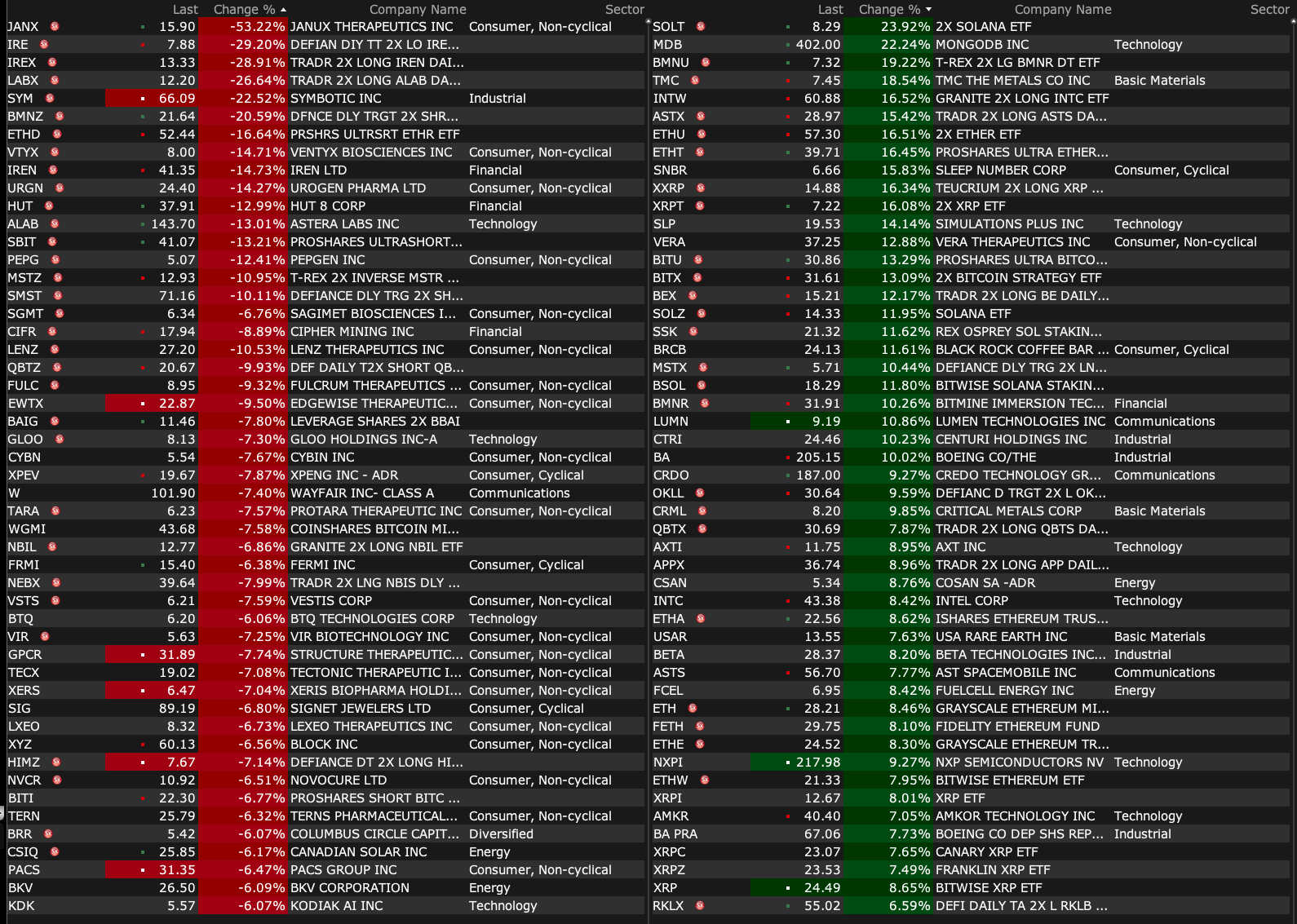

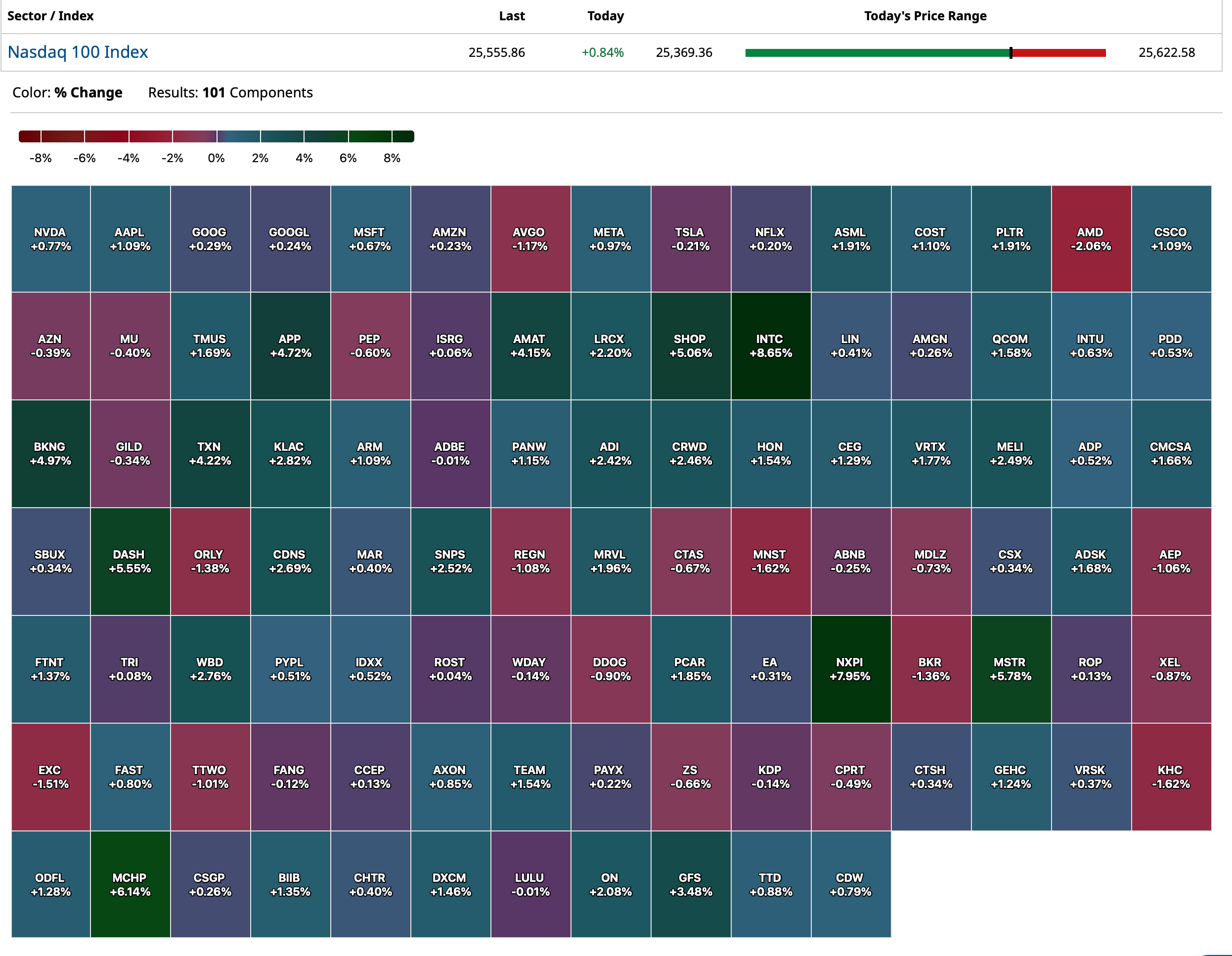

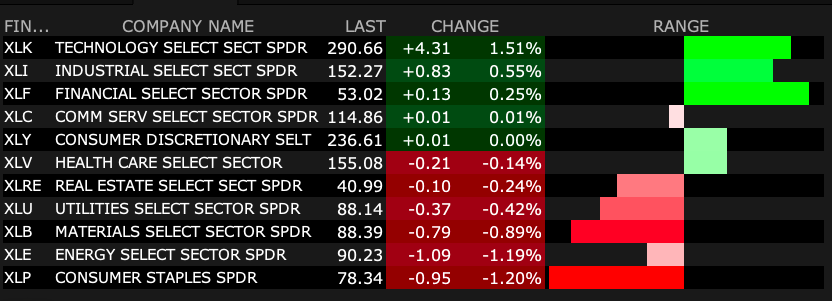

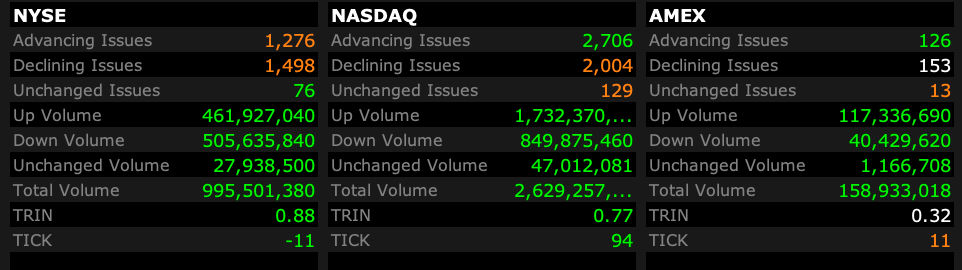

Tuesday's After-Hours Gainers and Losers

After-Hours % Gainers

After-Hours % Losers

BY Doug Kass · Dec 2, 2025, 4:40 PM EST

BY Doug Kass · Dec 2, 2025, 4:40 PM EST

- NYSE volume 18% below its one-month average

- NASDAQ volume 22% below its one-month average

- VIX index: down 3.77% to 16.59

BY Doug Kass · Dec 2, 2025, 4:26 PM EST

BY Doug Kass · Dec 2, 2025, 3:12 PM EST

BY Doug Kass · Dec 2, 2025, 2:20 PM EST

Consumer non-durables PepsiCo (PEP) and Kimberly-Clark (KMB) are down hard today on a severe rotation away from defensive equities.

I am a $145 buyer of PEP and $105 buyer of KMB.

BY Doug Kass · Dec 2, 2025, 2:06 PM EST

sbickleyinreno

I keep waiting for your follow-up post regarding today's rally in BTC? Is that not forthcoming?

Dougie Kass

pray tell, why?

sbickleyinreno

So that your subscribers can see you are objective and acknowledge both sides of the coin, as you do with so many other market developments, but refuse to do with crypto or AI. I don't have a problem with the flip-flopping around, like your coverage of weed stocks, for example. Developments occur, and you adjust accordingly based on your proprietary analysis. But your lack of depth, critical thinking, and abandonment of level 2 thinking on the topics of crypto and AI is offensive. Will you stop adding Hedgeye to your BTC tweets now that he sees a potential bottom forming? Your analysis is world-class when unclouded by emotion.

Dougie Kass

On AI I am showing the negative side of the equation. There are multiple resources (99.9% of the comments are bullish) by analysts, managements and others. In doing so I think I am providing a service in the More Tales series by pointing out bona fide issues, before the herd has.

On bitcoin, I am in Charlie Munger's camp - I dont see that it has ANY value. Just my view and I dont really discuss bitcoin, save some tweets that I feel are interesting. My only real involvement has been to be short MSTR for the last year or so. I covered, as posted, late last week around $174. I recognize here too I am in the minority. Oh well, SB.

On weed stocks, I have done very well in the last 7-8 trades by buying weakness and selling strength. Overall, I believe the outlook for the industry is poor so I try to opportunistically capitalize with some bold trading. I dont think I have flip flopped at all. I have bought weakness and sold strength in the weed space.

Thanks for the "world class" designation, but I am not worthy SB.

sbickleyinreno

I appreciate the thoughtful response Dougie, I truly do. I'll leave well enough alone, however, I will say you comment and post BTC tweets quite a bit and your position carries weight. But you addressed it above - you just don't care about it.

BY Doug Kass · Dec 2, 2025, 1:59 PM EST

The semis are downside leaders — a possible tell.

BY Doug Kass · Dec 2, 2025, 1:20 PM EST

I'm back shorting (GRNY) at $24.86.

BY Doug Kass · Dec 2, 2025, 1:11 PM EST

With S&P cash +21 handles, I am adding to my index call shorts.

I have converted all of my index common shorts to short calls (taking in premium given the level of VIX).

BY Doug Kass · Dec 2, 2025, 12:50 PM EST

Previously I showed a chart which showed that corporate adoption rates for AI were actually declining at the consumer level.

The novelty of the new toy is wearing off, at both the corporate and consumer level, as people figure out it is not all it was cracked up to be. And of course, everyone forgets, the Chinese are now doing this equally as well, for a small fraction of the cost and capital investment and power consumption due to more smartly engineered software (

No wonder OpenAI is in expense-cutting mode all of the sudden.(https://www.theinformation.com/articles/openai-ceo-declares-code-red-combat-threats-chatgpt-delays-ads-effort). While Google (GOOGL) is getting all the hype all of the sudden, they too are not close to cost competitive with the Chinese and are also spending close to 25% of revenue on CAPEX, multiples of steel companies and auto manufacturers.

Being the least loser does not make one a winner. This is what happens when too much capital is thrown at an industry, especially one where the investment hypothesis does not turn out to be right (no scaling, no path to AGI, permanent buggy and limited technology).

BY Doug Kass · Dec 2, 2025, 12:35 PM EST

BY Doug Kass · Dec 2, 2025, 12:19 PM EST

- NYSE volume 21% below its one-month average;

- Nasdaq volume 26% below its one-month average;

- VIX index: down 4.41% to 16.48

BY Doug Kass · Dec 2, 2025, 11:25 AM EST

* This wasn't supposed to happen... at least the bitcoin bulls thought not!

Bitcoin Prices vs Global Liquidity

BY Doug Kass · Dec 2, 2025, 11:00 AM EST

From Peter Boockvar:

While the 10 yr JGB yield didn’t really fall, down ½ bp, it at least stopped going up after the solid 10 yr auction overnight. The bid to cover of 3.59 was well above the previous 12 month average of 3.20 as the higher yield and now likelihood the BoJ raises rates to help cool inflation brought out the buyers. I keep talking about what’s going on in the JGB market for a few reasons. One, Japan has been the land of interest rate repression for many decades and the architect of modern day QE, which others obviously copied. Two, Japan is the largest foreign holder of US Treasuries and JGB yields continue to get more attractive relative to US bonds. Three, while we can separate out correlations week to week, month to month, global sovereign developed country bond yields have generally moved around in the same direction over the past 15+ years when global central banks all held hands with the ZIRP/NIRP experiment and massive QE. Lastly, debts and deficits now matter in the eyes of bond investors.

US Treasury yields in white, JGBs in blue, Bunds in orange, Gilts in purple

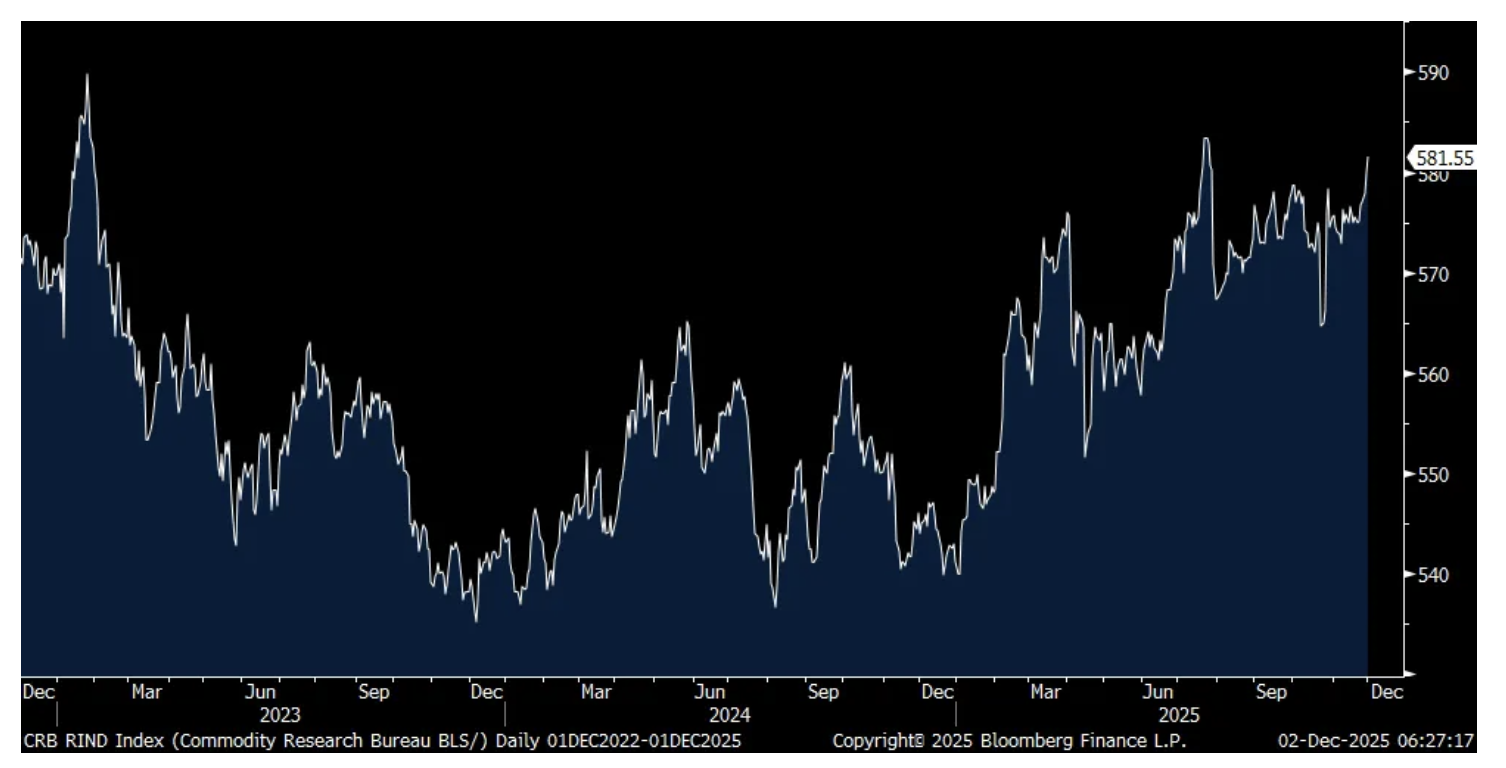

While silver and copper are taking a breather this morning after the big run, still keep your eye on the entire industrial metal complex. The CRB raw industrials index closed yesterday just 2 pts from the highest level since January 2023.

CRB Raw Industrials Index

Because of its very wide AI ecosystem tentacles, I’ve referred to OpenAI as too big to fail. Not from the perspective that the government will backstop/bail them out but from the angle that its success or failure will have far and wide implications for both the GenAI tech trade and the economic buildout of all these data centers. In case you didn’t see the article today in the WSJ titled, “OpenAI’s Altman Declares ‘Code Red’ to Improve ChatGPT as Google Threatens AI Lead...A companywide memo is the most decisive indication yet of the pressure OpenAI faces from competitors.” https://www.wsj.com

I believe that the GenAI tech trade is transitioning from the ‘everybody wins, buy every stock tied to it’ to one that will differentiate between the winners and losers.

I don’t know much about the business of MongoDB but the stock is ripping higher on good earnings and they said this of note:

“We are also seeing meaningful traction among large enterprises that are starting to build AI applications that have a material impact on their business.”

On their overall business, “Existing customers are expanding with us, and net new customer additions continue to show strength. Companies in nearly every industry and across every geography are choosing MongoDB because we deliver the features, performance, cost effectiveness, and AI readiness they need in a single data platform.”

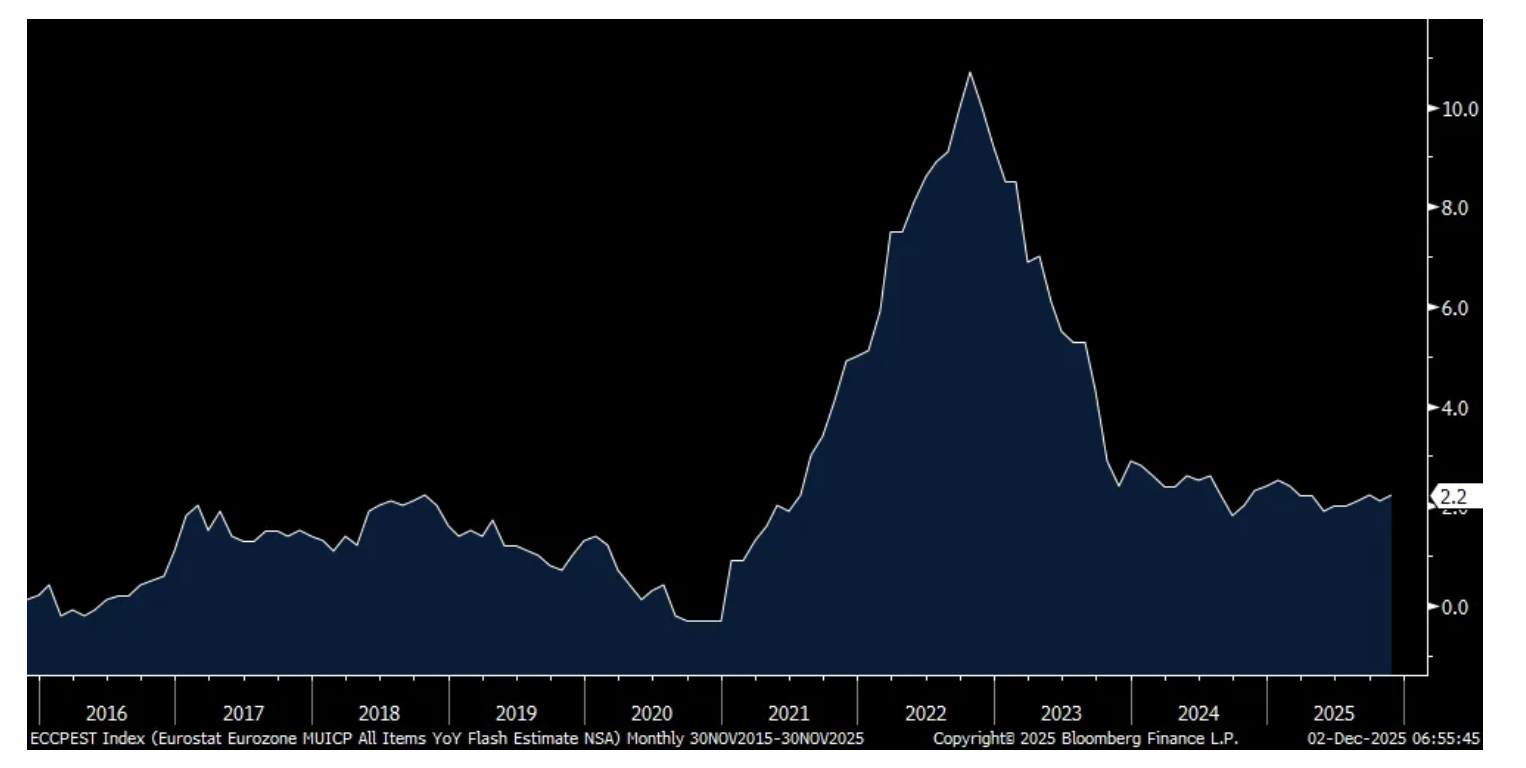

Of note data wise overseas was the November Eurozone CPI which rose 2.2% y/o/y vs 2.1% in October and one tenth above the estimate of 2.1%. The core rate was higher by 2.4% y/o/y as expected and unchanged from last month. Services inflation of 3.5% continues to be the inflationary sticky point in the region as non-energy industrial goods prices were higher by just .6% y/o/y. The ECB deposit rate of 2% is therefore about a zero REAL rate when compared to CPI and only if do they want to experiment again with the highly economically distortive negative REAL rate policy, and/or inflation takes another leg down, the ECB is on hold for now with rates.

Eurozone CPI y/o/y

BY Doug Kass · Dec 2, 2025, 10:05 AM EST

Today marks the first anniversary of Sir Arthur's passing:

Here was my tribute, last year, to Sir Arthur:

Sir Arthur 'Held Court' in My Diary on a Daily Basis for Decades

"Never bet on the end of the world, because it only happens once, and even if it does, who are you going to settle the trade with?"

- Art Cashin

On Sunday morning, at 83 years young, my buddy Arthur Cashin passed away. Art Cashin, New York Stock Exchange fixture for decades, dies at age 83

For thousands of market participants Arthur was our boat's captain — steering the market's sometimes rough seas with agility and poetic grace:

- Walt Whitman, Oh Captain! My Captain!

With Arthur Cashin's permission I reposted his daily market thoughts in my Diary for almost 20 years.

Arthur seemed to like me and I revered him — perhaps it was our mutual sense of history of the markets that brought us so closely together.

We both spoke our mind — dull to the consequences of transparency and honesty.

We both enjoyed writing our thoughts down on paper. (He literally used "paper," preferring to write out his notes by hand and delivering them to his assistant and my pal, Judi).

We both "didn't suffer fools" as he and I lacked patience and had little tolerance for the incompetent and foolish.

Arthur was religious and his religious market views were steeped in history and historical perspective. His thoughts and opinions were austere, humble and contemplative as if filled with almost monastic clarity.

Over the past three decades I spent many early evenings marinating the ice cubes with Arthur.

All of us were better off having Arthur in our lives — his pearls of wisdom will reverberate for years to come.

Art appeared frequently on CNBC — I especially remembered this interview as he reminisced about 9/11 20 years after that tragedy... UBS's Art Cashin remembers working on Wall Street on 9/11

And here was what I believe to have been his last (or one of his last) interviews that Art had on CNBC about 11 months ago with his dear friend CNBC's Bob Pisani. UBS' Art Cashin: Election year tends to be 'good' for the market

To honor my friend, here is the last "Sir Arthur Holds Court" in my Diary in early 2024 — right before his health began to fail:

From Arthur Cashin:

The main influence on Wall Street during the second trading session of the year was not Spartacus or Hitler or any other notable celebrities. Rather, it was a somewhat rotund red cheeked fellow named Santa Claus and what was happening to the supposed Santa Claus rally, which seemed to be disappearing rapidly before the eyes of Wall Street traders. After a setback on the first trading day of the year, things began to look a little difficult for the Wall Street bulls as we were headed for a negative session in the second trading day of the year.

As you probably recall from the writings of Yale Hirsch, who developed the now proverbial Santa Claus rally, it is the last five trading days of the outgoing year and the first two of this year. The first trading day was a lousy session to begin with and traders became more concerned as they moved into the second session, and it did not seem to hold many promises. In fact, as they struggled through the morning, that became the topic among traders, and we touched on a good deal of that in this late morning update: The Wall Street bulls are beginning to worry that a rebellious elf has pushed Santa out of the sleigh.

This is the final day of the so-called Santa Claus rally and the last couple of days it has swung into negative territory. This is not a very good sign for the seasonal success marker. My friend, Jeff Hirsch, editor of the invaluable Stock Trader's Almanac reminds that when the Santa Claus rally fails, it puts in jeopardy or at least puts on the alert signal from a variety of other early seasonal indicators, making it a bit of an uphill fight for the bulls.

The process so far has not been at all helpful to the bulls and the lingering weakness in Apple continues to provide a slight negative tone to the market overall.

Unless the bulls can get the Cavalry out and promote a rescue rally for the afternoon, the old rule of thumb will be getting talked about and that is - if Santa comes to Broad and Wall, the bears may return to make the call. The yields are not providing much influence either way and does seem to look like the markets moving pretty much on its own internals.

Let's see if the newsticker can provide some help because the algorithms are not finding much hope in the internals. If nothing else, a negative close today may, at the very least, slowdown the insertion of funds for the New Year as money managers start to look for sectors that are showing any real promise. Remain alert. Certainly, remain wary, but please stay safe.

Shortly after the update went out, it was convenient that my pal, Josh Brown, partnered with another of my Wall Street trading friends, Barry Ritholz, was on the screen and in Josh's own plain-speaking way nailed down what may be the causation of the Santa Claus rally disappearing and it had little to do with chart angles and moving averages and the like. It had more to do with capital gains and taxes as Josh aptly pointed out. A lot of people with that super late rally in 2023 were thinking about taking some profits and shifting sectors and not making a major decision, but basically repositioning themselves and their portfolios.

As Josh succinctly pointed out, one of things they normally would have to think about was their financial officers looking over their shoulder and saying - if you trim your position or shift your position here in the closing days of 2023, you are going to have to declare it on the taxes of this year that is now ending or if you wait and change those positions and make those decisions in the opening days of the new year 2024, you had the luxurious latitude of waiting days, weeks or even months before you had to declare for taxation purposes the day of that trade and make payments on the capital gains you might or might not owe.

What prompted this selling in the first two trading of this month - shooting Santa Claus in the foot - in all likelihood was something that had technically nothing to do with the stock market but more to do with tax positions of the entity who is doing the trading. Simply succinct and right on the mark as usual and once again, Josh laid it out to all of us that the answer was something you did not need a slide rule, calculator or a computer to determine.

Just tax timing. Pretty simple. Well, simple it may have been, but it did cause them to shoot the Santa Claus rally in its foot, perhaps even in both feet as it raised questions about the indications of the first few trading days toward the overall trading for the year 2024 and that will cause us and many others over the next several days to try and compute - are we seeing a true indication of what the balance of the years trading may look like or are we just stubbing our toe on an axiom of tax declarations. Nonetheless, the guidelines of an indicator are certainly the guidelines of the indicator. We were going to review those rather rare occurrences when the Santa Claus rally does not kick in, but overnight, our friend Jeff has magnanimously dipped into his prodigious files, and this is what he wrote:

On the heels of last year's momentous rally, the market is showing some signs of weakness causing the Santa Claus Rally to fail to materialize. Profit taking in January has become more commonplace in the last 25 years or so and January is notably softer in election years like 2024. Some profit taking is understandable following the massive rally from the end of October ranging from just over 16% for DJIA and S&P 500 to 19.9% for NASDAQ and 26.2% for Russell 2000 at their respective recent highs just before yearend. But the selling over the past few days is notable and a warning sign. Defined in the Stock Trader's Almanac, the Santa Claus Rally (SCR) is the propensity for the S&P 500 to rally the last five trading days of December and the first two of January with an average gain of 1.3% since 1950.

This indicator was discovered and first published by Yale Hirsch in the 1973 edition of the Almanac. The lack of a rally can be a preliminary indicator of tough times to come. This was certainly the case in 2008 and 2000. A 4.0% decline in 2000 foreshadowed the bursting of the tech bubble and a 2.5% loss in 2008 preceded the second worst bear market in history. Down SCRs were followed by flat years in 1994, 2005 and 2015, and a mild bear that ended in February 2016. Of the 15 down SCRs since 1950, 10 years have been up and 5 down, but the average gain is a measly 5.0%. As Yale Hirsch's now famous line states, "If Santa Claus should fail to call, bears may come to Broad and Wall."

With the Santa Claus Rally a no show we will be watching for a positive First Five Days (FFD) and January Barometer (JB), the second and third legs of our January Indicator Trifecta. Since 1950 there have been only three occurrences when SCR was down and both the FFD and JB were positive. Two out of three of those years were up over 20% and 1994 was a flat -1.5% with a 14.8% average gain on all three. Since there are only three down SCR years with up FFDs and JBs we present to you the other years with one of the Trifecta components down and the other two up. Of these 18 years 14 years were up and 4 were down with an average gain of 7.9%. So, as we said 2 out of 3 ain't bad when it comes to our January Indicator Trifecta.

Remember: if these seasonal indicators are negative and the market does not rally as it normally does during this time, we will likely shift to a less bullish posture - if not outright bearish. Thank you, Jeffrey, for that thorough review of some past occurrences.

Okay, now back to this morning. Overnight, global equity markets are once again showing signs of individuality. Japan closed down the equivalent of 180 Dow points. Hong Kong was flat. Mainland China was off about 130 Dow points and India was a bit of an odd man out, closing up the equivalent of about 250 Dow points. As we go to press, Europe is marginally optimistic. London is fractionally higher, but Paris and Frankfurt are up about the equivalent of 100 Dow points.

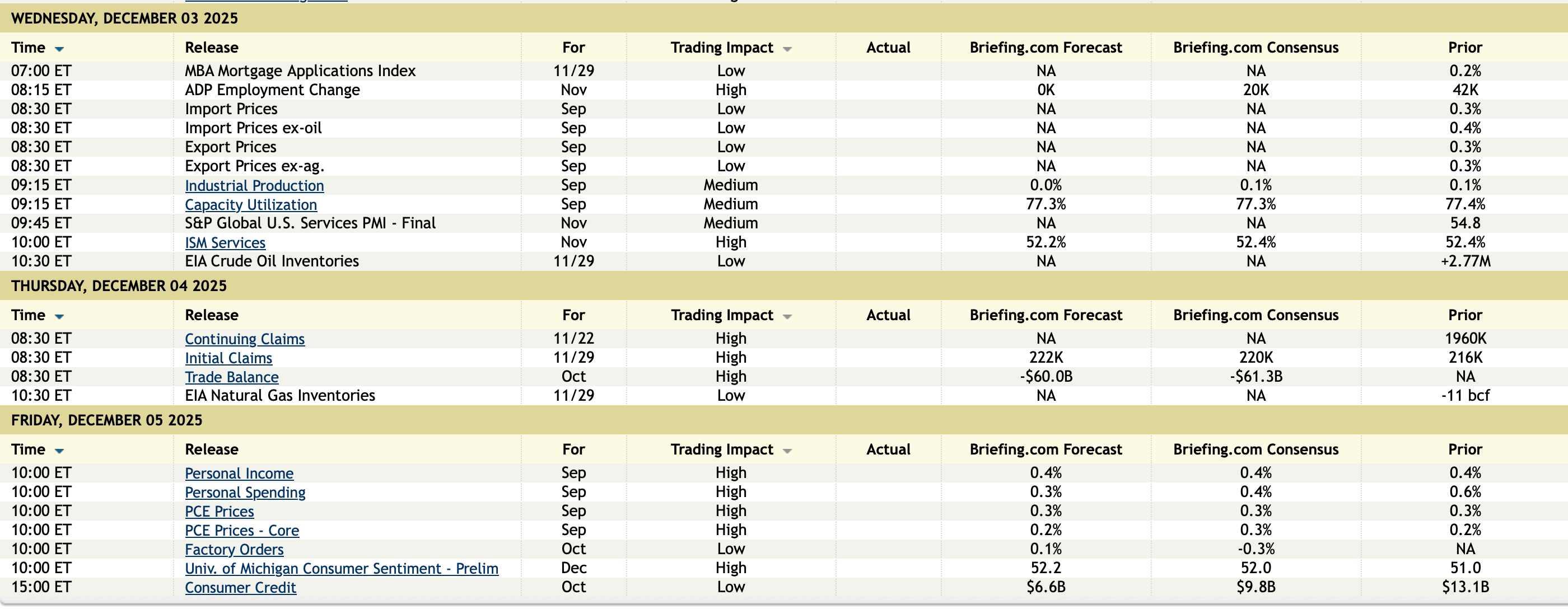

The calendar is not overly busy, but we begin with some job type information. Early on, we get the Challenger Layoff Report and at 8:15, we get the ADP Payroll Estimate and then at 8:30, of course, the Initial Jobless Claims and right after the opening, we get the PMI Composite. In midmorning, we get Natural Gas Inventories and, a little bit later, we get the Oil Inventories because of the New Year holiday earlier in the week.

After the close, traders will go to the newsticker to see what the Fed Balance Sheet looks like and if quantitative tightening continues and to what degree. A lot of finger pointing in the Middle East and some speculation that a further crackdown with the Houthi rebels may be in order, but no official confirmation one way or another.

Given the fact that geopolitics is bubbling up again, best stick to the current drill and that is stay very close to the newsticker. Keep your seatbelt fastened.

Stay nimble and alert and given these fractious times, please stay safe.

By Doug Kass Jan 4, 2024 9:35 AM EST

BY Doug Kass · Dec 2, 2025, 9:45 AM EST

With S&P cash +27 handles I am adding to my short index calls.

BY Doug Kass · Dec 2, 2025, 9:41 AM EST

BY Doug Kass · Dec 2, 2025, 9:30 AM EST

-EB +78% (to be acquired by Bending Spoons at $4.50/shr all-cash or ~$500M)

-FTEL +38% (announces Interim Dividend and Shareholder Loyalty Program)

-MDB +23% (earnings, guidance)

-JSPR +18% (announces Positive Preliminary Data from ETESIAN Study of Briquilimab in Asthma and Findings from BEACON Study Internal Investigation)

-CRDO +17% (earnings, guidance)

-BYND +15% (momentum with potential short squeeze)

-NRXP +15% (announces US FDA Receipt of ANDA for KETAFREE, a Preservative-Free IV Ketamin)

-PDSB +14% (schedules Type C Meeting with U.S. FDA)

-INVZ +12% (Daimler Truck and Torc Robotics Select Innoviz Technologies as LiDAR Partner for Series Production of Level 4 Autonomous Trucks)

-UNFI +8.3% (earnings, guidance)

-CTRN +8.0% (earnings, guidance)

-FLNT +7.4% (secured new $30M financing facility with Bay View Funding)

-ALAB +5.3% (higher in sympathy with CRDO)

-FUN +4.6% (Truist Raised FUN to Buy from Hold)

-U +3.6% (hearing has been added to Wedbush Best Ideas List)

-SNOW +3.4% (higher in sympathy with MDB)

-TER +3.2% (Stifel Nicolaus Raised TER to Buy from Hold, price target: $225)

-BA +2.9% (guides FY26 FCF positive)

-NET +2.8% (Barclays Initiates NET with Overweight, price target: $235)

-PNTG +2.6% (Truist Raised PNTG to Buy from Hold, price target: $34)

-SHOP +2.2% (discloses Black Friday/Cyber Monday results)

-JANX -41% (JANX007 clinical data disappoints)

-VTYX -7.3% (provides update on ongoing Phase 2 study of VTX2735)

-SIG -4.2% (earnings, guidance)

-XPO -3.8% (Nov NA LTL operating data)

BY Doug Kass · Dec 2, 2025, 9:14 AM EST

Fed speakers:

10 a.m.: Fed Vice Chair for Supervision Bowman (Voter) testifies before the House Financial Services Committee hearing on Oversight of Financial Regulators, Washington, DC

Treasury auctions:

11 a.m.: Treasury Announces a 4, 8 and 17 Week Bill Auction;

11 a.m.: Treasury buyback announcement (Cash Management);

11:30 a.m.: Treasury hosts a $75B 6-Week Bill Auction

Economic calendar:

8 a.m.: Fed Treasury Repo Reference Rate;

8:55 a.m.: Johnson Redbook Retail Sales Reports (w/e 11/29);

10 a.m.: RCM/TIPP Economic Optimism (December);

10 a.m.: JOLTS Job Openings; JOLTS Job Openings Rate; JOLTS Quits Level; JOLTS Quits Rate; JOLTS Layoffs Level; JOLTS Layoffs Rate (October);

BY Doug Kass · Dec 2, 2025, 9:10 AM EST

BY Doug Kass · Dec 2, 2025, 8:52 AM EST

BY Doug Kass · Dec 2, 2025, 8:21 AM EST

* It is not only Google that is a threat

* OpenAI may end up being the high-cost player in a commodity business...

And a solid interpretation of DeepSeek's claims:

Per below on DeepSeek, sorry Scammy, too little too late, you are the high-cost player in a commodity business and Google (GOOGL) is the least of your problems:

OpenAI CEO Declares ‘Code Red’ to Combat Threats to ChatGPT, Delays Ads Effort

They all got problems. In the whole Google frenzy, folks have forgotten about the Chinese and also have forgotten about how much CAPEX Google themselves is also spending (almost 25% of revenue now).

So Google will lose less badly. That does not make one a winner!

BY Doug Kass · Dec 2, 2025, 8:10 AM EST

BY Doug Kass · Dec 2, 2025, 8:00 AM EST

BY Doug Kass · Dec 2, 2025, 7:45 AM EST

BY Doug Kass · Dec 2, 2025, 7:35 AM EST

With the Oscillator now overbought and a reversal of breadth (lower):

I am a more enthusiastic seller (short) on strength now.

And the fact that Japanese bond yields are moving to multi-decade highs, taking our rates higher, emboldens me.

Then there is the circular financing nonsense and other issues in AI that I remain skeptical of.

See yesterday's opener (Part 1, Part 2, Part 3) for my many and growing fundamental concerns.

Color me more bearish (though I currently only have a small index short).

But that will soon likely change.

BY Doug Kass · Dec 2, 2025, 7:20 AM EST

BY Doug Kass · Dec 2, 2025, 7:10 AM EST

BY Doug Kass · Dec 2, 2025, 7:00 AM EST

BY Doug Kass · Dec 2, 2025, 6:45 AM EST

*Silver is this week's technical darling; if history prevails.. its time to grow more cautious

Bonus — Here are some great links:

The Most Important Charts in the Market Now

"Jazzy" Jeff Hirsch on the Real Santa Claus Rally

BY Doug Kass · Dec 2, 2025, 6:45 AM EST

From my pal Abie

For a the last few years, the rate of inflation was the B side of popular conversation everywhere with the raging bull market in manana AI stocks as the A side of the same conversations. This was a big difference from the 70s when inflation was the A side and there was no contravailing B side.

The problem with the inflation conversation is that it was misleading in two critical ways. First of all, the numbers of inflation as misleadingly reported by our government, the one that is run by liars, grifters and idealogues, is usually a single digit number which can lull one into thinking it's no big deal. Yes it briefly reached (on an as bullshyt reported number) double digits but they cooked the books enough with rent-equivalent costs of housing and hedonistic adjustments to make you think that $50,000 car is costing you no more than that $1900 chevy impala did in the late 1950s to bring monthly horseshyt reported number that back to "single digits" only a "little worse than" the famous 2% target level. The second problem is they completely ignore the compounding and kid you into thinking that a return to 0% inflation or even 2% (not such a big number - what are you worried about) undoes all that tight feeling you had when you realized that the $100k or $150k you and your spouse are earning ISN"T ENOUGH...that YOU ARE FALLING BEHIND and YOU OWE $73 Large on your f....ing credit cards and you will NEVER pay them down and you start Googling "How do I go bankrupt".

Well, a simple but massively important election just took place in New York where a very attractive and well spoke Commie took all our govt grifters and their tech and wall st billionaire owners out behind the same barn that they took the Russian czar and kinfolk behind and put an electoral bullet into the back of their heads...How you ask did he do that? With one word...one single word he named the Beast slouching towards modern Bethlehem where the money changers had recaptured the Temple....AFFORDABILITY ....AFFORDABILITY!!

Not inflation - not 2% of 3% or even 10%..that is a distraction....the real BEAST is the compounded TOTAL-AFFORDABILITY!

He educated everyone in America as what the real BEAST is ....the total of all the little insults - the diner that raised its prices 50% using covid as the excuse first and then made you tip the people they used to pay and finally, to shove it up your peasant arse,,,,,REMODELED, raised the prices yet again AND started closing early because they didn't need that annoying after 6 pm business anymore.

AFFORDABILITY... "THE RENTS IS TOO HIGH" and now even rich little college kids find out "THE HOUSES IS TOO HIGH TOO NOW"!!!

AFFORDABILITY - it is the commie candidates drone weapon...the name of the BEAST and the BEAST is the TRUTH. The pols owned by the bankers who also own their DEATH STAR weapon that has kept them rich for decades - THE FED - have screwed us one 2% and 3% and 5% at a time and convinced you that if they paused and let you get back to 2% for a while (sort of ...3% is sort of 2%) you're OK again...except you really aren't are you? you just didn't know how to say it... Well Mr. Mamdani told us all what the name of the BEAST is...AFFORDABILITY..... and every frigging politician on the planet knows it. The speed with which even Trump has picked up the WORD drafting right behind the Democrats who, forgetting their own guilt in the creation and unleashing of the BEAST as they sold out year after year after year to the bankers, are wearing white again.

The public is ready for Volcker again and by God, they will have him again because if they aren't given him again - just for a while at least - they may soon elect Stalin..I mean Mamdani to be King or First Citizen or President..won't matter what you call him...that club in his red right hand will be named AFFORDABILITY.

Won't be long before Lin-Manuel Miranda writes the new Les Mis for these new times.....

Many thought a new third party was coming and needed in America but it's fair to say that "many" thought it would be a centrist between the woke left pandering to one bunch of voters to get elected to sell themselves to the bankers and billionaires who could cut them in on real estate deals and weapons systems contracts and hot companies before they went public and the "holier than thou" right wingers - half of them in the same sellout and grifting game same as the left and the other half --well, you come up with your own description.

Well, looks like the third party is going to look a lot more like the commie who retired the Czar and the rest of Russian royalty violently. Yes, the same individual violence we have been seeing and watching and watching it grow in our schools, in clubs in poor neighborhoods late at night, in random shootings and beatings of even old people everywhere, in the NY subways where everyone has learned to stand back away from the platform edge lest a so far solo revolutionist - sick and tired of hopeless choking poverty - start a small personal revolution and rejection of a system with NO AFFORDABILITY for him.

Now that Mr Mamdani has named and outed the BEAST, nothing will get the BEAST back into his bottle or cage or wherever he lived for a long time. I think the Communist Party - in the USA so far called Democratic Socialists - ARE the new THIRD PARTY in America...

Don't know where this train will end up but I bet the getting there will not be fun for a lot politicians and their owners...no wonder Hollywood is presciently making movies about a bunker for them built deep under a lake...and private communities with armed guards....think of them as the Cassandra movies.

AFFORDABILITY....sounds like such an innocent middle and working class goal...sounds like a BEAST to me.

BY Doug Kass · Dec 2, 2025, 6:35 AM EST

Peter Boockvar (on why oil could be next year's gold), as always, is great.

VIDEO: Why Oil Could Be Next Year’s Gold - The Compound with Josh Brown and Michael Batnick

BY Doug Kass · Dec 2, 2025, 6:25 AM EST

BY Doug Kass · Dec 2, 2025, 6:15 AM EST

Wolf Street howls about higher interest and mortgage rates.

I have recently highlighted the unprecedented rise in Japanese Bond yields, which finally had some influence on our rate structure.

I am surprised the "AI all of the time market" is unfocused on this.

BY Doug Kass · Dec 2, 2025, 6:05 AM EST

The S&P Short Range Oscillator remains in overbought territory at 1.45% vs. 1.64%.

BY Doug Kass · Dec 2, 2025, 5:55 AM EST

* On a scale...

At around 535 AM, with futures +12 handles, I started (giving market wider berth than usual) to short the indices, again:

* (SPY) $681.39

* (QQQ) $618.16

BY Doug Kass · Dec 2, 2025, 5:45 AM EST

DeepSeek released V3.2-Speciale an open reasoning model with gold-level IMO/IOI capabilities 25× cheaper than GPT-5 and 30× cheaper than Gemini 3 Pro btw