Buying More Amazon

I am moving towards medium sized, buying Amazon (AMZN) after the close at around $221.75.

BY Doug Kass · Dec 17, 2025, 6:19 PM EST

I am moving towards medium sized, buying Amazon (AMZN) after the close at around $221.75.

BY Doug Kass · Dec 17, 2025, 6:19 PM EST

BY Doug Kass · Dec 17, 2025, 4:50 PM EST

BY Doug Kass · Dec 17, 2025, 4:43 PM EST

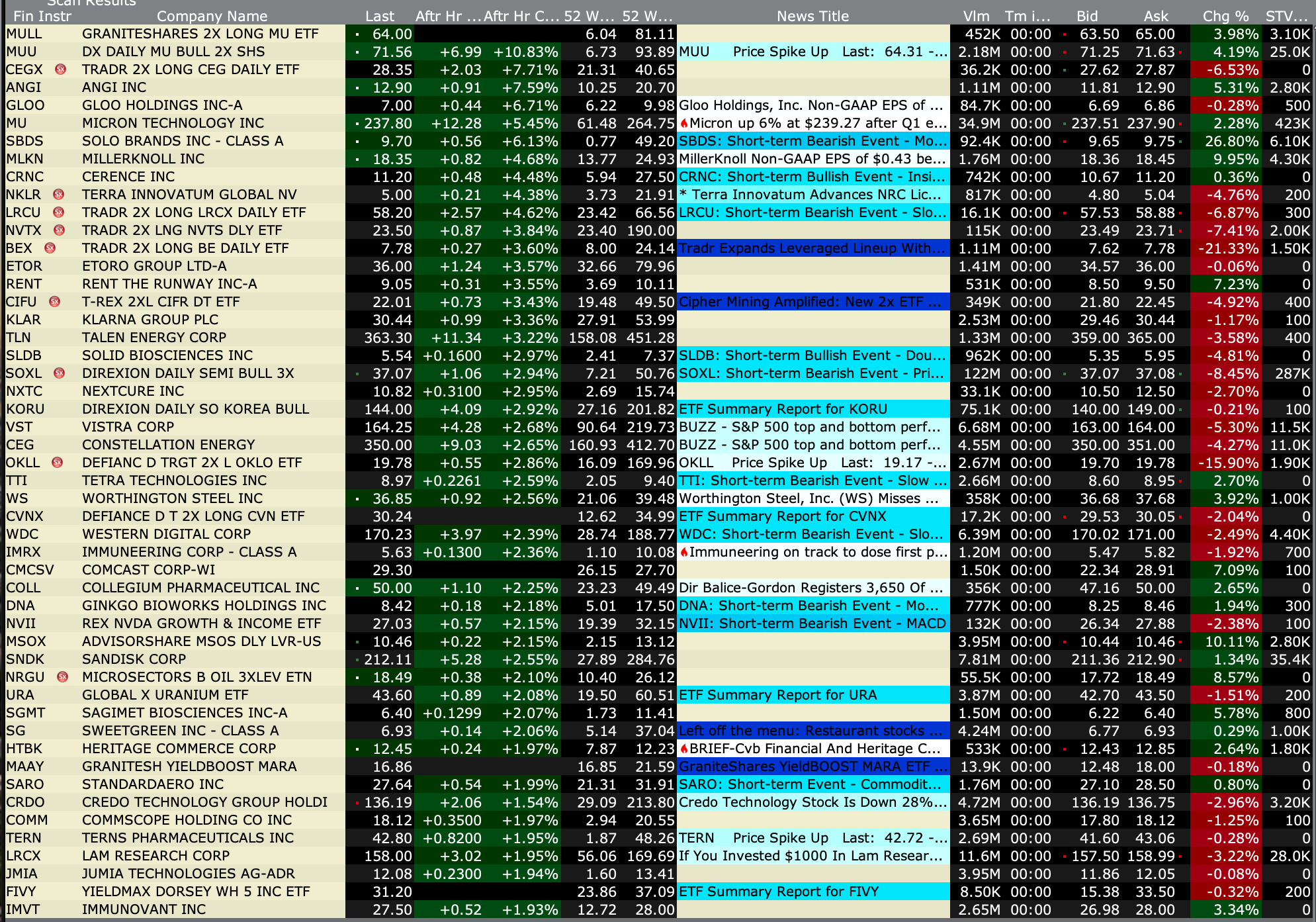

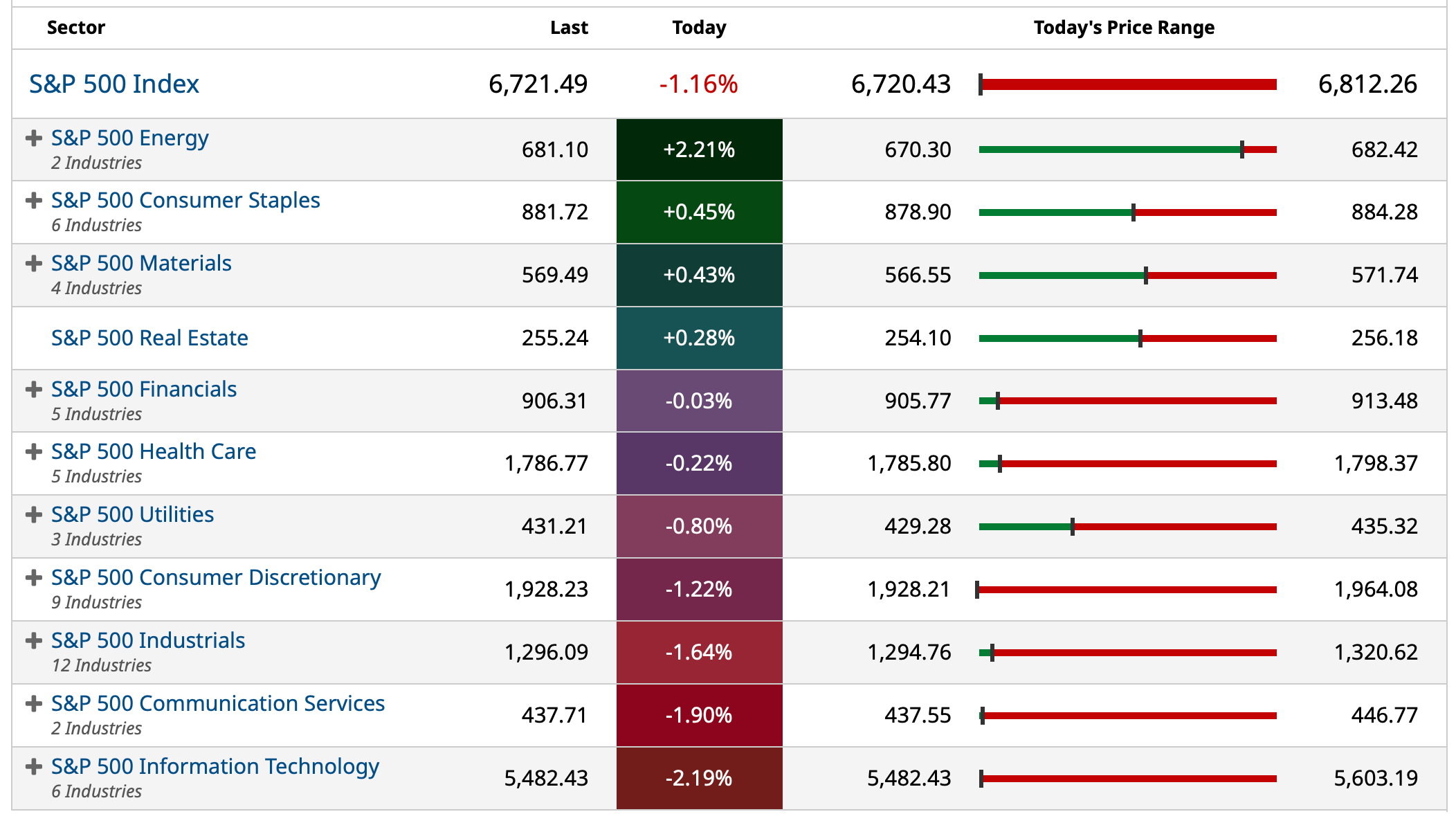

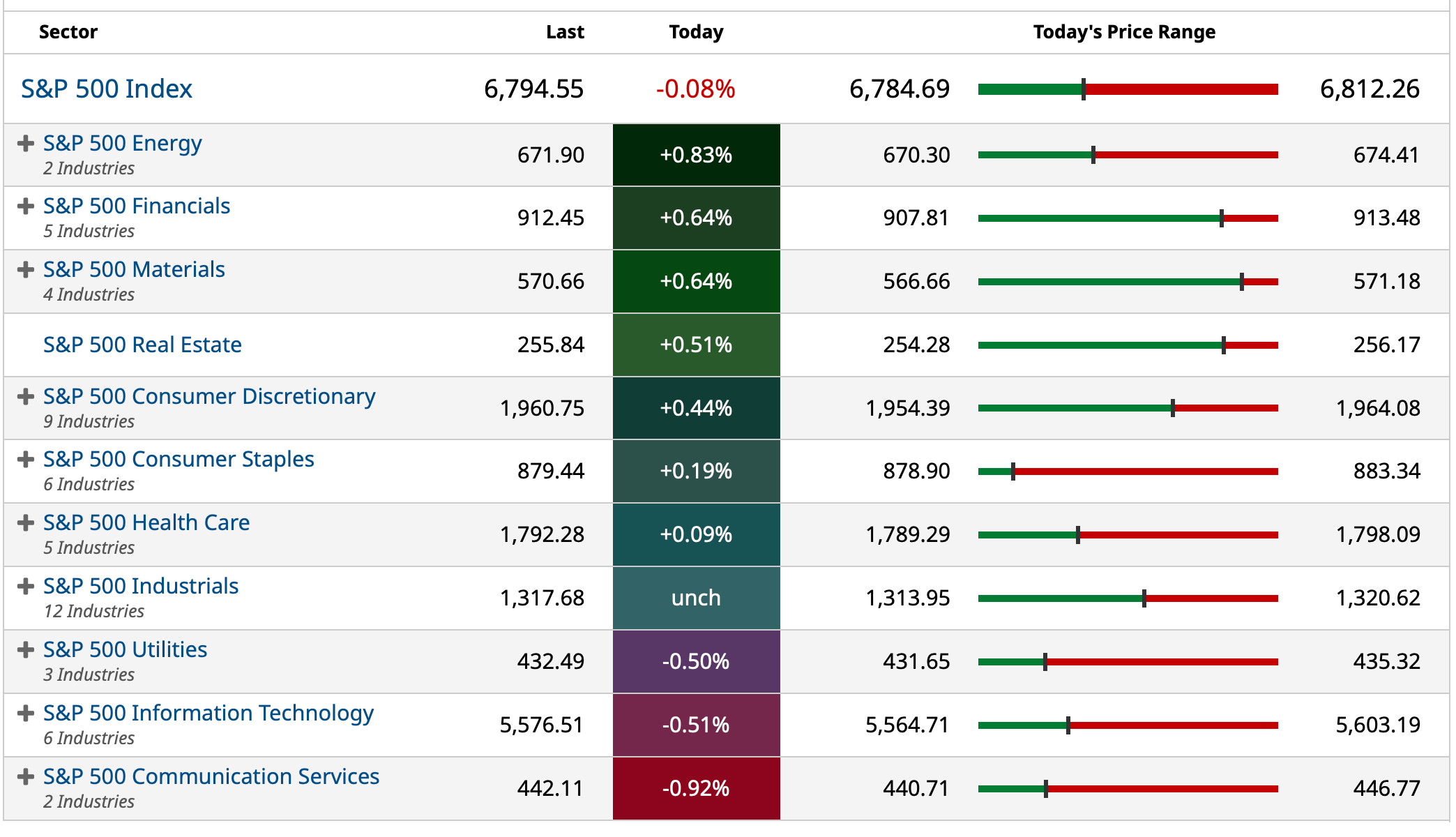

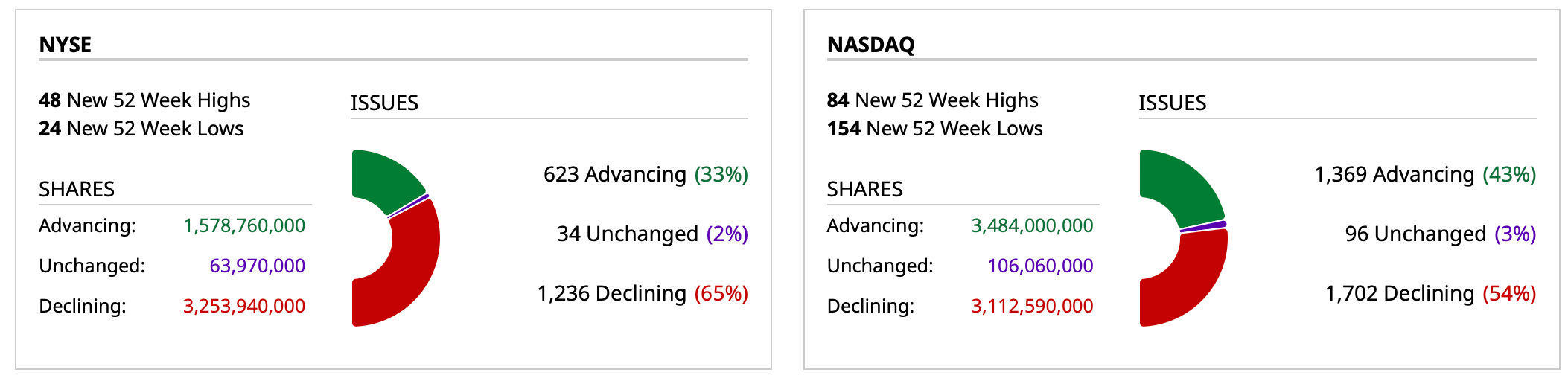

- NYSE volume 3% above its one-month average

- NASDAQ volume trading flat to its one-month average

- VIX index: up 8.62% to 17.90

BY Doug Kass · Dec 17, 2025, 4:35 PM EST

As promised, I am out of my trading long rental in the indices:

* (SPY) $672.43

* (QQQ) $602.24

A push.

BY Doug Kass · Dec 17, 2025, 4:09 PM EST

I am covering half of my Shake Shack (SHAK) short at $81.99.

BY Doug Kass · Dec 17, 2025, 3:58 PM EST

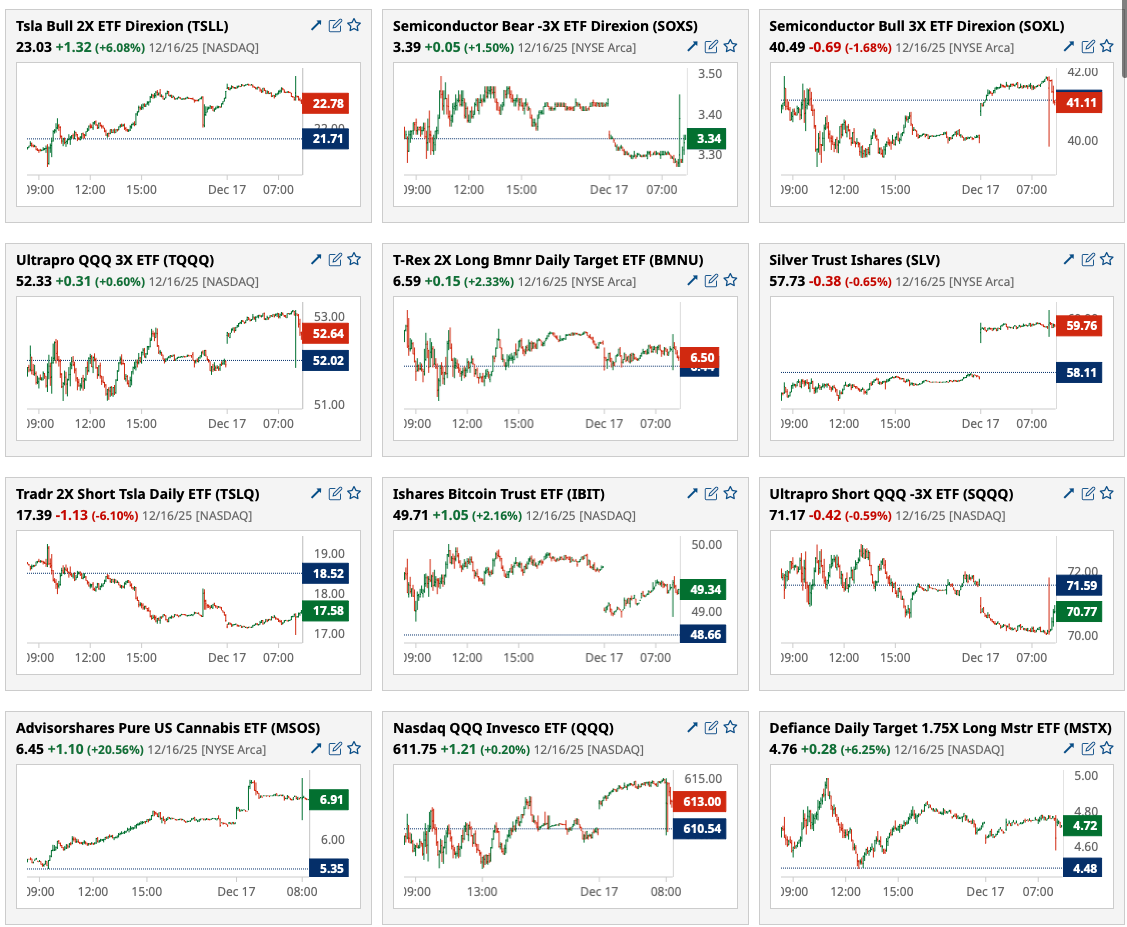

I added to Amazon (AMZN) at $222.09.

BY Doug Kass · Dec 17, 2025, 3:51 PM EST

I shorted more Morgan Stanley (MS) at $178.69 this morning.

I just covered all of my MS short at $174.83.

Similarly I shorted JPMorgan Chase (JPM) at $318.01 this morning.

I just covered all of my JPM short at $315.48.

I now have no bank shorts in my portfolio.

BY Doug Kass · Dec 17, 2025, 3:41 PM EST

I have a research call at 3:30 PM and another one at 4:30 PM.

BY Doug Kass · Dec 17, 2025, 3:36 PM EST

BY Doug Kass · Dec 17, 2025, 3:00 PM EST

I'm covering my (JOET) short now.

BY Doug Kass · Dec 17, 2025, 2:50 PM EST

Housekeeping item.

I covered my small (GRNY) short at $24.38.

BY Doug Kass · Dec 17, 2025, 2:40 PM EST

I took a small trading long rental in (SPY) at $672.52.

I don't expect to be long by the end of the day... maybe sooner!

BY Doug Kass · Dec 17, 2025, 2:34 PM EST

BY Doug Kass · Dec 17, 2025, 1:00 PM EST

BY Doug Kass · Dec 17, 2025, 12:45 PM EST

I covered my CoreWeave (CRWV) (-$3.88) short at $65.65.

I plan to re-short any strength.

BY Doug Kass · Dec 17, 2025, 12:20 PM EST

“You have enemies? Good. That means you've stood up for something, sometime in your life.”

- Winston Churchill

My mantra? The best ideas are hammered out on the anvil of dissent, discourse and debate.

Creative thought cannot be sustained by approval any more than it can be destroyed by criticism.

As for me I want to read EVERYTHING that doesn't agree with me - especially if the analysis is rigorous.

And also, as for me, I have no air of superiority - none whatsoever. I admit that I am often wrong and always in doubt.

From my perch, the inability to consider a contrary view is an investing flaw - a measure of one's hubris.

Feeling superior doesn't make one superior. Hubris does not humble others.

To wit, I received this from Tom Lee's executive assistant on Monday - a request for Tom Lee to be taken off my distribution list:

Good afternoon, Please remove thomas@fundstrat.com, and any other @fundstrat.com related email addresses from subscribing. Thank you

Res ipsa loquitur.

BY Doug Kass · Dec 17, 2025, 12:13 PM EST

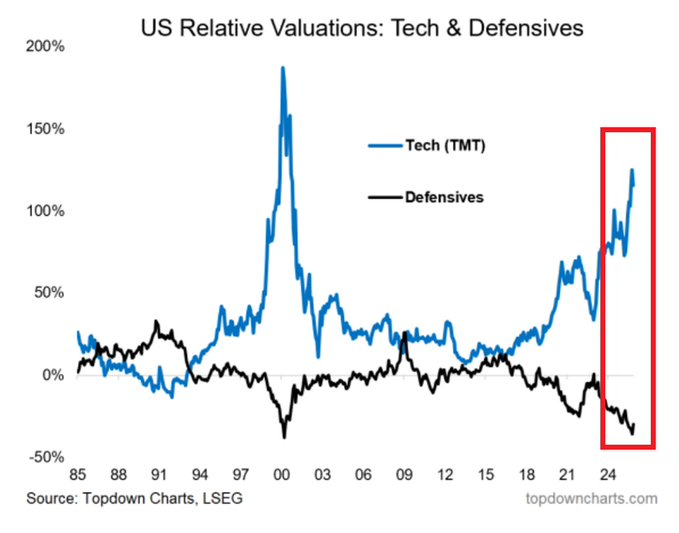

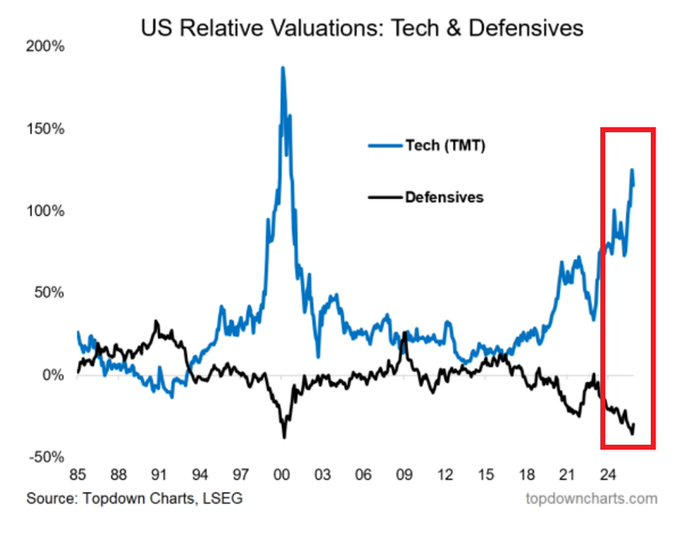

Defensives are the world's fair: (PG) , (PEP) and (KMB) .

From earlier today:

DEC 17, 2025 6:35 AM EST

* Large-cap tech has rarely been as expensive relative to defensive consumer non-durable equities

* I am long PEP, KMB and PG...

Defensive stocks have rarely been so inexpensive:

BY Doug Kass · Dec 17, 2025, 11:50 AM EST

Housekeeping item.

I have covered my Nvidia (NVDA) short at $170.65 (-$7.05 on the day).

I plan to re-short on strength.

BY Doug Kass · Dec 17, 2025, 11:42 AM EST

While it is anticipated that the President will sign an Executive Order on Schedule 3 this week (Thursday, likely) - it is not so easy as most believe.

The President can instruct the Attorney General to act on rescheduling - which is a process.

But he can't just mandate it immediately with an Executive Order.

BY Doug Kass · Dec 17, 2025, 11:25 AM EST

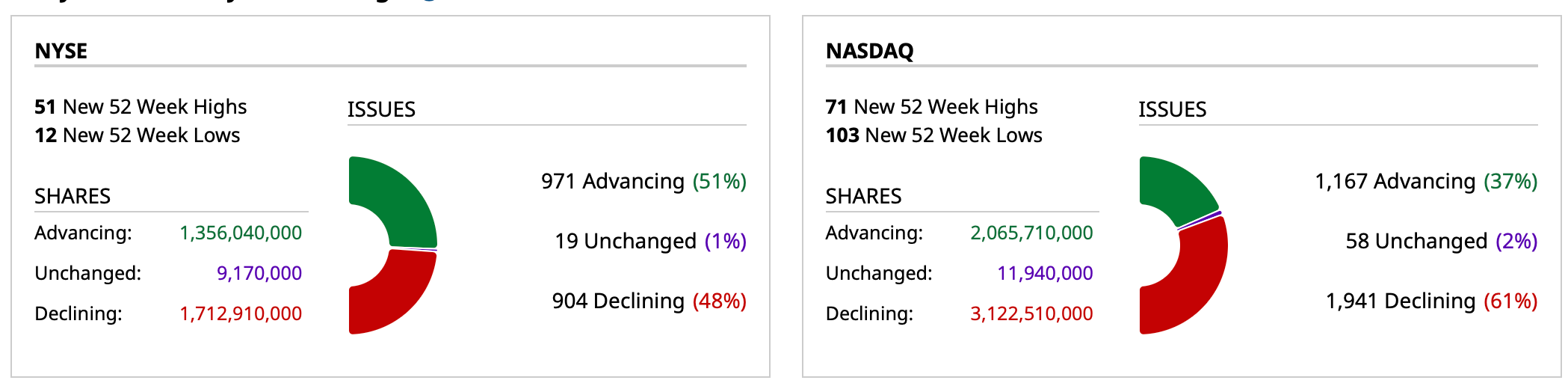

- NYSE volume 1% above its one-month average;

- Nasdaq volume 1% below its one-month average;

- VIX index: down 0.61% to 16.38

BY Doug Kass · Dec 17, 2025, 11:10 AM EST

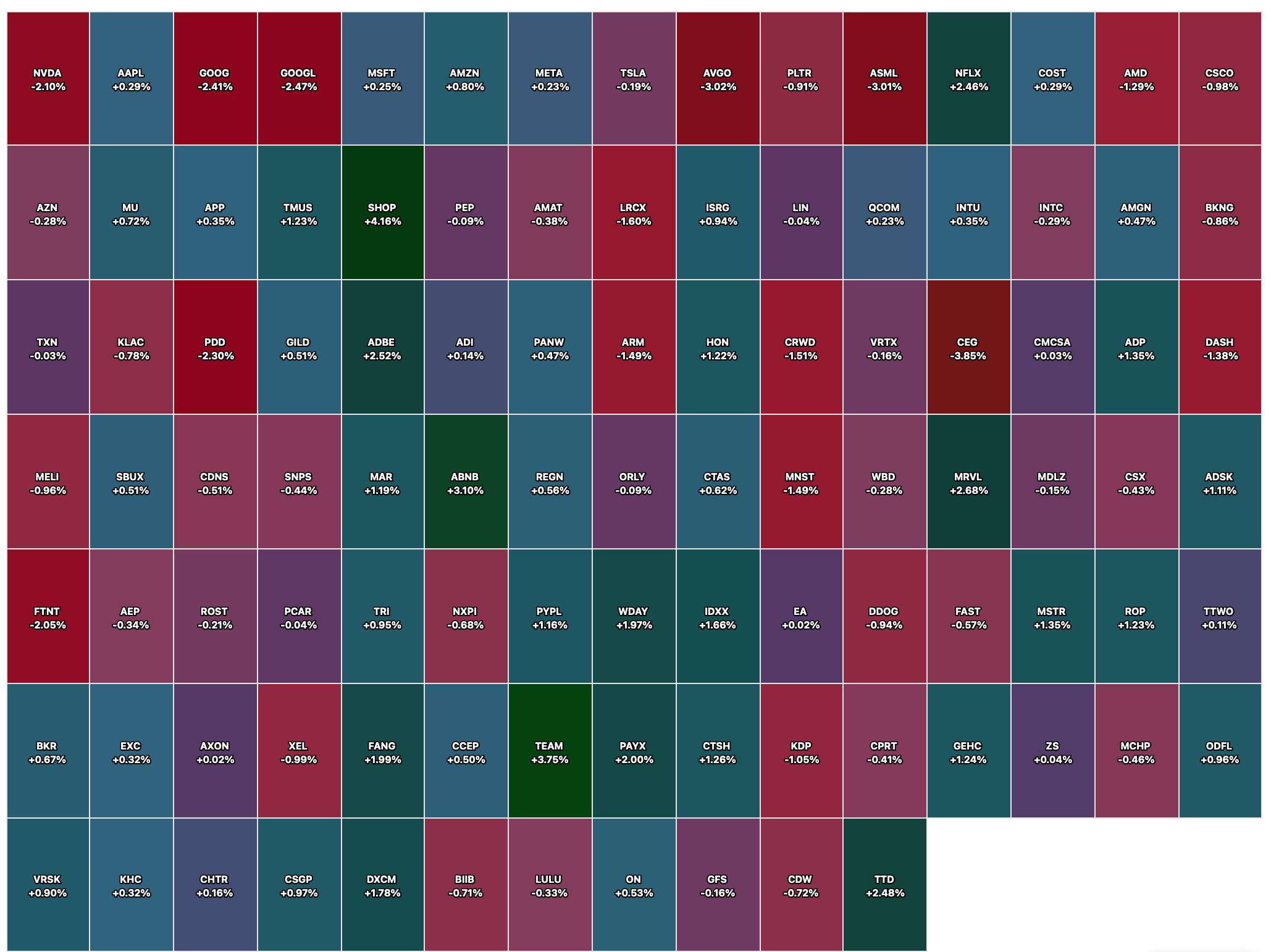

I added to (NVDA) and (CRWV) shorts.

BY Doug Kass · Dec 17, 2025, 10:59 AM EST

This is from QTR’s Fringe Finance:

...and things can unravel faster than expected.

Dec 17, 2025

Blue Owl Capital’s decision this morning to walk away from a $10bn data center deal for Oracle may prove to be an important inflection point in the AI infrastructure boom.Blue Owl isn’t a marginal player or a nervous tourist—it has been one of Oracle’s most significant financial partners, repeatedly stepping in with equity and debt to help fund large-scale data centre projects. When a firm that specializes in financing hyperscale infrastructure decides that a flagship AI project no longer makes sense on its terms, it suggests that the economics of these deals may be becoming harder to justify. In my opinion, this isn’t about headlines or short-term sentiment; it’s about the underlying numbers becoming less forgiving.

For the rest, click here.

BY Doug Kass · Dec 17, 2025, 10:55 AM EST

I am short Zillow.

From my friends at BTIG:

December 17, 2025

Zillow Group, Inc. (ZG) Neutral

GOOG Test of Sponsored For-Sale Listings in Mobile Still Going

--------------------------------------------------------------

### What You Should Know:

A Google (GOOG, Not Rated) test placing for-sale home listings at the top of mobile search results sparked concern last weekend that it could be mounting a challenge to ZG & CoStar's (CSGP, Neutral) Homes.com. The test appeared to run afoul of industry advertising rules & by yesterday nobody we spoke to was able to surface the listings anymore, leading to speculation that the test had been pulled & sparking some relief for ZG. We were able to surface the mobile for-sale listings test in a search conducted this morning, w/listings still including data from the same platform as before along w/sponsored links paid for by brokers. This saga may not be over just yet...While scary, this isn't relevant to near-term estimates & we are not contemplating any related impact to numbers.

BY Doug Kass · Dec 17, 2025, 10:40 AM EST

Added to (PEP) at $149.86.

BY Doug Kass · Dec 17, 2025, 10:19 AM EST

From Peter Boockvar:

Within yesterday’s US December PMI where the services component (again, doesn’t include key sectors like construction and retail) fell to a 6 month low and manufacturing was at a 3 month low, these comments on pricing stood out to me:

“Input cost inflation accelerated markedly in December, hitting the fastest since November 2022. Although manufacturers reported slightly slower inflation, the increase in input prices was historically elevated. In contrast, services cost inflation was the steepest in over three years. Cost increases were mostly blamed on tariffs alongside rising labor costs.”

“Increased costs again fed through to higher selling prices, with the overall rate of inflation rising to the steepest since July and therefore amongst the greatest since the pandemic related price-surge of 2022. Although intensifying competition often restricted the ability of manufacturers to pass on higher costs, resulting in the slowest rate of selling price inflation since January, prices were raised in the service sector to a degree not seen since August 2022.”

While I expect service price inflation to moderate further because of slowing rents, I’m amazed how many people are so sanguine on inflation.

Speaking of inflation, it remains elevated in the UK but the November read came in lower than expected and basically clinches a BoE rate cut tomorrow. Headline CPI was higher by 3.2% y/o/y but down from 3.6% in October and below the estimate of 3.5%. The core rate also was up 3.2% vs 3.4% in the month before and which was also the forecast. Services inflation still remains high at 4.4% vs 4.5% in October. The Office for National Statistics said the drop in the inflation rate of change can be mostly attributed to falls in the price of cakes, biscuits, cereals and confectionery along with tobacco and Black Friday discounts on women’s clothes.

In response, the 2 yr gilt yield is down by 4.6 bps to 3.72% and the 10 yr yield is lower by 3.4 bps to 4.48%. The British pound is lower off a two month high vs the US dollar.

On the flip side with rates, the Japanese 10 yr JGB yield closed at the highest level since July 2006 ahead of Friday’s rate hike and as the market digests the fiscal spending package recently unveiled. I have no idea what is left of the yen carry trade but I will argue that JGB yields are becoming more and more attractive to global investors and particularly Japanese ones that still own a lot of US assets, particularly US Treasuries. Also out of Japan was the 6.1% y/o/y gain in November exports, above the estimate of 5% helped by both volume and price, and with the weaker yen. Semi equipment and medical supplies drove the gain.

Central bank meetings in Asia today resulted in a rate cut by the Bank of Thailand as expected to 1.25% and a rate hold from Bank Indonesia at 4.75%, also the consensus. The Bank of Thailand said this supporting the cut, and which was also in response to a strong currency of theirs which they want to weaken, “Given apparent economic slowdown as well as heightened risks, monetary policy can be more accommodative to ensure that financial conditions support economic recovery and alleviate debt burden of vulnerable groups.” As for the possibility of another cut, the Assistant Governor said “we are quite neutral now.”

10 yr JGB Yield

With respect to the very interest rate sensitive US construction industry, the November Architecture Billings Index fell to 45.3 in November from 47.6 in October, thus remaining below 50. The chief economist there said “Weakness in business conditions at architecture firms continues to be widespread, with declining billings across all major specializations and in every region except the Midwest. However, inquiries for new projects continued to increase, and design activity at firms in the Midwest - a region that traditionally has had a disproportionate share of manufacturing activity - appears to have hit its bottom for this cycle and is expected to continue to improve.”

On the transportation side of the US economy, the November Cass Freight shipments index was out yesterday and saw a 2.7% m/o/m increase seasonally adjusted after a 2.1% drop in October. Versus last year they are still down 7.6%, “putting the index on track for a 6% decline in 2025” said Cass.

They also said, “After truckload volumes briefly improved in Q3 ahead of the October 5 import tariff deadline, they have softened again so far in Q4 as pre-tariff stocks are drawn down. Resilient early holiday consumer spending data suggest some pent-up demand could be building, but tariffs are likely to continue to press prices higher and affordability lower in 2026.”

Ahead of Lennar’s earnings call, the stock is trading down pre-market after missing delivery numbers and bottom line estimates as discounting continues. They said this of note in their earnings release:

“Even as interest rates moved slightly lower in our fourth quarter, the overall market remained challenged. Accordingly, our fourth quarter and full year 2025 results reflect a disciplined commitment to increasing housing supply in a market constrained by affordability challenges, as well as weak consumer confidence.”

“To address continued market declines, we maintained approximately 14% in incentives and price adjustments, while continuing to focus on volume...We continued to utilize incentives, including mortgage rate buydowns, to sustain sales momentum.”

“Even as market conditions softened, we prioritized providing supply for a healthier housing market, while driving down costs to support affordability.”

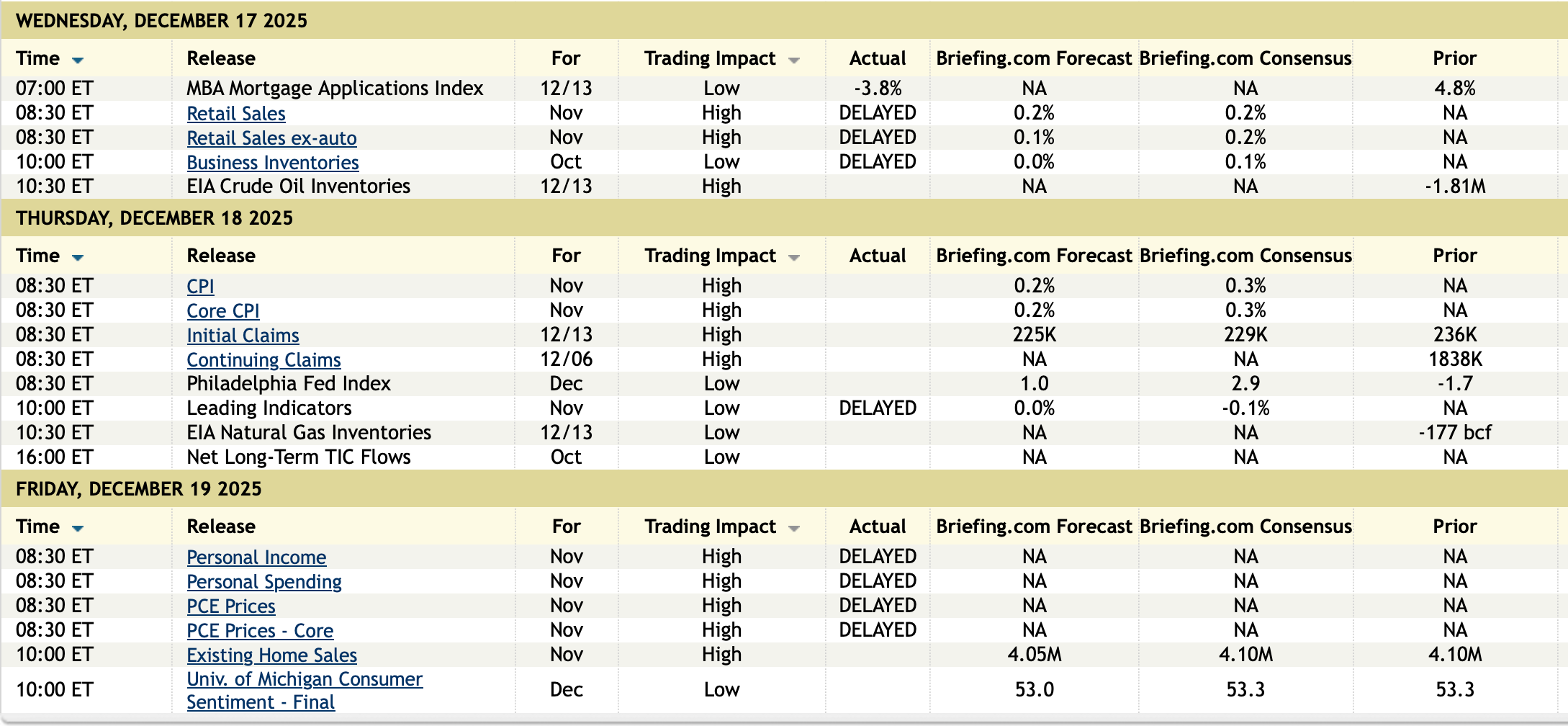

Mortgage applications for the week ended 12/12 fell w/o/w with purchases down for a 2nd week by 2.8% while refi’s dropped by 3.6% after a jump of 14% last week.

Back to Europe, the December German IFO business confidence index fell a touch to 87.6 from 88 and below the estimate of 88.2. The Current Assessment was unchanged at 85.6 but the Expectations component fell slightly to 89.7 from 90.5 and vs the forecast of no change. The IFO said succinctly, “The year is ending without any sense of optimism.” As we look to 2026 we know German industry is still dealing with high energy costs relative to its global competitors and China is directly threatening their auto industry with its great cars at affordable prices.

The December UK CBI industrial orders index remained deeply negative but less so at -32 vs -37 in November and vs the estimate of -35. The CBI said “Manufacturing output is still falling, but the pace of decline has eased. Activity was clearly held back by uncertainty ahead of the Budget, and with that now out of the way firms can look to 2026 with a little more certainty.”

“Significant headwinds remain nonetheless, with demand still soft, high energy, labor and regulatory costs squeezing margins, and uncertainty around key policies and global conditions continuing to weigh on confidence.”

They also gave some advice to the UK government which certainly is under a lot of scrutiny after doing little but raise the cost of doing business over the past year. “To build momentum through 2026, the government must take action to lower the cost of doing business. This includes expediting and broadening support to tackle punitive industrial energy costs, collaborating to agree to balanced solutions on the Employment Rights Bill through secondary legislation, and overhauling regulatory barriers to unlock investment and innovation.”

BY Doug Kass · Dec 17, 2025, 10:00 AM EST

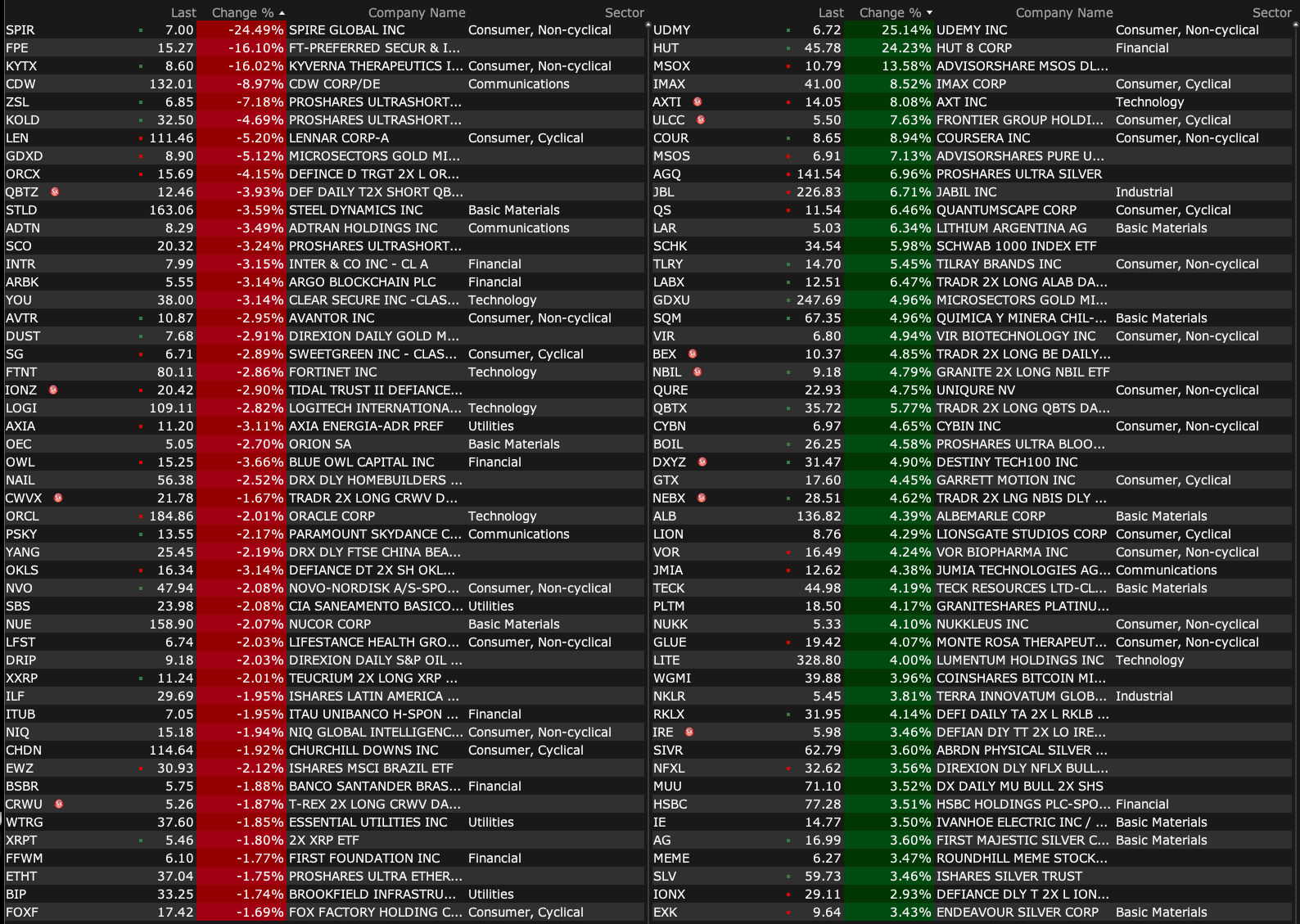

Covered cannabis shorts:

* (MSOS) $6.89

* MSOX $10.85

BY Doug Kass · Dec 17, 2025, 9:51 AM EST

With stocks reversing the premarket gains, I have taken a quick and small profit in trading short rental in the indexes from this morning:

* (SPY) $678.38

* (QQQ) $610.37.

From very early this morning:

Adding to my index shorts (5:55 AM):

* (SPY) $681.41

* (QQQ) $614.60

Position: Short SPY common (VS), QQQ common (VS)

By Doug KassDec 17, 2025 6:05 AM EST

BY Doug Kass · Dec 17, 2025, 9:49 AM EST

Knowledge@Wharton on Decoding AI. Decoding the AI Bubble: Tulips, Dot-Coms, or Something Else? - Knowledge at Wharton

BY Doug Kass · Dec 17, 2025, 9:45 AM EST

I shorted (MSOS) $7.32 and AdvisorShares MSOS Daily Leveraged ETF (MSOX) $11.80 in premarket trading.

I plan to cover these early this morning = win, lose or draw.

BY Doug Kass · Dec 17, 2025, 9:37 AM EST

I have long been of the view that Coreweave (CRWV) is a short, here is JustDario's view:

BY Doug Kass · Dec 17, 2025, 9:30 AM EST

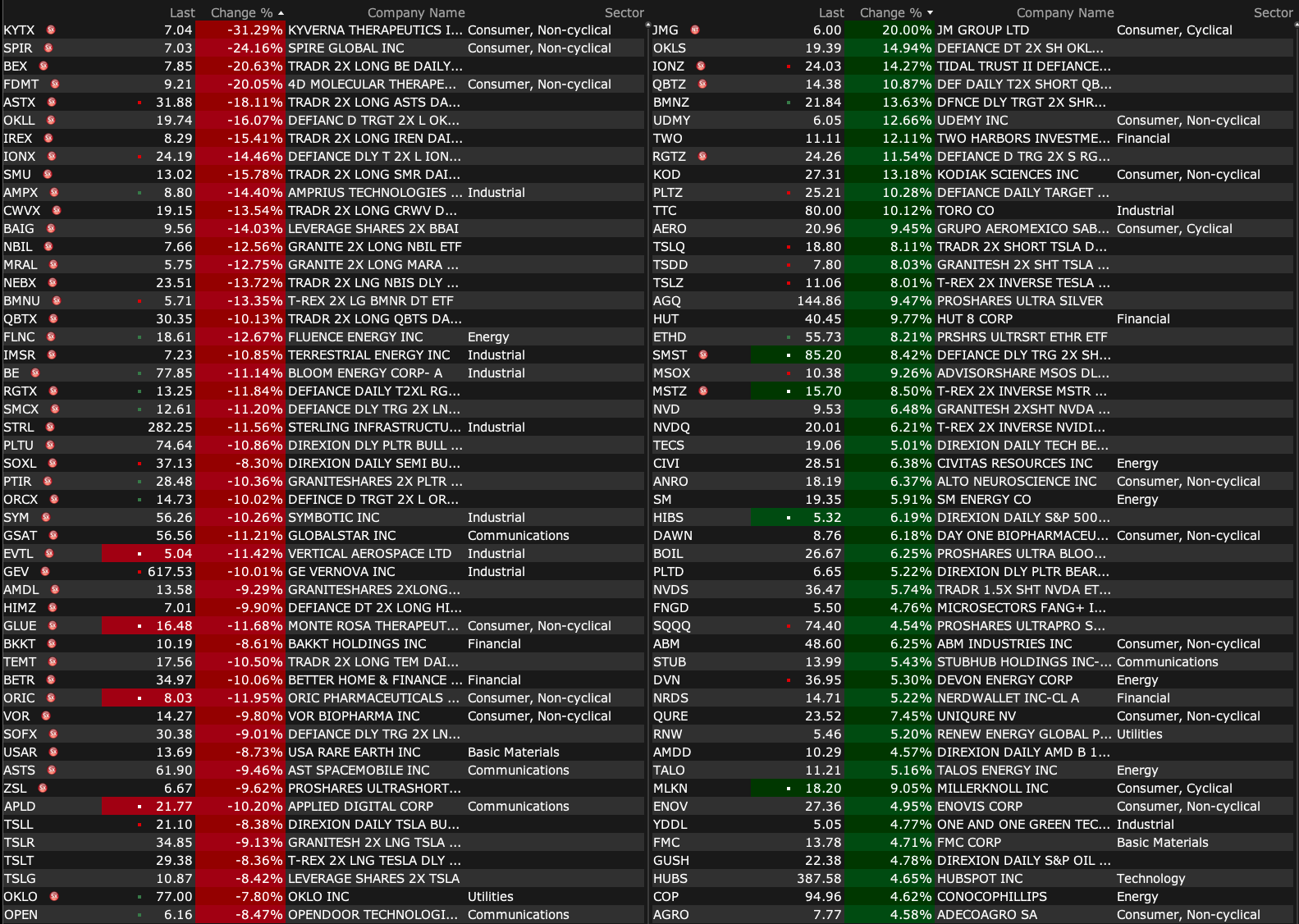

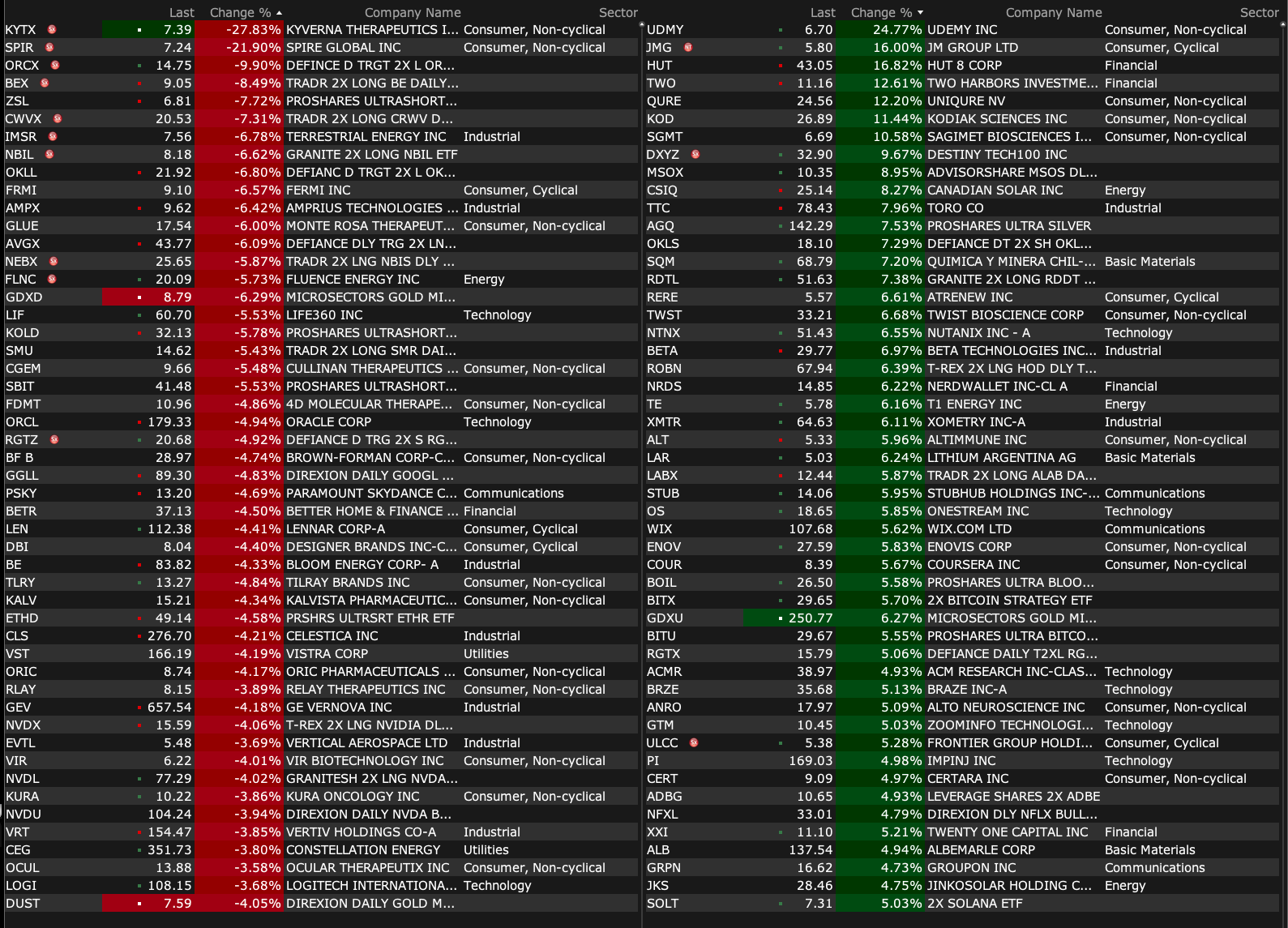

-MBRX +27% (announces Positive Results from Phase 1 Clinical Trial Evaluating WP1066 for treatment of Pediatric Recurrent Malignant Brain Tumors)

-UDMY +25% (Coursera to combine with Udemy in $2.5B all-stock deal; Udemy stockholders will receive 0.800 shares of Coursera common stock)

-VERU +11% (earnings, color)

-COUR +9.5% (Coursera to combine with Udemy in $2.5B all-stock deal; Udemy stockholders will receive 0.800 shares of Coursera common stock)

-TWO +9.0% (UWM acquires Two Harbors in all-stock deal)

-JBL +7.0% (earnings, guidance)

-ULCC +6.9% (reportedly Spirit Airlines considering merger with Frontier amid ongoing restructuring)

-NTZ +4.4% (earnings)

-VSCO +2.5% (Telsey Advisory Group Raised VSCO to Outperform from Market Perform, price target: $66)

-CRDO +2.4% (bounce off recent weakness)

-URBN +2.0% (Telsey Advisory Group Raised URBN to Outperform from Market Perform, price target: $98)

-PLCE -34% (earnings)

-SPIR -24% (earnings, guidance)

-WOR -9.1% (earnings)

-LEN -5.0% (earnings, guidance)

-OWL -3.4% (reportedly Oracle’s $10B Michigan data centre in limbo after Blue Owl funding talks stall)

-NUE -2.6% (guidance)

-UWMC -2.6% (UWM acquires Two Harbors in all-stock deal)

-PSKY -2.2% (WBD Board of Directors Unanimously Recommends Shareholders Reject Paramount Tender Offer)

BY Doug Kass · Dec 17, 2025, 9:22 AM EST

BY Doug Kass · Dec 17, 2025, 9:15 AM EST

BY Doug Kass · Dec 17, 2025, 9:10 AM EST

I thought these passages were important in Peter Boockvar's missive this morning:

Within yesterday’s US December PMI where the services component (again, doesn’t include key sectors like construction and retail) fell to a 6 month low and manufacturing was at a 3 month low, these comments on pricing stood out to me:

“Input cost inflation accelerated markedly in December, hitting the fastest since November 2022. Although manufacturers reported slightly slower inflation, the increase in input prices was historically elevated. In contrast, services cost inflation was the steepest in over three years. Cost increases were mostly blamed on tariffs alongside rising labor costs.”

“Increased costs again fed through to higher selling prices, with the overall rate of inflation rising to the steepest since July and therefore amongst the greatest since the pandemic related price-surge of 2022. Although intensifying competition often restricted the ability of manufacturers to pass on higher costs, resulting in the slowest rate of selling price inflation since January, prices were raised in the service sector to a degree not seen since August 2022.”

While I expect service price inflation to moderate further because of slowing rents, I’m amazed how many people are so sanguine on inflation.

BY Doug Kass · Dec 17, 2025, 9:00 AM EST

11 a.m.: Treasury buyback (liquidity support);

11 a.m.: Treasury hosts a $69B 17-Week Bill Auction;

1 p.m.: Treasury hosts $13B a 20-Year Bond Auction;

2 p.m. : Treasury buyback (liquidity support)

8:15 a.m.: Fed Board Governor Waller (Voter) speaks on the economic outlook before the Yale University CEO Summit, NYC (No text. Q&A from moderator and audience. Livestream at www.cnbc.com/);

9:05 a.m.: Fed Bank of New York President Williams (Voter) gives opening remarks before the 2025 FX (Foreign Exchange) Market Structure Conference hosted by the Federal Reserve Bank of New York, NYC (Livestream available. Text and Q&A are not expected);

9:15 a.m.: New York Federal Reserve Bank Head of Markets Group Anna Nordstrom speaks at FX Market Structure Conference;

12:30 p.m.: Fed Bank of Atlanta President Bostic (Non-Voter) participates in discussion on the economic outlook before the Gwinnett County Chamber of Commerce, Duluth, GA (Audience Q&A expected. No media Q&A. No embargoed text. Livestream here.)

BY Doug Kass · Dec 17, 2025, 8:50 AM EST

Equities getting hit a bit on a data center delay.

Blue Owl has been in discussions with lenders and Oracle (ORCL) about investing in a data center being built to serve OpenAI in Saline Township, Michigan. Apparently the agreement will not go forward after negotiations stalled.

BY Doug Kass · Dec 17, 2025, 8:28 AM EST

* This is only the third time this has happened in the last 75 years — the last two times ended very poorly for stocks

* I call B.S. to the "stocks are climbing a wall of worry" argument

"A time to be born, a time to die

A time to plant, a time to reap

A time to kill, a time to heal

A time to laugh, a time to weep

To everything, turn, turn, turn

There is a season, turn, turn, turn

And a time to every purpose, under heaven

A time to build up, a time to break down

A time to dance, a time to mourn

A time to cast away stones

A time to gather stones together"

- The Byrds, Turn Turn Turn

"To everything there is a season, and a time for every purpose under heaven" is a Biblical quote that speaks to life's cycles, acknowledging that different experiences — joy, sorrow, war, peace, birth, death — have their designated time, and that all human events occur in a divinely ordained pattern.

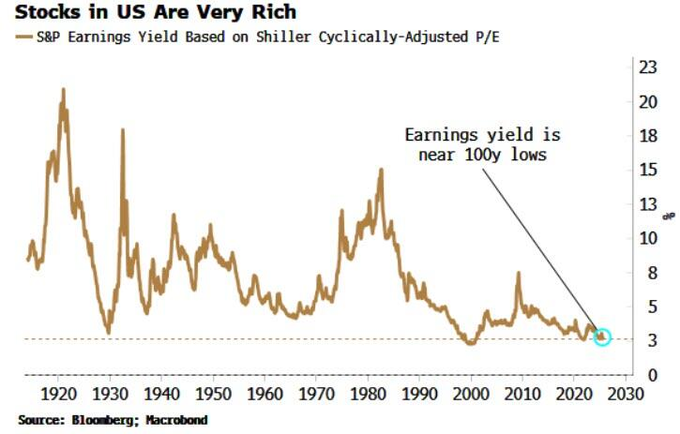

I recognize fully that buying equities creates wealth (

I have argued that today's valuations (which are in the 96%-tile), the S&P earnings yield (Shiller ratio) near a 100-year low (see graph below) and the equity risk premium turning into an equity risk discount (!!!!!) are all poor launching pads for future investment returns and that now is a time to be concerned with return of capital rather than return on capital:

Market observers (Wall of worry? Markets are climbing it anyway | J.P. Morgan Private Bank EMEA) like Tom Lee are fond of saying that investor pessimism is high and that the market is climbing a wall of worry. From Tom Lee on climbing that wall!

Like the misleading "cash on the sidelines" argument, "stocks climbing the wall of worry" is another false and fatuous narrative.

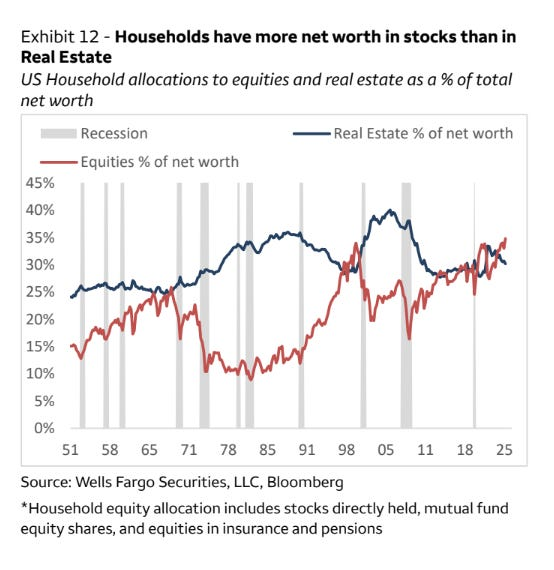

To me, Tom and others couldn't be more wrong as the wealth of U.S. households has never been more concentrated in equities. This is not "climbing a wall of worry." It represents a degree of market exuberance rarely seen in history.

In fact, for only the third time in the last three quarters of a century household's equity investments (as a percentage of net worth) exceeds their investment in real estate (i.e. principally their homes).

The last two times this occurred was in the late 1960s and in the late 1990s (at the end of the dot-com bubble) when long-lasting and brutal bear markets ensued:

"To everything, turn, turn, turn

There is a season, turn, turn, turn

And a time to every purpose under heaven"

BY Doug Kass · Dec 17, 2025, 7:30 AM EST

Bonus — Here are some great links:

Thirty Stocks. Thirty Stories. One Index.

The Growth Forecast Was Hidden

BY Doug Kass · Dec 17, 2025, 7:15 AM EST

BY Doug Kass · Dec 17, 2025, 6:55 AM EST

Citi raises the price target on PepsiCo (PEP) from $165 to $170.

BY Doug Kass · Dec 17, 2025, 6:45 AM EST

* Large-cap tech has rarely been as expensive relative to defensive consumer non-durable equities

* I am long PEP, KMB and PG...

Defensive stocks have rarely been so inexpensive:

BY Doug Kass · Dec 17, 2025, 6:35 AM EST

BY Doug Kass · Dec 17, 2025, 6:20 AM EST

Adding to my index shorts (5:55 AM):

* (SPY) $681.41

* (QQQ) $614.60

BY Doug Kass · Dec 17, 2025, 6:05 AM EST

Wolf Street howls about housing price changes around the country.

BY Doug Kass · Dec 17, 2025, 5:55 AM EST

The S&P Short Range Oscillator remains overbought at 1.82% vs. 2.11%.

BY Doug Kass · Dec 17, 2025, 5:45 AM EST

I've never met a rich client who's made money as a bear. Zero. - @fundstrat

Join us on spaces at the top of the hour to talk charts and more! x.com/i/spaces/1nAKE…