From Peter Boockvar:

Positives,

1) The Fed cut interest rates to address the worries about the slowing pace of hiring’s. The coming expansion of their balance sheet will help alleviate year end funding issues and also any liquidity constraints ahead of April tax day.

2) There was a big drop in continuing claims for the week ended 11/29 to 1.838mm, 100k less than expected and down from 1.937mm in the week before. Your guess is as good as mine as to why, outside of the holiday influence.

3) Job openings in October at 7.67mm was little changed with the 7.66mm seen in September.

4) The November NFIB Small Business Optimism index rose to 99 from 98.2 in October, vs 98.8 in September and 100.8 in August.

5) Refi’s rebounded by 14.3% w/o/w after 5 weeks of declines.

6) In the November Consumer Expectations survey from the NY Fed, the one year inflation guess held at 3.2% and for the time frame past this, was unchanged at 3%. The labor market components as well as income both improved a touch but delinquency expectations rose. Spending expectations also rose slightly.

7) The US September trade deficit narrowed to $52.8 b from $59.3b led by a 3% increase in exports but it was almost all gold and whose export is not included in the GDP calculation.

8) From Costco: “Traffic or shopping frequency increased 3.1% worldwide, and our average transaction or ticket was up 3.2% worldwide, both with and without the impacts of gas price deflation and FX.”

9) From AutoZone: “At the end of the day, I would kind of characterize it as the lower end consumer has been under pressure for frankly quite some time. I’d say more than two years. And what I would say is they’ve been relatively stable. So there hasn’t been a significant wobble in that lower end consumer. The higher end consumer, we think, is still doing okay, and we think that’s been relatively stable over the last couple of quarters.”

10) From Ollie’s Bargain Outlets: “Our comp trends since early October have been strong, and we feel great about our momentum heading into the final weeks of the holiday season…Both the younger and higher income groups were the fastest growing cohorts in the quarter, which we think is in part driven by the continued reallocation of marketing dollars to digital, consumers seeking value, and customers trading down.”

11) From JP Morgan: “the consumer and small businesses both continue to be resilient. They continue to be healthy. The metrics continue to demonstrate that whether it’s cash buffers which have normalized but are also stable, whether it’s credit metrics, really across asset classes, spend trends, payment rates, the metrics themselves are underlying really quite healthy.” On credit quality, “credit trends in the card business look pretty good right now. And I always want to touch on wood, but I won’t do that. And then auto is another one where there is a lot of anxiety about auto delinquencies, subprime auto delinquencies. And there were across the industry a couple of pretty negatively selected vintages in ‘22 and ‘23...And so as we look at the vintage performance, you’re seeing the ‘22 and ‘23 vintages now normalized. The ‘24 and ‘25 vintages are looking much more normal.”

12) The Bank of Canada held rates unchanged at 2.25% as expected. Governor Macklem of the Bank of Canada said “It’s been a difficult year for Canadians and Canadian businesses. But as the year is closing, it’s looking better than it looked in the spring, in the summer.” And, “Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy.”

13) The Swiss National Bank held its interest rate at zero, thankfully not going back to the dark side and back to NIRP.

14) The Reserve Bank of Australia held rates unchanged as expected at 3.6% and explicitly told us that they are done cutting and might even hike rates next year. Governor Bullock said “I don’t think there are interest rate cuts on the horizon for the foreseeable future. The question is, is it just an extended hold for here or is it the possibility of a rate rise. I couldn’t put a probability on those but I think they’re the two things that the board will be looking closely at coming into the new year.”

15) Reflecting still robust tech shipments, Taiwan’s November exports popped by 56% y/o/y, above the estimate of 42%. Imports, much of which makes its way into eventual exports, jumped 45% y/o/y, well more than the estimate of 17%.

16) China continues to rely less on selling stuff to the US (though they still sell things to use indirectly via Vietnam and others) . Overall exports for them in November rose 5.9% y/o/y, above the estimate of 4%. Exports to the US fell a large 29% y/o/y but more than offset by a 15% increase in exports to the EU, a 27% jump to Africa, an 8.2% rise to Southeast Asia and a 36% spike to Australia. Their overall trade surplus is now over $1 trillion this year year-to-date thru November.

Negatives,

1) The Fed cut interest rates even with inflation still well above 2%, both absolutely and on a sustainable basis. Inflation is the disease, the slowing pace of hiring is the symptom. QE, not QE!? Isn’t there another way of managing liquidity issues than having the Fed step in AGAIN to grease the wheels? Long term interest rates rise in response to the cut and go up around the world too.

2) Initial jobless claims for the week ended 12/6 totaled 236k, 16k more than expected and now we can smooth out all the holiday distortions which seasonal adjustments have a hard time with around Thanksgiving. The 4 week average is 217k vs 215k last week but down from 224k in the week before that.

3) In the JOLTS report, the hiring rate remained subdued at just 3.2% which matches the lowest level since January 2011 not including Covid. As part of this, the number of layoffs touched its most since January 2023. Also of note, the quit rate slipped to 1.8% from 2%, and that is the lowest since January 2014, also not including Covid as less people are willing to jump ship to another job.

4) In the November NFIB Small Business Optimism index there was a 13 pt spike in ‘Higher Selling Prices’ to 34%, the highest since March 2023 and the biggest one month percentage increase on record. The Quality of Labor still remains the biggest business problem at 21% but down 6 pts and the Inflation worry rose 3 pts to 15%.

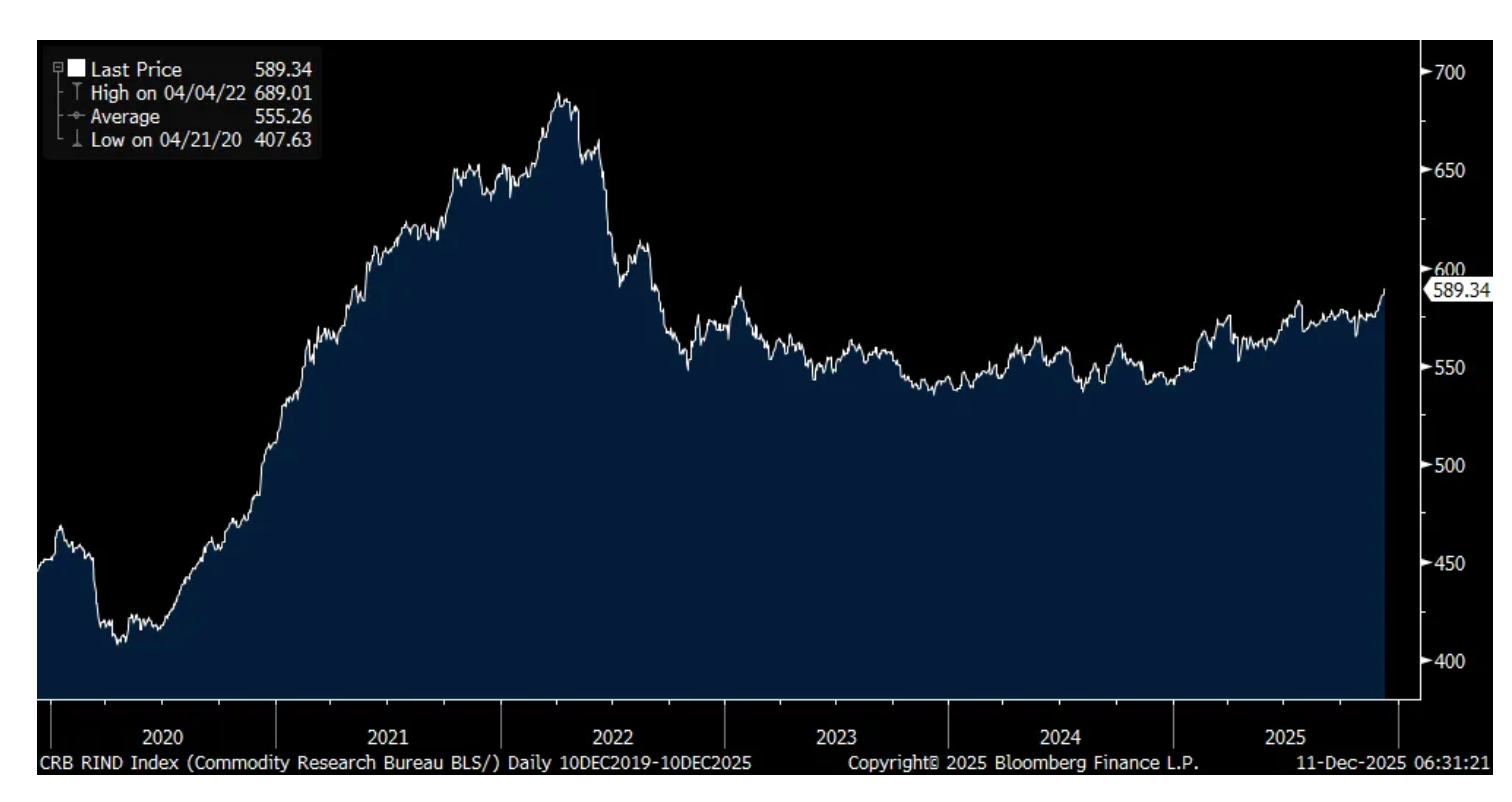

5) The CRB raw industrials index touches the highest level since August 2022.

6) Coming out of the holiday, the MBA said purchase applications fell 2.4% w/o/w after rising by a like amount last week.

7) From the NY Fed’s Consumer Expectations survey, “Perceptions about households’ current financial situations compared to a year ago deteriorated notably with a larger share of respondents reporting that their households were worse off compared to a year ago, and a smaller share reporting they were better off. Expectations about year-ahead financial situations also deteriorated slightly with a smaller share of respondents reporting that their households are expecting to be better off a year from now.”

8) From RH: While certainly positive long term about his business, “there is no denying what an unusual time it is in our industry. And we also believe it’s not a time to underestimate risk. We’re in the third year of the worst housing market in almost 50 years. In 1978, there were 4.09 million existing homes sold in the US when the US had a population of 223 million people. We are on track to average 4.07 million existing homes sold over the three years from 2023 to 2025 with a population of 341 million or 53% higher than 1978. This is a market we’ve never seen before…Not a time to underestimate risk. Tariffs are disrupting supply chains and driving higher prices. There have been 16 different tariff announcements over the past 10 months that have resulted in significant resourcing, product delays, out of stocks and driven multiple rounds of price negotiations and increases.”

9) From Lululemon: “in terms of trading down, we’ve seen a bit of that behavior throughout the year. I’ve talked about the uncertain behavior of the consumer we’re seeing. We’re seeing a little bit in terms of how they’re responding to the promotional activity in the marketplace today and they’re definitely looking for ways in which they can save and value. And it’s behavior we’ve seen throughout the year and continued into Q3.”

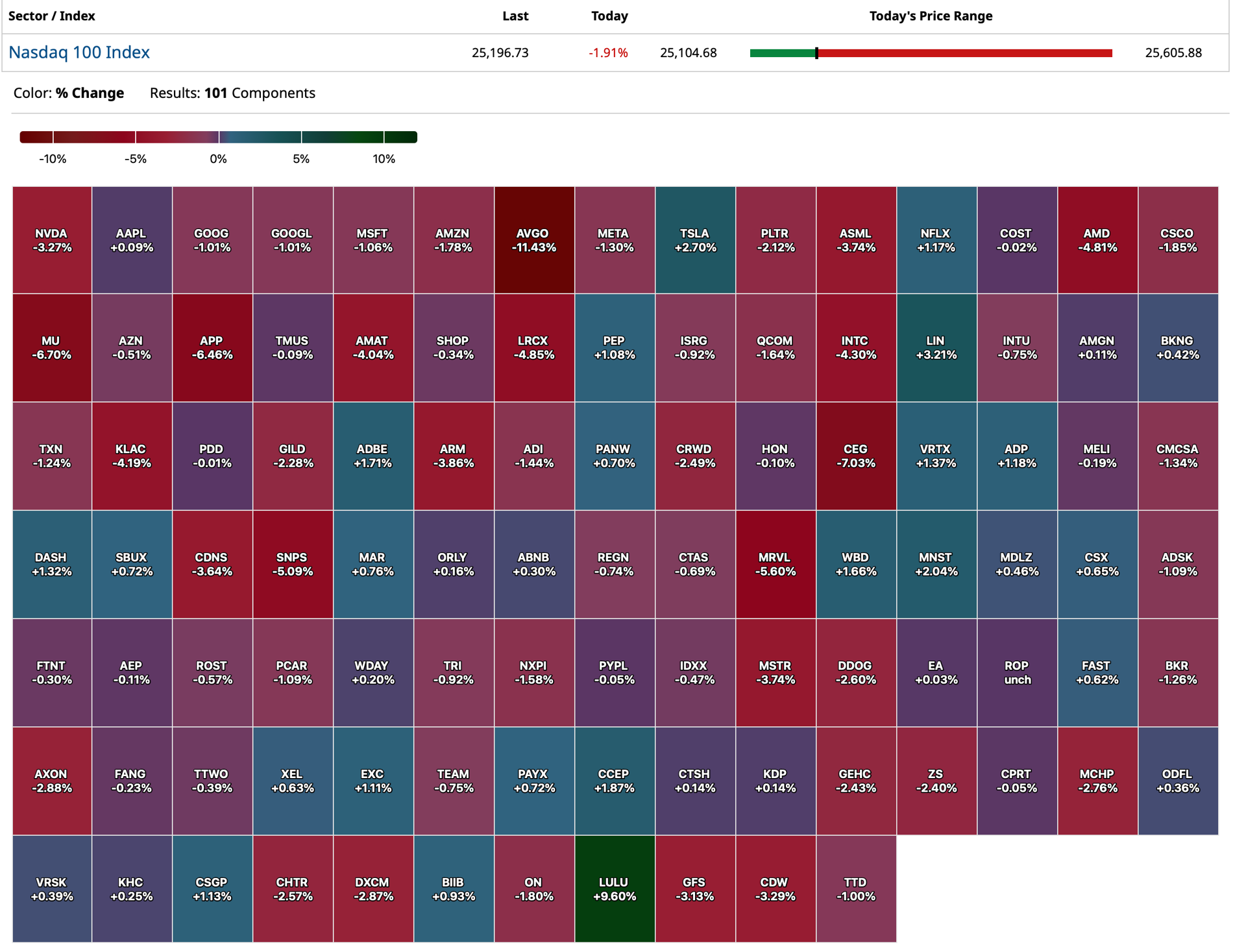

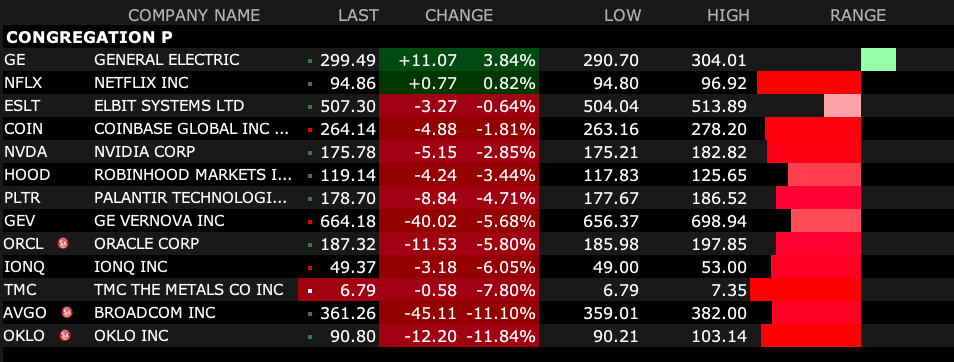

10) From Broadcom: Another sign that the GenAI tech trade is tiring out. With respect to AI revenue guidance for next year, it’s a “moving target” and “It’s hard for me to pinpoint what ‘26 is going to look like precisely. So I’d rather not give you guys any guidance.”

11) From Toll Brothers: “Given soft demand across many markets, we remain focused on running our business in a disciplined manner and consistent with our long-term strategic objective of maximizing returns for stockholders.”

12) From JP Morgan: “But it is also true that retailers and restaurants are seeing people be more discerning, trading down a little, being more promotion aware, because they have to be in order to bring those things back into balance. And so the good news is that so far, even our lower income customers are continuing to tread water and stability is more of the narrative than sort of deterioration or anything else.” And this, “there’s less capacity to weather an incremental stress, because cash buffers have normalized. And price levels absolutely are high, even as inflation has come down at least. So I would just say that I would characterize the environment as being a little bit more fragile. And as the labor market goes, typically, so will consumers. Our outlook for next year would be for unemployment to grind a little higher, and therefore, that to be reflected in consumption. And from there, it will depend.”

13) For their balance sheet and exposure, Oracle raised their fiscal year ’26 CapEx forecast to $50 billion which is a whopping 75% of expected revenue.

14) The UK economy unexpectedly contracted in October by one tenth m/o/m vs the estimate of up one tenth. Weakness in construction, services and manufacturing were the main factors.

15) The December Sentix Investor Confidence index was -6.2, though up from -7.4 in November. Sentix said “The Eurozone economy remains in a phase of stagnation.” They said the German economy in particular “remains firmly in the grip of recession.”

16) China CPI in November ex food and energy rose 1.2% y/o/y, holding at its quickest pace since last year, though quite stable and low. PPI fell 2.2% y/o/y, with continued pressure due to the ‘involution’ issues they are facing.