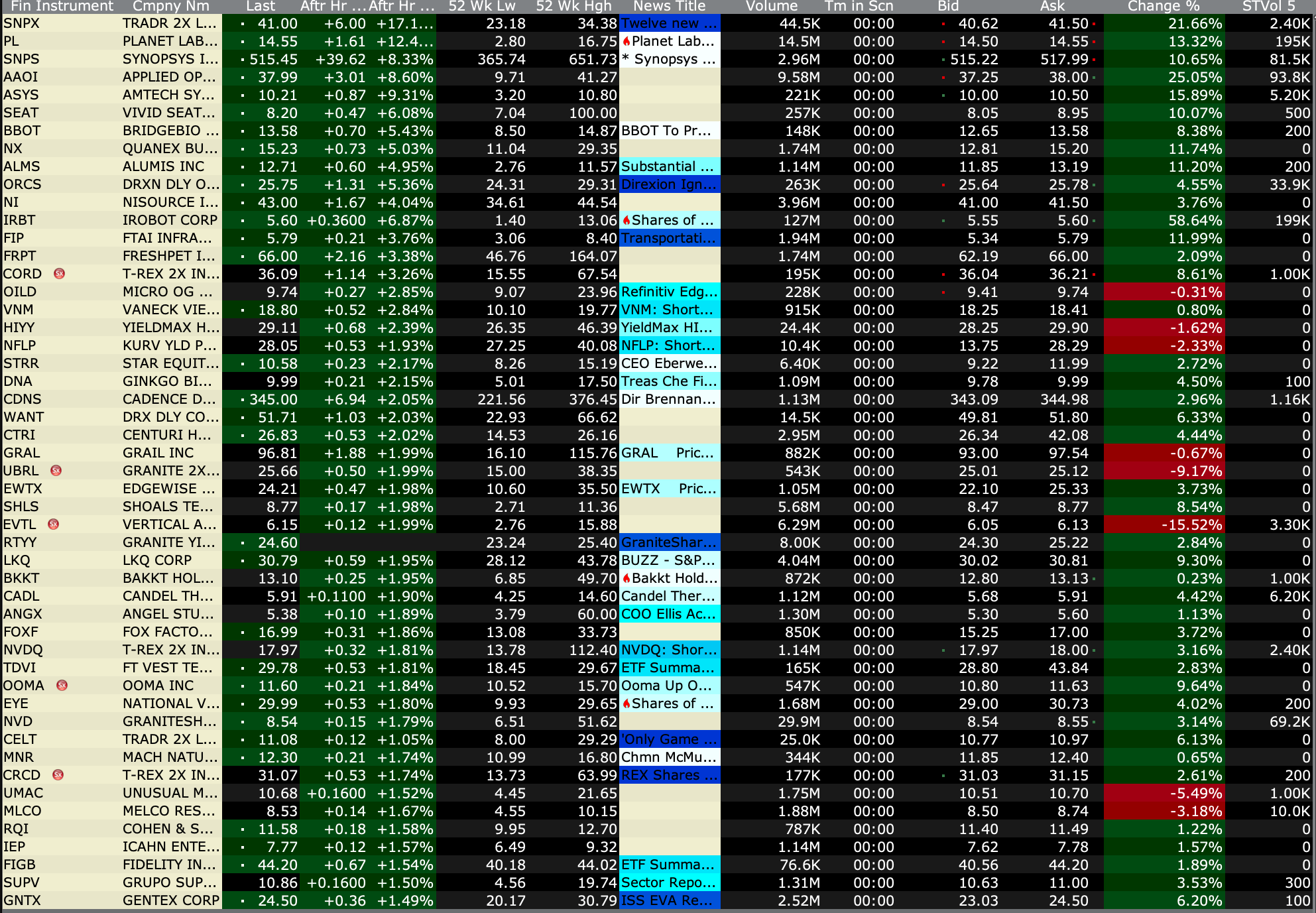

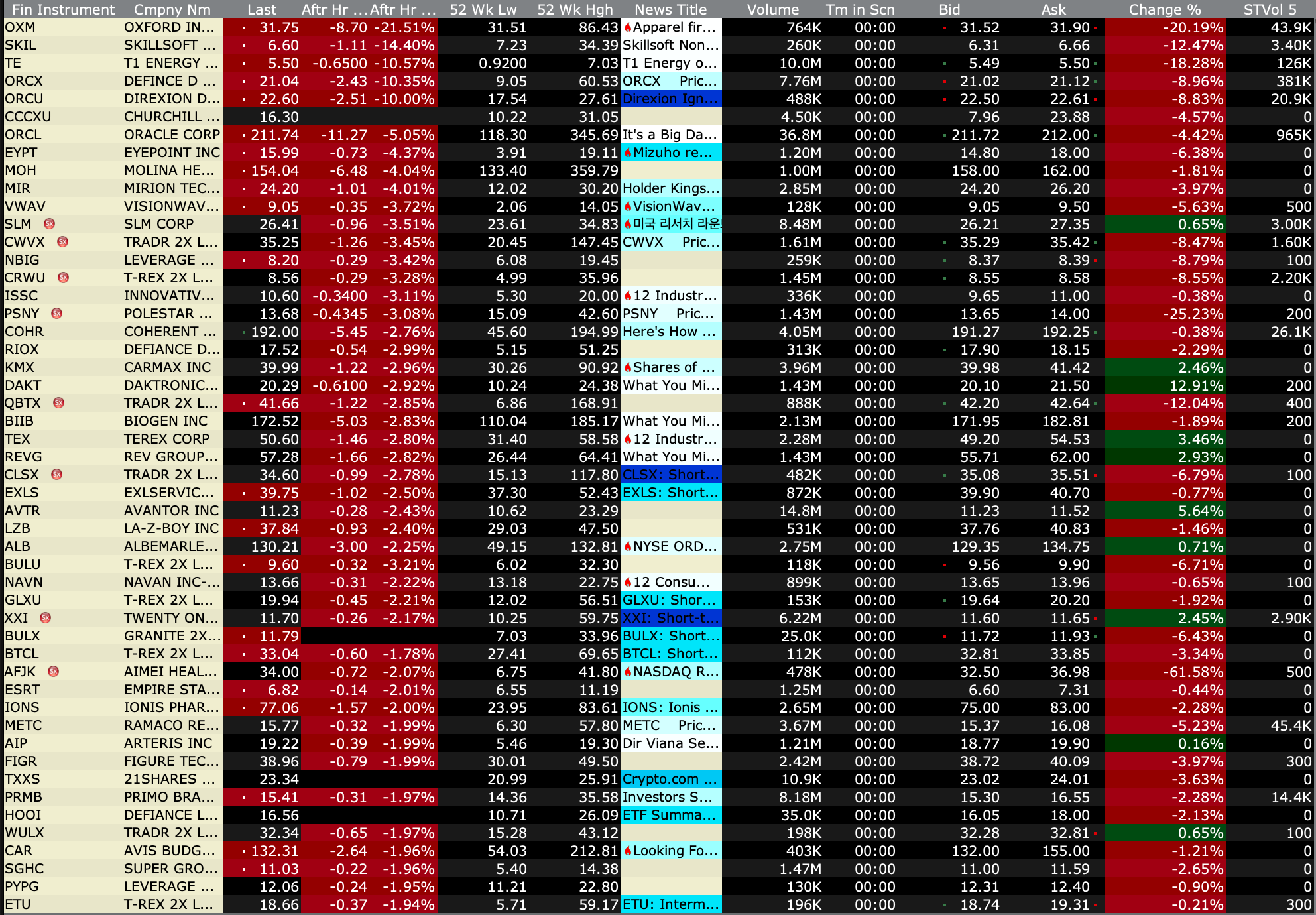

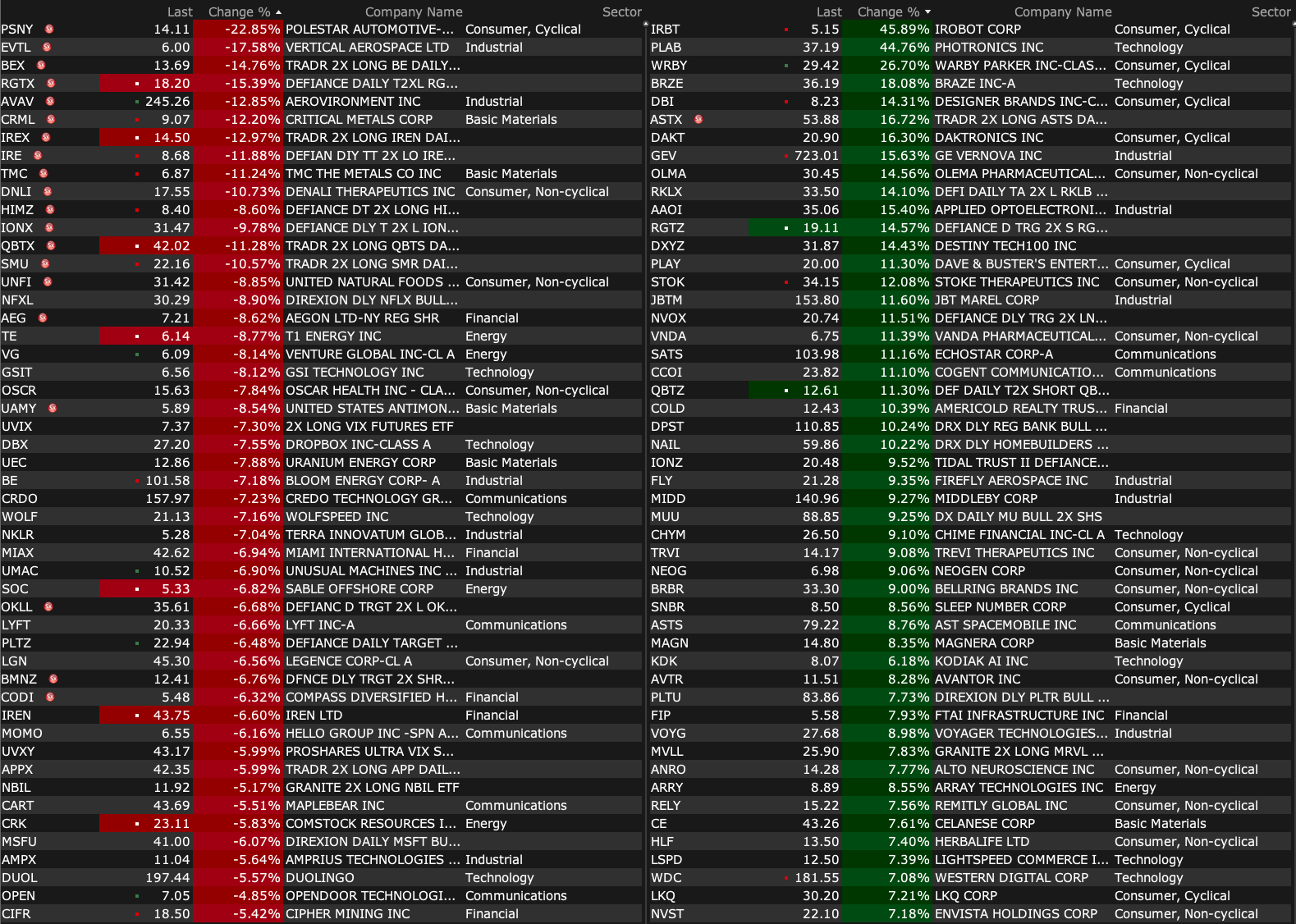

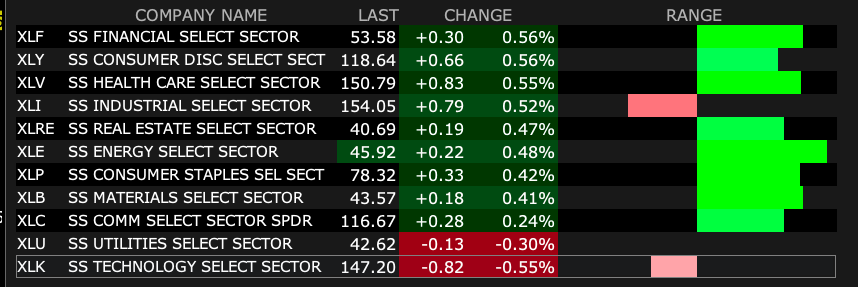

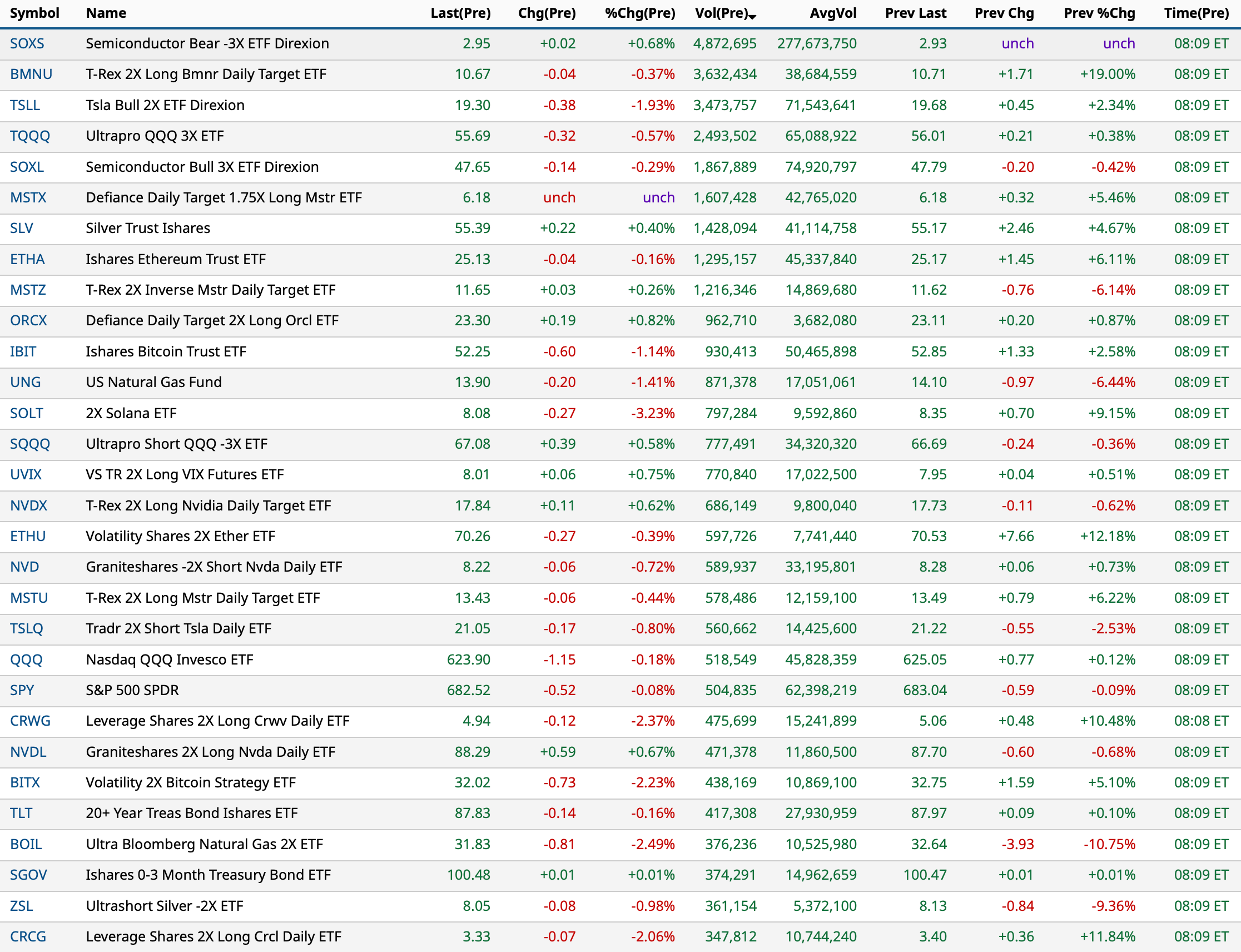

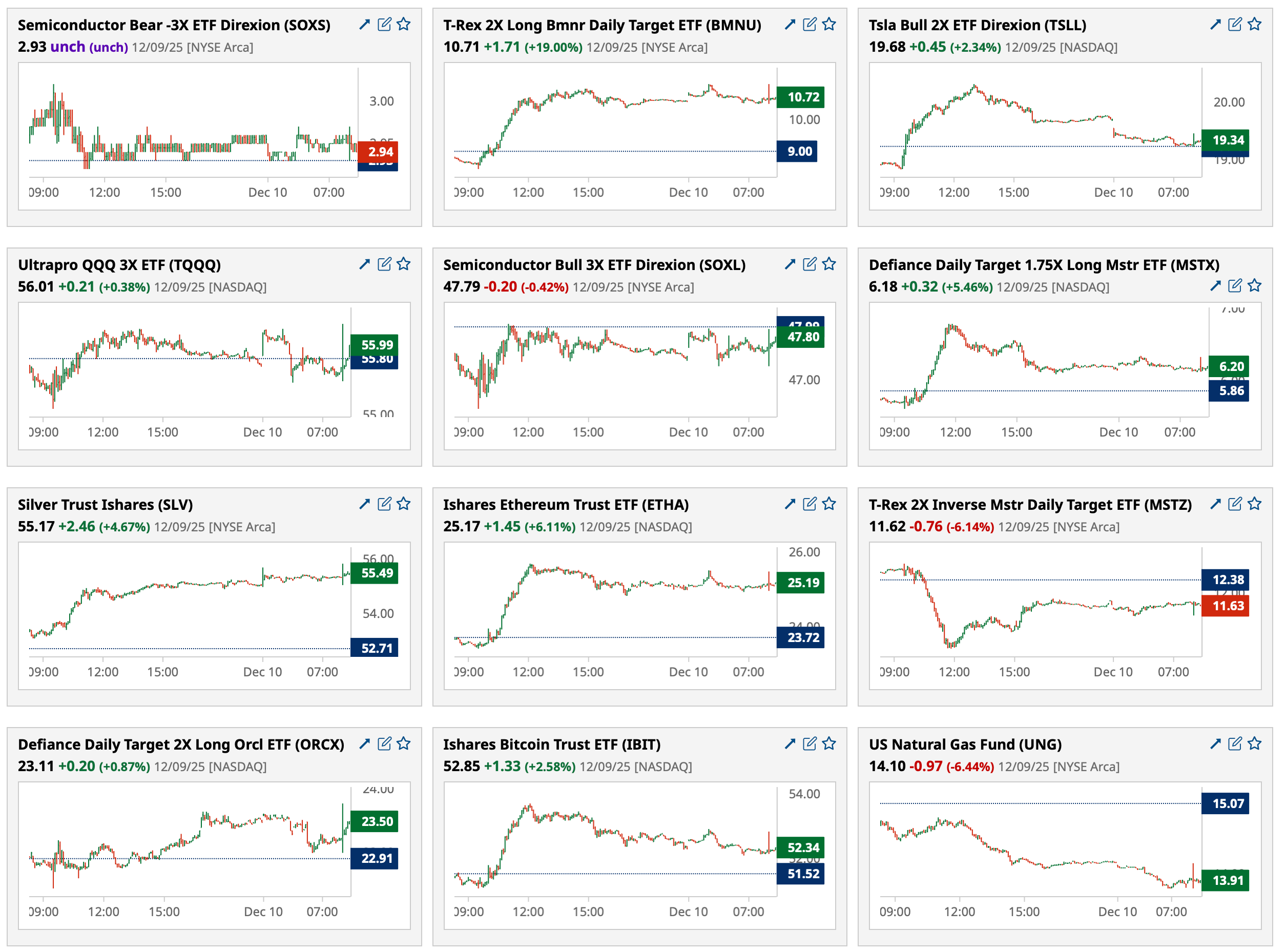

After-Hours Gainers and Losers

After-Hours Gainers (%)

After Hours Losers (%)

BY Doug Kass · Dec 10, 2025, 4:40 PM EST

BY Doug Kass · Dec 10, 2025, 4:40 PM EST

- NYSE volume 2% below its one-month average;

- NASDAQ volume 14% below its one-month average;

- VIX index: down 6.08% to 15.90

BY Doug Kass · Dec 10, 2025, 4:26 PM EST

Thanks for reading my Diary today.

I am stepping out early as I have a trip in front of me.

I will see everyone bright and early on Friday morning.

Enjoy the evening.

Be safe.

BY Doug Kass · Dec 10, 2025, 3:50 PM EST

I re-shorted index calls with S&P cash +51 handles.

But baby steps.

I am now a scale seller.

BY Doug Kass · Dec 10, 2025, 3:05 PM EST

(META) and (MSFT) are trading well below my recent long sales.

I am bidding under the market for both.

BY Doug Kass · Dec 10, 2025, 2:54 PM EST

I have covered my (SPY) and (QQQ) common and calls for a small gain:

* (SPY) $684.18

* (QQQ) $623.44

BY Doug Kass · Dec 10, 2025, 2:48 PM EST

From Peter Boockvar:

With not much to go by hard data wise in the initial paragraph on the economy, the Fed repeated that “economic activity has been expanding at a moderate pace.” They only have jobs data from the BLS thru September and said “the unemployment rate has edged up” as of then and “More recent indicators are consistent with these developments.” They repeated that “Inflation has moved up since earlier in the year and remains somewhat elevated.”

Everything else in the statement was the same seen in September, thus leaving the presser open to new insight from Powell.

Miran again wanted a 50 bps cut and Schmid dissented again against any cut, now joined by Austen Goolsbee. Susan Collins gave in, as did Alberto Musalem and voted for a cut even though they both hinted a few weeks ago that they wanted to sit tight.

With respect to the dots, the REAL rate long term expectation remained at 1% and they are now slightly below that. They tweaked down by one tenth their 2025 inflation forecast to 2.9% headline and 3% core vs 2.8% for each seen for September’s data. With next year, the dots only show one more cut to a median of 3.4%, coincident with their 2.4% PCE forecast headline and 2.5% core, thus holding to the 1% REAL rate. They also raised their 2026 GDP forecast to 2.3% while keeping their unemployment rate estimate at 4.4%.

Lastly, the Fed will step up their purchases of T-bills “and if needed, other Treasury securities with remaining maturities of 3 years or less to maintain an ample level of reserves.” No, this is NOT QE but I’m not clear on why the Fed is doing this, outside of just naturally growing the balance sheet in line with nominal GDP.

Bottom line, while we knew exactly what the Fed was going to do because John Williams told us, it still is a very tricky time for the Fed in balancing their two mandates especially I would argue where they are still missing on one (inflation) which is resulting in softness in the other. The difficulty of having a dual focus. As long as Powell is Fed chair I’ll say again that I think he’s done cutting rates UNLESS inflation decelerates from here and/or unemployment takes another leg higher. Once he’s gone, of course all bets are off.

And, either way, the long end will have its say. In response to the T-bill purchase news, the 2 yr yield is down 2.5 bps but the 10 yr yield is unchanged and the 30 yr yield is up 1.5 bps post statement. We just got lower interest rates but only on the very short end, again.

BY Doug Kass · Dec 10, 2025, 2:45 PM EST

I have a 2:45 PM research call.

It should take about an hour.

BY Doug Kass · Dec 10, 2025, 2:40 PM EST

I'm adding to individual short names with S&P cash +19 handles.

BY Doug Kass · Dec 10, 2025, 2:26 PM EST

With S&P cash +22 handles, I am adding to my short index calls.

BY Doug Kass · Dec 10, 2025, 2:17 PM EST

With S&P cash now +26 handles, I'm adding to index shorts:

* (SPY) $685.45

* (QQQ) $625.88

BY Doug Kass · Dec 10, 2025, 2:14 PM EST

With S&P cash +12 handles I am re-shorting index common:

* (SPY) $684.40

* (QQQ) $624.63

BY Doug Kass · Dec 10, 2025, 2:07 PM EST

PepsiCo (PEP) is trading +$4.55 to $149.20 on a JPMorgan upgrade. We purchased stock as low as $144 yesterday.

I am taking in some premium and locking in some gains and I am selling some January calls against my core long investment holding in the name.

BY Doug Kass · Dec 10, 2025, 1:00 PM EST

BY Doug Kass · Dec 10, 2025, 12:45 PM EST

BY Doug Kass · Dec 10, 2025, 12:30 PM EST

BY Doug Kass · Dec 10, 2025, 12:00 PM EST

PepsiCo (PEP) is trading over $149 (+$4.40).

BY Doug Kass · Dec 10, 2025, 11:45 AM EST

With S&P cash now +6 handles I am selling (very very small) index calls.

I have no plans to do anything "radical" before the Fed rate cut this afternoon.

BY Doug Kass · Dec 10, 2025, 11:32 AM EST

- NYSE volume 18% below its one-month average;

- Nasdaq volume 33% below its one-month average; -

- VIX index: up 0.71% to 17.05

BY Doug Kass · Dec 10, 2025, 11:20 AM EST

I covered my premarket index common shorts for a quick gain:

* (SPY) $681.61

* (QQQ) $622.01

I will reshort on strength.

From earlier:

I am back shorting the Index common:

* (SPY) $683.43

* (QQQ) $624.97

Position: Short SPY common S QQQ common S

By Doug KassDec 10, 2025 8:37 AM EST

BY Doug Kass · Dec 10, 2025, 9:44 AM EST

Modifying the last "More Tales" (Issue #163) Doug's Daily Diary - TheStreet Pro....

This one from Gary Marcus' Substack is interesting as well: Has the Chinese Government Figured out the Fact That GPUs ≠ AGI?

The key line in the substack:

“But maybe, maybe, just maybe, China’s reticence to stock up on H200s is also a sign that China has realized that GPU’s aren’t the royal road to AGI. And realized that loading up on AI infrastructure that is likely to rapidly depreciate might be premature — and not the massive competitive or economic advantage many once people thought it was. The first country to really appreciate all this may get a huge competitive advantage, in whatever comes next, after LLMs.”

So, maybe China doesn’t care about getting Nvidia (NVDA) parts all of a sudden, because the Chinese have figured out Generative AI isn’t all it is cracked up to be and no longer view it as a national security priority and the road to future prosperity. Maybe instead China is directing its efforts toward alternative approaches that are in a development phase that will require different architectures. Therefore, China just does not care about unfettered access to current NVDA parts, because generative AI is a commodity product, and it is really about being the low-cost provider as opposed to having the latest and greatest silicon (which is increasingly non-differentiated anyway).

The other interesting thing in the article is the interview the author, Gary Marcus, did with the Conservative Review, which is part of The Blaze. This is one of the more conservative media organizations out there. The author interestingly is liberal. In a world where nobody agrees on anything, both the interviewer and the interviewee are quite united in their disdain for what is going on with generative AI, and U.S. policy in this regard. As I have said before, distaste for AI is seemingly the only thing that both the left and the right agree on.

It is a political loser. Yet the current administration continues to favor and support/promote it in almost unprecedented fashion, despite all of its issues (dis-economic, power bills, not working like it was meant to, and generally hated by everyone). Why? Once again, I think two issues:

* The overwhelming influence of the technocrats, who want socialism for the wealthy to help bail them out of the ka-jillions that have wrongly bet at absurd valuations.

* The current administration's realization that the AI trade is what has propped up the stock market and policy is really about keeping the stock market supported as opposed to national security or anything of that ilk, which by definition is also socialism for the technocrats.

BY Doug Kass · Dec 10, 2025, 9:30 AM EST

BY Doug Kass · Dec 10, 2025, 9:20 AM EST

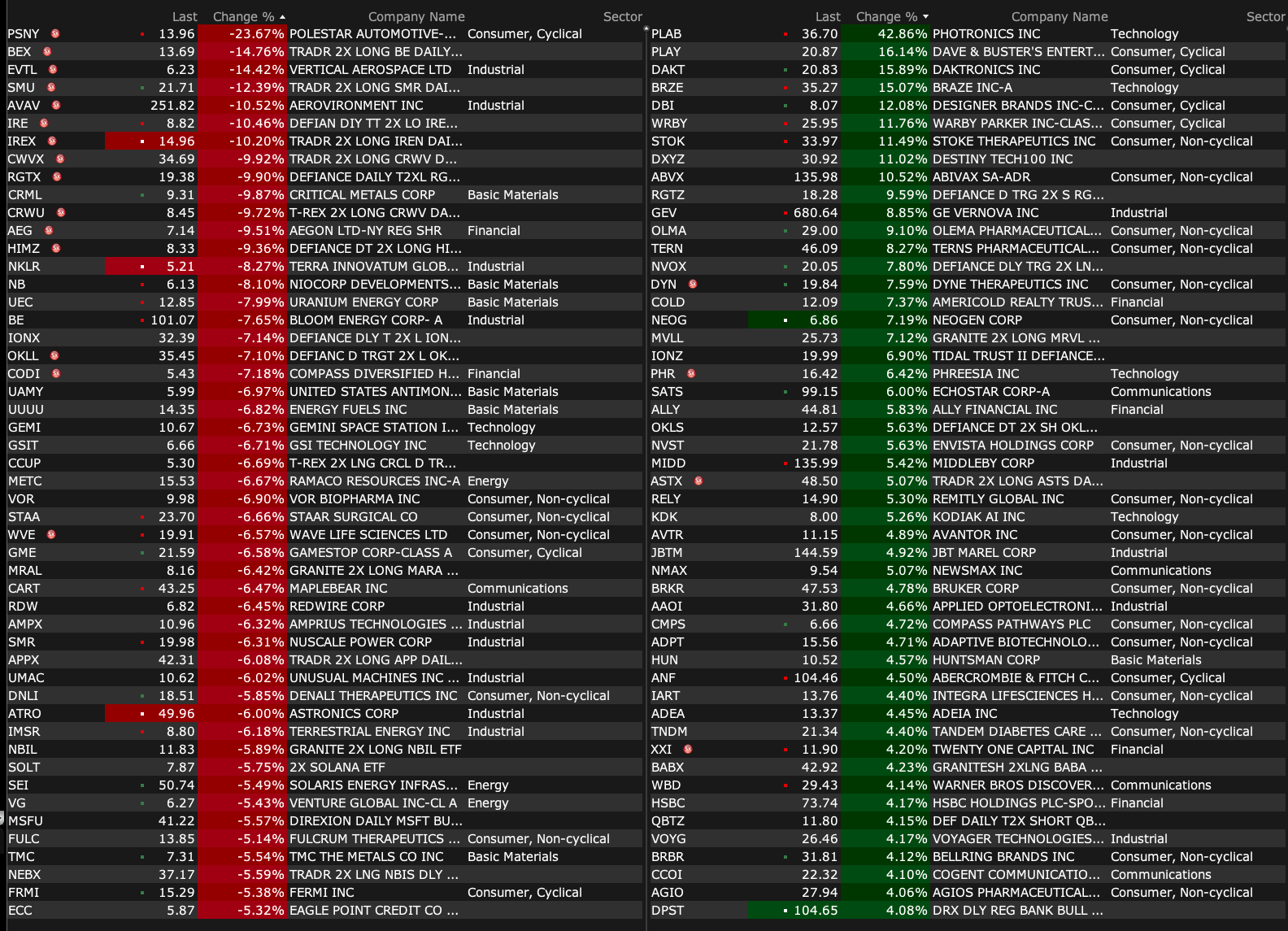

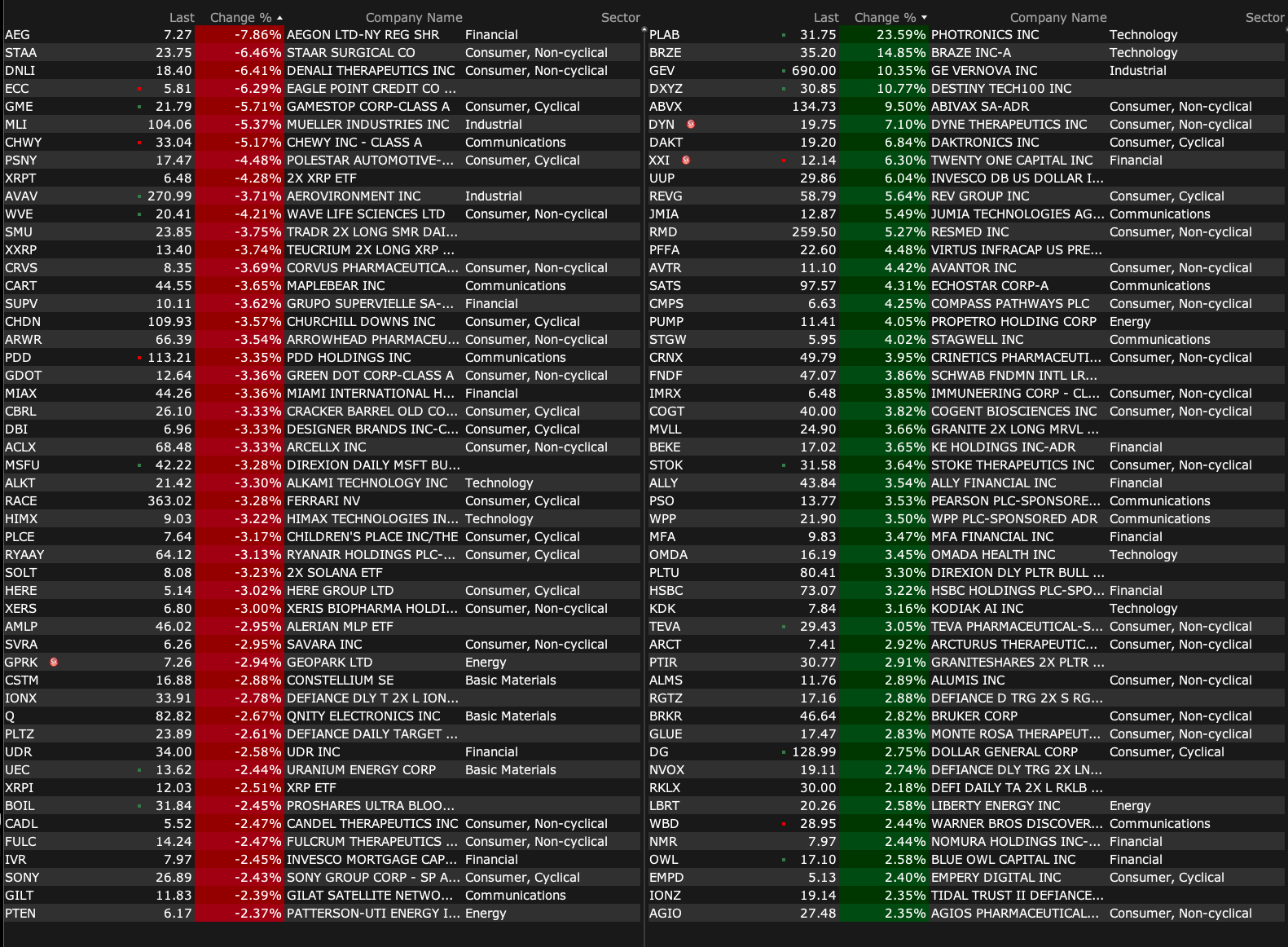

-PLAB +22% (earnings, guidance)

-BRZE +15% (earnings, guidance)

-ALOT +14% (earnings, guidance)

-DAKT +11% (earnings; increases share buyback authorization by $20M)

-GEV +10% (issues initial FY26 guidance; raises dividend)

-AOUT +7.0% (earnings, guidance)

-USAR +6.3% (accelerates timeline for round top deposit commercial production by two years)

-REVG +4.6% (earnings)

-ALLY +3.8% (announces $2.0B share repurchase program)

-DYN +3.8% (Oppenheimer Raised DYN to Outperform from Perform, price target: $40 from $11; prices 19.0M shares at $18.44/share)

-VBNK +3.7% (earnings)

-SATS +3.6% (Morgan Stanley Raised SATS to Overweight from Equal Weight, price target: $110 from $82)

-MODD -25% (prices $4.68M underwritten public offering)

-AGRO -8.8% (files to sell $300M common stock offering)

-AEG -7.8% (announces share buyback and guidance along with new strategic objectives)

-JILL -6.1% (earnings, guidance)

-GME -5.9% (earnings)

-CBRL -4.8% (earnings, guidance)

-AVAV -4.3% (earnings, guidance)

-UEC -3.9% (earnings)

BY Doug Kass · Dec 10, 2025, 9:10 AM EST

Jrlee

1 minute ago

Higher prices should be laid at the feet of Team Red and Team Blue as Trillions of deficit spending are monetized resulting in steady erosion of our money. All DC dwellers contribute to this mess. Congress spends like there is no problem with the constant

Decline in the value of money. Both parties live in a never never land of elitism.

BY Doug Kass · Dec 10, 2025, 9:05 AM EST

11:30 a.m.: Treasury hosts a $69B 17-Week Bill Auction

BY Doug Kass · Dec 10, 2025, 8:55 AM EST

BY Doug Kass · Dec 10, 2025, 8:40 AM EST

I am back shorting the Index common:

* (SPY) $683.43

* (QQQ) $624.97

BY Doug Kass · Dec 10, 2025, 8:37 AM EST

From Peter Boockvar:

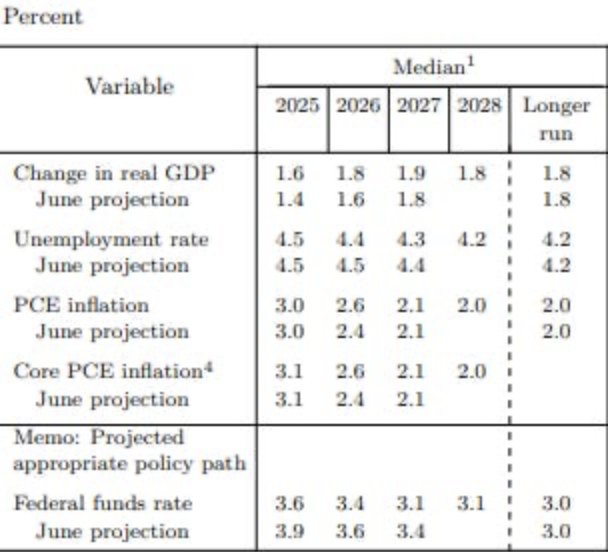

Here is the dot plot from the September meeting and as we haven’t seen much government data since, assume today it won’t be much different. So, off the 2.8% September PCE seen last week, the fed funds rate after today’s cut will be less than 1% on a REAL basis, below the ‘longer run’ median view, at the same time the unemployment rate is around the Fed’s year end forecast. Thus, I continue to believe that Jay Powell will tell us today that what would need to be triggered in order to get another rate cut or two in his last three meetings as Chair will have to be another deceleration in inflation and/or a further rise in the unemployment rate. If it happens, he’ll cut again. If it doesn’t, he won’t. And then of course we’ll have a whole different playbook with the next Fed Chair, though they will have to still extend hands to his and her colleagues who might not agree.

Either way, Fed policy with the short end will still have to contend with where the market wants to price the longer end (10 yr yield today at 4.20%) because the former has much less influence on the latter right now as seen. And I’ll argue again, inflation is the disease in the economy, both for households and the cost pressures that many small and medium sized businesses are facing. The softer labor market is the symptom. I believe in fully treating the disease because if successful, the symptoms go away.

Lastly on this and the economic downside of rate cuts, for those savers out there, you’re about to get clipped by another 25 bps on your interest income and by 175 bps since last September.

This is what was said by Marianne Lake yesterday, the CEO of Consumer & Community Banking at JP Morgan which precipitated the fall in the stock and which comes across as a mixed read on things:

“the consumer and small businesses both continue to be resilient. They continue to be healthy. The metrics continue to demonstrate that whether it’s cash buffers which have normalized but are also stable, whether it’s credit metrics, really across asset classes, spend trends, payment rates, the metrics themselves are underlying really quite healthy.”

“And so as I think about the concerns that people are worried about, they’re also true, right? It is also true that the labor market and demand for labor is weakening. It is true that consumer sentiment is quite low and the absolute price levels are high. It is true that auto, subprime auto delinquencies have been high through the pandemic, even as they are improving, and that has caused concern.”

“But I think the thing to remember is that we’ve been talking for the last three years about the fact that cash buffers are normalizing. And what that means, like mathematically, is that people have been spending more than they have been bringing in for some period of time. And so when you reach the point of normal, right, when you get back to the levels of cash that is required for people to sort of maintain, then it requires there to be adjustments to spending patterns. And so it is not entirely inconsistent to be able to say that people are still treading water, that the cash buffers are stable and that spend is still solid.”

“But it is also true that retailers and restaurants are seeing people be more discerning, trading down a little, being more promotion aware, because they have to be in order to bring those things back into balance. And so the good news is that so far, even our lower income customers are continuing to tread water and stability is more of the narrative than sort of deterioration or anything else.”

And finally with this, “there’s less capacity to weather an incremental stress, because cash buffers have normalized. And price levels absolutely are high, even as inflation has come down at least. So I would just say that I would characterize the environment as being a little bit more fragile. And as the labor market goes, typically, so will consumers. Our outlook for next year would be for unemployment to grind a little higher, and therefore, that to be reflected in consumption. And from there, it will depend.”

On credit quality, “credit trends in the card business look pretty good right now. And I always want to touch on wood, but I won’t do that. And then auto is another one where there is a lot of anxiety about auto delinquencies, subprime auto delinquencies. And there were across the industry a couple of pretty negatively selected vintages in ‘22 and ‘23...And so as we look at the vintage performance, you’re seeing the ‘22 and ‘23 vintages now normalized. The ‘24 and ‘25 vintages are looking much more normal.”

They expect this year’s charge off rate to be 3.3% which would be better than the 3.6% expectations they entered the year with as “charge-offs are stable and modestly improving.” They expect it to rise though to 3.6% to 3.9% in 2026 but of course all depending on how the macro plays out.

Casey’s General Store has been an incredible growth story, quite a stock and always a helpful view on the consumer, all income cohorts. They reported last night, with a call this morning, and said this in their earnings release of note:

Inside comps rose 3.3% (thus ex fuel) and “Casey’s delivered a great second quarter highlighted by strong sales and traffic growth across the entire store. Our inside same store sales continued the strong momentum, as our prepared foods offering and value proposition are resonating with guests.”

“Same store inside sales were driven by strong performance in the prepared food and dispensed beverage category, including whole pizzas and hot sandwiches as well as non-alcoholic beverages in the grocery and general merchandise category.”

Also in the consumer space was Auto Zone yesterday and whose stock fell 7.2%. They said this:

“Our domestic DIY same store sales growth grew 1.5%, while our domestic commercial sales grew by 14.5% vs last year’s Q1 and up sequentially from 12.5% on a 16 week basis in the fourth quarter of last year.”

With DIY and its modest comp gain, “Our merchandise categories performed as we would have expected, but less favorable weather comparisons in certain regions definitely impacted our results. More specifically, sales in the northern half of the country outperformed our markets in the southern half of the US.” They sell more parts when the weather is cold and during hurricane season, with the latter non-existent this year.

Tariffs and inflation were obvious as “we saw like-for-like same SKU inflation up approximately 4.8% for the quarter, the same with our DIY average ticket that was up 4.8%. Based on our inflation expectations, we continue to expect our average ticket to grow sequentially through the third fiscal quarter.”

The gain in commercial was self help and “continued strength of our Duralast brand” along with SKU inflation of 6% which about matched the “average ticket growth of 6.1%.”

Their comments on the US consumer now sounds very familiar. “At the end of the day, I would kind of characterize it as the lower end consumer has been under pressure for frankly quite some time. I’d say more than two years. And what I would say is they’ve been relatively stable. So there hasn’t been a significant wobble in that lower end consumer. The higher end consumer, we think, is still doing okay, and we think that’s been relatively stable over the last couple of quarters.”

From Ollie’s Bargain Outlets:

“Our comp trends since early October have been strong, and we feel great about our momentum heading into the final weeks of the holiday season.”

“Both the younger and higher income groups were the fastest growing cohorts in the quarter, which we think is in part driven by the continued reallocation of marketing dollars to digital, consumers seeking value, and customers trading down.” Something we hear more and more.

And more on this, “In terms of the state of the consumer, we’re seeing strength in the higher income consumer above $100,000 in household income. Strength in upper middle, it’s $65,000 and above. It’s solid lower middle, and we’ve seen a little bit of, I don’t know if it’s trade out or a little bit of softness in the lower income consumer, which we could potentially attribute to the government shutdown and some of the disruption that happened as a result of that. But we’re seeing on the whole that the strength of the upper middle and upper income consumer more than offsets a little bit of the weakness with that lower income consumer, and that middle has been hanging in there.”

From Campbell’s:

“Consumers remain intentional in their shopping behaviors with at-home cooking trends continuing to benefit our brands within our Meals & Beverages portfolio that deliver quality, convenience and value.”

“Our Snacks business remained under pressure as consumers continued to be increasingly intentional with their purchases.”

Coming out of the holiday, the MBA said purchase applications fell 2.4% w/o/w after rising by a like amount last week. Refi’s rebounded by 14.3% w/o/w after 5 weeks of declines.

Reflecting still robust tech shipments, Taiwan’s November exports popped by 56% y/o/y, above the estimate of 42%. Imports, much of which makes its way into eventual exports, jumped 45% y/o/y, well more than the estimate of 17%.

China CPI in November ex food and energy rose 1.2% y/o/y, holding at its quickest pace since last year, though quite stable and low. PPI fell 2.2% y/o/y, with continued pressure due to the ‘involution’ issues they are facing.

BY Doug Kass · Dec 10, 2025, 8:27 AM EST

BY Doug Kass · Dec 10, 2025, 8:20 AM EST

* But it still has a real good beat

"Dougie Kass, 14 years old. Yeah, I am from Long Island."

- American Bandstand American Bandstand - Record Review Beatle Edition

Over the last few months, the daily action has become increasingly hard to predict — in a market that has little memory from day to day.

As the contestants used to say on American Bandstand, "I like the melody of the song, but it is hard to dance to; I liked the 'B' side better."

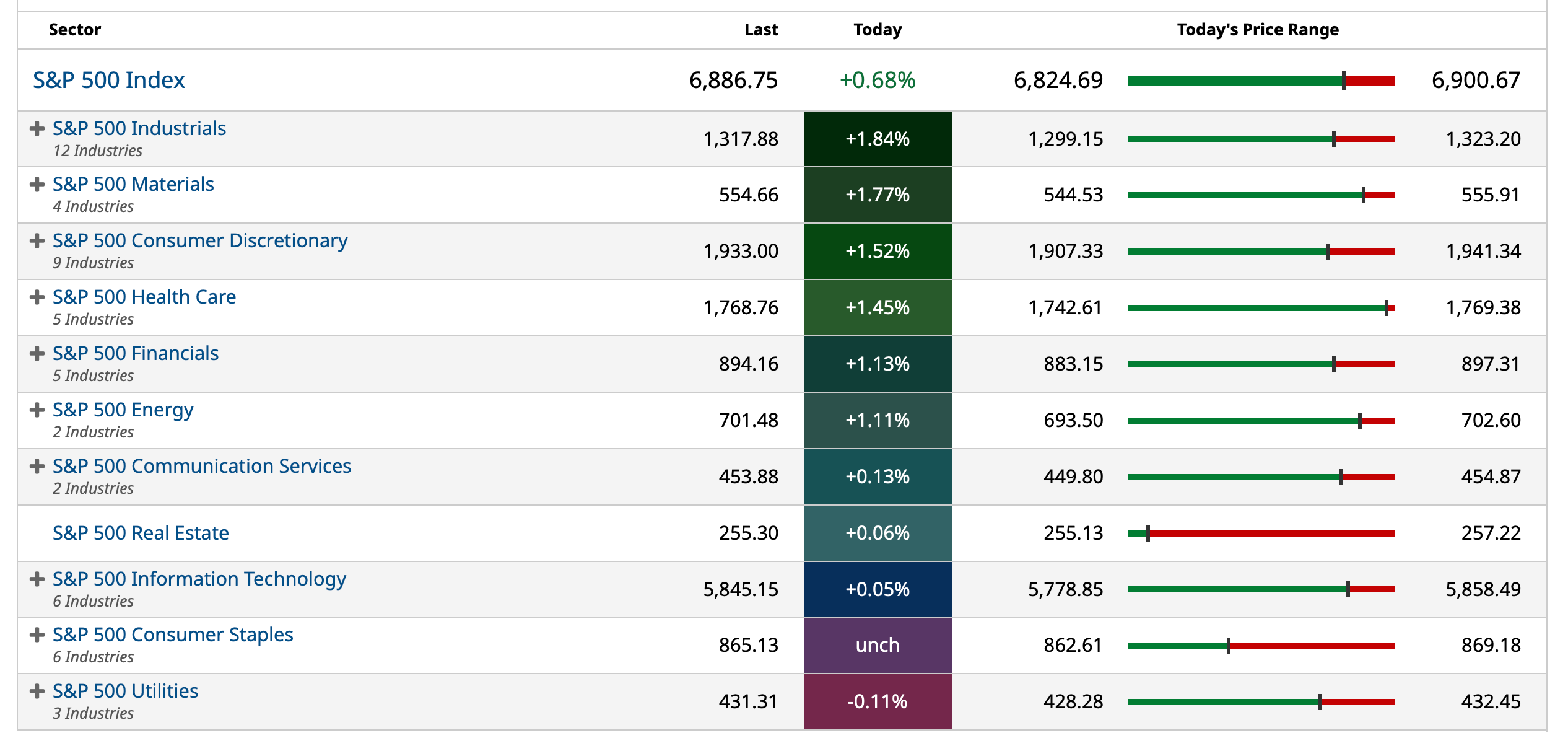

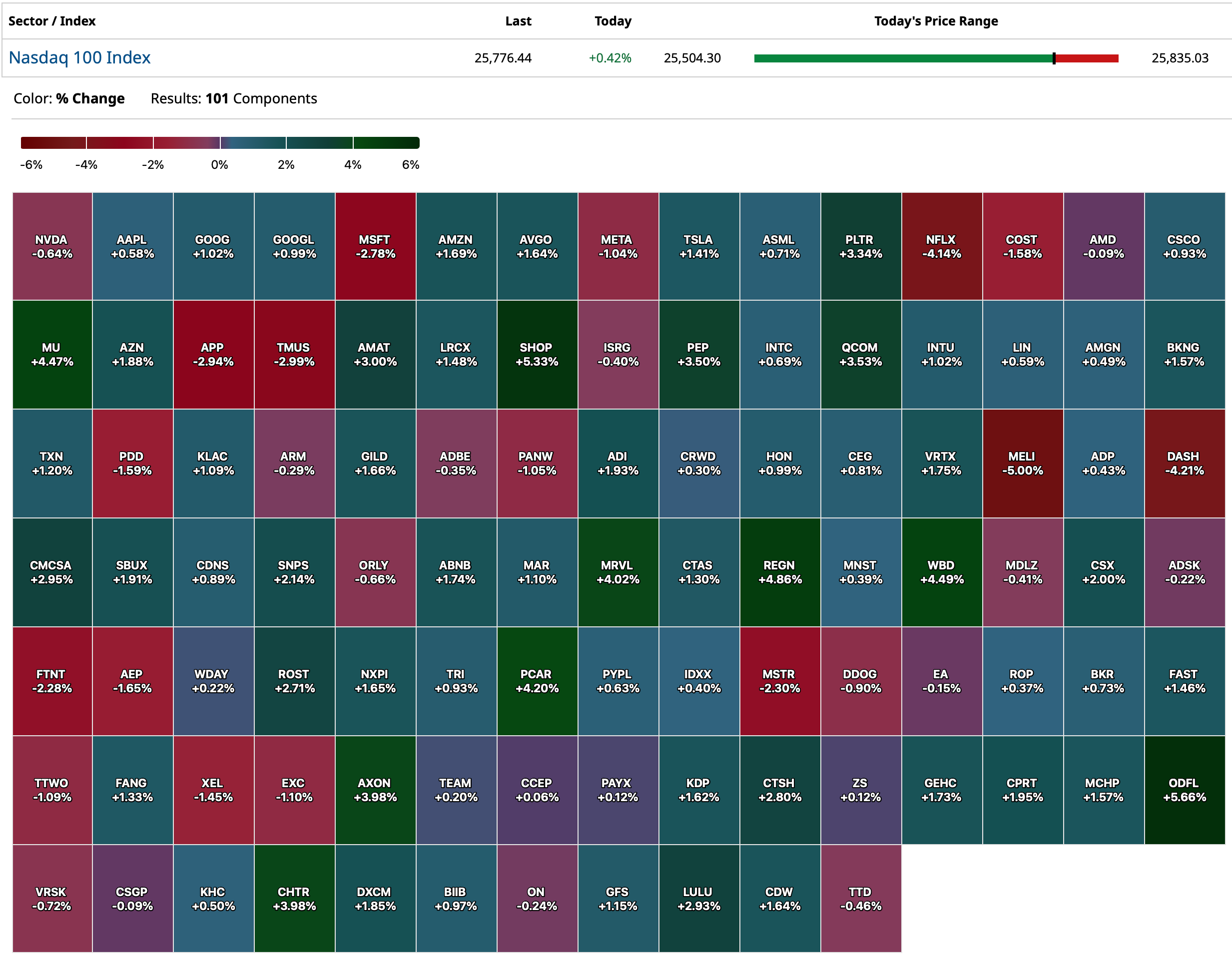

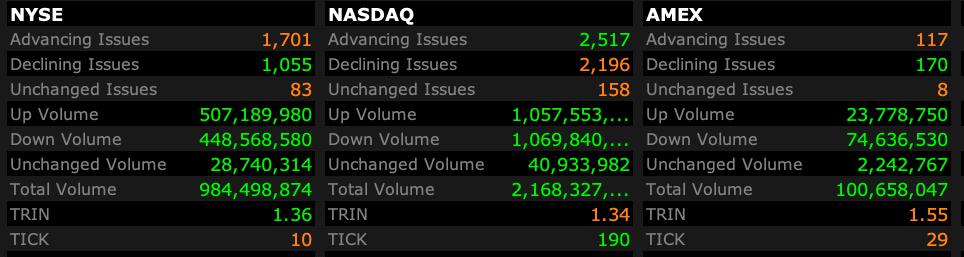

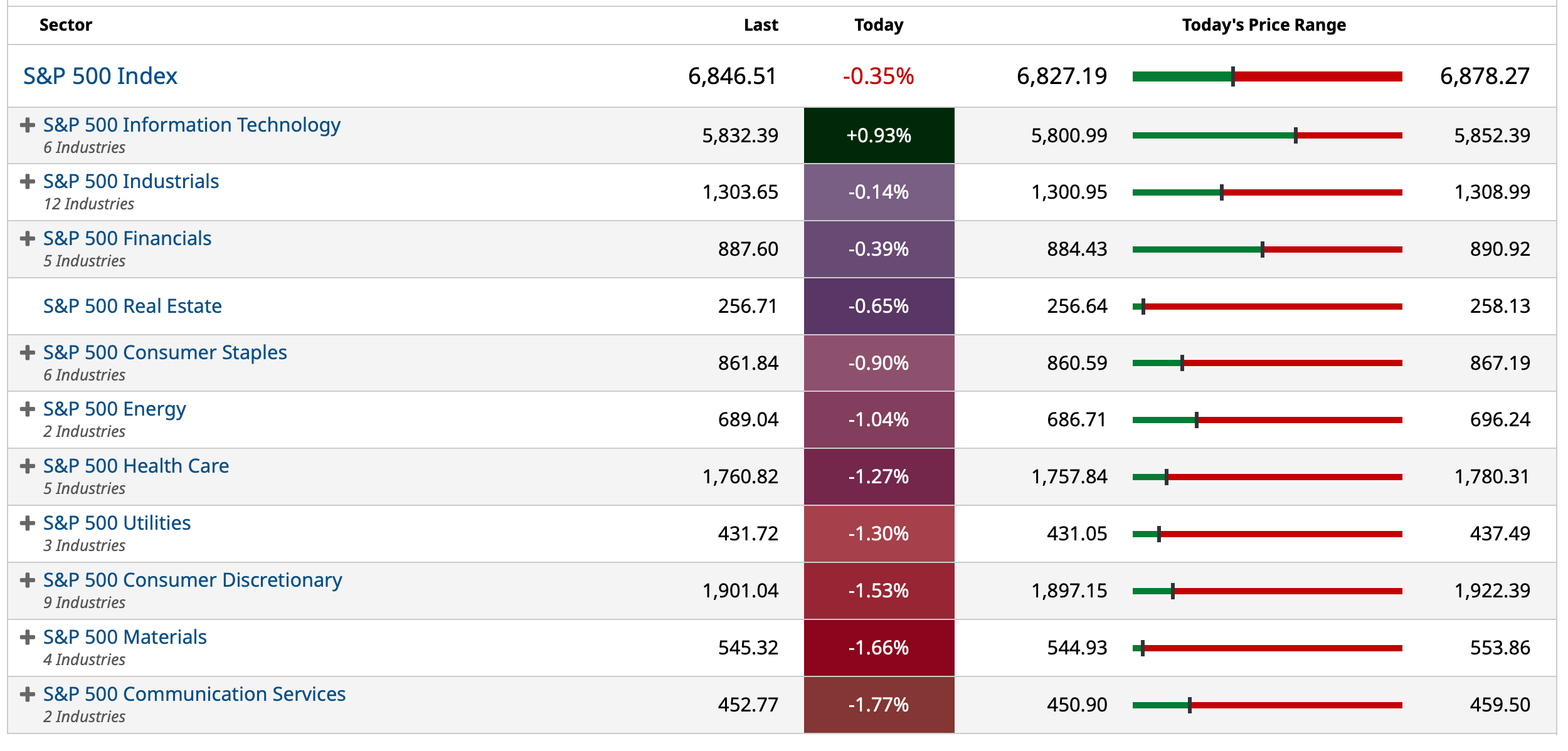

Equities were essentially flat on Tuesday:

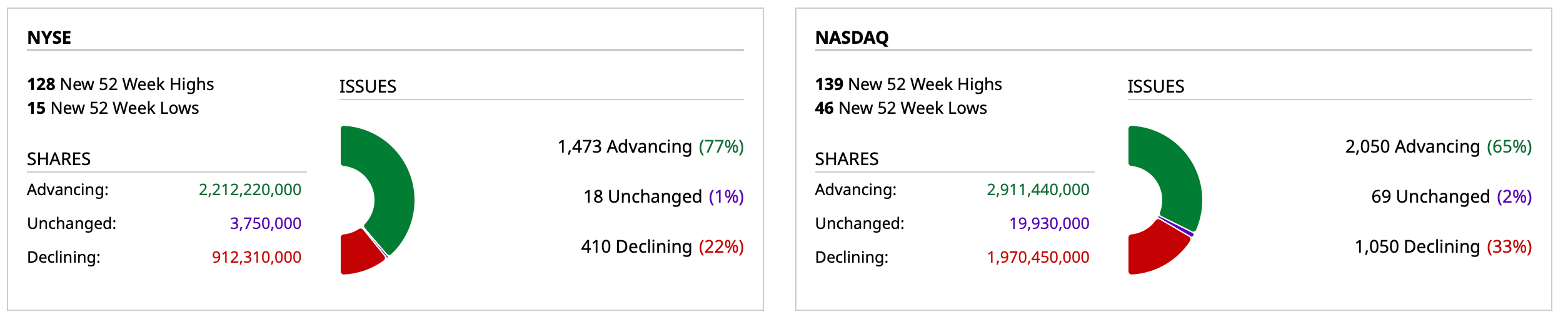

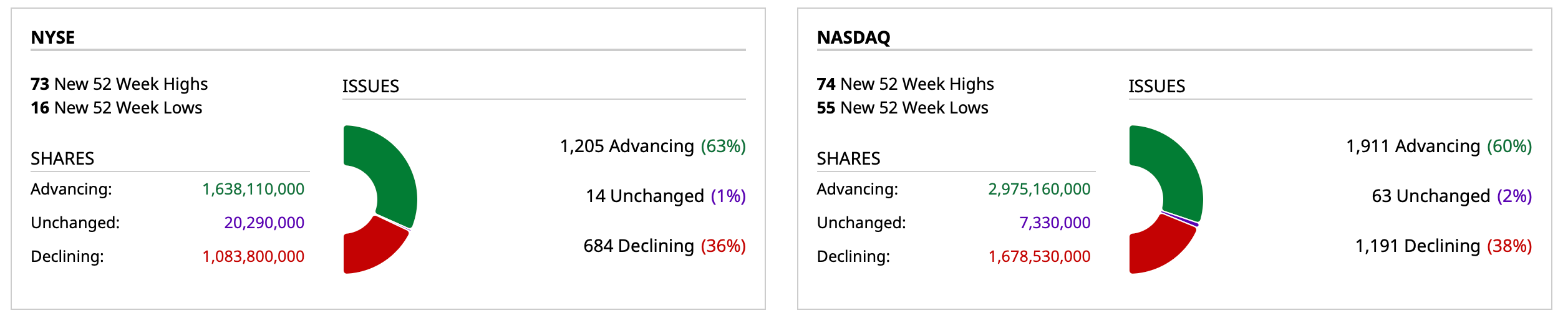

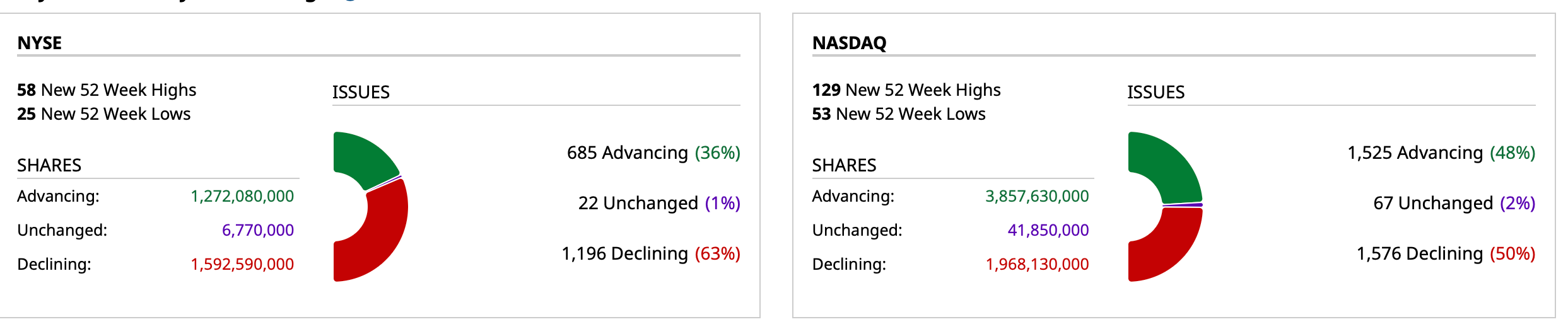

But breadth was very robust (at almost 2-1):

Nonetheless, my near-term concerns remain in place — and equities still seem overbought.

Here are some solid technical observations From The Divine Ms M this morning:

The market continues to work off the short-term overbought condition that developed late last week. The DSI on the VIX got to 15 (it is now 18, so not a big rise), which coupled with the overbought condition, signaled to me that we were due for a pullback.

I don’t have any strong feel for whether or not the market will rally on Fed Day (Wednesday), but I still think it has not worked off enough of the overbought condition. If we can stay down or at least sorta down the way we’ve been the last two days, then I think we’d get back to a short-term oversold reading by next week. If you are looking to trade the market, that might be the best way to look at it.

It would be helpful if the intermediate-term indicators were oversold, but they are not. It would be helpful if they were overbought, but they are not. As we saw in yesterday’s missive, the 30-day moving average of the advance/decline line has been hovering either side of the zero line for two months now. Right now, it looks to me as if it is due for another short trip up and over the zero line.

Yesterday we made the case for a lower market over the short term:

* Nonetheless, I am using the market's stubborn firmness as an opportunity to expand the size of my short book...

Normally the conditions of rising global interest rates, a weak dispersion of S&P index sector strength, sour aggregate market breadth, an overbought S&P Short Range Oscillator, generally ebullient investor sentiment and a pattern of market instability when rates are cut by the Fed (when the S&P is close to an all-time high) would satisfy the bears and contribute to a trend towards weaker stock prices.

Yesterday's foul breadth continued the pattern of the last several days.

The S&P Short Range Oscillator stands at 3.65% (vs 4.6%). That's firmly in overbought territory.

But this is not our father's market!

By Doug Kass Dec 9, 2025 9:30 AM EST

BY Doug Kass · Dec 10, 2025, 8:00 AM EST

Dougie Kass

Now that most of the MAG7 have fallen well below their 52 week highs - we hear nothing from the "generational compounder" proponents.

Having sold META and MSFT (and having profitably covered our AAPL short), we are only long AMZN in MAG7.

BY Doug Kass · Dec 10, 2025, 7:50 AM EST

BY Doug Kass · Dec 10, 2025, 7:40 AM EST

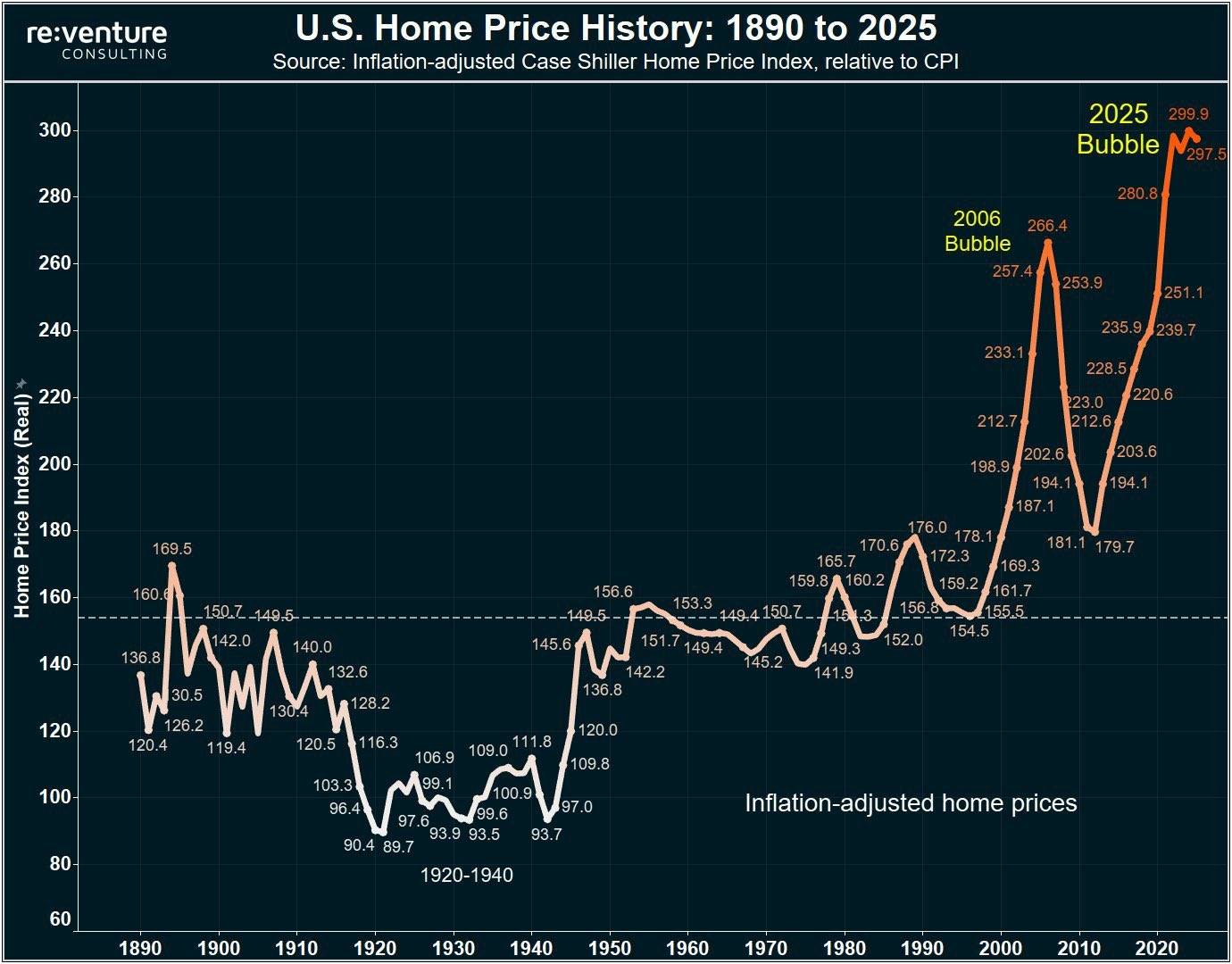

The current level of affordability is the worst in history:

Moreover, in excess of 75% of homes across America are unaffordable for the average household (source: AI):

More than 75% of homes across America are unaffordable for the average household, according to a recent analysis by Bankrate. This statistic highlights the significant gap between household incomes and home prices, making homeownership increasingly difficult for many families. The analysis indicates that only a small fraction of the housing market is affordable, with only 24% of housing sales last year being to first-time homebuyers, down from 50% in 2010. The average home price now exceeds $435,000, and in high-cost cities like New York and San Francisco, households must earn at least $200,000 to afford a median-priced home.

BY Doug Kass · Dec 10, 2025, 7:30 AM EST

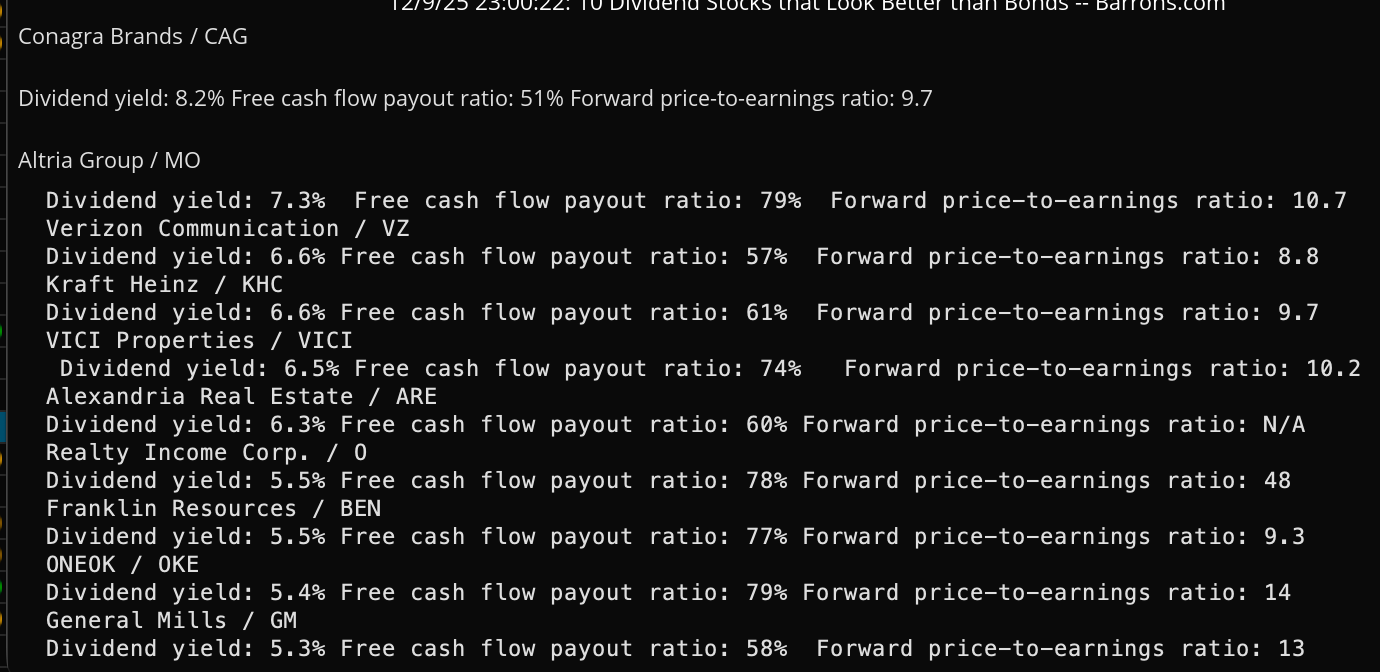

DaveInKenya

Barron's with 10 stocks for income...

BY Doug Kass · Dec 10, 2025, 7:20 AM EST

* More cannabis opposition from the Republican Party...

BY Doug Kass · Dec 10, 2025, 7:10 AM EST

BY Doug Kass · Dec 10, 2025, 7:00 AM EST

* Micro-caps take the wheel...

Bonus — Here are some great links:

Risk Appetite Is Back, and Micro Caps Proved It

S&P Results Mixed on Fed Cut Announcement Days ("Jazzy" Jeff Hirsch)

BY Doug Kass · Dec 10, 2025, 6:45 AM EST

BY Doug Kass · Dec 10, 2025, 6:35 AM EST

The rise in global interest rates is a bonafide headwind to equity prices and valuations:

In the U.S., the equity risk premium (the S&P earnings yield (the inverse of the P/E ratio) minus the risk free rate of return (10-year Treasury yield)) has become an equity risk discount!

BY Doug Kass · Dec 10, 2025, 6:25 AM EST

BY Doug Kass · Dec 10, 2025, 6:15 AM EST

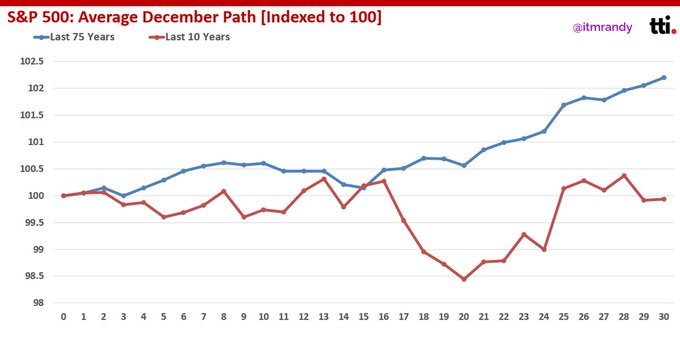

* Does choppiness lie ahead?

Maybe, like many four-year presidential cycles, we will see a period of choppiness ahead:

BY Doug Kass · Dec 10, 2025, 6:05 AM EST

* JPMorgan rerates PepsiCo...

This morning JPMorgan moved from neutral to overweight in PepsiCo (PEP) , raising the price target from $151 to $164.

The shares are trading +$2 in the premarket.

Yesterday we moved to a very long position in PEP:

At $144.68 I moved to very large long (PEP).

By Doug Kass Dec 9, 2025 10:26 AM EST

BY Doug Kass · Dec 10, 2025, 5:55 AM EST

The S&P Short Range Oscillator remains overbought at 3.26% vs. 3.60%.

BY Doug Kass · Dec 10, 2025, 5:45 AM EST

Join us on spaces at the top of the hour to talk charts and more! x.com/i/spaces/1BRKj…