Tuesday's Closing Breadth, Sectors & Heat Map

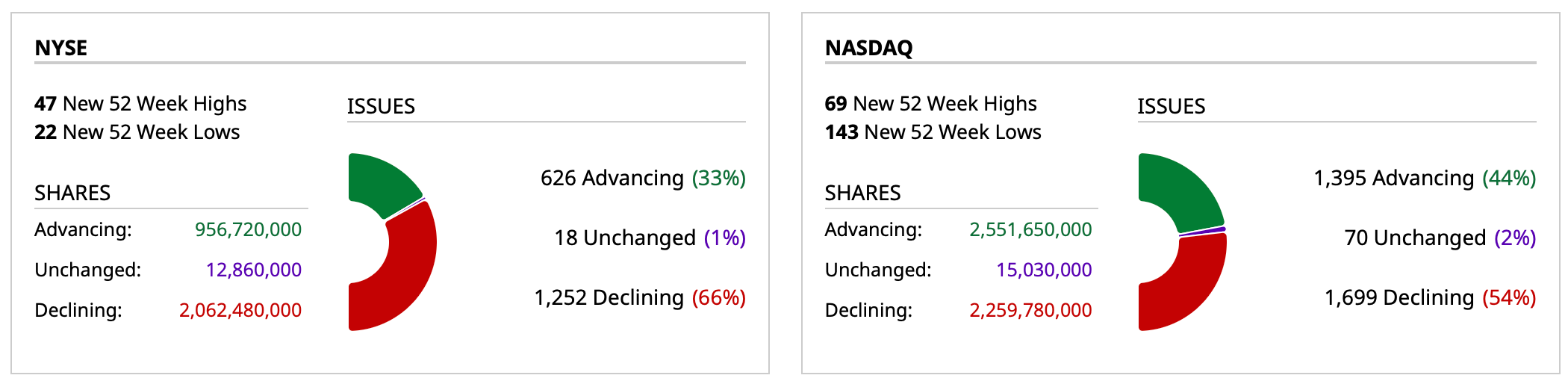

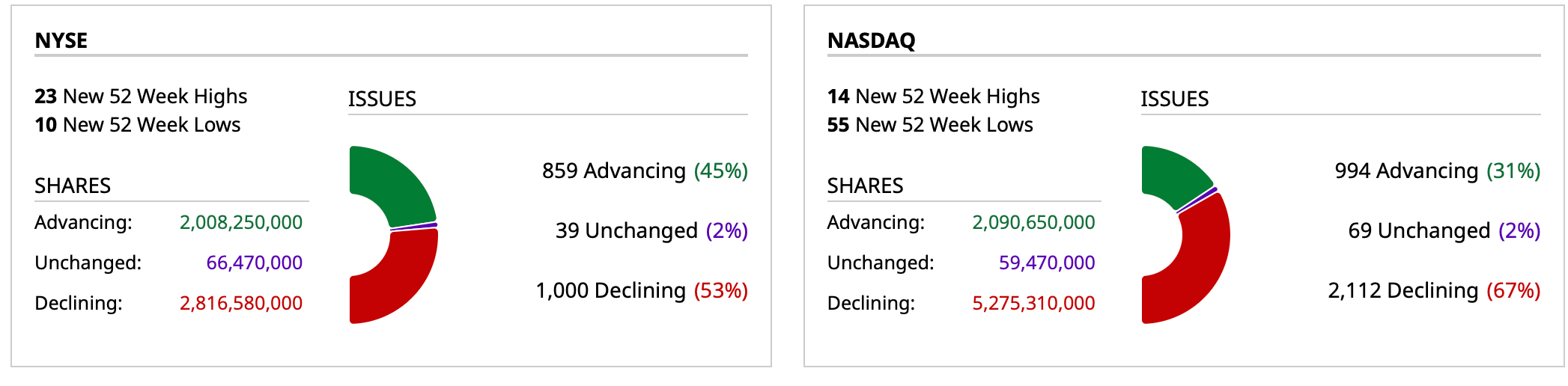

Closing Breadth

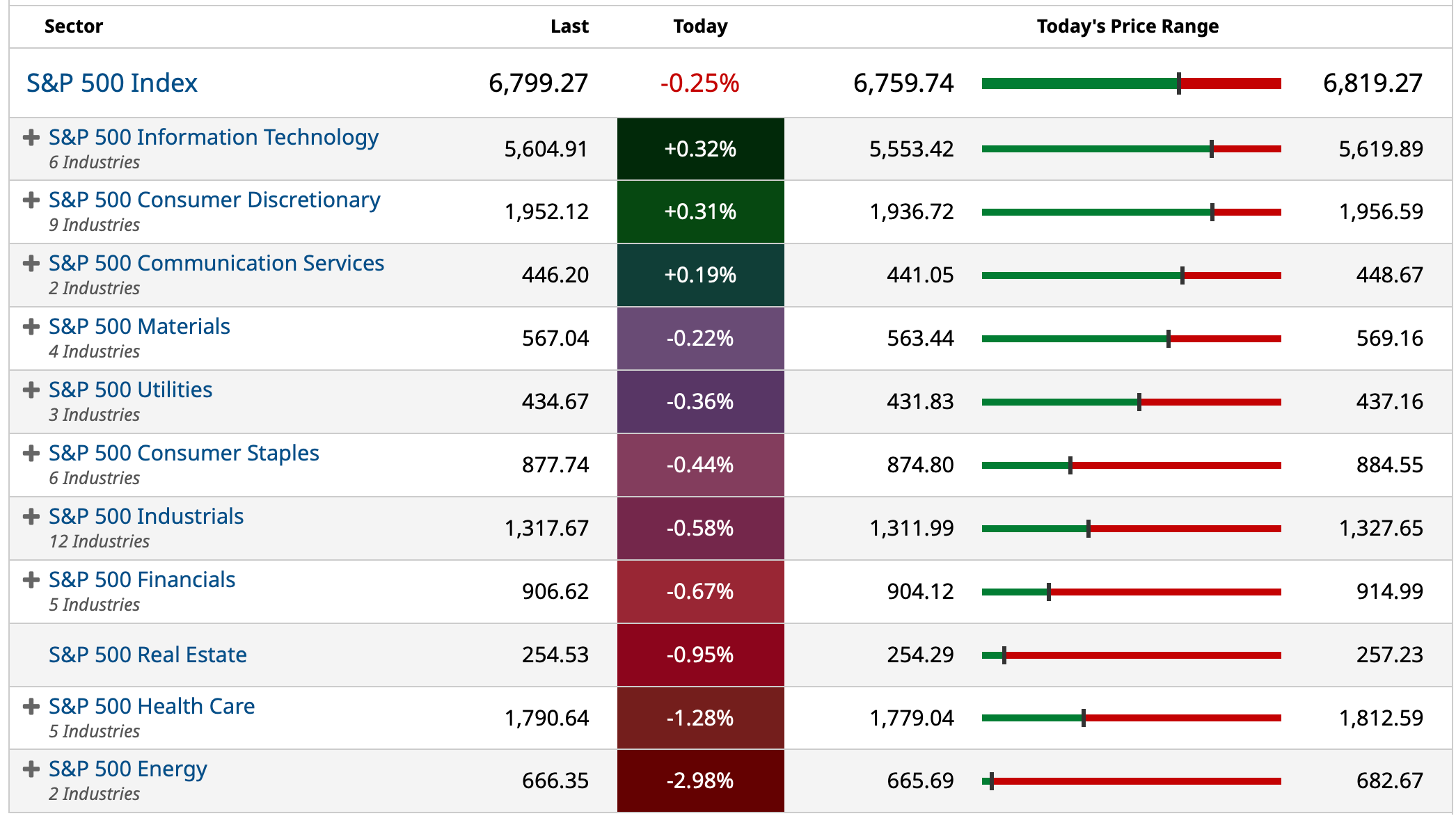

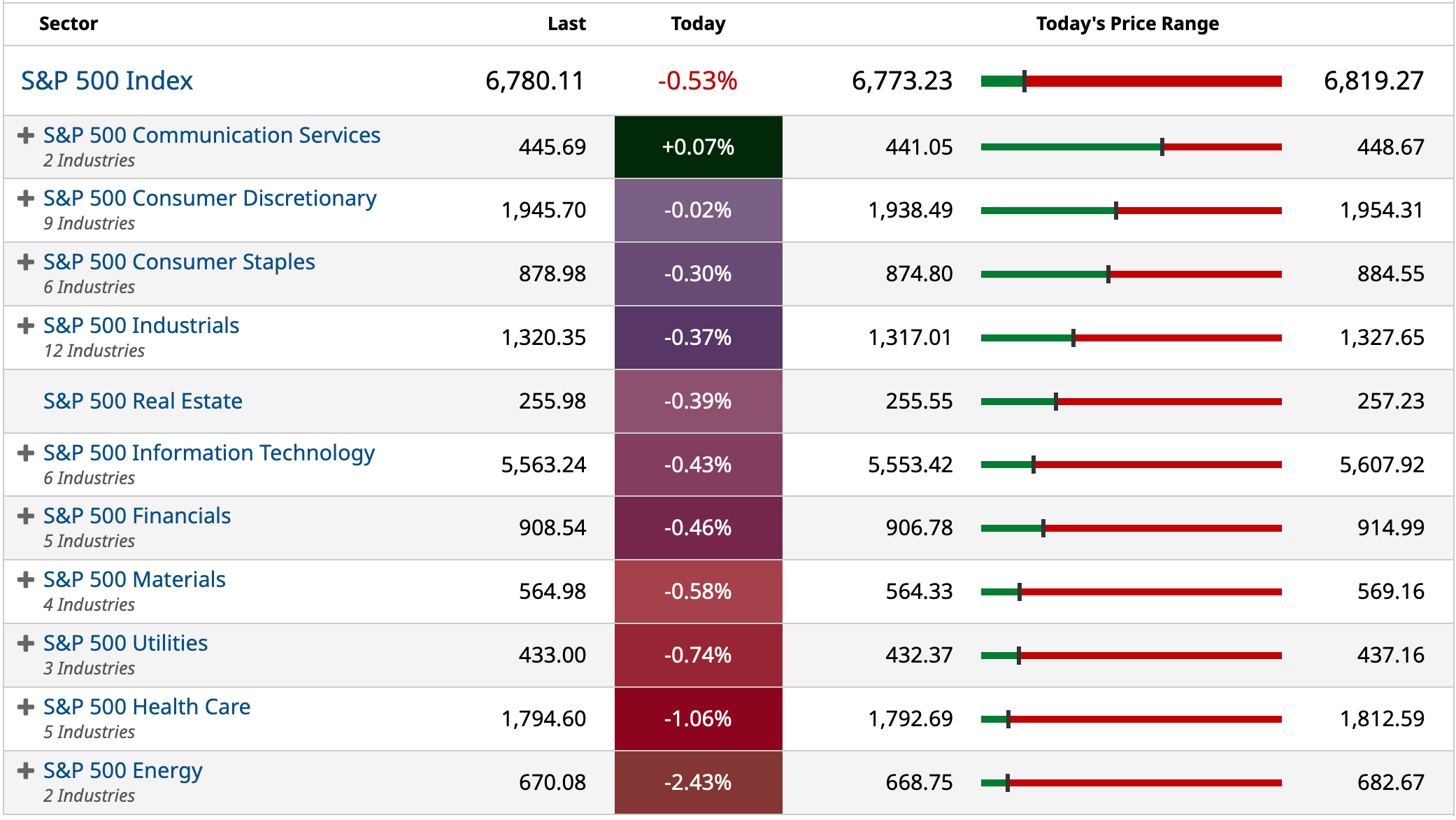

Sectors

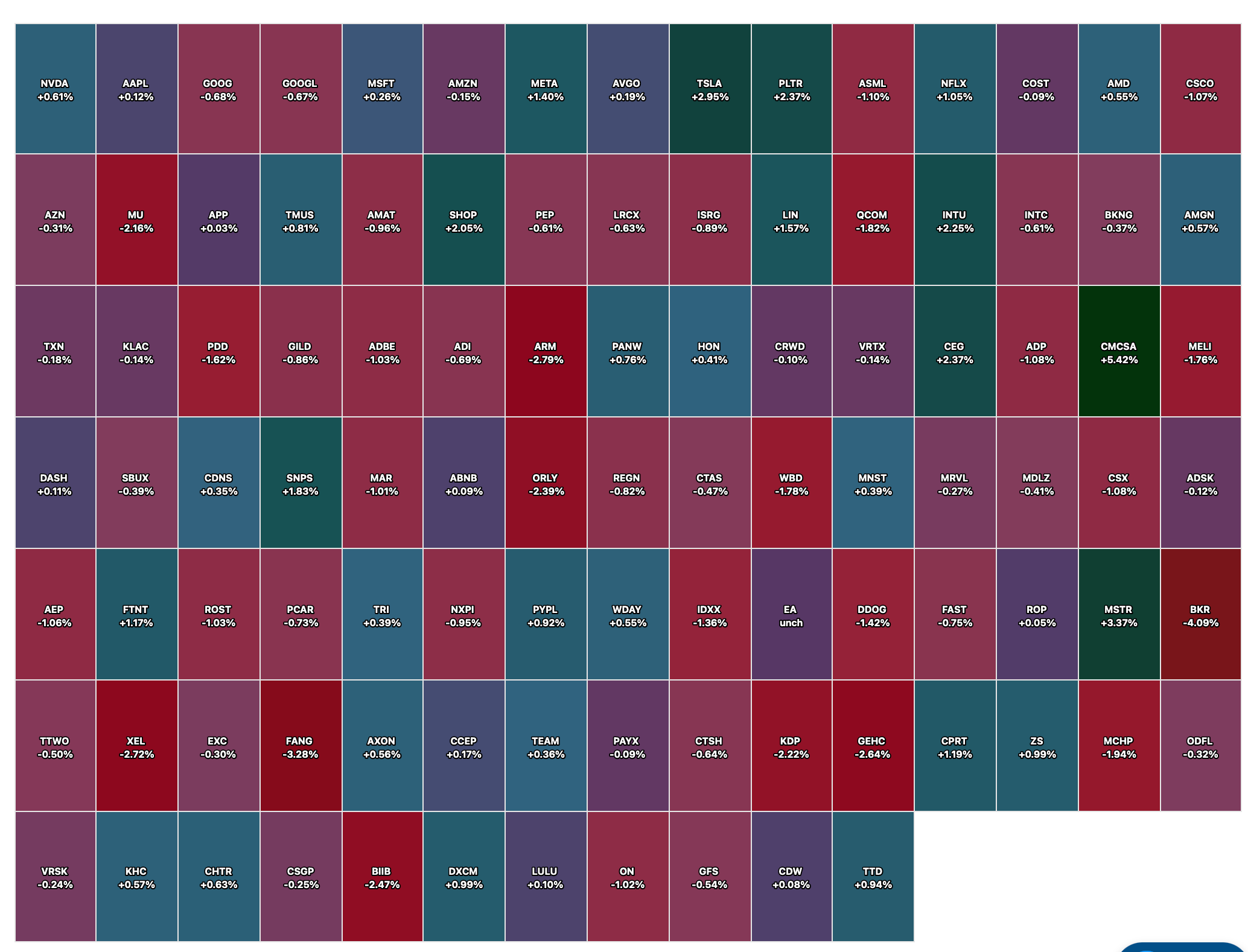

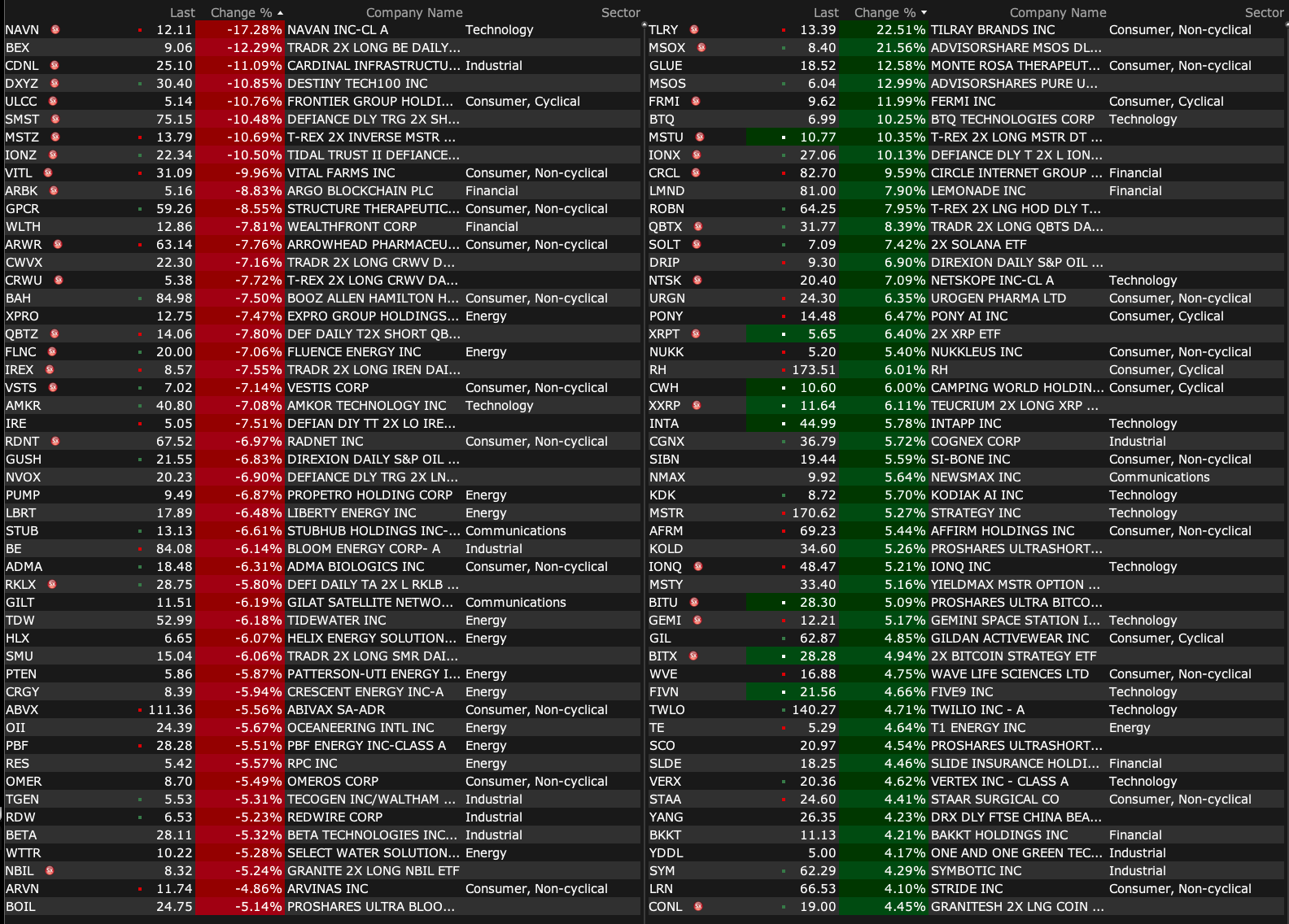

Nasdaq 100 Heat Map

BY Doug Kass · Dec 16, 2025, 4:20 PM EST

BY Doug Kass · Dec 16, 2025, 4:20 PM EST

Weak close.

Glad I re-shorted.

Thanks for reading my Diary. I hope my output was useful.

Enjoy the evening.

Be safe.

BY Doug Kass · Dec 16, 2025, 4:06 PM EST

With S&P cash -15 handles, I am re-shorting the indices and shorting calls:

* (SPY) $679.22

* (QQQ) $611.81

BY Doug Kass · Dec 16, 2025, 3:31 PM EST

An excellent short and simple summary:

BY Doug Kass · Dec 16, 2025, 2:50 PM EST

BY Doug Kass · Dec 16, 2025, 2:35 PM EST

BY Doug Kass · Dec 16, 2025, 2:18 PM EST

No trades since this morning.

BY Doug Kass · Dec 16, 2025, 1:43 PM EST

- NYSE volume 3% below its one-month average

- NASDAQ volume 11% below its one-month average

- VIX index: up 1.94% to 16.82

BY Doug Kass · Dec 16, 2025, 11:45 AM EST

(RACE) is getting jiggy and (PEP) keeps on truckin'.

BY Doug Kass · Dec 16, 2025, 11:34 AM EST

Today's intraday volatility is something else!

I normally consider myself an opportunistic trader who can take advantage of said volatility.

But, Jeez Louise, this is one wild day.

Sitting on my hands.

BY Doug Kass · Dec 16, 2025, 11:14 AM EST

From Peter Boockvar:

Thank you health, social assistance hiring as unemployment rate rises to highest since Sept '21

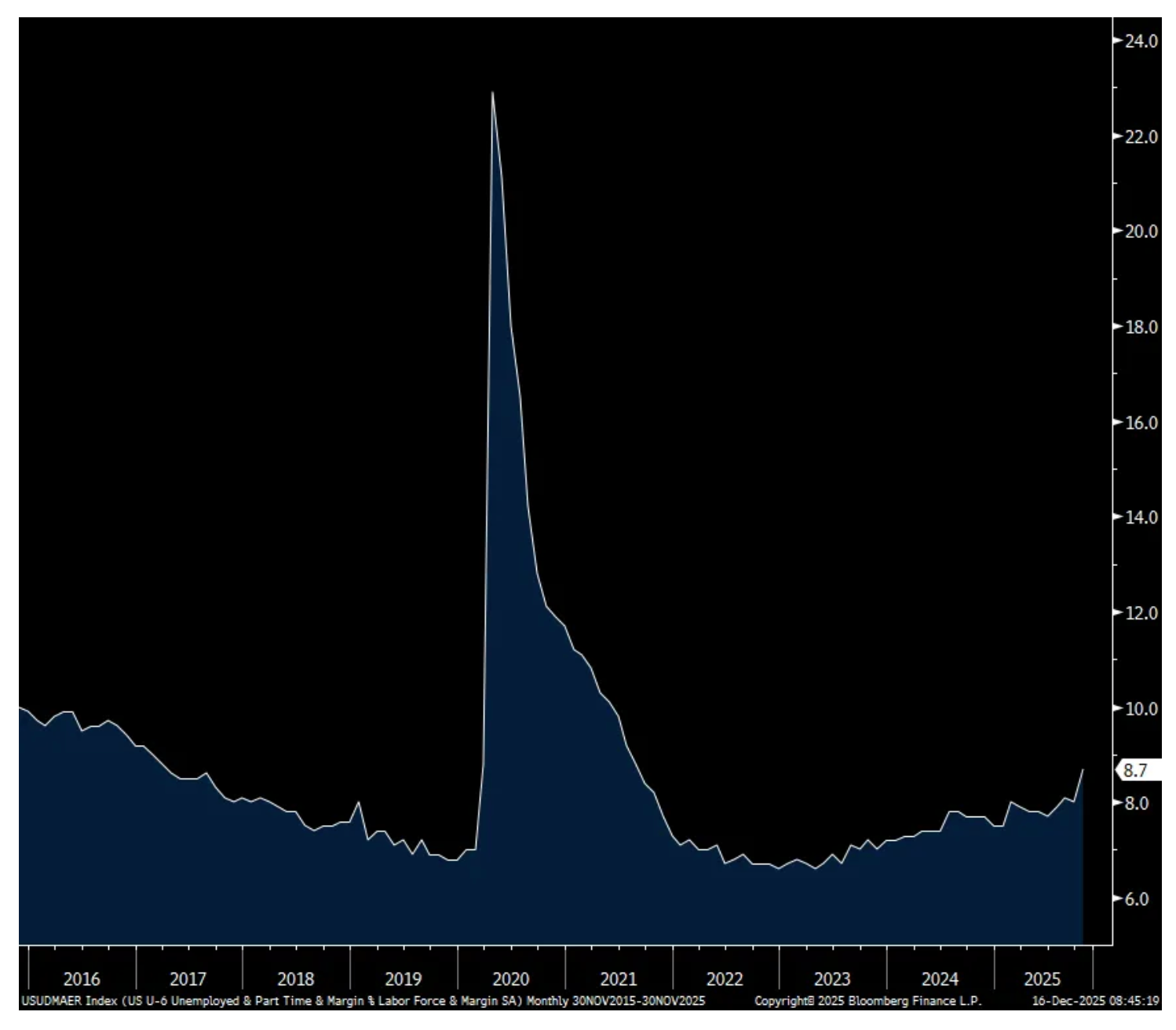

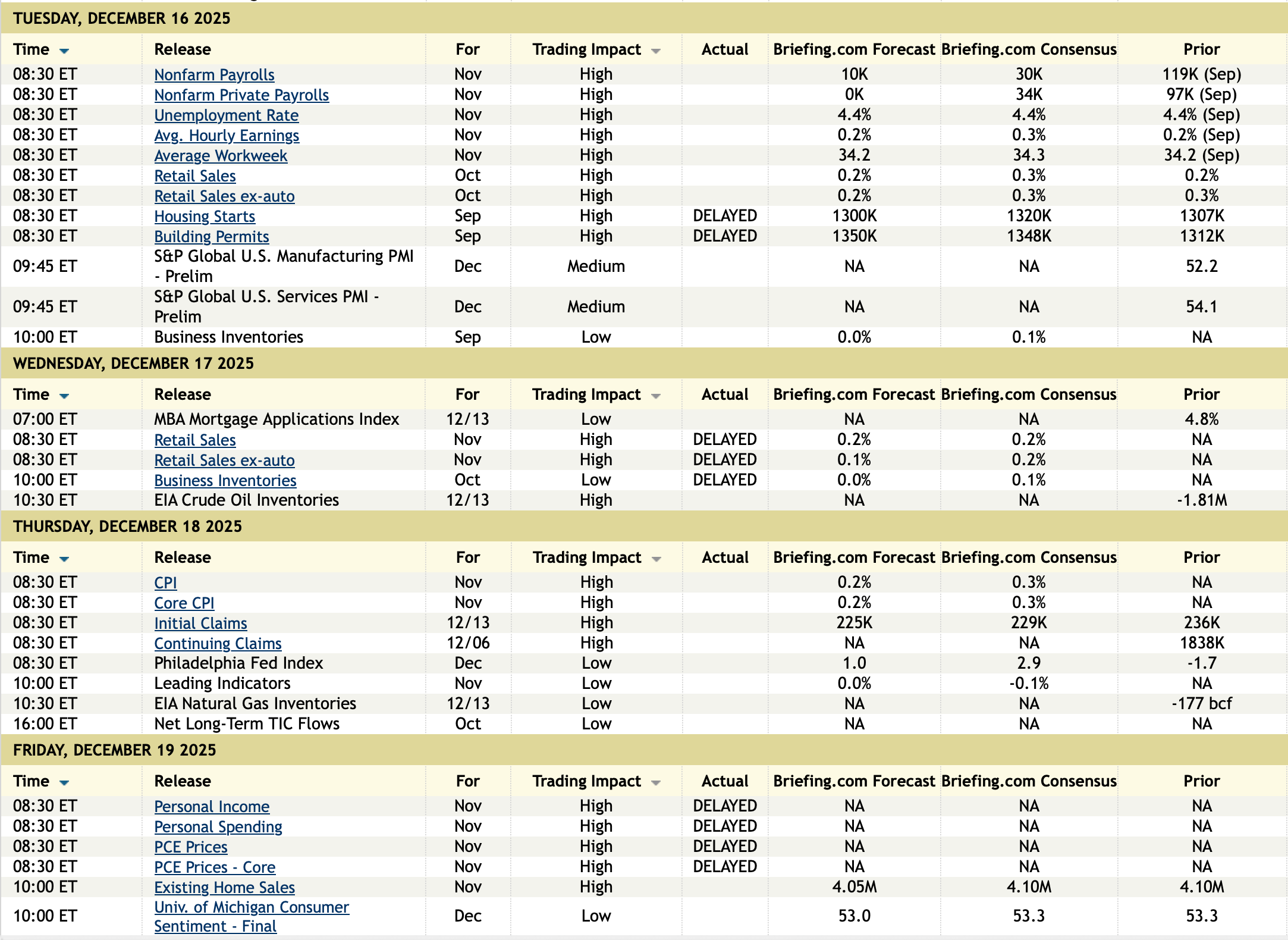

November payrolls grew by 64k, above the estimate of 45k but after falling by 105k in October (government shutdown of course the main factor). September was up 108k vs the initial print of 119k. The shutdown by the way cut government jobs by 157k in October. The household survey showed a gain of 96k from September but because it trailed the 323k increase in the size of the labor force, the unemployment rose to 4.6% from 4.4% in September, the highest since September 2021. Of particular note, the all in U6 rate jumped to 8.7% from 8% in September and that is the highest since August 2021 and March 2017 before that not including Covid.

Smoothing out the noise and separating out the government shutdown, though private contractors were impacted, private sector payrolls have averaged 75k over the past three months vs 44k over the past six months and 88k over the past 12.

The services sector added 50k but again most of the job growth is led by health/social assistance which contributed 64k jobs. Job losses were seen in leisure/hospitality, temporary help, financial services, information, transportation/warehouse, and wholesale trade. Retail hired a net 6k and jobs were added in professional business services of 12k.

On the goods side, manufacturing shed 5k, down for a 3rd month while construction hiring jumped by 28k with I’m sure help with the building of data centers.

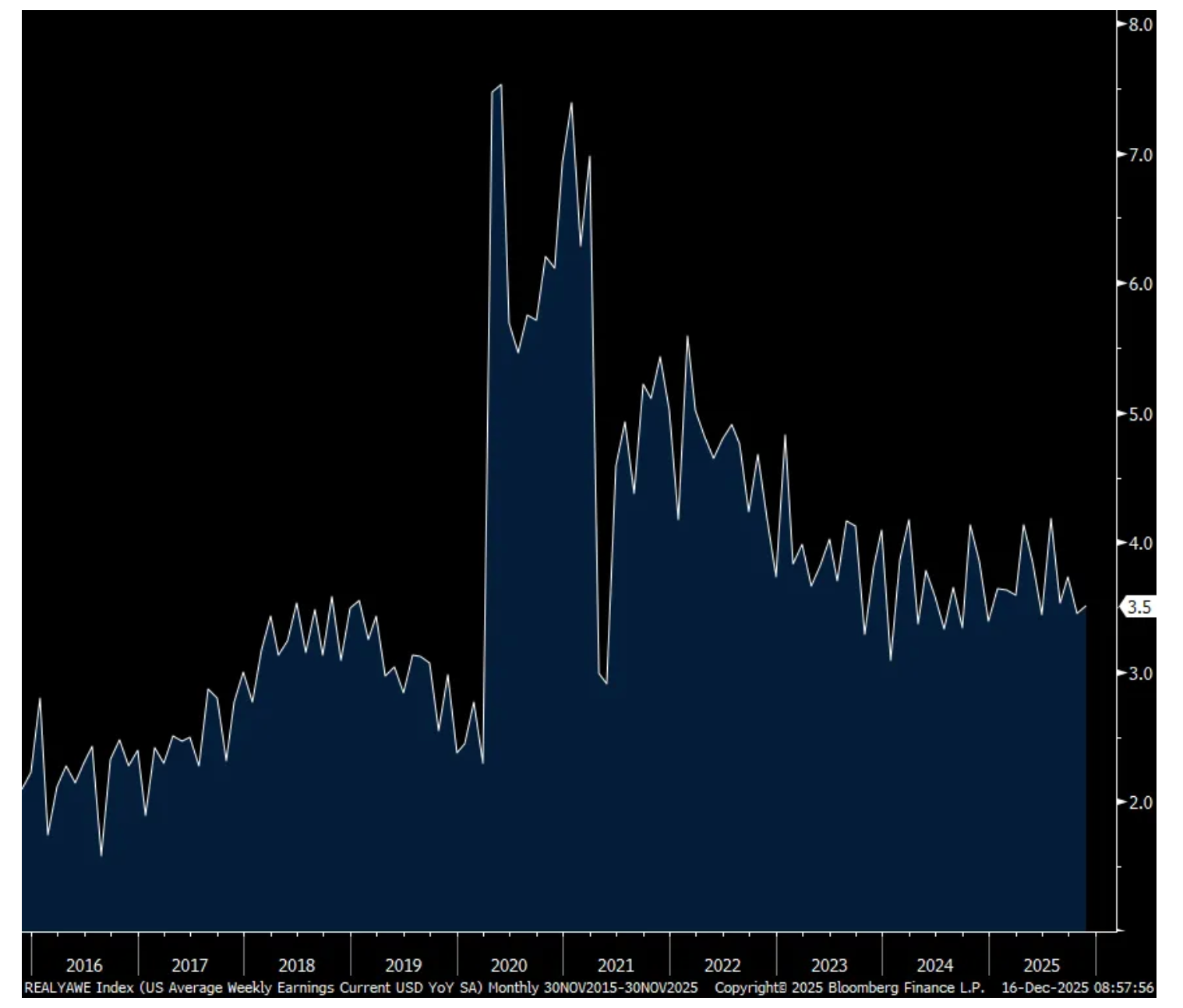

Average hourly earnings rose by .4% m/o/m in October and off that was up .1% in November. With hours worked at 34.3 vs 34.2 in the two months prior, average weekly earnings were up .4% m/o/m and 3.5% y/o/y, moderating but still hanging in there and still above the pre Covid pace that had a 2 handle.

The participation rate was 62.5% vs 62.4% in September. The key 25-54 yr old cohort saw a rate of 83.8% which is the highest since August 2024.

Bottom line, a lot of confusion here but it’s hard to ignore that rise in the unemployment rate and that about all of the job gains came from healthcare/social assistance. It did nothing though to help long end rates as I guess the establishment survey is the focus with the jobs upside relative to expectations. The 2 yr is down 1 bp to 3.49% but the 10 yr yield is up 1 bp at 4.18% and the 30 yr yield is up 3 bps to 4.86%. The US dollar index is at the weakest since early October.

U6 Unemployment Rate

Average Weekly Earnings y/o/y

BY Doug Kass · Dec 16, 2025, 10:55 AM EST

With S&P cash -42 handles I am covering my financial shorts for gains on the "whoosh" lower:

* (JPM) $315.72

* (C) $111.23

* (GS) $881.98

* (MS) $175.68

BY Doug Kass · Dec 16, 2025, 10:32 AM EST

From Peter Boockvar:

Another failure of government industrial policy/Now I understand where he's coming from/Some data

We’re seeing real time again the failure of government driven industrial policy, this time with EVs. Ford is taking $19.5 billion of charges related to this business after losing $13 billion over the past 3 years. Also announced today, after massive pressure from European auto makers, the EU is relaxing its ban on combustion engine vehicles that would have ended the sale of them by 2035. Bottom line, hybrids are winning vs full EVs and ICE vehicles still sell because that is what the market wants. It’s also the main reason why we own platinum as hybrids use more platinum per car than an ICE vehicle and where full EVs use none.

After watching the interview yesterday with Fed Governor Stephen Miran on CNBC’s Money Movers I have a better understanding of his perspective and why it deviates as it does from the rest of his colleagues in terms of both wanting to cut rates and the more aggressive pace at which he wants to. Relative to his fellow doves, it’s more a difference in time horizon and how far out one’s forecast goes and the belief in the long lags monetary policy has in landing its impact. Miran said that the Fed “needs to make monetary policy now for 2027.” The view of many of his colleagues instead is based on “data dependency” which means they will respond to what they see in the data now.

There was one flaw though in Miran’s thinking I believe. In the interview, he focused on the current slowdown in rental growth which will further moderate services inflation, offsetting any lift in goods prices from tariffs. I agree with him on this but if he’s focused today on calibrating monetary policy for 2027, I’ll argue by then, rental growth will be reaccelerating because of the large slowdown in current construction of multi family buildings as the market absorbs the large 2024 and 2025 supply. Either way, his crystal ball is much better than mine if he’s comfortable with what the world will look like in 2027.

In case you didn’t see the article in the WSJ late Sunday online (in hard copy yesterday) titled “CEOs to Keep Spending on AI, Despite Spotty Returns,” it talked about the results of a survey from Teneo of 350 public company CEOs with revenues north of $1 billion that I thought had some interesting insights. A few things:

1) ”68% of CEOs plan to spend even more on AI in 2026.”

2) ”Less than half of current AI projects had generated more in returns than they had cost.”

3) When will it start generating returns on investments?, “84% of CEOs of large companies (those with revenue of $10 billion or more)...believe it will take more than six months.”

4) This stood out, “67% of CEOs believe AI will increase their entry level head count, while 58% believe AI will increase senior leadership head count.”

A few other things of note in the survey:

5) 31% of large company CEOs said they expect the global economy to improve in the first six months of 2026, down from 51% a year ago.”

6) ”78% of CEOs believe there will be more M&A activity in 2026” vs 83% in 2025.

Ahead of the December US PMI release at 9:45am est, we saw some from overseas. Japan’s manufacturing PMI rose 1 pt m/o/m but still below 50 at 49.7 while services downshifted to 52.5 from 53.2. Australia’s was mixed too with manufacturing rising to 52.2 from 51.6 and services slipping to 51 from 52.8. India continues to be the standout with a composite index of 58.9 with manufacturing at 55.7 and services at 59.1.

In the Eurozone, its manufacturing PMI fell to 49.2 from 49.6 and the services component was down by 1 pt to 52.6 with both below expectations. S&P Global said this, “Economic growth slowed at the end of the year due to a slight contraction in the manufacturing sector and weaker momentum in the service sector. The weaker performance is primarily attributable to German industry, where the downturn intensified. In France, on the other hand, there are signs of a cautious recovery in industry, although a single monthly figure should not be overrated. However, the service sector, which had expanded last month, is stagnating there, while Germany’s service companies saw another solid rise in activity. All in all, the runway into the new year seems pretty unstable.”

And this on inflation, “December data pointed to a marked rise in input costs, with the pace of inflation at a nine-month high. Sharper increases were seen across both monitored sectors, with services continuing to post a faster rise than manufacturing. That said, the rate of inflation in the latter was the sharpest since August 2024.” In terms of the pass through, “The rate of inflation in output prices remained modest and was only slightly quicker than that seen in the previous survey period. Here, a faster rise in services charges was accompanied by broadly unchanged selling prices in the manufacturing sector.”

In the UK, both manufacturing and services rose about 1 pt m/o/m to 51.2 and 52.1 respectively. S&P Global attributed the improvement to “the post Budget lifting of uncertainty” but with this too, “However, the overall pace of output and demand growth remains lackluster, and the expansion is still very dependent on technology and financial services activity, with many other parts of the economy struggling to grow or in decline.”

While the BoE will cut rates on Thursday most likely, S&P Global also said this, “rising staff costs continue to be reported as one of the key concerns of businesses. These higher cost pressures were in turn cited as the key cause of a renewed upturn in selling price inflation across both goods and services.”

The BoE is focused, as is the Fed, more on the labor market where the UK unemployment rate rose to 5.1% thru October, the highest since early 2021.

Nothing market moving with any of these data points.

BY Doug Kass · Dec 16, 2025, 10:15 AM EST

* Pride goeth before a fall....

At words poetic, I'm so pathetic

That I always have found it best

Instead of getting 'em off my chest

To let 'em rest unexpressed

I hate parading my serenading

As I'll probably miss a bar

But if this ditty is not so pretty

At least it'll tell you how great you are

You're the top

You're the Colosseum

You're the top

You're the Louvre Museum

You're a melody from a symphony by Strauss

You're a Bendel bonnet, a Shakespeare sonnet

You're Mickey Mouse

- Cole Porter, You're The Top

The phrase "pride goeth before destruction and a haughty spirit before a fall" comes from Proverbs 16:18 in the Bible. It's a warning that pride and arrogance can lead to one's downfall and it emphasizes the importance of humility and the dangers of overestimating oneself:

BY Doug Kass · Dec 16, 2025, 10:00 AM EST

I have added to my Citigroup (C) and JPMorgan Chase (JPM) shorts.

BY Doug Kass · Dec 16, 2025, 9:44 AM EST

Upside:

-CPAC +29% (Holcim Ltd. to buy majority stake in Peruvian producer of building materials Cementos Pacasmayo for ~$1.5B)

-RILY +28% (earnings)

-CMND +15% (successfully completes Second Cohort Enrollment in Ongoing FDA-Approved Phase I/IIa Trial for CMND-100 for the treatment of Alcohol Use Disorder)

-CLPT +11% (momentum)

-ORGO +11% (announces Successful FDA Meeting and Plan to File BLA for ReNu for Knee Osteoarthritis Pain)

-CGNX +5.2% (Goldman Sachs Raised CGNX to Buy from Sell, price target: $50)

-ROKU +5.0% (Morgan Stanley Raised ROKU to Overweight from Underweight, price target: $135)

-ACN +3.0% (hearing Morgan Stanley Raised ACN to Overweight from Equal Weight, price target: $320)

-ANGX +3.0% (ROTH Initiates ANGX with Buy, price target: $9)

-EL +2.9% (hearing named as Tier 1 firm top pick for 2026 in beauty)

-ALDX +2.8% (US FDA extends PDUFA date to March 16, 2026 (prior December 16, 2025) for Reproxalap NDA for Treatment of Dry Eye Disease)

-SLXN +2.7% (submits Phase 2/3 Clinical Trial Application to Israel for SIL204 in Locally Advanced Pancreatic Cancer; regulatory filings in Germany and the EU are planned for 1Q26)

-GAP +2.1% (Wells Fargo Raised GAP to Overweight from Equal Weight, price target: $30)

Downside:

-VITL -7.2% (cuts FY25 Rev guidance, guides initial FY26)

-NAVN -5.2% (earnings, guidance)

-ABVX -3.9% (earnings)

-STUB -3.9% (Citizens JMP Securities Cuts STUB to Market Perform from Market Outperform)

-HUM -3.6% (affirms FY25 guidance)

-BAH -3.1% (appoints Kristine Martin Anderson Interim CFO)

-GTLB -2.4% (Keybanc/Pacific Crest Cuts GTLB to Sector Weight from Overweight, price target: $49)

BY Doug Kass · Dec 16, 2025, 9:23 AM EST

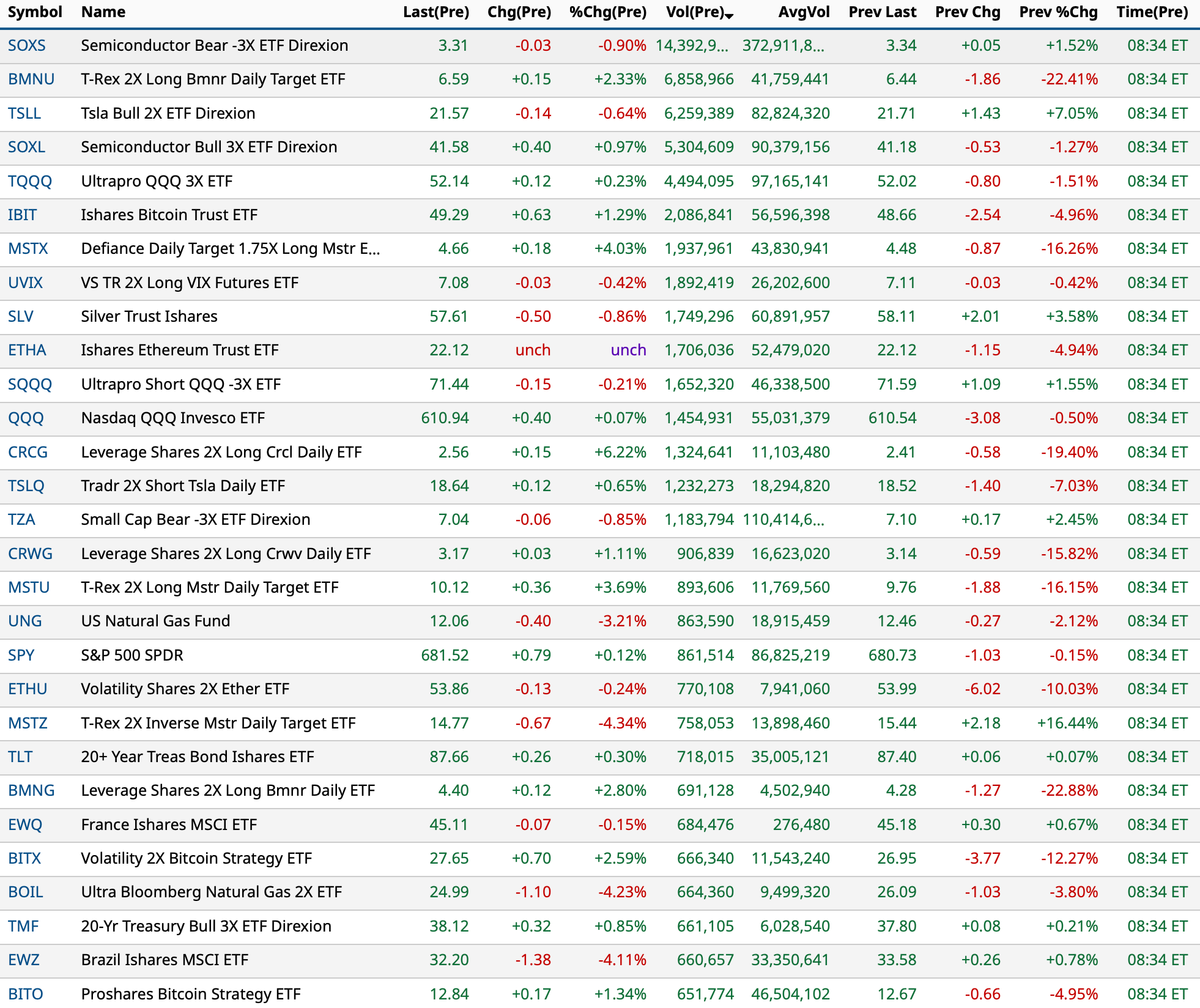

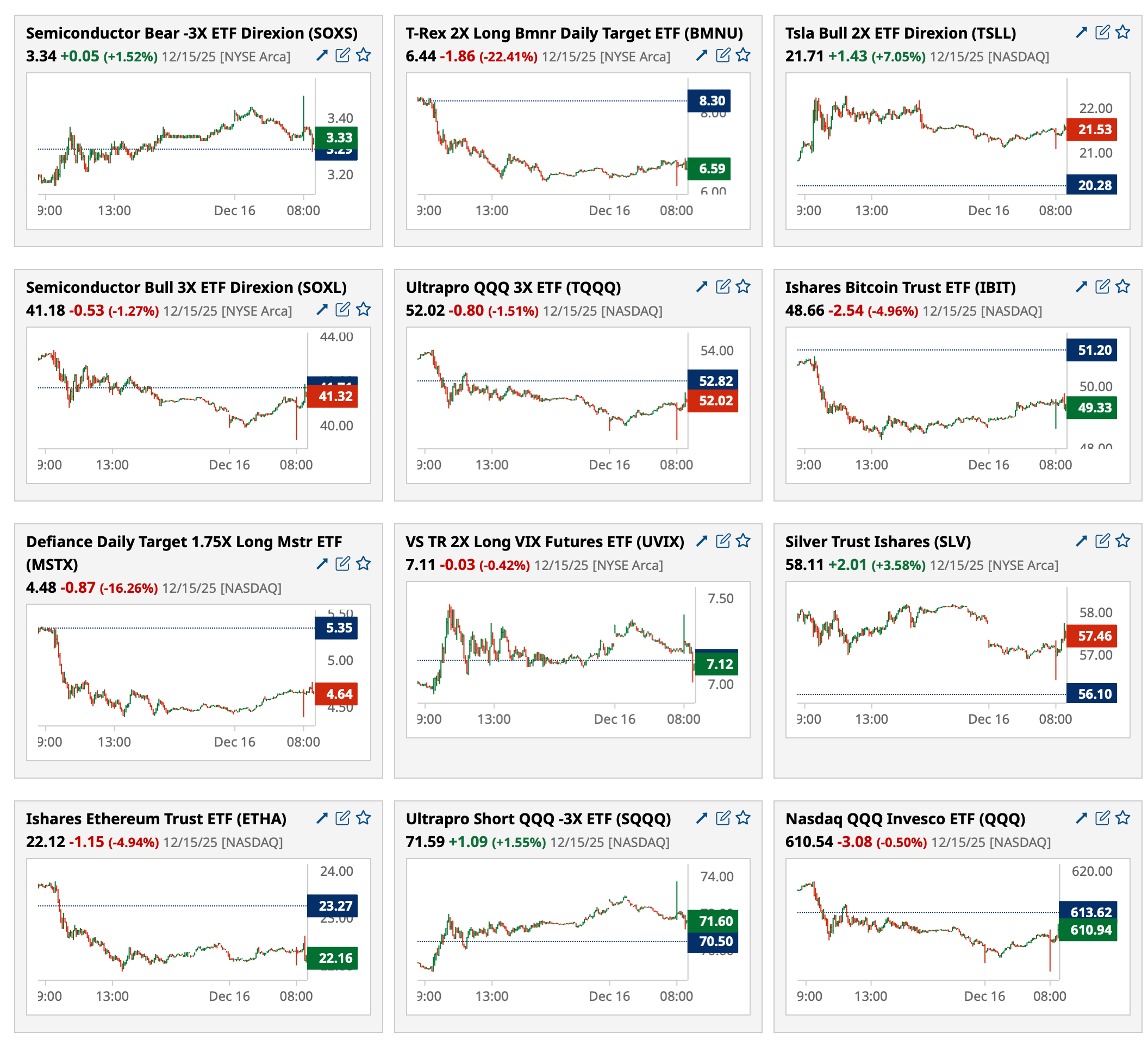

As of 8:34 AM:

BY Doug Kass · Dec 16, 2025, 9:12 AM EST

I am taking a quick and small profit, covering up my index shorts:

* (SPY) $679.58

* (QQQ) $608.59

The gains of these trading rentals are adding up.

I want to give the market a wider berth and plan to short strength.

From early this morning:

I have aggressively shorted the post-jobs ramp:

* (SPY) $681.86

* (QQQ) $611.21

Position: Short SPY common (S), QQQ common (S)

By Doug Kass Dec 16, 2025 8:37 AM EST

BY Doug Kass · Dec 16, 2025, 9:02 AM EST

At 8:51 AM:

BY Doug Kass · Dec 16, 2025, 8:58 AM EST

I have aggressively shorted the post-jobs ramp:

* (SPY) $681.86

* (QQQ) $611.21

BY Doug Kass · Dec 16, 2025, 8:37 AM EST

11:00AM: Treasury Announces a 4, 8 and 17 Week Bill Auction;

11:00AM: Treasury buyback (liquidity support);

11:30AM: Treasury hosts a $75B 6-Week Bill Auction;

BY Doug Kass · Dec 16, 2025, 8:20 AM EST

Dougie Kass

S&P futures were down by nearly -50 handles last night.

Now, down by only -3 handles I am reshorting the Indices:

BY Doug Kass · Dec 16, 2025, 8:10 AM EST

Look into any eyes you find by you

You can see clear through to another day

Maybe it's been seen before through other eyes

On other days while going home

What do you want me to do

To do for you to see you through?

It's all a dream we dreamed

One afternoon long ago

Walk into splintered sunlight

Inch your way through dead dreams to another land

Maybe you're tired and broken

Your tongue is twisted with words half spoken

And thoughts unclear

What do you want me to do

To do for you to see you through?

A box of rain will ease the pain

And love will see you through

Just a box of rain, wind and water

Believe it if you need it

If you don't, just pass it on

Sun and shower, wind and rain

In and out the window

Like a moth before a flame

And it's just a box of rain

I don't know who put it there

Believe it if you need it

Or leave it if you dare

And it's just a box of rain

Or a ribbon for your hair

Such a long, long time to be gone

And a short time to be there

- "Box of Rain" (Performed by The Grateful Dead and written by Robert Hunter and Phil Lesh)

This week marks my 28th year writing for multiple iterations of TheStreet.com.

The nearly three decades have been characterized by changes in management and editorial teams, a number of different owners (starting with the iconic Jim "El Capitan" Cramer who started it all), plenty of corporate name makeovers and, perhaps most importantly a transformation in market structure from active investing to passive investing.

I have tried to give it my all — waking up at 4 AM to get a start on the day, writing late in the evening when there are breaking events or developments and even writing outlines of my week's openers during the weekends.

As I start outlining my Surprises for 2026 and I get older, I get more sentimental. It is only natural. And the events of the last few days have made me even more emotional and introspective:

I am aware of only a few writers that have written in the same spot for nearly 30 years consecutively.

Writing comes easy for me, while, sometimes, other parts of my life are not so easy.

But, importantly, what my Diary has brought to me is more important than I think I have brought to subscribers. I have been the recipient of many important personal relationships (like TLR, Smails and Johnny The Greek, among others) that transcend markets and politics. You all would be very surprised how many subscribers I text or direct message on twitter (X) daily.

It is this that I am so grateful for.

Along with the friendships have come tragedies. The loss of Bill Meehan and Chuck "Brown Bear" Zion in the World Trade Center attack on 9/11. The deaths of legendary Sir Arthur Cashman, Byron Wien, Joe Rosenberg and Vince Farrell come to mind also.

"What do you want me to do

To do for you to see you through?"

As to the columns, I have tried to deliver value-added non-consensus views, outlooks, forecasts that don't resemble the herd. I have always felt the bullish case dominated the business media and was easy to access — the skeptical case not so much. I wanted to deliver the contrarian case with strong analytical support and common sense reasoning.

Increasingly, I have been critical of mainstream Fin TV because I feel they are letting viewers down. I will continue to call out the B.S. and recommend ways in which the business media can be better.

I recognize that the best ideas are hammered out on the anvil of dissent, debate and discourse — so I try to be open minded.

I have received my share of public criticism (some deserved) but my skin is thick after all these years. And when the criticism is constructive, thoughtful and justified I listen... carefully. And I try to modify and get better — recognizing that I don't have the concession on the truth.

I am honest with our subscribers. I take ownership of my investment boners and don't sweep them under the rug. I time stamp my trades and investments.

I have tried to shroud my writing with humor and pop culture — in order to make dry ideas more digestible.

And of course my Diary is populated by a lot of music:

The German philosopher Friedrich Nietzsche once said that “without music, life would be a mistake.” Nietzsche's quote is often attributed to his work Twilight of the Idols, which highlights music's vital role in human existence, emotion, and meaning, suggesting life lacks depth and joy without it. He saw music, as I do, as a way to uplift, express the inexpressible, and connect to deeper truths beyond mere language.

Perhaps the American cartoonist Charles M. Schulz (of Peanuts fame) put the role of music in our lives even better:

Throughout the last 28 years we all have had a set of cherished, personal and shared reference points, common memories and experiences.

Thanks, as always, for reading my musings and missives over the years — I think I have a few good years that still lie ahead.

"Such a long, long time to be gone

And a short time to be there"

BY Doug Kass · Dec 16, 2025, 7:10 AM EST

Bonus — Here are some great links:

The World Is On The Right Side of 200

David vs Goliath: The Small-Cap Setup for the Next 12 Months

If Value Is Really Back, These Two Stocks Will Tell Us First

BY Doug Kass · Dec 16, 2025, 6:50 AM EST

BY Doug Kass · Dec 16, 2025, 6:35 AM EST

I am short Zillow (Z) :

BY Doug Kass · Dec 16, 2025, 6:20 AM EST

BY Doug Kass · Dec 16, 2025, 6:10 AM EST

BY Doug Kass · Dec 16, 2025, 5:55 AM EST

The S & P Short Range Oscillator moved into a greater overbought — now at 2.11% vs. 1.3%.

BY Doug Kass · Dec 16, 2025, 5:45 AM EST