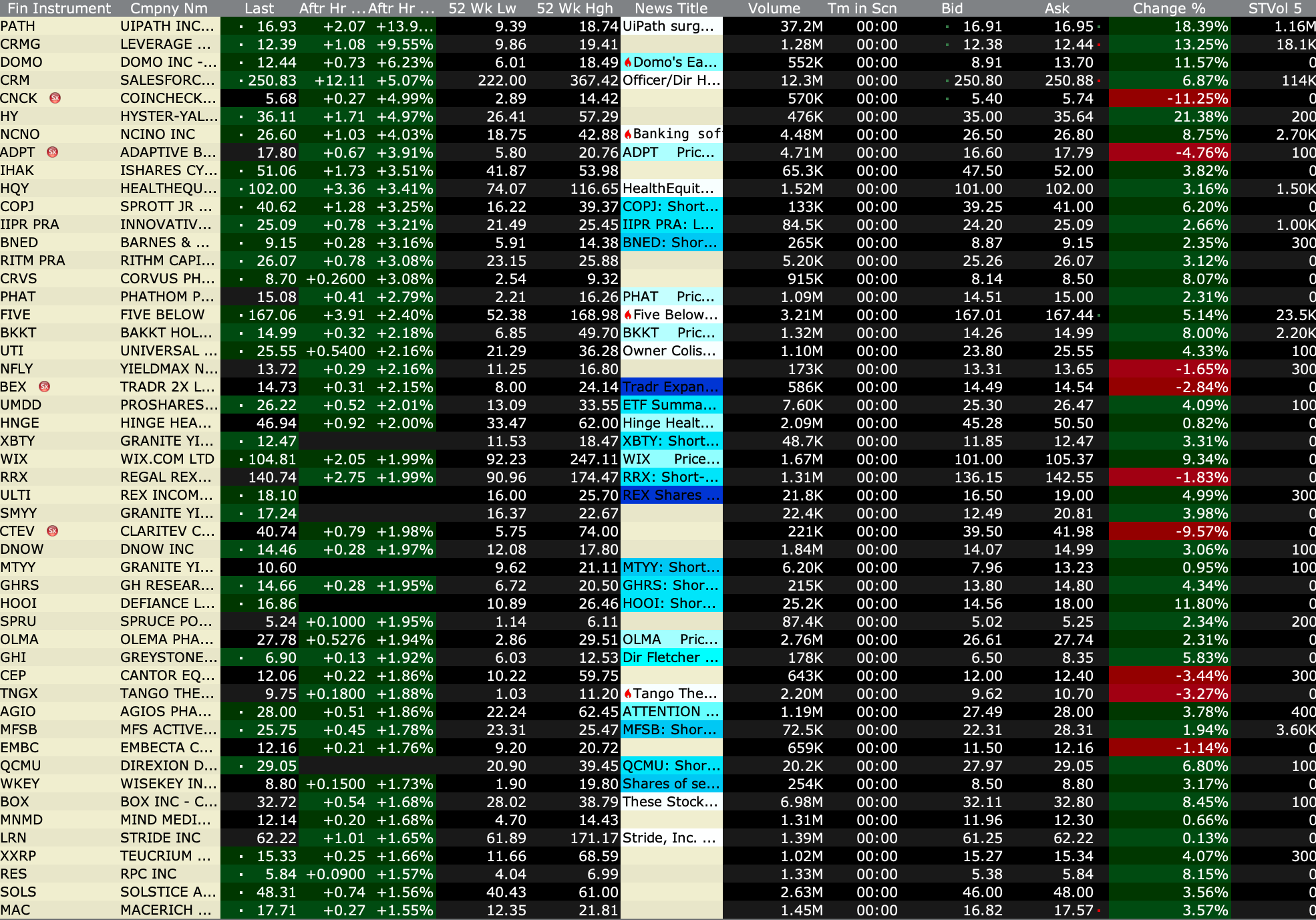

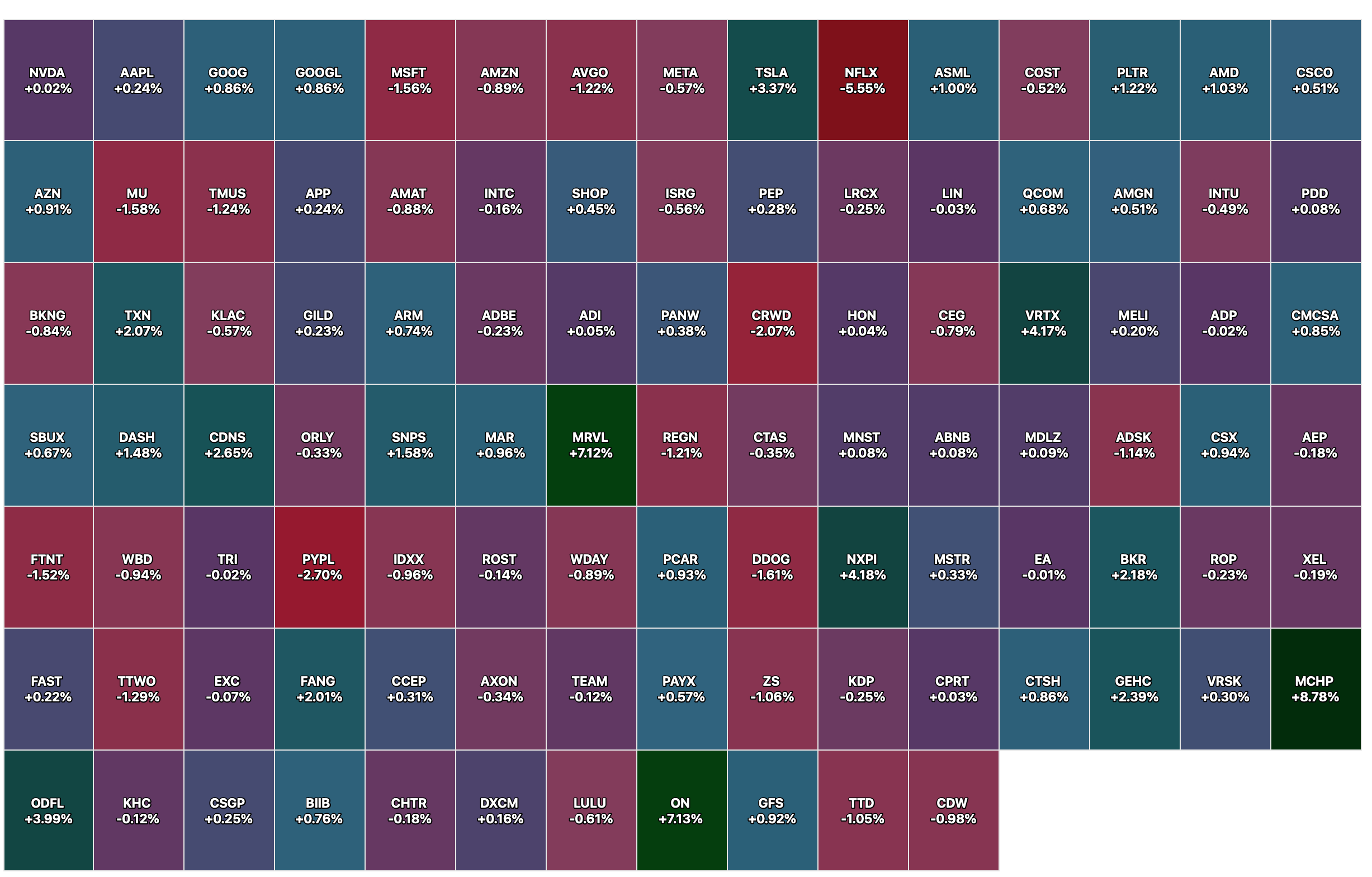

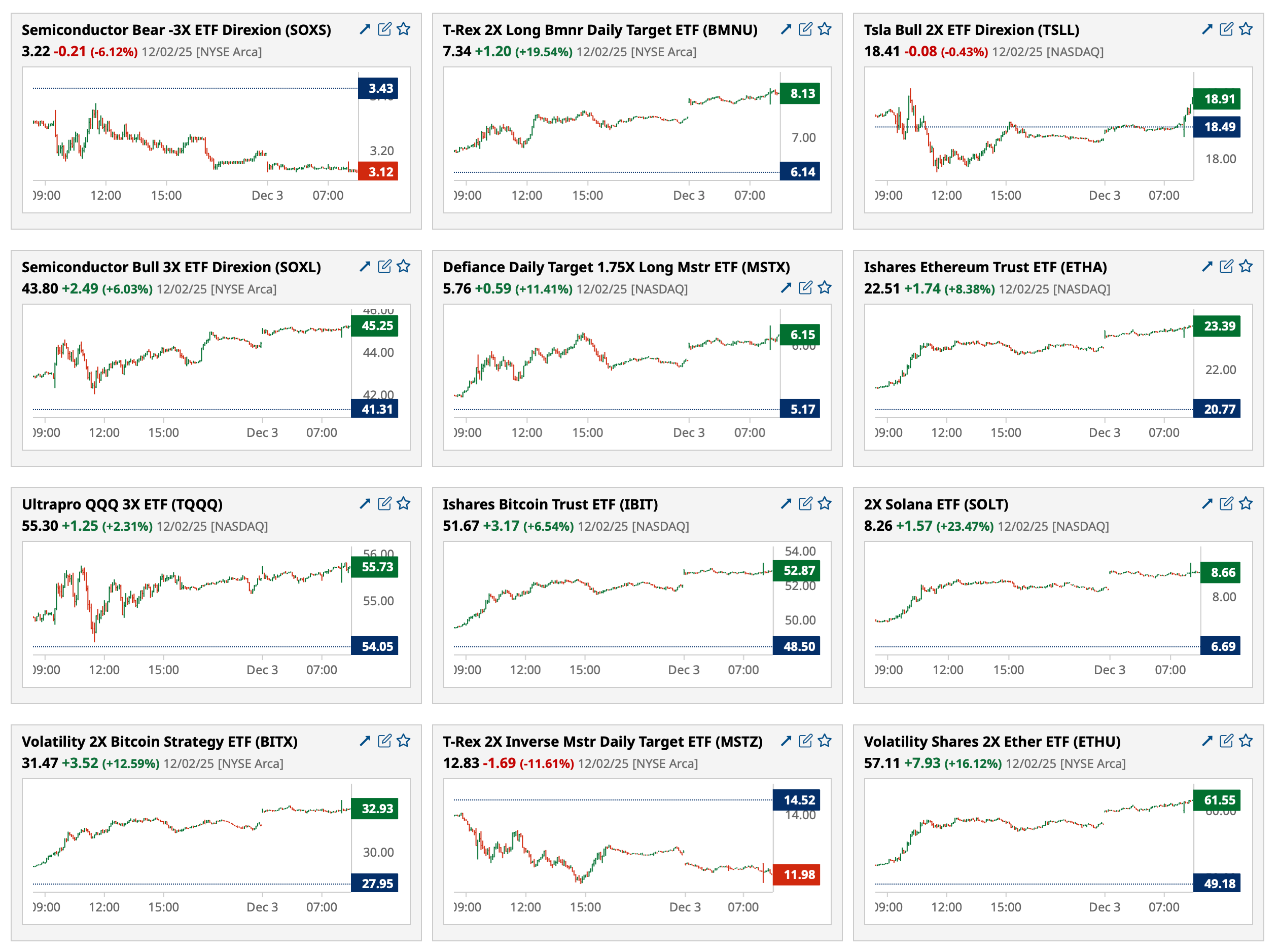

After-Hours Gainers and Losers

After-Hours % Gainers

After-Hours % Losers

BY Doug Kass · Dec 3, 2025, 4:55 PM EST

BY Doug Kass · Dec 3, 2025, 4:55 PM EST

BY Doug Kass · Dec 3, 2025, 4:45 PM EST

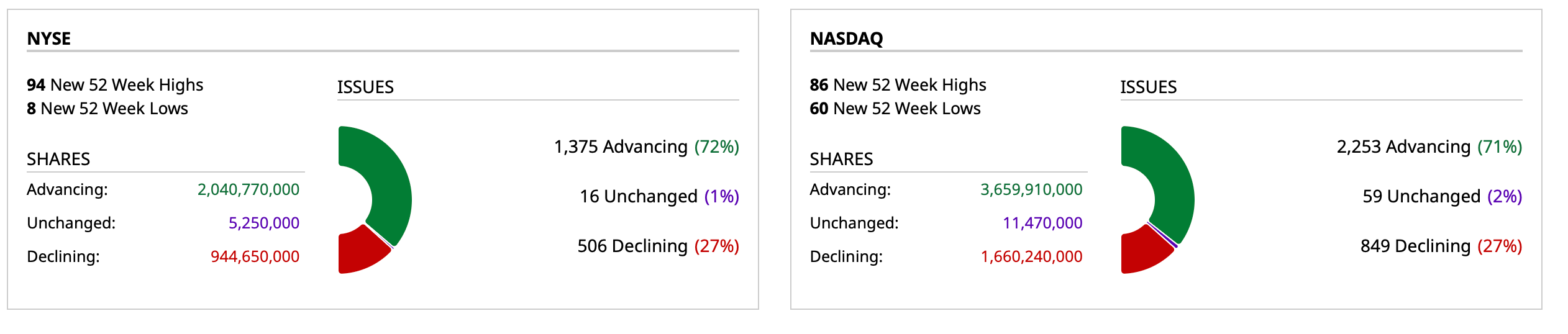

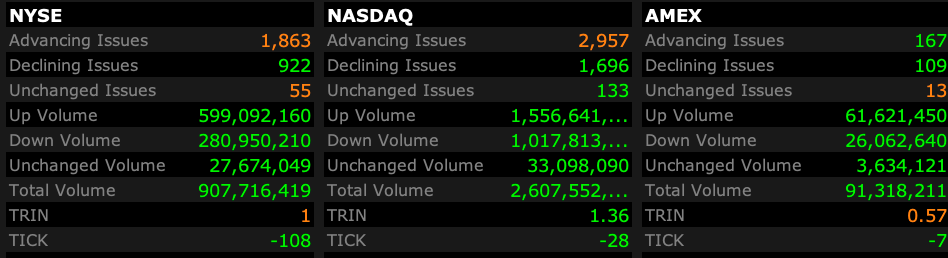

- NYSE volume 13% below its one-month average

- NASDAQ volume 16% below its one-month average

- VIX index: down 3.07% to 16.08

BY Doug Kass · Dec 3, 2025, 4:40 PM EST

BY Doug Kass · Dec 3, 2025, 2:25 PM EST

lonestar

49 minutes ago

Doug, this comment isn't to be a cheerleader for you or defend you from some of the comments I've read which are critical of you not capturing day to day trends (i.e. crypto up after dropping 30% of it's value). What I love and pay for on this site is a consistency and a narrative that isn't based upon momentum, mania or fashion but rather one of rational logic. I work in the cpu and gpu land, and develop on Hopper and Blackwell, I'm intimately familiar with the mania, lack of reliability and power consumption story that doesn't add up. You've written 150+ articles (sometimes when it's up, sometimes when it's down) and it shows commitment when the wind is at your back or in the front. I've questioned people here as to PLTR, MSTR and other liquid investments and I respect their willingness to "trade" with the masses and momentum even though there are no fundamentals to believe in their quality. That's just not my cup of tea but you also call out these as well which of course I personally like but I also respect because you're raising awareness to those sheep which will get slaughtered on the way out when those trading get out of these positions. Lastly, another thing you're criticized for, is the critique of financial media. This is another illustration of you in the sheep dog role, calling out their hypocrisy. So many people are on TV presenting assurances as to the future (Tom Lee, Michael Saylor, etc.) and people are going to be hurt. My only regret is more people don't get the chance to read your daily message and educate themselves, not by being a follower of Doug Kass but by reading, thinking and vetting investment choices upon reason. Thanks Doug for being the sheep dog

https://youtu.be/uxZ0UZf0mkk?si=eGSTIZkXFACj9S0u

BY Doug Kass · Dec 3, 2025, 12:45 PM EST

My older dog, Ollie, just had a seizure - I am at the Vet now and will not likely be returning today.

BY Doug Kass · Dec 3, 2025, 12:00 PM EST

BY Doug Kass · Dec 3, 2025, 11:35 AM EST

From Peter Boockvar:

ADP’s November private sector payroll change was down 32k vs the estimate of up 10k and vs the October print of 47k (revised up by 5k). The biggest labor market pain point continues to be small business which shed a large 120k people. Medium sized businesses, those with 50-499 employees, hired a net 51k and larger companies with an employee size above that added 39k.

Understand that small business hiring really started to slow in April and I attribute some of this to tariffs and the higher cost of doing business that small companies are much less able to absorb. The natural reaction is to cut costs elsewhere and we know that labor is their biggest cost.

The distribution of job changes was highly mixed with gains seen in education/health services again leading the way, followed by leisure/hospitality and natural resources/mining on the goods side. Trade/transportation/utilities added 1k. Job losses were seen in professional/business services, information, financial services, construction and manufacturing.

On the wage side, for ‘job stayers’ pay rose 4.4% y/o/y vs 4.5% in the month before. For ‘job changers’, wages rose 6.3% y/o/y vs 6.7% in October. Levels that are still good but moderating.

The bottom line from ADP was succinct, “Hiring has been choppy of late as employers weather cautious consumers and an uncertain macroeconomic environment.”

BY Doug Kass · Dec 3, 2025, 11:20 AM EST

BY Doug Kass · Dec 3, 2025, 11:15 AM EST

BY Doug Kass · Dec 3, 2025, 11:00 AM EST

BY Doug Kass · Dec 3, 2025, 10:29 AM EST

BY Doug Kass · Dec 3, 2025, 10:10 AM EST

From Peter Boockvar:

What stood out to me yesterday news wise was what the CFO of Procter & Gamble said at the MS consumer & retail conference.

After talking about strength in Latin America, China and even share growth in Western Europe, they said this about the US, “I think the context in the US is more volatile, probably the most volatile we’ve seen in a long time. There were a few elements that we knew coming into quarter two out of the last earnings call. We knew the consumer was more nervous and cautious. We knew that there was a stronger competitive environment, and we also knew that we had a stronger base period with consumer loading due to two port strikes in the base, where consumers stocked up in fear of product rationing. So all of those things were known.”

“What we didn’t know was obviously the incremental context that was provided with the government shutdown, SNAP benefits, etc...And you can see that in the macro growth in our categories in quarter two. Our most recent reading has the category down both in volume and in value significantly in October. I don’t expect November to be materially different. So, as you say, that sets a tougher context for the US business.” I bolded for emphasis.

Also on the consumer, but certainly from a different angle was the earnings report from Signet Jewelers and whose stock fell 7% yesterday. They saw a comp gain of 3% and “Our three largest brands, Kay, Zales and Jared, delivered a combined same store sale performance of 6% to last year. That reflects our intentional focus on the core of our business with growth in both bridal and fashion categories.”

That said, their guidance was muted. “We believe it prudent to have a cautious approach to guidance, given we’ve seen softer traffic in the past five weeks, particularly among brands with more exposure to lower to middle income households.”

“And I do think we’ve got a customer that is going to be more intently focused on value as they come through the holiday, and our guide and our actions are really focused on that.”

American Eagle is jumping after good numbers.

“As discussed last quarter, we have made incremental investments in advertising, which is contributing to stronger demand, while better positioning our business for enhanced long term brand awareness and overall customer engagement. At the same time, we are focused on operational improvements and cost efficiencies to drive higher profitability in what continues to be a dynamic macro environment.”

“Improvement was made across both brands and channels, all posting positive comps...Growth accelerated throughout the period, which has continued into the fourth quarter, where we are seeing exceptional demand so far.”

From the Dollar Tree earnings press release just out:

“Our multi price strategy drove strong momentum across our business in the third quarter and helped deliver an all-time record Halloween season...With 85% of our assortment priced at two dollars or less, we continue to deliver exceptional value.”

Comps were up 4.2% with “a 4.5% increase in average ticket and a .3% decline in traffic.”

Macy’s beat both top and bottom line estimates and said:

“As we enter the holiday season, we are well positioned with compelling new merchandise and an omni channel customer experience that delivers both inspiration and value.”

JB Hunt, the trucker, spoke at a UBS conference and said this of note:

With respect to the holidays, “it’s not the biggest peak we’ve seen. It’s not the worst peak we’ve seen. But one good thing, I think, is that our customers have really moved out of that Covid era where they had a hard time forecasting what demand would look like. They’re really a lot more on target to that.”

“The other comments that we’ve made is that we see a few pockets of tightness mostly in the brokerage space, but it’s not overall. And I don’t know what word you used to describe the market, but I would say extremely challenging market. It’s just the demand is good, but the inflation side is significant and supply, there’s still plenty of supply out there. So it’s a challenging freight market.”

On the holidays, “I don’t think there have been surprises. I don’t think we have feedback that Black Friday sales were significantly going to change the way their transportation demands would work out through the end of the year. So really continue to get feedback from customers that it’s kind of steady as she goes and their forecast hasn’t changed from what it was before Black Friday.”

From Eastman Chemical speaking at a Citi basic materials conference:

“I would say demand overall is probably a bit lighter than we expected, but that’s being offset by great cost control and utilization as we look at the quarter.”

According to CrowdStrike, we are in an “agentic society” and that “No matter how the market swings, geopolitical tensions evolve, or what technologies are in vogue, our digital society mandates cybersecurity as a necessity. And now more than ever, synonymous with that, CrowdStrike is a necessity.”

“Businesses are onboarding a whole new type of workforce today, the agentic workforce. Humans using agents to do more and agents working by themselves, each with access to data, applications, compute, and sometimes even other agents.”

Sounding very Terminator like to me.

I’ll shift to November vehicle sales which after the September EV lift and the October EV sales crash after the tax credit expired, auto sales totaled 15.6mm in November, above the estimate of 15.4mm but below the 16.5mm seen in November 2024. In case you didn’t see this WSJ article yesterday, “American Consumers Lose Patience With High Car Prices”...”Shoppers are downsizing, buying used vehicles, taking on longer car loans and holding out for deals.” source: www.wsj.com

Two days ago Apartment List released its National Rent Report for November and new leases fell 1% m/o/m in the seasonally soft period. Rents are down 1.1% y/o/y. The vacancy rate of 7.2% was unchanged m/o/m. They said, “We’re past the peak of a multifamily construction surge, but healthy supply of new units are still hitting the market and colliding with sluggish demand, causing vacancies to continue trending up.”

Austin remains the weakest market with median rents down 6.8% y/o/y while Providence, RI saw the quickest rental growth of 5.2%.

The bottom line from Apartment List, “All of our key indicators are pointing toward ongoing sluggishness in the multifamily rental market – rent prices are down and the vacancy rate is at an all-time high. As construction slows further during the tail end of this year and into 2026, rent prices and occupancy should begin to stabilize, and a return to tighter market conditions remains on the horizon. That said, the supply boom still has a bit of runway remaining, and the demand outlook has begun to appear weaker amid a shaky labor market. These factors could lengthen the time that it takes for the market to metabolize the recent growth in the rental stock.”

FYI, renewal rates from the publicly traded multi family REITS are in the +2-4% range.

Holiday distorted, purchase applications for the week ended 11/28 rose 2.5% w/o/w but refi’s fell again, by 4.4%.

China’s November private sector weighted services PMI fell .5 pt m/o/m to 52.1 but as expected. Hong Kong’s PMI was 52.9 vs 51.2. Singapore’s PMI fell 2 pts but still well above 50 at 55.4.

With Hong Kong, S&P Global said “Demand conditions strengthened at home, abroad and across Mainland China, with overall new orders rising at the steepest rate since April 2023.” That said, “Business expectations for the year ahead remained downbeat, however, despite the overall degree of pessimism moderating from October. Firms cited concerns regarding the economic outlook, geopolitical tensions and the impact of higher trade barriers.”

Both the Eurozone and UK services PMI’s were revised up from their initial prints with the former up .6 pts m/o/m but the UK one was still down 1 pt m/o/m. S&P Global said, “The service sector in the Eurozone is showing clear signs of recovery. The strong performance in the service sector was even enough to more than offset the weakness in the manufacturing sector, meaning that economic output in the Eurozone grew slightly faster in November than in the previous month. We therefore expect the growth rate in the final quarter of the year to show a slight acceleration.”

On the UK, “”November data revealed an abrupt end to the steady improvement in order books seen since the summer. Unfavorable demand conditions were signaled in both domestic and export markets. Lower workloads led to a renewed slowdown in business activity growth across the UK service economy, with the latest expansion much softer than the post-pandemic trend. Moreover, staffing numbers were trimmed to the greatest extent since February.”

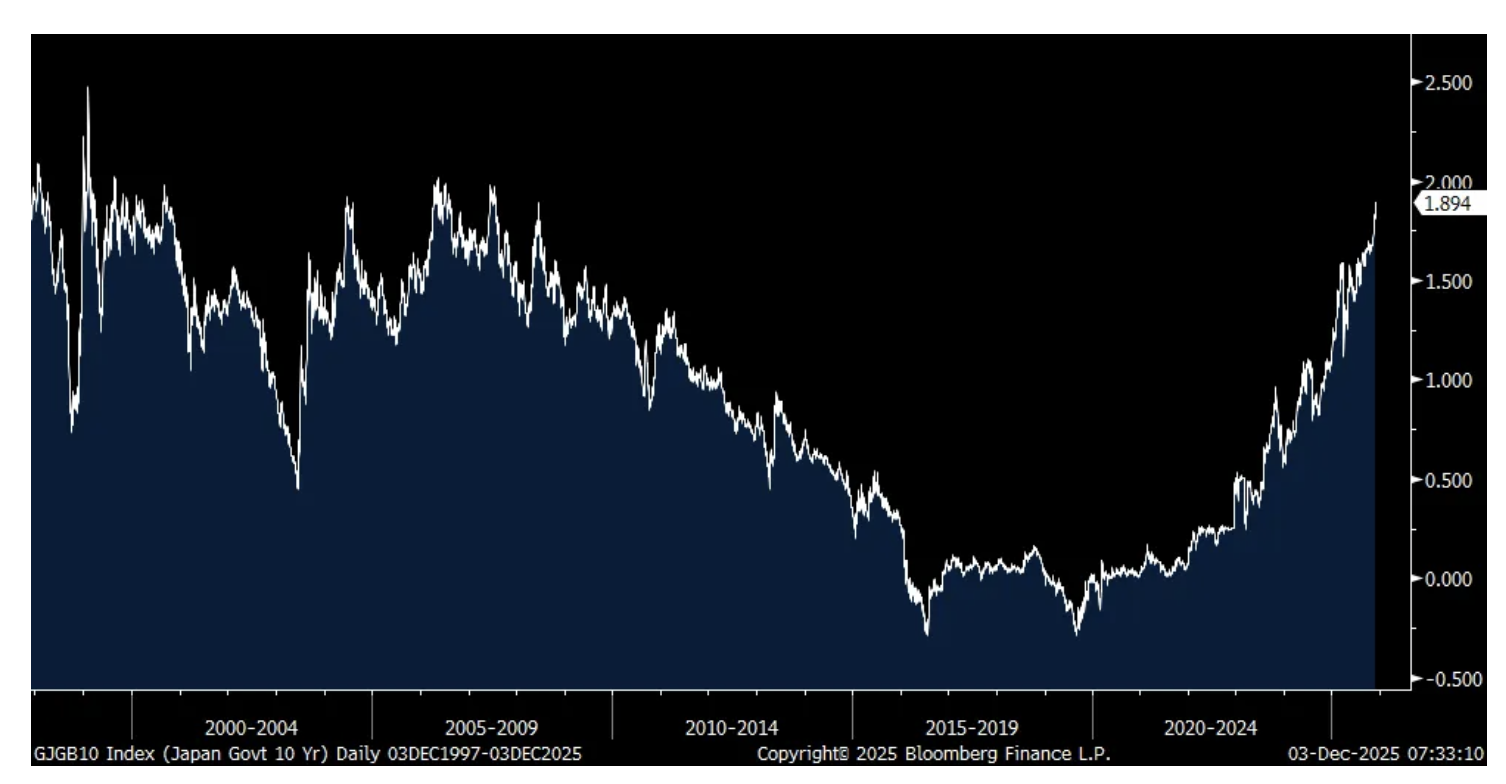

Lastly, JGB yields continue higher with the 10 yr yield up 2.6 bps to 1.89%, now the highest since July 2007. The yen is rallying in turn to a 2 ½ week high vs the US dollar. The dollar index by the way is down for the 8th straight day.

10 yr JGB Yield

BY Doug Kass · Dec 3, 2025, 9:55 AM EST

Shorted more (AAPL) and (NVDA) .

BY Doug Kass · Dec 3, 2025, 9:45 AM EST

BY Doug Kass · Dec 3, 2025, 9:40 AM EST

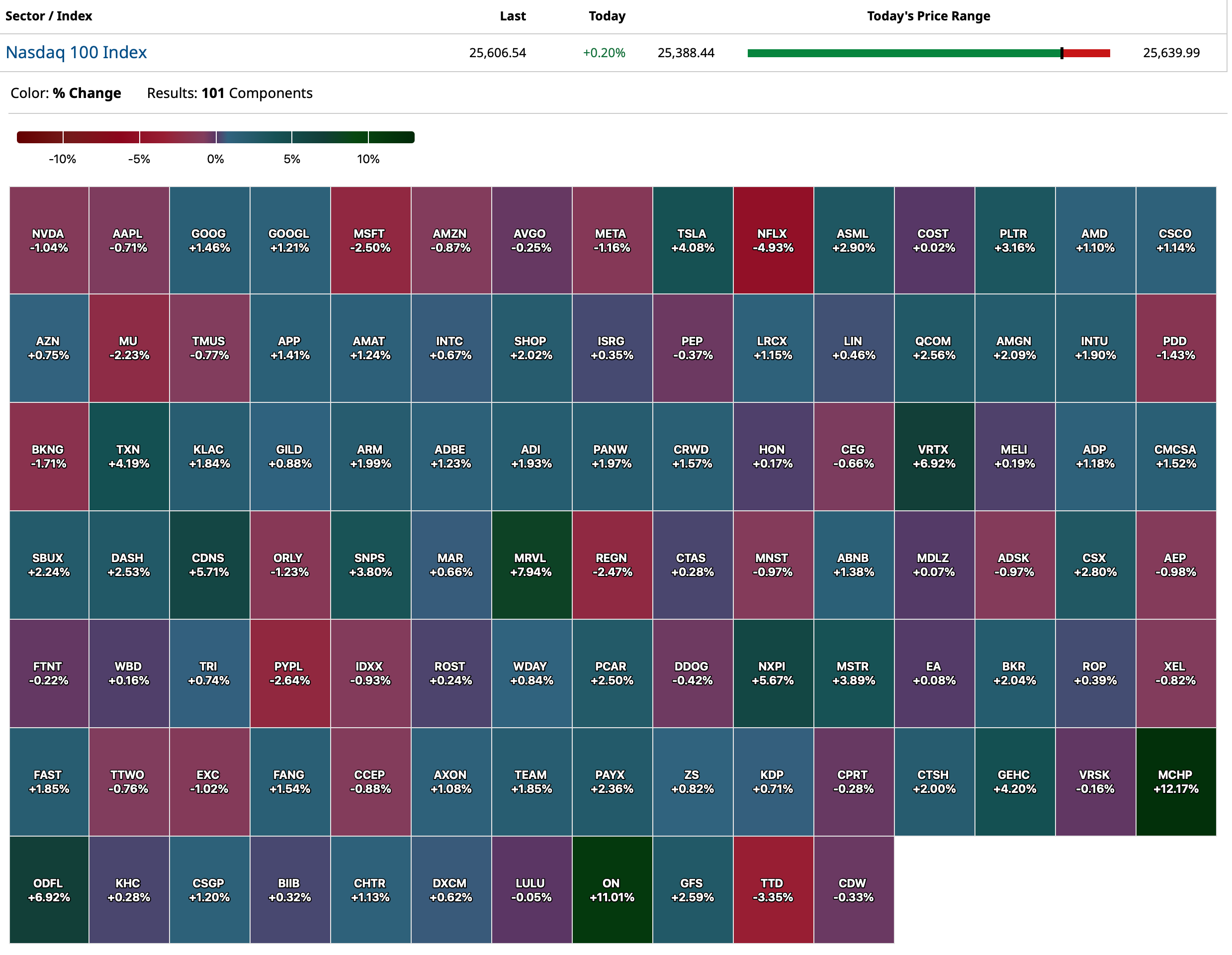

-CAPR +15% (pivotal Phase 3 HOPE-3 Study of Deramiocel in Duchenne Muscular Dystrophy met primary endpoint (PUL v2.0) and key secondary cardiac endpoint)

-AEO +13% (earnings, guidance)

-LTRN +12% (LP-184 Phase 1a meets all endpoints)

-YB +11% (earnings, color)

-AEVA +10% (wins Exclusive Global LiDAR Supply Contract from Top European Automaker)

-MRVL +9.2% (earnings, guidance; confirms to acquire Celestial AI, Accelerating Scale-up Connectivity for Next-Generation Data Centers for $3.25B in cash and stock deal)

-SERV +9.0% (reportedly Trump Admin considering issuing executive order on Robotics next year)

-ONDS +7.7% (wins major government contract to develop autonomous border-protection drone system)

-CXM +6.6% (earnings, guidance)

-PYPD +5.8% (announces Positive FDA Pre-NDA Meeting Minutes for D-PLEX₁₀₀ Supporting NDA Submission)

-ARTL +5.6% (announces Publication of New Peer-Reviewed Study Demonstrating Intraperitoneal Administration of a Novel Fatty Acid Binding Protein 5 (FABP5) Inhibitor Significantly Reduces Stress-Induced Anxiety and Depression Behaviors in Preclinical Models)

-GRO +5.6% (initiates AI powered X-Ray Ore Sorting Trial)

-CDIO +4.7% (receives final gapfill payment rates for AI-driven cardiovascular tests from the Centers for Medicare and Medicaid Services)

-PHVS +4.5% (Phase 3 RAPIDe-3 primary endpoint met with median symptom-relief onset at 1.28 hours vs >12 hours for placebo; all secondary endpoints also met)

-ASAN +3.7% (earnings, guidance)

-BMY +3.3% (announces Continuation of ADEPT-2 Phase 3 Cobenfy Study in Psychosis Associated with Alzheimer's Disease following Data Monitoring Committee (DMC) recommendation)

-PPIH +2.0% (secured $52M in project awards during Q3)

-LESL -13% (earnings, guidance)

-PSTG -13% (earnings, guidance)

-BOX -10% (earnings, guidance)

-GTLB -10% (earnings, guidance)

-M -6.9% (earnings, guidance)

-OKTA -5.5% (earnings, guidance)

-ARE -3.0% (guidance; cuts dividend)

BY Doug Kass · Dec 3, 2025, 9:31 AM EST

I have taken in this morning's Index shorts:

* (SPY) $680.02

* (QQQ) $618.44

From early this morning:

I am back shorting the indices:

* (SPY) $682.95

* (QQQ) $623.20

Position: Short SPY common (VS) and calls (S), QQQ common (VS) and calls (S)

By Doug KassDec 3, 2025 5:45 AM EST

BY Doug Kass · Dec 3, 2025, 9:29 AM EST

BY Doug Kass · Dec 3, 2025, 9:15 AM EST

Sold most of my (MSFT) on the announcement.

Microsoft Lowers AI Software Sales Quotas as Customers Resist Newer Products — The Information

BY Doug Kass · Dec 3, 2025, 9:10 AM EST

BY Doug Kass · Dec 3, 2025, 9:05 AM EST

Treasury Auctions Today:

10:00 a.m.: ISM Services Index; ISM Services PricesPaid; ISM Services New Orders; ISM Services Employment (November);

11:00 a.m.: Treasury buyback (Liquidity Support);

11:30 a.m.: Treasury hosts a $69M17-Week Bill Auction;

2:00 p.m.: Treasury buyback (Cash Management)

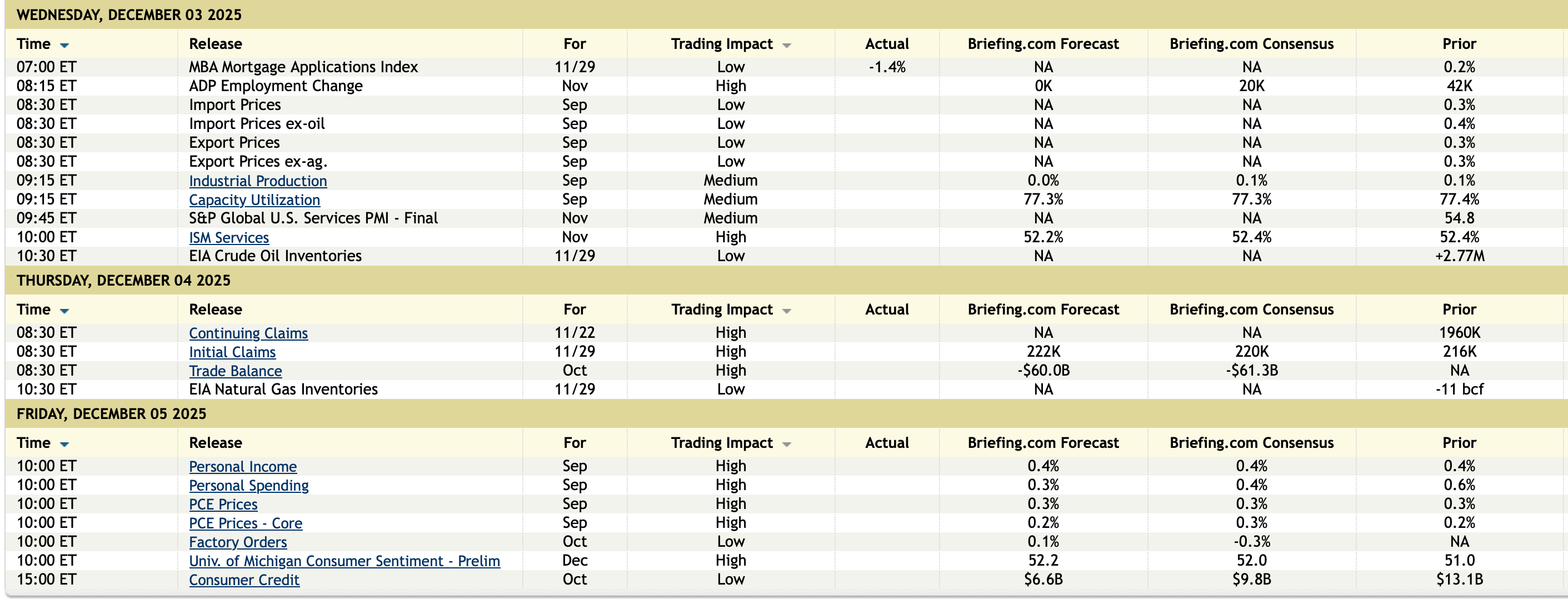

Economic Calendar for the Week

BY Doug Kass · Dec 3, 2025, 8:55 AM EST

From JPMorgan:

US: Futs are higher led by RTY. Pre-market, Mag 7 are mostly higher led by NVDA (+0.4%) and AMZN (+0.3%); MRVL is up +10% post-earnings given the robust long-term guidance. Bond yields are moderately lower; USD is lower. Commodities are mixed: Oil higher, while metals are lower. On the news front, increment updates were relatively muted overnight except for MRVL’s positive earnings that trigger the rebound in global tech.

and...

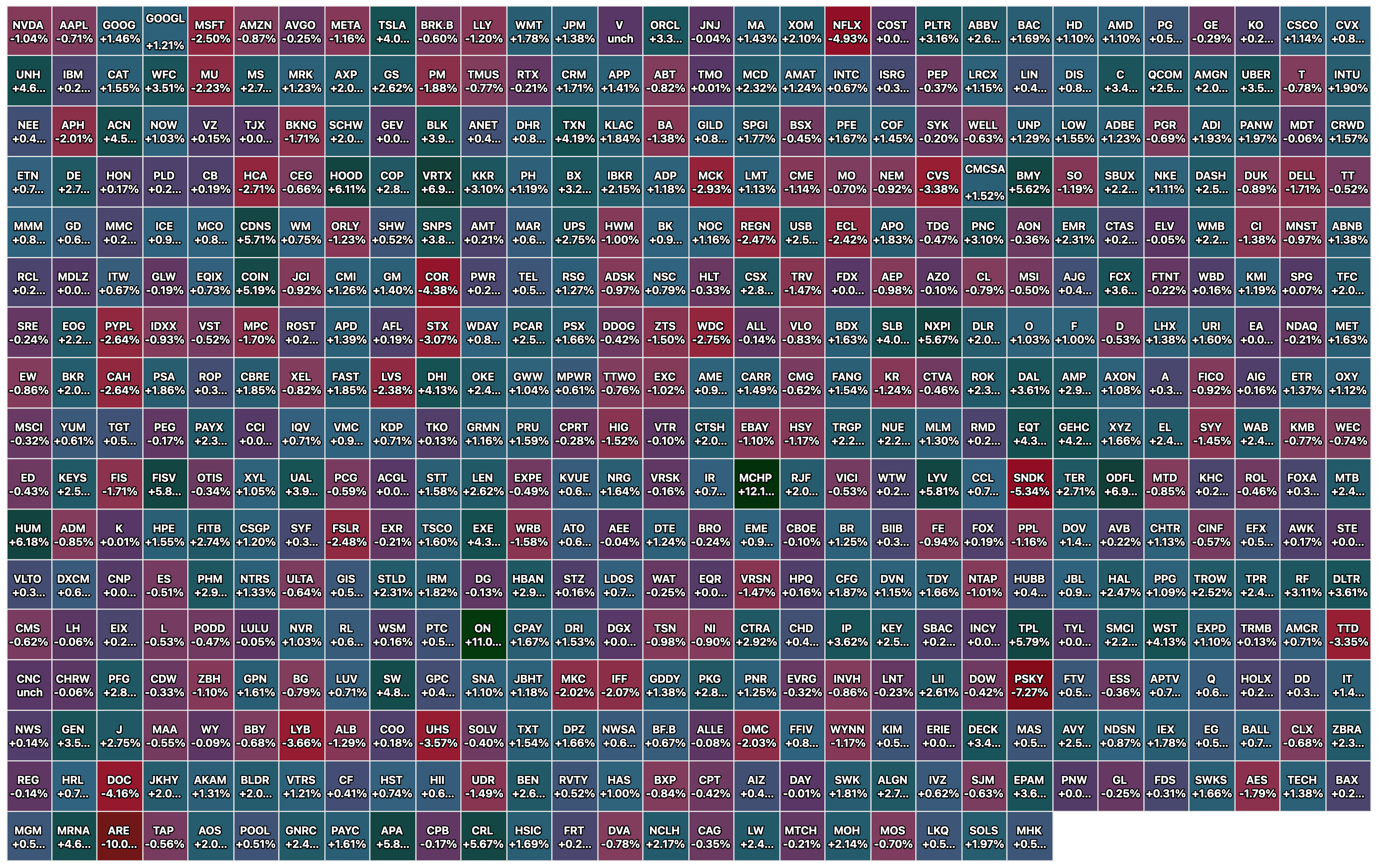

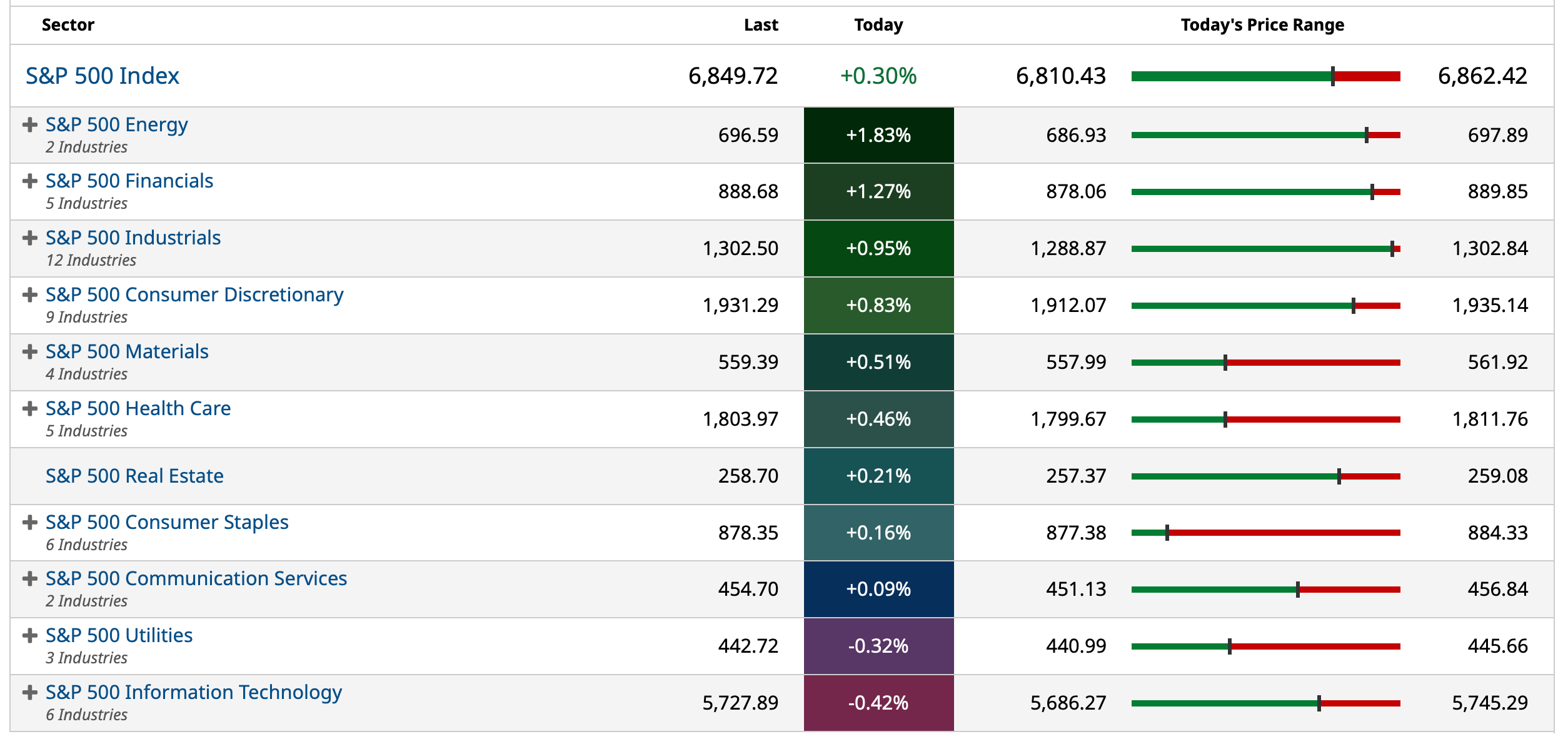

A tech-led rally yesterday with narrow breadth: 57% of the stocks within SPX, or 8 out of 11 sectors, actually finished lower on the day. AAPL, NVDA, and MSFT did the heavy lifting for the index-level gain, representing over 70% of yesterday’s SPX gains. Several key themes of yesterday’s price actions: (i) the broad rebound in Semi/Tech ahead of MRVL earnings (so far, earnings call were quite bullish; stock +16%) and OpenAI’s new reasoning model/ORCL earnings next week. (ii) Fed independence discussion. In Feroli’s 2026 outlook, he pointed out that the biggest risk event next year could be Supreme Court’s decision on Cook’s case. See below for his full comments. Overall, macro views remain the same with more comments from credit card and software companies pointing to quite healthy holiday shopping. Incremental news flow since yesterday’s close were largely muted.

BY Doug Kass · Dec 3, 2025, 8:40 AM EST

BY Doug Kass · Dec 3, 2025, 8:30 AM EST

I added to my Index shorts (8:15 a.m.):

* (SPY) $683.47

* (QQQ) $623.77

BY Doug Kass · Dec 3, 2025, 8:24 AM EST

BY Doug Kass · Dec 3, 2025, 8:20 AM EST

I added to my (AAPL) short (in premarket) at $286.43.

BY Doug Kass · Dec 3, 2025, 8:19 AM EST

BY Doug Kass · Dec 3, 2025, 8:10 AM EST

BY Doug Kass · Dec 3, 2025, 8:00 AM EST

BY Doug Kass · Dec 3, 2025, 7:50 AM EST

I have a business lunch between 1 PM and 2:30 PM today.

BY Doug Kass · Dec 3, 2025, 7:40 AM EST

Everyone knows it, including the Silicon Valley touts and David Sacks, which is why they want the government to be prepared to bail them out:

From Gary Marcus:

BY Doug Kass · Dec 3, 2025, 7:30 AM EST

BY Doug Kass · Dec 3, 2025, 7:20 AM EST

From The Divine Ms M this morning:

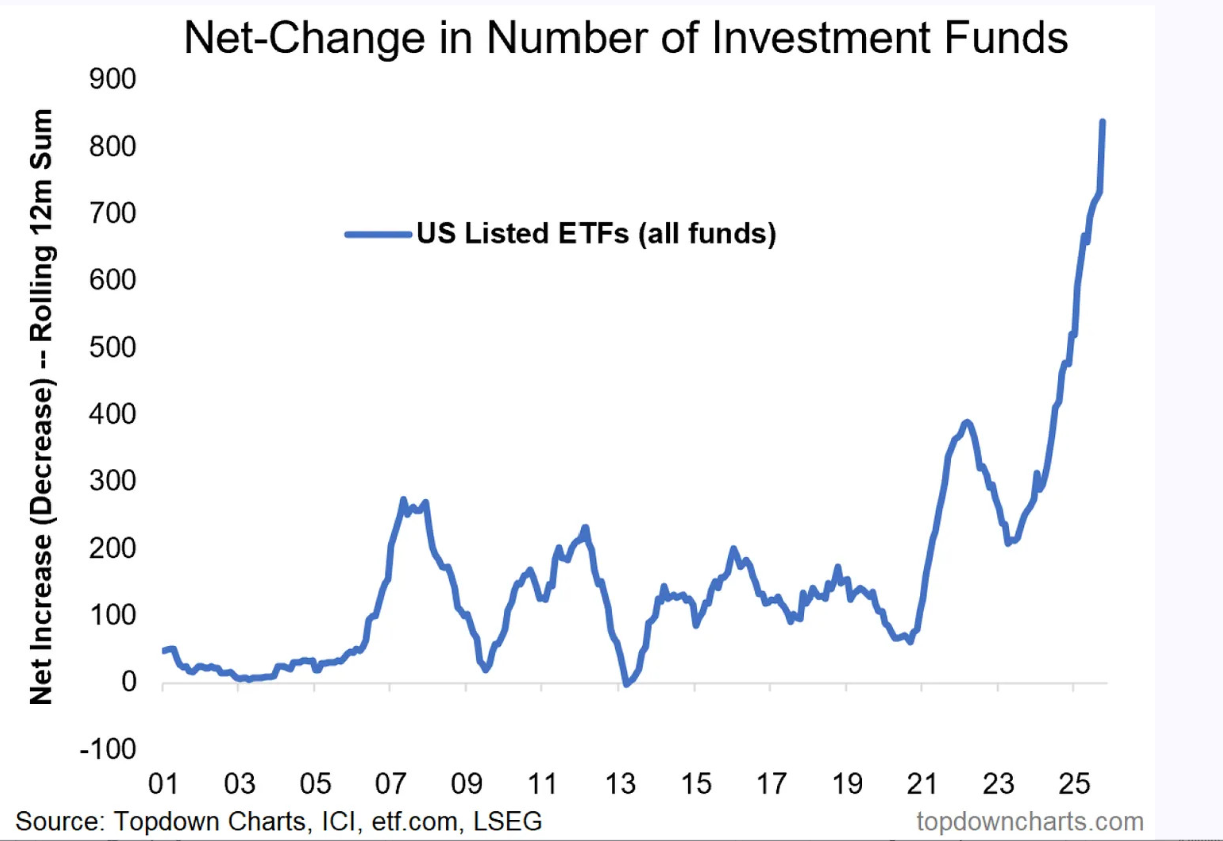

This One Chart Can Tell Us What Stage of the Bull Market We're In

I have seen arguments that, typically, by this stage of a bull market, we should see companies IPO’ing all over the place. I honestly do not recall a gazillion IPOs in 2006-2007, but I do remember it was a daily occurrence in the late 1990s.

In late 2020 and early 2021, it wasn’t IPOs either but rather SPACs. So when I saw this chart of the explosion in ETFs created since 2023 (courtesy of Topdown Charts), I just had to share it with you.

I realize ETF creation is not the same as SPACs nor IPOs, but consider that a good majority of these ETFs have the same ten stocks in them. Then I look at the chart, and I see that it turns out we may not have had an IPO boom in 2007, but we surely had an ETF boom. Look at that growth in ETFs in 2006-07.

BY Doug Kass · Dec 3, 2025, 7:10 AM EST

BY Doug Kass · Dec 3, 2025, 7:00 AM EST

Bonus — Here are some great links:

Is The Russell Breakout a Fakeout? ("Jazzy" Jeff Hirsch)

BY Doug Kass · Dec 3, 2025, 6:45 AM EST

BY Doug Kass · Dec 3, 2025, 6:35 AM EST

BY Doug Kass · Dec 3, 2025, 6:25 AM EST

BY Doug Kass · Dec 3, 2025, 6:15 AM EST

BY Doug Kass · Dec 3, 2025, 6:05 AM EST

The S&P Short Range Indicator is now at 3.02% vs. 1.45% — that's back into a more extreme overbought.

BY Doug Kass · Dec 3, 2025, 5:55 AM EST

I am back shorting the indices:

* (SPY) $682.95

* (QQQ) $623.20

BY Doug Kass · Dec 3, 2025, 5:45 AM EST