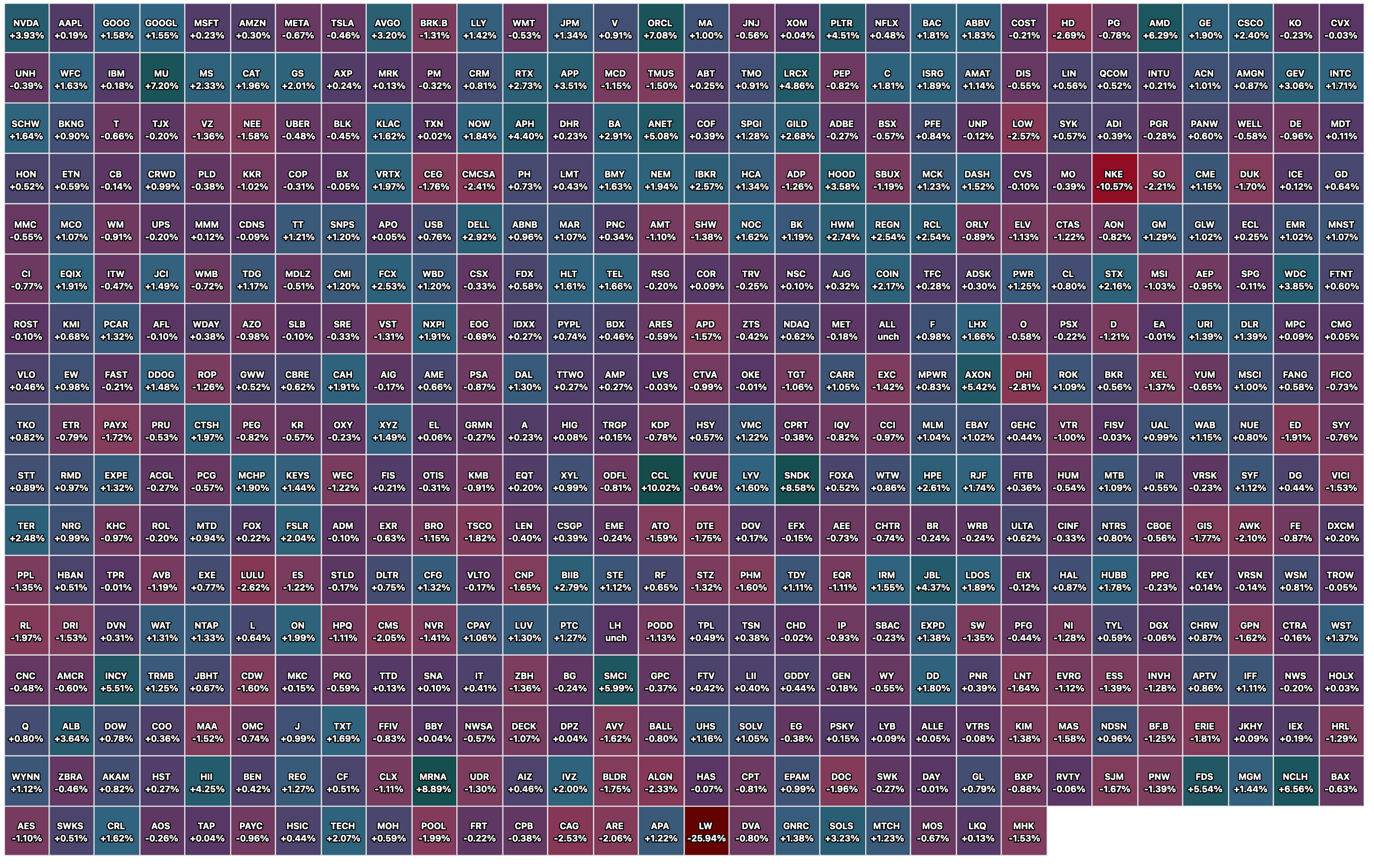

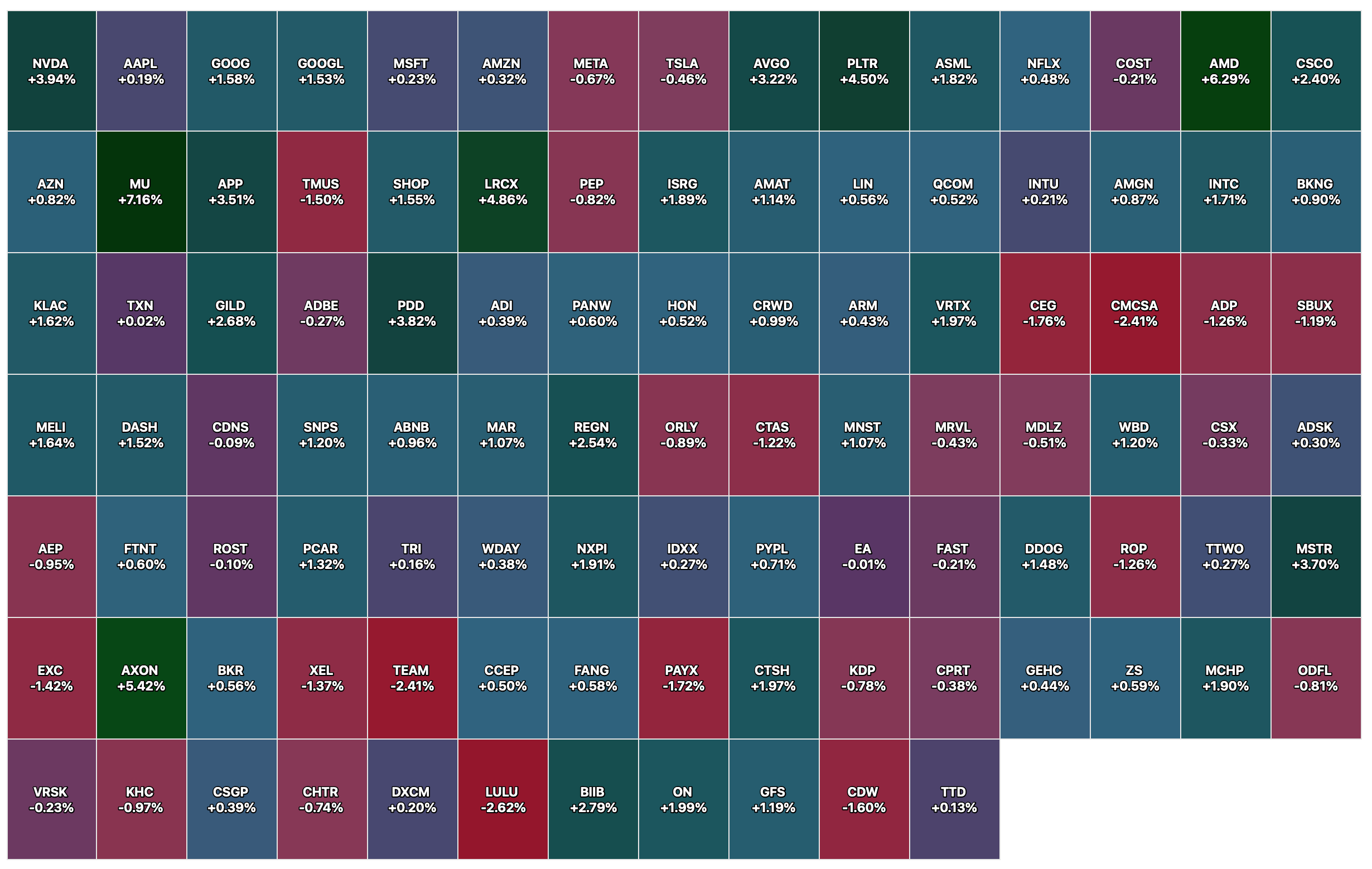

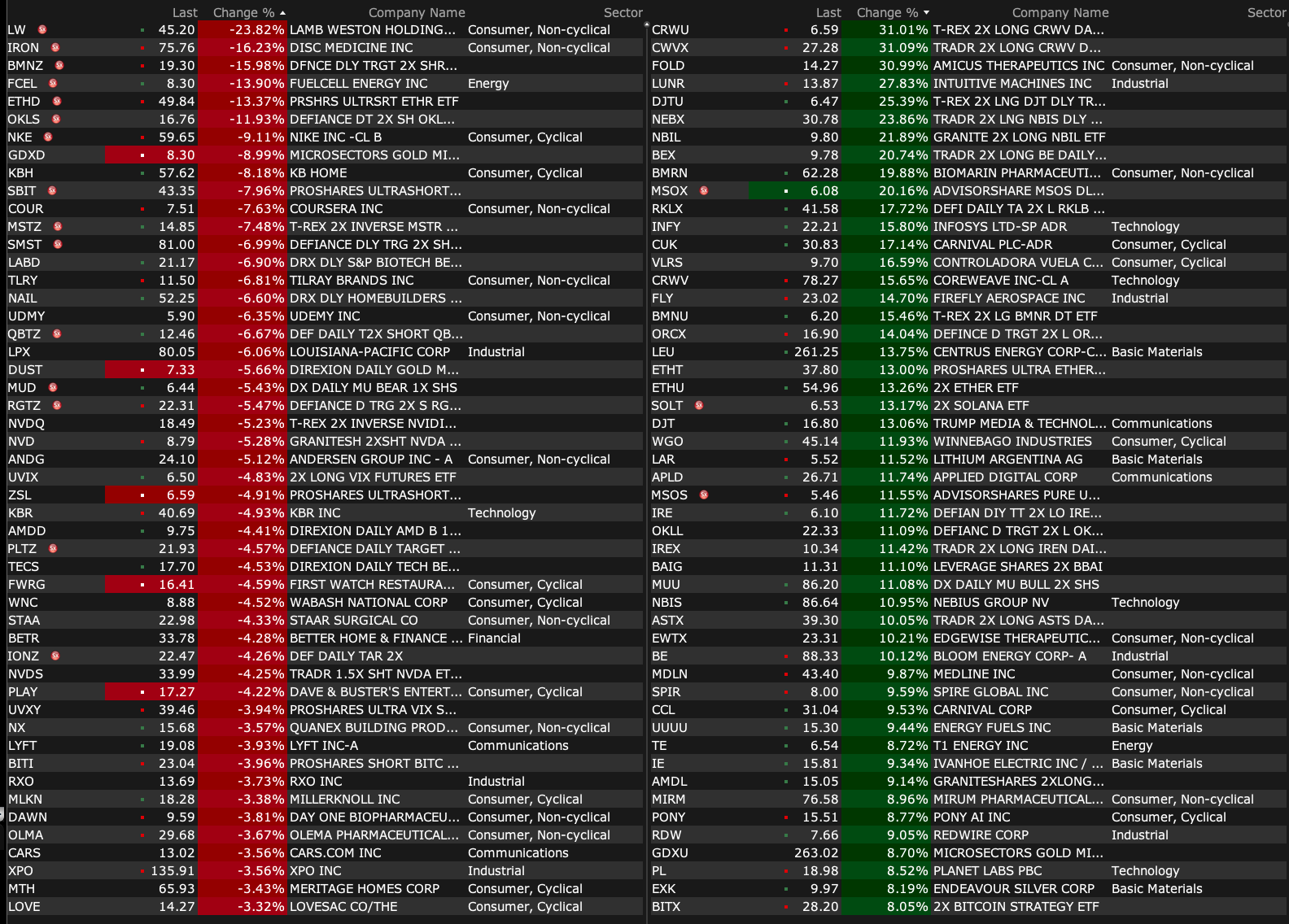

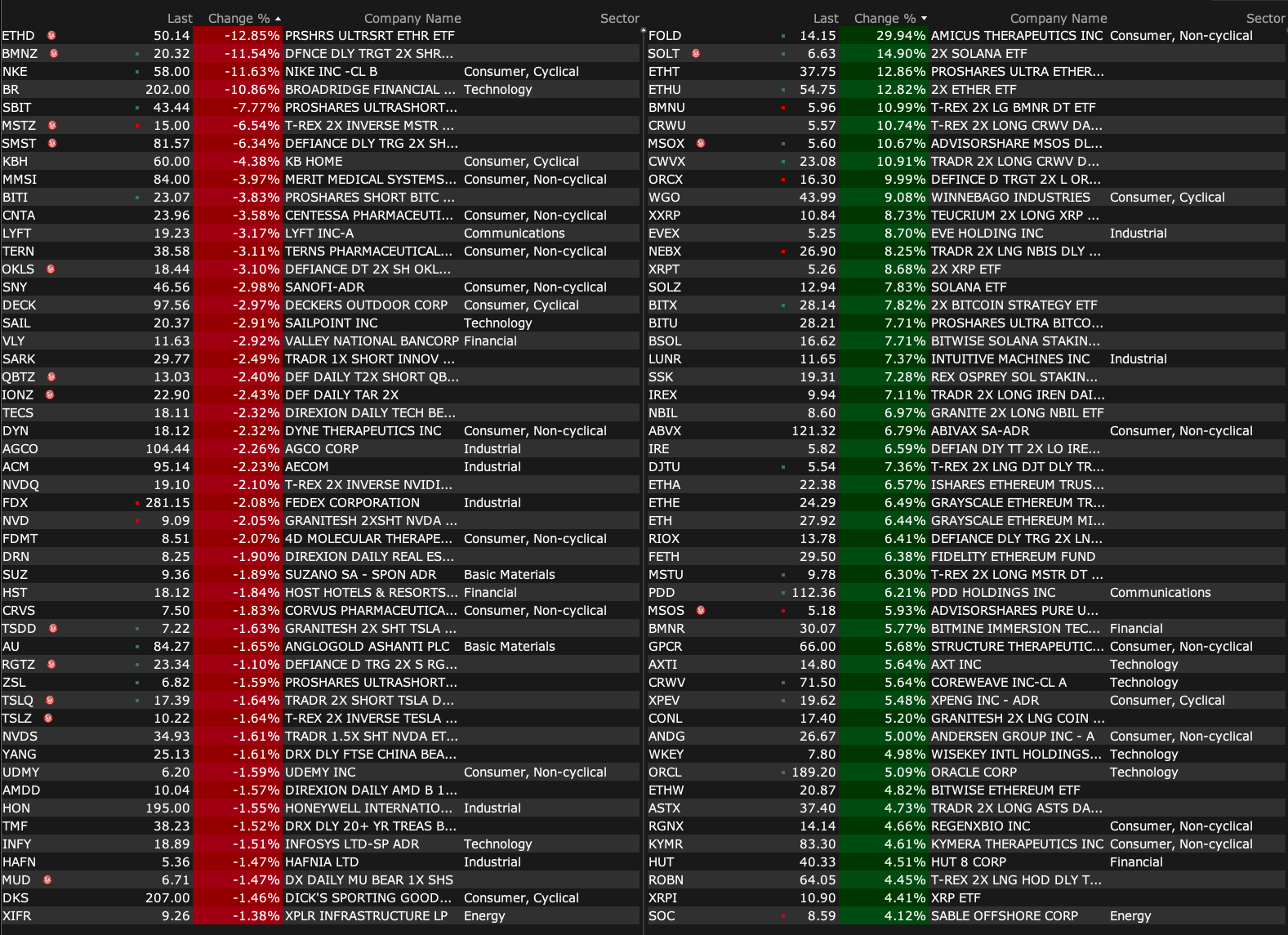

Closing S&P 500 Heat Map

BY Doug Kass · Dec 19, 2025, 4:35 PM EST

BY Doug Kass · Dec 19, 2025, 4:35 PM EST

Closing Volume

- NYSE volume 52% above its one-month average;

- NASDAQ volume 9% above its one-month average;

- VIX index: down 11.20% to 14.98

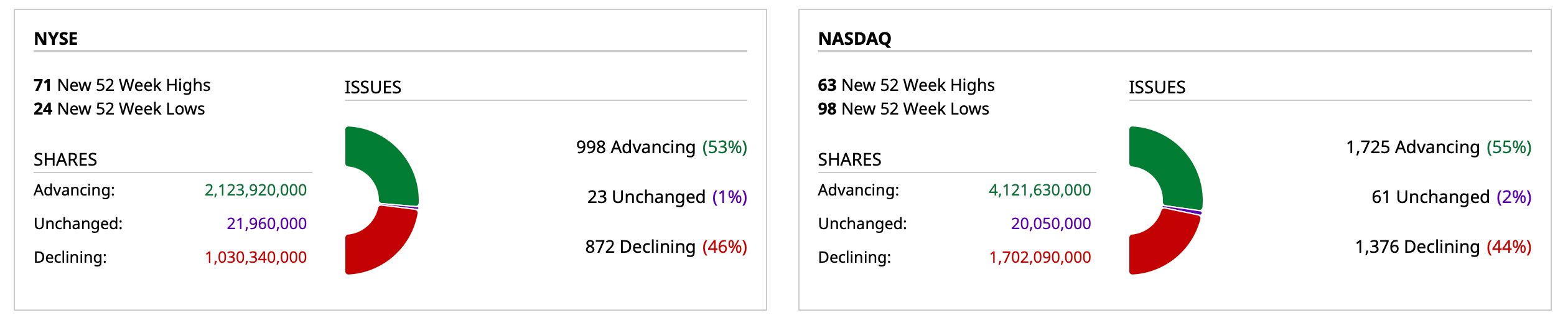

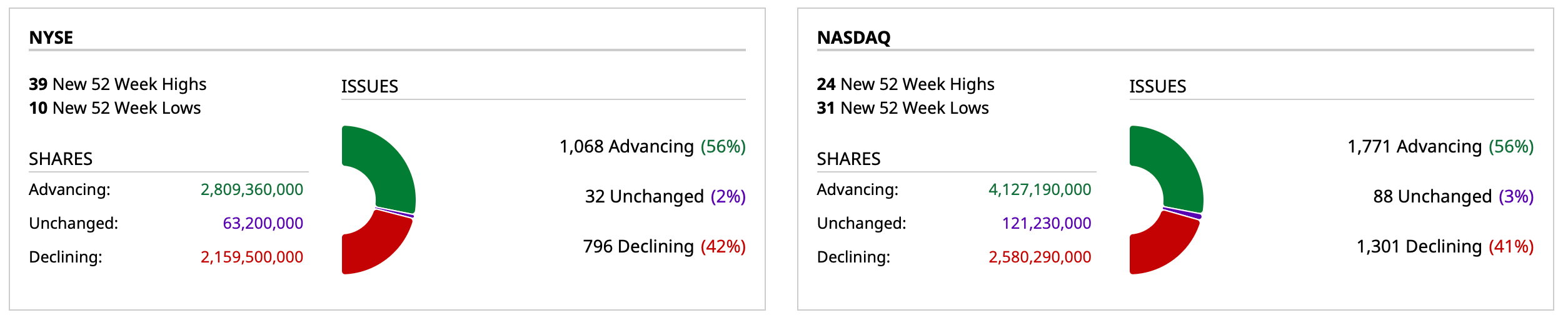

Breadth

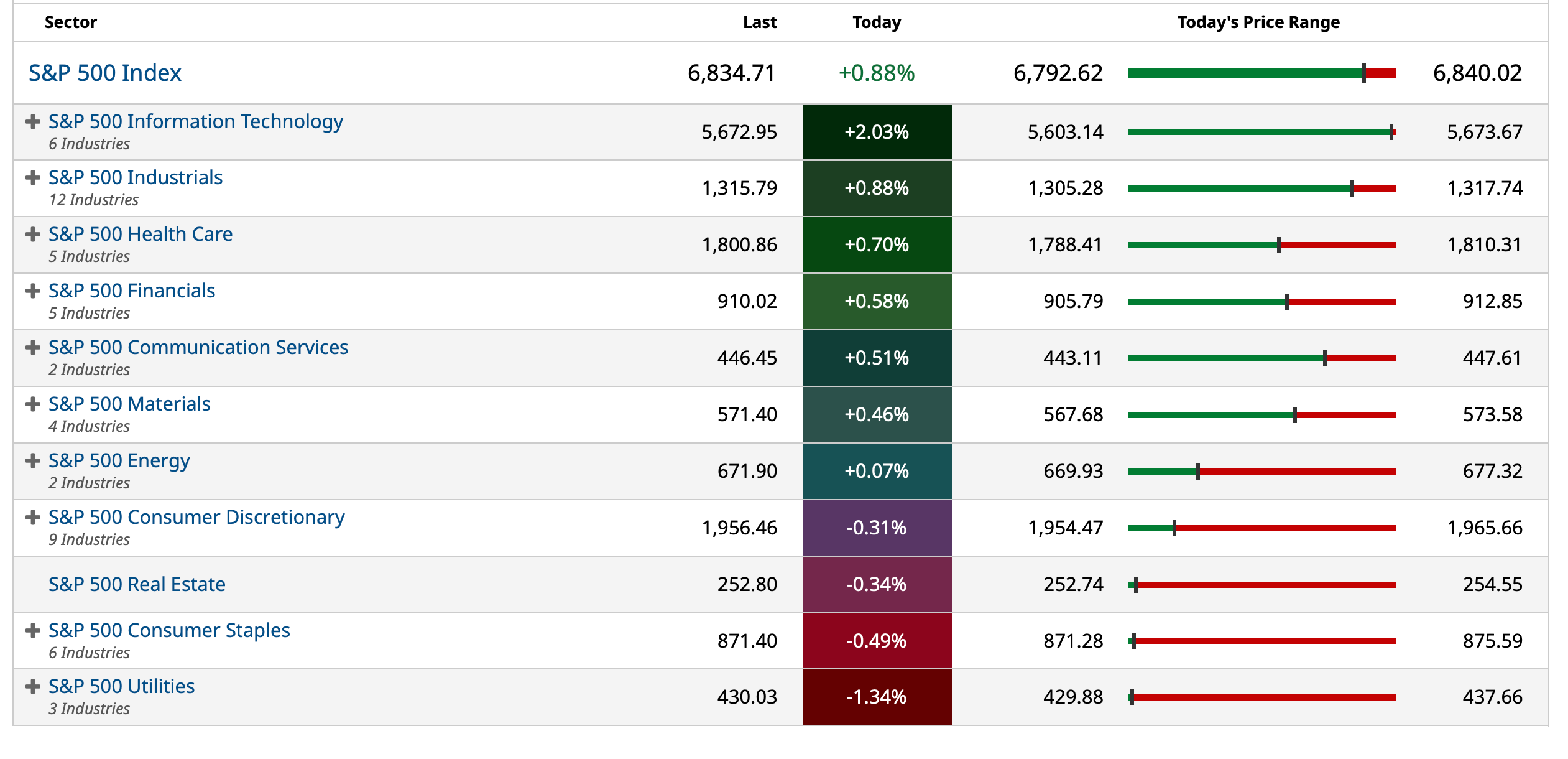

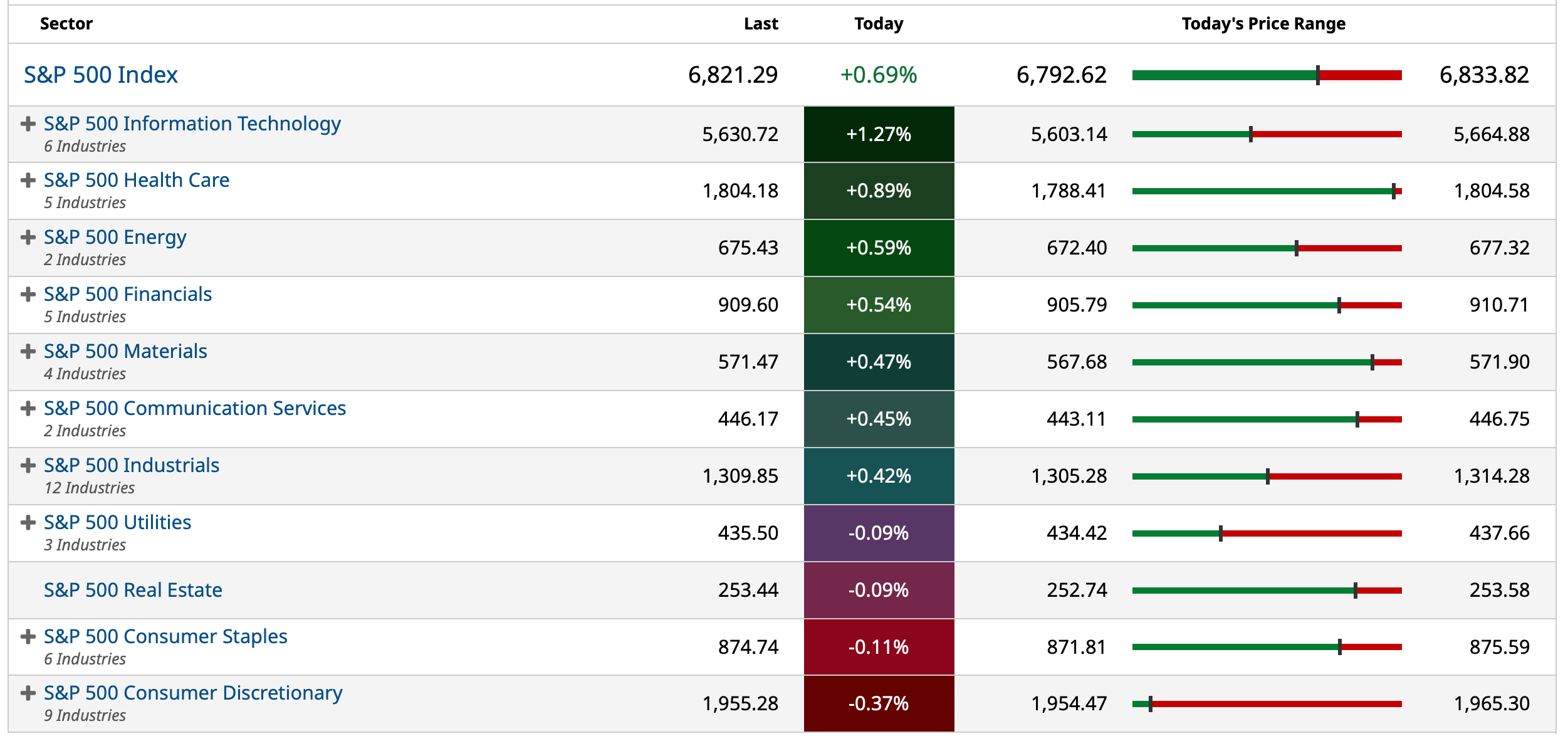

S&P 500 Sectors

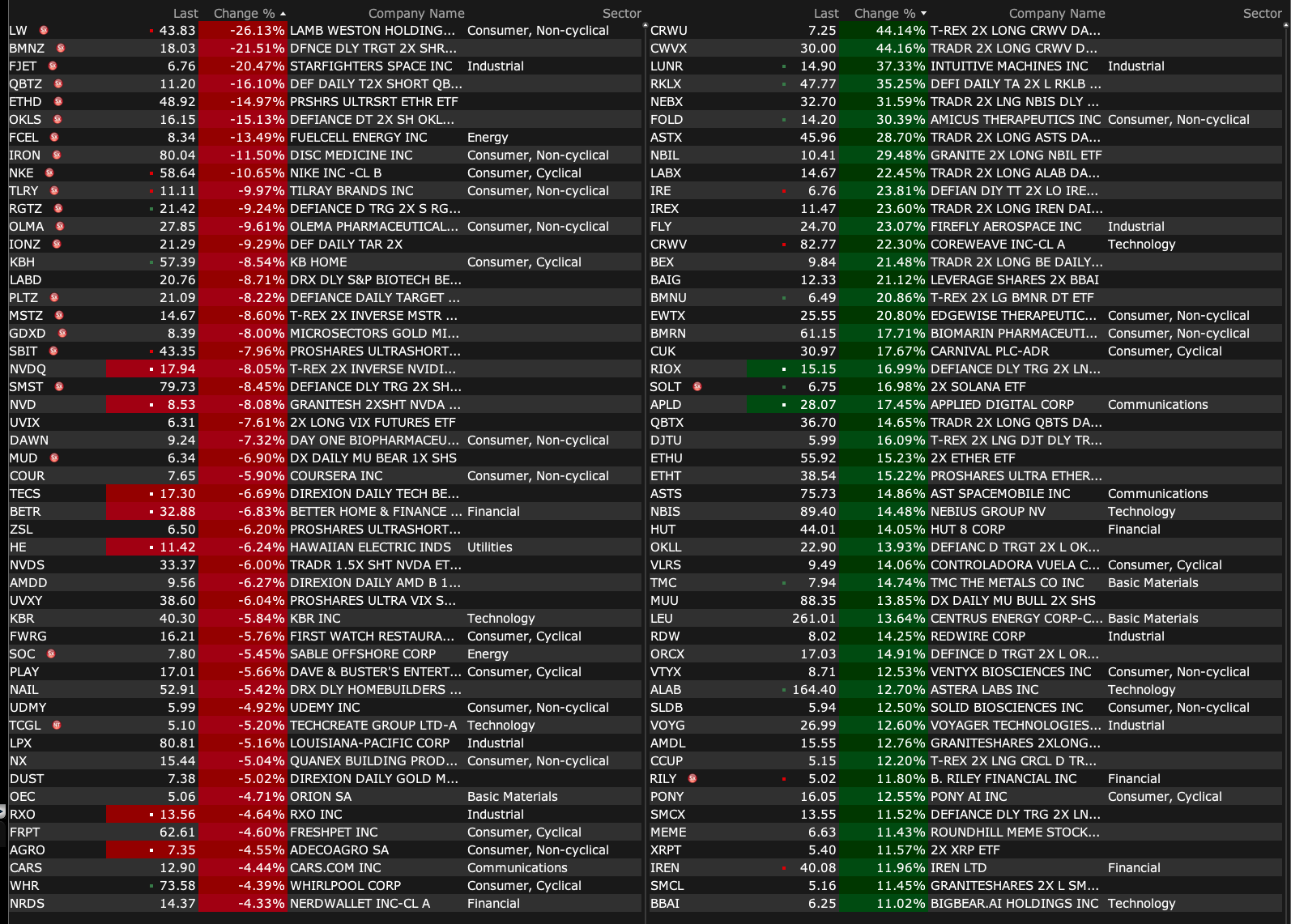

% Movers

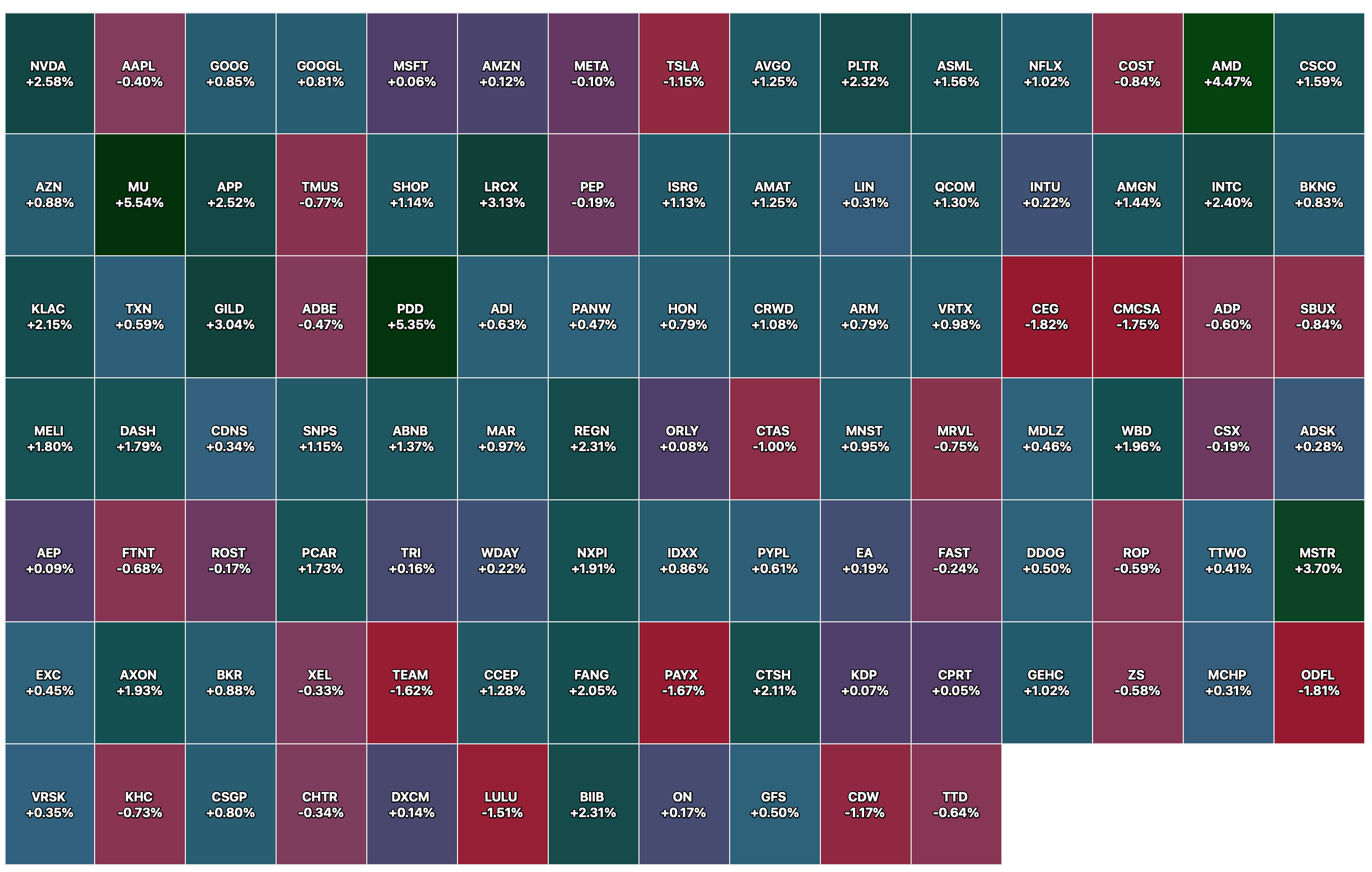

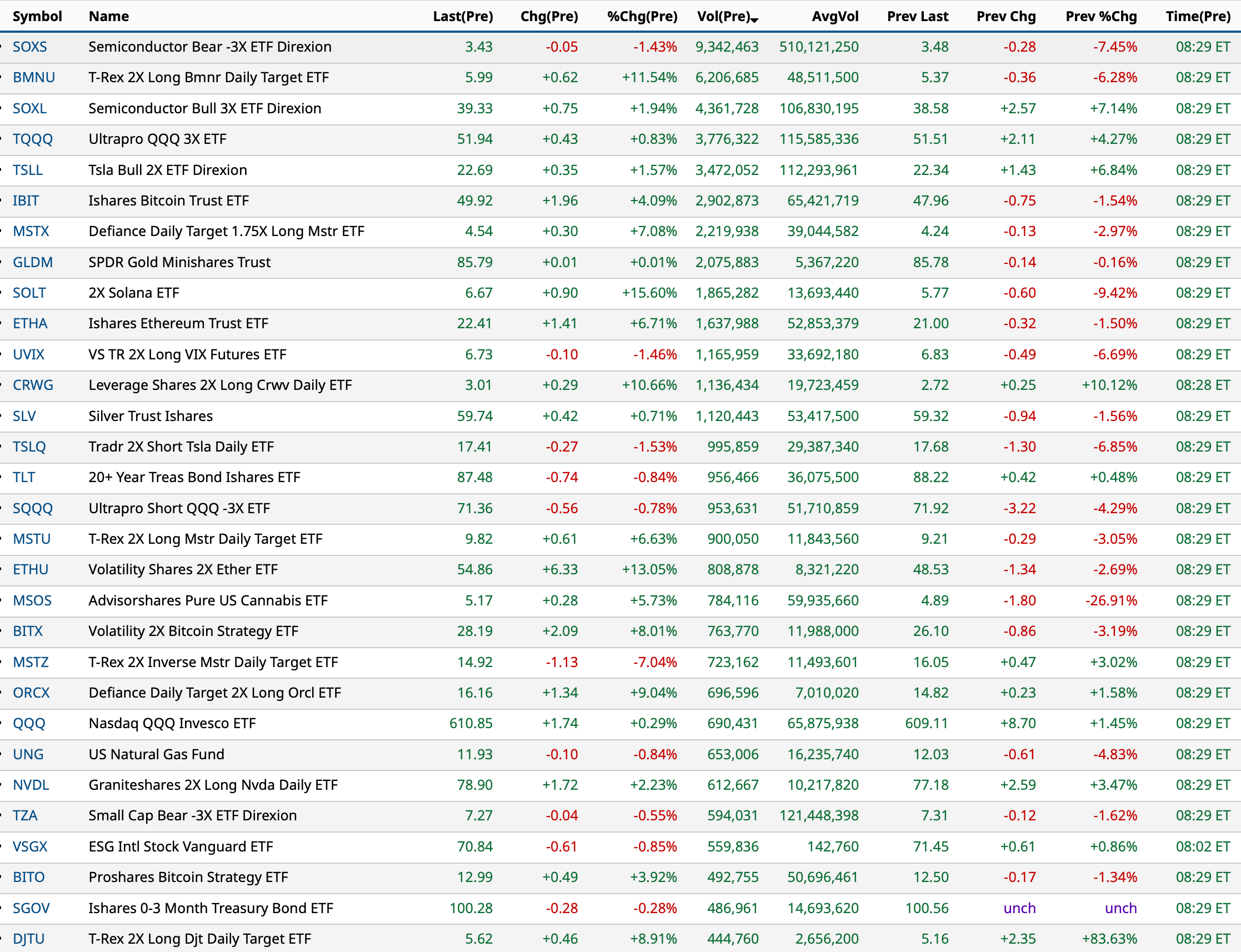

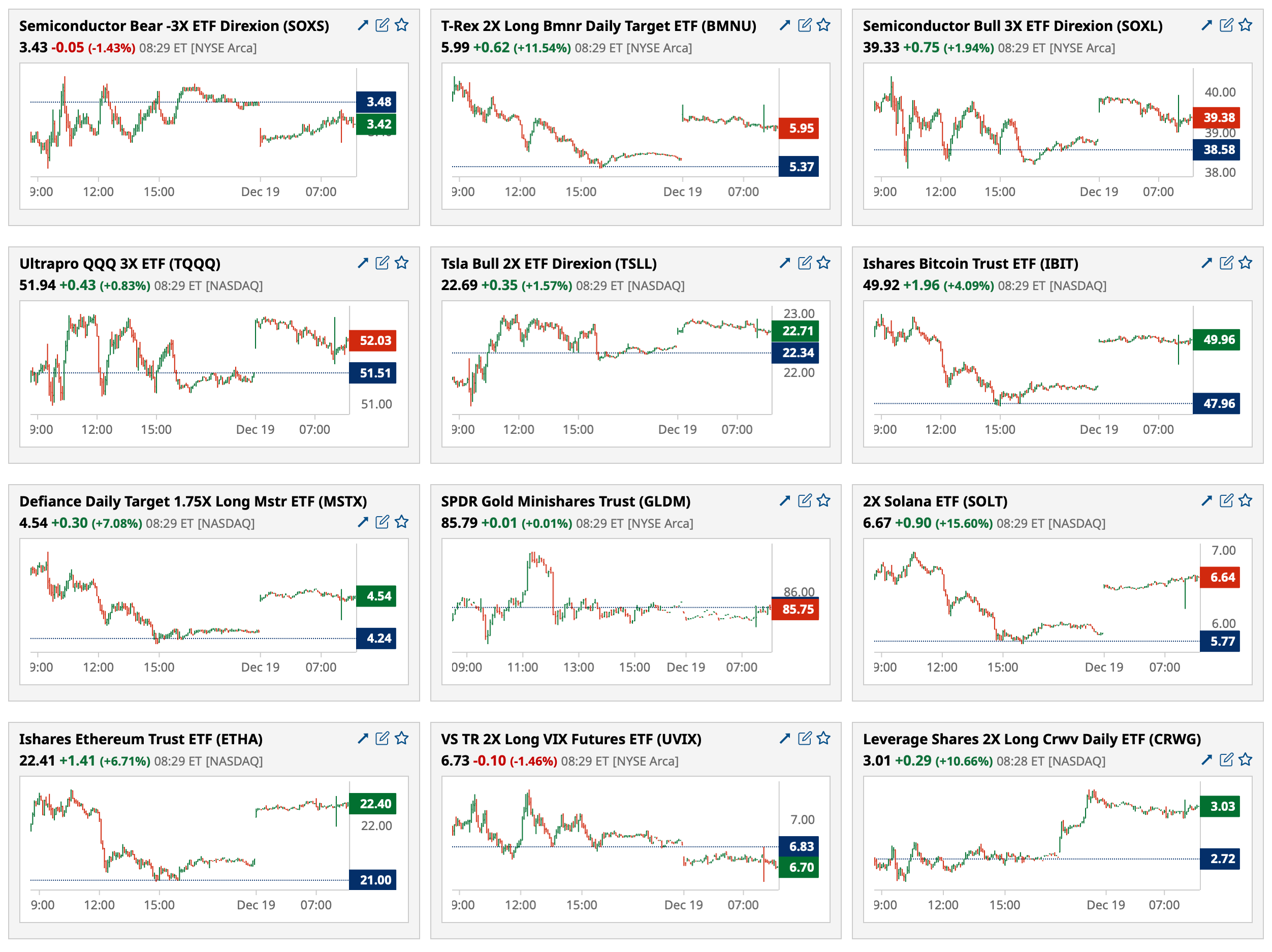

Nasdaq 100 Heat Map

BY Doug Kass · Dec 19, 2025, 4:25 PM EST

Thanks for reading my Diary today and all week — I hope it has been helpful.

Enjoy your weekend.

Be safe.

BY Doug Kass · Dec 19, 2025, 3:30 PM EST

Wolf Street howls about expanding housing inventory:

BY Doug Kass · Dec 19, 2025, 3:17 PM EST

BY Doug Kass · Dec 19, 2025, 3:02 PM EST

I admire "The Dales Report" for its thoroughness, insights and objectivity.

Let's go to the tape:

BY Doug Kass · Dec 19, 2025, 2:06 PM EST

From Quoth The Raven

BY Doug Kass · Dec 19, 2025, 1:25 PM EST

Bond yields continue to climb while the S&P earnings yield (the inverse of the price/earnings multiple) continues to decline.

This means the equity risk premium (which is now a discount!) is growing ever more extreme — auguring even more poorly for future investment returns.

BY Doug Kass · Dec 19, 2025, 12:54 PM EST

From Peter Boockvar:

Positives,

1) With inflation running at 3%, the BoJ raised rates by 25 bps to .75%.

2) In a tight 5-4 vote, the BoE cut rates by 25 bps to 3.75%.

3) The ECB, Riksbank, Norges Bank and Bank Indonesia held rates unchanged. Thailand cut by 25 bps as expected.

4) US CPI in November rose 2.7% y/o/y and 2.6% core but key line items were literally missing. Also, the BLS plugged in zero for rent growth and while real world new rents might be flattish, renewal rates are still rising 2-3%. Treasuries didn’t believe it either.

5) November payrolls grew by 64k, above the estimate of 45k but after falling by 105k in October (government shutdown of course the main factor) . September was up 108k vs the initial print of 119k. The shutdown cut government jobs by 157k in October. Hiring in health care/social assistance drove most of the job gains, again. Average hourly earnings rose by .4% m/o/m in October and off that was up .1% in November. With hours worked at 34.3 vs 34.2 in the two months prior, average weekly earnings were up .4% m/o/m and 3.5% y/o/y. The participation rate was 62.5% vs 62.4% in September. The key 25-54 yr old cohort saw a rate of 83.8% which is the highest since August 2024.

6) Initial jobless claims fell to 224k from 237k as expected and the 4 week average was little changed at 218k vs 217k. Continuing claims totaled 1.897mm vs 1.83mm but below expectations of 1.93mm.

7) The UoM consumer confidence index for December did lift to 52.9 from 51 but only off one of the lowest readings on record. They said, “While lower-income consumers posted gains, sentiment for higher income consumers was little changed.” And, “Despite some signs of improvement to close out the year, sentiment remains nearly 30% below December 2024, as pocketbook issues continue to dominate consumer views of the economy.”

8) From FedEx: FedEx Express saw revenue up 8%, “driven by US domestic package revenue growth with strength across all services.”

9) From Nike: “The geography that is leading the way for Nike right now is North America.”

10) From Darden: “During the quarter, our casual brands saw an increase of visits y/o/y from guests within middle to higher income groups...We did see strong traffic growth from guests 55 and over as well on the demographic side, but there was a little pullback in those earning less than $50,000 in the casual brands.”

11) From Micron: “We achieved a number of records in fiscal Q1. Total company revenue, DRAM and NAND revenue, as well as HBM and data center revenue, and revenue in each of our business units also reached new records…Sustained and strong industry demand, along with supply constraints, are contributing to tight market conditions, and we expect these conditions to persist beyond calendar 2026.”

12) The November Cass Freight shipments index saw a 2.7% m/o/m increase seasonally adjusted after a 2.1% drop in October. Versus last year they are still down 7.6%, “putting the index on track for a 6% decline in 2025” said Cass. They also said, “After truckload volumes briefly improved in Q3 ahead of the October 5 import tariff deadline, they have softened again so far in Q4 as pre-tariff stocks are drawn down. Resilient early holiday consumer spending data suggest some pent-up demand could be building, but tariffs are likely to continue to press prices higher and affordability lower in 2026.”

13) Headline CPI in the UK was higher by 3.2% y/o/y in November but down from 3.6% in October and below the estimate of 3.5%. The core rate also was up 3.2% vs 3.4% in the month before and which was also the forecast. Services inflation still remains high at 4.4% vs 4.5% in October. The Office for National Statistics said the drop in the inflation rate of change can be mostly attributed to falls in the price of cakes, biscuits, cereals, and confectionery along with tobacco and Black Friday discounts on women’s clothes.

14) From overseas PMI’s: Japan’s manufacturing PMI rose 1 pt m/o/m but still below 50 at 49.7 while services downshifted to 52.5 from 53.2. Australia’s was mixed too with manufacturing rising to 52.2 from 51.6 and services slipping to 51 from 52.8. India continues to be the standout with a composite index of 58.9 with manufacturing at 55.7 and services at 59.1.

15) In the UK, both manufacturing and services rose about 1 pt m/o/m to 51.2 and 52.1 respectively. S&P Global attributed the improvement to “the post Budget lifting of uncertainty” but with this too, “However, the overall pace of output and demand growth remains lackluster, and the expansion is still very dependent on technology and financial services activity, with many other parts of the economy struggling to grow or in decline.”

16) Japan reported its Q4 Tankan report on both manufacturing and non-manufacturing and for large and small businesses and was mostly flat to slightly better vs Q3.

17) In case you missed it, https://peterboockvar.substack.com/p/video-louis-vincent-gave-on-the-real

Negatives,

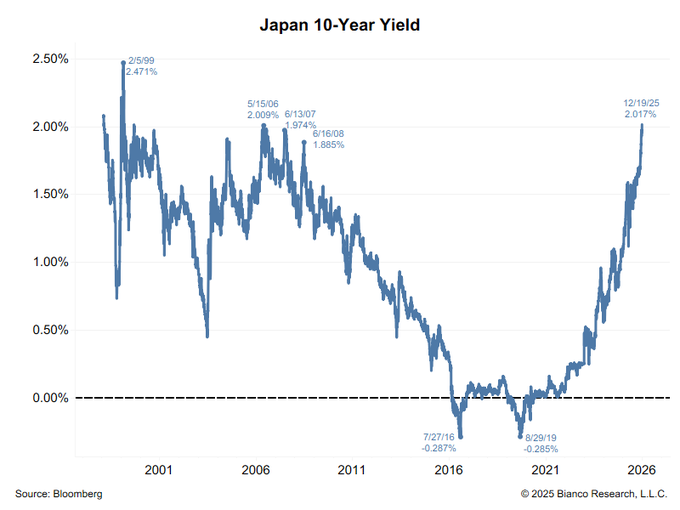

1) With inflation running at 3%, the BoJ raised rates by only 25 bps to .75% and while Governor Ueda said rates should rise further in 2026, he didn’t say so with conviction. Yields went higher across their curve, again, and yen got hit hard in response.

2) In the November US jobs report, the household survey showed a gain of 96k from September but because it trailed the 323k increase in the size of the labor force, the unemployment rose to 4.6% from 4.4% in September, the highest since September 2021. Of particular note, the all in U6 rate jumped to 8.7% from 8% in September and that is the highest since August 2021 and March 2017 before that not including Covid.

3) In the October Treasury International Capital flow data, ‘official’ holdings of US Treasuries, as opposed to ‘private’ activity, fell by $25b in October and has declined by $46b year to date after dropping by $27b in 2024. Their holdings are now down to about 13% of US marketable Treasury securities vs about 33% 10 years ago and almost 40% 15 years ago.

4) Commentary within the S&P Global US PMI was noteworthy. “Input cost inflation accelerated markedly in December, hitting the fastest since November 2022. Although manufacturers reported slightly slower inflation, the increase in input prices was historically elevated. In contrast, services cost inflation was the steepest in over three years. Cost increases were mostly blamed on tariffs alongside rising labor costs…Increased costs again fed through to higher selling prices, with the overall rate of inflation rising to the steepest since July and therefore amongst the greatest since the pandemic related price-surge of 2022. Although intensifying competition often restricted the ability of manufacturers to pass on higher costs, resulting in the slowest rate of selling price inflation since January, prices were raised in the service sector to a degree not seen since August 2022.”

5) The November Architecture Billings Index fell to 45.3 in November from 47.6 in October, thus remaining below 50. The chief economist there said “Weakness in business conditions at architecture firms continues to be widespread, with declining billings across all major specializations and in every region except the Midwest. However, inquiries for new projects continued to increase, and design activity at firms in the Midwest - a region that traditionally has had a disproportionate share of manufacturing activity - appears to have hit its bottom for this cycle and is expected to continue to improve.”

6) Mortgage applications for the week ended 12/12 fell w/o/w with purchases down for a 2nd week by 2.8% while refi’s dropped by 3.6% after a jump of 14% last week.

7) The December NAHB home builder sentiment index was 39 vs 38 in November and as estimated. While the present situation remains well below 50 at 42, optimism still reigns as the Expectations component was 52 from 51 in November. Prospective Buyers Traffic though remains punk at 26, unchanged and about half the 50 breakeven level. The still subdued builder sentiment can be attributed, not surprisingly, to the following factors stated by the NAHB, “rising construction costs, tariff and economic uncertainty, and many potential buyers remaining on the sidelines due to affordability concerns.” And as seen with the public builders and what they are doing to move product, “Market conditions remain challenging with two-thirds of builders reporting they are offering incentives to move buyers off the fence.”

8) Existing home sales in November totaled 4.13mm annualized, about as expected but still hovering around the lowest levels since the mid 1990’s when the US population was much smaller.

9) The always volatile December NY manufacturing index that bounces around like an EKG chart fell to -3.9 vs 18.7 in November. The Philly manufacturing index fell to -10.2 from -1.7. The KC index fell to 1 from 8.

10) From FedEx: “Freight results remain pressured, driven primarily by lower volumes, partially offset by higher weight and revenue per shipment.” Revenue here was down 2%.

11) From Nike: “In Greater China, we highlighted last quarter that we were facing a longer road to a healthier business...What we’ve done is a start, but it’s not happening at the level or the pace we need to drive wider change.” Also, “near term investments to clean up and elevate the marketplace have put real pressures on margins. Tariffs have also obviously added a significant headwind to overcome.” The cost to them from tariffs? “As we highlighted last quarter, we are also navigating new structural headwinds from the $1.5 billion of annualized incremental product costs due to higher US tariffs.”

12) From Darden: “Commodity headwinds were stronger than we anticipated as beef prices remained at historically high levels throughout the quarter.”

13) From KB Home: “Near-term conditions continue to reflect underlying demand for homes, supported by population, household formation, job and wage growth; however, low consumer confidence, affordability concerns, and elevated mortgage rates continue to constrain the pool of actionable buyers. Consumers are demonstrating their interest in buying a home, reflected in our website visits, leads, and traffic to our communities. They’re just taking much longer to make their homebuying decisions.”

14) From Lennar: “As you may recall, last quarter I noted that declining interest rates could signal the start of a market recovery. Unfortunately, that turnaround has not yet materialized. As rates slowly moderated in September, eased more in October and remained flat in November, the customer response remained fairly tepid, suggesting that a combination of affordability and consumer confidence issues were continuing to limit demand. Of course, the coincident threat of government shutdown in September and the actual shutdown from October 1st through mid November further eroded already weak consumer confidence. While traffic was consistent, customers were both hesitant and limited by what they could afford to purchase.”

15) From Accenture: “Starting with the demand environment, clients continue to prioritize their most strategic and large scale transformational programs, which convert to revenue more slowly, but position us at the center of the reinvention agendas. The pace of overall spending and discretionary spend in our market is at the same levels we have seen over the last year.”

16) From General Mills: “While we’re encouraged by the progress we’re making in improving volume, we’ve seen a change in consumer behavior this year that is driving an increase in the cost of volume across our categories. More specifically, with lower and middle-income consumers continuing to feel significant economic pressure, we’ve seen them make a greater proportion of their food purchases on promotion rather than at everyday prices. And this has not been driven by increased frequency or depth of promotions by General Mills or our competitors - those metrics are essentially unchanged from a year ago - it’s simply a reflection of stressed consumers finding ways to stretch their dollars further.”

17) The December German IFO business confidence index fell a touch to 87.6 from 88 and below the estimate of 88.2. The Current Assessment was unchanged at 85.6 but the Expectations component fell slightly to 89.7 from 90.5 and vs the forecast of no change. The IFO said succinctly, “The year is ending without any sense of optimism.”

18) The December UK CBI industrial orders index remained deeply negative but less so at -32 vs -37 in November and vs the estimate of -35. The CBI said “Manufacturing output is still falling, but the pace of decline has eased. Activity was clearly held back by uncertainty ahead of the Budget, and with that now out of the way firms can look to 2026 with a little more certainty…Significant headwinds remain nonetheless, with demand still soft, high energy, labor and regulatory costs squeezing margins, and uncertainty around key policies and global conditions continuing to weigh on confidence.”

19) In the Eurozone, its manufacturing PMI fell to 49.2 from 49.6 and the services component was down by 1 pt to 52.6 with both below expectations. S&P Global said this, “Economic growth slowed at the end of the year due to a slight contraction in the manufacturing sector and weaker momentum in the service sector. The weaker performance is primarily attributable to German industry, where the downturn intensified. In France, on the other hand, there are signs of a cautious recovery in industry, although a single monthly figure should not be overrated. However, the service sector, which had expanded last month, is stagnating there, while Germany’s service companies saw another solid rise in activity. All in all, the runway into the new year seems pretty unstable.”

20) In China, retail sales rose just 1.3% y/o/y, well under the estimate of up 2.9% and this coincided with another drop in home prices, both new and used. Industrial production rose 4.8% y/o/y, about as forecasted. The weakness in housing and construction was reflected in the 15.9% ytd decline in property investment vs the estimate of down 15.4%.

BY Doug Kass · Dec 19, 2025, 12:39 PM EST

Bret Jensen

I definitely agree the CPI reading was an absolute joke. That said, people should factor in how deflationary the shelter component (the largest portion of the CPI calculation) will become going forward. Mass re-migration (2.5M migrants to date) is a huge factor in rents declining nationally for four straight months now on a year-over-year basis. In addition, 640K apartments came on line in 2024. The largest number since 1973. While completions (500,000) were down in 2025, they were far above pre-pandemic levels (375,000).

Then we have existing home sales which have muddled along at their lowest levels since 1995 starting in 2023. Average home prices have flatlined over the past couple of years after surging from 2012-2022, especially after Covid. A survey from Kiplinger this spring had the all-in costs to own a single family at 57% above that of renting the same home across 100 major U.S. metros. With incentives, new home prices are lower than used home prices. With rents falling, it is hard to see how average existing home prices do not fall in the years ahead. Whether that happens quickly like the Housing Bust or is a slow grind down over a decade is the primary question. Either way, rent/housing will be a deflationary force in the years ahead. JMTC

BY Doug Kass · Dec 19, 2025, 11:35 AM EST

BY Doug Kass · Dec 19, 2025, 11:20 AM EST

* President Trump's endorsement of rescheduling was not forceful and failed to resolve a number of important issues

* Trade cannabis equities, don't invest in cannabis stocks

"I have always told me kids, 'don't take drugs'... No drinking, no smoking. Just stay away from drugs."

- President Trump (at yesterday's rescheduling press conference)

Throughout the last five years, I have aggressively traded cannabis equities, buying cannabis stocks on weakness and selling on the slightest hint of regulatory reform and relief.

In most cases, this sort of positioning (and trading) has been quite profitable.

At the same time I have consistently had misgivings about investing in the cannabis space, for several fundamental and structural reasons:

* To begin with, the total addressable market (TAM) for cannabis is likely much smaller than the industry optimists have forecast. Already, recently permitted states have experienced a disappointing adoption curve. Revenues, cash flow and profits have been well below analysts' and managements' projections. Some multiple state operators are are even exiting some states/jurisdictions.

* The current structure of state silos (and dispensary restrictions in some states) result in diseconomies of scale and an inability of creating (hoped for) oligopolistic industry consumer brands (and, with it, pricing power).

* Product pricing remains under pressure (as do revenues, cash flows and profits) and, if anything, rescheduling could exacerbate this condition.

* Past uncertain tax liabilities (from 280E) are massive, and though likely to be eventually resolved, represent still large company liabilities. Industry balance sheets are in poor shape -- with secondary/tertiary state operators facing an almost impossible "debt refinancing cliff" (and an inevitable dilution of shareholders equity).

* Based on the president's comments, banking and custodian issues (important in order to attract institutional investors) are unlikely to be resolved in the (reasonable) near term.

* Without institutional sponsorship, I am of the view that a depleted retail base of investors will not be able to sustain rallies in the sector.

This brings us to yesterday's announcement that Pres. Trump endorses the process of rescheduling of cannabis (from a Schedule 1 to a Schedule 3 substance).

Here is Pres. Trump's rescheduling recommendation and reclassification comments from Thursday.

Cannabis equities collapsed all Thursday afternoon, surprising and disappointing most (but not me).

Let me try to explain why I think the stocks fared so poorly yesterday and why I don't expect much of a rally from currently depressed levels:

1. The stocks anticipated this news and had rallied into the announcement. (I had shorted that ramp, as posted. I have since covered).

2. In listening to Pres. Trump, he did not exactly provide a ringing endorsement for cannabis. He did not sanction its use as a recreational drug. Rather, he is in support of medical research and actually distanced himself from recreational use of cannabis.

3. Trump emphasized the benefit of hemp; he apparently is in favor liberalizing the use of hemp. This is a competitive threat to cannabis.

4. The decision was heavily influenced by his dear friend Howard Kessler (a leader in cannabis research) and by Kim Rivers Trulieve (TCNNF) and some other multiple state operators.

5. As I noted earlier this week, the President's rescheduling request is a request to proceed with the process of rescheduling. This could take one or two months. This means that the punitive impact of 280e tax liabilities might still be felt in the 2025 tax year.

6. The uncertain tax status of past 280e tax liabilities remain an issue for the cannabis companies that have not yet paid those taxes.

7. Banking, custodian and uplisting issues remain unresolved. Nothing in the President's comments suggest that there is an immediacy to resolve these important issues.

8. Without institutional support, the depleted ranks of cannabis traders and investors don't have the bones to sustain a rally in the sector.

There will continue to be trading opportunities in cannabis stocks.

Nonetheless, rescheduling has not resolved important structural and fundamental problems facing the industry and investors.

Trade cannabis stocks, don't invest in cannabis stocks.

And say no to drugs.

BY Doug Kass · Dec 19, 2025, 10:45 AM EST

Dougie Kass

STAFF

Just Now

Moved to S/M short SPY $680.08 and QQQ $617.05 with S and P cash +56 handles.

BY Doug Kass · Dec 19, 2025, 10:12 AM EST

Back shorting the indexes with S&P cash +34 handles:

Dougie Kass

STAFF

1 minute ago

Set as featured

Report

With S&P cash +34 handles I am back shorting the indexes.

(SPY) $678.05

(QQQ) $614.02

BY Doug Kass · Dec 19, 2025, 9:50 AM EST

BofA analyst Peter Galbo raised the firm's price target on PepsiCo to $164 from $155 and keeps a Neutral rating on the shares. Entering 2026, the largest unresolved question for staples remains consumption growth and valuations remain dispersed across the group, but "there feels little to get them off the sidelines in '26 until fundamentals signal a greater turning of the tide," the analyst tells investors in a year-ahead note for the consumer staples group.

BofA analyst Peter Galbo raised the firm's price target on Coca-Cola to $85 from $80 and keeps a Buy rating on the shares. Entering 2026, the largest unresolved question for staples remains consumption growth and valuations remain dispersed across the group, but "there feels little to get them off the sidelines in '26 until fundamentals signal a greater turning of the tide," the analyst tells investors in a year-ahead note for the consumer staples group.

BY Doug Kass · Dec 19, 2025, 9:38 AM EST

BY Doug Kass · Dec 19, 2025, 9:22 AM EST

-FOLD +30% (to be acquired by BioMarin in $4.8B all-cash deal at $14.50/shr)

-WYFI +20% (WhiteFiber and Nscale announce 10-Year, 40 MW Colocation Agreement Representing Approximately $865M in Total Contract Value at NC-1 AI Data Center Campus)

-WGO +15% (earnings, guidance)

-LUNR +7.6% (Keybanc/Pacific Crest Initiates LUNR with Overweight, price target: $20)

-PDD +6.1% (appoints Jiazhen Zhao and Lei Chen as co-chairmen and names new senior executives)

-MSOS +5.7% (President Trump signs executive order to expedite reclassification of marijuana as a schedule III substance)

-CRWV +5.6% (confirms joined Department of Energy’s Genesis Mission to Advance U.S. Research and Innovation)

-ORCL +4.7% (TikTok signs agreements to sell US TikTok to JV controlled by American investors; Oracle, Silver Lake and Abu Dhabi's MGX will collectively own 45% of TikTok's US entity)

-GNRC +3.8% (Wells Fargo Raised GNRC to Overweight from Equal Weight, price target: $195)

-IREN +3.1% (momentum following broker upgrade)

-PAYX +2.6% (earnings, guidance)

-COIN +2.5% (momentum)

-SCHL +2.5% (earnings, guidance)

-PANW +2.4% (confirms significant expansion of strategic partnership with Google Cloud to enable the secure development and deployment of AI solutions)

-AVO +2.1% (earnings, outlook)

-BMRN +2.0% (FOLD to be acquired by BioMarin in $4.8B all-cash deal at $14.50/shr)

-NKE -12% (earnings, guidance)

-BB -6.5% (earnings, guidance)

-KBH -5.4% (earnings, guidance)

-LYFT -3.0% (Wedbush, Inc. Cuts LYFT to Underperform from Neutral, price target: $16)

-FDX -2.8% (earnings, guidance)

-AGCO -2.5% (Barclays Cuts AGCO to Underweight from Equal Weight, price target: $93)

-LW -2.3% (earnings, guidance)

BY Doug Kass · Dec 19, 2025, 9:15 AM EST

BY Doug Kass · Dec 19, 2025, 9:05 AM EST

BY Doug Kass · Dec 19, 2025, 8:45 AM EST

The shares of Ferrari, (RACE) my newest long, are up by another eight dollars in premarket trading - after yesterday's surge.

Two columns from the last week:

* Playing the K-shaped U.S. economy...

I have taken a starter investment position in Ferrari (RACE) .

By no means, cheap, the shares have fallen from $519 to about $370, but the company is achieving software margins with its unique niche.

More analysis later in the week:

* Ferrari shares down 13% on fears of slowdown

* Calls of the Day: Netflix, Coinbase and Ferrari

Position: Long Race (VS)

By Doug KassDec 15, 2025 8:00 AM EST

I added to Ferrari (RACE) at $368.88.Position: Long RACE (S)By Doug KassDec 15, 2025 11:37 AM EST

BY Doug Kass · Dec 19, 2025, 8:25 AM EST

I have covered my Index shorts - quick and profitable trade:

* (SPY) $675.32

* (QQQ) $610.72

From early this morning:

I'm shorting the indices in early premarket trading:

* (SPY) $677.03

* (QQQ) $612.49

Position: Short SPY common (VS), QQQ common (VS)

BY Doug Kass · Dec 19, 2025, 8:18 AM EST

BY Doug Kass · Dec 19, 2025, 8:15 AM EST

The header of this column ("Lies, Damned Lies and Statistics") is a quote commonly believed to be sourced by Mark Twain who has attributed it to the British Prime Minister Benjamin Disraeli. It is a phrase that describes the persuasive power of statistics to bolster weak arguments.

I call B.S. to yesterday's cooler-than-expected CPI print.

It was "fake news." But I should add that the CPI readings are all fake to begin with — especially with all those hedonistic adjustments that have been made. But this monthly print was more fake than normal!

Moreover, the CPI was an "easy" compare against a very hot CPI a year ago.

From Peter Boockvar:

November CPI, where only some of the month was captured as info didn’t start being calculated until November 14th because of the shutdown, rose 2.7% y/o/y headline and 2.6% ex food and energy better than the estimate of up 3.1% and 3% respectively.

All of these figures are y/o/y because of the lack of October data. Energy prices were up 4.2% y/o/y because of an 11.3% jump in fuel oil. Food prices were up 2.6% y/o/y mostly led by ‘food away from home’ where prices were up 3.7% vs 1.9% for ‘food at home.’

Services inflation ex energy rose 3% y/o/y vs 3.5% in September and with Owners’ Equivalent Rent up by 3.4% (yes, overstating but never captured the full rise a few years ago) vs 3.8% in September. Rent of Primary Residence was up 3% vs 3.4% in September. ‘Tenant and household insurance’ prices spiked by 7% y/o/y. Medical care costs were up by 3.3% y/o/y with a 5.7% jump in ‘medical services.’ Not reality was the .6% y/o/y rise in health insurance prices. I’ll take that plan. We’re going to hear much more about this, electricity prices were up by 6.9% y/o/y.

They did not include vehicle insurance which I’m not sure why (I guess couldn’t get the data) and wonder if that was one reason why the overall data was less than expected. Other items were missing too. Motor vehicle maintenance costs jumped by 6.9% y/o/y. After three months of gains, airline fares fell by 5.4% y/o/y and hotel prices declined by 5.7% y/o/y.

On the core goods side, they rose 1.4% y/o/y vs 1.5% in September and which has been an acceleration after months of disinflation. We can blame tariffs for the reversal up. Used car prices rose 3.6% y/o/y while new car prices gained .6%. Apparel prices rose .2% y/o/y after a one tenth drop in September. Prices of household furnishings & supplies gained 2.6% y/o/y.

Bottom line, the deceleration of rental growth helped to moderate services inflation and is the main reason for the inflation miss. Medical care costs also slipped. What inflation would have been if the full data was collected will remain to be seen and again, I’m not sure why auto insurance was not included in the y/o/y figure as that has been a hot spot of price gains as we know. Other prices were missing too. I expect further rental price growth into the first half of 2026 but reversing back higher in the latter part of next year and into 2027 because of the lack of new construction.

While the S&P futures are excited about the data, Treasury yields are not moving much, down by just 1 bp for the 2s and flat with the 10s and 30s vs 8:29am est. But, inflation breakevens are falling with the 2 yr down by 7 bps, the 5 yr lower by 4.5 bps and the 10 yr down by 3 bps.

BY Doug Kass · Dec 19, 2025, 8:05 AM EST

BY Doug Kass · Dec 19, 2025, 7:55 AM EST

BY Doug Kass · Dec 19, 2025, 7:45 AM EST

BY Doug Kass · Dec 19, 2025, 7:35 AM EST

BY Doug Kass · Dec 19, 2025, 7:25 AM EST

BY Doug Kass · Dec 19, 2025, 7:15 AM EST

* Which is one of the reasons that forward stock market returns will be negligible...

BY Doug Kass · Dec 19, 2025, 7:05 AM EST

BY Doug Kass · Dec 19, 2025, 6:55 AM EST

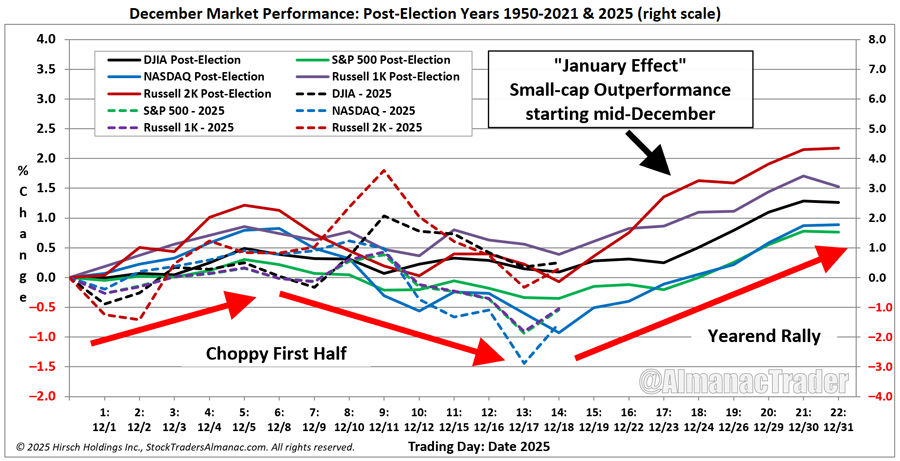

For those that track the Decennial Cycle (STA page 131), years ending in “6,” are on a solid run. In addition to DJIA’s streak of five straight gains in years ending in 6, S&P 500 has matched that streak, while NASDAQ and Russell 2000 have never declined in a year ending in 6. S&P 500’s average gain in years ending in 6 since 1976 is an impressive 15.4%. All the tables and data for the Decennial Cycle were included in yesterday’s 2026 Annual Forecast webinar.

Although we did not provide specific forecasts for gold, silver, bitcoin, crude oil, natural gas, and copper, we did cover their respective performance in midterm years and 6th years of presidential terms with seasonal pattern charts for all. Midterm seasonals for gold, silver, and copper suggest the current rally could easily extend into the New Year. Current weakness in energy could also persist in 2026 based upon midterm seasonal patterns for crude and natural gas. Bitcoin has historically had a tough time in midterm years, and its recent weakness could morph into a nasty bear next year if investor interest continues to wane.

In the near-term, we remain bullish and are encouraged by today’s rally. Compared to December’s performance in previous post-election years, today’s advance appears to have arrived right on seasonal cue following a choppy and volatile first half of December. The volatility this December is clearly visible in the following chart with 2025 plotted on the right scale which is double the historical averages.

As of today’s close, DJIA and Russell 2000 are positive for December, up 0.49% and 0.30% respectively. NASDAQ has been the weakest, down 1.54% with tech-heavy S&P 500 and Russell 1000 also down just over 1%. It is also notable that this December’s NASDAQ and S&P 500 underperformance is consistent with past post-election years. Provided the market can hold today’s gains the second half of December rally has likely begun. Historically bullish week after quarterly options expiration (STA page 108) combined with holiday cheer (STA page 80) could propel the market higher through year end.

Stock Portfolio Updates

Over the past six weeks, through the close on December 17, the Almanac Investor Stock Portfolio slipped 1.6% lower, excluding dividends and any potential interest generated by the cash position, compared to a 1.1% decline by S&P 500 and a 1.1% gain by Russell 2000. Across the portfolio, small-cap positions were best on average, advancing 3.5% while mid- and large-cap positions declined on average.

HealWell AI (HWAIF) is on Hold. Broader market AI valuation concerns and likely tax-loss selling has driven HWAIF to its lowest levels ever. The magnitude of the sell-off does appear overdone and we will be looking for a rebound early next year and a likely exit as patience has run thin with management. Management did deliver on its revenue and earnings forecasts, but it still needs a mainstream exchange listing. HWAIF was and still is a highly speculative trade.

EZCorp (EZPW) was added to the portfolio on November 7 when it first traded below its updated buy limit. EZPW can still be considered on dips below its buy limit. As an owner and operator of pawn businesses in the US and Latin America, it is likely to continue to benefit from a murky US labor market and record high prices for silver and gold. EZPW’s double-digit gain since addition to the portfolio contributed to small-cap outperformance.

Collegium Pharmaceutical (COLL) has continued to climb since last month’s earnings report, and it closed at a new 52-week and all-time highs today. Major analysts have begun to notice and price targets are on the rise. Earnings estimates are also bullishly moving higher while its valuation appears reasonable. COLL can still be considered on dips.

Super Micro Computer (SMCI) woes have persisted, and its retreat is responsible for a substantial amount of the portfolio’s overall decline. Broader AI valuation concerns combined with SMCI’s tumultuous history are most likely the main forces behind its retreat. SMCI appears to be on course to test its April lows. If that level holds, it could be the support shares are desperately seeking. SMCI is on Hold.

Grand Canyon Ed (LOPE) was stopped out on November 6 and has been closed out of the portfolio for a total gain of 22.0%.

InterDigital (IDCC) and OSI Systems (OSIS) have also come under pressure and retreated from their respective highs from October and early November. Their combined declines were another drag on overall portfolio performance. IDCC and OSIS are both technology companies and are likely suffering from broad tech weakness and profit taking. Their valuations do not appear to be at the extremes associated with other technology companies. IDCC and OSIS are on Hold.

Rambus (RMBS) was added to the portfolio on November 13 when it dipped below its buy limit of $95. RMBS uptrend off its April low appears intact but it has gotten much more volatile over the past few months. RMBS can still be considered at current levels up to its buy limit.

Encompass Health (EHC) has struggled since releasing earnings in late October. Earnings were better than estimates but apparently not enough to appease investors. At its current price it has relatively attractive valuation metrics and trades at a sizable discount to analyst’s price targets. EHC can be considered at current levels up to a buy limit of $110.

Please see table below for most recent advice. Note some stop losses and buy limits have been updated to account for recent market moves.

BY Doug Kass · Dec 19, 2025, 6:45 AM EST

Cryptocurrency is a modern technology so the Bible fails to directly mention it.

But the Bible offers timeless principles on money, greed and stewardship that apply to it — by warning against get-rich-quick schemes (Proverbs 13:11), covetousness (Luke 12:15) and worshiping at the altar of money (Timothy 6:10).

BY Doug Kass · Dec 19, 2025, 6:35 AM EST

Back to my "thing."

I'm shorting the indices in early premarket trading:

* (SPY) $677.03

* (QQQ) $612.49

BY Doug Kass · Dec 19, 2025, 6:24 AM EST

As I mentioned in yesterday's opening missive, the only value of short-term market forecasts is to make fortune tellers look good:

BY Doug Kass · Dec 19, 2025, 6:15 AM EST

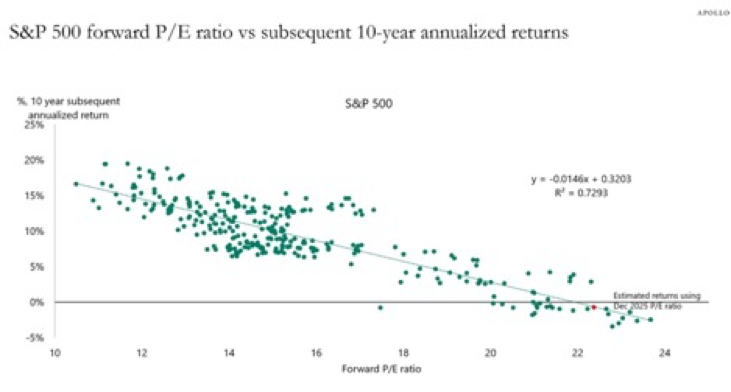

The chart below is from Torsten Slok, Apollo's Chief Economist.

The chart indicates the relationship between starting valuations and subsequent 10-year market returns.

With the S&P 500 Index trading at 23x, the historical implication is that the real, inflation-adjusted return over the next 10 years is poor:

BY Doug Kass · Dec 19, 2025, 6:05 AM EST

BY Doug Kass · Dec 19, 2025, 5:55 AM EST

The S&P Short Range Oscillator moved slightly to more overbought at 0.97% vs. 0.41%.

BY Doug Kass · Dec 19, 2025, 5:45 AM EST