Is this the RMBS/CDO/CDO-squared/synthetic CDO machine of 2008 all over again? Is it the dot-com era—when flimsy business plans minted 20- and 30-year-old billionaires in backwards baseball caps being paraded on CNBC?

No opportunity ever repeats itself exactly. There are always differences. There are also always rhymes.

A few observations:

The business media will not give airtime to too many half-empty-glass voices. Fear doesn’t sell ads, and no one wants to be told their portfolio is about to get crushed.

The business media also won’t seriously examine how many trillions of dollars are being spent on data-center build-outs, nor the fact that much of this infrastructure runs on 4–5 year refresh cycles. Even fewer people ask the harder question: how, exactly, these investments are supposed to earn an economic return sufficient to justify their cost. In many cases, the media doesn’t know—and doesn’t care.

What is the real difference between Global Crossing / Cisco in 1999 and today’s hyperscalers and “neo-cloud” providers? In my view, there are more similarities than differences. The capital expenditures are extraordinary. The certainty around monetization is not. No one truly knows how AI, at scale, will generate profits commensurate with the capital being deployed. The build-out itself is profitable—for the builders. Manufacturing GPUs, constructing data centers, and upgrading electrical grids is not AI; it’s industrial infrastructure.

Meanwhile, investment advisors call me daily trying to sell “AI this” and “AI that”: Google, Oracle, Microsoft, NVIDIA, Palantir—pick your flavor. The narrative is everywhere. The nuance is nowhere.

There is very little doubt in my mind that this market will eventually get crushed—not just “AI stocks,” but the broader market. The open question is timing.

The same crowded, momentum-driven names sit inside index funds, passive strategies, and robo-advisors across the street. When this turns, it won’t be contained.

I am short this market designed to minimize capital at risk, maintain flexible timing, and maximize my upside. I will trade at the fringes. I will not invest one dollar of my hard earned money on the US stock market n 2026.

VIDEO: Louis Vincent-Gave on the Real Winners of the U.S.–China Trade War

The RiskReversal Podcast

I joined Dan Nathan on the RiskReversal Podcast where we once again hosted Louis Vincent-Gave, CEO and founder of Gavekal. It’s a great conversation where we dive deep on how the U.S. and China economic rivalry is evolving, from the unintended consequences of past trade embargoes, to how China’s response has reshaped its industrial base.

We also talk through what this means for global markets and U.S. companies, the strategic shift toward state capitalism and AI, and how the asset centric US economy makes it so difficult to compete on those terms.

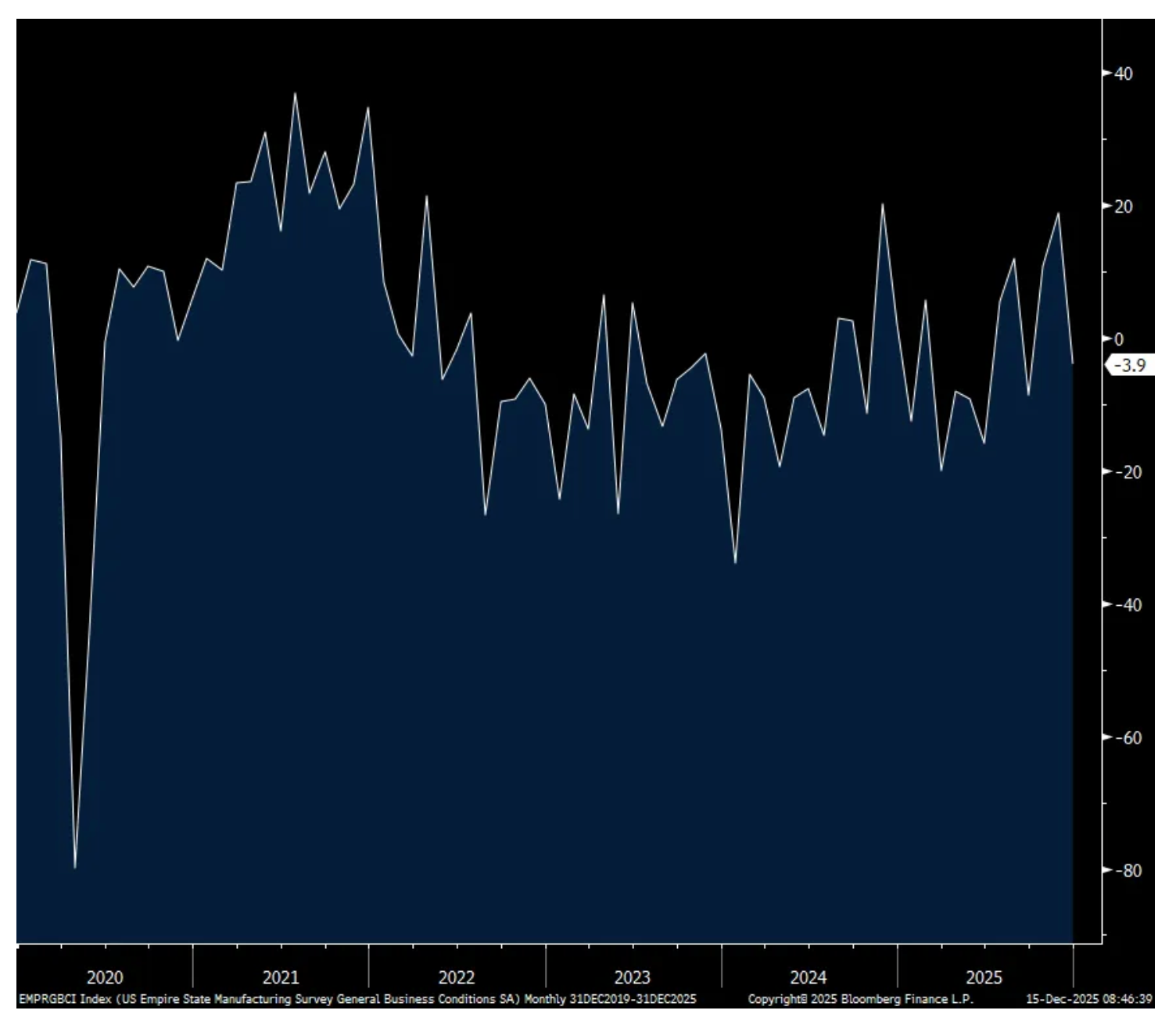

Boockvar on NY Manufacturing Index and Homebuilder Sentiment

From Peter Boockvar:

NY mfr'g index moves like an EKG chart/Homebuilder sentiment

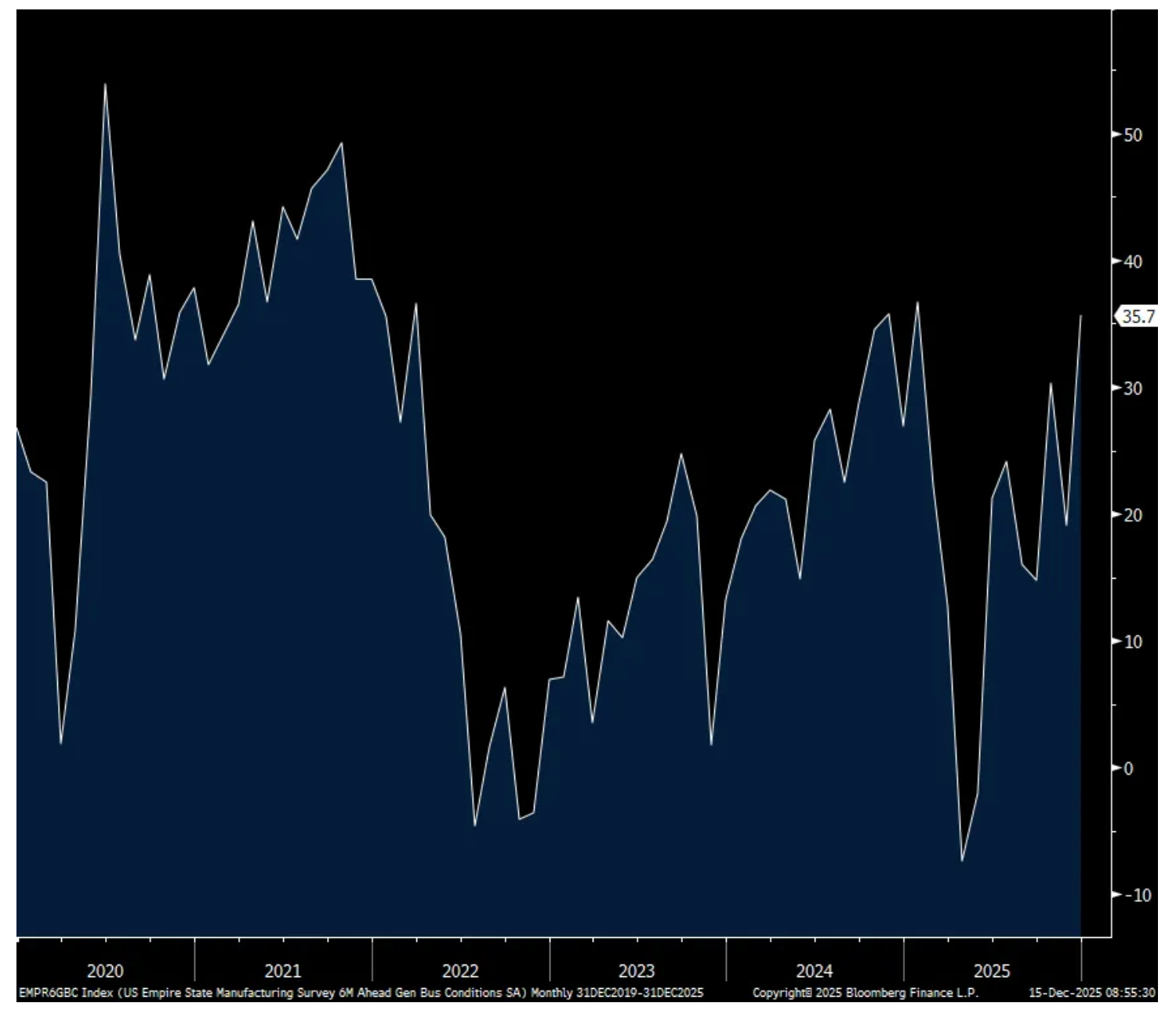

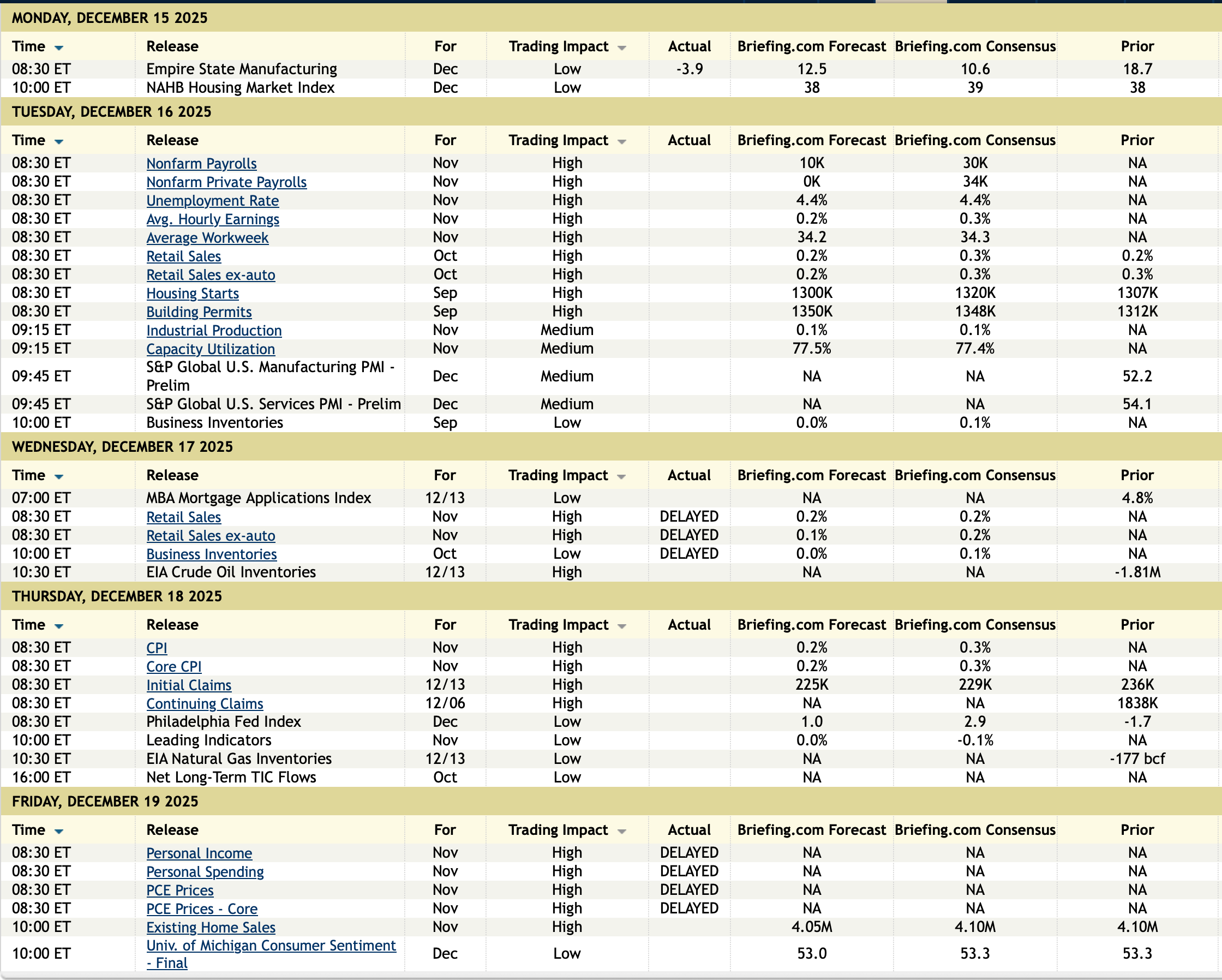

The always volatile December NY manufacturing index that bounces around like an EKG chart fell to -3.9 vs 18.7 in November, 10.7 in October and -8.7 in September. The 6 month average is 5.7 for reference.

To smooth out the components also relative to its 6 month average, new orders were zero vs 2.9 while backlogs fell to -14.9 vs -7.2. Inventories were 4 vs 2.3.

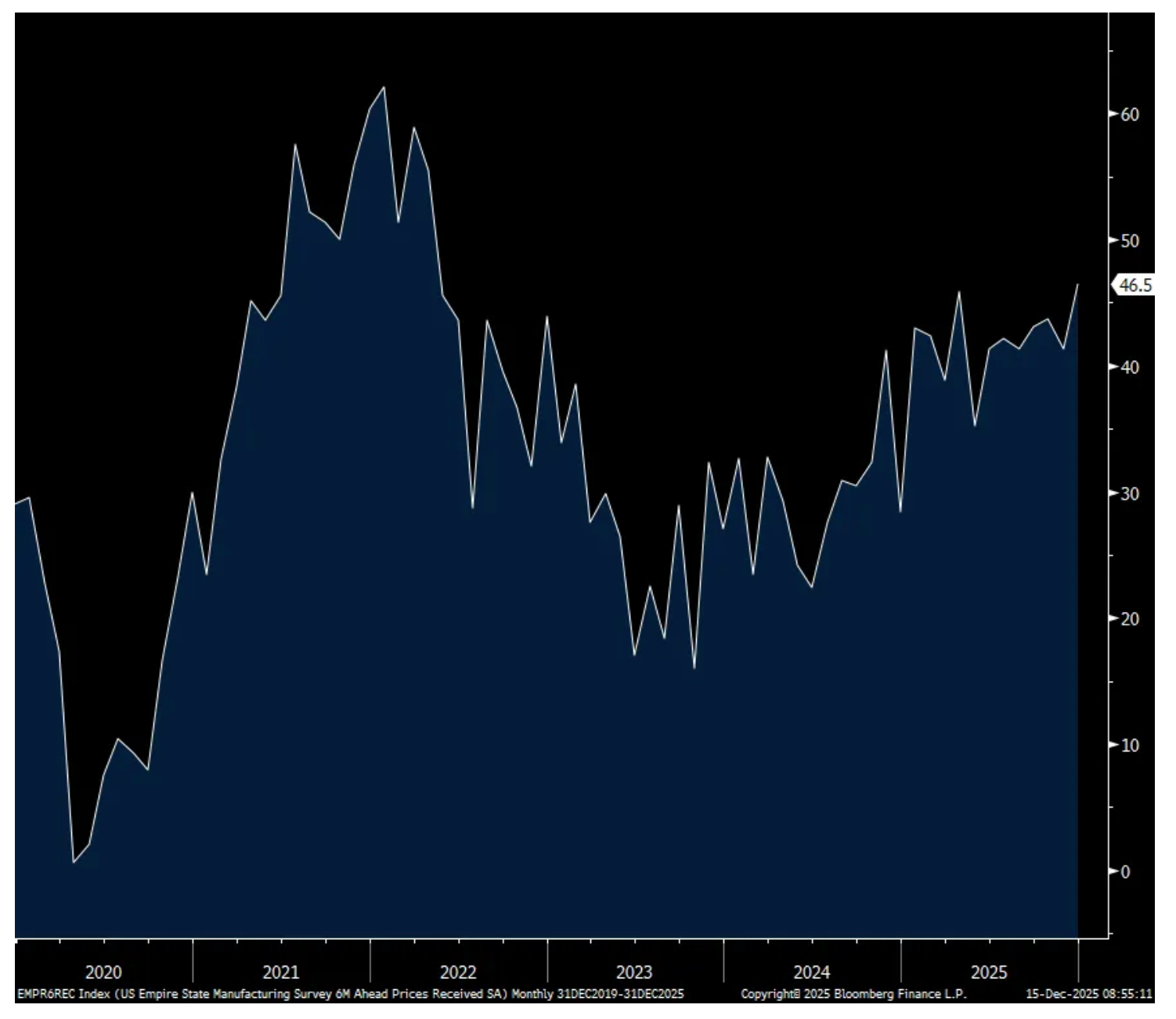

The employment component was 7.3 vs 5.4 while the workweek at 3.5 was above the six month average of 1.1. Prices paid and received at 37.6 and 19.8 are also now below the 6 month average of 49.2 and 23.5.

Of note too, the 6 month business activity was 35.7 vs 23.3. Capital spending plans fell m/o/m but at 6.9 is above the half yr average of 3.3. Expectations for prices received rose to the highest level since April 2022.

Bottom line, it’s likely that the manufacturing recession continued on in December.

NY Mfr’g

6 Month Expectations for Business

6 Month Expectations for Prices Received

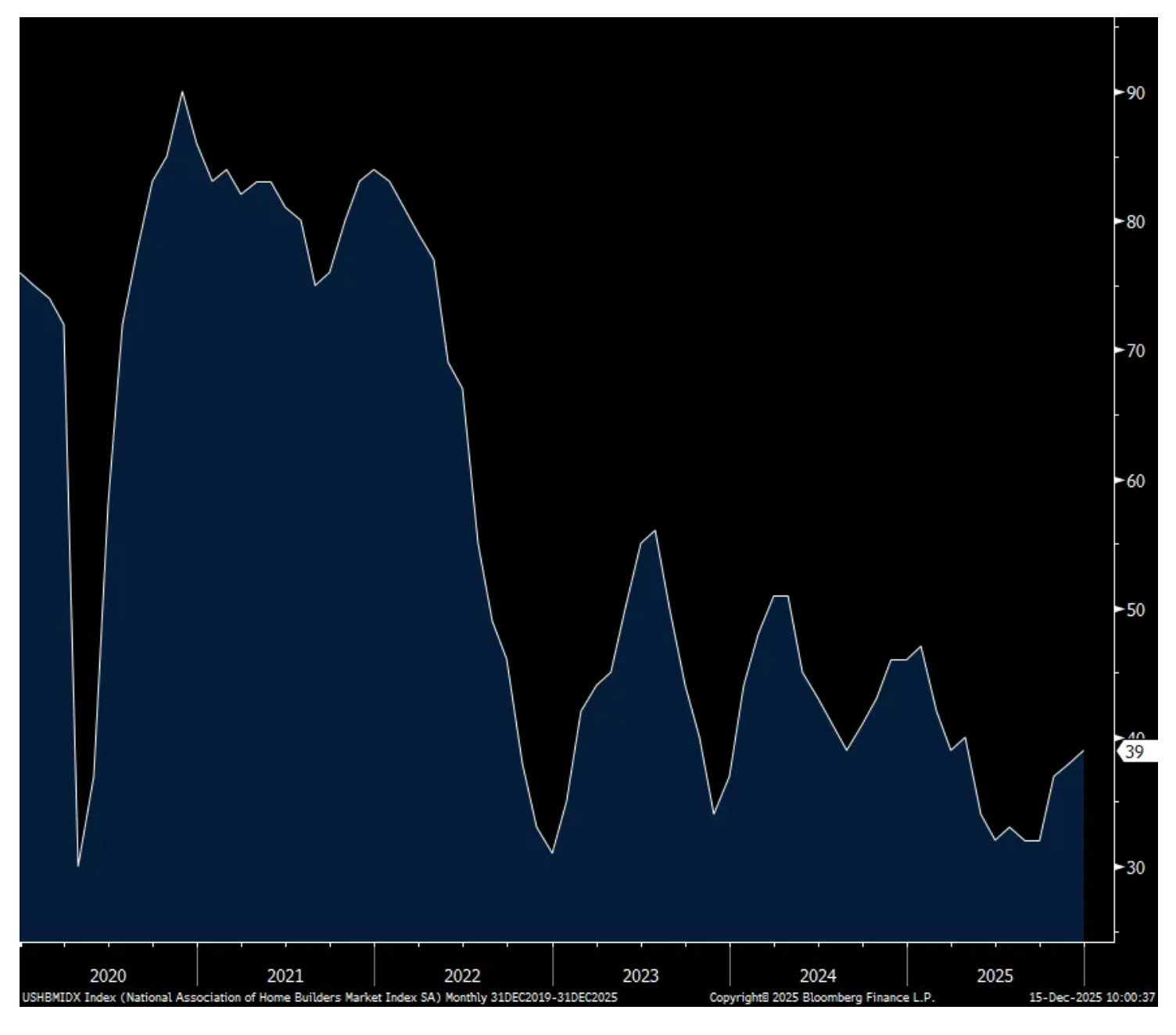

The December NAHB home builder sentiment index was 39 vs 38 in November and as estimated. While the present situation remains well below 50 at 42, optimism still reigns as the Expectations component was 52 from 51 in November. Prospective Buyers Traffic though remains punk at 26, unchanged and about half the 50 breakeven level.

The still subdued builder sentiment can be attributed, not surprisingly, to the following factors stated by the NAHB, “rising construction costs, tariff and economic uncertainty, and many potential buyers remaining on the sidelines due to affordability concerns.”

And as seen with the public builders and what they are doing to move product, “Market conditions remain challenging with two-thirds of builders reporting they are offering incentives to move buyers off the fence.”

To what extent? “40% of builders reported cutting prices in December, marking the second consecutive month the share has been at 40% or higher since May 2020. It was 41% in November. Meanwhile, the average price reduction was 5% in December, down from the 6% rate in November. The use of sales incentives was 67% in December, the highest percentage in the post-Covid period.” I bolded for emphasis.

With the pickup in existing home supply, “Rising inventory also has increased competition for newly built homes.”

Bottom line, we all want rate relief to alleviate the affordability problem that so many first time home buyers face but we also need more supply and a softening of home prices to help too. With the former, we’re learning again that cuts to the fed funds rate doesn’t necessarily mean long rates drop. On the latter, the slowing pace of home price gains, helped by growing supply, is needed in order to increase the rate of transactions. Big picture and longer term, we need baby boomers to downsize to help add more existing home supply to the market.

Released in 1972 (and now the name of a motion picture), "Song Sung Blue" was inspired by the second movement of Mozart's Piano Concerto #21. As part of the Moods album, the song was a No. 1 hit - Diamond's second after 1970's "Cracklin' Rosie."

Mortimer Duke: [after Louis and Billy Ray turn the people towards him and the price starts dropping from their short selling] That's not right. How can the price be going down?

Randolph Duke: Something's wrong. Where's Wilson?

Billy Ray Valentine: [On the floor] SELL! SELL! SELL! SELL!

Mortimer Duke: [Sees him and Lewis] What are *they* doing here?

Randolph Duke: They're *selling*, Mortimer!

Mortimer Duke: Why, that's ridiculous!

[Then a look of shock washes over him]

Mortimer Duke: Unless that crop report...

Randolph Duke: [They both look at one another, then start heading to the pit] God help us!

- Trading Places: Sell!

* Even previously bearish Morgan Stanley's (Mike) Wilson is now a market enthusiast - he apparently is not familiar with the movie, "Trading Places." Morgan Stanley sees S&P 500 climbing another 11% — to 6,500 — next year

* But, something's wrong Wilson, sell!

* The bullish cabal, apparently influenced importantly by the strong price momentum of the indexes, have grown more optimistic with higher stock prices.

* By contrast, we believe there are a plethora of developing market headwinds that are being ignored by most market participants.

* From our perch, the market's upside reward is now dwarfed by the downside risk and that there is virtually no "margin of safety" in current share price levels.

* Indeed, given the "paper thin" equity risk premium, it is our view that the S&P 500 Index (using today's prices as a base) will provide substandard to negative returns over the next few years.

* Short selling opportunities now abound...

* In this morning's market update I take into account the wisdom of Jerry Garcia, Warren Buffett, Charlie Munger, Richard Russell and Rosie (David Rosenberg)

“A bull market tends to bail you out of all your mistakes. Conversely, bear markets make you pay for your mistakes.”

- Richard Russell

"You need to divorce your mind from the crowd. The herd mentality causes all these IQs to become paralyzed."

- Warren Buffett

The foundation of Seabreeze's ursine market view is based on some of the following concerns:

* Interest rates will likely be higher for longer. The peak easing this year priced in for year-end 2025 was an expected federal funds rate of about 2.80%. That is now about 3.90%, so the market has taken away 110 bps of rate cuts. Treasury Sec. Janet Yellen has front loaded Treasury issuance in bills, above the recommended level of 15%-20% of total offerings by the Treasury Borrowing Advisory Committee. This, instead of issuing more longer-term coupons when the 10-year yield was back under 4%.

While no one at the Treasury will admit it, they were playing the yield curve, didn't want to upset the longer end of the curve with too much supply and instead with the back up in short rates, missed an opportunity to term out U.S. debt.

Stated simply, the Fed blew it.

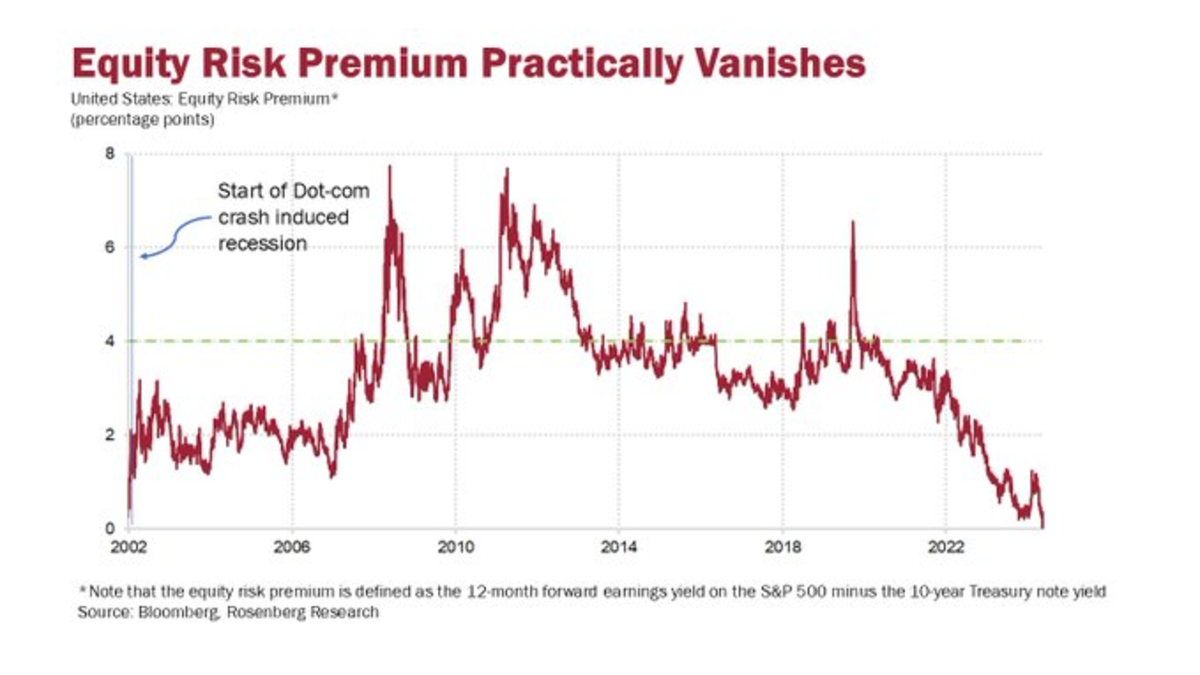

Over the last five decades interest rates (the 10-year Treasury note yields 4.48%) have never been so high, at 3.5-times relative to the S&P dividend yield (1.27%). The S&P equity risk premium (forward earnings yield less the 10-year yield) has turned negative for the first time since 2002. In other words, investors are now paying to take risk rather than being compensated for taking risk:

Here is a longer-term chart of the S&P earnings yield vs. the yield on the 10-year Treasury note:

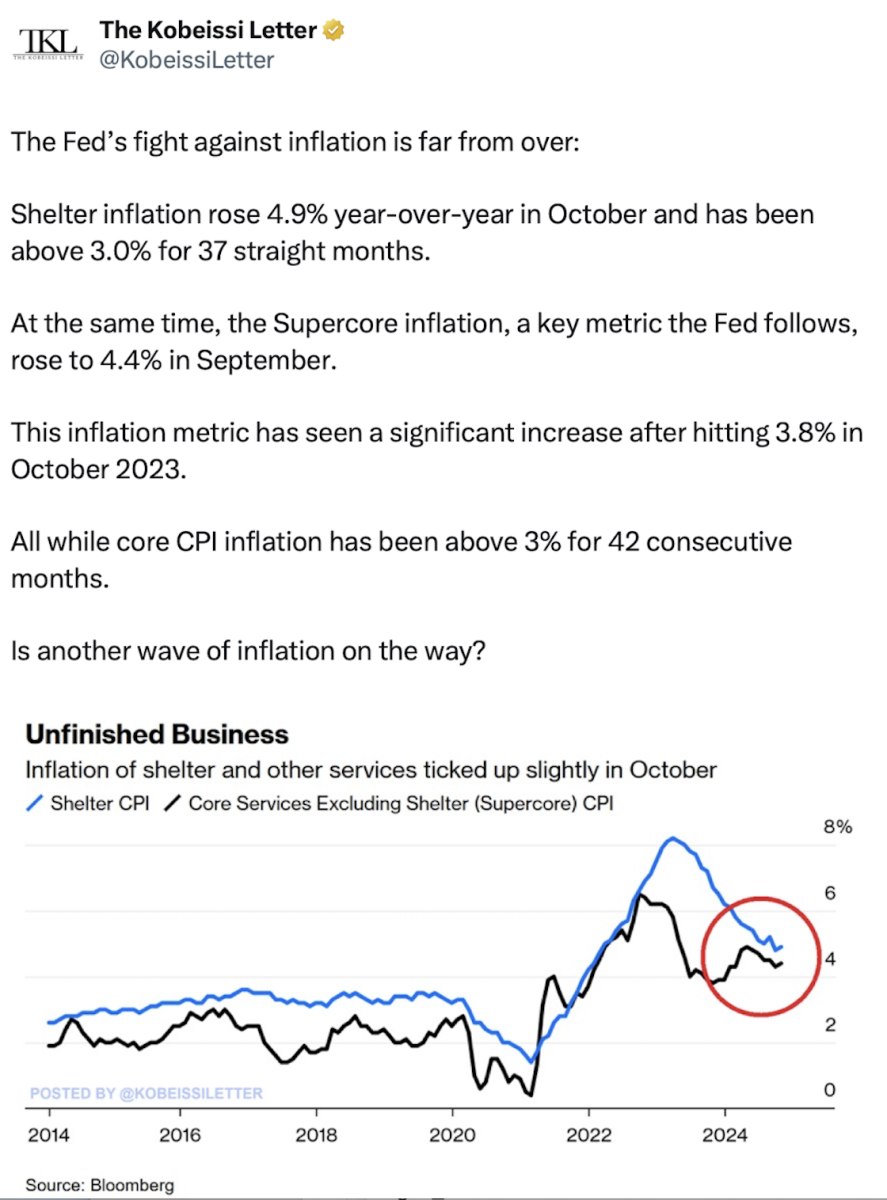

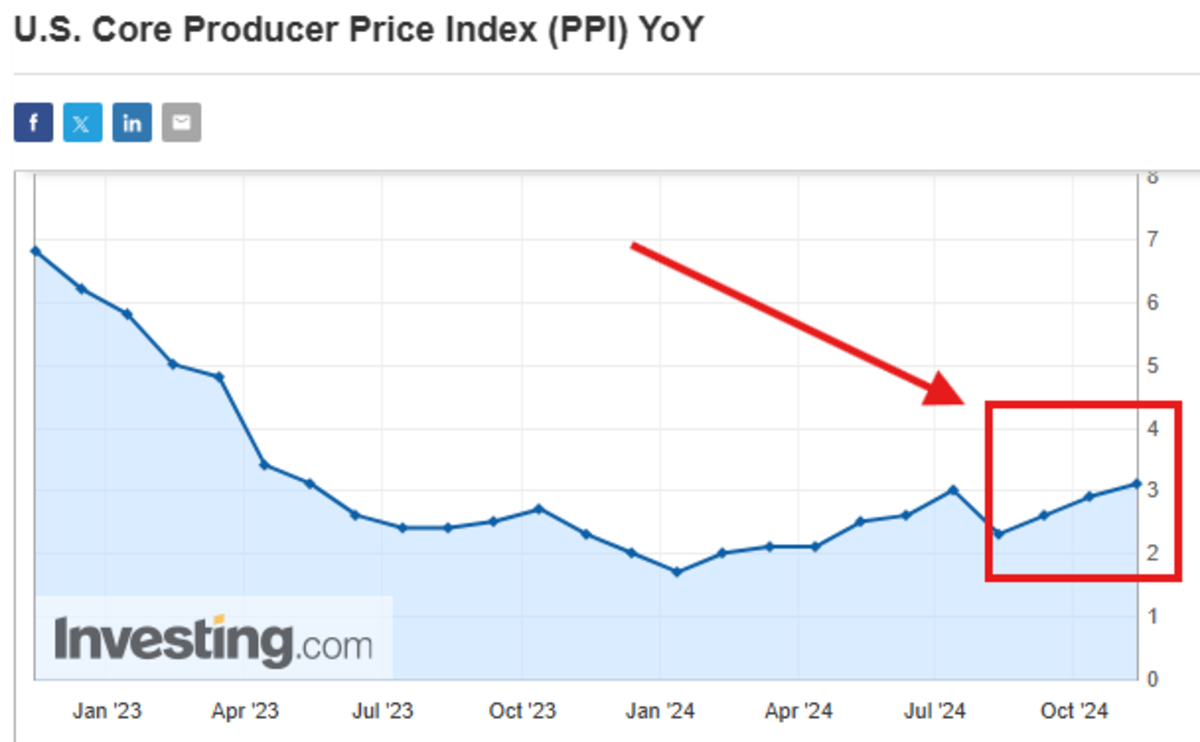

* Inflation will likely remain sticky. For the first time since April 2023, core producer price index and consumer price index inflation are back above 3%. Even as the Fed thought inflation was heading to its 2% target, it clearly is not. Inflation has leveled off well above the Fed's 2% target, yet the Fed keeps cutting interest rates.

While the Fed still prefers the PCE inflation statistic (mistakenly we believe) and running monetary policy off it, core CPI has risen by +0.3% (month over month) for a third straight month and remains sideways (year over year) still above three percent. Services inflation continues to be where it is coming from, as it always does, while goods prices are about flat:

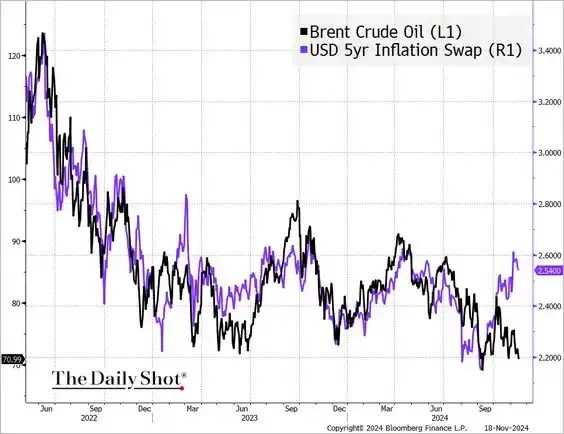

It is important to note that inflation is rising despite weakness in the price of oil:

Inflation will worsen if the new administration follows through with tariffs (raising import prices) and a tough immigration policy. The first Trump Administration took tariffs from 0.5% to 3%. Currently the President Elect is talking about taking tariffs to at least 15%. This will likely drive import and export prices higher.

* Sluggish global economic growth with persistent inflation means that the era of "slugflation" has likely begun. Indeed, as mentioned previously, for the first time since September 2022, both CPI and PPI inflation are officially back on the rise just as economic growth is decelerating.

The Liscio Report just updated its state-level tax sales receipt database, which has been an excellent indicator of domestic growth. According to the state tax data, there are recessionary warnings as reflected in that only about 1/3 of the states met their targets in October and just half recorded any year over year growth at all. This data is consistent with The Beige Book which also has struck a recessionary tone.

* Reduced corporate profit expectations. Last month we noted diminished 3Q2024 S&P expectations (in July +8% EPS growth was forecast, now +4% seems likely). 4Q2024 profit expectations have come off by an additional -2.1% since the start of the quarter and are currently at their lowest point since estimates began (at $62.40/share). Full year 2025 EPS projections are not far behind, falling -1.1% over the same time frame and at the lowest level since March (at $272.30/share).

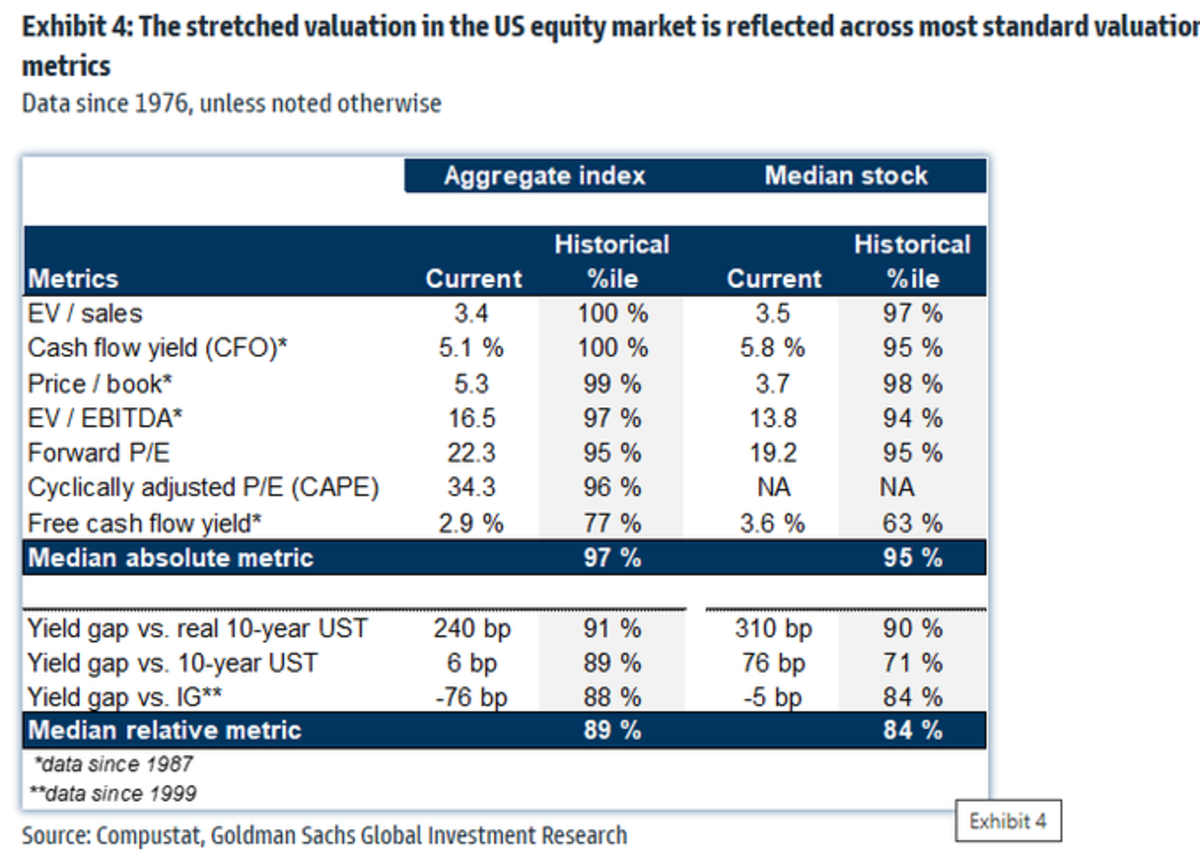

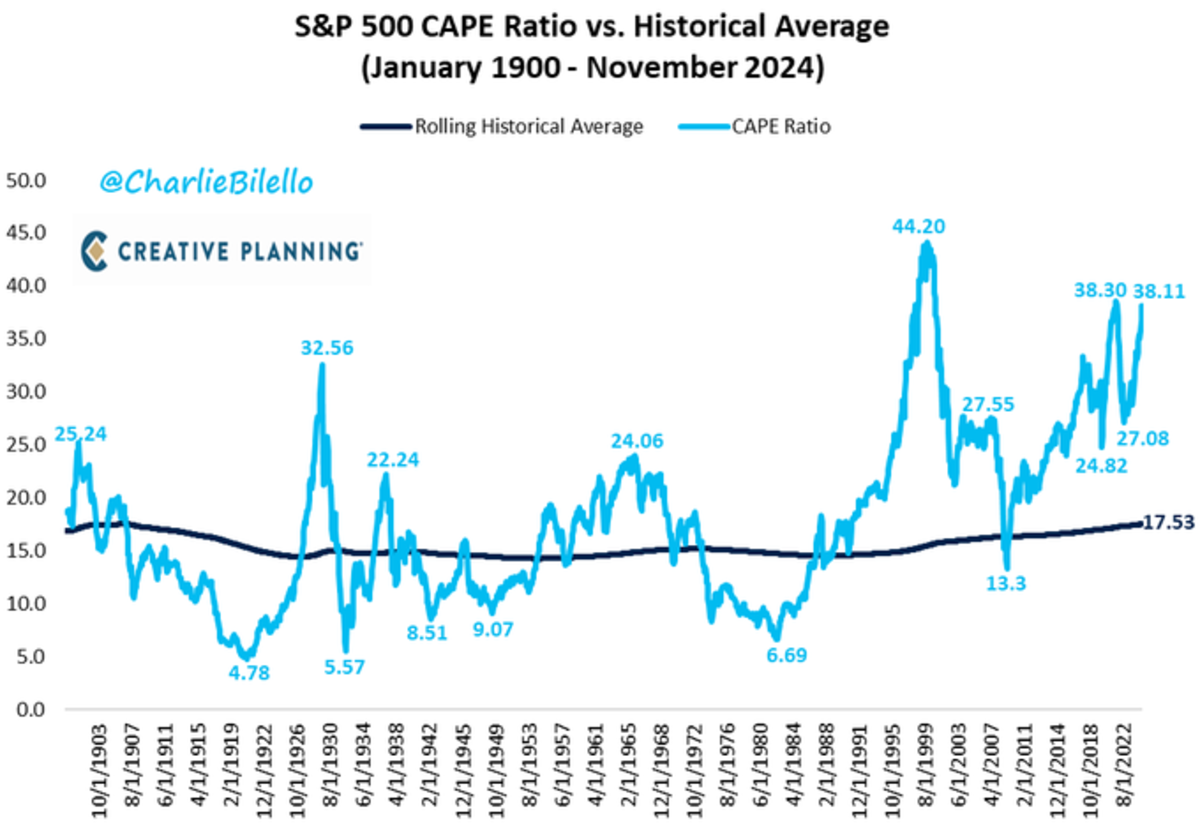

* Elevated valuations. The Chart below highlights the stretched valuation of the US stock market along almost every traditional valuation metric:

The S&P CAPE Ratio (the cyclically adjusted price-to-earnings ratio) has crossed above 38 for the third time in history and is now higher than 98% of all historical valuations:

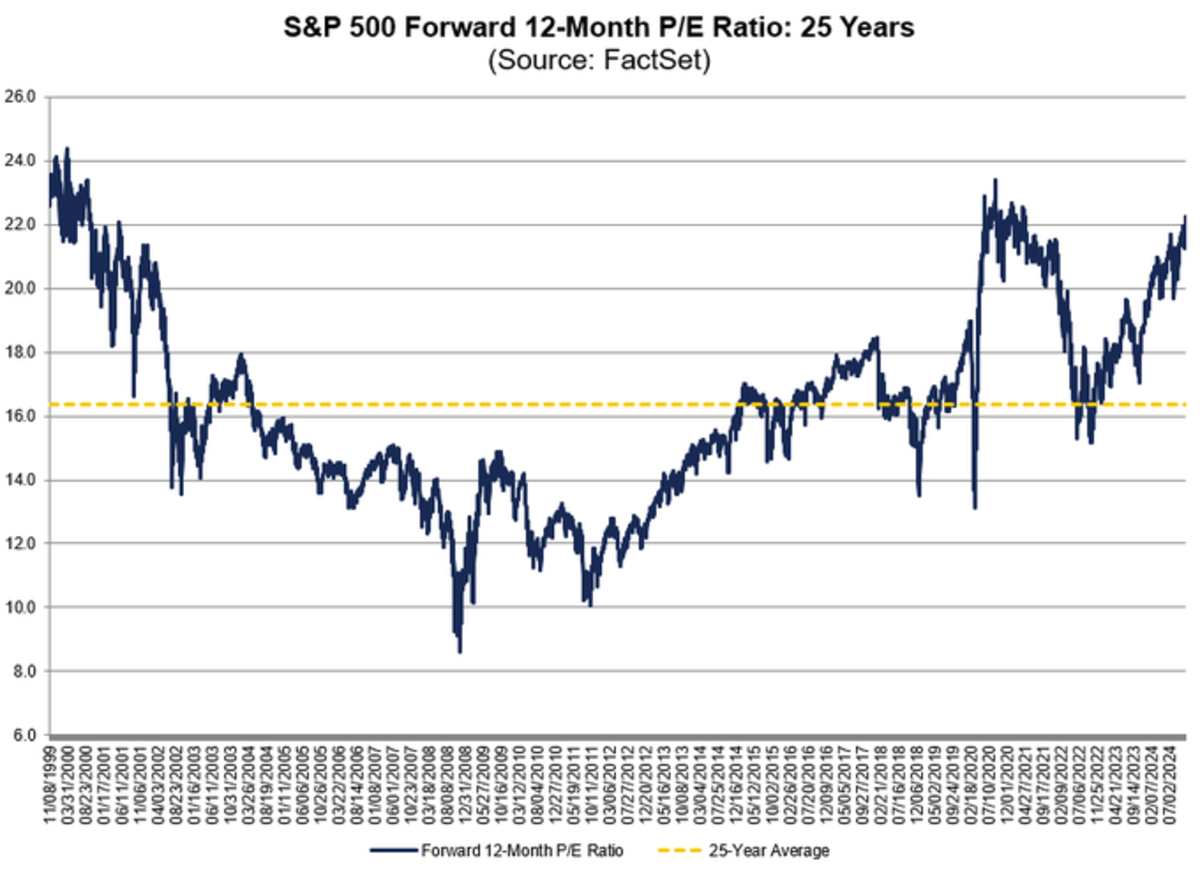

Here is a chart which demonstrates how high forward multiples are with an historical perspective:

* Feckless monetary and fiscal policies (leading to ever higher deficits and unprecedented national debt loads). We have covered this issue extensively over the last twelve months.

* Geopolitical risks abound as evidenced by Ukraine's retaliation into Russia and Putin's saber rattling and threatening response. Arguably, should the new Administration become more isolationist those risks will likely multiply.

* Market structure risks. We have also covered this subject extensively.

Bottom Line

Trouble ahead

Trouble behind

And you know that notion

Just crossed my mind

- The Grateful Dead, Casey Jones Grateful Dead - Casey Jones (Winterland 12/31/78)

Four weeks ago in my Diary, I underscored our risk averse strategy by quoting Warren Buffett and Charlie Munger:

Warren Buffett: I would rather be 100x too cautious than 1% too incautious -- and that will continue as long as I'm around.

Charlie Munger: If we had used the leverage that a lot of successful operators did, Berkshire would be a lot bigger-- but we would have been sweating at night.

This month, too, we have widely quoted Buffett - whose cash hoard he manages at Berkshire Hathaway has risen by another $50 billion (to $325 billion) in recent weeks.

The troubling factors and conditions included in today's commentary suggest to us that the market's upside reward is dwarfed by downside risk.

Thus far in 2024 our fears have not been well realized as the equity market has advanced meaningfully. Though we have managed to deliver a positive investment return this year - while being net short (!) - we have, thus far, failed to capture the opportunity set in equities. (We give ourselves a "D" grade for market outlook (and positioning) and an "A" grade for risk control).

Nonetheless, we feel more strongly that we will be correct in view and continue to embrace a cautious and defensive strategy based on the expectations that stocks will fall to more attractive levels to buy in the next few months.

To be direct, "group stink" (a term we use for the consensus) has a foul odor these days.

Investment data is available more conveniently and faster today, but the behavior of investors is often no more intelligent than in the past. How people react will not change. Their psychological makeup stays constant. In managing money through multiple market cycles, an investment manager should often divorce his mind from the crowd.

The herd mentality and the dominance of passive products and strategies that worship at the altar of price momentum sometimes causes market participants' IQs to become paralyzed. Arguably, this is one of those times.

Given the rising risks and nosebleed valuations, we don't think investors in the last few months are acting very intelligently.

In markets, smart doesn't always equal rational and can produce some unexpected and unwelcomed outcomes:

Long Term Capital Management had hundreds of millions of dollars of their own money and had all that experience. The list included Nobel Prize winners. They probably had the highest IQ of any 100 people working in the country - yet the place still blew up. It went to zero in a matter of days. How can people who are rich and no longer need money do such foolish things?

- Warren Buffett

We are of the strong belief that to be a successful investor over several market cycles, you must divorce yourself from the fears and greed of the people around you, although, at times, it is almost impossible.

It remains our view that the U.S. stock market is overvalued against interest rates, earnings, cash flow and sales -- and most other metrics that have stood the test of time.

As reflected in the vanishing equity risk premium, fear and doubt has left Wall Street.

Slugflation may lie ahead as the labor market weakens and, for the first time in over two years, both consumer price index and producer price index inflation are back rising -- at a time in which price earnings multiples are, on average, in the 95%-tile and interest rates are resuming their rise (the yield on the 10-year Treasury now stands at near 4.50%).

Still wondering why gold is where it's at?/Tiring trade/Other notables

Oh my what a tragic weekend in too many ways.

Wondering still why gold has risen so much and continues to trade as well as it does? Front page of the Weekend FT, “EU freezes 210bn euros of Russian assets.” When these assets were first frozen in 2022, that freeze had to be renewed every six months by the 27 EU countries. What this does is now indefinitely freeze them. And, “The freezing paves the way for a loan to be raised against the assets to prop up Ukraine’s defense.”

The Russians immediately sued Euroclear in Belgium where the assets are being held but by owning gold that one can hold on its own territory is not subject to any confiscation. And that foreign government/central bank buying really began in earnest in 2022, as we know, when the Russian asset freeze first took place and has continued robustly since. This news over the weekend should perpetuate the trend as we look to 2026 and we remain positive and long, along with silver and platinum among the precious metals.

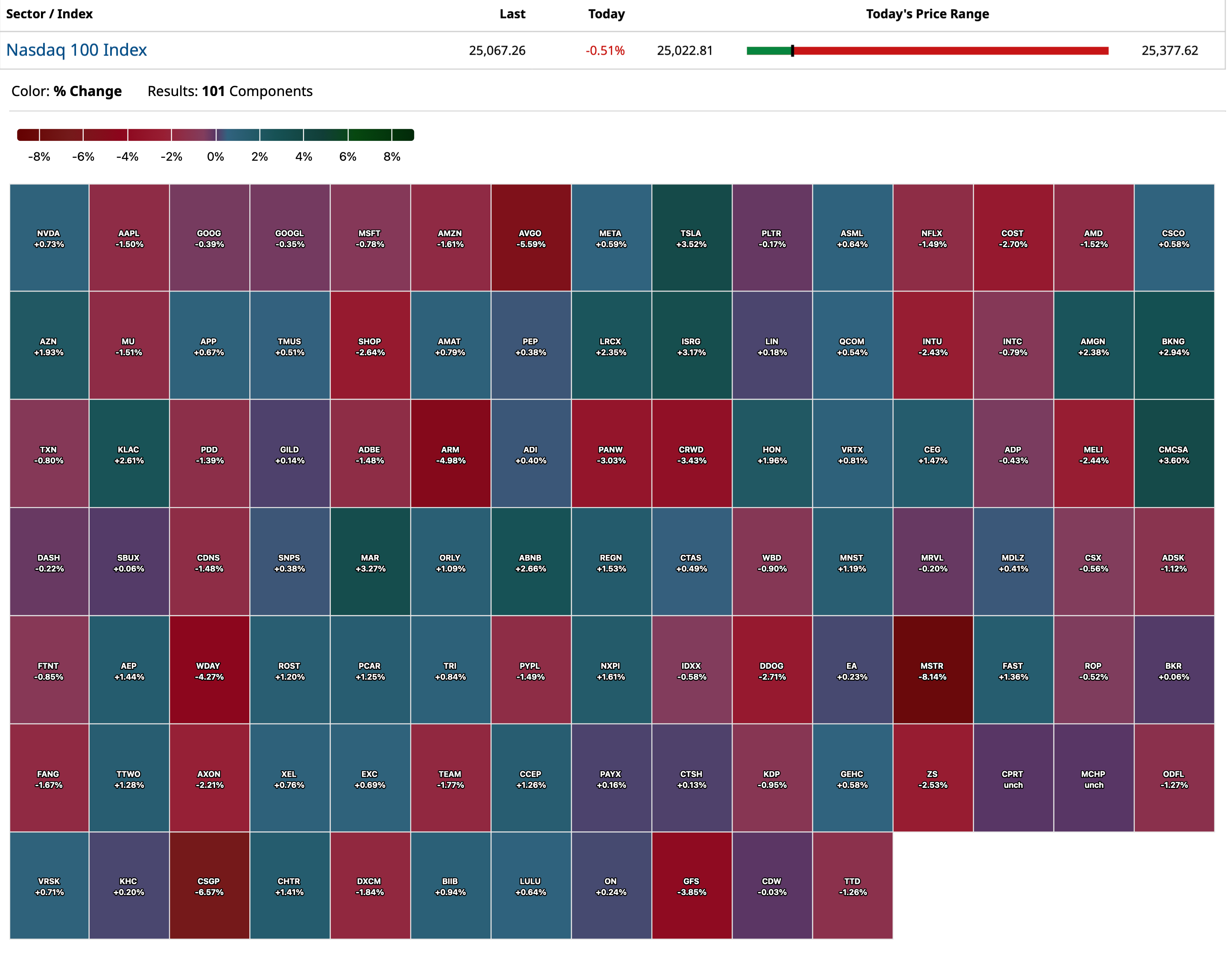

Also as we look to next year, what comes of the tremendous GenAI tech trade? On November 25th I wrote “This is no longer a one way ride” in light of the Gemini 3 LLM model news beating Open AI on certain capability criteria. I said, “Investors are clearly in the process of shifting from GenAI being one big trade, to now trying to figure out who will win and who will not.” After seeing the stock market reaction Nvidia’s earnings, Oracle and Broadcom too, among others, this entire trade is seemingly tiring out. Luckily for now though, investors are finding other things to buy.

The two laggard groups we own and like a lot for next year are energy stocks and consumer staples with many in the latter group yielding bond like dividend yields and have equity upside too. There are also smaller cap value names we own and like that have been left for dead over the past few years. I believe too that the huge outperformance of international stocks and emerging market local currency bonds are not just a one year thing and should continue, again helped by US dollar weakness that more Fed rate cuts will bring. The US dollar by the way is trading this morning at the weakest level since early October.

The November economic data out of China is highlighting again how mixed and uneven their economy is too with particular challenges with household spending and continued stress in their housing market. Retail sales rose just 1.3% y/o/y, well under the estimate of up 2.9% and this coincided with another drop in home prices, both new and used. I believe no amount of government incentives are going to sustainably encourage the Chinese to spend and that the only thing that will is when home prices stop going down with residential real estate being such a large piece of consumer net worth.

Industrial production rose 4.8% y/o/y, about as forecasted with parts of Chinese manufacturing producing some of the world’s most technologically advanced and competitive stuff, especially in autos, technology, AI, solar, robotics, automation and electricity production. The weakness in housing and construction was reflected in the 15.9% ytd decline in property investment vs the estimate of down 15.4%.

The Shanghai comp fell .6% and the Hang Seng was lower by 1.3%. I still like stocks there and believe its outperformance will continue next year.

For another great podcast with Louis Vincent Gave of Gavekal and a broad discussion on China and the growing competition with the US, Dan Nathan and I chatted with him Friday and I’ll be posting later a link to it.

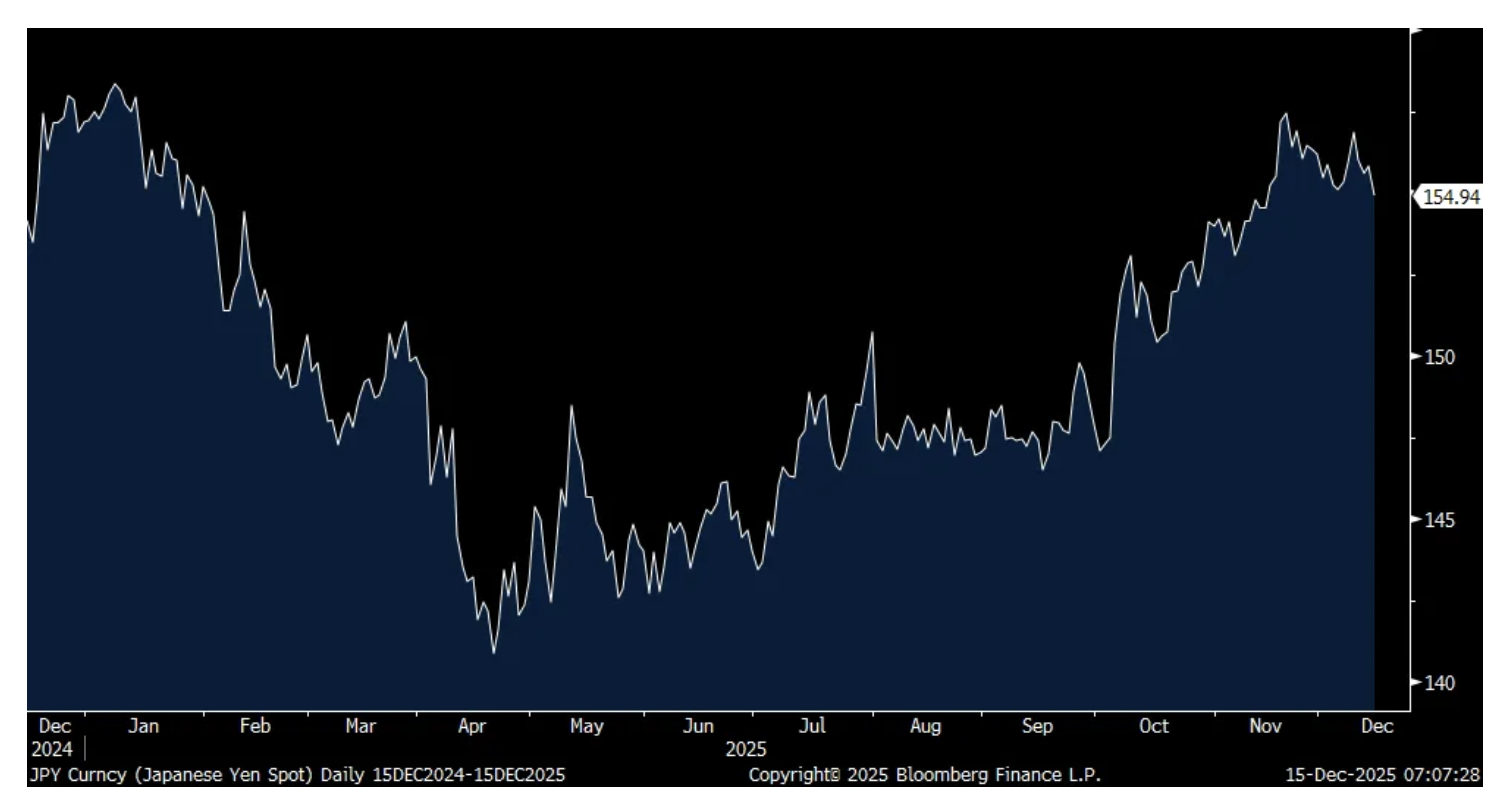

Japan reported its Q4 Tankan report on both manufacturing and non-manufacturing and for large and small businesses and was mostly flat to slightly better vs Q3. We of course await the BoJ on Friday who will raise rates but markets are most interested now in the pace at which they will follow through in 2026. The yen is quietly at a one month high in anticipation of a signaling that more hikes are to come and with the notable rise in JGB yields we’ve seen.

-GLSI +30% (announces Preliminary Analysis Showing 80% Recurrence Rate Reduction in the Open Label Arm of FLAMINGO-01)

-IMNM +25% (Phase 3 RINGSIDE Trial of Varegacestat in patients with Desmoid Tumors met primary endpoint)

-MIST +24% (receives FDA Approval of CARDAMYST (etripamil) as First and Only Self-Administered Nasal Spray for Adults with Paroxysmal Supraventricular Tachycardia (PSVT))

-HSCS +8.6% (announces FDA 510(k) Submission for MyoVista wavECG Device; Expect to announce initial customer deployments as these discussions progress)

-ACTU +6.0% (announces Publication of Positive Phase II Clinical Data for Elraglusib Combined with Platinum Chemotherapy and Sequential Immunotherapy in Recurrent, Metastatic Salivary Gland Carcinoma)

-DOCS +5.6% (Morgan Stanley Raised DOCS to Overweight from Equal Weight, price target: $65)

-ZIM +5.0% (reportedly MSC submits purchase bid)

-LITE +4.4% (momentum)

-IMAX +4.1% (JPMorgan Chase and Co Raised IMAX to Overweight from Neutral, price target: $47 from $32)

-TER +3.4% (Goldman Sachs Raised TER to Buy from Sell, price target: $230)

-BMY +2.7% (Tier1 firm Raised BMY to Buy from Neutral, price target: $61 from $52)

-FTRE +2.0% (Barclays Raised FTRE to Equal Weight from Underweight, price target: $15)

-DG +1.9% (JPMorgan Chase and Co Raised DG to Overweight from Neutral, price target: $166 from $128)

Downside:

-IRBT -69% (enters into a Ch 11 Restructuring Support Agreement with its secured lender and its primary contract manufacturer, Shenzhen PICEA Robotics Co., Ltd. and Santrum Hong Kong Co., Limited, for Picea to acquire iRobot through a court-supervised process)

-Z -6.1% (recent notable premarket weakness being attributed to report that Google putting for sale listings directly into search results)

-NOW -5.9% (reportedly in late stage talks to acquire cybersecurity startup Armis for as much as $7B)

-FRPT -2.2% (Deutsche Bank Cuts FRPT to Hold from Buy, price target: $62)

9:30 a.m.: Fed Board Governor Stephen Miran (Voter) speaks on the inflation outlook before an event hosted by Columbia University, NYC (Text available.Q&A from moderator. Livestream link; 10:30 a.m.: Fed Bank of New York President Williams (Voter) participates in economic growth dis-cussion before event organized by the New Jersey Bankers Association, Jersey City, NJ (Text and moderated Q&A expected. Media availability follows for reporters in attendance)

Have to catch an early train, got to be to work by nine

And if I had an aeroplane, I still couldn't make it on time 'Cause it takes me so long just to figure out what I'm gonna wear Blame it on the train, but the boss is already there

It's just another manic Monday (Ooh-oh) Wish it were Sunday (Ooh-oh) 'Cause that's my fun day (Ooh-oh) My I-don't-have-to-run day (Ooh) It's just another manic Monday

For those subs that have questioned the value of my "More Tales" series (now almost 170 articles) - my year long concerns, presented before ANYONE was concerned, are starting to gain some voices:

Palantir's Alex Karp at the Recent DealBook Summit

Palantir's (PLTR) Alex Karp appeared in an interview with Andrew Ross Sorkin at the DealBook Summit for The New York Times (which was briefly aired on CNBC):