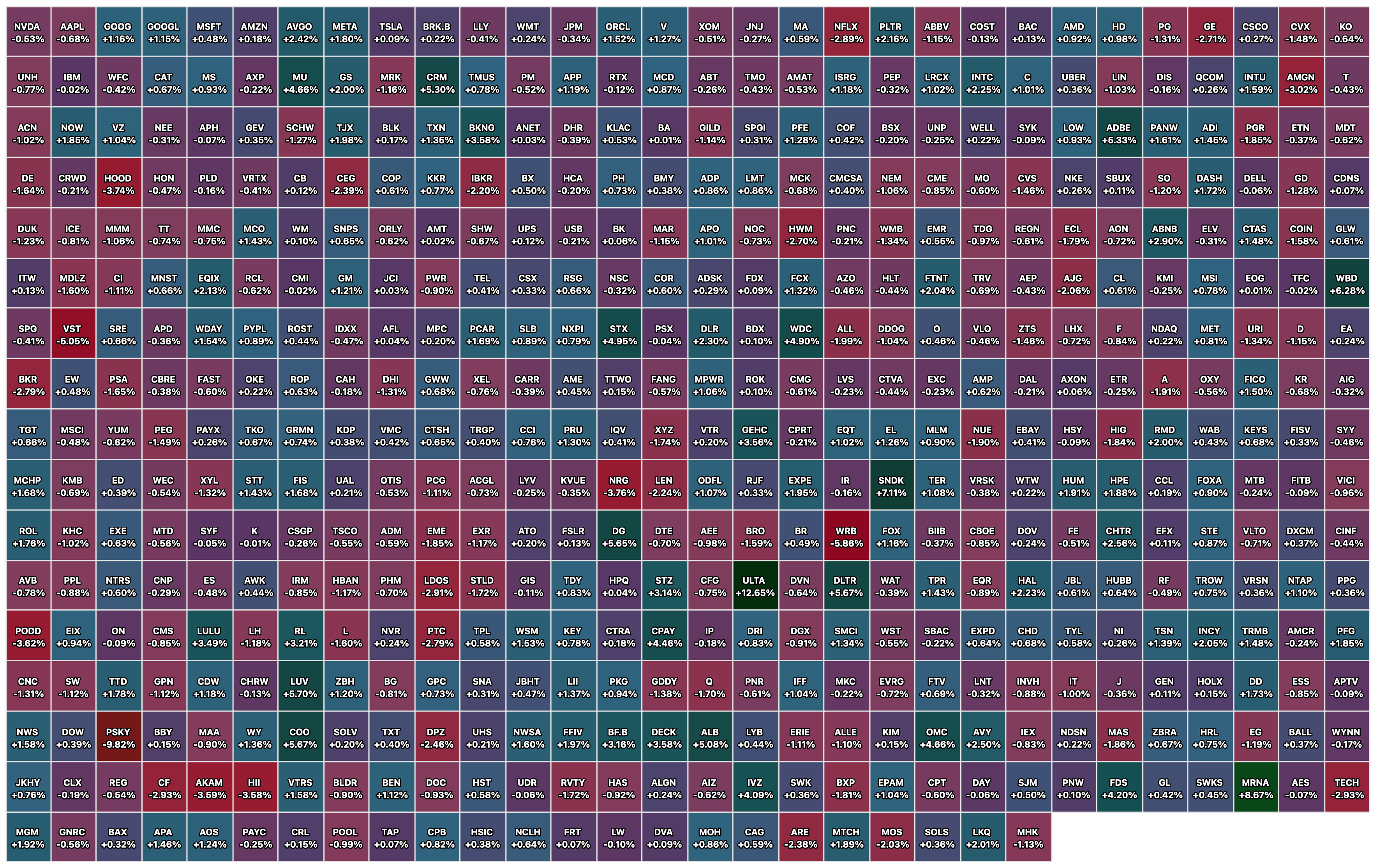

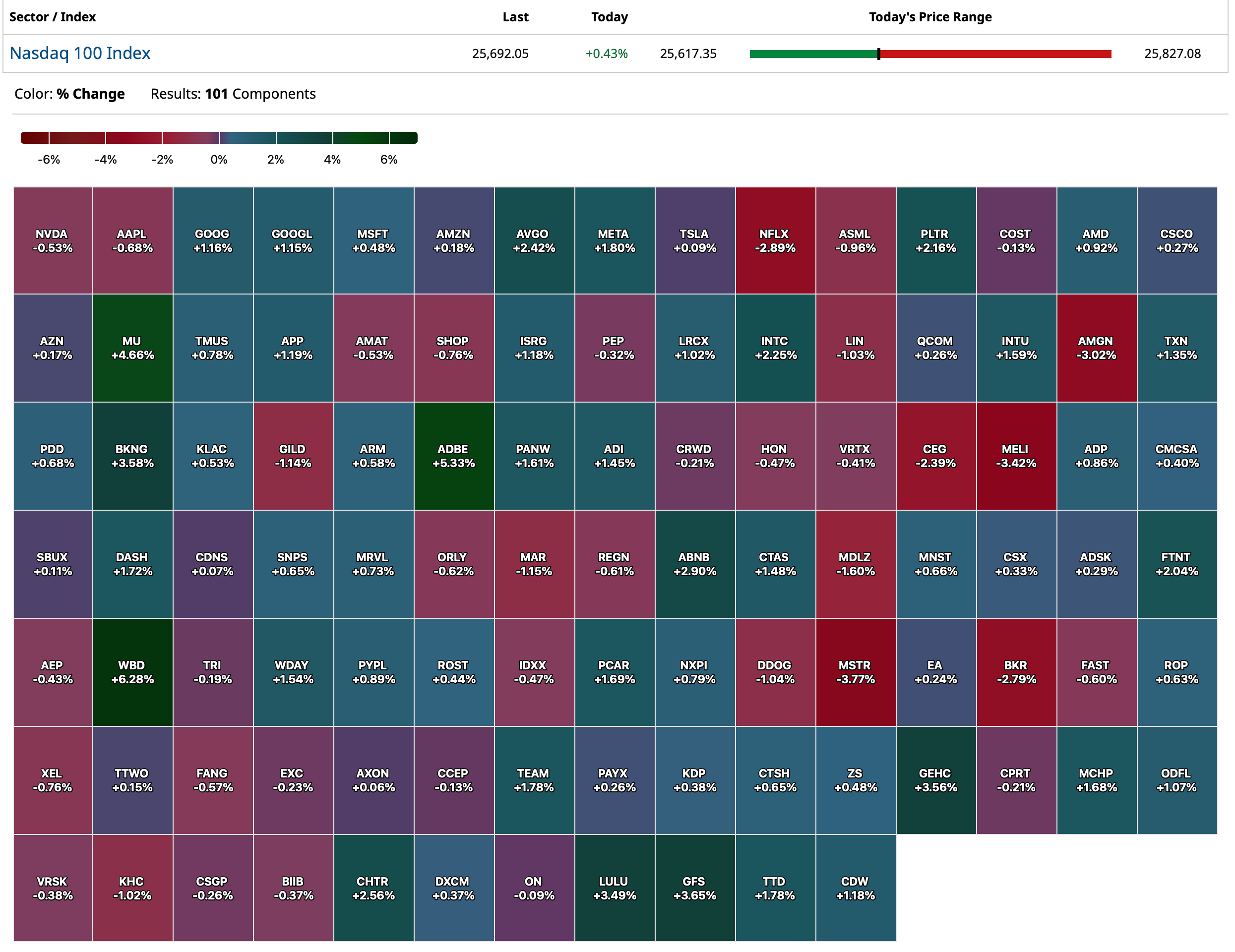

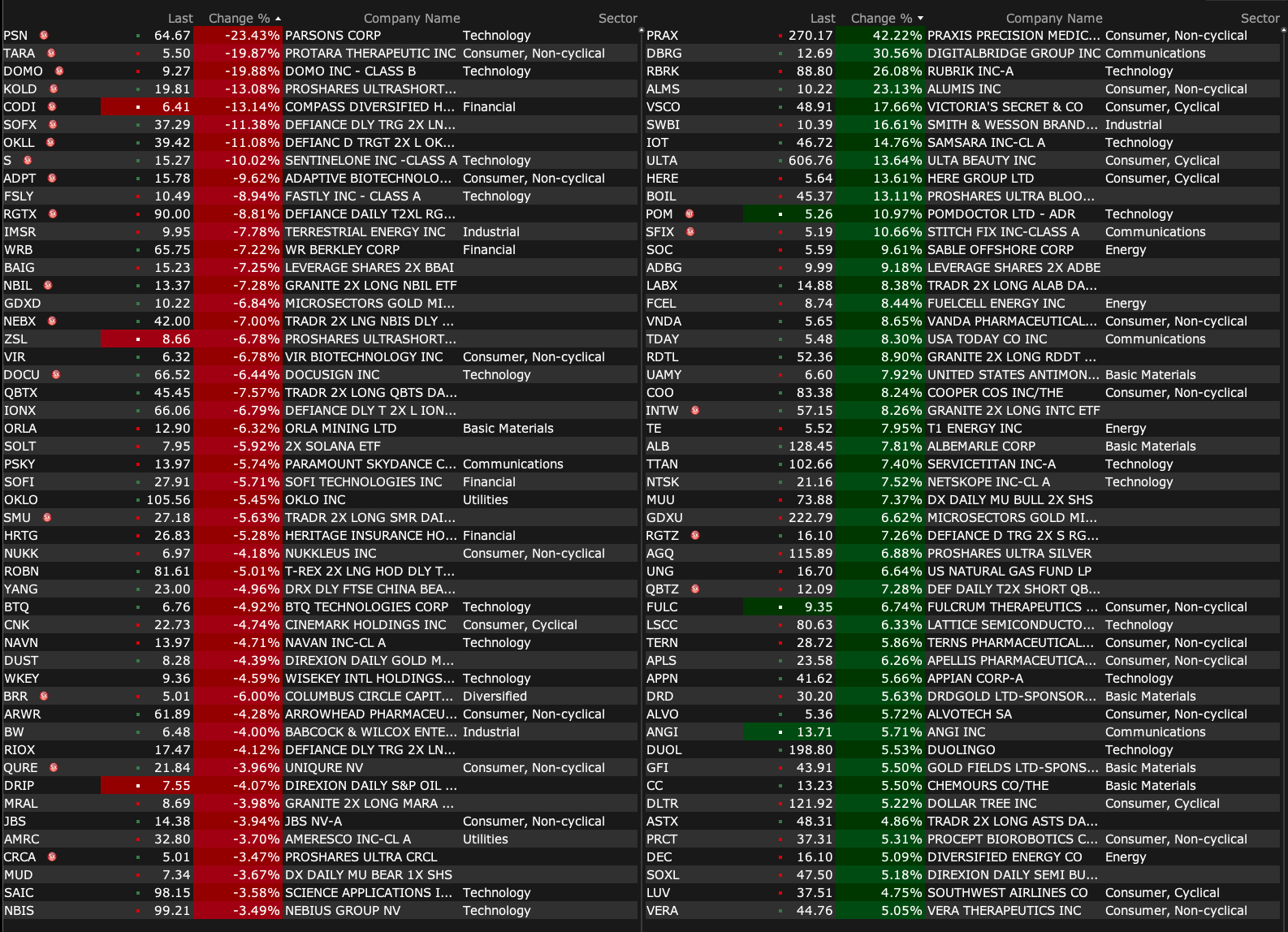

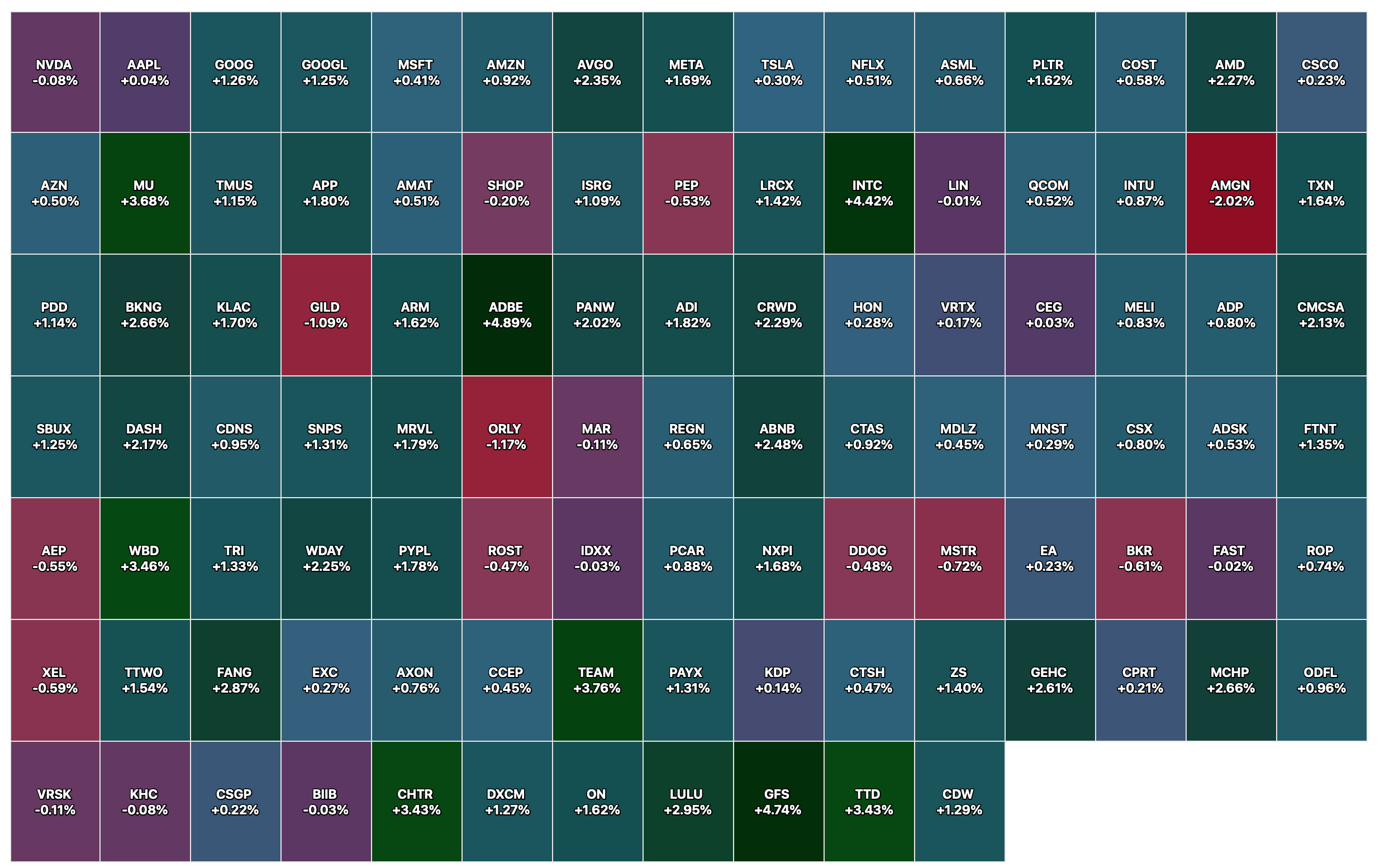

Friday's Closing S&P 500 Heat Map

BY Doug Kass · Dec 5, 2025, 4:50 PM EST

BY Doug Kass · Dec 5, 2025, 4:50 PM EST

- NYSE volume 6% below its one-month average;

- NASDAQ volume 9% below its one-month average

- VIX index: down 2.66% to 15.36

BY Doug Kass · Dec 5, 2025, 4:40 PM EST

BY Doug Kass · Dec 5, 2025, 3:15 PM EST

Scott Galloway's No Mercy/No Malice: The Cult of Therapy.

BY Doug Kass · Dec 5, 2025, 3:00 PM EST

Here are today's "things":

* I shorted index calls (twice) and covered both trades profitably.

* I shorted (SPY) / (QQQ) very early in the morning and covered for a profit during the trading session.

* I added to (JOET) short at $42.64.

* I added to (NVDA) short at $184.56.

* I shorted (JPM) at $317.09 and (MS) at $176.21.

* I added to (KMB) long at $103.19.

* I added to (PEP) long at $144.95.

BY Doug Kass · Dec 5, 2025, 2:45 PM EST

* LLM is ikely a commodity-like product — only the lower-cost player will win

* Nobody is fond of AI (except those companies that are betting a huge amount on it)

* Metafarce

Three points in my closing "More Tales" of the week:

* Finally, someone in Silicon Valley speaks the truth, the CEO and founder of Salesforce.com (CRM) .

LLMs are a commodity product. The lower-cost player will win (at what, I am not exactly sure) because the benefits are still less than clear. Barbell strategy. Chinese approach, do the same thing 99% as well for a fraction of the cost and capital and resource (power) consumption, while also trying a new approach that might actually work.

The U.S. economy, and U.S. policy, should not be bet on the high-cost players in a commodity industry for a product that is providing less value add than cement. The only people that want this to happen are the ones that have invested immense amounts of money in something that has turned out to not do what it was expected to do, and they have done it in the highest cost fashion possible in the race to be first and biggest. They should bear the cost of being wrong, not society:

* As far as society is concerned, this article is indicative. In a divided country, this is about the only thing people are unified on. Nobody, and I mean nobody, likes AI. Not the right, not the left, not the populists, and not the progressives.

Once again, the only people that like it are the ones that have bet money on it, and are making money selling their stock that has been run up based on it. This article is one more example. It is interesting, it is a political loser, yet it continues to be supported. This once again tells you the power that the donor class and technocrats have. There really are four branches of government:

The time has come to declare war on AI

* Remember the Metaverse, the last big thing? $77 billion down the drain so far and now Meta (META) is being rewarded for finally cutting the spending on the thing. At least they didn’t ask for a government bailout! Now they can focus on wasting more money on high-cost not-scaling generative AI with no path to AGI, while still selling scam ads that account for a massive portion of their economics:

Meta Plans to Shift Spending Away From the Metaverse

And for a little humor (back to the second bullet point above too):

https://www.youtube.com/watch?v=RcPthlvzMY8&feature=youtu.be

BY Doug Kass · Dec 5, 2025, 2:10 PM EST

BY Doug Kass · Dec 5, 2025, 1:38 PM EST

BY Doug Kass · Dec 5, 2025, 1:24 PM EST

Wolf Street howls about the CMBS market.

BY Doug Kass · Dec 5, 2025, 12:55 PM EST

From Peter Boockvar:

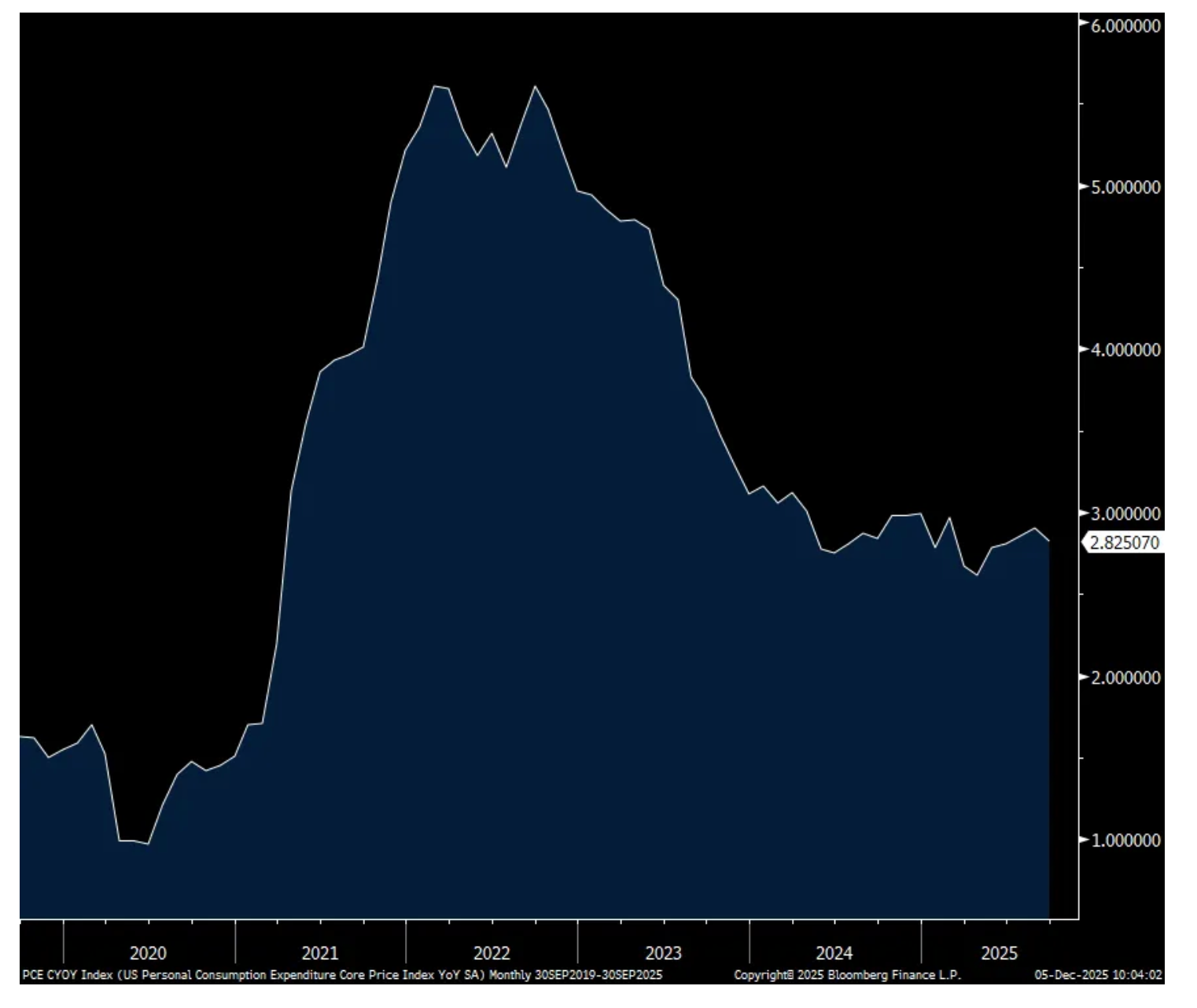

While obviously a very dated number, we’ll take any inflation read we can get. September headline PCE rose .3% m/o/m and 2.8% y/o/y while the core figure saw a .2% m/o/m increase and also a 2.8% y/o/y gain. Both are as expected. Goods prices, in part due to tariffs, picked up to a 1.4% y/o/y gain from .9% in August, .6% in July and June and vs .1% in May. Services inflation remains where most of the inflation is, rising 3.4% y/o/y but a slowdown from 3.6% in August and 3.5% in both July and June.

The income and spending figures were about as forecasted, up .4% and .3% respectively. As both saw similar gains, the savings rate held at 4.7%, matching the lowest since December 2024.

Bottom line, with the Fed relying on PCE but with older data, it will be really interesting with what comes of the dot plot. I say that because all year their long term REAL rate expectation is 1% and a rate cut relative to the 2.8% core inflation figure will take that REAL rate to below that. Thus, if the dot plot stays the same, Jay Powell might not be cutting rates again during the last three meetings of his term unless inflation decelerates further and/or the unemployment rises more. Which of course could happen but needs to in order to get more cuts I believe.

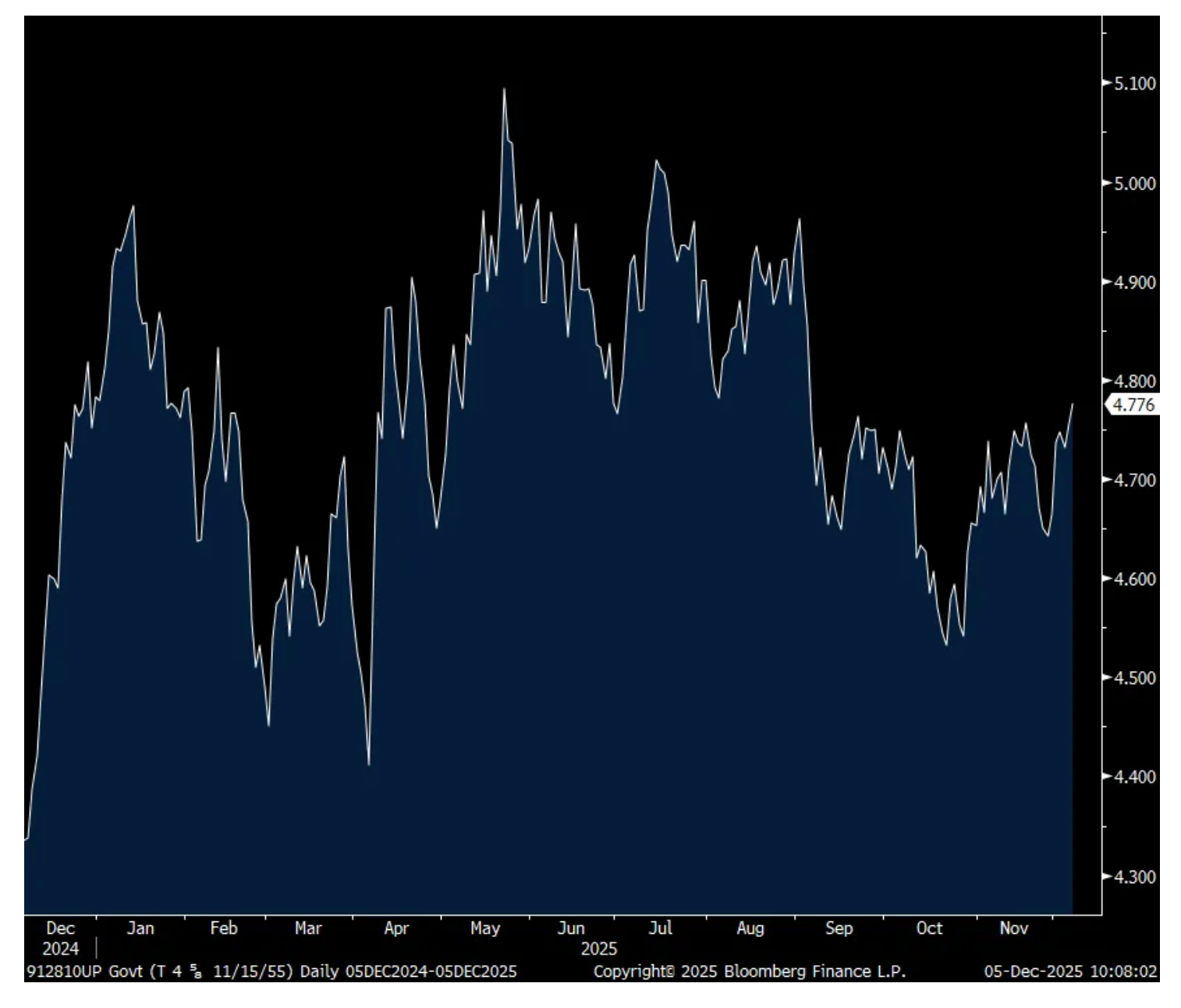

While about all in line, Treasury yields remain at the highs of the day with the 10 yr yield touching 4.12% and the 30 yr yield at 4.77-.78% which is quietly at the highest level since early September.

Core PCE y/o/y

30 yr Yield

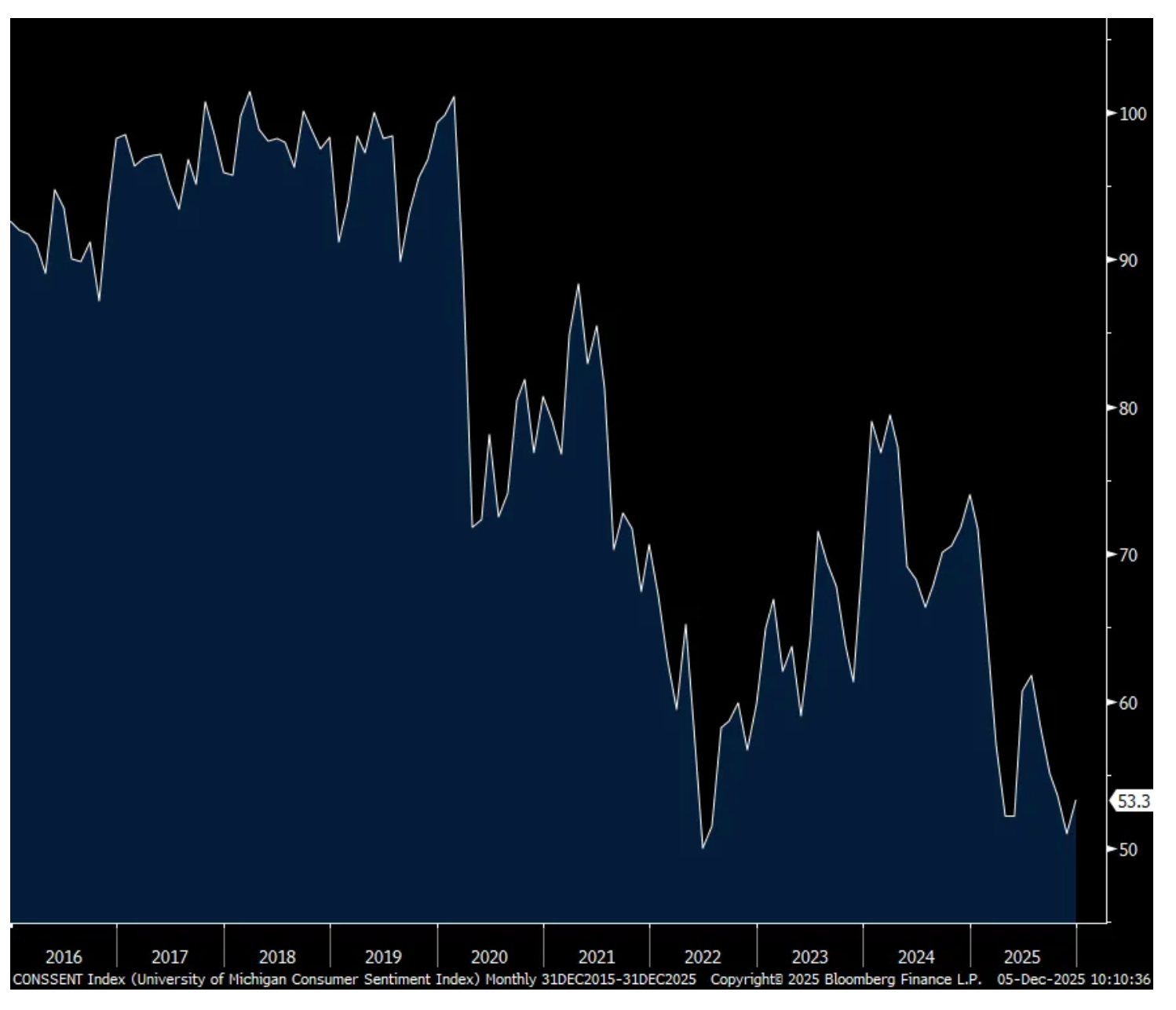

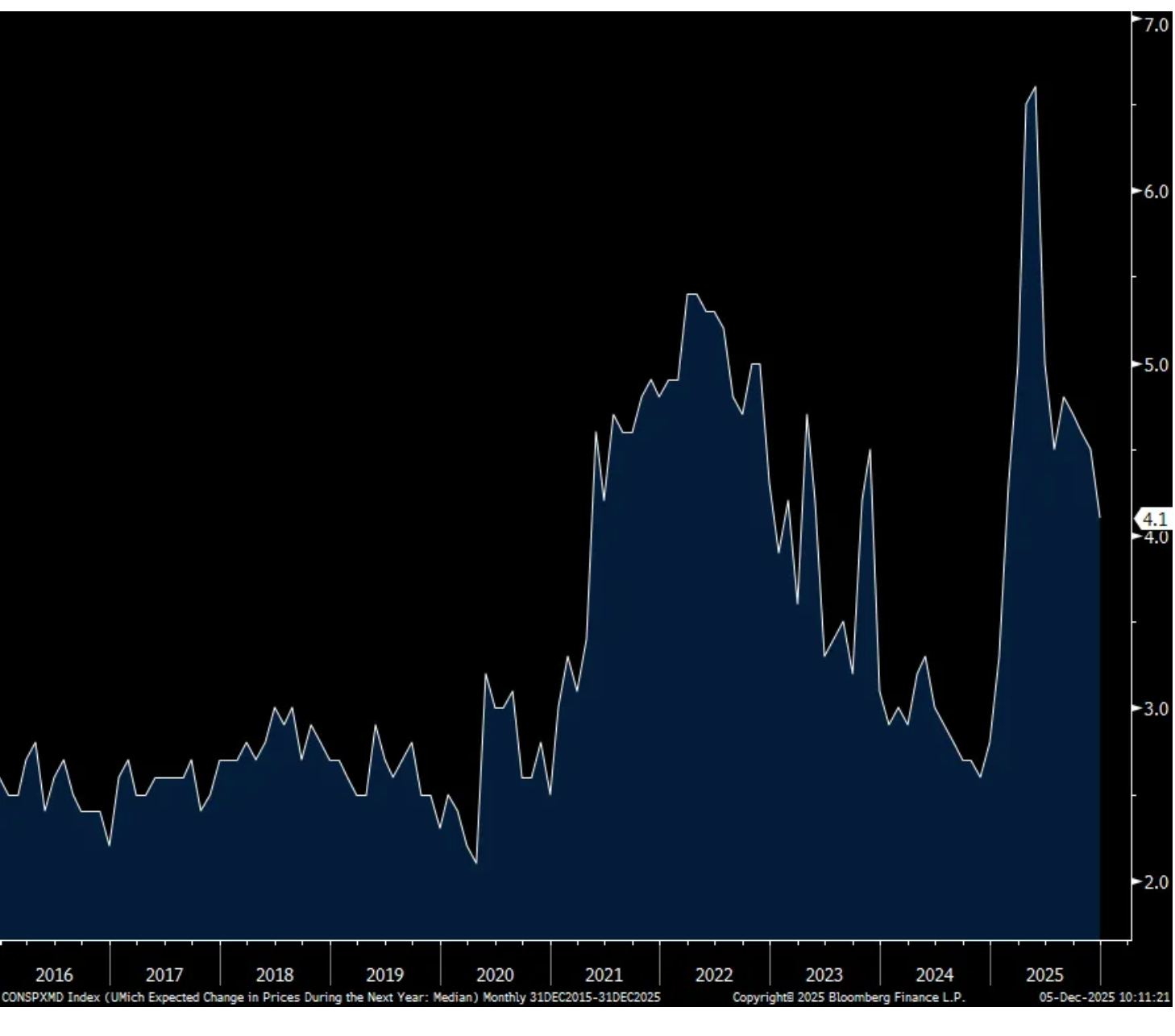

The December UoM consumer confidence index rose to 53.3 off one of the lowest reads on record of 51 in November. The estimate was 52. All of the gain was in the Expectations component which rose 4 pts m/o/m while Current Conditions were down a hair. Positively, one year inflation expectations fell to 4.1% from 4.5% and the 5-10 yr guess slipped to 3.2% from 3.4%, though both remain elevated.

After dropping by 8 pts in October, employment expectations rebounded by 9 pts but the UoM said the current level “remained relatively dismal.” The income component was negative for a 5th month at -6 vs -14 in October and -2 in September.

Spending intentions did fall with a 4 pt drop in homebuying plans and 1 pt dips for vehicles and major household items. Reflecting the growing stories of people taking their homes off the market, ‘good time to sell a house’ fell 6 pts to the lowest level since June 2020.

With respect to the topline confidence gain, UoM said “This month’s increase was concentrated primarily among younger consumers.”

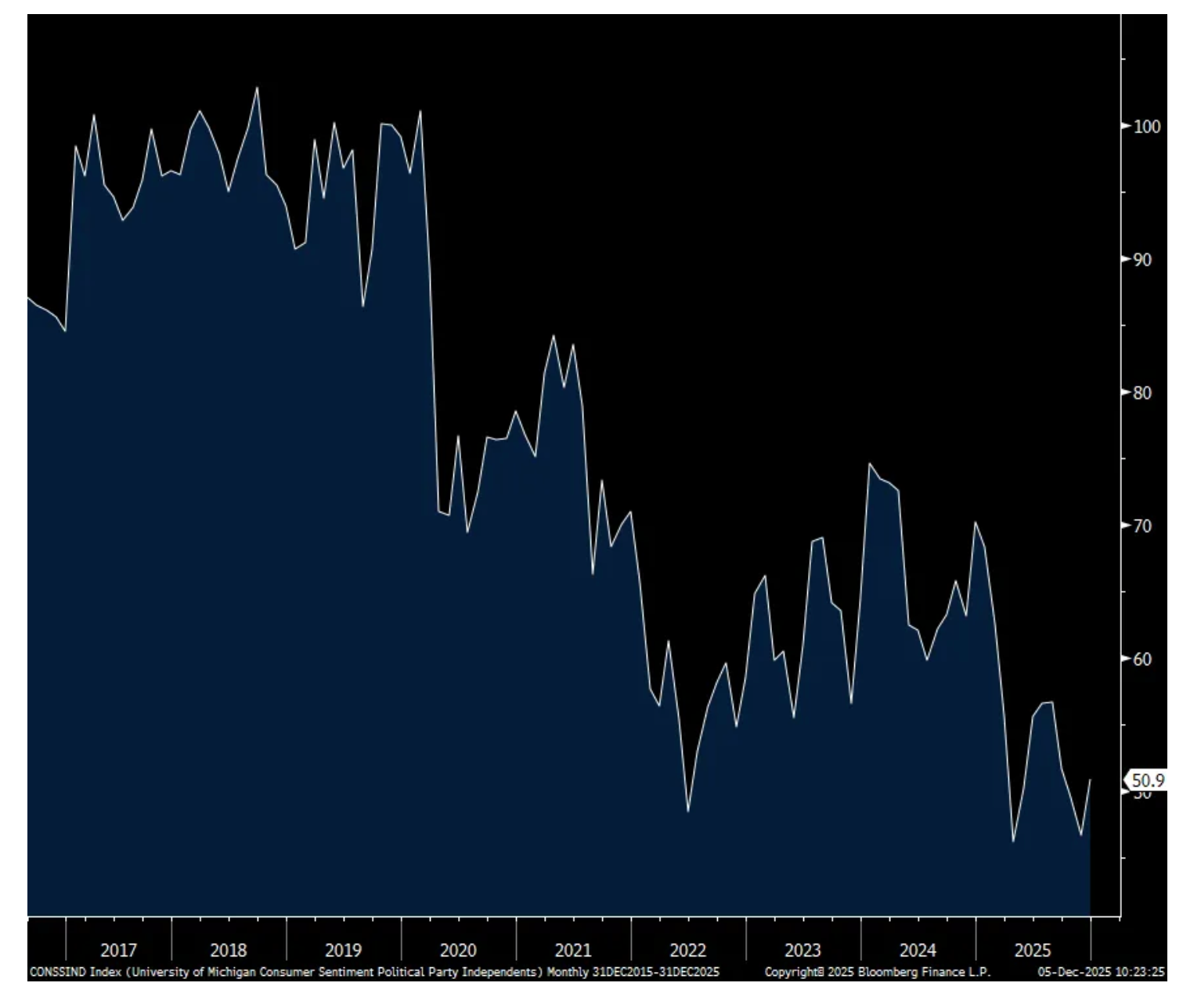

Isolating the political extremes, the confidence of Independents lifted to 50.9 from 46.7 in November, 49.5 in October and 51.7 in September and 56.7 in August.

The bottom line from UoM, “Consumers see modest improvements from November on a few dimensions, but the overall tenor of views is broadly somber, as consumers continue to cite the burden of high prices…consumers still expect elevated inflation to persist, even if they no longer anticipate an imminent surge. Many believe that the economic effects of tariffs have not yet been fully realized. About 54% provided unprompted comments about tariffs, down from May’s 66%, but still a clear majority.”

And finally on this, “Moreover, consumers remain frustrated by the persistence of high prices. About 47% of consumers this month spontaneously mentioned that high prices weighed down on their personal finances, unchanged from November and considerably higher than the 35% who mentioned this a year ago.”

I have nothing more to add as we know the pressure that higher inflation has put on lower to middle income consumers and where even upper income ones, particularly those making more than $100,000, are increasingly seeking value too.

UoM Consumer Confidence

One yr Inflation Expectations

Confidence of Independents

BY Doug Kass · Dec 5, 2025, 12:40 PM EST

With S&P cash up by less than +10 handles I am taking in the (SPY) and (QQQ) calls I sold higher this morning.

BY Doug Kass · Dec 5, 2025, 11:45 AM EST

* Nothing really matters

Is this the real life? Is this just fantasy?

Caught in a landslide, no escape from reality

Open your eyes, look up to the skies and see

I'm just a poor boy, I need no sympathy

Because I'm easy come, easy go

Little high, little low

Any way the wind blows doesn't really matter to me, to me- Queen, Queen – Bohemian Rhapsody (Official Video Remastered)

(TLT) makes a multi week low in price (and bonds make a multi week high in yields).

Carry on, carry on.

Nothing really matters...

BY Doug Kass · Dec 5, 2025, 11:39 AM EST

- NYSE volume 18% below its one-month average;

- Nasdaq volume 5% below its one-month average;

- VIX index: down 1.08% to 15.61

BY Doug Kass · Dec 5, 2025, 11:20 AM EST

I am adding to two financial shorts:

* (JPM) $317.31

* (MS) $176.60

BY Doug Kass · Dec 5, 2025, 10:26 AM EST

With S&P cash +23 handles I have moved to medium-sized (from small) in my Index call short positions.

BY Doug Kass · Dec 5, 2025, 10:05 AM EST

I shorted more (NVDA) in premarket at $184.56. (Sorry for the delay!)

BY Doug Kass · Dec 5, 2025, 9:43 AM EST

With S&P cash +18 handles I am shorting index calls.

BY Doug Kass · Dec 5, 2025, 9:37 AM EST

From Peter Boockvar:

The BoJ has now just about locked us into a December 19th rate hike. Bloomberg News is reporting that “Bank of Japan officials are ready to raise interest rates at a policy meeting later this month, provided there’s no major shock to the economy or financial markets in the meantime, according to people familiar with the matter.” And importantly too, “The central bank will also indicate it will continue to raise rates if its economic outlook is realized while remaining cautious on how far they will eventually push rates up, the people said.” The 2 yr yield was up another 2.7 bps to 1.05%, a fresh 18 yr high, though the yen is little changed after the slight bounce over the past few weeks. Global bond yields are a touch higher in response.

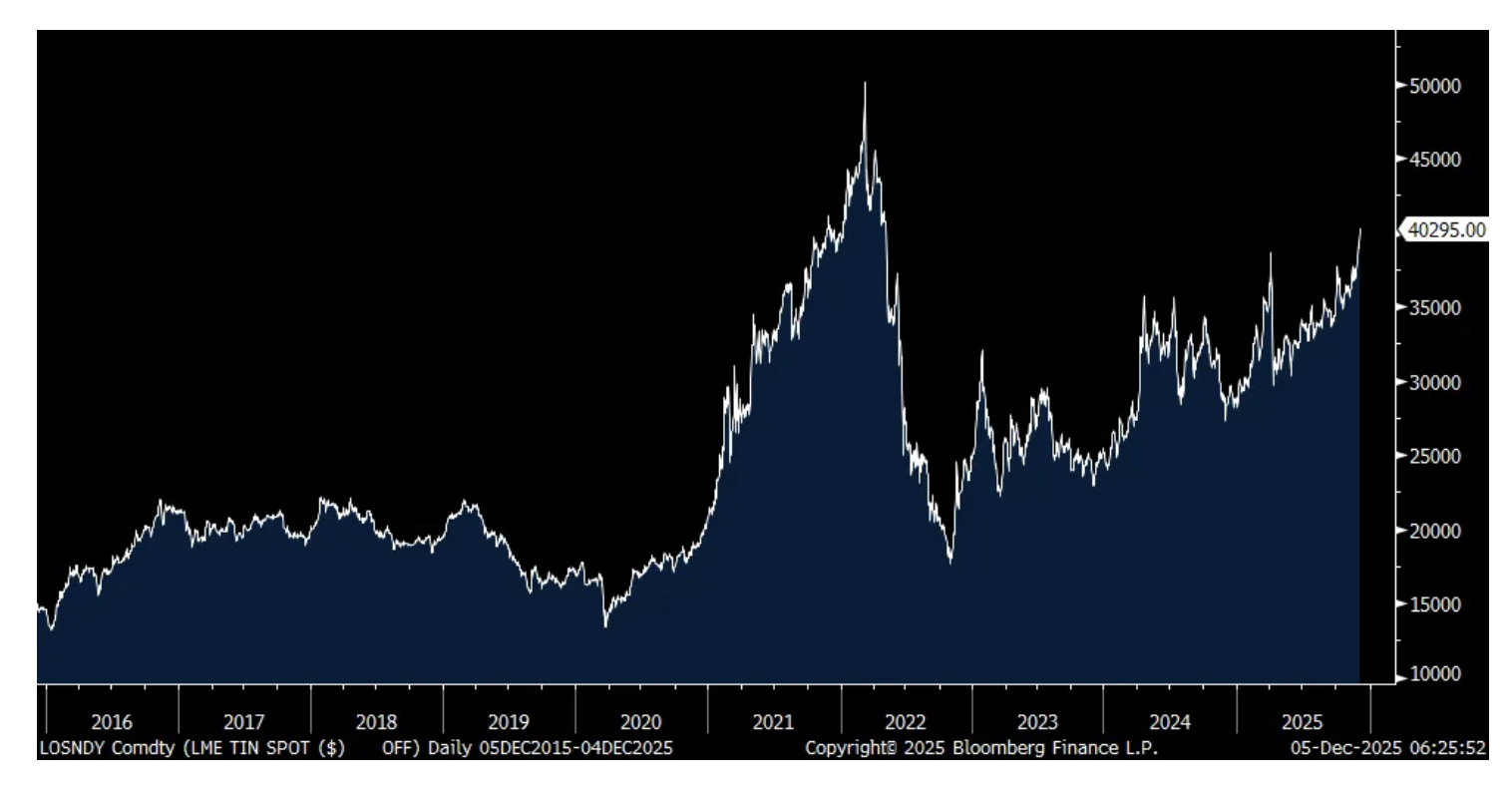

We talk copper, gold, silver but did you know that the price of tin yesterday closed at the highest level since April 2022. According to Gemini, “Tin is a critical mineral in data centers, primarily used as solder to create reliable electrical connections in circuit boards and other electronic components. It acts as a conductive glue that holds the digital infrastructure together.”

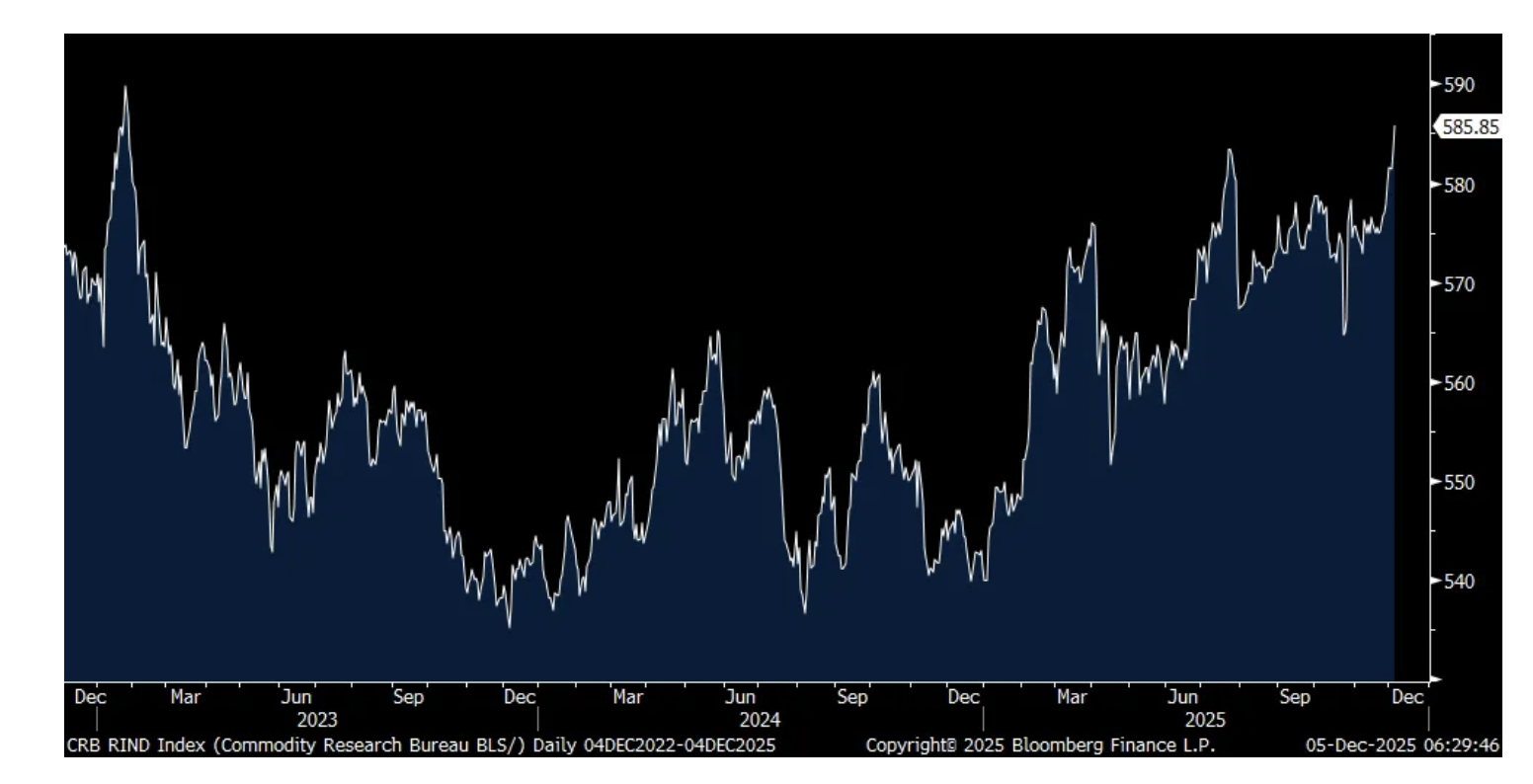

As for the CRB raw industrials index, it closed yesterday at the highest level since January 2023. This index includes everything from copper scrap, lead scrap, steel scrap, tin, and zinc to things used in textiles like burlap and cotton and also hides, rosin, rubber and tallow. Something to watch as the world splinters up and companies/countries hoard key raw materials, along with the need for important inputs to the data center/tech buildout.

Tin on the LME

CRB Raw Industrials Index

Company comments are still highlighting the extraordinarily mixed US economy and consumer.

Marriott was down 3.5% yesterday after speaking at a Barclays conference and said this:

“as we started the year, we were looking at overall RevPAR for the company globally that had a midpoint of 3. We are now where the midpoint is 2 for the year.”

“And I think where we’ve ended up is that group and BT (business travel) have ended up underperforming a little bit relative to the beginning of our year expectations, although I will say group RevPAR is still expected to be positive.”

“And that leisure has completely and utterly held up exactly where we thought it would be.”

With respect to BT, “I think, in many respects it’s more a function of the government cutbacks and government shutdown, uncertainty in general, smaller businesses trying to deal with margin pressures, etc...”

“So when you talk about October, October RevPAR was globally 2%, and that was absolutely right on the money relative to what we expected when we gave guidance at the end of Q3. The reality is though at the margin, the US was a little bit lower than expectations, and international was a little bit higher. The US was actually 20 bps down in the month of October. And I think you clearly saw that connected to continued uncertainty around the pace of the economy and kind of decisions around possible government shutdown, etc...And as we get into November, clearly the government shutdown extended longer than anyone expected. And I think that is part of what you’re seeing when you think about Q4 RevPAR overall.”

From Dollar General whose stock spiked by 14%:

“We grew market share in both dollars and units in highly consumable product sales once again during the quarter, in addition to growing market share in non-consumable product sales.”

“Same store sales increased 2.5% during the quarter, driven by customer traffic. The average basket size essentially was flat. Within the basket, an increase in average unit retail price per item was offset by fewer items on average. This traffic and basket composition is consistent with what we have historically observed when our core customer feels more pressured on their spending as they come in more often but have smaller basket sizes.”

“From a monthly cadence perspective, all three periods were positive, led by August...And despite the delay in SNAP payments in early November, we are pleased with our strong sales performance to begin quarter four.”

“we’re pleased to see growth once again in our total customer count, with disproportion of growth coming from higher income households.” Something we heard from Dollar Tree, Walmart, and others for many quarters now, as we know.

“we continue to be pleased with our pricing positions, which remains within our targeted range of 3 to 4 percentage points on average for mass retailers.”

From Kroger and whose stock fell almost 5%:

“Macroeconomic uncertainty continues to influence customer behavior, and we’re seeing a split across income groups. Spending from higher income households continue strong while middle income customers are feeling increased pressure. Similar to what we’ve seen from lower income households over the past several quarters. They’re making smaller, more frequent trips to manage budgets, and they are cutting back on discretionary purchases.”

“Food spend has been more resilient than non-food spend. Categories like natural and organics continue to perform well, reflecting continued interest in healthy and premium options. At the same time, customers are turning to promotions in Our Brands as smart ways to save without sacrificing quality.”

“Inflation and uncertainty around government funding, combined with the pause in SNAP benefits during the final weeks of the quarter, added incremental pressure to our third quarter identical sales without fuel.”

Ulta Beauty is jumping pre market after a good quarter and we’ve heard from a variety of retailers for multiple quarters that beauty spend is a priority of consumers. They said of note:

Comps grew 6.3% with “Positive comps across all categories and channels, with notable double digit strength in our e-commerce results.”

They also gained market share in mass and prestige beauty.

“Despite a softening in overall consumer confidence in Q3, beauty engagement remained healthy. During the third quarter, both mass and prestige beauty markets delivered mid single digit growth, according to Circana.”

Tariff induced price increases are still flowing thru the supply chains and they said “we are starting to see more market wide price increases come through in this with select brands versus Q2.”

“there were plenty of publicly traded companies that announced that they were taking price increases, Elf, Coty, and Helen of Troy, just to name a few, that we were seeing price increases with this quarter.”

MMM had comments on the consumer and other things at the Goldman industrials conference yesterday.

“auto has been relatively soft. The build rate has been up, but it’s mostly been China and not the US, and I think all regions are expected to be down in the build rate in the fourth quarter.”

“Electronics has been pretty good, aerospace and defense has been pretty decent for us...The abrasives business has been challenged in the last couple of years...Our roofing granules business has been under some pressure.”

“So, we’re seeing some pressure in a couple of parts of the business, but the consumer has been relatively weak all year and not getting much better going into Q4.”

Overseas, the Reserve Bank of India cut rates by 25 bps to 5.25% as expected and Governor Malhotra implied more rate cuts could come. He referred to the Indian economy as in a “rare Goldilocks period.”

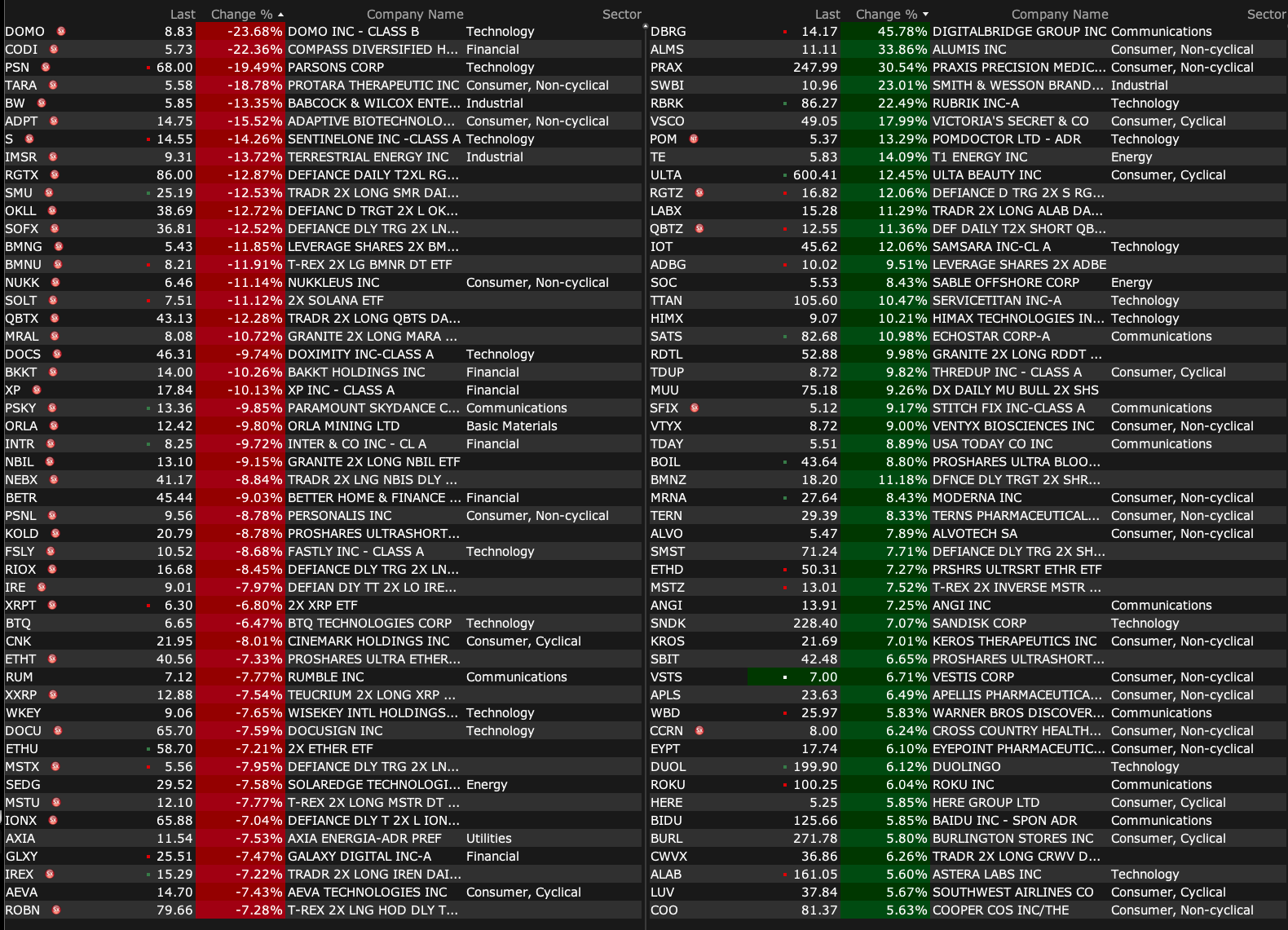

BY Doug Kass · Dec 5, 2025, 9:35 AM EST

-PRAX +32% (announces Positive Pre-NDA Meeting with FDA for Ulixacaltamide in Essential Tremor)

-RBRK +18% (earnings, guidance)

-COO +13% (earnings, guidance)

-QCLS +13% (momentum)

-VSCO +13% (earnings, guidance)

-ZUMZ +13% (earnings, guidance)

-TTAN +9.4% (earnings, guidance)

-CHPT +7.4% (earnings, guidance)

-ULTA +7.1% (earnings, guidance)

-DNA +5.3% (selected by PNNL to Deliver a Modular, High‑Throughput Phenotyping Platform for DOE's M2PC Under $47M Contract)

-IDT +5.0% (earnings)

-NFE +5.0% (receives approval for Milestone Agreement for Long-Term Gas Supply with Puerto Rican Government)

-KNOP +4.4% (earnings)

-WBD +4.3% (confirms to be acquired by Netflix for $23.25 cash + $4.50 Netflix stock per WBD shr)

-MP +3.1% (Morgan Stanley Raised MP to Overweight from Equal Weight, price target: $71)

-SWBI +2.8% (earnings)

-SFIX +2.1% (earnings, guidance)

-SPWH -22% (earnings, guidance)

-PLRZ -19% (entered into a securities purchase agreement for 552.3K shares at $9.00/shr)

-PSN -19% (loses potential contract as FAA selects Peraton for air traffic control system overhaul)

-DOMO -18% (earnings, guidance)

-AGX -13% (earnings)

-HPE -9.6% (earnings, guidance)

-S -8.2% (earnings, guidance)

-DOCU -7.7% (earnings, guidance)

-SOFI -7.3% (prices 54.5M shares at $27.50/shr)

-CODI -5.2% (guidance)

-OKLO -4.6% (enters $1.5B ATM equity offering program)

-NFLX -4.2% (acquiring WBD for $23.25 cash + $4.50 Netflix stock per WBD shr)

-PSKY -2.4% (weakness following NFLX/WBD deal)

-SYM -2.0% (prices 10M shares at $55/share)

BY Doug Kass · Dec 5, 2025, 9:15 AM EST

BY Doug Kass · Dec 5, 2025, 9:05 AM EST

* (SPY) $684.26

* (QQQ) $622.80

BY Doug Kass · Dec 5, 2025, 8:58 AM EST

BY Doug Kass · Dec 5, 2025, 8:39 AM EST

* S&P futures are starting my trading day at +15 handles (around 3:30 AM)

* Despite that I am being emboldened on the short side...

We started Thursday morning by citing that despite an improvement in market breadth — the potential unraveling of the AI trade, rising global interest rates and climbing bullish investor sentiment — as reasons to expand our net short exposure.

Those conditions continue to be supportive of expanding shorts — even more so today than yesterday:

* Despite the one-off move higher in Meta (META) (we used that strength to sell our long at $682 (+$42 on the day), most of the Mag 7 was weaker in Thursday's trading session.

* Global interest rates continue to firm:

With the recent rise in rates, the equity risk premium has turned into an equity risk DISCOUNT. This means that investors are assigning more risk to bonds than to equities!

* At the close of trading yesterday, the S&P Short Range Oscillator climbed from 4.06% to 4.60%. That is a deepening overbought.

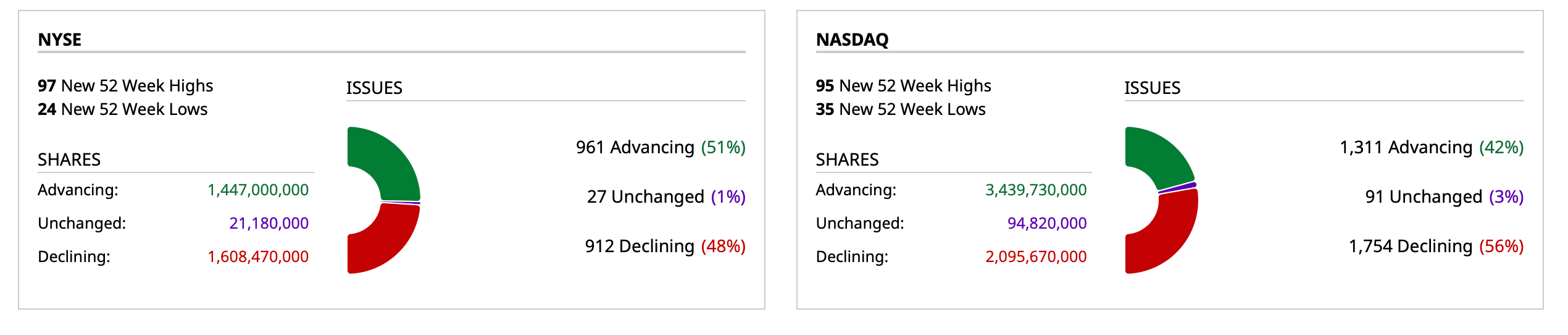

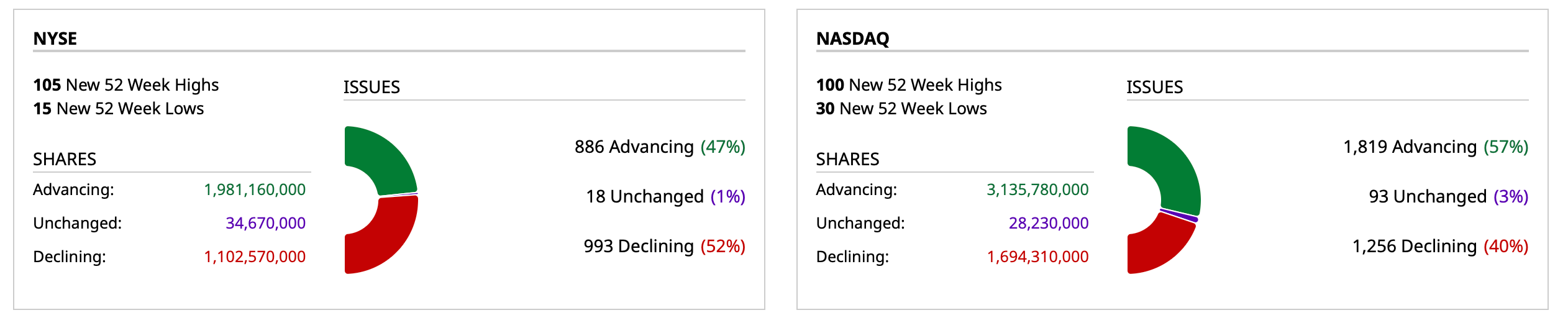

Meanwhile, though financials were the world's fair and The Russell Index crowed again, overall market breadth cooled off from Thursday — with declining issues outnumbering advancing issues on the NYSE and the Nasdaq at only a positive 1.5:1 ratio:

Finally, here is some good data on the LEI/CEI ratio from my friend Lance Roberts, indicating an economic warning signpost:

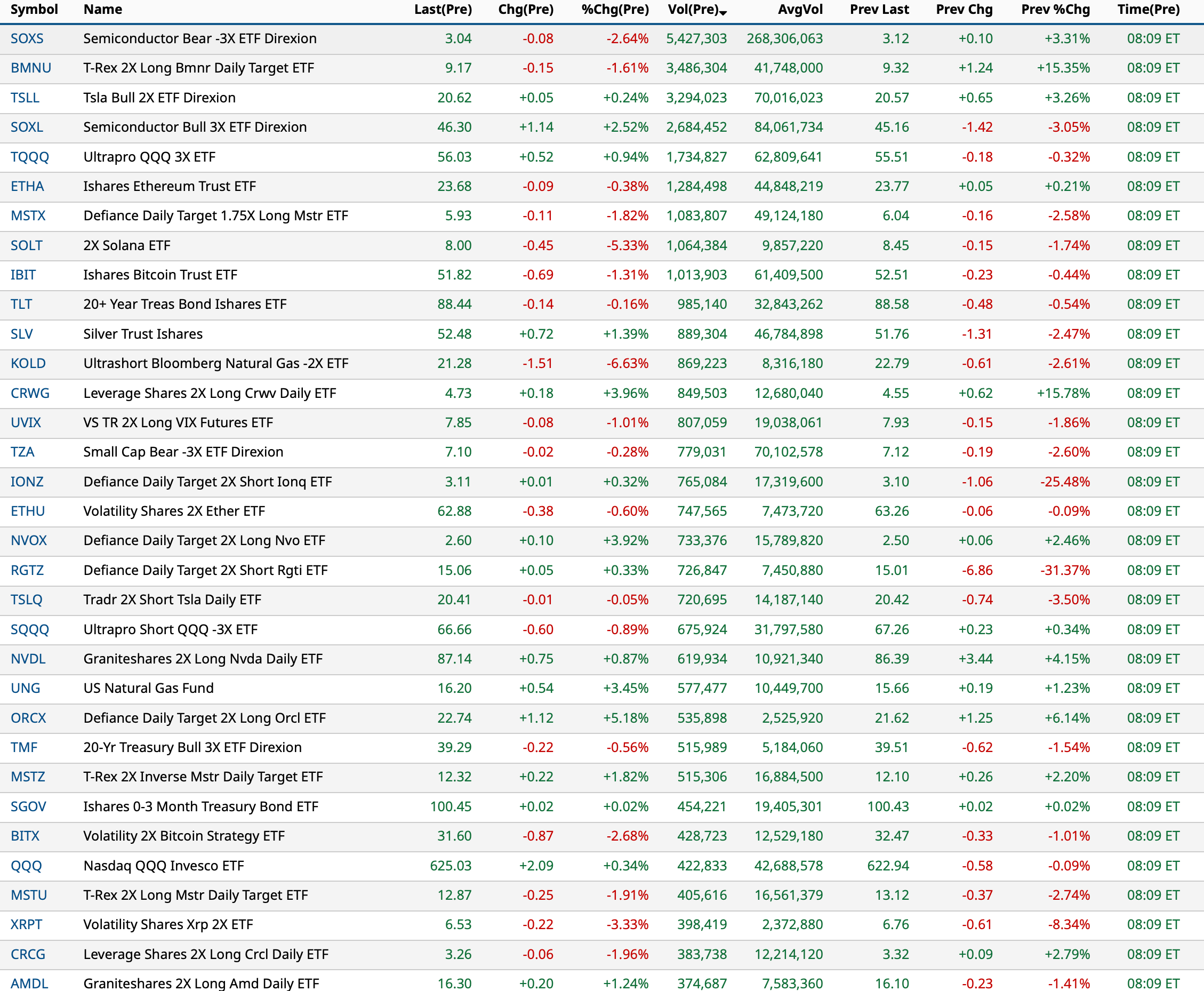

Before I recap Thursday's comments, I want to again emphasize how few are discussing the potentially adverse consequences of changing market structure (and the proliferation of leveraged ETFs):

Yesterday's opener:

* A rapid rotation characterized Wednesday's action (beneficiaries were the Russell and financials)

* As the AI trade (representing over 40% of the S&P Index) looks like it could be unravelling

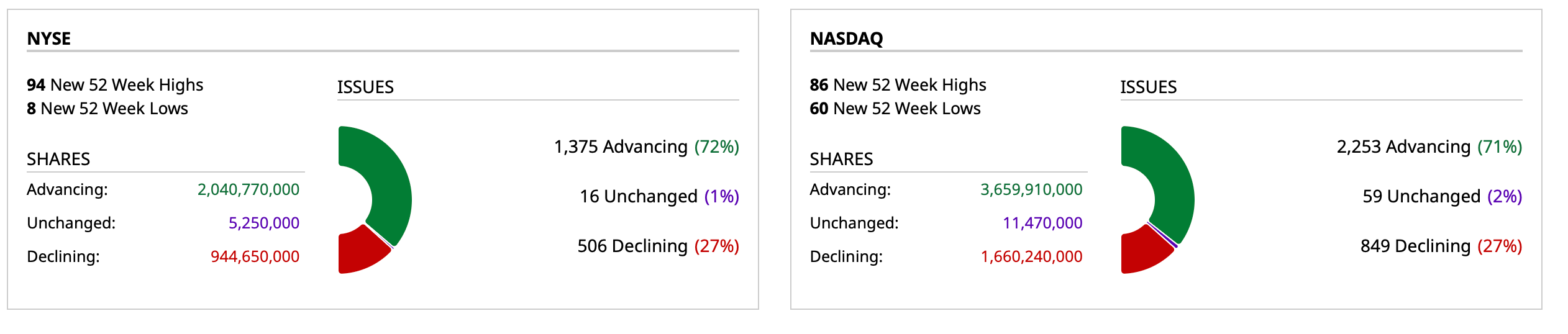

On Wednesday market breadth improved as technology gave way in favor of the Russell Index and financials:

Though the move in financials was massive, I believe the move in financials will be restricted by historically high valuations. (JPMorgan (JPM) now trades at nearly 3x tangible book value).

With the Japanese bond market (still weakening, above) and providing a "floor" to U.S. interest rates — the equity risk premium (as I noted in my recent market update) has become an equity risk discount. This ERP status, virtually at the lowest level in three decades, is not a good launching point for future investment returns.

Moreover, the AI trade (which comprises about 42% of the S&P index) seems to be growing frayed at the edges and may be growing older with age as some of my fundamental concerns ("More Tales From Nvidia") may be emerging.

Finally, with equities now in a deeper overbought (S&P Oscillator is over 4.00%), I think the up move this year may be at the beginning of the end and not the end of the beginning.

As I also mentioned yesterday, rising volatility may be an important market feature going forward:

Does Higher Stock Market Volatility Lie Ahead?

I raised my net short exposure yesterday.

Position: Short SPY calls (M), QQQ calls (M)

By Doug Kass Dec 4, 2025 7:34 AM EST

BY Doug Kass · Dec 5, 2025, 8:00 AM EST

* That have no value added...

BY Doug Kass · Dec 5, 2025, 7:15 AM EST

* What could go wrong, here?

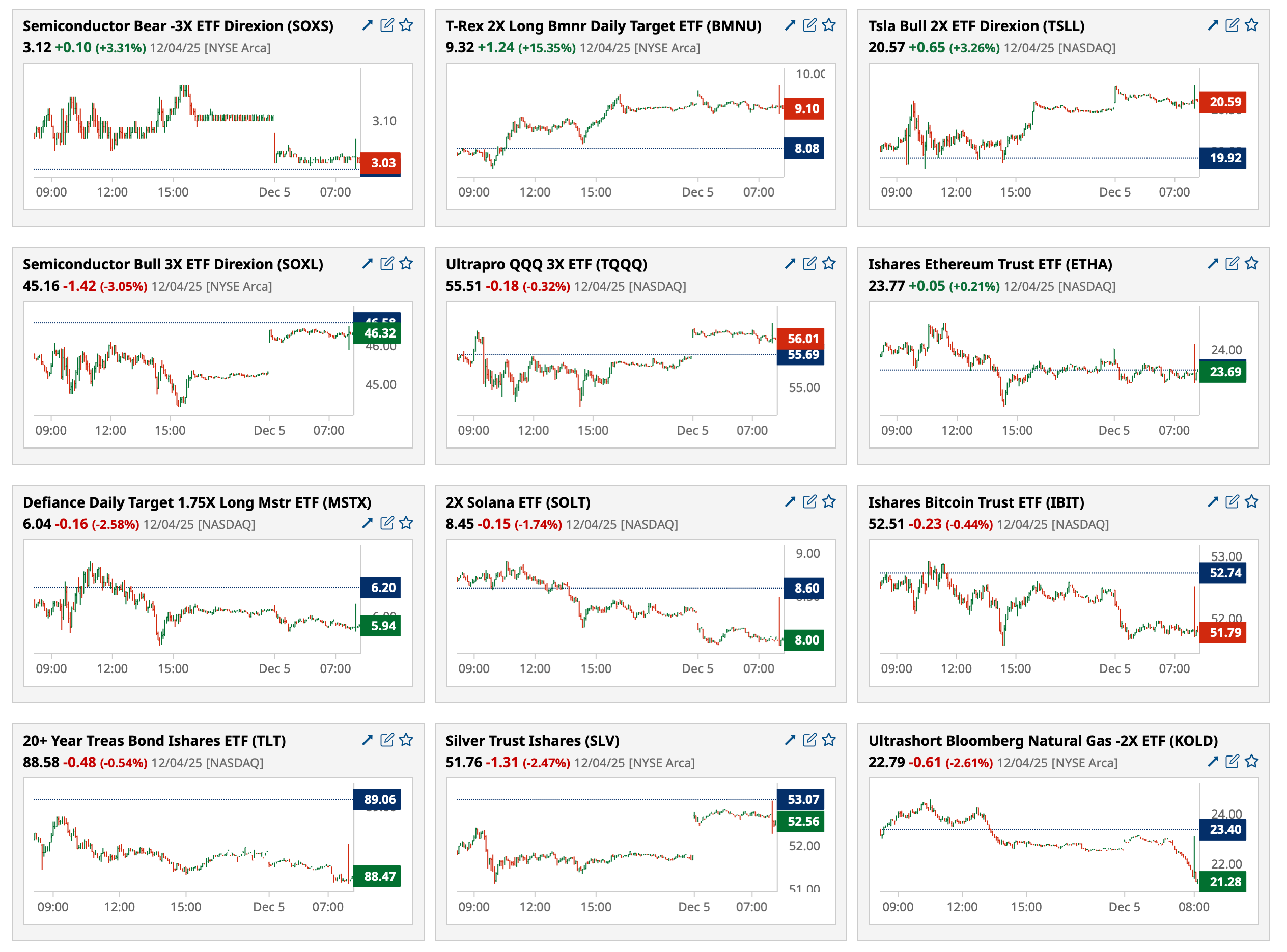

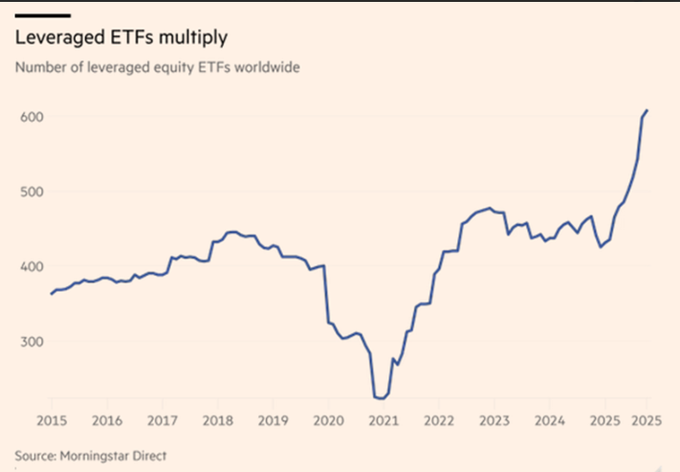

It isn't dangerous enough that leveraged ETFs are multiplying geometrically:

Our markets may be doomed as an often featured guest on CNBC, MrBeast, plans to launch a financial services platform:

BY Doug Kass · Dec 5, 2025, 7:00 AM EST

Bonus — Here are some great links:

Energy Set to Lead the Next Rotation

BY Doug Kass · Dec 5, 2025, 6:45 AM EST

BY Doug Kass · Dec 5, 2025, 6:35 AM EST

BY Doug Kass · Dec 5, 2025, 6:25 AM EST

BY Doug Kass · Dec 5, 2025, 6:15 AM EST

BY Doug Kass · Dec 5, 2025, 6:05 AM EST

The S&P Short Range Indicator stands at 4.60% vs. 4.06% — that is well into the overbought.

BY Doug Kass · Dec 5, 2025, 5:55 AM EST

Back shorting index common:

* (SPY) $686.14

* (QQQ) $625.95

BY Doug Kass · Dec 5, 2025, 5:45 AM EST