Shorting Indexes on Nvidia Euphoria

I am back shorting index common on the heels of the Nvidia (NVDA) euphoria:

* (SPY) $684.22

* (QQQ) $625.02

BY Doug Kass · Dec 8, 2025, 5:21 PM EST

I am back shorting index common on the heels of the Nvidia (NVDA) euphoria:

* (SPY) $684.22

* (QQQ) $625.02

BY Doug Kass · Dec 8, 2025, 5:21 PM EST

Nvidia (NVDA) is flying after the close on this news:

I am shorting more (NVDA) at $190.55.

BY Doug Kass · Dec 8, 2025, 5:10 PM EST

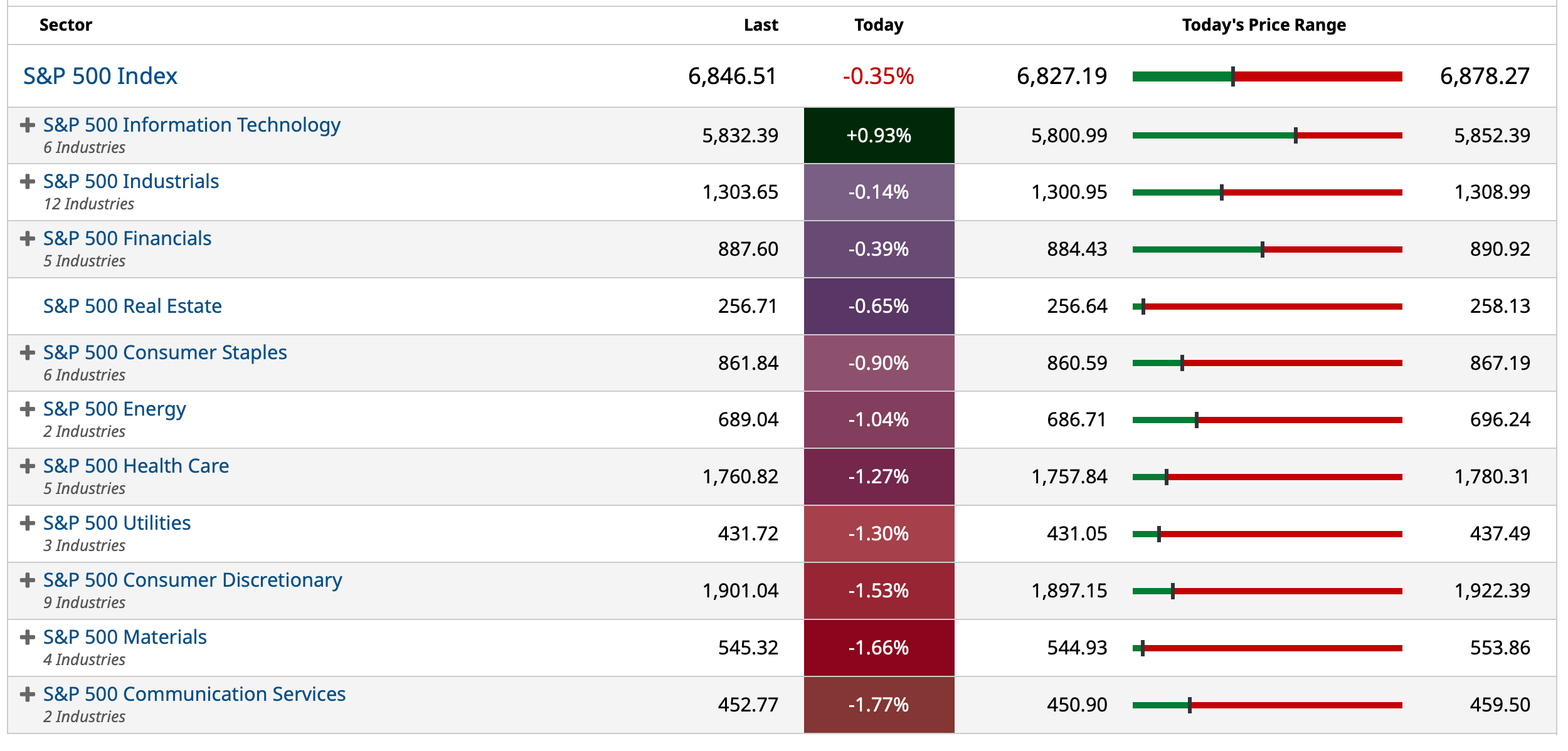

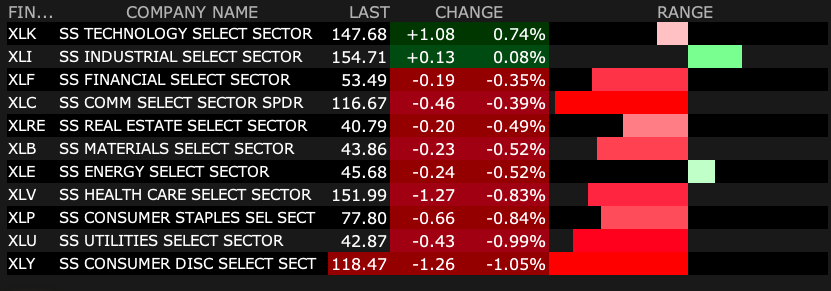

Only one out of 12 S&P sectors was positive today — information technology:

BY Doug Kass · Dec 8, 2025, 4:55 PM EST

BY Doug Kass · Dec 8, 2025, 4:45 PM EST

BY Doug Kass · Dec 8, 2025, 4:35 PM EST

- NYSE volume 12% below its one-month average

- NASDAQ volume 4% below its one-month average

- VIX index: up 8.11% to 16.66

BY Doug Kass · Dec 8, 2025, 4:30 PM EST

I added to Amazon (AMZN) long at $226.86.

BY Doug Kass · Dec 8, 2025, 3:19 PM EST

BY Doug Kass · Dec 8, 2025, 2:45 PM EST

While I am on it...

The less well AI works, the more additive it is to GDP over the short term.

The solution always is to throw more dollars at what is not working.

Like a heroin addict needing more to get high.

The same applies to the U.S. economy with regard to debt accumulation and ever looser forms of monetary policy.

It all seemingly never ends. A good solution is almost never to do more of what is not working, it is to do things differently, and more smartly, or just not do it!

From Gary Marcus:

BY Doug Kass · Dec 8, 2025, 2:30 PM EST

BY Doug Kass · Dec 8, 2025, 2:15 PM EST

I call BS to Davis Sacks:

AI is not causing job losses — because it is not working. It fails in real world implementations.

Therefore, the GDP growth that comes from it is the equivalent of paying people to dig holes and fill them back up. It is dis-economic investment. We should not be orienting the whole of economic and government policy to support the private sector acting like drunken idiots (just like Zuck did on the metaverse).

The same applies to BTC and the other things his cronies have piled into.

Stay out of it. Sacks is no different than the socialist-oriented that he rails against on your podcast.

And as for the lack of overall job growth in total, it is because the K-shaped economy stinks and eventually someone is going to figure out easy money is not the panacea or solution — it ultimately only makes things worse and more unbalanced.

Sometimes it is better to keep your mouth shut and appear stupid than it is to open it and remove all doubt. Much too arrogant and self-absorbed in their own circular self-reinforcing BS. Once again, it is no different than the other close-minded thought loops they rail against.

Frankly, they are all clueless in their own ivory towers.

BY Doug Kass · Dec 8, 2025, 1:50 PM EST

I have added to two individual shorts:

* (NVDA) $187.04

* (CVNA) $454.37

BY Doug Kass · Dec 8, 2025, 1:37 PM EST

With S&P cash now -30 handles (a nearly -50 swing from the day's highs) I have covered my short index calls for a profit.

I plan to re-short on strength.

Again, I continue to expect a sawtooth pattern of lower highs and lower lows from here over the next few months.

Ideal for opportunistic trading but not hot for the buy-and-hold crowd.

BY Doug Kass · Dec 8, 2025, 12:26 PM EST

- NYSE volume 4% below its one-month average

- NASDAQ volume 5% above its one-month average

- VIX index: up 7.79% to 16.61

BY Doug Kass · Dec 8, 2025, 11:00 AM EST

* With a small gain...

I covered this morning's Index common shorts:

* (SPY) $684.08

* (QQQ) $624.42

At the same time I added earlier (very small) to my short index calls.

From earlier:

I have shorted the indices in premarket trading:

* (SPY) $686.53

* (QQQ) $627.05

I have shorted Carvana (CVNA) (on the S&P inclusion) at $441.20.

Position: Short CVNA, SPY common (VS) and calls (VS), QQQ common (VS) and calls (VS)

By Doug Kass Dec 8, 2025 6:25 AM EST

BY Doug Kass · Dec 8, 2025, 10:32 AM EST

BY Doug Kass · Dec 8, 2025, 10:30 AM EST

Excerpt from The Information's AI Agenda newsletter by Stephanie Palazzolo:

There’s rising skepticism among researchers, including OpenAI co-founder Ilya Sutskever, about the effectiveness of RL and whether it can advance AI to the level of artificial general intelligence, on par with human experts in scientific research, healthcare and other domains.

Sutskever, who left OpenAI last year to start his own AI lab, explained in a rare interview on the Dwarkesh podcast why AI models are struggling to handle real-world tasks that aren’t part of the evaluations that researchers use when they develop the models.

He said researchers use RL to help the models ace the evaluations, but that doesn’t improve the way the models generalize, or handle a wide variety of tasks.

His lukewarm opinion of RL puts him in a similar camp as another OpenAI co-founder, Andrej Karpathy.

Sutskever also questioned the definition of artificial general intelligence, the concept of AI that outperforms humans at most economically valuable work. Sutskever said AGI should instead refer to AI that can learn how to excel at tasks after it starts working on them, much like a teenager who can learn how to drive in the real world after just a few hours behind the wheel.

Read the whole piece here:

BY Doug Kass · Dec 8, 2025, 10:00 AM EST

* It is my continuing view that the downside risks materially dwarf the upside rewards and that there is a limited "margin of safety" at current stock price levels

* Current traditional valuation metrics (e.g., the trailing 12-month P/E ratio is the 98%-tile) are a poor launching pad for future investment returns

* The global bond markets are not cooperating with equities

* Bullish investor sentiment (both short term (oscillator) and intermediate term) is at an extreme

* Everything old is new again...

Today, market participants remain optimistic, are arguably reckless (in what they own and in their concentrated holdings) and are convinced that they will see the top before others see it. By contrast, we see another era of overconfidence coming to an end very soon:

There has rarely been so much uncertainty of outcomes — with many of them adverse. We see early signposts of the sort of instability and bad actions that we have witnessed in past market and economic downturns. Nonetheless, valuations are in the 97%-tile and the equity risk premium has turned into a discount (something not seen in almost three decades).

I hold to a number of other concerns. Here are some of the ones that I find most worrisome:

* Country debt loads are burgeoning around the globe — it’s not simply a U.S. phenomenon.

* Our base case remains one of anticipated "slugflation" — slowing economic growth and persistently high inflation.

* The rise in Japanese bond yields poses a threat to the capital markets.

The rise in interest rates is a global phenomenon:

And, over here:

* The AI system (without whose growth the domestic economy would likely be experiencing modest, if any real growth) is massively interconnected with circular financings, non-disclosed leverage and dubious accounting.

Proponents of AI have argued that productivity gains from artificial intelligence and machine learning represent the best last hope for economic prosperity. But thus far it seems that these applications may primarily eliminate jobs and otherwise shrink rather than grow corporate spending. An MIT study claims that AI can already replace 11.7% of the U.S. workforce. As hyperscalers charge ahead trying to perfect their LLMs and other AI models, our society seems ill-prepared for the consequences if they succeed in achieving their goals — and our markets are also poorly positioned if they fail.

As was the case as the dot-com boom matured in late 1999 and just before The Great Recession commenced during the winter of 2007, investor sentiment is inflated and price-earnings multiples are elevated. Eighteen years ago, market participants were committed to dancing until the music stopped — and the majority was confident or haughty enough to think that they could anticipate the signposts of a market top. In retrospect, these periods represented the end of the bull market in hubris and complacency — and large market drawdowns followed.

But there are some differences that exist today. Since Covid, the average consumer has been plagued by a K-shaped economy featuring a steady five-year accumulation of higher food costs, healthcare, housing, utilities and other essentials. As we end 2025 the magnitude of the mal investment is multiples larger that during the dot-com boom and the public financial system (at the state and national levels) is more significantly leveraged.

What is also different is the leverage in the cryptocurrency and private-equity markets. Also different are the risks associated with a more levered market structure in which passive investing (quant strategies and ETFs that "worship at the altar of price momentum") now dominate active investing.

Finally, as I have noted in my recent commentary, for the first time in modern times, economic and regulatory policy are being determined by the very same managements of technology companies that are so pivotal to our economic prosperity.

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We're still dancing.”

- Chuck Prince, former Citigroup CEO (Financial Times interview on July 8, 2007)

To this observor, so much could go wrong in the time ahead, yet so few are anticipating the potential potholes.

We are all Chuck Prince now...

BY Doug Kass · Dec 8, 2025, 9:30 AM EST

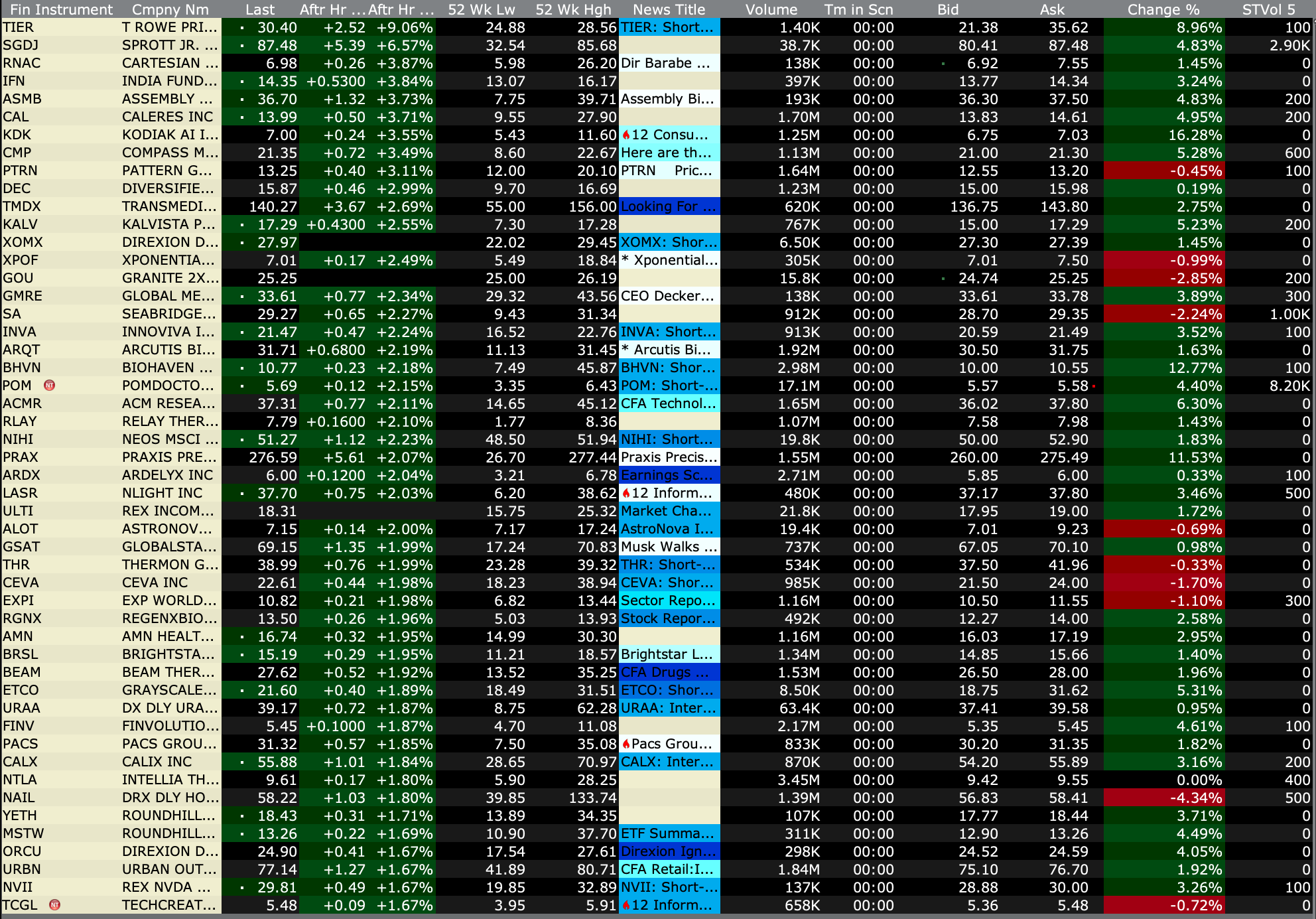

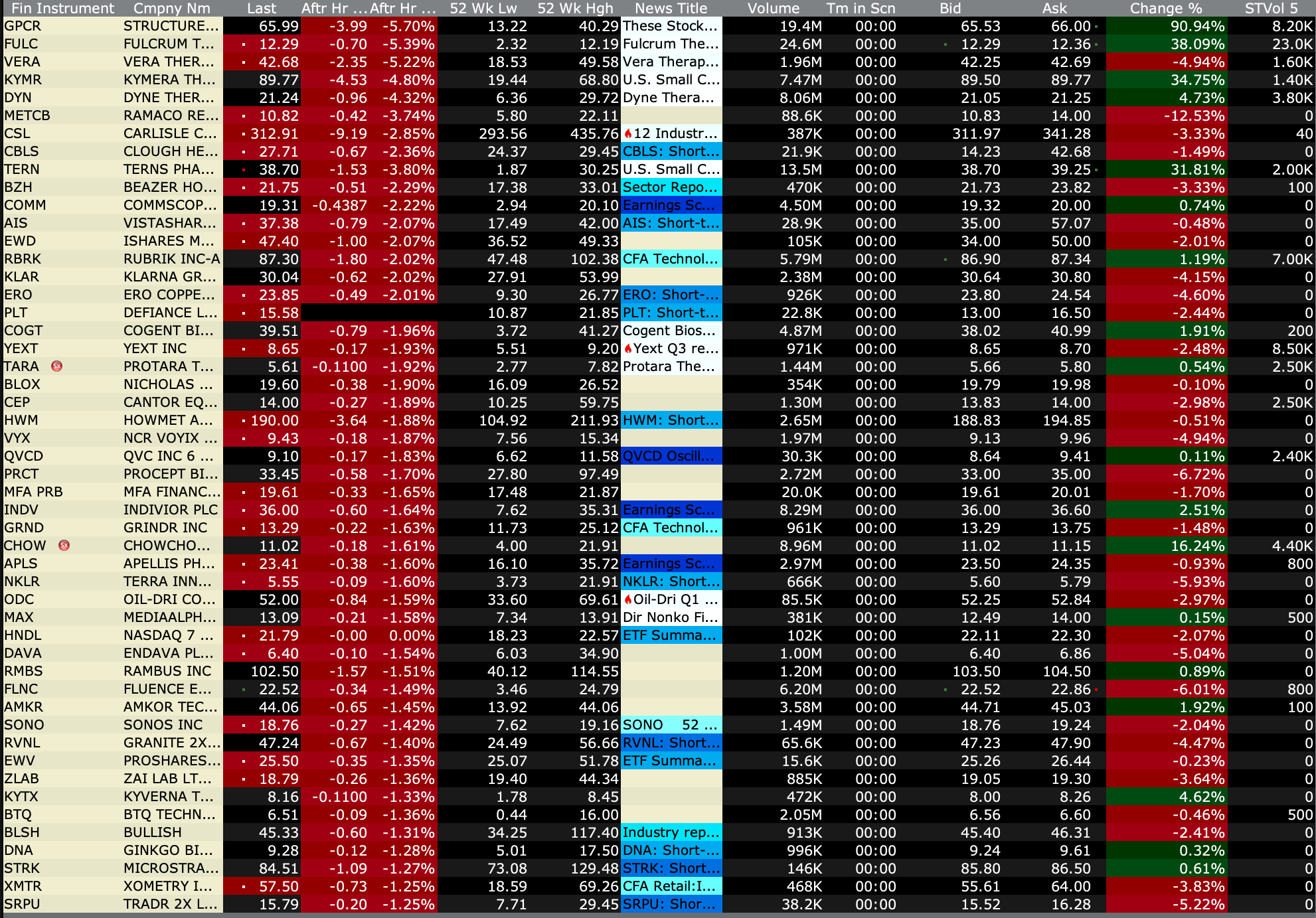

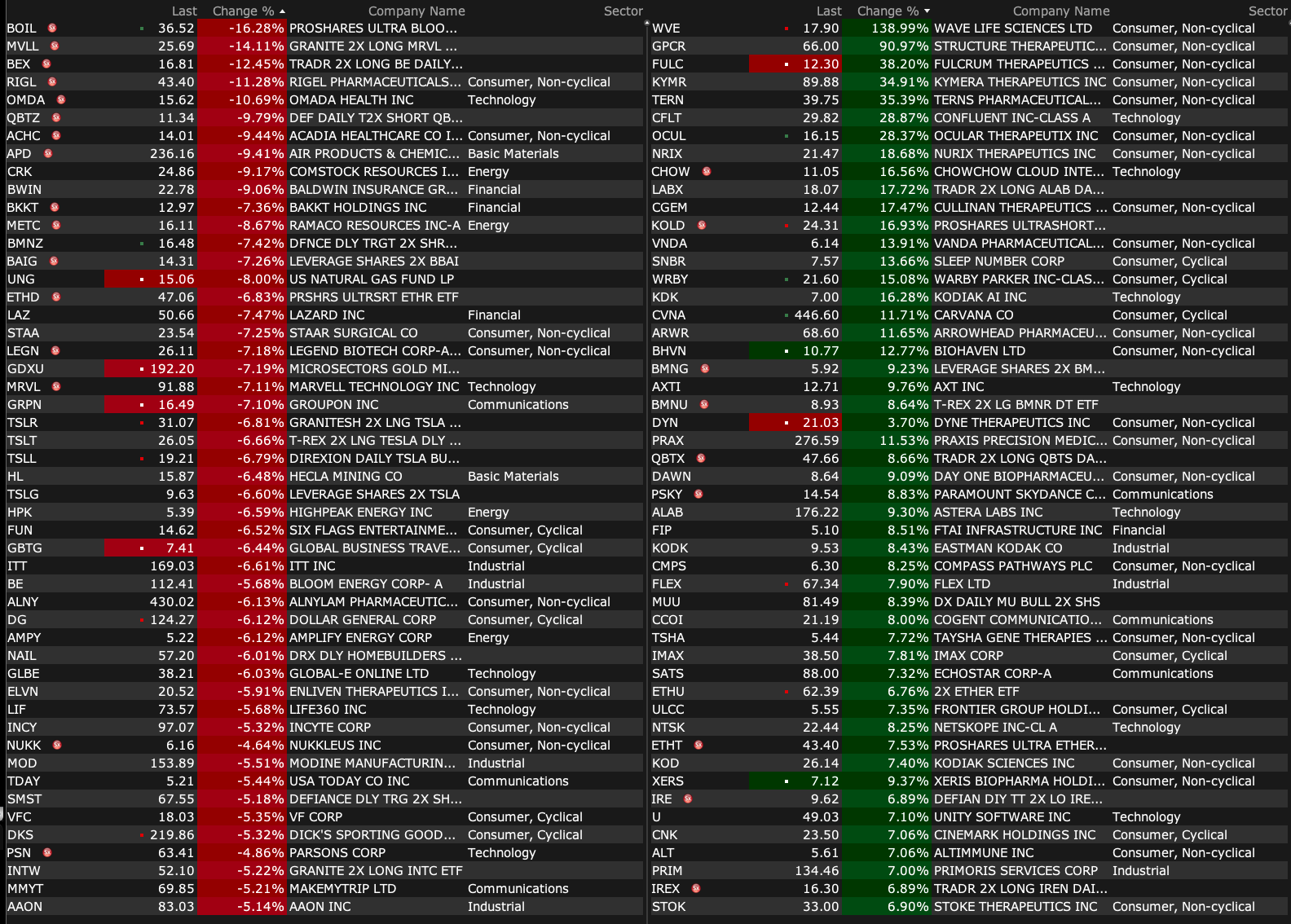

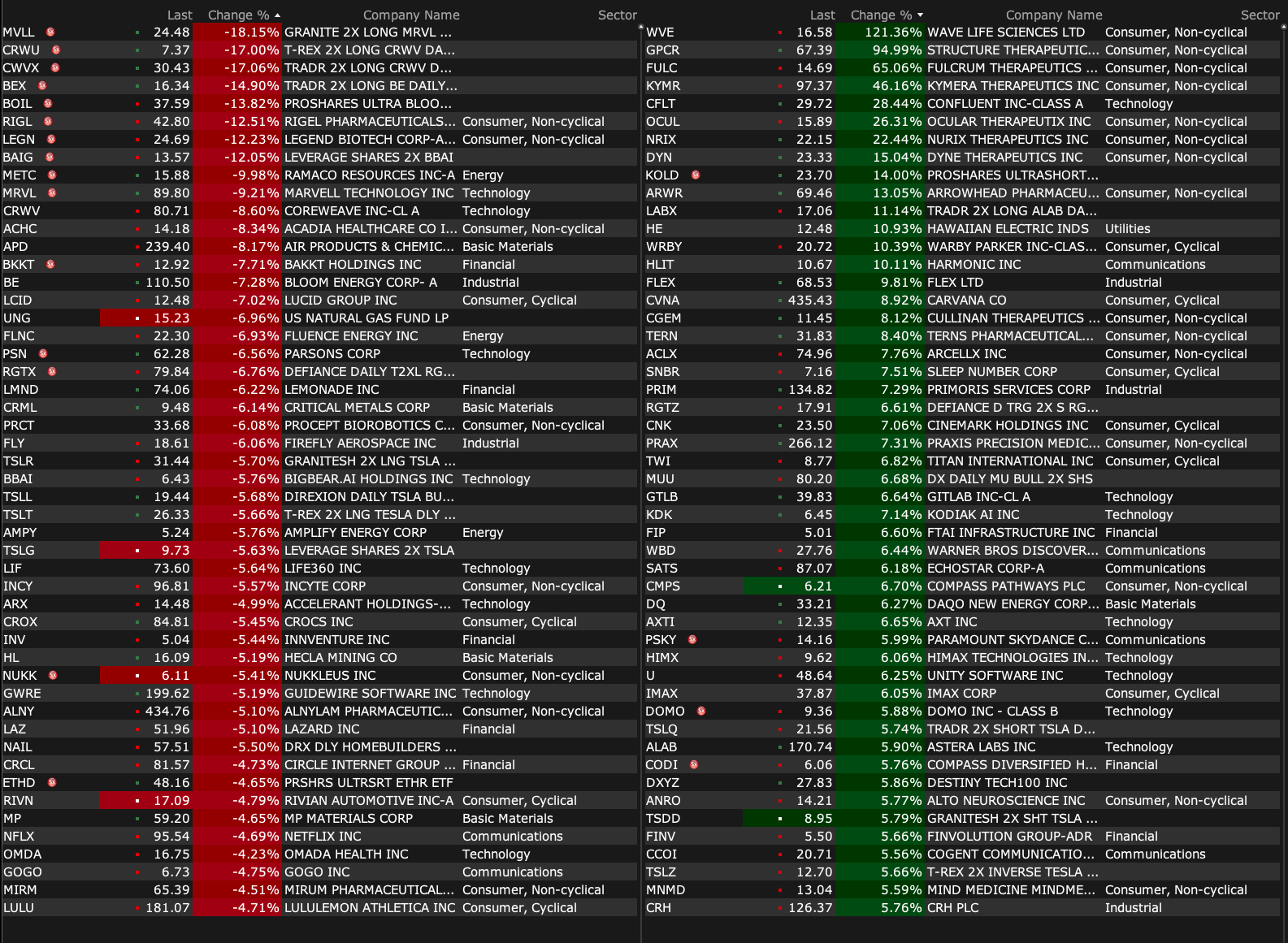

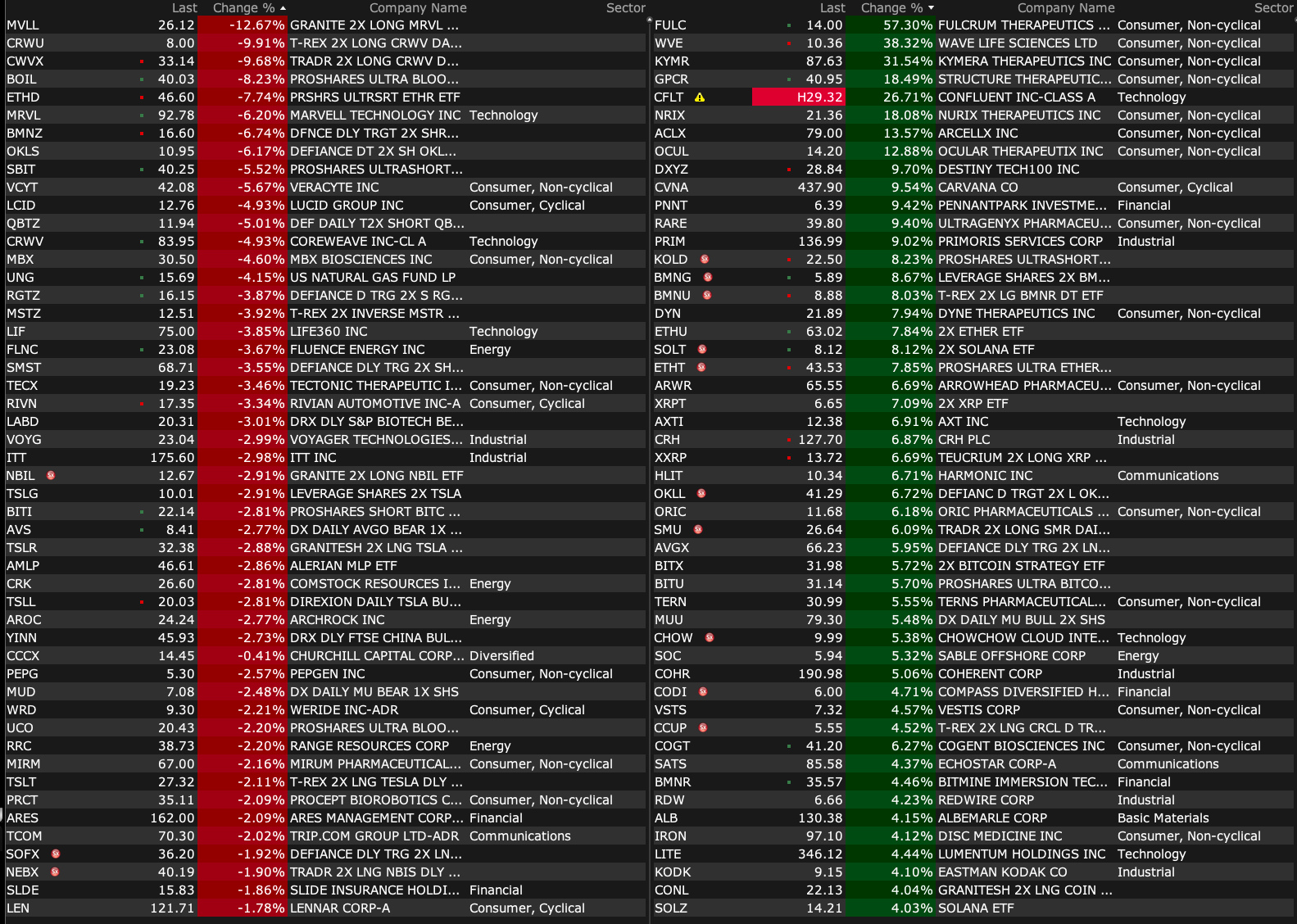

Upside:

-WVE +78% (announces Positive Interim Data from Phase 1 INLIGHT Trial of WVE-007 (INHBE) for Obesity)

-FULC +68% (announces Positive Initial Results from the 20 mg Dose Cohort of the Phase 1b PIONEER Trial of Pociredir in Sickle Cell Disease at the 67th American Society of Hematology Annual Meeting)

-KYMR +34% (KT-621 BROADEN2 Phase 2b trial in moderate to severe AD is ongoing, with data expected by mid-2027 and Phase 2b BREADTH trial in moderate to severe asthma patients is on track to start 1Q26)

-CFLT +29% (confirms to be acquired by IBM at $31.00/shr in cash in $11B deal)

-NRIX +20% (presents New Data from Phase 1 Trial of Bexobrutideg (NX-5948) in Waldenström Macroglobulinemia at the 67th American Society of Hematology (ASH) Annual Meeting and Exposition)

-ACLX +13% (announces New Positive Data for Its iMMagine-1 Study in Patients with Relapsed and/or Refractory Multiple Myeloma)

-DTST +12% (intends to commence a Tender Offer for up to 6.2M Shares)

-CVNA +8.3% (to be added to S&P 500 Index)

-GPCR +7.3% (reports Placebo-adjusted mean weight loss of 11.3% (27.3 lbs) with 120 mg dose in the 36-week Phase 2b ACCESS study with a 10.4% adverse event-related treatment discontinuation)

-CRH +6.1% (to be added to S&P 500 Index)

-SSII +5.6% (submits 510(k) Premarket Notification to FDA for SSi Mantra Surgical Robotic System)

-ALB +3.6% (UBS Raised ALB to Buy from Neutral, price target: $185)

-JEF +3.4% (acquires 50% interest in credit-focused asset manager Hildene Holding Company, LLC)

-AVGO +2.9% (reportedly Microsoft is in talks to shift its custom chip business to Broadcom from Marvell)

-COMP +2.6% (Barclays Raised COMP to Overweight from Equal Weight, price target: $13 from $9)

Downside:

-MRVL -6.4% (reportedly Microsoft is in talks to shift its custom chip business to Broadcom from Marvell)

-FLNC -4.4% (Mizuho Securities Cuts FLNC to Underperform from Neutral, price target: $15)

-CRWV -4.1% (files to sell $2B in convertible senior notes due 2031 with option for +$300M)

BY Doug Kass · Dec 8, 2025, 9:15 AM EST

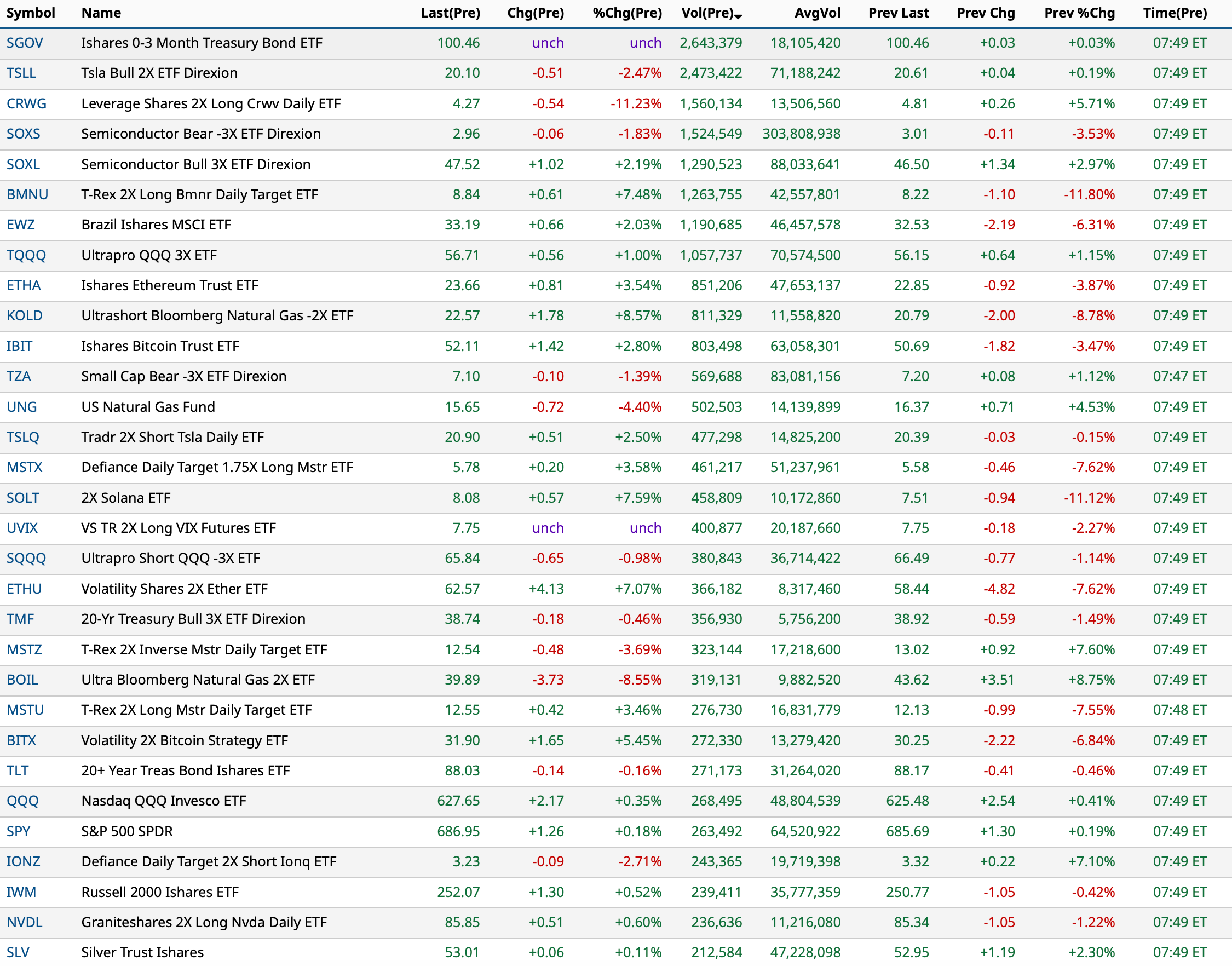

As of 7:49 AM

BY Doug Kass · Dec 8, 2025, 8:55 AM EST

BY Doug Kass · Dec 8, 2025, 8:45 AM EST

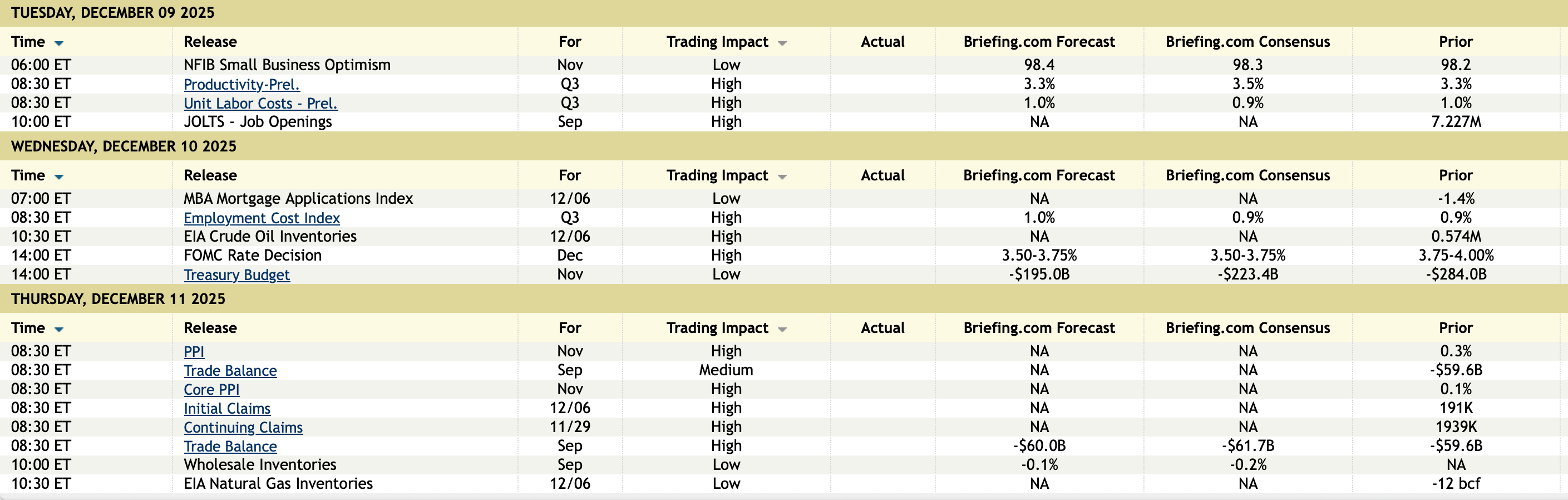

11:30AM: Treasury hosts an $86B 3 and a $77B 6-Month Bill Auction

1:00PM: Treasury hosts a $58B 3-Year Note Auction

BY Doug Kass · Dec 8, 2025, 8:25 AM EST

Today in 1978 Microsoft (MSFT) took its first staff photo:

BY Doug Kass · Dec 8, 2025, 8:15 AM EST

* (SPY) $686.88

* (QQQ) $627.54

BY Doug Kass · Dec 8, 2025, 8:00 AM EST

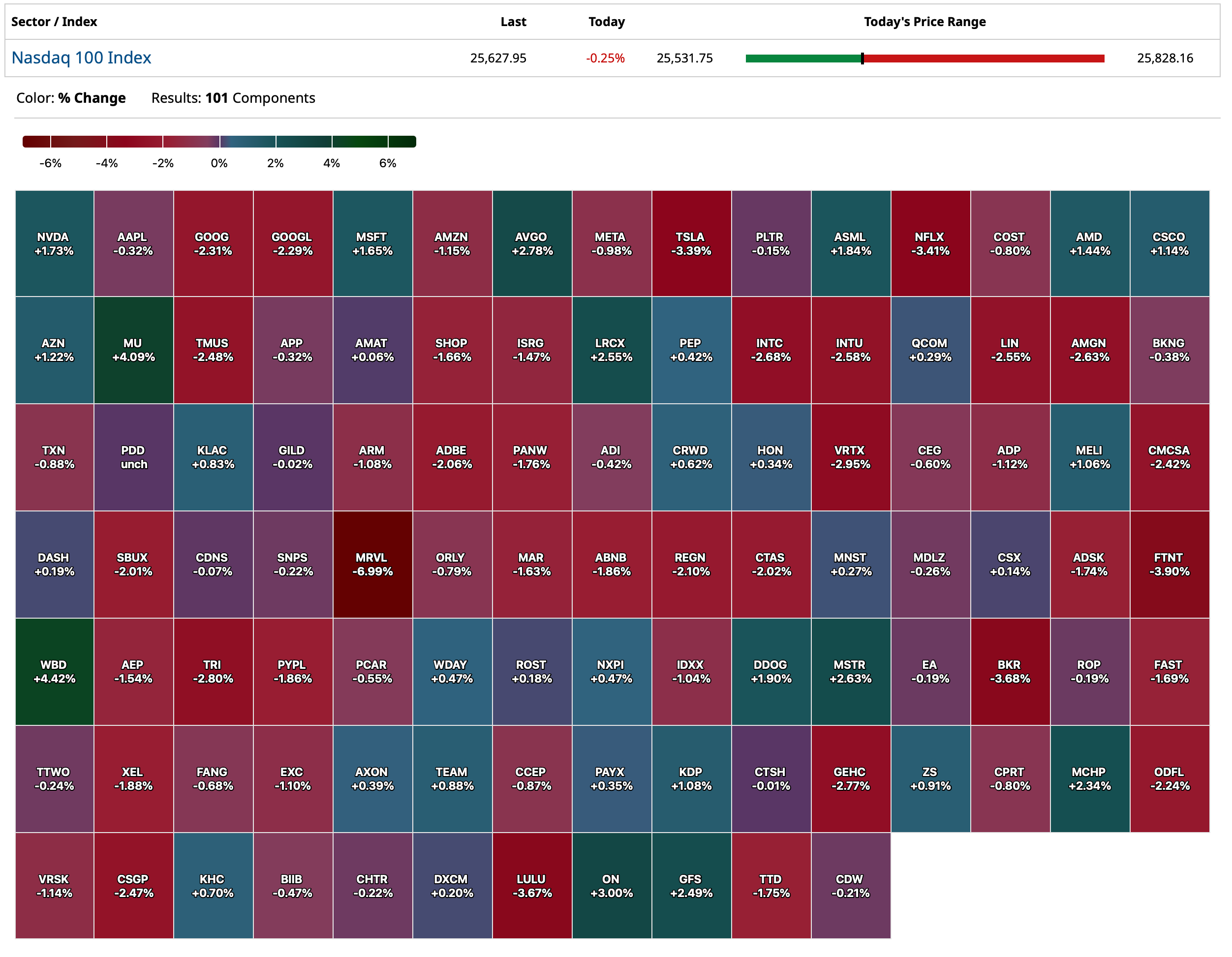

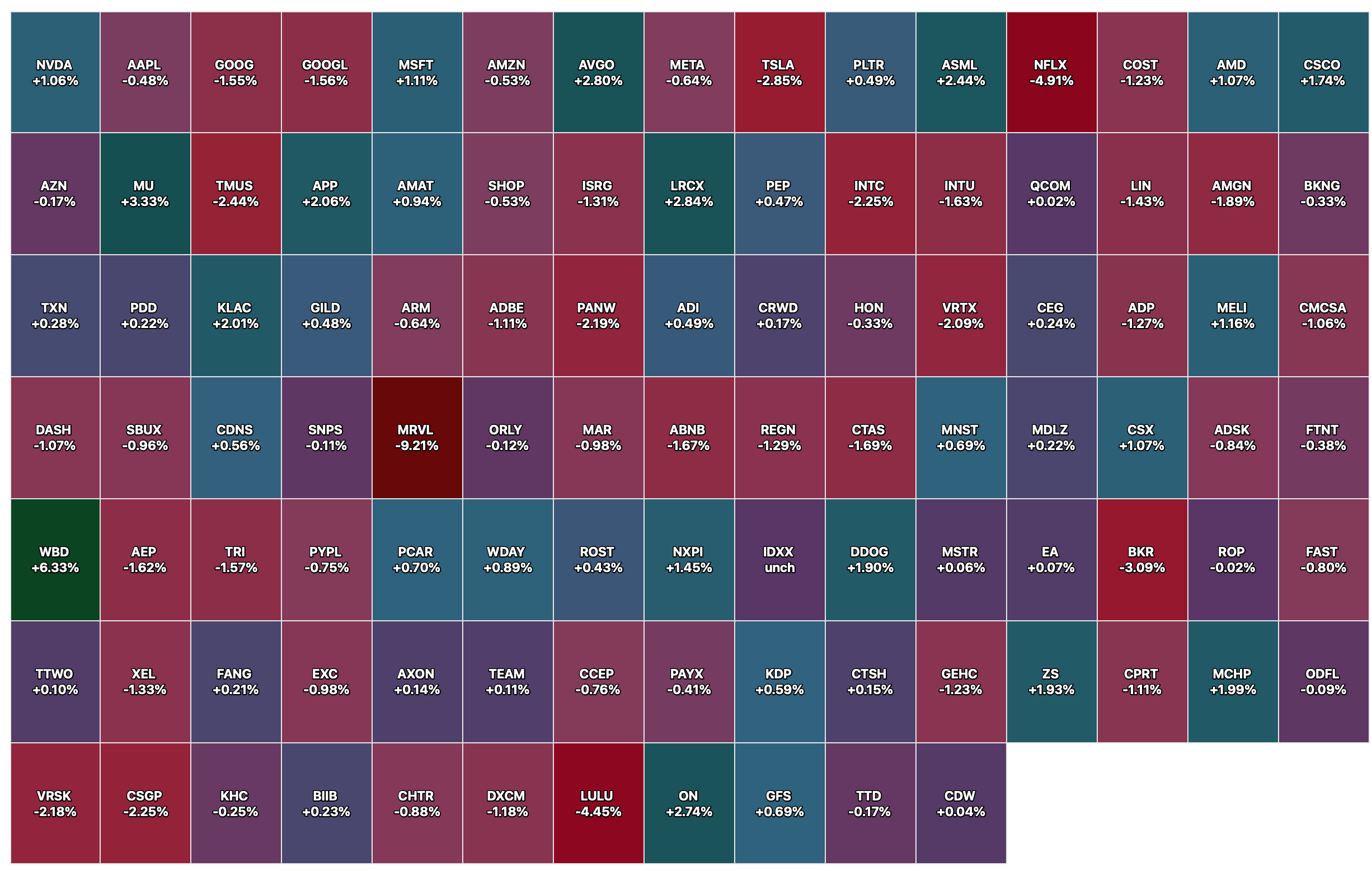

* Funny how software, the worst, is ripping...

Bonus — Here are some great links:

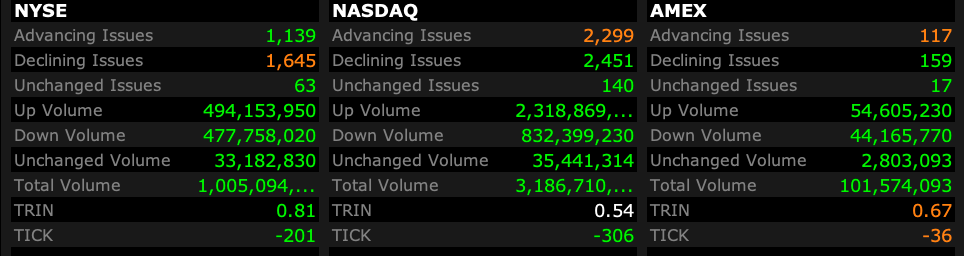

A Significant Streak Continues

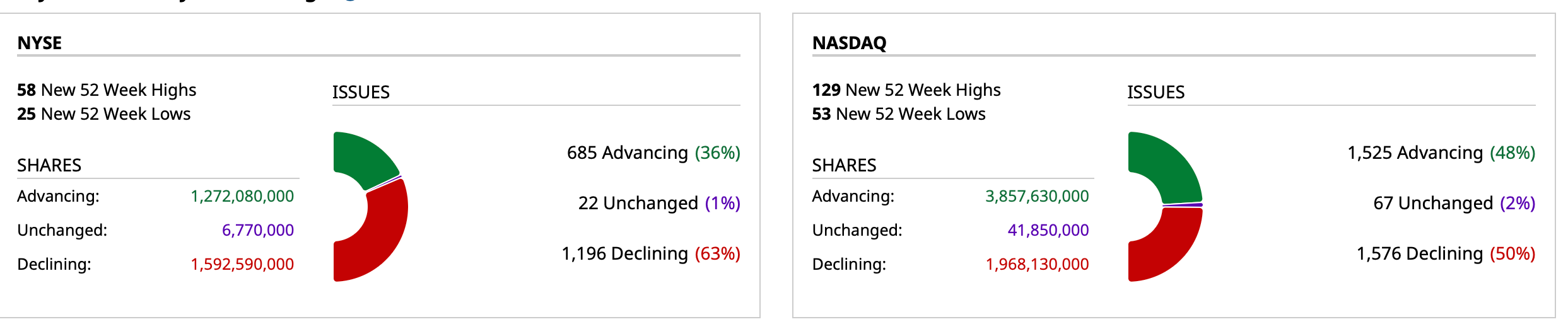

Breadth Not Ideal, but Still Net Bullish

Regional Banks: The Most Crowded Wrong Trade on Earth Right Now

BY Doug Kass · Dec 8, 2025, 7:45 AM EST

Investors, as I recently noted, are ignoring the rise in interest rates. I am not:

BY Doug Kass · Dec 8, 2025, 7:35 AM EST

BY Doug Kass · Dec 8, 2025, 7:25 AM EST

BY Doug Kass · Dec 8, 2025, 7:15 AM EST

From JPMorgan:

US: Futs are higher led by RTY. Pre-market, Mag 7 are mostly unchanged except for a -1.3% decline in TSLA. Bond yields are 1-2bp higher; USD is lower. Commodities are mixed: oil and most base metals are down small, while precious metals are higher. Over the weekend, there were several corporate headlines: (i) MSFT is considering shift custom chip business to Broadcom from Marvell (The Information). (ii) Trump warned the Netflix-Warner deal may post antitrust problem (BBG); (iii) IBM close to buy Confluent.

and...

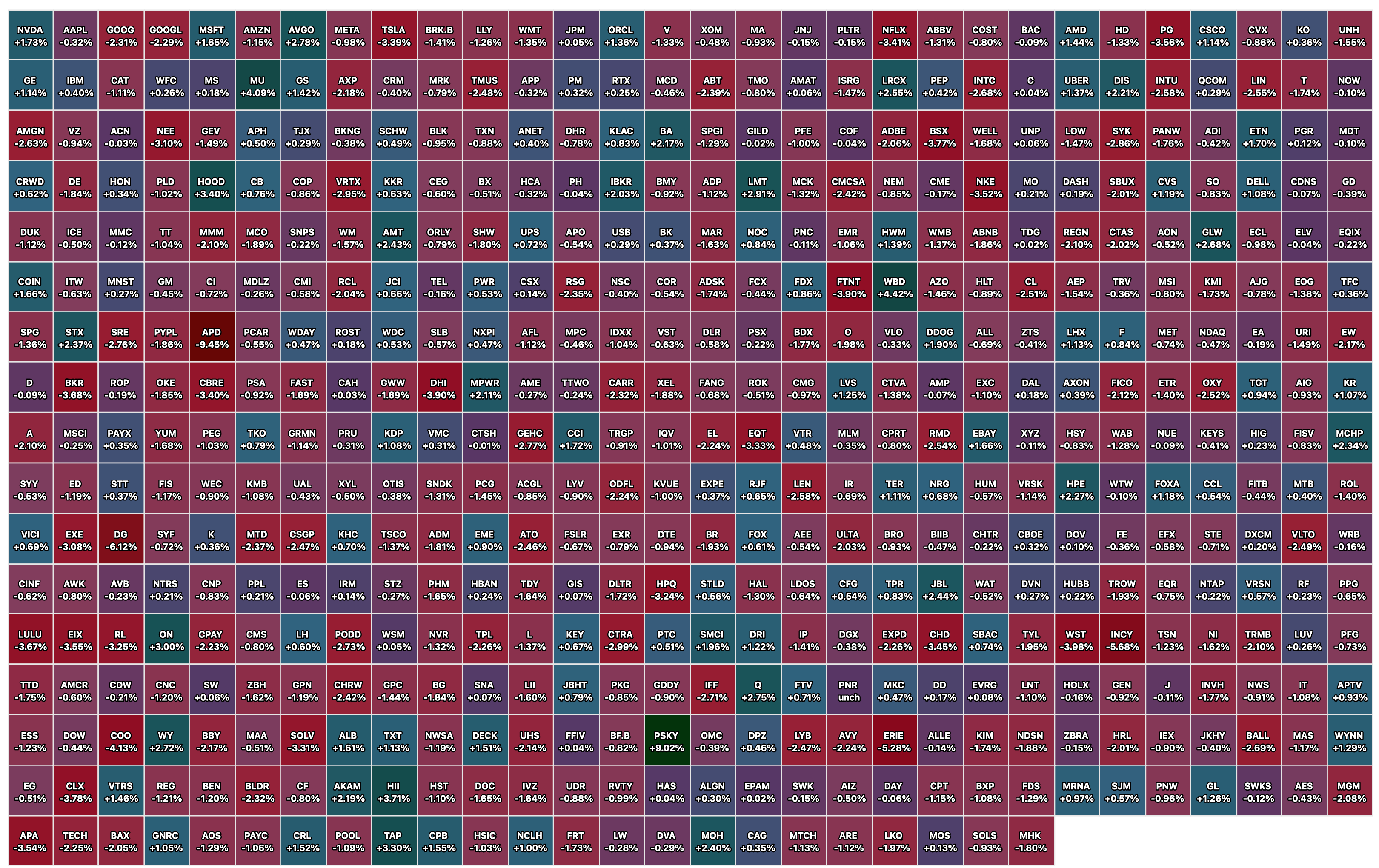

The SPX added +0.3%, NDX added +1.0%, and RTY added +0.8%. SPW (equal-weighted SPX) added 0.2% and QQEW (equal-weighted NDX) added +1.9%. Stocks continued their momentum with major indices all closed in the green; the SPX remains less 1% below its ATH. 6 out of 11 sectors of SPX finished higher led by Energy (+1.4%) and Tech (+1.4%). Recession L/S added 1.1% (+0.9z); Quality added +0.9% (+1.2z). Airlines, Retail and Tariff Short were among the outperformers last week.

Notably, bond yields spiked last week amid global bond market selloff (Japan and UK) and positioning; 10y added 7bp alone last Monday and ended the week 12bp higher. On bond market positioning, Jay Barry told us last Monday that (here): “Positioning technicals likely further weighed on the long end as our positioning indicators suggest investors have moved significantly longer in recent weeks, alongside a dip in liquidity aided by the holiday and the CME outage on Friday.”

This week, key catalyst are (i) FOMC (Dec 10), (ii) ORCL Earnings (Dec 10) and (iii) AVGO Earnings (Dec 11). In addition, OpenAI will likely release new model on Tuesday (TBD). See below for Roadmap to Year-end for thoughts of key market catalysts towards year-end.

BY Doug Kass · Dec 8, 2025, 7:05 AM EST

BY Doug Kass · Dec 8, 2025, 6:55 AM EST

BY Doug Kass · Dec 8, 2025, 6:45 AM EST

BY Doug Kass · Dec 8, 2025, 6:35 AM EST

I have shorted the indices in premarket trading:

* (SPY) $686.53

* (QQQ) $627.05

I have shorted Carvana (CVNA) (on the S&P inclusion) at $441.20.

BY Doug Kass · Dec 8, 2025, 6:25 AM EST

The S&P Short Term Oscillator moves much higher into an overbought — at 5.84% vs. 4.6%.

BY Doug Kass · Dec 8, 2025, 6:15 AM EST

Wolf Street howls about the upcoming Fed meeting.

BY Doug Kass · Dec 8, 2025, 6:05 AM EST