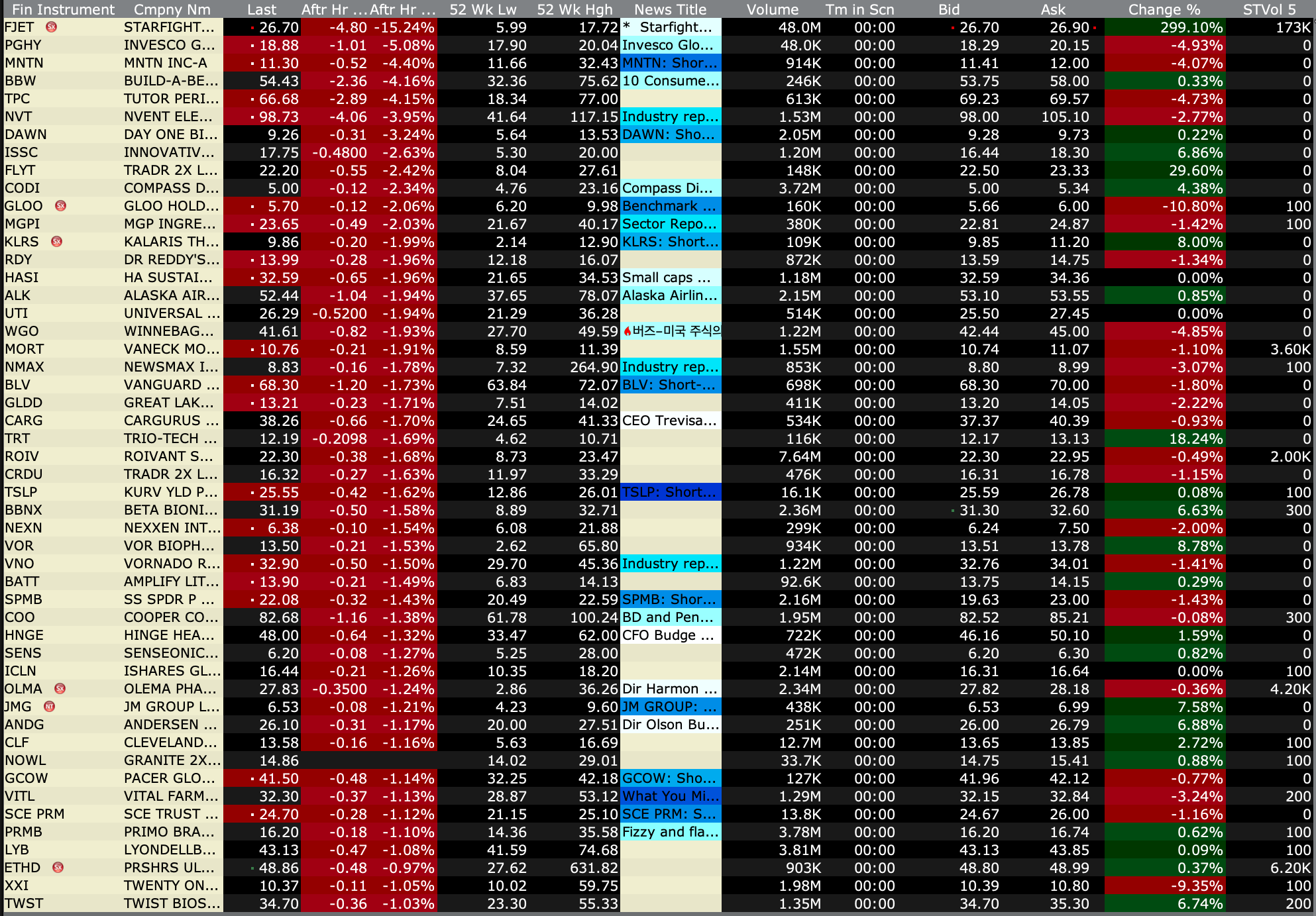

After-Hours % Losers

BY Doug Kass · Dec 22, 2025, 4:55 PM EST

After-Hours % Gainers

After-Hours % Losers

BY Doug Kass · Dec 22, 2025, 4:55 PM EST

BY Doug Kass · Dec 22, 2025, 4:45 PM EST

- NYSE volume 11% below its one-month average;

- NASDAQ volume 13% below its one-month average;

- VIX index: down 5.57% to 14.08

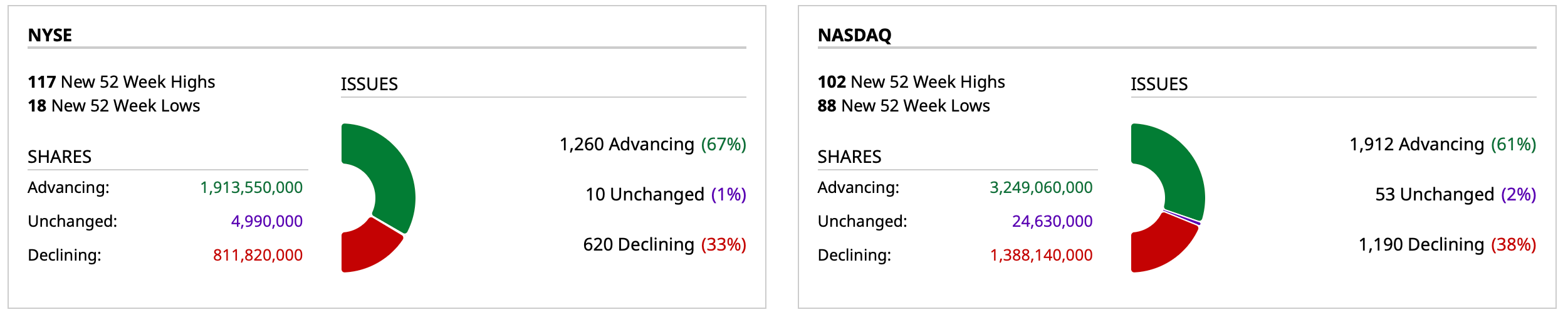

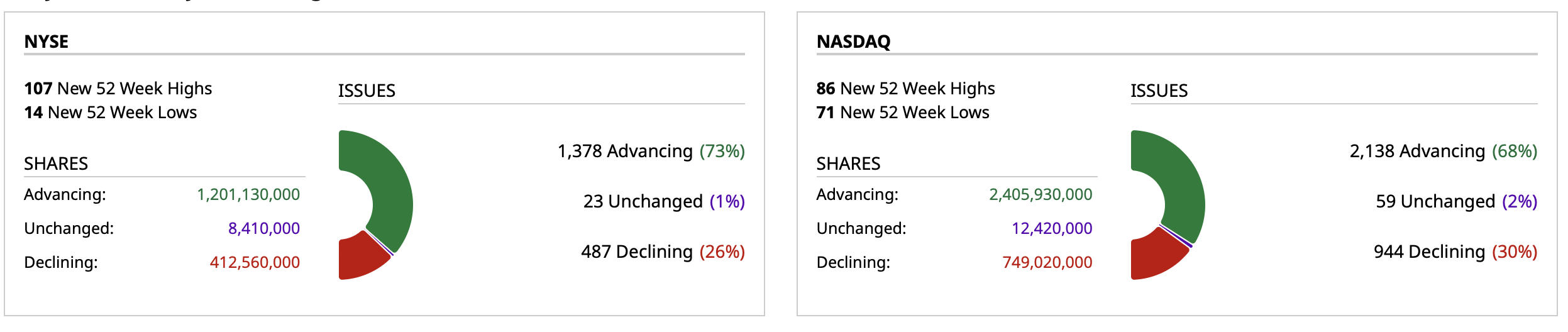

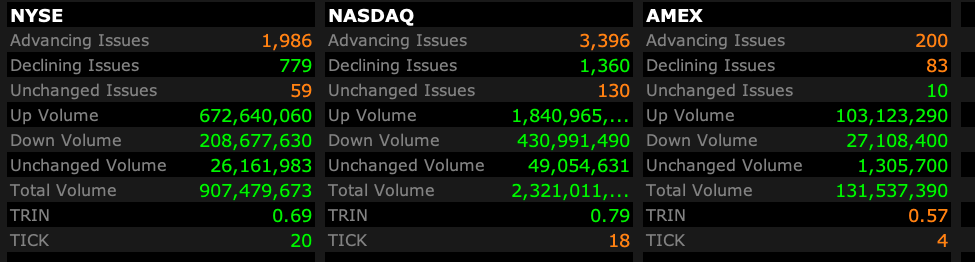

Breadth

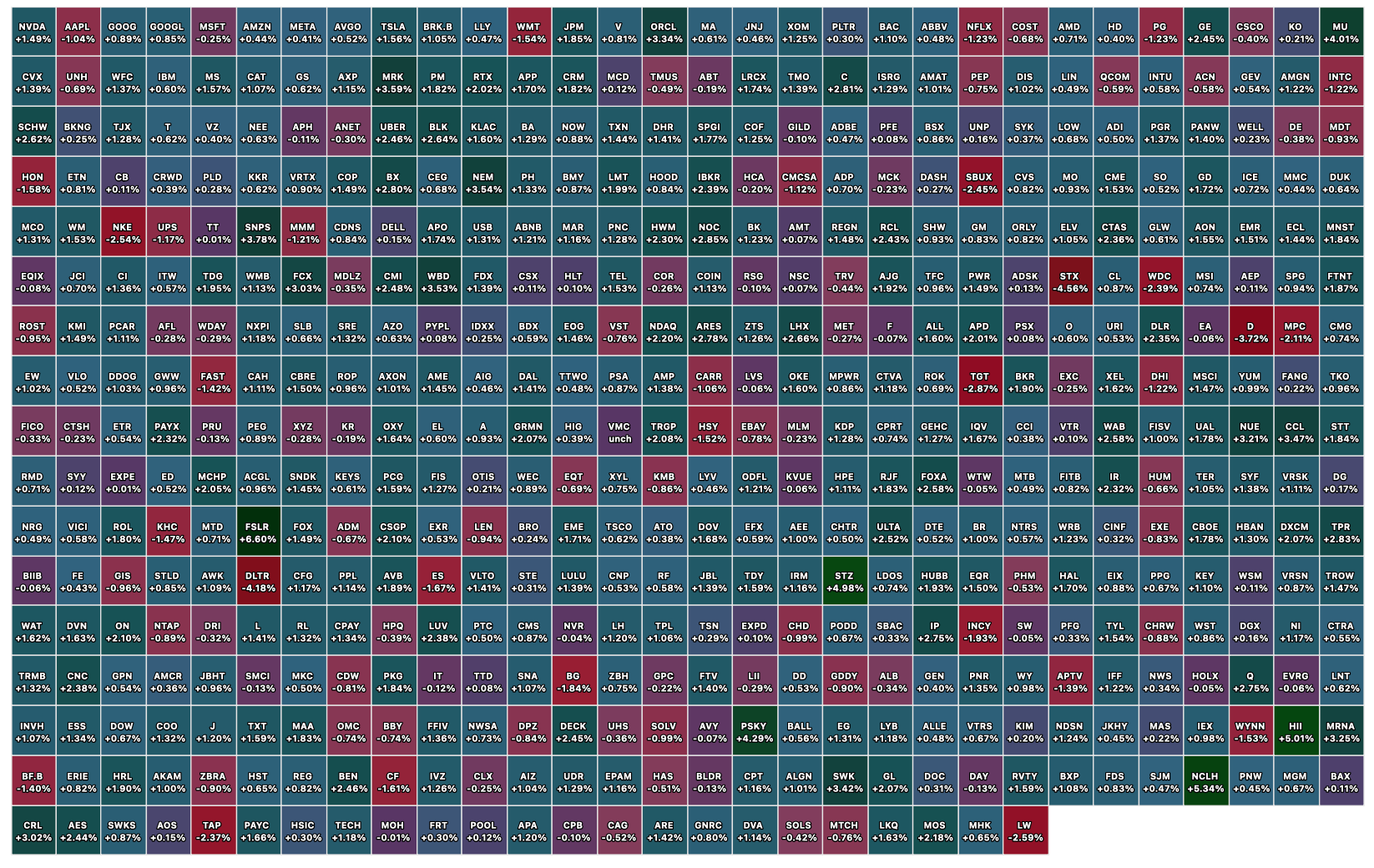

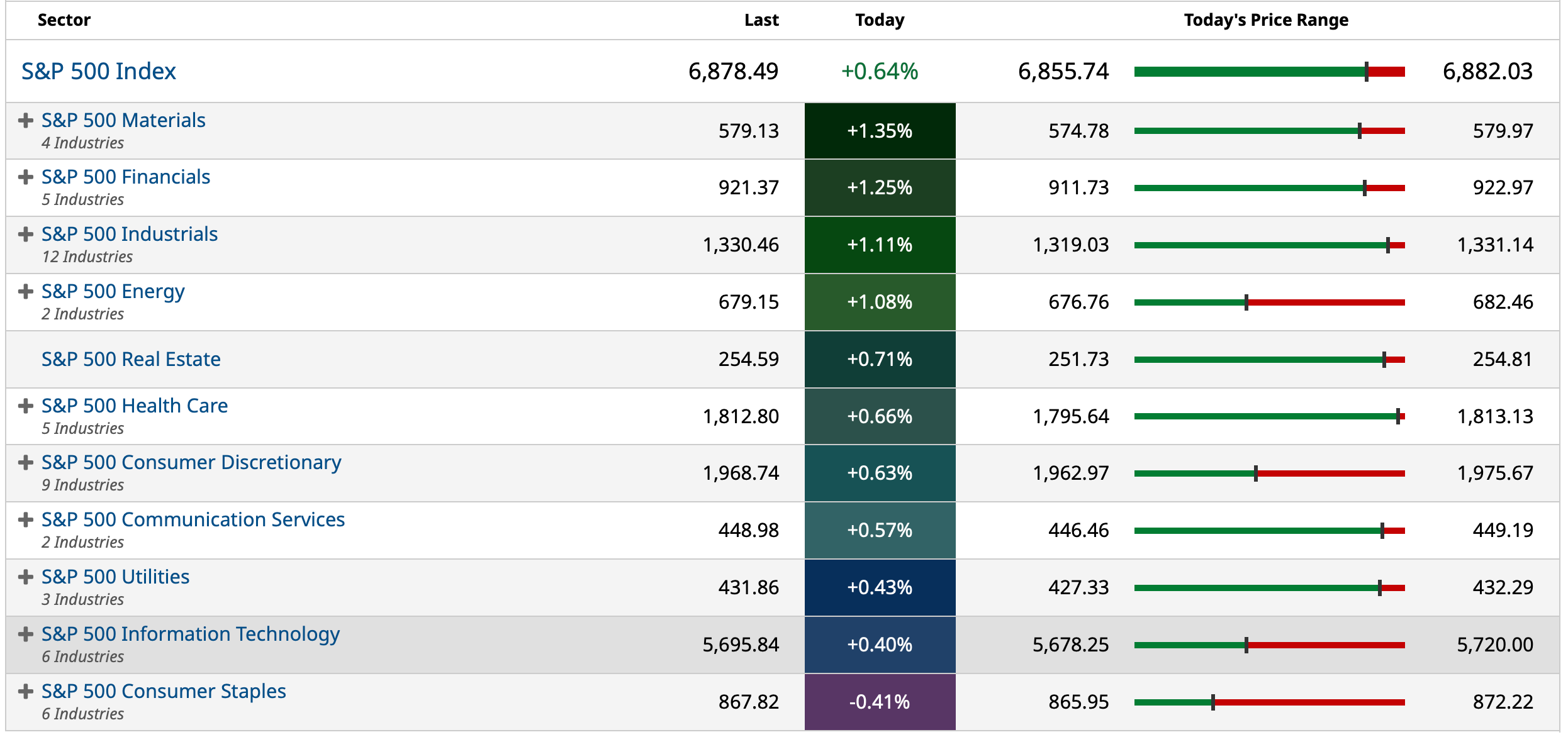

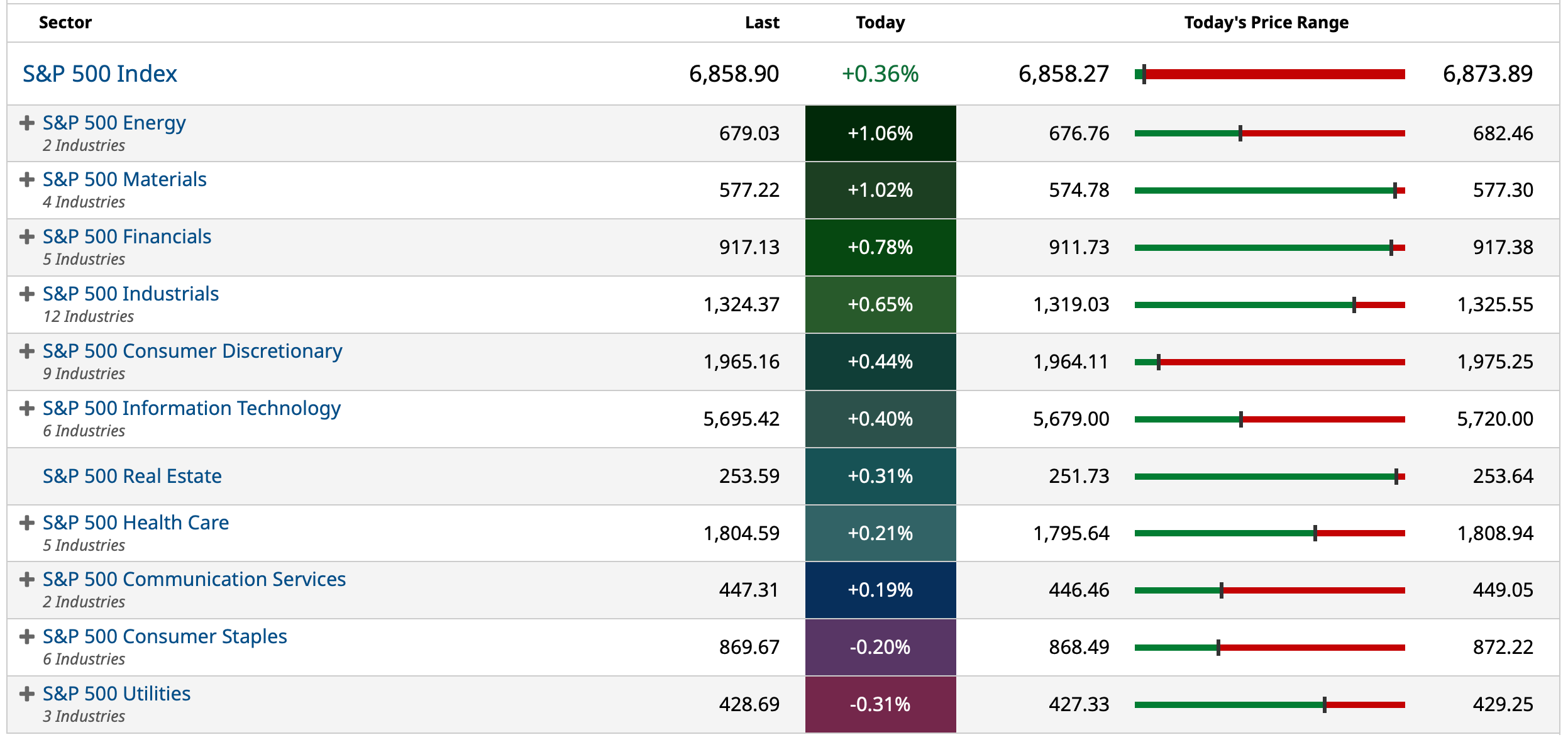

S&P 500 Sectors

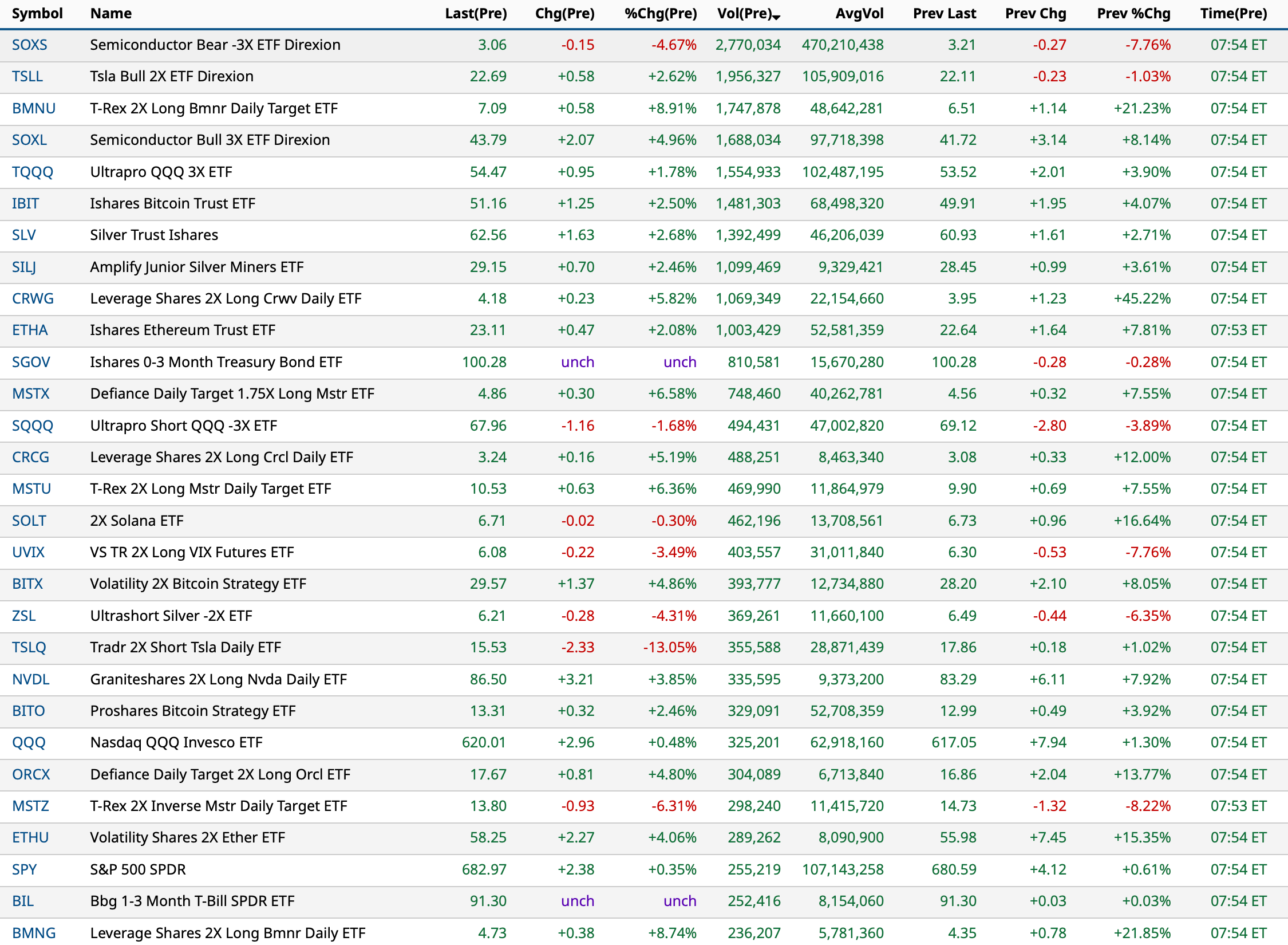

% Movers

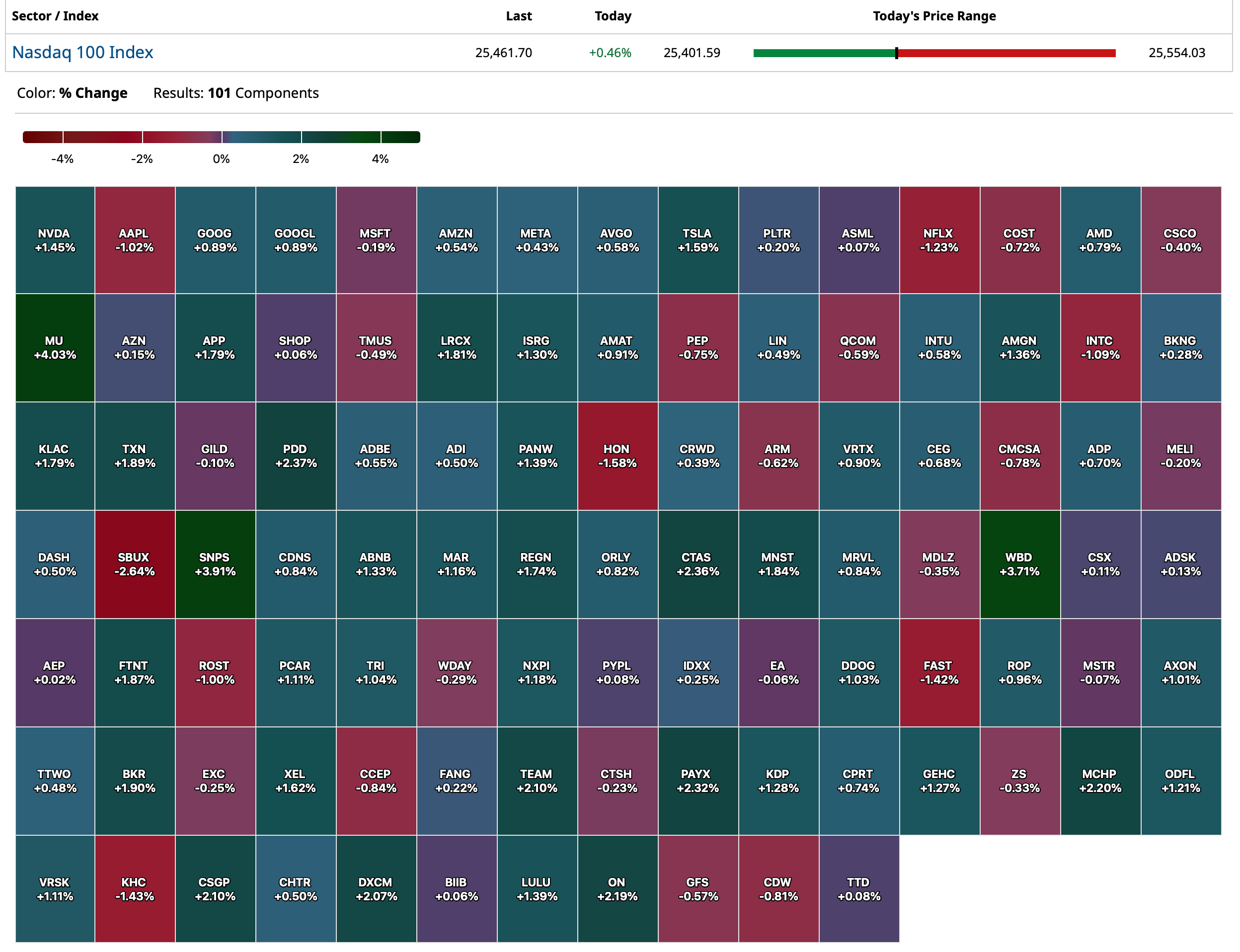

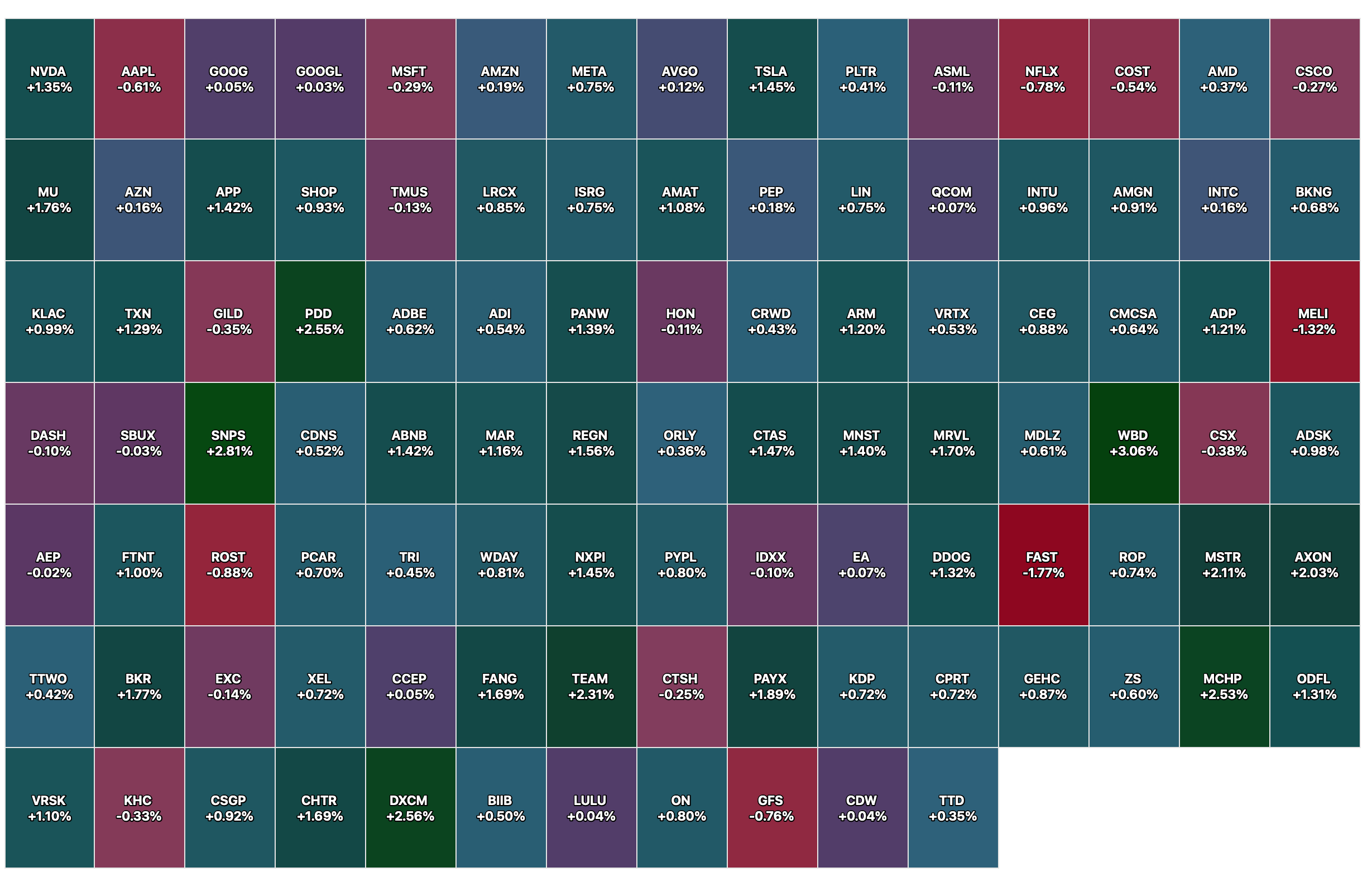

Nasdaq 100 Heat Map

BY Doug Kass · Dec 22, 2025, 4:37 PM EST

"After Rescheduling: What Really Happened?"

Shadd Dales and Anthony Varrell are the premier cannabis observers — run, don't walk, to watch them(!) if you still remain interested in the sector:

BY Doug Kass · Dec 22, 2025, 3:38 PM EST

Carvana (CVNA) shares are -$19.15 today.

I have covered my short but plan to put it out again on strength.

BY Doug Kass · Dec 22, 2025, 2:45 PM EST

With S&P cash +43 handles, I am adding to my index shorts.

BY Doug Kass · Dec 22, 2025, 2:43 PM EST

BY Doug Kass · Dec 22, 2025, 2:33 PM EST

Consumer staples are clearly playing second fiddle today and over the last several days.

Will soon be adding more aggressively.

BY Doug Kass · Dec 22, 2025, 2:20 PM EST

Breadth

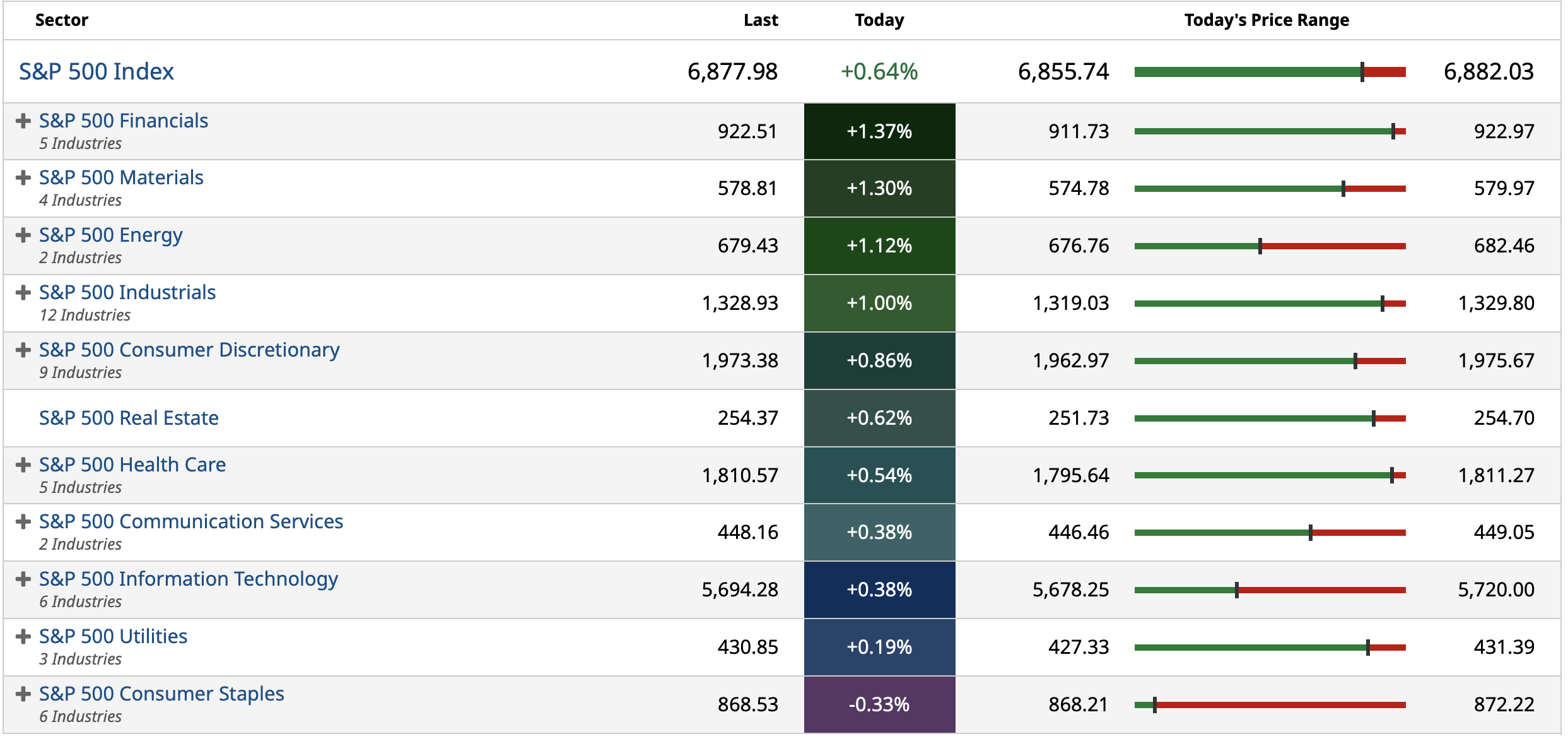

S&P 500 Movers

BY Doug Kass · Dec 22, 2025, 2:07 PM EST

What a mistake last week in covering shorts of (MSOS) (last sale $4.60) and (MSOX) ($4.29)!:

Covered cannabis shorts:

* MSOS $6.89

* MSOX $10.85

Position: none.

BY DOUG KASS DEC 17, 202 9:51 AM EST

I shorted (MSOS) $7.32 and AdvisorShares MSOS Daily Leveraged ETF (MSOX) $11.80 in premarket trading.

I plan to cover these early this morning = win, lose or draw.

Position: Short MSOS (VS), MSOX (VS)

BY DOUG KASS DEC 17, 2025 9:37 AM EST

BY Doug Kass · Dec 22, 2025, 12:48 PM EST

BY Doug Kass · Dec 22, 2025, 12:25 PM EST

Howard Marks:

BY Doug Kass · Dec 22, 2025, 11:56 AM EST

From my pal, Larry:

BY Doug Kass · Dec 22, 2025, 11:49 AM EST

As you all know our office keeps a tab of the sentiment of guests/panelists/strategists that parade on CNBC during the week.

We use this as a contrarian indicator.

Over the last five trading sessions there was 57 bulls and 2 bears.

Res ipsa loquitur

BY Doug Kass · Dec 22, 2025, 11:35 AM EST

BY Doug Kass · Dec 22, 2025, 11:15 AM EST

Here are today's things:

* I shorted more Indices:

(SPY) $683.20

(QQQ) $620.10

* I added to the following longs: (NFLX) $94.33 and (KMB) $100.32.

* Shorted two financials: (JPM) $320.27 and MS $178.31.

* Shorted (JOET) $42.63.

BY Doug Kass · Dec 22, 2025, 10:50 AM EST

I have received a number of emails from subscribers over the weekend regarding cannabis stocks.

Here is a repost of last week's analysis after the Administration's rescheduling "announcement:"

DEC 19, 2025 10:45 AM EST

* President Trump's endorsement of rescheduling was not forceful and failed to resolve a number of important issues

* Trade cannabis equities, don't invest in cannabis stocks

"I have always told me kids, 'don't take drugs'... No drinking, no smoking. Just stay away from drugs."

- President Trump (at yesterday's rescheduling press conference)

Throughout the last five years, I have aggressively traded cannabis equities, buying cannabis stocks on weakness and selling on the slightest hint of regulatory reform and relief.

In most cases, this sort of positioning (and trading) has been quite profitable.

At the same time I have consistently had misgivings about investing in the cannabis space, for several fundamental and structural reasons:

* To begin with, the total addressable market (TAM) for cannabis is likely much smaller than the industry optimists have forecast. Already, recently permitted states have experienced a disappointing adoption curve. Revenues, cash flow and profits have been well below analysts' and managements' projections. Some multiple state operators are are even exiting some states/jurisdictions.

* The current structure of state silos (and dispensary restrictions in some states) result in diseconomies of scale and an inability of creating (hoped for) oligopolistic industry consumer brands (and, with it, pricing power).

* Product pricing remains under pressure (as do revenues, cash flows and profits) and, if anything, rescheduling could exacerbate this condition.

* Past uncertain tax liabilities (from 280E) are massive, and though likely to be eventually resolved, represent still large company liabilities. Industry balance sheets are in poor shape -- with secondary/tertiary state operators facing an almost impossible "debt refinancing cliff" (and an inevitable dilution of shareholders equity).

* Based on the president's comments, banking and custodian issues (important in order to attract institutional investors) are unlikely to be resolved in the (reasonable) near term.

* Without institutional sponsorship, I am of the view that a depleted retail base of investors will not be able to sustain rallies in the sector.

This brings us to yesterday's announcement that Pres. Trump endorses the process of rescheduling of cannabis (from a Schedule 1 to a Schedule 3 substance).

Here is Pres. Trump's rescheduling recommendation and reclassification comments from Thursday.

Cannabis equities collapsed all Thursday afternoon, surprising and disappointing most (but not me).

Let me try to explain why I think the stocks fared so poorly yesterday and why I don't expect much of a rally from currently depressed levels:

1. The stocks anticipated this news and had rallied into the announcement. (I had shorted that ramp, as posted. I have since covered).

2. In listening to Pres. Trump, he did not exactly provide a ringing endorsement for cannabis. He did not sanction its use as a recreational drug. Rather, he is in support of medical research and actually distanced himself from recreational use of cannabis.

3. Trump emphasized the benefit of hemp; he apparently is in favor liberalizing the use of hemp. This is a competitive threat to cannabis.

4. The decision was heavily influenced by his dear friend Howard Kessler (a leader in cannabis research) and by Kim Rivers Trulieve (TCNNF) and some other multiple state operators.

5. As I noted earlier this week, the President's rescheduling request is a request to proceed with the process of rescheduling. This could take one or two months. This means that the punitive impact of 280e tax liabilities might still be felt in the 2025 tax year.

6. The uncertain tax status of past 280e tax liabilities remain an issue for the cannabis companies that have not yet paid those taxes.

7. Banking, custodian and uplisting issues remain unresolved. Nothing in the President's comments suggest that there is an immediacy to resolve these important issues.

8. Without institutional support, the depleted ranks of cannabis traders and investors don't have the bones to sustain a rally in the sector.

There will continue to be trading opportunities in cannabis stocks.

Nonetheless, rescheduling has not resolved important structural and fundamental problems facing the industry and investors.

Trade cannabis stocks, don't invest in cannabis stocks.

And say no to drugs.

BY Doug Kass · Dec 22, 2025, 10:45 AM EST

BY Doug Kass · Dec 22, 2025, 10:25 AM EST

I am back shorting (MS) at $178.30.

Adding to (NFLX) long at $93.33.

BY Doug Kass · Dec 22, 2025, 10:13 AM EST

I have been scaling (on strength) into more index shorts all morning.

Here is my cost basis today:

* (SPY) $683.19

* (QQQ) $620.04

BY Doug Kass · Dec 22, 2025, 9:42 AM EST

-SIDU +61% (awarded contract under Missile Defense Agency's SHIELD IDIQ Program)

-UNF +32% (Cintas confirms proposal to acquire UniFirst at $275/shr in cash)

-ADEA +21% (raises guidance)

-ABVX +17% (reportedly Lilly mulls acquiring Abivax)

-VELO +12% (files to sell $30M private placement of common stock)

-CWAN +8.5% (to be acquired for $8.4B by Permira and Warburg Pincus)

-TE +7.9% (signs three-year contract to supply independent power producer Treaty Oak Clean Energy, LLC with a minimum of 900MW of solar modules built with domestic solar cells from T1’s planned G2_Austin solar cell fab)

-KULR +6.9% (to pause its at-the-market equity offering program through June 30, 2026)

-ADGM +4.9% (announces new corporate roles)

-GLSI +4.5% (provides additional updates on FLAMINGO-01 and corporate strategy)

-WBD +3.9% (PSKY amends $30/shr all-cash offer for Warner Bros. to address WBD's stated concerns regarding Paramount's superior offer)

-MU +3.7% (momentum)

-GEO +3.0% (awarded Contract by U.S. Immigration and Customs Enforcement for Provision of Skip Tracing Services)

-OLLI +2.7% (Loop Capital Raised OLLI to Buy from Hold, price target: $135)

-MRVL +2.6% (momentum)

-BNBX -4.4% (earnings)

BY Doug Kass · Dec 22, 2025, 9:22 AM EST

BY Doug Kass · Dec 22, 2025, 8:55 AM EST

I have taken a trading long rental in (NFLX) at $94.82 on the news of the revised Paramount offer.

PARAMOUNT AMENDS ITS SUPERIOR $30 PER SHARE ALL-CASH OFFER FOR WARNER BROS. DISCOVERY

BY Doug Kass · Dec 22, 2025, 8:37 AM EST

BY Doug Kass · Dec 22, 2025, 8:30 AM EST

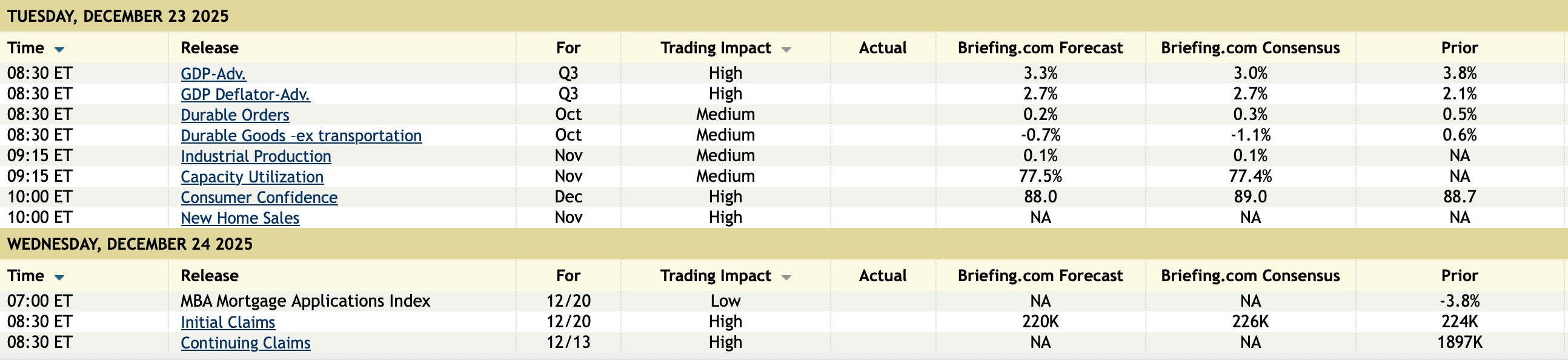

Auctions:

11:30 a.m.: Treasury hosts an $86 billion 3 and a $77B 6-Month Bill Auction;

1 p.m.: Treasury hosts a $69 billion 2-Year Note Auction

Economic Calendar

8 a.m.: Fed Treasury Repo Reference Rate;

8:30 a.m.: Chicago Fed National Activity Index (November);

8:45 a.m.: S&P Global Composite PMI/ S&P Global Services PMI (December-Final); TBD: Housing Starts (waiting on update from census.gov to confirm release schedule) (October);

10:00 a.m.: ISM Manufacturing PMI; ISM Manufacturing Prices Paid/ ISM Manufacturing Employment Index/ ISM Manufacturing New Orders Index (December);

BY Doug Kass · Dec 22, 2025, 8:20 AM EST

From Peter Boockvar:

This will be my last note of the year. I thank you again for taking the time to read what I write as I know you’re flooded each day with so much information. I hope for you a relaxing few weeks and cheers to 2026.

As we look to 2026 and we all debate the extent at which the data center buildout is too much or too little, I finally found some forecasts that searches for some answers. With the permission of my friend Jim Grant I will post here what his colleague Joel Wallenberg wrote in the newly published issue of Grant’s Interest Rate Observer last week:

“It isn’t merely possible, or probably, that data center supply will outstrip even heroic forecasts of data center demand. It’s a mathematical certainty, contends Andy DeVries, head of utilities and investment grade credit at CreditSights.”

“On the one hand, he reasons, a Nov. 13 review by CreditSights of 30 analyst estimates of data center demand through 2030, excluding those from data center providers or utilities, shows a current average estimate of 51 gigawatts of growth, to 86GW, by 2030. The highest estimate of demand growth was 99.4GW, to a total of 134.4GW in 2030.”

“On the other hand, utilities show that supply will be higher still. These companies report a 110GW backlog of contractually agreed upon ‘commtted and confirmed’ power, specifically intended for computation. Beyond the 110GW sits a 735GW pipeline of connection requests (which includes some duplicates). Thus, even according to the highest demand estimate, data center supply will exceed demand by 2030, whether or not any new power contracts are signed. Using the average, data center will overbuild by more than 59GW before another contract is signed.”

“Research provider Bloomberg, New Energy Finance, or BloombergNEF, on Dec. 1 estimated total data center demand will reach 77.4GW in 2030, or 59.5GW specifically for computation, an increase of only 24.5GW from today’s amount. That speculation implies 85.5GW of overbuilding, again before the request backlog is considered. Furthermore, the data center operators submitting the most connection requests are not the ones with top earnings-per-share estimates through 2028, according to a Dec. 8 CreditSights report. The risk of stranded assets is clear and present.”

Whether right or wrong, now we have some numbers to go by when analyzing the data center buildout dynamics and whether we’re in a GenAI CapEx bubble or not. It seems that we most likely are in one.

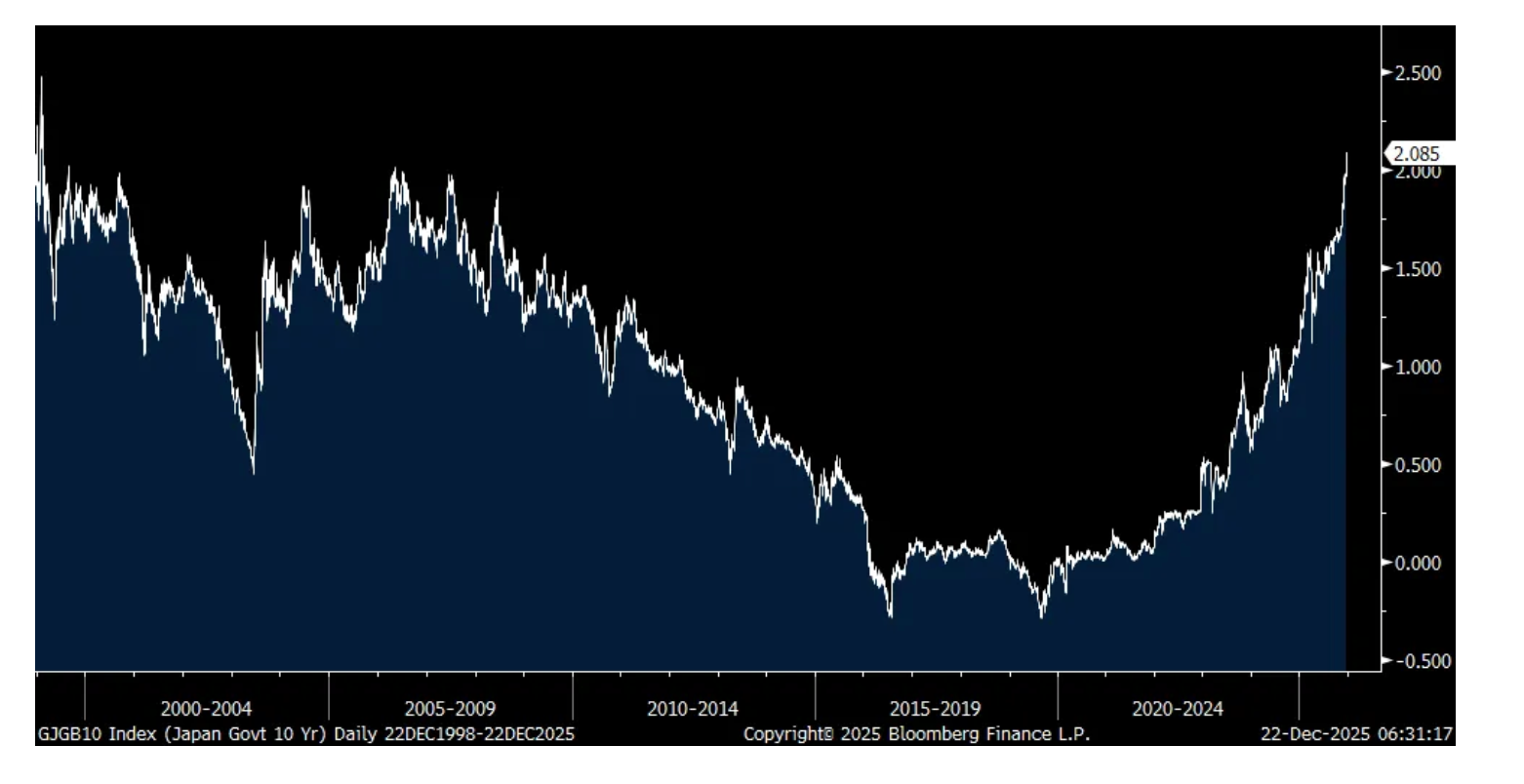

The other big deal for 2026 I think will be the direction of the world’s bond markets as long end rates are just not accommodating the decline in short term rates and as we know in Japan, rates are rising across its curve.

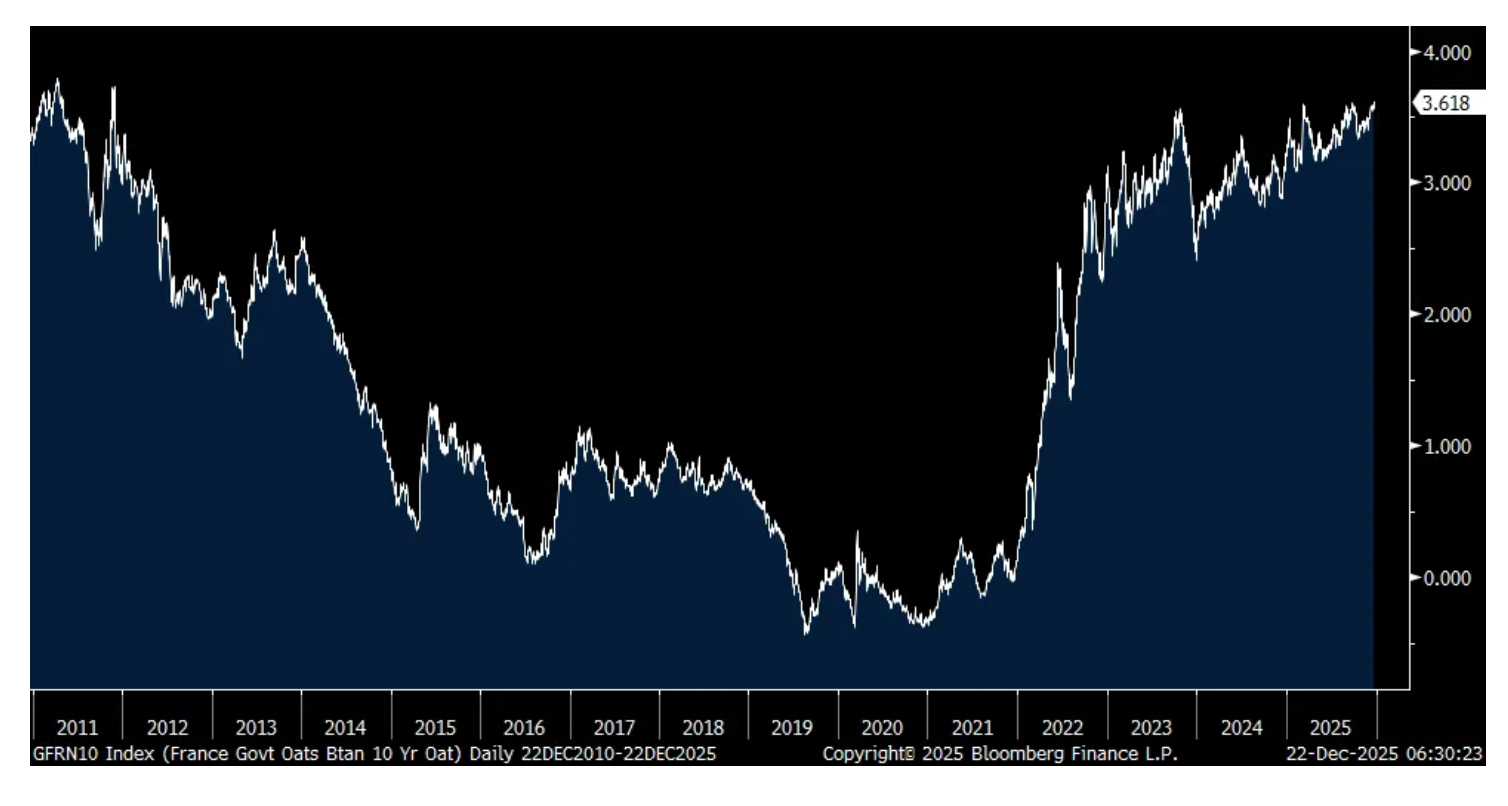

The ECB has cut its deposit rate by 200 bps beginning in June 2024 but the 10 yr German bund today is rising to the highest level since October 2023 and is just 6 bps from a level last seen in 2011. The 10 yr French oat yield today is at the highest since November 2011. This is happening in concert with the 10 yr JGB yield which jumped another 6 bps to 2.09%. And with US Treasuries, we know the Fed has cut the fed funds rate by 175 bps and longer term rates remain about the same. I believe the long duration sovereign bond bear market will continue in 2026.

German 10 yr Bund Yield

French 10 yr Oat Yield

Japanese 10 yr JGB Yield

Speaking of the Fed, Cleveland Fed president Beth Hammack votes in 2026 and she said this yesterday (in WSJ interview posted which was conducted on Thursday), “Where we are today is my base case that we can stay here for some period of time until we get clearer evidence that either inflation is coming back down to target or the employment side is weakening more materially.”

“We took 75 bps off of the policy rate, which should help support that labor side of our mandate, but we do need to be mindful…I’m very focused on making sure that we can get inflation back to target. That is one of our primary objectives and it’s important that we complete the job.”

Something to watch too in 2026 will be the US dollar which still can’t get out of its own way, outside of its performance against the yen. It’s a bit weaker today with the DXY back below 98.5 with precious metals rallying again in kind. The yen today is getting some help from some verbal intervention from Atsushi Mimura, Japan’s chief currency official. He said “We’re seeing one-directional, sudden moves especially after last week’s monetary policy meeting, so I’m deeply concerned. We’d like to take appropriate responses against excessive moves.” We own and like emerging market sovereign local currency bonds that have generous real and absolute yields.

Expect too the lower case ‘i’ to continue with the dot being upper income spending (helped of course by the record high stock market) and the lower part being everyone else. Conagra, a stock we own that’s had a very rough year, and the largest maker of frozen foods in the US and the owner of Slim Jim beef jerky, said this on Friday in their earnings call, more of the same:

“consumer sentiment remained fairly weak in Q2. Household budgets continued to be strained, and value seeking behavior persisted, with these pressures weighing most heavily on low and middle-income consumers.”

“We also saw some unanticipated dynamics this quarter, many of which we expect will be timing related. The government shutdown spanned about half the quarter along with the related pause in SNAP payments.”

BY Doug Kass · Dec 22, 2025, 7:50 AM EST

Sometimes I ask myself... Self, is anyone but me watching the U.S. and Japanese bond markets?

BY Doug Kass · Dec 22, 2025, 7:27 AM EST

BY Doug Kass · Dec 22, 2025, 6:45 AM EST

BY Doug Kass · Dec 22, 2025, 6:35 AM EST

BY Doug Kass · Dec 22, 2025, 6:25 AM EST

BY Doug Kass · Dec 22, 2025, 6:15 AM EST

The S&P Short Range Oscillator remains slightly overbought at 1.11% vs. 0.75%.

BY Doug Kass · Dec 22, 2025, 5:55 AM EST

I added to index shorts:

* (SPY) $682.92

* (QQQ) $619.33

BY Doug Kass · Dec 22, 2025, 5:45 AM EST